JUNE 14/GOLD CLOSED UP $10.30 TO $1955.50// SILVER ROSE BY 29 CENTS TO $24,03//PLATINUM WAS DOWN $2.00 TO $978.80 WHILE PALLADIUM WAS UP A STRONG $37.30//FOMC : THE FED CONVENED AND DECIDED TO PAUSE AS THE ECONOMY IS NOT DOING SO GOOD BUT THEY ALSO BECAME HAWKISH WITH THE THREAT OF MORE HIKES WHICH SENT THE DOW AND GOLD/DOWN//GERMAN DEINDUSTRALIZATION WILL HAVE A NEGATIVE EFFECT ON THE ENTIRE EU// RUSSIA VS UKRAINE UPDATES//COVID UPDATES/VACCINE IMPACT//DR PAUL ALEXANDER/SLAY NEWS/EVOL NEWS//SWAMP STORIES FOR YOU TONIGHT///

132 C SG AMERICAS 1 190 H BMO CAPITAL 25 323 C HSBC 45 323 H HSBC 17 363 H WELLS FARGO SEC 6 435 H SCOTIA CAPITAL 3 661 C JP MORGAN 43 661 H JP MORGAN 3 690 C ABN AMRO 1 880 H CITIGROUP 16 905 C ADM 20

TOTAL: 90 90 MONTH TO DATE: 18,152

JPMorgan stopped 43/90 contracts

FOR JUNE:

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2023. CONTRACT: 90 NOTICES FOR 9,000 OZ or 0.2799 TONNES

total notices so far: 18,152 contracts for 1,815,200 oz (56.4603 tonnes)

FOR JUNE:

SILVER NOTICES: 0 NOTICE(S) FILED FOR NIL OZ/

total number of notices filed so far this month : 423 for 2,115,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $10.30

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

/NO CHANGES IN GOLD INVENTORY AT THE GLD:////

INVENTORY RESTS AT 931.44 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 29 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.735 MILLION OZ FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 465.019 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY AN ATMOSPHERIC SIZED 4382 CONTRACTS TO 153,853 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUMONGOUS SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.25 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. TAS ISSUANCE WAS AN ULTRA- HUMONGOUS SIZED 3417 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH . CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: A MONSTER SIZED 3417 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.25). BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A HUMONGOUS GAIN ON OUR TWO EXCHANGES OF 4883 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 7.5MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION.

WE MUST HAVE HAD:

A FAIR SIZED ISSUANCE OF EXCHANGE FOR PHYSICALS( 501 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.935 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP + 0 MILLION OZ EXCHANGE FOR RISK(ISSUED TODAY: TOTAL ISSUED SO FAR: 7.5 MILLION OZ)// TOTAL STANDING FOR THE MONTH 4.270 MILLION OZ + 7.5 MILLION EXCHANGE FOR RISK = 11.77 MILLION OZ// ) // HUMONGOUS SIZED COMEX OI GAIN/ FAIR SIZED EFP ISSUANCE/VI) UBER =HUMONGOUS NUMBER OF T.A.S. CONTRACT ISSUANCE (3417CONTRACTS)//CONSIDERABLE T.A.S LIQUIDATION THROUGHOUT THE COMEX SESSION //TUESDAY //

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –366 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTRACTS for 9 days, total 4484 contracts: OR 22.420 MILLION OZ (498 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 22.420 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 22.42 MILLION OZ//

RESULT: WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4382 CONTRACTS DESPITE OUR FALL IN PRICE OF $0.25 IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR SIZED EFP ISSUANCE CONTRACTS: 501 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.935 MILLION OZ FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP+ 0 MILLION EXCHANGE FOR RISK TODAY + 7.5 MILLION EXCHANGE FOR RISK(PRIOR)//NEW TOTAL STANDING: 11.77 MILLION OZ////// .. WE HAVE A GIGANTIC SIZED GAIN OF4382 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: AN EXTRA -TERRESTRIAL HUMONGOUS 3417//CONSIDERABLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY SESSION. THE NEW TAS ISSUANCE TODAY (3417) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE.

WE HAD 0 NOTICE(S) FILED TODAY FOR NIL OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A TINY SIZED 14 CONTRACTS TO 432,898 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED – 439 CONTRACTS

WE HAD A FAIR SIZED INCREASE IN COMEX OI ( 2018 CONTRACTS) DESPITE OUR $10.70 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JUNE. AT 70.79 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0.9984 TONNE QUEUE JUMP: NEW TOTAL 63.841 TONNES STANDING SO FAR // + /A HUMONGOUS ISSUANCE OF 2150 T.A.S. CONTRACTS/HUGE FRONT END OF TAS LIQUIDATION TUESDAY ////YET ALL OF..THIS HAPPENED WITH A $10.70 LOSS IN PRICEWITH RESPECT TO TUESDAY’S TRADING.WE HAD A FAIR SIZED GAIN OF 1585 OI CONTRACTS (4.9300 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1599 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 432,898

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1585 CONTRACTS WITH 14 CONTRACTS DECREASED AT THE COMEX//TAS CONTRACTS INITIATED (ISSUED): A HUGE 2150 CONTRACTS) AND 1599 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1585CONTRACTS OR 4.9300 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1599 CONTRACTS) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (14) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 1585 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 70.79 TONNES FOLLOWED BY TODAY’S 32,100 OZ QUEUE JUMP //// NEW STANDING FALLS TO 63.841 TONNES// /3) ZERO LONG LIQUIDATION//4) SMALL SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: HUMONGOUS T.A.S. ISSUANCE: 2150 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

TOTAL EFP CONTRACTS ISSUED: 18,891 CONTRACTS OR 1,889,100 OZ OR 58.759 TONNES IN 9 TRADING DAY(S) AND THUS AVERAGING: 2099 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES 58.759 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 58.759/3550 x 100% TONNES 1.666% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 58.759 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUMONGOUS SIZED 4382 CONTRACTS OI TO 153,853 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 501 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 501and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 501 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 4382 CONTRACTS AND ADD TO THE 501OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 4883 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 24.42 MILLION OZ

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED DOWN 4.68 PTS OR 0.14% //Hang Seng CLOSED DOWN 113.00 PTS OR 0.58% /The Nikkei closed UP 483.77 OR 1.47% //Australia’s all ordinaries CLOSED UP 0.34 % /Chinese yuan (ONSHORE) closed DOWN 7.1581 /OFFSHORE CHINESE YUAN DOWN TO 7.1679 /Oil UP TO 70.31 dollars per barrel for WTI and BRENT DOWN AT 75.25 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A TINY SIZED 14 CONTRACTS DOWN TO 432,898 DESPITE OUR STRONG LOSS IN PRICE OF $10.70 ON TUESDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1599 EFP CONTRACTS WERE ISSUED: : AUGUST 1599 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1599 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1585 CONTRACTS IN THAT 1599LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED LOSS OF 14 COMEX CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $10.70. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A HUGE 2150 CONTRACTS. THROUGHOUT LAST WEEK, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THIS SPELLS TROUBLE AHEAD CONSTANT RAIDS WILL SURELY BE UPON US!

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (62.843) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 62.843 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $10.70) //// BUT WERE UNSUCCESSFUL IN KNOCKING A FEW SPECULATOR LONGS AS WE HAD OUR FAIR SIZED GAIN OF 2018 CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE TAS LIQUIDATION THROUGHOUT THE COMEX SESSION ON TUESDAY . THE TAS ISSUED TUESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 4.9300PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE. (70.709 TONNES) FOLLOWED BY TODAY’S 32,100 OZ QUEUE JUMP..NEW STANDING REMAINS AT 63.841 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $10.70

WE HAD – REMOVED 439 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 1585 CONTRACTS OR 158,500 OZ OR 4.93 TONNES.

Total monthly oz gold served (contracts) so far this month

18,152 notices 1,815,200 OZ 56.4603 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

No dealer withdrawals

Customer deposits: 1

i) Into Ashai: 47,896.750 oz

total deposits: 47,896.750 oz

Withdrawals: 1

i) Out of Brinks: 161,538.770 oz

Adjustments;0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 2463 contracts having GAINED 281 contracts. We had 40 contracts served on Tuesday so we gained 321 contracts or an additional 32,100 oz will stand for gold at the comex.

The next front month after June is the non active delivery month of July. Here, July gained 43 contracts to stand at 2905 contracts.

