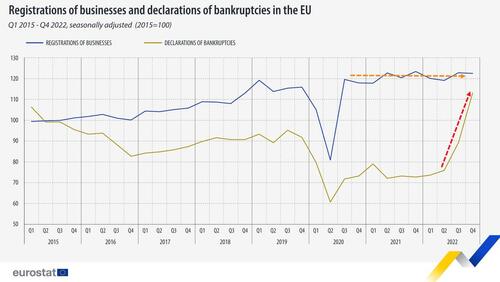

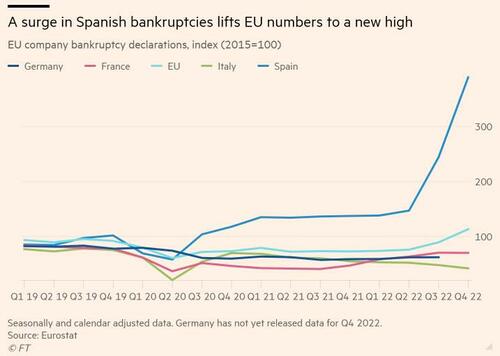

FEB 23/GOLD CLOSED DOWN $13.05 TO $1819.55//SILVER CLOSED DOWN 32 CENTS TO $21.30//PLATINUM CLOSED DOWN $7.25 TO $941.00//PALLADIUM TOOK A HUGE HIT DOWN $54.75 TO $1437.20//COVID UPDATES: DR PAUL ALEXANDER//VACCINE IMPACT//SLAY NEWS//RUSSIA VS UKRAINE UPDATES//EAST PALESTINE DIASTER UPDATES//SPAIN RECORDS RECORD NO. OF BANKRUPTCIES IN 2022-2023//FED-EX READY TO STRIKE WHICH WILL HAVE A DRAMATIC EFFECT ON WORLD ECONOMY//SWAMP STORIES FOR YOU TONIGHT//

118 C MACQUARIE FUT 90 435 H SCOTIA CAPITAL 89 624 H BOFA SECURITIES 100 661 C JP MORGAN 30 685 C RJ OBRIEN 1 737 C ADVANTAGE 1 800 C MAREX SPEC 8 905 C ADM 39 991 H CME 20

TOTAL: 189 189

JPMORGAN STOPPED 30/189

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR FEB/2023. CONTRACT: 189 NOTICES FOR 18,900 OZ or 0.5879 TONNES

total notices so far: 15,036 contracts for 1,503,600 oz (46.768 tonnes)

SILVER NOTICES: 6 NOTICE(S) FILED FOR 30,000 OZ/

total number of notices filed so far this month :866 for 4,330,000 oz

END

GLD

WITH GOLD DOWN $13.05

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/NO CHANGES IN GOLD INVENTORY AT THE GLD////

INVENTORY RESTS AT 919.92TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 32 CENTS

AT THE SLV// SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 487.072. MILLION OZ (CORRECTED)

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 1388 CONTRACTS TO 125,284 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THE STRONG GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.22 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. WE HAVE NOW SURPASSED OUR ALL TIME LOW OF 124,000 OI CONTRACTS RECORDED YESTERDAY. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.22). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS, AS WE HAD A HUGE SIZED LOSS ON OUR TWO EXCHANGES 1581 CONTRACTS. AS WELL, WE HAD 0 NOTICES FOR EXCHANGE FOR RISK TRANSFER ( AS THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 6.225 MILLION OZ. WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD: A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 711 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 0.540. MILLION OZ FOLLOWED BY TODAY’S 10,000 OZ QUEUE JUMP// NEW TOTALS STANDING = 4.40 MILLION OZ + 6.225 MILLION OF EXCHANGE FOR RISK//TOTAL STANDING 10.655 MILLION OZ//// V) STRONG SIZED COMEX OI GAIN/ GOOD SIZED EFP ISSUANCE/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL ADDED +517

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB:

TOTAL CONTRACTS for 16 days, total 14,778 contracts: OR 73.890 MILLION OZ . (923 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 73.890 MILLION OZ

.

LAST 17 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 73.890/ MILLION OZ/INITIAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1388 DESPITE OUR $0.22 LOSS IN SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE CONTRACTS: 711 CONTRACTS ISSUED FOR MAR AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB OF 0.54 MILLION OZ FOLLOWED BY TODAY’S 10,000 OZ QUEUE JUMP = NEW STANDING: 4.430 MILLION OZ + 6.225 MILLION OZ EXCHANGE FOR RISK://NEW STANDING INCREASES TO 10.655 MILLION OZ .. WE HAVE A GIGANTIC SIZED GAIN OF 2099OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 6 NOTICE(S) FILED TODAY FOR 30,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 3368 CONTRACTS TO 426,016 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED 26 CONTRACTS. (AS AN ASIDE: HOW CAN YOU ADD CONTRACTS TO YESTERDAY’S TRADING OF CONTRACTS?)

.

WE HAD A FAIR SIZED INCREASE IN COMEX OI ( 3368 CONTRACTS) DESPITE OUR $0.60 LOSS IN PRICE. WE ALSO HAD A SMALL INITIAL STANDING IN GOLD TONNAGE FOR FEB. AT 41.601 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 4200 OZ //NEW STANDING: 47.209 TONNES//(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S ) (EFP is the transfer of contracts immediately to London for potential gold deliveries originating from London). TONNES

YET ALL OF..THIS HAPPENED WITH OUR $0,60 LOSS IN PRICEWITH RESPECT TO WEDNESDAY’S TRADING

WE HAD A GOOD SIZED GAIN OF 5215 OI CONTRACTS (16.220 PAPER TONNES) ON OUR TWO EXCHANGES

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1847 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 426,016

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5215 CONTRACTS WITH 3368CONTRACTS INCREASED AT THE COMEX AND 1847 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 5215 CONTRACTS OR 16.146 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1847 CONTRACTS) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (3368) TOTAL GAIN IN THE TWO EXCHANGES 5215 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 41.601 TONNES FOLLOWED BY TODAY’S 4,200 OZ QUEUE JUMP // ///3) ZERO LONG LIQUIDATION //4) FAIR SIZED COMEX OPEN INTEREST GAIN// 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

FEB

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB :

40,734 CONTRACTS OR 4073400 OZ OR 126.70 TONNES 16 TRADING DAY(S) AND THUS AVERAGING: 2545 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES 126.70 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 126.70/3550 x 100% TONNES 3.57% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247,44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 126.70 TONNES/INITIAL

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF BOTH GOLD (

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF OCT HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 1388 CONTRACTS OI TO 125,294 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A RECORD LOW OF 124,080 CONTRACTS TODAY.

EFP ISSUANCE 711 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 711 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 711 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1388 CONTRACTS AND ADD TO THE 711 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE GAIN OF 2099 OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES 10.495 MILLION OZ//

OCCURRED DESPITE OUR TINY $0.22 LOSS IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

4. Chris Powell of GATA provides to us very important physical commentaries

end

5. Other gold/silver commentaries

6. Commodity commentaries//

7/CRYPTOCURRENCIES/BITCOIN ETC

3. ASIAN AFFAIRS

i)THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 3.67 PTS OR 0.11% //Hang Seng CLOSED DOWN 72.49 PTS OR 0.35% /The Nikkei closed //Australia’s all ordinaries CLOSED DOWN 0.33% /Chinese yuan (ONSHORE) closed DOWN 6.8984 //OFFSHORE CHINESE YUAN DOWN TO 6.9043// /Oil DOWN TO 74.86dollars per barrel for WTI and BRENT AT 81.20 / Stocks in Europe OPENED MOSTLY GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 C CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 3368 CONTRACTS UP TO 426,016 DESPITE OUR LOSS IN PRICE OF $0.60. I THINK WE HAVE HIT OUR LOW IN OPEN INTEREST FOR THE YEAR/FEB 22/2023 AT 422,516.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF FEB… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1847 EFP CONTRACTS WERE ISSUED: : APRIL 1847 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1847 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 5215 CONTRACTS IN THAT 1847LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED COMEX OI GAIN OF 3368 CONTRACTS..AND THIS GOOD SIZED GAIN ON OUR TWO EXCHANGES HAPPENED (DESPITE OUR FALL IN PRICE OF $0.60). WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: FEB (47.209)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.2099 tonnes

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $0.60) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A GOOD SIZED GAIN OF 5215 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 16.220 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR FEB. (41.219 TONNES) FOLLOWED BY TODAY’S QUEUE. JUMP OF 4200 OZ OR 0.1306 TONNES//NEW STANDING INCREASES TO 47.209 tonnes … ALL OF THIS WAS ACCOMPLISHED DESPITE OUR FALL IN PRICE TO THE TUNE OF $0.60.

