by harveyorgan · in Uncategorized · Leave a comment·Edit

GOLD PRICE CLOSED: UP $2.80 TO $1958.30

SILVER PRICE CLOSED: DOWN $0.17 AT $23.85

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1957.90

Silver ACCESS CLOSE: 23.88

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

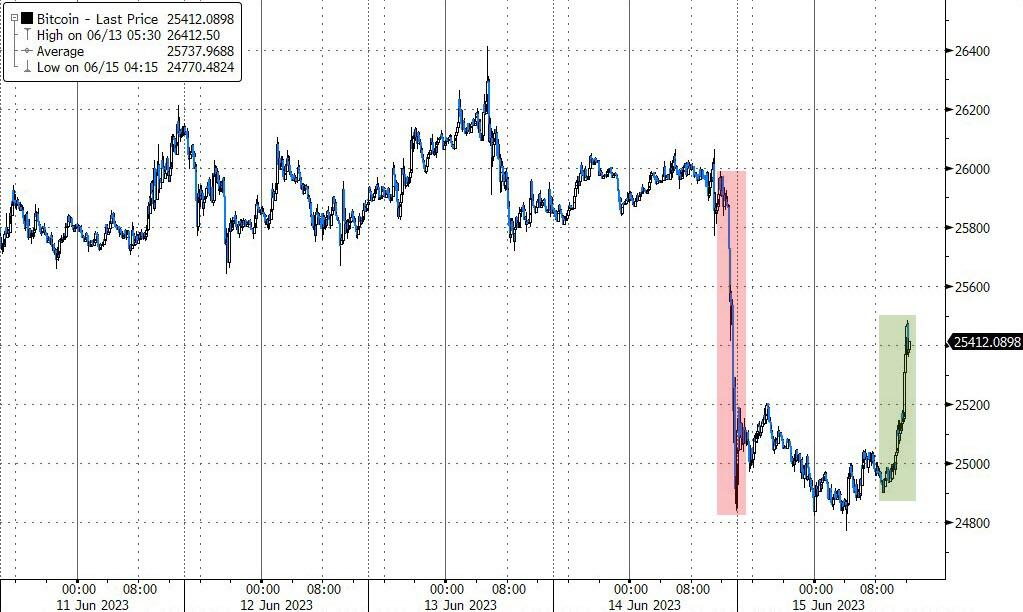

Bitcoin morning price:, $24,944 DOWN 977 Dollars

Bitcoin: afternoon price: $25,444 DOWN 477 dollars

Platinum price closing $990.85 UP $12.05

Palladium price; $1400.10 DOWN $.40

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,587.60 DOWN 4.73 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1531.54 DOWN 5.60 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1788.40 DOWN 8.13 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JUNE 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,955.300000000 USD

INTENT DATE: 06/14/2023 DELIVERY DATE: 06/16/2023

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 12

323 C HSBC 480

323 H HSBC 142

357 C WEDBUSH 1

363 H WELLS FARGO SEC 4

435 H SCOTIA CAPITAL 19

657 C MORGAN STANLEY 5

661 C JP MORGAN 255 367

661 H JP MORGAN 20

685 C RJ OBRIEN 1

690 C ABN AMRO 16 24

709 C BARCLAYS 5

737 C ADVANTAGE 5

880 H CITIGROUP 130

905 C ADM 16

TOTAL: 751 751

MONTH TO DATE: 18,903

JPMorgan stopped 387/751 contracts

FOR JUNE:

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2023. CONTRACT: 751 NOTICES FOR 75,100 OZ or 2.3359 TONNES

total notices so far: 18,903 contracts for 1,890,300 oz (58.796 tonnes)

FOR JUNE:

SILVER NOTICES: 0 NOTICE(S) FILED FOR NIL OZ/

total number of notices filed so far this month : 423 for 2,115,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $2.80

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:////A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//

INVENTORY RESTS AT 929.70 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 17 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.377 MILLION OZ FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 463.642 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 2019 CONTRACTS TO 151,874 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUMONGOUS SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.29 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. TAS ISSUANCE WAS A SMALL SIZED 384 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH . CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: A SMALL SIZED 384 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.29). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A HUMONGOUS GAIN ON OUR TWO EXCHANGES OF 3401 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 7.5 MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION.

WE MUST HAVE HAD:

AN ATMOSPHERIC SIZED ISSUANCE OF EXCHANGE FOR PHYSICALS( 4950 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.935 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP + 0 MILLION OZ EXCHANGE FOR RISK(ISSUED TODAY: TOTAL ISSUED SO FAR: 7.5 MILLION OZ)// TOTAL STANDING FOR THE MONTH 4.270 MILLION OZ + 7.5 MILLION EXCHANGE FOR RISK = 11.77 MILLION OZ// ) // HUMONGOUS SIZED COMEX OI LOSS/ ATMOSPHERIC SIZED EFP ISSUANCE/VI) SMALL NUMBER OF T.A.S. CONTRACT ISSUANCE (384 CONTRACTS)//ZERO T.A.S LIQUIDATION THROUGHOUT THE COMEX SESSION //WEDNESDAY BUT CONSIDERABLE LIQUIDATION DURING THE ACCESS MARKET//

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –470 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTRACTS for 10 days, total 9434 contracts: OR 47.170 MILLION OZ (943 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 47.170 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 47.170 MILLION OZ//

RESULT: WE HAD A HUMONGOUS SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2019 CONTRACTS DESPITE OUR GAIN IN PRICE OF $0.29 IN SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD AN ATMOSPHERIC SIZED EFP ISSUANCE CONTRACTS: 4950 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.935 MILLION OZ FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP+ 0 MILLION EXCHANGE FOR RISK TODAY + 7.5 MILLION EXCHANGE FOR RISK(PRIOR)//NEW TOTAL STANDING: 11.77 MILLION OZ////// .. WE HAVE A GIGANTIC SIZED GAIN OF 2931 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A SMALL 384//ZERO FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION BUT CONSIDERABLE LIQUIDATION DURING THE ACCESS MARKET. THE NEW TAS ISSUANCE TODAY (384) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE.

WE HAD 0 NOTICE(S) FILED TODAY FOR NIL OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2511 CONTRACTS TO 430,805 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED – 418 CONTRACTS

WE HAD A FAIR SIZED DECREASE IN COMEX OI ( 2511 CONTRACTS) DESPITE OUR $10.30 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JUNE. AT 70.79 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0.0246 TONNE QUEUE JUMP: NEW TOTAL 63.863 TONNES STANDING SO FAR // + /A SMALL ISSUANCE OF 742 T.A.S. CONTRACTS/ZERO FRONT END OF TAS LIQUIDATION WEDNESDAY COMEX SESSION BUT CONSIDERABLE LIQUIDATION DURING ACCESS MARKET ////YET ALL OF..THIS HAPPENED WITH A $10.30 GAIN IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING.WE HAD A TINY SIZED LOSS OF 439 OI CONTRACTS (1.3654 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2072 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 430,805

IN ESSENCE WE HAVE A TINY SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 21 CONTRACTS WITH 2093 CONTRACTS DECREASED AT THE COMEX//TAS CONTRACTS INITIATED (ISSUED): A SMALL 742 CONTRACTS) AND 2072 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 21 CONTRACTS OR 0.6531 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2072 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (2511) //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 439 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 70.79 TONNES FOLLOWED BY TODAY’S 800 OZ QUEUE JUMP //// NEW STANDING FALLS TO 63.863 TONNES// /3) ZERO LONG LIQUIDATION//4) FAIR SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: SMALL T.A.S. ISSUANCE: 742 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

TOTAL EFP CONTRACTS ISSUED: 20,963 CONTRACTS OR 2,096,300 OZ OR 65.204 TONNES IN 10 TRADING DAY(S) AND THUS AVERAGING: 2099 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAY(S) IN TONNES 65.204 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 65.204/3550 x 100% TONNES 1.830% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 65.204 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUMONGOUS SIZED 2019 CONTRACTS OI TO 151,834 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 4950 CONTRACTS (RECORD ISSUANCE)

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 4950 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 4950 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2019 CONTRACTS AND ADD TO THE 4950 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN AN ATMOSPHERIC SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2931 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 17.005 MILLION OZ

OCCURRED WITH OUR $0.29 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING//WEDNESDAY NIGHT