AUGUST lost 2206 contracts down to 365,574 contracts

We had 90 contracts filed for today representing 9000 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 90 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 43 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2023. contract month,

we take the total number of notices filed so far for the month (18,152 x 100 oz ), to which we add the difference between the open interest for the front month of JUNE (2463 CONTRACT) minus the number of notices served upon today 90 x 100 oz per contract equals 2,052,500 OZ OR 63.841 TONNES the number of TONNES standing in this active month of June.

thus the INITIAL standings for gold for the JUNEcontract month: No of notices filed so far (18,152) x 100 oz + 2463) [OI for the front month minus the number of notices served upon today (90)x 100 oz} which equals 2,052,500 oz standing OR 63.841 TONNES

TOTAL COMEX GOLD STANDING: 63.841 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,798,871.044 OZ

TOTAL REGISTERED GOLD: 11,654,123.196 (362.49 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 11,258,409.968 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,598,877 OZ (REG GOLD- PLEDGED GOLD) 298.565 tonnes//

END

SILVER/COMEX

JUNE 14//2023// THE JUNE 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

1,764,618.583 oz CNT Delaware JPMorgan Loomis

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

786,891.220 oz Brinks JPMorgan

No of oz served today (contracts)

0 CONTRACT(S) (NIL OZ)

No of oz to be served (notices)

431 contracts (2,155,000 oz)

Total monthly oz silver served (contracts)

423 Contracts (2,115,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposits

total dealer deposit: nil oz

total dealer deposits: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We had 2 deposits customer account:

i) Into Brinks 299,784.720 oz

iii) Into JPMorgan: 487,106.500 oz

total customer deposits: 786,891.220 oz

JPMorgan has a total silver weight: 142,366 million oz/272.375 million =52.14% of comex .//dropping fast

Comex withdrawals 4

i) Out of Delaware: 476,723,893 oz

ii) Out of CNT: 100,005.320 oz

iii) out of JPMorgan: 587,587.100 oz

iv) Out of Loomis; 600,302.271 oz

total withdrawals: 1,764,618.583 oz

adjustments: none

TOTAL REGISTERED SILVER: 27.117 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 272.375 million oz

DEALER SILVER DROPPING FAST. (moves into the 27 million oz column)

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE /2023 OI: 431 CONTRACTS HAVING LOST 0 CONTRACT(S).

WE HAD 0 NOTICES FILED ON MONDAY SO WE LOST 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF JUNE

JULY HAD A 3167 CONTRACT LOSS TO 78,244 CONTRACTS

AUGUST GAINED 2 CONTRACTS TO STAND AT 30

SEPT HAS A GAIN OF 7296 CONTRACTS UP TO 63,787

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes// est. volume today 62,255 good /

Comex volume: confirmed yesterday:90,921 strong

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 423 x 5,000 oz = 2,115,000 oz

to which we add the difference between the open interest for the front month of JUNE(431) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2023 contract month: 423 (notices served so far) x 5000 oz + OI for the front month of JUNE (431) – number of notices served upon today (0 )x 500 oz of silver standing for the JUNE contract month equates to 4.270 million oz +7.5MILLION OZ EXCHANGE FOR RISK//NEW TOTAL: 11.77 MILLION OZ STANDING

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

JUNE 14/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 931.44 TONNES

JUNE 13/WITH GOLD DOWN $10.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.01 TONNES FORM THE GLD///INVENTORY RESTS AT 931.44

JUNE 12/WITH GOLD DOWN $7.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.65 TONNES

JUNE 9/WITH GOLD DOWN $1.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.65 TONNES

JUNE 8/WITH GOLD UP $20.45 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.46 TONNES FROM THE GLD///INVENTORY RESTS AT 934.65 TONNES

JUNE 7 WITH GOLD DOWN $22.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 938.11 TONNES

JUNE 6/WITH GOLD UP $6.90 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 939.56 TONNES

JUNE 5/WITH GOLD UP $5.00 TODAY : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 938.11 TONNES

JUNE 2/WITH GOLD DOWN $24.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 938.11 TONNES

JUNE 1/WITH GOLD UP $14.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 939.56 TONNES

MAY 31/WITH GOLD UP $5.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 939.56 TONNES

MAY 30/WITH GOLD UP $14.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 26/WITH GOLD UP $.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 941.29 TONNES

MAY 25/WITH GOLD DOWN $19.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 24/WITH GOLD DOWN $9.50 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 941.29 TONNES

MAY 23/WITH GOLD $2.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 942.74 TONNES

MAY 22/WITH GOLD DOWN $4.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.83 TONES OF GOLD INTO THE GLD DESPITE THE L0SS IN PRICE//INVENTORY RESTS AT 942.74 TONNES

MAY 19/WITH GOLD UP $22.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 936.96 TONNES

MAY 18/WITH GOLD DOWN $23.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 936.96 TONNES

MAY 17/WITH GOLD DOWN $8.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.94 TONNES

MAY 16/WITH GOLD DOWN 28.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.57 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 934,07

MAY 15/WITH GOLD UP $2.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 937.64 TONNES

MAY 12/WITH GOLD DOWN $.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 937.84 TONNES

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 934.95 TONNES

GLD INVENTORY: 931.44 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 14/WITH SILVER UP 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 735,000 OZ FROM THE SLV///INVENTORY RESTS AT 465.019 MILLION OZ//

JUNE 13/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.515 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 465.754 MILLION OZ//

JUNE 12/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.269 MILLION OZ//

JUNE 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF SILVER TO THE TUNE OF 550,000 OZ//INVENTORY RESTS AT 467.269 MILLION OZ

JUNE 8/WITH SILVER UP $0.63 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 467.819 MILLION OZ/

JUNE 7/WITH SILVER DOWN 17 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.01 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 467.819 MILLION OZ/

JUNE 6/WITH SILVER UP 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.809 MILLION OZ//

JUNE 5/WITH SILVER DOWN $.13 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 266,000 OZ FROM THE SLV////INVENTORY RESTS AT 466.809 MILLION OZ/

JUNE 2/WITH SILVER DOWN 23 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV./INVENTORY RESTS AT 467.015 MILLION OZ/

JUNE 1/WITH SILVER UP 49 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.933 MILLION OZ

MAY 31/WITH SILVER UP 37 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 367,000 OZ FROM THE SLV////INVENTORY RESTS AT 467.933 MILLION OZ//

MAY 30/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 26/WITH SILVER UP $0.44 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.306 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 25.WITH SILVER DOWN $0.32 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 471.606 MILLION OZ//

MAY 24/WITH SILVER DOWN $.35 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 23/WITH SILVER DOWN 22 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.801 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 22/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ//

MAY 19/WITH SILVER UP 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ

MAY 18/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.529 MILLION OZ/

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

MAY 16/WITH SILVER DOWN 34 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .643 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.448 MILLION OZ.

MAY 15/WITH SILVER UP 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.091 MILLION OZ/

MAY 12/WITH SILVER DOWN $.26 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 3,123 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 470.091 MILLION OZ./

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

3,Chris Powell of GATA provides to us very important physical commentaries

This state is using common sense as they want state savings to be held as gold bullion

(NCNewline.com/GATA)

North Carolina House Republicans want state savings held as gold bullion

Submitted by admin on Tue, 2023-06-13 20:33Section: Daily Dispatches

By Lynn Bonner NCNewsline.com, Raleigh, North Carolina Tuesday, June 13, 2023

North Carolina House Republicans want the state to use some of its savings to buy gold bullion and bury it in Texas.

A group of House Republicans filed a bill in mid-April that would have the state use $2 billion from its savings reserve to buy gold bullion. The bill sat idle in the House Appropriations Committee until Thursday, when it was sent to the Committee on State Government. It’s set for a committee hearing tomorrow.

Rep. Mark Brody, the bill’s lead sponsor, said in an email last week that the value of the gold proposed for purchase will be lowered to $400 million to $500 million in a revised bill. House Bill 721 proposes to store North Carolina’s gold in a bullion depository the state of Texas created in 2015. Deposits were stored in Austin until a new facility opened outside the city in 2020.

Dissatisfaction with the Federal Reserve is at the heart of the North Carolina bill.

“The reason — the federal government is consistently and increasingly devaluing our currency,” Brody said in his email. “To begin to set aside an amount of physical gold over a number of years will put North Carolina in a better financial position should the devaluing process turn into hyperinflation.”

Under the bill, North Carolina’s gold would be stored in Texas while the state treasurer studies the cost and benefits of establishing a North Carolina-administered bullion depository. The gold would be moved from Texas if North Carolina establishes its own vault or if it needs to be sold to help North Carolina pay its bills. …

5 a. IMPORTANT COMMENTARIES ON COMMODITIES: CHOCOLATE

Huge shortage of cocoa beans means soaring crises for chocolate and I am a chocoholic and thus

I mourn!

(zerohedge)

Global Cocoa Shortage Sends Prices Soaring As “Consumers Should Brace” For ‘Chocolateflation’

WEDNESDAY, JUN 14, 2023 – 04:15 AM

Cocoa prices have soared 44% over the last nine months to seven-year highs as the global cocoa bean deficit worsens for the second consecutive year.

“The cocoa market has experienced a remarkable surge in prices … This season marks the second consecutive deficit, with cocoa ending stocks expected to dwindle to unusually low levels,” S&P Global Commodity Insights’ Principal Research Analyst Sergey Chetvertakov told CNBC via email.

Cocoa prices in New York surged more than 3% to $3,253 per metric ton — the highest since May 2016. The commodity last traded at $3,182 in the late US cash session on Tuesday.

Chetvertakov said the El Nino weather phenomenon might worsen the global supply shortage because less rain is expected across West Africa, where cocoa is primarily grown. About 60% of the world’s cocoa production is based in Côte d’Ivoire and Ghana. He warned prices could reach as high as $3,600 later this year.

He warned, “Consumers should brace themselves for the likelihood of higher chocolate prices,” adding chocolate producers are raising prices due to all-around higher costs.

Nick Gentile, a partner at NickJen Capital Management, told Bloomberg that chocolate producers usually have 11 months of physical cover on New York and London markets, though the future ratio only covers about five months.

