JUNE 27//TODAY IS OPTIONS EXPIRY DAY FOR THE COMEX PRECIOUS METALS//GOLD CLOSED DOWN $9.15 TO $1914.30 BUT SILVER CLOSED UP 7 CENTS TO $22.87//PLATINUM CLOSED UP 50 CENTS TO $929.45 WHEREAS PALLADIUM WAS HIT HARD FOR A LOST OF $17.30 TO $1298.15//IMPORTANT READS TODAY: MIKE MAHARREY//2 COMMENTARIES//THE BIG SHOCKER OF THE DAY IS THAT GERMAN AUTHORITIES THINK THAT THE BUNDESBANK MAY NEED A BAILOUT//SWEDEN ABANDONS THE STUPID ENERGY RENEWALS AND GOING FOR NUCLEAR ENERGY//MORE UPDATES ON THE PRIGOZHIN AFFAIR//COVID UPDATES/DR PAUL ALEXANDER/DR PANDA/SLAY NEWS/EWOL NEWS//SWAMP STORIES FOR YOU TONIGHT//

323 H HSBC 2 363 H WELLS FARGO SEC 2 435 H SCOTIA CAPITAL 5 661 C JP MORGAN 5 737 C ADVANTAGE 4 905 C ADM 10

TOTAL: 14 14 MONTH TO DATE: 20,115

JPMorgan stopped 5/14 contracts

FOR JUNE:

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2023. CONTRACT: 14 NOTICES FOR 1400 OZ or 0.0435 TONNES

total notices so far: 20,115 contracts for 2,011,500 oz (62.566 tonnes)

FOR JUNE:

SILVER NOTICES: 429 NOTICE(S) FILED FOR 2,145,000 OZ/

total number of notices filed so far this month : 852 for 4,260,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $9.15

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

/HUGE CHANGES IN GOLD INVENTORY AT THE GLD:////A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD.

INVENTORY RESTS AT 925.65 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 7 CENTS AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 734,000 OZ INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 470.527 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A UBER ATMOSPHERIC SIZED 7492 CONTRACTS TO 134,156 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.44 GAIN IN SILVER PRICING AT THE COMEX ON MONDAY. TAS ISSUANCE WAS A STRONG SIZED 861 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH . CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 861 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE THIS YEAR SET ANOTHER RECORD LOW AT 117,395 CONTRACTS ///MARCH 29.2023. OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.44). AND WERE SUCCESSFUL IN KNOCKING SOME SPEC LONGS AS WE HAD A HUGE LOSS ON OUR TWO EXCHANGES OF 7090CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 13.370MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION. TODAY WE WITNESSED HUGE SPREADER LIQUIDATION ON THE COMEX

WE MUST HAVE HAD:

A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS( 402 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.935 MILLION OZ(FIRST DAY NOTICE) FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP + 0 MILLION OZ EXCHANGE FOR RISK(ISSUED TODAY: TOTAL ISSUED SO FAR: 13.370 MILLION OZ)// TOTAL STANDING FOR THE MONTH 4.270 MILLION OZ + 13.370 MILLION EXCHANGE FOR RISK = 17,640 MILLION OZ// ) // HUGE SIZED COMEX OI LOSS/ FAIR SIZED EFP ISSUANCE/VI) STRONG NUMBER OF T.A.S. CONTRACT ISSUANCE (861CONTRACTS)//HUGE COMEX SPREADER LIQUIDATION//

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –400 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE:

TOTAL CONTRACTS for 17 days, total 20,230 contracts: OR 101.150 MILLION OZ (1190 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 101.150 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 101.150 MILLION OZ//MUCH LARGER THAN LAST MONTH

RESULT: WE HAD A HUMONGOUS SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 7492 CONTRACTS DESPITE OUR GAIN IN PRICE OF $0.44 IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR EFP ISSUANCE CONTRACTS: 402 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.935 MILLION OZ FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP+ 0 MILLION EXCHANGE FOR RISK TODAY + 13.37 MILLION EXCHANGE FOR RISK(PRIOR)//NEW TOTAL STANDING: 17.640 MILLION OZ////// .. WE HAVE A HUGE SIZED LOSS OF7090 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG 861//SOME FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION BUT THE REAL LIQUIDATION TODAY WAS THAT OF COMEX SPREADERS . THE NEW TAS ISSUANCE TODAY (861) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE.

