APRIL 10//GOLD FINISHED DOWN $21.40 TO $1989.25//SILVER CLOSED DOWN 17 CENTS TO $24.78//PLATINUM FINISHED DOWN $4.30 TO $997.50//PALLADIUM CLOSED DOWN $19.70 TO $1416.10//ANDREW MAGUIRE A MUST VIEW TAPE//COVID UPDATES//VACCINE IMPACT//SLAY NEWS//FRIDAY JOBS REPORT PLUS OTHER IMPORTANT DATA RELEASES//USA UPDATE ON HUGE TROUBLES IN THE REAL ESTATE SECTOR AND THE BANKS WHICH HOLD THEIR DEBT//SWAMP STORIES FOR YOU TONIGHT//

The final comex data tonight is totally compromised. It made no sense. So i am recording the preliminary data as the final set,

the volumes (final) was also compromised.

Also Europe was closed for Easter Monday and it was easy for the crooks to sell paper gold with no risk of paper gold becoming real gold. Watch for gold to go beyond 2,000 dollars on Tuesday.

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2688.42 DOWN 23.22 CDN dollars per oz (ALL TIME HIGH 2732.50)

BRITISH GOLD: 1607.86 DOWN 9.59 pounds per oz//(ALL TIME HIGH//1629.84)

EURO GOLD: 1833.20 DOWN 4.43 euros per oz //(ALL TIME HIGH//1860.82)

072 C GOLDMAN 7 104 C MIZUHO 3 118 C MACQUARIE FUT 136 132 C SG AMERICAS 3 363 H WELLS FARGO SEC 32 435 H SCOTIA CAPITAL 431 523 H INTERACTIVE BRO 1 624 C BOFA SECURITIES 2 624 H BOFA SECURITIES 82 657 C MORGAN STANLEY 41 661 C JP MORGAN 29 732 C RBC CAP MARKETS 8 800 C MAREX SPEC 13 15 880 C CITIGROUP 14 880 H CITIGROUP 69 905 C ADM 1 3

TOTAL: 445 445

MONTH TO DATE: 21,129

JPMORGAN stopped 28.445 contracts

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2023. CONTRACT: 445 NOTICES FOR 44,500 OZ or 1.384 TONNES

total notices so far: 21,128 contracts for 2,112,800 oz (66.011 tonnes)

SILVER NOTICES: 2 NOTICE(S) FILED FOR 10,000 OZ/

total number of notices filed so far this month : 289 for 1,445,000 oz

END

GLD

WITH GOLD DOWN $21.40

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/NO CHANGES IN GOLD INVENTORY AT THE GLD://////

INVENTORY RESTS AT 930.91 TONNES

Silver//SLV

WITH NO SILVER AROUND AND SILVER DOWN 17 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 468,585 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 1105 TO 135,279 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS GIGANTIC SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR SMALL $0.02 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. WITH LAST WEEK’S READING AT THE COMEX , WE HAVE NOW SET ANOTHER RECORD LOW AT 117,395 CONTRACTS , MARCH 29.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.02). BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A MONSTER GAIN ON OUR TWO EXCHANGES 1530CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 8.5 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD: A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS( 425CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.055 MILLION OZ(FIRST DAY NOTICE)+ THE 8.5 MILLION OZ OF EXCHANGE FOR RISK//THUS TOTAL NEW STANDING 10.050MILLION OZ/ //// V) HUGE SIZED COMEX OI GAIN/ GOOD SIZED EFP ISSUANCE/.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –57 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTRACTS for 5days, total 9584 contracts: OR 47,920 MILLION OZ . (1917 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR:47,920 MILLION OZ

.

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE BUT BELOW LAST MONTH

APRIL 47.920 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1105 CONTRACTS WITH OUR $0.02 GAIN IN SILVER PRICING AT THE COMEX//FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE CONTRACTS: 425 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL OF 1.055 MILLION OZ//FIRST DAY NOTICE// 15,000 OZ QUEUE JUMP (WHICH INCREASES THE AMOUNT OF SILVER STANDING) + 8.5 MILLION NEW EXCHANGE FOR RISK ISSUED EARLY IN APRIL (INCREASES THE AMOUNT OF SILVER STANDING) //NEW STANDING 10.050 MILLION OZ .. WE HAVE A GIGANTIC SIZED GAIN OF 1530 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 2 NOTICE(S) FILED TODAY FOR 10,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 980 CONTRACTS TO 477,088 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED + 946 CONTRACTS

WE HAD A SMALL SIZED DECREASE IN COMEX OI ( 980 CONTRACTS) WITH OUR $9,15 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR APR. AT 66.892 TONNES ON FIRST DAY NOTICE // PLUS A 33,900 OZ QUEUE JUMP:(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)YET ALL OF..THIS HAPPENED WITH OUR $9,15 LOSS IN PRICEWITH RESPECT TO THURSDAY’S TRADING.WE HAD A SMALL SIZED GAIN OF 398 OI CONTRACTS (1.238 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1378 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 476,142

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 398 CONTRACTS WITH 980 CONTRACTS DECREASED AT THE COMEX AND 1378 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 398 CONTRACTS OR 1.238 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1378 CONTRACTS) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (980 //TOTAL GAIN IN THE TWO EXCHANGES 398 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 66.892 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 33M900 OZ//NEW STANDING 68.267 TONNES // ///3) ZERO LONG LIQUIDATION//4) SMALL SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 22,091 CONTRACTS OR 2,209,100 OZ OR 68,712 TONNES IN 5TRADING DAY(S) AND THUS AVERAGING: 4418 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5TRADING DAY(S) IN TONNES 68.712 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 68,712 /3550 x 100% TONNES 1.91% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 68.712 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 1105 CONTRACTS OI TO 135,279 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 425 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 2180and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 425 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1105 CONTRACTS AND ADD TO THE 425OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE GAIN OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1530 CONTRACTS.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES //7.650 MILLION OZ

OCCURRED DESPITE OUR TINY $0.02 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

NORTH KOREA/SOUTH KOREA

i)MONDAY MORNING//SUNDAY NIGHT

SHANGHAI CLOSED DOWN 12.29 PTS OR .37% //Hang Sang CLOSED UP 56.61 POINTS OR .25% /The Nikkei closed UP 115.35 PTS OR 0.43% //Australia’s all ordinaries CLOSED DOWN .30 % /Chinese yuan (ONSHORE) closed DOWNTO 6.8790 /OFFSHORE CHINESE YUAN UP TO 6.8856 /Oil UP TO 80.89 dollars per barrel for WTI and BRENT AT 85.22 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 980 CONTRACTS DOWN TO 477,088 WITH OUR LOSS IN PRICE OF $9.15 ON THURSDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF APRIL… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1378 EFP CONTRACTS WERE ISSUED: : JUNE 1378 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1378 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL TOTAL OF 398 CONTRACTS IN THAT 1378 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED LOSS OF 980 COMEX CONTRACTS..AND THIS SMALL SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $9.15. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: APRIL (68.267) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 68.267 tonnes

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $9.15 //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR SMALL SIZED GAIN OF 398 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 1.238PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL. (66.892 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 33,900 OZ… ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $9.15

WE HAD + ADDED 820 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 398 CONTRACTS OR 39,800 OZ OR 1.238 TONNES.

