JUNE 21//GOLD CLOSED DOWN $2.45 TO $1934.15//SILVER CLOSED DOWN $.0.40 TO $22.79/PLATINUM CLOSED DOWN $15.45 TO $950.45 WHILE PALLADUM CLOSED DOWN $30.65 TO $1350.60//IMPORTANT READ FOR TODAY: JAMES RICKARDS//CHINA LASHES OUT AGAINST BIDEN FOR CALLING XI A DICTATOR//UKRAINE VS RUSSIA UPDATES//COVID VACCINE UPDATES/DR PAUL ALEXANDER/SLAY NEWS//TUCKER CARLSON PODCAST NO 5//SWAMP STORIES FOR YOU TONIGHT..

132 C SG AMERICAS 7 323 C HSBC 480 323 H HSBC 83 363 H WELLS FARGO SEC 12 435 H SCOTIA CAPITAL 47 661 C JP MORGAN 8 218 661 H JP MORGAN 11 685 C RJ OBRIEN 1 690 C ABN AMRO 10 22 709 C BARCLAYS 3 737 C ADVANTAGE 2 6 880 H CITIGROUP 76 905 C ADM 14

TOTAL: 500 500 MONTH TO DATE: 19,677

JPMorgan stopped 229/500 contracts

FOR JUNE:

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2023. CONTRACT: 500 NOTICES FOR 50,000 OZ or 1.552 TONNES

total notices so far: 19,677 contracts for 1,967,700 oz (61.203 tonnes)

FOR JUNE:

SILVER NOTICES: 0 NOTICE(S) FILED FOR NIL OZ/

total number of notices filed so far this month : 423 for 2,115,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $2.45

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

/NO CHANGES IN GOLD INVENTORY AT THE GLD:////

INVENTORY RESTS AT 934.03 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 40 CENTS AT THE SLV// ???

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 5.4784 MILLION OZ INTO THE SLV///

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 468.967 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GIGANTIC SIZED 1042 CONTRACTS TO 152,632 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR GIGANTIC $0.89 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. TAS ISSUANCE WAS A HUMONGOUS SIZED 1419 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH . CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 1419 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.89). BUT WERE SUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD AN ATMOSPHERIC GAIN ON OUR TWO EXCHANGES OF 1658CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 13.370MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION.

WE MUST HAVE HAD:

A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 616 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.935 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP + 0 MILLION OZ EXCHANGE FOR RISK(ISSUED TODAY: TOTAL ISSUED SO FAR: 13.370 MILLION OZ)// TOTAL STANDING FOR THE MONTH 4.270 MILLION OZ + 13.370 MILLION EXCHANGE FOR RISK = 17,640 MILLION OZ// ) // HUGE SIZED COMEX OI GAIN/ STRONG SIZED EFP ISSUANCE/VI) STRONG NUMBER OF T.A.S. CONTRACT ISSUANCE (790CONTRACTS)//

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –339 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTRACTS for 13 days, total 15,137 contracts: OR 75.685 MILLION OZ (1164 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 75.685 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.430 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 75.685 MILLION OZ//MUCH LARGER THAN LAST MONTH

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1042 CONTRACTS DESPITE OUR LOSS IN PRICE OF $0.89 IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG EFP ISSUANCE CONTRACTS: 616 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.935 MILLION OZ FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP+ 0 MILLION EXCHANGE FOR RISK TODAY + 13.37 MILLION EXCHANGE FOR RISK(PRIOR)//NEW TOTAL STANDING: 17.640 MILLION OZ////// .. WE HAVE AN ATMOSPHERIC SIZED GAIN OF1658 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE 1419//CONSIDERABLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION RAID. THE NEW TAS ISSUANCE TODAY (1419) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE.

WE HAD 0 NOTICE(S) FILED TODAY FOR NIL OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 6,000 CONTRACTS TO 438,037 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED – 1124 CONTRACTS

WE HAD A STRONG SIZED INCREASE IN COMEX OI ( 6,000 CONTRACTS) DESPITE OUR $22.40 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JUNE. AT 70.79 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0.0279 TONNE QUEUE JUMP: NEW TOTAL 64.195 TONNES STANDING SO FAR // + /A STRONG ISSUANCE OF 1162 T.A.S. CONTRACTS ////YET ALL OF..THIS HAPPENED WITH A $22.40 LOSS IN PRICEWITH RESPECT TO TUESDAY’S TRADING.WE HAD A VERY STRONG SIZED GAIN OF 9.394 OI CONTRACTS (29.219 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3394 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 438,037

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 9,394 CONTRACTS WITH 6,000 CONTRACTS INCREASED AT THE COMEX//TAS CONTRACTS INITIATED (ISSUED): A STRONG 1162 CONTRACTS) AND 3394 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 9,394CONTRACTS OR 29.219 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3394 CONTRACTS) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (6,000) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 9,394 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 70.79 TONNES FOLLOWED BY TODAY’S 900 OZ QUEUE JUMP //// NEW STANDING RISES TO 64.195 TONNES// /3) ZERO LONG LIQUIDATION//4) STRONG SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: STRONG T.A.S. ISSUANCE: 1162 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

TOTAL EFP CONTRACTS ISSUED: 31,210 CONTRACTS OR 3,121,000 OZ OR 97.076TONNES IN 13 TRADING DAY(S) AND THUS AVERAGING: 2400 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAY(S) IN TONNES 97.076 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 97.076/3550 x 100% TONNES 2.73% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 97.076 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 1042 CONTRACTS OI TO 152,632 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 616 CONTRACTS (RECORD ISSUANCE)

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 350and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 616 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1042 CONTRACTS AND ADD TO THE 616OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1658 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 8.290 MILLION OZ

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED DOWN 42.46 PTS OR 1.31% //Hang Seng CLOSED DOWN 388.73 PTS OR 1.98% /The Nikkei closed UP 186.23 OR 0.56% //Australia’s all ordinaries CLOSED DOWN 0.57 % /Chinese yuan (ONSHORE) closed DOWN 7.1884 /OFFSHORE CHINESE YUAN DOWN TO 7.1896 /Oil DOWN TO 71.16 dollars per barrel for WTI and BRENT UP AT 75.78 / Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 6,000 CONTRACTS DOWN TO 438,037 DESPITE OUR HUGE LOSS IN PRICE OF $22.40 ON TUESDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3394 EFP CONTRACTS WERE ISSUED: : AUGUST 3394 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3394 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG SIZED TOTAL OF 9,394 CONTRACTS IN THAT 3394LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED GAIN OF 6,000 COMEX CONTRACTS..AND THIS VERY STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $22.40//TUESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A STRONG 1162 CONTRACTS. THROUGHOUT LAST WEEK, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THE HUGE NUMBER OF T.A.S. CONTRACTS INITIATED OVER THE PAST SEVERAL WEEKS SPELLS TROUBLE FOR THE GOLD/SILVER MARKET AS RAIDS WILL SURELY BE UPON US.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (64.195) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.541 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.195 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $22.40) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR HUGE GAIN OF 9,394 CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE TAS LIQUIDATION THROUGHOUT THE TUESDAY COMEX SESSION . THE TAS ISSUED TUESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 32.715PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE. (70.709 TONNES) FOLLOWED BY TODAY’S 900 OZ QUEUE JUMP..NEW STANDING REMAINS AT 64.195 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR HUGE LOSS IN PRICE TO THE TUNE OF $22.40

WE HAD – REMOVED 1124 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 9394 CONTRACTS OR 939400 OZ OR 29.219 TONNES.

