April 11/2023 · by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSED: UP $14.30, TO $2003.55

SILVER PRICE CLOSED: UP 27 CENTS AT $25.05

Access prices: closes : 4: 15 PM

Gold ACCESS CLOSE $1998.95

Silver ACCESS CLOSE: 25.03

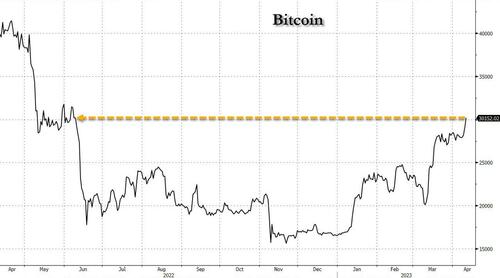

Bitcoin morning price:, $30,122 UP 1012 Dollars

Bitcoin: afternoon price: $30,349 UP 1239 dollars

Platinum price closing $998.85 UP $1.35

Palladium price; closing $1455.865 UP $19.85

END

The final comex data tonight is totally compromised. It made no sense. So i am recording the preliminary data as the final set,

the volumes (final) was also compromised

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2698.95 UP 8.49 CDN dollars per oz (ALL TIME HIGH 2732.50)

BRITISH GOLD: 1612,94 UP 5.10 pounds per oz//(ALL TIME HIGH//1629.84)

EURO GOLD: 1836,06UP 2.91 euros per oz //(ALL TIME HIGH//1860.82)

COMEX DATA EXCHANGE:

COMEX//NOTICES

EXCHANGE: COMEX

CONTRACT: APRIL 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,989.100000000 USD

INTENT DATE: 04/10/2023 DELIVERY DATE: 04/12/2023

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 2

104 C MIZUHO 1

118 C MACQUARIE FUT 55

132 C SG AMERICAS 1

363 H WELLS FARGO SEC 136

435 H SCOTIA CAPITAL 320

523 H INTERACTIVE BRO 1

624 C BOFA SECURITIES 1

624 H BOFA SECURITIES 42

657 C MORGAN STANLEY 27

661 C JP MORGAN 30 15

732 C RBC CAP MARKETS 8

737 C ADVANTAGE 1

800 C MAREX SPEC 15 13

880 C CITIGROUP 7

880 H CITIGROUP 35

905 C ADM 20

TOTAL: 365 365

MONTH TO DATE: 21,494

JPMORGAN STOPPED 15/365

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2023. CONTRACT: 365 NOTICES FOR 36,500 OZ or 1.135 TONNES

total notices so far: 21,494 contracts for 2,149,400 oz (66.855 tonnes)

SILVER NOTICES: 8 NOTICE(S) FILED FOR 40,000 OZ/

total number of notices filed so far this month : 297 for 1,485,000 oz

END

GLD

WITH GOLD UP $14.30

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/NO CHANGES IN GOLD INVENTORY AT THE GLD://////

INVENTORY RESTS AT 930.91 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 27 CENTS

AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 468,585 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 3239 TO 138,5476 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS GIGANTIC SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR STRONG $0.17 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. WITH LAST WEEK’S READING AT THE COMEX , WE HAVE NOW SET ANOTHER RECORD LOW AT 117,395 CONTRACTS , MARCH 29.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.17). BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A MONSTER GAIN ON OUR TWO EXCHANGES 3482 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 8.5 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS( 243 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.055 MILLION OZ(FIRST DAY NOTICE)+ THE 8.5 MILLION OZ OF EXCHANGE FOR RISK//THUS TOTAL NEW STANDING 10.058 MILLION OZ/ //// V) HUGE SIZED COMEX OI GAIN/ GOOD SIZED EFP ISSUANCE/.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –42 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAR:

TOTAL CONTRACTS for 6 days, total 9827 contracts: OR 49.135 MILLION OZ . (1637 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR:49.135 MILLION OZ

.

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE BUT BELOW LAST MONTH

APRIL 49.135 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3197 CONTRACTS DESPITE OUR $0.17 LOSS IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE CONTRACTS: 243 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL OF 1.055 MILLION OZ//FIRST DAY NOTICE// 30,000 OZ QUEUE JUMP (WHICH INCREASES THE AMOUNT OF SILVER STANDING) + 8.5 MILLION NEW EXCHANGE FOR RISK ISSUED EARLY IN APRIL (INCREASES THE AMOUNT OF SILVER STANDING) //NEW STANDING 10.058 MILLION OZ .. WE HAVE A GIGANTIC SIZED GAIN OF 3482 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 8 NOTICE(S) FILED TODAY FOR 40,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2727 CONTRACTS TO 474,361 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 138 CONTRACTS

WE HAD A FAIR SIZED DECREASE IN COMEX OI ( 2727 CONTRACTS) WITH OUR $21.40 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR APR. AT 66.892 TONNES ON FIRST DAY NOTICE // PLUS A 34,600 OZ QUEUE JUMP:(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)YET ALL OF..THIS HAPPENED WITH OUR $21.40 LOSS IN PRICE WITH RESPECT TO THURSDAY’S TRADING.WE HAD A FAIR SIZED LOSS OF 1430 OI CONTRACTS (4.447PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1297 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 474,361

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1430 CONTRACTS WITH 2727 CONTRACTS DECREASED AT THE COMEX AND 1297 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 1292 CONTRACTS OR 4.447 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1297 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (2727 //TOTAL LOSS IN THE TWO EXCHANGES 1292 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 66.892 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 34,600 OZ//NEW STANDING 69.315 TONNES // ///3) ZERO LONG LIQUIDATION//4) FAIR SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 23,388 CONTRACTS OR 2,338,800 OZ OR 72,746 TONNES IN 6 TRADING DAY(S) AND THUS AVERAGING: 3898 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 6 TRADING DAY(S) IN TONNES 72.746 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 72.746/3550 x 100% TONNES 2.02% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 72.746 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 3197 CONTRACTS OI TO 138,476 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 243 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 243 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 243 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 3197 CONTRACTS AND ADD TO THE 243 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE GAIN OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 3440 CONTRACTS.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES //17.200 MILLION OZ

OCCURRED DESPITE OUR $0.17 LOSS IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

NORTH KOREA/SOUTH KOREA

i)TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED DOWN 1.79 PTS OR .05% //Hang Sang CLOSED UP 130.16 POINTS OR .64% /The Nikkei closed UP 289.71 PTS OR 1.05% //Australia’s all ordinaries CLOSED UP 1.24 % /Chinese yuan (ONSHORE) closed DOWN TO 6.8842/OFFSHORE CHINESE YUAN DOWN TO 6.88579 /Oil DOWN TO 80.36 dollars per barrel for WTI and BRENT AT 84.68 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 2727 CONTRACTS DOWN TO 474,499 WITH OUR LOSS IN PRICE OF $21.40 ON MONDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF APRIL… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1297 EFP CONTRACTS WERE ISSUED: : JUNE 1297 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1297 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1430 CONTRACTS IN THAT 1297 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED LOSS OF 2589 COMEX CONTRACTS..AND THIS FAIR SIZED LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $21.60. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: APRIL (69.315) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 69.315 tonnes

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $21.40 //// AND WERE SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD OUR FAIR SIZED LOSS OF 1292 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE LOST A TOTAL OI OF 4.447 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL. (66.892 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 34,600 OZ… ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $21.60

WE HAD – 138 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 1430 CONTRACTS OR 143000 OZ OR 4.447 TONNES.

