april 14/2023 · by harveyorgan · in Uncategorized · Leave a comment·Editi

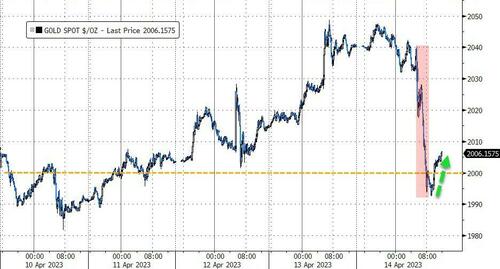

GOLD PRICE CLOSED: DOWN $38.90, TO $2002.10

SILVER PRICE CLOSED: DOWN 51 CENTS AT $25.32

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE $2004.90

Silver ACCESS CLOSE: 25.37

Bitcoin morning price:, $30,816 UP 542 Dollars

Bitcoin: afternoon price: $30,249 DOWN 25 dollars

Platinum price closing $1042.35 DOWN $13.30

Palladium price; closing $1490.20 DOWN $30.15

END

I am back to my usual routine.

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2680/00 DOWN 41.34 CDN dollars per oz (ALL TIME HIGH 2732.50)

BRITISH GOLD: 1614.75 DOWN 13.73 pounds per oz//(ALL TIME HIGH//1629.84)

EURO GOLD: 1823/22 DOWN 22.37 euros per oz //(ALL TIME HIGH//1860.82)

COMEX DATA EXCHANGE:

COMEX//NOTICES

GOLDMAN 3

104 C MIZUHO 1

118 C MACQUARIE FUT 100

132 C SG AMERICAS 1

323 C HSBC 12

363 H WELLS FARGO SEC 66

435 H SCOTIA CAPITAL 195

523 C INTERACTIVE BRO 2

624 C BOFA SECURITIES 1

624 H BOFA SECURITIES 20

657 C MORGAN STANLEY 13

661 C JP MORGAN 257

685 C RJ OBRIEN 1

690 C ABN AMRO 3

726 C CUNNINGHAM COM 1

732 C RBC CAP MARKETS 25

737 C ADVANTAGE 2

800 C MAREX SPEC 4 14

880 C CITIGROUP 3 4

880 H CITIGROUP 701

905 C ADM 15

DLV615-T CME CLEARING

BUSINESS DATE: 04/13/2023 DAILY DELIVERY NOTICES RUN DATE: 04/13/2023

PRODUCT GROUP: METALS RUN T

JPMorgan stopped 257/733 contracts

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation.

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2023. CONTRACT: 722 NOTICES FOR 72,200 OZ or 2.2457 TONNES

total notices so far: 22,492 contracts for 2,259,200 oz (69.959 tonnes)

SILVER NOTICES: 3 NOTICE(S) FILED FOR 15,000 OZ/

total number of notices filed so far this month : 307 for 1,535,000 oz

END

GLD

WITH GOLD DOWN $38.90

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD://////A WITHDRAWAL OF 3.47 TONNES OF GOLD INTO THE GLD

INVENTORY RESTS AT 930.61 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 51 CENTS

AT THE SLV// NO CHANGES IN SILVER INVENTORY AT THE SLV: //: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV

CLOSING INVENTORY: 470.974 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY AN ATMOSPHERIC SIZED 6668 TO 152,363 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS GIGANTIC SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG $0.48 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. WE HAVE NOW SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.48). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A MONSTER GAIN ON OUR TWO EXCHANGES 8134 CONTRACTS. WE HAD 1,000 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 5.0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 18.330 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS( 1466 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.055 MILLION OZ(FIRST DAY NOTICE)+ THE 18.33 MILLION OZ OF EXCHANGE FOR RISK//THUS TOTAL NEW STANDING 19.975 MILLION OZ/ //// V) HUGE SIZED COMEX OI GAIN/ HUGE SIZED EFP ISSUANCE/.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –55 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL:

TOTAL CONTRACTS for 9 days, total 14,516 contracts: OR 72.580 MILLION OZ . (1612 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 72.580 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE BUT BELOW LAST MONTH

APRIL 72.580 MILLION OZ

RESULT: WE HAD AN ATMOSPHERIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 6668 CONTRACTS WITH OUR $0.48 GAIN IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED EFP ISSUANCE CONTRACTS: 1466 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL OF 1.055 MILLION OZ//FIRST DAY NOTICE// 15,000 OZ QUEUE JUMP (WHICH INCREASES THE AMOUNT OF SILVER STANDING) + 5.0 MILLION NEW EXCHANGE FOR RISK TODAY (INCREASES THE AMOUNT OF SILVER STANDING) //NEW EXCHANGE FOR RISK STANDING 18.33 MILLION OZ, THUS TOTAL SILVER OZ STANDING FOR DELIVERY IN APRIL TOTALS 19.975 MILLION .. WE HAVE AN ATMOSPHERIC SIZED GAIN OF 8189 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 3 NOTICE(S) FILED TODAY FOR 15,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 8917 CONTRACTS TO 492,348 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED 511 CONTRACTS

WE HAD A STRONG SIZED INCREASE IN COMEX OI ( 8917 CONTRACTS) WITH OUR $31.70 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR APR. AT 66.892 TONNES ON FIRST DAY NOTICE // PLUS A 86,000 OZ QUEUE JUMP:(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)YET ALL OF..THIS HAPPENED WITH OUR $31.70 GAIN IN PRICE WITH RESPECT TO THURSDAY’S TRADING.WE HAD A VERY STRONG SIZED GAIN OF 12,960 OI CONTRACTS (40.311 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4043 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 492,348

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 12,960 CONTRACTS WITH 8917 CONTRACTS INCREASED AT THE COMEX AND 4043 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 12,960 CONTRACTS OR 40.311 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4043 CONTRACTS) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (8917 //TOTAL GAIN IN THE TWO EXCHANGES 12,960 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 66.892 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 86,000 OZ//NEW STANDING 72.252 TONNES // ///3) ZERO LONG LIQUIDATION//4) STRONG SIZED COMEX OPEN INTEREST GAIN/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

MAR

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 35,455 CONTRACTS OR 3,645,500 OZ OR 110.28 TONNES IN 9 TRADING DAY(S) AND THUS AVERAGING: 3939 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES 110.28 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 110.28/3550 x 100% TONNES 3.09% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 110.28 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY AN ATMOSPHERIC SIZED 6668 CONTRACTS OI TO 152,363 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 1466 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1466 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1466 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 6668 CONTRACTS AND ADD TO THE 1466 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE GAIN OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 8134 CONTRACTS.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES //40.670 MILLION OZ

