April 4//2023 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSED: UP $0, TO $2019.80

SILVER PRICE CLOSED: DOWN $.04 AT $24.93

work in progress.

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE 2020.70

Silver ACCESS CLOSE: 24.93

Bitcoin morning price:, $28,522 UP 379 Dollars

Bitcoin: afternoon price: $28,177 UP 143 dollars

Platinum price closing $1001.80 UP $11.85

Palladium price; closing $1435.80 DOWN $25.80

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2729.23 UP 1.70 CDN dollars per oz (ALL TIME HIGH 2732.50)

BRITISH GOLD: 1621.45 UP 3.94 pounds per oz//(ALL TIME HIGH//1629.84)

EURO GOLD: 1853,35 UP 8,13 euros per oz //(ALL TIME HIGH//1860.82)

COMEX DATA EXCHANGE:

EXCHANGE: COMEX

CONTRACT: APRIL 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,022.200000000 USD

INTENT DATE: 04/04/2023 DELIVERY DATE: 04/06/2023

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 11

104 C MIZUHO 5

132 C SG AMERICAS 5

323 C HSBC 412

363 H WELLS FARGO SEC 30

435 H SCOTIA CAPITAL 61

624 C BOFA SECURITIES 3

624 H BOFA SECURITIES 151

657 C MORGAN STANLEY 76

661 C JP MORGAN 88 60

661 H JP MORGAN 90

690 C ABN AMRO 2

732 C RBC CAP MARKETS 2

800 C MAREX SPEC 16 17

880 C CITIGROUP 55

880 H CITIGROUP 128

905 C ADM 1 5

TOTAL: 609 609

MONTH TO DATE: 20,498

PMORGAN stopped 60/ 689 contracts

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2023. CONTRACT: 689 NOTICES FOR 68900 OZ or 2.1430 TONNES

total notices so far: 20,498 contracts for 2,049,800 oz (62,363 tonnes)

SILVER NOTICES: 11 NOTICE(S) FILED FOR 55,000 OZ/

total number of notices filed so far this month : 223 for 1,115,000 oz

END

GLD

WITH GOLD UP $36.30

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:////// A HUGE DEPOSIT OF 2.02TONNES FROM THE GLD.

INVENTORY RESTS AT 930.02 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER UP $1,11

WOW!! WHAT CROOKS:

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE WITHDRAWAL OF 1.47 MILLION OZ FROM THE SLV: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 463.942 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A MONSTER SIZED 7472 TO 131,344 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS GIGANTIC SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR HUGE $1.11 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. WITH LAST WEEK’S READING AT THE COMEX , WE HAVE NOW SET ANOTHER RECORD LOW AT 117,395 CONTRACTS , MARCH 29.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $1.11). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A MONSTER GAIN ON OUR TWO EXCHANGES 11,027 CONTRACTS. WE HAD 500 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 8.5 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS( 3555 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.055 MILLION OZ(FIRST DAY NOTICE)+ THE 8.5 MILLION OZ OF EXCHANGE FOR RISK//THUS TOTAL NEW STANDING 9.255 MILLION OZ/ //// V) HUGE SIZED COMEX OI GAIN/ HUGE SIZED EFP ISSUANCE/.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –134 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTRACTS for 3 days, total 6979 contracts: OR 30.395 MILLION OZ . (2326 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR:30.395 MILLION OZ

.

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE BUT BELOW LAST MONTH

APRIL 30.395 MILLION OZ

RESULT: WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 7472 CONTRACTS WITH OUR $1.11 GAIN IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 3555 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL OF 1.055 MILLION OZ//FIRST DAY NOTICE// 65,000 OZ QUEUE JUMP (WHICH INCREASES THE AMOUNT OF SILVER STANDING) + 8.5 MILLION NEW EXCHANGE FOR RISK ISSUED EARLY IN APRIL (INCREASES THE AMOUNT OF SILVER STANDING) //NEW STANDING 9.255 MILLION OZ .. WE HAVE A GIGANTIC SIZED GAIN OF 11,161 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 11 NOTICE(S) FILED TODAY FOR 55,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GIGANTIC SIZED 15,440 CONTRACTS TO 476,392 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED 634 CONTRACTS

WE HAD A HUGE SIZED INCREASE IN COMEX OI ( 15,440 CONTRACTS) WITH OUR $36.30 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR APR. AT 66.892 TONNES ON FIRST DAY NOTICE // PLUS A 7000 OZ E.F.P. JUMP:(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)YET ALL OF..THIS HAPPENED WITH OUR $36.30 GAIN IN PRICE WITH RESPECT TO TUESDAY’S TRADING.WE HAD AN ATMOSPHERIC SIZED GAIN OF 24,556 OI CONTRACTS (76.38 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 9116 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 475,958

IN ESSENCE WE HAVE A HUMONGOUS SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 24,556 CONTRACTS WITH 15,440 CONTRACTS INCREASED AT THE COMEX AND 9116 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 24,556 CONTRACTS OR 76,38 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A HUMONGOUS SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (9116 CONTRACTS) ACCOMPANYING THE GIGANTIC SIZED GAIN IN COMEX OI (15,440 //TOTAL GAIN IN THE TWO EXCHANGES 24,556 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 66.892 TONNES FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 7000 OZ//NEW STANDING 67.269 TONNES // ///3) ZERO LONG LIQUIDATION//4) GIGANTIC SIZED COMEX OPEN INTEREST GAIN/ 5) HUMONGOUS ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAR :

TOTAL EFP CONTRACTS ISSUED: 13,747 CONTRACTS OR 1,374,700 OZ OR 42.76 TONNES IN 3 TRADING DAY(S) AND THUS AVERAGING: 4582 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAY(S) IN TONNES 42.76 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 42.76 /3550 x 100% TONNES 1.21% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 42.76 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A GIGANTIC SIZED 7472 CONTRACTS OI TO 131,210 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 3555 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 3555 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3555 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 7472 CONTRACTS AND ADD TO THE 3555 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE GAIN OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 11,027 CONTRACTS.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES //55.805 MILLION OZ(WHICH REPRESENTS AROUND 7% OF ANNUAL SILVER PRODUCTION FROM ALL MINING)

OCCURRED WITH OUR $1.11 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

NORTH KOREA/SOUTH KOREA

i)WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED //Hang Sang CLOSED /The Nikkei closed DOWN 474.16PTS OR 1.68% //Australia’s all ordinaries CLOSED UP 1.19 % /Chinese yuan (ONSHORE) closed UP TO 6.8795 /OFFSHORE CHINESE YUAN UP TO 6.8795 /Oil UP TO 80.54 dollars per barrel for WTI and BRENT AT 84.83 / Stocks in Europe OPENED MOSTLY MIXED// ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A HUGE SIZED 15,440 CONTRACTS UP TO 476,392 WITH OUR HUGE GAIN IN PRICE OF $36.30 ON TUESDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF APRIL… THE CME REPORTS THAT THE BANKERS ISSUED A HUMONGOUS SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 9116 EFP CONTRACTS WERE ISSUED: : JUNE 9116 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 9116 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: AN ASTRONOMICAL TOTAL OF 24,556 CONTRACTS IN THAT 9116 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A HUGE SIZED GAIN OF 15,440 COMEX CONTRACTS..AND THIS STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $36,30. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: APRIL (67.269) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 67.269 tonnes

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $36.30 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR MONSTER SIZED GAIN OF 24,556 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 76,38 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL. (66.892 TONNES) FOLLOWED BY TODAY’S EFP JUMP TO LONDON OF 7000 OZ… ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $36.30

WE HAD + ADDED 634 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 24,556 CONTRACTS OR 2,455,600 OZ OR 76,38TONNES.

