April 27/2023 · by harveyorgan · in Uncategorized · Leave a comment·Editi

GOLD PRICE CLOSED: UP $4.00 TO $1989.90

SILVER PRICE CLOSED: UP 16 CENTS AT $24.94

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE $1988.05

Silver ACCESS CLOSE: 24.92

Bitcoin morning price:, $29,023 UP 1134 Dollars

Bitcoin: afternoon price: $29,648 UP 1759 dollars

Platinum price closing $1082.60 DOWN $10.00

Palladium price; $1503.75 DOWN $21.85

We have now entered options expiry week, with the Comex options expired April 25/2023 and LBMA/OTC expiring on Friday April 28.2023. The crooks can only whack once London is put to bed as they fear that many are demanding physical delivery against their short sales. Their attention span is less than one day. They will worry about physical deliveries tomorrow

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2702.30 DOWN 10.50 CDN dollars per oz (ALL TIME HIGH 2732.50)

BRITISH GOLD: 1590.73 DOWN 5.60 pounds per oz//(ALL TIME HIGH//1629.84)

EURO GOLD: 1802,68 UP 1.50 euros per oz //(ALL TIME HIGH//1860.82)

DONATE

EXCHANGE: COMEX

CONTRACT: APRIL 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,985.700000000 USD

INTENT DATE: 04/26/2023 DELIVERY DATE: 04/28/2023

FIRM ORG FIRM NAME ISSUED STOPPED

363 H WELLS FARGO SEC 3

435 H SCOTIA CAPITAL 213

661 C JP MORGAN 42 38

685 C RJ OBRIEN 30

880 H CITIGROUP 227

905 C ADM 45

TOTAL: 299 299

MONTH TO DATE: 24,224

JPMorgan stopped 0/299 contracts

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2023. CONTRACT: 299 NOTICES FOR 29,900 OZ or 0.9300 TONNES

total notices so far: 24,224 contracts for 2,422,400 oz (75.5023 tonnes)

SILVER NOTICES: 0 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month : 388 for 1,940,000 oz

END

GLD

WITH GOLD UP $4.00

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD

/NO CHANGES IN GOLD INVENTORY AT THE GLD://////

INVENTORY RESTS AT 930.04 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 16 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ OF SILVER FROM THE SLV.//: INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 469.182 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUMONGOUS SIZED 5729 CONTRACTS TO 143,043 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.10 LOSS IN SILVER PRICING AT THE COMEX ON WEDNESDAY. WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.10). AND WERE SUCCESSFUL IN KNOCKING A FEW SPEC LONGS AS WE HAD A HUGE LOSS ON OUR TWO EXCHANGES OF 3,164 CONTRACTS WITH MOST OF THAT LOSS DUE TO CONTINUATION OF SPREADER LIQUIDATION IN THE SILVER ARENA.. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 35.83 MILLION OZ.) WE HAVE FINISHED WITH OUR SPECS BEING SHORT AS THEY COVERED WITH THE RISE IN PRICE IN JANUARY . WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG.

WE MUST HAVE HAD:

A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS( 2415 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 1.055 MILLION OZ(FIRST DAY NOTICE)+ THE 35.83 MILLION OZ OF EXCHANGE FOR RISK/+ 1.940 MILLION OZ NORMAL SILVER STANDING FOR APRIL///THUS TOTAL NEW STANDING 37.770 MILLION OZ/ //// V) GIGANTIC SIZED COMEX OI LOSS/ HUGE SIZED EFP ISSUANCE/.VI) CONTINUATION OF SPREADER LIQUIDATION

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –150 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL:

TOTAL CONTRACTS for 17 days, total 22,595 contracts: OR 112.975 MILLION OZ . (1329 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 112.975 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105/ MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 112.975 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 5729 CONTRACTS WITH OUR $0.10 LOSS IN SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A GIGANTIC SIZED EFP ISSUANCE CONTRACTS: 2415 CONTRACTS ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL OF 1.055 MILLION OZ//FIRST DAY NOTICE// 0 OZ E.F.P. JUMP TO LONDON (WHICH DECREASES THE AMOUNT OF SILVER STANDING) AND ZERO QUEUE JUMP + 0 MILLION NEW EXCHANGE FOR RISK TODAY (INCREASES THE AMOUNT OF SILVER STANDING) //NEW EXCHANGE FOR RISK STANDING 35.83 MILLION OZ, THUS TOTAL SILVER OZ STANDING FOR DELIVERY IN APRIL TOTALS 37.770 MILLION .. WE HAVE A GIGANTIC SIZED LOSS OF 3314 OI CONTRACTS ON THE TWO EXCHANGES ALTHOUGH MOST OF THE LOSS WAS DUE TO CONTINUATION OF SPREADER LIQUIDATION

WE HAD 0 NOTICE(S) FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 6,047 CONTRACTS TO 478,569 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: added 687 CONTRACTS

WE HAD A GOOD SIZED INCREASE IN COMEX OI ( 6047 CONTRACTS) DESPITE OUR $8.45 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR APR. AT 66.892 TONNES ON FIRST DAY NOTICE // PLUS A 36,200 OZ QUEUE. JUMP :(QUEUE JUMPING = EXERCISING LONDON BASED EFP’S, ATTACHED TO COMEX CONTRACTS ) (EFP is the transfer of COMEX contracts immediately to London for potential gold deliveries originating from London)////YET ALL OF..THIS HAPPENED WITH OUR $8.45 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING.WE HAD A STRONG SIZED GAIN OF 12,227 OI CONTRACTS (38.03 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 6180 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 479,256

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 12,227 CONTRACTS WITH 6047 CONTRACTS INCREASED AT THE COMEX AND 6180 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 12,227 CONTRACTS OR 38.03 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (6180 CONTRACTS) ACCOMPANYING THE GOOD SIZED GAIN IN COMEX OI (6047 //TOTAL GAIN IN THE TWO EXCHANGES 12,277 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 66.892 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 36,200 OZ (1.125 TONNES)/ // ///3) ZERO LONG LIQUIDATION//4) GOOD SIZED COMEX OPEN INTEREST GAIN/ 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER/

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 59,976 CONTRACTS OR 5,997,600 OZ OR 186.55 TONNES IN 17 TRADING DAY(S) AND THUS AVERAGING: 3528 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAY(S) IN TONNES 186.55 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 186.55/3550 x 100% TONNES 5.26% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 186.55 TONNES ( MUCH SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAR HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF APRIL., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (NOV), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A GIGANTIC SIZED 5729 CONTRACTS OI TO 143,963 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 2415 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 2415 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2415 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 5729 CONTRACTS AND ADD TO THE 2415 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 3314 CONTRACTS WITH MOST OF THE LOSS DUE TO CONTINUATION OF SPREADER LIQUIDATION

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 10.307 MILLION OZ

OCCURRED WITH OUR $0.10 LOSS IN PRICE ….. OUR SPEC SHORTS HAVE NOWHERE TO HIDE!

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED UP 21.78 PTS OR 0.67% //Hang Seng CLOSED UP 83.01 POINTS OR 0.42% /The Nikkei closed UP 83.01 PTS OR 0.42% //Australia’s all ordinaries CLOSED DOWN 0.28 % /Chinese yuan (ONSHORE) closed DOWN TO 6.923/OFFSHORE CHINESE YUAN DOWN TO 6.9348 /Oil DOWN TO 74.29 dollars per barrel for WTI and BRENT AT 77.94 / Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GOOD SIZED 6047 CONTRACTS UP TO 479,254 DESPITE OUR LOSS IN PRICE OF $8.45 ON WEDNESDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF APRIL… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 6180 EFP CONTRACTS WERE ISSUED: : JUNE 6180 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 6180 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 12,227 CONTRACTS IN THAT 6180 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED GAIN OF 6047 COMEX CONTRACTS..AND THIS STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $8.45. WE ARE NOW WITNESSING THE BANKERS GOING NET SHORT AND THE SPECS GOING NET LONG.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: APRIL (75.675) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes (TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.675 tonnes

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $8.45) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR STRONG SIZED GAIN OF 12,227 CONTRACTS ON OUR TWO EXCHANGES

WE HAVE GAINED A TOTAL OI OF 23.122 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL. (66.892 TONNES) FOLLOWED BY TODAY’S QUEUE JUMP OF 36,200 OZ… ALL OF THIS WAS ACCOMPLISHED WITH OUR FALL IN PRICE TO THE TUNE OF $8.45

WE HAD +ADDED 687 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 12,227 CONTRACTS OR 1,222,700 OZ OR 38.03 TONNES.

