GOLD PRICE CLOSED: UP $10.15 at $1796,49

SILVER PRICE CLOSED: UP $0.29 to $23.72

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1797.30

Silver ACCESS CLOSE: 23.74

Bitcoin morning price:, 16,865 UP 208 DOLLARS

Bitcoin: afternoon price: $16,826 UP 170 dollars

Platinum price closing $1023.65 UP $41.60

Palladium price; closing 1759,15 UP 8.70

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2442,56 DOWN $2.52 CDN dollars per oz

BRITISH GOLD: 1491,86 UP 1.96 pounds per oz

EURO GOLD: 1693.07 UP 1.36 euros per oz

EXCHANGE: COMEX

COMEX//NOTICES FILED

EXCHANGE: COMEX

CONTRACT: DECEMBER 2022 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,787.000000000 USD

INTENT DATE: 12/22/2022 DELIVERY DATE: 12/27/2022

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 2

365 H MAREX CAPITAL M 1

435 H SCOTIA CAPITAL 141

657 C MORGAN STANLEY 18

661 C JP MORGAN 225

661 H JP MORGAN 100

737 C ADVANTAGE 7

905 C ADM 11

991 H CME 53

TOTAL: 279 279

MONTH TO DATE: 20,566

COMEX//NOTICES FILED re JPMorgan 225/279

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR DEC. CONTRACT: 0 NOTICES FOR nil OZ or nil TONNES

total notices so far: 20,287 contracts for 2,028700 oz (63.100 tonnes)

SILVER NOTICES: 264 NOTICE(S) FILED FOR 1,320,000 OZ/

total number of notices filed so far this month 4209 for 21,045,000 oz

END

GLD

WITH GOLD UP $10.15

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//BIG CHANGES IN GOLD INVENTORY AT THE GLD: /////NO CHANGES IN GLD INVENTORY:

INVENTORY RESTS AT 913.88 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 29 CENTS

AT THE SLV// :/NO CHANGES IN SILVER INVENTORY AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 507.90 MILLION OZ (THIS IS ALSO A CRIME SCENE@!!!!

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 1312 CONTRACTS TO 127,691 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.53 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. OUR SHORTERS/HFT WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.53 AND WERE SUCCESSFUL IN KNOCKING SOME SPEC LONGS, AS WE HAD A STRONG LOSS ON OUR TWO EXCHANGES OF 822 CONTRACTS. AS WELL WE HAD EXCHANGE FOR RISK TRANSFER OF 0 CONTRACTS. WE HAD MINOR SPEC SHORT COVERINGS OF THEIR SHORTFALL . BUT WE HAD HUGE SHORT ADDITIONS WITH THE HUGE PRICE FALL OF THE SILVER. // OUR BANKERS CONTINUE TO BE PURCHASERS OF NET COMEX LONGS. BUT THEY ALSO SUPPLIED THE NECESSARY SHORT CONTRACTS>>> SOME MINOR INCREASE OF NEWBIE SPEC LONGS ADDING TO THEIR POSITIONS CAUSING ADDITIONAL MISERY TO OUR SHORTERS.

WE MUST HAVE HAD:

A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 23 .24. MILLION OZ FOLLOWED BY TODAY;S QUEUE.. JUMP of 20,000 OZ // V) STRONG SIZED COMEX OI LOSS/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL – 15

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS DEC. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF DEC:

TOTAL CONTRACTS for 19 days, total 10,403 contracts: OR 52.015 MILLION OZ PER DAY. (548 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 52.015 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 52.015 MILLION OZ INITIAL( VERY SMALL)

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1312 WITH OUR $0.53 LOSS IN SILVER PRICING AT THE COMEX// THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE CONTRACTS: 475 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR DEC OF 23.24 MILLION OZ FOLLOWED BY TODAY:S 20,000 QUEUE.. JUMP //NEW STANDING 23.380 MILLION OZ + EFR 11.5 = 34.88 MILLION OZ. .. WE HAVE A STRONG SIZED LOSS OF 822 OI CONTRACTS ON THE TWO EXCHANGES FOR 4.110 MILLION OZ.. THE SILVER SHORTS ARE NOW TRAPPED AS THEY ARE HAVING CONSIDERABLE DIFFICULTY IN COVERING THOSE SHORTS.

WE HAD 264 NOTICE(S) FILED TODAY FOR 1,320,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2794 CONTRACTS TO 438,592 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 493 CONTRACTS.

.

THE FAIR SIZED DECREASE IN COMEX OI CAME WITH OUR $29.35 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR DEC. AT 58.86 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY:S 21,600 OZ QUEUE JUMP (216 CONTRACTS)//(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S WILL CONTINUE UNTIL MONTH’S END) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). NEW STANDING 63.576 TONNES

YET ALL OF..THIS HAPPENED DESPITE OUR $29.35 LOSS IN PRICE WITH RESPECT TO THURSDAY’S TRADING

WE HAD A FAIR SIZED GAIN OF 1778 OI CONTRACTS (5.530 PAPER TONNES) ON OUR TWO EXCHANGES..

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 5065 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 438,592

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1778 CONTRACTS WITH 3287 CONTRACTS DECREASED AT THE COMEX AND 5065 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1778 CONTRACTS OR 5.530 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5065 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (3287) TOTAL GAIN IN THE TWO EXCHANGES 1778 CONTRACTS. WE NO DOUBT HAD 1) MINIMAL SPECULATOR SHORT COVERINGS // CONTINUED GOOD BANKER ADDITIONS BUT THEY ALSO SUPPLIED THE NECESSARY PAPER SHORT. WE HAD CONSIDERABLE SHORT SPEC ADDITIONS/// // MINOR NEWBIE SPEC ADDITIONS ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR DEC. AT 58.86 TONNES FOLLOWED BY TODAY’S QUEUE. JUMP of 21,600 oz// //NEW STANDING 64.432 TONNES///3) ZERO LONG LIQUIDATION //.,4) FAIR SIZED COMEX OPEN INTEREST GAIN 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2022 INCLUDING TODAY

DEC

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC :

47,379 CONTRACTS OR 4,737,900 OZ OR 147.34 TONNES 19 TRADING DAY(S) AND THUS AVERAGING: 2493 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAY(S) IN TONNES:147.34 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2021, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 147.34/3550 x 100% TONNES 4.14% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2022

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 147.34 tonnes Initial//VERY SMALL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW NON ACTIVE FRONT MONTH OF NOV. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH SILVER AND GOLD (WILL BE SMALL AS SPREADERS DO NOT PAY ATTENTION TO NOVEMBER)

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE NON ACTIVE DELIVERY MONTH OF NOV., FOR BOTH GOLD AND SILVER:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER, FELL BY A HUGE SIZED 1312 CONTRACTS OI TO 127,691 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO.

EFP ISSUANCE 475 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 475 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 475 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1312 CONTRACTS AND ADD TO THE 475 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE LOSS OF 837 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES 4.185 MILLION OZ//

OCCURRED WITH OUR 53 CENT LOSS IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

OUTLINE FOR TODAY’S COMMENTARY

1/COMEX GOLD AND SILVER REPORT

(report Harvey)

2 ) Gold/silver trading overnight Europe,

(Peter Schiff,

end

3. Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com,

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)FRIDAY MORNING//THURSDAY NIGHT