Estimated gold comex today 117,600 poor

final gold volumes/yesterday 144,785 poor

//APRIL 11/ APRIL 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 128.600 oz 5 kilobars BRINKS . |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | 32,151.000 OZ MANFRA 1000 KILOBARS |

| No of oz served (contracts) today | 365 notice(s) 36,500OZ 1.135 TONNES |

| No of oz to be served (notices) | 801 contracts 80100 oz 2.4914 TONNES |

| Total monthly oz gold served (contracts) so far this month | 21,484 notices 2,148,400 OZ 66,855 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i) Into Manfra: 32,151.000 oz (1000 kilobars)

total deposits: 32,150.00 oz

customer withdrawals: 1

i) Out of Brinks: 128.600 oz (5 kilobars)

total withdrawals: 128,600 oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of APRIL we have an oi of 1165 contracts having LOST 99 contracts. We had 445 contracts served upon yesterday so we GAINED 346 contracts or 34,600 oz were QUEUE JUMPED.

May gained 144 contracts up to 1979.

June lost 3843 contracts down to 402,291 contracts.

We had 365 contracts filed for today representing 36,500 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 30 notices were issued from their client or customer account. The total of all issuance by all participants equate to 365 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 15 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2023. contract month,

we take the total number of notices filed so far for the month (21,149 x 100 oz ), to which we add the difference between the open interest for the front month of (APRIL. 1166 CONTRACTS) minus the number of notices served upon today 365 x 100 oz per contract equals 2,228,500 OZ OR 69.315TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month:No of notices filed so far (21,494 x 100 oz)+ 1166OI for the front month minus the number of notices served upon today (445)x 100 oz} which equals 2,228,500 oz standing OR 69.315 TONNES in this active delivery month of APRIL..

TOTAL COMEX GOLD STANDING: 69.315 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,629,392,410 OZ 50.6809 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,800,639.266 OZ

TOTAL REGISTERED GOLD: 12,260,115,116 (381.34 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 9,540,524,150 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,630,723 OZ (REG GOLD- PLEDGED GOLD) 330.66 tonnes//

END

SILVER/COMEX

APRIL 11//2023// THE APRIL 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 496,642.130 oz CNT . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | NIL oz |

| No of oz served today (contracts) | 8 CONTRACT(S) (40,000 OZ) |

| No of oz to be served (notices) | 19 contracts (95,000 oz) |

| Total monthly oz silver served (contracts) | 297 Contracts (1,485,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 0 deposits into the customer account

Total deposits: nil oz

JPMorgan has a total silver weight: 141.723 million oz/274.037 million =51.45% of comex .//dropping fast

Comex withdrawals: 2

i) Out of CNT: 496,642.130 oz

Total withdrawals; 496,642.130 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 35.486 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 274,037 million oz

CALCULATION OF SILVER OZ STANDING FOR MAR

silver open interest data:

FRONT MONTH OF APRIL /2023 OI: 27 CONTRACTS HAVING GAINED 4 CONTRACT(S. WE HAD 2 NOTICES FILED ON MONDAY SO WE GAINED 6 CONTRACTS OR AN ADDITIONAL 30,000 OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF APRIL.

MAY SAW A LOSS OF 360 CONTRACTS DOWN TO 92,198

JUNE HAD A 5 CONTRACT LOSS TO 30

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 2 for 10,000 oz

Comex volumes// est. volume today 117,600 poor

Comex volume: confirmed yesterday: 144,785 poor

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 297 x 5,000 oz = 1,485,000 oz

to which we add the difference between the open interest for the front month of APRIL(27) and the number of notices served upon today 8 (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL/2023 contract month: 297 (notices served so far) x 5000 oz + OI for the front month of APRIL (27) – number of notices served upon today (8 )x 500 oz of silver standing for the APRIL. contract month equates 1.580 million oz +/ EXCHANGE FOR RISK NOW TOTALS 8.58 MILLION OZ //new total standing 10.058 million oz

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

APRIL 10/WITH GOLD DOWN $21.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91 TONNES

APRIL 6//WITH GOLD DOWN $9.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91

APRIL 5//WITH GOLD UP 0 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04

APRIL 4/WITH GOLD UP $36.30 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

APRIL 3/WITH GOLD UP $14.20 TODAY;NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.02 TONNES

MARCH 31/WITH GOLD DOWN $10.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD////INVENTORY RESTS AT 928.02 TONNES

MARCH 30//WITH GOLD UP XX TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A DEPOSIT OF 2.24 TONNES FROM THE GLD/INVENTORY RESTS AT 929.47 TONNES

MARCH 29/WITH GOLD DOWN $4.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4,16 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 927,23

MARCH 28/WITH GOLD UP $19.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

MARCH 15/THE IDES OF MARCH: WITH GOLD UP $18.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 913.27 TONNES

MARCH 14/WITH GOLD DOWN $4.75 TODAY: HUGE CHANGES: A MONSTER DEPOSIT OF 11.85 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 913.27 TONNES

MARCH 13/WITH GOLD UP $48.85 TODAY: VERY STRANGE HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY REST AT 901.42 TONNES

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

FEB 28/WITH GOLD UP $12.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 917.61 TONNES

FEB 27/WITH GOLD UP $6.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.32 TONNES

FEB 24/WITH GOLD DOWN $9.10 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 917.32 TONNES

FEB 23/WITH GOLD DOWN $13.05 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 919.92 TONNES

FEB 22/WITH GOLD DOWN 22 CENTS TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 919.92 TONNES

FEB 21/WITH GOLD DOWN $7.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 919.92 TONNES

FEB 17/WITH GOLD DOWN $1.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 921.08 TONNES

FEB 16/WITH GOLD UP $6.80 TODAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSITOF .29 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 921.08 TONNES

FEB 15/WITH GOLD DOWN $19.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 14/WITH GOLD UP $1.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 920.79 TONNES

FEB 13/WITH GOLD DOWN $9.90 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD///INVENTORY RESTS AT 920.79 TONNES

FEB 10/WITH GOLD DOWN $4.05 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF .0.38 TONNES/INVENTORY RESTS AT 920.79 TONNES