Estimated gold comex today 203,931 fair//

final gold volumes/yesterday 256,815 fair

//APRIL 27/ APRIL 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 201.751 oz HSBC . |

| Deposit to the Dealer Inventory in oz | nil OZ |

| Deposits to the Customer Inventory, in oz | 160,755.000 Oz JPM 5,000 kilobars |

| No of oz served (contracts) today | 299 notice(s) 29,900 OZ 0.9300 TONNES |

| No of oz to be served (notices) | 106 contracts 10,600 oz 0.3297 TONNES |

| Total monthly oz gold served (contracts) so far this month | 24,224 notices 2,422,400 OZ 75.5023 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

i)Dealer deposits: 0

total dealer deposit: nil oz

No dealer withdrawals

Customer deposits: 1

i) Into JPMorgan: 160,755.000 oz (5000 kilobars)

total deposits: 160,755.000 oz

customer withdrawals: 1

i) out of HSBC: 201.751 oz

total withdrawals: 201.751 oz

Adjustments; 4 all dealer to customer

i) HSBC 5887.487 oz

ii) Int Delaware 482.265 oz

iii) JPMorgan: 5632.723 oz

iv) Manfra: 3795.636 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of APRIL we have an oi of 405 contracts having GAINED 208 contracts. We had 154 contracts served ON WEDNESDAY so we GAINED 362 contracts or AN ADDITIONAL 36,200 oz will stand at the comex.

May LOST 380 contracts DOWN to 1194.

June GAINED 732 contracts UP to 383,473 contracts.

We had 299 contracts filed for today representing 29,900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 42 notices were issued from their client or customer account. The total of all issuance by all participants equate to 299 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the APRIL /2023. contract month,

we take the total number of notices filed so far for the month (24,224 x 100 oz ), to which we add the difference between the open interest for the front month of (APRIL. 405 CONTRACTS) minus the number of notices served upon today 199 x 100 oz per contract equals 2,433,000 OZ OR 75.675 TONNES the number of TONNES standing in this active month of APRIL.

thus the INITIAL standings for gold for the APRIL contract month: No of notices filed so far (24,224 x 100 oz)+405 OI for the front month minus the number of notices served upon today (299)x 100 oz} which equals 2,433,000 oz standing OR 75.675 TONNES

TOTAL COMEX GOLD STANDING: 75.675 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 1,713,349.037 OZ 53.29 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,340,997.251 OZ

TOTAL REGISTERED GOLD: 12,299,140.79 (382.55 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,041,856.461 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,585,791 OZ (REG GOLD- PLEDGED GOLD) 329.262 tonnes//

END

SILVER/COMEX

APRIL 27//2023// THE APRIL 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 582,752.200 oz JPMorgan . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 80,376.471 oz Delaware |

| No of oz served today (contracts) | 0 CONTRACT(S) (nil OZ) |

| No of oz to be served (notices) | 0 contracts (NIL oz) |

| Total monthly oz silver served (contracts) | 388 Contracts (1,940,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposits: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We have 1 deposits into the customer account

i)Into Delaware: 80,376.471 oz

Total deposits: 80,376.471 oz

JPMorgan has a total silver weight: 140,198 million oz/271,314 million =51.60% of comex .//dropping fast

Comex withdrawals: 1

i) Out of JPMorgan; 582,752.200 oz

Total withdrawals; 582,752.200 oz

adjustments: 2

i) Dealer to customer: CNT: 80,826.04 oz

ii) customer to dealer jPMorgan: 1,831,048.780 oz

the silver comex is in stress!

TOTAL REGISTERED SILVER: 32,294 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 271.314 million oz

CALCULATION OF SILVER OZ STANDING FOR APRIL

silver open interest data:

FRONT MONTH OF APRIL /2023 OI: 0 CONTRACTS HAVING LOST 2 CONTRACT(S). WE HAD 2 NOTICES FILED ON WEDNESDAY SO WE LOST 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF APRIL

MAY SAW A LOSS OF 13,199 CONTRACTS DOWN TO 7702 CONTRACTS. WE HAVE ONE MORE READING DAYS BEFORE FIRST DAY NOTICE.

JUNE HAD A 41 CONTRACTS GAIN TO 614

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes// est. volume today 78,644 very strong //raid

Comex volume: confirmed yesterday: 122,510 huge//raid

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 388 x 5,000 oz = 1,940,000 oz

to which we add the difference between the open interest for the front month of APRIL(0) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL/2023 contract month: 388 (notices served so far) x 5000 oz + OI for the front month of APRIL (0) – number of notices served upon today (0 )x 500 oz of silver standing for the APRIL. contract month equates to 1.940 million oz +/ NEW EXCHANGE FOR RISK TODAY: 0 MILLION OZ //NEW TOTALS EXCHANGE FOR RISK FOR MONTH OF APRIL: 35.83 MILLION OZ// THUS TOTAL SILVER OZ STANDING: 37.770 MILLION OZ//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

APRIL 18/WITH GOLD UP $12.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.03 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 925.70 TONNES/

APRIL 17/WITH GOLD DOWN $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 927.72 TONNES

APRIL 14/WITH GOLD DOWN $38.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 930.61 TONNES

APRIL 13/WITH GOLD UP$31.70 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.17 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.08 TONNES

APRIL 11/WITH GOLD UP $14.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 903.91 TONNES

APRIL 10/WITH GOLD DOWN $21.40 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91 TONNES

APRIL 6//WITH GOLD DOWN $9.15 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.91

APRIL 5//WITH GOLD UP 0 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04

APRIL 4/WITH GOLD UP $36.30 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

APRIL 3/WITH GOLD UP $14.20 TODAY;NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.02 TONNES

MARCH 31/WITH GOLD DOWN $10.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FROM THE GLD////INVENTORY RESTS AT 928.02 TONNES

MARCH 30//WITH GOLD UP XX TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A DEPOSIT OF 2.24 TONNES FROM THE GLD/INVENTORY RESTS AT 929.47 TONNES

MARCH 29/WITH GOLD DOWN $4.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4,16 TONNES OF GOLD INTO THE GLD.//INVENTORY RESTS AT 927,23

MARCH 28/WITH GOLD UP $19.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 923.07 TONNES

MARCH 27/WITH GOLD DOWN $28.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD./INVENTORY RESTS AT 923.97 TONNES

MARCH 23/WITH GOLD UP $47.70 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT 87 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 925.42 TONNES

MARCH 21/WITH GOLD DOWN $38.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: ANOTHER HUGE DEPOSIT OF 3.4 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 924.55 TONNES

MARCH 20//WITH GOLD UP $9.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 6.36 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 921.08 TONNES

MARCH 17/WITH GOLD UP $50.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 914.72TONNES

MARCH 16/WITH GOLD DOWN $6.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 914.72 TONNES

MARCH 15/THE IDES OF MARCH: WITH GOLD UP $18.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 913.27 TONNES

MARCH 14/WITH GOLD DOWN $4.75 TODAY: HUGE CHANGES: A MONSTER DEPOSIT OF 11.85 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 913.27 TONNES

MARCH 13/WITH GOLD UP $48.85 TODAY: VERY STRANGE HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY REST AT 901.42 TONNES

MARCH 10//WITH GOLD UP $31.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 3.47 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 903.15 TONNES

MARCH 9/WITH GOLD UP $16.50 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 906.62 TONNES

MARCH 8/WITH GOLD DOWN $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.5 TONNES FROM THE GLD////INVENTORY RESTS AT 906.62 TONNES

MARCH 7/WITH GOLD DOWN $33.20 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.12 TONNES

MARCH 6/WITH GOLD UP $0.55 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .57 TONNES FROM THE GLD///INVENTORY RESTS AT 912.12 TONNES

MARCH 3/WITH GOLD UP $14,10 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 912.69 TONNES

MARCH 2/WITH GOLD DOWN $4.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.61 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 912.69 TONNES

MARCH 1/WITH GOLD UP $18.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 915.30 TONNES

GLD INVENTORY: 930.04 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

APRIL 19/WITH SILVER UP 11 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.023 MILLION OZ//

APRIL 18/WITH SILVER UP 18 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.757 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 467.023 MILLION OZ

APRIL 17/WITH SILVER DOWN 33 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 469.780 MILLION OZ//

APRIL 14/WITH SILVER DOWN 48 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.974 MILLION OZ/

APRIL 13/WITH SILVER UP HUGELY BY 48 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.389 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 470.974 MILLION OZ

APRIL 11/WITH SILVER UP 27 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 10/WITH SILVER DOWN 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.585 MILLION OZ

APRIL 6/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV; A DEPOSIT OF 4.643 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 468.585 MILLION OZ//

APRIL 5/WITH SILVER DOWN 4 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.942 MILLION OZ

APRIL 4/WITH GOLD UP $1.11 TODAY CRIMINAL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.47 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 463,942 MILLION OZ

APRIL 1/WITH SILVER DOWN 14 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 465.412

MARCH 31/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE GLD/: A MASSIVE 4.779 MILLION OZ DEPOSITED INTO THE SLV///INVENTORY RESTS AT465.412 MILLION OZ