Estimated gold comex today 198,444/fair

final gold volumes/yesterday 245,200 //FAIR

//APRIL 5/ APRIL 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 15,593.235 OZ DELAWARE HSBC INT. DELAWARE 220 KILOBARS 250 KILOBARS 15 KILOBARS . |

| Deposit to the Dealer Inventory in oz | 48,226,500 OZ MANFRA 1500 KILOBARS |

| Deposits to the Customer Inventory, in oz | 160,753.000 oz MANFRA 5,000 KILOBARS |

| No of oz served (contracts) today | 689 notice(s) 68,900 OZ 2.2143 TONNES |

| No of oz to be served (notices) | 1129 contracts 112900 oz 3.511 TONNES |

| Total monthly oz gold served (contracts) so far this month | 20,498 notices 2,049,800 OZ 62.363 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 1

I) INTO MANFRA: 48,226.500 OZ 5000 KILOBARS

total dealer deposit: 48,226.500 oz

No dealer withdrawals

Customer deposits: 1

I) INTO JPMORGAN: 160,755.000 OZ (5,000 KILOBARS)

total deposits: 160,755.000 oz

customer withdrawals: 3

I) OUT OF DELAWARE: 7073.22 OZ

II) OUT OF HSBC 8037.75 OZ

III) OUT OF INT. DELAWARE 482.265 OZ

total withdrawals: 15,593.235 oz

in tonnes:0.

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of APRIL we have an oi of 1818 contracts having LOST 781 contracts.

We had 711 contracts filed on Monday, so we LOST 70 contracts or 7000 oz (0.2177 tonnes) were EFP’d to London

May LOST 39 contracts to stand at 1528

JUNE GAINED 13,785 contracts to 409,885

We had 689 notice(s) filed today for 68900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 88 notices were issued from their client or customer account. The total of all issuance by all participants equate to 689 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 60 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2023. contract month,

we take the total number of notices filed so far for the month (20,498x 100 oz ), to which we add the difference between the open interest for the front month of (APRIL. 1818 CONTRACTS) minus the number of notices served upon today 689 x 100 oz per contract equals 2,162,700 OZ OR 67.269 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month:No of notices filed so far (20,498 x 100 oz+ XX OI for the front month minus the number of notices served upon today (689)x 100 oz} which equals 2,162700 oz standing OR 67.269 TONNES in this active delivery month of APRIL..

TOTAL COMEX GOLD STANDING: 67.713 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,643,341.368 OZ 51.114 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,769,099.131 OZ

TOTAL REGISTERED GOLD: 12,274,064.074 (381.77 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 9,495,035,057 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,630,723 OZ (REG GOLD- PLEDGED GOLD) 330.66tonnes//

END

SILVER/COMEX

APRIL 5//2023// THE APRIL 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 668,940.006oz Brinks CNT Delaware JPMorgan . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | NIL oz WITHDRAWALS 814,070.470 OZ BRINKS CNT LOOMIS |

| No of oz served today (contracts) | 11 CONTRACT(S) (55,000 OZ) |

| No of oz to be served (notices) | 28 contracts (140,000 oz) |

| Total monthly oz silver served (contracts) | 223Contracts (1,115,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 0 deposits into the customer account

i

Total deposits: NIL oz

JPMorgan has a total silver weight: 143,075 million oz/276.742 million =51.81% of comex .//dropping fast

Comex withdrawals: 3

i)Out of Brinks 112,373.900 oz

ii) Out of CNT 101,197.260 oz

iii) out of LOOMIS 600,499.310 oz

Total withdrawals; 814,070.470 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 35.486 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 276.782million oz

CALCULATION OF SILVER OZ STANDING FOR MAR

silver open interest data:

FRONT MONTH OF APRIL /2023 OI: 39 CONTRACTS HAVING LOST 1 CONTRACT(S. WE HAD 14 NOTICES FILED ON TUESDAY SO WE GAINED 13 CONTRACTS OR AN ADDITIONAL 65,000 OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF APRIL.

MAY SAW A GAIN OF 3702 CONTRACTS UP TO 93,420 (UNBELIEVABLE//WITH MAY THE FRONT MONTH??)

JUNE HAD A 7 CONTRACT GAIN I AND RISES TO 31

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 11 for 55,000 oz

Comex volumes// est. volume today 72,256 good

Comex volume: confirmed yesterday: 92,366 Contracts ( EXCELLENT)

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 223 x 5,000 oz = 1,115,000 oz

to which we add the difference between the open interest for the front month of APRIL(39) and the number of notices served upon today 11 X (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL/2023 contract month: 223 (notices served so far) x 5000 oz + OI for the front month of APRIL (39) – number of notices served upon today (11 )x 500 oz of silver standing for the APRIL. contract month equates 1.255 million oz +/ EXCHANGE FOR RISK NOW TOTALS 8.5 MILLION OZ //new total standing 9.755 million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

APRIL 5//WITH GOLD UP XX TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT XXXX

APRIL 4/WITH GOLD UP $36.30 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

APRIL 3/WITH GOLD UP $14.20 TODAY;NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.02 TONNES

MARCH 31/WITH GOLD DOWN $10.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD////INVENTORY RESTS AT 928.02 TONNES

MARCH 30//WITH GOLD UP XX TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A DEPOSIT OF 2.24 TONNES FROM THE GLD/INVENTORY RESTS AT 929.47 TONNES

MARCH 29/WITH GOLD DOWN $4.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4,16 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 927,23

MARCH 28/WITH GOLD UP $19.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

MARCH 15/THE IDES OF MARCH: WITH GOLD UP $18.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 913.27 TONNES

MARCH 14/WITH GOLD DOWN $4.75 TODAY: HUGE CHANGES: A MONSTER DEPOSIT OF 11.85 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 913.27 TONNES

MARCH 13/WITH GOLD UP $48.85 TODAY: VERY STRANGE HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY REST AT 901.42 TONNES

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

FEB 28/WITH GOLD UP $12.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 917.61 TONNES

FEB 27/WITH GOLD UP $6.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.32 TONNES

FEB 24/WITH GOLD DOWN $9.10 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 917.32 TONNES

FEB 23/WITH GOLD DOWN $13.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 919.92 TONNES

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

GLD INVENTORY: 930.04 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 5/WITH SILVER UP XX TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.942 MILLION OZ

APRIL 4/WITH GOLD UP $1.11 TODAY CRIMINAL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.47 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 463,942 MILLIONOZ

