by harveyorgan · in Uncategorized · Leave a comment·Edit

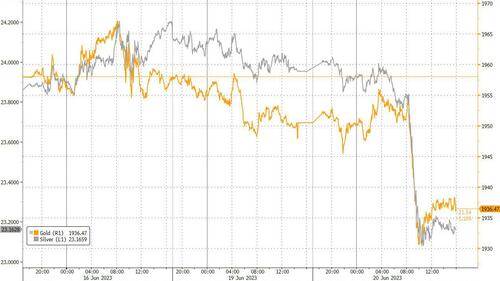

GOLD PRICE CLOSED: DOWN $22.40 TO $1936.60

SILVER PRICE CLOSED: DOWN $0.89 AT $23.19

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1936,40

Silver ACCESS CLOSE: 23.16

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Bitcoin morning price:, $26,797 UP 441 Dollars

Bitcoin: afternoon price: $27.892 UP 1536 dollars

Platinum price closing $965.90 DOWN $21.00

Palladium price; $1381.25 DOWN $43.60

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,561.68 DOWN 18.32 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1516.83 DOWN 10.20 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1773.82 DOWN 15.1 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JUNE 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,958.400000000 USD

INTENT DATE: 06/16/2023 DELIVERY DATE: 06/21/2023

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 3

323 C HSBC 160

323 H HSBC 35

363 H WELLS FARGO SEC 51

435 H SCOTIA CAPITAL 21

657 C MORGAN STANLEY 1

661 C JP MORGAN 98

661 H JP MORGAN 4

690 C ABN AMRO 8

709 C BARCLAYS 1

737 C ADVANTAGE 2

880 H CITIGROUP 33

905 C ADM 5

TOTAL: 211 211

MONTH TO DATE: 19,17

JPMorgan stopped 102/211 contracts

FOR JUNE:

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2023. CONTRACT: 211 NOTICES FOR 210,000 OZ or 0.6562 TONNES

total notices so far: 19,177 contracts for 1,917,700 oz (59.648 tonnes)

FOR JUNE:

SILVER NOTICES: 0 NOTICE(S) FILED FOR NIL OZ/

total number of notices filed so far this month : 423 for 2,115,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $22.40

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

/NO CHANGES IN GOLD INVENTORY AT THE GLD:////

INVENTORY RESTS AT 934.03 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 89 CENTS AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 463.183 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 1509 CONTRACTS TO 151,591 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.23 GAIN IN SILVER PRICING AT THE COMEX ON FRIDAY. TAS ISSUANCE WAS A STRONG SIZED 790 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH . CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON FRIDAY NIGHT: 790 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.23). BUT WERE SUCCESSFUL IN KNOCKING A FEW SPEC LONGS AS WE HAD A STRONG LOSS ON OUR TWO EXCHANGES OF 1159 CONTRACTS. WE HAD ANOTHER IDENTICAL 587 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 2.935 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 13.370 MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION.

WE MUST HAVE HAD:

A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS( 350 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.935 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP + 2.935 MILLION OZ EXCHANGE FOR RISK(ISSUED TODAY: TOTAL ISSUED SO FAR: 13.370 MILLION OZ)// TOTAL STANDING FOR THE MONTH 4.270 MILLION OZ + 13.370 MILLION EXCHANGE FOR RISK = 17,640 MILLION OZ// ) // HUGE SIZED COMEX OI LOSS/ FAIR SIZED EFP ISSUANCE/VI) STRONG NUMBER OF T.A.S. CONTRACT ISSUANCE (790 CONTRACTS)//

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –477 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTRACTS for 12 days, total 14,521 contracts: OR 72.695 MILLION OZ (1210 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 72.695 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 72.695 MILLION OZ//MUCH LARGER THAN LAST MONTH

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1509 CONTRACTS DESPITE OUR GAIN IN PRICE OF $0.23 IN SILVER PRICING AT THE COMEX//FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL EFP ISSUANCE CONTRACTS: 350 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.935 MILLION OZ FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP+ 2.935 MILLION EXCHANGE FOR RISK TODAY + 10.435 MILLION EXCHANGE FOR RISK(PRIOR)//NEW TOTAL STANDING: 17.640 MILLION OZ////// .. WE HAVE A STRONG SIZED LOSS OF 1159 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG 790//MINOR FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE FRIDAY COMEX SESSION. THE NEW TAS ISSUANCE TODAY (790) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE.

WE HAD 0 NOTICE(S) FILED TODAY FOR NIL OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 125 CONTRACTS TO 432,223 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED – 186 CONTRACTS

WE HAD A SMALL SIZED INCREASE IN COMEX OI ( 125 CONTRACTS) WITH OUR $0.70 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JUNE. AT 70.79 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0.1648 TONNE QUEUE JUMP: NEW TOTAL 64.230 TONNES STANDING SO FAR // + /A SMALL ISSUANCE OF 482 T.A.S. CONTRACTS ////YET ALL OF..THIS HAPPENED WITH A $2.80 GAIN IN PRICE WITH RESPECT TO FRIDAY’S TRADING.WE HAD A FAIR SIZED GAIN OF 1566 OI CONTRACTS (4.8709 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1752 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 432,037

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1566 CONTRACTS WITH 125 CONTRACTS INCREASED AT THE COMEX//TAS CONTRACTS INITIATED (ISSUED): A SMALL 482 CONTRACTS) AND 1441 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1752 CONTRACTS OR 5449 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1441 CONTRACTS) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (311) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 1566 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 70.79 TONNES FOLLOWED BY TODAY’S 5300 OZ QUEUE JUMP //// NEW STANDING FALLS TO 64.230 TONNES// /3) ZERO LONG LIQUIDATION//4) SMALL SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: SMALL T.A.S. ISSUANCE: 482 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

TOTAL EFP CONTRACTS ISSUED: 27,816 CONTRACTS OR 2,781,600 OZ OR 86,519 TONNES IN 12 TRADING DAY(S) AND THUS AVERAGING: 2318 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES 86,519 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 86.519/3550 x 100% TONNES 2.42% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 86.519 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUGE SIZED 1509 CONTRACTS OI TO 151,591 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 350 CONTRACTS (RECORD ISSUANCE)

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 350 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 350 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1509 CONTRACTS AND ADD TO THE 350 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1159 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 5,795 MILLION OZ