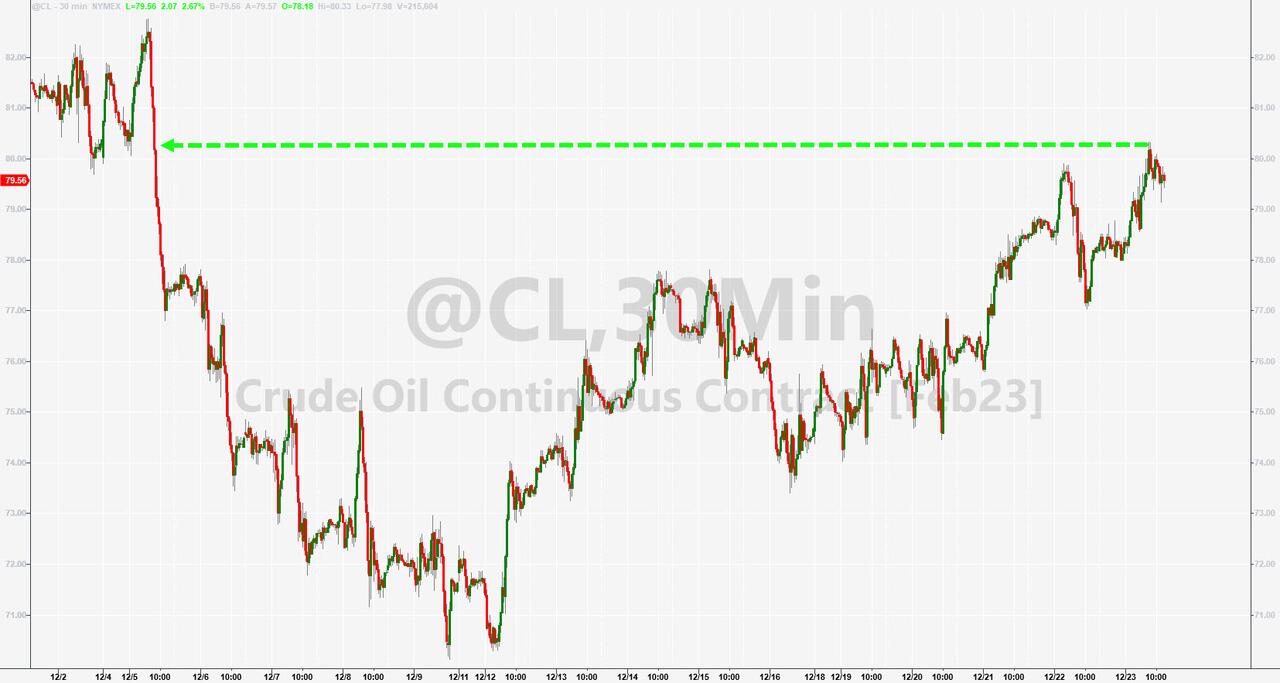

SHANGHAI CLOSED DOWN 8.56 PTS OR 0.28% //Hang Sang CLOSED DOWN 272.62 OR 1.03% /The Nikkei closed DOWN 272.62 OR 1.03% //Australia’s all ordinaries CLOSED DOWN 0.65% /Chinese yuan (ONSHORE) closed DOWN TO 6.9853//OFFSHORE CHINESE YUAN DOWN TO 6.9955// /Oil DOWN TO 79.09 dollars per barrel for WTI and BRENT AT 82.65 / Stocks in Europe OPENED MOSTLY GREEN (EXCEPT FRANCE). ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 3287 CONTRACTS UP TO 438,592 WITH OUR THE FALL IN PRICE OF $29.35

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE -ACTIVE DELIVERY MONTH OF DEC… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 5065 EFP CONTRACTS WERE ISSUED: ;: , . 0 FEB: 5065 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5065 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1778 CONTRACTS IN THAT 5065 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI LOSS OF 3287 CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $29.35. WE ARE WITNESSING CONSIDERABLE SPEC SHORTS ADDITIONS TO THEIR SHORTFALL BUT ZERO SPEC SHORT LIQUIDATIONS. BANKERS CONTINUE AS NET BUYERS OF COMEX GOLD CONTRACTS AS THEY HAVE BEEN NET LONG FOR THE PAST FEW MONTHS. WE ALSO HAD FEW NEWBIE SPECS ADDITIONS BUT CONSIDERABLE NEWBIE SPEC LONG LIQUIDATIONS

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING DEC (64.432)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL (TOTAL SO FAR THIS YEAR 591.535 TONNES)

Dec. 64.432 tonnes

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $29.35) //// AND WERE ALSO UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR GAIN OF 1778 CONTRACTS ON OUR TWO EXCHANGES >. WE HAD CONSIDERABLE NEW SPEC SHORT ADDITIONS AND FEW SPEC SHORT COVERINGS.. // WE HAVE GAINED A TOTAL OI OF 7.063 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR DEC. (54.57 TONNES), FOLLOWING OUR QUEUE JUMP OF 21,600 oz//NEW STANDING RISING TO 64.432 tonnes…THIS WAS ACCOMPLISHED DESPITE OUR FALL IN PRICE DUE TO TUNE OF $29.35.

WE HAD – 493 CONTRACTS COMEX TRADES REMOVED FROM OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 1778 CONTRACTS OR 177,800 OZ OR 5,53 TONNES

Estimated gold comex today 102,750// awful//

final gold volumes/yesterday 183,688/ poor

INITIAL STANDINGS FOR DECEMBER 2022 COMEX GOLD //DEC 23

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 9324.79 oz Manfra 290 kilobars . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | 211,457.127 oz BRINKS HSBC 1101 kilobars and 5476 kilobars |

| No of oz served (contracts) today | 279 notice(s) 27,900 OZ 0.8678 TONNES |

| No of oz to be served (notices) | 149 contracts 14,900 oz 0.4634 TONNES |

| Total monthly oz gold served (contracts) so far this month | 20,566 notices 2,056,600 63.9689 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

customer withdrawals: 1

i) Out of Manfra 9324.79 oz (290 kilobars)

Total withdrawals: 9324.79 oz

total in tonnes: 0.29 tonnes

Adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR DECEMBER.

For the front month of DECEMBER we have an oi of 428 contracts having GAINED 216 contracts

We had 0 contracts served on THURSDAY, so we gained 216 contracts or an additional 21,600 oz will stand for gold at the COMEX.

JANUARY LOST 75 contracts to stand at 11917

February LOST 5360 contacts to 370,378

We had 279 notice(s) filed today for 27,900 oz

Today, 100 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 279 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 225 notice(s) was (were) stopped/ Received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the DEC. /2022. contract month,

we take the total number of notices filed so far for the month (20,566 x 100 oz , to which we add the difference between the open interest for the front month of (DEC. 428 CONTRACTS) minus the number of notices served upon today 279 x 100 oz per contract equals 2,071,500 OZ OR 64.432 TONNES the number of TONNES standing in this active month of DEC.

thus the INITIAL standings for gold for the DEC contract month:

No of notices filed so far (20,566 x 100 oz+ (428 OI for the front month minus the number of notices served upon today (279} x 100 oz} which equals 2,071,500 oz standing OR 64.432 TONNES in this active delivery month of DEC..

TOTAL COMEX GOLD STANDING: 64.432 TONNES (A POOR STANDING//COMEX RUNNING OUT OF PHYSICAL TO SERVE UPON OUR LONGS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

we had one adjustment of 110,631.591 oz Brinks

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,062,155.871 OZ 64,14 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 23,235,785,659 OZ

TOTAL REGISTERED GOLD:11,342,356.837 OZ (352.79 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 11,893,428.822 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,280,201 OZ (REG GOLD- PLEDGED GOLD) 288.65 tonnes//rapidly declining

END

SILVER/COMEX

DEC 23//INITIAL DEC. SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,258,901.347 oz Brinks CNT Delaware Manfra |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 607,267,900 oz JPM |

| No of oz served today (contracts) | 126 CONTRACT(S) (1,320,000 OZ) |

| No of oz to be served (notices) | 341 contracts (1,705,000 oz) |

| Total monthly oz silver served (contracts) | 4335 contracts (21,675,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) Into JPmorgan: 607,267.900 oz

Total deposits: 607,267.900 oz

JPMorgan has a total silver weight: 148.595 million oz/298.672 million =49.74% of comex .//dropping fast

Comex withdrawals: 4

i) Out of Delaware 1996,913 oz

ii) Out of Brinks: 208,867.820 oz

iii) Out of CNT:: 12,076.06 oz

iv)Out of Manfra: 1,035,960.804 o

Total withdrawals; 1,255,901.397 oz

adjustments: 1

b) customer to dealer Brinks 619,287,210 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 36.638 MILLION OZ (declining rapidly).TOTAL REG + ELIG. 298.672 MILLION OZ (also declining)

CALCULATION OF SILVER OZ STANDING FOR SEPT

silver open interest data:

FRONT MONTH OF DEC OI: 467 CONTRACTS HAVING LOST 260 CONTRACT(S.)

WE HAD 264 NOTICES FILED ON TUESDAY. SO WE GAINED 4 CONTRACTS OR 20,000 oz

AS A QUEUE JUMP. WE ALSO HAD 0 CONTRACT EXCHANGE FOR RISK ISSUED FOR ZERO OZ.

JANUARY SAW A LOSS OF 64 CONTRACTS LOWERING TO 1335 CONTACTS.