WE HAD +24 ADDED CONTRACTS COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 5215 CONTRACTS OR 521500 OZ OR 16.220 TONNES

Estimated gold comex today 173,755// //poor

final gold volumes/yesterday 149,878/// poor

INITIAL STANDINGS FOR FEB 2023 COMEX GOLD //FEB 23//

Total monthly oz gold served (contracts) so far this month

15,036 notices 1,503600 46.768TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i)Into JPMorgan: 13,393.975 oz (real gold)

total deposits: 13,393.975 oz

customer withdrawals: 3

i) out of Brinks 160.750 oz 5 kilobars

ii) Out of HSBC: 10,303.684 oz

iii) out of Manfra: 31,984.155 oz

total withdrawals: 42,452.592 oz real gold except the 5 kilobars form Birnks

in tonnes: 1.32 tonnes

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEBRUARY.

For the front month of FEBRUARY we have an oi of 331 contracts having LOST 165 contracts. We had 207 notices

filed on Wednesday so we gained 42 contracts or an additional 4200 oz will stand searching for metal at the comex

March lost 11 contracts to stand at 2029.

April gained 119 contracts down to 332,344

We had 189 notice(s) filed today for 18900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 189 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer notice(s) was (were) stopped 30/ Received) by J.P.Morgan//customer account 3 and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the FEB. /2023. contract month,

we take the total number of notices filed so far for the month (15.036 x 100 oz ), to which we add the difference between the open interest for the front month of (FEBRUARY 331 CONTRACTS) minus the number of notices served upon today 189 x 100 oz per contract equals 1,517,800 OZ OR 47.209 TONNES the number of TONNES standing in this active month of February.

thus the INITIAL standings for gold for the FEB contract month:

No of notices filed so far (15,036 x 100 oz+ 331 OI for the front month minus the number of notices served upon today (189)x 100 oz} which equals 1,513,600 oz standing OR 47.209 TONNES in this active delivery month of FEBRUARY..

TOTAL COMEX GOLD STANDING: 47.209TONNES. SO JUST LIKE LAST MONTH WE START WITH A LOW INITIAL AMOUNT OF GOLD STANDING BUT THIS WILL GROW AS THE MONTH PROCEEDS TO ITS CONCLUSION.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,702,817.120 OZ

TOTAL REGISTERED GOLD: 10,976,047.431 (341.401 tonnes)..dropping fast

TOTAL OF ALL ELIGIBLE GOLD: 10,726,769.689 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,196,591 OZ (REG GOLD- PLEDGED GOLD) 286.05 tonnes//dropping like a stone

END

SILVER/COMEX

FEB 23/2023//INITIAL. SILVER CONTRACT FOR FEBRUARY

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

1,095,488.290 oz brinks CNT Delaware HSBC Loomis

Deposits to the Dealer Inventory

nil OZ

Deposits to the Customer Inventory

597,155.710 oz Delaware JPMorgan Manfra

No of oz served today (contracts)

6 CONTRACT(S) (30,000 OZ)

No of oz to be served (notices)

20 contracts (100,000 oz)

Total monthly oz silver served (contracts)

866 contracts (4,330,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 3 deposits into the customer account

i)Into JPMorgan: 578,057.403 oz

ii) Into Delaware: 13,058,667

iii) Into Manfra: 6039.640 oz

Total deposits: 597,155.710 oz

JPMorgan has a total silver weight: 147.167 million oz/287.959 million =51.09% of comex .//dropping fast

Comex withdrawals: 5

i) Out of Brinks 65,886.560 oz

ii) Out of CNT: 125,053.402 oz

iii) Out of Delaware: 3896.100 oz

iv) Out of Loomis 300,189.040 oz

Total withdrawals; 1,095,488.290 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 31.873MILLION OZ (declining rapidly).TOTAL REG + ELIG. 287,959 million o

CALCULATION OF SILVER OZ STANDING FOR FEB

silver open interest data:

FRONT MONTH OF FEB/2023 OI: 26 CONTRACTS HAVING LOST 2 CONTRACT(S.).

WE HAD 4 NOTICES FILED ON WEDNESDAY, SO WE GAINED 2 CONTRACTS OR AN ADDITIONAL 10,000 OZ OF SILVER WILL STAND AT THE COMEX

March LOST 6980 CONTRACTS DOWN TO 29,020 contracts

April GAINED 28 CONTRACTS TO STAND at 200.

TOTAL NUMBER OF NOTICES FILED FOR TODAY:6 for 30,000 oz

Comex volumes// est. volume today 82,737// very good

Comex volume: confirmed yesterday: 79,636 contracts ( very good)

To calculate the number of silver ounces that will stand for delivery in FEBRUARY. we take the total number of notices filed for the month so far at 866 x 5,000 oz = 4,330,000 oz

to which we add the difference between the open interest for the front month of FEB(26) and the number of notices served upon today 6 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB./2023 contract month:866 (notices served so far) x 5000 oz + OI for the front month of FEB 26 – number of notices served upon today (6) x 500 oz of silver standing for the FEB. contract month equates 4.430 million oz + PREVIOUS 6.225 MILLION OZ ( EXCHANGE FOR RISK) = 10.655 MILLION OZ//(TOTAL OZ OF SILVER STANDING).

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

FEB 23/WITH GOLD DOWN $13.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 919.92 TONNES

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

FEB 8/WITH GOLD UP $6.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.9 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 920.82 TONNES

FEB 7/WITH GOLD UP $5.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.32 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 917.92 TONNES

FEB 6/WITH GOLD UP $3.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.24 TONNES

FEB 3/WITH GOLD DOWN $52.55 TODAY: STRANGE: BIG CHANGES AGAIN IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 920.24 TONNES

FEB 2/WITH GOLD $10.95 TODAY: BIG CHANGE IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 918.50 TONNES

FEB 1/WITH GOLD DOWN $2.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 31/WITH GOLD UP $6.55 TODAY; BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 30/WITH GOLD DOWN $6.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 918.50 TONNES

JAN 27/WITH GOLD DOWN $0.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 919.37 TONNES

JAN 26/WITH GOLD DOWN $11.55 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.03 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 919.37 TONNES

JAN 25/WITH GOLD UP $7.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 917.34 TONNES

JAN 24/WITH GOLD UP $7.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.06 TONNES

JAN 23/WITH GOLD UP $0.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.63 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 917.06 TONNES

JAN 20/WITH GOLD UP $4.75 TODAY;BIG CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 912.43 TONNES

JAN 19/WITH GOLD UP $16.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES INTO THE GLD///INVENTORY RESTS AT 910.98TONNES

JAN 18/WITH GOLD DOWN $1.95 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.9 TONNES FROM THE GLD////INVENTORY RESTS AT 909.24 TONNES

JAN 17/WITH GOLD DOWN $11.45 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.14 TONNES

JAN 13/WITH GOLD UP $22.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES FROM THE GLD///INVENTORY RESTS AT 912.14 TONNES

JAN 12/WITH GOLD UP $20.55 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES FROM THE GLD///INVENTORY RESTS AT 912.43 TONNES

JAN 11/WITH GOLD UP $1.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.17 TONNES

JAN 10/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD///INVENTORY RESTS AT 915.33 TONNES

JAN 9/WITH GOLD UP $ 8.60 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD//.//INVENTORY RESTS AT 915.33 TONNES

JAN 6/WITH GOLD UP $28.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 916.77 TONNES

JAN 5/WITH GOLD DOWN $17.05 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 916.77 TONNES

JANUARY 4/WITH GOLD UP $32.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.64 TONNES

JAN 3/WITH GOLD UP $20.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:STRANGE: A WITHDRAWAL OF .87 TONNES FORM THE GLD////INVENTORY RESTS AT 917.64 TONNES

GLD INVENTORY: 919.92 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

FEB 23/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.072 MILLION OZ//

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 485.693 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards:

END

3. Chris Powell of GATA provides to us very important physical commentaries//

Craig Hemke at Sprott talks about gold’s first pullback of 2023

(Craig Hemke)

Craig Hemke at Sprott Money: Gold’s first pullback of 2023

Submitted by admin on Wed, 2023-02-22 16:29Section: Daily Dispatches

By Craig Hemke Sprott Money, Toronto Wednesday, February 22, 2023

In our annual forecast printed in January, we tried to warn everyone that although the Comex precious metals were set up for a very strong 2023, the first half of the year would include several false starts and fakeouts.

As if right on schedule, you just got your first one. …

Jan Nieuwenhuijs: Estimating the true size of China’s gold reserves

Submitted by admin on Thu, 2023-02-23 11:39Section: Daily Dispatches

11:40a ET Thursday, February 23, 2023

Dear Friend of GATA and Gold:

Gold market analyst Jan Nieuwenhuijs today gives his estimate of the gold reserves held by the People’s Bank of China: twice the tonnage officially reported.

