April 25/2023 · by harveyorgan · in Uncategorized · Leave a comment·Editi

GOLD PRICE CLOSED: UP $4.90, TO $1994.35

SILVER PRICE CLOSED:DOWN 34 CENTS AT $24.88

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE $1996.00

Silver ACCESS CLOSE: 24.99

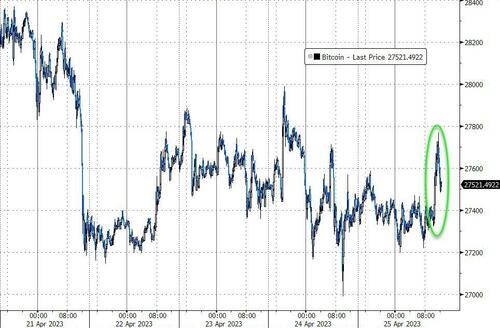

Bitcoin morning price:, $27,332 DOWN 26 Dollars

Bitcoin: afternoon price: $27,532 UP 174 dollars

Platinum price closing $1091.40 DOWN $0.20

Palladium price; $1488.65 DOWN $43.20

We have now entered options expiry week, with the Comex options expiring today April 25/2023 and LBMA/OTC expiring on Friday April 28.2023.

Today was quite a day. Last night, the cartel allowed gold to break $2000.00 only to lower the boom and start the avalanche on options expiry day for the Comex. However the demand for gold is just too strong and this forced the shorts to hurry their covering. The problem huge demand for gold and nobody supplying. A great day for gold today!

QUOTE THE DAY:

ROBERT KENNEDY JR:

@RobertKennedyJr: Fox fires Tucker Carlson five days after he crosses the red line by acknowledging that the TV networks pushed a deadly and ineffective vaccine to please their Pharma advertisers. Carlson’s breathtakingly courageous April 19 monologue broke TV’s two biggest rules: Tucker told the truth about how greedy Pharma advertisers controlled TV news content and he lambasted obsequious newscasters for promoting jabs they knew to be lethal and worthless… Fox just demonstrated the terrifying power of Big Pharma.

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2719.57 UP 35.20 CDN dollars per oz (ALL TIME HIGH 2732.50)

BRITISH GOLD: 1608.26 UP 15.77 pounds per oz//(ALL TIME HIGH//1629.84)

EURO GOLD: 1818.57 UP.14.20 euros per oz //(ALL TIME HIGH//1860.82)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

COMEX DATA EXCHANGE:

COMEX//NOTICES

EXCHANGE: COMEX

CONTRACT: APRIL 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,989.100000000 USD

INTENT DATE: 04/24/2023 DELIVERY DATE: 04/26/2023

FIRM ORG FIRM NAME ISSUED STOPPED

167 C MAREX 1

523 H INTERACTIVE BRO 1

661 C JP MORGAN 5 100

726 C CUNNINGHAM COM 2

737 C ADVANTAGE 6

880 H CITIGROUP 101

905 C ADM 2

991 H CME 10

TOTAL: 114 114

MONTH TO DATE: 23,771

JPMorgan stopped 100/114 contracts

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2023. CONTRACT: 114 NOTICES FOR 11,400 OZ or 0.3546 TONNES

total notices so far: 23,771 contracts for 2,377,100 oz (73.937 tonnes)

SILVER NOTICES: 1 NOTICE(S) FILED FOR 5 OZ/

total number of notices filed so far this month : 386 for 1,930,000 oz

END

GLD

WITH GOLD UP $4.90

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD://////A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD/

INVENTORY RESTS AT 927,43 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 34 CENTS AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 7.304 MILLION OZ OF SILVER FROM THE SLV.//: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV. WHAT A FRAUD..THERE IS NO SILVER AROUND SO HOW DID THESE JERKS GET A HOLD OF 7.304 MILLION OZ/

CLOSING INVENTORY: 471.387 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 778 CONTRACTS TO 156,290 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS GOOD SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.21 GAIN IN SILVER PRICING AT THE COMEX ON MONDAY. WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.21). BUT WERE SUCCESSFUL IN KNOCKING A FEW SPEC LONGS AS WE HAD A TINY LOSS ON OUR TWO EXCHANGES OF 77 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 35.83 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS( 350 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.055 MILLION OZ(FIRST DAY NOTICE)+ THE 35.83 MILLION OZ OF EXCHANGE FOR RISK/+ 1.940 MILLION OZ NORMAL SILVER STANDING FOR APRIL///THUS TOTAL NEW STANDING 37.770 MILLION OZ/ //// V) GOOD SIZED COMEX OI LOSS/ GOOD SIZED EFP ISSUANCE/.

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –352 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL:

TOTAL CONTRACTS for 15 days, total 19,078 contracts: OR 95.390 MILLION OZ . (1192 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 95/390 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE BUT BELOW LAST MONTH

APRIL 95.390 MILLION OZ(SLIGHTLY LESS STRONG THAN LAST MONTH)

RESULT: WE HAD A GOOD SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 778 CONTRACTS DESPITE OUR $0.21 GAIN IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE CONTRACTS: 350 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL OF 1.055 MILLION OZ//FIRST DAY NOTICE// 5,000 OZ E.F.P. JUMP TO LONDON (WHICH DECREASES THE AMOUNT OF SILVER STANDING) + 0 MILLION NEW EXCHANGE FOR RISK TODAY (INCREASES THE AMOUNT OF SILVER STANDING) //NEW EXCHANGE FOR RISK STANDING 35.83 MILLION OZ, THUS TOTAL SILVER OZ STANDING FOR DELIVERY IN APRIL TOTALS 37.770 MILLION .. WE HAVE A TINY SIZED LOSS OF 77 OI CONTRACTS ON THE TWO EXCHANGES

WE HAD 1 NOTICE(S) FILED TODAY FOR 5,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 1044 CONTRACTS TO 473,847 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVE 238 CONTRACTS

WE HAD A SMALL SIZED INCREASE IN COMEX OI ( 1044 CONTRACTS) WITH OUR $9.45 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR APR. AT 66.892 TONNES ON FIRST DAY NOTICE // PLUS A 8,200 OZ QUEUE. JUMP :(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)YET ALL OF..THIS HAPPENED WITH OUR $9.45 GAIN IN PRICE WITH RESPECT TO MONDAY’S TRADING.WE HAD A FAIR SIZED GAIN OF 2,672 OI CONTRACTS (8.311 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1628 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 473,847