WE HAD 429 NOTICE(S) FILED TODAY FOR 2,145,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 503 CONTRACTS TO 437,216 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED –1727 CONTRACTS

WE HAD A SMALL SIZED DECREASE IN COMEX OI ( 503 CONTRACTS) DESPITE OUR $4.65 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JUNE. AT 70.79 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0.02799 TONNE E.F.P JUMP TO LONDON: NEW TOTAL 64.307 TONNES STANDING SO FAR // + /A SMALL ISSUANCE OF 531 T.A.S. CONTRACTS ////YET ALL OF..THIS HAPPENED WITH A $4.65 GAIN IN PRICEWITH RESPECT TO MONDAY’S TRADING.WE HAD A SMALL SIZED GAIN OF 452 OI CONTRACTS (1.405 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 955 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 437,216

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 452 CONTRACTS WITH 503 CONTRACTS DECREASED AT THE COMEX//TAS CONTRACTS INITIATED (ISSUED): A SMALL 531 CONTRACTS) AND 955 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 452CONTRACTS OR 1.405 TONNES.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (955 CONTRACTS) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (503) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 452 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 70.79 TONNES FOLLOWED BY TODAY’S 900 OZ E.F.P. JUMP TO LONDON //// NEW STANDING FALLS TO 64.307 TONNES// /3) ZERO LONG LIQUIDATION//4) SMALL SIZED COMEX OPEN INTEREST LOSS/ 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: SMALL T.A.S. ISSUANCE: 531 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE :

TOTAL EFP CONTRACTS ISSUED: 41,047 CONTRACTS OR 4,104,700 OZ OR 127.67 TONNES IN 17 TRADING DAY(S) AND THUS AVERAGING: 2414 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAY(S) IN TONNES 127.67 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 127.67/3550 x 100% TONNES 3.57% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 127.67 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY AN ATMOSPHERIC SIZED 7492 CONTRACTS OI TO 134,156AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE SET A NEW RECORD LOW OF 117,395 CONTRACTS MARCH 27/2022

EFP ISSUANCE 402 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 402and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 402 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 7492 CONTRACTS AND ADD TO THE 402OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GIGANTIC SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 7190 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 35.450 MILLION OZ

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED UP 38.42 PTS OR 1.48% //Hang Seng CLOSED UP 354.00 PTS OR 1.88% /The Nikkei closed DOWN 160.48 OR 0.49% //Australia’s all ordinaries CLOSED UP 53 % /Chinese yuan (ONSHORE) closed UP 7.2164 /OFFSHORE CHINESE YUAN UP TO 7.2188 /Oil DOWN TO 68.18 dollars per barrel for WTI and BRENT DOWN AT 72.32 / Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 503 CONTRACTS UP TO 437,216 WITH OUR GAIN IN PRICE OF $4.65 ON MONDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE… THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 955 EFP CONTRACTS WERE ISSUED: : AUGUST 955 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 955 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 452 CONTRACTS IN THAT 955LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED LOSS OF 503 COMEX CONTRACTS..AND THIS SMALL SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $4.65//MONDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS A SMALL 531 CONTRACTS. THROUGHOUT LAST WEEK, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THE HUGE NUMBER OF T.A.S. CONTRACTS INITIATED OVER THE PAST SEVERAL WEEKS SPELLS TROUBLE FOR THE GOLD/SILVER MARKET AS RAIDS WILL SURELY BE UPON US.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (64.307) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.307 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $5.15) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD OUR SMALL GAIN OF 452 CONTRACTS ON OUR TWO EXCHANGES. WE HAD MINOR TAS LIQUIDATION THROUGHOUT THE MONDAY COMEX SESSION . THE TAS ISSUED MONDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 1.405PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE. (70.709 TONNES) FOLLOWED BY TODAY’S 900 OZ E.F.P. JUMP TO LONDON..NEW STANDING FALLS TO 64.307 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $4.65

WE HAD –REMOVED A WHOPPING 1727 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 452 CONTRACTS OR 45200 OZ OR 1.405 TONNES.