Gentile said the price increases are a combination of some fund buying and some manufacturers just throwing a towel in and doing some buying. He added, “The cocoa market knows that the manufacturers are underbought and need to buy.”

With cocoa consumption at record highs in some Western countries, a worsening global bean deficit will only support higher prices.

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS/WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.1581

OFFSHORE YUAN: 7.1679

SHANGHAI CLOSED DOWN 4.68 PTS OR 0.14%

HANG SENG CLOSED DOWN 113.00 PTS OR 0.58%

2. Nikkei closed UP 483.77 PTS OR 1.47%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 102.72 EURO RISES TO 1.0806 UP 17 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.428 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 139.99/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN// OFF- SHORE:DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.4645***/Italian 10 Yr bond yield RISES to 4.096*** /SPAIN 10 YR BOND YIELD RISES TO 3.412…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 3.724

3j Gold at $1946.60 silver at: 23.81 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 1 AND 14 /100 roubles/dollar; ROUBLE AT 84.16//

3m oil into the 70 dollar handle for WTI and 75 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 139.99 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .428% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9025 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9752 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.832 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 3.943 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.676 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 23.53…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.475 UP 4 BASIS PTS (RATES RISING RAPIDLY)

end

2. Overnight: Newsquawk and Zero hedge:

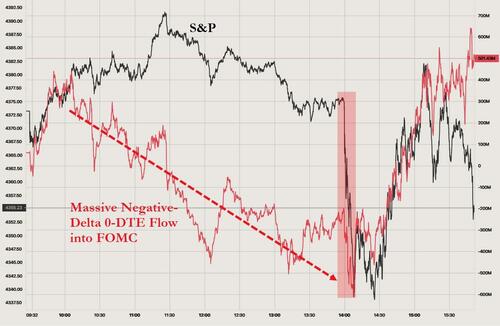

Futures Extend Gains Into Fed’s Pause Announcement

WEDNESDAY, JUN 14, 2023 – 08:19 AM

US equity futures are higher – again – with markets positioned for Jerome Powell to announce a hawkish, yet bullish pause, in the Fed’s rate hiking campaign at 2pm today. S&P futures rose 0.15% as of 7:45am ET following the S&P 500’s fourth consecutive increase — the longest winning stretch since early April – which approached the 4,400 mark, the highest level in over a year. Small caps/Russell outperformed (in line with what we said last night) as bond yields reverse an earlier drop into Fed Day, while the USD is again weaker pre-mkt. Commodities are rallying led by Energy and Metals, WTI oil rises back over $70 and base metals are up 4% – 7% MTD on hopes of Chinese stimulus. In Europe, a rally in miners helped push the Stoxx 600 benchmark to the highest in three weeks.

In premarket trading, Google parent Alphabet slipped as the European Union accused the unit of abusing its dominance over advertising technology. Advanced Micro Devices shares gained 1.6% in premarket trading after the chipmaker showed off its planned line of artificial intelligence processors. The shares had drifted lower during the presentation in San Francisco, closing down 3.6%, but analysts responded positively to the event. Meanwhile, Tesla was set to extend gains for a record 14th consecutive session, after already adding $240 billion during its winning streak, as the world’s most valuable automaker shows no sign of stopping. Here are some other notable premarket movers:

Nikola leads fellow electric- vehicle stocks higher in premarket trading as the cohort looks set to extend Tuesday’s gains.

NextDecade rose as much as 17% in US premarket trading after TotalEnergies agreed to buy a 17.5% stake in the company, which is developing a terminal to export liquefied natural gas in Texas.

RadNet dropped 8% in postmarket trading Tuesday after the network of outpatient imaging centers offered $175 million shares via Jefferies and Raymond James.

MicroVision shares slumped 14% postmarket after the company filed a shelf registration for potential sale of common and preferred shares and warrants.

Iteris shares dropped 14% in extended trading, after the engineering services company reported adjusted fourth quarter Ebitda below expectations. It also gave a full-year revenue forecast.

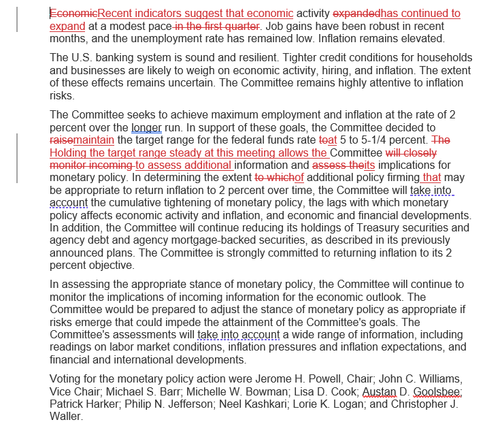

Global investors rejoiced at Tuesday’s CPI data which showed the 11th consecutive month of slowing inflation as confirmation that the FOMC will hold rates in the 5%-5.25% range. Swap traders put the odds of an increase at only 10%, while still seeing the potential for a July move, given that inflation is still more than twice the central bank’s goal.

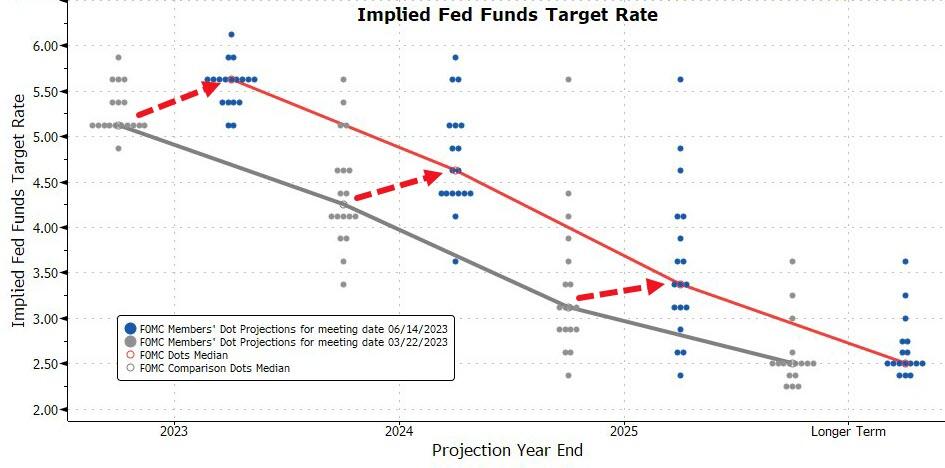

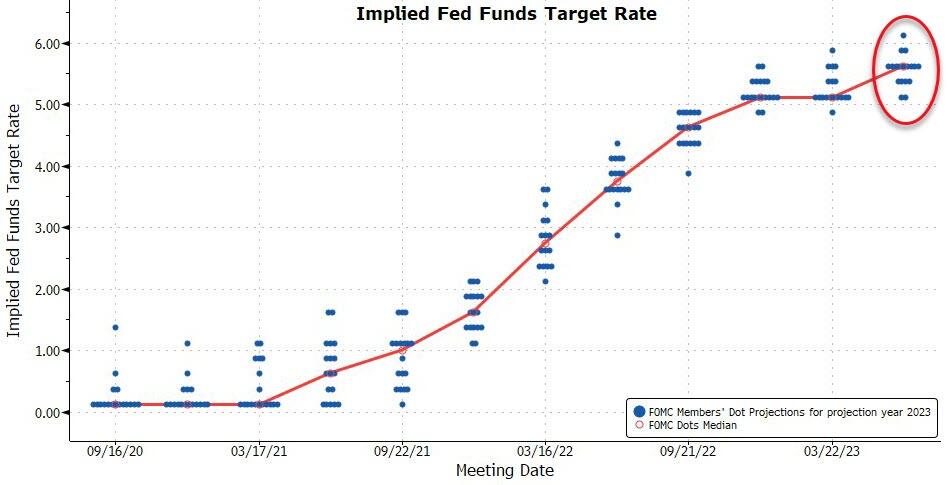

Indeed, as noted earlier, the Fed is poised to pause the hiking cycle for the first time in 15 months, in a rate decision that will land at 2:00 p.m. (see our full FOMC preview post is here).

Fed Chair Jerome Powell has signaled that he’d prefer to wait to evaluate the impact of past hikes on the economy, as well as the recent banking turmoil. The Fed’s likely to keep options open to hike again. Meanwhile, Ken Griffin’s hedge fund Citadel is bracing for a US recession by ramping up high yield credit trades. He expects the Fed to raise interest rates one more time this year and then pause for an extended period.

“A hawkish skip is the most likely scenario for today’s FOMC,” said Evelyne Gomez-Liechti and Helen Rodriguez, strategists at Mizuho International. “We expect Powell will follow up with a relatively hawkish tone in the press conference in order to prevent a dovish market reaction, stressing that inflation is still too high and the Fed will be resolute in returning inflation to target.”

Meanwhile, CNBC is reporting that CFOs have told regional Fed presidents to halt the hiking cycle and not just skipping a meeting or two. Expectations of a pause have pushed the VIX back below 15, against an average of 23 for the past year, underscoring support for risk assets. In another sign of the calm prevailing in equity markets, it’s now almost 80 trading days since the S&P 500 declined by 2% or more.

