JUNE 12//ANOTHER T.A.S. INDUCED GOLD AND SILVER RAID: GOLD CLOSED DOWN $7.10 TO $1955.50, SILVER CLOSED DOWN $.26 TO $23.98//PLATINUM CLOSED DOWN $19.95 TO $994.15 WHEREAS PALLADIUM CLOSED UP $22.45 TO $1346.85//IMPORTANT GOLD COMMENTARIES TODAY FROM MATHEW PIEPENBURG AND MICHAEL MAHARRY OF SCHIFFGOLD//ALSO AMBROSE EVANS PRITCHARD ON THE PLIGHT OF CHINA AND WHAT IT MEANS TO US://CHINA AND USA CONFIRM THAT CHINA ORCHESTRATED SPY RINGS IN CUBA SPYING ON USA//GERMANY WILL HAVE ENERGY PROBLEMS FOR QUITE SOME TIME//COVID 19 PROVEN TO COME FROM WUHAN LAB//LAW SUITS FLYING OVER COVID VACCINE/DR PAUL ALEXANDER//SLAY NEWS/EVOL NEWS//UPDATES ON RUSSIAN UKRAINE WAR//UPDATES ON CANADIAN FIRES AND QUALITY OF AIR//HUGE SWAMP STORIES FROM GATEWAY PUNDIT ON THE CROOKED BIDEN FAMILY//OTHER SWAMP STORIES FOR YOU TONIGHT//

323 C HSBC 2 323 H HSBC 1 661 C JP MORGAN 3 737 C ADVANTAGE 3 880 H CITIGROUP 1

TOTAL: 5 5 MONTH TO DATE: 18,022

JPMorgan stopped 3/5 contracts

FOR JUNE:

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2023. CONTRACT: 5 NOTICES FOR 500 OZ or 0.1555 TONNES

total notices so far: 18,022 contracts for 1,802,200 oz (56.055 tonnes)

FOR JUNE:

SILVER NOTICES: 2 NOTICE(S) FILED FOR 10,000 OZ/

total number of notices filed so far this month : 423 for 2,115,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $7.10

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

/NO CHANGES IN GOLD INVENTORY AT THE GLD:////

INVENTORY RESTS AT 934,65 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 7 CENTS AT THE SLV//

SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 550,000 OZ FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 467.269 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY AN ATMOSPHERIC SIZED 2610 CONTRACTS TO 145,963 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUMONGOUS SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR TINY $0.07 GAIN IN SILVER PRICING AT THE COMEX ON FRIDAY. TAS ISSUANCE WAS AN ULTRA- HUMONGOUS SIZED 2770 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH . CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON FRIDAY NIGHT: A MONSTER SIZED 2772 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.07). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A HUGE GAIN ON OUR TWO EXCHANGES OF 2670 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 2.5MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION.

WE MUST HAVE HAD:

A FAIR SIZED ISSUANCE OF EXCHANGE FOR PHYSICALS( 400 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.935 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S 5,000 OZ QUEUE JUMP + 2.5 MILLION OZ EXCHANGE FOR RISK(ISSUED PRIOR)// TOTAL STANDING FOR THE MONTH 4.775MILLION OZ ) // HUMONGOUS SIZED COMEX OI GAIN/ FAIR SIZED EFP ISSUANCE/VI) HUMONGOUS NUMBER OF T.A.S. CONTRACT INITIATION (2772CONTRACTS)//ZERO T.A.S LIQUIDATION THROUGHOUT THE COMEX SESSION //FRIDAY //

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -ADDED 340 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTRACTS for 7 days, total 3909 contracts: OR 19.545 MILLION OZ (558 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 19.545 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 19.545 MILLION OZ//

RESULT: WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2610 CONTRACTS WITH OUR RISE IN PRICE OF $0.07 IN SILVER PRICING AT THE COMEX//FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE CONTRACTS: 400 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.935 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ E.F.P. JUMP+ 2.5 MILLION EXCHANGE FOR RISK(PRIOR)//NEW TOTAL STANDING: 6.775 MILLION OZ////// .. WE HAVE A GIGANTIC SIZED GAIN OF2670 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUMONGOUS 2670//ZERO FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE FRIDAY SESSION. THE NEW TAS ISSUANCE TODAY (2772) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE.

WE HAD 2 NOTICE(S) FILED TODAY FOR 10,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 702 CONTRACTS TO 435,890 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED – 292 CONTRACTS

WE HAD A SMALL SIZED DECREASE IN COMEX OI ( 994 CONTRACTS) WITH OUR $1.00 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JUNE. AT 70.79 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0.0528 TONNE E.F.P JUMP TO LONDON.: NEW TOTAL 62.855 TONNES STANDING SO FAR // + /A HUMONGOUS ISSUANCE OF 2563 T.A.S. CONTRACTS/SOME FRONT END OF TAS LIQUIDATION FRIDAY ////YET ALL OF..THIS HAPPENED WITH A $1.00 LOSS IN PRICEWITH RESPECT TO FRIDAY’S TRADING.WE HAD A SMALL SIZED LOSS OF 467 OI CONTRACTS (1.452 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 527 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 435,598

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 467 CONTRACTS WITH 994 CONTRACTS DECREASED AT THE COMEX//TAS CONTRACTS INITIATED (ISSUED): A HUGE 2563 CONTRACTS) AND 527 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 467CONTRACTS OR 1.452 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (527 CONTRACTS) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (994) //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 467 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 70.79 TONNES FOLLOWED BY TODAY’S 1,700 OZ E.F.P. JUMP TO LONDON//// NEW STANDING FALLS TO 62.855 TONNES// /3) ZERO LONG LIQUIDATION//4) SMALL SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: HUMONGOUS T.A.S. ISSUANCE: 2772 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

TOTAL EFP CONTRACTS ISSUED: 15,686 CONTRACTS OR 1,568,600 OZ OR 48.79 TONNES IN 7 TRADING DAY(S) AND THUS AVERAGING: 2240 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAY(S) IN TONNES 48.79 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 48.79/3550 x 100% TONNES 1.380% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 48.79 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUMONGOUS SIZED 2610 CONTRACTS OI TO 145,963 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 400 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1011 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 400 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2670 CONTRACTS AND ADD TO THE 400OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 3010 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 15.050 MILLION OZ

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

MONDAY MORNING//SUNDAY NIGHT

SHANGHAI CLOSED DOWN 2.59 PTS OR 0.08% //Hang Seng CLOSED UP 14.36 PTS OR 0.07% /The Nikkei closed UP 168.88 OR 0.52% //Australia’s all ordinaries CLOSED UP 0.33 % /Chinese yuan (ONSHORE) closed DOWN 7.1424 /OFFSHORE CHINESE YUAN DOWN TO 7.1517 /Oil DOWN TO 68.47 dollars per barrel for WTI and BRENT UP AT 76.26 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 994 CONTRACTS DOWN TO 435,598 WITH OUR LOSS IN PRICE OF $1.00 ON FRIDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE… THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 527 EFP CONTRACTS WERE ISSUED: : AUGUST 527 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 527 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 467 CONTRACTS IN THAT 527LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED LOSS OF 702 COMEX CONTRACTS..AND THIS SMALL SIZED LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $1.00. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR FRIDAY NIGHT WAS A GIGANTIC 2563 CONTRACTS. THROUGHOUT LAST WEEK, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THIS SPELLS TROUBLE AHEAD AS ANOTHER RAID WILL SURELY BE UPON US!