FEB> GAINED 5 CONTRACTS TO 125 CONTRACTS

March LOST 921 contracts DOWN to 113,107 contracts

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 126 for 630,000 oz

Comex volumes// est. volume today 30,421//awful

Comex volume: confirmed yesterday: 47,333 contracts ( poor)

To calculate the number of silver ounces that will stand for delivery in DEC. we take the total number of notices filed for the month so far at 4335 x 5,000 oz = 21,675,000 oz

to which we add the difference between the open interest for the front month of DEC(467) and the number of notices served upon today 126 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the DEC./2022 contract month: 4335 (notices served so far) x 5000 oz + OI for front month of DEC (467 – number of notices served upon today (126) x 500 oz of silver standing for the DEC. contract month equates 23.380 million oz.. Also we have another criminal element to our silver oz standing, the use of Exchange for Risk/ Today an addition of 0 EFR contract transfers which are “Exchange for risk” settlements. I do not want to bore you but needless to say they are not physical transfers so are criminal in nature. There have been 2300 Exchange for Risk contracts settled during the first 22 days of the month for 11.500 million oz. Thus total delivery: 34.880 million oz.

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

Comex volumes:21,547// est. volume today// awful

Comex volume: confirmed yesterday: 74,745 contracts ( good)

END

GLD AND SLV INVENTORY LEVELS

DEC 23/WITH GOLD UP $19,15 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 913.88 TONNES/

DEC 22/WITH GOLD DOWN $29.35 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 913.88 TONNES

DEC 21/WITH GOLD FLAT TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 913.88 TONNES

DEC 20/WITH GOLD UP $27.05: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES INTO THE GLD////INVENTORY RESTS AT 912.14 TONNES

DEC 19/WITH GOLD DOWN $2.10: HUGE CHANGES IN GOLD INVENTORY AT THE GLD> A BIG WITHDRAWAL OF 3.47 TONNES FROM THE GLD//INVENTORY RESTS AT 910.41 TONNES

DEC 16/WITH GOLD UP $12.45: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD//INVENTORY RESTS AT 913.88 TONNES

DEC 15//WITH GOLD DOWN $31.00: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 911.56 TONNES

DEC 14/WITH GOLD DOWN $6.20: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 912.72 TONNES

DEC 13/WITH GOLD UP $32.75: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.32 TONNES INTO THE GLD///INVENTORY RESTS AT 910.41

DEC 12/WITH GOLD DOWN $17.60: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

DEC 9/WITH GOLD UP $8.90//NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.09 TONNES

Dec 8/WITH GOLD UP $4.05, OVER THE PAST 3 WEEKS WE LOST 2.04 TONNES//INVENTORY RESTS AT 908.09 TONNES

NOV 14/WITH GOLD UP $7.30: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 910.12 TONNES

NOV 11/WITH GOLD UP $15.25//BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.19 TONNES INTO THE GLD////INVENTORY RESTS AT 911.57 TONNES

NOV 10/WITH GOLD UP $40.75: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 908.38 TONNES

NOV 9/WITH GOLD DOWN $2.00: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES INTO THE GLD////INVENTORY RESTS AT 908.38 TONNES

NOV 8/WITH GOLD UP $34.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.47 TONNES FROM THE GLD//: INVENTORY RESTS AT 905.49 TONNES

NOV 7/WITH GOLD UP $2.95: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.63 TONNES FROM THE GLD//INVENTORY RESTS AT 906.96. TONNES

NOV 4/WITH GOLD UP $44.45 TO $1673.30: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.48 TONNES FROMTHE GLD////INVENTORY RESTS AT 911.59 TONNES.

NOV 3/WITH GOLD DOWN $18.30 TO $1628.85: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.05 TONNES FROM THE GLD////INVENTORY RESTS AT 915.07 TONNES

NOV 2/WITH GOLD UP 55 CENTS TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 919.12 TONNES.

NOV 1/WITH GOLD UP $9.20 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES FORM THE GLD../INVENTORY RESTS AT 920.57 TONNES

OCT 31/WITH GOLD DOWN $4.00; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES FROM THE GLD//INVENTORY RESTS AT 922.59. TONNES//

OCT28/WITH GOLD DOWN $19.70 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.19 TONNES FROM THE GLD..///INVENTORY RESTS AT 925.20 TONNES

OCT 27/WITH GOLD DOWN $3.80: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 26/WITH GOLD UP $11.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.39 TONNES

OCT 25/WITH GOLD UP $3.85: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 928.39 TONNES

OCT 24/WITH GOLD DOWN $1.80 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES FROM THE GLD////INVENTORY RESTS AT 928.10 TONNES

OCT 21/WITH GOLD UP $19.10: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 930.99 TONNES

OCT 20/WITH GOLD UP $2.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.08 TONNES FROM THE GLD///INVENTORY RESTS AT 932.73 TONNES

OCT 19/WITH GOLD DOWN $20.65:: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD////INVENTORY RESTS AT 938.81 TONNES

OCT 18/WITH GOLD DOWN $7.40: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES FROM THE GLD////INVENTORY RESTS AT 939.10 TONNES

OCT 17/WITH GOLD UP $14.55: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.28 TONNES FROM THE GLD///INVENTORY RESTS AT 941.13 TONNES

OCT 14/WITH GOLD DOWN $26.50 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES FROM THE GLD///INVENTORY RESTS AT 944.31 TONNES

OCT 13/WITH GOLD DOWN $0.40 TODAY: A DEPOSIT OF 1.16 TONNES INTO THE GLD// CHANGE IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 945.47 TONNES

OCT 12/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 944.31 TONNES

GLD INVENTORY: 913.88 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

DEC 23/WITH SILVER UP 29 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT507.900 MILLION O//

DEC 22/WITH SILVER DOWN 53 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 507.90 MILLION OZ//

DEC 21/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.0 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 507.90 MILLION OZ//

DEC 20/WITH SILVER UP 105 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV:: A DEPOSIT OF 700,000 OZ INTO THE SLV///INVENTORY RESTS AT 509.90 MILLION OZ//

DEC 19/WITH SILVER DOWN 13 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.05 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 509.20 MILLION OZ//

DEC 16/WITH SILVER UP 2 CENTS; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.85 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 508.15 MILLION OZ//

DEC 15/WITH SILVER DOWN 78 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF EXACTLY 2.00 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 510.000 MILLION OZ

DEC 14/WITH SILVER UP 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 512.000 MILLION OZ//

DEC 13/WITH SILVER UP 59 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 600,000 OZ FROM THE SLV////INVENTORY RESTS AT 513.900 MILLION OZ//

DEC 12/WITH SILVER DOWN 33 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 514.500 MILLION OZ//

DEC 9/WITH SILVER RISING 77 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.2 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 514.500 MILLION OZ.

DEC 8/WITH SILVER RISING 34 CENTS TODAY: OVER THE PAST 3 WEEKS, WE HAVE GAINED A STRONG: 44.777 MILLION OZ/INVENTORY RESTS AT 516.700 MILION OZ.

NOV 14/WITH SILVER UP 41 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.923 MILLION OZ//

NOV 11/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 553,000 OZ FROM THE SLV///INVENTORY RESTS AT 471.923 MILLION OZ//

NOV 10/WITH SILVER UP 39 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 368,000 OZ INTO THE SLV///INVENTORY RESTS AT 472.476 MILLION OZ//

NOV 9/WITH SILVER DOWN 10 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV/; A WITHDRAWAL OF 3.821 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 472.108 MILLION OZ//

NOV 8/WITH SILVER UP 48 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.751 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 475.929 MILLION OZ//

NOV 7/WITH SILVER UP 12 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 4/WITH SILVER UP $1.31 TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.972 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 477.678 MILLION OZ//

NOV 3.WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 566,000 OZ FROM THE SLV////INVENTORY RESTS AT 482.650 MILLION OZ//

NOV 2/WITH SILVER DOWN 9 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 92,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.216 MILLION OZ//

NOV 1/WITH SILVER UP 53 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 415,000 OZ FORM THE SLV////INVENTORY RESTS AT 483.308 MILLION OZ

OCT 31: WITH SILVER FLAT: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .644 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 483.723 MILLION OZ//

OCT 28/WITH SILVER DOWN 35 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.367 MILLION OZ//

OCT 27/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE S: A WITHDRAWAL OF 2.579 MILLION OZ FROMTHE SLV/////INVENTORY RESTS AT 484.091 MILLION OZ//

OCT 26/WITH SILVER UP 11 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.013 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 486.670 MILLION OZ./.