OCCURRED DESPITE OUR $0.23 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED DOWN 15.44 PTS OR 0.47% //Hang Seng CLOSED DOWN 305.81 PTS OR 1.54% /The Nikkei closed UP 18.49 OR 0.06% //Australia’s all ordinaries CLOSED UP 0.79 % /Chinese yuan (ONSHORE) closed DOWN 7.1760 /OFFSHORE CHINESE YUAN DOWN TO 7.1845 /Oil UP TO 72.09 dollars per barrel for WTI and BRENT UP AT 76.75 / Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A TINY SIZED 125 CONTRACTS DOWN TO 432,037 WITH OUR GAIN IN PRICE OF $0.70 ON FRIDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1441 EFP CONTRACTS WERE ISSUED: : AUGUST 1441 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1441 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1566 CONTRACTS IN THAT 1441 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A TINY SIZED GAIN OF 125 COMEX CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $0.70//FRIDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR FRIDAY NIGHT WAS A SMALL 482 CONTRACTS. THROUGHOUT LAST WEEK, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THE HUGE NUMBER OF T.A.S. CONTRACTS INITIATED OVER THE PAST SEVERAL WEEKS SPELLS TROUBLE FOR THE GOLD/SILVER MARKET AS RAIDS WILL SURELY BE UPON US.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (64.230) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.230 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $0.70) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR FAIR GAIN OF 1566 CONTRACTS ON OUR TWO EXCHANGES. WE HAD MINOR TAS LIQUIDATION THROUGHOUT THE FRIDAY COMEX SESSION . THE TAS ISSUED FRIDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 4.8709 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE. (70.709 TONNES) FOLLOWED BY TODAY’S 5300 OZ QUEUE JUMP..NEW STANDING REMAINS AT 64.230 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $0.70

WE HAD – REMOVED 186 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 1566 CONTRACTS OR 156600 OZ OR 4.809 TONNES.

Estimated gold volume today:// 244,824 fair

final gold volumes/yesterday 164,395 poor

//JUNE 20/ FOR THE JUNE 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 96.453 OZ int.Delaware 3 kilobars . |

| Deposit to the Dealer Inventory in oz | 16,012.057 oz Brinks |

| Deposits to the Customer Inventory, in oz | 16,001.885 oz Brinks |

| No of oz served (contracts) today | 211 notice(s) 21100 OZ 0.6562 TONNES |

| No of oz to be served (notices) | 1453 contracts 145,300 oz 4.519 TONNES |

| Total monthly oz gold served (contracts) so far this month | 19,177 notices 1,917,700 OZ 59.648 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

No dealer withdrawals

Customer deposits: 1

i)Into Brinks 16,012.057 oz

total dealer deposits: 16,012.057 oz

we had one customer deposit:

i) Into Brinks: 16,001.885 oz

total deposits: 16,001.885 oz

Withdrawals: 1

i) out of Int. Delaware: 96.453 oz (3 kilobars)

total 96.453 oz

Adjustments;1 dealer to customer

i) Out of Brinks 13,210.510 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 1664 contracts having LOST 10 contracts. We had 63 contracts served on Friday so we gained 53 contracts or an additional 5300 oz will stand for gold at the comex.

The next front month after June is the non active delivery month of July. Here, July lost 72 contracts to stand at 2469 contracts.

AUGUST LOST 150 contracts up to 364,879 contracts

We had 211 contracts filed for today representing 21,100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 211 contract(s) of which 4 notices were stopped (received) by j.P. Morgan dealer and 98 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2023. contract month,

we take the total number of notices filed so far for the month (19,177 x 100 oz ), to which we add the difference between the open interest for the front month of JUNE (1664 CONTRACT) minus the number of notices served upon today 211 x 100 oz per contract equals 2,065,000 OZ OR 64.230 TONNES the number of TONNES standing in this active month of June.

thus the INITIAL standings for gold for the JUNE contract month: No of notices filed so far (19,177) x 100 oz + (1664) {OI for the front month} minus the number of notices served upon today (211) x 100 oz) which equals 2,065,000 oz standing OR 64.230 TONNES

TOTAL COMEX GOLD STANDING: 64.230 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 o

total pledged gold: 2,055,246.664 OZ 63.92 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,584,958.309 OZ

TOTAL REGISTERED GOLD: 11,704,821,493 (364.06 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,880,136.816 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,649,285 OZ (REG GOLD- PLEDGED GOLD) 300.13 tonnes//

END

SILVER/COMEX

JUNE 20//2023// THE JUNE 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 858,998.378 oz CNT Int. Delaware Manfra . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 103,138.454 oz Delaware |

| No of oz served today (contracts) | 0 CONTRACT(S) (NIL OZ) |

| No of oz to be served (notices) | 431 contracts (2,155,000 oz) |

| Total monthly oz silver served (contracts) | 423 Contracts (2,115,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposits

total dealer deposit: nil oz

total dealer deposits: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: oz

We had 1 deposits customer account:

i) Into Delaware 103,138.454 oz

total customer deposits: 103,138.454 oz

JPMorgan has a total silver weight: 142,366 million oz/271.379 million =52.45% of comex .//dropping fast

Comex withdrawals 3

i) Out of CNT: 22,985.950 oz

ii) Out of Int. Delaware 228,390.928 oz

iii) out of Manfra: 607,621.500 oz

total withdrawals: 858,998.378 oz

adjustments: 1

dealer to customer: manfra

20,680.600 oz

TOTAL REGISTERED SILVER: 27.096 MILLION OZ (declining rapidly).TOTAL REG + ELIGIBLE. 271.379 million oz

DEALER SILVER DROPPING FAST. (moves into the 27 million oz column)

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE /2023 OI: 431 CONTRACTS HAVING LOST 0 CONTRACT(S).