Total monthly oz gold served (contracts) so far this month

21,128 notices 2,112,800 OZ 66,011 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i) Into Int. Delaware: 482.265 oz (15 kilobars)

total deposits: nil oz

customer withdrawals: 0

total withdrawals: nil oz

in tonnes:0.

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of APRIL we have an oi of 1265 contracts having GAINED 153 contracts. We had 186 contracts served upon yesterday so we GAINED 339 contracts or 33,900 oz were QUEUE JUMPED.

May gained 282 contracts up to 1835.

June lost 3047 contracts down to 405,201 contracts.

We had 445 contracts filed for today representing 44,500 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 445 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 28 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2023. contract month,

we take the total number of notices filed so far for the month (21,128 x 100 oz ), to which we add the difference between the open interest for the front month of (APRIL. 1265 CONTRACTS) minus the number of notices served upon today 445x 100 oz per contract equals 2,194,800 OZ OR 68.267 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month:No of notices filed so far (21,128 x 100 oz)+ 1265 OI for the front month minus the number of notices served upon today (445)x 100 oz} which equals 2,161,000 oz standing OR 68.267 TONNES in this active delivery month of APRIL..

TOTAL COMEX GOLD STANDING: 68.267 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

total pledged gold: 1,629,392,410 OZ 50.6809 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,768,616,766 OZ

TOTAL REGISTERED GOLD: 12,260,115,116 (381.34 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 9,508,501.750 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,630,723 OZ (REG GOLD- PLEDGED GOLD) 330.66 tonnes//

END

SILVER/COMEX

APRIL 10//2023// THE APRIL 2023 SILVER CONTRACTAPRIL 5//2023// THE APRIL 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

652,524.230 oz Delaware

Loomis

.

Deposits to the Dealer Inventory

nil

Deposits to the Customer Inventory

NIL oz

No of oz served today (contracts)

64 CONTRACT(S) (320,000 OZ)

No of oz to be served (notices)

41 contracts (205,000 oz)

Total monthly oz silver served (contracts)

289 Contracts (1,445,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i) Into Delaware 16,965.127 oz

Total deposits: 16,965.127 oz

JPMorgan has a total silver weight: 141.723 million oz/274.534 million =51.45% of comex .//dropping fast

Comex withdrawals: 2

i) Out of Loomis: 250,850.830 oz

iii) out of Delaware 1961.000 oz

Total withdrawals; 652,524.230 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 35.486 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 274,534 million oz

CALCULATION OF SILVER OZ STANDING FOR MAR

silver open interest data:

FRONT MONTH OF APRIL /2023 OI: 23 CONTRACTS HAVING LOST 61 CONTRACT(S. WE HAD 64 NOTICES FILED ON THURSDAY SO WE GAINED 3 CONTRACTS OR AN ADDITIONAL 15,000 OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF APRIL.

MAY SAW A LOSS OF 360 CONTRACTS DOWN TO 92,198

JUNE HAD A 5 CONTRACT LOSS TO 30

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 2 for 10,000 oz

Comex volumes// est. volume today 44,219 poor

Comex volume: confirmed yesterday: data corrupted

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 289 x 5,000 oz = 1,1445,000 oz

to which we add the difference between the open interest for the front month of APRIL(23) and the number of notices served upon today X 2 (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL/2023 contract month: 289 (notices served so far) x 5000 oz + OI for the front month of APRIL (23) – number of notices served upon today (2 )x 500 oz of silver standing for the APRIL. contract month equates 1.550 million oz +/ EXCHANGE FOR RISK NOW TOTALS 8.5 MILLION OZ //new total standing 10.050 million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

APRIL 10/WITH GOLD DOWN $21.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91 TONNES

APRIL 6//WITH GOLD DOWN $9.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91

APRIL 5//WITH GOLD UP 0 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04

APRIL 4/WITH GOLD UP $36.30 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

APRIL 3/WITH GOLD UP $14.20 TODAY;NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.02 TONNES

MARCH 31/WITH GOLD DOWN $10.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD////INVENTORY RESTS AT 928.02 TONNES

MARCH 30//WITH GOLD UP XX TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A DEPOSIT OF 2.24 TONNES FROM THE GLD/INVENTORY RESTS AT 929.47 TONNES

MARCH 29/WITH GOLD DOWN $4.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4,16 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 927,23

MARCH 28/WITH GOLD UP $19.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

MARCH 15/THE IDES OF MARCH: WITH GOLD UP $18.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 913.27 TONNES

MARCH 14/WITH GOLD DOWN $4.75 TODAY: HUGE CHANGES: A MONSTER DEPOSIT OF 11.85 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 913.27 TONNES

MARCH 13/WITH GOLD UP $48.85 TODAY: VERY STRANGE HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY REST AT 901.42 TONNES

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

FEB 28/WITH GOLD UP $12.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 917.61 TONNES

FEB 27/WITH GOLD UP $6.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.32 TONNES

FEB 24/WITH GOLD DOWN $9.10 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 917.32 TONNES

FEB 23/WITH GOLD DOWN $13.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 919.92 TONNES

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

GLD INVENTORY: 930.91 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 10/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 6/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 4.643 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 468.585 MILLION OZ//

APRIL 5/WITH SILVER DOWN 4 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.942 MILLION OZ

APRIL 4/WITH GOLD UP $1.11 TODAY CRIMINAL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.47 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 463,942 MILLION OZ

APRIL 1/WITH SILVER DOWN 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.412

MARCH 31/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE GLD/: A MASSIVE 4.779 MILLION OZ DEPOSITED INTO THE SLV///INVENTORY RESTS AT465.412 MILLION OZ

MARCH 30/WITH SILVER UP XX CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV.: A DEPOSIT OF 550,000 OZ INTO THE SLV/.INVENTORY RESTS AT 460.633 MILLION OZ

MARCH 29/WITH SILVER UP 11 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 460.082

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

MARCH 17/WITH SILVER UP 79 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE WITHDRAWAL OF 10.478 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 462.748 MILLION OZ//

MARCH 16/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 5.009 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 473.226 MILLION OZ//

MARCH 15/WITH SILVER DOWN 7 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 643,000 OZ INTO THE SLV//INVENTORY RESTS AT 478.235 MILLION OZ/

MARCH 14/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.287 MILLION OZ FROM THE SLV////INVENTORY REST AT 477.592 MILLION OZ//

MARCH 13/WITH SILVER UP $1.35 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ//

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWALOF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

FEB 28/WITH SILVER UP 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.241 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.188

FEB 27/WITH SILVER DOWN 15 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.471 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 482.429 MILLION OZ

FEB 24/WITH SILVER DOWN 46 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.172 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.900 MILLION OZ//

FEB 23/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.072 MILLION OZ//

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 468.585 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