Total monthly oz gold served (contracts) so far this month

20,115 notices 2,011,500 OZ 62.566 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

No dealer withdrawals

Customer deposits: 0

total dealer deposits: nil oz

we had 0 customer deposit:

total deposits: nil oz

Withdrawals: 1

i) out of Brinks: 32.151 oz

total 32.151 oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE.

For the front month of JUNE we have an oi of 574 contracts having LOST 37 contracts. We had 28 contracts served on Monday so we LOST 9 contracts or an additional 900 oz will NOT stand for gold at the comex as these guys were EFP’d to London

The next front month after June is the non active delivery month of July. Here, July LOST 173 contracts to stand at 2065 contracts.

AUGUST LOST 2961 contracts DOWN to 352,829 contracts

We had 14 contracts filed for today representing 1400 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 14 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 5 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JUNE /2023. contract month,

we take the total number of notices filed so far for the month (20,115 x 100 oz ), to which we add the difference between the open interest for the front month of JUNE (574 CONTRACT) minus the number of notices served upon today 14 x 100 oz per contract equals 2,067,500 OZ OR 64.307 TONNES the number of TONNES standing in this active month of June.

thus the INITIAL standings for gold for the JUNEcontract month: No of notices filed so far (20,115) x 100 oz + (574) {OI for the front month} minus the number of notices served upon today (14) x 100 oz) which equals 2,067,500 oz standing OR 64.307 TONNES

TOTAL COMEX GOLD STANDING: 64.307 TONNES WHICH IS HUGE FOR AN ACTIVE DELIVERY MONTH.

To calculate the number of silver ounces that will stand for delivery in JUNE. we take the total number of notices filed for the month so far at 852 x 5,000 oz = 4,260,000 oz

to which we add the difference between the open interest for the front month of JUNE(431) and the number of notices served upon today 429 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2023 contract month: 852 (notices served so far) x 5000 oz + OI for the front month of JUNE (431) – number of notices served upon today (429 )x 500 oz of silver standing for the JUNE contract month equates to 4.270 million oz + 2.935 EXCHANGE FOR RISK TODAY + 10.435MILLION OZ EXCHANGE FOR RISK (PRIOR)//NEW TOTAL: 17.640 MILLION OZ STANDING

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

JUNE 27/WITH GOLD DOWN $9.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD./INVENTORY RESTS AT 925.65 TONNES

JUNE 26/WITH GOLD UP $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD/////INVENTORY RESTS AT 927.10 TONNES

JUNE 23/WITH GOLD UP $5.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: WITHDRAWALS OF 4.33 TONNES OF GOLD OVER THE PAST TWO DAYS. /INVENTORY RESTS AT 929.70 TONNES

JUNE 21/WITH GOLD DOWN $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 934.03 TONES

JUNE 20/WITH GOLD DOWN $22.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.03 TONNES

JUNE 16/WITH GOLD UP $0.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.33 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.03 TONNES

JUNE 15/WITH GOLD UP $2.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 929.70 TONNES

JUNE 14/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 931.44 TONNES

JUNE 13/WITH GOLD DOWN $10.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.01 TONNES FORM THE GLD///INVENTORY RESTS AT 931.44

JUNE 12/WITH GOLD DOWN $7.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.65 TONNES

JUNE 9/WITH GOLD DOWN $1.00: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.65 TONNES

JUNE 8/WITH GOLD UP $20.45 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.46 TONNES FROM THE GLD///INVENTORY RESTS AT 934.65 TONNES

JUNE 7 WITH GOLD DOWN $22.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 938.11 TONNES

JUNE 6/WITH GOLD UP $6.90 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 939.56 TONNES