WE HAD 0 NOTICES FILED ON FRIDAY SO WE LOST 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF JUNE

JULY HAD A 4823 CONTRACT LOSS TO 63,082 CONTRACTS

AUGUST GAINED 8 CONTRACTS TO STAND AT 117

SEPT HAS A GAIN OF 3296 CONTRACTS UP TO 76,500

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes// est. volume today 127,197 huge /

Comex volume: confirmed yesterday:75,183 good

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 423 x 5,000 oz = 2,115,000 oz

to which we add the difference between the open interest for the front month of JUNE(431) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2023 contract month: 423 (notices served so far) x 5000 oz + OI for the front month of JUNE (431) – number of notices served upon today (0 )x 500 oz of silver standing for the JUNE contract month equates to 4.270 million oz + 2.935 EXCHANGE FOR RISK TODAY + 10.435MILLION OZ EXCHANGE FOR RISK (PRIOR)//NEW TOTAL: 17.640 MILLION OZ STANDING

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

JUNE 19/WITH GOLD DOWN $22.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.03 TONNES

JUNE 16/WITH GOLD UP $0.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.33 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.03 TONNES

JUNE 15/WITH GOLD UP $2.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 929.70 TONNES

JUNE 14/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 931.44 TONNES

JUNE 13/WITH GOLD DOWN $10.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.01 TONNES FORM THE GLD///INVENTORY RESTS AT 931.44

JUNE 12/WITH GOLD DOWN $7.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.65 TONNES

JUNE 9/WITH GOLD DOWN $1.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.65 TONNES

JUNE 8/WITH GOLD UP $20.45 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.46 TONNES FROM THE GLD///INVENTORY RESTS AT 934.65 TONNES

JUNE 7 WITH GOLD DOWN $22.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 938.11 TONNES

JUNE 6/WITH GOLD UP $6.90 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 939.56 TONNES

JUNE 5/WITH GOLD UP $5.00 TODAY : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 938.11 TONNES

JUNE 2/WITH GOLD DOWN $24.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 938.11 TONNES

JUNE 1/WITH GOLD UP $14.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 939.56 TONNES

MAY 31/WITH GOLD UP $5.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 939.56 TONNES

MAY 30/WITH GOLD UP $14.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 26/WITH GOLD UP $.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 941.29 TONNES

MAY 25/WITH GOLD DOWN $19.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 24/WITH GOLD DOWN $9.50 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 941.29 TONNES

MAY 23/WITH GOLD $2.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 942.74 TONNES

MAY 22/WITH GOLD DOWN $4.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.83 TONES OF GOLD INTO THE GLD DESPITE THE L0SS IN PRICE//INVENTORY RESTS AT 942.74 TONNES

MAY 19/WITH GOLD UP $22.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 936.96 TONNES

MAY 18/WITH GOLD DOWN $23.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 936.96 TONNES

MAY 17/WITH GOLD DOWN $8.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.94 TONNES

MAY 16/WITH GOLD DOWN 28.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.57 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 934,07

MAY 15/WITH GOLD UP $2.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 937.64 TONNES

MAY 12/WITH GOLD DOWN $.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 937.84 TONNES

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 934.95 TONNES

GLD INVENTORY: 934.03 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 19/WITH SILVER DOWN 89 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 16/WITH SILVER UP 23 CENTS TODAY :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 463.183 MILLION OZ

JUNE 15/WITH SILVER DOWN 17 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.377 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 463.642 MILLION OZ//

JUNE 14/WITH SILVER UP 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 735,000 OZ FROM THE SLV///INVENTORY RESTS AT 465.019 MILLION OZ//

JUNE 13/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.515 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 465.754 MILLION OZ//

JUNE 12/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.269 MILLION OZ//

JUNE 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF SILVER TO THE TUNE OF 550,000 OZ//INVENTORY RESTS AT 467.269 MILLION OZ

JUNE 8/WITH SILVER UP $0.63 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 467.819 MILLION OZ/

JUNE 7/WITH SILVER DOWN 17 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.01 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 467.819 MILLION OZ/

JUNE 6/WITH SILVER UP 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.809 MILLION OZ//

JUNE 5/WITH SILVER DOWN $.13 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 266,000 OZ FROM THE SLV////INVENTORY RESTS AT 466.809 MILLION OZ/

JUNE 2/WITH SILVER DOWN 23 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV./INVENTORY RESTS AT 467.015 MILLION OZ/

JUNE 1/WITH SILVER UP 49 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.933 MILLION OZ

MAY 31/WITH SILVER UP 37 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 367,000 OZ FROM THE SLV////INVENTORY RESTS AT 467.933 MILLION OZ//

MAY 30/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 26/WITH SILVER UP $0.44 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.306 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 25.WITH SILVER DOWN $0.32 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 471.606 MILLION OZ//

MAY 24/WITH SILVER DOWN $.35 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 23/WITH SILVER DOWN 22 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.801 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 22/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ//

MAY 19/WITH SILVER UP 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ

MAY 18/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.529 MILLION OZ/

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

MAY 16/WITH SILVER DOWN 34 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .643 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.448 MILLION OZ.

MAY 15/WITH SILVER UP 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.091 MILLION OZ/

MAY 12/WITH SILVER DOWN $.26 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 3,123 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 470.091 MILLION OZ./

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

CLOSING INVENTORY 463.183 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

END

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

Solid Gold In a Broken World

Matthew Piepenburg

June 18, 2023

Below, we look at gold in a broke(n) world of hubris, debt, Realpolitik and a rising east.

For well over a year, we’ve openly declared that the Fed is cornered.

That is, Powell knows he needs higher rates to allegedly “fight” inflation but also knows that raising rates into an historical debt bubble means one “credit event” (or “crunch”) after the next, from tanking USTs in 2020 to tanking banks in 2023.

It seems only now that the WSJ (Mr. Timiraos), along with a former Indian central banker (Mr. Rajan) is confessing the same.

Human, All Too Human

But Powell is more than just a cornered banker, he’s an insecure and “human, all too human” political man with admittedly more concerns about his legacy than a tanking market or painful recession.

As he himself declared: “I will not become ‘just another Arthur Burns,’” which translates to: “I’m not going to be a dove as the economy and markets race toward a financial horror-film that the Fed itself directed since Greenspan killed capitalism.”

Thus, and with almost zero regard for common sense, basic math and history, this cornered banker is trying instead to be Paul Volcker, but has forgotten that Volcker raised rates to fight inflation when public debt was at $800B not $32T.

Not Volcker, All Too Volcker

Furthermore, Volcker led the Fed at a time when USTs were loved rather than unloved.

Since 2014 in general, and 2022 in particular, the level of foreigners dumping Uncle Sam’s IOUs is breath-taking and makes it all too clear to any holding even a rudimentary understanding of the bond market that the US will be financing its own deficits at levels (and trillions) which end empires.

For years, the US has pretended to be what it once was: Respected and credible. But its balance sheet, as argued elsewhere, is no different than just any other banana republic.

Like the very nations Uncle Sam once mocked (think Argentina), the US has been issuing more IOUs despite a world that is buying less of the same.

Thus, and like Argentina circa 2000, the US has already begun regulating (forcing?) US banks and money market funds to buy its over-issued debt, with the end result of simply crushing some of those banks and money markets in a toxic wave of QT.

