April 26/2023 · by harveyorgan · in Uncategorized · Leave a comment·Editi

GOLD PRICE CLOSED: DOWN $8.45 TO $1985.90

SILVER PRICE CLOSED:DOWN 10 CENTS AT $24.78

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE $1989.15

Silver ACCESS CLOSE: 24.89

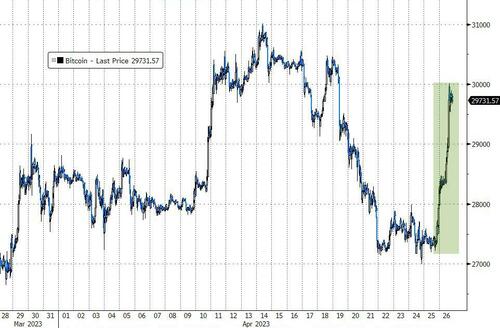

Bitcoin morning price:, $28,317 UP 785 Dollars

Bitcoin: afternoon price: $27,884 UP 352 dollars

Platinum price closing $1092.60 UP $1.20

Palladium price; $1525.60 UP $36.95

We have now entered options expiry week, with the Comex options expired April 25/2023 and LBMA/OTC expiring on Friday April 28.2023. The crooks can only whack once London is put to bed as they fear that many are demanding physical delivery against their short sales. Their attention span is less than one day. They will worry about physical deliveries tomorrow

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2712.80 DOWN 7.50 CDN dollars per oz (ALL TIME HIGH 2732.50)

BRITISH GOLD: 1595.50 DOWN 15.66 pounds per oz//(ALL TIME HIGH//1629.84)

EURO GOLD: 1801,40 DOWN 17.80 euros per oz //(ALL TIME HIGH//1860.82)

DONATE

EXCHANGE: COMEX

CONTRACT: APRIL 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,994.000000000 USD

INTENT DATE: 04/25/2023 DELIVERY DATE: 04/27/2023

FIRM ORG FIRM NAME ISSUED STOPPED

167 C MAREX 1

523 H INTERACTIVE BRO 1

661 C JP MORGAN 150

737 C ADVANTAGE 3 3

905 C ADM 3

991 H CME 147

TOTAL: 154 154

MONTH TO DATE: 23,925

JPMorgan stopped 0/154 contracts

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2023. CONTRACT: 154 NOTICES FOR 15,400 OZ or 0.4790 TONNES

total notices so far: 23,925 contracts for 2,392,500 oz (74.416 tonnes)

SILVER NOTICES: 2 NOTICE(S) FILED FOR 10,000 OZ/

total number of notices filed so far this month : 388 for 1,940,000 oz

END

GLD

WITH GOLD DOWN $8.45

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD://////A DEPOSIT OF 2.61 TONNES OF GOLD INTO THE GLD/

INVENTORY RESTS AT 930.04 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 10 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWL OF 1.102 MILLION OZ OF SILVER FROM THE SLV.//: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 470.285 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUMONGOUS SIZED 6500 CONTRACTS TO 149,693 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS GOOD SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.34 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.34). AND WERE SUCCESSFUL IN KNOCKING A FEW SPEC LONGS AS WE HAD A HUGE LOSS ON OUR TWO EXCHANGES OF 5398 CONTRACTS WITH SOME OF THAT LOSS DUE TO INITIATION OF SPREADER LIQUIDATION IN THE SILVER ARENA.. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 35.83 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS( 1102 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.055 MILLION OZ(FIRST DAY NOTICE)+ THE 35.83 MILLION OZ OF EXCHANGE FOR RISK/+ 1.940 MILLION OZ NORMAL SILVER STANDING FOR APRIL///THUS TOTAL NEW STANDING 37.770 MILLION OZ/ //// V) GIGANTIC SIZED COMEX OI LOSS/ HUGE SIZED EFP ISSUANCE/.VI) INITIATION OF SPREADER LIQUIDATION

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –338 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL:

TOTAL CONTRACTS for 16 days, total 20,180 contracts: OR 100.900 MILLION OZ . (1261 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 100.900 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 100.900 MILLION OZ(SLIGHTLY LESS STRONG THAN LAST MONTH)

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 6500 CONTRACTS WITH OUR $0.34 LOSS IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A GIGANTIC SIZED EFP ISSUANCE CONTRACTS: 1102 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL OF 1.055 MILLION OZ//FIRST DAY NOTICE// 0 OZ E.F.P. JUMP TO LONDON (WHICH DECREASES THE AMOUNT OF SILVER STANDING) AND ZERO QUEUE JUMP + 0 MILLION NEW EXCHANGE FOR RISK TODAY (INCREASES THE AMOUNT OF SILVER STANDING) //NEW EXCHANGE FOR RISK STANDING 35.83 MILLION OZ, THUS TOTAL SILVER OZ STANDING FOR DELIVERY IN APRIL TOTALS 37.770 MILLION .. WE HAVE A GIGANTIC SIZED LOSS OF 5398 OI CONTRACTS ON THE TWO EXCHANGES ALTHOUGH MOST OF THE LOSS WAS DUE TO INITIATION OF SPREADER LIQUIDATION

WE HAD 2 NOTICE(S) FILED TODAY FOR 10,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 638 CONTRACTS TO 473,209 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: added 856 CONTRACTS

WE HAD A SMALL SIZED DECREASE IN COMEX OI ( 856 CONTRACTS) DESPITE OUR $4.90 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR APR. AT 66.892 TONNES ON FIRST DAY NOTICE // PLUS A 8,100 OZ QUEUE. JUMP :(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)YET ALL OF..THIS HAPPENED WITH OUR $4.90 GAIN IN PRICE WITH RESPECT TO TUESDAY’S TRADING.WE HAD A GOOD SIZED GAIN OF 4,100 OI CONTRACTS (12.752 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4738 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 472,353

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4100 CONTRACTS WITH 638 CONTRACTS DECREASED AT THE COMEX AND 4738 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 4100 CONTRACTS OR 12.752 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4738 CONTRACTS) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (638 //TOTAL GAIN IN THE TWO EXCHANGES 4,100 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 66.892 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 8100 OZ//NEW STANDING 74.550 TONNES // ///3) ZERO LONG LIQUIDATION//4) SMALL SIZED COMEX OPEN INTEREST LOSS/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 53,786 CONTRACTS OR 5,378,600 OZ OR 167.29 TONNES IN 16 TRADING DAY(S) AND THUS AVERAGING: 3269 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES 167.29 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 167.29/3550 x 100% TONNES 4.70% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 167.29 TONNES ( MUCH SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A GIGANTIC SIZED 6,500 CONTRACTS OI TO 149,693 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 1102 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1102 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1102 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 6162 CONTRACTS AND ADD TO THE 1102 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 5398 CONTRACTS WITH MOST OF THE LOSS DUE TO INITIATION OF SPREADER LIQUIDATION

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 26.99 MILLION OZ

OCCURRED WITH OUR $0.34 LOSS IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED DOWN 0.77 PTS OR 0.02% //Hang Seng CLOSED UP 139.39 POINTS OR 0.71% /The Nikkei closed DOWN 203.60 PTS OR 0.71% //Australia’s all ordinaries CLOSED DOWN 0.12 % /Chinese yuan (ONSHORE) closed DOWN TO 6.9238/OFFSHORE CHINESE YUAN DOWN TO 6.9340 /Oil UP TO 76.89 dollars per barrel for WTI and BRENT AT 80.15 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 638 CONTRACTS DOWN TO 473,209 DESPITE OUR GAIN IN PRICE OF $4.90 ON MONDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF APRIL… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4738 EFP CONTRACTS WERE ISSUED: : JUNE 4738 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4738 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 4100 CONTRACTS IN THAT 4738 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED LOSS OF 638 COMEX CONTRACTS..AND THIS GOOD SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $4.90. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: APRIL (74.550) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 74.550 tonnes

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $4.90) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR GOOD SIZED GAIN OF 4,100 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 12.752 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL. (66.892 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 8,300 OZ… ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $4.90

WE HAD +ADDED 856 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 4100 CONTRACTS OR 410,000 OZ OR 12.752 TONNES.