APRIL 1/WITH SILVER DOWN 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.412

MARCH 31/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE GLD/: A MASSIVE 4.779 MILLION OZ DEPOSITED INTO THE SLV///INVENTORY RESTS AT465.412 MILLION OZ

MARCH 30/WITH SILVER UP XX CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV.: A DEPOSIT OF 550,000 OZ INTO THE SLV/.INVENTORY RESTS AT 460.633 MILLION OZ

MARCH 29/WITH SILVER UP 11 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 460.082

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

MARCH 17/WITH SILVER UP 79 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE WITHDRAWAL OF 10.478 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 462.748 MILLION OZ//

MARCH 16/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 5.009 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 473.226 MILLION OZ//

MARCH 15/WITH SILVER DOWN 7 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 643,000 OZ INTO THE SLV//INVENTORY RESTS AT 478.235 MILLION OZ/

MARCH 14/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.287 MILLION OZ FROM THE SLV////INVENTORY REST AT 477.592 MILLION OZ//

MARCH 13/WITH SILVER UP $1.35 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ//

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWALOF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

FEB 28/WITH SILVER UP 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.241 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.188

FEB 27/WITH SILVER DOWN 15 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.471 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 482.429 MILLION OZ

FEB 24/WITH SILVER DOWN 46 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.172 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.900 MILLION OZ//

FEB 23/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.072 MILLION OZ//

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 463.942MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

End

2 Lawrie Williams//Pam and Russ Martens/Jim Rickards/Mathew Piepenburg/Von Greyerz//Rickards/John Rubino

Rickards: Why The Panic Is Just Beginning

WEDNESDAY, APR 05, 2023 – 02:20 PM

Authored by James Rickards via DailyReckoning.com,

Let’s step back from today’s banking financial crisis and look at the bigger picture. That will help us to understand the system dynamics, and estimate how long the crisis might last, and how destructive it might be.

As a preliminary matter, let’s distinguish between a recession (even a bad one) and a financial crisis. They’re different.

A recession is a part of the business cycle. It involves some combination of tighter monetary conditions, higher unemployment, business failures, inventory dumping, declines in industrial output and declining GDP.

In recent decades, we’ve had recessions in 1973, 1980, 1981, 1990, 2000, 2007 and 2020. That’s a tempo of one recession about every seven years, although the recessions of 1980 and 1981 show that back-to-back recessions are possible.

Of those, the 2007 recession lasted the longest (one year and six months). The 2020 recession produced the most severe decline in GDP (down 19.2%).

The U.S. is likely in another recession right now, but we won’t have confirmation of that until more first-half data is revealed.

Over the same 50-year period, we’ve had a succession of financial crises.

These included the Latin American debt crisis (1982–1987), the Savings & Loan Crisis (1986–1989), the Black Monday crash (Oct. 19, 1987), the Nikkei collapse (1990), the Mexican Tequila Crisis (1994), The Asia-Russia-LTCM crisis (1997–1998), the dot-com crash (2000) and the subprime mortgage crisis (2007–2008).

That’s eight crises in 50 years or a tempo of one crisis about every six years.

So much for the “Black Swan” theory, and the idea of 5-sigma events that occur once every 14,000 years. That’s junk science. These things happen all the time.

What’s interesting about financial crises is that they are rarely the same. Some produce large losses but there’s no acute stage where the financial system is hanging by a thread. The Latin American debt crisis, the S&L crisis, and the Nikkei collapse fit into that category.

They lasted for years, but they were manageable in a cash and accounting sense. In some ways, the Nikkei collapse is still going on thirty-five years after it happened because the Nikkei stock index has never recovered the 40,000 level it hit in late 1989.

Other crises were acute but came and went without threatening the banking system. The 1987 flash crash was a good example. It happened, but not much else happened. Two days after the crash turned out to be a great time to buy stocks!

A similar analysis applies to the Mexican Tequila Crisis and the Dot.com collapse. They were over quickly, the banking system as a whole was never threatened, and astute investors with cash could buy in at the low and ride the next wave up.

The only two crises that did come close to destroying the global financial system were the Asia-Russia-LTCM crisis in 1998, and the Subprime Mortgage Crisis in 2007 – 2008.

Even those crises had important differences.

The Asia-Russia-LTCM crisis was acute but there was no recession. Economic growth and the stock market bubble didn’t peak until 2000.

What sets the 2007 – 2008 crisis apart is that it was an existential financial crisis and a severe recession. (The 2020 recession was the most severe, but there was no financial crisis).

If we set the clock at 1973 and count 1998 and 2008 as the only existential crises, then the tempo is once every twenty-five years. That’s a small sample. The last acute crisis was fifteen years ago.

We can draw several conclusions from this data.

- The first is that recessions and financial crises are different.

- The second is that recessions have much in common but financial crises tend to be idiosyncratic and unpredictable.

- The third is that existential financial crises really are rare; only two in the past fifty years.

- The fourth and most important conclusion is that the combination of a recession and an existential financial crisis is extremely rare.

The events of 2007 – 2008 are the only such combined case in our timeline.

You have to go back to the Great Depression of 1929 – 1940 to find a similar case. That period involved two recessions (1929-1933 and 1937-1938), a massive wave of bank failures (1931-1933), continual currency devaluations, and a collapse of world trade.

Now for the all-important question: Is history repeating itself?

Read on for the answer.

Is History Ready to Repeat Itself?

For our purposes, this history shines a light on the combined crises of 2008. Is history now repeating in its own curvilinear way?

The evidence that we are in a recession is powerful. Low unemployment is almost irrelevant because labor force participation is also low. World trade is contracting. Industrial output is declining. Wholesale inventories are high, which means markdowns and lower profit margins are on the way. Interest rates are still going up and inflation is still sapping real wages.

Much of Europe and Japan are already in recession. The China “reopening” is a flop. The stock market has been volatile but the trend is not your friend. Treasury yield curves are steeply inverted, a condition last seen in 2007. The recession part of the Recession+Crisis condition is already here.

What about another global financial crisis? We know that a banking crisis has already begun. Here’s the casualty list from just this month:

- Silvergate Bank – Announced its bankruptcy on March 8

- Silicon Valley Bank – Taken over by the FDIC on March 10

- Signature Bank – Taken over by the FDIC on March 12

- First Republic Bank – $30 billion liquidity rescue by 11 banks on March 16

- Credit Suisse – Swiss government shotgun wedding with UBS on March 19

That’s five bank failures or rescues in eleven days including Credit Suisse, one of the largest banks in the world and the second largest in Switzerland. Combined losses of stockholders and creditors of these institutions exceed $200 billion. Market losses in the banking sector are much greater.

These failures and rescues were accompanied by extraordinary regulatory actions. The FDIC abandoned its $250,000 deposit insurance limit and effectively guaranteed all the depositors in Silicon Valley Bank and Signature Bank, a guarantee of over $200 billion in deposits. This will deplete the FDIC insurance fund and require higher insurance premiums from solvent banks, the cost of which will ultimately be borne by consumers.