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (62.855) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 62.855 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $1.00) //// AND WERE SUCCESSFUL IN KNOCKING A FEW SPECULATOR LONGS AS WE HAD OUR SMALL SIZED LOSS OF 467 CONTRACTS ON OUR TWO EXCHANGES. WE HAD SOME TAS LIQUIDATION THROUGHOUT THE COMEX SESSION ON FRIDAY . THE TAS ISSUED FRIDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 1.452PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE. (70.709 TONNES) FOLLOWED BY TODAY’S 1700 OZ EFP JUMP TO LONDON..NEW STANDING REMAINS AT 62.855 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $1.00

WE HAD – REMOVED 292 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 467 CONTRACTS OR 46,700 OZ OR 1.452 TONNES.

Total monthly oz gold served (contracts) so far this month

18,022 notices 1,802,200 OZ 56.055 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

Withdrawals: 0

Adjustments;3 all dealer to customer:

a) Out of Manfra: 31,732.139 oz

b) Out of Brinks 10,031.112 oz

c) Out of Ashai: 11,460.720 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 2191 contracts having LOST 303 contracts. We had 286 contracts served on Friday so we lost 17 contracts or an additional 1700 oz will not stand for gold at the comex. as these guys were EFP’d over to London where they will exercise these contracts on the T + 2 basis and take delivery over there.

The next front month after June is the non active delivery month of July. Here, July lost 44 contracts to stand at 2862 contracts.

AUGUST lost 1294 contracts up to 370,907 contracts

We had 5 contracts filed for today representing 500 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 5 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 3 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2023. contract month,

we take the total number of notices filed so far for the month (18,022 x 100 oz ), to which we add the difference between the open interest for the front month of JUNE (2191 CONTRACT) minus the number of notices served upon today 5 x 100 oz per contract equals 2,020,800 OZ OR 62.855 TONNES the number of TONNES standing in this active month of June. (CME data corrected)

thus the INITIAL standings for gold for the JUNEcontract month: No of notices filed so far (18,022) x 100 oz + (2191) [OI for the front month minus the number of notices served upon today (5)x 100 oz} which equals 2,020,800 oz standing OR 62.855 TONNES

TOTAL COMEX GOLD STANDING: 62.855 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,912,629.517 OZ

TOTAL REGISTERED GOLD: 11,677,240.804 (363.211 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 11,243,388,7123 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,6621,994 OZ (REG GOLD- PLEDGED GOLD) 299.284 tonnes//

END

SILVER/COMEX

JUNE 12//2023// THE JUNE 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

87,988.760 oz cnt

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

542,609.500 oz jpm

No of oz served today (contracts)

2 CONTRACT(S) (10,000 OZ)

No of oz to be served (notices)

432 contracts (2,160,000 oz)

Total monthly oz silver served (contracts)

423 Contracts (2,115,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposits

total dealer deposit: nil oz

total dealer deposits: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We had one deposit customer account:

542,609.500 oz JPMorgan

total customer deposits: 542,609.500 oz

JPMorgan has a total silver weight: 142,466 million oz/273,527 million =52.08% of comex .//dropping fast

Comex withdrawals 1

i) 87,984.760 oz

total withdrawals: 87,984.760 oz

adjustments: none

TOTAL REGISTERED SILVER: 27.117 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 273.527 million oz

DEALER SILVER DROPPING FAST. (moves into the 27 million oz column)

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE /2023 OI: 434 CONTRACTS HAVING GAINED 1 CONTRACT(S).

WE HAD 0 NOTICES FILED ON FRIDAY SO WE GAINED 1 CONTRACTS OR AN ADDITIONAL 5,000 OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF JUNE

JULY HAD A 3759 CONTRACT LOSS TO 86,163 CONTRACTS

AUGUST GAINED 19 CONTRACTS TO STAND AT 30

SEPT HAS A GAIN OF 6207 CONTRACTS UP TO 48,397

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes// est. volume today 63,647 good /

Comex volume: confirmed yesterday:78,040 very strong

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 423 x 5,000 oz = 2,115,000 oz

to which we add the difference between the open interest for the front month of JUNE(434) and the number of notices served upon today 2 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2023 contract month: 423 (notices served so far) x 5000 oz + OI for the front month of JUNE (434) – number of notices served upon today (2 )x 500 oz of silver standing for the JUNE contract month equates to 4.275 million oz +2.5MILLION OZ EXCHANGE FOR RISK//NEW TOTAL: 6.775 MILLION OZ STANDING

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

JUNE 12/WITH GOLD DOWN $7.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.65 TONNES

JUNE 9/WITH GOLD DOWN $1.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.65 TONNES

JUNE 8/WITH GOLD UP $20.45 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.46 TONNES FROM THE GLD///INVENTORY RESTS AT 934.65 TONNES

JUNE 7 WITH GOLD DOWN $22.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 938.11 TONNES

JUNE 6/WITH GOLD UP $6.90 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 939.56 TONNES

JUNE 5/WITH GOLD UP $5.00 TODAY : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 938.11 TONNES

JUNE 2/WITH GOLD DOWN $24.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 938.11 TONNES

JUNE 1/WITH GOLD UP $14.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 939.56 TONNES

MAY 31/WITH GOLD UP $5.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 939.56 TONNES

MAY 30/WITH GOLD UP $14.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 26/WITH GOLD UP $.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 941.29 TONNES

MAY 25/WITH GOLD DOWN $19.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 24/WITH GOLD DOWN $9.50 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 941.29 TONNES

MAY 23/WITH GOLD $2.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 942.74 TONNES

MAY 22/WITH GOLD DOWN $4.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.83 TONES OF GOLD INTO THE GLD DESPITE THE L0SS IN PRICE//INVENTORY RESTS AT 942.74 TONNES

MAY 19/WITH GOLD UP $22.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 936.96 TONNES

MAY 18/WITH GOLD DOWN $23.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 936.96 TONNES

MAY 17/WITH GOLD DOWN $8.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.94 TONNES

MAY 16/WITH GOLD DOWN 28.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.57 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 934,07

MAY 15/WITH GOLD UP $2.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 937.64 TONNES

MAY 12/WITH GOLD DOWN $.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 937.84 TONNES

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 934.95 TONNES

MAY 9/WITH GOLD UP $9.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MONSTER DEPOSIT OF 5.88 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 937.64 TONNES

MAY 8/WITH GOLD UP $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 931.77 TONNES

MAY 5/WITH GOLD DOWN $30.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: AS DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 930.04 TONNES

MAY 4/WITH GOLD UP $19.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 928.30 TONNES

MAY 3/WITH GOLD UP $13.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.47 TONNES INTO THE GLD////INVENTORY RESTS AT 928.30 TONNES

MAY 2/WITH GOLD UP $32.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FORM THE GLD/////INVENTORY RESTS AT 924.83 TONNES

MAY 1/WITH GOLD DOWN $8.85 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 28/WITH GOLD UP $1.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 926.28 TONNES