With friends like the Fed, who needs enemies?

And like the banana republics, the US is now in a corner wherein inflation is too sticky to cut rates yet bank (and other credit participant) pains are too high to raise rates.

Clear, All Too Clear Bar Tab

Since 2014, it has become harder to export Uncle Sam’s inflation (or launder its debt burdens) by expecting other nations to simply absorb his increasingly unwanted USTs and openly embarrassing bar tab.

As the following graph provided by Luke Gromen makes “clear, all too clear,” the gap between Uncle Sam’s embarrassing deficit (blue line) and the meek level of foreign buyers of his debt (red line) reveals two historical points:

- US deficits are appalling; and

- Who or what is going to fill that “gap”?

Kill the Currency or Save the (Broken) “System”?

If the history of broke empires, nations and regimes is any guide, and if the psychology of short-sighted politicians seeking re-election (i.e., bribing the electorate with mouse-clicked dollars) over sound-money is equally so, then we can be almost certain that the Fed and Uncle Sam’s end-game boils down to choosing between saving the system or killing the currency.

For us, the choice ahead is fairly obvious, which also means that gold, which hovers like a vulture over debased currencies, will be licking its chops in the years ahead.

China Licking Its Chops and Expanding Its Swaps

But gold is not the only vulture about to get fatter in an increasingly de-dollarized backdrop.

China, love it or hate it, has been sharpening its knives and forks for years in a patient and long-sited play to win an economic and currency war with Uncle Sam.

After all, emperors for life, like Xi, can afford to be more far-sighted than US politicians who prostitute sound money responsibilities for easy money re-election.

This may be why tiny-thinkers like Trudeau, or folks who probably never had a girlfriend in college, like Klaus Schwab, have such a crush on Xi and the kind of power he can wield without having to worry about silly little things like democratic elections…

It’s Good to be King (But not a USD)

Getting back to those emerging market “banana republics” which the US so often mocked, it’s worth noting that Argentina has just doubled its currency swap access to $10B, but here’s the kicker: The swap is in CNY not USD…

Meanwhile, Pakistan just signed a deal with Russia to buy crude oil, but guess what, Pakistan is paying that bill in CNY and not USDs…

See a trend?

It’s the very trend we warned of the moment Uncle Sam weaponized the world reserve currency in those insanely myopic (i.e., stupid) sanctions against Russia in early 2022.

Settlement deals like these (FX and energy) almost certainly involve swap lines with Chinese fingerprints and with countries (like Argentina and Pakistan) who hold less and less US FX reserves, which is no surprise given that few countries wish to hold “reserve assets” that can be turned off at a political whim.

In short, if the world is slowly but steadily looking outside the USD, it’s because the US has slowly but steadily shot itself (and its Dollar) in the foot since March of 2022.

In fact, throughout Q1, global central banks have been engaging in record-breaking levels of CNY currency stacking (109B yuan by end of March) via FX swap lines.

To date, the Chinese central bank (PBOC) hasn’t listed the names of these nations and banks, but the SLOW trend away from an increasingly distrusted USD and rising China is pretty hard to ignore as more nations are using the yuan for energy and real asset deals while holding the USD/UST merely to pay down old debts.

Why?

Because the rest of the world is seeing what American media outlets and store-bought DC politicos are refusing to confess, namely: China was winning the global trade war even before DC weaponized the USD:

See the trend?

Playing the Long Game in the World of the Short-Sighted

But as indicated in many recent articles and interviews, the CNY is not about to become the world reserve currency.

It’s bond market and rule of law are decades beyond such credibility or use.

But this doesn’t mean that China or its CNY has to worry, for the yuan’s increasing role as trade a settlement currency rather than reserve currency suits China just fine for now.

In Gold They Trust

Furthermore, China, like Russia, is fully aware of the Realpolitik (i.e., distrust) of their laws and bond markets.

They know, as George Washington knew, that “nations have neither permanent friends nor enemies, just permanent interests.”

In other words, for China and Russia to win the long game (rather than putting green), they need to win the trust of other nations by appealing to their interests rather than platitudes.

And nothing holds the interests of skeptical yet USD-tired nations like gold, as gold, love it or hate it, is far more trustworthy than men, be they from DC, Buenos Aires, Moscow, Beijing or Paris.

How the USD Lost Trust

For a brief window after 1944, when the USD was backed by gold, other nations could trust the USD as a life raft in times of crisis.

Nixon, of course, sank that raft in 1971 and took away the gold standard to ensure his re-election at the long-term expense of his country.

How’s that for a “profile in courage”?

Now, some 50+ years later, the slow end of the USD as a life-raft, trusted asset or even trade currency is reaping the costs of its political, human and monetary sins.

Weaponizing that dollar only added to this gradual yet eventual fall.

China is now creating more liquidity with each passing day, as it has swap lines with just about everyone.

Xi, like Putin, are also stacking gold at un-disclosed levels, but even the official numbers are telling.

And what are they telling us? Or what, for example, is Sergei Glasyex concocting behind the scenes?

Well, I’m guessing it has a lot to do with building trust the old-fashioned way—namely: With gold in the mix of its trade settlement platforms and swaps.

In the coming years, this “guess” is going to emerge as a reality, and like a chess-player or polo player, I, like many other investors, nations and central banks, am playing gold three moves ahead as gold becomes a net settlement asset.

Peak Cheap Gold

Notwithstanding the otherwise undeniable and changing patterns in the aforementioned global FX and geopolitical stage, one merely has to consider the seemingly unlimited supply of otherwise unwanted USTs with their intrinsically limited duration and then compare such toxicity with a simple bar of gold, which, unlike Uncle Sam’s IOUs, has an infinite duration and limited supply.

In short: Supply and demand still matter.

Toward this end, it’s worth noting that gold discoveries are shrinking in supply as demand for the same is, and will continue, to rise.

In the 1990’s, for example, there were over 180 major gold discoveries (i.e., 1m oz. and higher); in the 2000’s there were 120 such discoveries, 40 in the 2010’s and NONE since 2019.

Think about that for a second or two.

Also, think about the simple fact that Uncle Sam, the holder of the world reserve currency, has been hiking rates into the greatest debt bubble in once proud national history, thereby increasing US solvency risk (and thus pointing toward dollar debasement down the road) with neon-flashing clarity.

Gold, quite simply, is separating from real rates and acting more and more on its own, as the fear trade gets easier and easier to see, and gold gets easier and easier to, well…TRUST.