The Federal Reserve went further and offered to lend money at par for any government securities tendered as collateral by member banks even if the collateral was worth only 80% or 90% of par. These collateralized loans will be financed with newly printed money, which might exceed $1 trillion.

These actions have thrown the U.S. banking system and bank depositors into utter confusion. Are all bank deposits now insured or just the ones Janet Yellen decides are “systemically important?” What’s the basis for that decision? What about the fact that unrealized losses on U.S. bank portfolios of government securities now exceed $700 billion?

If those losses are realized to provide cash to fleeing depositors, it could wipe out much of the capital of the banking system.

The most important question is: Is the crisis over? Has the Fed done enough to reassure depositors that the system is sound? Has the panic subsided?

The answer is, no. The panic is just getting started.

We base that answer on the history of the two acute financial crises in recent decades — 1998 and 2008. The 1998 crisis reached the acute stage on September 28, 1998, just before the rescue of LTCM. We were hours away from the sequential shutdown of every stock and bond exchange in the world.

But that crisis began in June 1997 with the devaluation of the Thai Baht and massive capital flight from Asia and then Russia. It took fifteen months to go from a serious crisis to an existential threat.

Likewise, the 2008 crisis reached the acute stage on September 15, 2008, with the bankruptcy filing of Lehman Brothers. But that crisis began in the spring of 2007 when HSBC surprised markets with an announcement that mortgage losses had exceeded expectations.

It then continued through the summer of 2007 with the failures of two Bear Stearns high-yield mortgage funds, and the closure of a Société Générale money market fund. The panic then caused the failures of Bear Stearns (March 2008), Fannie Mae and Freddie Mac (June 2008), and other institutions before reaching Lehman Brothers.

For that matter, the panic continued after Lehman to include AIG, General Electric, the commercial paper market, and General Motors before finally subsiding on March 9, 2009. Starting with the HSBC announcement, the subprime mortgage panic and domino effects lasted twenty-four months from March 2007 to March 2009.

Averaging our two examples (1998, 2008) the average duration of these financial crises is about twenty months. This new crisis is one-month old. It could have a long way to run.

On the other hand, this crisis could reach the acute stage faster. That’s because of technology that makes a bank run move at the speed of light. With an iPhone you can initiate a $1 billion wire transfer from a failing bank while you’re waiting in line at McDonald’s. No need to line up around the block in the rain waiting your turn.

In addition, the regulatory response is faster because they’ve seen this movie before. That begs the question of whether regulators are out of bullets because they’ve already guaranteed almost everything so they don’t have more rabbits to pull out of the hat.

This could be the crisis where the panic moves from the banks to the dollar itself. If savers lose confidence in the Fed (we’re almost there) not only will the banks collapse, but the dollar will collapse also. At that point, the only solution is gold bullion.

Further evidence comes from the fact that no sooner was the Credit Suisse shotgun wedding completed than investors aimed their sights at Deutsche Bank, another perennial weak link in the chain. Who’s next? Barclays? Santander? We don’t know. Neither do regulators or investors. But we do know more failures are coming.

By the way, this is not really a banking crisis even though it plays out in the form of bank failures. What’s going on is a crisis caused by a shortage of Treasury bill collateral to support derivatives positions and shrinking balance sheets as a consequence of the collateral shortage.

Why doesn’t the Treasury just issue, say, $2 trillion of new T-bills and let the primary dealers and Fed underwrite them with as much printed money as needed? One reason is that neither Jay Powell nor Janet Yellen understands what we just described.

The other reason is that we’re up against the X-Date when the Treasury runs out of cash and can’t borrow more because of the debt ceiling. Is Congress ready to raise the debt ceiling? Nope. It’s the usual Democrat versus Republican game of chicken with no resolution in sight.

So, we go from bank runs to a Treasury bill shortage to a debt ceiling standoff in no time. Do regulators and financial journalists understand this? No, they don’t know how to connect the dots. But you get it.

We may not be able to prevent the crisis, but we can see it coming and prepare accordingly to preserve wealth. Step one is to get gold. That will see you through the storm.

END

3,Chris Powell of GATA provides to us very important physical commentaries

END

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

.

END

5.IMPORTANT COMMENTARIES ON COMMODITIES:

END

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 6.8795

OFFSHORE YUAN: 6.8795

SHANGHAI CLOSED

HANG SANG CLOSED

2. Nikkei closed DOWN 474.16 PTS OR 1.68 %

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 101.328 EURO RISES TO 1.0945 UP 5BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.468 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 131.63 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN-// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.2950 ***/Italian 10 Yr bond yield RISES to 4,161*** /SPAIN 10 YR BOND YIELD RISES TO 3.284…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.145

3j Gold at $2022.75 silver at: 24.81 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 78/100 roubles/dollar; ROUBLE AT 79.57//

3m oil into the 80 dollar handle for WTI and 84 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 131.63 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .468% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9047 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9914 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.365 UP 3 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.605 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.88545 UP 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.25…

GREAT BRITAIN/10 YEAR YIELD: UP 9 BASIS PTS AT 3.530

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Dip Ahead Of Private Payrolls Data, After Hawkish Surprise Out Of New Zealand

BY TYLER DURDEN

WEDNESDAY, APR 05, 2023 – 03:11 PM

US stock futures edged lower on Wednesday, extending Tuesday’s post-JOLTs declines into a second day ahead of even more employment data including the ADP private payrolls report, as hawkish messages from New Zealand and Australian central banks signaled a prolonged fight against price pressures and revived concerns about a deeper economic slowdown. Gold extended a 13-month high. The two-year Treasury yield rose for the first time in four days and the dollar fluctuated.

Contracts on the Nasdaq 100 and the S&P 500 were both down by about 0.1% as of 7:30 a.m. in New York. The indexes had dropped on Tuesday following soft labor market data. In Europe the FTSE100 is up 0.5%, boosted by AstraZeneca gains after positive drug trial results.

Among notable premarket movers, Johnson & Johnson was set for its biggest gain in nearly a year after the drugmaker agreed to pay $8.9 billion to resolve all cancer lawsuits related to its talc-based powders. Nvidia Corp. slid 1.6% in US premarket trading as traders weighed Japan’s decision to join a US alliance to restrict chip-making exports to China. Western Alliance Bancorp dropped 4.8% after the lender’s quarter-end update, with analysts saying that the lack of an explicit deposit balance was frustrating for investors, and the rise in insured deposits also raised questions.Here are other notable premarket movers:

- C3.ai (AI) is poised to extend its losses after plunging 26% on Tuesday — the most ever in a single day — as short-seller Kerrisdale Capital alleged “serious accounting and disclosure issues” at the enterprise-software developer. Shares decline 4% in premarket trading.

- Dlocal (DLO) drops 5.7% after the Uruguay- based payments services company reported earnings per share for the fourth quarter that missed the average analyst estimate.

- Dutch Bros Inc. (BROS) rises 3.6% after a Wedbush analyst raised the recommendation on the operator of drive-thru beverage shops to outperform from neutral, citing 2023 adjusted Ebitda guidance that is “not only realistic, but conservative.”