APRIL 27/WITH GOLD UP $4.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 930.04 TONNES/

APRIL 26/WITH GOLD DOWN $8.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.61 TONNES FROM THE GLD.//INVENTORY RESTS AT 930.04 TONNES

APRIL 25/WITH GOLD UP $4.90 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 927.43 TONNES

APRIL 24/WITH GOLD UP $9.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 21/WITH GOLD DOWN $27.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 926.57 TONNES

APRIL 20/WITH GOLD UP $12.70: HUGE CHANGES TODAY IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.57 TONNES

APRIL 19//WITH GOLD DOWN $12.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 925.70 TONNES

GLD INVENTORY: 934.65 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 12/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.269 MILLION OZ//

JUNE 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF SILVER TO THE TUNE OF 550,000 OZ//INVENTORY RESTS AT 467.269 MILLION OZ

JUNE 8/WITH SILVER UP $0.63 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 467.819 MILLION OZ/

JUNE 7/WITH SILVER DOWN 17 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.01 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 467.819 MILLION OZ/

JUNE 6/WITH SILVER UP 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.809 MILLION OZ//

JUNE 5/WITH SILVER DOWN $.13 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 266,000 OZ FROM THE SLV////INVENTORY RESTS AT 466.809 MILLION OZ/

JUNE 2/WITH SILVER DOWN 23 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV./INVENTORY RESTS AT 467.015 MILLION OZ/

JUNE 1/WITH SILVER UP 49 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.933 MILLION OZ

MAY 31/WITH SILVER UP 37 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 367,000 OZ FROM THE SLV////INVENTORY RESTS AT 467.933 MILLION OZ//

MAY 30/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 26/WITH SILVER UP $0.44 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.306 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 25.WITH SILVER DOWN $0.32 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 471.606 MILLION OZ//

MAY 24/WITH SILVER DOWN $.35 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 23/WITH SILVER DOWN 22 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.801 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 22/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ//

MAY 19/WITH SILVER UP 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ

MAY 18/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.529 MILLION OZ/

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

MAY 16/WITH SILVER DOWN 34 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .643 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.448 MILLION OZ.

MAY 15/WITH SILVER UP 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.091 MILLION OZ/

MAY 12/WITH SILVER DOWN $.26 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 3,123 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 470.091 MILLION OZ./

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

MAY 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A TINY DEPOSIT OF .08 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 465.682 MILLION OZ//

MAY 8/WITH SILVER DOWN 7 CENTS: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 465.602 MILLION OZ//

MAY 5/WITH SILVER DOWN 31 CENTS TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 368,000 OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 466.876 MILLION OZ//

MAY 4/WITH SILVER UP 53 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL DEPOSIT OF .174 MILLION OZ INTO SLV.//INVENTORY RESTS AT 467.174 MILLION OZ//

MAY 3/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.194 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 467.070 MILLION OZ//

MAY 2/WITH SILVER UP 37 CENTS TODAY;NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 468.264 MILLION OZ//

MAY 1/WITH SILVER DOWN ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.264 MILLION OZ

APRIL 28/WITH SILVER UP 1 CENT TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.482 MILLION OZ//

APRIL 27/WITH SILVER UP 16 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.103 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.182 MILLION OZ//

APRIL 26/WITH SILVER UP 10 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.102 MILLION OZ FORM THE SLV////INVENTORY RESTS AT 470.285 MILLION OZ

APRIL 25/WITH SILVER DOWN 34 CENTS TODAY: THIS IS UNBELIEVABLE!!! HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 7.304 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.387 MILLION OZ.

APRIL 24/WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 464.083 MILLION OZ/

APRIL 21/WITH SILVER DOWN 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE GLD////INVENTORY RESTS AT 464.083 MILLION OZ//

APRIL 20/WITH SILVER UP 2 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.021 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 465.002 MILLION OZ/

The debt ceiling drama ended with fake budget cuts and a shiny new credit card with no limit for the federal government. We can now expect a big surge in the national debt as the US government plays catch up after nearly six months up against its borrowing limit.

And you can expect more eye-popping single-day national debt increases in the days ahead. In fact, it won’t surprise me if the national debt eclipses $32 trillion this week. Not only does the Treasury have to borrow to replenish its checking account (called the Treasury General Account or TGA at the New York Federal Reserve Bank), but it will also have to borrow to cover the budget deficits the Biden administration runs month after month.

And despite what Republicans tell you, spending is set to go up the next two years, even if Congress sticks to this deal. The US government is blowing through nearly half a trillion dollars every month and the deficit for fiscal 2023 was already close to $1 trillion with five months to go. The spending with its accompanying deficits isn’t ending in the foreseeable future.

What’s This Mean for Gold?

Typically, big spikes in the national debt correspond with a rising gold price.

Elements by Visual Capitalist put together a graphic showing how the price of gold typically tracks with big debt increases.

As you can see, the price of gold has generally trended upward along with the national debt. Of course, there are other factors that impact the price of gold, but the general trend is worth noting.

This correlation makes sense for a couple of reasons.

In the first place, a rising national debt creates economic uncertainty and that drives safe haven buying.

Even though the mainstream doesn’t talk much about the national debt, at some level, most people recognize that the trajectory is unsustainable. The longer the debt climbs and the political class kicks the can down the road, the shorter the road gets.

In the second place, a surging national debt will ultimately mean more inflation.

At some point, this unlimited borrowing is going to force the Federal Reserve to monetize some of this debt. That will require a return to quantitative easing.

Even if it doesn’t happen immediately, QE is in the future. There is no other way for the market to absorb all of the debt the Treasury will have to issue to support spending that will mostly go onto a credit card with no limits.

In order to prop up the bond market and keep prices higher than they otherwise would be (and interest rates lower), the Fed will ultimately have to buy bonds to boost demand. It will buy those Treasuries with money created out of thin air.

With this in mind, it makes sense that people would turn to gold as an inflation hedge.

Here is some raw data to go along with the chart.

At under $2,000 an ounce, gold has plenty of room to run up. And one thing is for certain — the debt problem isn’t going away.

When Humpty Dumpty fell off the wall and took a big fall, “all the king’s horses and all the king’s men could not put Humpty-Dumpty together again.”

I see a similar fate for the US debt egg, whose cracks are just about, well… everywhere.

Cracks in the Debt Egg

The first obvious (but media ignored) signs of this breaking egg emerged in September of 2019, when the TBTF banks no longer trusted each other’s collateral and the repo markets spiked overnight, prompting Uncle Fed to be the lender of last resort to its spoiled little banking nephews.

This required hundreds and hundreds of billions in mouse-clicked liquidity.

But then again, what does a billion or trillion even mean anymore to a mouse-clicker and $31+T (and growing) Public debt?

Numbers, like debts, have effectively become abstractions in what I previously described as a “banalization of debt.”

Since the repo crisis, as Uncle Sam’s twin deficits expanded at a fairytale pace alongside rising rate policies which neutered the price of sovereign bonds and hence the balance sheets and the life-cycles of regional banks, the Humpty-Dumpty US arrived at yet another climatic debt-ceiling reality-check.

Can-Kicking the Breaking Egg

As predicted, this “crisis” was “solved” by a predictable can-kicking of its debt responsibilities (and reality-checks) into a post-election-cycle.