MARCH 30/WITH SILVER UP XX CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV.: A DEPOSIT OF 550,000 OZ INTO THE SLV/.INVENTORY RESTS AT 460.633 MILLION OZ

MARCH 29/WITH SILVER UP 11 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 460.082

MARCH 28/WITH SILVER UP 28 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.887 MILLION OZ//

MARCH 27/WITH SILVER DOWN 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 230,000 OZ FROM THE SLV///INVENTORY RESTS AT 459.255 MILLION OZ

MARCH 23 WITH SILVER UP 62 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF 919,000 0z INTO THE SLV/INVENTORY RESTS AT 459.485 MILLION OZ//

MARCH 21/WITH SILVER DOWN 24 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 781,000 OZ FORM THE SLV////INVENTORY RESTS AT 458.566 MILLION OZ/

MARCH 20./WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER MASSIVE WITHDRAWAL OF 3.401 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 459.347 MILLION OZ//

MARCH 17/WITH SILVER UP 79 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE WITHDRAWAL OF 10.478 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 462.748 MILLION OZ//

MARCH 16/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 5.009 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 473.226 MILLION OZ//

MARCH 15/WITH SILVER DOWN 7 CENTS TODAY; BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 643,000 OZ INTO THE SLV//INVENTORY RESTS AT 478.235 MILLION OZ/

MARCH 14/WITH SILVER UP 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.287 MILLION OZ FROM THE SLV////INVENTORY REST AT 477.592 MILLION OZ//

MARCH 13/WITH SILVER UP $1.35 : NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ//

MARCH 10.WITH SILVER UP 36 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 478.879 MILLION OZ…

MARCH 9/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.195 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 478.979 MILLION OZ

MARCH 8/WITH SILVER DOWN 6 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 477.684 MILLION OZ

MARCH 7/WITH SILVER DOWN 88 CENTS TODAY;HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,000 OZ FROM THE SLV/////INVENTORY RESTS AT 478.143 MILLION OZ

MARCH 6/WITH SILVER DOWN 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 3/WITH SILVER UP 67 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.369 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 479.063 MILLION OZ//

MARCH 2/WITH SILVER DOWN $.16 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 920,00 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 477.694 MILLION OZ

MARCH 1/WITH SILVER UP 4 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.574 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 478.614 MILLION OZ.

CLOSING INVENTORY 469.182 MILLION OZ//

PHYSICAL GOLD/SILVER STORIES

1:Peter Schiff

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//

Mathew Piepenburg….

So Many Open Signs Of Financial Disaster Ahead And Gold Working

THURSDAY, APR 27, 2023 – 07:20 AM

Authored by Matthew Piepenburg via GoldSwitzerland.com,

From oil markets to treasury stacking, backdoor QE, investor fantasy and hedge fund prepping, it’s becoming more and more clear that the big boys are bracing for disaster as gold stretches its legs for a rapid run north.

Recently, I dove into the cracks in the petrodollar as yet another symptom of a world turning its back on USTs and USDs.

Gold, of course, has a role in these headlines if one looks deep enough.

So, let’s look deeper.

Diving Deeper into the Oil Story

The headlines of late, for example, are all about “surprise” OPEC production cuts.

Why is this happening and what does it say about gold down the road?

First, let’s face the politics.

As noted many times, it seems US policy, on everything from short-sighted (suicidal?) sanctions to the “green initiative” makes just about zero sense in the real world, which is miles apart from the “keep-me-elected” fantasy-world of DC.

After all, energy, matters, which means oil matters.

But the current regime in DC has been losing friends in Saudi Arabia and cutting its prior and once admirable shale production outputs (think 2016-2020) in the US despite a world that still runs on black gold fighting against green politics.

The DC attack on shale may make the Greta Thunbergs happy, but let’s be blunt: It defies economic common sense.

Saudi, by cutting production, is now showing a still very much oil-dependent world it is not afraid of losing market share to the USA in the face of rising oil for the simple reason that the USA just aint got enough oil to fill the gap or flex its energy muscles.

In the meantime, Chinese demand for crude is peaking while Russian oil flows to the east (including to Japan) are hitting new highs at prices above the US-led price cap of $60/barrel.

If DC has any blunt realists (wrongly castigated as tree-killers) left, it will have to re-think its anti-oil policies and get back toward that recent era when US shale was responsible for 90% of total global oil supply growth.

If not, oil prices can and will spike, making Powell’s war on inflation even more of an open charade.

Speaking of inflation…

Ghana Oil-for-Gold Beats Inflation

When it comes to oil and the decades-long bully-effect of a usurious USD (See: Confessions of an Economic Hitman), we have argued countless times that a strong USD and an imposed petrodollar was gutting developing economies around the world.

We also warned that developing economies (spurned by global distrust of the Greenback in a post-Putin-sanction era of a weaponized reserve currency) would respond by turning their backs on US policies and its dollar.

In the old days, the US could export its inflation abroad. But those days, as we warned as early as March 2022, would be slowly but steadily coming to a hegemonic end.

Again, this does not mean (nod to the Brent Johnson) the end of the USD as a reserve currency, just the slow end of the USD as a trusted, used or effective currency.

Toward that slow but steady end, it’s perhaps worth noting that Ghana’s inflation rate has fallen from 156% to just over 60% since it began trading oil for gold rather than weaponized USDs.

Hmmm.

Gold Works Better than Inflated Greenbacks

The most obvious conclusion we can draw from such a predictable correlation is that gold seems to be working better than fiat dollars to fight/manage inflation, a fact we’ve been arguing for well…decades.

From India to China, Ghana, Malaysia, China and 37 other countries engaged in non-USD bilateral trade agreements, the inflation-infected USD is losing its place in more than just the critical oil trade.

Nations trapped in USD-denominated debt-traps (thanks to a rate-hiked and hence stronger and more expensive USD) are now finding ways to tie their exports (i.e., oil) to a more stable monetary asset (i.e., GOLD).

This, of course, makes me that much more confident that as the world moves closer to its global (and USD-driven) “Uh-Oh” moment, that the already-telegraphed Bretton Woods 2.0 will have to involve a new global order tied to something golden rather than just something fiat.

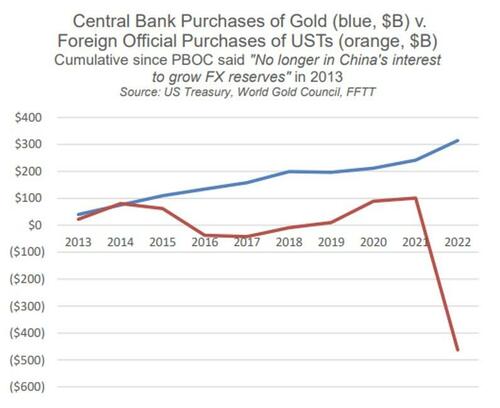

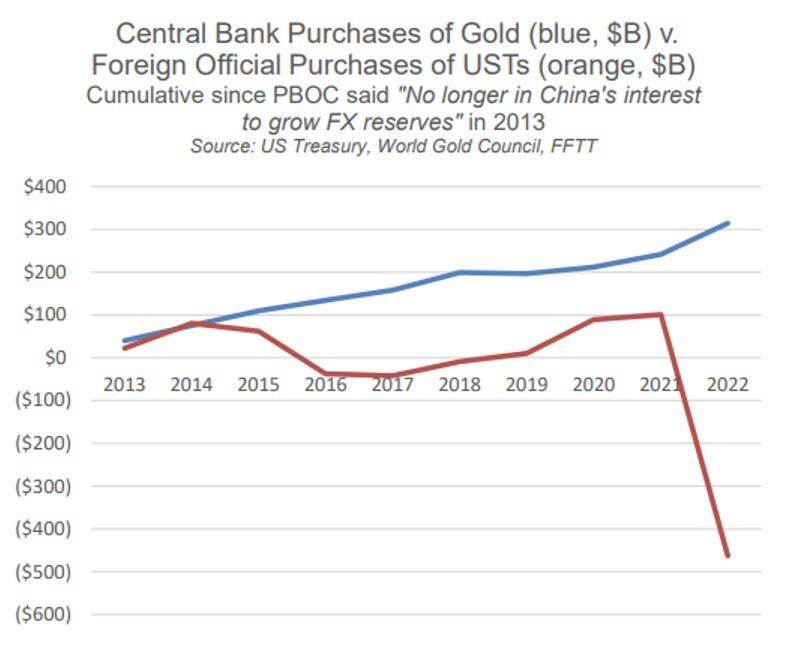

This, again, explains why so many of the world’s central banks are loading up on gold rather than Uncle Sam’s IOUs.

Gosh. Just see for yourself:

Ouch.

Uh-oh?

US Investors: Still High on Past Fantasy Rather than Current Reality

Sadly, however, the US in general, and US investors in particular, remain trapped in a spiral of cognitive dissonance and still believe today and tomorrow’s America is the America of magical leaders, deficits without tears and the balanced-budget honesty of the Eisenhower era.