OCCURRED WITH OUR $0.48 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

NORTH KOREA/SOUTH KOREA

i)FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED UP 19.79 PTS OR .60% //Hang Seng CLOSED UP 94.33 POINTS OR .46% /The Nikkei closed UP 94.33 PTS OR 0.46% //Australia’s all ordinaries CLOSED UP 0.53 % /Chinese yuan (ONSHORE) closed UP TO 6.8545/OFFSHORE CHINESE YUAN UP TO 6.8539 /Oil UP TO 82.35 dollars per barrel for WTI and BRENT AT 86.38 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 8917 CONTRACTS UP TO 492,378 WITH OUR GAIN IN PRICE OF $31.70 ON THURSDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF APRIL… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4043 EFP CONTRACTS WERE ISSUED: : JUNE 4043 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4043 CONTRACTS

WHEN WE HAVE BACKWARDATION, EFP ISSUANCE IS VERY COSTLY BUT THE REAL PROBLEM IS THE SCARCITY OF METAL AND IT IS FAR BETTER FOR OUR BANKERS TO PAY OFF INDIVIDUALS THAN RISK INVESTORS ESPECIALLY FROM LONDON STANDING FOR DELIVERY. THE LOWER PRICES IN THE FUTURES MARKET IS A MAGNET FOR OUR LONDONERS SEEKING PHYSICAL METAL. BACKWARDATION ALWAYS EQUAL SCARCITY OF METAL!

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG SIZED TOTAL OF 12,960 CONTRACTS IN THAT 4043 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED GAIN OF 8917 COMEX CONTRACTS..AND THIS VERY STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $31.70. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: APRIL (72.252) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 72.252 tonnes

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $31.70 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR VERY STRONG SIZED GAIN OF 12,960 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 38.721 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL. (66.892 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 86,000 OZ… ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $31.70

WE HAD + ADDED 511 CONTRACTS ADDED(REMOVED) TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 12,960 CONTRACTS OR 1,296,000 OZ OR 40.311 TONNES.

Estimated gold comex today 201,424 FAIR

final gold volumes/yesterday 210,229 fair

//APRIL 14/ APRIL 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 128.604 oz 5 kilobars BRINKS . |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | NIL OZ |

| No of oz served (contracts) today | 722 notice(s) 72200 OZ 2.2457 TONNES |

| No of oz to be served (notices) | 737 contracts 73700 oz 2.292 TONNES |

| Total monthly oz gold served (contracts) so far this month | 22,492 notices 2,249,200 OZ 69.959 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: NIL oz

customer withdrawals: 1

i) Out of BRINKS: 128.604 oz (5 kilobars)

total withdrawals: 128.604 oz

Adjustments; 1

I) OUT OF MANFRA: 1157.456 OZ DEALER TO CUSTOMER

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAR.

For the front month of APRIL we have an oi of 1459 contracts having GAINED 769 contracts. We had 91 contracts served upon yesterday so we GAINED 860 contracts or 86,000 oz were QUEUE JUMPED.

May gained 36 contracts up to 2024.

June GAINED 6181 contracts UP to 414,720 contracts.

We had 722 contracts filed for today representing 72,200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 722 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 257 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2023. contract month,

we take the total number of notices filed so far for the month (22,492 x 100 oz ), to which we add the difference between the open interest for the front month of (APRIL. 1459 CONTRACTS) minus the number of notices served upon today 722 x 100 oz per contract equals 2,322,900 OZ OR 72.252 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month: No of notices filed so far (22,492 x 100 oz)+ 1459 OI for the front month minus the number of notices served upon today (722)x 100 oz} which equals 2,322,900 oz standing OR 72.262 TONNES in this active delivery month of APRIL..

TOTAL COMEX GOLD STANDING: 72.262 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,703,295.912 OZ 52,97 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,948,598.168 OZ

TOTAL REGISTERED GOLD: 12,278,562.952 (381.91 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 9,670,035.216 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,575.267 OZ (REG GOLD- PLEDGED GOLD) 328.93 tonnes//

END

SILVER/COMEX

APRIL 14//2023// THE APRIL 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 937,900.722 oz BRINKS CNT LOOMIS . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 600,449.980 oz CNT |

| No of oz served today (contracts) | 3 CONTRACT(S) (15,000 OZ) |

| No of oz to be served (notices) | 22 contracts (110,000 oz) |

| Total monthly oz silver served (contracts) | 307 Contracts (1,535,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 0 deposits into the customer account

Total deposits: nil oz

JPMorgan has a total silver weight: 141.738 million oz/274.064 million =51.82% of comex .//dropping fast

Comex withdrawals: 3

i) Out of Brinks 2979.02 oz

ii) Out of CNT 5024.590 oz

iii) Out of Loomis: 929,897.112 oz

Total withdrawals; 937,900.722 oz

adjustments: 1

dealer to customer INT DELAWARE: 53,713.560 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 34.063 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 274.064 million oz

CALCULATION OF SILVER OZ STANDING FOR MAR

silver open interest data:

FRONT MONTH OF APRIL /2023 OI: 25 CONTRACTS HAVING LOST 2 CONTRACT(S). WE HAD 5 NOTICES FILED ON THURSDAY SO WE GAINED 3 CONTRACTS OR AN ADDITIONAL 15,000 OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF APRIL.

MAY SAW A LOSS OF 1949 CONTRACTS DOWN TO 79,904

JUNE HAD A 15 CONTRACT LOSS TO 111

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 3 for 15,000 oz

Comex volumes// est. volume today 108,920 HUGE

Comex volume: confirmed yesterday: 95,307 STRONG

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 307 x 5,000 oz = 1,535,000 oz

to which we add the difference between the open interest for the front month of APRIL(25) and the number of notices served upon today 3 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL/2023 contract month: 307 (notices served so far) x 5000 oz + OI for the front month of APRIL (25) – number of notices served upon today (3 )x 500 oz of silver standing for the APRIL. contract month equates 1.645 million oz +/ NEW EXCHANGE FOR RISK TODAY: 5.0 MILLION OZ //NEW TOTALS EXCHANGE FOR RISK FOR MONTH OF APRIL: 18.33 MILLION OZ// THUS TOTAL SILVER OZ STANDING: 19.975 MILLION OZ//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

APRIL 14/WITH GOLD DOWN $38.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 930.61 TONNES

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

APRIL 10/WITH GOLD DOWN $21.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91 TONNES

APRIL 6//WITH GOLD DOWN $9.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91

APRIL 5//WITH GOLD UP 0 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04

APRIL 4/WITH GOLD UP $36.30 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

APRIL 3/WITH GOLD UP $14.20 TODAY;NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.02 TONNES

MARCH 31/WITH GOLD DOWN $10.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD////INVENTORY RESTS AT 928.02 TONNES

MARCH 30//WITH GOLD UP XX TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A DEPOSIT OF 2.24 TONNES FROM THE GLD/INVENTORY RESTS AT 929.47 TONNES