How politically convenient.

In fact, political convenience at the expense of economic common sense or fiscal accountability is the very hallmark of our math-blind yet power-smug “representatives” in DC.

For those paying attention, however, the US not only voted past it’s $31.4T debt ceiling, it removed/suspended that ceiling all together.

This effectively allows the children in DC to borrow and spend without limit until 2025.

In short: The Humpty-Dumpty debt egg is getting fatter and fatter, and wobbling on the wall.

How a Dollar-Thirsty Humpty-Dumpty Wobbles

Having artificially “solved” (postponed) an otherwise very real/toxic debt crisis, the post-debt ceiling policy makers will now have to decide where the much-needed liquidity will come from to keep Humpty Dumpty alive, as debt (paid for with synthetic liquidity) is the only thing keeping him from a fall.

Re-Filling an Empty Treasury—Complex Games, with No Winners

Toward this end, the question is now about how much the US Treasury is willing to “liquify” (refill) a very thirsty Treasury General Account (TGA), which has been the invisible source of funding to offset the Fed’s mid-2022 policy of so-called balance sheet “tightening”?

Whenever Powell grabs headlines for “tightening” liquidity, the TGA quietly provides more of the same behind a TGA curtain of complexity.

But now that TGA needs a re-fill of USDs to continue this charade of musical-dollar-chairs.

Stated simply, there is a great big “sucking sound” coming from the TGA, which is thirsty, very thirsty for USDs.

Where Will the “Money” Come From?

Should the US Treasury make a generous liquidity injection into the TGA from bank reserves, this will dry up other corners of a breaking US system equally thirsty for similar injections of USDs.

In short: This liquidity option is dangerous and unlikely.

Alternatively, however, the Fed’s Reverse Repo liquidity water-cannon could spray the TGA with the necessary liquidity (USDs) to buy more of Uncle Sam’s IOUs and thus buy the TGA’s borrow-and-spend system more time rather than solutions.

In the past, the banks were buyers of these IOUs, but we all know how well that worked for them in 2023…

So, once again, and amidst all this deliberate DC confusion, the simple question remains: Who will buy the IOUs (Treasury Bills) needed to keep Humpty Dumpty alive?

The US Treasury’s bank reserves? The Fed’s Reverse Repo Program? The UST-weary banks? The Money Market Funds?

Yes, The Bond Market Is Still the Thing

To see through this maze more clearly, one must always look at the bond market, however “boring.”

If the Fed keeps raising rates and tightening its balance sheet, those T-Bills needed to keep Humpty Dumpty on the wall will fall in price and hence rise in yields, becoming far more expensive for Uncle Sam to repay?

This is a problem.

Yellen In a Corner and Waking to Reality?

But perhaps far more important, and far less discussed or understood, is Yellen’s preference to issue IOUs to refill the TGA from the short end of the duration spectrum (i.e., short-term T-Bills) rather than longer-term UST bonds.

But would it not be cheaper for Uncle Sam to issue longer-term bonds at lower yields (interest expense) to continue his debt orgy of extend and pretend?

In short: What the heck is going on behind the scenes of Yellen’s Treasury Department?

Yellen, many argue, is still under the illusion that the UST market in general, and the US T-Bill market in particular, is the safest, most loved and hence most liquid IOU in the world.

But even Yellen can not have ignored the simple fact that a post-sanction world of weaponized dollars is dumping (rather than buying) those IOUs and stacking gold instead…

Perhaps Yellen is now desperately aware that to keep the debt Humpty Dumpty egg alive, she’ll now have to issue more and more “yield-sexy” (but harder-to-repay) T-Bills to buy time in a debt-soaked nation that is running out of time?

But far more ominously, perhaps Yellen is slowly coming to a sober conclusion which the markets and mathematical realists understood long before the fork-tongued policy makers, namely: Uncle Sam’s debt cancer is simply too fatal to cure with longer-duration bonds—or at some point, any bonds at all.

For now, a desperate Yellen has no choice but the last resort of issuing more of the sacred yet more expensive T-Bills to keep the yield-curve from inverting to levels so grotesque that the sound of Humpty Dumpty’s fall would echo through eternity.

Back to Basics: The Fed as Buyer/Lender/Spender of Last Resort

But the question still remains: Who will buy these T-Bills/IOUs at levels (trillion-dollar) necessary to cushion Humpty-Dumpty’s fall?

My opinion, and for now, it is only an opinion (one based on flow probabilities, the math of interest expense Realpolitik, the reality of UST-weary banks and the historical lessons of nations over their skis in debt) is that the ultimate buyer of Uncle Sam’s debt will be the Fed itself.

In short, and as warned since quantitative tightening began in earnest in 2022, I still see an unavoidable and inevitable pivot to either open QE or hidden repo/reverse repo QE once Powell’s “higher-for-longer” efforts to become Volcker-reborn are won at the expense of Humpty Dumpty’s demise.

Stated otherwise: Once the tightening and rate hiking breaks the national economy into a dis-inflationary or even deflationary spiral, the thirst for more mouse-clicked and inflationary trillions will be obvious.

Save the System or the Currency?

This thirst will force the system into a stagflationary “solution” of more fake, debased money in which the currency is sacrificed to save an otherwise unworthy, rigged and broken “system.”

I’ll say it again: In the end, the last bubble to “pop” is always the currency.

From Humpty Dumpty to Gold

It’s no secret that gold is insurance for currencies already dying.

Regardless of the USD’s relative (but ever-weakening) strength/hegemony, its (and other currencies’) inherent purchasing power when measured against gold has fallen by greater than 98% since Nixon closed the gold window in 1971.

Many can, will and do anxiously track and ask about the daily gold price, a price, which, is ironically measured in increasingly worthless fiat currencies.

This price fixation is especially true (and understandable) of speculators and traders.

But we are gold investors and wealth preservers. As such, our perspective, bias and convictions are comfortably patient and far-sighted.

We feel that measuring gold, as well as one’s own wealth, in such fiat fantasy is a dangerous and consensus-driven habit, and thus we measure wealth in ounces and grams not euros, dollars, pesos etc.

Gold, unlike the various US bonds discussed above, are of infinite duration and finite supply.

This so-called “pet rock” (of which central banks just bought over 1100 tons in 2022) serves as a constant as the USD races and scatters about the repo, Eurodollar and derivative markets in a complex, and often sexy madness which hides the fact that it is just a player in a familiar and losing game in which all fiat money reverts to its zero mean.

From Humpty Dumpty to the Big Bad Wolf

To the many who cannot conceive that tomorrow will be different than yesterday, or that the USA and its USD are not immortal, such statements are castigated as “sensational.”

If, however, one steps back and objectively observes the slow but steady history of the Greenback, it becomes undeniable that gold never really rises, currencies just fall.

Like the fable of the Three Little Piggies, there will always be those who prefer building their homes of straw and mud to have more time to enjoy the seductive call of rising asset bubbles and pet rock jokes.

After all, who can deny the high-times (and record-breaking wealth inequality) handed to us by years of an asset-inflating yet price-discovery-destroying and capitalism-killing central bank whose decades of fake liquidity and unprecedented debt have created an artificial sense of endless pleasure.

I mean, this was pretty fun, no?

