MARCH 28//GOLD AND SILVER REVERSE COURSE AND END THE DAY MUCH STRONGER: GOLD UP $19.70 TO $1972.50//SILVER FINISHED THE DAY UP A STRONG $.28 TO $23.27//PLATINUM WAS DOWN $14.00 TO $968.30//PALLADIUM WAS UP $7.30 TO $1437.00//COVID UPDATES//VACCINE IMPACT/SLAY NEWS/DR PAUL ALEXANDER//UKRAINE VS RUSSIA UPDATES//CANADIAN INSOLVENCIES ON THE RISE FROM MILLENNIALS//SWAMP STORIES FOR YOU TONIGHT

TODAY IS COMEX OPTIONS EXPIRY AND TRUE TO FORM THE CROOKS RAID SO THAT THE BANKS CAN MAKE THEIR PENNIES. THE BIGGER OTC/LONDON OPTIONS EXPIRY IS FRIDAY’

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 1972.20

Silver ACCESS CLOSE: 23.32

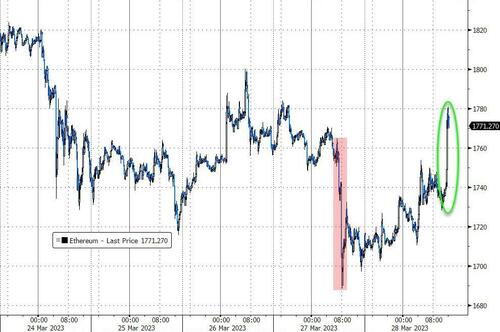

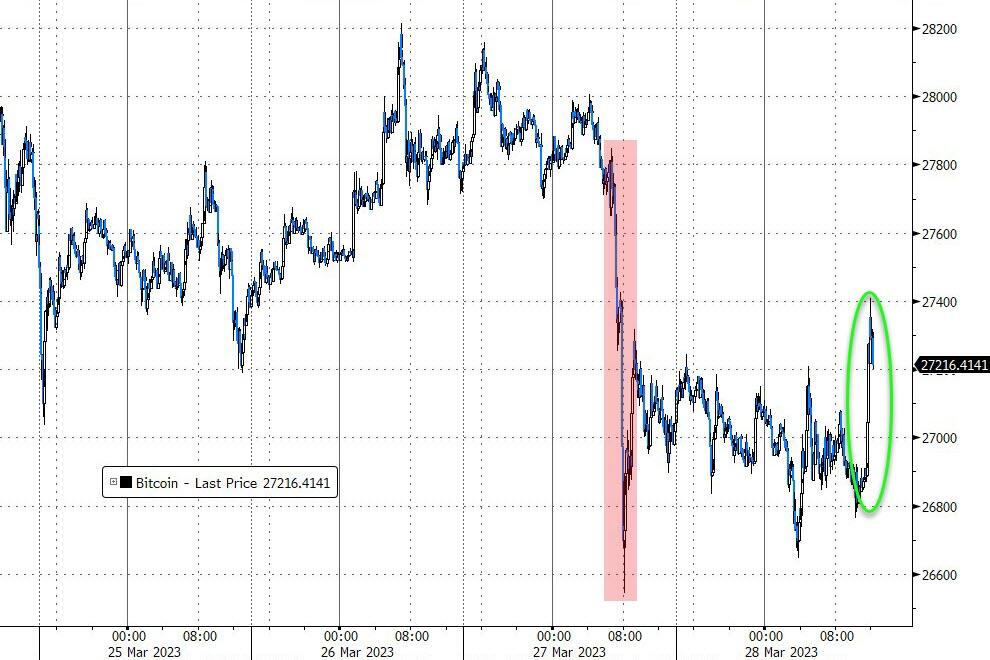

Bitcoin morning price:, $27,261 UP 771 Dollars

Bitcoin: afternoon price: $27,120 DOWN 630 dollars

Platinum price closing $982,30 DOWN $14.00

Palladium price; closing $1437.00 UP $7.30

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2681.45 UP 7.63 CDN dollars per oz (ALL TIME HIGH 2732.50)

BRITISH GOLD: 1598,03 UP 1.50 pounds per oz//(ALL TIME HIGH//1629.84)

EURO GOLD: 1813.83 UP 1.14 euros per oz //(ALL TIME HIGH//1860.82)

363 H WELLS FARGO SEC 468 435 H SCOTIA CAPITAL 18 624 H BOFA SECURITIES 840 661 C JP MORGAN 1 661 H JP MORGAN 400 737 C ADVANTAGE 4 880 H CITIGROUP 1 905 C ADM 4

TOTAL: 868 868

MONTH TO DATE: 6,070END

COMEX DATA EXCHANGE:

: COMEX 868 CONTRACTS

:

JPMORGAN stopped 0/868 contracts

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR MAR/2023. CONTRACT: 868 NOTICES FOR 86800 OZ or 2.6998 TONNES

total notices so far: 6070 contracts for 607,000 oz (18.880 tonnes)

SILVER NOTICES: 5 NOTICE(S) FILED FOR 25,000 OZ/

total number of notices filed so far this month : 3160 for 15,850000 oz

END

GLD

WITH GOLD UP $19.70

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:////// A HUGE WITHDRAWAL OF 0.86 TONNES FROM THE GLD.

INVENTORY RESTS AT 923.07 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP 28 CENTS

AT THE SLV// SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF OF 0.368 MILLION OZ FROM THE SLV: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 458.887MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 157 TO 117,842 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS SMALL SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.15 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. WITH YESTERDAY’S READING AT THE COMEX, WE HAVE NOW SET ANOTHER RECORD LOW AT 117,682 CONTRACTS , MARCH 27.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.15). BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A GIGANTIC GAIN ON OUR TWO EXCHANGES 1232 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 1 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD: A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS( 1075 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 15.58 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S ZERO JUMP TO LONDON OF nil OZ//NEW STANDING: 15.915 MILLION OZ + THE 1.0 MILLION OZ OF EXCHANGE FOR RISK//THUS TOTAL NEW STANDING 16.915 MILLION OZ/ //// V) SMALL SIZED COMEX OI GAIN/ HUGE SIZED EFP ISSUANCE/. WE HAVE NOW REACHED THE POINT THAT THE CROOKS CANNOT LIQUIDATE ANY MORE SILVER SPEC LONGS.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –46 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAR. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTRACTS for 20 days, total 16,993 contracts: OR 84.965 MILLION OZ . (849 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 84.965 MILLION OZ

.

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 84.965 MILLION OZ//INITIAL//STRONG ISSUANCE BUT BELOW LAST MONTH

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 157 CONTRACTS DESPITE OUR $0.15 LOSS IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 1075 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAR OF 15.58 MILLION OZ//FIRST DAY NOTICE// FOLLOWED BY TODAY’S ZERO OZ/QUEUE JUMP (WHICH INCREASES THE AMOUNT OF SILVER STANDING) + 1.0 MILLION OF EXCHANGE FOR RISK ISSUED EARLY IN MARCH (INCREASES THE AMOUNT OF SILVER STANDING) //NEW STANDING 16.915 MILLION OZ .. WE HAVE A HUGE SIZED GAIN OF 1232 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 5 NOTICE(S) FILED TODAY FOR 25,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GOOD SIZED 6508 CONTRACTS TO 483,178AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED-1370 CONTRACTS.

WE HAD A GOOD SIZED DECREASE IN COMEX OI ( 5,138 CONTRACTS) WITH OUR $28.50 LOSS IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR MAR. AT 4.9953 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 86,500 OZ (2.6905TONNES) //(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)YET ALL OF..THIS HAPPENED WITH OUR $28,50 LOSS IN PRICEWITH RESPECT TO MONDAY’S TRADING

WE HAD A FAIR SIZED LOSS OF 3,442 OI CONTRACTS (10.706 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 3066 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 483,178.