JUNE 5/WITH GOLD UP $5.00 TODAY : NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 938.11 TONNES

JUNE 2/WITH GOLD DOWN $24.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES FROM THE GLD///INVENTORY RESTS AT 938.11 TONNES

JUNE 1/WITH GOLD UP $14.10 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 939.56 TONNES

MAY 31/WITH GOLD UP $5.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 939.56 TONNES

MAY 30/WITH GOLD UP $14.55 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 26/WITH GOLD UP $.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 941.29 TONNES

MAY 25/WITH GOLD DOWN $19.70 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 941.29 TONNES

MAY 24/WITH GOLD DOWN $9.50 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 941.29 TONNES

MAY 23/WITH GOLD $2.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 942.74 TONNES

MAY 22/WITH GOLD DOWN $4.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.83 TONES OF GOLD INTO THE GLD DESPITE THE L0SS IN PRICE//INVENTORY RESTS AT 942.74 TONNES

MAY 19/WITH GOLD UP $22.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 936.96 TONNES

MAY 18/WITH GOLD DOWN $23.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 936.96 TONNES

MAY 17/WITH GOLD DOWN $8.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF .87 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.94 TONNES

MAY 16/WITH GOLD DOWN 28.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.57 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 934,07

MAY 15/WITH GOLD UP $2.85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 937.64 TONNES

MAY 12/WITH GOLD DOWN $.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.89 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 937.84 TONNES

MAY 11/WITH GOLD DOWN $15.15 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 934.95 TONNES

MAY 10/WITH GOLD DOWN $5.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.70 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 934.95 TONNES

GLD INVENTORY: 925.65 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 27/WILVER SILVER UP 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 734,000 OZ INTO THE SLV////INVENTORY RESTS AT 470.527 MILLION OZ

JUNE 26/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 469.793 MILLION OZ.

JUNE 23/WITH SILVER DOWN 9 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A NET DEPOSIT OF 6.61 MILLION OZ INTO THE SLV OVER THESE PAST TWO DAYS//INVENTORY RESTS AT 469.793 MILLION OZ//

JUNE 21/WITH SILVER DOWN $.40 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.784 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 20/WITH SILVER DOWN 89 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 16/WITH SILVER UP 23 CENTS TODAY :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 463.183 MILLION OZ

JUNE 15/WITH SILVER DOWN 17 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.377 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 463.642 MILLION OZ//

JUNE 14/WITH SILVER UP 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 735,000 OZ FROM THE SLV///INVENTORY RESTS AT 465.019 MILLION OZ//

JUNE 13/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.515 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 465.754 MILLION OZ//

JUNE 12/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.269 MILLION OZ//

JUNE 9/WITH SILVER UP 7 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF SILVER TO THE TUNE OF 550,000 OZ//INVENTORY RESTS AT 467.269 MILLION OZ

JUNE 8/WITH SILVER UP $0.63 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 467.819 MILLION OZ/

JUNE 7/WITH SILVER DOWN 17 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.01 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 467.819 MILLION OZ/

JUNE 6/WITH SILVER UP 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.809 MILLION OZ//

JUNE 5/WITH SILVER DOWN $.13 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 266,000 OZ FROM THE SLV////INVENTORY RESTS AT 466.809 MILLION OZ/

JUNE 2/WITH SILVER DOWN 23 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 918,000 OZ FROM THE SLV./INVENTORY RESTS AT 467.015 MILLION OZ/

JUNE 1/WITH SILVER UP 49 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.933 MILLION OZ

MAY 31/WITH SILVER UP 37 CENTS TODAY:SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 367,000 OZ FROM THE SLV////INVENTORY RESTS AT 467.933 MILLION OZ//

MAY 30/WITH SILVER DOWN 9 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 26/WITH SILVER UP $0.44 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.306 MILLION OZ FROM THE SLV//INVENTORY RESTS AT 468.300 MILLION OZ//

MAY 25.WITH SILVER DOWN $0.32 TODAY; SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 276,000 OZ INTO THE SLV////INVENTORY RESTS AT 471.606 MILLION OZ//