But that Big Bad Wolf of rising debt levels and disingenuous policy makers is lurking beyond the tree line and occasionally smiling at the happy little piggies playing (or politicking) in the distance.

Soon, the debt wolf will stand, stretch and roll his mighty neck.

Then he will slowly trot, then cantor and finally gallop toward the straw and mud huts, and “he will huff, and he will puff and then blow those houses (and Humpty Dumpty) down.”

We feel, however, that the little piggy who built his financial house of bricks rather than straw is very much like those few nations, enterprises and individuals (the 0.5%) who have been quietly purchasing physical gold.

When the debt wolf comes, only the strongest houses will thrive – and it’s not always in the “houses” you’d expect.

end

END

3,Chris Powell of GATA provides to us very important physical commentaries

A must read

China is deflating and this deflation is heading our way

(zerohedge)

Ambrose Evans-Pritchard: Forget inflation, for deflation is the real danger now

Submitted by admin on Fri, 2023-06-09 10:36Section: Daily Dispatches

By Ambrose Evans-Pritchard The Telegraph, London via MSN Money, Redmond, Washington Thursday, June 8, 2023

The global inflation shock of the last two years is over except for the shouting. Legacy effects will generate much noise for a few months but the one-off spike is reversing almost everywhere with an elegant symmetry.

China is sliding into outright deflation as its post-Covid recovery peters out. Wage cuts are spreading in a sureal replay of what happened in Europe and America during the 1930s. Such is the Spartan ethos of Xi Jinping’s “common prosperity” campaign.

The Chinese producer price index has been negative for seven months, and the downward slide is accelerating. The headline CPI inflation rate has already dropped to 0.1% and will soon be negative. The Shanghai region is at minus 1.1% already.

This has large implications. China remains the workshop of the world, with the scale to shift the global pricing structure. It needs to export its way out of an economic depression and will not hesitate to do so with a cheaper yuan, down 12% since early 2022. A wave of disinflation is coming our way.

Wei Yao from Societe Generale says the regime seems paralysed in the face of a deepening Japan-style trap. “The zero-COVID shock and the housing crash last year seem to have brought China’s implicit government debt stress close to a breaking point. For China to escape a severe deflation scenario, the policy mindset requires a reset. We have seen little willingness so far,” she said.

Land sales for developers underpinned local government budgets during the property bubble. The real estate crash has dried up the revenue, setting off a funding crisis. Forced belt-tightening has neutralised a key instrument used by Beijing to inject stimulus into the economy.

Caixin magazine reported last week that the local authorities are drowning under $10 trillion of “hidden debt” they can no longer fully service. Some are having to cut medical benefits for the elderly.

The orthodox — IMF — way out is to wipe the slate clean with root-and-branch restructuring of debts, which is what Japan failed to do in the 1990s, and China is now failing to do, because it is traumatic and runs into powerful vested interests. …

How the Shanghai International Gold Exchange can facilitate de dollarization

(JanNieuwenhuijs)

Jan Nieuwenhuijs: The Shanghai International Gold Exchange and de-dollarization

Submitted by admin on Fri, 2023-06-09 16:46Section: Daily Dispatches

By Jan Nieuwenhuijs Gainsville Coins, Lutz, Florida Friday, June 9, 2023

This article is a primer on the Chinese gold market, more specifically the Shanghai International Gold Exchange (SGEI).

The SGEI facilitates “offshore” gold trading in renminbi and can play a crucial role in de-dollarization, as it allows countries to use renminbi as a trade currency that can be converted into gold without affecting China’s balance of payments.

De-dollarization can be accomplished by using yuan to settle international trade and store surpluses in gold through the SGEI. …

Ghana is doing just fine as it regains top spot in gold production at 3.7 million oz (115 tonnes)

Ghana regains top gold spot in Africa as output jumps 32%

Submitted by admin on Fri, 2023-06-09 19:50Section: Daily Dispatches

By Christian Akorlie Reuters Friday, June 9, 2023

ACCRA, Ghana — Ghana recorded a 32% increase in gold production last year, enabling it to win back the top spot from South Africa as the largest gold producer on the continent, the president of the mines chamber said today.

Ghana lost the position to South Africa in 2021 after a drastic fall in output.

Gold output in Ghana rose to 3.7 million ounces in 2022 from 2.8 million ounces the previous year, driven by growth in the output of both large- and small-scale sectors …

A poll from the Cato Institute indicates that, while about half of Americans do not have an opinion regarding whether the Federal Reserve should “begin offering a government-issued digital currency, called a ‘central bank digital currency’ (CBDC),” among those with an opinion on the matter over twice as many – 34 percent of poll participants – oppose the prospect as support it – 16 percent.

This result of the poll conducted from February 27 through March 8 in collaboration with YouGov is promising for Americans concerned about the threat a CBDC, which the Federal Reserve and big financial companies have been testing in preparation for its potential introduction, poses to freedom and privacy in America.

The poll results further indicate that, if Americans can be educated about the abusive government powers a CBDC can advance, many Americans currently undecided regarding the introduction of a CBDC will see good reason to oppose it. Emily Ekins and Jordan Gygi wrote in their May 31 in-depth Cato Institute article concerning the poll results:

Overwhelming majorities would oppose the adoption of a CBDC if it meant that the government could control what people spend their money on (74%), that the government could monitor their spending (68%), that a CBDC would abolish all U.S. cash (68%), that a CBDC would attract cyberattacks (65%), that the government could charge a tax on those who don’t spend money during recessions (64%), or that the government could freeze the digital bank accounts of political protesters (59%). Americans were marginally opposed (52%) if a CBDC could cause some people to stop using private banks, resulting in some banks going out of business.

The candidates now in second place in the Republican and Democratic presidential primaries – Ron DeSantis and Robert F. Kennedy, Jr. – appear to be in the anti-CBDC camp.

Hopefully, we will see more and more politicians joining them over the coming months in standing up against this threat posed by the Federal Reserve and US government.

Meanwhile, it is also important that Americans across the country educate the people they come into contact with about why a CBDC in America is unacceptable.

The new poll from the Cato Institute suggests that many people will be receptive to this message.

END

Binance CEO ‘CZ’ Responds As Data Points To Billions In Exchange Outflows

Data analytics platforms have reported billions of dollars in outflows from Binance over the last week, but this can be misinterpreted, argues Changpeng Zhao.

While data suggests that crypto assets have been flowing out of centralized exchanges at an accelerated pace over the last week, Binance CEO Changpeng Zhao argues it may not be as bad as it appears.

Leading analytics platforms such as Nansen and DefiLlama have all measured increased exchange outflows from Binance over the past seven days after news of the Securities and Exchange Commission’s lawsuit against the firm hit the airwaves.

According to Nansen, there has been a net outflow of $2.36 billion from Binance over the past seven days, along with $123.7 million flowing out of Binance.US.

DefiLlama reported an even larger figure of $3.35 billion in outflows from Binance, while Glassnode data shows the exchange’s balance having declined by 5.7% or around $1 billion over the past seven days.

CEX asset flows. Source: DeFiLlama

However, in a June 10 Twitter post, CZ argued that some exchange outflow data can be skewed as some third-party analytics measure change in assets under management as “outflow,” which would include times when crypto prices decline.