Total monthly oz gold served (contracts) so far this month

19,677 notices 1,967,700 OZ 61.203 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

No dealer withdrawals

Customer deposits: 0

Dealer deposit: 1

i)Into ASHAI 47,948.709 oz

total dealer deposits: 47,948.709 oz

Customer Withdrawals: 3

i) out of Brinks: 64.300 oz (2 kilobars)

ii) Out of JPMorgan: 192.906 oz (6 kilobars)

iii) Out of HSBC: 10,807.843 oz

total 11,065.049 oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 1462 contracts having LOST 202 contracts. We had 211 contracts served on Tuesday so we gained 9 contracts or an additional 900 oz will stand for gold at the comex.

The next front month after June is the non active delivery month of July. Here, July gained 69 contracts to stand at 2538 contracts.

AUGUST gained 3441 contracts up to 368,320 contracts

We had 500 contracts filed for today representing 50,000 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 8 notices were issued from their client or customer account. The total of all issuance by all participants equate to 500 contract(s) of which 11 notices were stopped (received) by j.P. Morgan dealer and 218 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2023. contract month,

we take the total number of notices filed so far for the month (19,677 x 100 oz ), to which we add the difference between the open interest for the front month of JUNE (1462 CONTRACT) minus the number of notices served upon today 500 x 100 oz per contract equals 2,065,900 OZ OR 64.195 TONNES the number of TONNES standing in this active month of June.

thus the INITIAL standings for gold for the JUNEcontract month: No of notices filed so far (19,677) x 100 oz + (xxx) {OI for the front month} minus the number of notices served upon today (500) x 100 oz) which equals 2,065,900 oz standing OR 64.195 TONNES

TOTAL COMEX GOLD STANDING: 64.195 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 423 x 5,000 oz = 2,115,000 oz

to which we add the difference between the open interest for the front month of JUNE(431) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2023 contract month: 423 (notices served so far) x 5000 oz + OI for the front month of JUNE (431) – number of notices served upon today (0 )x 500 oz of silver standing for the JUNE contract month equates to 4.270 million oz + 2.935 EXCHANGE FOR RISK TODAY + 10.435MILLION OZ EXCHANGE FOR RISK (PRIOR)//NEW TOTAL: 17.640 MILLION OZ STANDING

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

JUNE 21/WITH GOLD DOWN $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 934.03 TONES

JUNE 20/WITH GOLD DOWN $22.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.03 TONNES

JUNE 16/WITH GOLD UP $0.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.33 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.03 TONNES

JUNE 15/WITH GOLD UP $2.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 929.70 TONNES

JUNE 14/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 931.44 TONNES

JUNE 13/WITH GOLD DOWN $10.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.01 TONNES FORM THE GLD///INVENTORY RESTS AT 931.44

JUNE 12/WITH GOLD DOWN $7.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.65 TONNES

JUNE 9/WITH GOLD DOWN $1.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.65 TONNES

JUNE 8/WITH GOLD UP $20.45 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.46 TONNES FROM THE GLD///INVENTORY RESTS AT 934.65 TONNES

JUNE 7 WITH GOLD DOWN $22.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 938.11 TONNES

JUNE 6/WITH GOLD UP $6.90 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 939.56 TONNES

JUNE 5/WITH GOLD UP $5.00 TODAY : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 938.11 TONNES

JUNE 2/WITH GOLD DOWN $24.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 938.11 TONNES

JUNE 1/WITH GOLD UP $14.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 939.56 TONNES

MAY 31/WITH GOLD UP $5.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 939.56 TONNES

MAY 30/WITH GOLD UP $14.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 26/WITH GOLD UP $.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 941.29 TONNES

MAY 25/WITH GOLD DOWN $19.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 24/WITH GOLD DOWN $9.50 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 941.29 TONNES

MAY 23/WITH GOLD $2.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 942.74 TONNES

MAY 22/WITH GOLD DOWN $4.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.83 TONES OF GOLD INTO THE GLD DESPITE THE L0SS IN PRICE//INVENTORY RESTS AT 942.74 TONNES

MAY 19/WITH GOLD UP $22.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 936.96 TONNES

MAY 18/WITH GOLD DOWN $23.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 936.96 TONNES

MAY 17/WITH GOLD DOWN $8.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.94 TONNES

MAY 16/WITH GOLD DOWN 28.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.57 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 934,07

MAY 15/WITH GOLD UP $2.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 937.64 TONNES

MAY 12/WITH GOLD DOWN $.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 937.84 TONNES

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 934.95 TONNES

GLD INVENTORY: 934.03 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 21/WITH SILVER DOWN $.40 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 20/WITH SILVER DOWN 89 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 16/WITH SILVER UP 23 CENTS TODAY :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 463.183 MILLION OZ

JUNE 15/WITH SILVER DOWN 17 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.377 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 463.642 MILLION OZ//

JUNE 14/WITH SILVER UP 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 735,000 OZ FROM THE SLV///INVENTORY RESTS AT 465.019 MILLION OZ//

JUNE 13/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.515 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 465.754 MILLION OZ//

JUNE 12/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.269 MILLION OZ//

JUNE 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF SILVER TO THE TUNE OF 550,000 OZ//INVENTORY RESTS AT 467.269 MILLION OZ

JUNE 8/WITH SILVER UP $0.63 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 467.819 MILLION OZ/

JUNE 7/WITH SILVER DOWN 17 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.01 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 467.819 MILLION OZ/

JUNE 6/WITH SILVER UP 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.809 MILLION OZ//

JUNE 5/WITH SILVER DOWN $.13 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 266,000 OZ FROM THE SLV////INVENTORY RESTS AT 466.809 MILLION OZ/

JUNE 2/WITH SILVER DOWN 23 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV./INVENTORY RESTS AT 467.015 MILLION OZ/

JUNE 1/WITH SILVER UP 49 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.933 MILLION OZ

MAY 31/WITH SILVER UP 37 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 367,000 OZ FROM THE SLV////INVENTORY RESTS AT 467.933 MILLION OZ//

MAY 30/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 26/WITH SILVER UP $0.44 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.306 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 25.WITH SILVER DOWN $0.32 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 471.606 MILLION OZ//

MAY 24/WITH SILVER DOWN $.35 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 23/WITH SILVER DOWN 22 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.801 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 22/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ//

MAY 19/WITH SILVER UP 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ

MAY 18/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.529 MILLION OZ/

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

MAY 16/WITH SILVER DOWN 34 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .643 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.448 MILLION OZ.