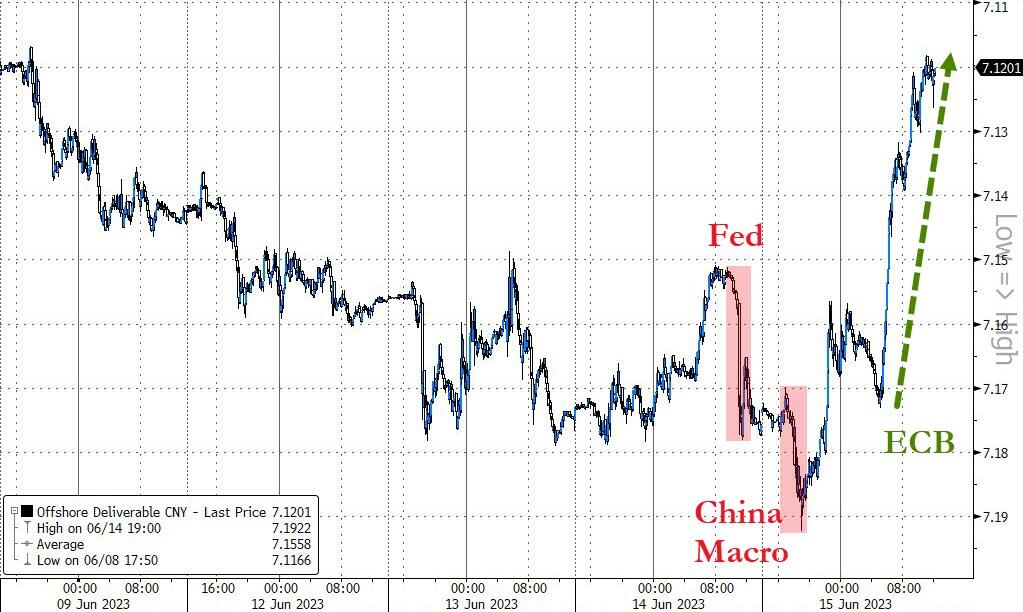

SHANGHAI CLOSED UP 23.99 PTS OR 0.74% //Hang Seng CLOSED UP 420.50 PTS OR 2.17% /The Nikkei closed DOWN 16.93 OR 0.05% //Australia’s all ordinaries CLOSED UP 0.22 % /Chinese yuan (ONSHORE) closed DOWN 7.1602 /OFFSHORE CHINESE YUAN DOWN TO 7.1700 /Oil DOWN TO 69.10 dollars per barrel for WTI and BRENT DOWN AT 73.87 / Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 2511 CONTRACTS DOWN TO 430,387 DESPITE OUR STRONG GAIN IN PRICE OF $10.30 ON WEDNESDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2072 EFP CONTRACTS WERE ISSUED: : AUGUST 2072 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2072 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A TINY SIZED TOTAL OF 439 CONTRACTS IN THAT 2072 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED LOSS OF 2511 COMEX CONTRACTS..AND THIS TINY SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR GAIN IN PRICE OF $10.30. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT WAS A SMALL 742 CONTRACTS. THROUGHOUT LAST WEEK, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THE HUGE NUMBER OF T.A.S. CONTRACTS INITIATED OVER THE PAST SEVERAL DAYS SPELLS TROUBLE FOR THE GOLD/SILVER MARKET AS RAIDS WILL SURELY BE UPON US.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (62.863) ( NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2003:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 62.863 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $10.30) //// AND WERE UNSUCCESSFUL IN KNOCKING A FEW SPECULATOR LONGS AS WE HAD OUR TINY SIZED LOSS OF 439 CONTRACTS ON OUR TWO EXCHANGES. WE HAD ZERO TAS LIQUIDATION THROUGHOUT THE COMEX SESSION ON WEDNESDAY BUT CONSIDERABLE CONTRACTS WERE LIQUIDATED IN THE ACCESS MARKET . THE TAS ISSUED WEDNESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 0.6531 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE. (70.709 TONNES) FOLLOWED BY TODAY’S 800 OZ QUEUE JUMP..NEW STANDING REMAINS AT 63.863 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $10.30

WE HAD – REMOVED 418 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET LOSS ON THE TWO EXCHANGES 439 CONTRACTS OR 43900 OZ OR 1.3654 TONNES.

Estimated gold volume today:// 258,962 fair

final gold volumes/yesterday 206,364 fair

//JUNE 15/ FOR THE JUNE 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 24,567.040 OZ ASAHI 578.728 oz BRINKS 18 kilobars . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 751 notice(s) 75,100 OZ 2.3359 TONNES |

| No of oz to be served (notices) | 1630 contracts 163000 oz 5.0699 TONNES |

| Total monthly oz gold served (contracts) so far this month | 18,902 notices 1,890,300 OZ 58.796 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

No dealer withdrawals

Customer deposits: 0

total deposits: nil oz

Withdrawals: 2

i) Out of Brinks: 578.72 oz

ii) Out of ASAHI: 24,567.040 oz

total 25,145.760 oz

Adjustments;1

i) ASAHI: 47,896.750 oz was adjusted out of the customer account into dealer

leaving zer0 oz eligible for ASAHI

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 2381 contracts having LOST 82 contracts. We had 90 contracts served on WEDNESDAY so we gained 8 contracts or an additional 800 oz will stand for gold at the comex.

The next front month after June is the non active delivery month of July. Here, July lost 243 contracts to stand at 2661 contracts.

AUGUST lost 2338 contracts down to 363,236 contracts

We had 751 contracts filed for today representing 75,100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 255 notices were issued from their client or customer account. The total of all issuance by all participants equate to 751 contract(s) of which 20 notices were stopped (received) by j.P. Morgan dealer and 367 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2023. contract month,

we take the total number of notices filed so far for the month (18,903 x 100 oz ), to which we add the difference between the open interest for the front month of JUNE (2381 CONTRACT) minus the number of notices served upon today 751 x 100 oz per contract equals 2,053,200 OZ OR 63.863 TONNES the number of TONNES standing in this active month of June.

thus the INITIAL standings for gold for the JUNE contract month: No of notices filed so far (18,903) x 100 oz + (2381) {OI for the front month} minus the number of notices served upon today (751) x 100 oz) which equals 2,053,200 oz standing OR 63.863 TONNES

TOTAL COMEX GOLD STANDING: 63.863 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,055,246.664 OZ 63.92 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,773,725,284 OZ

TOTAL REGISTERED GOLD: 11,702,019,946 (363.98 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 11,071,705.338 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,646,773 OZ (REG GOLD- PLEDGED GOLD) 300.05 tonnes//

END

SILVER/COMEX

JUNE 15//2023// THE JUNE 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 607,324.650 oz CNT Delaware HSBC . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 5023.400 oz Brinks |

| No of oz served today (contracts) | 0 CONTRACT(S) (NIL OZ) |

| No of oz to be served (notices) | 431 contracts (2,155,000 oz) |

| Total monthly oz silver served (contracts) | 423 Contracts (2,115,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposits

total dealer deposit: nil oz

total dealer deposits: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We had 1 deposits customer account:

i) Into Brinks 5023.400 oz

total customer deposits: 5023.400 oz

JPMorgan has a total silver weight: 142,366 million oz/271.773 million =52.39% of comex .//dropping fast

Comex withdrawals 3

i) Out of Delaware: 5940.300 oz

ii) Out of CNT: 1013.520 oz

iii) out of HSBC 600,370.830 oz

total withdrawals: 607,324.650 oz

adjustments: none

TOTAL REGISTERED SILVER: 27.117 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 271.773 million oz

DEALER SILVER DROPPING FAST. (moves into the 27 million oz column)

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE /2023 OI: 431 CONTRACTS HAVING LOST 0 CONTRACT(S).

WE HAD 0 NOTICES FILED ON WEDNESDAY SO WE LOST 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF JUNE

JULY HAD A 6332 CONTRACT LOSS TO 71,912 CONTRACTS

AUGUST LOST 2 CONTRACTS TO STAND AT 28

SEPT HAS A GAIN OF 4305 CONTRACTS UP TO 68,092

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes// est. volume today 95,852 very strong /

Comex volume: confirmed yesterday:75,876 good

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 423 x 5,000 oz = 2,115,000 oz

to which we add the difference between the open interest for the front month of JUNE(431) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2023 contract month: 423 (notices served so far) x 5000 oz + OI for the front month of JUNE (431) – number of notices served upon today (0 )x 500 oz of silver standing for the JUNE contract month equates to 4.270 million oz +7.5MILLION OZ EXCHANGE FOR RISK//NEW TOTAL: 11.77 MILLION OZ STANDING

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

JUNE 15/WITH GOLD UP $2.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 929.70 TONNES

JUNE 14/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 931.44 TONNES

JUNE 13/WITH GOLD DOWN $10.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.01 TONNES FORM THE GLD///INVENTORY RESTS AT 931.44

JUNE 12/WITH GOLD DOWN $7.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.65 TONNES

JUNE 9/WITH GOLD DOWN $1.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.65 TONNES

JUNE 8/WITH GOLD UP $20.45 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.46 TONNES FROM THE GLD///INVENTORY RESTS AT 934.65 TONNES

JUNE 7 WITH GOLD DOWN $22.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 938.11 TONNES

JUNE 6/WITH GOLD UP $6.90 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 939.56 TONNES

JUNE 5/WITH GOLD UP $5.00 TODAY : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 938.11 TONNES

JUNE 2/WITH GOLD DOWN $24.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 938.11 TONNES

JUNE 1/WITH GOLD UP $14.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 939.56 TONNES

MAY 31/WITH GOLD UP $5.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 939.56 TONNES

MAY 30/WITH GOLD UP $14.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 26/WITH GOLD UP $.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 941.29 TONNES

MAY 25/WITH GOLD DOWN $19.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 24/WITH GOLD DOWN $9.50 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 941.29 TONNES