- Exxon (XOM) slips 0.3% after the energy producer said that its first-quarter profit took a hit of as much as $1.8 billion due to a slump in oil and gas prices.

- Fluence Energy (FLNC) rises as much as 5% after the renewable energy storage equipment provider was upgraded to buy from neutral at Guggenheim on increased confidence in the company’s competitive position.

- Johnson & Johnson (JNJ) rises as much as 3% after the drugmaker agreed to pay $8.9 billion to resolve all cancer lawsuits related to its talc-based powders. Analysts note that the amount is lower than expected and the development would be positive for the stock, though questions remained whether the settlement would be approved in court.

US stocks slumped on Tuesday after the latest jobs data yesterday showed a drop in job vacancies, boosting recession fears; economists expect data Wednesday to show private employers added a more modest number of jobs in March. The crucial non-farm payrolls report is due Friday.

Economic data are “pointing toward a potential recession, but the upside might be a pause in interest rates, which would typically be a positive for stocks,” said Danni Hewson, head of financial analysis at AJ Bell. “The concern is the Fed might have to sound the retreat before its war on inflation is truly done. This could leave us with the worst of all worlds – the dreaded stagflation where the economy is shrinking but prices are continuing to surge higher.”

With worries about a recession driving bets on lower interest rates, growth stocks and tech names have rallied in recent weeks but UBS Global Wealth Management strategists said they still preferred more defensive sectors such as consumer staples and utilities as growth valuations remain expensive. They also recommend non-US assets.

Meanwhile, on the inflation-fighting front, the Reserve Bank of New Zealand surprised markets with a half-point interest rate hike, twice as much as forecast. Governor Adrian Orr said inflation is too high and that expectations for price increases may also remain elevated despite a weaker economy. Meanwhile, Reserve Bank of Australia Governor Philip Lowe pushed back against bets its tightening cycle is ending, saying policymakers still expect a need for higher rates.

“The battle against inflation looks far from won,” said Ivailo Vesselinov, chief strategist at Emso Asset Management Ltd. in London. “Notwithstanding the latest signs of softening economic activity, should disinflation hit a wall later this year, major central banks would struggle to validate the current market pricing for rate cuts.”

European stocks followed US futures and Asian markets lower as investors fret over a stuttering global economy and the prospect of additional monetary tightening. The Stoxx 600 is down 0.2% after hitting its best level in almost four-weeks on Tuesday. The FTSE 100 has outperformed with gains of 0.4%, boosted by AstraZeneca which has rallied after positive drug trial results. Sodexo SA, a provider of catering services, jumped 11% in Paris after announcing plans to spin off its benefits and rewards business. Here are the biggest European movers:

- Iberdrola shares rise as much as 2.3% after Mexico agreed to buy a fleet of natural gas plants and a wind farm for $6 billion from Spain’s biggest power company

- Direct Line bounces as much as 5.9% in early trading, after Citi double-upgraded it to buy from sell, saying the motor-insurance pricing cycle has now bottomed out

- Sodexo shares jump as much as 11% to their highest level in more than three years after the French food services and facilities management company reported a 1H profit beat

- SIG Group shares rise as much as 2.8% as Stifel upgrades the firm to buy from hold, saying it expects consumables packaging firms to deliver above-average growth in 2023

- Nexans falls as much as 9% after an offering of 4.2m shares by holder Invexans priced at €80 apiece, representing a 9.6% discount to last close

- De Nora falls as much as 6.2% after an offering of 11.5m shares by holders Snam, Federico de Nora SpA, Norfin priced at a 7.5% discount to last close

- RS Group shares fall as much as 4.8%, with analysts saying sales growth for the UK industrial and electronic products distributor slowed more than anticipated

- SBB shares slide as much as 5.2% after Nordea lowers its price target on the Swedish real estate company to a Street-low, in note maintaining a sell rating

- Barry Callebaut declines as much as 2% after the Swiss chocolate maker announced the surprise exit of CEO Peter Boone and lowered its full year volume growth guidance

Asian stocks fell, led by a slump in the heavyweight Japanese market, as investors remain concerned about the impact of higher borrowing costs on the world economy. The MSCI Asia Pacific Index fell as much as 0.5% with Toyota Motor and Daiichi Sankyo among the biggest drags on the gauge. New Zealand’s equity benchmark erased gains to fall 0.3% while its currency jumped after the central bank unexpectedly raised interest rates by 50 basis points. Markets in China, Hong Kong and Taiwan were shut for a holiday. Japan’s Topix slid 1.9% with the yen’s recent strength also weighing on local shares. The currency has climbed about 5% from its March low against the dollar and a renewed focus on the narrowing gap between US and Japanese yields has opened up the door for further gains, some traders say.

“The US economy itself may be a principal factor for the decline” in Japanese shares, said Ikuo Mitsui, fund manager at Aizawa Securities Group. “The domestic market began the day with a selloff due to concerns about the US and global economies.” The decline in Asian equities came after US peers ended a four-day winning streak amid a selloff in bank shares and softer data on job openings. Federal Reserve Bank of Cleveland President Loretta Mester said policymakers should move their benchmark rate above 5% this year and hold it at restrictive levels for some time to quell inflation. Stocks in India gained as trading resumed after a local holiday. The nation’s central bank will likely increase borrowing costs for a seventh straight time on Thursday.

Japanese equities fell, following US peers lower, as the yen strengthened and a dip in US job openings fanned investor concerns about the global economy. The Topix fell 1.9% to 1,983.84 at the close in Tokyo, while the Nikkei declined 1.7% to 27,813.26. Toyota Motor Corp. contributed the most to the Topix’s decline, decreasing 2.4%. Out of 2,160 stocks in the index, 83 rose and 2,048 fell, while 29 were unchanged. “The yen appreciating and the US economy worsening is the most unfavorable pattern for Japanese stocks,” said Kiyoshi Ishigane, chief fund manager at Mitsubishi UFJ Kokusai Asset Management. The recent surge in Japanese stocks may have been “too rapid, which made profit-taking more likely,” Ishigane said

India’s key stock indexes were the best performers in Asia Pacific, led by stronger financial services, fast-moving consumer goods, and information technology companies. The S&P BSE Sensex rose 1% to 59,689.31 in Mumbai, while the NSE Nifty 50 Index increased 0.9% to 17,557.05. In contrast, the MSCI Asia-Pacific Index ended 0.6% lower, while MSCI Emerging Markets Index climbed just 0.2%. The Nifty rose for a fourth session, it’s longest streak since early December. Sub-gauges of consumer staples, IT and financial services companies closed more than 1% higher. HDFC Bank, up 2.7%, contributed the most to the Sensex’s rally as the lender’s deposit growth in the three-month period ended March surpassed Citigroup’s estimate. HDFC, Larsen & Toubro and ITC were other major contributors to the benchmark index’s gains. Out of 30 shares in the Sensex index, 22 rose and 8 fell.