MARCH 29/WITH GOLD DOWN $4.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4,16 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 927,23

MARCH 28/WITH GOLD UP $19.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

MARCH 15/THE IDES OF MARCH: WITH GOLD UP $18.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 913.27 TONNES

MARCH 14/WITH GOLD DOWN $4.75 TODAY: HUGE CHANGES: A MONSTER DEPOSIT OF 11.85 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 913.27 TONNES

MARCH 13/WITH GOLD UP $48.85 TODAY: VERY STRANGE HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY REST AT 901.42 TONNES

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

GLD INVENTORY: 930.61 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 14/WITH SILVER DOWN 48 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.974 MILLION OZ/

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 10/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 6/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 4.643 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 468.585 MILLION OZ//

APRIL 5/WITH SILVER DOWN 4 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.942 MILLION OZ

APRIL 4/WITH GOLD UP $1.11 TODAY CRIMINAL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.47 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 463,942 MILLION OZ

APRIL 1/WITH SILVER DOWN 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.412

MARCH 31/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE GLD/: A MASSIVE 4.779 MILLION OZ DEPOSITED INTO THE SLV///INVENTORY RESTS AT465.412 MILLION OZ

MARCH 30/WITH SILVER UP XX CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV.: A DEPOSIT OF 550,000 OZ INTO THE SLV/.INVENTORY RESTS AT 460.633 MILLION OZ

MARCH 29/WITH SILVER UP 11 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 460.082

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

MARCH 17/WITH SILVER UP 79 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE WITHDRAWAL OF 10.478 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 462.748 MILLION OZ//

MARCH 16/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 5.009 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 473.226 MILLION OZ//

MARCH 15/WITH SILVER DOWN 7 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 643,000 OZ INTO THE SLV//INVENTORY RESTS AT 478.235 MILLION OZ/

MARCH 14/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.287 MILLION OZ FROM THE SLV////INVENTORY REST AT 477.592 MILLION OZ//

MARCH 13/WITH SILVER UP $1.35 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ//

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWALOF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

CLOSING INVENTORY 470.974 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//

end

END

3,Chris Powell of GATA provides to us very important physical commentaries

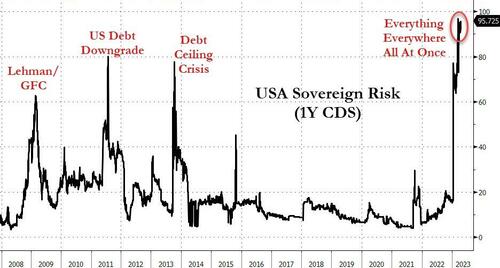

This is interesting: debt ceiling jitters is causing credit default swaps on the uSA to rise

(London’sFinancialTimes/GATA)

Debt ceiling jitters drive up cost of insuring against U.S. default

Submitted by admin on Thu, 2023-04-13 16:38Section: Daily Dispatches

By Kate Duguid, Lauren Fedor, and Colby Smith

Financial Times, London

Thursday, April 13, 2023

The cost of buying insurance against a U.S. government default has shot to its highest level in more than a decade, in an early sign of market concerns about the political impasse in Washington over the debt ceiling.

Amid a stalemate between the White House and congressional Republicans on raising the federal borrowing limit, the price of five-year credit default swaps — the most widely traded form of debt insurance — reached its highest

A default on U.S. federal debt — an outcome U.S. Treasury Secretary Janet Yellen has warned would lead to “catastrophe” — is still viewed as unlikely.

But investors are moving to protect themselves against the possibility, which could theoretically come as soon as June, or to profit from a protracted game of chicken that upends markets. …

… For the remainder of the report:

https://www.ft.com/content/0ffc5460-09b8-4d0f-9f52-66337916cac4

end

For your interest….

Bloomberg columnist admits and contrives a rationale for dollar imperialism

Submitted by admin on Thu, 2023-04-13 16:15 Section: Daily Dispatches

4:20p ET Thursday, April 13, 2023

Dear Friend of GATA and Gold:

An opinion column by Tyler Cowen of Bloomberg News today offered an awfully contrived rationale for U.S. dollar imperialism and exploitation throughout the world. But Cowen’s acknowledging that imperialism and exploitation was service enough.

In his column, “What De-Dollarization? The Dollar Rules the World” —

He writes: “Think of ‘a sound and focal dollar’ as a good or service that the U.S. produces, just as China manufactures phones or Japan makes cars. When Americans trade dollars for foreign goods and services, that measures as a U.S. trade deficit, but it can also be seen as America exporting dollars and ‘dollar services.’ The U.S. brands and markets its dollar, just as Zara or the Gap brands and markets clothing.

“So the much-vaunted U.S. trade deficit can be reconceptualized as a form of barter: One service (dollar stability) is being exchanged for another good or service (e.g., whatever America buys from China). In essence, branding and selling dollars so effectively — also known as ‘buying things’ — enables U.S. consumers to have a higher standard of living.”

Forget for a moment that the dollar’s “stability” has been a joke since dollar convertibility into gold was ended in 1971 and especially in the last several years, during which the primary export of the United States has been the inflation that is devastating the world.

Instead, consider whether the world could not devise an impartial currency that did not confer on a single country such an “exorbitant privilege,” to use the long-ago term of a French finance minister — the privilege to exploit the world economically to any extent.

Of course the world once had such an impartial currency — gold.

Yes, to some extent the rest of the world may be getting what it deserves for its complicity with the longstanding U.S. policy of pushing gold outside the world financial system. But at least much of the rest of the world seems to be wising up to its enslavement and reawakening to the old virtues of the monetary metal.

Cowen may be right that the resentment felt by the rest of the world, no matter how justified, will never manage to overthrow the dollar. Even so, he inadvertently has acknowledged the justice of such a change.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

For sure; the Fed has more than a credibility problem

Veronique de Rugy/Creators Syndicate)

Veronique de Rugy: The Fed has more than a credibility problem

Submitted by admin on Thu, 2023-04-13 12:32Section: Daily Dispatches

By Veronique de Rugy

Creators Syndicate, Hermosa Beach, California

Thursday, April 13, 2023

I have heard some people say that the Federal Reserve has a credibility problem. The agency missed the biggest inflation spike since the 1980s, was slow to start rolling back pandemic policies, and failed to spot the risks that some banks, such as Silicon Valley Bank, were facing. Instead of instilling confidence and stability, the Fed’s policy communication has at times been so unclear and confused that it has only served to exacerbate market volatility.

Credibility is a big enough problem, but unfortunately the Fed’s issues go beyond that. The Fed as an institution, along with its policies, seem to be a main source of the economic instability America faces. In fact, David Stockman, budget director under President Ronald Reagan, calls the Fed an “SDI” — a Systematically Dangerous Institution.