That’s why the vast majority (and their consensus-think, safety-in-numbers advisors) are still huddling in correlated 60/40 stock bond allocations rather than physical gold according to a recent BofA survey of wealth “advisors.”

This always reminds me of a phrase circling around Tokyo just before the grotesquely inflated Nikkei bubble lost greater than 80% of its hot air in the crash of 1989, namely: “How can we get hurt if we’re all crossing the road at the same time?”

Well, a large swath of US investors (and their “advisors”) is about to find out how.

Doubling Down on Return Free Risk

This may explain why US households (a statistical term of art which includes hedge funds) have upped their allocations to USTs by 165% ($1.6T) since Q4 of 2022 at the same time that the rest of the world (see above) has been dumping them.

But in all fairness, this does make some sense, as higher rates in the US give investors in USTs (especially in short-duration/money market securities) a greater return than their checking or savings accounts.

Unfortunately, where the masses go is also where bubbles go; but as I like to remind: All bubbles pop.

Of course, when adjusted for inflation, these poor US investors are still getting a negative return on USTs.

Foreigners, of course, have stopped falling for this, but when Americans themselves get suckered en masse into this same bond-trap, they’re basically just paying an invisible tax while chipping away at GDP growth and unknowingly helping Uncle Sam finance his debt for free (namely: at a loss to themselves).

Crazy?

Yep.

Negative Returning IOUs—The Lesser of Evils

But why are hedge funds (i.e., the “smart money”) falling for this? Why are they loading up on USTs?

Because they see trouble ahead, and even a negative returning UST is safer (less evil) than a tanking S&P–and that’s exactly what the pros are bracing for/anticipating.

Waiting for a Market Bottom

In short: The big-boys are safe-havening today in negative-USTs so that they’ll have dry powder at hand to buy a pending and massive market bottom tomorrow.

Once they can buy a bottom, they too will dump Uncle Sam’s IOUs as the QE (along with inflation) kicks back to new highs thereafter.

And speaking of QE…

Backdoor QE: Coordinated and Synthetic Liquidity by Another Name

I have always endeavored to simplify the complex with big-picture common sense.

Toward this end, let’s keep it simple.

And the simple truth is this: With US debt at unprecedented and unsustainable levels, it is a matter of national survival to prevent bond yields—and hence bond-driven rather than Fed- “set” interest rates–from spiking.

Such a natural, and bond-driven spike, after all, would make Uncle Sam’s embarrassing debt too expensive to function.

Survival vs. Debate

Thus, and to repeat: Keeping bond yields controlled is not a matter of pundit debate but national survival.

Since bond yields spike when bond prices fall, it is thus a matter of sovereign survival to keep national bond prices at reasonably high levels.

This, however, is naturally impossible when bond demand (and hence price) is naturally sinking.

This natural reality opens the door to the un-natural “solution” wherein central banks un-naturally print trillions (“synthetic demand”) to buy their own bonds/debt.

Of course, this game is otherwise known as QE, or “Quantitative Easing”–that ironic euphemism for un-natural, anti-capitalist, anti-free market and anti-free-price-discovery Wall Street socialism whose inflationary consequences cause Main Street feudalism.

In short: QE has backstopped a modern system of central-bank-created lords and serfs.

Which one are you?

See why Thomas Jefferson and Andrew Jackson feared a Federal Reserve, which is neither “federal,” nor a solvent “reserve.”

The ironies, they do abound…

How Can there be QE if the Headlines Say QT?

But the official narrative and headlines are still telling us only stories of QT (Quantitative Tightening) rather than QE, so what’s the problem?

Well, as with just about everything from CPI data and transitory inflation memes to recession re-defining, the official narrative is not always the truthful narrative…

In fact, back-door or “hidden QE” is all around us, from the Fed bailing out/funding repo markets and dead regional banks to central banks making secret deals behind the scenes.

Although it’s not officially QE when the central bank of one country is buying the IOUs (bonds) of another country, it is more than likely that leading central banks are acting in a coordinated way to “QE each other’s debt,” a system which former Fed official, Kathleen Tyson, describes as a “Daisy Chain.”

And if we look at the IMF’s own data, we can connect the dots of this Daisy Chain with relative (rather than tin-foil-hatted) clarity.

Since Q4 of 2022, for example, overall FX reserves are now up by over $340B, the equivalent of over $100B per month of central bank QE by another name.

Toward that end, the math is simple, with: 1) GBP reserves up 10% (no surprise given the gilt implosion of Oct. 2022), JPY reserves up nearly 8%, EUR reserves up 7% and USD reserves only up only 0.5%.

Not only does this look like backdoor QE masquerading as “building excess reserves,” it looks to me, at least, like a coordinated attempt by DXY central banks to collectively weaken the 2022 USD which Powell’s rate hikes had made painfully too high for the rest of the world, a fact/pivot of which we warned throughout 2022.

Since the above G7 policies kicked in, the USD has fallen 11% into 2023 as the other DXY currencies (JPY, EUR and GBP) gave themselves a little backdoor/QE boost.

It seems, in short, that the need for artificial liquidity in a world thirsty for USDs found a clever way to weaken the relative strength (and cost) of that USD (and confront/tame skyrocketing volatility in USTs) without overtly requiring Powell to mouse-click dollars from his own laptop.

Why Markets Rise into a Recession

This unofficial but likely coordinated play to constructively weaken the USD among the big boys helps explain why the S&P has been rising into 2023 despite open indicators that the country is itself marching toward a recession.

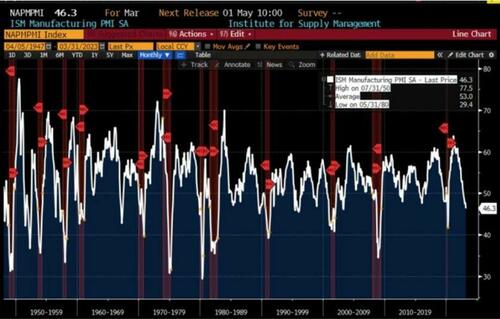

US Manufacturing data (ISM) is now at levels consistent with a recession…

Again: The ironies (and un-natural manipulations) abound.