FEB 9/WITH GOLD DOWN $10.90 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .38 TONNES OF GOLD INTO THE GLD./INVENTORY RESTS AT 921.10 TONNES

GLD INVENTORY: 930.91 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 10/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 6/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 4.643 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 468.585 MILLION OZ//

APRIL 5/WITH SILVER DOWN 4 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.942 MILLION OZ

APRIL 4/WITH GOLD UP $1.11 TODAY CRIMINAL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.47 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 463,942 MILLION OZ

APRIL 1/WITH SILVER DOWN 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.412

MARCH 31/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE GLD/: A MASSIVE 4.779 MILLION OZ DEPOSITED INTO THE SLV///INVENTORY RESTS AT465.412 MILLION OZ

MARCH 30/WITH SILVER UP XX CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV.: A DEPOSIT OF 550,000 OZ INTO THE SLV/.INVENTORY RESTS AT 460.633 MILLION OZ

MARCH 29/WITH SILVER UP 11 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 460.082

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

MARCH 17/WITH SILVER UP 79 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE WITHDRAWAL OF 10.478 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 462.748 MILLION OZ//

MARCH 16/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 5.009 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 473.226 MILLION OZ//

MARCH 15/WITH SILVER DOWN 7 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 643,000 OZ INTO THE SLV//INVENTORY RESTS AT 478.235 MILLION OZ/

MARCH 14/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.287 MILLION OZ FROM THE SLV////INVENTORY REST AT 477.592 MILLION OZ//

MARCH 13/WITH SILVER UP $1.35 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ//

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWALOF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

FEB 28/WITH SILVER UP 26 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.241 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 481.188

FEB 27/WITH SILVER DOWN 15 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.471 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 482.429 MILLION OZ

FEB 24/WITH SILVER DOWN 46 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.172 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 483.900 MILLION OZ//

FEB 23/WITH SILVER DOWN 32 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.379 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 487.072 MILLION OZ//

FEB 22/WITH SILVER DOWN 22 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 689,000 OZ FROM THE SLV////INVENTORY RESTS AT 485.693 MILLION OZ

FEB 21/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.5363 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 486.382 MILLION OZ//

FEB 17/WITH SILVER UP 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 827,000 OZ INTO THE SLV////INVENTORY RESTS AT 484.819 MILLION OZ/

FEB 16/WITH SILVER UP 8 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 690,000 OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 483.992 MILLION OZ//

FEB 15/WITH SILVER DOWN $0.26 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 14/WITH SILVER DOWN 1 CENT TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV” A WITHDRAWAL OF 460,000 OZ FROM THE SLV////INVENTORY RESTS AT 483.302 MILLION OZ//

FEB 13 WITH SILVER DOWN 17 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY RESTS AT 483.762 MILLION OZ//

FEB 10/WITH SILVER DOWN 8 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY RESTS AT 483.762 MILLION OZ

FEB 9/WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: INVENTORY RESTS AT 483.76 MILLION OZ (CORRECTED).//

CLOSING INVENTORY 468.585 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//

3,Chris Powell of GATA provides to us very important physical commentaries

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

.

END

5.IMPORTANT COMMENTARIES ON COMMODITIES:

END

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//,MONDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 6.8842

OFFSHORE YUAN: 6.8879

SHANGHAI CLOSED DOWN 1.79 POINTS OR .05%

HANG SANG CLOSED UP 130.16 PTS OR .64%

2. Nikkei closed UP 289.71 PTS OR 1.05%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 101.84 EURO RISES TO 1.0903 UP 35 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.448Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 133.07 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morninG

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.2345***/Italian 10 Yr bond yield RISES to 4.092*** /SPAIN 10 YR BOND YIELD RISES TO 3.281…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.102.

3j Gold at $2001.25 silver at: 25.01 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 34 /100 roubles/dollar; ROUBLE AT 81.95//

3m oil into the 80 dollar handle for WTI and 84 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 133.07 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .448% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9048 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9858 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

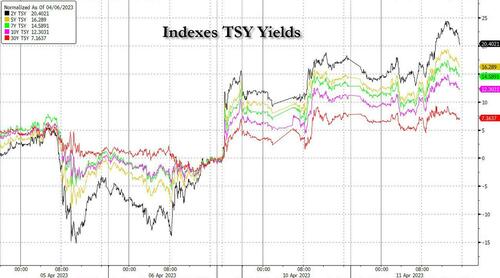

USA 10 YR BOND YIELD: 3.4000 DOWN 12BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.614 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.9848 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.29…

GREAT BRITAIN/10 YEAR YIELD: DOWN 1 BASIS PTS AT 3.514

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

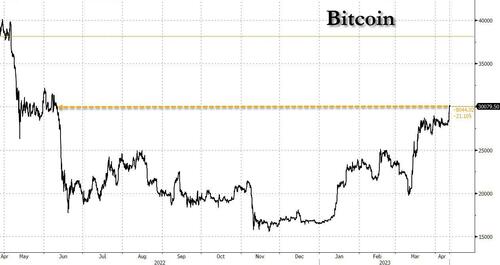

Futures Flat, Europe At 5 Week Highs, Bitcoin Over $30K

TUESDAY, APR 11, 2023 – 03:06 PM

US equity futures held on to post-holiday gains as traders awaited tomorrow’s inflation data for clues about whether the Fed’s tightening cycle is done or if it will hike once more in May (currently market odds are 74% after Friday’s strong jobs report) and also prepared for the start of the first-quarter earnings season when the big banks report on Friday. S&P 500 contracts were flat as of 7:40 a.m. ET, fading earlier gains after the underlying benchmark pulled off another late recovery on Monday as investors shrugged off fears of one more Fed rate hike in the wake of Friday’s strong US employment data. Nasdaq 100 futures dipped 0.2% after rising modestly earlier.

Overnight, China printed slowest annual CPI pace since Sept 2021. Also last night, Fed Pres Williams said he doesn’t worry if market view on rates is different than the Fed’s view and rejected arguments that rate hikes are to blame for banking sector turmoil. ECB member De Cos (historically leans dovish) said that the central bank’s baseline scenario would allow for further hikes. BOJ Governor Ueda held his inaugural press conference where he reiterated the need to maintain easy monetary policy.

European stocks rose to a 5 week high after reopening from a long holiday; Japanese equities also climbed after a Nikkei report that Warren Buffett plans to boost investments in Japan and on new Bank of Japan Governor Kazuo Ueda’s dovish remarks on monetary policy; Japanese trading companies including Mitsubishi Corp. rose after Nikkei reported that Warren Buffett is weighing investment beyond his stakes in trading houses, which he recently increased. Treasury yields retreated across the curve, but rebounded from session lows. Oil dipped and gold climbed.