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3442 CONTRACTS WITH 6508 CONTRACTS DECREASED AT THE COMEX AND 3066 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 3442 CONTRACTS OR 10.706 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3066 CONTRACTS) ACCOMPANYING THE GOOD SIZED LOSS IN COMEX OI (6508) //TOTAL LOSS IN THE TWO EXCHANGES 3442 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR MAR. AT 4.9953 TONNES FOLLOWED BY TODAY’S 86,500OZ QUEUE JUMP//NEW STANDING 19.0139TONNES // ///3) SOME LONG LIQUIDATION //4) GOOD SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

TOTAL EFP CONTRACTS ISSUED: 86,130 CONTRACTS OR 8,613,000OZ OR 267.90TONNES IN 20 TRADING DAY(S) AND THUS AVERAGING: 4307EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20TRADING DAY(S) IN TONNES 267.90 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 267.90/3550 x 100% TONNES 7.54% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 267.90 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A SMALL SIZED 157 CONTRACTS OI TO 117,842 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,685 CONTRACTS MARCH 27/2022

EFP ISSUANCE 1075 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1075 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1075 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 233 CONTRACTS AND ADD TO THE 1075 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE GAIN OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1232 CONTRACTS.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES //6.160 MILLION OZ

OCCURRED DESPITE OUR $0.15 LOSS IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

i)TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED DOWN 6.02 PTS OR 0.19% //Hang Sang CLOSED UP 216.96BPTS OR 1.11% /The Nikkei closed UP 41.38 PTS OR 0.15% //Australia’s all ordinaries CLOSED UP 1.04% /Chinese yuan (ONSHORE) closed DOWN TO 6.8821//OFFSHORE CHINESE YUAN DOWN TO 6.8849 /Oil UP TO 73.25 dollars per barrel for WTI and BRENT AT 78.53 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 6508 CONTRACTS UP TO 483,174WITH OUR STRONG LOSS IN PRICE OF $28.50 ON MONDAY

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAR… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3066 EFP CONTRACTS WERE ISSUED: : APRIL 3066 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3066 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR TOTAL OF 3,442 CONTRACTS IN THAT 3066LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED LOSS OF 6508 COMEX CONTRACTS..AND THIS FAIR SIZED LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR STRONG LOSS IN PRICE OF $28.50 WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAR (19.0139) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0139 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $28.50 //// AND WERE SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD OUR FAIR SIZED LOSS OF 3,442 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE LOST A TOTAL OI OF 10.706 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAR. (4.9953 TONNES) FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 86500OZ (2.69 TONNES)… ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $28.50.

WE HAD -1370 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 3442 CONTRACTS OR 344,200 OZ OR 10.706 TONNES

TONNES

Estimated gold comex today 289,178/ //fair

final gold volumes/yesterday 320,696///FAIR TO GOOD

Total monthly oz gold served (contracts) so far this month

6070 notices 607 18.880 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 0

total withdrawals: NIL oz

in tonnes:

0

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of MARCH we have an oi of 911 contracts having GAINED 862 contracts. We had 4 notices filed on MONDAY so we

gained 865 contracts or an additional 86,500 oz will stand for metal at the comex . IT SEEMS THAT OUR GOOD FRIENDS IN LONDON WHERE WAITING IN THE WINGS FOR THE ATTACK AND GOBBLED UP CONSIDERABLE PHYSICAL GOLD.

April LOST A CONSIDERABLE 26,904 contracts DOWN to 77,597 contracts. It is here that our banker friends have to worry as many will try and take delivery in this upcoming delivery month. WE HAVE 3 MORE READING DAYS BEFORE FIRST DAY NOTICE.

May GAINED 156 contracts to stand at 1222

We had 868 notice(s) filed today for 86800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 868 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the MAR. /2023. contract month,

we take the total number of notices filed so far for the month (6070 x 100 oz ), to which we add the difference between the open interest for the front month of (MAR. 911 CONTRACTS) minus the number of notices served upon today 868x 100 oz per contract equals 611,300 OZ OR 19.0139 TONNES the number of TONNES standing in this active month of MARCH.

thus the INITIAL standings for gold for the MAR contract month:No of notices filed so far (6070 x 100 oz+ 911 OI for the front month minus the number of notices served upon today (868)x 100 oz} which equals 611,300 oz standing OR 19.0139 TONNES in this active delivery month of MARCH..

TOTAL COMEX GOLD STANDING: 19.0139 TONNES WHICH IS HUGE FOR AN INACTIVE DELIVERY MONTH.

To calculate the number of silver ounces that will stand for delivery in MARCH. we take the total number of notices filed for the month so far at 3160 x 5,000 oz = 15,880,000 oz

to which we add the difference between the open interest for the front month of MAR(28) and the number of notices served upon today 5 (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAR./2023 contract month: 3160(notices served so far) x 5000 oz + OI for the front month of MAR (28) – number of notices served upon today (5 x 500 oz of silver standing for the MAR. contract month equates 15.910 million oz +the 1.0 million oz of exchange for risk//new total standing 16.910 million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

MARCH 28/WITH GOLD UP $19.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

MARCH 15/THE IDES OF MARCH: WITH GOLD UP $18.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 913.27 TONNES

MARCH 14/WITH GOLD DOWN $4.75 TODAY: HUGE CHANGES: A MONSTER DEPOSIT OF 11.85 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 913.27 TONNES

MARCH 13/WITH GOLD UP $48.85 TODAY: VERY STRANGE HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY REST AT 901.42 TONNES

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

FEB 28/WITH GOLD UP $12.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 917.61 TONNES

FEB 27/WITH GOLD UP $6.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.32 TONNES

FEB 24/WITH GOLD DOWN $9.10 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 917.32 TONNES

FEB 23/WITH GOLD DOWN $13.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 919.92 TONNES

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

GLD INVENTORY: 923.07 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

MARCH 17/WITH SILVER UP 79 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE WITHDRAWAL OF 10.478 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 462.748 MILLION OZ//

MARCH 16/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 5.009 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 473.226 MILLION OZ//

MARCH 15/WITH SILVER DOWN 7 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 643,000 OZ INTO THE SLV//INVENTORY RESTS AT 478.235 MILLION OZ/

MARCH 14/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.287 MILLION OZ FROM THE SLV////INVENTORY REST AT 477.592 MILLION OZ//

MARCH 13/WITH SILVER UP $1.35 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ//

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWALOF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

FEB 28/WITH SILVER UP 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.241 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.188

FEB 27/WITH SILVER DOWN 15 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.471 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 482.429 MILLION OZ

FEB 24/WITH SILVER DOWN 46 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.172 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.900 MILLION OZ//

FEB 23/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.072 MILLION OZ//

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 459.255 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

end

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards/John Rubino

3,Chris Powell of GATA provides to us very important physical commentaries

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

END

5.IMPORTANT COMMENTARIES ON COMMODITIES: LITHIUM

END

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

SBF Charged With Funneling $40M In Crypto To Bribe CCP Officials

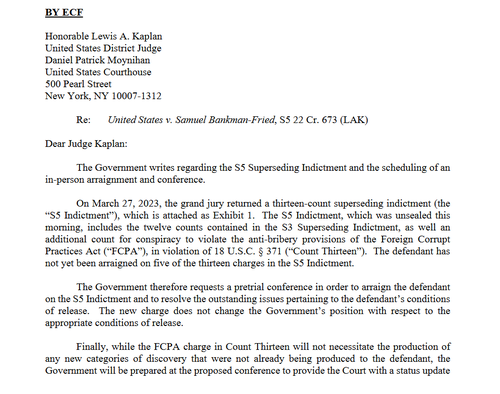

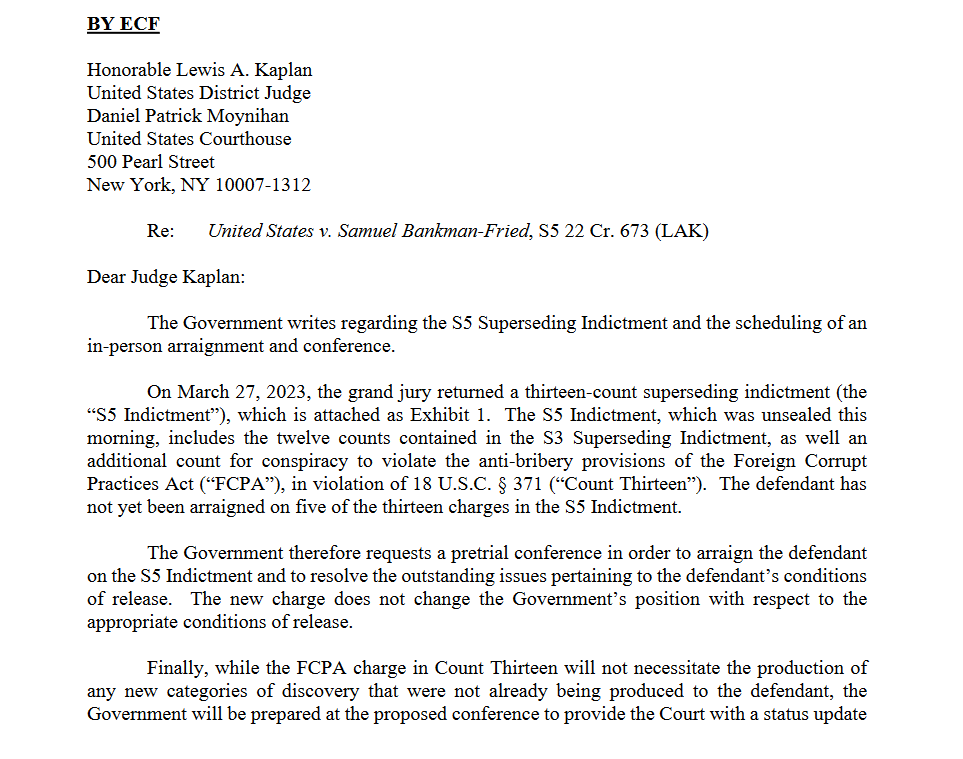

TUESDAY, MAR 28, 2023 – 04:39 PM

Federal prosecutors in Manhattan have hit FTX founder Sam Bankman Fried (“SBF”) with a new 13-count indictment accusing him of funneling $40 million in cryptocurrency to ‘one or more’ Chinese government officials, in order to “influence and induce them” to unfreeze Alameda Research trading accounts holding over $1 billion in crypto.