Estimated gold comex today 229,563 fair//

final gold volumes/yesterday 235,094 fair

//APRIL 26/ APRIL 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | NIL oz . |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | 128.604 Oz brinks 4 kilobars |

| No of oz served (contracts) today | 154 notice(s) 15400 OZ 0.3546 TONNES |

| No of oz to be served (notices) | 43 contracts 4300 oz 0.1337 TONNES |

| Total monthly oz gold served (contracts) so far this month | 23,925 notices 2,392500 OZ 74.416 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i) Into Brinks: 128.604 oz (4 kilobars)

total deposits: 128.604 oz

customer withdrawals: 0

total withdrawals: nil oz

Adjustments; 1

i) customer to dealer JPMorgan 10,053.125 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of APRIL we have an oi of 197 contracts having LOST 197 contracts. We had 114 contracts served ON TUESDAY so we GAINED 83 contracts or AN ADDITIONAL 8300 oz will stand at the comex.

May LOST 147 contracts DOWN to 1574.

June LOST 3667 contracts DOWN to 382,741 contracts.

We had 154 contracts filed for today representing 15400 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 150 notices were issued from their client or customer account. The total of all issuance by all participants equate to 154 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2023. contract month,

we take the total number of notices filed so far for the month (23,925 x 100 oz ), to which we add the difference between the open interest for the front month of (APRIL. 197 CONTRACTS) minus the number of notices served upon today 154 x 100 oz per contract equals 2,392,500 OZ OR 74.550 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month: No of notices filed so far (23,925 x 100 oz)+197 OI for the front month minus the number of notices served upon today (154)x 100 oz} which equals 2,392,500 oz standing OR 74.550 TONNES in this active delivery month of APRIL..

TOTAL COMEX GOLD STANDING: 74.550 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,713,349.037 OZ 53.29 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,180,444.002 OZ

TOTAL REGISTERED GOLD: 12,314,938.901 (383.04 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 9,865,505.101 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,601.594 OZ (REG GOLD- PLEDGED GOLD) 329.753 tonnes//

END

SILVER/COMEX

APRIL 26//2023// THE APRIL 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 808,126.560 oz CNT Loomis Manfra . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 190,078.475 oz Loomis Manfra |

| No of oz served today (contracts) | 2 CONTRACT(S) (10,000 OZ) |

| No of oz to be served (notices) | 0 contracts (NIL oz) |

| Total monthly oz silver served (contracts) | 388 Contracts (1,940,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 2 deposits into the customer account

i)Into Loomis 29,516.006 oz

ii)Into Manfra: 160,562,409 oz

Total deposits: 190,078.475 oz

JPMorgan has a total silver weight: 140,781 million oz/271,818 million =51.87% of comex .//dropping fast

Comex withdrawals: 3

i) Out of CNT 597,526.930 ox

ii) Out of Loomis: 4769.000 oz

iii)Out of Manfra 205,830.610 oz

Total withdrawals; 808,126.560 oz

adjustments: 0

the silver comex is in stress!

TOTAL REGISTERED SILVER: 30.544 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 271.816 million oz

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL /2023 OI: 2 CONTRACTS HAVING LOST 1 CONTRACT(S). WE HAD 1 NOTICES FILED ON MONDAY SO WE LOST 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL NOT STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF APRIL AS THEY WERE E.F.P.’d TO LONDON.

MAY SAW A LOSS OF 13,974 CONTRACTS DOWN TO 20,919 CONTRACTS. WE HAVE TWO MORE READING DAYS BEFORE FIRST DAY NOTICE. WE SHOULD HAVE A STRONG STANDING FOR SILVER FOR MAY

JUNE HAD A 5 CONTRACTS LOSS TO 573

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 2 for 10,000 oz

Comex volumes// est. volume today 110,132 huge //raid

Comex volume: confirmed yesterday: 127,723 huge

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 388 x 5,000 oz = 1,940,000 oz

to which we add the difference between the open interest for the front month of APRIL(2) and the number of notices served upon today 2 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL/2023 contract month: 388 (notices served so far) x 5000 oz + OI for the front month of APRIL (2) – number of notices served upon today (2 )x 500 oz of silver standing for the APRIL. contract month equates to 1.940 million oz +/ NEW EXCHANGE FOR RISK TODAY: 0 MILLION OZ //NEW TOTALS EXCHANGE FOR RISK FOR MONTH OF APRIL: 35.83 MILLION OZ// THUS TOTAL SILVER OZ STANDING: 37.770 MILLION OZ//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

APRIL 18/WITH GOLD UP $12.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 925.70 TONNES/

APRIL 17/WITH GOLD DOWN $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 927.72 TONNES

APRIL 14/WITH GOLD DOWN $38.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 930.61 TONNES

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

APRIL 10/WITH GOLD DOWN $21.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91 TONNES

APRIL 6//WITH GOLD DOWN $9.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91

APRIL 5//WITH GOLD UP 0 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04

APRIL 4/WITH GOLD UP $36.30 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

APRIL 3/WITH GOLD UP $14.20 TODAY;NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.02 TONNES

MARCH 31/WITH GOLD DOWN $10.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD////INVENTORY RESTS AT 928.02 TONNES

MARCH 30//WITH GOLD UP XX TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A DEPOSIT OF 2.24 TONNES FROM THE GLD/INVENTORY RESTS AT 929.47 TONNES

MARCH 29/WITH GOLD DOWN $4.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4,16 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 927,23

MARCH 28/WITH GOLD UP $19.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

MARCH 15/THE IDES OF MARCH: WITH GOLD UP $18.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 913.27 TONNES

MARCH 14/WITH GOLD DOWN $4.75 TODAY: HUGE CHANGES: A MONSTER DEPOSIT OF 11.85 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 913.27 TONNES

MARCH 13/WITH GOLD UP $48.85 TODAY: VERY STRANGE HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY REST AT 901.42 TONNES

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

GLD INVENTORY: 930.04 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

APRIL 18/WITH SILVER UP 18 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.757 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 467.023 MILLION OZ

APRIL 17/WITH SILVER DOWN 33 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 469.780 MILLION OZ//

APRIL 14/WITH SILVER DOWN 48 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.974 MILLION OZ/

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 10/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 6/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 4.643 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 468.585 MILLION OZ//

APRIL 5/WITH SILVER DOWN 4 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.942 MILLION OZ

APRIL 4/WITH GOLD UP $1.11 TODAY CRIMINAL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.47 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 463,942 MILLION OZ

APRIL 1/WITH SILVER DOWN 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.412

MARCH 31/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE GLD/: A MASSIVE 4.779 MILLION OZ DEPOSITED INTO THE SLV///INVENTORY RESTS AT465.412 MILLION OZ

MARCH 30/WITH SILVER UP XX CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV.: A DEPOSIT OF 550,000 OZ INTO THE SLV/.INVENTORY RESTS AT 460.633 MILLION OZ

MARCH 29/WITH SILVER UP 11 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 460.082

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

MARCH 17/WITH SILVER UP 79 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE WITHDRAWAL OF 10.478 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 462.748 MILLION OZ//

MARCH 16/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 5.009 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 473.226 MILLION OZ//

MARCH 15/WITH SILVER DOWN 7 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 643,000 OZ INTO THE SLV//INVENTORY RESTS AT 478.235 MILLION OZ/

MARCH 14/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.287 MILLION OZ FROM THE SLV////INVENTORY REST AT 477.592 MILLION OZ//

MARCH 13/WITH SILVER UP $1.35 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ//

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

CLOSING INVENTORY 470.285 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//

Rickards: We’re Our Own Worst Enemy

WEDNESDAY, APR 26, 2023 – 12:05 PM

Authored by James Rickards via DailyReckoning.com,

It’s a fact of life that in any group of students, some are likely to be smarter and quicker than others while some just can’t keep up.