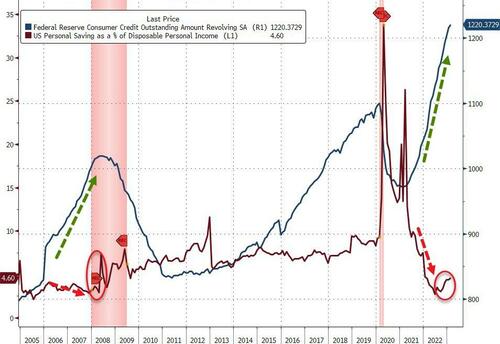

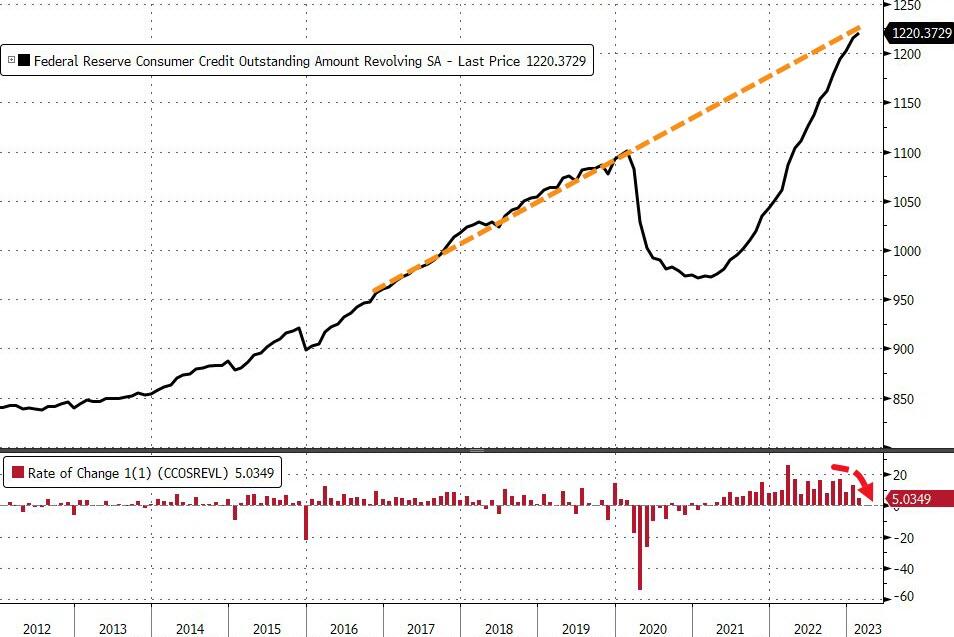

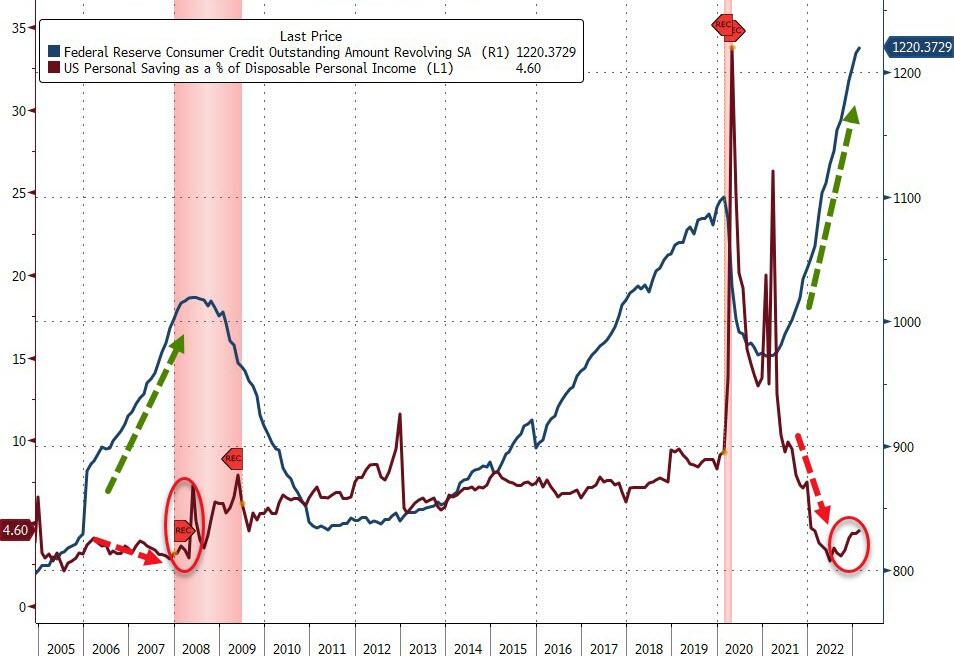

Recession Warning? Consumer Debt Climbs But Pace Slowing

American consumers continued to pile on debt in February, but the pace of borrowing slowed significantly, another sign the economy could be heading toward a recession.

Overall, consumer debt grew by $15.3 billion in February, a 3.8% annual increase, according to the latest data from the Federal Reserve. That compares with an upwardly revised 19.5 billion increase in January.

Americans now owe a record $4.82 trillion in consumer debt.

The Federal Reserve consumer debt figures include credit card debt, student loans, and auto loans, but do not factor in mortgage debt. When you include mortgages, US households are buried under more than $16.9 trillion in debt. Household debt charted the biggest increase in two decades in the fourth quarter of 2022.

Credit card debt grew at a much slower pace in February, in line with the drop in retail sales. Lower fuel and energy prices gave consumers some relief, even as price inflation remains elevated. As Forbes reported in February, retail sales that month told a “story of consumers leaning into value and curtailed spending.” The borrowing data confirms this.

Revolving debt, primarily reflecting credit card borrowing increased by $5 billion in February, a 3.8% increase. In absolute terms, it was the smallest increase in revolving credit since April 2021. But credit card borrowing still remains slightly higher than the prepandemic average even with higher interest rates as Americans continue to cope with rapidly increasing prices.

To put the numbers into perspective, the annual increase in 2019, prior to the pandemic, was 3.6%. It’s pretty clear that Americans are still heavily relying on credit cards to make ends meet.Bloomberg reported, “Still, many Americans are leaning on credit cards to keep up with rising prices. A Census Bureau survey in early March showed about a third of Americans said they used credit cards or loans to meet their spending needs.”

Americans now owe a record $1.22 trillion in revolving debt.

The bigger problem is the double whammy of rising debt and rising interest rates.

Average credit card interest rates eclipsed the record high of 17.87% months ago. The average annual percentage rate (APR) currently stands at 20.11%.

NBC News revealed just the impact of rising interest rates on indebted consumers.

Bankrate data shows it would take 16 years for someone to pay off the current average credit card balance of $5,474 by making the minimum payments at 19.2%. At that point, they would have shelled out $7,365 in interest alone.”

Given that the CPI is still closer to last year’s high than it is to the Fed’s 2% target, the central bank still needs to raise rates higher to slay price inflation. This is going to be difficult given the amount of debt piled up not only by consumers but also governments and corporations. As economist Daniel Lacalle put it, rising interest rates are on a collision course with a wall of debt.

People are already struggling to pay the bill. According to a Moody’s Analytics analysis of Equifax data, nearly 25 million people are behind on credit card, auto loan, or personal loan payments. We haven’t seen delinquency levels like this since 2009.

The growth of non-revolving credit has cratered in the last three months. This debt includes auto loans, student loans, and borrowing for other big-ticket items.

Revolving credit grew by just $10.3 billion in February, a 3.4% increase. This was up from the meager 1.7% increase in December and the 2.2% increase in January, but it remains below the average growth of 5% in recent years.