He is accused of conspiring to violate anti-bribery provisions of the Foreign Corrupt Practices Act.

In the Tuesday court filing, prosecutors asked US District Judge Lewis Kaplan to arrange a court hearing in order to arraign Bankman-Fried on the new charges.

“The S5 Indictment, which was unsealed this morning, includes the twelve counts contained in the S3 Superseding Indictment, as well an additional count for conspiracy to violate the anti-bribery provisions of the Foreign Corrupt Practices Act (‘FCPA’), in violation of 18 U.S.C. § 371,” reads a letter to the judge, Coindesk reports.

The 31-year-old previously pleaded guilty to eight counts related to the collapse of FTX, after prosecutors accused him of stealing billions of dollars in customer assets to try and stop Alameda Research – his crypto hedge fund – from imploding.

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 6.8821

OFFSHORE YUAN: 6.8849

SHANGHAI CLOSED DOWN 6.02 PTS OR 0.19%

HANG SANG CLOSED UP 216.996PTS OR 1.11%

2. Nikkei closed UP 46.38 PTS OR 0.15%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 102.26 EURO RISES TO 1.0828 UP 122 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.319 J apan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 130.97 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: UP-// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.290***/Italian 10 Yr bond yield RISES to 4,156*** /SPAIN 10 YR BOND YIELD RISES TO 3.335…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.160

3j Gold at $1956.60silver at: 23.04 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 5/100 roubles/dollar; ROUBLE AT 76.57//

3m oil into the 73 dollar handle for WTI and 78 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 130.97 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .319% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9168as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9864 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.554 UP 3 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.762 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.023 UP 6 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.11…

GREAT BRITAIN/10 YEAR YIELD: UP 13 BASIS PTS AT 3.489

end

2. Overnight: Newsquawk and Zero hedge:

Futures Flat As Attention Turns To Fed Rate Hikes

TUESDAY, MAR 28, 2023 – 03:09 PM

US futures are flat with bond yields reversing an overnight drop, lifted by the belly of the curve; the USD weaker for 8 of the past 9 days, and commodities mostly higher as investors shift their focus back to concerns about inflation and potential further monetary tightening from the recent banking-industry chaos; after all, a bank hasn’t failed in at least a few days. WTI has soared 5.6% this week.

S&P 500 contracts were little changed as of 7:45 a.m. ET, after earlier gaining as much as 0.4% and closing 0.2% higher on Monday. Nasdaq 100 futures slid 0.2% after the tech-heavy benchmark lost 0.7% on Monday following strong gains over the previous two weeks. European stocks advanced along with Asian equities and the dollar traded lower as fears of broader contagion from the banking turmoil eased.

According to JPM, If bank contagion fears subside, we may see a resurgence in both bond yields and commodities as growth, before the banking crises, was stronger than expected led by the US and a reopened China. “However, banking crises typically have wide-ranging, and negative, impacts on growth and employment.” Today’s macro data focus includes inventories, housing prices, regional mfg updates, and Consumer Confidence. Keep an eye on the confidence number as that can impact spending.

In premarket trading, Alibaba shares soared 9% after the Chinese e-commerce company planned to split into six units that will individually explore IPOs. Shares in fellow Chinese ADRs also rallied. First Republic Bank gained 3.1% adding to a 12% jump on Monday after First Citizens BancShares’s agreement to buy Silicon Valley Bank reassured investors in regional lenders. PVH climbed 12% in premarket as the owner of Calvin Klein and Tommy Hilfiger issued stronger-than-expected earnings forecasts. Lyft rose as much as 5.2% after the ridesharing company appointed David Risher as CEO. Here are some other notable premarket movers:

Array Technologies gains 3.7% after Truist Securities raises the solar equipment manufacturer to buy from hold, saying it has made significant progress addressing past challenges related to its product portfolio, execution and margin structure.

Carnival Corp. is raised to equal-weight from underweight at Wells Fargo as the cruise operator has low near-term refinancing risk, its business in Europe is holding up well, and its annual Ebitda forecast is reasonable. Its shares gain 1.7% after dropping 4.8% on Monday following its earnings report.

Ciena Corp. shares are up 3.2% in premarket trading after Raymond James upgraded the communications equipment company to strong buy from outperform.

Occidental Petroleum advances as much as 2.2% after being upgraded to outperform from market perform at Cowen, with the broker saying the oil and gas company stands out for its “superior” exposure to oil pricing, share support, capital structure and differentiated catalyst rich profile. .

PVH shares surge 12% after the parent company of Calvin Klein and Tommy Hilfiger issued stronger-than-expected forecasts for revenue growth and reported fourth-quarter earnings per share that beat estimates. Analysts found the company’s performance to be strong, flagging the beat to EPS as well as the strong outlook. .

Viking Therapeutics said it plans to initiate a Phase 2 study of VK2735 in patients with obesity in mid-2023 based on Phase 1 trial results. Shares gain 50%.

Virgin Orbit fell more than 9.5% after the launch provider placed workers on furlough as it seeks rescue financing or bankruptcy.

“For now, it looks like the major stress around the banking crisis is calming down and markets can switch back to monitoring the inflation-recession dynamics,” said Marija Veitmane, senior multi-asset strategist at State Street Global Markets in London.

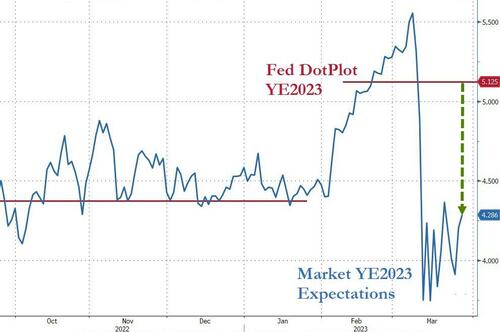

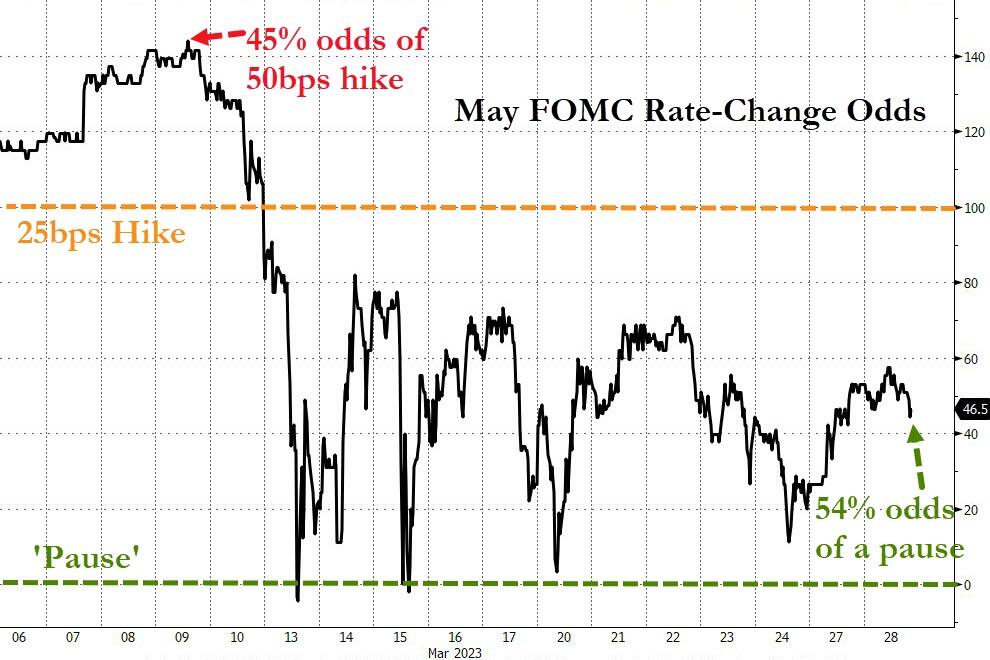

As jitters in the banking sector subside, investors are again turning their attention to economic fundamentals and the outlook for Federal Reserve policy. Swaps have meanwhile priced in a more than 50% probability of a rate hike at the next meeting; they continue to expect sharp easing later however, with pricing suggesting the policy rate will slide to around 4.3% in December, down from around 4.95% in May.