It’s unfortunate that Treasury Secretary Janet Yellen has turned out to be the slow kid in the class when it comes to economic sanctions and financial warfare.

Almost 10 years ago, I sat in a secure conference room at the Pentagon and explained to a group of U.S. national security officials from the military, CIA, Treasury and other agencies that the overuse of the U.S. dollar in financial warfare would eventually drive countries away from using dollars in international transactions for fear that they could become the next target of U.S. displeasure.

Some took note, some ignored the warning and one Treasury official slammed the table and said, “The dollar has been the global reserve currency, it is the global reserve currency now and it always will be the global reserve currency!”

I told him I felt like I was in Whitehall in London in 1913 listening to John Bull say the same thing about sterling. Sterling would begin to be pushed aside by the dollar just one year later with the start of World War I.

We’re Our Own Worst Enemy

More recently, I taught a seminar at the U.S. Army War College on financial warfare in which I explained that U.S. financial sanctions would not have a material impact on Russia, that Russia would not change its behavior in Ukraine based on the sanctions and that the U.S. would suffer more from its own sanctions than Russia because adversaries and neutral countries would create alternative payment platforms that did not use dollars.

I encountered skepticism from the class (that’s OK; the purpose of a seminar is to engender competing views).

I’ve said to the military and intelligence community, “I don’t think other countries can destroy the dollar, but we can do it ourselves. We are our own worst enemy.”

We, of course, meaning the United States. We’re destroying the dollar with the sanctions (and through other misguided policies). The U.S. is doing more to destroy the dollar than our enemies.

Events of the past year have proved my forecast in every respect.

Many others have pointed out the same weaknesses in the weaponization of the dollar. It seems the only parties who didn’t see the danger to the dollar were the Wall Street cheerleaders and top U.S. government officials.

Russia Has Been Preparing for This

Russia saw all this coming, and has been preparing accordingly.

In 2009. Russia’s gold reserves were about 600 tons. By the time the sanctions were imposed in 2022, Russia’s gold reserves were close to 3,000 tons. They had spent that 13-year period acquiring 2,400 metric tons of gold.

If you think that’s easy, it isn’t. It’s not easy at all to acquire anywhere near that amount of gold. But they were like Steady Eddie, The Little Engine That Could.

They bought 10 to 30 tons per month like clockwork, about 250 tons a year, sometimes more, sometimes less, but over 13 years they got to that 3,000-ton level.

They’re very transparent about it. But they were anticipating financial warfare from the U.S. and its allies.

So when the sanctions were imposed, Russia’s total reserves were approximately $600 billion, but almost 25% of that, about $150 billion, was in gold. And I’m talking about actual gold bullion held in safe storage in Russia, not gold futures contracts or ETFs because they’re just as easy to freeze as any other asset.

That was not a complete answer to the sanctions they were facing, but it was a very substantial move in the direction of insulating themselves from being kicked out of the dollar system.

Well, all I can say is that I warned the Pentagon about this in 2009 when I conducted financial war games. I also wrote about it in my book Currency Wars, which came out in 2011. Now it’s all playing out before our eyes. China, of course, has been doing the same thing as Russia to escape dollar dominance.

Could the Russian Economy Outperform the U.S. Economy This Year?

Incidentally, Russia’s growth should be higher than the United States this year, believe it or not. Russia’s estimated by the IMF to grow slightly less than 3%. And the U.S.? We’re probably already in recession, so we won’t get anywhere near 3%.

Meanwhile, Russian oil exports are higher than ever.

Russia’s buying high-tech goods from China, including some military hardware and other manufactured goods. China’s buying Russian oil and natural gas, in addition to agricultural output and weapons. That’s a big two-way trade, and the dollar isn’t being used. Russia’s paying yuan, and China’s paying rubles.

Now, the failure of U.S. dollar-based sanctions has become too obvious to ignore. The failure is so obvious that even Janet Yellen admits that sanctions are not working.

She recently said, “There is a risk when we use financial sanctions that are linked to the role of the dollar that over time it could undermine the hegemony of the dollar. Of course, it does create a desire on the part of China, of Russia, of Iran to find an alternative.”

One could say that realizing the dangers ten years too late is still better late than never.

Why the Dollar Hasn’t Tanked — Yet

The issue is whether it’s already too late to undo the damage. Once new trading currencies and new payment channels are put in place (which is happening quickly), there’s little incentive to go back to a dollar system where the U.S. can threaten your economy.

I should add that there are reasons why the dollar is strong today that have nothing to do with what I’ve been discussing. It has to do with the banking crisis (that’s far from over, by the way). There’s high demand for dollar-denominated collateral, particularly short-term Treasury bills. That’ll break at some point, but not yet.

And so, the dollar is being propped up by the demand for dollar-denominated collateral, even though it’s under attack from all sides based on these new payment currency alternatives that are rapidly emerging.

Yellen is once again putting her incompetence on full display. She’s a textbook neo-Keynesian with little understanding of monetary policy, fiscal policy, or the international monetary system.

I’ve consistently said that the greatest threat to the dollar comes not from abroad but from the U.S. Treasury because they take confidence in the dollar for granted. We’re doing this to ourselves.

Yellen is proving my point.

END

Jamie Dimon’s Deeply Conflicted Role as “Rescuer” of First Republic Bank Requires a Credible Investigation

By Pam Martens and Russ Martens: April 26, 2023

The Board of Directors and shareholders at the largest bank in the U.S., JPMorgan Chase – which has more than 5,000 Chase Bank branches dotting the landscape from coast to coast – have ample reason to ask themselves where the loyalties of the bank’s Chairman and CEO Jamie Dimon exactly lie.

Dimon, who has come under withering negative publicity for the bank’s many years of catering to the cash payoff needs of child sex trafficker Jeffrey Epstein, had an urgent incentive to want to change the subject. So a media blitz ensued around his role as rescuer of the sinking carcass of a much smaller bank, First Republic Bank – which has its own dubious distinction of being the bank that wired the hush money to porn star Stormy Daniels by Trump attorney, Michael Cohen.

For just how broadly Dimon’s “rescue” of First Republic Bank has been reported, scroll down at this link. Only someone living off the grid or in a coma did not hear that Jamie Dimon was riding to the rescue of First Republic Bank.

But as early as Tuesday, March 28, during a Senate Banking hearing, it became clear that when First Republic finally got around to updating the public on the severity of its distressed situation (which it finally did on Monday in a 12-minute earnings call that took no questions from anyone), the news was going to be devastating to the bank.

At the Senate Banking hearing, the Vice Chairman for Supervision at the Fed, Michael Barr, explained just how fast deposits can evaporate from a bank in the new digital age, especially when tens of billions of dollars of those deposits exceed the FDIC insurance cap of $250,000 per depositor, per bank. Barr told the Senators that in the case of Silicon Valley Bank, $42 billion in deposits had left the bank on Thursday, March 9, and bank customers had queued up $100 billion more to exit the following day. Silicon Valley Bank did not have adequate collateral to post at the Fed to borrow funds to meet that $100 billion in withdrawals, thus the bank was put into FDIC receivership on March 10.