In rates, treasury futures were lower, following wider losses in core European rates during London morning, erasing a portion of Tuesday’s gains; shorter-dated maturities have taken the brunt of selling in the bond markets with US two-year yields rising 5bps to 3.88% after declining 14 basis points on Tuesday following softer jobs-opening data. Euro-area government bonds also fell, sending the yield on Germany’s two-year note higher by 7 basis points to 2.67%. Yields are cheaper by up to 5bp across front-end of the curve, flattening 2s10s, 5s30s spreads by 2bp and 3bp on the day; 10- year yields around 3.34%, unchanged on the day after erasing a move higher in yields, with bunds and gilts underperforming by 2bp and 4bp in the sector.

In FX, the Bloomberg Dollar Spot Index is up 0.1% while the Swiss franc is the slight outperformer among the G-10’s while the Australian dollar and Norwegian krone are the weakest. . Swap contracts downgraded the odds of a quarter-point rate hike at the Fed’s May meeting, easing to around 50% from a peak of 70% on Tuesday

- Kiwi climbed to the highest since mid-February but then surrendered its gain after the RBNZ increased the official cash rate to 5.25% from 4.75%, wrong-footing most economists who had expected a 25 basis point hike

- The euro was little changed against the dollar at 1.0950

- The pound slipped after its first close above $1.25 since June on Monday. Domestic focus is on the announcement of a new member to the Bank of England’s Monetary Policy Committee, which the UK Treasury is preparing to name as soon as this week

In commodities, crude futures declined with WTI falling 0.4% to trade near $80.40. Spot gold rises 0.2% to around $2,025.

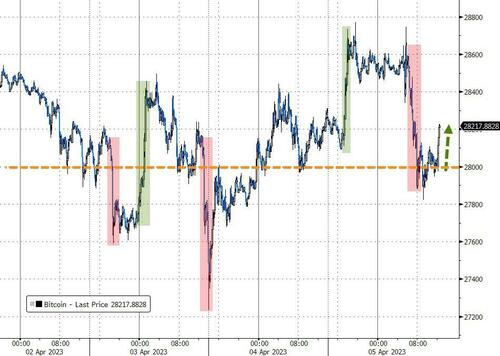

Bitcoin is modestly firmer within narrow and familiar parameters that have been in play for several weeks; currently, holding at the mid-point of USD 28.08-28.76k boundaries.

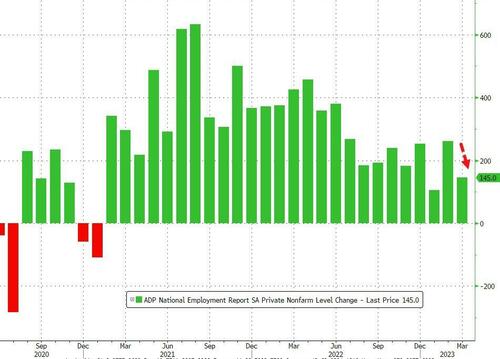

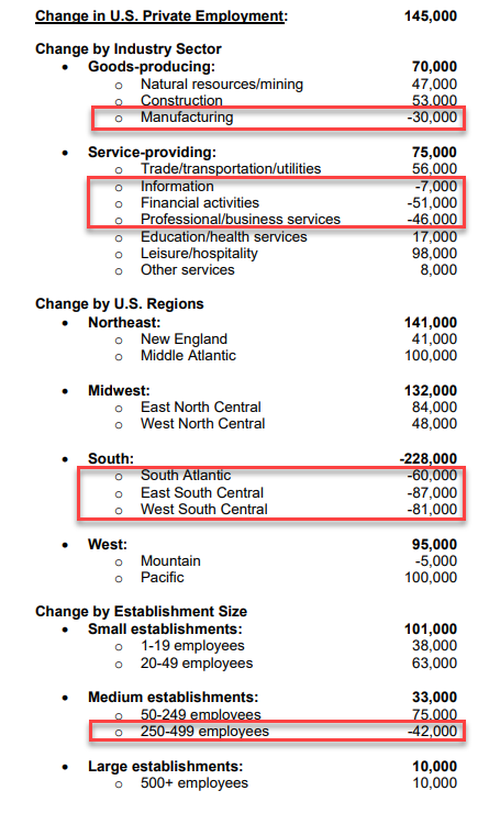

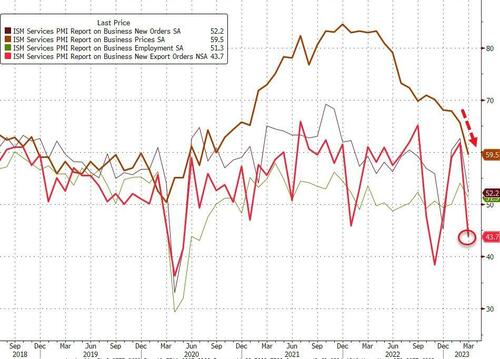

Looking at today’s calendar, the US economic data slate includes March ADP employment change (8:15am), February trade balance (8:30am), March S&P Global services PMI (9:45am) and ISM services index (10am)

Market Snapshot

- S&P 500 futures down 0.2% to 4,121.00

- STOXX Europe 600 down 0.2% to 456.44

- MXAP down 0.4% to 162.21

- MXAPJ little changed at 523.55

- Nikkei down 1.7% to 27,813.26

- Topix down 1.9% to 1,983.84

- Hang Seng Index down 0.7% to 20,274.59

- Shanghai Composite up 0.5% to 3,312.56

- Sensex up 0.8% to 59,597.67

- Australia S&P/ASX 200 little changed at 7,237.21

- Kospi up 0.6% to 2,495.21

- German 10Y yield little changed at 2.28%

- Euro little changed at $1.0953

- Brent Futures up 0.5% to $85.37/bbl

- Gold spot up 0.3% to $2,026.78

- U.S. Dollar Index little changed at 101.59

Top Overnight News

- New Zealand surprises markets with large hike of 50bp to 5.25% (economists were anticipating only a 25bp increase) while other central banks slow/stop their tightening cycles. WSJ

- The Australian central bank’s decision to keep interest rates unchanged this week doesn’t mean an end to its tightening cycle, Governor Philip Lowe said, while acknowledging the board is prepared for a slower return of inflation to target than its global counterparts. BBG

- A recent drop in global bond yields has created favorable conditions for the Bank of Japan to scrap its yield curve control program this month, according to a former BOJ executive director in charge of monetary policy. BBG

- French president Emmanuel Macron has landed in Beijing in the latest bid by a European leader to urge China’s Xi Jinping to wield his influence with Vladimir Putin to push for a withdrawal of Russian troops from Ukraine. FT

- Credit Suisse’s integration will take three to four years, excluding winding down the investment bank, UBS Chairman Colm Kelleher said at the bank’s AGM. “Great uncertainty” will remain until the deal closes, and UBS will consider all options for CS’s local business, its vice chairman said. The Swiss banking regulator said it weighed a CS bankruptcy before choosing the UBS route. BBG

- Fed’s Mester says the Funds Rate will need to move a bit higher and remain at an elevated level for an extended period (she was the latest Fed official to push back against the market’s expectation for rate cuts). RTRS