Stated even more simply, demand for this “pet rock” is increasing as its supply is falling.

If you took high school econ, then you know what that does to the price of gold and the fall of the USD’s purchasing power.

Again: See the trend?

end

JPMorgan/Jeffrey Epstein Cases Are a Cross Between the Bank’s Chinese Princeling Scandal and Madoff Fraud, Using Sex with Minors as a Bribe

By Pam Martens and Russ Martens: June 20, 2023 ~

The tenure of Jamie Dimon as Chairman and CEO of JPMorgan Chase, the largest federally-insured bank in the United States and the largest trading casino on Wall Street, has copiously revealed the following: the bank is more than willing to look the other way at crime if it means an increase in assets, profits or business referrals.

Each of those three ingredients were present in the bank’s decades long involvement with Bernie Madoff, with its Chinese Princeling scandal and in the unfolding details of its intimate relationship with child sex trafficker Jeffrey Epstein.

This reality may be difficult for the New York business press to acknowledge – since it has mostly covered Jamie Dimon as the grand statesman of Wall Street – but this is the hard reality nonetheless.

Yesterday, the Wall Street Journal’s Khadeeja Safdar and David Benoit revealed the contents of a 22-page internal report that JPMorgan Chase had prepared in 2019 as a timeline of its relationship with Jeffrey Epstein. The bank was apparently attempting to assess its liability after Epstein was arrested on July 6, 2019 by the Justice Department and charged with sex trafficking. (Epstein was found dead in his jail cell on August 10, 2019. The Medical Examiner ruled his death a suicide.)

The 22-page internal report had been filed under seal with the federal district court in Manhattan that is hearing two lawsuits against the bank for aiding and abetting Epstein’s sex trafficking. Apparently, someone leaked the full contents of the report to the reporters. One paragraph of the Wall Street Journal article is particularly enlightening. It reads as follows:

“The 2019 JPMorgan report said that Epstein had appeared to have forged close relationships with senior executives and government officials, including Dubai’s Sultan Ahmed bin Sulayem and British politician Peter Mandelson. Epstein tried to connect these associates to Staley and the bank for business deals and international expansions.”

The reference to “Staley” is to Jes Staley, a former executive of the bank who worked a few hundred feet from Dimon’s office, according to a deposition given by Dimon. Disturbing internal emails show that Staley was closely aligned with Epstein, even visiting him while he was serving his sentence for sex with a minor. Now consider the above paragraph in combination with what Virginia Giuffre has alleged in her prior lawsuits against Epstein: that, beginning when she was just 17 years old, Epstein and his girlfriend/procurer, Ghislaine Maxwell, arranged sexual encounters for Giuffre with royalty and powerful politicians. Prince Andrew settled monetary damages with Giuffre last year.

To put it simply, Epstein was an asset gatherer, and profit gatherer, and new business gatherer for JPMorgan Chase. And he dangled sex with underage women as an inducement to get meetings and make connections. And that is why, despite Epstein’s conviction in 2008 for procuring sex with a minor, despite his forced registration as a life-long sex offender, and despite his settling of dozens of cases of sexual assault of minors, JPMorgan Chase retained him as a client from 1998 to 2013.

There is a serious and deeply disturbing pattern of looking the other way at crime in order to gain a business advantage at JPMorgan Chase under Jamie Dimon’s “stewardship.”

In November 2016, units of JPMorgan Chase agreed to pay more than $264 million to the U.S. Department of Justice, the Securities and Exchange Commission and the Federal Reserve in what was widely known as its Chinese “Princeling” scandal.

In announcing the settlement in the Princeling scandal in 2016, officials at the Justice Department said this:

“The so-called Sons and Daughters Program was nothing more than bribery by another name…Awarding prestigious employment opportunities to unqualified individuals in order to influence government officials is corruption, plain and simple. This case demonstrates the Criminal Division’s commitment to uncovering corruption no matter the form of the scheme…

“In this case, JPMorgan employees designed a program to hire otherwise unqualified candidates for prestigious investment banking jobs solely because these candidates were referred to the bank by officials in positions to award business to the bank. In certain instances, referred candidates were hired with the understanding that the hiring was linked to the award of specific business. This is no longer business as usual; it is corruption.”

In January 2014, JPMorgan Chase paid $2.6 billion in fines and restitution, signed a deferred prosecution agreement with the Justice Department, and walked away from their 22-year involvement with Bernie Madoff’s Ponzi scheme.

After digesting the related documents released by the Justice Department in the Madoff matter, the Los Angeles Times asked the following: “Bernie Madoff: Was he part of the JPMorgan ring, or was JPMorgan part of his ring? “

The same thing could now be asked in the Epstein matter: Was Epstein part of the JPMorgan ring or was JPMorgan part of Epstein’s ring?

The Justice Department prosecutors who settled the case against JPMorgan Chase used much of the investigative material from Irving Picard, the Trustee of the Madoff victims’ fund, to bring their charges against JPMorgan Chase. According to Picard, JPMorgan Chase used unaudited financial statements from Madoff and skipped the required steps of bank due diligence to make $145 million in loans to Madoff’s business.

Lawyers for Picard write that from November 2005 through January 18, 2006, JPMorgan Chase loaned $145 million to Madoff’s business at a time when the bank was on “notice of fraudulent activity” in Madoff’s business account and when, in fact, Madoff’s business was insolvent. The reason for the JPMorgan Chase loans was because Madoff’s business account was “reaching dangerously low levels of liquidity, and the Ponzi scheme was at risk of collapsing.” JPMorgan, in fact, “provided liquidity to continue the Ponzi scheme,” according to Picard.

But was Madoff also generating new business deals or profits for JPMorgan Chase? The accounts of Norman F. Levy come immediately to mind.

JPMorgan Chase and its predecessor banks extended tens of millions of dollars in loans to Norman F. Levy and his family so they could invest with the insolvent Madoff. (Levy died in 2005 at age 93 without being charged with any crimes.)

According to Picard, Levy had $188 million in outstanding loans in 1996, which he used to funnel money into Madoff investments. Picard’s lawyers told the court that JPMorgan Chase referred to these investments as ‘special deals,’ and adding:

“Indeed, these deals were special for all involved: (a) Levy enjoyed Madoff’s inflated return rates of up to 40% on the money he invested with Madoff; (b) Madoff enjoyed the benefits of large amounts of cash to perpetuate his fraud without being subject to JPMC’s due diligence processes; and (c) JPMC [JPMorgan Chase] earned fees on the loan amounts and watched the ‘special deals’ from afar, escaping responsibility for any due diligence on Madoff’s operation.”