Not all agree. “We see major central banks moving away from a ‘whatever it takes’ approach, stopping their hikes and entering a more nuanced phase that’s less about a relentless fight against inflation but still one where they can’t cut rates,” strategists at BlackRock Investment Institute, including Wei Li and Alex Brazier, wrote in a note.

Hugh Gimber, global market strategist at JPMorgan Asset Management, also doesn’t foresee rate cuts anytime soon, even if hikes pause, and cautions against stock-market optimism on it. “I think the market is right to price a Fed pause,” he said in an interview on Bloomberg TV. “The question here is how big the feed through from a deterioration in lending standards is to really get inflation lower towards target, and I’m not that convinced we will see that very quickly. I think we would need a pretty significant economic shock to get there in 2H. Rate cuts are more of a 2024 story.”

European stocks are in the green although they’ve pared gains since the open as investors remain cautious amid risks to the global financial system. The Stoxx 600 has trims gains to 0.2% while Deutsche Bank swings to a ~2% fall from from ~2% rise. Energy, miners and autos are the strongest-performing sectors. Here are the most notable European movers:

GSK gains as much as 0.9% after it announced positive results from an endometrial cancer drug trial. Shore Capital describes the published data as “promising”

Ocado shares rise as much as 5.7% after the online grocer’s retail joint venture with Marks & Spencer beat sales expectations in the first quarter

Zalando shares rise as much as 3.2% as HSBC upgrades the online fashion retailer to buy from hold, saying its momentum is moving in the right direction

Marks & Spencer shares gain as much as 3.1% as Credit Suisse hikes its price target, saying the UK retailer’s recovery momentum is building

Eurocash jumps as much as 11% after the retailer posted record 4Q Ebitda of 308m zloty and cut debt ratios, seen by analysts as a soothing signal

Telecom Italia shares rise as much as 3.4% after Bloomberg reported that Italian state-backed lender CDP plans to raise its offer for the carrier’s landline network

Diageo shares slip as much as 0.9% after the British distiller said Ivan Menezes plans to retire as chief executive officer, which analysts say is a loss

Embracer shares slump as much as 15%, after the video-game maker said licensing deals with several industry partners are unlikely to be completed before the month ends

Norma shares fall as much as 15% as Baader highlights the tech hardware firm’s conservative FY23 margin outlook due to ongoing burdens from efforts to restructure

CMC Markets falls as much as 6.3%, adding to a 21% drop Monday when the online trading company released a downbeat earnings update late in the session

Schibsted shares drop as much as 9.6% as a weaker short-term guidance for the Norwegian media and classified advertising group offsets higher longer-term targets

Synthomer shares drop as much as 19% with Morgan Stanley saying it sees further consensus downgrades ahead for the UK chemicals firm following its FY results

Elsewhere in markets, Asian stocks gained as a lull in new developments in the banking sector gave investors a chance to adjust positions and assess whether the Federal Reserve will lower rates to buttress the US economy. The MSCI Asia Pacific Index rose as much as 0.9%, halting a two-day losing streak. A sub-gauge of financial shares jumped more than 1% as they followed US peers higher. Australia, Japan and South Korea advanced. Hong Kong’s Hang Seng Index gained about 1%, while China’s mainland indexes fluctuated. “Asia still remains relatively well insulated from the latest round of US/European bank turmoil,” Citigroup analysts including Johanna Chua wrote in a note. “Direct exposure of Asia to the affected financial institutions is very limited.” Asia’s regional equity gauge has climbed more than 2% over the past week as US bank shares regained their footing after tumbling last week and fanning fears of a looming economic slowdown. Doubleline Capital’s Jeffrey Gundlach said on CNBC that he expects a US recession to start in a few months, and that the Federal Reserve will need to respond “very dramatically.”

Japanese stocks rose for a second day as concerns around financial institutions cooled after First Citizens BancShares Inc. agreed to buy failed Silicon Valley Bank. The Topix rose 0.2% to close at 1,966.67, while the Nikkei advanced 0.2% to 27,518.25. Sumitomo Mitsui Financial Group contributed the most to the Topix gain, increasing 2.7%. Out of 2,159 stocks in the index, 799 rose and 1,232 fell, while 128 were unchanged. “Overall risk tolerance has increased now that the Silicon Valley Bank situation appears to have calmed down,” said Ryuta Otsuka, strategist at Toyo Securities. “However, it is hard to expect large market moves in Japan as we are approaching the end of the fiscal year.”

Australian stocks extended rose with the S&P/ASX 200 index rising 1% to close at 7,034.10, extending gains for a second session, boosted by mining shares and banks. Lithium miners, some of the benchmark’s most shorted names, rallied after Liontown rebuffed a takeover bid from Albemarle. Equities across Asia climbed, US stock futures edged higher and the dollar declined as fears of broader contagion from the banking turmoil eased. Investors await Australia’s CPI print due Wednesday. In New Zealand, the S&P/NZX 50 index rose 1.4% to 11,771.27

Stocks in India were mostly lower on Tuesday as key gauges headed for their fourth consecutive monthly decline amid tepid sentiment for global equities. The S&P BSE Sensex fell 0.1% to 57,613.72 in Mumbai, while the NSE Nifty 50 Index declined 0.2%. The benchmark gauge has slipped about 2.1% this month and is on course for its longest losing monthly streak since Feb. 2016. Software major Infosys contributed the most to the Sensex’s decline, decreasing 0.8%. Out of 30 shares in the Sensex index, 11 rose, while 19 fell. All 10 companies related to the Adani Group fell, led by a 7% plunge in flagship firm Adani Enterprises after a newspaper report said the conglomerate will probably seek more time to repay a $4 billion loan it took out last year. Foreign investors have been buyers of $1.3b of local shares this month through March 24, mainly on back of GQG Partners’ stake purchase in Adani companies. “Barring gains in select banking and metal stocks, other sectors witnessed profit-taking as caution prevailed ahead of the F&O expiry on Wednesday,” Kotak Securities analyst Shrikant Chouhan said.

In FX, the Bloomberg Dollar Spot Index slipped 0.1%, marking its eighth day of declines in the past nine sessions, weighed by a jump in the yen on domestic demand ahead of the fiscal year-end in Japan. Exporters in Japan and Australia added to the selling of the dollar as they increased hedging to cover prior long positions in the greenback, Asia- based FX traders said. The New Zealand dollar and Japanese yen are the best performers among the G-10s while the Swiss franc is the weakest.

In rates, the five-year Treasury yield rises as much as 7 basis points to 3.67%, while the two-year yield climbs 4 basis points to 4.04% after sliding as low as 3.89% earlier in the session; a selloff in Treasuries since the start of the week has lifted most yields from six-month lows reached on Friday. 10-year yields around 3.55%, cheaper by 2bps on the day with bunds lagging by additional 5bp in the sector; 2-year yields cheaper by around 7bp on the day, remain above 4% level vs. Monday’s 3.954% auction stop. As BBG’s Beth Stanton notes, Monday’s poorly-bid 2Y auction is now under water vs its 3.954% stop with May rate hike back in favor. Auction cycle continues with $43b 5Y at 1pm. WI yield 3.65% is between last two 5Y stops. The US auction cycle resumes with $43b 5-year note sale at 1pm, follows Monday’s poor 2-year result; WI 5-year at 3.63% is ~48bp richer than February’s stop-out. German two-year borrowing costs are up 12bps.

Traders are now betting on a roughly 50/50 chance that the Fed will deliver a final quarter-point hike in May, followed by a similar-sized cut in September; market pricing reflects a diminishing outlook for a series of cuts in the coming months, and a growing view that the Fed may keep rates on hold for longer. BlackRock sees the Fed continuing to raise interest rates despite traders betting otherwise as fears of a banking crisis convulse markets. “We don’t see rate cuts this year – that’s the old playbook when central banks would rush to rescue the economy as recession hit,” its strategists write in a note. “We see a new, more nuanced phase of curbing inflation ahead: less fighting but still no rate cuts.”