MAY 15/WITH SILVER UP 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.091 MILLION OZ/

MAY 12/WITH SILVER DOWN $.26 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 3,123 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 470.091 MILLION OZ./

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

3,Chris Powell of GATA provides to us very important physical commentaries

A terrific read from Craig Hemke. He notes that the gold mining shares closely correlate to the rigged silver price

a must read…

(Craig Hemke)

Craig Hemke at Sprott Money: Comex silver and the GDX price

Submitted by admin on Tue, 2023-06-20 20:46Section: Daily Dispatches

8:46p ET Tuesday, June 20, 2023

Dear Friend of GATA and Gold:

Market analyst Craig Hemke, writing today at Sprott Money, notes that the price of the gold-mining share exchange-traded fund GDX seems to correlate closely with the silver price and not so much with the gold price.

Why? Hemke suggests that high-frequency trading of mining shares and market manipulation may have something to do with it, and that, indeed, rigging the silver price could be the key mechanism for rigging the whole monetary metals sector.

Hemke’s analysis is headlined “Comex Silver and the GDX” and it’s posted at Sprott Money here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

END

The following is a very important commentary from Rickards where the BRICS will start a new currency backed by gold on August 22

(Jim Rickards)

Jim Rickards: The biggest monetary shock in 52 years is due in August

Submitted by admin on Tue, 2023-06-20 20:55Section: Daily Dispatches

By James G. Rickards The Daily Reckoning, Baltimore Tuesday, June 20, 2023

I recently revealed that the so-called “BRICS+” countries will announce the creation of a new currency at their annual leaders summit conference from August 22–24.

This will be the biggest upheaval in international finance since 1971. It’s taking direct aim at the dollar.

The world is unprepared for this geopolitical shock wave.

It appears likely that the new BRICS+ currency will be linked to a weight of gold. This plays to the strengths of BRICS members Russia and China. These countries are the two largest gold producers and are ranked sixth and seventh respectively among the 100 nations with gold reserves.

One difficulty in considering the impact of the new BRICS currency on the dollar is that all dollar indexes compare currency to currency. But that’s meaningless since the dollar, euro, and sterling could all suffer from a loss of confidence at the same time.

If gold goes from $2,000 to $10,000 per ounce, that is better understood as an 80% devaluation of the dollar: from 0.0005 ounces per dollar to 0.0001 ounces per dollar. That’s a collapse of confidence but you’ll miss it if you’re looking at euros or yen.

Those currencies will all be collapsing at the same time. …

I recently revealed that the so-called “BRICS+” countries will announce the creation of a new currency at its annual leaders’ summit conference on August 22–24.

This will be the biggest upheaval in international finance since 1971. It’s taking direct aim at the dollar.

Quite simply, the world is unprepared for this geopolitical shock wave.

It appears likely that the new BRICS+ currency will be linked to a weight of gold. This plays to the strengths of BRICS members Russia and China. These countries are the two largest gold producers in the world, and are ranked sixth and seventh respectively among the 100 nations with gold reserves.

One difficulty in considering the impact of the new BRICS currency on the dollar is that all dollar indexes compare currency to currency. But that’s meaningless since the dollar, euro and sterling could all suffer from a loss of confidence at the same time.

If gold goes from $2,000 to $10,000 per ounce, that is better understood as an 80% devaluation of the dollar: from 0.0005 ounces per dollar to 0.0001 ounces per dollar. That’s a collapse of confidence but you’ll miss it if you’re looking at euros or yen.

Those currencies will all be collapsing at the same time.

The Only Way to Measure the Dollar

The only objective metric for dollar strength is the dollar price of gold by weight since gold is not a central bank currency. This resolves any valuation conundrum as follows:

1. Dollar strength can only properly be measured in gold.

2. Gold is money but it is also a commodity.

3. BRICS are dollar poor but commodity rich.

4. A new BRICS+ currency will be linked to gold.

So the collapse of the dollar really means higher inflation and a much higher dollar price for gold. That means other commodity prices will rise in lockstep. A commodity boom favors BRICS generally speaking.

This dynamic could lead the BRICS+ currency to displace the dollar as a dominant payment currency more quickly than most expect because of the link to gold.

Except for direct participants, the world has mostly ignored this prospect. The result will be a shock to the international monetary system coming in a matter of weeks.

Still, the impact on investors won’t end when the new BRICS+ currency is rolled out. The market implications will roil exchange rates and capital markets for years to come. Most people still have no idea how to even approach the subject.

Isn’t Gold Too Volatile to Support a Currency?

After I introduced this subject earlier this month, I received a reader question that I think needs to be addressed:

Jim, since the gold price is really a function of the paper gold market and is therefore subject to manipulation – and significant volatility – wouldn’t a gold-backed.currency require that gold be fixed at a certain price, such as it was fixed at $20.67 under the classic gold standard?

Otherwise, it would lack the stability a currency requires, even a gold-backed currency. Again, the paper market subjects gold to manipulation.

The U.S. obviously doesn’t want a rival currency bloc, especially one led by Russia and China, and would have every motivation to sabotage it.

The U.S., in conjunction with the big banks, could create all kinds of havoc in the paper market to undercut gold prices.

There really can’t be two parallel gold markets, one fixed at a certain price that BRICS recognizes and the other one fluctuating constantly.

In other words, can a trading bloc really adopt a gold-backed currency in the absence of an updated version of the classic gold standard with a fixed price?

Otherwise the volatility introduced by the paper market would render the underlying commodity unsuitable as a currency, which is meant to be stable. Or so it seems to me.

Am I missing something here?

It’s a good question, and that reader is months ahead of the rest of the world in figuring this out.

Gold Manipulation Is Real

The reader is correct that gold prices are manipulated. There is hard statistical evidence to make the case, in addition to anecdotal evidence and forensic evidence. The evidence is very clear, in fact.

I spoke to a Ph.D. statistician who works for one of the biggest hedge funds in the world. I can’t mention the fund’s name but it’s a household name. You’ve probably heard of it. He looked at Comex (the primary market for gold) opening prices and Comex closing prices for a 10-year period.

He was dumbfounded. He said it was the most blatant case of manipulation he’d ever seen. He said if you went into the aftermarket, bought after the close and sold before the opening every day, you would make risk-free profits.

He said statistically that’s impossible unless there’s manipulation occurring.

I also spoke to Professor Rosa Abrantes-Metz at the New York University Stern School of Business. She is the leading expert on globe price manipulation. She has actually testified in gold manipulation cases.

She wrote a report reaching the same conclusions. It’s not just an opinion, it’s not just a deep, dark conspiracy theory. Here’s a Ph.D. statistician and a prominent market expert lawyer, an expert witness in litigation qualified by the courts, who independently reached the same conclusion.

There’s no need to get into the nuts and bolts of how the manipulation is carried out; it’s enough to realize that it does actually happen.

Anyway, here’s how I’d answer the reader’s question…

It’s All About Weight

There will not be two prices for gold. There can only be one price (with small differences for paper versus physical, commissions, etc.).