Perhaps more important Nieuwenhuijs documents how China’s central banks and central banks in Europe appear to be working together to match their gold reserves with their nations’ gross domestic product in preparation for some sort of new gold standard or gold price targeting system.

Nieuwenhuijs notes that China’s central bank especially has an interest in keeping the gold price down while it acquires the metal necessary to reach a balance with its GDP.

Nieuwenhuijs also essentially reminds us that gold is the secret knowledge of the financial universe, a mechanism surreptitiously used by governments for purposes like manipulating currency and other markets — a subject that simply cannot be addressed by mainstream financial news organizations and most market analysts who aspire to respectability.

Nieuwenhuijs’ analysis is headlined “Estimating the True Size of China’s Gold Reserves” and it’s posted at the Gainesville Coins internet site here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

end

Your weekend reading material//a must read!!

Alasdair Macleod…(GATA)

Alasdair Macleod: Central bank digital currencies — the good, the bad, and the ugly

Submitted by admin on Thu, 2023-02-23 11:54Section: Daily Dispatches

By Alasdair Macleod GoldMoney, Toronto Thursday, February 23, 2023

There has been much comment over the likelihood that central bank digital currencies will be introduced. In this essay conclude they are unnecessary — a red herring. But this does allow us to discuss their possible relevance to a new Asian super-currency.

This month the Bank of England, in partnership with the UK Treasury, produced a white paper on the subject, which considerably waters down the objectives identified by the Bank for International Settlements. The British proposal is a bad idea because it is pointless.

I will describe how a new gold-backed currency can entirely do away with the U.S. dollar for trade settlements and commodity purchases between participating nations in the Russia-China axis.

Some informed commentary on the topic suggests that a blockchain will be involved, and Sberbank, the Russian state-owned lender, has already issued a gold-linked fund designed to be available to the public by being compatible with ethereum. Perhaps the bank is front-running developments…

The ugly side in our title is found in the BIS’ dystopian proposals, which see CBDCs as an opportunity to allow central banks to double down on their attempts to manage economic outcomes while restricting personal freedom.

Messing about with fiat currency alternatives such as CBDCs could end up revealing the fragility of the former. CBDCs will take years to implement in any major currency, during which fiat currencies led by the dollar are likely to fail anyway. …

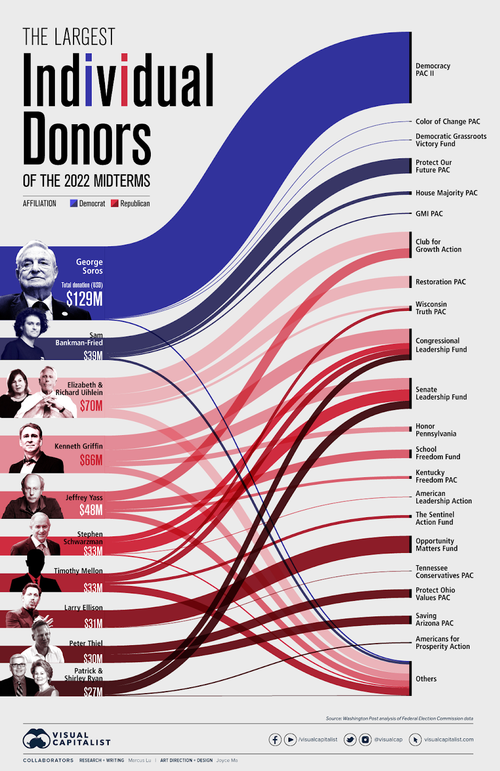

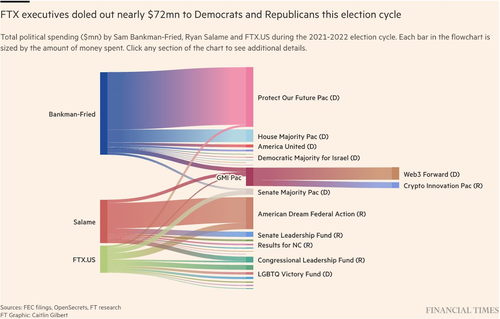

Poor guy: the charges keep adding up. I think he was a pawn for the Democrats

(zerohedge)

Sam Bankman-Fried Charged With Conspiracy To Make Unlawful Political Donations, Defraud Federal Election Commission

THURSDAY, FEB 23, 2023 – 09:46 AM

Disgraced FTX founder Sam Bankman-Fried was charged on Thursday with 12 new counts, including illegally making over 300 political contributions to the tune of tens of millions of dollars through straw donors and using corporate funds.

“Bankman-Fried’s use of straw donors allowed him to evade contribution limits on individual donations to candidates to whom he had already donated,” reads the indictment, which adds that the “fraudulent conduct” impaired the FEC’s functioning.

“In dozens of instances, BANKMAN-FRIED’s use of straw donors allowed him to evade contribution limits on individual donations to candidates to whom he had already donated.”

“As a result of this fraudulent conduct,” SBF and his co-conspirators caused false information to be reported by campaigns and PACs to the FEC.”

SBF had previously only faced charges of conspiracy to commit wire fraud on customers and lenders, as well as commodities fraud, securities fraud, money laundering, conspiracy to defraud the United States, and violating campaign finance laws.

According to the new indictment, Bankman-Fried and others, while attempting to open a bank account, “falsely represented to a financial institution that the account would be used for trading and market making,” when in fact it was used to receive and transmit customer funds.

SBF and co-conspirators “agreed to and did make corporate contributions to candidates and committees in the Southern District of New York that were reported in the name of another person,” the indictment continues.

FTX’s former CEO wanted to give at least $1 million to a pro-LGBTQ political action group, but couldn’t find anyone bisexual or gay at the company whom he trusted, the document said. One unnamed executive, believed to be Nishad Singh, was urged to make the donation, while another right-wing executive, apparently Ryan Salame, did so for Republican causes, the document said. –Coindesk