MAY 23/WITH GOLD $2.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 942.74 TONNES

MAY 22/WITH GOLD DOWN $4.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.83 TONES OF GOLD INTO THE GLD DESPITE THE L0SS IN PRICE//INVENTORY RESTS AT 942.74 TONNES

MAY 19/WITH GOLD UP $22.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 936.96 TONNES

MAY 18/WITH GOLD DOWN $23.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 936.96 TONNES

MAY 17/WITH GOLD DOWN $8.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.94 TONNES

MAY 16/WITH GOLD DOWN 28.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.57 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 934,07

MAY 15/WITH GOLD UP $2.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 937.64 TONNES

MAY 12/WITH GOLD DOWN $.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 937.84 TONNES

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 934.95 TONNES

GLD INVENTORY: 929.70 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 15/WITH SILVER DOWN 17 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.377 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 463.642 MILLION OZ//

JUNE 14/WITH SILVER UP 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 735,000 OZ FROM THE SLV///INVENTORY RESTS AT 465.019 MILLION OZ//

JUNE 13/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.515 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 465.754 MILLION OZ//

JUNE 12/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.269 MILLION OZ//

JUNE 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF SILVER TO THE TUNE OF 550,000 OZ//INVENTORY RESTS AT 467.269 MILLION OZ

JUNE 8/WITH SILVER UP $0.63 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 467.819 MILLION OZ/

JUNE 7/WITH SILVER DOWN 17 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.01 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 467.819 MILLION OZ/

JUNE 6/WITH SILVER UP 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.809 MILLION OZ//

JUNE 5/WITH SILVER DOWN $.13 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 266,000 OZ FROM THE SLV////INVENTORY RESTS AT 466.809 MILLION OZ/

JUNE 2/WITH SILVER DOWN 23 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV./INVENTORY RESTS AT 467.015 MILLION OZ/

JUNE 1/WITH SILVER UP 49 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.933 MILLION OZ

MAY 31/WITH SILVER UP 37 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 367,000 OZ FROM THE SLV////INVENTORY RESTS AT 467.933 MILLION OZ//

MAY 30/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 26/WITH SILVER UP $0.44 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.306 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 25.WITH SILVER DOWN $0.32 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 471.606 MILLION OZ//

MAY 24/WITH SILVER DOWN $.35 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 23/WITH SILVER DOWN 22 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.801 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 22/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ//

MAY 19/WITH SILVER UP 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ

MAY 18/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.529 MILLION OZ/

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

MAY 16/WITH SILVER DOWN 34 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .643 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.448 MILLION OZ.

MAY 15/WITH SILVER UP 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.091 MILLION OZ/

MAY 12/WITH SILVER DOWN $.26 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 3,123 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 470.091 MILLION OZ./

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

CLOSING INVENTORY 463.642 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

END

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

3,Chris Powell of GATA provides to us very important physical commentaries

USA has swapped more gold and the amount is 188 tonnes from the beginning of 2023. The BIS is nervous that they will not get their gold back.

(Robert Lambourne)

Robert Lambourne: BIS gold swaps rose 39% in May amid U.S. debt turmoil

Submitted by admin on Wed, 2023-06-14 15:12Section: Daily Dispatches

By Robert Lambourne

Wednesday, June 14, 2023

Gold swaps by the Bank for International Settlements rose markedly in May, according to the bank’s monthly account statement, published this week:

The bank’s gold swaps are estimated to be 188 tonnes as of May 31, a 39% increase over the 135 tonnes reported as of April 30. As shown in Table B below, recent months have brought much volatility in the level of swaps.

Evidence of the significant trading carried out via BIS gold swaps is provided by the changes in the monthly volumes of swaps since October 2022. At that time there were an estimated 7 tonnes of swaps outstanding, but this increased to 105 tonnes at November 30 and then fell back to none at December 31.

Significant changes and continued this year, with 103 tonnes of gold swaps estimated as of January 31, followed by 136 tonnes as of February 28, 78 tonnes as of March 31, 135 tonnes as of April 30, and 188 tonnes as of May 31.

Once again it seems reasonable to suspect that the BIS has entered these swaps on behalf of the U.S. Federal Reserve. With the new deal on the U.S. federal government debt ceiling causing political turmoil in May, a rising gold price probably would have been unwelcome by U.S. authorities.

The basic transaction that the BIS undertakes with gold swaps is to exchange dollars for gold from a bullion bank and then deposit the gold in a gold sight account at a central bank, almost certainly being the central bank that is using the BIS to execute the gold swap on its behalf.

Given the recent volatility in the level of BIS gold swaps, it seems likely that the swaps are mainly of a short duration. Why a central bank would need the BIS to undertake these gold swaps isn’t clear, but the swaps may be linked to short-term trading needs. This trading could aim to suppress the gold price.

Using the May 31 gold price of $1,966 (per USAGold.com), the 188 tonnes of BIS gold swaps as of May 31 are valued at about $11.9 billion. Hence it is evident that the recent volatility in BIS gold swaps involves high value and shows that gold remains a significant monetary asset.

As ever with the BIS, it remains unlikely that more information about the reasons for the bank to undertake these transactions, presumably on behalf of a central bank client, will ever be provided. This secrecy implies that central bank gold policy involves much deception of the public and the markets — that it is a form of currency market intervention for which the BIS provides camouflage.

The worsening finances of Western governments, especially the U.S. government, may reduce the appeal of gold swaps to the BIS and the central bank or banks for which the BIS has been acting. In this context a report issued by GATA in 2012 —

https://www.gata.org/node/11304

— is worth revisiting, since it highlights acknowledgment of gold price suppression by a former chairman of the BIS, Jelle Zilstrra, a Dutch politician and economist. BIS management almost certainly understands very well what the swaps are being used for and why they are camouflaged.

The recent strength of the gold price together with the conundrum facing the Federal Reserve about raising dollar interest rates must reduce the appeal of having to return swapped gold to bullion banks.

Despite its rhetoric about pushing interest rates higher, the Fed needs to avoid more erosion of confidence in the U.S. Treasuries market when the U.S. government’s rising debt recently has been so controversial.

The Treasury Department’s May report demonstrates three continuing adverse trends. Lower cumulative revenues than were received in the same period a year ago and higher cumulative expenditure contributed to much higher interest costs aided by higher interest rates set by the Federal Reserve:

https://www.fiscal.treasury.gov/files/reports-statements/mts/mts0523.pdf

Because of the special measures taken by the Treasury Department to avoid breaching the former debt ceiling, it seems likely that the portion of the underlying interest cost payable to government-sponsored trust funds has been underreported recently, but this presumably will be corrected in June and subsequent months, providing a clearer picture of the growing interest cost. The cumulative interest charge on the externally held debt is up by 33% over the same period in 2022, indicating the problem that higher interest costs cause for the U.S. government’s borrowing.

In these circumstances the room for the Fed to keep raising interest rates seems restricted and hence it seems that the BIS and some of its owners — other central banks — might be questioning the role of the bank in these swaps and the obligation to make future deliveries of gold.

Indeed, a cynic might claim that the recent deal on the federal government debt makes it easier to defend a banking crisis by allowing the U.S. government to offer more bank deposit guarantees. The debt ceiling deal may even make a revaluation of gold easier for the United States to carry out.

As is clear from Table B below, the level of BIS swaps had been significantly higher in the first half of last year, and the October and December totals were easily the lowest in more than four years.

* * *

Table A below highlights the level of gold swaps reported in the annual reports of the BIS back to 2010, when the bank’s use of gold swaps appears to have begun. At only one year-end since then, in March 2016, has the swap level been zero.

(The BIS’ half-year report to September 30, 2022, discloses that the BIS still holds 102 tonnes of its own gold and that very little of its activities in derivatives are with central banks. An assumption that the gold held by the BIS remains at 102 tonnes has been used to make the estimate of the gold swap level for December. The low level of derivatives reported by the BIS using central banks as counterparties, disclosed in the last interim report, is a reason to assume that the swaps are almost certainly done with gold bullion banks rather than central banks. Historically, the first swaps described below were done with bullion banks.)

* * *

… Historical context …

The BIS rarely comments publicly on its gold activities, but its first use of gold swaps was considered important enough to cause the bank to give some background information to the Financial Times for an article published July 29, 2010, coinciding with publication of the bank’s 2009-10 annual report.

The general manager of the BIS at the time, Jaime Caruana, said the gold swaps were “regular commercial activities” for the bank, and he confirmed that they were carried out with commercial banks and so did not involve central banks. It also seems highly likely that the BIS’ remaining swaps are still all made with commercial banks, because the BIS annual report has never disclosed a gold swap between the BIS and a major central bank.

The swap transactions potentially created a mismatch at the BIS, which may have ended up being long unallocated gold (the gold held in BIS sight accounts at major central banks) and short allocated gold (the gold required to be returned to swap counterparties). This possible mismatch has not been reported by the BIS.