If there were two prices in the same currency the difference would quickly disappear due to arbitrage (buying a security in one market and simultaneously selling it in another market at a higher price).

The gold “price” may be expressed in dollars, euros or BRICS+. Of course, you’ll get different absolute values in each currency but that’s a function of exchange rates, not different prices for gold.

The BRICS+ currency will be valued in units of gold by weight.

I don’t know what value they plan to use, but an example would be BRICS1.00 = 1 oz. gold. At today’s market, that would make BRICS1.00 = USD1,950 — but that is not a peg.

The peg is 1.0 oz. So the BRICS currency will have a fixed value in gold.

At the same time, the dollar will have a floating value in gold as it has since 1971. That means the BRICS/USD cross-rate will float based on the value of gold measured in each currency. You will be able to calculate the value of BRICS1.00 measured in dollars, but that is not a peg.

Here’s where it gets interesting for investors and for your asset allocation…

“China and Russia Are Likely to Call the Shots”

If the dollar price of gold goes up, the value of BRICS1.00 will go up against the dollar. If the dollar price of gold goes down, the value of BRICS1.00 will go down against the dollar.

If I’m a BRICS member, I might want the dollar price of gold to go up so I can buy U.S. goods and services on the cheap. Conversely, if I’m a BRICS member and a commodity exporter, I might want the dollar price of gold to go down so parties with dollars will buy more of my commodities.

Of course, that undermines the point of the BRICS currency to some extent because the whole idea is to get away from dollar-based transactions.

China and Russia are likely to call the shots. My estimate is they will want a high dollar price for gold in order to make their BRICS currency more valuable. This will help to increase their own wealth and destroy confidence in the dollar.

This policy backed up by physical gold purchases could drive the dollar price of gold to $3,000 per ounce or higher very quickly. In reality, the BRICS currency and physical gold are pegged and unchanged. If gold goes to $3,000 per ounce, we are actually witnessing the collapse of the dollar.

That’s the whole idea.

The dollar stands to lose in value measured in gold or BRICS currency. The dollar will also lose value due to inflation resulting from the lower value. It will take more dollars to buy imported goods or take vacations abroad.

Moving money to stocks, bonds or savings accounts won’t protect you because they’re all denominated in dollars.

There’s a simple solution to this coming currency crisis. Just buy gold. That will preserve wealth and protect you from inflation. You can always sell the gold if you need cash; it’s just that you’ll get more cash than what you used to buy it. That’s what the BRICS are doing and you can too.

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS/WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.1884

OFFSHORE YUAN: 7.1896

SHANGHAI CLOSED DOWN 42.46 PTS OR 1.31%

HANG SENG CLOSED DOWN 388.73 PTS OR 1.98%

2. Nikkei closed UP 186.23 PTS OR 0.56%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 102.14 EURO RISES TO 1.0925 UP 5 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.371 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 141.77/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.403***/Italian 10 Yr bond yield FALLS to 4.037*** /SPAIN 10 YR BOND YIELD FALLS TO 3.345…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 3.671

3j Gold at $1934.25 silver at: 23.05 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 55 /100 roubles/dollar; ROUBLE AT 84.23//

3m oil into the 71 dollar handle for WTI and 75 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 141.77// 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO .371% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8972 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9802 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.755 UP 3 BASIS PTS…

USA 30 YR BOND YIELD: 3.836 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.715 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 23.56…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.42 UP 10 BASIS PTS (RATES RISING RAPIDLY)

end

2. Overnight: Newsquawk and Zero hedge:

Futures Flat Ahead Of Powell Testimony

WEDNESDAY, JUN 21, 2023 – 08:07 AM

US equity futures are flat and global markets grind lower, as bond yields and breakevens rise in reaction to the latest “shockingly” hot UK inflation data (May U.K. CPI unchanged at 8.7% vs. exp. of a drop to 8.4% y/y ) which saw the odds of a 50 bps BOE hike tomorrow jump to 50%. At 7:30am, S&P futures were down -0.1%, flipping between modest gains and losses after trading in a narrow range after the S&P index notched its first back-to-back losses in nearly four weeks. Economic bellwether FedEx Corp. tumbled 3% in premarket trading after its outlook fell short of analyst consensus estimates on weakened demand. The Bloomberg gauge of the dollar moved higher and Group-of-10 currencies were mixed, with the pound the worst performer. Treasury yields drifted higher across the curve, following their UK counterparts. Gold and oil were little changed, while Bitcoin climbed for a third-straight day. BBG reports that Equity ETFs have seen $102BN in inflows vs. $93bn for FICC ETFs; if ECM and M&A turn back on, could flow outperformance increase.

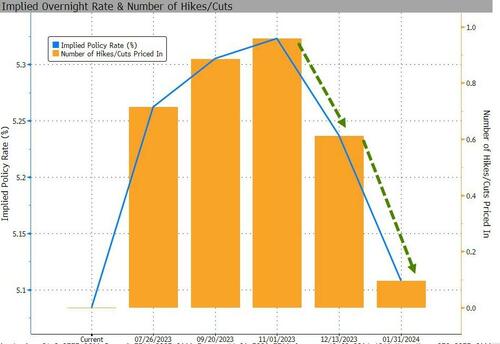

There are no notable economic reports in the U.S. today (the MBA mortgage applications index rose 0.5% after last week’s 7.2% jump). Powell testifies today and tomorrow at 10am ET, with at least 8 more Fed speakers on deck for the rest of the week including Jefferson (10:00 a.m. ET), Goolsbee (12:25 p.m. ET), Mester (E: 4:00 p.m. ET). More hawkish rhetoric is expected, which may push July hike odds even higher (~74% pre-mkt). There is a 20-Yr Treasury Bond auction at 1:00 p.m. ET.

In premarket trading, FedEx shares dropped as much as 3.3% after the parcel company gave a 2024 forecast that came in below analyst expectations, while fourth-quarter revenue lagged the consensus. Analysts noted that the macro environment remained tough and the tepid guidance will pressure the stock. Tesla gained 2% premarket, set to extend its 35% rally in June. CEO Elon Musk said the automaker is likely to make a significant investment in India. Meanwhile, China extended tax breaks for consumers buying clean cars through 2027 and auto sales in Europe continued their upward trajectory in May as demand for electric cars outpaced the broader market. Here are some other notable premarket movers:

Peloton Interactive shares decline 3.4% in premarket trading after Wolfe Research analyst Zach Morrissey assumed coverage of the exercise-equipment maker and downgraded the firm’s recommendation to underperform from peerperform.

Li Auto leads gains in Chinese electric vehicle makers during US premarket trading, after China extended tax breaks through 2027 for consumers buying clean-energy cars.

Nikola shares rise as much as 9.1% in premarket trading, setting the electric-truck maker up for a ninth day of gains in 10.

Exact Sciences Corp. gains 6% in US premarket trading after the life sciences firm published study results on Tuesday showing its new Cologuard test, used to screen for colorectal cancer, met all study endpoints and “improved every top-line metric.”