European stocks gained as miners rallied for a second day, while investors awaited the Federal Reserve’s policy decision for clues on the path of interest-rate hikes. The Stoxx Europe 600 Index was up 0.6% and on course to rise for a third straight session with miners gaining 1.8% as optimism around stimulus in China kept iron ore prices near a two-month high. Barclays strategists upgraded their rating on the sector to overweight, saying bets on the stimulus would boost cyclical sectors in the second half. Autos and real estate stocks also rose, while tech and travel & leisure underperformed. Shell shares recovered early declines as the energy giant said it would increase its dividend by 15% and boost natural gas production. Casino Guichard-Perrachon SA jumped after billionaire Xavier Niel and two partners approached the grocer with a €1.1 billion-euro ($1.2 billion) rescue plan. Logitech International SA dropped after it said Chief Executive Officer Bracken Darrell would leave the company. Here are the most notable European movers:

Grifols shares surge as much as 12%. The Spanish pharmaceutical firm expects to get $1.5b upon “satisfactory closing” of Shanghai RAAS deal, according to regulatory filing

Shell shares turned positive after falling as much as 0.5%, with brokers highlighting the oil major’s capex reduction plan as positive, tempering the effect of a smaller-than-expected dividend increase

Colruyt shares jump as much as 11% after the Belgian retailer reported better-than-expected full-year results. The outlook suggests “significant” upgrades to consensus earnings estimates, MS says

Games Workshop shares advance as much as 6.2% after the maker of the Warhammer series of games showed an “impressive” improvement in revenue growth in 2H, Jefferies says

DoValue gains as much as 8.6% after the loan management servicer said Fortress and Bain Capital signed a shareholders’ agreement related to corporate governance. Equita said the move is positive

Entain shares fall as much as 11% after the gambling operator raised about £600m through a stock offering to fund the acquisition of Poland sports-betting operator STS

Boliden shares fall as much as 9.1%, the most since October, after the Swedish mining firm cut its guidance following a large fire at the Ronnskar copper smelter in northern Sweden

Victrex shares drop as much as 11% to the lowest since June 2016 after the UK-based chemicals company gave a full-year earnings outlook that missed analyst estimates

Robert Walters shares drop as much as 20% and drag down other recruitment stocks in the UK and Europe after the firm said its FY profit is set to be “significantly” below expectations

CompuGroup Medical drops as much as 6.5% as Morgan Stanley cuts to underweight, giving the stock its only negative analyst rating. The broker sees better risk/reward elsewhere within its coverage

Earlier in the session, APAC stocks were mixed with the region’s bourses tentative ahead of the FOMC policy announcement.

Hang Seng and Shanghai Comp. were kept afloat after the PBoC cut rates for its Standing Lending Facility by 10bps and the NDRC issued a notice on lowering costs this year with VAT to be exempted and reduced for small businesses until year-end. China was also said to be weighing broad stimulus with property support and rate cuts, although the gains in Chinese stocks were limited amid ongoing growth concerns and following softer-than-expected loans and financing data.

ASX 200 was led by strength in the commodity-related sectors after China’s support pledges and PBoC cuts.

Nikkei 225 extended its advances as automakers and other exporters benefitted from recent currency moves and amid broad consensus for the BoJ to maintain its ultra-easy policy later this week

Indian stock markets rose for a third session, supported by gains in metal and commodities firms. The S&P BSE Sensex rose 0.1% to 63,228.51 in Mumbai, while the NSE Nifty 50 Index advanced 0.2%. Reliance Industries contributed the most to the Sensex’s gain, increasing 1.2%. Key stock gauges in India traded near their all-time highs, after gaining more than 9% since March, helped by the strength of India’s domestic economy and purchases by foreigners. “India’s growth cycle is here to stay,” Morgan Stanley equity strategist Ridham Desai said in an interview with Bloomberg Television. “A lot of factors have combined together, like political, social, and economic, and it does seem like a sweet spot.”

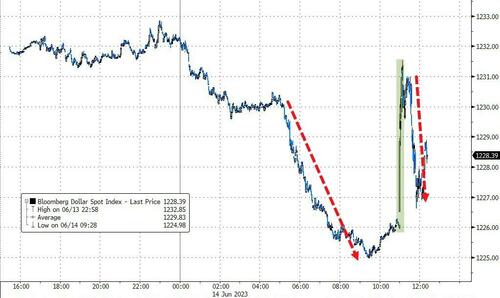

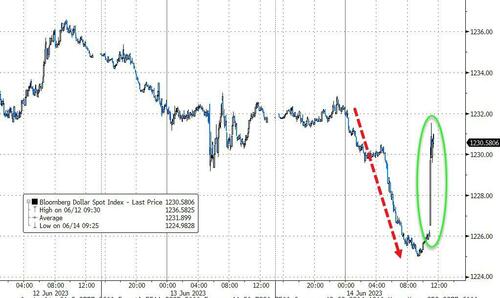

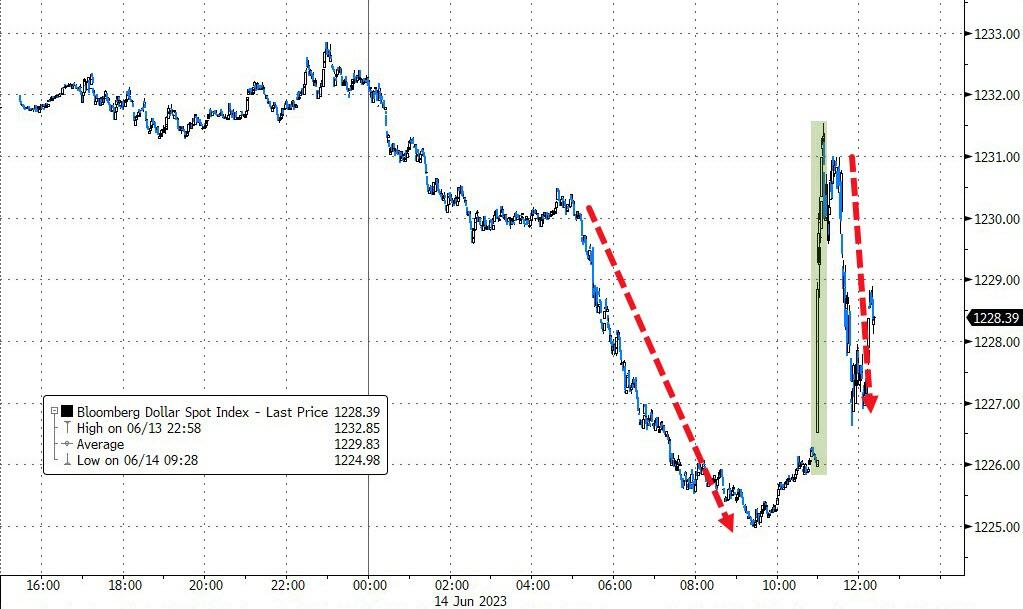

In FX, the Bloomberg dollar index held near a one-month low, dropping another 0.1% on Wednesday on speculation the Federal Reserve will skip an interest-rate hike at a policy meeting ending Wednesday. “Although US bond yields are now back up near late-May highs, that hasn’t helped the US dollar,” Australia & New Zealand Banking Group Ltd. analysts Miles Workman and David Croy wrote in a research note. While US CPI data has cemented bets on a Fed pause, “it also suggests we’ll see more tightening later, and that’ll ultimately slow the US economy,” they said.

Kiwi underpinned around 0.6150 vs Greenback and 1.1000 against Aussie after better than expected NZ current account data, AUD/USD relatively bid near 0.6800 with support via strength in iron ore.

Sterling retains 1.2600+ status vs Dollar as UK GDP matches consensus and Euro probes 1.0800 where mega option expiry interest resides.

Yen takes advantage of softer US Treasury yields to rebound through 140.00.

Lira regains poise as Turkish President gives new Finance Minister and CBRT Governor go ahead to revert to orthodox policies ahead of next week’s CBRT.

In rates, Treasuries are marginally cheaper across the curve after Tuesday’s sharp post-CPI drop, led by German bonds, where 10s trade cheaper by around 4bp vs Treasuries. Treasuries bull steepened slightly in muted price action ahead of the FOMC rate decision when policymakers are expected to pause tightening for the first time this cycle. Money markets assign 15% odds on a quarter-point increase later and maintain an 80% probability of such a hike at next month’s outcome. Yields are cheaper by around 1bp across the Treasuries curve with 10-year around 3.81% and spreads within 1bp of Tuesday session close.