A responsible political class would pay more attention to an organization’s failures and significantly reform it. Instead politicians will likely do what they have done in the past: give the Fed even more power to regulate the economy in ways that will only cause further harm. …

… For the remainder of the commentary:

https://www.creators.com/read/veronique-de-rugy/04/23/the-fed-has-more-than-a-credibility-problem

end

Lula, the member of Klaus Schwab’s WEF calls for the end of the dollar’s trade dominance

(London’s FinancialTimes)

Brazil’s Lula calls for end to dollar trade dominance

Submitted by admin on Thu, 2023-04-13 11:48Section: Daily Dispatches

By Joe Leahy and Hudson Lockett

Financial Times, London

Thursday, April 13, 2023

Brazil’s president, Luiz Inácio Lula da Silva, has called on developing countries to work toward replacing the U.S. dollar with their own currencies in international trade, lending his voice to Beijing’s efforts to end the greenback’s dominance of global commerce.

Kicking off his first state visit to China since taking office in January, Lula called for the countries of the so-called BRICS group of nations — which in addition to Brazil and China includes Russia, India, and South Africa — to come up with their own alternative currency for use in trade

“Every night I ask myself why all countries have to base their trade on the dollar,” Lula said in an impassioned speech at the New Development Bank in Shanghai, known as the “BRICS bank.”

“Why can’t we do trade based on our own currencies?” he added, drawing loud applause from the audience of Brazilian and Chinese dignitaries. “Who was it who decided that the dollar was the currency after the disappearance of the gold standard?” …

… For the remainder of the report:

https://www.ft.com/content/669260a5-82a5-4e7a-9bbf-4f41c54a6143

end

Your weekend reading material

(Alasdair Macleod)

Alasdair Macleod: It’s all hotting up

Submitted by admin on Thu, 2023-04-13 11:32Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, April 13, 2023

Increasing numbers of national governments are abandoning the U.S. sphere of influence. Opportunities from trade with Asia compare favourably with rising currency and banking risks in a dollar-centric world.

Against an imploding banking system in long-established financial markets, China’s renminbi looks like a safe haven. Thanks to a savings-driven economy, China’s consumer price inflation remained very low, when those of the western alliance soared.

Now we face a credit crunch, as banks struggle to reduce their operational gearing, which has become uncomfortably high. Consequently, borrowing rates will be driven higher, taking interest rate control out of central banking hands. Higher interest rates and therefore bond yields due to a credit crunch will escalate the banking crisis, which is only in its early stages.

Consequently, central bank credit will be inflated to prevent the commercial banking network from collapsing and to fund rising government budget deficits. It is the prospect and realisation of these conditions that will lead ultimately to a collapse of fiat currency values, and foreign holders of dollars, euros, and sterling are only beginning to understand the danger. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/its-all-hotting-up?gmrefcode=gata

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

Episode 118

1 day ago

100+ nations to simultaneously pull out of the dollar system? Feat. Andrew Schectman

In this week’s Live from the Vault, Andrew Maguire sits down with the founder of Miles Franklin Investments, Andrew Schectman, to address the exacerbating levels of global financial anxiety, as people flock to gold, seeking alternatives to traditional banking.

The two precious metals informers explore the dynamic expansion of BRICS and SCO nations as they continuously form new relationships, united in a common goal of economic betterment away from the US dollar hegemony.

-END-

.

END

5.IMPORTANT COMMENTARIES ON COMMODITIES:

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

1. YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//,FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 6.8545

OFFSHORE YUAN: 6.8539

SHANGHAI CLOSED UP 19.79 POINTS OR .60%

HANG SENG CLOSED UP 94,33 PTS OR .46%

2. Nikkei closed UP 94,33 PTS OR 0.46%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 100.72 EURO RISES TO 1.1052 UP 0 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.456Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 132.67 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morninG

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.3715***/Italian 10 Yr bond yield RISES to 4.219*** /SPAIN 10 YR BOND YIELD RISES TO 3.409…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.241

3j Gold at $2033.00 silver at: 25.98 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 13 /100 roubles/dollar; ROUBLE AT 81.53//

3m oil into the 82 dollar handle for WTI and 86 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 132.67 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .456% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8891 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9827 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.464 UP 1 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.714 UP 3 BASIS PTS/

USA 2 YR BOND YIELD: 3.9916 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.37…

GREAT BRITAIN/10 YEAR YIELD: UP 0 BASIS PTS AT 3.6180

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Flat As Tumbling Boeing Shares Offset Stellar JPM Earnings

FRIDAY, APR 14, 2023 – 08:07 AM

US stock futures were flat in yet another listless overnight session after Thursday’s bear-vexing rally as traders braced for a slew of earnings from major banks like JPMorgan Chase and Citigroup Inc. Contracts on the S&P 500 dipped 0.1% by 7:45am ET largely as a result of a big drop in Boeing shares, partially offset by solid JPM gains following stellar earnings, while those on the Nasdaq 100 fell by 0.5% after the underlying index added 2% in the last session.

In premarket trading, JPMorgan (JPM) jumps 5.9% after the bank boosted its net interest income forecast for the full year to $81 billion from about $73 billion. This was more than offset by a tumble in Boeing which fell after the aerospace company paused deliveries of some 737 Max jets over a parts issue, about which it was notified by Spirit AeroSystems a day earlier. Analysts said that the news was negative for Boeing and could result in a slowdown of deliveries, as well as impacting the broader sector. Boeing (BA) shares fall as much as 6.4%. Here are the other notable premarket movers:

- Cryptocurrency-exposed stocks gain as the Bitcoin rally gains momentum, with the digital token holding above the $30,000 level amid hopes that the Fed could eventually pause interest-rate hikes.

- Lucid (LCID) fell 6.3% on Friday after the EV maker reported preliminary-vehicle deliveries for the first quarter that missed the average analyst estimate.

- PNC Financial (PNC) rises as much as 8.2% after the firm reported earnings per share for the first quarter that were higher than consensus analyst estimates and reported deposits at end-period for that met the average analyst estimate.

- Rivian Automotive (RIVN) falls 3.5% after Piper Sandler downgraded the EV maker’s stock to neutral from overweight, saying the company’s capital intensive model may discourage investors in the current macro environment.

- A longtime bull on Rivian Automotive Inc. (RIVN) slashed his price target on the stock by three quarters, giving up on the electric-vehicle maker after a 92% wipeout in its shares.

- Tesla (TSLA) shares drop as much as 1.8% after the electric-car maker said it will cut prices for new Model 3 and Model Y vehicles by as much as 5% in Singapore.

- VF Corp. (VFC) gains 5.4% after Goldman Sachs upgrades the apparel and footwear company to buy from sell, saying strategic actions are starting to improve the profitability outlook.