Spotify Technology advanced 1.5% in US postmarket trading Tuesday after Wolfe Research analyst Zach Morrissey assumed coverage of the audio streaming company and upgraded the firm’s recommendation to outperform from peerperform.

PureCycle Technologies Inc. rose 11% in postmarket trading after successfully producing the first run of Ultra-Pure Recycled resin from post-industrial recycled material at commercial scale.

Gilts slumped at the open after red hot UK inflation surprised to the upside. Two-year yields are now off the highs but still up 7bps as traders firm up bets on the BOE raising interest rates to 6%. The pound rallied initially but has since turned lower, falling 0.4% versus the greenback. To that point, Pooja Kumra, senior European rates strategist at Toronto Dominion Bank said that rampant price pressures in the UK may sway global central banks against a downshift to easier policy.

“A key risk for markets is whether Powell provides any conditions for the FOMC getting back to their hiking cycle after a pause in June,” Kumra said.

“Everybody is expecting a strong, higher-for-longer message from Powell,” said Derek Halpenny head of research at MUFG of the Fed Chair’s testimony later today. “But it is hard to envisage this message resonating with markets in a dramatically different way to last week.”

Powell prepares to give his semi-annual report to Congress on Wednesday, where he’s expected to reiterate warnings that higher rates may be needed to combat inflation. While Fed policymakers kept interest rates unchanged at their meeting last week, their forecasts imply around two additional quarter-point rate hikes or one half-point increase.

European equities were steady as investors prepared for the congressional testimony of Federal Reserve Chair Jerome Powell, while hotter-than-expected UK inflation figures kept a lid on sentiment. The Stoxx Europe 600 was down less than 0.1% with the FTSE 100 Index erasing losses of as much as 0.6% to trade flat. Real estate stocks were among the worst performers while automotive shares outperformed after a report showed auto sales in Europe continued their upward trajectory in May. Here are some of the most notable European movers:

Adidas rises as much as 4.4% as UBS upgrades shares to buy, citing early signs of brand inflection driven by its Lifestyle offering, as well as improved margins

Argenx rises as much as 3.3% after the US drug regulator approved Vyvgart Hytrulo subcutaneous injection to treat generalized myasthenia gravis, news analysts say might further boost sales

Husqvarna gains as much as 7.1%, the most since April, after the Swedish lawn-care firm was upgraded to hold from sell at DNB, which said it’s time to focus on the investment case beyond 2023

Halfords shares rise as much as 8%, the most since April, after the car parts and bicycles retailer said recent trading has been solid and Peel Hunt upgraded the stock to buy from add

THG shares jump as much as 11% after the online retailer said it sees a “significant” increase in 1H profitability, a trading update that Jefferies called “encouraging”

AO World shares advance 3.1%, reaching the highest level since April 2022, after Davy upgraded the home- appliances retailer to outperform, saying the firm continues to overdeliver

Beijer Ref falls as much as 9.2% after an offering of 40m class B shares by EQT IX fund priced at SEK140 apiece, representing a discount of 7.2% to Tuesday’s closing price

Aedifica falls as much as 4.9%, as the Belgian real estate firm announced a public offering of approximately €380 million, with new shares to be issued at a discount to Tuesday’s closing price

Kojamo is the the worst performer on the Stoxx 600 Real Estate index after Barclays double-downgraded the shares to underweight on a disappointing occupancy rate recovery

Real estate is overall the worst-performing sector in Europe Wednesday after UK inflation remained higher than expected for a fourth month, stoking bets that interest rates need to keep rising

Pirelli shares fall as much as 2.3% after Oddo BHF downgraded the Italian tiremaker to neutral from outperform, noting that the departure of designated CEO successor Giorgio Bruno is the “last straw”

European delivery companies fall on Wednesday after FedEx gave a 2024 profit outlook below analyst expectations as a drop in package demand offsets the CEO’s $4 billion cost-cutting plan

Earlier in the session, Asian stocks were mixed following the negative handover from Wall Street as participants look ahead to Fed Chair Powell’s testimony in Congress.

Hang Seng and Shanghai Comp. were lower again with Hong Kong underperforming on tech losses and as sentiment in the mainland remained dampened by the weaker outlook with HSBC cutting China’s GDP forecast to 5.3% from 6.3%, while the PBoC’s continued liquidity efforts and the recent US-China rhetoric did little to spur risk appetite.

Australia’s ASX 200 was dragged lower by weakness in the commodity-related sectors and the mood was not helped by the deterioration in the Australian Westpac Leading Index.

Japan’s Nikkei 225 was initially pressured but then clawed back losses with SoftBank among the biggest gainers during its AGM where CEO Son noted that AI is about to grow explosively and the time has come to shift to offence mode, while there were also comments from BoJ’s Adachi who stuck to the dovish script.

Indian stocks jumped to new all-time highs, driven by a rise in HDFC Bank and Housing Development Finance Corp. The S&P BSE Sensex rose 0.3% to close at 63,523.15 in Mumbai, while the NSE Nifty 50 Index advanced 0.2% to 18,856.85. Strong foreign inflows, improving outlook for corporate earnings and one of the fastest economic growth rates among major economies have also buttressed gains in the stock market. “FPI inflows into India in recent months may simply be driven by the top-down excitement of foreign households around India,” Sanjeev Prasad, co-head of institutional equities at Kotak Institutional Equities said in a note. HDFC Bank contributed the most to the Sensex’s gain, increasing 1.7%. Out of 30 shares in the Sensex index, 14 rose, while 16 fell.

In FX, the Bloomberg Dollar spot index is up 0.1%, while the pound fell after erasing early gains on the back of another shock inflation reading. TSDJPY rose as much as 0.5% reversing yesterday’s drop on intervention jawboning, while USDGBP reversed its earlier 0.3% decline to climb as much as 0.5%, as the pound whipsawed after a hotter-than-expected UK inflation print

In rates, treasuries were slightly cheaper across the curve while gilts slide in a sharp bear-flattening move after UK inflation data surprised to the upside. Treasury yields cheaper by 1bp to 2bp across the curve with spreads broadly remaining within 1bp of Tuesday session close; 10-year yields around 3.75% are cheaper by 2bp on the day with gilts underperforming by additional 6bp in the sector. UK benchmark gilt yields climbed six basis points as traders ramped up bets for further Bank of England interest-rate hikes to a level not seen since the turn of the century a day before a policy meeting. UK 2-year yields off cheapest levels of the day, although remain higher by 12.5bp into early US session after latest UK infaltion shock. US session focus will be on Fed Chair Powell’s congressional testimony at 10am New York time, before focus shifts to 20-year bond auction later.

In commodities, crude futures are flat with WTI trading near $71.10. Spot gold is little changed around $1,935. Bitcoin rises 2.6%

Bitcoin is firmer on the day and approaching USD 29,000 to the upside whilst Ethereum rose above USD 1,800 earlier in the session.