The most notable overnight move came in crypto where in a broad thrust late on Monday, bitcoin breached the key $30,000 level for the first time since June on Tuesday…

… adding to its steady gains as investors raised bets that the Fed will not only soon end its aggressive monetary tightening campaign, but will start rate cuts and – according to Apollo chief economist, Torsten Slok, who like us believes the CRE crash will send the economy into a tailspin – launch QE in 2024.

In premarket trading, Tilray Brands shares slumped as much as 9.9% after the cannabis producer reported net revenue for the third quarter that missed the average analyst estimate. The company also announced the acquisition of Hexo Corp. Analysts were positive about the deal, but cautioned that challenges remain for the cannabis industry. Hexo shares declined 21% in US premarket trading. Gold miner Newmont Corp. lost 2.3% after it sweetened its bid for Australia’s Newcrest Mining. Here are some of the biggest US movers today:

- Cryptocurrency-exposed stocks rose in US premarket trading on Tuesday as Bitcoin trades above $30,000 for the first time since June 2022, surging more than 80% this year. Riot Platforms (RIOT US) +4%, Marathon Digital (MARA US) +4.2%, MicroStrategy (MSTR US) +3.3% and Coinbase (COIN US) +2.9%.

- Nasdaq Inc. (NDAQ US) shares slide 0.9% after the stock exchange operator was downgraded to equal-weight from overweight at Morgan Stanley, while the broker raised Virtu Financial (VIRT US) to equal weight from underweight, saying that it prefers more defensive and transactional exchanges due to the uncertain macroeconomic outlook.

- Akamai Technologies (AKAM US) stock gains 2.2% on low volumes after it was upgraded to overweight from neutral at Piper Sandler, with the broker saying that recent pullback in the cloud-computing company’s shares offers an opportunity to own a contrarian stock on prospect of a pullback in capex.

- Adtran (ADTN US) falls 13% in premarket trading, set to hit its lowest level since December 2020, after the communications equipment company released preliminary 1Q results, and said revenue is expected to fall short of guidance due to customer inventory corrections.

While the S&P 500 has gained 7% year-to-date amid growing bets that the Fed’s rate-hiking campaign is coming to an end, dashing countless bearish hopes that stocks should trade far lower because a recession is looming, Wednesday’s CPI reading is seen as key for policy makers as they consider such a decision.

“It’s an important number, it’s really among the data which will determine whether the Fed pivots,” said Jean-François Robin, head of global market research at Natixis. “The big risk for markets would be for the data to crush that narrative and then tech and financial stocks would get a beating.”

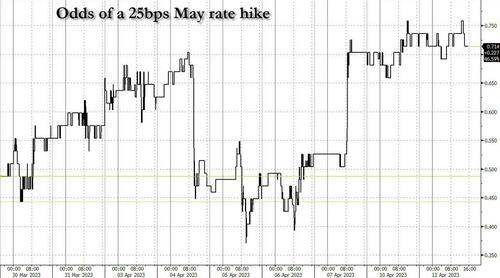

A scenario where the Fed halts rate hikes in May, which markets had briefly entertained last month as fragility in banks raised recession fears, looks increasingly remote after Friday’s unexpectedly strong jobs report. “The Fed has maintained its resolute inflation narrative despite banking sector stress, switching to liquidity tools to tackle the funding squeeze, and keeping its monetary policy toolkit intact,” Mizuho International Plc strategists including Evelyne Gomez-Liechti wrote in a note.

After May, though, markets are pricing in a pivot to easier policy. Tighter financial conditions following the failure of Silicon Valley Bank could pave the way. Investors predict rates will peak below 5%, with the Fed then cutting by roughly 50 basis points before end 2023.

Investors are also readying for an earnings season that some forecast could be the worst since the depths of the pandemic. Friday will provide a major test of sentiment when JPMorgan, Wells Fargo and Citigroup all report after weeks of market stress across the US banking sector following the failure of Silicon Vally Bank.

Meanwhile, cracks in 2023’s equity advance are appearing, as hedge funds and other speculators amass the deepest short position since November 2011 when the US sovereign credit rating was cut. In other words, another short squeeze is imminent.

“It remains a very tricky trading environment,” Chris Turner, a strategist at ING Bank wrote in a note to clients. “Experienced commentators are refusing to dismiss last month’s events as a one-off and instead prefer to see bank failures as a harbinger of forthcoming stress in the global financial system.”

European stocks returned from the Easter holiday on the front foot and risen to their best level in five weeks. The Stoxx 600 is up 0.6% with miners, autos and retailers the best performing sectors. Here are some of the biggest movers on Tuesday:

- HelloFresh shares rise as much as 7.3% as JPMorgan double- upgrades the meal-kit delivery firm to overweight from underweight, seeing the right combination of attractions to turn positive.

- Nordic Semiconductor shares fall as much as 6.1% after DNB Markets cut its price target on the chipmaker, citing several headwinds on both supply and demand sides.

- UBS shares climb as much as 2.1%, most since March 30, as JPMorgan says the Swiss bank’s “transformative deal” to take over Credit Suisse will create a wealth management “powerhouse.”

- Soitec shares climb along with other European chip stocks on Tuesday, rising as much as 6%. The wafer maker’s cautious targets for fiscal 2024 and its reduction to FY26 revenue outlook were broadly anticipated, with the weakness in the smartphone market a “well-known” culprit, according to Jefferies.

- Accor shares gain as much as 3.5% after the company is raised to overweight from equal-weight at Morgan Stanley on upside from its exposure to the luxury and lifestyle segment of the hotel sector.

- ASR Nederland shares rise as much as 6.6%, the most since October, as UBS double-upgrades the Dutch insurer to buy from sell and Citi lifts its rating to buy from neutral.

- Spirax-Sarco shares decline as much as 3% as UBS cuts its rating on the UK steam management and pumps manufacturer to neutral from buy on a weaker risk-reward.

Earlier in the session, Asian stocks rose, on track for a third day of gains, amid a report Warren Buffett plans to boost investment in Japan while the Bank of Korea kept interest rates on hold. The MSCI Asia Pacific Index climbed as much as 1.1%, with Alibaba Group and South Korea’s LG Chem among the biggest contributors. Japanese stocks gained after the Nikkei reported Buffett is weighing investment beyond his stakes in trading houses, which he recently increased. “Clearly, this news is having a significant impact on stock prices,” said Hiroshi Namioka, chief strategist at T&D Asset Management Co Ltd. “This may encourage foreign investors to invest in Japanese stocks, especially in value stocks.”