- Contingent convertible bonds issued by banks have rebounded from the market-wide losses inflicted by the terms of Credit Suisse Group AG’s rescue, another sign that stress from the recent financial turmoil is subsiding. The Bloomberg Global CoCo Banking Statistics Index, a dollar-based gauge of such lender debt, rose on Tuesday to its highest since March 16. BBG

- Chicago elected progressive Brandon Johnson in the mayoral runoff over fellow Democrat Paul Vallas. He plans to raise taxes on major firms to boost city revenue. In Wisconsin, a Democratic-backed judge won the high-stakes Supreme Court race, flipping the swing state’s highest court for the first time in 15 years, the AP reported. BBG

- Exxon Mobil has ended a major campaign to find oil in Brazil, after coming up empty-handed on a multibillion-dollar wager that produced a series of disappointing wells, according to people familiar with the matter. WSJ

A More detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded mixed after the negative lead from Wall St where risk assets were pressured as weak JOLTS data stoked growth concerns, with trade also hampered by the closures in the Greater China region. ASX 200 was rangebound with early support from strength in healthcare, tech and gold-related stocks although gains were later pared amid weakness in the commodity-related sectors and confirmation of a contraction to PMIs. NZX 50 wiped out initial gains and was pressured after the RBNZ delivered a more aggressive than expected rate hike of 50bps and signalled a further rate increase to return inflation to its target. Nikkei 225 underperformed and fell below 28,000 amid broad weakness across sectors and as retailers including index heavyweight Fast Retailing failed to benefit from the recent monthly comparable store sales updates. Foxconn (2317 TT) March sales -21.1% Y/Y, Q1 +3.9% Y/Y; Q2 outlook expects to see aQ/Q and Y/Y decrease due to the seasonal off peak period and a high base from unseasonably strong pull-in in H1-2022.

Top Asian News

- Taiwan President Tsai is to meet with US House Speaker McCarthy today at 10:00PDT (18:00BST/13:00EDT)

- RBNZ raised the OCR by 50bps to 5.25% (exp. 25bps hike), while it stated that the OCR needs to increase and the Committee agreed it must continue to raise the OCR to return inflation to the 1%-3% target and to fulfil its remit. RBNZ Board discussed a 25bp and 50bps hike at this meeting and the Committee expects to see a continued slowing of domestic demand, as well as a moderation in core inflation and inflation expectations with the extent of this moderation to determine the direction of future monetary policy. MPC also agreed the OCR needs to be at a level that will reduce inflation and inflation expectations to within the target range over the medium-term and members observed inflation is still too high and persistent, while they viewed risks to inflation pressure from fiscal policy as skewed to the upside.

- RBA Governor Lowe said the decision to hold rates steady does not imply interest rate rises are over and noted that the board expects that some further tightening of monetary policy may well be needed. Lowe also commented that it was prudent to hold rates steady this month to allow more time to assess the impact of past increases and that this approach is consistent with their practice in earlier interest rate cycles. Furthermore, Lowe said the board is prepared to have a slightly slower return to the inflation target than some other central banks, while he said that he is not 100% certain they will have to hike rates again but added that the balance of risks lean toward further rate rises.

European bourses are mixed but with a modest negative skew overall, Euro Stoxx 50 -0.3%, in another session of sparse newsflow. Sectors are similarly mixed with defensive names faring incrementally better. Stateside, futures reside just below the neutral mark and by extension within Tuesday’s parameters ahead of ISM Services and Fed speak.

Top European News

- EU nations/lawmakers are reportedly likely to agree a deal on the CHIPS act on April 18th, via Reuters citing sources.

- ECB’s Vujcic says the biggest part of the rate-hiking cycle is behind the ECB; may need further hikes to address core inflation.

FX

- DXY trades on either side of 101.50 and briefly dipped under yesterday’s low, participants now eye ISM Services and US ADP.

- NZD/USD retraces gains following RBNZ’s 50bps rate hike surprise to 5.25%. AUD struggles due to RBA/RBNZ divergence and base metals pullback.

- EUR/USD maintains gains near 1.0950; Eurozone Final PMIs indicate recession likely avoided. GBP/USD trades around 1.2475 after PMI revisions.

- JPY benefits from cautious market sentiment. USD/JPY moves between 131.84 high and 131.31 low, with key support at 131.00 and 130.75.

Fixed Income

- Overall, a comparably contained morning for the fixed complex after a holiday-thinned APAC session ahead of US data and Central Bank speak.

- The modest pressure in core counterparts is perhaps a function of concession from both corporates and sovereign supply this morning alongside hawkish undertones from the RBNZ.

- Specifically, the Bund is at the session low of 135.85 vs the initial 136.56 peak, despite the circa 50-tick decline the benchmark remains an equal distance from Tuesday’s 135.59 trough and thereafter the WTD 135.15 low.

- Stateside, USTs are directionally in-fitting with the above but with magnitudes even more contained.

Commodities

- WTI May and Brent June futures have come off overnight high price action this morning is seemingly a function of risk after futures traded sideways in APAC hours.

- Spot gold edges higher, with price action relatively contained, but above the USD 2,000/oz mark following the move seen in wake of the US JOLTS data yesterday.

- Base metals are mostly lower amid the soured risk tone and slightly firmer Dollar

- Exxon (XOM) has reportedly ended drilling in Brazil after failing to find oil, but hasn’t ruled out other projects in the country, according to WSJ sources.

Geopolitical

- US President Biden and French President Macron held a call on Tuesday in which they discussed China and mentioned a willingness to engage China to accelerate the end of the Ukraine war, according to Reuters.