The gold banking activities of the BIS have been a regular part of the services it offers to central banks since the bank’s establishment 90 years ago. The first annual report of the BIS explains these activities in some detail:

http://www.bis.org/publ/arpdf/archive/ar1931_en.pdf

A June 2008 presentation made by the BIS to potential central bank members at its headquarters in Basel, Switzerland, noted that the bank’s services to its members include secret interventions in the gold and foreign exchange markets:

https://www.gata.org/node/11012

The use of gold swaps to take gold held by commercial banks and then deposit it in gold sight accounts held in the name of the BIS at major central banks doesn’t appear ever to have been as large a part of the BIS’ gold banking business as it has been in recent years, although the recent declines suggest this is changing.

As of March 31, 2010, excluding gold owned by the BIS, there were 1,706 tonnes held in the name of the BIS in gold sight accounts at major central banks, of which 346 tonnes or 20% were sourced from gold swaps from commercial banks.

If the BIS was adopting the level of disclosures made by publicly held companies, such as commercial banks, some explanation of these changes probably would have been required by the accounting regulators. This irony may not be lost on those dealing with regulatory activities at the BIS. Presumably the shrinkage of the BIS’ gold banking business shows that even central banks now prefer to hold their own gold or hold it in earmarked form — that is, as allocated gold.

A review of Table B below highlights recent BIS activity with gold swaps, and despite the recent declines, the recent positions estimated from the BIS monthly statements have regularly been large, especially in early 2022, and the volume of trading has been significant.

No explanation for this continuing use of swaps has been published by the BIS. Indeed, no comment on the bank’s use of gold swaps has been offered since 2010.

This gold is supplied by bullion banks via the swaps to the BIS. The gold is then deposited in BIS gold sight accounts (unallocated gold accounts) at major central banks such as the Federal Reserve.

The reasons for this activity have never been fully explained by the BIS and various conjectures have been made as to why the BIS has facilitated it. One conjecture is that the swaps are a mechanism for the return of gold secretly supplied by central banks to cover shortfalls in the gold markets. The use of the BIS to facilitate this trade suggests of a desire to conceal the rationale for the transactions.

As can be seen in Table A below, the BIS has used gold swaps extensively since its financial year 2009-10. No use of swaps is reported in the bank’s annual reports for at least 10 years prior to the year ended March 2010.

The February 2021 estimate of the bank’s gold swaps (552 tonnes) was higher than any level of swaps reported by the BIS at its March year-end since March 2010. The swaps reported at March 2021 were at the highest year-end level reported, as is clear from Table A.

—–

Table A — Swaps reported in BIS annual reports

March 2010: 346 tonnes.

March 2011: 409 tonnes.

March 2012: 355 tonnes.

March 2013: 404 tonnes.

March 2014: 236 tonnes.

March 2015: 47 tonnes.

March 2016: 0 tonnes.

March 2017: 438 tonnes.

March 2018: 361 tonnes.

March 2019: 175 tonnes

March 2020: 326 tonnes

March 2021: 490 tonnes

March 2022: 358 tonnes

—–

The table below reports the estimated swap levels since August 2018. It can be seen that the BIS is actively involved in trading gold swaps and other gold derivatives with changes from month to month reported in excess of 100 tonnes in this period.

—–

Table B – Swaps estimated by GATA from BIS monthly statements of account

Month …. Swaps

& year …. in tonnes

May-23 … /188

Apr-23 … /135

Mar-23 … /78

Feb-23 … /136

Jan-23 …/103

Dec-22 … /0

Nov-22 … /105

Oct-22 ….. /7

Sep-22 …../57

Aug -22 ….. /75

Jul-22 ….. /56

Jun-22 ….. /202

May-22 ….. /270

Apr-22 ….. /315

Mar-22 …. /358

Feb-22 …. /472

Jan-22 ….. /501

Dec-21…. /414

Nov-21…. /451

Oct-21…. /414

Sep-21 …. /438

Aug-21 …. /464

Jul-21 …. /502

Jun-21 …./471

May-21 …./517

Apr-21 …. /472

Mar-21…. /490±

Feb-21 …../552

Jan-21 …. /523

Dec-20 …. /545

Nov-20 …. /520

Oct-20 …. /519

Sep-20…../ 520

Aug-20…../ 484

Jul-20 ….. / 474

Jun-20 …. / 391

May-20 …. / 412

Apr-20 …. / 328

Mar-20 …. / 326**

Feb-20 …. / 326

Jan-20 …. / 320

Dec-19 …. / 313

Nov-19 …. / 250

Oct-19 …. / 186

Sep-19 …. / 128

Aug-19 …. / 162

Jul-19 ….. / 95

Jun-19 …. / 126

May-19 …. / 78

Apr-19 ….. / 88

Mar-19 …. / 175

Feb-19 …. / 303

Jan-19 …. / 247

Dec-18 …. / 275

Nov-18 …. / 308

Oct-18 …. / 372

Sep-18 …. / 238

Aug-18 …. / 370

± The estimate originally reported by GATA was 487 tonnes, but the BIS annual report states 490 tonnes, It is believed that slightly different gold prices account for the difference.

** The estimate originally reported by GATA was 332 tonnes, but the BIS annual report states 326 tonnes. It is believed that slightly different gold prices account for the difference.

GATA uses gold prices quoted by USAGold.com to estimate the level of gold swaps held by the BIS at month-ends.

—–

As noted already, the BIS in recent times has refused to explain its activities in the gold market, nor for whom the bank is acting:

https://www.gata.org/node/17793

Despite this reticence the BIS has almost certainly acted on behalf of central banks in taking out these swaps, as they are the BIS’ owners and control its Board of Directors. Historically, the BIS has often acted on behalf of the Federal Reserve.

This refusal to explain prompts some observers to believe that the BIS acts as an agent for central banks intervening surreptitiously in the gold and currency markets, providing those central banks with access to gold as well as protection from exposure of their interventions.

As mentioned above, it is possible that the swaps provide a mechanism for bullion banks to return gold originally lent to them by central banks to cover bullion bank shortfalls of gold. Some commentators have suggested that a portion of the gold held by exchange-traded funds and managed by bullion banks is sourced directly from central banks.

—–

Robert Lambourne is a retired business executive in the United Kingdom who consults with GATA about the involvement of the Bank for International Settlements in the gold market.

END

end

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES/

Is this the start? China calls for an Internation silver market reform!

(James Anderson)

Chinese Call for International Silver Market Reform

Updated June 12, 2023

By James Anderson

Gold & Silver News

We begin with an update from China where silver bullion demand for industrial inputs and jewelry demand is outpacing diminishing silver bullion supply levels.

How is their state run media covering this ongoing, underreported story?

This week it was announced that one of China’s largest banks, the China Construction Bank is increasing its global capacity to service its local and global client base in precious metals and bulk commodity trading.

Meanwhile early this week, there was an open article written in China Bai news calling for international silver market reform. Explicitly citing the ridiculous outsized paper derivative leverage used by the COMEX and City of London’s LBMA markets in order to keep gold and especially silver values at still suppressed price levels.

The author cuts to the chase regarding diminishing silver bullion supplies stating the following.

Two weeks ago on this SD Bullion youtube channel, we showed you the record sized silver bullion withdrawal that the author was referring to at the end of his plea for higher silver values for future civilization’s industrial development.

Certainly every industry Elon Musk is involved in will require more and more industrial silver moving ahead.

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

This should cause Bitcoin prices to fall: Blackrock is close to filing for a Bitcoin ETF

(zerohedge)

BlackRock Close To Filing For Bitcoin ETF: Report

THURSDAY, JUN 15, 2023 – 10:34 AM

After dumping overnight on the latest negative development in what has been a relentless onslaught of bad news for crypto – when South Korean bitcoin lending platforms Delio and Haru announced the temporary suspension of customer withdrawals “in order to safely protect the assets of customers currently in custody” – this morning the crypto space finally got some welcome news when CoinDesk reported that BlackRock, the world’s biggest asset manager, is close to filing an application for a Bitcoin ETF.

According to the report, BlackRock will be using Coinbase Custody for the ETF and the crypto exchange’s spot market data for pricing.

BlackRock began working with Coinbase to make crypto directly available to institutional investors midway through last year.

It wasn’t clear if the ETF will be spot or futures; to date, the Securities and Exchange Commission, led by political activist Gary Gensler whose primary objective is to follow Democrat demand that the US crypto industry be crippled, which oversees ETFs in the U.S., has rejected every application for a spot bitcoin ETF, though it has approved several bitcoin futures ETFs for trading.

The fact that the world’s largest asset manager is again stepping up in the crypto space is a welcome development at a time when the politicized SEC has been weaponized to execute Democrat marching orders to crush the crypto industry in the US (thereby making the future of bitcoin a key issue in the 2024 elections), and comes just one day after the FT reported that in a surprising twist, China appears to also be warming up to crypto after years of crackdowns, and that Hong Kong’s banking regulator is pressuring lenders including HSBC and Standard Chartered to take on crypto exchanges as clients, at a time of unprecedented crackdowns by US regulators on the industry.