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2910 CONTRACTS WITH 1044 CONTRACTS INCREASED AT THE COMEX AND 1628 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2672 CONTRACTS OR 8.311 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1628 CONTRACTS) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (1044 //TOTAL GAIN IN THE TWO EXCHANGES 2,672 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 66.892 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 8200 OZ//NEW STANDING 74.808 TONNES // ///3) ZERO LONG LIQUIDATION//4) SMALL SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 49,048 CONTRACTS OR 4,904,800 OZ OR 152.55 TONNES IN 15 TRADING DAY(S) AND THUS AVERAGING: 3269 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15 TRADING DAY(S) IN TONNES 152.55 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 152.55/3550 x 100% TONNES 4.38% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 152.55 TONNES ( MUCH SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A STRONG SIZED 778 CONTRACTS OI TO 156,290 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 350 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 350 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 350 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 778 CONTRACTS AND ADD TO THE 350 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GOOD SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 428 CONTRACTS.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 2.140 MILLION OZ (EX EXCHANGE FOR RISK)

OCCURRED WITH OUR $0.21 GAIN IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED DOWN 10.54 PTS OR 0.32% //Hang Seng CLOSED DOWN 342.06 POINTS OR 1.71% /The Nikkei closed UP 26.55 PTS OR 0.09% //Australia’s all ordinaries CLOSED DOWN 0.14 % /Chinese yuan (ONSHORE) closed DOWN TO 6.9217/OFFSHORE CHINESE YUAN DOWN TO 6.9343 /Oil UP TO 77.98 dollars per barrel for WTI and BRENT AT 81.92 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 1044 CONTRACTS DOWN TO 473,847 WITH OUR STRONG GAIN IN PRICE OF $9.45 ON MONDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF APRIL… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1628 EFP CONTRACTS WERE ISSUED: : JUNE 1628 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1628 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2672 CONTRACTS IN THAT 1628 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED GAIN OF 1044 COMEX CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $9.45. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: APRIL (74.808) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 74.808 tonnes

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $9.45) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR FAIR SIZED GAIN OF 2,672 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE LOST A TOTAL OI OF 8.311 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL. (66.892 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 8,200 OZ… ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $9.45

WE HAD – REMOVED 238 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 2672 CONTRACTS OR 267200 OZ OR 8.311 TONNES.

Estimated gold comex today 210,978 poor//raid failure

final gold volumes/yesterday 148,834 poor

//APRIL 25/ APRIL 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 353.66 oz 11 kilobars Brinks . |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | 0.Oz |

| No of oz served (contracts) today | 114 notice(s) 11400 OZ 0.3546 TONNES |

| No of oz to be served (notices) | 280 contracts 28000 oz 0.8709 TONNES |

| Total monthly oz gold served (contracts) so far this month | 23,771 notices 2,377,100 OZ 73.937 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

customer withdrawals: 1

i) Out of Brinks: 353.66 oz (11 kilobars)

total withdrawals: 353.66 oz

Adjustments; 1

i) dealer to customer HSBC 482.365 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of APRIL we have an oi of 394 contracts having LOST 24 contracts. We had 106 contracts served ON MONDAY so we GAINED 82 contracts or AN ADDITIONAL 8200 oz will stand at the comex.

May LOST 42 contracts DOWN to 1721.

June LOST 2323 contracts DOWN to 386,408 contracts.

We had 114 contracts filed for today representing 11400 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 5 notices were issued from their client or customer account. The total of all issuance by all participants equate to 114 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 100 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2023. contract month,

we take the total number of notices filed so far for the month (23,771 x 100 oz ), to which we add the difference between the open interest for the front month of (APRIL. 394 CONTRACTS) minus the number of notices served upon today 114 x 100 oz per contract equals 2,405,100 OZ OR 74.808 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month: No of notices filed so far (23,771 x 100 oz)+394x OI for the front month minus the number of notices served upon today (114)x 100 oz} which equals 2,405,100 oz standing OR 74.553 TONNES in this active delivery month of APRIL..

TOTAL COMEX GOLD STANDING: 74.808 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,703,295.912 OZ 52,97 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 23,180,315.395 OZ

TOTAL REGISTERED GOLD: 12,304,855.776 (382.732 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 9,875,429.622 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,601.590 OZ (REG GOLD- PLEDGED GOLD) 329.753 tonnes//

END

SILVER/COMEX

APRIL 25//2023// THE APRIL 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 293,185.600 oz JPmorgan . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 1,122,702.024 oz Delaware Manfra |

| No of oz served today (contracts) | 1 CONTRACT(S) (5,000 OZ) |

| No of oz to be served (notices) | 2 contracts (10,000 oz) |

| Total monthly oz silver served (contracts) | 386 Contracts (1,930,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 2 deposits into the customer account

i)Into Delaware 539,818.000 oz

ii)Into Manfra: 582,884.024 oz

Total deposits: 1,122,702.024 oz

JPMorgan has a total silver weight: 140,781 million oz/272,436 million =51.83% of comex .//dropping fast

Comex withdrawals: 1

i) Out of jPMorgan; 293,185.600 oz

Total withdrawals; 293,185.600 oz

adjustments: 1/dealer to customer/ CNT 49,571.200 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 30.544 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 272.434 million oz

CALCULATION OF SILVER OZ STANDING FOR MAR

silver open interest data:

FRONT MONTH OF APRIL /2023 OI: 3 CONTRACTS HAVING LOST 12 CONTRACT(S). WE HAD 11 NOTICES FILED ON MONDAY SO WE LOST 1 CONTRACTS OR AN ADDITIONAL 5,000 OZ WILL NOT STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF APRIL AS THEY WERE E.F.P.’d TO LONDON.

MAY SAW A LOSS OF 9928 CONTRACTS DOWN TO 34,893

JUNE HAD A 36 CONTRACTS GAIN TO 578

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1 for 5,000 oz

Comex volumes// est. volume today 119,637 huge //raid failure

Comex volume: confirmed yesterday: 90,775 very strong

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 386 x 5,000 oz = 1,930,000 oz

to which we add the difference between the open interest for the front month of APRIL(3) and the number of notices served upon today 1 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL/2023 contract month: 386 (notices served so far) x 5000 oz + OI for the front month of APRIL (3) – number of notices served upon today (1 )x 500 oz of silver standing for the APRIL. contract month equates to 1.940 million oz +/ NEW EXCHANGE FOR RISK TODAY: 0 MILLION OZ //NEW TOTALS EXCHANGE FOR RISK FOR MONTH OF APRIL: 35.83 MILLION OZ// THUS TOTAL SILVER OZ STANDING: 37.770 MILLION OZ//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

APRIL 18/WITH GOLD UP $12.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 925.70 TONNES/