South Korean shares advanced as the central bank held policy, though it said it intends to remain in “restrictive” territory to combat inflation. Australian equities were also among the biggest regional gainers as data showed strong consumer confidence and business sentiment. Benchmarks edged higher in Hong Kong while Chinese stocks slipped as weak China inflation data suggested more monetary or fiscal stimulus may be needed. Investors will be watching US inflation data later this week for further signals on the Federal Reserve’s policy. The Fed isn’t “close to being done,” Catherine Yeung, an investment director at Fidelity International, told Bloomberg Television. While the US equity market has “basically traded sideways” the past ten months, Chinese and Asian equity markets are “looking a lot more appealing,” she added.

Stocks in India rose as forecast of a normal monsoon later this year eased concerns over growth, while a risk-on mood in Asian equities also boosted sentiment. Key stock gauges extended their winning run to the seventh session, the longest gaining streak this year, helping them rebound about 5% from their March lows. “While bond yields are still more attractive, the correction in Indian listed equities seems overdone,” Rajesh Cheruvu, managing director and chief investment officer, LGT Wealth said in a note. The S&P BSE Sensex rose 0.5% to 60,157.72 in Mumbai, while the NSE Nifty 50 Index advanced 0.6% to 17,722.30. Kotak Mahindra Bank contributed the most to the Sensex’s gain, increasing 5% as analysts expect the stock’s weighting in MSCI indexes to rise. TCS was among the biggest losers ahead of the technology major’s fourth quarter earnings announcement on Wednesday. Out of 30 stocks in the index, 21 rose and nine fell.

Japanese equities climbed amid a report that Warren Buffett plans to boost investments in Japan and on new Bank of Japan Governor Kazuo Ueda’s dovish remarks on monetary policy. The Topix Index rose 0.8% to 1,991.85 as of market close Tokyo time, while the Nikkei advanced 1% to 27,923.37. Sony Group Corp. contributed the most to the Topix Index gain, increasing 1.5%. Out of 2,158 stocks in the index, 1,610 rose and 438 fell, while 110 were unchanged. Japanese trading companies including Mitsubishi Corp. rose after Nikkei reported that Warren Buffett is weighing investment beyond his stakes in trading houses, which he recently increased. Meanwhile, Ueda said yield curve control and negative interest rates are appropriate amid the current economy. Buffett’s investment “had a moderately positive effect in the intermediate to long term regarding foreign perceptions of Japan’s market,” said John Vail, Chief Global Strategist at Nikko Asset Management. “It also supports domestic optimism, too.”

Australian stocks rose to a 3 month high; the S&P/ASX 200 index rose 1.3% to 7,309.90, boosted by miners and banks to cap its best session since Jan. 4. The advance came as Asian equities and European stock futures gained following a late recovery in post-holiday trading on Wall Street. Read: Stocks Climb Amid Buoyant Sentiment; Dollar Slips: Markets Wrap Australia’s consumer confidence surged and business sentiment showed ongoing resilience after the country’s central bank left its key interest rate unchanged for the first time in its almost yearlong tightening cycle. In New Zealand, the S&P/NZX 50 index was little changed at 11,873.58. Meanwhile, house sales fell to a record low in the three months through December as interest-rate hikes and plunging property prices pushed buyers to the sidelines

In FX, the Bloomberg Dollar Spot Index is down 0.3% with the euro and pound both rising ~0.5% versus the greenback; the Norwegian krone is the only G-10 currency that trades in the red versus the dollar, meeting a fresh round of selling from early New York flows. USD/NOK up by 0.7% to 10.6037, highest since March 21; EUR/NOK rallies 1.3% to 11.5748, a level last seen in April 2020, Real money demand sends EUR/NOK higher, while the common currency also hits fresh cycle highs versus the kiwi and the Aussie.

In rates, treasuries gained with 10-year yields falling 2bps to 3.40%, inside Monday’s selloff ranges. Most yields slid to session lows during the London morning as bund and gilt yields pared their moves; however they have since erased much of the move. Yields rose when trading resumed after a four-day weekend following Friday’s strong jobs report. US yields are lower by 2bp-3bps, led by the 3Y despite auction of that tenor ahead at 1pm New York time — the first of three Treasury coupon sales this week; the 10Y yield was down 2bps to 3.40% after earlier dipping to 3.38%. Treasury yields reached their highest levels in several days Monday as Fed swaps priced in higher odds of a 25bp May rate hike; little changed at around 75%. IG credit issuance slate includes only Mitsubishi UFJ Financial Group $benchmark so far; four high-grade offerings totaling about $2b were priced Monday. German 10-year yields have risen 6bps while the UK equivalent adds 7bps as they react to Friday’s US jobs data for the first time.

In commodities, oil extended Monday’s loss, with West Texas Intermediate dipping back below $80 a barrel after briefly crossing it. Gold was slightly higher and near $2,000 an ounce.

As noted above, Bitcoin surpassed the $30k mark, rising as high as $30,430 intraday high before paring modestly back towards the figure.

Looking to the day ahead, the event calendars is light, with just the NFIB small business confidence (90.1, exp. 89.8, Last 90.9) on deck, however things pick up tomorrow when the March CPI report and minutes of the Fed’s March policy meeting are ahead as well as auctions of 10-year notes and 30-year bonds over the next two days.

Market Snapshot

- S&P 500 futures up 0.1% to 4,139

- STOXX Europe 600 up 0.6% to 461.64

- MXAP up 0.9% to 162.31

- MXAPJ up 0.7% to 526.21

- Nikkei up 1.0% to 27,923.37

- Topix up 0.8% to 1,991.85

- Hang Seng Index up 0.8% to 20,485.24

- Shanghai Composite little changed at 3,313.57

- Sensex up 0.5% to 60,161.08

- Australia S&P/ASX 200 up 1.3% to 7,309.89

- Kospi up 1.4% to 2,547.86

- German 10Y yield little changed at 2.24%

- Euro up 0.5% to $1.0917

- Brent Futures up 0.6% to $84.66/bbl

- Gold spot up 0.7% to $2,005.09

- US Dollar Index down 0.50% to 102.07

Top Overnight News

- China’s CPI for March undershot the Street at +0.7% (vs. the St +1% and down from +1% in Feb) while the PPI slumped to -2.5% (inline with the St and down from -1.4% in Feb) as the country remains one of the world’s biggest sources of disinflation. WSJ

- Chinese provinces plan to boost spending on major construction projects by almost a fifth this year as Beijing continues to rely on infrastructure to spur an economy being hindered by consumers still bruised from years of pandemic restrictions. About two thirds of China’s regions have announced spending plans for major projects such as transport infrastructure, energy generation and industrial parks this year, adding up to more than 12.2 trillion yuan ($1.8 trillion). That’s an increase of 17% compared to last year. BBG