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS/THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.1602

OFFSHORE YUAN: 7.1700

SHANGHAI CLOSED UP 23.99 PTS OR 0.74%

HANG SENG CLOSED UP 420.50 PTS OR 2.17%

2. Nikkei closed DOWN 16.93 PTS OR 0.05%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 102.78 EURO FALLS TO 1.0829 DOWN 13 BASIS PTS

3b Japan 10 YR bond yield: FALLSS TO. +.424 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 141.22/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN// OFF- SHORE:DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.508***/Italian 10 Yr bond yield RISES to 4.180*** /SPAIN 10 YR BOND YIELD RISES TO 3.471…** DANGEROUS//

3i Greek 10 year bond yield RISES TO 3.853

3j Gold at $1927.95 silver at: 23.34 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 62 /100 roubles/dollar; ROUBLE AT 83.54//

3m oil into the 69 dollar handle for WTI and 73 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 141.22 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .424% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9021 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9769 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.835 UP 4 BASIS PTS…

USA 30 YR BOND YIELD: 3.906 UP 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.757 UP 8 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 23.66…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.4605 UP 7 BASIS PTS (RATES RISING RAPIDLY)

end

2. Overnight: Newsquawk and Zero hedge:

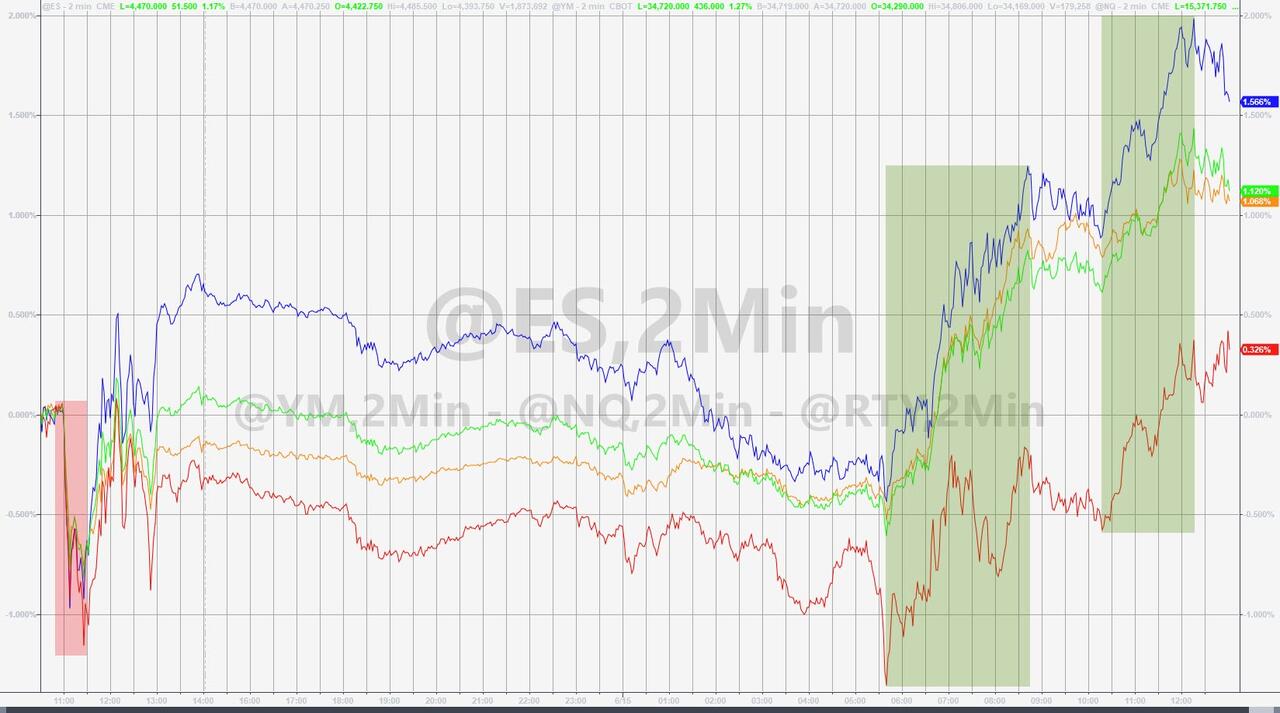

Futures Drop As Markets Reassess Fed’s Hawkish Skip; ECB Looms

THURSDAY, JUN 15, 2023 – 08:02 AM

Futures are lower, reversing much of the post-hawkish FOMC euphoria, as markets digest the Fed meeting, the decision to halt rates while projecting two more rate hikes, the increase in the terminal rate, and when the Fed begins an easing cycle, and concluding that the mix is not as bullish as they thought less than 24 hours ago. As of 7:30am, emini S&P futures were down 0.4% to 4,400 while Nasdaq futures dropped 0.7%. Treasury yields are climbing after warnings from the Fed yesterday that rates will go higher in the coming months, which also helped pull the USD higher. Commodities are seeing a modest relief rally with Ags leading while gold prices are falling, with the higher rate outlook generally a dampener on appetite for bullion, while oil and iron ore both climb. Today’s macro focus is on Retail Sales and Jobless Claims as CPI and unemployment become the two major data points ahead of the July Fed where the market is pricing ~70% chance of a 25bps hike. The next CPI is on July 12 and NFP is July 7.

In premarket trading, Tesla fell as much as 3% on course to extend losses after the world’s most valuable automaker snapped its record-setting 13-session streak of gains on Wednesday. US-listed Chinese stocks gained after China’s central bank cut interest rates again, this time on one-year loans just minutes before releasing the latest dismal economic data dump, lifting hope for more policy stimulus to come as the latest data pointed to a darkening economic picture. Crypto-related stocks fell in US premarket trading, tracking a dip in Bitcoin as worries re-emerge over the sector’s risks following news that two South Korea-linked crypto platforms have halted withdrawals. Coinbase shares fall as much as 3.6%, Riot Platforms -3.5%. Here are some other notable premarket movers:

- Coherent rose as much as 4.3% in premarket trading, set to extend Wednesday’s gains spurred by the company’s unveiling of new laser processing heads aimed at electric-vehicle manufacturing.

- Domino’s Pizza rises 2.1% in US premarket trading after Stifel upgrades the restaurant chain to buy from hold, predicting delivery sales to stabilize over the next 12 months, while carryout sales grow to new record highs

- Nikola jumps as much as 22% in premarket trading, set to extend gains for a seventh consecutive session — which would be its longest winning streak since November 2020.

- Nvidia falls as much as 1.3% in premarket trading, putting the stock on course to snap a five-day winning streak that has boosted the market value of the world’s most valuable chip company beyond $1 trillion.

- SoFi Technologies drops 3.5% in US premarket trading as Oppenheimer downgrades the online lender to perform from outperform, with the stock’s valuation now seen capturing its positive outlook