- ViewRay (VRAY) falls as much as 7.1% after a pair of analysts downgrade their ratings on the medical-equipment company following its annual outlook cut and announcement of its plan to explore strategic alternatives. The stock had plunged 39% on Thursday in the biggest drop since August 2019.

- Wells Fargo (WFC) gains 3.1% after the firm reported net interest income and earnings per share for the first quarter that beat the average analyst estimate.

US equities have climbed this week ahead of the lenders’ results as traders assessed a key measure of US inflation, which showed hints of moderating in March, and minutes from the Federal Reserve’s last meeting. Investors will parse earnings statements for signs of an economic slowdown, while gauging how companies have managed to cope with headwinds like the banking system stress and higher rates.

“It’s going to be the outlook that investors are going to be fixated on,” Susannah Streeter, head of money and markets at Hargreaves Lansdown, said on Bloomberg Television. “Since the banking scare erupted, there are so many questions which have now been thrown in to the mix — not least a forecast of a mild recession from the Fed, but also this deposit flight.”

BofA’s Hartnett Prefers Global Stocks to Tech-Heavy US Market Bank of America Corp.’s Michael Hartnett said investors should avoid US stocks as expectations of a recession have become universal, specifically tech amid the backdrop of higher rates. For earnings, he said all lead indicators point to a deeper profit recession than expected

“What I see is that the market is seeing bad news as good news, so any sign of slowdown in the economy is expected to bring down inflation and force central banks to cut rates. That’s the narrative at the moment and hence the positive sentiment,” said Flavio Carpenzano, investment director at Capital Group in London.

“Investors will remain wary of any indication that the regional banking turmoil has translated into materially tighter lending standards throughout the system,” BMO strategists Ian Lyngen and Benjamin Jeffery wrote in a note.

Meanwhile, JPMorgan Chase and Well Fargo kicked off a busy earnings season. JPMorgan jumped about 8% in the premarket after reporting first-quarter deposits unexpectedly rose. Wells Fargo fell about 1% in the premarket after the lender increased provisions for credit losses for commercial real estate loans among others.

European stocks look set to finish the week on the front foot amid speculation that the global monetary tightening cycle is reaching its conclusion. The Stoxx 600 is up 0.4% and on course for a fifth consecutive gain with real estate, healthcare and food & beverages the strongest performing sectors. However, US equity futures are in the red with bank earnings in focus. Here are the most notable European movers:

- Hermes gained as much as 2% to a record after its quarterly sales leaped past estimates on the back of strong global demand, notably in China.

- 888 jumped as much as 17% after the British gambling company reported earnings and gave Middle East revenue guidance ahead of expectations after finishing an internal investigation on money-laundering claims.

- Comet Holding fell as much as 6.4%, the biggest intraday drop since November, after the Swiss tech firm’s 2023 sales guidance came in well below expectations.

- Alstom slid as much as 8.5% after Deutsche Bank downgraded to hold, saying the departure of the French train maker’s CFO brings additional uncertainties regarding financial targets and potential disruption in communications with Moody’s.

- Philips fell as much as 4.5% after the US drug regulator said the number of replacement and remediated devices that have been shipped to consumers in the US as a result of Philips’ sleep apnea device recall is considerably less than number of ‘new replacement devices and repair kits’ listed on the Dutch company’s website.

- National Grid declined as much as 1.5% as in- line results were overshadowed by the introduction of full expensing for capex, per the UK Spring Budget, which points to a broadly neutral cash and economic position for the British utility, according to Jefferies.

- Dechra Pharmaceuticals jumped as much as 40% to 3,882p after as the global veterinary supplies company confirmed talks with Swedish investment firm EQT about a possible all-cash takeover at a price of 4,070p/share.

- Superdry plunged as much as 20%, hitting the lowest since March 2020, as the clothing brand pulled full-year earnings guidance after retail sales for the first two months of the year failed to meet expectations. Additionally, the company said capital raise options were being considered.

Earlier in the session, Asian stocks reached the highest level in almost two months, as a slew of weaker-than-expected US economic data fueled bets that the Federal Reserve may soon pause its interest rate hikes. The MSCI Asia Pacific Index rose as much as 0.6% Friday, lifted by technology and industrial shares. Most markets in the region advanced, with Japanese stocks leading gains after Fast Retailing climbed the most in two years on higher profit guidance. India and Thailand were closed for holidays. A surprise decline in US producer prices and higher-than-expected jobless claims have anchored rate expectations, adding to earlier data that headline consumer prices were slowing. That, along with a retreat in the US dollar, are boding well for emerging market assets in Asia. Singapore’s central bank surprised the market by keeping its monetary policy settings unchanged, joining other central banks in Canada and Australia in pausing monetary tightening given rising global recession risks and ebbing inflation.

The Asian stock benchmark headed for a 1.6% gain this week, as the prospect of a peak in interest rates helped offset worries about the global economic outlook. China’s upbeat trade data also served to bolster investor confidence on the nation’s economic recovery. “Earnings growth for the region as a whole is really going to accelerate into 2024 and the market will start pricing that as we get deeper into the second half,” said Timothy Moe, chief Asia-Pacific equity strategist at Goldman Sachs, in a Bloomberg TV interview. He added that returns in China may be better than the rest of the region given “a much better near-term recovery.”

Japanese stocks were up for a sixth day, as Warren Buffett continues to ramp up excitement in the country’s shares and as weaker-than-expected US economic data boosted expectations of a cooling rate hiking cycle. The Topix Index rose 0.5% to 2,018.72 as of market close Tokyo time, while the Nikkei advanced 1.2% to 28,493.47. Earlier this week, Buffett, the billionaire investor, said he’s mulling a boost to his stock investments in Japan shortly after Berkshire Hathaway Inc. kicked off a yen bond sale. Sony Group Corp. contributed the most to the Topix Index gain, increasing 1.8%. Out of 2,158 stocks in the index, 1,404 rose and 645 fell, while 109 were unchanged. “Buffett’s comments continue to provide considerable tailwind to Japanese stocks, which are undervalued in terms of valuations, and are attracting more attention,” said Ayako Sera, a market strategist at Sumitomo Mitsui Trust Bank.

In Australia, the S&P/ASX 200 index rose 0.5% to close at 7,361.60, its highest level in five weeks, boosted by a rebound in mining shares and banks. The benchmark gained 2% for the week, the third consecutive weekly advance. The rise comes as a gauge of global stocks headed for its highest close in 10 weeks on speculation the Federal Reserve and other central banks are nearing the end of their hiking cycles. In New Zealand, the S&P/NZX 50 index fell 0.4% to 11,880.57.