The plunge in non-revolving credit indicates that consumers have cut back spending on big-ticket items. That could signal that the economy is slowing under the weight of high interest rates.

And now we’re seeing a similar slowdown in credit card debt.

Does this indicate Americans are getting close to the end of their ropes?

The American economy depends on consumers spending money. They relied on plastic to make ends meet as price inflation blazed through the economy. Prices are still going up, but a lot of people have to be getting close to their borrowing limit.

So, what happens when consumers max out those credit cards? How will they make ends meet? How will it impact an economy that relies on borrowing and spending to limp along? And how will the Fed slay price inflation without popping the massive debt bubble?

Mainstream pundits and policy analysts don’t seem to be asking these questions. They probably should.

END

Peter Schiff: This Banking Crisis Is the Cusp Of A Much Worse Financial Crisis

Peter Schiff appeared on TraderTV to talk about the failure of Silicon Valley Bank and Signature Bank, the bailout, and what might lie ahead. Peter emphasized that this banking crisis isn’t over. In fact, it is just the beginning of a much worse financial crisis.

Peter started out the interview by pointing out that the failure of these two banks was the very obvious result of Fed policy combined with the moral hazards inherent in government-insured banking.

The reason that we’re going to have so many failures is because the Fed kept interest rates so low for so long. That’s what enabled Silicon Valley Bank, Signature Bank and just about every other bank to load up on overpriced US Treasuries and mortgages.”

Peter said Silicon Valley Bank was just the weak link in the chain. They were forced to sell some of those overpriced assets for a loss. That created a panic run and an exodus of deposits from the bank.

[The bank] was insolvent for a while. It just didn’t recognize that because it didn’t have to mark-to-market its bonds. But that’s true with all the other banks. Nobody is marking this stuff to market. Everybody is just putting it in their ‘hold to maturity’ bucket and they don’t have to take a haircut, they don’t have to mark it to market. So, the can pretend that 60 cents worth of bonds is worth a dollar. But if they had to stop pretending then they would all be insolvent.”

Peter explained that a bank deposit is your asset, but it is a liability to the bank. It owes you that money if you ask for it.

If they take the money that they owe you, and they blow it on overpriced mortgage-backed securities, then they can’t pay you back.”

Of course, in the US banking system, the government steps in and covers at least some of your loss. And in the case of Silicon Valley Bank and Signature Bank, they covered 100% of the loss. In effect, FDIC insurance now goes to infinity.

Well, the US government doesn’t have any money. Where does the US government get the money? From the Fed. The Fed just prints the money. That’s where the FDIC gets the money, which is why everybody is going to lose.”

The mainstream pundits, central bankers, and politicians all claim the banking system is sound. “You don’t need to worry about your money,” they say. Peter said you had better worry even more about your money.

The only way the government can make sure your bank doesn’t fail is by destroying the value of the money that you have on deposit. It’s inflation that is going to wipe out the value of everybody’s bank accounts.”

In another recent interview, Peter said this is a sequel to 2008 and like all sequels, it’s going to be worse than the original. In this interview, Peter noted that nobody wants to call this a financial crisis. They want to call it a banking crisis. Why?

They don’t want to evoke any memories of the ’08 criris. They don’t want to invite any comparison to that crisis. So, they’re trying to label it something different. No! This is a financial crisis. The 2008 financial crisis was also a banking crisis. Unless people forget, it was the banks that were failing. Yes, they were failing because of bad mortgages. But that was the debt that was failing. And so that’s what’s happening now. Banks are failing because of bad debt.”

Peter said this is just the cusp of the crisis.

It’s going to get much, much worse.”

Peter reminded us that in the days leading up to the 2008 financial crisis, everybody insisted the problems were “contained” to subprime mortgages and there was nothing to worry about.

That’s exactly what they’re saying now. ‘This is nothing. It’s no big deal.’ It is a big deal. It’s not nothing.”

Peter said this isn’t a black swan event.

This is your garden-variety white swan. They’re all over the place. This is what swans look like. If you keep interest rates at zero for 10 years, this is what you get. It’s not a surprise.”

3,Chris Powell of GATA provides to us very important physical commentaries

London metals trader Maguire reviews movement to escape dollar

Submitted by admin on Sat, 2023-04-08 17:00Section: Daily Dispatches

5p ET Saturday, April 8, 2023

Dear Friend of GATA and Gold:

Commenting on Kinesis Money’s “Live from the Vault” program this week, London metals trader Andrew Maguire reviews the maneuvers of more countries to escape the U.S. dollar and the U.S.-controlled international payment system. The program is 41 minutes long and can be seen at YouTube here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc.

The world is holding its breath for a simmering bank crisis in the United States triggered by the spectacular collapse of Silicon Valley Bank and Signature Bank.

Across the Atlantic, the repercussions are reverberating. As European banks edge closer to a similar crisis, concerns are growing that the regional crisis could become systemic.

The real culprit for the festering crisis is the US Federal Reserve’s monetary policy based on the US dollar’s hegemony, which has plundered global wealth on several occasions.

After World War II, the US deliberately established the dollar’s hegemony.

In the third quarter of 2022, the dollar comprised nearly 60 percent of global foreign exchange reserves. In January, the dollar accounted for about 40 percent of international payments.

Given that the dollar is so embedded in the system of international transactions, the US has turned it into a tool to bleed other countries by collecting seigniorage revenue.

With a $100 greenback costing about 17 cents to print, the US could reap $100 worth of goods and services from other nations.

Just as former French president Charles de Gaulle grumbled more than half a century ago, the US enjoyed “exorbitant privilege” and “deficit without tears” created by its dollar and used its worthless paper note to plunder the resources and factories of other nations.

From the gold dollar to the petrodollar, credit dollar and now the debt dollar, the world has been witnessing the basis of the dollar as an international currency weakening over the past decades.

To salvage the dollar’s hegemony, the US has recklessly exhausted all military, finance and trade means, attempting to continuously export risks to and reap benefits from other countries through the lucrative dollar business.

To boost its domestic economy, the US often pumps excess money into global markets during periods of economic expansion, creating the illusion of a worldwide boom.

After the international financial crisis in 2008, the Fed introduced multiple rounds of quantitative easing.

Following the outbreak of the COVID-19 pandemic in 2020, it implemented “unlimited” quantitative easing, pushing global inflation to a 40-year high, forming a colossal asset bubble and exacerbating risks to the world economy.

While the oversupply of US dollars has brought “inflationary pressures not seen in a generation” to the US, other economies were hit harder. In February, annual inflation in Argentina reached the 100-percent mark for the first time since 1991.

Most of the excess dollars are exported to other countries through imports and overseas investment, allowing the US to harvest the wealth of other countries at nearly zero cost.

The world is holding its breath for a simmering bank crisis in the United States triggered by the spectacular collapse of Silicon Valley Bank and Signature Bank.

… ‘Irrational prosperity’

The oversupply of the dollar also creates “irrational prosperity” that deviates from the actual economic situation and exacerbates turmoil in the global financial market.

More economists are waking up to the detriments of the current dollar-based monetary system.

David E. Sumual, chief economist of Bank Central Asia in Indonesia, said the current dollar-centered monetary system does not reflect the dynamic global market. He also said the sudden policy changes of the Fed always cause volatility in other countries.