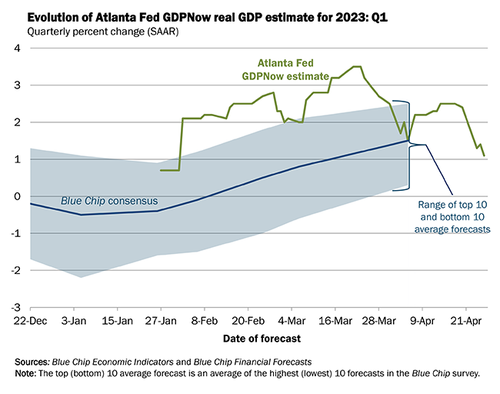

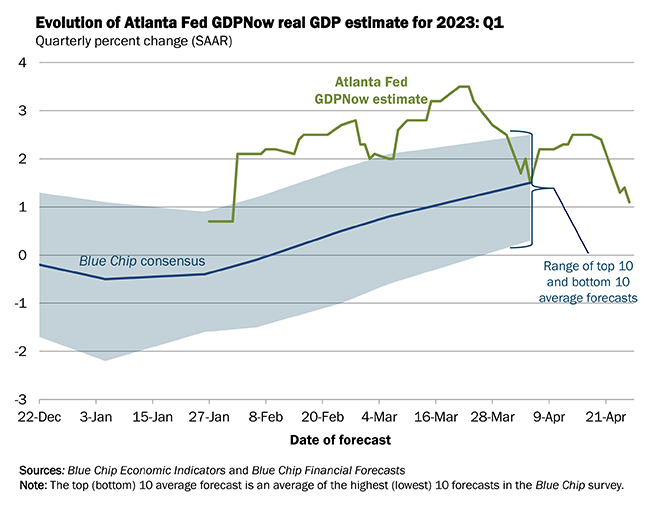

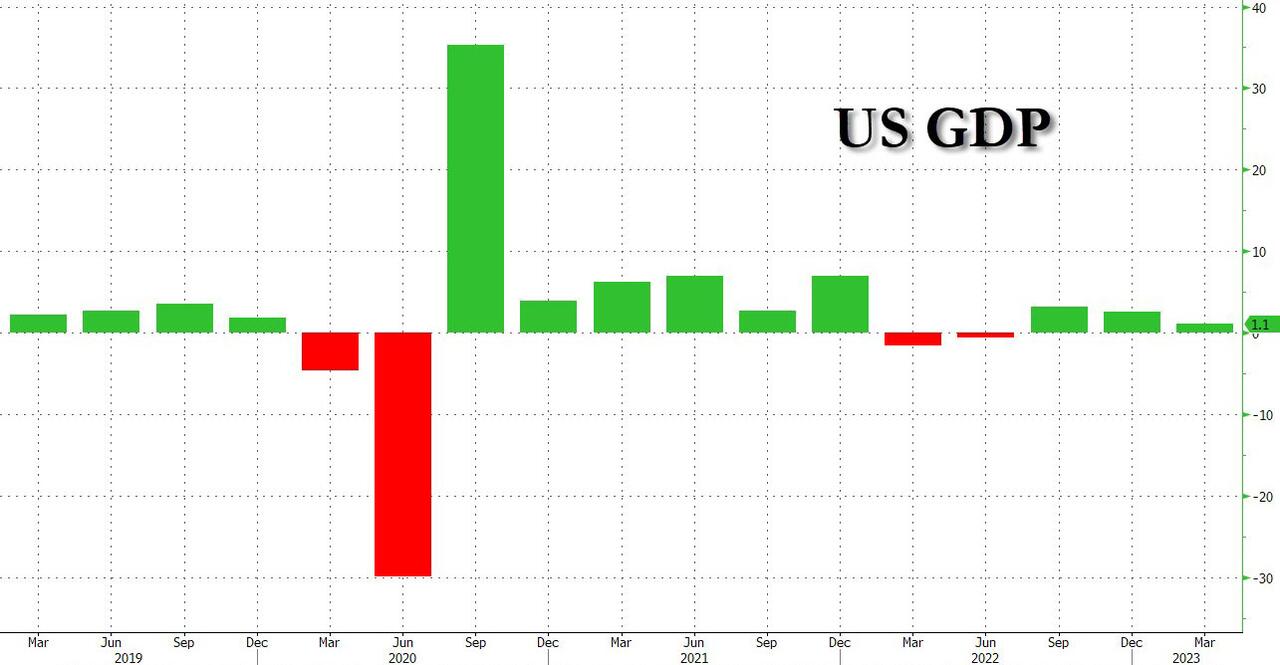

Meanwhile, the Atlanta Fed’s GDPNow is down 1.5% from March’s 3.2% figure.

But hey, who needs growth, productivity, tax receipts or even a modicum of national economic health to keep a liquidity-supported stock market from defying reality—at least for now…

Waiting to Pay the Debt Piper…

Ultimately, of course, debt will get the last, cruel laugh, and with the US heading toward a deficit that is greater than 50% of GLOBAL GDP (!), I personally believe the Fed will need to return to its own money printer in a big way once this market charade ends in an historical “uh-oh” moment.

This seemingly inevitable return to mouse-click trillions (inflationary) will likely come after a deflationary implosion in equity assets currently supported by the foregoing tricks and fantasy rather than earnings and growth.

In the interim, and like those hedge fund jocks discussed above, we can only wait for things to get S&P ugly as gold, often sympathetic in the first hours of a market crash, rips toward all-time highs thereafter.

end

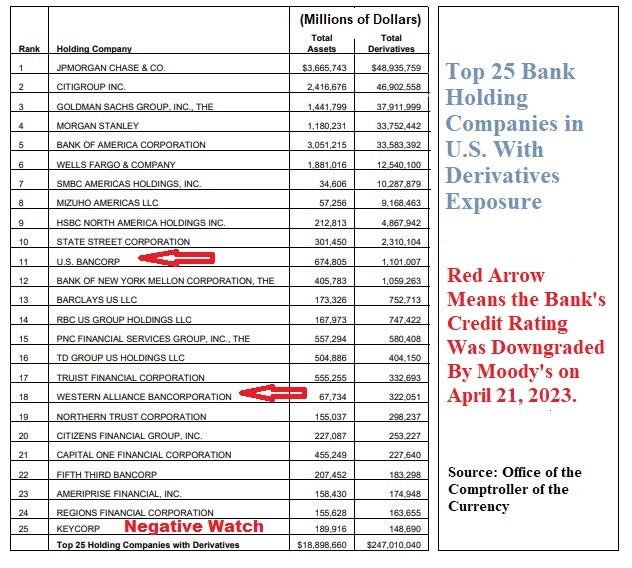

Banks that Put Up $30 Billion to “Rescue” First Republic May Have Been Trying to Rescue their Own Exposure to $247 Trillion in Derivatives

By Pam Martens and Russ Martens: April 27, 2023

Ever since 11 banks on March 16 donned the garb of heroic fire fighters, rushing to extinguish an inferno at a competitor bank before it spread further, we have been asking ourselves the question – why just this group of 11 banks.

We’re talking about the action on March 16 when 11 banks chipped in a total of $30 billion and bizarrely placed those funds as uninsured deposits into First Republic Bank – which was in full scale unraveling mode because of bond losses and – wait for it – too many uninsured deposits. Four banks contributed two- thirds of the total deposits with JPMorgan Chase, Bank of America, Citigroup and Wells Fargo ponying up $5 billion each. Morgan Stanley and Goldman Sachs deposited $2.5 billion each; while BNY Mellon, State Street, PNC Bank, Truist and U.S. Bank each deposited $1 billion, together making up the other one-third of the $30 billion.

According to the Federal Deposit Insurance Corporation, as of December 31, 2022 there were 4,706 federally-insured commercial banks and savings associations in the U.S. The 11 banks rushing to “rescue” First Republic Bank represent less than a fraction of one percent of the total banks.

Banking in the U.S. is not particularly regarded as an altruistic industry. In fact, it frequently resembles a blood sport. So why this uncanny display of generosity to a competitor and why were just these 11 banks involved?

Yesterday, we had an epiphany. We pulled up the most recent table from the Office of the Comptroller of the Currency showing the 25 bank holding companies that have the largest exposure to derivatives. Sure enough, each of those 11 banks is on the list. (See page 19 at this link.) The data is as of December 31, 2022.

Equally noteworthy, the four banks that chipped in the giant sums of $5 billion each, control 58 percent of the total $247 trillion notional (face amount) in derivatives controlled by all 25 banks.

And if that wasn’t already plenty to raise one’s blood pressure, for many of these banks the dollar amount of derivatives is exponentially more than the total assets of the bank holding company. For example, SMBC Americas Holdings, Inc. has $34.6 billion in assets and $10.3 trillion in derivatives. (You can’t make this stuff up.)

It also caught our eye that three of the 25 banks on this list had their credit ratings impacted by the big action taken by Moody’s on April 21 when it downgraded the credit ratings of 11 banks on that date and put five more on negative watch. (See chart below.)

So let’s look back a little further at what was going on in terms of credit ratings during the two days just preceding that $30 billion display of goodwill toward First Republic Bank.

On Monday, March 13, Moody’s downgraded the entire U.S. banking system outlook to negative from stable. On that same date, a bank with ties to crypto customers, Metropolitan Commercial Bank, lost 44 percent of its market value and a California regional bank, Western Alliance Bancorp, lost 47 percent of its market value. By Wednesday morning, March 15, Dow futures were down more than 600 points just after 8:00 a.m. in New York; major banks in Europe had been temporarily halted from trading after steep selloffs; and Credit Suisse, with deep interconnections to the mega banks on Wall Street, had plunged to less than 2 bucks.

Also, on March 15, the Wall Street Journal ran this subhead: “JPMorgan, Bank of America, Citigroup and Wells Fargo have lost about $91 billion in market value over the past week,” indicating that the contagion had spread to the biggest banks.

To put it succinctly, the actions of those big derivative banks on March 16 might have had a lot more to do with white knuckles over the potential for this contagion to focus on the big derivative counterparty banks than a warm and fuzzy feeling toward First Republic Bank.

-END-

3,Chris Powell of GATA provides to us very important physical commentaries

Craig Hemke…

Craig Hemke’s options price balancing successfully predicts Comex gold price

Submitted by admin on Thu, 2023-04-27 05:45Section: Daily Dispatches

4:43p ICT Thursday, April 27, 2023

Dear Friend of GATA and Gold:

Comex gold futures options levels seem to have predicted the closing price of the June Comex gold contract just as the TF Metals Report’s Craig Hemke said it would, “near or just below $1,990,” more evidence of market manipulation by the bullion banks that buy and sell the options.

But Hemke counsels against despair for gold investors, writing:

“Even though there have now been criminal convictions for precious metals price manipulation, the bullion bank trading desks continue to attempt to manage price on a daily basis. Knowing this will allow you to better time your purchases of physical metal going forward.

“Additionally, you must understand that, even though the manipulation continues, prices can and will go higher regardless. Recall that Comex gold was $300 in 2003 and $1,100 in 2015. It’s now near $2,000 and the average annual gain in dollar terms this century is 9.3%.”