OCT 25/WITH SILVER UP 17 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.083 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 487.683 MILLION OZ/

OCT 24/WITH SILVER UP 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .553 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 485.610 MILLION OZ//

OCT 21/WITH SILVER UP 43 CENTS: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .46 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 486.163MILLION OZ//

OCT 20/WITH SILVER UP 33 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .921 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 485.703 MILLION OZ//

OCT 19/WITH SILVER DOWN 27 CENTS: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.105 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 486.624 MILLION OZ///

OCT 18/WITH SILVER DOWN 5 CENTS:BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.658 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.729 MILLION OZ///

OCT 17/WITH SILVER UP 53 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.151 MILLION OZ INTO THE SLV////INVENTORY REST AT 486.071 MILLION OZ//

OCT 14/WITH SILVER DOWN 77 CENTS TODAY: BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.211 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 484.920 MILLION OZ//

OCT 13/WITH SILVER DOWN 2 CENTS TODAY: BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.513 MILLION OZ INTO THE SLV//INVENTORY RESTS AT 482.709 MILLION OZ//

CLOSING INVENTORY 507.90 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

end

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

Jim Rickards: Paul Volcker’s Historic Mistake

FRIDAY, DEC 23, 2022 – 11:48 AM

Authored by James Rickards via DailyReckoning.com,

I’ve frequently said that forecasting Fed policy is easy. The Fed actually tells you what they plan to do in advance. This is the “no drama” Fed.

All you have to do is listen to what they say and believe them. They don’t want to surprise markets or trigger any unexpected volatility. So they signal in advance and move accordingly.

In reality, there’s a bit more to it than that.

The Fed also signals through leaks to chosen reporters. You need to know which reporters are the chosen ones and what publications they write for. The Fed also rotates to new reporters from time to time so you have to be alert to any shifts.

Still, it’s easy to know what’s coming if you know where to look and who to listen to.

The hard part is knowing when the Fed is on the wrong course (they usually are) and when they will realize it (usually too late). Based on that, you can forecast how much harm the Fed will do and how badly the economy will be damaged before the Fed changes course.

That’s more difficult and the timing can be tricky, but that’s the real art of Fed forecasting.

Sorry, Wall Street

With all that said, the Fed has announced two policies: The first is that they raised interest rates 0.50% on December 14. The second is that they may continue raising rates for much longer than the market expects.

The market keeps trying to rally on the Fed pivot narrative of lower rates, while Powell keeps trying to steer markets away from that narrative with his speeches.

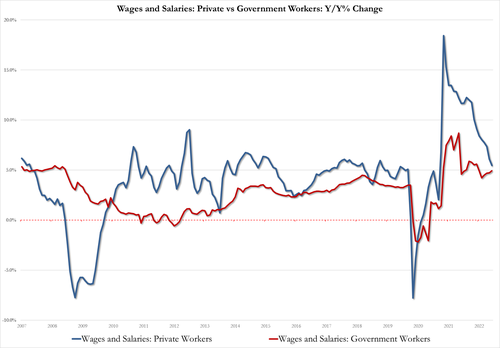

For example, stocks got a lift on Friday, December 2 when the November employment report showed declining real wages, declining hours worked, and declining labor force participation.

The bulls cheered because that negative bit of news seemed to confirm their view that rate cuts are on the way. But it didn’t last.

Powell has maintained a hawkish stance in a series of four high-profile speeches (August 26, September 21, November 2, and November 30), and now through press leaks.

Powell’s Not Done

I believe we should expect at least two more rate hikes. My estimate is a 0.50% rate hike on February 1, 2023 and a 0.25% rate hike on March 22. Those are the dates of the next two FOMC meetings.

There’s another meeting on May 3. It’s too soon to form a good estimate of what the Fed will do in May, but Powell has not ruled out another rate hike then.

But the economy will suffer a severe recession due to the rate hikes, and probably soon. Since the impact of monetary policy on the economy generally has a lag of maybe nine months to a year, we can expect the economy to be impacted by last year’s aggressive rate hikes in Q1 and Q2 of this year.

But once we’re in a recession, rate cuts won’t do any good. Nor will QE. The recession will happen in a context of higher energy prices, supply chain disruption (it’s baaack), and a Chinese collapse. Good luck getting through that. In this scenario, Goldilocks gets eaten by the bears.

The Fed will slam on the brakes on rate hikes and will probably have to cut rates by next June. Why won’t he cut rates sooner?

The Volcker Mistake

Jay Powell does not want to repeat the mistake of Paul Volcker, who also fought inflation with rate hikes, but cut rates too early and came to regret it.

When Paul Volcker was appointed Fed Chair in 1979, he immediately set about ending the worst inflation the U.S. has seen since the end of World War II by raising rates.

Then the U.S. was hit with a recession in January 1980.

Unemployment rose to 7%. Inflation was still 14.7% in April 1980, but Volcker was under intense pressure to cut rates in the face of a recession and layoffs.

The Fed blinked. Volcker lowered the fed funds target rate by 7 percentage points.

The recession was over by July 1980, but inflation was not. Inflation at the end of 1980 was still over 12%. The Fed and Volcker had damaged their credibility as inflation fighters.

This became known as the infamous Volcker Mistake.

From there Volcker doubled down. Because of the credibility damage from the Volcker Mistake, interest rates had to go even higher. It was in this stretch that the fed funds target rate hit 20% in June 1981.

This extreme level triggered another recession in July 1981, the second in two years. The 1981 – 1982 recession was the worst since the end of World War II, and interest rates were still 15% in the middle of 1982.

The severity of that recession was not surpassed until the global financial crisis of 2008.

The point is that when Volcker lowered rates in 1980, the job of beating inflation was not done. Inflation went even higher and Volcker had to take even more extreme measures finally to get it under control.

“The Lesson for the Fed Today Is Obvious”

If Volcker had ignored the 1980 recession, inflation might have come down by 1981. Instead, it lasted until 1983 and was only defeated by a recession worse than the one Volcker was initially worried about.

The lesson for the Fed today is obvious.

The Fed first ignored inflation in mid-2021 by calling it transitory. At the time, the Fed’s policy rate was 0%. The Fed’s battle against inflation began in March 2022 with a rate hike of 0.25%.

Inflation rose at an annualized rate of 9.1% in June 2022, 8.5% in July, 8.3% in August, 8.2% in September, and 7.7% in October. In other words, inflation is coming down but at a painfully slow pace.

The problem is that Powell may soon find himself facing exactly the dilemma that Volcker faced in May 1980 – the mission to lower inflation is not finished, but higher unemployment and a recession create enormous pressure to lower interest rates.

The question for market observers and investors is: Will Jay Powell blink the way Volcker did in 1980? Will the Fed cut rates in a recession or keep up the inflation fight until it’s over?

Powell Doesn’t Want to Repeat the Volcker Mistake

The answer begins with the fact that Jay Powell does not want to repeat the Volcker Mistake. He knows how that turned out and doesn’t want to end up in the history books for the same thing.

That means rate hikes will continue until March 2023 and possibly May, even in the face of declining growth and falling inflation. The Fed may pivot by June, but it will be too late.

The recession will already be here — and Powell will have some really hard choices to make.

END

3. Chris Powell of GATA provides to us very important physical commentaries//

Interesting: suddenly many are hunting for alternatives to the USA dollar

(Bloomberg News/GATA)

Suddenly everyone is hunting for alternatives to the U.S. dollar

Submitted by admin on Thu, 2022-12-22 10:22Section: Daily Dispatches

Didn’t the world once use some kind of metal with monetary properties? Is that still around?

* * *

By Michelle Jamrisko and Ruth Carson

Bloomberg News

via Yahoo News, Sunnyvale, California

Wednesday, December 21, 2022

King Dollar is facing a revolt.

Tired of a too-strong and newly weaponized greenback, some of the world’s biggest economies are exploring ways to circumvent the US currency.

Smaller nations, including at least a dozen in Asia, are also experimenting with de-dollarization. And corporates around the world are selling an unprecedented portion of their debt in local currencies, wary of further dollar strength.

No one is saying the greenback will be dethroned any time soon from its reign as the principal medium of exchange. Calls for “peak dollar” have many times proven premature. But not too long ago it was almost unthinkable for countries to explore payment mechanisms that bypassed the US currency or the SWIFT network that underpins the global financial system.

Now, the sheer strength of the dollar, its use under President Joe Biden to enforce sanctions on Russia this year, and new technological innovations are together encouraging nations to start chipping away at its hegemony. Treasury officials declined to comment on these developments.

“This will simply intensify the efforts in Russia and China to try to manage their part of the world economy without the dollar,” said Paul Tucker, a former deputy governor of the Bank of England in a Bloomberg podcast.

Writing in a newsletter last week, John Mauldin, an investment strategist and president of Millennium Wave Advisors with more than three decades of markets experience said the Biden administration made an error in weaponizing the US dollar and the global payment system.

“That will force non-US investors and nations to diversify their holdings outside of the traditional safe haven of the U.S.,” said Mauldin. …

… For the remainder of the report:

https://www.yahoo.com/now/suddenly-everyone-hunting-alternatives-us-130000587.html

END

How foolish can one get?