But the Fed will continue to manipulate global markets and wreak havoc on the world economy, so long as other countries do not cut their reliance on the dollar.

Analysts have warned that the Fed had driven up asset bubbles worldwide to an extremely dangerous level, and the first signs of those bubbles bursting are beginning to appear.

After years of frothy markets, real trouble is on the horizon.

While the Western banking industry is teetering on the edge of catastrophe, the Fed shows no signs of stopping its rate hikes.

Aggressive interest rate hikes have led to a global liquidity tightening, resulting in capital outflows and currency depreciation in emerging markets.

According to data from the International Monetary Fund, the pressure on debt repayment for countries denominated in the dollar has increased sharply. More than 60 percent of low-income countries are already at high risk of or in debt distress.

If the past is any indication, once a country falls into debt distress, its assets would be exposed to US plundering.

As the Fed flip-flops on its monetary policy, the US also suffers temporary economic pain. Still, with its hegemonic currency, Uncle Sam can shuffle the risks to others and emerge largely unscathed from a crisis it started.

After the 2008 global financial crisis, it took the European Union 13 years to return GDP per capita to its pre-crisis level, while it took the US only two years to do so.

Despite a brief jolt, the United States continues to plunder the world.

However, the abuse of the dollar, weaponization of global financial infrastructure, and the country’s irresponsible monetary policy are backfiring and eroding US credibility.

END

Peter Hambro: He who has the gold makes the rules

Submitted by admin on Fri, 2023-04-07 13:13Section: Daily Dispatches

By Peter Hambro Reaction, London Thursday, April 6, 2023

Straws in the wind presage the oncoming storm, and not everyone notices in time. One such straw has just appeared in the gold market and only the most beady-eyed of your readers will have noticed that JPMorganChase did not, as is usual, roll over its maturing derivatives position in gold. Instead the bank delivered physical gold to those standing for delivery. Gold expert Ted Butler writes at SilverSeek.com: “A major development last week was the large amount of gold issued by JPMorgan over the first two days of the Comex April contract. Total gold deliveries by JPMorgan of 14,326 contracts, including 10,682 contracts (1.07 million ounces) by JPM from its proprietary house account were the largest by JPM in history. This is big news because it demonstrates clear and blatant price manipulation by JPMorgan. With more than 19,000 contracts of gold standing for delivery, what would have been the price of gold had JPM not delivered more than 10,000 contracts from its house account?”

Given that the short positions were established at prices much lower than today’s, there must be substantial actual and mark-to-market losses involved.

Wall Street on Parade notes that JPMorganChase Bank holds 53% of all the monetary metals derivatives contracts in the U.S. banking system.

Could it be that the margin calls on its massive position — or those of its customer, whomever that may be — are now so large that it could no longer continue to meet them? If so, we are witnessing a substantial increase in the price of gold, as a reaction to the people’s need for a real investment when there is an absence of sellers. …

China reports fifth month of increasing gold reserves

Submitted by admin on Fri, 2023-04-07 12:44Section: Daily Dispatches

From Bloomberg News Friday, April 7, 2023

The People’s Bank of China raised its holdings by about 18 tons in March, according to data on its website on Friday. Total stockpiles now sit at about 2,068 tons, after growing by about 102 tons in the four months before March.

Nations have been building up stockpiles of bullion amid heightened geopolitical risks and high inflation. Central-bank demand rose for a second year in 2022, and the biggest buyers in January of this year were Turkey, China and Kazakhstan, according to the World Gold Council.

This flurry of purchases by China’s central bank is the first since a ten-month run that ended in September 2019. Prior to that, the last wave of inflows ended in late-2016. …

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//,MONDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 6.8790

OFFSHORE YUAN: 6.8856

SHANGHAI CLOSED DOWN 12.79 POINTS OR .37%

HANG SANG CLOSED UP 56.61 PTS OR .25%

2. Nikkei closed UP 115.35 PTS OR 0.43 %

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 102.04 EURO FALLS TO 1.0876 DOWN 15 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.463Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 132.95 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morninG

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.174***/Italian 10 Yr bond yield RISES to 4.039*** /SPAIN 10 YR BOND YIELD RISES TO 3.219…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.050

3j Gold at $2001 silver at: 24.97 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 48 /100 roubles/dollar; ROUBLE AT 81.61//

3m oil into the 80 dollar handle for WTI and 85 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 132.95 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .463% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9084 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9873 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.370 DOWN 1 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.587 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.9452 DOWN 7 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.27…

GREAT BRITAIN/10 YEAR YIELD: DOWN 1 BASIS PTS AT 3.4325

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Drop, Dollar Rises With Most Global Markets Still Closed

MONDAY, APR 10, 2023 – 03:06 PM

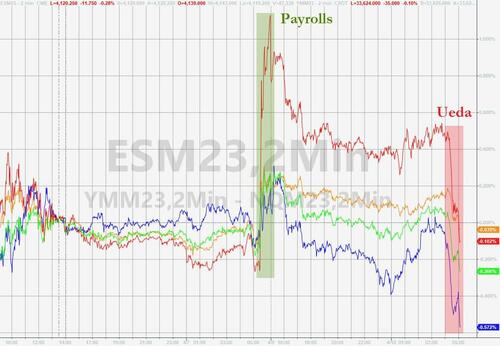

With much of Asia and Europe still closed for Easter Monday, US stock futures, already painfully illiquid, were trading in a narrow range for much of the session, before losing all of their post-payrolls gains as investors assessed the path of Federal Reserve monetary policy following Friday’s jobs report. Contracts on the S&P 500 dipped 0.2% at 7:30am while Nasdaq 100 futures dipped 0.4% as the dollar spiked to session highs on the back of yen weakness following the latest comments from the BOJ’s new head Ueda.

In premarket trading, Tesla edged lower after the electric car-maker again marked down all of its vehicles in the US as first-quarter price tweaks helped to yield an incremental sales gain.Pioneer Natural stock gained 7.2% in premarket trading after the Wall Street Journal reported that oil giant Exxon Mobil has held preliminary talks over a possible acquisition of the fracking company. Here are some other notable premarket movers:

Tupperware shares decline 7.9% after the company said on Friday that it has engaged financial advisers to help improve its capital structure and remediate doubts about ability to continue as a going concern.

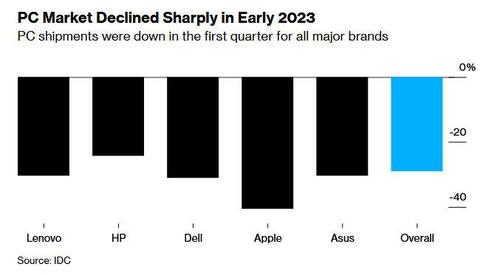

Shares of Apple and its PC maker peers may be active after data from IDC show a tough start to the year for the industry that’s still grappling with a glut of unsold inventory. Watch Apple, HP and Dell.

Micron Technology advanced 6.5% in US premarket trading after rival Samsung Electronics said Friday it would cut memory chip production.

Capital One Financial Corp. shares are lower by 4.1% in premarket trading after Walmart Inc. sued to end their credit-card partnership, in a move that analysts said wouldn’t be likely to meaningfully impact COF’s earnings per share.