Hemke’s analysis is headlined “Comex Gold Options Update” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/blog/COMEX-gold-options-update-april-26-2023

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

4. OTHER GOLD/SILVER RELATED COMMENTARIES/

END

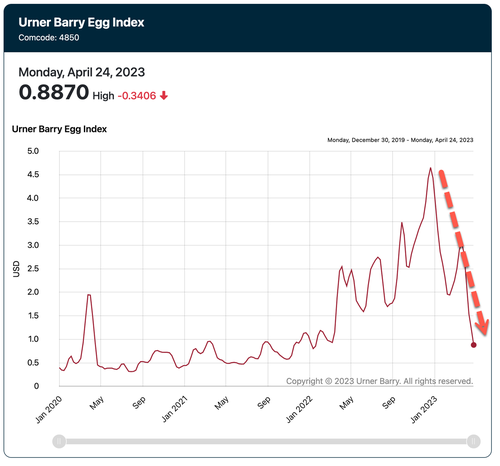

5.IMPORTANT COMMENTARIES ON COMMODITIES: EGGS

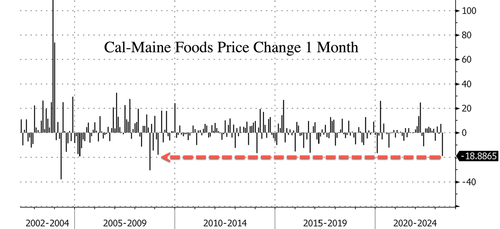

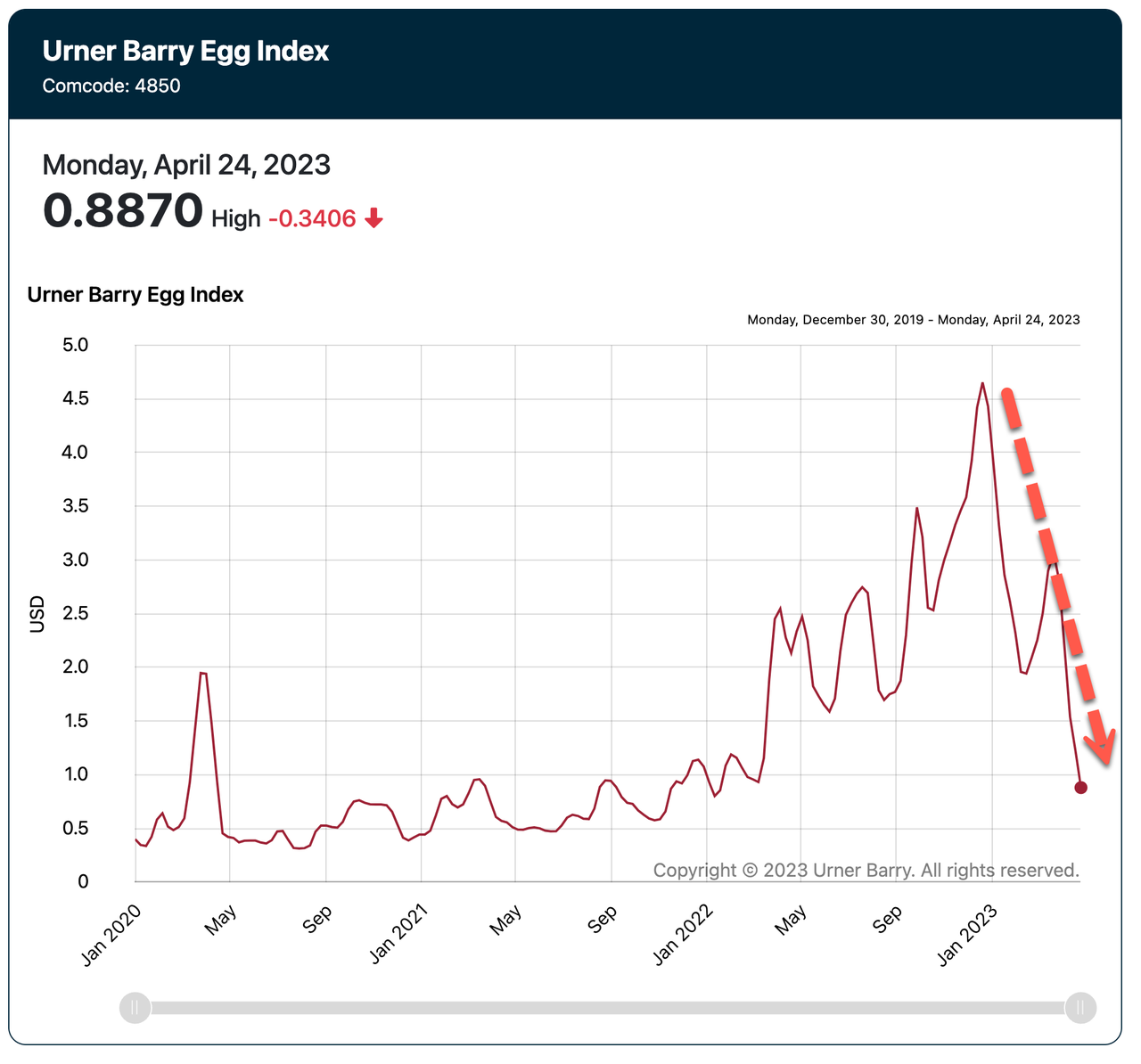

Eggflation Ends With Cal-Maine Shares Down The Most Since 2008

THURSDAY, APR 27, 2023 – 06:55 AM

On Tuesday, financial services firm Stephens Inc. lowered their rating of Cal-Maine Foods from overweight to equal weight, pointing to concerns about plunging wholesale egg prices as the reason.

Stephens research analyst covering the consumer staples, food and agribusiness, and grocery/c-store sectors Ben Bienvenu said in a recent conference call with Urner Barry, a market research firm that tracks wholesale food prices, that wholesale egg price trends were “understandably more downbeat.”

“When considering what’s currently playing out for eggs, we think it is best for us move to the sidelines on Cal-Maine as we think risk/reward is now more balanced,” the analyst said.

Bienvenu is one of a handful of Wall Street analysts covering Cal-Maine. He said collapsing egg prices threaten to depress the earnings of the egg producer, which recorded revenue last quarter that was more than double the same period last year. Net income for the company jumped more than 700% to $323 million.

Cal-Maine shares are down 19%, the most significant monthly plunge since September 2008. The analyst lowered his price target to $60 from $67. Shares currently trade around the $49 handle.

On Feb. 6, we were the first to point out: We’ve Got Great News: Wholesale Egg Prices “Collapse.”At the time, the index of wholesale egg prices plunged from around $4.65 to $2.01. Now the index stands at .887 cents.

Bienvenu said that a crucial factor for Cal-Maine investors to keep an eye on is the potential re-emergence of bird flu:

“While there certainly could still be cases that arise, and that would negatively impact production and consequently result in higher prices, we think at this point it is prudent to no longer recommend putting new money to work in the space.”

Retail egg prices at supermarkets have already begun to slide after the worst avian flu outbreak ever devastated domestic egg-laying bird populations last year.

Now comes egg deflation unless bird flu reemerges.

end

GLOBAL COMMODITIES ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY COMMENTARIES/

1.YOUR EARLY CURRENCY/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS//,THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 6.9232

OFFSHORE YUAN: 6.9348

SHANGHAI CLOSED UP 21.78 POINTS OR 0.67%

HANG SENG CLOSED UP 83.01 PTS OR 0.42%

2. Nikkei closed UP 41.21 PTS OR 0.14%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 101.155 EURO FALLS TO 1.1036 DOWN 9 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.456Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 133.48 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion usa

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.4095***/Italian 10 Yr bond yield RISES to 4.296*** /SPAIN 10 YR BOND YIELD RISES TO 3.457…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 4.192

3j Gold at $1997.25 silver at: 25.00 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 14 /100 roubles/dollar; ROUBLE AT 81.48//

3m oil into the 74 dollar handle for WTI and 77 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 133.48 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .456% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8932 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9858 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.458 UP 3 BASIS PTS…GETTING DANGEROUS//

USA 30 YR BOND YIELD: 3.727 UP 4 BASIS PTS/

USA 2 YR BOND YIELD: 3.955 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 19.43…

GREAT BRITAIN/10 YEAR YIELD: UP 3 BASIS PTS AT 3.7585

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

S&P Futures Rise Above 4,100 Propelled By Tech Earnings, Rate Hike Doubts

THURSDAY, APR 27, 2023 – 08:13 AM

US index futures gained on Thursday halting a two-day drop, led by the tech stocks, after Meta’s better-than-expected results helped mitigate investor concerns about the F(ailing)irst Republic Bank, economic outlook, inflation and monetary policy. S&P 500 futures traded just above 4,100, rising 0.7% as of 8:00 a.m. ET, while Nasdaq 100 futures rose 0.9%, extending Wednesday’s gains as the tech-heavy benchmark continues its outperformance of the broader market this year. According to JPM, “this week’s Equity performance highlights the divergence due to low market breadth” something we discussed yesterday. European stocks gained and were set to snap a three-day losing streak as Barclays, AstraZeneca and Unilever all rise after their respective updates. Asian markets were also green after a rebound in Chinese stocks. USD is weaker, longer-dated yields are higher, and commodities are mixed before US GDP and jobless claims to gauge the strength of the US economy. Yields on five-year notes dropped the most in a month on Tuesday, spurred by a wave of quant investors. The Federal Reserve’s preferred inflation gauge, the core PCE deflator, is due Friday.