No depositor has ever lost a dime of deposits in an FDIC- insured bank if they have kept those deposits in FDIC- insured accounts and within that $250,000 FDIC cap.

Both Silicon Valley Bank and First Republic Bank are California-headquartered regional banks. The contagion from Silicon Valley Bank had directly impacted First Republic Bank. By the date of that Senate Banking hearing on March 28, First Republic’s common stock had lost 90 percent of its market value – just in the month of March.

It might be possible to come back from that if one is a start-up tech firm, or an acknowledged high-risk innovator. But Americans put their money in federally-insured banks because they want safety; because they want the peace of mind of knowing their deposits will be protected despite what happens in the Wall Street casino on any given day. In that vein, Jamie Dimon was the worst possible choice to head up a rescue of First Republic Bank as he is the personification of what happens when a trading casino is allowed to own the largest federally-insured bank in America. Under Dimon’s tenure at the helm of JPMorgan Chase, it has been charged with losing $6.2 billion of depositors’ money by gambling in derivatives in London; its precious metals traders have been charged under RICO – the statute used to prosecute the mob; it has received an unprecedented five felony counts from the U.S. Department of Justice, including aiding and abetting the largest Ponzi scheme in history by Bernie Madoff, and on and on.

But Jamie Dimon has a legion of public relations flacks shaping his image as a titan of Wall Street wisdom and he has clearly gotten high on his own p.r. supply. So Dimon cajoled three other mega banks on Wall Street to join his bank and dump $5 billion each of uninsured deposits into First Republic Bank on March 16. Those banks were Bank of America, Citigroup and Wells Fargo. In addition, Morgan Stanley and Goldman Sachs deposited $2.5 billion each; while BNY Mellon, State Street, PNC Bank, Trust and US Bank each deposited $1 billion, bringing the total infusion to $30 billion.

In addition, according to First Republic, JPMorgan Chase had also provided a line of credit to the bank. Multiple media outlets also reported that JPMorgan Chase and Lazard were advisors to First Republic Bank on its options going forward. (See here and here.)

Yesterday, the share price of First Republic plunged another 49 percent, closing at an all-time low of $8.10. In response, CNBC is reporting that there is now a plan afoot to attempt to cajole the 11 banks that sluiced the $30 billion in temporary deposits to First Republic to convert that into an equity stake. Seriously? What the devil is going on here and why aren’t the shareholders of these banks wielding pitchforks?

S&P Global has already downgraded First Republic Bank into junk territory; excluding the $30 billion in strong- armed deposits from the mega banks, First Republic lost a staggering 58 percent of its deposits in the first quarter of this year; and its wealth advisors are leaving and taking billions of dollars in clients assets with them to new firms.

Since when did it become a rational move for one federally-insured bank to link its brand and reputation to an imploding bank?

Dimon needs to be hauled before the Senate Banking Committee in a public hearing, put under oath, and grilled as to what exactly his motivation was to get so enmeshed in the hot mess at First Republic Bank. Likewise, the perpetually blind-folded and conflicted Board at JPMorgan Chase needs to hire an independent, credible law firm to investigate the conflicts inherent in the many hats Jamie Dimon was wearing in this debacle.

end

3,Chris Powell of GATA provides to us very important physical commentaries

Bank run on First Republic continues:

(London’s Financial Times)

Sharp selloff in First Republic shares causes alarm in Washington

Submitted by admin on Wed, 2023-04-26 04:14Section: Daily Dispatches

By James Fontanella-Khan, Colby Smith, Stephen Gandel, and Brooke Masters

Financial Times, London

Wednesday, April 26, 2023

Shares of First Republic continued to plunge on Tuesday as regulators in Washington and financiers on Wall Street scrambled to come up with a plan to stabilise the ailing bank.

The California-based lender’s stock price, which is down by more than 93 per cent this year, fell by a further 49.4 per cent, a day after it revealed its customers had withdrawn $100 billion of deposits during last month’s turmo

First Republic on Monday said it was pursuing “strategic options”, but multiple people briefed on the situation said it was struggling to come up with a viable solution, such as a sale of all or part of the bank.

The people said the bank was in touch with the US government, which is on high alert following the failure of Silicon Valley Bank and Signature Bank last month. …

… For the remainder of the report:

https://www.ft.com/content/32439fdf-3215-4e9a-91fb-eb6b3e821451

end

Emergency money eases but the risk still remains

(Associated Press)

Central banks reduce crisis cash offers as bank system fears ease

Submitted by admin on Wed, 2023-04-26 01:27Section: Daily Dispatches

Much of this money could be used for surreptitious market interventions and no one outside central banking would ever know — and financial news organizations will never ask.

* * *

By David McHugh

Associated Press

via ABC News, New York

Wednesday, April 25, 2023

FRANKFURT, Germany — In a sign fears about the global financial system have eased for now, major central banks are scaling back their offer of emergency dollar loans to banks, a crisis step launched after the collapse of Silicon Valley Bank in the U.S. fed fears about wider troubles.

The European Central Bank said Tuesday that it and other central banks found that pressure on banks’ cash needs has dropped and the crisis credits were not being used much lately.

As of May 1 the central banks will move from daily offerings of dollars to any bank that needs them to the previous availability of every seven days.

Making extra dollars available has been a tool in times of trouble because banks need the U.S. currency to handle many international transactions. The so-called dollar swap lines were used during the 2008 global financial crisis and the economic turmoil in the early days of the COVID-19 pandemic to ease the impact on the supply of credit to consumers and businesses. …

… For the remainder of the report:

end

This will not go over well!

(London Telegraph)

People should just accept their falling standard of living, Bank of England exec says

Submitted by admin on Tue, 2023-04-25 11:37Section: Daily Dispatches

Yes, that might make life easier for central bankers, whose own living standards aren’t likely to fall.

* * *

People Need to Accept They Are Poorer, Bank of England Exec Says

By Eir Nolsoe

The Telegraph, London

Tuesday, April 25, 2023

Britons have to accept they have become poorer, a senior Bank of England official has said, claiming that an unwillingness to accept the nation’s downward mobility was fuelling inflation.

Huw Pill, Threadneedle Street’s chief economist, said people “need to accept that they’re worse off and stop trying to maintain their real spending power by bidding up prices, whether [through] higher wages or passing the energy costs through onto customers.”

Pill said people and businesses were trying to maintain their standards of living and profits by either demanding higher pay or putting up prices.

However, he argued this was only likely to fuel inflation and compared the dynamic to a game of pass the parcel, where each player was unwilling to accept the burden of higher prices that make them poorer. …

… For the remainder of the report:

https://www.telegraph.co.uk/business/2023/04/25/people-accept-poorer-bank-of-england-huw-pill/

end

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

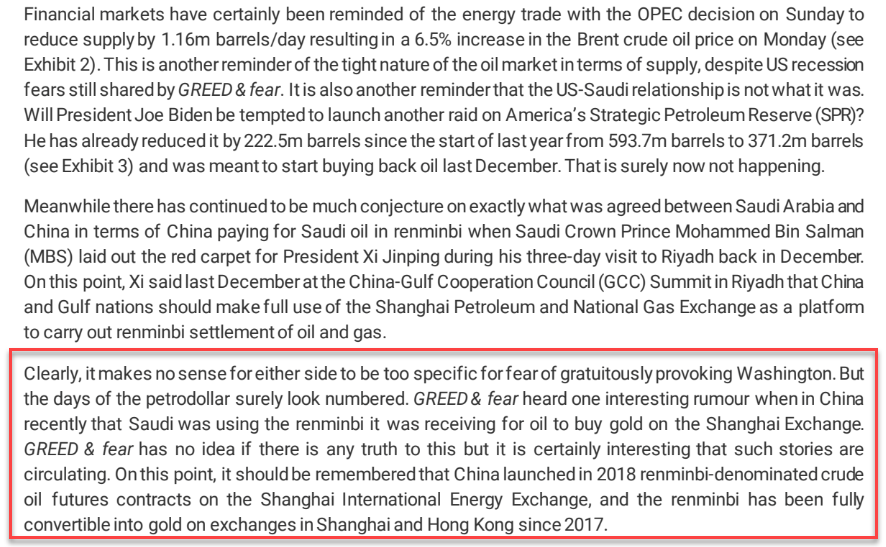

this would be deadly to the west if true! We know that Saudi Arabia is selling oil to China for yuan. The question is whether

Saudi Arabia is converting the yuan earned for gold. They do not need yuan!