To the day ahead now, and one of the main highlights will be Chair Powell’s testimony before the House Financial Services Committee. Over at the Senate Banking Committee, there’ll also be Fed nomination hearings for Governor Jefferson to become Vice Chair, Governor Cook for an additional full term as Governor, and for Adriana Kugler to become a Governor. Alongside that, we’ll hear from the Fed’s Goolsbee, and the ECB’s Schnabel, Nagel and Kazimir. On the data side, we’ll get the UK CPI reading for May.

Market Snapshot

S&P 500 futures little changed at 4,435.50

MXAP down 0.7% to 166.31

MXAPJ down 1.0% to 523.16

Nikkei up 0.6% to 33,575.14

Topix up 0.5% to 2,295.01

Hang Seng Index down 2.0% to 19,218.35

Shanghai Composite down 1.3% to 3,197.90

Sensex up 0.3% to 63,488.37

Australia S&P/ASX 200 down 0.6% to 7,314.91

Kospi down 0.9% to 2,582.63

STOXX Europe 600 little changed at 458.87

German 10Y yield little changed at 2.43%

Euro up 0.1% to $1.0930

Brent Futures down 0.3% to $75.71/bbl

Gold spot down 0.1% to $1,934.11

U.S. Dollar Index little changed at 102.56

Top Overnight News

Chinese policymakers are facing growing calls for economic stimulus, this time from several prominent state media and top government advisers. The country’s three main state-run securities newspapers ran front-page articles Wednesday saying the central bank is likely to ease monetary policy further, citing well-known economists. BBG

China extended tax breaks for consumers buying clean cars through 2027, estimated to be worth 520 billion yuan ($72.3 billion) in the coming four years, in an effort to bolster its flagging electric-vehicle industry. BBG

China said US President Joe Biden had made a “public political provocation” by referring to his Chinese counterpart Xi Jinping as a “dictator,” as fresh tensions flared in bilateral ties just days after meetings to stabilize relations. Chinese Foreign Ministry spokeswoman Mao Ning called the US leader’s comments “irresponsible” at a regular press briefing in Beijing. BBG

BlackRock’s Larry Fink says investors are shifting money out of Chinese equities and into Japanese ones due to rising geopolitical risks between Beijing and the West. Nikkei

Three Federal Reserve nominees (Philip Jefferson, Adriana Kugler, Lisa Cook) said tackling US inflation would be their top priority if confirmed to roles at the central bank. BBG

UK inflation runs hot in May, with the CPI overshooting the Street on headline (+8.7% vs. the St +8.4% and vs. +8.7% in April) and core (+7.1% vs. the Street +6.8% and vs. +6.8% in April), raising pressure on the BOE ahead of the Thurs meeting. FT

Corporate America is feeling the pinch from the slowdown in Wall Street’s $1.4tn market for junk-rated loans, with a growing list of companies forced either to pay more or abandon borrowing plans. Borrowers have been hit by shifts in the market for collateralized loan obligations, or CLOs, the investment vehicles that own roughly two-thirds of lowly rated US corporate loans. FT

Silicon Valley companies are dumping office space at an accelerating pace, as tech leaders such as Google and Facebook parent Meta Platforms close locations and reassess their commitments to the workplace. WSJ

FedEx gave a 2024 profit outlook below analyst expectations as a drop in package demand offsets Chief Executive Officer Raj Subramaniam’s $4 billion cost-cutting plan. BBG

Money-market funds are placing less cash in a Federal Reserve borrowing program, a sign that efforts to replenish government coffers after the debt-ceiling fight aren’t disrupting markets. Instead, funds are likely stepping up to buy more Treasury bills. WSJ

A more detailed look at global markets courtesy of Newsquawk

Asian stocks were mostly subdued following the negative handover from Wall St amid the lack of bullish macro drivers and as participants look ahead to Fed Chair Powell’s testimony in Congress. ASX 200 was dragged lower by weakness in the commodity-related sectors and the mood was not helped by the deterioration in the Australian Westpac Leading Index. Nikkei 225 was initially pressured but then clawed back losses with SoftBank among the biggest gainers during its AGM where CEO Son noted that AI is about to grow explosively and the time has come to shift to offence mode, while there were also comments from BoJ’s Adachi who stuck to the dovish script. Hang Seng and Shanghai Comp. were lower with Hong Kong underperforming on tech losses and as sentiment in the mainland remained dampened by the weaker outlook with HSBC cutting China’s GDP forecast to 5.3% from 6.3%, while the PBoC’s continued liquidity efforts and the recent US-China rhetoric did little to spur risk appetite.

Top Asian News

US President Biden said Chinese President Xi didn’t know where the balloons were and didn’t know a balloon was blown off course. Furthermore, Biden referred to Xi as a dictator and stated that Xi is in a position where he desires a resumption of relations with the US, while Biden also commented that climate envoy John Kerry may travel to China soon, according to Reuters.

EU Summit draft conclusions call on China to engage in global challenges including climate change, biodiversity and debt relief, according to an EU official.

Nasdaq executives plan to visit China this year to restart data partnership talks with companies there about access to economic data desperately sought by Western investors, according to Semafor.

BoJ Governor Ueda says Japan’s economy is picking up; the economy is likely to recover moderately; BoJ will patiently maintain easy monetary policy, according to Reuters.

BoJ Board Member Adachi said inflation is faster than he expected but noted it is too early to tweak easy monetary policy and that their baseline price scenario is bound with uncertainty. Adachi said there are both upside and downside risks to the price outlook and longer-run downside risks appear to be bigger, while he reiterated it is appropriate to continue monetary easing under the YCC framework. Adachi said if the bond market function remains in the current state, then the chance of tweaking YCC in July is low.

BoJ April meeting minutes stated members said it is important to continue with monetary easing and that a few members pointed out that past price increases in commodities and raw materials continued to be passed on to consumer prices with a time lag. BoJ minutes stated that they must support wage moment with easing and wage gains are needed for sustainable inflation goal, while some members said it was appropriate for the Bank to continue with current monetary easing due to the difficulty of assessing the suitability of future wage hikes and developments in inflation expectations.

Japanese PM Kishida said they are to mobilise all policy steps to ensure wage growth; positive moves are emerging in Japan’s economy, according to Reuters.

European bourses trade with little in the way of firm direction with the main macro story of the session thus far coming via UK inflation metrics. US equity futures trade in close proximity to the unchanged mark with the ES holding below the 4450 mark after yesterday’s selling pressure. Equity sectors in Europe have a slight negative bias with Real Estate names lagging peers as UK homebuilders suffer post-UK CPI.

Top European News

The Times’ Shadow MPC voted 6-3 in favour of the BoE raising rates by 50bps this week (vs. market expectations of a 25bps move) in an “aggressive move to fight back against stubbornly high inflation”

UK Chancellor Hunt says will not hesitate in our resolve to support the BoE as it seeks to squeeze inflation out of the economy, according to Reuters.

ECB’s Kazimir said in September a continuation of tightening policy is not certain; does not expect inflation to drop soon, via Reuters.