CZ instead claimed the firm’s outflow over the past 24 hours on June 9 was around $392 million, which pales in comparison to the $7 billion in one-day outflow that was recorded last year in November, around the time of FTX’s collapse.

CZ continued to explain that large inflows and outflows are perfectly normal during times of volatility.

“Some even only measure outflow, not inflows. On a sharp price movement day like today, many arbitrage traders move a lot of funds between exchanges, usually exponentially more than on normal days.”

On June 9, Cointelegraph reported that decentralized finance volumes surged more than 400% following the twin lawsuits targeting thecentralized exchanges.

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS/MONDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.1434

OFFSHORE YUAN: 7.1517

SHANGHAI CLOSED DOWN 2.57 PTS OR 0.08%

HANG SENG CLOSED UP 14,36 PTS OR 0.07%

2. Nikkei closed UP 168.88 PTS OR 0.52%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 103.07 EURO RISES TO 1.0768 UP 26 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.425 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 139.38 /JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE YUAN: DOWN// OFF- SHORE:DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.353***/Italian 10 Yr bond yield FALLS to 4.033*** /SPAIN 10 YR BOND YIELD FALLS TO 3.314…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 3.657

3j Gold at $1962.95 silver at: 24.12 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 0 /100 roubles/dollar; ROUBLE AT 82.64//

3m oil into the 68 dollar handle for WTI and 73 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 139.38 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .425% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9055 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9751 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.726 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 3.876 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.582 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 23.59…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.307 UP 7 BASIS PTS (RATES RISING RAPIDLY)

end

2. Overnight: Newsquawk and Zero hedge:

2. a)FIRST, ZEROHEDGE (PRE USA OPENING// MORNING

S&P Futures Hit Fresh 52 Week High With Fed Meeting On Deck

MONDAY, JUN 12, 2023 – 08:08 AM

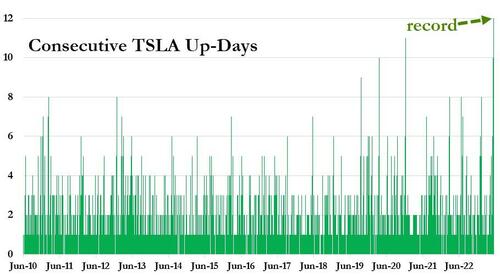

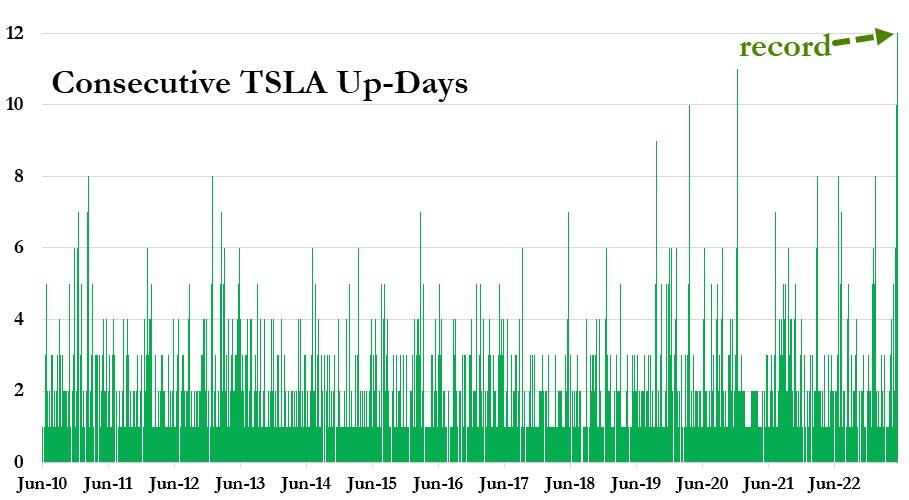

US equity futures, Asian markets and European bourses are all higher as part of a global risk-on tone, ahead of a week packed with central bank decisions. S&P 500 futures and contracts on the Nasdaq are both well in the green this morning, up 0.3% and 0.6% respectively as at 7:30 a.m. ET. The S&P is poised to surpass its August 2022 closing high, rising to the highest level since April of last year. Paradoxically, treasury yields are also ticking higher across the curve, with the sharpest rises in two- and three-year notes. A measure of the dollar is weakening, helping drive gains in spot gold prices. Oil prices are continuing their decline following another price cut forecast from Goldman Sachs, while iron ore drops slightly as recession fears once again outweighing fundamentals in commodities but certainly not in equities. Tesla was poised to set a record winning streak, rising for a 12th consecutive day. Keep an eye on labor strikes across US ports and potential stall supply chain normalization.

Tech led in pre-market trading; the underinvested sector may see additional position squaring ahead of what could be a large drop in CPI and Fed that pauses or skips. Tesla shares rose as much as 1.6% in premarket trading as its electric-car chargers become the industry standard. If gains hold, as noted above, it would be a 12-day winning streak for the electric-car maker, the longest on record. Here are some other notable premarket movers:

Biogen shares jump 6.8% in premarket trading after Leqembi, the Alzheimer’s drug being developed with Japanese firm Eisai, gained support from advisers to the US Food and Drug Administration. Analysts expect the drug to receive full FDA approval.

Coinbase Global Marathon Digital, and Riot Platforms lead cryptocurrency-exposed stocks lower in US premarket trading as Bitcoin falls. The largest cryptocurrency has remained rangebound under the closely watched $30,000 level since briefly breaching it in April.

Joby Aviation and Archer Aviation (ACHR US) were rallying in premarket trading as the two electric vertical take-off and landing (eVTOL) aircraft companies were on course to extend gains for a second session. On Friday, Canaccord Genuity said it views the firms as the closest to receiving regulatory certification. .

SentinelOne rose as much as 5.2% in premarket trading, with Morgan Stanley upgrading the software company to overweight from equalweight, saying the stock is mis-priced and should benefit in the long term as it gains market share from peers.

XPeng shares soar as much as 10% in US premarket trading, after the Chinese electric-vehicle maker said on social media that over 25,000 customers have pre-ordered its new G6 model in three days.

A busy calendar for investors kicks off with the US consumer price data on Tuesday and the Fed’s latest policy decision the next day. With the pace of inflation still proving sticky, positioning in rates markets suggests one more hike in July.

While the consensus is for the Fed to pause this week, unexpected hikes from the Bank of Canada and the Reserve Bank of Australia have added an extra element of uncertainty to markets. The European Central Bank is projected to lift its benchmark rate Thursday and the Bank of Japan is expected to stand pat on Friday.

“It feels like markets have been underpricing the probability of a June hike,” said Pooja Kumra, senior European rates strategist at Toronto Dominion Bank. “Data is moving in the right direction, but still not where central banks would like inflation to be.”

Meanwhile in stocks, Wall Street’s top strategists are giving divergent views on what the S&P 500 will likely do next. Goldman Sachs strategists expect the gains to continue as other sectors catch up with the searing rally for technology shares. Morgan Stanley’s Michael Wilson, meanwhile, remains bearish and points instead to the example of the bear market of the 1940s, when the S&P 500 rallied 24% before returning to a new low.