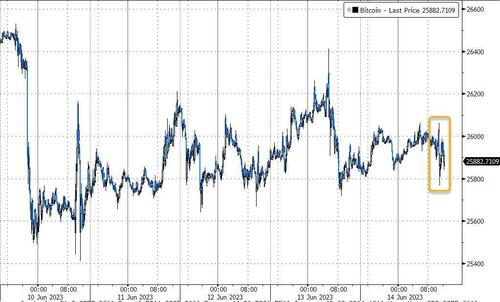

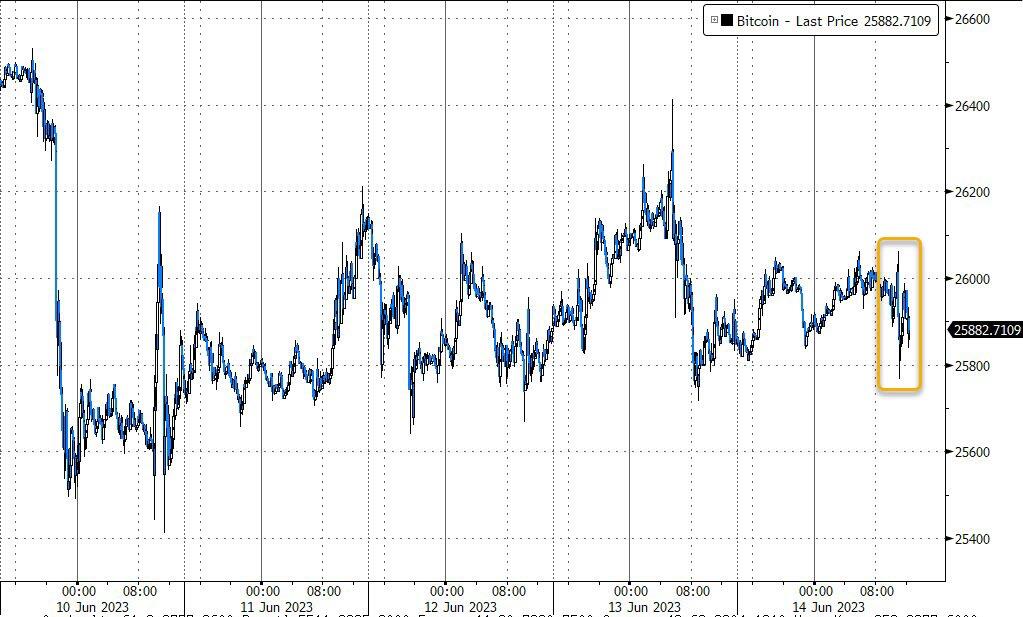

In commodities, crude futures advance with WTI rising 0.9% to trade near $70.00. Spot gold adds 0.4% to around $1,951. Bitcoin gains 0.3%

Looking the day ahead now, and the main highlight will be the Federal Reserve policy decision, along with Chair Powell’s press conference. Data releases will include the US PPI reading for May, as well as UK GDP and Euro Area industrial production for April.

Market Snapshot

S&P 500 futures up 0.2% to 4,381.25

MXAP up 0.4% to 168.02

MXAPJ down 0.2% to 526.61

Nikkei up 1.5% to 33,502.42

Topix up 1.3% to 2,294.53

Hang Seng Index down 0.6% to 19,408.42

Shanghai Composite down 0.1% to 3,228.99

Sensex up 0.2% to 63,253.81

Australia S&P/ASX 200 up 0.3% to 7,161.75

Kospi down 0.7% to 2,619.08

STOXX Europe 600 up 0.3% to 464.84

German 10Y yield little changed at 2.43%

Euro little changed at $1.0797

Brent Futures up 1.3% to $75.23/bbl

Gold spot up 0.4% to $1,950.56

U.S. Dollar Index down 0.13% to 103.21

Top Overnight News

China’s foreign minister tells Blinken in a phone call that the US should “show respect” to Beijing and stop undermining the country’s sovereignty, security, and development (Blinken is supposed to visit China this weekend, although the trip hasn’t been confirmed). SCMP

Senior Chinese officials are holding urgent meetings with economists and business leaders on how to supercharge the economy, people familiar said. In response, execs are calling on the government to adopt a more market-oriented, rather than planning-led approach, to growth. BBG

Citadel’s Ken Griffin expresses optimism about the growth outlook in China (“They’re very clearly putting economic growth back at the top of their priority list”). FT

India’s wholesale price index for May sinks to -3.48% Y/Y, down from -0.92% in April and below the Street’s -2.5% forecast. RTRS

Generative AI could boost the global economy by up to $4.4T annually by enhancing worker productivity according to a new McKinsey report. NYT

Biden coming under growing pressure to support an accelerated timeline for bringing Ukraine into NATO. NYT

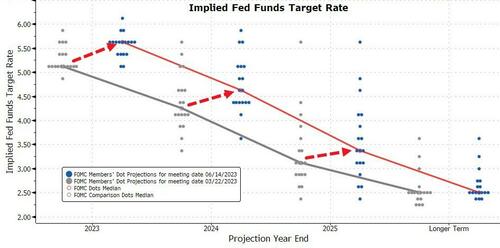

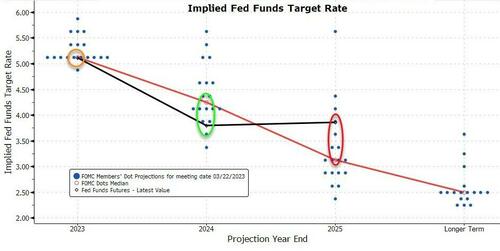

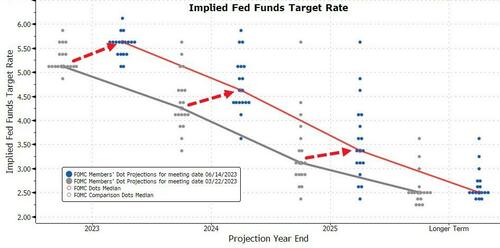

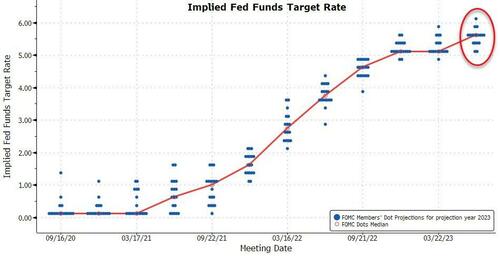

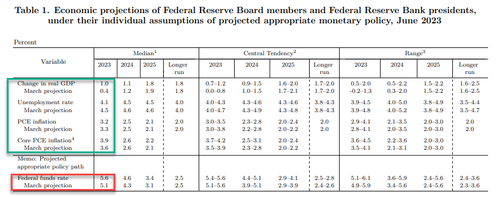

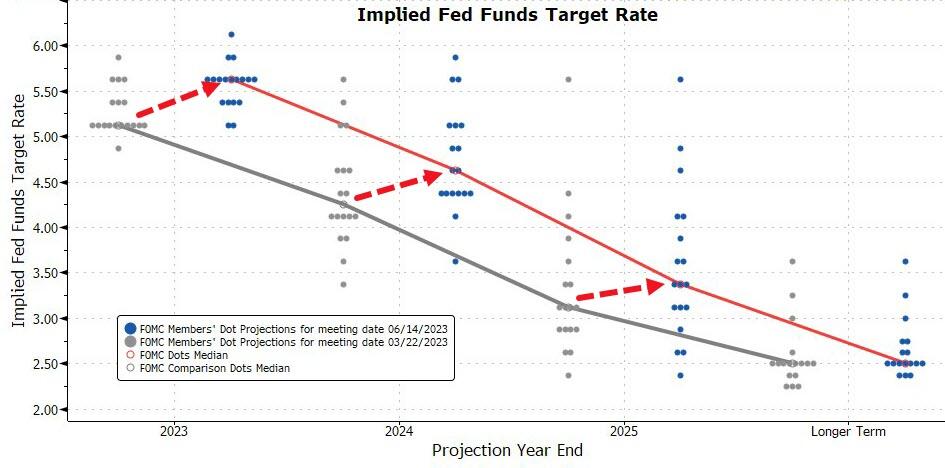

The FOMC is likely to pause today and let the haze clear before it considers another rate hike. The Fed leadership has signaled that it sees pausing as the prudent course because uncertainty about both the lagged effects of the rate hikes it has already delivered and the impact of tighter bank credit increases the risk of accidentally overtightening. We expect the median dot to show one additional hike to a new peak of 5.25-5.5%, in line with our own forecast. GIR

Global oil demand is nearing its peak and will slow sharply in the next few years as high prices and Russia’s war in Ukraine speed the transition from fossil fuels, the IEA said. In the near term, oil markets may tighten “significantly” as China’s consumption rebounds from the pandemic. In the US, crude and fuel inventories rose last week. BBG

Money-market funds are already scooping up the Treasury’s growing bill issuance now that the government has suspended the debt ceiling until 2025 and the Federal Reserve is nearing the end of its rate-hiking cycle. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were somewhat mixed with the region’s bourses mostly tentative ahead of the FOMC policy announcement. ASX 200 was led by strength in the commodity-related sectors after China’s support pledges and PBoC cuts. Nikkei 225 extended its advances as automakers and other exporters benefitted from recent currency moves and amid broad consensus for the BoJ to maintain its ultra-easy policy later this week. Hang Seng and Shanghai Comp. were kept afloat after the PBoC cut rates for its Standing Lending Facility by 10bps and the NDRC issued a notice on lowering costs this year with VAT to be exempted and reduced for small businesses until year-end. China was also said to be weighing broad stimulus with property support and rate cuts, although the gains in Chinese stocks were limited amid ongoing growth concerns and following softer-than-expected loans and financing data.

Top Asian News

Chinese Foreign Minister Qin Gang held a call with US Secretary of State Blinken and said the US should stop interfering with China’s internal affairs and should respect China’s concerns such as the Taiwan issue, while he added the US should stop hurting China under the excuse of competition and hopes the US will meet China halfway, effectively manage differences and promote communication and cooperation, according to state media.