APRIL 17/WITH GOLD DOWN $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 927.72 TONNES

APRIL 14/WITH GOLD DOWN $38.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 930.61 TONNES

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

APRIL 10/WITH GOLD DOWN $21.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91 TONNES

APRIL 6//WITH GOLD DOWN $9.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91

APRIL 5//WITH GOLD UP 0 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04

APRIL 4/WITH GOLD UP $36.30 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

APRIL 3/WITH GOLD UP $14.20 TODAY;NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.02 TONNES

MARCH 31/WITH GOLD DOWN $10.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD////INVENTORY RESTS AT 928.02 TONNES

MARCH 30//WITH GOLD UP XX TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A DEPOSIT OF 2.24 TONNES FROM THE GLD/INVENTORY RESTS AT 929.47 TONNES

MARCH 29/WITH GOLD DOWN $4.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4,16 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 927,23

MARCH 28/WITH GOLD UP $19.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

MARCH 15/THE IDES OF MARCH: WITH GOLD UP $18.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 913.27 TONNES

MARCH 14/WITH GOLD DOWN $4.75 TODAY: HUGE CHANGES: A MONSTER DEPOSIT OF 11.85 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 913.27 TONNES

MARCH 13/WITH GOLD UP $48.85 TODAY: VERY STRANGE HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY REST AT 901.42 TONNES

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

GLD INVENTORY: 927.43 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

APRIL 18/WITH SILVER UP 18 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.757 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 467.023 MILLION OZ

APRIL 17/WITH SILVER DOWN 33 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 469.780 MILLION OZ//

APRIL 14/WITH SILVER DOWN 48 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.974 MILLION OZ/

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 10/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 6/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 4.643 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 468.585 MILLION OZ//

APRIL 5/WITH SILVER DOWN 4 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.942 MILLION OZ

APRIL 4/WITH GOLD UP $1.11 TODAY CRIMINAL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.47 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 463,942 MILLION OZ

APRIL 1/WITH SILVER DOWN 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.412

MARCH 31/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE GLD/: A MASSIVE 4.779 MILLION OZ DEPOSITED INTO THE SLV///INVENTORY RESTS AT465.412 MILLION OZ

MARCH 30/WITH SILVER UP XX CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV.: A DEPOSIT OF 550,000 OZ INTO THE SLV/.INVENTORY RESTS AT 460.633 MILLION OZ

MARCH 29/WITH SILVER UP 11 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 460.082

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

MARCH 17/WITH SILVER UP 79 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE WITHDRAWAL OF 10.478 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 462.748 MILLION OZ//

MARCH 16/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 5.009 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 473.226 MILLION OZ//

MARCH 15/WITH SILVER DOWN 7 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 643,000 OZ INTO THE SLV//INVENTORY RESTS AT 478.235 MILLION OZ/

MARCH 14/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.287 MILLION OZ FROM THE SLV////INVENTORY REST AT 477.592 MILLION OZ//

MARCH 13/WITH SILVER UP $1.35 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ//

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

CLOSING INVENTORY 464.083 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

Peter Schiff: A Higher Debt Ceiling Won’t Solve The Problem; It Will Make The Problem Worse

TUESDAY, APR 25, 2023 – 07:20 AM

In January, the US government ran up against the debt ceiling, kicking off another fake debt ceiling fight. Three months later, Congress still hasn’t agreed on a plan to raise the borrowing limit. Peter Schiff talked about it in his podcast, saying the lack of a higher debt ceiling isn’t the problem; the ever-increasing spending and the debt are the problems. Refusing to raise the ceiling would provide the solution.

In just the first six months of fiscal 2023, the Biden administration ran a $1.1 trillion budget deficit. Excessive spending is pushing the government toward a crisis point when it will no longer be able to finance spending through extraordinary measures. But Republicans in Congress want to attach strings to the new debt ceiling. Democrats want a “clean” bill to raise the spending limit.

Peter zeroed in on a key point in this “fight” – everybody wants to raise the debt ceiling.

It’s not like the Republicans are saying, ‘We’re not going to raise the debt ceiling.’”

Peter ran for Senate in 2010 and a key part of his platform was to stop raising the debt ceiling.

I didn’t want to come up with some gimmick to allow the ceiling to be raised. I wanted it to stop. I wanted to create a permanent ceiling that could never be raised.”

But Democrats (and most Republicans) claim, “We must raise the debt ceiling because we pay our bills!” Peter said it’s the exact opposite.

We never pay our bills. If you pay your bills, you don’t have any debt. Where does the debt come from? It’s unpaid bills. We have $31.7 trillion in debt. That’s $31.7 trillion of bills that we have not paid. We didn’t pay them. We borrowed the money. And we want to keep on borrowing the money. Nobody wants to pay any of these bills.”

This exacerbates the government spending problem. Uncle Sam never has to rein it in as long as he can keep borrowing.

We can keep putting all the spending on a credit card. As long as they raise the debt ceiling, we can continue to not pay our bills.”

Of course, eventually, the borrowing and the accompanying money printing will precipitate a currency crisis.

It’s not about America not wanting to borrow. It’s about the rest of the world not wanting to lend because they know we’re not going to pay them back. And one of the reasons they know that is because we’ve already told them. We are telling them that repeatedly in the debt ceiling battle.”

Meanwhile, the mainstream media spins the debt ceiling as a problem. Peter said the debt ceiling is actually the solution to the problem.

The problem is the debt. The problem is that Congress and the president keep running up more and more debt and every time we get to the ceiling, we either raise it or suspend it. … The problem is that we keep raising the ceiling, not that we won’t raise it. In fact, the threat is that we raise it again.”

The mainstream, along with Democrats, also claim that if Congress doesn’t raise the debt ceiling, the US will default. Peter said that’s the dumbest thing you can say when you’re running a Ponzi scheme, which is what this is.

We are admitting that every time we tell our creditors that if we can’t borrow more money, ‘You’re out of luck, you’re not getting paid.’”

Peter pointed out that the interest on the debt is around $600 billion. The US government collects about $4.6 trillion in tax receipts.

We’ve got plenty of revenue to pay the interest on the national debt if we want to prioritize paying interest on the national debt. But clearly, we don’t want to do that. Not only are we not prioritizing it; we’re telling our bondholders that they’re the low man on the totem pole. We don’t talk about anything else that’s going to not get paid. Nobody is saying, ‘Well if we don’t raise the debt ceiling, we’re going to have to cut back on congressional salaries,’ or, ‘We’re going to have to fire some of our staffers.’ They don’t say, ‘Well if we don’t raise the debt ceiling, we might have to cut Social Security, and we’re going to have to cut defense.’ No! The only thing they talk about cutting is paying interest on the national debt. That tells you where you are as a creditor.”