Arrival surges as much as 80% premarket on Monday after announcing that it has entered into business combination agreement with Kensington Capital Acquisition to advance US commercialization plans.

AudioCodes tumbles 15% in premarket trading after the communications equipment company said revenue for 1Q is anticipated to be lower than previously estimated internally when the company provided guidance for the year in February.

Block slips 1.2% in premarket trading after Keefe, Bruyette & Woods analyst Steven Kwok cut the recommendation to market perform from outperform, citing a “growing number of risks” for the firm.

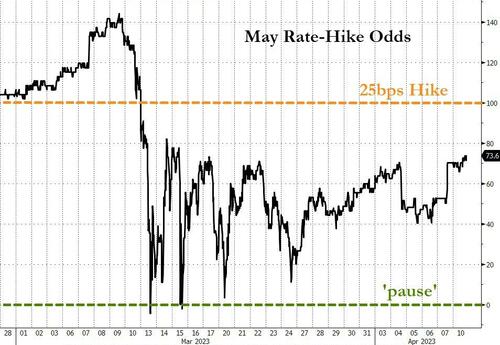

Last Friday, the BLS reported that US payrolls rose at a firm pace, just beating expectations, in March with the unemployment rate dropping again near record lows. Bond traders are betting that the Fed probably has one more interest-rate hike to go in this tightening cycle as the economy shows resilience, despite recent banking turmoil. Traders’ next focus will be on Wednesday’s consumer price index reading to assess whether the Fed is managing to tame inflation. Treasury Secretary Janet Yellen told AFP that she anticipates the US economy will growth and the labor market will remain strong as inflation comes down.

“The Fed will still see the need for further cooling in the labor market,” Win Thin, global head of currency strategy at Brown Brothers Harriman, wrote in a research note. “This week’s CPI and PPI data are likely to underscore the fact that inflation remains stubbornly high and so we look for the hawkish tilt in Fed comments to continue.”

Traders are also looking ahead to earnings season, which officially kicks off on Friday when JPMorgan Chase & Co. and Citigroup report results. “Stocks have benefited from expectations of an end of the hiking cycle and the advent of rapid rate cuts in the second half and into 2024, so they could be disappointed,” said Rajeev De Mello, a global macro portfolio manager at GAMA Asset Management SA. “However, investor positioning in stocks seem to be very cautious and while data has been weakening, it doesn’t signal a hard recession.”

With most European markets closed for Easter, attention instead turned to Asia where stocks edged higher in holiday-thinned trading as investors assessed the outlook for Federal Reserve policy in the wake of key US jobs data. The MSCI Asia Pacific Index rose 0.2%, driven by gains in materials and technology shares. South Korea’s Kospi was among the top-performing regional benchmarks, on the back of a rally in stocks tied to electric vehicles. China’s onshore equities edged lower, while Hong Kong and Australia were among markets shut for holidays.

Japanese stocks climbed, boosted by the marine transport sector and Nintendo shares. The Topix Index rose 0.6% to close at 1,976.53, while the Nikkei advanced 0.4% to 27,633.66. Nintendo Co. contributed the most to the Topix Index gain, increasing 4% after The Super Mario Bros. Movie marked the biggest opening weekend for a film so far this year. Of 2,158 stocks in the index, 1,578 rose and 473 fell, while 107 were unchanged.

Stocks in Asia have traded in a narrow range so far this month as uncertainty over global interest rates, China’s economic recovery and possible recessions in advanced economies keeps risk appetite in check. US payrolls rose at a firm pace last month, data showed Friday, paving the way for the Fed to increase interest rates at its next meeting in early May. “For the Asian equity market, the direction searching journey won’t get any easier ahead,” said Hebe Chen, a market analyst at IG. “Instead, the ‘glass half-full’ sentiment is poised to bake into more divided and fragile risk appetite.” Geopolitical issues are another reason for investor caution amid a technology trade standoff between Beijing and Washington. China held two days of military drills around Taiwan, with multiple exercises involving aircraft and ships on Sunday, after the island’s president, Tsai Ing-wen, returned from a visit to the US.

Most stocks in India advanced on Monday, led by an extension of rally in real estate companies, buoyed by the local central bank’s surprise pause on rate hikes last week. The S&P BSE Sensex rose as much as 0.5% before closing little changed at 59,846.51 in Mumbai, while the NSE Nifty 50 Index advanced 0.1%. Gauges of small- and mid-sized companies gained 0.2% and 0.4%, respectively. Broader markets in India have now gained for six consecutive sessions, helping trim their yearly losses. Investors will now be shifting focus to start of earnings season later this week. Tata Consultancy Services contributed the most to the Sensex’s gain, increasing 1.3%. Out of 30 shares in the Sensex index, 17 rose, while 13 fell

In rates, treasuries hold small gains as trading resumes in US, with most European markets closed, erasing a portion of Friday’s curve-flattening selloff sparked by robust March jobs data during a shortened session. Yields are lower led by 2-year, down ~4.5bp at 3.935%; it climbed 15bp Friday as swap contracts referencing Fed’s policy rate upgraded the odds of another quarter-point rate increase next month to about three in four.

In FX, the dollar gained after trading unchanged for much of the session; the yen came under mild selling pressure after Kazuo Ueda refrained from sending any hawkish signals in his first comments after taking over as governor of the Bank of Japan. In his inaugural speech, Ueda says he’ll do all he can to ensure stability in prices and the financial system and that the current monetary easing is very powerful; while the BOJ could review policy in the long term, it’s appropriate to continue with yield curve control framework for now. USD/JPY traded 0.5% higher at 132.85, versus 131.83-132.80 day range. The currency was initially lower versus the dollar on increased expectations for another Federal Reserve rate hike before erasing losses amid thin flows ahead of Ueda’s inaugural speech.

In commodities, oil was little changed while gold rebounded after dipping below $2,000 an ounce.

Monday’s event calendars are light, however this week includes March CPI report and minutes of the Fed’s March policy meeting on Wednesday, as well as auctions of 3- and 10-year notes and 30-year bonds over the next three days.

Market Wrap

S&P 500 futures down 0.2% at 4,124

MXAP up 0.2% to 161.71

MXAPJ up 0.2% to 523.49

Nikkei up 0.4% to 27,633.66

Topix up 0.6% to 1,976.53

Hang Seng Index up 0.3% to 20,331.20

Shanghai Composite down 0.4% to 3,315.36

Sensex up 0.1% to 59,904.57

Australia S&P/ASX 200 down 0.3% to 7,218.98

Kospi up 0.9% to 2,512.08

Brent Futures little changed at $85.14/bbl

Gold spot down 0.4% to $1,999.06

US Dollar Index little changed at 102.02

Top Overnight News

China’s financial sector is reeling from a series of new corruption probes and a surge in surprise audits of venture funds, as President Xi Jinping sharpens his focus on an industry he sees as failing to serve the broader economy. FT

State oil giant Saudi Aramco will supply full crude contract volumes loading in May to several North Asian buyers despite its pledge to cut output by 500,000 barrels per day. RTRS

A US Navy destroyer conducted “freedom of navigation” operations in the South China Sea near the Spratly Islands in a show of force as China holds military exercises around Taiwan. The drills are on par with the reaction last year after Nancy Pelosi visited the island, Taiwan said. BBG