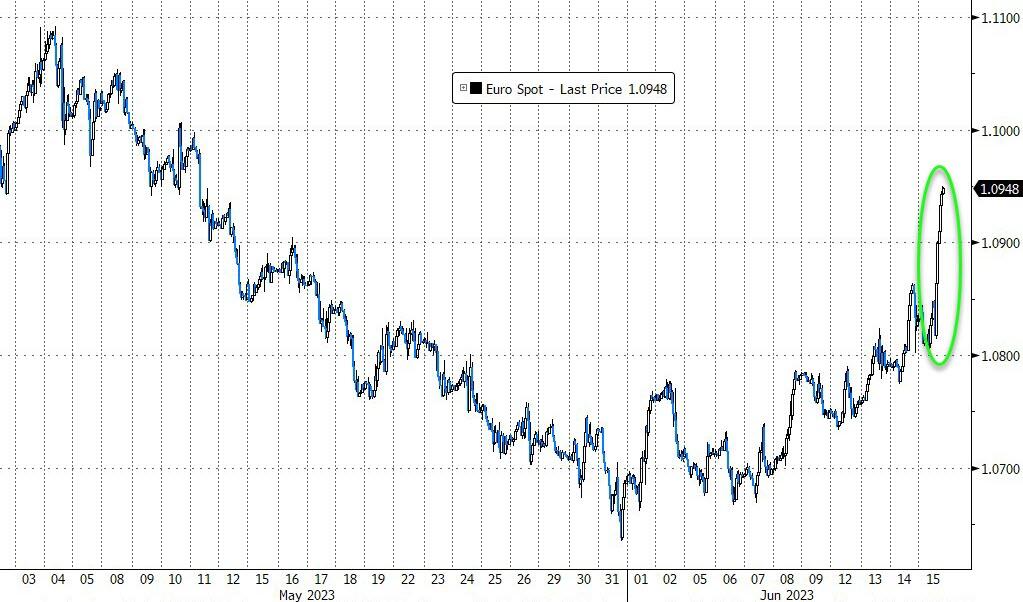

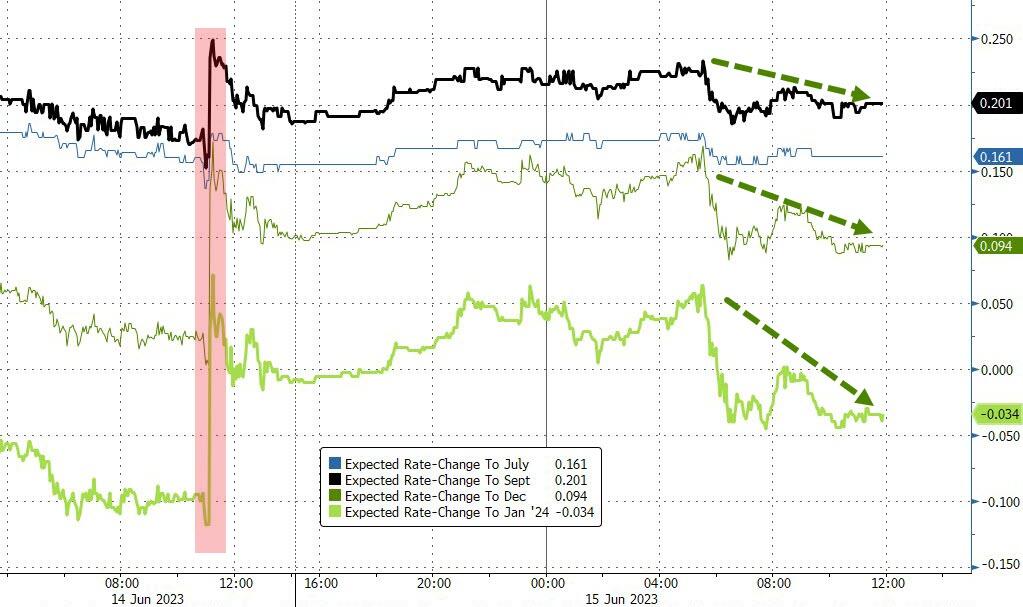

After the Fed quashed enthusiasm in markets about the potential for imminent rate cuts, investors are about to get an update from the ECB. The bank is expected to raise its deposit rate by a quarter-point to 3.5% later Thursday – even though Europe officially entered a technical recession just a few days ago – with attention mostly focused on what else officials intend to do to tackle inflation that’s still three times the 2% target.

“With the Fed’s policy rate likely to peak soon, the ECB may not want to be too far behind,” said Geoff Yu, a foreign exchange and macro strategist at BNY Mellon. “As tempting it may be to price a turn, we believe this week’s meeting is far too soon.”

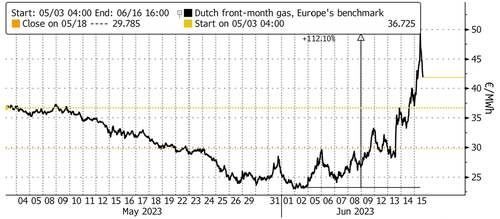

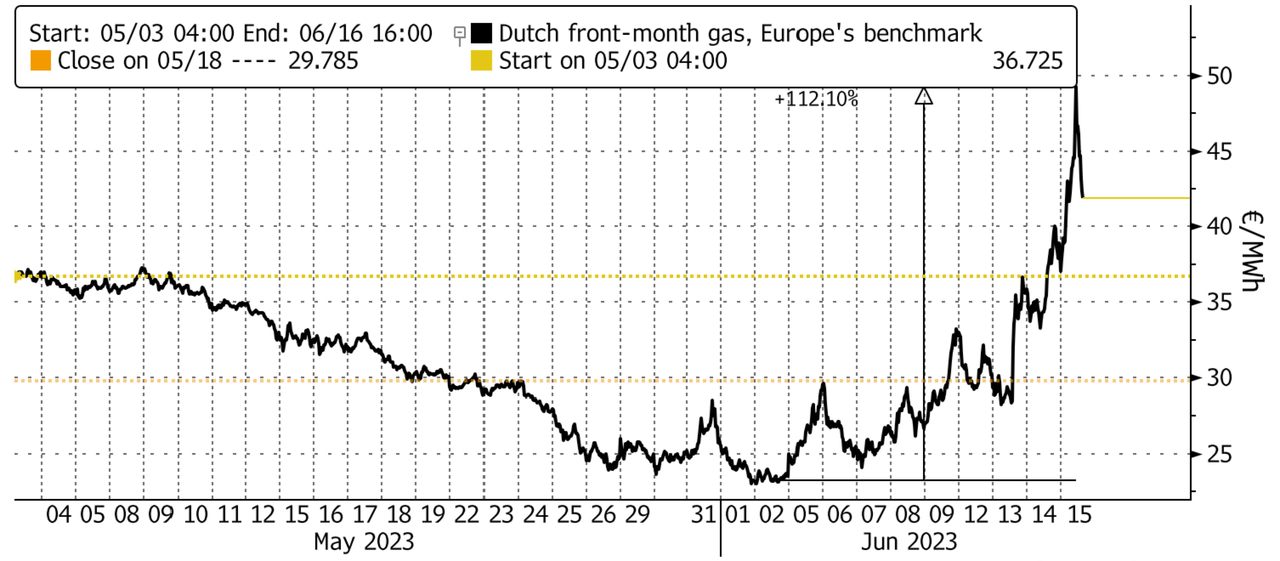

Meanwhile, in a stark reminder just how fragile Europe’s inflationary picture is, concerns over European gas supplies are back on traders’ radar. Bloomberg reported that European natural gas prices spiked as the Netherlands is set to announce it will close the region’s biggest gas site later this year. Benchmark futures soared as much as 24% on Thursday to their highest level since early April.

European stocks were also on the back foot ahead of the ECB decision later today. The Stoxx 600 is down 0.4% and on course to snap a three-day winning streak as mining stocks underperform. In corporate news, SoftwareOne Holding AG surged as much as 21% after Bain Capital offered about $3.2 billion to take the Swiss IT services provider private. Global miners Anglo American and Rio Tinto fell as basic resources stocks led declines in Europe following news that Chinese economic activity softened in May. But retailers were a bright spot, with H&M and Asos Plc rallying on improving prospects. Here are the most notable European movers:

- Hennes & Mauritz shares rise as much as 6.9%, reaching the highest since April 25 and gaining for the fourth session in a row. Jefferies highlights a strong start for the fiscal year’s third quarter

- Informa gains as much as 4.3% to the highest level since February 2020, after the events and publishing firm boosts revenue and operating profit guidance ranges ahead of its AGM

- Asos shares rise as much as 16%, the most since Jan. 12, after the online fast-fashion retailer provided a 3Q sales update and kept its outlook unchanged for the year

- PostNL rises as much as 6.5% after being raised to buy from hold at ING, based on the Dutch delivery company’s 1Q beat and recovery in the parcel volume trend in March and April

- Krones advances as much as 6.4%, the most since early November, as Hauck & Aufhaeuser lifts its rating to buy, citing improving margin expansion for the maker of packaging robots

- SoftwareONE shares rise as much as 21% after Bain Capital offered 2.93 billion Swiss francs ($3.2 billion) in cash to take the company private, a bid the board said materially undervalues the business

- Halma shares drop as much as 9.4%, the most since March 2020, after the UK health and safety sensor tech firm’s FY results showed a decline in its return on sales in the second half of its FY

- Bachem falls as much as 5.7% after Baader Helvea downgrades the shares to reduce from add, giving the Belgian biotech its only negative analyst rating, one reason being currency drag

- Billerud shares fall as much as 11%, the most since May 25, before trimming most losses after the Swedish paper and pulp manufacturer flagged its second-quarter profit will be lower than previously predicted

- Bunzl shares decline as much as 2.8% after the UK distribution group’s trading update implied a slowdown in organic growth in 2Q and flagged volume weakness in its North American business

- HMS Networks falls as much as 7%, the most since December, after the industrial communications firm was downgraded to sell from hold at ABG Sundal Collier, expecting negative order growth

Earlier in the session, Asian markets traded mostly higher; Chinese equities gained after the People’s Bank of China cut a key lending rate amid speculation that more stimulus is on the way. That also boosted US-listed Chinese stocks, with Alibaba Group and Baidu among those advancing in premarket trading. The PBOC’s move also forms part of broader stimulus efforts to support real estate and domestic demand. Data showing retail sales moderated more than expected in May added to worries about further slowing in China. Industrial production was also lower, but met consensus forecasts.

- Hang Seng and Shanghai Comp. were positive with outperformance in Hong Kong after the HKMA kept rates unchanged for the first time since March 2022 in lockstep with the Fed, while the advances were led by property names amid expectations for more support measures for the industry and after Chinese House Prices returned to growth. Furthermore, the PBoC cut its 1-year MLF rates by 10bps following similar cuts to short-term funding rates although participants also digested disappointing activity data from China in which both Industrial Production and Retail Sales missed estimates.

- ASX 200 was kept afloat in rangebound trade with stellar jobs data partly clouded by yield curve inversion.

- Nikkei 225 benefitted from currency depreciation and encouraging data including Exports and Machinery Orders.