In FX, a gauge of the dollar extended its descent on Friday, heading for a fifth straight week of losses, its longest losing streak since 2020 on increasing market expectations that the Federal Reserve will cut interest rates later this year. The Swiss Franc hovered around a two-year high and the euro traded at the strongest in one year; the Swedish krona was also among the best G10 performers. The Bloomberg Dollar Spot Index eased 0.1%, helped by continued buying of the euro by macro and overlay funds to top the 12- month high hit in London on Thursday, according to an Asia-based FX trader. The index is down 0.8% this week, marking the longest weekly losing streak since July 2020. “We expect each condition for dollar weakness to fall into place in the weeks ahead,” Kit Juckes, chief FX strategist at Societe Generale wrote in a note

- USD/CHF fell as much as 0.3% to 0.8871, near the 0.8860 two-year low reached on Thursday. The rally on the Swiss franc has propelled it past the pound as the best performing G-10 currency this year

- EUR/USD rose as much as 0.3% to 1.1076, the highest since April 2022

- USD/CAD fell as much as 0.2% to 1.3317, the lowest in a month. o “Our preferred way to express dollar weakness is probably through USD/CAD, because that’s where long USD positioning is most evident,” SocGen’s Juckes wrote

- USD/JPY dropped 0.1% to 132.48; yen is the only G-10 currency to weaken against the dollar this week. USD/JPY two-week implied volatility is signaling that there is a 72% probability spot will trade in a 129.18-135.53 range during this period based off spot trading at 132.57; that means the pair would remain within the trading range it has been in since mid-March

- USD/SEK slipped as much as 0.4% to 10.2366 even as Swedish inflation slowed for the first time in more than a year. The Riksbank has said it expects to raise the key rate from 3% when the executive board gathers on April 25 and Governor Erik Thedeen has said that data published ahead of that meeting would be “more important than ever” for determining its course of action

In rates, treasuries were slightly cheaper from front-end out to intermediates, adding to Thursday’s selloff as stock futures rose after strong JPM earnings. US yields cheaper by up to 1bp across belly. 10-year yields around 3.46%, richer by 2bps vs. Thursday close with gilts lagging by additional 1bp in the sector and bunds trading broadly inline. IG issuance slate empty so far; volumes for the week sit at around $11b vs. projections of $10b to $15b. Three-month dollar Libor +0.14bp at 5.26171%.

In commodities, Crude futures edge up with WTI rising 0.2% to trade near $82.30. Spot gold falls 0.2% to around $2,036. Bitcoin adds 1.6% but has been overshadowed by Ethereum, which has jumped 5.2%.

To the day ahead now, and US data releases include retail sales, industrial production and capacity utilisation for March, along with the University of Michigan’s preliminary consumer sentiment index for April. From central banks, we’ll hear from the Fed’s Waller, the ECB’s Nagel and the BoE’s Tenreyro. Finally, today’s earnings releases will include JPMorgan, Citigroup, Wells Fargo, BlackRock and UnitedHealth.

Market Snapshot

- S&P 500 futures down 0.1% to 4,166.50

- STOXX Europe 600 up 0.4% to 466.10

- MXAP up 0.5% to 163.91

- MXAPJ up 0.5% to 529.15

- Nikkei up 1.2% to 28,493.47

- Topix up 0.5% to 2,018.72

- Hang Seng Index up 0.5% to 20,438.81

- Shanghai Composite up 0.6% to 3,338.15

- Sensex little changed at 60,431.00

- Australia S&P/ASX 200 up 0.5% to 7,361.58

- Kospi up 0.4% to 2,571.49

- German 10Y yield little changed at 2.38%

- Euro up 0.1% to $1.1058

- Brent Futures little changed at $86.12/bbl

- Gold spot down 0.3% to $2,033.91

- US Dollar Index little changed at 100.93

Top Overnight News

- Singapore’s central bank kept its monetary policy settings unchanged after five straight tightening moves since October 2021, joining a growing list of central banks that have opted to pause amid global growth risks and ebbing inflation. BBG

- China approved “provision of lethal aid” to Russia in its war in Ukraine earlier this year and planned to disguise military equipment as civilian items, according to a U.S. intercept of Russian intelligence revealed in leaked secret documents. WaPo

- Sweden’s underlying inflation slowed for the first time in more than a year, raising hopes of a turnaround for the Nordic nation’s households and its central bank, which remains under pressure to raise borrowing costs. BBG

- Hopes for a deal to end some of the rail strikes that have hit UK passengers rose on Friday after train companies made another offer to transport unions. The Rail Delivery Group, which represents train operators, said its latest proposal to the RMT union added “important clarifications and reassurances” around job terms and conditions to its longstanding offer of a 9 per cent pay rise over two years. FT

- The cost of buying insurance against a US government default has shot to its highest level in more than a decade, in an early sign of market concerns about the political impasse in Washington over the debt ceiling. FT

- House Speaker Kevin McCarthy is preparing to unveil next week a plan that would suspend the nation’s debt ceiling for a year in return for spending concessions, according to people familiar with the talks. BBG

- Boeing said on Thursday that a production issue will affect its ability to deliver a “significant” number of 737 Max jets, potentially exacerbating aircraft shortages for airlines around the world. FT

- Russian oil exports in March soared to the highest since April 2020 thanks to surging product flows that returned to levels last seen before Russia invaded Ukraine. IEA

- BlackRock beat consensus with net inflows of $110.32 billion and AUM of $9.09 trillion, which was a decline year on year but topped estimates. The firm’s also been selling off asset-backed securities for Credit Suisse over the last two weeks including at least $300 million of bonds, people familiar said. BBG

- A weakening outlook for corporate spending coupled with emergent concerns about the lending environment represent downside risks to dividends. According to Bloomberg bottom-up consensus forecasts, regional banks and office REITs are expected to contribute less than $1 to S&P 500 DPS in 2023. This would represent just 6 bp of the index-level growth implied by Bloomberg bottom-up forecasts. If these groups were to simply maintain their current dividend policy for the rest of the year, the index would be on track to realize 5% year/year growth.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded with modest and cautious gains with upside momentum somewhat waning in what was a catalyst-light session. ASX 200 was indecisive and moved between gains and losses in early trade, with the heavy outperformance of gold miners cushioning losses for the index. Nikkei 225 outperformed and was propped up by almost all of its sectors at one point in the aftermath of Warren Buffett’s bullish comments on Japanese stocks earlier this week, whilst Fast Retailing shares gained over 8% post-earnings after upping its earnings forecasts. Hang Seng and Shanghai Comp saw mild gains for most of the session, but ranges were contained with traders cautious ahead of next week’s key economic data including GDP, whilst PBoC Governor Yi Gang said he expects China’s 2023 GDP growth at “around 5%” – in line with the government target.

Top Asian News

- PBoC Governor Yi Gang and Fed Chair Powell discussed the economic and financial situations of the US and China on Tuesday, according to Bloomberg.