MAY 24/WITH SILVER DOWN $.35 TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 23/WITH SILVER DOWN 22 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.801 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 471.330 MILLION OZ//

MAY 22/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ//

MAY 19/WITH SILVER UP 38 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.529 MILLION OZ

MAY 18/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 919,000 OZ FROM THE SLV////INVENTORY RESTS AT 468.529 MILLION OZ/

MAY 17/WITH SILVER DOWN 2 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 469.448 MILLION OZ//

MAY 16/WITH SILVER DOWN 34 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .643 MILLION OZ FROM THE SLV////INVENTORY RESTS AT 469.448 MILLION OZ.

MAY 15/WITH SILVER UP 13 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.091 MILLION OZ/

MAY 12/WITH SILVER DOWN $.26 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 3,123 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 470.091 MILLION OZ./

MAY 11/WITH SILVER DOWN $1.18 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 466.968 MILLION OZ

MAY 10/WITH SILVER DOWN 23 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.286 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 466.968 MILLION OZ//

CLOSING INVENTORY 470.527 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

What Would The Founding Fathers Say About Our National Debt?

As we approach America’s birthday on July 4, it might be a good time to consider what the founding fathers would have thought about this massive indebtedness.

James Madison might have summed it up best when he called a national debt “a national curse.”

I go on the principle that a Public Debt is a Public curse and in a Rep. Govt. a greater than in any other.”

The antifederalist writer Brutus made a similar point, writing.

I can scarcely contemplate a greater calamity that could befall this country, than to be loaded with a debt exceeding their ability ever to discharge.”

Thomas Jefferson said he considered “public debt as the greatest of the dangers to be feared,” and he warned that in order to preserve the people’s independence, “we must not let our rulers load us with perpetual debt.”

He also talked about the urgency of paying off debts, saying it would help preserve peace.

It is incumbent on every generation to pay its own debts as it goes. A principle which, if acted on, would save one half the wars of the world”

Jefferson went on to explain just what would happen if we failed to heed his warning.

If we run into such debts as that we must be taxed in our meat and in our drink, in our necessaries & our comforts, in our labors & our amusements, for our callings and our creeds, as the people of England are, our people, like them, must come to labor 16 hours in the 24 give the earnings of 15 of these to the government for their debts and daily expences; and the 16th being insufficient to afford us bread, we must live, as they now do, on oatmeal & potatoes.”

Benjamin Franklin warned that running into debt gives “to another Power over your Liberty.”

Madison shared Franklin’s view, naming debt among a trio of tools that people with power use to establish tyranny.

Armies, and debts, and taxes are the known instruments for bringing the many under the domination of the few.” [Emphasis added]

In his Farewell Address, George Washington urged the country to use debt sparingly and pay it off as quickly as possible.

As a very important source of strength and security, cherish public credit. One method of preserving it is to use it as sparingly as possible, avoiding occasions of expense by cultivating peace, but remembering also that timely disbursements to prepare for danger frequently prevent much greater disbursements to repel it.”

He made a similar point in his Fifth Annual Message to Congress.

No pecuniary consideration is more urgent than the regular redemption and discharge of the public debt. On none can delay be more injurious or an economy of time more valuable.”

Jefferson gave us a blueprint for how to handle the debt.

I am for a government rigorously frugal and simple, applying all the possible savings of the public revenue to the discharge of the national debt and not for a multiplication of officers & salaries merely to make partizans, & for increasing, by every device, the public debt, on the principle of it’s being a public blessing.” [Emphasis added]

For many in the founding generation, loading future generations with debt was morally unacceptable and something that should be rejected. Washington referred to it as “ungenerously throwing upon posterity the burden which we ourselves ought to bear.”

Jefferson agreed, writing to John Taylor that “the principle of spending money to be paid by posterity, under the name of funding, is but swindling futurity on a large scale.”

A $32 trillion national debt is just another example of how far America has drifted from its founding principles.