In Europe, consumer-products shares led the advance in Europe, where Adidas AG rallied after analysts at Bernstein upgraded the German sportswear maker; autos and retailers were also among the strongest performing sectors, while energy stocks were the biggest laggards in European trading as oil extended losses amid persistent concerns around the demand outlook, with Goldman Sachs cutting its price forecast again. Shell Plc and BP Plc both slipped more than 1%. Miners were also weaker after iron ore slumped almost 5%, falling for the first time in nine sessions because of worries about weakness in China’s property industry. Here are some of the most notable European movers:

Novartis shares rise as much as 1.4% after the company announced plans to buy Chinook Therapeutics for as much as $3.5 billion. The purchase will add two promising treatments for a rare kidney disease to the healthcare conglomerate’s business but there are also development risks, according to ZBK.

Adidas shares gain as much as 4.9% after being upgraded to outperform from market perform at Bernstein, which says in a note that the German sportswear maker is seeing its brand heat revving up again after having “languished” in 2022.

Ocado rises as much as 7.2% and is among the leading gainers on the Stoxx 600 on Monday after BNP Paribas Exane upgrades the online grocer to neutral and says it sees a lack of further negatives.

Uponor shares jump as much as 8.6% after Swiss industrial company Georg Fischer made the strongest bid so far for the Finnish plumbing-equipment manufacturer, offering €28.85 per share.

ProSieben shares gain as much as 4.7% after Oddo BHF raised the German broadcaster to outperform from neutral, saying consensus expectations on the firm’s advertising recovery and cost-cutting efforts have been “too cautious.”

SES shares fall as much as 15% to the lowest level since April 2020, after the satellite operator said its CEO Steve Collar will step down at the end of June, without naming a permanent successor. Analysts say the management change added to uncertainties when the company is in talks to merge with rival Intelsat.

Citycon senior unsecured bonds cut to Ba1 from Baa3 by Moody’s. Citycon Oyj, Samhallsbyggnadsbolaget i Norden AB and Fastighets AB Balder all trading lower.

CompuGroup Medical shares drop as much as 7.4%, their worst day since the end of Oct., after Berenberg downgraded the e-health solutions provider to hold from buy, saying that short-term upside now appears more limited following a strong year-to-date rally.

Earlier in the session, Asian stocks traded mixed with the region mostly cautious at the start of a risk-packed week as markets await the upcoming key events including major central bank meetings and data releases, while Australian markets were shut in observance of the King’s Birthday holiday.

China’s Shanghai Comp and HK’s Hang Seng were subdued amid weakness in healthcare and the property sector, with the latter pressured by a warning from Goldman Sachs. However, losses were stemmed amid some expectations for potential PBoC rate cuts to support the economy as more banks reduced their deposit rates and following comments last week from PBoC Governor Yi that there is plenty of room for policy adjustment and that they will continue targeted and forceful monetary policy.

Nikkei 225 initially outperformed and tested the 32,500 level amid expectations for the BoJ to maintain ultra-easy policy settings later this week and after PPI data was softer-than-expected and showed wholesale inflation eased for a 5th consecutive month which further supports the case for the BoJ to refrain from policy tweaks.

India stocks ended higher after declines in the previous two sessions, with gains in information technology and real estate companies supporting the market. The S&P BSE Sensex rose 0.2% to 62,724.71 in Mumbai, while the NSE Nifty 50 Index advanced by a similar measure. Infosys contributed the most to the Sensex’s gains, increasing 2%. Out of 30 shares in the index, 18 rose, while 12 fell

In emerging markets, Turkish stocks surged to record highs, while the lira traded near all-time lows, despite the appointment of two former Wall Street bankers to the country’s new economy team which some erroneously said “offered hopes of a return to orthodox and conventional policies.” Sorry: it won’t happen.

Nigerian international debt surged after the surprise weekend ouster of the central bank governor, with investors wagering that his removal will allow President Bola Tinubu to better pursue his pledge to shake up monetary policy settings blamed for holding back Africa’s biggest economy.

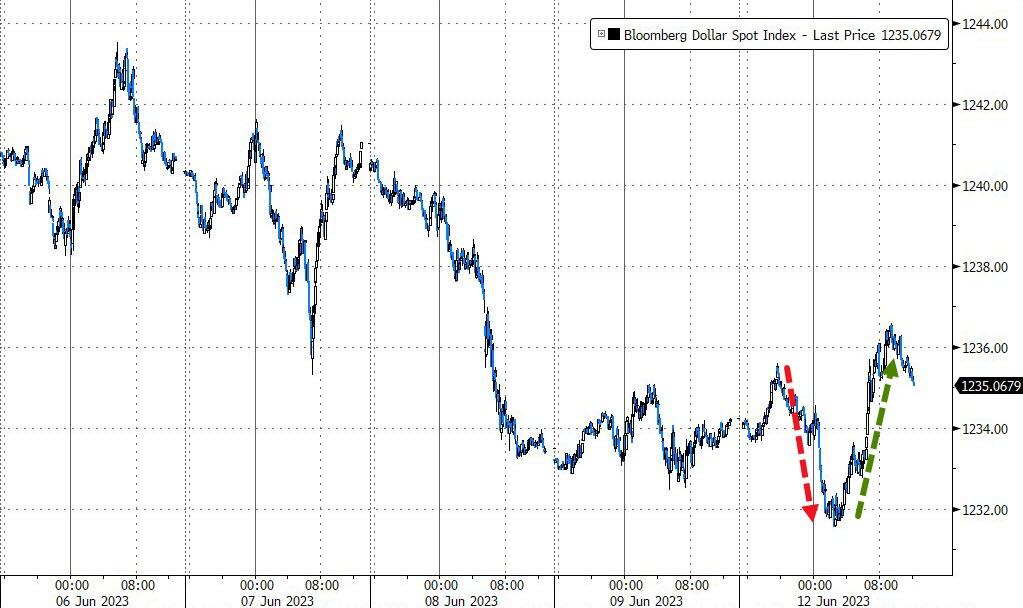

In FX, the Bloomberg Dollar Index fell as much as 0.2%, led by losses against the higher-risk Swedish krona and Australian dollar; the index has fallen for the past two weeks as traders have decreased bets for a Fed rate rise this week. The Turkish lira led declines, weakening 1% past 23.6 against the dollar to a record low; Turkey’s current-account deficit widened to $5.4 billion, worse than analysts’ estimates.

In rates, treasuries were mixed with the curve flatter as S&P 500 futures hold near Friday’s YTD high. Yields cheaper by ~2bp across front-end of the curve with long- end little changed, flattening 2s10s by ~0.5bp, 5s30s by ~1.5bp; 10-year near 3.75%, with bunds outperforming by 1.5bp in the sector and gilts lagging by 2bp. Two-year Treasury yields edged up 2 bps to 4.62%, just below a 2 1/2-month high of 4.64% touched late last month. A compressed auction cycle begins with $40b 3-year new issue at 11:30am followed by $32b 10-year reopening at 1pm. WI 3-year yield around 4.225% is ~53bp cheaper than last month’s, which stopped 2.8bp through the WI level. Gilts underperform Treasuries and bunds across the curve, led by the 10-year.

In commodities, WTI drifts 2.1% lower to trade near $68.67. Spot gold rises roughly $3 to trade near $1,965/oz.