- Alibaba entered the ChatGPT fray. The firm will integrate its new AI model into its Slack-like office chat software and smart speakers. Meanwhile, China plans to mandate security reviews for ChatGPT-like bots before they can operate. The US opened an inquiry into how regulators and firms can ensure systems are trustworthy, legal and ethical. BBG

- Warren Buffett likes Japan. Shares of the country’s major trading houses jumped after Buffett told the Nikkei he’s raised his holdings in them and wants to increase his exposure to Japanese stocks. Berkshire kicked off a yen bond sale that may price this week, a person familiar said. Nikkei

- Alecta CEO Magnus Billing was forced to step down after Sweden’s biggest pension fund became one of the largest overseas casualties of the SVB meltdown. And the Swiss government is being grilled in parliament on UBS’s takeover of Credit Suisse. Lawmakers can do little to derail the deal, but they’ll probably try to push for an overhaul of too-big-to-fail rules and pursue legal action against CS management. BBG

- NY Fed chief John Williams played down the significance of market expectations “well off into the future” when it comes to policy decisions. Investors bet the Fed will increase by 25 bps in May, but cut later this year — which officials don’t see, according to their forecasts. Williams also said he didn’t think aggressive hikes precipitated financial strains highlighted by recent banking failures. BBG

- Yellen to tell international financial officials at this week’s IMF-World Bank spring meetings that the US banking system is on solid ground (she will hold a press conf. at 11:30amET Today). Politico

- Money supply growth is collapsing in the UK, eurozone and US, and they read that as a warning of recession and deflation. Central bankers have raised interest rates too far and, if the so-called monetarists are proved right again, they say there should be a “clear out” of officials. BBG

- Fed officials will get an early copy of the Senior Loan Officer Opinion Survey at their 5/2-3 meeting with the results acting as one input into their policy decision (the survey will be released publicly the following week). RTRS

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mostly higher following the recovery seen on Wall Street and as some major markets returned from the long weekend. ASX 200 saw its first session of the week propped up by mining names after Newmont upped its offer for Newcrest Mining. Nikkei 225 reclaimed 28k+ status with the index underpinned by the recent Yen weakness. Hang Seng and Shanghai Comp were mixed with Hong Kong playing catch-up, whilst the latter overlooked cooling inflation data and traded subdued throughout the session amid heightened tensions over Taiwan.

Top Asian News

- China could make cash injections via MLF at an unchanged rate, according to China Daily.

- PBoC said some Chinese banks cut deposit rates in April as part of normal interest rate self-discipline mechanism, according to Bloomberg.

- PBoC injected CNY 5bln via 7-day reverse repos with the rate at 2.00% for a CNY 3bln net injection.

- BoK maintained its base rate at 3.50%, as expected. BoK Governor Rhee said the decision was unanimous, and five board members wanted to keep the door open for one more possible rate hike. He said several board members see the need to give a warning against an early rate cut expectations, and added the BoK does not target an FX level, according to Reuters. BoK said economic growth is seen slower than previously expected, inflation to slow to 3% range after Q2 – in line with prior expectations, and the tightening stance to remain in place for a considerable period.

- Australian Treasurer Chalmers says global economic conditions are getting worse, according to Bloomberg.

- Japanese Finance Minister Suzuki said specific monetary policy is up to the BoJ to decide, according to Reuters.

- Japan’s Labour Confederation Chief does not think a one-off wage hike for the year is adequate, and will seek further increases next year and the year after.

- Warren Buffet said he intends to add more investments in Japanese stocks, according to Nikkei.

European bourses are mostly in the green, Euro Stoxx 50 +0.7%, continuing the positive APAC handover on their return to the market with newsflow otherwise limited. Sectors are similar and feature outperformance in Basic Resources while Food, Beverage and Tobacco names lag. Stateside, futures are steady with a slight positive bias, ES +0.3%, with action elsewhere playing catch-up to the late-Monday US upside. China Vehicle sales (Mar): 9.7% YY (prev. 13.5% in February), via Industry Association; NEVs +34.8% YY

Top European News

- UK PM Sunak plans on calling for general elections in the autumn of 2024, according to The Telegraph; Sunak’s Conservatives Are Gaining Ground on Labour, Poll Shows

- British Households Cut Luxuries and Dining Out After Prices Jump

- BP Expands UK Carbon Capture Bet With Harbour Energy Deal

- IPO Pipeline Gets Fillip From Investment Firm: The London Rush

- Italy upgrades 2023 GDP growth forecast to 1% (prev. 0.6% set in Nov) but downgrades 2024 forecast to 1.4% (prev. 1.9%), according to government officials cited by Reuters.

FX

- Dollar loses post-payrolls momentum to the benefit of major peers, as DXY drifts down towards 102.000 from just over 102.500.

- Franc probes 0.9050 after defending 0.9100, Euro probes 1.0900, Sterling back on the 1.2400 handle and Yen eyes 133.00 following breaches of the 100 and 50 DMAs.

- Aussie outperforms down under on the back of encouraging improvements in business and consumer confidence alongside a resolution on WTO disputes with China.

- PBoC sets USD/CNY mid-point at 6.8882 vs exp. 6.8884 (prev. 6.8764)

- HKMA bought HKD 3.81bln after the currency reached the weak end of the trading band, according to Reuters.

- Russian President Putin to discuss the “situation on currency market” with CBR’s Nabiullina and Fin Min Siluanov later on Tuesday. Follows the CBR saying the share of USD and EUR deposits in Russian banks are still high and significantly higher than CNY; FX deposits abroad exceeded FX deposits in Russia in 2022.

Fixed Income

- EGBs remain pressured, in catch-up to the post-NFP hawkish trade, but have bounced markedly off initial lows with USTs positive throughout but directionally in-fitting.

- Specifically, Bunds retested the overnight Eurex peak after initially dipping to a 136.12 trough while more recently Gilts climbed to a 103.83 high before easing off best.

- Stateside, action has been more contained with USTs in a circa. 10 tick range and the yield curve under modest but broad-based pressure with the docket thin until Fed speak/3yr supply.

Commodities

- Crude benchmarks retain an underlying positive bias from the supportive APAC tone, with fresh developments and price action since limited amid a thin docket for the session

- Currently, WTI and Brent have been back above USD 80/bbl and USD 85/bbl respectively at best, albeit the latter has slipped incrementally back below the figure.

- Spot gold is firmer and holding just above the USD 2k/oz mark around USD 10/oz above the 10-DMA at USD 1991/oz while base metals also derive support from the improving tone between Australia and China.

Geopolitics

- Taiwan Defence Ministry said as of late Tuesday morning, they have spotted 26 Chinese military planes and nine Chinese ships around Taiwan, according to Reuters.