(Jan Nieuwenhuijs)

Is Saudi Arabia Selling Oil To China For Gold?

TUESDAY, APR 25, 2023 – 08:25 PM

By Jan Nieuwenhuijs of Gainesville Coins

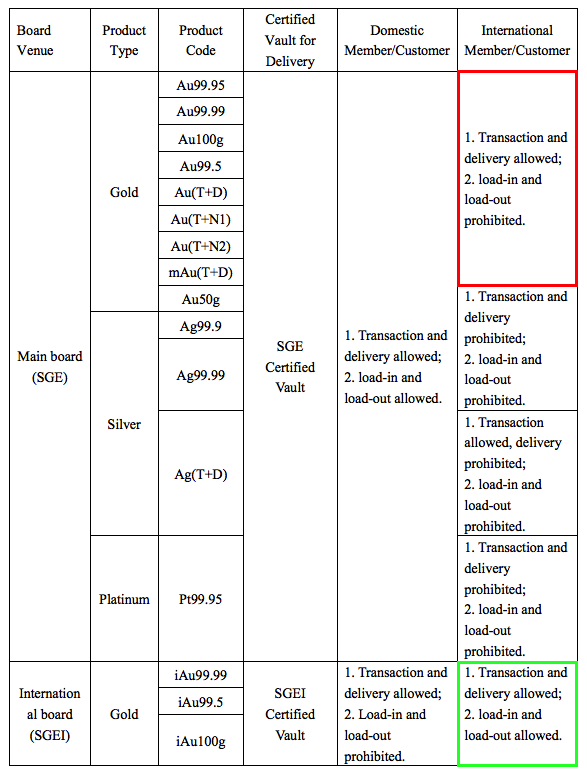

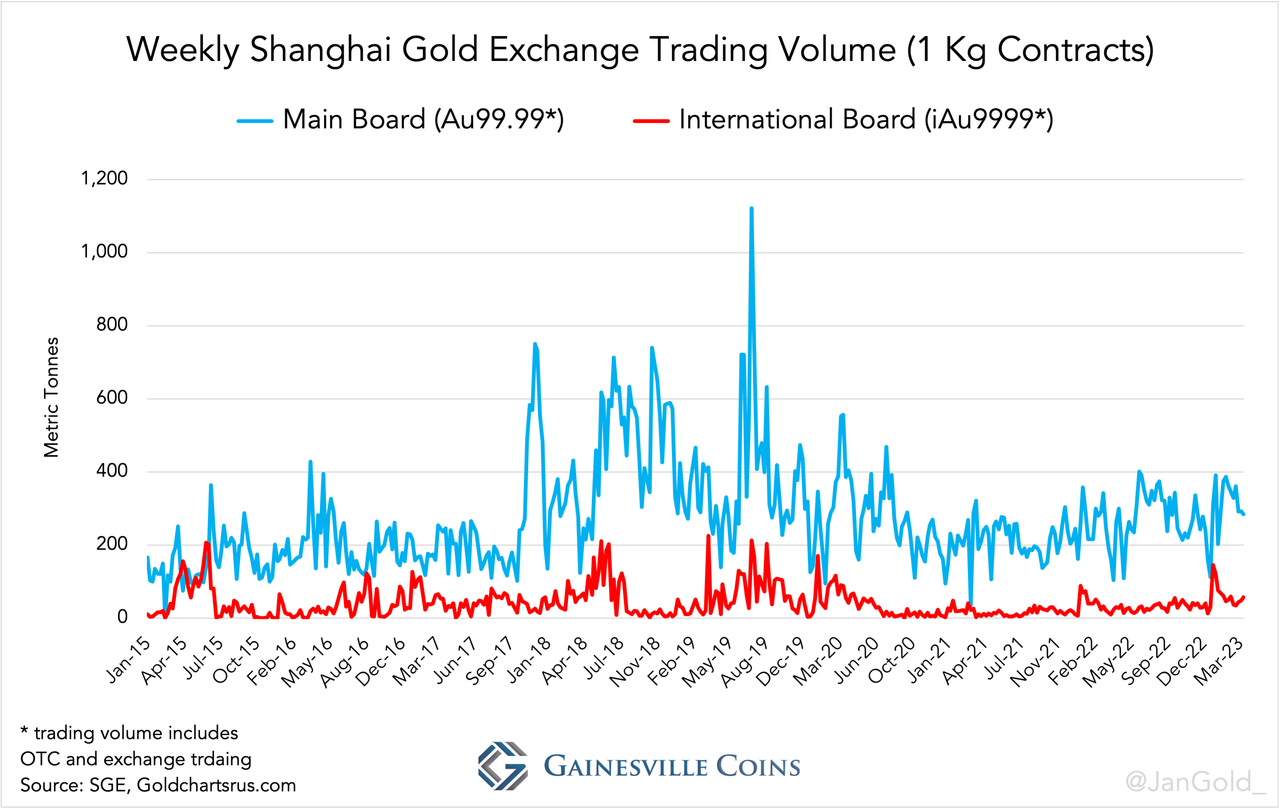

Rumors are making rounds that Saudi Arabia is selling oil for yuan, which it converts into gold on the Shanghai International Gold Exchange (SGEI). Such a development would make sense as large parts of the world want to de-dollarize, but the renminbi is not suitable to be used as a reserve currency. China has a closed capital account and a weak rule of law. Not using the dollar could be done by using the renminbi as a trade currency and converting yuan revenue into gold on the SGEI. If the rumor is true, Saudi Arabia is buying 1 Kg bars as there is virtually no trading in 12.5 Kg bars on the SGEI. The benefit of 1 Kg bars is that they are more fitting for fully allocated trading.

The SGEI was set up in 2014 for foreigners to access gold trading on the Shanghai Gold Exchange Main Board in the Chinese domestic gold market and trading on the International Board in the Shanghai Free Trade Zone (SFTZ). Foreigner entities can’t load-in and load-out gold into and from Main Board certified vaults, but they can load-in and load-out gold into and from International Board certified vaults (and thus import into and export from the SFTZ).

The objective of the International Board is to facilitate “offshore” gold trading in renminbi in the SFTZ, which has almost no effect on China’s current account. This is comparable to offshore gold trading in US dollars in London (offshore dollars pricing internationally traded commodities). Through the SGEI China wants to increase the role of the renminbi in the global economy.

Investment possibilities for foreigners in Chinese financial assets are limited, but there are no restrictions to converting yuan into gold on the SGEI. I will write more on the mechanics of the Chinese gold market in a forthcoming article because this will be important in the coming years with respect to de-dollarization.