(Peter Hobson/Reuters)

Russian gold was removed from some Western funds after Ukraine war

Submitted by admin on Thu, 2022-12-22 10:42Section: Daily Dispatches

By Peter Hobson

Reuters

Wednesday, December 21, 2022

LONDON — Hidden inside high-security bank vaults in London, Zurich, and New York, billions of dollars’ worth of gold of Russian origin has quietly changed hands in recent months in response to Moscow’s invasion of Ukraine.

Data from 11 Western investment funds show that Russian bullion worth a total of $2.2 billion at current prices was removed from their accounts between July and November.

Funds storing gold have shrunk in recent months as rising interest rates triggered disinvestment from bullion.

But the data, compiled by Reuters, shows Russian gold being removed at a significantly faster pace than that from other countries.

For the remainder of the report:

END

Your weekend reading material:

Alasdair Macleod…

Alasdair Macleod: Inflation, recession, and declining U.S. hegemony

Submitted by admin on Thu, 2022-12-22 11:32Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, December 22, 2022

In the distant future we might look back on 2022 and 2023 as pivotal years.

So far we have seen the conflict between America and the two Asian hegemons emerge into the open, leading to a self-inflicted energy crisis on the western alliance. The 40-year trend of declining interest rates has ended, replaced by a new rising trend, the full consequences and duration of which are as yet unknown.

The Western alliance enters the New Year with increasing fears of recession. Monetary policy makers face an acute dilemma: Do they prioritize inflation of prices by raising interest rates, or do they lean toward yet more monetary stimulation to ensure that financial markets stabilise, their economies do not suffer recession, and government finances are not driven into crisis?

This is the conundrum that will play out in 2023 for the U.S., U.K., E.U., Japan, and others in the alliance camp.

But economic conditions are starkly different in continental Asia.

China is showing the early stages of making an economic comeback. Russia’s economy has not been badly damaged by sanctions, as the Western media would have us believe. All members of Asian trade organisations are enjoying the benefits of cheap oil and gas while the Western alliance turns its back on fossil fuels.

The message sent to Saudi Arabia, the Gulf Cooperation Council, and even to OPEC+ is that their future markets are with the Asian hegemons. Predictably, they are all gravitating into this camp. They are abandoning the American-led sphere of influence.

The year 2023 will see the consequences of Saudi Arabia ending the petrodollar. Energy exporters are feeling their way toward new commercial arrangements in a bid to replace yesterday’s dollar. There’s talk of a new Asian trade settlement currency.

But we can expect oil exports to be offset by inward investment, particularly between Saudi Arabia, the GCC, and China. The most obvious surplus emerging in 2023 is of internationally held dollars, whose use value is set to drop away, leaving it as an empty shell.

It amounts to a perfect storm for the dollar, and all those who sail with it.

Those of us who live long enough to look back on these years are likely to find them to have been pivotal for both currencies and global alliances. They will likely mark the end of Western supremacy and the emergence of a new, Asian economic domination. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/inflation-recession-and-declining-us-hegemony?gmrefcode=gata

GOLD/SILVER

/4. OTHER PHYSICAL SILVER/GOLD COMMENTARIES

Andrew Maguire goes mainstream

must view…

Thanks H! BTW was on Mainstream news here in the UK yesterday talking manipulation and why Gold and Silver are money. The Zalenski Biden meeting came in live as we did it so we had to shorten it. However, we can go deeper down the rabbit hole in an upcoming slot shortly

END

6/CRYPTOCURRENCIES/BITCOIN ETC

END

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//

FRIDAY MORNING.7:30 AM

ONSHORE YUAN: DOWN TO 6.9853

OFFSHORE YUAN: 6.9935

SHANGHAI CLOSED DOWN 8.56 PTS OR 0.28%

HANG SANG CLOSED DOWN 86.16 OR 0.44%

2. Nikkei closed DOWN 272,62 PTS OR 1.03%

3. Europe stocks SO FAR: MOSTLY GREEN

USA dollar INDEX DOWN TO 103.93 Euro RISES TO 106.16 UP 16 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.370!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 132.69/JAPANESE YEN RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy the 9 TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.385%***/Italian 10 Yr bond yield RISES to 4.495%*** /SPAIN 10 YR BOND YIELD RISES TO 3.451…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.529//

3j Gold at $1797.80//silver at: 23.72 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 8/100 roubles/dollar; ROUBLE AT 69.04//

3m oil into the 79 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 132.69

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9296– as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9868 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.712% UP 4 BASIS PTS…GETTING DANGEROUS

USA 30 YR BOND YIELD: 3.779% UP 6 BASIS PTS//

USA DOLLAR VS TURKISH LIRA: 18,69…

GREAT BRITAIN/10 YEAR YIELD: 3.662 % UP 1 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Tick Higher Ahead Of Key PCE Print

FRIDAY, DEC 23, 2022 – 08:03 AM

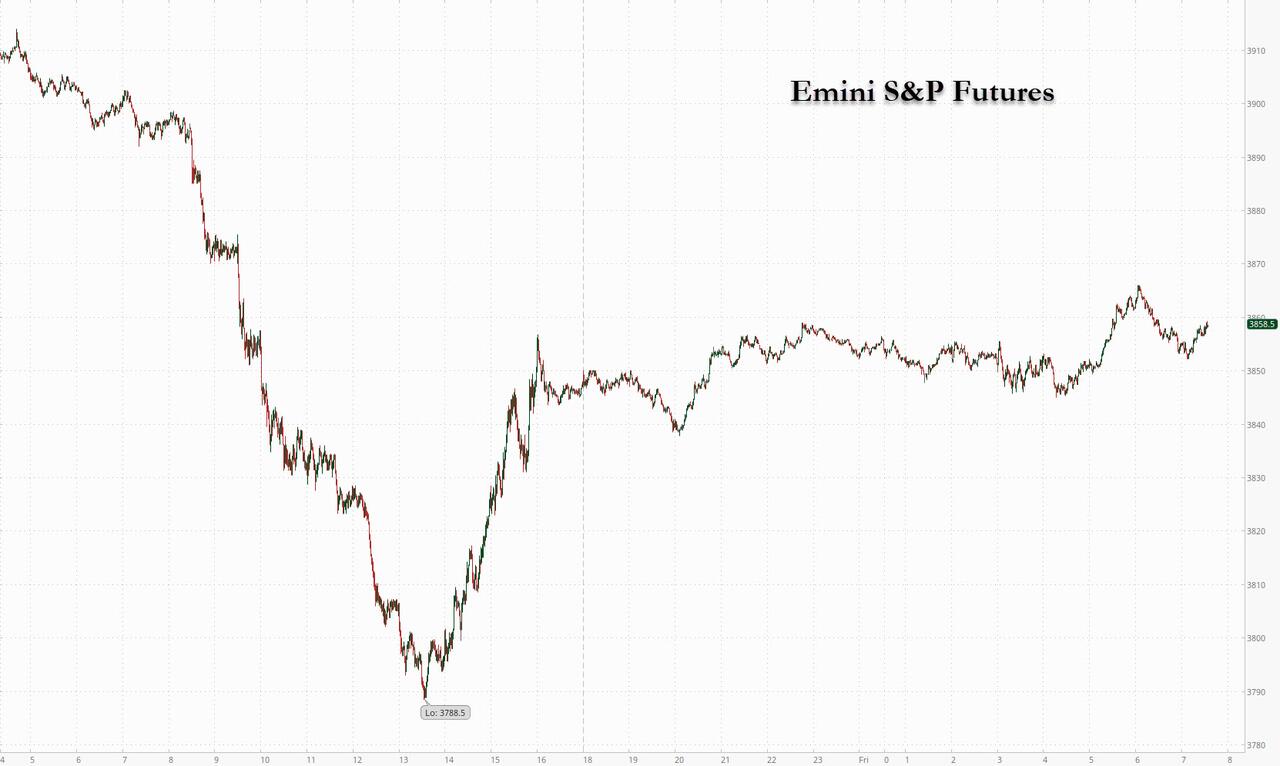

US stock futures edged higher after Thursday’s slump as investors weighed strong job data and prospects of further policy tightening to cool inflation ahead of today’s closely watched core PCE print which may reverse the negative sentiment (especially if it comes at 4.5% Y/Y or lower) and send stocks sharply higher (see here for more). Contracts on the Nasdaq 100 and the S&P 500 gained 0.3% by 7:30 am ET one day after the S&P 500 cash index plunged 1.5% on Thursday and was set for a third consecutive weekly loss, the longest losing streak since September. The index is also on pace for its second-worst December on record, while the Nasdaq 100 is on course for its steepest slump in the month since 2002.