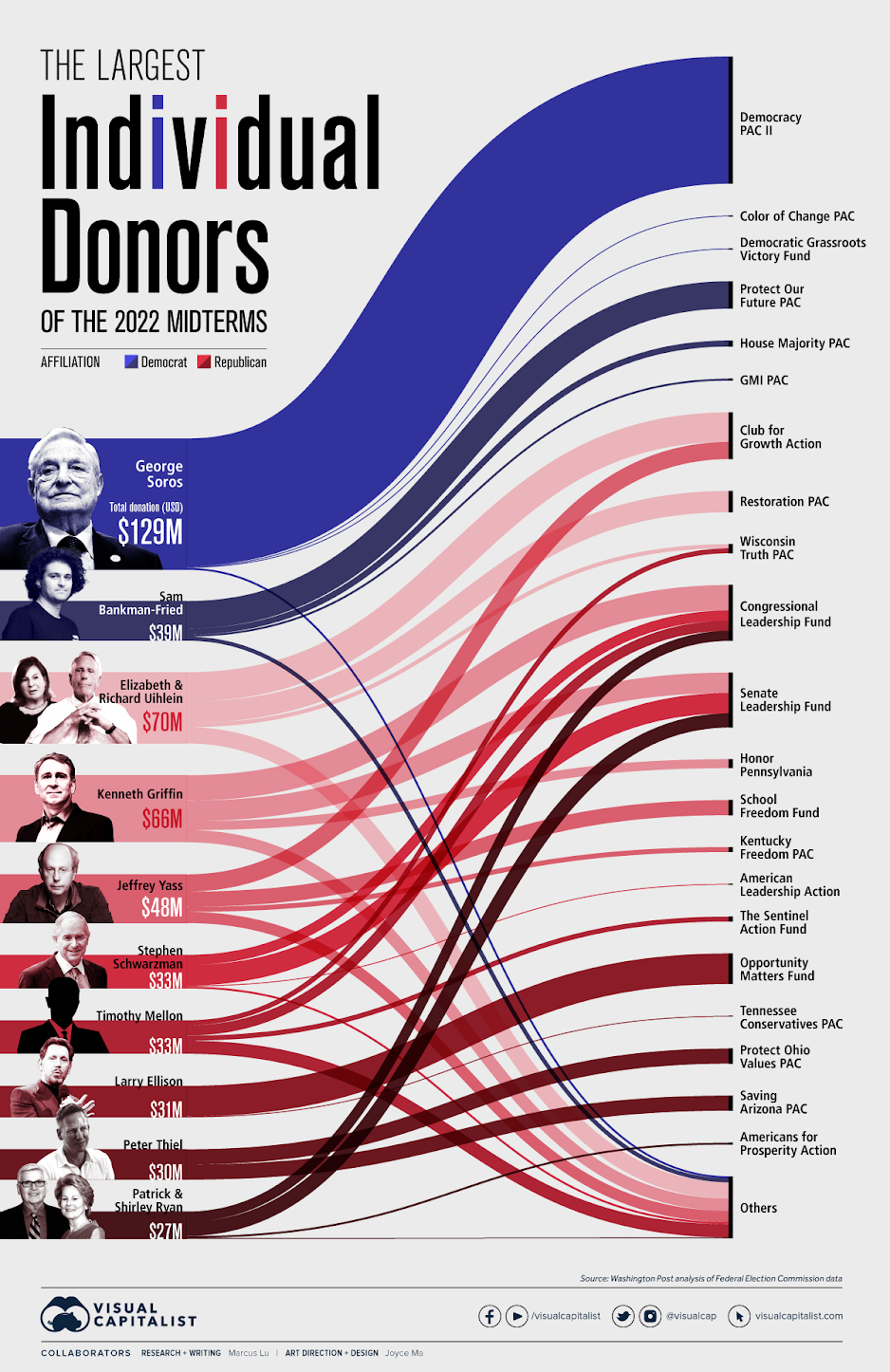

Bankman-Fried was the second largest individual donor during the 2022 US midterm elections, contributing $39 million to various Democrat causes.

It wasn’t just Bankman-Fried that made donations to politicians with $72 million overall donated by FTX execs…

Here is the full list of politicians who received donations from FTX executives

end

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 6.8984

OFFSHORE YUAN: 6.9043

SHANGHAI CLOSED DOWN 3.67 PTS OR 0.11%

HANG SENG CLOSED DOWN 72.49 PTS OR 0.35%

2. Nikkei closed

3. Europe stocks SO FAR: MOSTLY GREEN

USA dollar INDEX UP TO 104.46 Euro RISES TO 1.0613 UP 8 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.5000!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 135.02/JAPANESE YEN RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.5370%***/Italian 10 Yr bond yield FALLS to 4.449%*** /SPAIN 10 YR BOND YIELD FALLS TO 3.584…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.393//(ITALY WORSE THAN GREECE?)

3j Gold at $1837.95//silver at: 21.84 7 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 00/100 roubles/dollar; ROUBLE AT 75.000//

3m oil into the 74 dollar handle for WTI and 81 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 135.02/10 YEAR YIELD AFTER BREAKING .54%, REMAINS AT .5000% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9322–as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9893well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.948% UP 2 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.938 UP 1 BASIS PTS//INVERTED TO THE 10 YEAR!!

UK 2 YR BOND YIELD: 4.7015 DOWN 1 BASIS PT

USA DOLLAR VS TURKISH LIRA: 18,87…

GREAT BRITAIN/10 YEAR YIELD: 3.6825% UP 8 BASIS PTS

end

i.b Overnight: Newsquawk and Zero hedge:

FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

S&P Futures Rebound Above 4,000, Boosted By Surging Nvidia

THURSDAY, FEB 23, 2023 – 08:02 AM

US futures rebounded from yesterday’s post FOMC selloff, rising back over 4,000 as concern about aggressive monetary tightening eased and Nvidia soared 10% after giving a bullish revenue outlook. Contracts on the Nasdaq 100 were up 1% as of 7:45 a.m. ET while S&P 500 futures rose 0.4%. The underlying stock gauges closed mixed on Wednesday as minutes from the Federal Reserve’s latest meeting signaled its determination to keep hiking interest rates to combat inflation. The tech rally may be short-lived thought: treasuries edged lower again, reversing yesterday’s gains. The Bloomberg Dollar Spot Index recovered from earlier lows, pressuring most Group-of-10 currencies. Gold was little changed, while oil advanced. Bitcoin rose nearly 2% following two days of losses, before fading some of its gains.

In premarket trading, tech stocks were among the best performers, with chipmaker Nvidia, which has a 4.2% weighting in the Nasdaq 100, surging 10% after it reported Q4 results that beat expectations and gave a bullish revenue outlook for the current quarter. Growth in sales of chips for data centers has helped the company weather a slowdown in the PC market as it gears up for an expected boom in artificial intelligence. By contrast, EV maker Lucid plunged 8.1% in premarket trading after it posted worse-than-expected results in the final months of what it called a “challenging” year. Unity Software dropped 7.3% after the company’s revenue forecasts trailed consensus estimates. Here are some other notable premarket movers:

EBay shares fall ~5% in US premarket trading after the online auction and retail company’s 2023 guidance came in weaker than expected, with a more difficult macro picture set to weigh and a “challenging” margin outlook.

Enovix shares rise ~gr15% in premarket trading after the electronic-components maker reported revenue for the fourth quarter that beat the average estimate. Analysts note the earnings call reiterated milestones disclosed in January’s presentation and progress on cash.

Graphite Bio soars 16% in premarket trading after the biotech company unveiled plans to trim its workforce by 50% while exploring “strategic alternatives.”.

Teladoc shares fall ~7% in US premarket trading after the online health services firm guided to a slowdown in revenue growth, which analysts said more than offset an improved margin outlook.

Unity Software shares drop as much as 8.9% in premarket trading after the software maker’s first-quarter and full-year revenue forecasts trailed consensus estimates. The guidance was the main point of discussion among analysts, with Citi saying it might weaken sentiment toward the stock.

Moderna Inc. shares climb 2.9% in postmarket trading after the personalized mRNA cancer vaccine that it’s developing in combination with Merck & Co.’s flagship immunotherapy, Keytruda, received Breakthrough Therapy Designation from the US Food and Drug Administration.

Etsy gained 6% in extended trading, after the online retailer focused on handmade and vintage items reported fourth-quarter results that beat expectations. It also gave an outlook that analysts see as mixed.

Rackspace Technology gained 8% in postmarket trading after reporting adjusted earnings per share and revenue for the fourth quarter that beat the average analyst estimates.

Nvidia provided “an excellent report and solid outperformance amid weakening macro trends,” CJ Muse, an analyst at Evercore ISI, wrote in a note. Still, others saw this as merely another modest bounce in an otherwise bearish slump. Further policy tightening “will create some small recessionary result probably in the third or fourth quarter of 2023, but we will still be in a scenario of soft landing,” said Stephane Monier, chief investment officer at Banque Lombard Odier. “In that scenario we expect the S&P 500 to be around 3,900,” he said on Bloomberg TV. “We are currently underweight US equities as we are expecting a little bit of a correction in the weeks to come,” Monier said. “And we have a strong preference for Asian equities, particularly China but not only.”

After months of divergence over the perceived path of monetary tightening, the Fed and markets are increasingly getting aligned in their expectations, reducing the scope for hawkish shocks. While the minutes and comments by Fed officials including James Bullard reiterated a continuing preference for rate hikes, they didn’t say anything that wasn’t factored in by the market’s aggressive repricing of Fed bets in recent weeks.

“One of our big concerns coming into this year was the market was anticipating an event that wasn’t likely to occur, that being a dovish Fed pivot,” Danielle Poli, co-portfolio manager of the diversified income fund for Oaktree Capital Management, said in an interview with Bloomberg Television. “The market has woken back up a little bit in these last two weeks.”

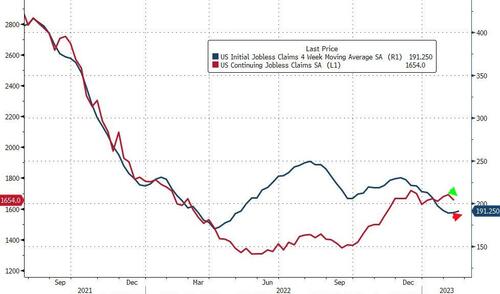

US Jobless claims data due Thursday may help shine a light on the strength of the labor market, which has remained stubbornly robust through the rate-hiking cycle. Eurozone inflation data due today will also help investors outline the health of the European economy.