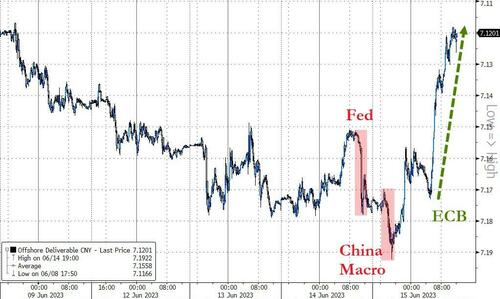

In FX, the dollar trimmed its first advance in three days, gains prompted by traders mulling prospects for further US rate hikes. The Aussie dollar is among the best-performing G10 currencies, rising 0.3% versus the greenback, after employment data smashed expectations. The euro strengthened ahead of the ECB policy announcement. Ahead of tomorrow’s BOJ rate decision, selling in the yen pushed the currency to the lowest level since November, prompting a warning from Japanese Chief Cabinet Secretary Hirokazu Matsuno that excessive movements weren’t desirable; not that Japan can do anything to contain said movements.

In rates, treasuries are lower with the US two-year yield up 3bps at 4.72% as euro-zone yields climb ahead of ECB rate decision and President Christine Lagarde’s press conference; German two-year yields add 6bps. The TSY curve is flatter with 2s10s, 5s30s spreads also rangebound. US yields are cheaper by 5bps across front-end of the curve with 2s10s, 5s30s spreads flatter by 1.2bp and 3bp on the day; 10- year yields at 3.825%, cheaper by 3.5bp vs Wednesday’s close with bunds lagging by 2.5bp in the sector ahead of ECB, while gilts mildly outperform.

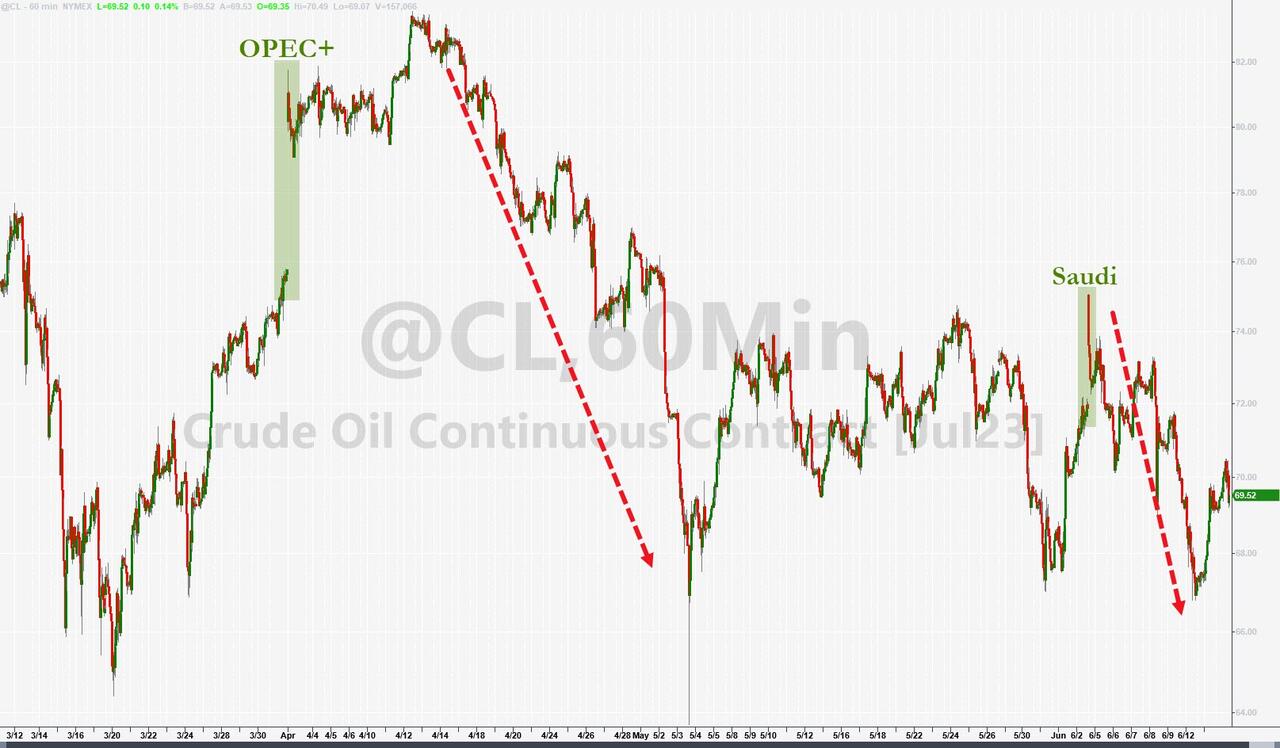

In commodities, crude futures advance with WTI rising 0.5% to trade near $68.60. Spot gold falls 0.4% to around $1,938. Bitcoin is down 0.3%

To the day ahead now, and the main highlight will be the ECB’s latest policy decision, along with President Lagarde’s press conference. In addition, we’ll hear from the ECB’s Nagel and Villeroy, and BoE Deputy Governor Cunliffe. On the data side, US releases include retail sales, industrial production, and capacity utilisation for May, the Philadelphia Fed’s business outlook and the Empire State manufacturing survey for June, as well as the weekly initial jobless claims.

Market Snapshot

- S&P 500 futures down 0.4% to 4,400

- MXAP little changed at 168.42

- MXAPJ up 0.7% to 531.29

- Nikkei little changed at 33,485.49

- Topix little changed at 2,293.97

- Hang Seng Index up 2.2% to 19,828.92

- Shanghai Composite up 0.7% to 3,252.98

- Sensex down 0.3% to 63,044.94

- Australia S&P/ASX 200 up 0.2% to 7,175.33

- Kospi down 0.4% to 2,608.54

- STOXX Europe 600 down 0.2% to 463.91

- German 10Y yield little changed at 2.49%

- Euro little changed at $1.0829

- Brent Futures up 0.7% to $73.69/bbl

- Gold spot down 0.5% to $1,932.09

- U.S. Dollar Index up 0.20% to 103.15

Top Overnight News from Bloomberg

- China’s economic momentum softens, with industrial production coming in at +3.5% in May (inline with the Street, but down from +5.6% in April) and retail sales +12.7% (down from +18.4% in April and below the Street’s +13.7% forecast). BBG

- China cuts rates – as expected, China lowered the MLF (medium-term lending facility) rate by 10bp (the move follows a cut to the 7-day repo rate earlier this week, and the gov’t is widely anticipated to take the Loan Prime Rate down 10bp next week). BBG

- China grapples with rising worker unrest as factory strikes hit a 7-year high amid soft growth, weak pay, and fewer job opportunities. RTRS

- The United States played down expectations of any breakthrough from the first trip by a U.S. Secretary of State to China in five years, after a tense call with China’s foreign minister ahead Antony Blinken’s visit to Beijing next week. RTRS

- Support for giving aid to Ukraine is starting to weaken in Congress amid growing calls for fiscal austerity. NYT

- The ECB is set to deliver what may be the penultimate increase of this hiking cycle. It’s expected to lift the deposit rate by a quarter point to 3.5%, but the focus is mostly on any guidance about future increases. Consensus is for one final hike next month. Markets don’t expect much but a more hawkish tone may boost the euro. BBG

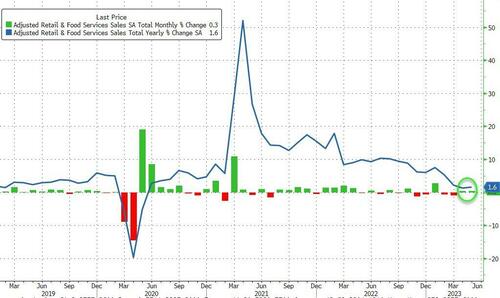

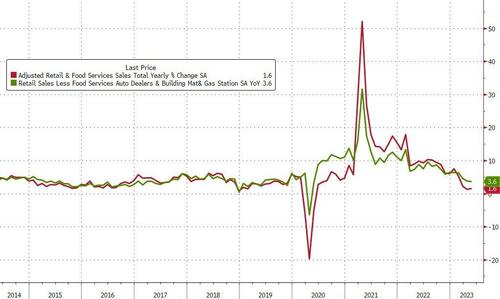

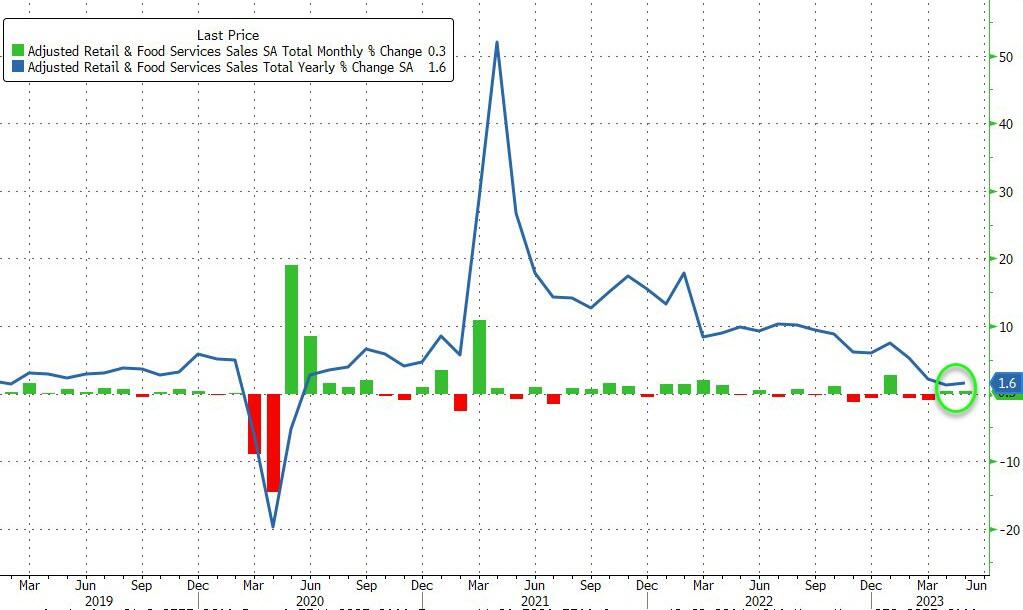

- US retail sales probably dipped 0.2% month on month in May, giving back some of April’s 0.4% gain, as consumers spent less on autos and energy, Bloomberg Economics said. Activity at restaurants and bars should show continued spending. Kroger reports sales premarket. BBG