- Egypt secretly planned to supply rockets to Russia, according to a leaked US document cited by the Washington Post. Egypt’s president in February planned to produce 40,000 rockets for Russia and instructed officials to keep production & shipment secret “to avoid problems with the West”.

- North Korea does not respond to the inter-Korean liaison office for a fifth straight day, according to Yonhap.

- US, Japan, and South Korea to discuss North Korea in defence talks on April 14th, according to Bloomberg.

- Australia is to suspend its WTO dispute against China on barley after reaching an agreement with China for the resolution of the dispute; China agreed to undertake a review of duties imposed on Australian barley, according to Reuters. Subsequently, China’s Foreign Ministry says it is willing to work with Australia to return relations to the right track.

- Brazilian President Lula said he is going to invite Chinese President Xi to Brazil, according to Reuters.

- Japanese Finance Minister Suzuki said they are to hold the G7 meeting on April 12th and will discuss the economy, supply chain, and the Ukraine crisis, according to Reuters.

US Event Calendar

- 06:00: March SMALL BUSINESS OPTIMISM, 90.1, est. 89.8, prior 90.9

Central Bank Speakers

- 13:30: Fed’s Goolsbee Speaks at Economic Club of Chicago

- 18:00: Fed’s Harker Discusses the Economic Outlook

- 19:30: Fed’s Kashkari Speaks in Town-Hall Event

DB’s Henry Allen concludes the overnight wrap

Welcome back and hope you all enjoyed the long weekend. Most European markets have been closed over the last couple of sessions, but there’s been a bit more trading in the US, where last week’s risk-off tone moderated somewhat. Indeed, the S&P 500 traded lower for the majority of yesterday’s session before recovering to close up +0.10%, and both Asian equities and US equity futures have seen further gains this morning. In the meantime US Treasuries sold off, with the 10yr yield up by another +2.6bps yesterday to 3.417%, which comes on the heels of an +8.6bps increase last Friday.

In many respects it’s been a fairly quiet period since our last edition, but one of the biggest stories was last Friday’s US jobs report, which showed another decent gain in nonfarm payrolls of +236k in March (vs. +230k expected). Furthermore, the unemployment rate fell back a tenth to 3.5% (vs. 3.6% expected) and the participation rate hit a post-Covid high of 62.6% (vs. 62.5% expected), so there was plenty of good news to digest.

With another strong jobs report in hand, investors have responded by dialling up the probability of another Fed rate hike at the next meeting. That’s now only three weeks from tomorrow, and since the jobs report, the odds of another 25bp hike have risen from a near-even 53% to a stronger 71% this morning. In addition, futures further out the curve are pricing in their most hawkish rate path for the Fed since the SVB collapse, with the year-end rate priced at 4.40% by yesterday’s close. That’s the highest it’s been in a month, even if it’s still over a full point beneath its pre-SVB level of 5.56%.

This sense that we might get a more hawkish Fed was bolstered by the New York Fed’s latest Survey of Consumer Expectations which came out yesterday. That showed inflation expectations rising in March at both the 1yr and 3yr horizons for the first time in 5 months. For instance, the 1yr expectation was up half a point to 4.7%, and the 3yr expectation rose a tenth to 2.8%. Nevertheless, there were some more dovish details in report, including that the share of households saying it was harder to obtain credit than a year ago rose to 58.2%, the highest since the survey began a decade ago.

Speaking of more dovish signals, the jobs report did actually contain several indicators pointing to a cooling labour market, even if the market’s main focus was on how it made a May hike more likely. For instance, the monthly gain in nonfarm payrolls of +236k was actually the slowest since December 2020. On top of that, average hourly earnings were up by +0.3% on a monthly basis, which took the annual change down to its lowest since June 2021, at +4.2% (vs. +4.3% expected). Another detail that caught our eye was the decline in the temporary help services category, which has historically been a leading indicator in previous cycles. That category has now seen a decline in payrolls of -4.1% relative to a year earlier, and whilst the data only goes back to 1990, on every occasion they’ve fallen by that much before, the US has either been in or near a recession.

This morning in Asia, equities are mostly positive following lower trading volumes in the region over the last couple of sessions. Currently, the KOSPI (+1.38%) is leading gains in the region, which follows the Bank of Korea’s decision to maintain interest rates at 3.5% as expected. And the Nikkei (+1.34%), the S&P/ASX 200 (+1.31%) and the Hang Seng (+0.07%) have all seen gains as well. By contrast, the CSI 300 (-0.25%) and the Shanghai Composite (-0.35%) both losing ground. That comes on the back of China’s March inflation data showing CPI fell to an 18-month low of +0.7% (vs. +1.0% expected). Looking forward, US equity futures are pointing a bit higher, with those on the S&P 500 up +0.11%, whilst Bitcoin has just surpassed the $30,000 mark for the first time since last June.

Staying on Asia, yesterday also brought a noticeable weakening in the Japanese Yen, which fell -1.08% against the US Dollar. That followed a press conference from new BoJ Governor Ueda, who said that “given the current economic, price and financial conditions, I think it’s appropriate to keep up the current yield curve control”. That was a more dovish tone than had been expected by some, since there had been anticipation that Ueda might seek to move away from the yield curve control policies of his predecessor.

Looking forward to this week now, the focus will likely remain on the Fed’s next decision, since tomorrow sees the release of the US CPI report for March. The February release showed that inflation was still running reasonably fast, with core CPI at a 5-month high of +0.45%, and this time around our US economists expect core inflation to come off a bit to +0.39%, although that would still leave the year-on-year change up a tenth at +5.6%. For headline inflation, they see a lower rate of +0.24%, taking the year-on-year rate down to +5.2%. Remember this month that there’ll be unusually large base effects at play, since the March 2022 surge in energy prices after Russia’s invasion of Ukraine will be dropping out of the annual comparisons.

Speaking of the Fed, we should get another window into their thinking from the release of the FOMC minutes for March tomorrow. That meeting took place shortly after the market turmoil, which created some doubt as to whether they would proceed with a rate hike at all. Indeed, it was reported by Nick Timiraos in the Wall Street Journal that it was “their closest call” in years and that the decision was only made to proceed with a hike two days beforehand. So it’ll be interesting to see their thoughts on how far they should keep hiking rates. Otherwise, this week’s main central bank policy decision comes from the Bank of Canada tomorrow. They announced a pause in rate hikes at their January meeting, so investors are expecting that rates will remain unchanged.

Elsewhere this week, global policymakers will be gathering in Washington for the IMF/World Bank spring meetings. As part of that, the IMF will be releasing their latest economic forecasts later today, and G20 finance ministers and central bank governors will also be meeting this week. Plenty of officials will be speaking publicly whilst there as well, including BoE Governor Bailey and Bundesbank President Nagel.