- PBoC Governor Yi Gang expects China’s 2023 GDP growth at around 5% (in line with the government target), and China’s economy is stabilising and rebounding, according to the statement from the G20 meeting. He said China’s inflation stays at low levels and China’s property market is showing positive changes.

- China’s top banks reportedly plan USD 5.8bln of bond sales to plug the capital hole, according to Bloomberg.

- “The scale of [Chinese] special bond issuance in the second quarter may continue to remain high. If the subsequent economic recovery falls short of expectations”, according to Securities Times.

- BoJ Governor Ueda said the BoJ will maintain current monetary easing; Japan’s core CPI, which is now above 3%, will likely slow back below 2% towards the latter half of this FY. He added they expect wages in Japan to continue rising, based on their view that the global economy will recover, according to Reuters.

- RBNZ Finance Minister Robertson says New Zealand has headroom on the balance sheet with borrowing below 20% of GDP, and the inflation impact from rebuild may be less than feared, according to Reuters.

- BoK Governor Rhee says not worried about a specific USD/KRW rate, according to Reuters.

- The Monetary Authority of Singapore (MAS) maintains the slope, width, and centre of the currency band; and said core inflation is expected to ease materially by end-2023.

- Taiwan’s leading tech companies suffered the biggest drop in revenue in at least a decade last month, according to Nikkei data.

- China’s Commerce Ministry says it is reviewing anti-dumping/anti-subsidy tariff on Australian barley.

European bourses are almost entirely firmer, Euro Stoxx 50 +0.3%, with catalysts ex-earnings lights and the Stoxx 600 on track to see the week out with gains of circa. 1.5%. Earnings from Hermes initially bolstered Consumer Products & Services, though now off best, with Real Estate leading while Energy and Insurance names lag. Stateside, futures are modestly in the red with action tentative ahead of US bank earnings and retail sales thereafter, ES -0.3%. UnitedHealth Group Inc (UNH) Q1 2023 (USD): EPS 6.26 (exp. 6.13), Revenue 91.9bln (exp. 89.78bln) +1.5% in pre-market trade. BlackRock Inc (BLK) Q1 2023 (USD): Adj. EPS 7.93 (exp. 7.76), Revenue 4.24bln (exp. 4.24bln)

Top European News

- ECB’s Kazaks said the risk of recession is non-trivial and rates will need to go up more to tame inflation, according to CNBC. He added the key issue is still very high inflation, and he wouldn’t exclude a 50bps hike in May.

- ECB’s Holzmann said that a 50bps rate hike is in the ballpark for May, according to CNBC.

- ECB’s Nagel said he doesn’t expect a recession, according to Reuters.

- ECB’s Wunsch says ECB could fully stop APP reinvestments this year; market pricing of terminal rate reasonable, but no quick rate cut likely thereafter.

- Spain’s Economy Minister Calviño said GDP at the start of the year has been very strong, according to Reuters.

- German Economy Ministry: Q1 GDP growth likely to have increased slightly QQ, as such a technical recession can be avoided.

- UK Chancellor Hunt said the latest GDP numbers show there’s absolutely no room for complacency. He noted confidence in the resilience of the UK economy among global finance officials, according to Reuters.

- UK Chancellor Hunt to “look at” raising deposit guarantees in wake of SVB collapse after recent turmoil showed banks could fail more rapidly than in the 2008 crisis, according to FT.

FX

- DXY dangling off minor new 2023 low within 101.010-100.780 range ahead of US retail sales, ip, UoM survey and dove/hawk Fed speakers.

- Majors narrowly mixed vs Greenback, but near peaks and big figure levels.

- Yen capped by decent option expiry interest at 132.00, Aussie and Kiwi straddle 100 DMAs at 0.6800 and 0.6302.

- PBoC sets USD/CNY mid-point at 6.8606 vs exp. 6.8614 (prev. 6.8658)

Fixed Income

- USTs flat-line awaiting busy agenda, as 10 year yield holds below 3.5% and T-note drift within 115-20+/114+ range.

- Bunds and Gilts underperform after brief bounces above 135.00 and towards 103.00, as w-t-d lows remain magnetic.

- Modest bounce in the space following Fed’s Bostic (2024 Voter), who said after one more interest rate hike the Fed can pause to assess.

- Berkshire Hathaway (BRK/B) has established the terms of five yen-denominated bonds, amounting to JPY 164.4bln, according to dealwatch.

Commodities

- Once again, a fairly contained session for the commodity space with crude little changed overall and metals just off Thursday’s best in limited newsflow.

- Crude specifically has been slightly choppy but is yet to meaningfully stray for the neutral mark with parameters particularly thin. Amidst this, the complex is on track to see the week out with upside just shy of USD 2.0/bbl.

- Angola expects its oil production to temporarily increase next year on the back of recent private investments, but will remain under 1.5mln BPD (vs current 1.12mln BPD); the budget assumes oil at USD 75/bbl; oil under USD 70/bbl becomes uncomfortable, according to Reuters.

- The Biden admin reportedly approved LNG exports from the proposed Alaska LNG project, according to a document cited by Reuters.

- IEA Monthly Oil Market Report: oil demand is set to increase by 2mln BPD in 2023 to a record of 101.9mln BPD (vs. March view of 101.9mln BPD)

- Chilean mining minister expects the current production slump in the local copper industry to rebound in the coming years; sees no large variation in copper price from Cochilco forecast of USD 3.85/lb this year; dialogue with industry is helping ease concerns, according to Reuters.

- Yellow metal has dipped by around USD 10/oz from the overnight USD 2047oz peak, which is around USD 1/oz shy of the WTD best; base metals firmer, though off best as the USD attempts to recover.

Geopolitics

- North Korean leader Kim guided Thursday’s solid-fuel ICBM test, according to local media KCNA – the new ICBM called Hwasong-18.

- China carried out missile launch drills in the Xinjiang region, according to Chinese state media.

- Russian Defence Ministry says the Pacific Fleet has been put on high alert in a surprise inspection, via Tass.

- US and South Korea are to stage air drills involving US B-52 bomber, according to Yonhap.