ECB’s Rehn will apply for leave of absence from the Central Bank if he becomes a presidential candidate, according to Reuters.

FX

DXY is on a firmer footing after finding overnight support at exactly 102.50, with a softer JPY and GBP keeping the index underpinned but a resilient EUR hampering gains.

GBP only knee-jerked higher on the hotter-than-expected CPI before shedding all and more of its gains in what seemed to be a realisation of the adverse economic implications from further and perhaps more aggressive BoE tightening.

Yen is softer as Treasuries retreated and BoJ Board member Adachi stuck to dovish guidance overnight.

Aussie remains top-heavy in the aftermath of not-so hawkish as anticipated RBA minutes yesterday alongside more pronounced Yuan depreciation overnight.

Euro maintains 1.0900+ status with tailwinds from EUR/GBP and EUR/JPY (latter almost matching the new midweek y-t-d peak)

PBoC set USD/CNY mid-point at 7.1795 vs exp. 7.1802 (prev. 7.1596)

Fixed Income

Bunds complete a full recovery from worst levels with the help of strong demand for long-end German issuance.

Gilts saw a remarkable bounce after gapping lower at the open as markets ponder the economic implications of further BoE tightening.

US Treasuries have also regained composure ahead of Fed Chair Powell alongside several other Fed speakers and supply on the calendar.

Commodities

WTI and Brent August futures see sideways trade in crude futures, with gains hampered by the hotter-than-expected UK CPI data ahead of tomorrow’s BoE announcement.

Spot gold consolidates ahead of Fed Chair Powell’s testimony and after the yellow metal’s hefty losses yesterday upon a breach of the 100 DMA.

Base metals are mixed amid the indecisive tone in the market, with copper prices relatively contained.

Russia’s Kremlin said there are no grounds to extend the Black Sea Grain Deal because it’s not being implemented, according to Reuters.

Geopolitics

Russian Defence Ministry says it has thwarted an attempt by Kyiv to launch an attack on the Moscow region with drones; all drones were shot down, according to Tass and Ria.

Russia’s Navy is to receive 2 new nuclear submarines by year-end, according to TASS.

China’s Ministry of Foreign Affairs commented on the US’ Taiwan position in which it stated that the US has distorted its political promise to China.

Shanghai Cyberspace Regulator says they have summoned three companies including Starbucks (SBUX) and Shake Shack (SHAK) for collecting excessive personal information, according to Reuters.

US event calendar

07:00: June MBA Mortgage Applications, prior 7.2%

DB’s Jim Reid concludes the overnight wrap

Tonight I’m going to see the Lion King……… performed by 7-year-olds. It will be a case of “Can you feel the out of tune singing and forgotten lines tonight”. Maisie is Timon the Meerkat and the 5-year-old twins are part of the choir with no evidence that they know many of the words. So like with the ChatGPT webinar there is plenty that can go wrong for our family today. It truly could be the longest day as we hit the summer solstice.

With markets largely taking a “hukana matata” attitude in recent weeks to all that has been thrown at it, some strains have appeared in the last few days. The S&P 500 (-0.47%) saw a moderate decline, with the equal weight index (-0.91%) again under-performing. This was the first back-to-back losses since the last full week of May, which shows the recent momentum. This wasn’t just a catch-up to Monday’s losses, since Europe’s STOXX 600 (-0.59%) lost ground for a second day running as well. These declines were evident across several asset classes, with HY credit and energy commodities seeing moderate losses of their own recheck. In fact, the only assets that managed to hold their ground were a few safe havens like sovereign bonds, with yields on 10yr bunds (-11.2bps) seeing their largest daily decline since April.

Whilst little was driving weaker sentiment over the last 48 hours, news flow should begin to pick up again today. Just after this arrives in your inbox, we’ll see UK inflation which given all the news flow about domestic rates and mortgages of late will be a must watch and could have 2-way spillover effects for global bonds and risk. Last month saw a big upside surprise that was then exacerbated by some very strong employment data, leading investors to ratchet up their expectations of future rate hikes (2yr yields c.+85bps since). For today’s reading, our UK economist is expecting a modest decline in headline inflation to +8.5%, having been at +8.7% in April.

Later on, we’ve got an appearance from Fed Chair Powell in front of the House Financial Services Committee at 15:00 London time, and then an appearance before the Senate Banking Committee tomorrow. That’s part of the regular semi-annual Monetary Policy Report to Congress and follows the FOMC’s decision last week to pause their rate hikes after 10 consecutive increases.

Given that the decision was only a week ago, it’s likely that Powell will stick to his main themes from the press conference. But it’ll be interesting to see how he frames the Fed’s decision last week, as the decision to pause rate hikes came alongside upgrades to their inflation and growth forecasts, as well as a signal in the dot plot that 2 further hikes were expected by December. Powell himself has said that he expects July to be a “live” meeting, and futures are pricing in a 74% chance that the Fed will deliver a hike next month. But there remains scepticism in markets that the Fed will be able to follow through on that second hike, with current terminal pricing only pointing to 23bps more hikes, rather than the 50bps indicated by the dot plot.

Ahead of that testimony, the yield curve grew increasingly inverted, with the 2s10s Treasury curve (-1.5bps) closing at -97bps. That’s the most inverted it’s been since SVB’s collapse, with only 3 days back in early March even more inverted over the last 41 years. There were fresh records set at other points on the curve. For instance, the 1s30s curve inverted to -144bps, which is the most in available data on Bloomberg back to 2002. Aside from the inversions themselves, yields fell in absolute terms across all maturities too, with the US 10yr yield coming down -4.1bps to 3.72%. Overnight, they have pushed back up 2bps to 3.74%.

Those US moves were fairly muted given the previous day’s holiday, but in Europe there was a much sharper decline in yields as they retraced Monday’s moves. That meant that yields on 10yr bunds (-10.6bps), BTPs (-9.1bps) and OATs (-10.8bps) all fell back. And when it came to German sovereign debt specifically, there was a big milestone as the 2s10s curve inverted beyond its low before SVB to -70.2bps, a level we haven’t seen since 1992. Here in the UK, we saw some of the most extreme moves once again, with 10yr gilts (-15.5bps) seeing a sharp move lower after their recent increase.

When it came to equities, as discussed at the top, the day was a negative one, with the S&P 500 down -0.47% despite paring its initial morning fall of almost 1%. The decline was broad-based across the main sector groups, with Energy (-2.29%) seeing the biggest losses amidst commodity price declines, but 21 of the 24 S&P industry groups lost at least some ground on the day. It was much the same story for the Dow Jones index (-0.71%), while the NASDAQ (-0.16%) fared better mostly thanks to Tesla (+5.43%), which gained following news that electric truck manufacturer Rivian would adopt Tesla’s charging standard. And in Europe it was another weakish day, with the STOXX 600 (-0.59%) and the DAX (-0.55%) down for a second consecutive session.