Ponzi scheme 101 is don’t tell anybody that you’re running a Ponzi scheme.

We’re so dumb; we’re running the world’s biggest Ponzi scheme and we’re telling everybody that it’s a Ponzi scheme.”

And Peter said he thinks the world is starting to wake up. That’s why you’re seeing a move to get out of the dollar.

It’s only a question of time. It’s not a question of if. It’s just a question of when. We will default on our debt. All the bad stuff that they’re saying is going to happen if we don’t raise the debt ceiling is guaranteed to happen because we do raise the debt ceiling.”

Peter said a default could take two forms. We could have an honest default where the government just doesn’t pay back bondholders. Or we could have a dishonest default where we pay with inflation. In that case, they just print money and pay people back with worthless or near-worthless paper.

Those are the only two choices and everybody knows that.”

Peter went on to put the debt into a broader perspective and gave an overview of the history of the debt ceiling.

In this podcast, Peter also talked about money-losing companies going public and how a strong stock market now signals a weak economy.

ernd

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//

END

3,Chris Powell of GATA provides to us very important physical commentaries

Chris’s interview: in preparation for Mining Investment Asia Conference in May

(GATA) GATA secretary interviewed in preparation for Mining Investment Asia conference

GATA secretary interviewed in preparation for Mining Investment Asia conference

Submitted by admin on Mon, 2023-04-24 20:15Section: Daily Dispatches

8:15a CST Tuesday, April 25, 2023

Dear Friend of GATA and Gold:

In preparation for next month’s Mining Investment Asia conference in Sinagpore, at which your secretary/treasurer will be speaking, Spencer Campbell of Southeast Asia Consulting Pte. Ltd. has interviewed me about GATA’s work exposing and opposing manipulation of the gold market. The interview can be found at the consultancy’s internet site here:

https://seasia-consulting.com/gata-gold-anti-trust-action-committee/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Good luck to them trying to get that quantity of gold into Zimbabwe(zerohedge)

Zimbabwe’s digital-currency plan needs $100 million of gold

Submitted by admin on Mon, 2023-04-24 13:03Section: Daily Dispatches

If the digital currency isn’t to be convertible to real metal, this is just another confidence trick.

* * *

By Ray Ndlovu and Godfrey Marawanyika

Bloomberg News

Monday, April24, 2023

Zimbabwe needs $100 million of gold to kick-start its proposed bullion-backed digital currency, as the southern African nation makes another attempt to stabilize its floundering dollar.

The central bank will rely on gold reserves, which it has been accumulating, to support the initiative and stem the local currency’s volatility, according to Persistence Gwanyanya, a member of the central bank’s monetary policy committee.

“Any amount around or less than $100 million will be able to deal with our challenge in a big way,” Gwanyanya said in an interview by phone from the capital, Harare. “We expect the central bank to bring a respectable quantity that can stabilize the Zimbabwe dollar and boost demand.”

Zimbabwe has been struggling to stem a decline in the currency in the nation where the U.S. dollar is the unit of choice. The central bank has been building gold reserves as well as acquiring other precious minerals since the introduction of a policy last year that compels miners to pay part of their royalties in cash and metal. It’s banking on the stash to help it with the latest plan. …

… For the remainder of the report:

end

For your interest…

Fire and rain show California still has plenty of gold to discover

Submitted by admin on Sun, 2023-04-23 23:30 Section: Daily Dispatches

By Hope Sloop

Daily Mail, London

Sunday, April 23, 2023

Recent wildfires and rain have caused a “Gold Rush 2.0” in California’s Central , where some people have located pieces of gold that were unearthed by the natural events.

According to historian Ed Allen of the Marshall Gold Discovery State Park in Coloma, only about 10-15% of California’s gold has been discovered.

Now, nearly 175 years after the first gold rush, groups of eager amateur miners are headed back to “Gold Country” — an area on the western slope of the Sierra Nevada— in search of the remaining 85%.

In an interview with the New York Times, Albert Fausel showed off the gold he located in a creek in Placerville after just 20 minutes of searching.

“Woooo-hoo-hoooo!” the man said of his find — a piece of gold just big enough to pinch between your fingers that is worth around $100.

The hunt is on for anyone looking for nuggets of the pricey metal. In 1850 a nugget of gold went for $20 an ounce. Today an ounce will fetch you around $1,900. …

… For the remainder of the report:

end

The author is perfectly correct: In this environment why on earth would gold miners hedge?

(Elouise Fowler)

Elouise Fowler: Why investors are sick of gold miners hedging

Submitted by admin on Sun, 2023-04-23 10:27Section: Daily Dispatches

By Elouise Fowler

Australian Financial Review, Sydney

Sunday, April 23, 2023

China, Russia, and Turkey bought vast amounts of gold via their central banks over the past year to bolster their foreign exchange reserves and diversify against the world’s most popular currency, the U.S. dollar.

Demand for gold jewellery in China has rebounded since lockdowns ended there. And fearful investors seeking safety from the global banking crisis have pumped money into physical gold exchange-traded funds, lifting ETF inflows in March for the first time in 10 months.

These drivers all suggest demand for gold will remain strong, says David Franklyn, managing partner of Perth-based fund Argonaut Resources.

“If you take a long-term view, the world is changing. I reckon we’ve entered an era of increased political risks,” Franklyn tells The Australian Financial Review. “So I think gold — as a store of value and as a hedge against uncertainty — is coming back.”

If Franklyn is right, why would gold miners choose to lock in prices with multi-year hedging agreements? It’s a temptation that other fund managers, such as David Baker, the managing partner of Baker Steel, urge them to resist.

Gold has rallied 10% this year and soft U.S. economic data pushed the gold price to $US2002 (A$2,991) an ounce on Friday, close to its one-year high.

Investors, fuelled by their conviction that the rally has further to run as tumult ripples through global markets, are seeking clean exposure to the precious metal, unencumbered by hedges struck when the gold price was lower.