European stocks struggled for direction as investors remained wary of the prospect of additional monetary tightening by the Fed when the latest Fed minutes revealed that a “few” officials favored a larger half-point hike. The Stoxx 600 was up less than 0.1% with autos, tech and media the best performing sectors. The FTSE loses 0.4%. Here are some of the biggest European movers:

Rolls-Royce shares soar as much as 20%, the most since November 2020, after the engine manufacturer’s full-year earnings and forecast topped expectations on all metrics

Axa climbed 3.8%, the top performing stock on the Stoxx 600 Insurance Index, after the French insurer announced it could buy back up to €1.1 billion worth of shares

HeidelbergCement rises as much as 3.1% as analysts say the outlook is positive for the German construction giant, noting diminishing energy cost headwinds from 2022

Accor shares rise as much as 2.8%, after the hospitality company reported full-year Ebitda and dividend per share that was ahead of analyst estimates

Bouygues shares rise as much as 3.9%, after the French conglomerate posted what Citi analysts described as a “solid” set of numbers, with top line ahead of consensus and margin up

Spectris rises as much as 7.6%, the most since April 2022, after the precision-measurement specialist released full- year results which Shore Capital says were a beat

Anglo American drops as much as 2.8% after the mining giant revealed a significant writedown at its Woodsmith polyhalite project

Munich Re slumped as much as 6.2%, the most since July, as analysts pointed to weaker underlying property and casualty underwriting despite an overall earnings beat for the German reinsurer

Earlier in the session, Asian stocks snapped a two-day decline as traders focused on US economic data due Thursday, while shares in Hong Kong entered correction territory. The MSCI Asia Pacific ex Japan Index rose as much as 0.9%, before paring gains to 0.3% in afternoon trading. South Korean shares were among the biggest advancers in the region as the Bank of Korea paused rate hikes for the first time in a year. Meanwhile, Hong Kong’s Hang Seng Index fell into correction amid growing geopolitical concerns and doubts over the strength of China’s economy. Japan was closed for a holiday. The US will release data on economic growth, consumption and employment, providing more clues on the Fed’s policy path.

The MSCI Asia gauge is trading about 6% lower than a peak reached in late January as investors assess higher bond yields and China’s path to recovery. Still, a gauge of tech stocks soared as the US 10-year Treasury yield eased toward 3.9% overnight, although it reversed the decline in the afternoon. Minutes of the latest Federal Reserve meeting showed that officials continued to anticipate further increases in borrowing costs, although most were in favor of smaller rate increases. Fed’s Williams Says Fed’s 2% Inflation Goal Key to Taming Prices The FOMC “sounded hawkish at the margin,” Saxo Capital Markets strategists wrote in a note. “While this risk of a recession was noted, data since the meeting including the most recent PMI numbers this week have continued to ease recession concerns.”

Australian stocks declined again, as the S&P/ASX 200 index fell 0.4% to close at 7,285.40, extending losses for a third day, dragged by mining shares and banks. National carrier Qantas was among the day’s laggards after the airline flagged higher-than-expected spending on planes, while Eagers, the top performer, rallied after the Australian auto dealer said demand for new cars remains strong. In New Zealand, the S&P/NZX 50 index rose 0.8% to 11,888.50.

Indian stocks ended lower after a volatile session as monthly derivative contracts expired on Thursday. The S&P BSE Sensex fell 0.2% to 59,605.80 in Mumbai, while the NSE Nifty 50 Index declined by a similar measure. The gauges have now dropped for five straight sessions, the longest run of declines since Sept. 29. The benchmark Sensex has nearly erased its gains for February, while the Nifty has fallen to its lowest levels since Oct. 18. All but two of ten companies controlled by the Adani Group closed lower as concerns linger about the conglomerate’s corporate structure. Expiry of monthly options also weighed on the stocks. India’s finance ministry on Thursday said that if predictions on the return of El Nino conditions are accurate, that could lead to a deficient monsoon, resulting in lower agricultural output and higher prices. Sixteen of 20 sector sub-gauges compiled by BSE Ltd. declined. Realty firms and utilities were the worst performers, while metal and services sector companies advanced. For the week, all but fast-moving consumer-goods companies have retreated. HDFC Bank contributed the most to the Sensex’s decline on Thursday, decreasing 0.7%. Out of 30 shares in the Sensex index, 13 rose and 17 fell.

In FX, the BBG Dollar Index traded marginally weaker, having come off day’s lows; the New Zealand dollar and Australian dollar are vying for top sport among the G-10’s, while the pound was the worst.

The euro edged lower, extending its slump into a fourth day, and touched 1.0587, the lowest since Jan. 6. The German yield curve twist-flattened very modestly. Three-week implied volatility in euro-dollar is up a third day for the first time this month as the tenor now captures the ECB meeting on March 16 and the release of US CPI data two days earlier

The pound slumped. Gilts underperformed European peers, with yields rising around 3bps across the curve, as traders added to BOE pricing after policymaker Catherine Mann said more interest-rate rises are needed to clamp down on inflation as she dismissed talk of a looming “pivot” to easier monetary policy

The Australian dollar climbed from a seven-week low as dip-buyers emerged and business spending beat estimates

In rates, Treasuries were under pressure as US trading day begins, with yields still inside Wednesday’s ranges. UST yields are higher by as much as 2.4bp in 10-year sector; Wednesday’s ranges included YTD highs for most tenors; the 10Y TSY rose 4bps to 9.449%, near session highs. The week’s auction cycle concludes with 7-year note sale at 1 p.m. New York time, last coupon auction until March 8 and poised to draw a record high yield. WI 7-year yield 4.08%; record high stop was 4.027% in October. In Europe, gilts underperformed their German counterparts after hawkish remarks from BOE policymaker Mann. UK 10-year yields are up 4bps while the German equivalent is up 2bps.

Traders are now pricing in a Fed peak rate of 5.55% by July, compared with 4.90% they were betting on at the start of year. However, Fed officials haven’t grown more aggressive during this time: Fed Bank of St. Louis President Bullard reiterated his earlier stance, saying “I’m still at 5.375%.” Markets fully price in a 25 basis-point hike in March, but assign a 24% probability for a 50-point hike.

In crypto, bitcoin is firmer on the session having successfully reclaimed the USD 24k mark after losing the figure on Wednesday, though it remains shy of recent USD 25k+ levels.

In commodities, oil gained — after the longest run of losses this year — as traders took stock of a mixed demand outlook of tightening US monetary policy and China’s reopening. WTI rose 0.7% to trade near $74.45. Spot gold is little changed around $1,826.

Looking to the day ahead now, and data releases include the final CPI release from the Euro Area in January, which came in just hotter than the Flash print, as well as the second estimate of US GDP in Q4. Otherwise, we’ll get the US weekly initial jobless claims, and the Kansas City Fed’s manufacturing index for February. Meanwhile from central banks, we’ll hear from the Fed’s Bostic and Daly, the ECB’s de Cos, and the BoE’s Cunliffe and Mann. Finally, today’s earnings releases include Booking Holdings and Moderna.

Market Snapshot

S&P 500 futures up 0.3% to 4,012.25

MXAP up 0.1% to 160.54

MXAPJ up 0.3% to 523.26

Nikkei down 1.3% to 27,104.32

Topix down 1.1% to 1,975.25

Hang Seng Index down 0.4% to 20,351.35

Shanghai Composite down 0.1% to 3,287.48

Sensex down 0.3% to 59,551.16

Australia S&P/ASX 200 down 0.4% to 7,285.40

Kospi up 0.9% to 2,439.09

STOXX Europe 600 little changed at 462.61

German 10Y yield little changed at 2.53%

Euro down 0.1% to $1.0593

Brent Futures up 0.1% to $80.72/bbl

Gold spot up 0.0% to $1,826.01

U.S. Dollar Index little changed at 104.62

Top Overnight News from Bloomberg

The global economy is in a better place today than many predicted months ago, US Treasury Secretary Janet Yellen said Thursday, while reiterating her calls for support to Ukraine on the eve of the one-year anniversary of Russia’s invasion. BBG

The EU and the US are close to an agreement on raw materials used in batteries that would allow EU companies access to some of the same benefits in President Joe Biden’s green investment plan as Washington’s free-trade partners, according to the bloc’s trade chief Valdis Dombrovskis. BBG

Sweden’s government budget is likely to be in the red for the first time since the pandemic hit in 2020, as tax income is set to drop and large-scale electricity-price support weighs on finances, according to the National Debt Office. BBG

Hong Kong’s CPI for Jan overshoots the St, coming in at +2.4% Y/Y (vs. the consensus forecast of +2.1% and up from +2% in Dec). BBG

BABA +4% pre mkt reported solid Q4 upside, including revenue +2% to RMB247.7B (vs. the St RMB245.8B), EBITDA +15% to RMB59.16B (vs. the St $RMB53.5B), and EPS +14% to RMB19.26 (vs. the St 16.57). Revenue upside was driven by the core China Commerce business along with Int’l Commerce and Cainiao Logistics while Local Consumer Services and Cloud Computing fell a bit short. During Q4 the company repurchased 45.4 million ADSs for approximately US$3.3 billion. They still have $21.3B left on the buyback (as of 12/31). BBG

Chinese leader Xi Jinping is preparing to shake up the leadership of the country’s financial system, installing key associates to run the central bank and reviving a Communist Party body to tighten political control over financial affairs, according to people familiar with the discussions. WSJ

Washington is considering releasing intelligence showing that China is considering supplying weapons to Russia as part of a campaign aimed at deterring Beijing from intervening militarily. WSJ