In commodities, crude futures advance with WTI up 0.5% to trade near $73.15. Spot gold falls 0.3% to around $1,951. European and US gas benchmarks diverge slightly in European trade; Morgan Stanley writes that “prices likely still need to move lower to incentivize an adequate supply response, but we may be approaching the bottom”.

Looking to the day ahead, we will have a number of data releases from the US including the Conference Board consumer confidence, the Richmond Fed manufacturing index and business conditions, the Dallas Fed services activity, the January FHFA house price index, and February’s wholesale and retail inventories and advance goods trade balance. We will also have Italy’s March manufacturing and consumer confidence as well as economic sentiment data, and from France the March manufacturing and consumer confidence data. The BoE’s Bailey will testify today on the Silicon Valley Bank crisis, and we will also hear from ECB’s Muller. Finally, we will have earnings releases from Micron, Walgreens Boots Alliance and Lululemon.

Market Snapshot

S&P 500 futures little changed at 4,009.00

STOXX Europe 600 up 0.3% to 446.06

MXAP up 0.6% to 159.53

MXAPJ up 0.6% to 512.94

Nikkei up 0.2% to 27,518.25

Topix up 0.2% to 1,966.67

Hang Seng Index up 1.1% to 19,784.65

Shanghai Composite down 0.2% to 3,245.38

Sensex little changed at 57,596.88

Australia S&P/ASX 200 up 1.0% to 7,034.09

Kospi up 1.1% to 2,434.94

German 10Y yield little changed at 2.30%

Euro up 0.2% to $1.0818

Brent Futures up 0.5% to $78.49/bbl

Gold spot down 0.2% to $1,952.30

US Dollar Index down 0.17% to 102.69

Top Overnight News

Alibaba plans to split its $220 billion business into six main units encompassing e-commerce, media and the cloud, each of which will explore fundraising or IPOs when the time’s right. Group CEO Daniel Zhang will head up the cloud intelligence division, a nod to the growing role AI will play in the e-commerce leader’s portfolio in the long run. BBG

Binance’s CEO Changpeng Zhao shot back at the CFTC, calling its lawsuit over alleged violations of derivatives regulations “unexpected and disappointing,” given compliance efforts and cooperation with regulators. His firm doesn’t trade for profit or manipulate the market, he said. The suit has “an incomplete recitation of facts.” BBG

China has significantly expanded its bailout lending as its Belt and Road Initiative blows up following a series of debt write-offs, scandal-ridden projects and allegations of corruption. A study published on Tuesday shows China granted $104bn worth of rescue loans to developing countries between 2019 and the end of 2021. The figure for these years is almost as large as the country’s bailout lending over the previous two decades. FT

Semiconductor companies seeking federal grants under the Chips Act could face a tough decision: take Washington’s help to expand in the U.S., or preserve their ability to expand in China. The Biden administration last week proposed new rules detailing restrictions chip companies would face on operations in China and other countries of concern if the companies accept taxpayer funding. WSJ

Balances at the Fed’s RRP facility climbed, even as rates in the private market rose as much as 15 bps above the central bank’s offering yield. Ninety-eight counterparties parked $2.22 trillion at the RRP, up $1.7 billion from Friday. BBG

The Federal Reserve’s top official on banking supervision has blamed the collapse of Silicon Valley Bank on a “textbook case of mismanagement”, saying the board of the US central bank had been briefed on the troubles at the California lender in mid-February. FT

The Treasury’s top domestic policy official Nellie Liang will tell Congress regulators are ready to repeat steps taken after recent bank failures. She testifies today with the Fed’s chief of banking supervision, Michael Barr, and FDIC head Martin Gruenberg. The ECB’s top oversight official urged global scrutiny of the CDS market. And BOE boss Andrew Bailey said UK banks are strong. BBG

Calm returned to Israeli cities Tuesday and protests against Israeli Prime Minister Benjamin Netanyahu’s judicial overhaul dispersed after the premier agreed to suspend the controversial plan and Israeli President Isaac Herzog offered to host compromise talks between the two sides. WSJ

DIS has eliminated its next-generation storytelling and consumer experiences unit, the small division that was developing metaverse strategies, according to people familiar with the situation, as part of a broader restructuring that is expected to reduce head count by around 7,000 across the company over the next two months. WSJ

In the battle for the biggest prize in China’s trillion-dollar pension market, BlackRock Inc. and other global firms have little chance of attracting clients like Judy Deng: BBG

The Federal Deposit Insurance Corp. stuck to its guns and didn’t offer bailouts to keep two lenders from collapsing. Instead, it struck deals that included millions of dollars of sweeteners for the acquiring banks that sent their stocks soaring: BBG

The US took its most forceful move yet on Monday to crack down on crypto exchange Binance Holdings Ltd. and its chief executive officer Changpeng Zhao: BBG

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded mixed with a mild positive bias as global banking sector fears continued to dissipate and with early advances led by energy after the recent surge in oil prices although gains were capped in the region as North Korean nuclear rhetoric stoked geopolitical concerns. ASX 200 was boosted amid strength in the commodity-related sectors with outperformance in energy after oil prices notched the largest daily gain since October and financials were also lifted as Australia downplayed the risks to domestic banks from the recent global banking issues. Nikkei 225 was indecisive despite Japan reiterating plans for a JPY 2.2tln economic stimulus package with trade stuck in a narrow range near 27,500 after the nuclear rhetoric by North Korea which called for the scaling up of weapons-grade nuclear materials and included similar language used before its last nuclear test in 2017. Hang Seng and Shanghai Comp. were choppy ahead of key earnings results and after PBoC liquidity efforts.

Top Asian News

China’s Foreign Ministry said Premier Li Qiang met with foreign representatives at the China Development Forum in Beijing on Monday and met with executives including Apple (AAPL) CEO Cook, while Li told executives China will unswervingly expand its opening up, according to Reuters.

US and Japan reached a trade deal for critical EV battery minerals in which the deal prohibits enacting export restrictions on lithium, cobalt, nickel, manganese and graphite, according to US officials. Furthermore, the deal includes provisions to combat non-market practices, while access for Japanese automakers to the battery minerals portion of USD 7,500 in US EV tax credit depends on the tax guidance this week from the US Treasury.

China is reportedly aiming to set up 30+ key auto chips standards by 2025, according to the Ministry of Industry and Information Technology.

A magnitude 5.7-5.9 earthquake occurred offshore Eastern Aomori Prefecture, Japan; NHK says it has a prelim. magnitude of 6.1; no tsunami warning issued.

European bourses were initially firmer across the board in a continuation of the APAC tone, though benchmarks have since eased from best and are flat/mixed. Sectors are mixed with Energy outperforming while Banking names were firmer but have eased off of best levels and incrementally into the red alongside the broader benchmarks throughout the morning. Stateside, futures are mixed/flat, though with the bias inching further into the red, as the region awaits todays Senate Banking Committee hearing on the recent banking turmoil with Fed’ Barr in attendance. Meta Platforms Inc. (META) plans to lower some bonus payouts and will more frequently assess employee performance, according to an internal memo, part of a sweeping revamp of the social-media company that includes large head-count reductions, WSJ reports. Alibaba (BABA/9988 HK) business unit can reportedly pursue fundraising and IPOs when ready, according to Bloomberg; Alibaba to restructure into six main business divisions.

Top European News

Kantar UK Supermarket update (Mar): Grocery price inflation has climbed again to reach 17.5% over the four weeks to 19 March 2023, a new record based on our latest market data.

ECB’s Muller says inflation is slowing but it is too early to declare a victory.

Banks

ECB’s Enria says current events confirm that strong, demanding supervision is needed more than ever. Adds, there have been some fast outflows of bank deposits in some cases.

BoE’s Bailey says does not think any of the features of recent banks issues are causing stress in the UK; Ramsden says will keep a close eye on bank funding costs.

US Treasury official Liang said the US government will use tools to prevent banking contagion again if warranted and that the US financial system is significantly stronger now due to stronger capital and liquidity requirements, while she added the US must ensure that banking regulations and supervision are appropriate for today’s risk and challenges, according to her prepared testimony, according to Reuters.

French PNF Financial Prosecutors says searches are underway at five banking/financial firms located within Paris and the Paris La Defense district re. a tax probe, German prosecutors assisting. Societe General (GLE FP) confirms its offices are being searched.

S&P says they are yet to see any meaningful contagion for APAC from the US regional banks/Credit Suisse (CSGN SW) turmoil.