“What I look for is companies that have zero or moderate levels of hedging, because we’re looking for pure gold exposure,” says Franklyn, who established a gold fund in November because he thought the sector was undervalued. …

… For the remainder of the analysis:

https://www.afr.com/companies/mining/why-investors-are-sick-of-gold-miners-hedging-20230418-p5d1dj

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

END

5.IMPORTANT COMMENTARIES ON COMMODITIES: LITHIUM

end

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

1.YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//,TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 6.9217

OFFSHORE YUAN: 6.9343

SHANGHAI CLOSED DOWN 10.54 POINTS OR 0.32%

HANG SENG CLOSED DOWN 342.06 PTS OR 1.71%

2. Nikkei closed UP 26.55 PTS OR 0.09%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 101.33 EURO FALLS TO 1.1016 UP 42 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.473Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 134.21 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.4610***/Italian 10 Yr bond yield RISES to 4.348*** /SPAIN 10 YR BOND YIELD FALLS TO 3.498…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.228

3j Gold at $1978.25 silver at: 24.54 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 29 /100 roubles/dollar; ROUBLE AT 81.62//

3m oil into the 77 dollar handle for WTI and 81 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 134.21 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .473% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8884 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9787 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.493 DOWN 7 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.679 DOWN 5 BASIS PTS/

USA 2 YR BOND YIELD: 4.059 DOWN 9 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.43…

GREAT BRITAIN/10 YEAR YIELD: DOWN 3 BASIS PTS AT 3.7800

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Slide Ahead Of Mega Tech Earnings

TUESDAY, APR 25, 2023 – 08:06 AM

US equity futures fell on Tuesday, as investors braced for the first earnings from the megatech giant “generals”, which incidentally are mostly lower premarket; bond yields are 3-5bp higher and the USD is higher.

Contracts on the S&P 500 and Nasdaq 100 both fell 0.5% in New York as of 7:45 a.m. after Wall Street benchmarks ended Monday’s session broadly unchanged. Commodities are mixed with weaker oil after several days of gains. Yesterday, FRC reported after the bell with deposits declining 41% QoQ vs. -9% survey; stock is down 21% after close. Today, the focal point will be GOOGL and MSFT’s earnings after-market: investors will look for cost outlook and revenue growth. GOOGL closed +0.5% yday and +20.1% YTD; the implied move is 4.6%; MSFT closed -1.4% yday and up 17.5% YTD pre-market; the implied move is 3.3%. Further, keep an eye on the April Conference Board Consumer Confidence and Richmond Fed survey data.

In premarket trading, Alphabet and Microsoft are slightly lower ahead of their results after the market close today. Weighing on the sentiment were shares of US regional lenders, which dropped as much as 22% in premarket trading, after peer First Republic reported a slump in deposits that was worse than expected, sparking worries that the bank is still contending with challenges. Other US regional lenders fall too: PacWest Bancorp -2.2%, Western Alliance Bancorp -2.5%. Other results were mixed, with General Motors Co. and PepsiCo Inc. gaining after beats, while United Parcel Service Inc. sank as guidance disappointed. Here are some other premarket movers:

- Chinese stocks listed in the US fall, setting the Nasdaq Golden Dragon China Index up for its longest streak of losses in a year as geopolitical tensions dent risk appetite. Alibaba (BABA US) falls 1.4%, Baidu (BIDU US) -2.4%.

- Luminar Technologies rises as much as 5.9% as Jefferies initiated the company with a buy rating, saying it is best positioned to capture a dominant share of the nascent lidar market.

The first tech giant results due today will move markets: so far in 2023 the Nasdaq 100 has strongly outperformed the broader US market, rising about 19%, while the S&P 500 and the Dow Jones have added only 7.8% and 2.2% respectively. The tech-heavy index has posted the best start of the year since 2012 as investors bet that softer economic growth will lead the Federal Reserve to soften its hawkish stance.

Meanwhile, an earnings recession looms: profits for information technology companies in the S&P 500 are projected to fall 15% in the first quarter, which would be the biggest contraction year-over-year since 2009, according to data compiled by Bloomberg Intelligence. The largest tech-related companies have been the biggest contributors to the the S&P 500’s advance this year, by virtue of their size and outperformance. Apple, Microsoft and Nvidia alone account for nearly half of the index’s gains, according to data compiled by Bloomberg.

“What will be crucial for the outlook in tech is the rate expectations, and currently the market is pricing in swift cuts by the Fed for the second half of this year, which we do not agree with,” Ann-Katrin Petersen, a senior investment strategist at BlackRock Investment Institute, said on Bloomberg TV. “This sector is very rate-sensitive, so it might have digest this potential for a reversal in Fed rate expectations for the second half of this year.”

“Markets seem to be convincingly anticipating that there will be no recession, that inflation will fall and that at the same time, the Fed and the ECB could lower rates,” said Frederic Rollin, senior investment adviser at Pictet Asset Management. “We’re not saying it’s impossible but that would be the best outcome possible.”

In the run-up to the Fed’s May 3 decision, investors are looking to figures on economic growth and consumer spending that will help determine the pace of the Fed’s rate increases this year. Economists expect Thursday’s GDP data to show US economic output decelerated to 2% annual growth in the first three months of 2023 from 2.6% in the fourth quarter.

Citigroup strategists led by Beata Manthey said that even if the European GDP outpaces that of the US, European equities and earnings will come under pressure as the region’s profits are more cyclical relative to American peers. Citi strategists prefer the US stock market over Europe as the US tends to perform more defensively than other markets during EPS slowdowns

In Europe, bank stocks are leading the broader market lower after updates from UBS and Santander prompted sharp declines in their share prices. The Stoxx 600 is down 0.5% and on course for its largest one-day drop in a month. European banks dropped after Banco Santander and UBS reported 1Q earnings that failed to impress analysts, at the start of a busy week for the region’s banks. The Stoxx 600 Banks Index was 2% lower, second- worst performing sector in Europe, while the Financial Services Index, in which UBS trades, was 1.2% lower. Banco Santander declined 4% as analysts note earnings beat was driven by trading, while deposit outflows in Spain were steeper and interest income missed in a few regions. Here are the most notable European movers:

- Novartis gains as much as 2.7%, reaching a two-month high, after reporting 1Q results that Citi said were solid, with sales for new prostate cancer drug Pluvicto beating estimates

- ABB climb as much as 3.9% after it reported beats across the board according to Citi, as the Swiss engineering and automation company increased its revenue guidance for the year

- Vodafone shares rise as much as 2.7% after its biggest shareholder Emirates Telecom initiated discussions with the UK carrier around non-executive board composition

- Kuehne + Nagel rises as much as 6% after it posted a beat driven by sea logistics division, analysts said, who also flagged some economic challenges looming for the logistics giant

- Whitbread shares rise as much as 5%, climbing to the highest since November 2021, after the hotel and restaurant group reported full-year adjusted pretax profit that beat consensus

- Wartsila gains as much as 6.9% after the power plant services company reported first-quarter results, with analysts highlighting the good order intake as the main positive

- UBS falls as much as 5.4% after reporting earnings that disappointed analysts who pointed to the possibility of consensus cuts on the back of weak net interest income guidance

- Banco Santander slides as much as 4.6% as analysts say the Spanish lender’s first- quarter earnings beat was offset by steeper deposit outflows in Spain and a net interest income miss. The wider European banking sector is the worst-performing Stoxx 600 subindex after UBS and Santander’s 1Q misses kick off a busy week for the region’s banks

- Associated British Foods shares drop as much as 7% after the food processing and retailing company reported interim adjusted operating profit that missed estimates

Earlier in the session, Asian stocks declined for a third day as investors continued to sell Chinese shares on economic and geopolitical risks. The MSCI Asia Pacific Index declined as much as 0.8% Tuesday, with Tencent and Alibaba among the biggest drags. Key indexes of Hong Kong-listed stocks fell by more than 1.7% as top leaders highlighted risks to China’s economy and as Beijing’s relations with the US remained strained.