US Event Calendar

- 08:30: March Import Price Index YoY, est. -4.0%, prior -1.1%

- 08:30: March Import Price Index MoM, est. -0.1%, prior -0.1%

- 08:30: March Export Price Index YoY, prior -0.8%

- 08:30: March Export Price Index MoM, est. 0%, prior 0.2%

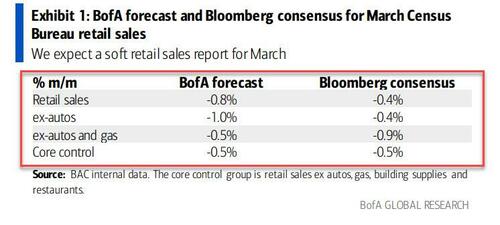

- 08:30: March Retail Sales Control Group, est. -0.5%, prior 0.5%

- 08:30: March Retail Sales Ex Auto and Gas, est. -0.6%, prior 0%

- 08:30: March Retail Sales Ex Auto MoM, est. -0.4%, prior -0.1%

- 08:30: March Retail Sales Advance MoM, est. -0.4%, prior -0.4%

- 09:15: March Industrial Production MoM, est. 0.2%, prior 0%

- 09:15: March Manufacturing (SIC) Production, est. -0.1%, prior 0.1%

- 09:15: March Capacity Utilization, est. 79.1%, prior 78.0%, revised 79.1%

- 10:00: Feb. Business Inventories, est. 0.3%, prior -0.1%

- 10:00: April U. of Mich. Sentiment, est. 62.1, prior 62.0

- 10:00: April U. of Mich. Expectations, est. 58.5, prior 59.2

- 10:00: April U. of Mich. Current Conditions, est. 66.0, prior 66.3

- 10:00: April U. of Mich. 1 Yr Inflation, est. 3.7%, prior 3.6%

- 10:00: April U. of Mich. 5-10 Yr Inflation, est. 2.9%, prior 2.9%

DB’s Henry Allen concludes the overnight wrap

Risk appetite returned to markets over the last 24 hours, aided by some weak US data that supported expectations the Fed might soon call it a day on their rate hikes. In particular, investors welcomed the news that US producer price inflation had surprised on the downside, with both headline and core PPI coming in at their slowest monthly pace since 2020. But even as markets were rallying, concerns about an economic slowdown remained prominent after Wednesday’s Fed minutes showed that the staff were now projecting a mild recession. Those fears then got some added support from other data yesterday, since the weekly initial jobless claims came in above expectations for a third week running.

The problem for many investors right now is that it’s still possible to construct fairly divergent narratives about the economy depending on which series you look at. On the one hand, an array of leading indicators are pointing to a US recession over the coming year, in line with our own House View at DB Research. For instance, yield curves have inverted, temporary jobs are declining, and on previous occasions when the Fed have hiked this fast and this quickly, a recession has followed shortly afterwards. But if you wanted to take the opposite view, you could point to unemployment around its lowest in decades, a high level of vacancies by historic standards, financial markets that have mostly shrugged off the SVB-related turmoil by now, along with growing signs that inflation is softening and the Fed are nearing a pause in their rate hikes.

For the time being at least, investors took hope in the soft PPI release, where the details were more positive for investors relative to the CPI release the previous day. That’s because the PPI reading saw both headline and core surprise on the downside, unlike for the CPI reading where core inflation was still resilient and in line with expectations. For instance, monthly headline PPI came in at -0.5% (vs. 0.0% expected), taking the year-on-year measure down to +2.7% (vs. +3.0% expected). In the meantime, core PPI which excludes food, energy and trade services came in at +0.1% (vs. +0.3% expected), taking the year-on-year measure down to +3.6% (vs. +3.8% expected).

This positive backdrop on the inflation side led to a strong equity performance, and the S&P 500 (+1.33%) posted its biggest advance of April so far with 78% of the index finishing the day higher. Those gains were led by the more rates-sensitive sectors like tech, and the NASDAQ had its best day in nearly a month (+1.99%), whilst the FANG+ index was up +2.44%. At the same time, equity volatility remained subdued as the VIX index (-1.3pts) closed at its lowest level since January 2022, at just 17.80pts, which is striking when you consider how tumultuous markets were only a month earlier. The next thing to look out for will be earnings season now, with several US financials reporting today, including JPMorgan, Citigroup, Wells Fargo and BlackRock.

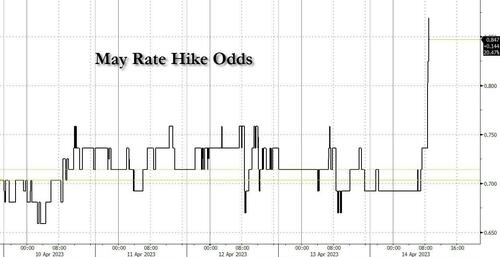

With softer inflation than previously expected, investors moved to slightly dial back how much they expected the Fed to keep hiking. For instance, the chances of a hike at the May meeting have fallen marginally to 69% overnight, having been above 70% for much of the last week. On the other hand, growing bullishness meant that longer-term rates moved a bit higher, and the rate priced in by the December meeting actually rose +2.1bps to 4.34%. In turn, shorter-dated Treasury yields were rather flat on the day, with the 2yr yield closing +1.1bps higher at 3.97%, and the 10yr yield saw a +5.4bps increase to 3.44%.

Another factor driving a modest selloff in shorter-dated US treasuries yesterday was the news that House Republicans were set to release a proposal to suspend the debt ceiling for a year in return for short-term spending concessions. This proposal is just the opening of GOP negotiations with the White House and congressional Democrats, and follows the release of the Biden administration’s budget proposal a few weeks back. The plan, as reported by Bloomberg, would suspend the debt ceiling until May 2024, which would also have political ramifications as it would be just 6 months before the 2024 presidential elections.

Over in Europe, there was also a reasonable dose of optimism, with the Euro itself closing above $1.10 for the first time since April 2022, just over a year ago. And overnight it’s seen a further increase that leaves it at $1.1072 right now. That optimism was echoed among equities, as the STOXX 600 (+0.40%) advanced for a 4th consecutive session to reach its highest level in over a month. This more positive backdrop came amidst growing expectations that the ECB might pursue another 50bp hike at their next meeting in May, rather than stepping down to 25bps like the Fed did earlier this year. Indeed, yesterday saw Belgium’s Wunsch and Slovenia’s Vasle say that the next decision would be between doing 25bps or 50bps, so explicitly opening the door to that option. Then Latvia’s Kazaks said “I don’t see any reason to slow down any time soon in terms of interest-rate increases, because inflation does remain very high”. That comes on the heels of Austria’s Holzmann endorsing a 50bp move the previous day, and yields on 10yr bunds (+0.2bps), OATs (+0.4bps) and BTPs (+0.7bps) all saw a modest increase.

Overnight in Asia, risk assets across the region have been supported by the strong handover from Wall Street overnight. Most of the major equity indices are trading higher, including the Nikkei (+1.07%), the KOSPI (+0.69%), the CSI 300 (+0.39%) and the Shanghai Composite (+0.33%). The only exception is the Hang Seng (-0.00%) which is almost unchanged. However, US stocks futures are struggling to gain traction this morning, with those on the S&P 500 (-0.05%) and NASDAQ 100 (-0.09%) both slightly lower. Another trend overnight has been the continued decline in the US dollar index (-0.20%), which has weakened for a fourth consecutive day and is currently trading close to a one-year low this morning.