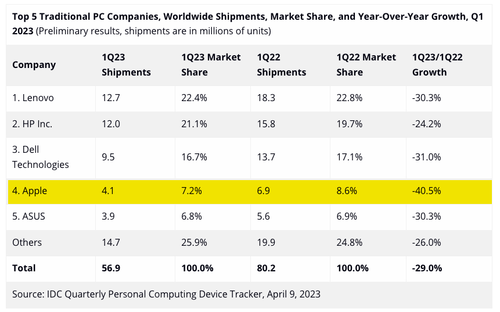

Apple PC shipments plunged 41% last quarter, an IDC tracker shows. Lenovo and Dell’s dropped more than 30% each. HP’s fell 24.2%. BBG

Russia begins evacuating people from territory it controls in southern Ukraine ahead of a major offensive from the Ukraine army expected to start in the coming weeks. NYT

Saudi Arabia’s production cut may not have as large an impact on markets as some think as countries outside OPEC+ ramp output. WSJ

Food costs for households are surging despite a drop in food raw material expense as packaged goods firms aggressively hike prices. WSJ

TSLA cut prices in the United States between 2% and nearly 6%, its website showed on Thursday, as the company extends a discount drive on its electric vehicles that analysts caution could hurt profitability. RTRS

First Republic Bank, beset by concerns over loan values and deposit flight, said in a regulatory filing that it will suspend payments of quarterly cash dividends on its preferred stock. WSJ

US bank lending contracted by the most on record in the last two weeks of March, indicating a tightening of credit conditions in the wake of several high-profile bank collapses that risks damaging the economy. Commercial bank lending dropped nearly $105 billion in the two weeks ended March 29, the most in Federal Reserve data back to 1973. The more than $45 billion decrease in the latest week was primarily due to a a drop in loans by small banks. BBG

10:00: Feb. Wholesale Inventories MoM, est. 0.2%, prior 0.2%

2 b) NOW NEWSQUAWK (EUROPE/REPORT)/ASIA REPORT

US Futures Tumble, Erase Payrolls Gains After BoJ’s Ueda Signals Nothing New

MONDAY, APR 10, 2023 – 03:23 PM

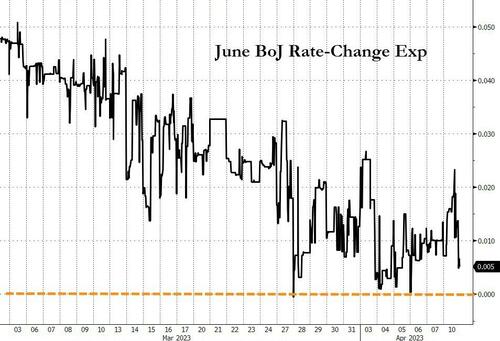

In his first public address, the new governor of Japan’s central bank disappointed policy hawks as he signaled that he plans no drastic changes in its ultra-low interest rate policy, sticking to earlier messaging on the topic.

“Markets have calmed and, as far as the impact on the Japanese system, we have maintained the easy monetary policy, and there is ample capital and fluidity,” Ueda said.

Ueda inauguration comes after his predecessor Kuroda presided over a decade-long monetary stimulus program centered around zero or minus long-term interest rates to nurture economic activity.

“As a result of appropriate policy from both the BOJ and the government we’re now in a situation where we’re not in a state of deflation,” Ueda told reporters in Tokyo Monday after meeting with Kishida at the prime minister’s office.

“We agreed the thinking behind the joint statement is appropriate, and there’s no need for an immediate review.”

Japan’s benchmark rate has been at minus 0.1% for years, and, as a reminder, Japanese inflation remains near 40-year cycle highs…

Ueda has repeatedly indicated he won’t take drastic action given Japan’s slow wage growth, shrinking and aging population and other challenges. He said it was vital to ensure the trend toward inflation will continue.

“There are difficult problems. But for right now, and we are speaking about Japan here, the situation is not such that there is a major raising of interest rates. For now, the financial system remains basically stable,” he said.

The 71-year old is scheduled to host his first policy meeting between April 27-28. Mainly due to increasing signs of deterioration in financial market functioning, most BoJ watchers expect some kind of policy tightening by June…

…but Ueda’s comments poured cold water on that to some extent…

“Right now, the yield curve control is considered most appropriate for the economy while tending to market functionality,” he said.

“Given the current economic, price and financial conditions, I think it’s appropriate to keep up the current yield curve control.”

The reaction was swift with Yen dropping to its weakest in a week…

And US equity futures tumbling (stronger USD), erasing all of the payrolls spike gains…

Ueda did offer a bone to an inflation-fighting stance as he concluded by saying he’s open to the idea of a policy review from a longer-term standpoint, although he’d like to discuss it with other board members before any decision.

But then again, Kuroda has been promising progress for years…

2 c. ASIAN AFFAIRS

ASIAN AND AUSTRALIAN CLOSINGS//EUROPE OPENING TRADING:

MONDAY MORNING/SUNDAY NIGHT

SHANGHAI CLOSED DOWN 12.29 PTS OR .37% //Hang Sang CLOSED UP 56.61 POINTS OR .25% /The Nikkei closed UP 115.35 PTS OR 0.43% //Australia’s all ordinaries CLOSED DOWN .30 % /Chinese yuan (ONSHORE) closed DOWNTO 6.8790 /OFFSHORE CHINESE YUAN UP TO 6.8856 /Oil UP TO 80.89 dollars per barrel for WTI and BRENT AT 85.22 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

2 d./NORTH KOREA/ SOUTH KOREA/

///NORTH KOREA/SOUTH KOREA/

END

2e) JAPAN

JAPAN/

END

3 CHINA /

CHINA/

China Sanctions Reagan Library After McCarthy’s Meeting With Taiwan President

Amid Chinese threats, McCarthy met with President Tsai Ing-wen on April 5 at the Reagan Library in Simi Valley, California.

McCarthy welcomed Tsai as a “great friend of America” during a high-level meeting on U.S. soil, risking China’s ire in a demonstration of U.S. support.

During her visit, Tsai accepted a leadership award from the Hudson Institute and spoke about Taiwan’s regional security challenges.

McCarthy joined an increasing number of foreign legislators who have met with Tsai to demonstrate their support for Taiwan in the face of Chinese intimidation.

“We will take resolute measures to punish the ‘Taiwan independence’ separatist forces and their actions, and resolutely safeguard our country’s sovereignty and territorial integrity,” the Chinese Cabinet’s Taiwan Affairs Office said in a statement on April 6, according to an English translation.

U.S.-Chinese relations have reached their lowest point in decades due to disagreements over the status of Taiwan, which separated from China in 1949 following a civil war, as well as security, technology, and Beijing’s treatment of Hong Kong and Muslim ethnic minorities.

The Chinese regime claims the democratic island as its own territory and has vowed to seize Taiwan, by force if necessary.

China’s Response

China’s Ministry of Foreign Affairs announced on April 7 that the Reagan Library and the Hudson Institute, a think tank in Washington, were sanctioned for “providing a platform and facilitation to Taiwan separatist activities.” It stated that Chinese institutions were prohibited from cooperating with or contacting them.