“Given geopolitical tensions, people are unsure about the long term and impatient to ‘buy and wait,’” Bank of America strategists including Winnie Wu wrote in a note dated Monday. “Investors discount the good data for ‘low base’ for being ‘unsustainable,’” as bottom-up corporate earnings and guidance remain soft, they added. Stocks also declined in South Korea and Taiwan, while equity benchmarks in Japan advanced. Australia, New Zealand and Indonesia were closed for holidays. The MSCI Asia gauge is down 1.4% so far in April, while its 90-day historical volatility has slumped to the lowest in more than one year. This week will be the busiest of the current Asian earnings season, with more than 800 firms in the MSCI Asia gauge scheduled to report, giving investors fodder for portfolio picks as they await the next Federal Reserve policy decision in early May.

Japanese stocks gained as better-than-expected earnings from major companies including Nidec boosted optimism. The Topix rose 0.2% to close at 2,042.15, while the Nikkei advanced 0.1% to 28,620.07. Mitsubishi Electric contributed the most to the Topix gain, increasing 3.3% on a plan to spin off its auto business. Out of 2,158 stocks in the index, 1,236 rose and 792 fell, while 130 were unchanged. “Nidec earnings were better than expected and associative buying is also taking place for other stocks” said Shingo Ide, chief equity strategist at NLI Research Institute

Amid the risk-off mood, investors favored perceived safe-haven assets with Treasuries on the front foot and US 10-year yields down 5bps at 3.44%, while the Japanese yen and Swiss franc sit atop the G-10 intraday rankings.

In rates, treasuries rise with gains led by belly of the curve, extending 5s30s spread through Monday’s range. Bid has support from risk-aversion as earnings reports roll in. US yields richer by 3bp-5.5bp across the curve with belly-led gains steepening 5s30s spread by ~1.5bp on the day; 10-year yields around 3.44%, richer by ~5bp vs Monday’s close with bunds slightly outperforming and gilts lagging by 1.5bp in the sector. Auction cycle comprises $42b 2-year note sale at 1pm and 5-year and 7-year sales Wednesday and Thursday. WI 2-year yield at 4.00% is ~4.5bp cheaper than March result, a 2.7bp tail. Focal points of US session include housing data, while final auction cycle of the February-April financing quarter begins with 2-year note sale. European bonds have also benefited, with 10-year borrowing costs falling by 6bps in Germany and 4bps in the UK.

Markets are now pricing the peak for US interest rates in June, and then a decline to end the year below 4.5%. The small shifts in Fed projections underscore the lack of direction at the start of a busy week for economic data and corporate earnings. Data published Monday showed US manufacturing data was weaker than economists forecast, while uncertainty over the debt ceiling persisted. Later this week, US GDP data is forecast to reveal slower growth, and the so-called core PCE deflator, the Fed’s preferred inflation gauge, is expected to show price growth cooled.

“The data justifies a 25 basis-point hike,” said Erick Muller, head of product and investment strategy at Muzinich & Co. in London. “But it’s going to be difficult for central banks to raise rates and then quickly within a few months to start reversing that.”

In FX, the Bloomberg Dollar Spot Index is up 0.2%; the Japanese yen and Swiss franc outperformed Group-of-10 peers. Large flows went through at the 8am London fix in EUR/JPY and EUR/CHF as European stocks fell at the open. The Australian dollar and Norway’s krone are the weakest.

In commodities, crude futures edge lower with WTI falling 0.3% to trade near $78.50. Spot gold is flat around $1,990.

Bitcoin is flat; Coinbase filed a petition to push the SEC to create new rules on crypto, according to Reuters.

To the day ahead now, and data releases from the US include the Conference Board’s consumer confidence for April, new home sales for March, and the FHFA house price index for February. Otherwise, we’ll hear from BoE Deputy Governor Broadbent. Finally, earnings releases include Microsoft, Alphabet, Visa, General Electric, General Motors, Pepsi and McDonald’s.

Market Snapshot

- S&P 500 futures down 0.5% to 4,140

- STOXX Europe 600 down 0.5% to 466.76

- MXAP down 0.6% to 159.78

- MXAPJ down 1.2% to 510.13

- Nikkei little changed at 28,620.07

- Topix up 0.2% to 2,042.15

- Hang Seng Index down 1.7% to 19,617.88

- Shanghai Composite down 0.3% to 3,264.87

- Sensex little changed at 60,097.44

- Australia S&P/ASX 200 down 0.1% to 7,321.99

- Kospi down 1.4% to 2,489.02

- German 10Y yield little changed at 2.45%

- Euro down 0.2% to $1.1029

- Brent Futures up 0.2% to $82.89/bbl

- Gold spot up 0.1% to $1,990.30

- U.S. Dollar Index up 0.13% to 101.48

Top Overnight News from Bloomberg

- China’s upcoming politburo meeting likely to shift the focus away from COVID stimulus and toward policies to ensure the economic recovery can be sustained. BBG

- The world’s car industry will shrink to only 10 companies over the coming decade, a Chinese rival to Elon Musk’s Tesla has said, as intense competition in China’s electric vehicle market spills on to the global stage. Brian Gu, vice-chair of Guangzhou-headquartered Xpeng, said for Chinese companies to be among the last carmakers standing, they would need to have annual sales of at least 3mn vehicles, underpinned by global exports. The world’s largest carmaker Toyota sold 10.5mn cars in 2022, while Tesla sold 1.3mn. FT

- The EU and Japan have pushed back against a US proposal for G7 countries to ban all exports to Russia, as part of negotiations ahead of a summit of the world’s most advanced economies. FT