FX

The USD has been incrementally softer throughout the morning within relatively narrow 102.52-102.76 parameters, most recently the DXY has attempted to pare initial downside.

Action which comes to the mixed fortune of peers, with AUD, NZD and JPY outperforming given the risk tone and as the JPY attempts to recover from Monday’s pressures; holding below 0.67, 0.625 and above 131.00 respectively.

CHF resides as the laggard, with downside seemingly stemming from the risk tone rather than any fresh Swiss banking concern, EUR/CHF above 0.99 to a 0.99300 peak.

In close proximity is the CAD which is unable to benefit from crude upside while GBP and EUR are contained around 1.08 and 1.23 respectively vs USD with Central Bank speak thus far not moving the dial.

Citi month-end model: Prelim. estimate points to moderate USD selling vs all major currencies ex-EUR, via Reuters. Click here for more detail.

PBoC set USD/CNY mid-point at 6.8749 vs exp. 6.8737 (prev. 6.8714)

Fixed Income

EGBs are under pressure in a continuation of the firmer risk tone from APAC trade; however, benchmarks are off worst levels as equities inch into the red.

Specifically, Bunds are below 136.00 with the associated 10yr yield firmly above 2.30% though yet to breach 2.35%.

Gilts and the EZ periphery are in-line with mentioned core counterparts and have been unaffected by numerous Central Bank officials where the focus has been on recent banking turmoil.

Supply wise, the Italian and German sales passed without fanfare and were well-received overall though demand was slightly softer when compared to the prior outings.

Commodities

Crude benchmarks continue to climb aided by the softer dollar and the latest geopolitical tensions re. N. Korea; WTI and Brent holding above USD 73/bbl and USD 78/bbl respectively.

European and US gas benchmarks diverge slightly in European trade; Morgan Stanley writes that “prices likely still need to move lower to incentivize an adequate supply response, but we may be approaching the bottom”.

Spot gold is pressured by the risk tone and failing to benefit from the softer USD with the yellow metal below the USD 1959/oz 10-DMA and holding around USD 1950/oz currently, base metals conversely are modestly firmer.

Russian Deputy PM Novak says the domestic fuel and energy complex is sustainable despite challenges, hopes to agree on key contract terms for the Power of Siberia 2 gas pipeline to China this year. Russia should look to produce at least 100mln/T of LNG per year by 2030.

Geopoliitcs

Russian Defence Ministry said it fired supersonic anti-ship missiles at a mock target in the Sea of Japan.

North Korean leader Kim guided the nuclear weaponisation programme and inspected nuclear trigger technology during a recent simulation. Kim also called for constant efforts to improve nuclear capability and said the country should be fully ready to use nuclear weapons at any time, while he called for the scaling up of weapons-grade nuclear materials to exponentially increase nuclear weapons arsenal. North Korea also alleged that US and South Korea military drills involving an air carrier are aimed at pre-emptive nuclear strike and said that US anti-North Korean activities are intensifying to unacceptable levels, according to KCNA.

North Korea is reportedly preparing to resume foreign diplomatic activity after three years of COVID isolation, according to FT; North Korean officials recently resumed travels to Russia and China.

Belarus’ Foreign Minister says they have been forced to take steps ensuring security in the face of NATO potentially increasing within neighbouring nations, via Tass.

Crypto

Binance CEO said the CFTC complaint appears to have an incomplete recitation of the facts and they do not agree with the issues alleged in the complaint. Binance CEO said they intend to respect and collaborate with US and other regulators around the world, while he added that Binance.com does not trade for profit or manipulate the market under any circumstances, according to Reuters.