Asian equity markets are largely trading lower this morning, with Chinese related stocks leading losses. The Hang Seng (-1.91%) is sharply down, extending losses for the third consecutive session while the CSI (-0.70%) and the Shanghai Composite (-0.41%) are also sliding as China’s more modest rate cut yesterday is weighing on the sentiment. Elsewhere, the KOSPI (-0.65%) is also trading in the red while the Nikkei (+0.40%) is bucking the trend, reversing its opening losses. Outside of Asia, US stock futures are fluctuating with those on the S&P 500 (-0.03%) and NASDAQ 100 (-0.04%) just below flat. A profit warning from FedEx after the bell hasn’t damaged overall sentiment.

Minutes from the Bank of Japan’s April meeting indicated that several board members agreed that the central bank should continue to keep ultra-low interest rates. The meeting was the first to be held under the leadership of the new BOJ Governor Ueda Kazuo. Otherwise, the minutes revealed that one of the nine board members suggested that the bank should reconsider its policy of keeping bond yields low.

Amidst the negativity yesterday, one bright spot came from the US housing data for May. That showed housing starts leapt up to an annualised rate of 1.631m (vs. 1.4m expected), which is the highest they’ve been in 13 months. Furthermore, the one-month increase of +21.7% was the largest in a single month since October 2016, so these weren’t the sort of moves you regularly see. At the same time, building permits came in at a 7-month high of 1.491m (vs. 1.425m expected). The data adds to signs that the housing market has been stabilising, and on Monday we also saw the NAHB’s housing market index improve for a 6th consecutive month. With housing having been the sector most immediately affected following the initial hiking cycles last year, recent signs of its stabilisation may raise new questions over the transmission of central bank tightening into the economy.

To the day ahead now, and one of the main highlights will be Chair Powell’s testimony before the House Financial Services Committee. Over at the Senate Banking Committee, there’ll also be Fed nomination hearings for Governor Jefferson to become Vice Chair, Governor Cook for an additional full term as Governor, and for Adriana Kugler to become a Governor. Alongside that, we’ll hear from the Fed’s Goolsbee, and the ECB’s Schnabel, Nagel and Kazimir. On the data side, we’ll get the UK CPI reading for May.

2 b) NOW NEWSQUAWK (EUROPE/REPORT)/ASIA REPORT

2 c. ASIAN AFFAIRS/EUROPEAN AFFAIRS

Equities flat, GBP sinks on CPI, JPY falls on dovish BoJ; Fed’s Powell testimony due – Newsquawk US Market Open

WEDNESDAY, JUN 21, 2023 – 06:06 AM

European bourses are indecisive with the main macro story of the session thus far coming via UK inflation metrics.

GBP only knee-jerked higher on the hotter-than-expected CPI before shedding all and more of its gains on economic implications of further BoE tightening.

DXY is firmer pre-Powell whilst the JPY is softer following more dovish BoJ commentary.

US Treasuries have regained composure whilst Bunds saw a full recovery and Gilts trimmed a bulk of opening losses.

Russian Defence Ministry says it has thwarted an attempt by Kyiv to launch an attack on the Moscow region with drones.

Looking ahead, highlights include BoC Minutes, Speeches from Fed’s Powell, Jefferson, Cook, Goolsbee, Mester & ECB’s Schnabel, supply from the US.

DXY is on a firmer footing after finding overnight support at exactly 102.50, with a softer JPY and GBP keeping the index underpinned but a resilient EUR hampering gains.

GBP only knee-jerked higher on the hotter-than-expected CPI before shedding all and more of its gains in what seemed to be a realisation of the adverse economic implications from further and perhaps more aggressive BoE tightening.

Yen is softer as Treasuries retreated and BoJ Board member Adachi stuck to dovish guidance overnight.

Aussie remains top-heavy in the aftermath of not-so hawkish as anticipated RBA minutes yesterday alongside more pronounced Yuan depreciation overnight.

Euro maintains 1.0900+ status with tailwinds from EUR/GBP and EUR/JPY (latter almost matching the new midweek y-t-d peak)

PBoC set USD/CNY mid-point at 7.1795 vs exp. 7.1802 (prev. 7.1596)

WTI and Brent August futures see sideways trade in crude futures, with gains hampered by the hotter-than-expected UK CPI data ahead of tomorrow’s BoE announcement.

Spot gold consolidates ahead of Fed Chair Powell’s testimony and after the yellow metal’s hefty losses yesterday upon a breach of the 100 DMA.

Base metals are mixed amid the indecisive tone in the market, with copper prices relatively contained.

Russia’s Kremlin said there are no grounds to extend the Black Sea Grain Deal because it’s not being implemented, according to Reuters.

Fed Vice Chair nominee Jefferson (voter) said in prepared remarks for the Senate confirmation hearing that he remains focused on returning inflation to 2% and that they must remain attentive to all of inflation, banking-sector stress, and geopolitical uncertainty. Jefferson added that the US banking system is sound and resilient but he remains attuned to any threats to its stability, while he also noted that inflation has started to abate, according to Reuters.

Fed Board nominee Cook (voter) said in prepared remarks for the Senate hearing that she is focused on inflation until the job is done, while she added that the US economy is at a critical juncture and she has consistently supported the Fed’s work to lower inflation.

Fed Board nominee Kugler said in prepared remarks for the Senate confirmation hearing that she is deeply committed to setting monetary policy to reduce inflation and promote maximum employment. Kugler also stated that high inflation hurts workers and businesses alike, while she added it is important to bring inflation down to the Fed’s 2% target.

Amazon (AMZN) says its Prime Day event will be on July 11th and 12th, according to Reuters

NOTABLE EUROPEAN HEADLINES

The Times’ Shadow MPC voted 6-3 in favour of the BoE raising rates by 50bps this week (vs. market expectations of a 25bps move) in an “aggressive move to fight back against stubbornly high inflation”

UK Chancellor Hunt says will not hesitate in our resolve to support the BoE as it seeks to squeeze inflation out of the economy, according to Reuters.

ECB’s Kazimir said in September a continuation of tightening policy is not certain; does not expect inflation to drop soon, via Reuters.

ECB’s Rehn will apply for leave of absence from the Central Bank if he becomes a presidential candidate, according to Reuters.

NOTABLE DATA

UK CPI YY (May) 8.7% vs. Exp. 8.4% (Prev. 8.7%)

UK CPI MM (May) 0.7% vs. Exp. 0.5% (Prev. 1.2%)

UK Core CPI MM (May) 0.8% vs. Exp. 0.6% (Prev. 1.3%)

UK Core CPI YY (May) 7.1% vs. Exp. 6.8% (Prev. 6.8%)

CRYPTO

Bitcoin is firmer on the day and approaching USD 29,000 to the upside whilst Ethereum rose above USD 1,800 earlier in the session.

GEOPOLITICS

Russian Defence Ministry says it has thwarted an attempt by Kyiv to launch an attack on the Moscow region with drones; all drones were shot down, according to Tass and Ria.

Russia’s Navy is to receive 2 new nuclear submarines by year-end, according to TASS.

China’s Ministry of Foreign Affairs commented on the US’ Taiwan position in which it stated that the US has distorted its political promise to China.