- The world’s top central banks are cutting the frequency of their dollar liquidity operations with the U.S. Federal Reserve from May, sending the clearest signal yet that last month’s financial market volatility is essentially over. Central banks of the euro zone, Japan, Britain and Switzerland will now revert to their usual weekly tenders, indicating that the extraordinary backstop is no longer needed as markets are functioning as intended. RTRS

- UBS pulled in $28 billion from rich clients in the first quarter. Net new money at the wealth unit included $7 billion in the 10 days after its takeover of Credit Suisse. Profit missed as UBS set aside $665 million for litigation tied to its role in selling mortgage securities before the GFC. The bank said geopolitics and liquidity concerns are depressing client activity and may affect new money in coming months. Shares fell. BBG

- House Republican leaders insist they won’t change their debt ceiling bill to win over holdouts, but they may not have the necessary votes without some tweaks. Politico

- The next big debt ceiling events will be whether McCarthy can pass his blueprint this week (reports suggest it will be VERY close, and there may need to be revisions) while the Treasury will publish a new timeline for the “X date” in the next 1-2 weeks. BBG

- Trump will learn his fate in Georgia over the summer (between Jul 11 and Sept 1) as that’s when the DA said she will decide whether to press charges. NYT

- President Biden formally launched his reelection campaign with a video announcement Tuesday, a long-awaited declaration that puts him on the path to a potential rematch with the man he beat in 2020—former President Donald Trump. WSJ

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly lower after the mixed performance in the US where sentiment was clouded by a disappointing Dallas Fed Manufacturing survey and the tech sector was among the laggards ahead of the upcoming big tech earnings, with the mood in the Asia-Pac region also contained amid the closures in Australia and New Zealand for ANZAC Day. Nikkei 225 was positive amid softer Services PPI data and after the government raised its view on imports for the first time since July last year, while BoJ Governor Ueda repeated that the BoJ sees it appropriate to maintain YCC and easy monetary policy given the current economic, price and financial developments. KOSPI failed to hold on to early gains after South Korean GDP printed mixed but still showed the economy averted a recession. Hang Seng and Shanghai Comp weakened with Hong Kong pressured by underperformance in tech and after the local benchmark slipped beneath the 20k level, although losses in the mainland were stemmed following another firm PBoC liquidity injection and reports that China urged banks to cut deposit rates.

Top Asian News

- China’s Politburo is likely to shift focus from stimulus to reforms when top leaders meet which could take place this week as China’s economic recovery is well on track, according to Bloomberg.

- China’s Commerce Minister met with the European Commission EVP in Brussels and the sides exchanged views on topics including expanding trade and investment cooperation, according to MOFCOM.

- BoJ Governor Ueda said the BoJ sees it appropriate to maintain YCC and easy monetary policy given the current economic, price and financial developments, while he also said that Japan’s bond yield curve is currently smooth as a whole. Ueda said tightening monetary policy now could push down inflation in the future which is already likely to slow on dissipating effect of import costs and noted that if they see the risk of runaway inflation, they must normalise monetary policy but added that they see the risk of inflation undershooting forecast as a bigger risk than overshooting which is why the BoJ must maintain easy policy for now.

- China’s Foreign Ministry announced that airline companies will no longer check COVID-19 nucleic acid test results of passengers to China before boarding from April 29th, via Global Times.

European bourses are under pressure, Euro Stoxx 50 -0.6%, continuing the downbeat APAC tone with drivers light ex-earnings; SMI +0.2% outperforms after heavyweights Nestle, Novartis and ABB. Sectors are similarly pressured with Banks hit by UBS and Santander. US futures are lower, ES -0.4%, with attention almost exclusively on earnings. Note, Biden has as expected kicked off his re-election campaign. First Republic Bank (FRC) Q1 2023 (USD): EPS 1.23 (exp. 0.72), Revenue 1.2bln (exp. 1.22bln); Deposits 104.47bln (exp. 136.67bln), down 1.7% from March 31st. Cutting workforce by about 20-25% in Q2. -19.5% in pre-market trade. Nestle (NESN SW) – Q1 (CHF): Revenue 23.47bln (exp. 23.82bln), Organic Revenue +9.3% (exp. +7.25%). Confirms FY outlook for organic growth of 6-8%. +1.3% in European trade

Top European News

- BoE, BoJ, ECB and SNB in consultation with the Fed have decided to revert the frequency of their 7-day operations from daily to once per week, effective 1st May. Decision taken in view of the improvements in USD funding conditions and low demand at recent USD liquidity providing operations.

- ECB’s Lane said current data suggests that they have to raise interest rates again at the upcoming meeting, while he added that beyond the May 4th meeting, further rate hikes will depend on data, according to Reuters.

- German Finance Minister Lindner said they need to strengthen EU fiscal rules, not dilute them, and they are in discussions on the future design of the common European fiscal framework, according to FT.

- EU tweaked patent rules to make it easier for patent holders to seek injunctions, according to the latest draft rules cited by Reuters.

- German Chancellor Scholz to meet with Chinese leadership in Berlin on 20th June.

FX

- Initial cagey and contained trade has picked up slightly throughout the European morning, with the dollar index at the mid-point of 101.19-10151 parameters and dipping within this slightly as JPY advances.

- JPY is the relative outperformer irrespective of dovish Ueda commentary as UST yields dip and the US yield curve flattens, USD/JPY below 134.00 from initial 134.47 best.

- At the other end of the spectrum AUD has come under renewed pressure as base metals flounder further in holiday thinned conditions for ANZAC day, with further declines in AUD/NZD cross evidence of the Aussies recent underperformance and ahead of Q1 CPI.

- EUR and GBP continue to drift but remain above 1.10 and 1.245 respectively with specific drivers limited aside from Central Bank commentary that hasn’t fundamentally altered the narrative.

- PBoC set USD/CNY mid-point at 6.8847 vs exp. 6.8853 (prev. 6.8835)

Fixed Income

- Bonds remain bid after extending rebounds from Monday to 134.40, 101.40 and 115-15 for Bunds, Gilts and the T-note respectively.

- German 2 year supply reasonably well received in contrast to recent sales and ahead of the USD 42bln auction.

- USTs experienced a modest boost back towards earlier highs following a 10k five year block trade at 109.27+, with the US five year yield the incremental domestic laggard following this.

- UK DMO revises the 2023/24 Gilt issuance remit to GBP 237.8bln (prev. 241.1bln)

Commodities

- WTI and Brent futures are choppy but have been ultimately horizontal above USD 78.50 and USD 82.50/bbl respectively since around the settlement yesterday before some modest downside in recent trade.

- Spot gold remains sub-USD 2,000/oz and attempted to top the level before the Chinese cash opened last night.