South Korea’s central bank left rates on hold, as expected, joining the Bank of Canada as the second monetary authority to complete its hiking cycle. RTRS

The European Commission has banned its staff from using the TikTok app on their work-issued devices, widening across the Atlantic a patchwork of similar, limited bans affecting U.S. officials. WSJ

Europe’s final CPI for Jan was revised higher on core (from +5.2% to +5.3%) while the headline figure of +8.6% was kept unchanged. BBG

The US oil buildup continued. Inventories bumped up by just under 10 million barrels last week for a ninth weekly increase, the API is said to have reported. That would take total holdings to the highest in 21 months if confirmed by the EIA. More bearish pressures: Brent’s prompt timespread narrowed sharply yesterday, signaling a softer market, and the nearest spread for WTI indicates ample supply. BBG

New York Federal Reserve Bank President John Williams on Wednesday said the U.S. central bank is “absolutely” committed to bringing inflation back down to its 2% target over the next few years, by bringing demand down in line with constrained supply. RTRS

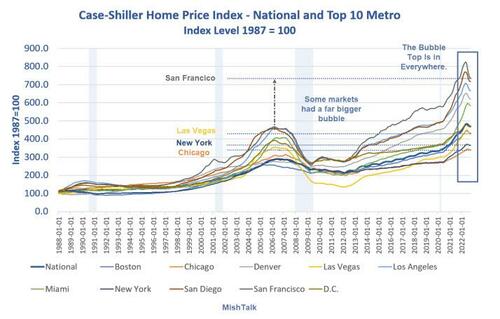

After peaking at $47.7 trillion in June, the total value of US homes declined by $2.3 trillion, or 4.9%, in the second half of 2022, according to real estate brokerage Redfin. That’s the largest drop in percentage terms since the 2008 housing crisis, when home values slumped by 5.8% from June to December. BBG

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks lacked firm direction with price action mostly rangebound amid thinned conditions due to the holiday closure in Japan and following the mixed performance stateside where the major indices faded mild gains in the aftermath of the FOMC minutes. ASX 200 was the laggard with the index weakened by underperformance in the mining industry after recent declines in commodity prices and a slump in Rio Tinto’s profits, although losses were limited as participants also digested better-than-expected capex data. KOSPI was the biggest gainer amid recent currency weakness and after the BoK kept its rate unchanged for the first time in a year, as unanimously expected. Hang Seng and Shanghai Comp. were indecisive with stocks initially led higher by strength in tech and after China vowed to improve measures to cut taxes and fees, although the gains were briefly pared amid ongoing global frictions and the PBoC’s liquidity drain.

Top Asian News

BoK maintained its base rate at 3.5%, as expected, while it noted uncertainties surrounding the policy decision are high and it deemed it warranted to keep a restrictive policy stance for a considerable time. BoK Governor Rhee said board member Cho Yoon-Je dissented and that the decision should not be taken as indicating the tightening cycle is over. Furthermore, Rhee stated that five members wanted to keep the chance open for the terminal rate to reach 3.75% and that the decision was based on the expectation that inflation will head down from March, while he added that it is time to stop and watch if the inflation trend goes along the expected path.

Chinese Commerce Ministry says the consumer market recovery momentum was strong in January, will take more measures to restore and expand consumption.

China is to shake up its financial system, according to WSJ; Citic Group Chairman Zhu Hexin is reportedly the leading candidate for PBoC governor, according to sources.

PLDT Said to Weigh Data Center Stake Sale After Spending Overrun

Janus Henderson Bets Big on Hedge Funds, Alts After Outflows

Astra Clinches Deal for China Drug to Boost Cancer Pipeline

European bourses are firmer on the session with a hefty earnings docket dictating action after an uninspiring APAC handover, Euro Stoxx 50 +0.4%. However, the FTSE 100 -0.5% is the exception following pressure from Anglo American and BAE Systems post earnings, though this is offset a touch by marked outperformance in Rolls Royce. Stateside, futures are broadly-speaking in-fitting with Europe though the NQ +0.7% outperforms given tailwinds from NVIDIA’s after-market update.

Top European News

BoE’s Mann says failing to do enough now risks the worst of both worlds – the higher inflation and lower activity – as monetary policy will have to stay tighter for longer. Believe that more tightening is needed, and caution that a pivot is not imminent. In her view preponderance of turning points is not yet in the data. BoE should weigh inflation more highly in our reaction function. Adding, she does not think UK monetary policy is in a restrictive stance particularly.

Axa Plans $1.2 Billion Buyback as Underlying Earnings Rise

Ukraine Latest: EU Rushes on Sanctions; Russians Still Back War

Eni Posts Record Annual Profit on High Oil and Gas Prices

Apollo Mulls $750 Million First Boston Leveraged-Finance Bet

EssilorLuxottica Falls After Profit Growth Slows in Second Half

WPP CEO Says AI Already ‘Fundamental’ to Advertising Giant

FX

The DXY continues to grind higher at the top-end of 104.30-65 parameters to the mixed fortune of peers.

Antipodeans are the modest outperformers with AUD benefitting from overnight data and NZD revisiting post-RBNZ highs amid commentary from Governor Orr; AUD/USD and NZD/USD printed peaks of 0.6841 and 0.6251 respectively.

Despite modest upside following hawkish commentary from BoE’s Mann, GBP is the incremental laggard vs USD, though Cable remains comfortably above 1.20 within 1.2015-74 boundaries.

Elsewhere, EUR was unreactive to unsurprising upwards revisions to January’s EZ HICP while the JPY is little changed ahead of domestic CPI and Ueda’s Lower House appearance; pivoting 1.06 and 134.90 respectively.

PBoC set USD/CNY mid-point at 6.9028 vs exp. 6.9028 (prev. 6.8759)

Fixed Income

Gilts are the incremental laggards post-Mann and down to a new 101.26 session low with the Sonia strip similarly dented; market pricing for a 25bp BoE hike in March is around the 95%, in-fitting with recent sessions.

Within the EZ, the hawkish direction remains in-play with Bunds at the lower-end of 133.92 to 134.41 parameters; similarly, USTs are underpressure ahead of 7yr supply and commentary from non-voters Bostic and Daly.

Commodities

WTI and Brent April futures are consolidating following another hefty session of losses on Wednesday which saw both benchmarks settle lower by almost USD 2.50/bbl apiece.

Nat Gas futures experienced modest divergence with TTF fairly contained while Henry Hub is firmer as attention turns to potential cold weather state-side ahead.

Exxon posted USD 2.5bln after-tax earnings in Kazakhstan and produced 246k bpd there for 2022, while it alerted against potential risks of disruptions of Kazakhstan oil through the CPC pipeline.

Spot gold has drifted towards the bottom of its intraday range as the Dollar picked up this morning, with the intraday low just under yesterday’s USD 1,823.56/oz trough

Geopolitics

Russian Defence Ministry accused Ukraine of planning to stage an ‘armed provocation’ in the near future against Transnistria, Moldova and noted that it is ready to respond to any changes in the situation, according to a Telegram and RIA news agency.

Russian President Putin said Moscow will pay increased attention to bolstering the country’s nuclear forces and will start mass deliveries of Zirkon sea-launched hypersonic missiles, according to Reuters.

US President Biden said Russian President Putin’s suspension of the New START treaty is a big mistake and is not very responsible, while Biden added that he does not read into Russian President Putin’s comments that he’s thinking of using nuclear weapons and sees no change in Russia’s nuclear posture, according to an interview with ABC News.

US mulls releasing intelligence on China’s potential arms transfer to Russia, according to WSJ.

Russian Defense Ministry plane has reportedly crashed near Belgorod, Russia, via AJA Breaking citing Tass.