In premarket trading Friday, Tesla Inc. shares rose after Elon Musk said he isn’t planning to sell any more shares for two years. Meme stock AMC Entertainment slid after the movie theater chain operator proposed converting preferred equity units into common shares. Meanwhile, avocado supplier Mission Produce reported fiscal fourth-quarter revenue and adjusted earnings per share that missed the average analyst estimates and predicted lower pricing in the first quarter.

Sentiment on Wall Street took a hit Thursday as jobless claims came in lower than expected, signaling the Federal Reserve has more work to do on inflation, while earnings disappointments sparked fears among investors of a recession. Technically, the set up isn’t looking good, according to Bloomberg intelligence strategist Gina Martin Adams, with a descent in equities that began at the start of 2022 looking set to persist into early 2023. “Momentum and breadth remain weak and industry cues hint at a prolonged struggle,” she wrote in a note.

With stocks sliding, global equity funds saw record weekly outflows of almost $42 billion in the week to Dec. 21, which were largely driven by US stock funds shedding $37 billion of assets, according to EPFR Global data. The outflows were mostly due to seasonal redemptions from US ETFs, Citigroup strategists said. And as a catastrophic year for stocks draws to a close, investors have also had a warning from strategists that they should brace for more pain heading into 2023.

“I think it’s going to be a very difficult year,” said James Athey, investment director at Abrdn. “The fact of the matter is that there’s been a significant monetary tightening we haven’t seen in a long time,” he said. “The effect of that on a global economy which is drowning in debt is highly likely to be deleterious.”

“Markets are in a state of flux at the moment, we have quite high inflation and interest rates that don’t quite seem able to catch up,” Richard Harris, chief executive officer at Port Shelter Investment Management, said in an interview on Bloomberg TV. “You have to be careful with equities, but they are still a better bet than bonds at the moment.”

Notable headlines overnight:

- Joe Biden said it will take time to get inflation back to normal levels, according to Yahoo News.

- Tesla CEO Musk said he will not sell any more Tesla stock for at least 18-24 months; waiting to see the extent of a recession before share buybacks, via Twitter Space. Musk said the economy will be in a “serious recession” in 2023, and demand will be lower.

Investors are now awaiting the PCE deflator, a key inflation measure tracked by the Fed. Analysts polled by Bloomberg expect a year-on-year 5.5% headline print, slowing from October’s 6%.

In Europe, the Stoxx 600 was on the rise, led by real estate, basic resources and retail stocks, and was headed for the first weekly gain in three as risk appetite returned before the Christmas holiday.

Earlier in the session, Asian stocks fell, on track for a second-straight weekly loss on concerns about aggressive US interest-rate hikes and the spread of the coronavirus in China. The MSCI Asia Pacific Index fell as much as 1.2%, with technology and energy stocks falling the most and dragging down South Korean and Taiwanese benchmarks. Trading was thin in much of the region ahead of year-end holidays. US economic growth in the third quarter was firmer than previously estimated, pushing a pause in the Federal Reserve’s policy tightening further out of reach. Investors are also wary that the core PCE deflator — a key US inflation measure — due later Friday may add to reasons for tighter policy. Meantime, a weaker sales outlook by memory maker Micron weighed on the chip sector. Friday’s decline put the MSCI Asia gauge on track for a 0.6% loss this week. While some strategists are optimistic that the year ahead could bring a rally after this year’s double-digit drop, the first half of 2023 looks riddled with challenges to profits as the global economy slows down and China’s path to reopening remains uncertain

“The Grinch selloff is firmly in place after Micron delivered a gloomy outlook and as better-than-expected US economic data supported the Fed’s case for more ongoing rate increases,” Edward Moya, a senior market analyst at Oanda, wrote in a note. “Global coordinated central bank tightening has yet to fully impact most of the economic readings for the major economies and that should have investors nervous over earnings downgrades and credit risks.” Key measures of Hong Kong and mainland stocks fell as the market digested China’s rising infection numbers and a sharp slowdown in economic activity.

Japan’s Nikkei 225 posted its worst week since June on fears that the Bank of Japan has begun to exit its easy-money policy. On Friday, Japanese stocks declined as resilient US economic data renewed investor worries that the Federal Reserve will continue raising interest rates aggressively. The Topix fell 0.5% to close at 1,897.94, while the Nikkei declined 1% to 26,235.25. Toyota Motor Corp. contributed the most to the Topix decline, decreasing 1.2%. Out of 2,162 stocks in the index, 677 rose and 1,384 fell, while 101 were unchanged. US Third-Quarter GDP Revised Higher to 3.2% on Firmer Spending “How long the Fed maintains its hawkish stance will depend on inflation,” said Tatsushi Maeno, a senior strategist at Okasan Asset Management. “There may be a mood of restrained buying ahead of the US PCE data this evening,” which could provide the next clue on the Fed’s moves

In Fx, the Bloomberg Dollar Spot Index weakened for first time in three days. The dollar pulled back against a basket of currencies and was headed for a weekly decline, having risen for the two previous weeks. The yen firmed, bringing this week’s gains to almost 3%, thanks to the Bank of Japan’s sudden hawkish policy pivot announced on Tuesday.

In rates, Treasury yields grind higher, following similar price action in bunds where ECB hike premium has edged up over early London session on no immediate catalyst. US session focus includes a busy data slate which includes PCE deflator and University of Michigan sentiment. Early 2pm New York close for cash Treasuries, recommended by SIFMA. US 10-year yields around 3.71%, cheaper by 3bp vs. Thursday close and trading broadly inline with bunds and gilts. 2-year TSY yields are steady at 4.27% while 10-year yields gain 1.1bps to 3.69%. In Thursday’s trading session yields rose after stronger-than expected US economic data with 2-year tenor gaining 5bps while 10-year finished up 2bps. Spreads pare portion of Thursday’s flattening move with Treasury 2s10s, 5s30s curves steeper by 1.4bp and 1.2bp on the day.

In commodities, crude oil is firmer with WTI & Brent up by roughly $2.0/bbl, with WTI needing another USD 1.00/bbl of upside to test Thursday’s WTD peak of USD 79.90/bbl; early on Friday Russia said it could cut oil output by 5-7% early next year as a response to the Western price caps, according to RIA citing Deputy PM Novak; Spot gold/silver are incrementally firmer given the Dollar continues to languish, though the yellow metal remains capped by USD 1800/oz and as such is well within recent ranges.

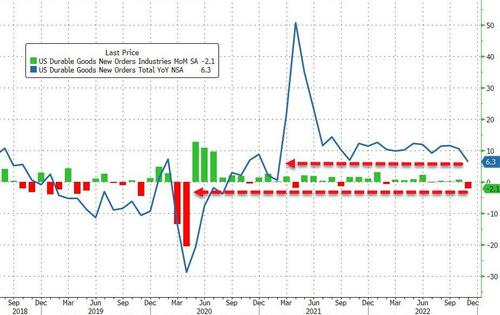

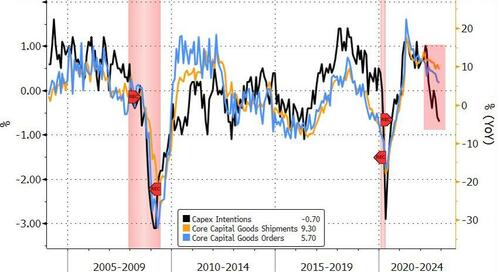

Looking at today’s busy calendar slate, we get Personal income and spending as well as the Fed’s favorite inflation metric, core PCE; we also get Durable Capital goods and new orders as well as the UMichigan sentiment indicator and new home sales.

Market Snapshot

- S&P 500 futures little changed at 3,848.50

- MXAP down 1.0% to 155.37

- MXAPJ down 1.1% to 503.74

- Nikkei down 1.0% to 26,235.25

- Topix down 0.5% to 1,897.94

- Hang Seng Index down 0.4% to 19,593.06

- Shanghai Composite down 0.3% to 3,045.87

- Sensex down 1.6% to 59,868.93

- Australia S&P/ASX 200 down 0.6% to 7,107.69

- Kospi down 1.8% to 2,313.69

- STOXX Europe 600 up 0.3% to 428.34

- German 10Y yield little changed at 2.40%

- Euro little changed at $1.0600

- Brent Futures up 1.8% to $82.45/bbl

- Gold spot up 0.2% to $1,796.18

- U.S. Dollar Index little changed at 104.37

Top Overnight News from Bloomberg

- Oil Pushes Higher as Russia May Cut Output in Response to Cap

- Jan. 6 Panel Releases Report Blasting Trump for Capitol Assault

- Tencent Rant, Sea Pay Freeze Hint at Deepening Gaming Crisis

- Sea Dives After Pay Freeze, Bonus Cuts Suggest Tougher 2023

- Biogen’s ALS Drug Raises Stakes in War Over Fast Drug Approvals

- Trump Asked About Using Troops on Protesters, Esper Told Panel

- Bankman-Fried’s $250 Million Bail Doesn’t Mean He Has Money

- US Stocks Snap Two Days of Gains; Dollar Rises: Markets Wrap

- Tech Bulls Face Worst December in 20 Years as Fed Anxiety Grows

- Well-Timed Shorts See Value Investor Notching 40% Gains for 2022

- Storm Upends Holiday Travel, Triggers White House Warning

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded mostly lower but drifted off worst levels following a similar session stateside. ASX 200 saw all of its sectors in the red with losses led by Tech, Energy and gold miners. Nikkei 225 was dragged lower by its industrial sector, whilst Japanese Core CPI in November rose at the fastest annual pace since 1981. Hang Seng and Shanghai Comp were mixed in which the former succumbed to the regional losses and the latter briefly moved into the green, whilst the PBoC injected a net CNY 704bln in the week via OMO – the largest weekly cash in nearly two months, according to Reuters calculations.