- Industrial metals are lower across the board as the greenback and soured risk tone pressure the complex

- China March YTD gold output rose 1.9% Y/Y to 84.97 tonnes and gold consumption rose 12.0% Y/Y to 291.58 tonnes.

- Russian Deputy Energy Minister says volatility and uncertainty on global energy markets will increase due to underinvestment, hope to share some results of the new energy strategy in the next few months.

Geopolitics

- Russia may withdraw from the treaty banning intermediate and shorter-range nuclear missiles, according to a foreign ministry official cited by TASS.

- Russian Foreign Ministry’s head of nuclear non-proliferation Yeramakov said the risks of a direct military confrontation between the two nuclear powers, Russia and the US, are increasing with Washington escalating the risks through its conduct, according to TASS.

- EU and Japan pushed back against a US proposal for the G7 to ban all exports to Russia, according to FT.

- UK Foreign Minister Cleverly is to call for constructive ties with China in his Mansion House speech on Tuesday, according to FT. However, The Telegraph reported that Cleverly is to also say that China must come clean on the ‘biggest military build-up in peacetime’ and is to warn of the danger of ‘tragic miscalculation’ if Beijing’s aggression continues.

- Egyptian Foreign Ministry announced the killing of the assistant administrative attaché at the Egyptian embassy in Khartoum, Sudan, according to Sky News Arabia.

- Deputy Chairman of the Russian Security Council, said “our competitors should not underestimate the possibility of our use of nuclear weapons”, via Al Jazeera.

US Event Calendar

- 09:00: Feb. S&P/Case-Shiller US HPI YoY, prior 3.79%

- 09:00: Feb. S&P/CS 20 City MoM SA, est. -0.35%, prior -0.43%

- 10:00: April Conf. Board Consumer Confidenc, est. 104.0, prior 104.2

- 10:00: April Conf. Board Expectations, prior 73.0

- 10:00: April Conf. Board Present Situation, prior 151.1

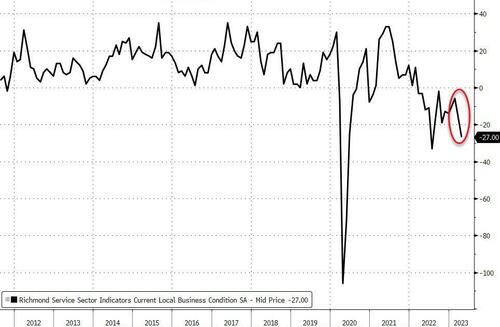

- 10:00: April Richmond Fed Business Conditio, prior -17

- 10:00: April Richmond Fed Index, est. -8, prior -5

- 10:00: March New Home Sales MoM, est. -1.2%, prior 1.1%

- 10:00: March New Home Sales, est. 632,000, prior 640,000

- 10:30: April Dallas Fed Services Activity, prior -18.0

DB’s Jim Reid concludes the overnight wrap

Whilst it might be an eventful week coming up ahead, so far it hasn’t got off to a particularly exciting start, with the last 24 hours seeing a broadly risk-off tone as investors looked forward to a raft of earnings releases that will start coming through today. That left yields on 10yr Treasuries down -8.2bps by the end of the session, and this morning they’ve shed a further -1.5bps, taking them down to 3.48%. Otherwise, the S&P 500 experienced a modest +0.09% gain, but elsewhere the picture has been more downbeat, with Chinese equities losing ground for a 5th consecutive session this morning, whilst the major European indices also experienced a modest pullback.

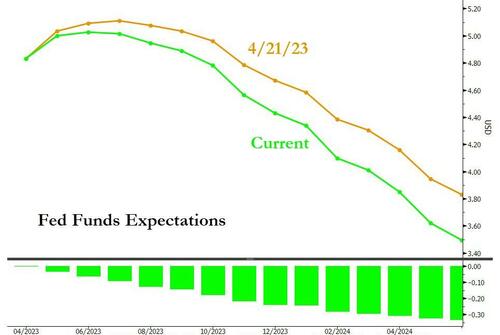

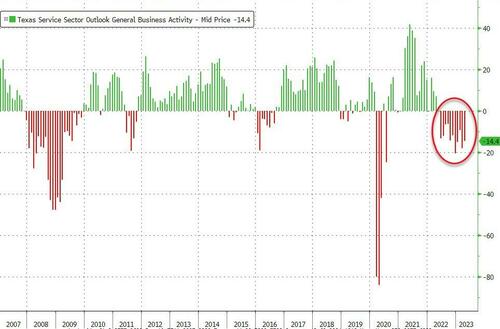

One factor that’s spurred the latest moves have been continued concern among investors about a US recession. In part that was down to fresh data out yesterday, with the Dallas Fed’s manufacturing outlook survey ticking down to a 9-month low of -23.4 (vs. -12.0 expected). But another reason were fears about the upcoming debt ceiling deadline that’s likely to arrive in the summer. Indeed, at one point yesterday the gap between the 1m Treasury yield and the 3m Treasury yield was on track to close at its highest level in available data on Bloomberg back to 2001, although it then tightened and is currently at 151bps this morning. Even with the tightening though, those sort of levels are still far steeper than normal for the 1m3m curve, and it speaks to the concern in markets about a potential issue occurring between one and three months’ time, which coincides with potential debt ceiling deadlines.

Speaking of the debt ceiling, DB’s US rates strategist Steven Zeng put out an update on the issue yesterday (link here). His view is that the most likely x-date remains in August in light of April’s tax receipts so far, but there are stressed scenarios that could bring the date forward to late-July. In terms of what to look out for next, Republican House Speaker McCarthy said after the US close that the House will vote on the Republican plan at some point this week. Bloomberg reported last night that he’s still short of the votes to pass it given the very slim Republican majority in the House, but the bill is expected to go to the Rules Committee later today which starts the process of bringing it to a vote. Even if it passed the House, the bill isn’t going to get through the Democratic-controlled Senate, but the idea is that McCarthy can demonstrate to Democrats what the Republicans are willing to get behind, as part of an opening move in any potential negotiation.

With growing fears in markets about the debt ceiling, investors brought forward the likelihood of rate cuts from the Fed over the months ahead. Looking at Fed funds futures, the rate priced in by the December meeting came down by -9.2bps yesterday to 4.49%, which is its lowest expected level in just over a week. Even so, there’s still a high degree of confidence that the Fed will proceed with another hike at their next meeting a week tomorrow, with futures pricing in an 88% chance of a move this morning. The various shifts in expectations helped Treasury yields to move lower across the curve, with those on 2yr yields down -9.3bps to 4.09%, and those on 10yr yields down -8.2bps to 3.49%.