Last week, Christopher Wood from Jefferies mentioned in a note that the Saudis might be converting yuan into gold on the SGEI (full note available to pro subs in the usual place):

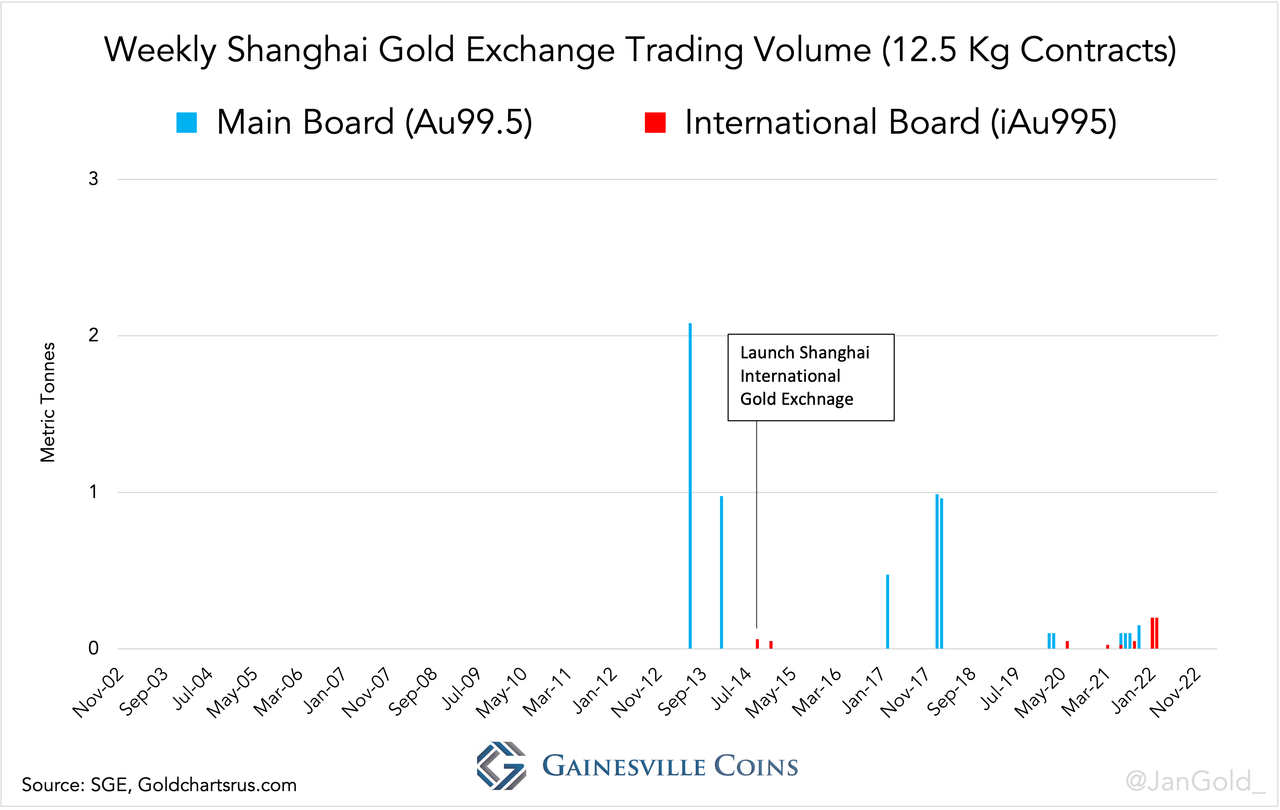

If Saudi Arabia would convert yuan into gold on the SGEI, I would expect them to buy large bars weighing 400 ounces (12.5 Kg). Data from the SGE and SGEI, though, reveals there has practically been no trading in 12.5 Kg bars since the SGE was erected in October 2002.

In the above chart volume is shown for exchange trading of 12.5 Kg contracts. Not shown, over-the-counter (OTC) trading in the 12.5 Kg contract on the International Board was zero in the past year. OTC trading in the 12.5 kg contract on the Main Board isn’t reported, which makes me think it’s not existent. All in all, large bar trading on the SGE(I) is extremely low.

Based on 12.5 Kg contract trading volume on the SGE(I) it’s hard to prove the rumor is true, which doesn’t mean it can’t be true. Saudi Arabia can also buy 1 Kg bars on the SGEI (and SGE, but it wouldn’t be able to export gold traded on the Main Board). Trading in 1 Kg contracts on the SGEI (iAu9999) and SGE (Au99.99) is not subdued. Although, there hasn’t been a significant uptick in trading of iAu9999 recently.

Interestingly, according to my sources, in China’s foreign exchange market (CFETS) all gold traded is settled and cleared through the SGE and is fully allocated. One of the reasons for this is because the underlying assets are the SGE 1 Kg (9999 fine) and 3 Kg (9995) contracts. In Western foreign exchange markets, the underlying for gold trading is usually the LBMA Good Delivery bar that weighs approximately 400 ounces, which is more convenient to trade on an unallocated basis. As an example, exchanging exactly 20,000 ounces in London is easy on an unallocated basis, while it’s difficult to collect a batch of large bars that together weigh precisely 20,000 ounces. Perhaps Asia is shifting to an alternative benchmark and that’s why the Saudis are buying 1 Kg bars? Time will tell.

Xi Jinping, President of the People’s Republic of China, visited Saudi Arabia in December 2022 where he pledged to continue buying oil and gas from Gulf Cooperation Council (GCC) nations, and proposed these trades to be settled in yuan. From Xi:

China will continue to import large quantities of crude oil from GCC countries, expand imports of liquefied natural gas, strengthen cooperation in upstream oil and gas development, engineering services, storage, transportation and refining, and make full use of the Shanghai Petroleum and National Gas Exchange as a platform to carry out yuan settlement of oil and gas trade…

Shortly after, in January 2023, Saudi Arabia shared it’s open to discussions about trade in currencies other than the US dollar, according to the kingdom’s finance minister.

The Wall Street Journal wrote in March 2023 that, “Saudi Arabia is in active talks with Beijing to price some of its oil sales to China in yuan.”

These statements tell us there is a will in both countries to de-dollarize. Selling oil for yuan and then converting those into gold would be a logical step, given the renminbi’s shortcomings as a reserve currency. But I would like to see more evidence before confirming this trend.

A few months ago, a person familiar with the matter but who prefers to stay anonymous told me Saudi Arabia is covertly buying gold, though he refrained from saying where it was bought. Perhaps the Saudis are slowly working on a transition; de-dollarization isn’t done overnight.

END

5.IMPORTANT COMMENTARIES ON COMMODITIES: LITHIUM

end

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

1.YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//,WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 6.9238

OFFSHORE YUAN: 6.9340

SHANGHAI CLOSED DOWN 0.77 POINTS OR 0.02%

HANG SENG CLOSED UP 139.39 PTS OR 0.71%

2. Nikkei closed DOWN 203.60 PTS OR 0.71%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 101.07 EURO RISES TO 1.1077 UP 69 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.456Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 134.21 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.3385***/Italian 10 Yr bond yield RISES to 4.243*** /SPAIN 10 YR BOND YIELD FALLS TO 3.401…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.156

3j Gold at $1997.40 silver at: 24.98 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 10 /100 roubles/dollar; ROUBLE AT 81.73//

3m oil into the 76 dollar handle for WTI and 80 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 133.33 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .456% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8887 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9818 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.390 DOWN 1 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.648 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.8893 DOWN 6 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.43…

GREAT BRITAIN/10 YEAR YIELD: DOWN 7 BASIS PTS AT 3.7070

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

Futures Rally Fizzles As Banking Fears Resurface

WEDNESDAY, APR 26, 2023 – 08:07 AM

US index futures are fractionally higher, led by tech, however continued turmoil surrounding First Republic Bank which tumbled as much as 30% this morning after losing half its value yesterday, has sapped much of the earlier optimism and gains. Yesterday was the SPX’s worst day in a month and was April’s second move that exceeded 1%, in either direction. As of 8:00am ET, S&P futures were up 0.1%, while Nasdaq futures gained 0.8%, but both were well of their highs. Google parent Alphabet and Microsoft Corp. both beat first-quarter earnings expectations in results published after the market close. Microsoft gained in the premarket Wednesday, while Alphabet reversed an advance to move into the red. Meta Platforms is due to report after the bell today.