Japanese PM Kishida is reportedly considering dissolving the Lower House of Parliament on the same day if the opposition submits a no-confidence vote on Friday, according to Fuji TV.

European bourses are firmer across the board, Euro Stoxx 50 +0.7%, having shrugged off the tepid open after a busy stock-specific pre-market though fresh macro drivers remain light. Sectors are similarly supported with Real Estate leading after marked UK-related pressure on Tuesday while Autos and Banks benefit from a Barclays note and yields/BBVA’s ATI sale respectively. Travel & Leisure bucks the trend after a downbeat update from Entain. Stateside, futures are edging higher and moving in tandem with the above as the ES attains a firmer hold above 4400 pre-FOMC; newsquawk preview available here. EU Antitrust Chief Vestager to hold a news conference at 11:45BST/06:45ET, expected to be on Alphabet’s (GOOGL) Google. Shell (SHEL LN) announces a 15% dividend/shr increase from Q2 2023; Capital Spending reduced to USD 22-25bln/year for 2024 & 2025; Buybacks of at least USD 5.5bln for H2 2023. Airbus (AIR FP) raises 20 year delivery forecast to 40.85k (prev. 39.45k); sees 17.1k aircraft replacements in the next 20 years (prev. 15.4k).

Top European News

Turkish President Erdogan says he has accepted steps that the CBRT and Finance Minister Simsek will take.

French Finance Minister Le Maire vowed to put France’s finances back on track with spending cuts, according to FT.

Downing Street has ordered banks to protect struggling homeowners from increasing mortgage costs as markets speculate over the possibility of the Bank Rate rising to as high as 6%, according to The Telegraph.

German Economy Ministry says economic data points to moderate recovery over further course of the year; “economic recession” in sense of more sustained downturn is not currently expected

FX

Buck on the backfoot approaching Fed, with DXY heavy on the 103.000 handle awaiting guidance after a widely expected FOMC pause.

Kiwi underpinned around 0.6150 vs Greenback and 1.1000 against Aussie after better than expected NZ current account data, AUD/USD relatively bid near 0.6800 with support via strength in iron ore.

Sterling retains 1.2600+ status vs Dollar as UK GDP matches consensus and Euro probes 1.0800 where mega option expiry interest resides.

Yen takes advantage of softer US Treasury yields to rebound through 140.00.

Lira regains poise as Turkish President gives new Finance Minister and CBRT Governor go ahead to revert to orthodox policies ahead of next week’s CBRT.

PBoC set USD/CNY mid-point at 7.1566 vs exp. 7.1550 (prev. 7.1498)

Fixed Income

US Treasuries retain bid ahead of PPI data and FOMC as T-note hovers closer to top of tight 113-00/112-24 range.

Bunds remain heavy between 133.71-33 parameters after less than rousing finale for German 2033 benchmark.

Gilts claw back post-UK labour data losses within 94.65-21 bounds as monthly GDP metrics match consensus.

Commodities

Crude continues to consolidate with WTI Jul’23 and Brent Aug’23 inching above the USD 70.00/bbl and USD 75.00/bbl handles, specific drivers light.

Spot gold is incrementally firmer and at the top-end of the sessions range which is yet to see it gain any real traction above the USD 1950/oz mark as the broader risk tone remains robust and serves to offset any USD-driven upside.

Base metals are somewhat mixed, though this is seemingly more a function of yesterday’s pronounced gains for the complex earlier in the week.

US Energy Inventory Data (bbls): Crude +1.0mln (exp. -0.5mln), Gasoline +2.1mln (exp. +0.3mln), Distillate +1.4mln (exp. +1.2mln), Cushing +1.5mln.

IEA Monthly Oil Market Report: oil demand is set to increase by 2.4mln BPD in 2023 to a record of 102.3mln BPD (vs. May view of 102mln BPD). Click here for more.

Geopolitics

Russia urged for a transparent investigation into the Nord Stream blasts after reports that the US warned Ukraine not to attack Nord Stream, according to Reuters.

White House said US President Biden met with the NATO chief and they underscored their shared desire to welcome Sweden to the alliance ASAP, while they also discussed the need for allies to build on the 2014 Wales summit defence investment pledge.

German National Security Strategy Document says China remains a partner without which cannot solve the many global challenges; China is increasingly pressuring regional stability and disrespecting human rights. Germany aims to spend 2% of GDP on defence on average over several years.

UN Nuclear Chief to visit Zaporizhzhia nuclear power plant on Thursday, one day later than planned, according to IFAX citing an official.

Turkish President Erdogan says constitutional amendments in Sweden are not enough to address Turkey’s concerns, the police should not allow such protests; adds, Sweden should not expect “anything different” from Turkey at the Nato summit.

Crypto

Binance and SEC are reportedly not far apart on a deal to avoid a full asset freeze, according to Bloomberg.

Binance CEO Zhao denies rumours of selling Bitcoin to bolster BNB, according to Cointelegraph.

US Event Calendar

07:00: June MBA Mortgage Applications 7.2%, prior -1.4%

08:30: May PPI Final Demand MoM, est. -0.1%, prior 0.2%

08:30: May PPI Final Demand YoY, est. 1.5%, prior 2.3%

08:30: May PPI Ex Food and Energy MoM, est. 0.2%, prior 0.2%

08:30: May PPI Ex Food and Energy YoY, est. 2.9%, prior 3.2%

14:00: June FOMC Rate Decision

DB’s Jim Reid concludes the overnight wrap

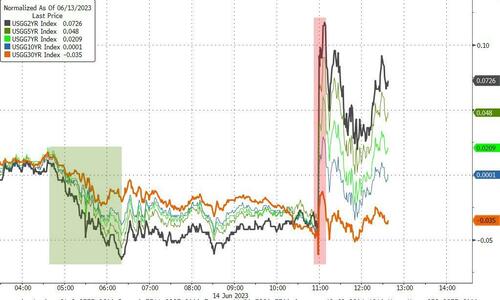

Investor risk appetite has remained pretty strong over the last 24 hours, with the S&P 500 (+0.69%) hitting a fresh one-year high and posting a 4th consecutive advance. That follows the US CPI print for May, which was broadly in line with consensus and means that the Fed are now widely expected to keep rates on hold today after 10 consecutive increases. This optimism was evident across multiple asset classes, with oil prices rising and credit spreads tightening as well. But the flip side of all this positivity has been growing scepticism that central banks will cut rates at all this year, which led to a sovereign bond selloff as investors priced in higher rates for longer. At the extreme end of this was the UK with 2yr notes soaring +26bps, comfortably past the Liz Truss related mini peak in October last year and to the highest since summer 2008. 2yr US yields rose +8.9bps and closed near the top of a +21bps range yesterday with a big lurch lower to c.4.49% after CPI but then trading above 4.70% late in the session before closing at 4.666%, a post-SVB high.

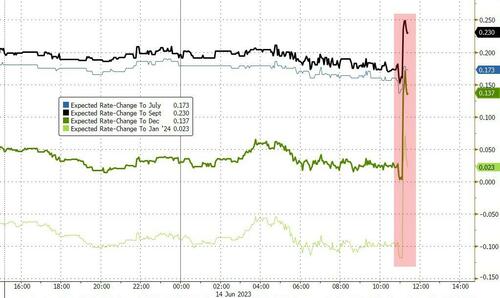

This focus on the front end makes tonight’s dot plot from the Fed one of the most important events today, since it’ll provide a big steer on how far the FOMC want to keep pushing rates. Market pricing is currently pointing towards just one more rate hike in July, so any indication there’ll be more (or less) than that could lead to a big reaction.

When it comes to the Fed today, the overwhelming consensus is that they’ll stay on hold, keeping the target range for the fed funds rate between 5% to 5.25%. In fact, futures are now pricing just a 12.6% chance of a hike at this meeting, so by this point anything other than a hold would be a big surprise. There had been some sense that a bad CPI print yesterday might lead to a further hike, but in reality, monthly headline CPI came in at just +0.1% as expected. In turn, that took the year-on-year rate down to just +4.0% (vs. +4.1% expected), which is the slowest inflation has been in 26 months.

The main problem for the Fed is that core CPI has still been stubbornly persistent, with yesterday seeing another +0.4% monthly rise (0.44% unrounded so a strong +0.4%). That’s the 6th consecutive month where core CPI has been at least +0.4%, and it meant that the year-on-year rate only fell back to +5.3% (vs. +5.2% expected). So whether you look at a 1m, 3m, 6m or even 12m horizon, core CPI has still been running at an annualised pace of more than 5%. That persistence means that investors still think that today will only mark a “skip” on rate hikes rather than a pause, with futures pointing to a 72% chance of a hike by next month’s meeting in July. If you were looking for hope, rents should ease in the months ahead if the models the likes of which we mentioned in CoTD here yesterday prove correct.

This rates sell-off was driven by real rates, with the 2yr real TIPS yield (+8.7bps) hitting a post-GFC high of 2.527%. 10yr nominal yields saw a similar strong move higher to the front end, with a +7.8bps rise to 3.813%. This morning in Asia, we’ve edged back down to 3.80% as we go to press.