08:30: Feb. Retail Inventories MoM, est. 0.2%, prior 0.3%

Wholesale Inventories MoM, est. -0.1%, prior -0.4%, revised -0.3%

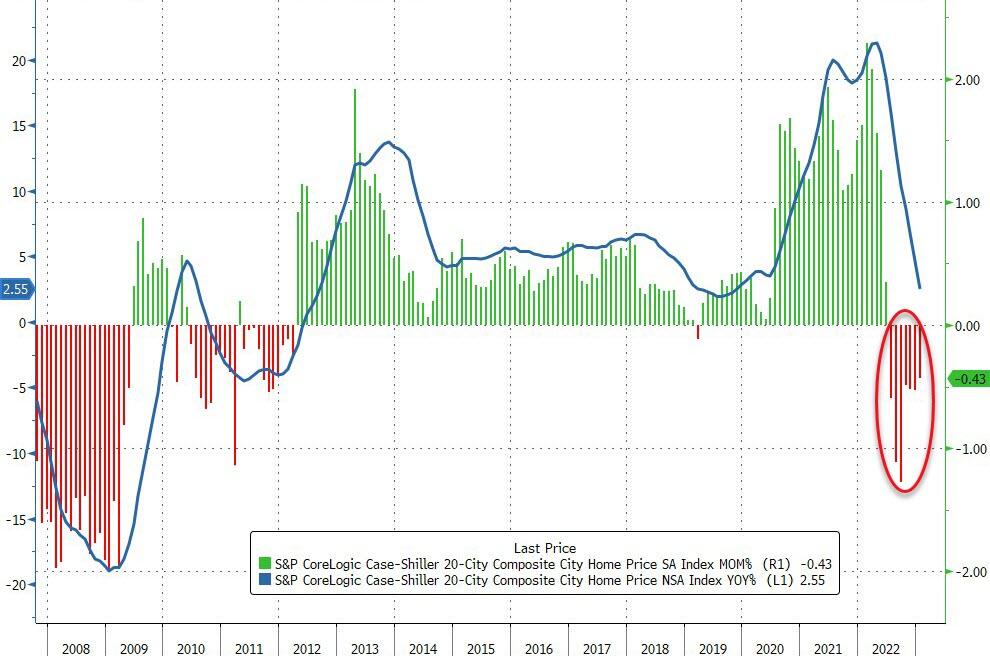

09:00: Jan. FHFA House Price Index MoM, est. -0.2%, prior -0.1%

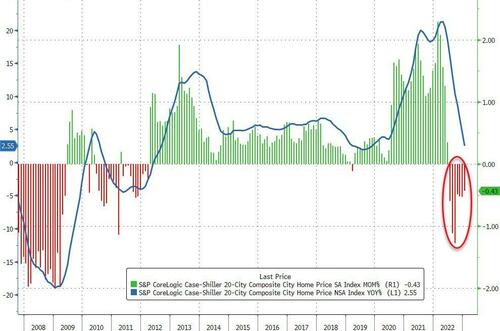

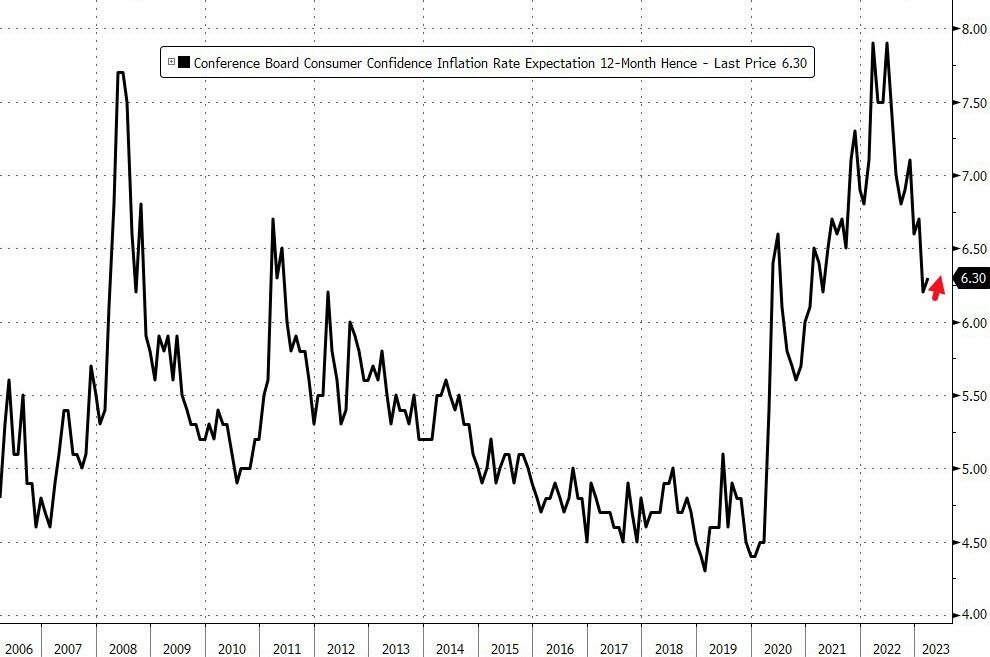

09:00: Jan. S&P Case Shiller Composite-20 YoY, est. 2.55%, prior 4.65%

S&P/Case-Shiller US HPI YoY, prior 5.76%

S&P/CS 20 City MoM SA, est. -0.50%, prior -0.51%

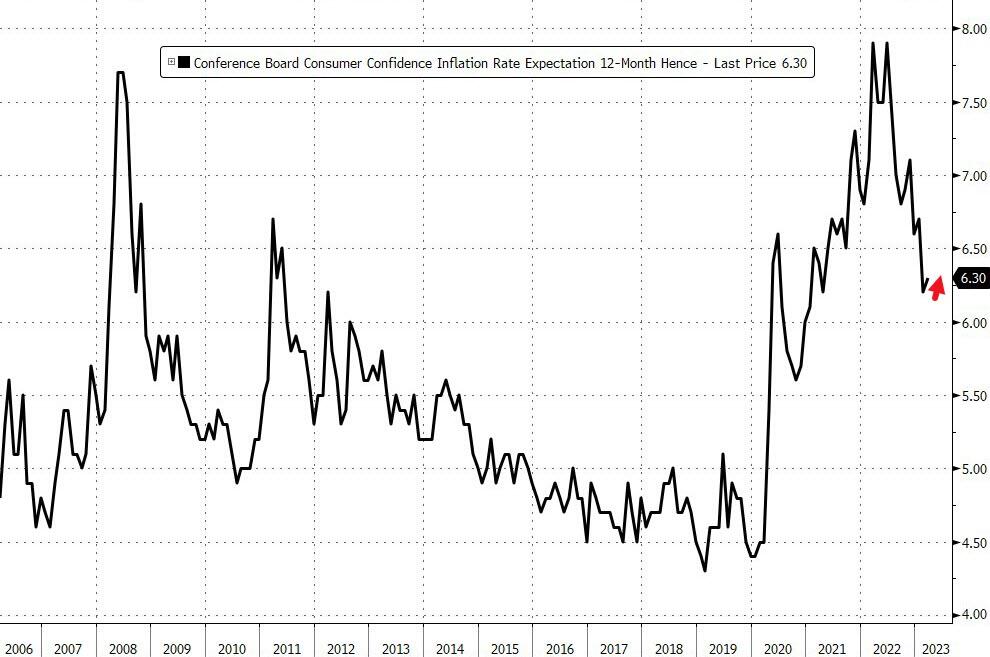

10:00: March Conf. Board Consumer Confidence, est. 101.0, prior 102.9

Expectations, prior 69.7

Present Situation, prior 152.8

10:00: March Richmond Fed Index, est. -10, prior -16

10:30: March Dallas Fed Services Activity, prior -9.3

Central Banks

10:00: Fed’s Barr Appears Before Senate Banking Panel

DB’s Jim Reid concludes the overnight wrap

After a hectic 2 and a half weeks that has felt like a year, the week has started on a much calmer footing. I’m on holiday for a couple of weeks from Thursday so I’m hoping that I don’t have to do zoom meetings from the ski slopes. My ski outfit and technique won’t make that a pretty sight.

As we highlighted in our CoTD yesterday (link here) we have to be careful not to fight the battle of the last war. Large banks in the US and Europe are completely different entities than they were going into the GFC. For large US banks for example, securities and loans/leases on their balance sheets as a % of deposits are lower than when our data starts in 1985 and at below 100% are massively down from their GFC peaks of over 150%. We don’t have the same long term data for Europe but the declines since the GFC are of similar magnitudes.

In contrast corporates are more levered now than during the GFC and this cycle could ultimately be more corporate default focused vs financials as per say 2001-2002 rather than 2008-09. See Steve Caprio’s full note here for more on this and how corporate spreads are too tight to financials now.

So no new news was good news yesterday and some risk premium was removed from the market. This was most evident in bonds with US 2yr and 10yr yields up +22.9 bps and +15.4bps respectively. The S&P 500 was up +0.80% in the first hour of trading but did retrace the entire move back to flat before rallying in the US afternoon to finish with a an overall modest gain of +0.17%, whilst the STOXX 600 climbed +1.05%. US banks led the US move higher, having traded off their lows from last week, with the S&P 500 banks index up +3.05%. European banks were earlier +1.69% higher.

Narrowing in, First Citizens jumped 49% at the market open after its agreement to buy SVB Financial Group’s Silicon Valley Bank, ending the day up by +53.74%. First Republic Bank similarly jumped at the open by +27.45% after a Bloomberg report that US authorities were considering an expansion to their emergency lending facility, the Bank Term Funding Program, that had been created on March 12 with the collapse of SVB and Signature Bank. Against this backdrop, the gauge of regional US banks, the KBW index, closed up +2.54% yesterday, with the leaders including First Republic (+12.14%), Comerica (+5.40%) and KeyCorp (+5.31%).

Improving risk sentiment saw investors pare back their expectations of Fed rate cuts, as the implied rate for the Fed’s May meeting gained +9.2bps, bringing it to 4.950%. In other words, fed futures are now pricing in a 53% chance of a +25bps hike in May. For December’s meeting, markets trimmed their expectations of rate cuts from over -94bps on Friday to nearly -74bps, as the implied rate rose +29.5bps to 4.206%.

Back on this side of the pond, the German March Ifo business confidence index printed above expectations at 91.2 (vs 88.3 expected), and up from 88.5 for February. The other two individual components of the release also beat expectations, with business climate rising to 93.3 (vs 91 expected) and current assessment at 95.4 (vs 94.1 expected). Although the Ifo survey typically demonstrates less sensitivity to financial market uncertainty relative to other surveys coming from Germany such as the ZEW survey, the release is consistent with last Friday’s PMIs that suggested the Eurozone economy remains in, or at least was in decent shape, before the banking crisis hit.

Consequently, the DAX outperformed relative to the broader STOXX 600 index, up +1.14%, whilst the STOXX 600 advanced by +1.05%. For the latter, all major sectors were in the green, with sector leaders including health care (+1.93%), utilities (+1.31%) and autos (+1.89%). The CAC also gained yesterday, up by +0.90%. Following from Friday’s jitters about European banking sector stability, ECB’s Simkus emphasised that ‘bank liquidity, capitalisation (are) high in euro area.’ ECB’s De Cos echoed this sentiment, stating ‘euro-zone banks (are) well-prepared for adverse scenarios’.

We also heard from several other ECB’s speakers yesterday, as ECB’s Schnabel stated she had pushed for the ECB statement to say that more hikes were a possibility as opposed to the verbal assurance that had been made by President Lagarde. ECB’s Centeno’s comments were more dovish, as he stated that they “don’t see long-term inflation expectations de-anchoring”, with “no signs of second-round effects in wage-setting.” Markets moved to price in a modestly higher terminal rate as Eurozone overnight index swaps for July were up +7.5bps bringing the rate to 3.321%. The rate for year-end also increased, up +11.5bps to 3.226%, pricing in a 1 in 3 chance of a -25bps rate cut by December. Against this backdrop, yields across the German sovereign yield curve were up yesterday, with the 10yr bund yield climbing +9.8bps higher bringing the yield to 2.227%. The 2yr yield gained +12.8bps to 2.521%

Asian equity markets are mostly higher overnight. As I type, the Hang Seng (+0.60%), the KOSPI (+0.44%) and the Nikkei (+0.07%) are higher but with stocks in mainland China mixed with the CSI (-0.16%) edging lower while the Shanghai Composite (+0.05%) is oscillating between gains and losses. US stock futures are a little higher with contracts tied to the S&P 500 (+0.16%) and NASDAQ 100 (+0.17%) printing mild gains. Meanwhile, yields on 10yr Treasuries (-1.89bps) are slightly lower, trading at 3.51% while 2Yr Treasuries (-3.5bps) are trading at 3.96% as we go to press.

In early morning data, retail sales in Australia rose +0.2% m/m in February, in-line with market expectations, down from a revised +1.8% increase in January, signifying that households are reining in spending in response to higher interest rates. The subdued data adds to the case for a pause by the Reserve Bank of Australia (RBA) at its April 4th meeting. Meanwhile, the CPI data scheduled to be released tomorrow will be of note for the central bank.