A critical piece of evidence against JPMorgan was that despite funneling loans to both Madoff and Levy, the bank “advised the rest of its Private Bank customers not to invest with Madoff,” according to Picard.

On paper, according to Picard, Levy was worth $1.5 billion in 1998. He was such an important customer to JPMorgan and its predecessor firms that he was given his own office at the bank.

Levy was a commercial real estate broker and, according to a 2009 Vanity Fair article, at one point Levy “had an ownership stake in 70 properties, including the Seagram Building and 21 shopping centers across America…”

According to Picard, once Levy was a Madoff client, the relationship included classic, unchecked evidence of money laundering for years and years that should have resulted in legally-mandated Suspicious Activity Reports (SARs) filed with the Financial Crimes Enforcement Network (FinCEN). But even after a different bank detected the suspicious activity in the late 1990s and reported the transactions to FinCEN, JPMorgan Chase and its predecessor banks failed to file their own mandated SARs. JPMorgan Chase not only allowed the activity to continue but allowed it to increase dramatically in dollar terms.

Contrast the above with information that James Dalessio, an employee of JPMorgan Chase, emailed to colleagues in October 2007 regarding Epstein’s cash withdrawals from the bank. Dalessio informed a control group at JPMorgan’s Private Bank that Epstein had withdrawn the following cash amounts in just a two-year span: 10 withdrawals of $40,000 year-to-date in 2007; cash withdrawals totaling $914,796 in 2006 consisting of 18 withdrawals of $40,000 in cash; two withdrawals of $60,000 in cash; one withdrawal of $30,000 in cash; and one withdrawal of $25,000 in cash. (Dalessio’s email was submitted to the Court, unsealed, in the pending U.S. Virgin Islands v JPMorgan Chase Bank case.)

Dalessio notes in his email that CTRs (Currency Transaction Reports) were filed for these cash withdrawals but there is no indication that Suspicious Activity Reports (SARs) were filed with FinCEN.

The U.S. Virgin Islands is alleging the following in its lawsuit against JPMorgan Chase:

“Plaintiff, the Government of the United States Virgin Islands (‘Government’), claims and will prove that Defendant JPMorgan Chase Bank, N.A. (‘JPMorgan’) violated the Trafficking Victims Protection Act, 18 U.S.C. §§ 1581- 1597 (‘TVPA’), by knowingly participating in and benefitting from Jeffrey Epstein’s sex-trafficking and by obstructing investigation through its concealment of Epstein’s suspicious transactions from law enforcement. Discovery confirms that JPMorgan knowingly, recklessly, and unlawfully provided and pulled the levers through which Epstein’s recruiters and victims were paid and was indispensable to the operation and concealment of Epstein’s trafficking. JPMorgan had real-time information on Epstein’s payments that the Government did not and had specific legal duties to report this information to law enforcement authorities, which it intentionally decided not to do.”

JPMorgan Chase’s unprecedented history of crimes has another distinction. It is the only U.S. domiciled bank that we know of that was compared to the Gambino crime family in a book authored by two trial attorneys.

In 2016, trial lawyers Helen Davis Chaitman and Lance Gotthoffer released the book JPMadoff: The Unholy Alliance Between America’s Biggest Bank and America’s Biggest Crook. Chaitman and Gotthoffer provide this analysis: (JPMC stands for JPMorgan Chase.)

“In Chapter 4, we compared JPMC to the Gambino crime family to demonstrate the many areas in which these two organizations had the same goals and strategies. In fact, the most significant difference between JPMC and the Gambino Crime Family is the way the government treats them. While Congress made it a national priority to eradicate organized crime, there is an appalling lack of appetite in Washington to decriminalize Wall Street. Congress and the executive branch of the government seem determined to protect Wall Street criminals, which simply assures their proliferation.”

Chaitman and Gotthoffer then suggested using the RICO statute to prosecute the bank, writing:

“If Jamie Dimon is running a criminal institution, he should be prosecuted for it. And law enforcement has the perfect tool for such a prosecution: the Racketeer Influenced and Corrupt Organizations ACT (RICO).

“Congress enacted RICO in 1970 in order to give law enforcement the statutory tools it needed to prosecute the people who committed crimes upon orders from mob leaders and the mob leaders themselves. RICO targets organizations called ‘racketeering enterprises’ that engage in a ‘pattern’ of criminal activity, as well as the individuals who derive profits from such enterprises. For example, under RICO, a mob leader who passed down an order for an underling to commit a serious crime could be held liable for being part of a racketeering enterprise. He would be subject to imprisonment for up to twenty years per racketeering count and to disgorgement of the profits he realized from the enterprise and any interest he acquired in any business gained through a pattern of ‘racketeering activity.’ “

To date, the U.S. Department of Justice has charged JPMorgan Chase with five felony counts between 2014 and 2020. In each case, the bank admitted to the charges and in each case the Justice Department gave it a deferred prosecution agreement, meaning it was put on probation and had to promise not to engage in more crimes. Nonetheless, the crimes continued. In the Princeling scandal, the bank was given a non-prosecution agreement.

Astonishingly, the Board of Directors of JPMorgan Chase did not see this unprecedented pattern of crime on Jamie Dimon’s watch as sufficient grounds to fire him. Instead, the Board made Dimon a billionaire with stock awards and bonuses. (See our report: If You’re Baffled as to Why JPMorgan Chase’s Board Hasn’t Sacked Jamie Dimon as the Bank Racked Up 5 Felony Counts – Here’s Your Answer.)

3,Chris Powell of GATA provides to us very important physical commentaries

A bank China built to challenge the dollar now needs it

Submitted by admin on Fri, 2023-06-16 11:10Section: Daily Dispatches

By Alexander Saeedy and Lingling Wei

The Wall Street Journal

Friday, June 16, 2023

A development bank China launched with its fellow Brics countries was supposed to reshape international finance. Russia’s invasion of Ukraine now risks turning it into a zombie bank.

Eight years after Chinese leader Xi Jinping and his counterparts from Brazil, Russia, India and South Africa established the New Development Bank, with headquarters in a swanky Shanghai skyscraper, it has all but stopped making new loans and is having trouble raising dollar funds to repay its debts, according to an examination of its finances and interviews with bankers and others familiar with the matter.

The New Development Bank is the lesser-known of two China-based multilateral lenders. Its larger cousin, the Asian Infrastructure Investment Bank, this week landed in the middle of a public-relations crisis after a disgruntled executive accused it of being controlled by members of China’s Communist Party.