Bitcoin is under modest pressure despite the constructive risk tone and as the USD pulls back, with specifics limited and the agenda ahead for today a particularly sparse one before a blockbuster week of key risk events.

There is nothing on today’s economic calendar but investors are closely waiting a US CPI report on Tuesday, which comes the day before the Fed decision and where traders see roughly a 30% possibility of a 25bps rise, while they see a nearly 90% chance of a hike in July. US session includes both 3- and 10-year note auctions, with May CPI report and FOMC decision ahead over next two days.

Market Wrap

Top Overnight News

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded mixed with the region mostly cautious at the start of a risk-packed week as markets await the upcoming key events including major central bank meetings and data releases, while Australian markets were shut in observance of the King’s Birthday holiday. Nikkei 225 initially outperformed and tested the 32,500 level amid expectations for the BoJ to maintain ultra-easy policy settings later this week and after PPI data was softer-than-expected and showed wholesale inflation eased for a 5th consecutive month which further supports the case for the BoJ to refrain from policy tweaks. Hang Seng and Shanghai Comp. were subdued amid weakness in healthcare and the property sector, with the latter pressured by a warning from Goldman Sachs. However, losses were stemmed amid some expectations for potential PBoC rate cuts to support the economy as more banks reduced their deposit rates and following comments last week from PBoC Governor Yi that there is plenty of room for policy adjustment and that they will continue targeted and forceful monetary policy.

Top Asian News

White House confirmed that China has had a spy base in Cuba since at least 2019, according to AP.

China’s Foreign Ministry issued a complaint to South Korea over recent criticism of its envoy and hopes that South Korea deeply reflects on problems in Sino-South Korea relations, according to state media.

Several Chinese lenders cut yuan deposit rates from Monday which follows similar action by China’s largest banks on Friday due to recent calls from Beijing to support the economy.

Goldman Sachs warned that property weakness will likely be a multi-year growth drag on China’s economy and it expects an L-shaped recovery in China’s property market, according to Bloomberg.

New Zealand PM Hipkins said he will lead a trade delegation during a China visit at the end of June.

European bourses are firmer across the board, Euro Stoxx 50 +1.0%, despite a lack of fresh drivers and newsflow light. Sectors are green across the board and feature outperformance in consumer-related names after updates for French Retail, European Gamers and favourable broker updates on Adidas, among others. On the flip side, Energy and Basic Resource names lag on benchmark pricing with the latter occurring despite the upside in Glencore after its latest Teck Resources proposal. Stateside, futures are firmer though with action slightly more contained while the NQ +0.5% outperforms incrementally amid/ahead of numerous AI-related updates, click here for details. GS on S&P 500 by end-2023: 4500 (prev. 4000), 25% chance of US recession within the next 12-months. EU antitrust regulators set to approve Broadcom’s (AVGO) USD 61bln bid for VMware (VMW), via Reuters citing sources.

Top European News

BoE’s Mann said Britain and other rich nations should consider a carbon tax to lower greenhouse gas emissions, while she refrained from commenting on the short-term economic outlook in her essay for Resolution Foundation think tank, according to Reuters. BoE’s Mann also urged the UK government to move economic policy away from being an emergency response tool and onto a more sustainable footing.

BoE’s Haskel says it is important we continue to lean against the risks of inflation momentum, further increases in interest rates cannot be ruled out*; monitoring indicators of inflation momentum and persistence closely.

EU’s VP Sefcovic says he will not be putting the trade deal “in the shredder”, scotching hopes in some quarters in the UK, of early renegotiation of the trade and cooperation agreement, according to Guardian’s O’Carroll.

Police in Scotland arrested former Scottish First Minister Sturgeon in an investigation into SNP finances but she was later released without charge pending further investigation, according to FT.

Acea estimates that EU-based auto names could pay as much as EUR 4.3bln in tariffs and lose sales between 2024-27, meaning 500k less vehicles would be made, if the EU does not agree to postpone the imposition of EU-UK tariffs, via FT.

FX

DXY wanes ahead of key risk events as the index tests recent lows within 103.700-240 range.

Aussie and Kiwi outperform as risk sentiment improves and the former extends post-RBA hike gains, AUD/USD approaches 0.6775 and NZD/USD probes 0.6150.

Euro rebounds from sub-1.0750 low towards a double top just shy of option expiries between 1.0790-1.0800 vs Greenback and Pound pulls up just shy of 1.2600 after hawkish-sounding commentary from BoE’s Haskel.

PBoC set USD/CNY mid-point at 7.1212 vs exp. 7.1214 (prev. 7.1115)

Indian Trade Minister says the RBI and the UAE central bank are in active dialogue for INR-AED trade.

Nigeria’s new President suspended the country’s Central Bank Governor, according to Reuters

Fixed Income

BTPs and JGBs buck bearish trend in debt ahead of data, Central Bank policy meetings and supply on technical and fundamental factors.

Gilts underperform between 95.76-96.26 parameters post-hawkish vibes from BoE’s Haskel.

Bunds and T-notes more restrained within 134.25-133.91 and 113-13+/06+ respective ranges.

Commodities

Crude and base metals continue to slip with the oil action a resumption of the post-OPEC+ downward trend and after GS cut their December forecasts.

Currently, WTI and Brent are at the lower-end of USD 67.67-70.33/bbl and USD 72.41-74.87/bbl parameters for the session.

Base metals remain under pressure on China-related growth concerns and exacerbated by the Goldman Sachs warning on the property market while spot gold has managed to glean some incremental upside from the softer USD.

Saudi Energy Minister said Saudi Arabia and China have plenty of synergies and that demand for oil in China is still growing, while he wouldn’t be surprised if there will be more announcements soon on Saudi-Chinese investments and China will be more engaged with them on mid-stream business. Saudi’s Energy Minister also said that they went through a comprehensive reform to achieve the OPEC+ agreement and they are working against uncertainty and sentiment, as well as noted that Saudi and OPEC+ are more interested in doing a regulator job, according to Reuters.

Saudi Aramco is to supply full contract volumes of crude oil to at least 5 North Asian refiners in July, according to sources cited by Reuters.

Iraq’s Parliament approved the 2023 Budget which set oil prices at USD 70/bbl and projects exports of 3.5mln bpd including 400k bps from the Kurdish region, according to Reuters.

US is expected to begin unloading oil from a seized Iranian tanker which risks escalating a shadow tanker war with Tehran, according to FT.

Venezuela’s PDVSA resumed operations in the El Palito refinery, according to Reuters.

Goldman Sachs cuts its December Brent crude forecast to USD 86/bbl from 95/bbl and cut WTI crude price forecast to USD 81/bbl from 89/bbl, while it noted that Russian and Iranian oil supply are significantly above expectations despite Saudi’s cut and it raised H2 2023-2024 global supply forecast excluding core OPEC by around 800k bpd.

Geopolitics

Ukraine said its troops recaptured three villages from Russian forces in the southeast of the country which were the first results of its counteroffensive. In relevant news, Russia said Ukraine made an unsuccessful attempt to attack a vessel which was protecting gas pipelines in the Black Sea, while it was also reported that 3 people were killed and 10 wounded by Russian shelling of an evacuation boat in the flooded Kherson region.