Top Asian News

- China reported zero new COVID deaths in the mainland on Dec 22nd vs zero a day earlier, according to Reuters.

- PBoC injected CNY 2bln via 7-day reverse repos with the rate maintained at 2.00%; injects CNY 203bln via 14-day reverse repos with the rate maintained at 2.15%; daily net injection CNY 164bln.

- PBoC injected a net CNY 704bln in the week via OMO; the largest weekly cash in nearly two months, according to Reuters calculations.

- Japanese PM Kishida could conduct a cabinet reshuffle as early as January 10th, according to ANN.

- Japanese government official said the next wave of food inflation is likely to come in February 2023; effects of government subsidies to cushion energy bills will likely start affecting CPI from February 2023, according to Reuters.

- BoJ October meeting minutes (two meetings ago): One member said the effects of BoJ’s easing may be heightening as a moderate increase in inflation expectations push down real interest rates.

- China reportedly estimates the COVID surge is affecting 37mln people per day, via Bloomberg.

- Indian Health Minister says in the next week, planning to make COVID-19 negative test report compulsory for passengers from nations with a high case load.

European bourses are marginally firmer, Euro Stoxx 50 +0.2%, with the Stoxx 600 on track to end the week with upside of circa. 0.6%. Sectors are, after a mixed open, mostly in the green though Utilities and Travel & Leisure remain incrementally softer.

Stateside, futures are similarly supported, ES +0.3%, though we await US monthly PCE metrics for another factor into the Fed’s deliberations. TSMC (TSM/2330 TT) is said to be in talks with suppliers over its first European plant, according to FT sources; Senior executives are heading to Germany early next year for discussions.

Top European News

- Janus Henderson’s New CEO To Expand In Latin America, Asia

- Meet the Improbable Stars of Turkey’s Year of Inflation Infamy

- Russia Says It May Cut Daily Oil Output by 700,000 Barrels

- Japan Begins Defense Upgrade With 26% Spending Increase for 2023

- Russia’s Novak: Decisions on Turkey Gas Hub May Be Taken in 2023

- Poland Sues EU Over Mounting Fine in Rule-of-Law Dispute

Geopolitical

- Senior Chinese Diplomat Wang Yi spoke to US Secretary of State Blinken and said US must stop supressing China’s development and should not challenge China’s red lines, according to Reuters.

- Chinese Foreign Ministry announced sanctions on Yu Maochun and Todd Stein as countermeasures to US’ sanction on two Chinese officials, citing human rights issues in Xizang (Tibet), according to Global Times.

- N. Korea has fired what could be a ballistic missile, via Japanese Coast Guard; Yonhap reports this as being a ballistic missile; landed outside of Japan’s EEZ.

FX

- Dollar wanes after GDP and IJC boost as the focus switches to PCE amidst a partial recovery in risk appetite, DXY roams from 104.160 to 104.510.

- Kiwi claws back losses vs Aussie and Buck as AUD/NZD retreats through 1.0650, NZD/USD breaches 200 DMA and AUD/USD scales 100 DMA with a slight lag.

- Pound, Euro and Loonie take advantage of softer Greenback, but Yen hampered by high yields, Cable firmer on 1.2000 handle, EUR/USD resilient around 1.0600, USD/CAD probing 1.3600 and USD/JPY hovering above 132.50.

- PBoC sets USD/CNY mid-point at 6.9810 vs exp. 6.9885 (prev. 6.9713)

Fixed Income

- Debt remains in virtual freefall, with Bunds extending losses sub-135.00, Gilts towards 100.00 and the T-note rooted within a 113-09+/15+ range

- Curves re-steepen marginally as the spotlight turns to US PCE data as the last potential macro market mover before the Xmas break

Commodities

- Crude benchmarks are firmer on the session with magnitudes more pronounced than across other asset classes; currently, WTI & Brent Fed’23 are firmer by just shy of USD 2.0/bbl, with WTI needing another USD 1.00/bbl of upside to test Thursday’s WTD peak of USD 79.90/bbl.

- Spot gold/silver are incrementally firmer given the Dollar continues to languish, though the yellow metal remains capped by USD 1800/oz and as such is well within recent ranges.

- Russia could cut oil output by 5-7% early next year as a response to the Western price caps, according to RIA citing Deputy PM Novak; Russia may cut oil output by 500-700k BPD, according to Tass citing Deputy PM Novak

- Colorado Interstate Gas Co. declared force majeure at CIG Wamsutter compressor station, according to Reuters.

- Phillips 66 (PSX) Wood River, Illinois (380k BPD) refinery reports a unit upset.

US Event Calendar

- 08:30: Nov. Durable Goods Orders, est. -1.0%, prior 1.1%; -Less Transportation, est. 0%, prior 0.5%

- Cap Goods Orders Nondef Ex Air, est. 0%, prior 0.6%

- Cap Goods Ship Nondef Ex Air, est. -0.3%, prior 1.5%

- 08:30: Nov. Personal Income, est. 0.3%, prior 0.7%

- Personal Spending, est. 0.2%, prior 0.8%

- Real Personal Spending, est. 0.1%, prior 0.5%

- 08:30: Nov. PCE Deflator MoM, est. 0.1%, prior 0.3%

- PCE Deflator YoY, est. 5.5%, prior 6.0%

- PCE Core Deflator MoM, est. 0.2%, prior 0.2%

- PCE Core Deflator YoY, est. 4.6%, prior 5.0%

- 10:00: Dec. U. of Mich. Sentiment, est. 59.1, prior 59.1

- U. of Mich. Current Conditions, est. 60.3, prior 60.2

- U. of Mich. Expectations, est. 58.5, prior 58.4

- U. of Mich. 1 Yr Inflation, est. 4.6%, prior 4.6%; 5-10 Yr Inflation, est. 3.0%, prior 3.0%

- 10:00: Nov. New Home Sales, est. 600,000, prior 632,000

- Nov. New Home Sales MoM, est. -5.1%, prior 7.5%

AND NOW NEWSQUAWK (EUROPE/REPORT)

Debt continues to falter and crude inches higher in limited trade – Newsquawk US Market Open

FRIDAY, DEC 23, 2022 – 06:13 AM

- European bourses are marginally firmer, Euro Stoxx 50 +0.2%, with the Stoxx 600 on track to end the week with upside of circa. 0.6%.

- Stateside, futures are similarly supported, ES +0.3%, though we await US monthly PCE metrics for another factor into the Fed’s deliberations.

- Dollar has waned with peers taking advantage with debt continuing to decline and curves re-steepening

- Crude benchmarks are firmer and eclipsing other assets following the latest updates from Russia and N. Korea

- Looking ahead, highlights include US monthly PCE, Canadian GDP, US University of Michigan Survey.

View the full premarket movers and news report.

Or why not try Newsquawk’s squawk box free for 7 days?

EUROPEAN TRADE

EQUITIES

- European bourses are marginally firmer, Euro Stoxx 50 +0.2%, with the Stoxx 600 on track to end the week with upside of circa. 0.6%.

- Sectors are, after a mixed open, mostly in the green though Utilities and Travel & Leisure remain incrementally softer.

- Stateside, futures are similarly supported, ES +0.3%, though we await US monthly PCE metrics for another factor into the Fed’s deliberations.

- TSMC (TSM/2330 TT) is said to be in talks with suppliers over its first European plant, according to FT sources; Senior executives are heading to Germany early next year for discussions.

- Click here for more detail.

FX

- Dollar wanes after GDP and IJC boost as the focus switches to PCE amidst a partial recovery in risk appetite, DXY roams from 104.160 to 104.510.