Trouble at both banks, as well as at China’s giant Belt and Road infrastructure push, which has seen China spend $1 trillion to expand its influence across Asia, Africa, and Latin America, spotlights growing difficulties for Beijing’s strategy to rearrange an international order it considers biased in favor of the West.

Both the AIIB and the New Development Bank were set up in large part to reduce developing countries’ dependence on dollar-based funding—alternatives to the International Monetary Fund that would help finance development in some of the world’s fastest-growing economies. …

… For the remainder of the report:

end

The dreadful story of J’Burg:

(Bloomberg News)

Africa’s richest city is crumbling under chaos and corruption

Submitted by admin on Sat, 2023-06-17 10:34Section: Daily Dispatches

By S’thembile Cele

Bloomberg News

Friday, June 16, 2023

Solomon Owa’s fingers work quickly as he speaks over the hum of his sewing machine. That’s because the hum of his sewing machine might stop at any moment. “In a few minutes, the power will go,” he said.

The 51-year-old runs a tailoring business from his garage in Johannesburg. Outages leave him idle for up to 10 hours a day. Surrounded by piles of colorful material, he needs to work while he can.

It’s a rush that South Africans have begrudgingly become accustomed to as they’re forced to use more and more ingenuity to navigate daily life: Charge devices, take a shower before the hot water goes off, and leave the house before the traffic lights go out. Schools, hospitals, restaurants and businesses rely on backup generators to keep running. Homeless people guide vehicles through potholed streets for cash.

The continent’s richest city was built on gold, but it’s now defined by chaos, crime and corruption more than ever. It encapsulates the wider collapse of basic services across South Africa. From a broken railway network disrupting trade to archaic sanitation that triggered a recent cholera outbreak near the capital, Pretoria, parts of the country increasingly look like a failing state. …

… For the remainder of the report:

END

A must view:

Gold revaluation is trump card in East-West power struggle, Maguire says

Submitted by admin on Sat, 2023-06-17 22:24Section: Daily Dispatches

10:24p ET Saturday, June 17, 2023

Dear Friend of GATA and Gold:

London metals trader Andrew Maguire, speaking on this week’s “Live from the Vault” program with Shane Morand from Kinesis Money, says gold revaluation is the trump card in the power struggle between East and West and will be played soon by either Russia and China or by the United States to pre-empt its adversaries.

This, Maguire says, brings urgency to the unwinding of the U.S.-underwritten short position in gold futures.

The program is 38 minutes long and can be seen at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Butler notes huge rise in banks’ metals derivatives positions, but whose are they really?

Submitted by admin on Mon, 2023-06-19 17:23Section: Daily Dispatches

5:29p ET Monday, June 19, 2023

Dear Friend of GATA and Gold (and Silver):

Market analyst Ted Butler today reports “stunning” increases in the monetary metals derivatives positions of JPMorganChase Bank and Bank of America and expresses concern that the latter bank could get in trouble with its derivatives insofar it is “inexperienced” in this market.

But what if the huge monetary metals derivatives positions attributed to these banks are not really the banks’ own positions at all? What if they are really U.S. government positions, with the banks acting as brokers?

After all, a few years ago JPMorgan executives insisted that the bank had no proprietary position in silver and traded the metal only for clients. Of course nobody asked the bank whether those clients included the government. But if the JPMorgan and Bank of America derivative positions in the monetary metals are as disproportionate as Butler finds — that they “tower” over gold and silver trading on the New York Commodities Exchange — more than ordinary trading is indeed going on.

Really, how can anyone not suspect U.S. government involvement with those outsized derivatives positions when the U.S. Commodity Futures Trading Commission repeatedly has refused to answer, even for a member of Congress, whether it has jurisdiction over manipulative trading undertaken by or at the behest of the U.S. government?:

https://www.gata.org/node/19917

The CFTC’s refusal to answer that question — and the failure of financial journalists and market analysts to ask it — gave the game away long ago.

Butler’s analysis is headlined “Another Stunning OCC Report” and it’s posted at GoldSeek’s companion site, SilverSeek, here:

https://silverseek.com/article/another-stunning-occ-report-1

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES/

A black swan event to trigger the gold price revaluation

https://kinesis.money/live-from-the-vault/black-swan-gold-price-revaluation/

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS/TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.1760

OFFSHORE YUAN: 7.1845

SHANGHAI CLOSED DOWN 15.44 PTS OR 0.47%

HANG SENG CLOSED DOWN 305.81 PTS OR 1.54%

2. Nikkei closed UP 18.49 PTS OR 0.06%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 102.08 EURO RISES TO 1.0927 UP 4 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.372 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 141.43/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.455***/Italian 10 Yr bond yield FALLS to 4.049*** /SPAIN 10 YR BOND YIELD FALLS TO 3.372…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 3.72

3j Gold at $1950.55 silver at: 23.81 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 33 /100 roubles/dollar; ROUBLE AT 84.47//

3m oil into the 72 dollar handle for WTI and 76 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 141.43// 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .385% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8975 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9806 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.768 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 3.855 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.700 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 23.56…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.394 DOWN 10 BASIS PTS (RATES RISING RAPIDLY)

end

2. Overnight: Newsquawk and Zero hedge:

MONDAY

Global Markets Drop, US Futures Flat In Muted Holiday Trading

MONDAY, JUN 19, 2023 – 08:13 AM

Global stocks fell on Monday after the recent powerful rally lost steam at the end of last week, while US equity futures were flat in thin trading celebrating the (“exploitative”) Juneteenth holiday following Wall Street’s slight decline on Friday amid concern about the economic outlook. S&P 500 futures traded between modest gains and losses and at last check were down 0.1% as of 8:00am ET while Nasdaq 100 futures were flat. Global investors were also disappointed by the ongoing lack of more stimulus from China after its State Council stopped short of releasing any specific proposals for new support measures for the economy.

The S&P 500 has rallied for the past five weeks, the longest such streak since November 2021, as investors anticipate the end of the Fed’s tightening cycle and that earnings will hold up better than expected. Several Fed officials, including Chair Powell, are slated to speak this holiday-shortened week. Investors will parse these statements for clues on the path of monetary policy and the direction of growth.

Despite the pressure of an $4.2 trillion options expiry at the end of last week, the S&P 500 index capped a fifth straight week of gains and is now higher than it was the day the Federal Reserve kicked off its campaign.