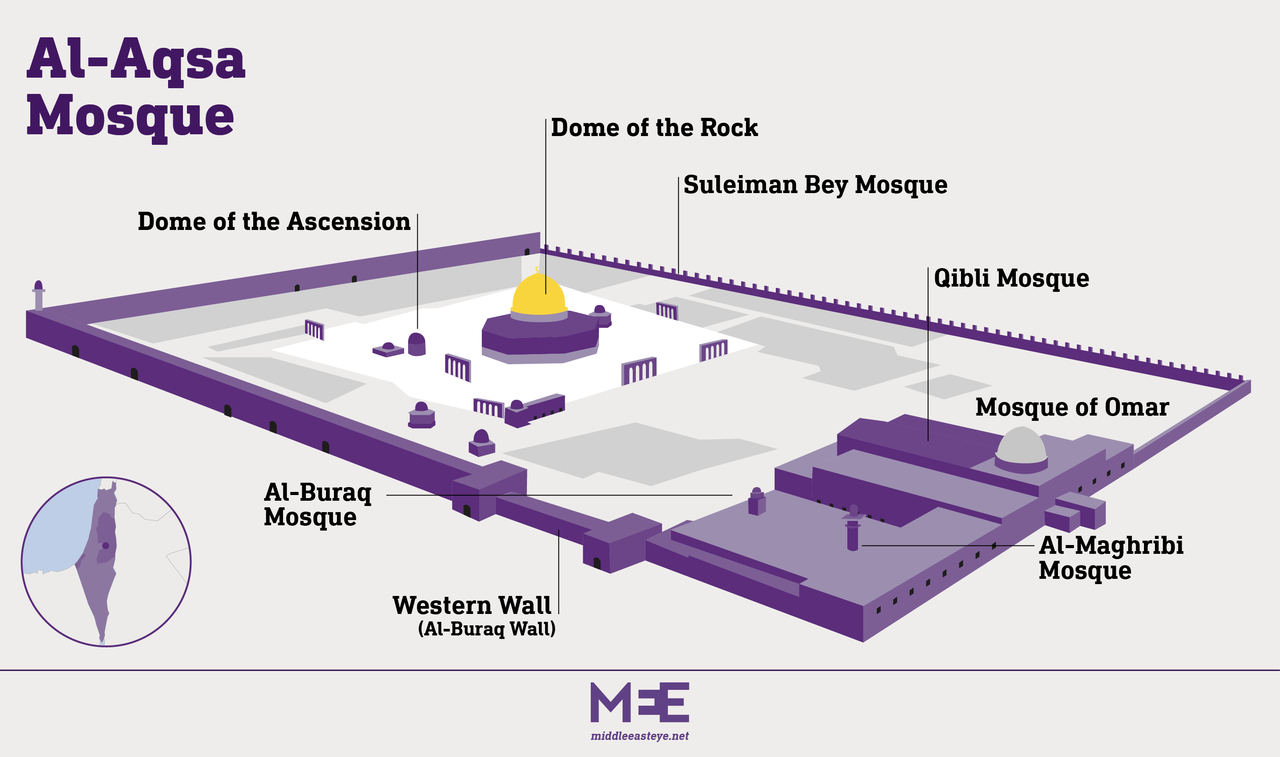

- Israeli police reported clashes inside the Al-Aqsa Mosque in Jerusalem and Hamas called on Palestinians to march to Jerusalem to defend the Al-Aqsa Mosque, according to AFP News Agency. Furthermore, Saudi and Jordanian Foreign Ministries condemned Israeli for storming the Al-Aqsa Mosque, while it was later reported that Israeli planes conducted a strike on Gaza following rockets from the enclave amid tensions in Al-Aqsa, according to Reuters.

- Iran foiled a drone attack against the ministry of defense complex in Isfahan, via Tasnim; subsequently, “The political and security deputy of the Iranian governor of Isfahan denies what was reported by the Iranian Tasnim Agency of an attempt to launch a drone attack on a compound of the Ministry of Defense in the province”, according to Sky News Arabia.

- US nuclear-capable fighter jets fly over the Korean Peninsula, in drills aimed at deterring N.Korea, Sky News Arabia reports.

- Belarus Air Defense will hold drills near Poland between April 5-7th.

US Event Calendar

- 07:00: March MBA Mortgage Applications, prior 2.9%

- 08:15: March ADP Employment Change, est. 210,000, prior 242,000

- 08:30: Feb. Trade Balance, est. -$68.8b, prior -$68.3b

- 09:45: March S&P Global US Services PMI, est. 53.8, prior 53.8

- 10:00: March ISM Services Index, est. 54.4, prior 55.1

- Prices Paid, prior 65.6

- Employment, prior 54.0

- New Orders, prior 62.6

DB’s Jim Reid concludes the overnight wrap

After a string of gains for risk assets over recent days, the last 24 hours have seen some steam come out of that rally, with investor nerves growing about the state of the economy once again. Equities lost ground, with US bank stocks leading the declines, and investors moved into sovereign bonds as doubts grew about whether the Fed would still go ahead with any more rate hikes. By the end of the session, that meant yields on 10yr US Treasuries had fallen -7.3bps to 3.339%, which is their lowest closing level since early-September, whilst the S&P 500 snapped a run of 4 consecutive gains to shed -0.58%.

Similar to the day before, the big turning point yesterday occurred following a US data release, with the retracement coming after the US job openings (JOLTS) report came out. That showed the number of job openings fell to 9.931m in February (vs. 10.5m expected), which marked the first time they’ve been beneath 10m since May 2021. The release added to the signs that the Fed’s tightening cycle was increasingly having an effect, and the historic levels of tightness in the labour market were finally beginning to ease. Furthermore, the ratio of job vacancies per unemployed individuals fell to 1.67, the lowest since November 2021, and that’s a measure that Fed Chair Powell himself has cited as something the Fed looks at.

On the back of that data release, investors immediately moved to downplay the chances that the Fed would keep hiking rates. According to futures, the chances of a hike at their next meeting in early May fell back to 47%, having been up to 63% at the close on Monday and as high as 70% in early morning trading yesterday. In the meantime, the rate priced in for their December meeting fell by -17.2bps to 4.130%, its lowest level in over a week. In turn, this sparked a big turnaround for Treasuries, with the 10yr yield having been up by +7.1bps ahead of the release, before turning around to end the day at -7.3bps at 3.339%. For 2yr Treasuries the decline was even more dramatic, with yields ending the day down -13.8bps at 3.825%.

Whilst the JOLTS report was the catalyst for a market shift, there were several details in the report that read in a less dovish light. First, it’s worth remembering that the number of openings and the ratio of vacancies per unemployed individual are still well above their peaks in previous cycles. So we’re talking about a labour market that remains very tight by historic standards. Secondly, the quits rate of those voluntarily leaving their jobs ticked back up a tenth in February to 2.6%, and that’s a measure that correlates well with wage growth and hence inflation. The private quits rate was similarly up a tenth to 2.9%.

Despite this, the sense among investors that inflation risks were beginning to ease was given further support from a couple of other sources. One was the ECB’s latest Consumer Expectations Survey for February. That showed inflation expectations at both the 12-month and the 3-year horizon falling to their lowest levels in a year, at 4.6% and 2.4% respectively. At the same time, oil prices stabilised after their big surge the previous day after the OPEC+ decision to cut output, with Brent crude seeing just a +0.01% increase to $84.94/bbl, although overnight it’s begun to tick up again, rising +0.49% to $85.36/bbl.

For equities, the main story was a further decline in bank stocks, with the KBW Banks Index down by -1.97%. All but one of the 22 banks in the index lost ground on the day, with the biggest underperformers including First Republic (-5.55%), KeyCorp (-5.17%), and Comerica (-5.14%). The bank losses were at the forefront of a broader equity decline, which left the S&P 500 down -0.58%. Defensives such as utilities (+0.52%) and telecoms (+0.85%) outperformed, while small-cap stocks were another big underperformer, leaving the Russell 2000 down by -1.81%.

European markets closed before the worst of the US losses, but they still saw an intraday turnaround after the JOLTS that meant the STOXX 600 gave up its intraday peak of +0.69% to close -0.08% lower. It was much the same story among sovereign bonds, with yields on 10yr bunds closing -0.7bps lower, but only after having been as high as +8.9bps higher earlier in the day.

Overnight in Asia, the tone has remained pretty negative, with the Nikkei (-1.62%) seeing a sharp fall, putting it on track for its worst daily performance in over three weeks. That’s in spite of some decent PMI numbers from Japan overnight, with the composite PMI rising to an 8-month high of 52.9 in March, whilst the services PMI rose to its highest since October 2013, at 55.0.