With all this in mind, our US economists think that the Fed’s statement will see a hawkish adjustment, and will note the potential for more tightening at “coming meetings”. They also think the dot plot will show a further hike pencilled in for this year. And at the press conference, they think there’s little downside from Chair Powell delivering a hawkish message, considering the resilient data recently, easing financial conditions, and a desire to prevent near-term rate cuts being priced. See there full preview here for more details.

Whilst attention will be on the Fed today, there were some interesting headlines out of the UK yesterday as we mentioned at the top, where investors priced another full 25bp rate hike from the BoE after the latest employment data showed a very tight labour market. In particular, wage growth excluding bonuses was up by +7.2% (vs. +6.9% expected), whilst the unemployment rate fell back to 3.8% over the three months to April (vs. +4.0% expected). And with that data in hand, markets are now pricing in more than five 25bp hikes by the December meeting, which if realised would take the Bank Rate up to 5.75% from its current 4.5%. Indeed, it’s worth noting that investors are even placing some weight on the prospect they might go as far as 6%. As someone with a 1.4% 5-year fixed mortgage that rolls off in January 2025, I’m going from fairly relaxed to starting to take some serious refinancing risk notice!!

Those numbers led to a massive selloff in gilts, with the 2yr yield (+26.1bps) hitting a post-2008 high of 4.90%, and the 10yr yield (+9.6bps) reaching its highest level since Liz Truss was PM back in October. Another effect was it left the 2s10s yield curve at its most inverted since 2007, although to be fair, the UK 2s10s has been a less reliable recession indicator than its US counterpart. We heard some brief comments from BoE Governor Bailey as well yesterday, who acknowledged that inflation was “taking a lot longer than expected” to come down. Their next meeting is a week tomorrow, and whilst a 25bp hike is fully priced, investors are still placing a 13% chance that it might be a larger 50bp move.

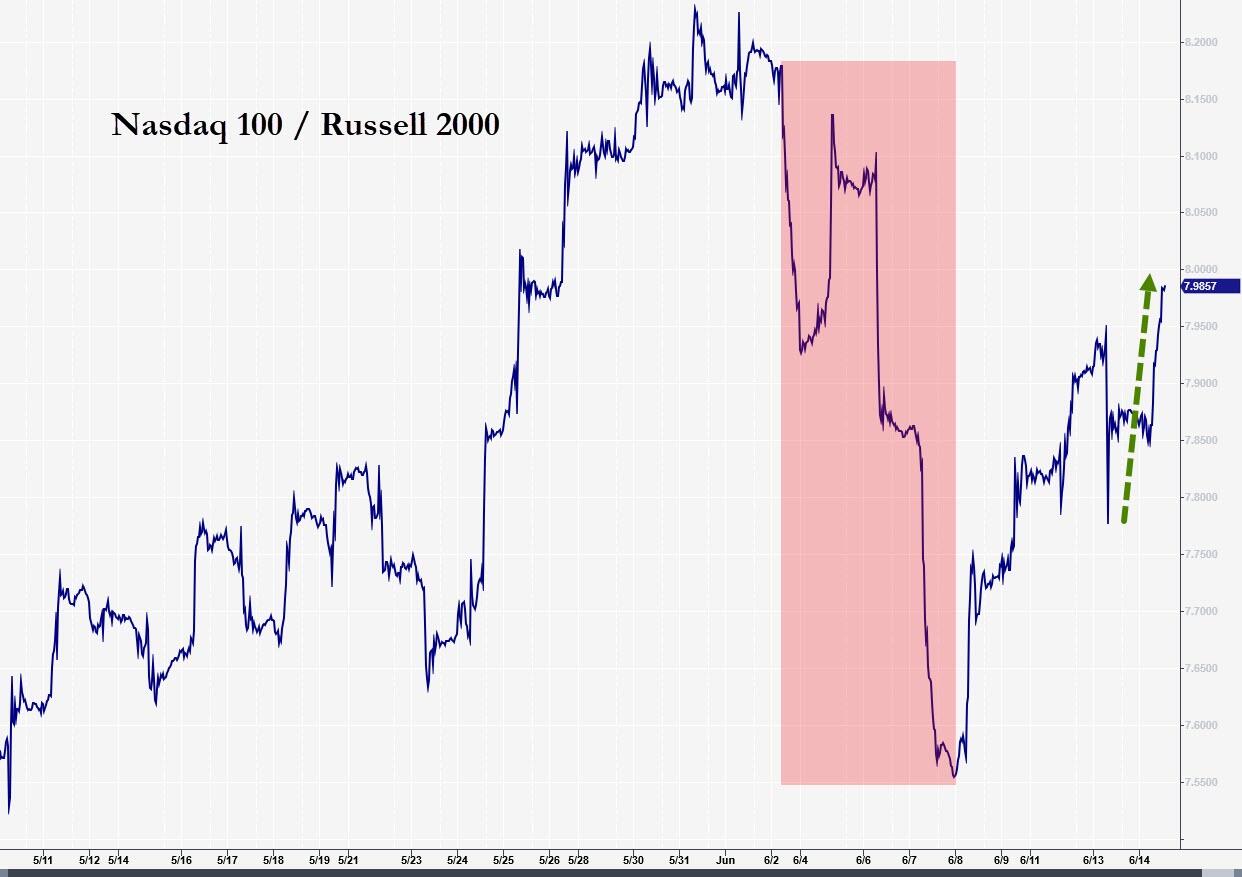

When it came to equities, there was no sign of any let-up in the latest rally, and the S&P 500 (+0.69%) continued to power forward. In fact, as it stands the index is on track for its 5th consecutive weekly advance, which is the first time that’s happened since late-2021. The big tech stocks again rose, with the FANG+ index gain (+0.89%) taking its YTD rally up to a massive +72.07%. That said, the equity rally was broader as small-cap stocks outperformed, with the Russell 2000 index up +1.23%, while the rate-sensitive utilities (-0.06%) and Telecom (-0.55%) stocks dragged on the broad equity rally.

Back in Europe, the picture was similarly buoyant, and the STOXX 600 posted a +0.55% advance. Growing risk appetite also meant there was a continued tightening in sovereign bond spreads, with the gap between Italian and German 10yr yields falling to another one-year low of 163bps. However, yields themselves mostly rose across the continent, with those on 10yr bunds (+3.5bps), OATs (+3.1bps) moving higher, while BTPs (-0.2bps) were virtually unchanged.

Asian equity markets are mostly trading higher this morning with the Nikkei (+0.87%) leading gains across the region and continuing to extend its three-decade highs. Meanwhile Chinese equities are also in the green with the CSI (+0.40%), the Shanghai Composite (+0.23%) and the Hang Seng (+0.10%) holding on to their gains. Elsewhere, the KOSPI (-0.47%) is the only major index trading in the red. US stock futures are little changed with those on the S&P 500 (-0.04%) and NASDAQ 100 (-0.02%) trading almost flat. Early morning data showed that the unemployment rate in South Korea unexpectedly dropped to 2.5% in May, a level last seen in August 2022 (v/s 2.7% expected) from 2.6% in April.

Although the data focus was on the CPI print yesterday, there were some interesting findings in the NFIB’s small business optimism index from the US. One notable warning was that the percentage of firms reporting an easing in credit conditions fell back to a net -10%, which is the lowest that’s been since 2012. Otherwise, the overall small business optimism index did rise to 89.4 (vs. 88.5 expected), but that’s still the second-worst reading of the last decade, having only seen a slight improvement on the previous month. Meanwhile in Germany, the ZEW survey showed a rebound in the expectations component to -8.5 (vs. -13.5 expected), ending three consecutive months of declines. However, the current situation fell back to a 5-month low of -56.5 (vs. -40.2 expected).

To the day ahead now, and the main highlight will be the Federal Reserve policy decision, along with Chair Powell’s press conference. Data releases will include the US PPI reading for May, as well as UK GDP and Euro Area industrial production for April.

end

2 b) NOW NEWSQUAWK (EUROPE/REPORT)/ASIA REPORT

Generally constructive risk tone in pre-FOMC trade – Newsquawk US Market Open

WEDNESDAY, JUN 14, 2023 – 06:28 AM

Equity bourses are firmer with the general risk tone constructive pre-FOMC

USD continues to wane and nears 103.00 to the modest benefit of peers, Antipodeans lead G10s

GBP is firmer post-GDP while EUR/USD is drawn to hefty 1.08 expiries

USTs bid before the Fed, Bunds slip after soft issuance and Gilts attempt to recoup from recent pressure

Crude consolidation continues, metals are mixed with fresh drivers limited

Looking ahead, highlights include US PPI. FOMC Policy Announcement & Fed Chair Powell’s Press Conference.

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

European bourses are firmer across the board, Euro Stoxx 50 +0.7%, having shrugged off the tepid open after a busy stock-specific pre-market though fresh macro drivers remain light.

Sectors are similarly supported with Real Estate leading after marked UK-related pressure on Tuesday while Autos and Banks benefit from a Barclays note and yields/BBVA’s ATI sale respectively.

Travel & Leisure bucks the trend after a downbeat update from Entain.

Stateside, futures are edging higher and moving in tandem with the above as the ES attains a firmer hold above 4400 pre-FOMC; newsquawk preview available here.

EU Antitrust Chief Vestager to hold a news conference at 11:45BST/06:45ET, expected to be on Alphabet’s (GOOGL) Google.