- Washington is hoping to strike an informal deal with Iran that would limit Tehran’s nuclear activities and free American prisoners. NYT

- The jump in used-car costs that propped up US inflation last month is widely expected to swing into reverse in June, finally delivering a slowdown in one of the most-watched price gauges. Leading indicators of auto prices compiled by private firms like Manheim have already begun falling — and those declines should begin filtering into the official Bureau of Labor Statistics data for consumer prices in the next monthly report, due July 12. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mostly higher but with gains capped in the aftermath of the FOMC where a hawkish knee-jerk reaction to the Fed’s dot plots was partially unwound during the press conference after Powell distanced himself from projections, while the attention in the region shifted to the slew of key data releases. ASX 200 was kept afloat in rangebound trade with stellar jobs data partly clouded by yield curve inversion. Nikkei 225 benefitted from currency depreciation and encouraging data including Exports and Machinery Orders. Hang Seng and Shanghai Comp. were positive with outperformance in Hong Kong after the HKMA kept rates unchanged for the first time since March 2022 in lockstep with the Fed, while the advances were led by property names amid expectations for more support measures for the industry and after Chinese House Prices returned to growth. Furthermore, the PBoC cut its 1-year MLF rates by 10bps following similar cuts to short-term funding rates although participants also digested disappointing activity data from China in which both Industrial Production and Retail Sales missed estimates.

Top Asian News

- PBoC conducted CNY 237bln in 1-year MLF lending with the rate cut by 10bps to 2.65%.

- HKMA maintained its base rate unchanged at 5.50%, as expected.

- China National Bureau of Statistics said the economic recovery is not yet solid but noted that Q2 growth will be significantly faster than Q1 and that China’s economy is resilient despite facing some pressures. China’s stats bureau also stated that pressure on employment and structural problems persist, while it added that consumption recovery faces some hurdles and China will support consumption growth.

- China’s commerce Ministry says will continue to improve consumption policies and introduce a series of policy measures to support the recovery and expansion of consumption; China faces relatively big pressure on exports.

- JP Morgan cuts China’s 2023 full year GDP growth forecast to 5.5% (prev. 5.9%).

- Japan’s opposition party is making final preparations to submit a no-confidence vote on Friday.

European bourses are somewhat mixed but have generally been edging lower throughout the morning pre-ECB & post-FOMC, Euro Stoxx 50 -0.4%. Sectors are similarly lower overall with Basic Resources lagging on base metals prices while Banks are weighed on by CJEU’s ruling on Polish mortgages; though, Retail names buck the trend after H&M’s update. Stateside, futures are lower across the board with the NQ -0.6% as yields continue to rise. Overall, the ES remains just above the 4400 mark ahead of US data and as the FOMC blackout lifts to feature Bullard, Barkin & Waller on Friday’s schedule.

Top European News

- UK PM Sunak abandoned the plan for a supermarket price cap following a backlash, according to The Telegraph.

- UK’s ONS says 17% of companies expect to increase prices in the month ahead; lowest since the series began in March 2022.

- Brussels is under pressure to impose restrictions on Chinese electric cars, over fears that imports are flooding the European market at a speed and scale that threaten the Continent’s own production of such vehicles, according to Politico.

- EU Top Court says Polish banks cannot charge for the cost of capital in FX mortgage contracts which have been deemed as invalid, consumers with such contracts can demand compensation from banks. In response, Polish Banking Regulator KNF says the CJEU ruling on Polish FX loans is negative for the Polish banking sector and the economy. Click here for details & analysis.

FX

- Hawkish dot plots help Dollar recover from pre-FOMC lows, DXY firmer within 103.380-102.910 range.

- Yen sharply lower pre-BoJ on yield and policy divergence dynamics, USD/JPY around 141.00 between 141.50-139.95 parameters.

- Euro eyeing ECB for independent direction via guidance beyond widely expected 25 bp hike, EUR/USD back above 1.0800.

- Aussie underpinned after stellar jobs data, but Kiwi undermined as NZ tech recession confirmed, AUD/USD reclaims 0.6800+ status, NZD/USD loses 0.6200 handle and AUD/NZD cross bounces almost big figure from sub-1.0950

- Norges Bank Regional Network Survey (Q2): Slightly better outlook, but wide variations. Click here for details & analysis.

Fixed Income

- Bonds extend post-Fed declines and curves remain flatter on balance on hawkish dot plot trajectory.

- Bunds pivot 133.00, Gilts sub-95.00, albeit holding up better having traded above par and T-note hovering within 112-31+/16+ range.

- ECB in focus and expected to hike 25 bp, but several top tier US data releases also ahead.

Commodities

- Commodities are generally in familiar ranges in what has been relatively quiet trade post-FOMC and pre-ECB; crude benchmarks firmer, but in familiar ranges.

- With the exception of base/industrial metals which are dented after China’s disappointing activity data whereby both industrial production and retail sales missed expectations.

- Spot gold is unable to glean any support from the modest equity pressure that has crept in throughout the European morning. Though, similarly, it hasn’t been tarnished too much by the stronger USD.

- Kremlin says it sees no positive prospects for future of Black Sea Grain Deal; parts of grain deal affected Russia remain unfulfilled, cannot go on like this forever.

US Event Calendar

- 08:30: May Retail Sales Advance MoM, est. -0.2%, prior 0.4%

- 08:30: May Retail Sales Ex Auto MoM, est. 0.1%, prior 0.4%

- 08:30: May Retail Sales Control Group, est. 0.2%, prior 0.7%

- 08:30: May Import Price Index MoM, est. -0.5%, prior 0.4%

- 08:30: May Import Price Index YoY, est. -5.6%, prior -4.8%

- 08:30: May Export Price Index MoM, est. -0.1%, prior 0.2%

- 08:30: May Export Price Index YoY, est. -8.4%, prior -5.9%

- 08:30: June Initial Jobless Claims, est. 245,000, prior 261,000

- 08:30: June Continuing Claims, est. 1.77m, prior 1.76m

- 08:30: June Philadelphia Fed Business Outl, est. -14.0, prior -10.4

- 08:30: June Empire Manufacturing, est. -15.1, prior -31.8

- 09:15: May Capacity Utilization, est. 79.7%, prior 79.7%

- 09:15: May Manufacturing (SIC) Production, est. -0.1%, prior 1.0%

- 09:15: May Industrial Production MoM, est. 0.1%, prior 0.5%

- 10:00: April Business Inventories, est. 0.2%, prior -0.1%

- 16:00: April Total Net TIC Flows, prior $56.7b

- 16:00: April Net Foreign Security Purchases, prior $133.3b

DB’s Jim Reid concludes the overnight wrap

So a dovish hike last month turned into a hawkish pause this month as the Fed ended a series of 10 successive rate hikes last night but signalled that more may well be required, especially via a more hawkish dot plot that signalled two more hikes this year. However we should say that two years ago at the June meeting the median dot for the end of 2023 was at a lowly 0.6%, so these aren’t destiny. To be fair, Chair Powell acknowledged the uncertainty in future forecasts and therefore cautioned against reading too much into the dots. If and when the facts change those dots will be forgotten. Rates and equities sold off after the statement but recovered to being broadly unchanged through the press conference and into the close. It’s only overnight that we’ve seen a more aggressive selloff in rates again, which has taken 2yr and 10yr Treasury yields up to their highest level since SVB’s collapse, although equity futures remain flat still.

In terms of the decision, holding rates was seen as allowing the committee to “assess additional information and its implications for monetary policy” and to determine “the extent of additional policy firming that may be appropriate”. The wording of the statement was largely unchanged from the last meeting, but the market initially took a clear hawkish interpretation in response to an upgrading of the Fed’s dot plot projection. This showed the median member expecting two more 25bp hikes by the end of 2023, with 12 of the 18 members at that point or above, whereas only two members pencilled in no further hikes. So a lot to talk down ahead of the next July meeting in under 6 weeks’ time. The projections also saw 2023 core PCE revised up to 3.9% (from 3.6% in March).