Amid escalating tensions between Taiwan’s self-governing democracy and China’s communist dictatorship, McCarthy urged Congress to expedite the delivery of military armaments to Taiwan.

During the Taiwanese official’s trip, McCarthy encouraged the United States and its allies to take a stand against China’s aggression with a clear and consistent unified message that promotes peace and protects democracy.

The House leader said it is crucial that congressional leaders speak with “one voice” so that China’s leaders understand “where we stand.”

“Don’t send a balloon over our air space. Don’t use authoritarian bully tactics,” McCarthy said. “It won’t go far.”

McCarthy was accompanied by a bipartisan delegation that uniformly emphasized Congress’ commitment to supporting Taiwan.

Alluding to Chinese threats, Rep. Mike Gallagher (R-Wis.), chair of the House China Select Committee, said the bipartisan delegation intended to “send a simple message—and that is, we are not afraid.”

“We support our friends in Taiwan,” he said. “We’re going to keep saying that whenever we have the opportunity, and we’re going to turn those words into action … because Taiwan is a small, very bright candle burning at the edge of a vast authoritarian darkness.”

Brad Jones and The Associated Press contributed to this report.

end

CHINA//EUROPE

FROM ROBERT H TO US:

Lepa on Twitter: “The German press notes that the President of the EC Ursula von der Leyen, had to leave China by the airport transit of the ordinary passages… a real diplomatic humiliation..https://t.co/8MSSPxmw1l” / Twitter A picture is worth far more than words. What does tell us about status ? Or that there was no one to see Macron off ? No victory to take to quell public unrest that grows daily in France. They’re not relevant on the board of where hegemony exists and their ordinary exit clearly demonstrates irrelevance. Even the Ship of Fools does not get why China no longer answers the phone. The world is clearly moving on with indifference to the West. Our world as we have known it is changing far beyond what daily reports tell us .

The German press notes that the President of the EC Ursula von der Leyen, had to leave China by the airport transit of the ordinary passages… a real diplomatic humiliation..🤷♀️ pic.twitter.com/8MSSPxmw1l

Escobar: Iran And Saudi Arabia – A Chinese Win-Win

SUNDAY, APR 09, 2023 – 05:30 AM

Authored by Pepe Escobar via The Cradle,

The single Iranian-Saudi handshake buried trillions of dollars of western divide-and-rule investments across West Asia, and has global leaders rushing to Beijing for global solutions.

The idea that History has an endpoint, as promoted by clueless neoconservatives in the unipolar 1990s, is flawed, as it is in an endless process of renewal. The recent official meeting between Saudi Foreign Minister Faisal bin Farhan al-Saud and Iranian Foreign Minister Hossein Amir-Abdollahian in Beijing marks a territory that was previously deemed unthinkable and which has undoubtedly caused grief for the War Inc. machine.

This single handshake signifies the burial of trillions of dollars that were spent on dividing and ruling West Asia for over four decades. Additionally, the Global War on Terror (GWOT), the fabricated reality of the new millennium, featured as prime collateral damage in Beijing.

Beijing’s optics as the capital of peace have been imprinted throughout the Global South, as evidenced by a subsequent sideshow where a couple of European leaders, a president, and a Eurocrat, arrived as supplicants to Xi Jinping, asking him to join the NATO line on the war in Ukraine. They were politely dismissed.

Still, the optics were sealed: Beijing had presented a 12-point peace plan for Ukraine that was branded “irrational” by the Washington beltway neocons. The Europeans – hostages of a proxy war imposed by Washington – at least understood that anyone remotely interested in peace needs to go through the ritual of bowing to the new boss in Beijing.

The irrelevance of the JCPOA

Tehran-Riyadh relations, of course, will have a long, rocky way ahead – from activating previous cooperation deals signed in 1998 and 2001 to respecting, in practice, their mutual sovereignty and non-interference in each other’s internal affairs.

Everything is far from solved – from the Saudi-led war on Yemen to the frontal clash of Persian Gulf Arab monarchies with Hezbollah and other resistance movements in the Levant. Yet that handshake is the first step leading, for instance, to the Saudi foreign minister’s upcoming trip to Damascus to formally invite President Bashar al-Assad to the Arab League summit in Riyadh next month.

It’s crucial to stress that this Chinese diplomatic coup started way back with Moscow brokering negotiations in Baghdad and Oman; that was a natural development of Russia stepping in to help Iran save Syria from a crossover NATO-Gulf Cooperation Council (GCC) coalition of vultures.

Then the baton was passed to Beijing, in total diplomatic sync. The drive to permanently bury GWOT and the myriad, nasty ramifications of the US war of terror was an essential part of the calculation; but even more pressing was the necessity to demonstrate how the Joint Comprehensive Plan of Action (JCPOA), or Iran nuclear deal, had become irrelevant.

Both Russia and China have experienced, inside and out, how the US always manages to torpedo a return to the JCPOA, as it was conceived and signed in 2015. Their task became to convince Riyadh and GCC states that Tehran has no interest in weaponizing nuclear power – and will remain a signatory of the Non-Proliferation Treaty (NPT).

Then it was up to Chinese diplomatic finesse to make it quite clear that the Persian Gulf monarchies’ fear of revolutionary Shi’ism is now as counter-productive as Tehran’s dread of being harassed and/or encircled by Salafi-jihadis. It’s as if Beijing had coined a motto: drop these hazy ideologies, and let’s do business.

And business it is, and will be: better yet, mediated by Beijing and implicitly guaranteed by both nuclear superpowers Russia and China.

Hop on the de-dollarization train

Saudi Crown Prince Mohammed bin Salman (MbS) may exhibit some Soprano-like traits, but he’s no fool: he instantly saw how this Chinese offer morphed beautifully into his domestic modernization plans. A Gulf source in Moscow, familiar with MbS’ rise and consolidation of power, details the crown prince’s drive to appeal to the younger Saudi generation who idolize him. Let girls drive their SUVs, go dancing, let their hair down, work hard, and be part of the “new” Saudi Arabia of Vision 2030: a global tourism and services hub, a sort of Dubai on steroids.

And, crucially, this will also be a Eurasia-integrated Saudi Arabia; future, inevitable member of both the Shanghai Cooperation Organization (SCO) and BRICS+ – just like Iran, which will also be sitting at the same communal tables.

From Beijing’s point of view, this is all about its ambitious, multi-trillion-dollar Belt and Road Initiative (BRI). A key BRI connectivity corridor runs from Central Asia to Iran and then beyond, to the Caucasus and/or Turkey. Another one – in search of investment opportunities – runs through the Arabian Sea, the Sea of Oman, and the Persian Gulf, part of the Maritime Silk Road.

Beijing wants to develop BRI projects in both corridors: call it “peaceful modernization” applied to sustainable development. The Chinese always remember how the Ancient Silk Roads plied Persia and parts of Arabia: in this case, we have History Repeating Itself.

A geopolitical revolution

And then comes the Holy Grail: energy. Iran is a prime gas supplier to China, a matter of national security, inextricably linked to their $400 billion-plus strategic partnership deal. And Saudi Arabia is a prime oil supplier. Closer Sino-Saudi relations and interaction in key multipolar organizations such as the SCO and BRICS+ advance the fateful day when the petroyuan will be definitely enshrined.