- Kiwi claws back losses vs Aussie and Buck as AUD/NZD retreats through 1.0650, NZD/USD breaches 200 DMA and AUD/USD scales 100 DMA with a slight lag.

- Pound, Euro and Loonie take advantage of softer Greenback, but Yen hampered by high yields, Cable firmer on 1.2000 handle, EUR/USD resilient around 1.0600, USD/CAD probing 1.3600 and USD/JPY hovering above 132.50.

- PBoC sets USD/CNY mid-point at 6.9810 vs exp. 6.9885 (prev. 6.9713)

- Click here for more detail.

Notable FX Expiries, NY Cut:

- Click here

FIXED INCOME

- Debt remains in virtual freefall, with Bunds extending losses sub-135.00, Gilts towards 100.00 and the T-note rooted within a 113-09+/15+ range

- Curves re-steepen marginally as the spotlight turns to US PCE data as the last potential macro market mover before the Xmas break

- Click here for more detail.

COMMODITIES

- Crude benchmarks are firmer on the session with magnitudes more pronounced than across other asset classes; currently, WTI & Brent Fed’23 are firmer by just shy of USD 2.0/bbl, with WTI needing another USD 1.00/bbl of upside to test Thursday’s WTD peak of USD 79.90/bbl.

- Spot gold/silver are incrementally firmer given the Dollar continues to languish, though the yellow metal remains capped by USD 1800/oz and as such is well within recent ranges.

- Russia could cut oil output by 5-7% early next year as a response to the Western price caps, according to RIA citing Deputy PM Novak; Russia may cut oil output by 500-700k BPD, according to Tass citing Deputy PM Novak

- Colorado Interstate Gas Co. declared force majeure at CIG Wamsutter compressor station, according to Reuters.

- Phillips 66 (PSX) Wood River, Illinois (380k BPD) refinery reports a unit upset.

- Click here for more detail.

NOTABLE HEADLINES

- US President Biden said it will take time to get inflation back to normal levels, according to Yahoo News.

- Tesla (TSLA) CEO Musk said he will not sell any more Tesla stock for at least 18-24 months; waiting to see the extent of a recession before share buybacks, via Twitter Space. Musk said the economy will be in a “serious recession” in 2023, and demand will be lower.

CRYPTO

- Bitcoin is marginally firmer, perhaps taking cues from the USD’s pressure, though remains within limited sub-USD 200 parameters.

GEOPOLITICAL

- Senior Chinese Diplomat Wang Yi spoke to US Secretary of State Blinken and said US must stop supressing China’s development and should not challenge China’s red lines, according to Reuters.

- Chinese Foreign Ministry announced sanctions on Yu Maochun and Todd Stein as countermeasures to US’ sanction on two Chinese officials, citing human rights issues in Xizang (Tibet), according to Global Times.

- N. Korea has fired what could be a ballistic missile, via Japanese Coast Guard; Yonhap reports this as being a ballistic missile; landed outside of Japan’s EEZ.

APAC TRADE

EQUITIES

- APAC stocks traded mostly lower but drifted off worst levels following a similar session stateside.

- ASX 200 saw all of its sectors in the red with losses led by Tech, Energy and gold miners.

- Nikkei 225 was dragged lower by its industrial sector, whilst Japanese Core CPI in November rose at the fastest annual pace since 1981.

- Hang Seng and Shanghai Comp were mixed in which the former succumbed to the regional losses and the latter briefly moved into the green, whilst the PBoC injected a net CNY 704bln in the week via OMO – the largest weekly cash in nearly two months, according to Reuters calculations.

NOTABLE ASIA-PAC HEADLINES

- China reported zero new COVID deaths in the mainland on Dec 22nd vs zero a day earlier, according to Reuters.

- PBoC injected CNY 2bln via 7-day reverse repos with the rate maintained at 2.00%; injects CNY 203bln via 14-day reverse repos with the rate maintained at 2.15%; daily net injection CNY 164bln.

- PBoC injected a net CNY 704bln in the week via OMO; the largest weekly cash in nearly two months, according to Reuters calculations.

- Japanese PM Kishida could conduct a cabinet reshuffle as early as January 10th, according to ANN.

- Japanese government official said the next wave of food inflation is likely to come in February 2023; effects of government subsidies to cushion energy bills will likely start affecting CPI from February 2023, according to Reuters.

- BoJ October meeting minutes (two meetings ago): One member said the effects of BoJ’s easing may be heightening as a moderate increase in inflation expectations push down real interest rates.

- China reportedly estimates the COVID surge is affecting 37mln people per day, via Bloomberg.

- Indian Health Minister says in the next week, planning to make COVID-19 negative test report compulsory for passengers from nations with a high case load.

DATA RECAP

- Japanese CPI, Core Nationwide YY (Nov) 3.7% vs. Exp. 3.7% (Prev. 3.6%); fastest annual pace since 1981

- Japanese CPI, Overall Nationwide (Nov) 3.8% (Prev. 3.7%)

- Australian Housing Credit (Nov) 0.4% (Prev. 0.4%); Private Sector Credit (Nov) 0.5% (Prev. 0.6%)

1.c FRIDAY/ THURSDAY NIGHT

SHANGHAI CLOSED DOWN 8.56 PTS OR 0.28% //Hang Sang CLOSED DOWN 272.62 OR 1.03% /The Nikkei closed DOWN 272.62 OR 1.03% //Australia’s all ordinaries CLOSED DOWN 0.65% /Chinese yuan (ONSHORE) closed DOWN TO 6.9853//OFFSHORE CHINESE YUAN DOWN TO 6.9955// /Oil DOWN TO 79.09 dollars per barrel for WTI and BRENT AT 82.65 / Stocks in Europe OPENED MOSTLY GREEN (EXCEPT FRANCE). ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

2 a./NORTH KOREA/ SOUTH KOREA/

///NORTH KOREA/RUSSIA

North Korea is supplying arms to Russia to mercenaries (Wagner grou)

(zerohedge)

North Korea Is Supplying Russia’s Wagner Mercenaries: White House

THURSDAY, DEC 22, 2022 – 08:00 PM

After months of issuing vague allegations that North Korea is supplying Russian forces with tens of thousands of artillery shells, which both sides have denied, the Biden administration on Thursday is finally out with something specific, saying that Pyongyang has delivered arms to Wagner group.

Wagner is the notorious private military contractor whose founder is said to be close to Vladimir Putin, and dubbed in Western reports as “Putin’s chef”. Western media has long accused Wagner operatives of committing war crimes in Ukraine, and before that on deployments in Syria.

“Wagner is searching around the world for arms suppliers to support its military operations in Ukraine,” White House national security spokesman John Kirby said in a Thursday press briefing. “We can confirm that North Korea has completed an initial arms delivery to Wagner, which paid for that equipment,” he added.

Kirby described the private Russian contractor as competing for power among official Kremlin ministries, acting as a “rival” also to the established defense ministry. A number of reports lately have suggested that Wagner mercenaries have operated with impunity and separate rules of engagement in Ukraine over the last ten months.

“Wagner is emerging as a rival power center to the Russian military and other Russian ministries,” Kirby explained, also stating that Wagner is spending over $100 million each month for Ukraine operations.

While European Parliament weeks ago formally slapped a ‘terror’ label on Wagner, the US is still said to be mulling the action, also vowing to ratchet sanctions on the Putin-connected firm.

More broadly, the White House has so far resisted calls from more hawkish corners of Congress to label Russia a state sponsor of terror, and is now said to be considering calling Russia an “aggressor state” – however, there’s no precedent for this term and it appears entirely made up by the administration in order to appease critics.

As CNN describes, “An aggressor state designation, unlike the label state sponsor of terrorism, is not an official State Department category that would trigger specific US sanctions, and critics say it would be easier for the president to rescind that designation than the state sponsor of terrorism one.”

It remains unclear at this point the precise type of weapons alleged to have been supplied to Wagner Group by the North Koreans. The broader Russian military is reportedly running low on artillery, which has been expended in the eastern and southern front lines at a rapid rate. In an official statement Pyongyang later in the evening denied the allegation.

end

2B JAPAN

3c CHINA /

CHINA/COVID

With China abandoning its zero COVID policy, now we witness huge numbers of experts and celebrities die over there. COVID 19 cases are flourishing as are injuries to their awful vaccine

(Lam/EpochTimes)

Dozens Of CCP-Linked Experts, Celebrities, Officials Die During Recent COVID-19 Outbreak

THURSDAY, DEC 22, 2022 – 11:00 PM

Authored by Sophia Lam via The Epoch Times (emphasis ours),