Pre-mkt MSFT +7.4%, AMZN +3.7%, NVDA +2.1%, META +2.0%, GOOGL, +0.5%, AAPL +0.4%. PACW seemingly gives more evidence that FRC is idiosyncratic. V is +0.9% pre-mkt after posting earnings; the more impactful news may be that the company states that the consumer remains in good shape amid decreasing inflation. Here are some other notable premarket movers:

- Boeing shares jump 4.1% in premarket trading, after the planemaker’s first-quarter revenue and cash flow both beat expectations. Shares off some Boeing suppliers also rose premarket. Spirit AeroSystems up 2.5%, Arconic up 1%, Howmet up 1.9%.

- Microsoft jumps as much as 7.7% after the software company’s third-quarter results beat expectations. Analysts highlighted strength in the company’s Azure cloud business and were optimistic about the overall resiliency of the business, leading at least 16 of them to raise their price target on the stock.

- Alphabet rises as much as 1.9% after the Google parent reported first-quarter results that beat expectations. Analysts noted strength in the company’s search business, as well as positive momentum in cloud. This coupled with strong results from fellow tech juggernaut Microsoft eased concerns that tech shares’ year-to-date rally is overdone.

- Midsize US banks, including First Republic (FRC US), rally following an update from peer PacWest which showed that deposits stabilized toward the end of March and rose in April, calming worries over the lender’s health.

- Enphase Energy shares plummet as much as 16%, on track for their worst day since June 2020, with analysts cutting their price targets on the solar equipment maker after its second-quarter revenue guidance missed expectations due to weakness in its US market and higher interest rates. Brokers say that Enphase’s first quarter performance was overall strong, and are positive regarding its prospects for the longer-term.

- Getty falls as much as 6.7% after the media firm rebuffed a takeover bid of almost $4 billion from Trillium, saying the activist investor hasn’t provided any evidence that its proposal, valuing the shares at nearly double the pre-offer price, is “sufficiently credible.”

- IonQ gains 3.6% after Morgan Stanley initiates coverage with an equal-weight recommendation, saying the quantum computing company is an early leader in the space, though the technology risk is high as quantum advantage is still unproven.

While layoffs dominate headlines, the US is still net adding jobs this year, from a strong starting point, 3.5% unemployment. The yield curve is steeper with USD lower; cmdtys staging a relief rally.

Today, the macro data focus is on durable/cap goods, inventories, and mtge applications. There may be a vote on McCarthy’s debt ceiling bill in the House, though this bill will fail in the Senate but is seeing a stronger negotiating move. Debt ceiling fears will continue to permeate markets near-term

“The question is to what extent central banks and regulators can contain market sentiment and make clear to investors they need to keep a cool head, to give depositors confidence that there is no need to run to other banks,” said Tatjana Puhan, deputy chief investment officer at Tobam SAS. “So far the Fed has been very clear that they will continue to hike rates as long as needed to contain inflation.”

European stocks fall to their lowest level in two weeks as investors continue to fret over the health of the global banking system. Software producer Dassault Systemes sank more than 8% after missing revenue estimates. The Stoxx 600 is down 0.8% with industrials, healthcare and tech the worst performing sectors. Bank stocks were leading declines at one stage but recovered after a positive premarket open for First Republic. Dutch chip-tool maker ASM International slumped more than 10% after offering a tepid outlook for the rest of the year. Roche Holding AG retreated even as its first-quarter sales exceeded expectations. Beats from Standard Chartered Plc and Sweden’s SEB AB failed to bolster sentiment. Here are the most notable European movers:

- Kindred shares jump 15% after the online gambling firm said it initiated a review of strategic alternatives, including a sale. Goodbody analyst says the firm is an “attractive asset”

- Temenos shares jump as much as 11%, the most in a year, after the Swiss financial software firm delivered a strong beat in the first quarter, even if its outlook remains clouded

- Persimmon shares gain as much as 5.3% after showing an improving outlook in its 1Q report, with other UK homebuilders also gaining. Peel Hunt says the report offers “comfort”

- SSAB rallies as much as 5.2% after reporting adjusted Ebitda for the first quarter that beat estimates, with analysts expecting the Swedish steelmaker’s estimates to rise

- SEB shares rise by as much as 6.2%, the most in a year, after the Swedish lender reported net interest income for the first quarter that beat the average analyst estimate

- Vonovia rises 5.9% after it sells minority common equity participation in “Suedewo” portfolio to Apollo on behalf of its affiliated and third party insurance clients and other investor

- ASM International shares fall as much as 13% in Amsterdam, their biggest intraday decline since 2020, after the Dutch chip-tool maker offered a tepid outlook for rest of the year

- Dassault Systemes shares fall as much as 7.8%, their biggest intraday decline since May 2022, after the French firm reported weaker-than-expected software license sales for 1Q

- CRH shares drop as much as 5% after the Irish building materials company reported 1Q like-for-like sales growth below that of peers, impacted by weather effects

- Axfood falls as much as 6.5% after the Swedish grocer reported 1Q adjusted Ebitda and net sales slightly below expectations, a miss Kepler Cheuvreux attributes to logistics arm Dagab

- Handelsbanken falls as much as 4.4% after its CET1 ratio missed the consensus, while Citi noted that a small beat in net interest income was driven by a reclassification of funding costs

“The markets are very much focused on some of the earnings story, but possibly overlooking the weight of economic deceleration that is playing through right now, particularly in the United States,” John Woods, Asia Pacific chief investment officer at Credit Suisse Group AG, said on Bloomberg Television. “I’m looking at a whole range of technical signals, which seem to be suggesting a risk-off environment.”

Earlier in the session, Asia stocks fell for a fourth straight day as weak US consumer confidence data sapped risk appetite, although the selloff in Chinese equities paused. The MSCI Asia Pacific Index slipped as much as 0.5%, trading near a one-month low, led by benchmarks in Japan and the Philippines. The moves come after declines in US markets overnight amid a drop in consumer confidence and a re-emergence of banking concerns. Hong Kong shares outperformed with gains, while mainland China equities trimmed earlier losses as traders sought catalysts after the rout this month. China’s high frequency indicators show the economy continued to expand in April, though geopolitical concerns are keeping optimism in check.

“The macro overlay is probably dominating the performance of equities, particularly in China,” said John Woods, Asia Pacific chief investment officer at Credit Suisse, told Bloomberg Television. “I’m looking at a whole range of technical signals which seem to be suggesting a risk-off environment” globally, he added. Despite strong results from Microsoft and Alphabet, a gauge of major tech stocks in the region was among the biggest sectoral decliners Wednesday. Earnings are front and center this week, with more than 800 members of the MSCI Asia gauge scheduled to report, as the market attempts to find direction amid low volatility.

Japanese stocks fell amid renewed concern over the health of the global banking system after First Republic Bank shares plunged on a proposed asset sale and decline in deposits. The Topix fell 0.9% to close at 2,023.90, while the Nikkei declined 0.7% to 28,416.47. Keyence contributed the most to the Topix decline, decreasing 2%. Out of 2,158 stocks in Topix, 329 rose and 1,767 fell, while 62 were unchanged. “I think it is unlikely that the problem of US banks will develop into a financial crisis,” said Masahiro Ichikawa, chief market strategist at Sumitomo Mitsui DS Asset Management. “However, there is a possibility that lending will tighten mainly for small and medium-sized companies, and attention must be paid to the risk of economic deterioration.”