Shell (SHEL LN) announces a 15% dividend/shr increase from Q2 2023; Capital Spending reduced to USD 22-25bln/year for 2024 & 2025; Buybacks of at least USD 5.5bln for H2 2023.

Airbus (AIR FP) raises 20 year delivery forecast to 40.85k (prev. 39.45k); sees 17.1k aircraft replacements in the next 20 years (prev. 15.4k).

Click here and here for a recap of the main European updates.

Buck on the backfoot approaching Fed, with DXY heavy on the 103.000 handle awaiting guidance after a widely expected FOMC pause.

Kiwi underpinned around 0.6150 vs Greenback and 1.1000 against Aussie after better than expected NZ current account data, AUD/USD relatively bid near 0.6800 with support via strength in iron ore.

Sterling retains 1.2600+ status vs Dollar as UK GDP matches consensus and Euro probes 1.0800 where mega option expiry interest resides.

Yen takes advantage of softer US Treasury yields to rebound through 140.00.

Lira regains poise as Turkish President gives new Finance Minister and CBRT Governor go ahead to revert to orthodox policies ahead of next week’s CBRT.

PBoC set USD/CNY mid-point at 7.1566 vs exp. 7.1550 (prev. 7.1498)

Crude continues to consolidate with WTI Jul’23 and Brent Aug’23 inching above the USD 70.00/bbl and USD 75.00/bbl handles, specific drivers light.

Spot gold is incrementally firmer and at the top-end of the sessions range which is yet to see it gain any real traction above the USD 1950/oz mark as the broader risk tone remains robust and serves to offset any USD-driven upside.

Base metals are somewhat mixed, though this is seemingly more a function of yesterday’s pronounced gains for the complex earlier in the week.

US Energy Inventory Data (bbls): Crude +1.0mln (exp. -0.5mln), Gasoline +2.1mln (exp. +0.3mln), Distillate +1.4mln (exp. +1.2mln), Cushing +1.5mln.

IEA Monthly Oil Market Report: oil demand is set to increase by 2.4mln BPD in 2023 to a record of 102.3mln BPD (vs. May view of 102mln BPD). Click here for more.

Binance and SEC are reportedly not far apart on a deal to avoid a full asset freeze, according to Bloomberg.

Binance CEO Zhao denies rumours of selling Bitcoin to bolster BNB, according to Cointelegraph.

NOTABLE EUROPEAN HEADLINES

Turkish President Erdogan says he has accepted steps that the CBRT and Finance Minister Simsek will take. Click here for more detail & newsquawk analysis/reaction.

French Finance Minister Le Maire vowed to put France’s finances back on track with spending cuts, according to FT.

Downing Street has ordered banks to protect struggling homeowners from increasing mortgage costs as markets speculate over the possibility of the Bank Rate rising to as high as 6%, according to The Telegraph.

German Economy Ministry says economic data points to moderate recovery over further course of the year; “economic recession” in sense of more sustained downturn is not currently expected

NOTABLE EUROPEAN DATA

UK GDP Estimate MM (Apr) 0.2% vs. Exp. 0.20% (Prev. -0.30%); YY (Apr) 0.5% vs. Exp. 0.50% (Prev. 0.30%)

UK Services YY (Apr) 0.7% vs. Exp. 0.60% (Prev. 0.40%); MM (Apr) 0.3% vs. Exp. 0.30% (Prev. -0.50%)

UK Goods Trade Balance GBP* (Apr) -14.996B GB vs Exp. -16.5bln (Prev. -16.356B GB, Rev. -16.356B GB)

Swedish CPIF Ex Energy YY (May) 8.2% vs. Exp. 7.80% (Prev. 8.40%); MM (May) 0.7% vs. Exp. 0.40% (Prev. 0.40%)

GEOPOLITICS

Russia urged for a transparent investigation into the Nord Stream blasts after reports that the US warned Ukraine not to attack Nord Stream, according to Reuters.

White House said US President Biden met with the NATO chief and they underscored their shared desire to welcome Sweden to the alliance ASAP, while they also discussed the need for allies to build on the 2014 Wales summit defence investment pledge.

German National Security Strategy Document says China remains a partner without which cannot solve the many global challenges; China is increasingly pressuring regional stability and disrespecting human rights. Germany aims to spend 2% of GDP on defence on average over several years.

UN Nuclear Chief to visit Zaporizhzhia nuclear power plant on Thursday, one day later than planned, according to IFAX citing an official.

Turkish President Erdogan says constitutional amendments in Sweden are not enough to address Turkey’s concerns, the police should not allow such protests; adds, Sweden should not expect “anything different” from Turkey at the Nato summit.

APAC TRADE

APAC stocks were somewhat mixed with the region’s bourses mostly tentative ahead of the FOMC policy announcement.

ASX 200 was led by strength in the commodity-related sectors after China’s support pledges and PBoC cuts.

Nikkei 225 extended its advances as automakers and other exporters benefitted from recent currency moves and amid broad consensus for the BoJ to maintain its ultra-easy policy later this week

Hang Seng and Shanghai Comp. were kept afloat after the PBoC cut rates for its Standing Lending Facility by 10bps and the NDRC issued a notice on lowering costs this year with VAT to be exempted and reduced for small businesses until year-end. China was also said to be weighing broad stimulus with property support and rate cuts, although the gains in Chinese stocks were limited amid ongoing growth concerns and following softer-than-expected loans and financing data.

NOTABLE ASIA-PAC HEADLINES

Chinese Foreign Minister Qin Gang held a call with US Secretary of State Blinken and said the US should stop interfering with China’s internal affairs and should respect China’s concerns such as the Taiwan issue, while he added the US should stop hurting China under the excuse of competition and hopes the US will meet China halfway, effectively manage differences and promote communication and cooperation, according to state media.

Japanese PM Kishida is reportedly considering dissolving the Lower House of Parliament on the same day if the opposition submits a no-confidence vote on Friday, according to Fuji TV.

DATA RECAP

New Zealand Current Account (Q1) -5.2B vs. Exp. -6.8B (Prev. -9.5B); Current Account/GDP (Q1) -8.5% vs. Exp. -9.0% (Prev. -8.9%)

2 c. ASIAN AFFAIRS

ASIAN AND AUSTRALIAN CLOSINGS//EUROPE OPENING TRADING:

WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED DOWN 4.68 PTS OR 0.14% //Hang Seng CLOSED DOWN 113.00 PTS OR 0.58% /The Nikkei closed UP 483.77 OR 1.47% //Australia’s all ordinaries CLOSED UP 0.34 % /Chinese yuan (ONSHORE) closed DOWN 7.1581 /OFFSHORE CHINESE YUAN DOWN TO 7.1679 /Oil UP TO 70.31 dollars per barrel for WTI and BRENT DOWN AT 75.25 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

2 d./NORTH KOREA/ SOUTH KOREA/

///NORTH KOREA/SOUTH KOREA/

2e) JAPAN

JAPAN

END

3 CHINA /

CHINA/

A must read

Pepe Escobar on the BRI initiative:

Escobar: China’s BRI Has Fundamentally Transformed Global Geopolitics

In less than a decade, China’s BRI has fundamentally transformed global geopolitics. It is already far too late for the west to compete…

It is important to recognize that the US/NATO proxy war against Russia in Ukraine is simultaneously a war designed to interrupt the progress of China’s Belt and Road Initiative (BRI).

As we approach the 10th anniversary of the BRI, to be marked by the third Belt and Road Forum later this year in Beijing, it is clear the original Silk Road Economic Belt – announced by President Xi Jinping in Astana, Kazakhstan, in September 2013 – has traveled a long way.

By January this year, 151 nations had already signed up to the BRI: No less than 75 percent of the world’s population that represents more than half of the global GDP. Even an Atlanticist outfit such as the London-based Center for Economic and Business Research admits that the BRI may increase global GDP by a whopping $7.1 trillion a year by 2040, dispensing “widespread” benefits.

Included in the Chinese Constitution since 2018, BRI constitutes the de facto overarching Chinese foreign policy framework all the way to 2049, marking the centenary of the People’s Republic of China.

The BRI advances along several overland connectivity corridors – from the Trans-Siberian to the “middle corridor” along Iran and Turkiye and the China-Pakistan Economic Corridor (CPEC) all the way to the Arabian Sea. Meanwhile, on the waterways front, the Maritime Silk Road offers a parallel network from southeast China to the Persian Gulf, the Red Sea, the Swahili Coast, and the Mediterranean Sea.

All that is mirrored by the Russian-driven Northern Sea Route, connecting the eastern and western sides of the Arctic, and reducing to and fro sailing time from Europe to Asia from one month to less than two weeks.

Such a massive Make Trade Not War project, centered on connectivity, infrastructure building, sustainable development, and diplomatic acumen – focusing on the Global South – could not but be interpreted by western elites as a supreme geopolitical and geoeconomic threat.

And that’s why every geopolitical turbulence across the chessboard is directly or indirectly linked to BRI. Including Ukraine.

“A brand new choice”

At the Lanting Forum in Shanghai last month, Chinese Foreign Minister Qin Gang was at ease presenting to a select foreign audience the key outlines of “modernization, the Chinese way” and how it can be applied across the Global South.