US Event Calendar

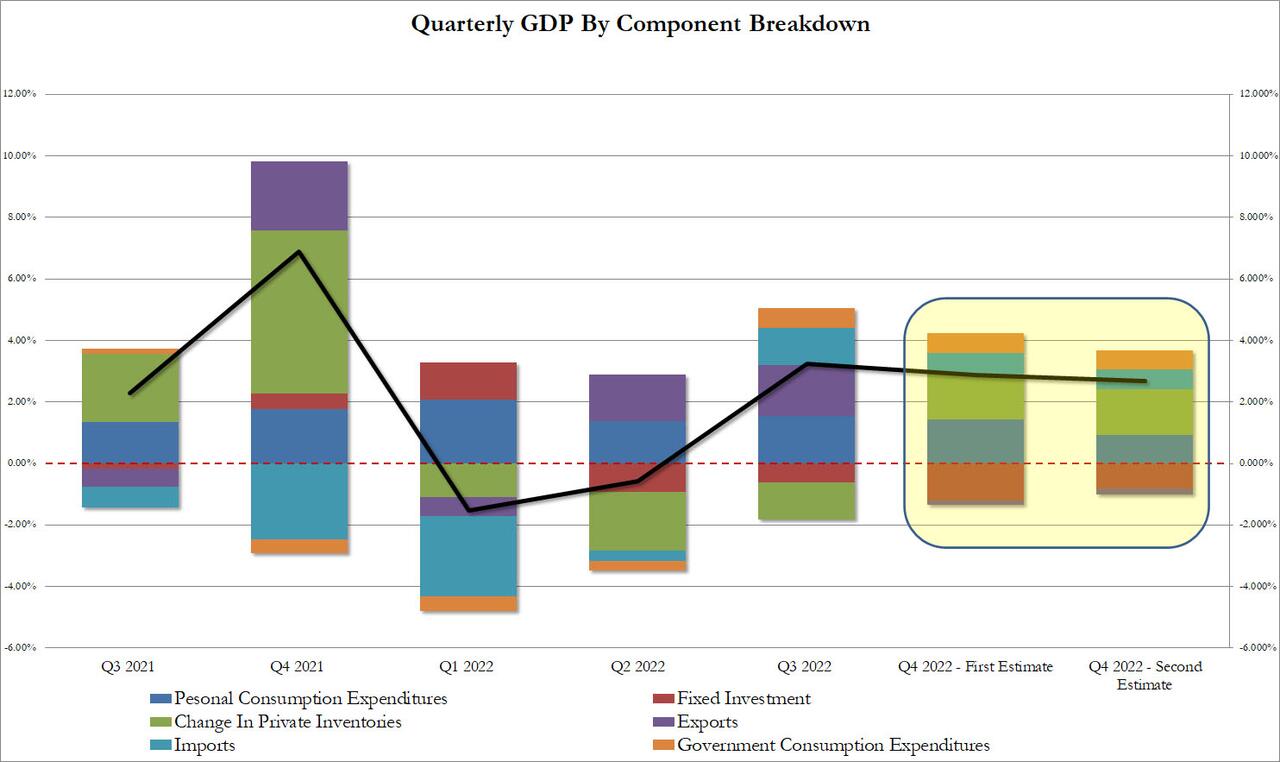

08:30: 4Q GDP Annualized QoQ, est. 2.9%, prior 2.9%

4Q Personal Consumption, est. 1.9%, prior 2.1%

4Q GDP Price Index, est. 3.5%, prior 3.5%

4Q PCE Core QoQ, est. 3.9%, prior 3.9%

08:30: Feb. Initial Jobless Claims, est. 200,000, prior 194,000

Feb. Continuing Claims, est. 1.7m, prior 1.7m

08:30: Jan. Chicago Fed Nat Activity Index, est. -0.25, prior -0.49

11:00: Feb. Kansas City Fed Manf. Activity, est. -2, prior -1

DB’s Jim Reid concludes the overnight wrap

Although markets have stabilised after Tuesday’s sell-off, the release of the FOMC minutes yesterday still led the S&P 500 (-0.16%) to lose ground for a 4th consecutive session, marking the longest run of declines of 2023 so far. Admittedly, the minutes were always going to feel a bit stale given the strong payrolls and CPI data as well as the upward revisions that have transpired since the meeting, but there were still some insights to be gleaned. In particular, they showed that “almost all” participants favoured downshifting to a 25bp hike, whilst “a few” still wanted a 50bp move. Furthermore, many on the committee “observed that a policy stance that proved to be insufficiently restrictive could halt recent progress in moderating inflationary pressures, leading inflation to remain above the Committee’s 2 percent objective for a longer period, and pose a risk of inflation expectations becoming unanchored.” That follows recent data prints indicating that policy may not yet be fully restrictive. And on financial conditions, the minutes noted that “a number of participants observed that financial conditions had eased in recent months, which some noted could necessitate a tighter stance of monetary policy.”

Following the minutes, pricing for the Fed’s terminal rate closed at its highest level of this cycle to date, with futures expecting a rate of 5.37% at the July meeting, ending the day up +0.5bps higher. Overall though, the curve was little changed, with the end-2023 rate for December down by -1.1bps to 5.18% by the close. In turn, that prompted US Treasuries to pare back their earlier gains, with the 10yr yield moving off its lows for the day prior to the minutes to only close down -3.7bps at 3.92%. Those swings were even more evident looking at the 2 year yield, which was down -7.1bps in the early US afternoon before spiking +4.1bps to end the day down -2.9bps at 4.69%.

The perception that the minutes had a hawkish tilt meant that market-based measures of US inflation expectations moved lower in response, having been on a consistent run higher over recent weeks. For instance, at one point yesterday the 2yr inflation breakeven was on track to close above 3% for the first time in over 6 months, before closing -1.9bps lower at 2.97%. Bear in mind it was only on January 18 that it closed at 2.04%, so the last month has seen a serious reappraisal about the likely path of inflation over the next couple of years. That’s been echoed at longer time horizons as well, with the 10yr breakeven on track to close at its highest level since early November yesterday just ahead of the minutes, before falling -4.1bps to 2.60%.

Ahead of the Fed minutes, we heard separately from St Louis Fed President Bullard who said in a CNBC interview that “I’m still at 5.375%” in terms of where he wanted to take rates. That would be 75bps above their current levels, and is roughly in line with where current market pricing is expecting terminal to get to. After the close, we then heard from New York Fed President Williams, who reiterated his previous stance that inflation would return to trend in the next “few years”. He noted that goods prices have come down, but not as quickly as he had hoped. He also echoed the FOMC minutes by emphasising they did not want the “inflation expectations anchor to slip.”

When it comes to the Fed’s hiking cycle, another interesting datapoint came from the Mortgage Bankers Association, whose index of home-purchase applications fell to its lowest level since 1995 in the week ending February 17. That comes as mortgage rates have begun to rise again following their decline at the end of last year, with the MBA’s data for a 30-year contract showing rates have gone up by +44bps in the last two weeks, which is the biggest two-week increase since September.

US equities had fluctuated between moderate gains and losses throughout the day, before moving lower following the FOMC minutes with the S&P 500 down -0.16%. The largest underperformers were mostly made up of cyclicals such as Real Estate (-1.02%), Transportation (-0.99%), and Energy (-0.77%), but also some defensives like Food & Staples (-1.15%). The best performers were led by Autos (+1.34%) due in large part to Tesla (+1.77%), and the NASDAQ (+0.13%) posted a modest gain as well.

Over in Europe, markets had similarly put in a pretty subdued performance ahead of the Fed minutes, with the STOXX 600 down a further -0.33%. That said, this marked a recovery from its earlier lows, when it had been down -1.03% during the European morning before recovering into the afternoon. It was much the same story for bonds, with yields on 10yr bunds as high as 2.57% intraday before closing -0.8bps lower at 2.52%. Those more positive moves came as we had further evidence that the economic situation was improving in Europe with the release of the Ifo Institute’s latest business climate indicator for February. That rose to 91.1 in February (vs 91.2 expected), which marked its 4th consecutive monthly advance and is its highest level since June. The expectations component also hit a 1-year high of 88.5 (vs. 88.4 expected), although the current assessment dipped slightly to 94.1 (vs. 94.9 expected).

Overnight in Asia, it’s a quieter session given the Japanese holiday today, but equity markets have remained subdued as in the US and Europe. For instance, the Hang Seng is up just +0.01% this morning, whilst the Shanghai Comp (-0.11%) and the CSI 300 (-0.11%) have both posted modest declines. The main exception to that pattern has come from the KOSPI (+1.01%), which follows the Bank of Korea’s decision to leave interest rates unchanged for the first time in a year, holding at 3.5%. The BoK’s Governor said that one member wanted a 25bp increase, and also that “I hope the hold this time isn’t going to be seen as meaning the rate-hike stance is over”. In response, the South Korean Won has strengthened by +0.62% against the US Dollar this morning. And looking forward, US equity futures are pointing to a better performance today, with those on the S&P 500 (+0.43%) and the NASDAQ 100 (+0.79%) posting decent gains.

To the day ahead now, and data releases include the final CPI release from the Euro Area in January, as well as the second estimate of US GDP in Q4. Otherwise, we’ll get the US weekly initial jobless claims, and the Kansas City Fed’s manufacturing index for February. Meanwhile from central banks, we’ll hear from the Fed’s Bostic and Daly, the ECB’s de Cos, and the BoE’s Cunliffe and Mann. Finally, today’s earnings releases include Booking Holdings and Moderna.