In premarket trading, Meta jumped as much as 11%, helping fuel gains in Snap and Amazon, both of which report after the close. First Republic Bank rose 2.8% after tumbling 64% in the previous two sessions. Cryptocurrency-exposed stocks also rose in premarket as Bitcoin gained for a third consecutive day, inching toward the closely watched $30,000 mark. Here are all the notable pre-market movers:

- EBay rose as much as 3.1% after the e-commerce company forecast better-than-expected net revenue for the second quarter. Analysts noted that the company’s focus categories, which include refurbished products and collectibles, outperformed the rest of the marketplace.

- Eli Lilly & Co. shares are up 4% after the pharmaceutical company reported first-quarter revenue that beat expectations, with sales for its Mounjaro antidiabetic medication notably above the consensus estimate. It also raised its forecast.

- Electronic Arts shares dip 0.5% after BMO Capital Markets downgrades the video- game company to market perform from outperform. Analysts led by Gerrick Johnson say the UK Competition and Markets Authority’s decision to block Microsoft’s acquisition of Activision could have wider implications for consolidation in the video-game industry, a key component to their buy-rated thesis for Electronic Arts.

- Enovix falls 5.3% as analysts say the silicon-battery company is signaling a slower-than-expected ramp at its Fab-2 manufacturing facility.

- Impinj shares are down ~25% in premarket trading on Thursday, after the maker of radio- frequency identification chips gave a second-quarter forecast that is weaker than expected.

- Jefferies gains 9% after SMBC Group announced plans to raise its economic ownership in the US firm to up to 15% on an as converted and fully diluted basis.

- Meta Platforms rose as much as ~12% on Thursday, after the Facebook parent forecast second-quarter revenue that beat expectations.

- Mobileye fell as much as 18% on Thursday — poised for its worst session ever since its debut last year if those declines hold — after the software and hardware maker for cars cut its revenue guidance for the full year.

- Seres Therapeutics shares surge, set for their biggest gain in six months, after the developer of biological drugs received FDA approval for its therapeutics Vowst to prevent the recurrence of C. difficile Infection (CDI) in adults.

- Southwest Air shares are down ~4% after the company’s first-quarter results missed analysts’ estimates.

- Vornado Realty shares dropped as much as 13% after the owner of offices delayed its dividend and authorized up to $200 million in buybacks, a move which surprised analysts and prompted a downgrade from Piper Sandler.

- Wolfspeed shares drop as much as ~15% after the maker of semiconductors gave a revenue forecast for the fourth quarter that fell short of estimates. Analysts cut price targets amid the company’s challenges in ramping its Mohawk Valley manufacturing facility

- Cryptocurrency-exposed stocks rise as Bitcoin climbs for a third consecutive session, again inching toward the closely watched $30,000 mark. Hut 8 Mining +7.4%, Marathon Digital +5.7%

Coming on the heels of strong earnings from Microsoft, Meta’s results buoyed sentiment as investors weigh risks from banking-sector turmoil and the likelihood of a US recession. GDP and jobless claims data later on Thursday, as well as the core PCE deflator due on Friday, could provide further clues about the Federal Reserve’s likely interest-rate path. “Tech seems to be acting as somewhat of a haven trade,” said Michael Hewson, chief analyst at CMC Markets in London.

The potential for a tightening of credit conditions linked to the banking turmoil may prompt the Fed to adjust the pace of its interest-rate increases, Evercore ISI’s head of central bank strategy Krishna Guha wrote in a note, citing issues at First Republic Bank. The US regional lender faces potential curbs on borrowing from the Fed.

“We cannot rule out the possibility developments around First Republic could unfold in a manner that would lead the FOMC to skip May, while signaling a hike in June,” Guha said.

Europe’s Stoxx 600 is up 0.2% and looking to snap a three-day losing streak as Barclays, AstraZeneca and Unilever all rise after their respective updates. Sanofi’s profit topped stimates as the French drugmaker’s blockbuster therapy Dupixent gained market share. AstraZeneca’s profit also rose in the first quarter, helped by sales of its blockbuster oncology treatments. Deutsche Bank AG dropped after trading revenue disappointed. Here are the biggest movers Thursday:

- SimCorp shares jump 39% to match the DKK735 price offered by Deutsche Börse to acquire the Danish financial software maker.

- Nel shares rally as much as 18%, most since July after posting 1Q results that Citi says are broadly supportive, noting that the Norwegian hydrogen equipment maker’s revenue beat consensus

- GN Store Nord jumps as much as 11% after the Danish hearing-aid and audio-equipment maker reported a strong set of earnings, with Handelsbanken highlighting a strong product launch in 4Q

- Unilever shares jump as much as 2% after the consumer-goods company reported underlying sales that beat estimates. Analysts said the results were good, highlighting better-than-expected volumes

- HelloFresh rises as much as 9.1% as the meal-kit company’s profitability beats estimates. Analysts say the firm is relying on a recovery in 2H as the toughest comparison of the year has now passed

- Barclays shares rise as much as 5.1% in early trading after the UK lender’s investment banking arm drove a first-quarter profit beat, which however was partially offset by a miss for costs

- Schneider Electric rises as much as 1.7% after the French maker of electrical products posted strong 1Q sales, as well as FY targets that RBC says imply higher consensus estimates

- STMicro shares fall by as much as 8.2% following second-quarter earnings. The strong results didn’t surprise after peer Infineon confirmed still-resilient demand for semiconductors earlier

- Tenaris shares fall as much as 6% in Milan after it flagged a sequential decline in sales and profit margins throughout 2023 which eclipsed positives from record 1Q sales and an earnings beat

- BASF shares slide as much as 4.6% after warning of a subdued demand outlook for its chemicals, though the firm reaffirmed its adjusted Ebit forecast for the year

- Universal Music Group drops as much as 6.9% with analysts saying a first-quarter beat was driven by less- predictable physical music sales, rather than the more recurring streaming line

- Deutsche Boerse shares fall as much as 7.5% as the German exchange operator announced the acquisition of Danish financial software firm SimCorp and reported an unimpressive 1Q beat

Pharmaceuticals are well-positioned to weather recession, according to Janet Mui, the head of market analysis at RBC Brewin Dolphin, who recommends shifting to defensives. “There has been some weakening in credit data which suggests it’s getting more difficult to get a loan,” Mui told Bloomberg TV. “This raises a chance of recession by the end of the year.”

Earlier in the session, Asian stocks rebounded as China markets extended gains, with investors digesting a slew of corporate earnings for clues on the recovery’s strength. The MSCI Asia Pacific Index erased losses to advance as much as 0.2%, set to snap a four-day losing streak. Ping An Insurance was among the biggest boosts after reporting a surge in its first-quarter profit as China’s rebound helped demand and investment returns. Financials hauled up mainland China and Hong Kong indexes in afternoon trading. Markets in the region were mixed, with stocks also advancing in South Korea, Japan and Taiwan while indexes in Thailand and Singapore posted declines. Investors were focused on results including those from tech heavyweight Samsung Electronics, which reported worse-than-expected earnings but gave an upbeat outlook.

Investors also parsed earnings from Chinese lenders following the recent pullback in mainland equities that at one point wiped out $446 billion in market value in April. China Merchants Bank fell in Hong Kong after reporting a softer set of first-quarter results than analysts had expected. The recent rout may offer “a good opportunity for long-term investors” in reopening bets, according to Pruksa Iamthongthong, senior investment director of Asian equities at abrdn. “The market itself had moved very much ahead in terms of expectations so the pullback that we have seen in first quarter results is actually a good thing.

Japanese stocks closed slightly higher as investors continue to digest earnings from key corporates amid resurfaced concerns over US regional banks. The Topix rose 0.4% to close at 2,032.51, while the Nikkei advanced 0.1% to 28,457.68. Sony contributed the most to the Topix gain, rising 3.5% after UK regulators decided to block Microsoft’s purchase of Activision Blizzard. Out of 2,158 stocks in the Topix, 1,149 rose and 905 fell, while 104 were unchanged. “While Japanese stocks started the day lower on the back of weaker US market, earnings results from major tech companies were good,” said Hirokazu Kabeya, chief global strategist at Daiwa Securities. The market is in a “wait-and-see mood” ahead of the BOJ meeting tomorrow, where the focus will be on inflation outlook, he said.