Turning to commodities, WTI crude futures performed strongly yesterday, rising +5.13% to over $72.81/bbl, whilst Brent crude gained +4.17% to $78.12/bbl. European natural gas futures also gained +3.49% yesterday. The rally in energy prices was due to both supply-side and demand-side pressures. On demand, the rally in bank stocks and purchase of SVB seemed to ease concerns of a wider financial crisis. Meanwhile, a legal dispute between the Iraqi semi-autonomous region of Kurdistan and Turkey has put about 400,000 bbl/day of exports in limbo. This come as French refineries are running at a fraction of normal capacity due to the ongoing protests in the country. A Bloomberg report had as much as 80% of the nation’s crude-processing capacity stalled.

Finally, yesterday also saw the release of the Dallas Fed Manufacturing Activity for March which fell below expectations at -15.7 (vs -10 expected). This was a further decline from -13.5 last month as perceptions of broader business conditions deteriorated over the month.

Now looking to the day ahead, we will have a number of data releases from the US including the Conference Board consumer confidence, the Richmond Fed manufacturing index and business conditions, the Dallas Fed services activity, the January FHFA house price index, and February’s wholesale and retail inventories and advance goods trade balance. We will also have Italy’s March manufacturing and consumer confidence as well as economic sentiment data, and from France the March manufacturing and consumer confidence data. The BoE’s Bailey will testify today on the Silicon Valley Bank crisis, and we will also hear from ECB’s Muller. Finally, we will have earnings releases from Micron, Walgreens Boots Alliance and Lululemon.

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Mildly positive bias to APAC trade, numerous Central Bank speakers ahead – Newsquawk Euro Market Open

TUESDAY, MAR 28, 2023 – 08:48 AM

APAC stocks traded mixed with a mild positive bias as global banking sector fears continued to dissipate.

European equity futures are indicative of a higher open with the Euro Stoxx 50 +0.3% after the cash market closed up 0.3% on Monday.

In FX, DXY extended declines below 103, JPY leads G10 FX, EUR/USD and Cable linger just above 1.08 and 1.23 respectively.

10yr USTs attempted to nurse recent losses, crude futures plateaued and held on to the spoils from its largest daily gain since October.

Looking ahead, highlights include US Senate Banking Committee re. SIVB, Speeches from ECB’s Lagarde, Enria, BoE’s Bailey, Ramsden & Fed’s Barr, Supply from Italy, Germany & US.

Or why not try Newsquawk’s squawk box free for 7 days?

US TRADE

EQUITIES

US stocks finished mixed albeit with the major indices mostly higher on receding fears around the banking crisis and surging oil prices which spurred outperformance in the energy sector and value stocks, while the acute bear-flattening weighed heavily on rate-sensitive industries such as tech and dragged the NDX in the red.

SPX +0.17% at 3,978, NDX -0.74% at 12,673, DJIA +0.60% at 32,432, RUT +1.08% at 1,754.

Fed’s Jefferson (voter) said inflation has come down and should fall back to towards the 2% target as demand falls but noted that inflation has been longer lasting and the current level is too high, while they want inflation to return to 2% sooner rather than later and don’t want expectations to become embedded. Jefferson also commented that they are still learning how much tight monetary policy has influenced the economy and inflation, as well as noted that Fed’s actions in recent weeks aimed to show depositors that there is someone out there willing to lend.

US Treasury official Liang said the US government will use tools to prevent banking contagion again if warranted and that the US financial system is significantly stronger now due to stronger capital and liquidity requirements, while she added the US must ensure that banking regulations and supervision are appropriate for today’s risk and challenges, according to her prepared testimony, according to Reuters.

FDIC Chairman said the agency is undertaking a comprehensive review of the deposit insurance system and has the authority to hold failed banks accountable, while the Chairman noted that losses to the FDIC insurance fund will be repaid and that the vast majority of banks are reporting no material deposit outflows.

US HHS Secretary declared a public health emergency for Mississippi in response to severe weather.

APAC TRADE

EQUITIES

APAC stocks traded mixed with a mild positive bias as global banking sector fears continued to dissipate and with early advances led by energy after the recent surge in oil prices although gains were capped in the region as North Korean nuclear rhetoric stoked geopolitical concerns.

ASX 200 was boosted amid strength in the commodity-related sectors with outperformance in energy after oil prices notched the largest daily gain since October and financials were also lifted as Australia downplayed the risks to domestic banks from the recent global banking issues.

Nikkei 225 was indecisive despite Japan reiterating plans for a JPY 2.2tln economic stimulus package with trade stuck in a narrow range near 27,500 after the nuclear rhetoric by North Korea which called for the scaling up of weapons-grade nuclear materials and included similar language used before its last nuclear test in 2017.

Hang Seng and Shanghai Comp. were choppy ahead of key earnings results and after PBoC liquidity efforts.

US equity futures (ES +0.1%) were rangebound overnight following the prior day’s indecisive performance.

European equity futures are indicative of a higher open with the Euro Stoxx 50 +0.3% after the cash market closed up 0.3% on Monday.

FX

DXY was marginally softer and extended further beneath the 103.00 level as the dollar made way for its major counterparts and after yields slightly eased with the US 2yr yield back beneath 4%.

EUR/USD gradually edged higher and reclaimed the 1.0800 following the recent slew of ECB rhetoric including reports that ECB’s Schnabel pushed for the ECB statement to say more hiking is possible.

GBP/USD continued to benefit alongside the mild positive bias and with recent comments from BoE Governor Bailey who said inflation is likely to fall steeply in the UK but also suggested further monetary tightening would be required if signs of persistent inflationary pressures become evident.

USD/JPY reversed Monday’s gains as yield differentials between US and Japan narrowed.

Antipodeans were firmer amid tailwinds from recent gains in commodities and Australian Retail Sales data.

PBoC set USD/CNY mid-point at 6.8749 vs exp. 6.8737 (prev. 6.8714)

FIXED INCOME

10yr UST futures attempted to nurse some of its recent losses and found slight reprieve from the bear flattening seen yesterday which coincided with receding banking sector fears and following a dismal 2yr auction.

Bund futures languished near the prior day’s lows after the hawkish ECB rhetoric and German Ifo data.

10yr JGB futures were subdued after the selling pressure across global peers but with prices off worse levels following stronger results at the latest 40yr JGB auction.

COMMODITIES

Crude futures plateaued and held on to the spoils from its largest daily gain since October as banking fears cooled, while the recent gains were also attributed to supply risk out of Iraq/Kurdistan and geopolitical concerns.

India was the largest buyer of Russia’s seaborne Urals oil in March which accounted for 65% of the total and kept Russia’s exports high, according to Reuters citing traders and Refinitiv data. Traders also noted that Russia may continue to maintain high oil exports in April to meet Indian refiner needs.

Spot gold was uneventful as the tailwinds from a softer dollar were offset by the lack of haven demand.

Copper futures were kept afloat amid a mild positive tone but with gains capped amid indecision in China.

CRYPTO

Bitcoin continued to pull back from this month’s surge and dipped beneath the USD 27,000 level.

Binance CEO said the CFTC complaint appears to have an incomplete recitation of the facts and they do not agree with the issues alleged in the complaint. Binance CEO said they intend to respect and collaborate with US and other regulators around the world, while he added that Binance.com does not trade for profit or manipulate the market under any circumstances, according to Reuters.

NOTABLE ASIA-PAC HEADLINES

China’s Foreign Ministry said Premier Li Qiang met with foreign representatives at the China Development Forum in Beijing on Monday and met with executives including Apple (AAPL) CEO Cook, while Li told executives China will unswervingly expand its opening up, according to Reuters.

US and Japan reached a trade deal for critical EV battery minerals in which the deal prohibits enacting export restrictions on lithium, cobalt, nickel, manganese and graphite, according to US officials. Furthermore, the deal includes provisions to combat non-market practices, while access for Japanese automakers to the battery minerals portion of USD 7,500 in US EV tax credit depends on the tax guidance this week from the US Treasury.

DATA RECAP

Australian Retail Sales MM Final (Feb) 0.2% vs. Exp. 0.1% (Prev. 1.9%, Rev. 1.8%)

GLOBAL NEWS

Israeli PM Netanyahu confirmed to delay the second and third readings of the justice bill and the Israeli labour union called off a nationwide strike after PM Netanyahu announced to delay the judicial overhaul.

GEOPOLITICAL

US senior admin official said at least 50 US government staffers stationed in ten countries were targeted with spyware and President Biden is set to sign an Executive Order to prevent the use of such tools.

Russian Defence Ministry said it fired supersonic anti-ship missiles at a mock target in the Sea of Japan.

Russia failed to get the UN Security Council to ask for an independent inquiry into the Nord Stream gas pipeline explosions which occurred in September last year, according to Reuters.

Hungary’s parliament approved Finland’s NATO membership.