AND NOW NEWSQUAWK (EUROPE/REPORT)

NQ outperforms given NVIDIA strength, Gilts lag post-Mann – Newsquawk US Market Open

THURSDAY, FEB 23, 2023 – 06:33 AM

European bourses are firmer on the session with a hefty earnings docket dictating action after an uninspiring APAC handover.

Stateside, futures are broadly-speaking in-fitting with Europe though the NQ +0.7% outperforms given tailwinds from NVIDIA’s after-market update.

The DXY continues to grind higher at the top-end of 104.30-65 parameters to the mixed fortune of peers; Antipodeans outperform and GBP lags despite Mann.

Gilts are the incremental laggards post-Mann and down to a new 101.26 session low with the Sonia strip similarly dented, EGBs & USTs in-fitting though incrementally more contained.

BoE’s Mann says she does not think UK monetary policy is in a restrictive stance particularly.

WTI and Brent April futures are consolidating following another hefty session of losses, Henry Hub firmer, spot gold contained but erring lower.

Looking ahead, highlights include US GDP/PCE Q4 (2nd Estimate), IJC Japanese CPI, Speeches from Fed’s Bostic & Daly, BoE’s Cunliffe, Supply from US, Earning from Moderna.

Or why not try Newsquawk’s squawk box free for 7 days?

EUROPEAN TRADE

EQUITIES

European bourses are firmer on the session with a hefty earnings docket dictating action after an uninspiring APAC handover, Euro Stoxx 50 +0.4%.

However, the FTSE 100 -0.5% is the exception following pressure from Anglo American and BAE Systems post earnings, though this is offset a touch by marked outperformance in Rolls Royce.

Stateside, futures are broadly-speaking in-fitting with Europe though the NQ +0.7% outperforms given tailwinds from NVIDIA’s after-market update.

The DXY continues to grind higher at the top-end of 104.30-65 parameters to the mixed fortune of peers.

Antipodeans are the modest outperformers with AUD benefitting from overnight data and NZD revisiting post-RBNZ highs amid commentary from Governor Orr; AUD/USD and NZD/USD printed peaks of 0.6841 and 0.6251 respectively.

Despite modest upside following hawkish commentary from BoE’s Mann, GBP is the incremental laggard vs USD, though Cable remains comfortably above 1.20 within 1.2015-74 boundaries.

Elsewhere, EUR was unreactive to unsurprising upwards revisions to January’s EZ HICP while the JPY is little changed ahead of domestic CPI and Ueda’s Lower House appearance; pivoting 1.06 and 134.90 respectively.

PBoC set USD/CNY mid-point at 6.9028 vs exp. 6.9028 (prev. 6.8759)

Gilts are the incremental laggards post-Mann and down to a new 101.26 session low with the Sonia strip similarly dented; market pricing for a 25bp BoE hike in March is around the 95%, in-fitting with recent sessions.

Within the EZ, the hawkish direction remains in-play with Bunds at the lower-end of 133.92 to 134.41 parameters; similarly, USTs are underpressure ahead of 7yr supply and commentary from non-voters Bostic and Daly.

WTI and Brent April futures are consolidating following another hefty session of losses on Wednesday which saw both benchmarks settle lower by almost USD 2.50/bbl apiece.

Nat Gas futures experienced modest divergence with TTF fairly contained while Henry Hub is firmer as attention turns to potential cold weather state-side ahead.

Exxon posted USD 2.5bln after-tax earnings in Kazakhstan and produced 246k bpd there for 2022, while it alerted against potential risks of disruptions of Kazakhstan oil through the CPC pipeline.

Spot gold has drifted towards the bottom of its intraday range as the Dollar picked up this morning, with the intraday low just under yesterday’s USD 1,823.56/oz trough

BoE’s Mann says failing to do enough now risks the worst of both worlds – the higher inflation and lower activity – as monetary policy will have to stay tighter for longer. Believe that more tightening is needed, and caution that a pivot is not imminent. In her view preponderance of turning points is not yet in the data. BoE should weigh inflation more highly in our reaction function. Adding, she does not think UK monetary policy is in a restrictive stance particularly.

DATA RECAP

EU HICP Final YY (Jan) 8.6% vs. Exp. 8.6% (Prev. 8.5%); X F & E Final YY (Jan) 7.1% (Prev. 7.0%); X F, E, A & T Final YY (Jan) 5.3% vs. Exp. 5.2% (Prev. 5.2%)

NOTABLE US HEADLINES

Fed’s Williams (voter) said 2% inflation is a foundational target and price stability is an absolute imperative, while he noted an absolute commitment to getting back to 2% over the next few years.Williams stated that although goods prices have come down in the last several months, there are signs this may not go as quickly as hoped and said they don’t want inflation expectations anchor to slip. Furthermore, he noted that demand exceeds supply and the labour market is exceptionally strong, while monetary policy must bring demand and supply back into balance.

US Treasury Secretary Yellen says she does not have a specific timeframe for a resumption of dialogue with China.

Russian Defence Ministry accused Ukraine of planning to stage an ‘armed provocation’ in the near future against Transnistria, Moldova and noted that it is ready to respond to any changes in the situation, according to a Telegram and RIA news agency.

Russian President Putin said Moscow will pay increased attention to bolstering the country’s nuclear forces and will start mass deliveries of Zirkon sea-launched hypersonic missiles, according to Reuters.

US President Biden said Russian President Putin’s suspension of the New START treaty is a big mistake and is not very responsible, while Biden added that he does not read into Russian President Putin’s comments that he’s thinking of using nuclear weapons and sees no change in Russia’s nuclear posture, according to an interview with ABC News.

US mulls releasing intelligence on China’s potential arms transfer to Russia, according to WSJ.

Russian Defense Ministry plane has reportedly crashed near Belgorod, Russia, via AJA Breaking citing Tass.

CRYPTO

Bitcoin is firmer on the session having successfully reclaimed the USD 24k mark after losing the figure on Wednesday, though it remains shy of recent USD 25k+ levels.

APAC TRADE

APAC stocks lacked firm direction with price action mostly rangebound amid thinned conditions due to the holiday closure in Japan and following the mixed performance stateside where the major indices faded mild gains in the aftermath of the FOMC minutes.

ASX 200 was the laggard with the index weakened by underperformance in the mining industry after recent declines in commodity prices and a slump in Rio Tinto’s profits, although losses were limited as participants also digested better-than-expected capex data.

KOSPI was the biggest gainer amid recent currency weakness and after the BoK kept its rate unchanged for the first time in a year, as unanimously expected.

Hang Seng and Shanghai Comp. were indecisive with stocks initially led higher by strength in tech and after China vowed to improve measures to cut taxes and fees, although the gains were briefly pared amid ongoing global frictions and the PBoC’s liquidity drain.

NOTABLE ASIA-PAC HEADLINES

BoK maintained its base rate at 3.5%, as expected, while it noted uncertainties surrounding the policy decision are high and it deemed it warranted to keep a restrictive policy stance for a considerable time.BoK Governor Rhee said board member Cho Yoon-Je dissented and that the decision should not be taken as indicating the tightening cycle is over. Furthermore, Rhee stated that five members wanted to keep the chance open for the terminal rate to reach 3.75% and that the decision was based on the expectation that inflation will head down from March, while he added that it is time to stop and watch if the inflation trend goes along the expected path.

Chinese Commerce Ministry says the consumer market recovery momentum was strong in January, will take more measures to restore and expand consumption.

China is to shake up its financial system, according to WSJ; Citic Group Chairman Zhu Hexin is reportedly the leading candidate for PBoC governor, according to sources.

DATA RECAP

Australian Capital Expenditure (Q4) 2.2% vs. Exp. 1.3% (Prev. -0.6%)

Australian Private Capital Expenditure 2023-2024 (AUD)(Est. 1) 129.7B; 2022-2023 (AUD)(Est. 5) 158.7B (Prev. 155.7B)

THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 3.67 PTS OR 0.11% //Hang Seng CLOSED DOWN 72.49 PTS OR 0.35% /The Nikkei closed //Australia’s all ordinaries CLOSED DOWN 0.33% /Chinese yuan (ONSHORE) closed DOWN 6.8984 //OFFSHORE CHINESE YUAN DOWN TO 6.9043// /Oil DOWN TO 74.86dollars per barrel for WTI and BRENT AT 81.20 / Stocks in Europe OPENED MOSTLY GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

China’s propagandists tell us the Chinese economy this year will “accelerate to 4.8%.” Foreign analysts are even more bullish. Goldman Sachs estimates growth of gross domestic product of 5.5%.

China’s National Health Commission announced the end of the Communist Party’s “dynamic zero-Covid” policy on December 7. It did not take long for Wall Street to crank up the optimism machine. Morgan Stanley, on the following day, issued a research note predicting that Chinese equities would outperform emerging markets and global peers.