Australian stocks declined for a 5th straigh session, with the S&P/ASX 200 index falling 0.3% to close at 7,292.70. Banks and health shares contributed most to the benchmark’s decline. The drop comes after US shares fell for a second day as concern over American regional banks outweighed better-than-expected technology earnings. In New Zealand, the S&P/NZX 50 index fell 0.1% to 11,918.22

Stocks in India surged for sixth consecutive session as investors remain optimistic of earnings recovery after initial disappointment from top technology names. The S&P BSE Sensex Index rose 0.6% to 60,649.38 in Mumbai, while the NSE Nifty 50 Index advanced by a similar measure. The gauges have risen more than 1% this week as earnings season rolls out. Software makers Wipro and Tech Mahindra will be reporting earnings for the March quarter later on Thursday. Hindustan Unilever disappointed with lower than expected profit on account of weaker margins as the FMCG major struggles to increase sales volumes. Infosys contributed the most to the Sensex’s gain, increasing 1.5%. Out of 30 stocks in the index, 23 rose and seven fell.

In FX, the Bloomberg Dollar Spot Index slipped 0.1% while the Treasury two-year yield fell one basis point to 3.94% ahead of key US jobless claims and GDP data. Risk-sensitive currencies including the New Zealand dollar and Scandinavian currencies outperformed other Group-of-10 peers amid improving risk appetite. “With the Federal Reserve nearing the end of its rate-hiking cycle, we continue to expect the global macro outlook to translate into an unwinding of previous USD overvaluation over the medium term,” Bank of American strategists wrote in a note

- The Yen was little changed at 133.69 per dollar after former Bank of Japan Governor Masazumi Wakatabe said there is a possibility that the central bank will change the wording of its forward guidance without adjusting its easing bias at the end of its policy meeting Friday. “There’s thin trading ahead of the BOJ decision tomorrow, and likely some technical pullbacks on the dollar which allows currencies like the kiwi to gain,” said Mingze Wu, an FX trader at StoneX Group

- EUR/USD little changed around 1.1047 after rising to 1.1095, highest for more than a year, on Wednesday. Recent rally was “testament to how markets seem to favour the euro among other currencies in instances when the dollar falls on the back of Fed dovish repricing and US banking concerns,” according to ING Bank strategist Francesco Pesole. A break above $1.1100 could trigger another substantial rally in the pair, he added

- GBP/USD fell 0.2% to 1.2442 in quiet trade, holding close to its highest level in nearly two weeks. The pound could see a slow move higher given that a less downbeat view of the UK economy has boosted speculative flows into the currency, according to HSBC. “Encouraging activity data, higher rates from the BoE, and a market which is not stretched in terms of positioning should offer further upside,” its strategists wrote in a note

- USD/CHF rose 0.3%

- NZD/USD climbed 0.4% to 0.6142; AUD/USD rose 0.1% to 0.6608

In rates, Treasuries were mixed, slightly cheaper at long-end of the curve where 20- and 30-year yields are up ~1bp vs Wednesday’s close following similar shift in German curve. US 10-year yields around 3.45%, little changed on the day, outperforming bunds slightly in the sector. German 10-year yields are up 3bps. The Treasury auction cycle concludes with $35b 7-year note sale; 2- and 5-year auctions produced good demand metrics. WI 7-year yield at 3.475% is ~15bp richer than last month’s, which tailed by 1.1bp.

In commodities, Crude futures advance with WTI up 0.3% to trade near $74.50 after a Wednesday fall. Gold traded near the highest level in a week and Bitcoin resumed an advance. Hong Kong Securities and Futures Commission chief said will issue crypto exchange guidelines in May.

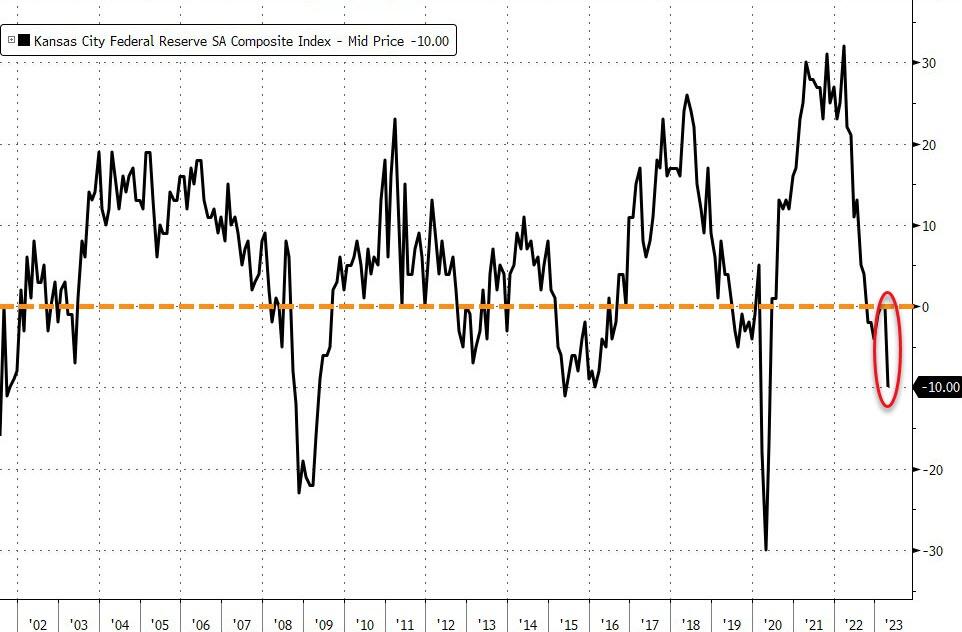

Focal points of US session include weekly jobless claims and 1Q GDP estimate, followed by 7-year note auction at 1pm New York time. Economic data includes initial jobless claims and 1Q GDP estimate (8:30am), March pending home sales (10am) and April Kansas City Fed manufacturing activity (11am). Fed slate remains blank with members in communication blackout period ahead of May 3 policy announcement. On the earnings side, today’s releases include Amazon, Mastercard, Eli Lilly, and Intel.

Market Snapshot

- S&P 500 futures up 0.5% to 4,096.00

- MXAP up 0.2% to 160.08

- MXAPJ up 0.2% to 511.87

- Nikkei up 0.1% to 28,457.68

- Topix up 0.4% to 2,032.51

- Hang Seng Index up 0.4% to 19,840.28

- Shanghai Composite up 0.7% to 3,285.89

- Sensex up 0.4% to 60,556.84

- Australia S&P/ASX 200 down 0.3% to 7,292.75

- Kospi up 0.4% to 2,495.81

- STOXX Europe 600 up 0.2% to 463.95

- German 10Y yield little changed at 2.43%

- Euro up 0.1% to $1.1057

- Brent Futures up 0.6% to $78.12/bbl

- Gold spot up 0.5% to $1,999.36

- U.S. Dollar Index down 0.11% to 101.36

Top Overnight News

- China’s industrial firms’ profits shrank at a slightly slower pace in January-March but the decline remained in the double-digits as the economy struggled to fully recover despite the country’s exit from its zero-COVID policy. In March alone, profits for the sector fell 19.2%, according to the data by the NBS which only occasionally discloses monthly figures. RTRS

- Former BOJ Deputy Governor Masazumi Wakatabe said there is a possibility that the central bank will change the wording of its forward guidance without adjusting its easing bias at the end of its policy meeting Friday. BBG

- Deutsche Bank and Barclays buoyed the market with solid results. The German firm posted its strongest top line since 2016, as a 35% jump in revenue at the corporate bank more than offset a 17% slide in fixed income trading. It laid out plans to cut about 800 senior back-office staff. DWS signaled recovery, with net inflows of €5.7 billion. Barclays beat as its trading helped offset a drop in dealmaking. Fixed income sales unexpectedly rose 9%, outweighing a slump in equities. BBG

- Russian Deputy Prime Alexander Novak said on Thursday the OPEC+ group of leading oil producers saw no need for further output cuts despite lower-than-expected Chinese demand, but that the organization can always adjust policy if necessary. RTRS

- Germany is in talks to limit the export of chemicals to China that are used to manufacture semiconductors, people familiar said. Such a step would limit German companies like Merck and BASF from selling some of their semiconductor chemicals to China. Merck’s products or services are found in almost every single chip in the world, while BASF is a market leader in Europe and Asia. BBG

- UniCredit will exercise the option to redeem an AT1 bond early in the first major test for such calls since the wipeout of $17.3 billion of Credit Suisse notes. It’ll repay the €1.25 billion note at face value June 3. Its price jumped 1.8 cents to around 100.2 cents on the euro, based on data compiled by Bloomberg. There’s been doubt over whether banks would follow convention and exercise AT1 calls as the cost of issuing replacement bonds jumped after the writedown. BBG

- Opec accused the International Energy Agency on Thursday of stoking “volatility” in energy markets, in an intensifying war-of-words between oil producers and consumers. FT

- Florida Gov. Ron DeSantis is poised to jump into the presidential fray as soon as mid-May, four GOP operatives familiar with the conversations told NBC News. NBC News