“We expect the US to head into a short, two-quarter, recession later this year,” said Joachim Klement, head of strategy, accounting and sustainability at Liberum Capital. That said, the “US recession is likely to be shallower and shorter than those in Europe and as a result, companies with a larger US revenue exposure will likely outperform companies with more exposure to Europe or the slowing Chinese consumer.”

Looking ahead, Fed Chair Jerome Powell will give his semi-annual report to Congress on Wednesday, while St. Louis Fed President James Bullard and his counterparts in New York and Chicago are among this week’s speakers.

As discussed previously, the S&P 500 index posted its mildest reaction on FOMC day in two years. Though it was the first in 11 meetings where policymakers held rates, they also lifted forecasts for higher borrowing costs of 5.6% in 2023, implying two additional quarter-point rate hikes or one half-point increase before the end of the year, although judging by the market reaction, few believed this particular forecast.

“Markets are still pricing in a lower path of interest rates compared to the Federal Reserve’s dot plot,” said Janet Mui, head of market analysis at RBC Brewin Dolphin. “While we are close to peak rates, it is uncertain how long rates will stay high. Markets have a more dovish lens on that.”

European stocks followed their Asian counterparts lower as investors were left disappointed by the lack of any fresh stimulus measures from China. Traders are also keeping an eye on details surrounding the meeting between Blinken and Xi in Beijing.

The Stoxx 600 is down 0.5% with with chemicals, construction and basic resources leading declines, while financials and insurance are the only sectors in the green. Among the biggest individual movers, Sartorius AG slumped 15% after issuing a bigger-than-expected profit warning. Here are some of the more notable movers:

- MTU Aero Engine gains as much as 4.5% after it raised its earnings forecast for the current financial year. Jefferies says the timing and magnitude of the revision so early in the year should be well received

- Granges gains as much as 7.4% after it was upgraded to buy from hold in the short term at Handelsbanken, which projected the Swedish aluminum engineering firm may post a record 2Q

- Crayon shares rise as much as 10% after Bloomberg News reported that the Norwegian IT consultancy is said to be exploring options including a sale

- Avacta shares rise as much as 12% after the life sciences-focused small-cap firm said it had a “strong” cash balance of £27 million and no fundraising is imminent

- Sartorius AG and its French-listed subsidiary Sartorius Stedim Biotech both plunge after cutting full-year forecasts, with Sartorius AG down as much as 15% and Sartorius Stedim down 16%

- Nordnet sinks as much as 12% after receiving its only negative analyst view as JPMorgan cuts the Swedish investment and savings platform to underweight, citing higher cost of deposits and weak inflows

- ALK-Abello shares fall as much as 9.4%, the most since April, after CEO Carsten Hellmann announced he will step down from his role at the Danish allergy drugmaker at the end of 2023

Earlier in the session, Chinese tech companies dropped after China disappointed hopes for further stimulus. Asian stocks were mostly negative following last Friday’s US losses while risk appetite was also contained as markets digested US-China talks and with US markets closed. Nonetheless, ASX 200 (+0.6%) bucked the trend with the index buoyed as strength in the defensive, financial and tech sectors made up for the losses in mining-related stocks. Nikkei 225 (-1.1%) was subdued and eventually breached through earlier support around the 33,500 level, after a torrid rally that helped send the index to the highest level since 1990.

Hang Seng (-0.8%) and Shanghai Comp. (-0.5%) were lower amid ongoing China growth concerns with the likes of Goldman Sachs, Nomura and UBS all cutting their Chinese GDP forecasts for 2023, while participants also digested the meeting between US Secretary of State Blinken and Chinese Foreign Minister Qin in Beijing which was said to be candid, substantive and constructive although lacked any major breakthroughs aside from agreeing to schedule a reciprocal visit at a suitable time.

Reports covering China’s State Council meeting on Friday, chaired by Premier Li Qiang, were light on details about any potential stimulus or timing. The lack of tangible evidence for support adds to worries over a slowing economy, unnerving investors who had bid up Chinese equities last week in the hope of a sweeping package.

Treasury futures are lower with cash markets closed for to the Juneteenth holiday in the US. Bunds and gilts are also in the red.

In Fx, the Bloomberg Dollar Spot Index is up 0.1%. The Norwegian krone is the weakest of the G10 currencies, falling 0.4% versus the greenback. The offshore yuan is down 0.4%.

In commodities crude futures decline with WTI falling 0.4% to trade near $71.50. Spot gold is little changed around $1,956

There is nothing on today’s US calendar.

* * *

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks were mostly negative following last Friday’s losses on Wall St, while risk appetite was also contained as markets digested US-China talks and with US markets closed on Monday for Juneteenth. ASX 200 bucked the trend with the index buoyed as strength in the defensive, financial and tech sectors made up for the losses in mining-related stocks. Nikkei 225 was subdued and eventually slipped below earlier support around the 33,500 level. Hang Seng and Shanghai Comp. were lower amid ongoing China growth concerns with the likes of Goldman Sachs, Nomura and UBS all cutting their Chinese GDP forecasts, while participants also digested the meeting between US Secretary of State Blinken and Chinese Foreign Minister Qin in Beijing which was said to be candid, substantive and constructive although lacked any breakthroughs aside from agreeing to schedule a reciprocal visit at a suitable time. US equity futures were uneventful after Friday’s retreat and approaching holiday lull. European equity futures are indicative of a lower open with the Euro Stoxx 50 -0.7% after the cash market closed up 0.7% on Friday.

Top Asian News

- US President Biden said he is hoping to meet with Chinese President Xi in the next several months.

- US Secretary of State Blinken held candid, substantive and constructive talks with Chinese Foreign Minister Qin in Beijing and emphasised the importance of diplomacy and maintaining open channels of communication to reduce the risk of misperception and miscalculation. Blinken raised issues of concern and opportunities to explore cooperation on shared transnational issues with China where interests align, while Blinken invited Qin to visit Washington to continue the discussions and they agreed to schedule a reciprocal visit at a suitable time, according to a State Department spokesperson cited Reuters.

- US State Department senior officials said US Secretary of State Blinken’s meeting with his Chinese counterpart was direct and it was clear there are profound differences between the two countries, while both officials were well-prepared and it was a “real conversation”. Furthermore, Blinken made it clear that the US does not want to decouple from China and the two sides expressed a desire to stabilise the relationship and prevent competition from veering into conflict, as well as agreed to work together to increase commercial flights between the US and China, according to Reuters.