Finally, the other important thing to watch out for will be the start of earnings season. Several US financials will be kicking things off on Friday, including JPMorgan Chase, Citigroup, Wells Fargo and BlackRock. US banks have already had a very weak start to the year given the market turmoil, with the KBW Banks Index now down by -19.60% on a YTD basis.

2 b) NOW NEWSQUAWK (EUROPE/REPORT)/ASIA REPORT

APAC bolstered after a Wall St. recovery as markets return from Easter – Newsquawk Europe Market Open

TUESDAY, APR 11, 2023 – 08:51 AM

- APAC stocks traded mostly higher following the recovery seen on Wall Street and as some major markets returned from the long weekend

- European equity futures gapped higher on the return from the Easter break and are indicative of a firmer cash open, with Euro Stoxx 50 +0.5%

- DXY traded subdued for most of the session, USD/JPY also saw choppy price action and AUD outperformed

- Bund futures gapped lower at the open but clambered off worst levels, Crude futures edged higher throughout the APAC session

- Looking ahead, highlights include Norwegian CPI, EZ Retail Sales and Sentix Index, EIA STEO, speeches from Fed’s Goolsbee (voter), Harker (voter), and supply from Germany and the US

View the full premarket movers and news report.

Or why not try Newsquawk’s squawk box free for 7 days?

EASTER HOLIDAY NEWS

- Click here to catch up on the main events from Easter

US TRADE

EQUITIES

- US stocks were ultimately flat on Easter Monday, unwinding earlier losses in the aftermath of Friday’s NFP report, some cited a Bloomberg sources piece during the NY lunchtime which suggested the Federal Home Loan Bank system had drastically cut the total amount of borrowing in the latest week as a factor behind the recovery in risk.

- SPX +0.10% at 4,109, NDX -0.09% at 13,051, DJIA +0.30% at 33,586, RUT +1.02% at 1,772.

- Click here for a detailed summary.

NOTABLE HEADLINES

- Federal Home Loan Bank (FHLB) debt issuance “plunges” in a signal of the easing US bank crisis; USD 37bln in the latest week vs 304bln in the two weeks prior, according to Bloomberg sources.

- Fed’s Williams (voter, neutral) said it is important to understand inflation dynamics are complicated; sees inflation this year at around 3.75% and expects to get to 2% inflation by 2025. He expects growth this year to be under 1% and said there is a lot of uncertainty around the inflation outlook. He said the stability of unemployment has been a striking development, and he expects to see the unemployment rate rise gradually to 4-4.5% (prev. saw the unemployment rate tick up to around 4.5% in late March). He sees rent-related price pressures coming down sharply. Williams said market policy expectations are tricky to measure, and he does not worry if the market’s view on rates differs from the Fed’s view. He is happy to see market rate expectations are reactive to data and said Fed rate hikes weren’t the driver of trouble at banks sparking the latest stresses. He hasn’t seen clear signs of credit tightening, via Reuters.

- Senior US Treasury Official views the US banking system as strong and resilient, according to Reuters.

DATA RECAP

- Atlanta Fed GDPnow (Q1): 2.2% (prev. 1.5%).

APAC TRADE

EQUITIES

- APAC stocks traded mostly higher following the recovery seen on Wall Street and as some major markets returned from the long weekend.

- ASX 200 saw its first session of the week propped up by mining names after Newmont upped its offer for Newcrest Mining.

- Nikkei 225 reclaimed 28k+ status with the index underpinned by the recent Yen weakness.

- Hang Seng and Shanghai Comp were mixed with Hong Kong playing catch-up, whilst the latter overlooked cooling inflation data and traded subdued throughout the session amid heightened tensions over Taiwan.

- US equity futures held a flat/mild upward bias for most of the session but within tight ranges.

- European equity futures gapped higher on the return from the Easter break and are indicative of a firmer cash open, with Euro Stoxx 50 +0.7%.

FX

- DXY was choppy within a tight 102.31-51 range, but overall traded subdued for most of the session.

- EUR/USD found some support around 1.0855 while GBP/USD topped 1.2400 in what was seemingly dollar-driven action.

- USD/JPY also saw choppy price action, with the pair pulling back towards its 100 and 50 DMAs (at 133.31 and 133.25 respectively) before finding support at the latter.

- AUD took the spot as the G10 outperformer after China and Australia reached an agreement on a WTO dispute regarding Chinese duties imposed on Australian barley.

- PBoC sets USD/CNY mid-point at 6.8882 vs exp. 6.8884 (prev. 6.8764)

- HKMA bought HKD 3.81bln after the currency reached the weak end of the trading band, according to Reuters.

FIXED INCOME

- 10yr UST futures attempted to claw back some losses following the prior day’s selling and ahead of a 3yr Note auction later today.

- Bund futures gapped lower at the open but clambered off worst levels as the German bond future played catchup from the Easter break.

- 10yr JGB futures traded on a firmer footing with the complex also propped up by a successful 5yr JGB auction.

COMMODITIES

- Crude futures edged higher throughout the session amid a mostly positive APAC mood, with WTI reclaiming USD 80/bbl+ status.

- Spot gold struggled to reach the USD 2,000/oz mark as DXY remained caged to a tight range.

- Copper futures traded flat on the LME, whilst CME copper met resistance at the USD 4/lb psychological mark.

CRYPTO

- Bitcoin prices were volatile with the crypto rising above USD 30k before meeting resistance near USD 30.5k.

NOTABLE ASIA-PAC HEADLINES

- China could make cash injections via MLF at an unchanged rate, according to China Daily.

- PBoC said some Chinese banks cut deposit rates in April as part of normal interest rate self-discipline mechanism, according to Bloomberg.

- PBoC injected CNY 5bln via 7-day reverse repos with the rate at 2.00% for a CNY 3bln net injection.

- BoK maintained its base rate at 3.50%, as expected. BoK Governor Rhee said the decision was unanimous, and five board members wanted to keep the door open for one more possible rate hike. He said several board members see the need to give a warning against early rate cut expectations, and added the BoK does not target an FX level, according to Reuters. BoK said economic growth is seen slower than previously expected, inflation to slow to 3% range after Q2 – in line with prior expectations, and the tightening stance to remain in place for a considerable period.

- French senators to visit Taiwan in the week of April 24th, and will discuss semiconductors during the visit, according to Senate office

- Australian Treasurer Chalmers says global economic conditions are getting worse, according to Bloomberg.

- Japanese Finance Minister Suzuki said specific monetary policy is up to the BoJ to decide, according to Reuters.

- Warren Buffet said he intends to add more investments in Japanese stocks, according to Nikkei.

DATA RECAP

- Chinese CPI YY (Mar) 0.7% vs. Exp. 1.0% (Prev. 1.0%)

- Chinese CPI MM (Mar) -0.3% (Prev. -0.5%)