Australian stocks were flat, as cooler inflation boosted the case for holding rates; the S&P/ASX 200 index was little changed to close at 7,316.30, as losses in mining shares offset gains in industrials and energy stocks. Australia’s core inflation decelerated in the first three months of 2023, lending weight to the Reserve Bank’s view that prices will steadily come down and supporting the case for it to extend an interest-rate pause. Read: Australia’s Cooler Inflation Boosts Case to Keep Rates on Hold In New Zealand, the S&P/NZX 50 index fell 0.8% to 11,934.98.

In FX, the Bloomberg Dollar Spot Index fell 0.3%, unwinding most of Tuesday’s gain, as US futures rose. Euro and pound outperform among G10 currencies, with both climbing more than 0.5% against the greenback. Australia’s dollar dropped against all its major peers as the country’s slower-than-estimated inflation supported the case for the central bank to extend its rate-hike pause. The trimmed-mean inflation gauge rose 1.2% in 1Q from the previous quarter, falling short of the 1.4% gain estimated by economists; it comes after the Reserve Bank of Australia paused its almost year-long tightening cycle earlier this month. The Swedish krona also dropped after the Riksbank signaled smaller rate increases going forward.

In rates, treasuries held on to Tuesday’s sharp gains following minimal price action during Asia session and London morning. US yields are 1bp lower on the day with 10-year around 3.39%, trailing bunds by 4bp in the sector. European bonds also gained, with German and UK 10-year yields falling by 5bps and 2bps respectively. The treasury auction cycle continues with $43b 5-year note sale at 1pm, following small tail in Tuesday’s 2-year sale. WI 5-year yield at ~3.43% is ~23bp richer than March auction, which stopped 1bp through the WI level.

Crude futures advance with WTI rising 0.5% to trade near $77.50. Spot gold is little changed around $2,000.

Bitcoin is firmer and has lifted back towards the USD 29k mark, but is yet to mount a convincing test of the figure with the high thus far circa. USD 100 shy; action which keeps BTC comfortably above last-week’s parameters but shy of the USD 30k+ seen earlier in April.

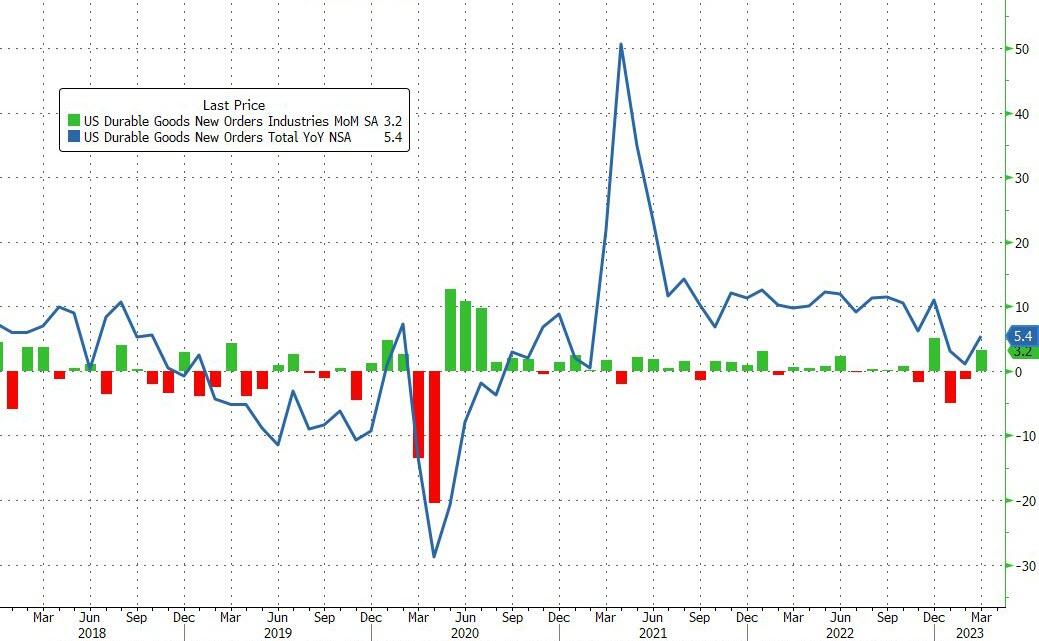

Looking to the day ahead now, and data releases from the US include preliminary durable goods orders and core capital goods orders for March. From central banks, we’ll hear from ECB Vice President de Guindos and the ECB’s Herodotou. Lastly, earnings releases include Meta and Boeing.

Market Snapshot

- S&P 500 futures up 0.1% to 4,098.00

- MXAP down 0.1% to 159.64

- MXAPJ up 0.2% to 510.57

- Nikkei down 0.7% to 28,416.47

- Topix down 0.9% to 2,023.90

- Hang Seng Index up 0.7% to 19,757.27

- Shanghai Composite little changed at 3,264.10

- Sensex up 0.1% to 60,210.93

- Australia S&P/ASX 200 little changed at 7,316.30

- Kospi down 0.2% to 2,484.83

- STOXX Europe 600 down 0.7% to 463.89

- German 10Y yield little changed at 2.35%

- Euro up 0.6% to $1.1037

- Brent Futures up 0.5% to $81.17/bbl

- Gold spot up to $1,997.49

- U.S. Dollar Index down 0.43% to 101.43

Top Overnight News

- BOJ widely expected to leave policy unchanged this week, but COVID could be dropped in the statement as a risk factor, a move that might be interpreted as the first step toward tightening measures later in the year. RTRS

- Australian inflation eased from 33-year highs in the first quarter as the cost of living saw the smallest rise in more than a year, while core inflation dipped below forecasts suggesting less pressure for another hike in interest rates. Data from the Australian Bureau of Statistics on Wednesday showed the consumer price index (CPI) rose 1.4% in the March quarter, just above market forecasts of 1.3% but the smallest increase since late 2021. RTRS

- South Korea will have a say in planning a potential U.S. nuclear response to a North Korean attack in return for not developing its own nuclear weapons. WSJ

- Sweden’s Riksbank raises rates by 50bp, as expected (although two members at the bank voted for 25bp), and guided for one additional increase at its June or Sept meeting, suggesting the tightening process is nearly over. BBG

- The White House chief of staff, Jeff Zients, said that while he can’t comment on specific banks, “you can be reassured that that the regulators are deeply involved in monitoring the situation and will take the necessary actions”. WSJ

- Almost one in five cars sold worldwide this year will be an electric vehicle, the International Energy Agency has forecast, after sales already passed the 10mn mark for the first time globally. The remarkable surge in demand for battery-powered models means electric vehicles will account for 18 per cent of global car sales compared with just 4 per cent of global car sales in 2020, according to the agency’s annual outlook. FT

- Opposition mounts in the House among Republicans to McCarthy’s debt ceiling bill, meaning it prob. can’t pass without revisions (the goal had been for a vote to take place today). The Hill

- US crude stockpiles slumped more than 6 million barrels last week, the API is said to have reported. That would be the biggest drop in four weeks if confirmed by the EIA today. Inventories at Cushing edged higher. Gasoline supplies resumed their decline, while distillate inventory climbed. BBG

- Stanley Druckenmiller is betting against the US dollar as his only high-conviction trade in what he believes is the most uncertain environment for markets and the global economy in his 45-year career. FT

- The SPAC boom took hundreds of risky companies to the stock market. The next stop for many is bankruptcy court. Dozens of companies that merged with SPACs are running out of cash, joining at least 12 that have already gone bankrupt after combining with special-purpose acquisition companies. WSJ

A more detailed look at global markets courtesy of Newsquawk