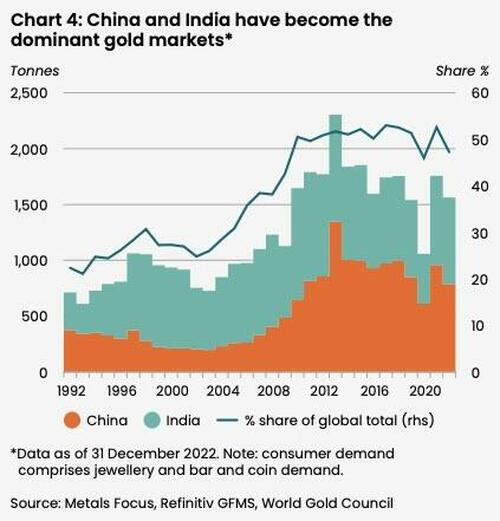

There has been a steady migration of gold from West to East over the last three decades.

When the World Gold Council published its first Gold Demand Trends report 30 years ago, Asian demand made up 45% of the world’s total. Today, the Asian share of global gold demand is approaching 60%.

China and India have driven this migration of gold East. The World Gold Council describes the two countries as “super consumers” of gold. Thirty years ago, China and India accounted for about 20% of annual consumer gold demand. Today, the two countries make up nearly 50% of gold demand.

The Indian gold revolution started in the early to mid-1990s when government policy changes freed up the market. In 1992, gold demand in India accounted for 340 tons. In 2022, that had more than doubled to 742 tons.

India now ranks as the second-largest gold-consuming country in the world behind China.

Gold is not just a luxury in India. Even poor people buy gold in the Asian nation. According to an ICE 360 survey in 2018, one in every two households in India purchased gold within the last five years. Overall, 87% of households in the country own some amount of the yellow metal. Even households at the lowest income levels in India own some gold. According to the survey, more than 75% of families in the bottom 10% had managed to buy gold.

Indians traditionally buy and hold gold. Collectively, Indian households own an estimated 25,000 tons of gold and that number may be higher given the large black market in the country. The yellow metal is interwoven into the country’s marriage ceremonies and cultural rites. Indians also value gold as a store of wealth, especially in poor rural regions. Two-thirds of India’s gold demand comes from these areas, where most people live outside the official tax system.

We’ve seen a similar trajectory in China. The country also has played a significant cultural role in China, but through the last half of the 1900s, Chinese individuals were banned from buying gold. The government eased restrictions in the 1990s, and in 2002, the Shanghai Gold Exchange. Within two years, the market was completely liberalized.

China’s annual gold consumption rose fivefold from just over 375 tons in the early 1990s to a record high of 1,347 tons in 2013. Since then, China has ranked as the world’s largest gold-consuming country.

Economic growth has helped spur demand for gold in the East. As the World Gold Council explained, “This surge in demand was not just an expression of exuberance by Chinese investors free to buy gold. It was also driven by explosive economic growth, rapid urbanization and the desire for a simple alternative to the limited range of investments available domestically. The industry, acknowledging this desire for gold investment products, responded with innovation and speed.”

In other words, rising affluence is intersecting with the East’s traditional affinity for gold.

Turkey, Thailand and Saudi Arabia have also reported increased imports of gold in recent years.

We also see the eastward shift of gold in central bank gold buying. The biggest buyers in recent years have all been in the East. Countries steadily increasing gold reserves include China, India, Turkey, and Singapore.

We saw the migration of gold from West to East on a micro level in late 2022. Many Western investors – particularly at the institutional level – were dumping bullion. Meanwhile, Asian buyers took advantage of lower prices to snap up less expensive jewelry, coins, and bars.

According to a fall 2022 Bloomberg report, “large volumes of metal are being drawn out of vaults in financial centers like New York and heading east to meet demand in Shanghai’s gold market or Istanbul’s Grand Bazaar.”

New York and London vaults reported an exodus of more than 527 tons of gold between April and October 2022, according to data from the CME Group and the London Bullion Market Association. At the same time, gold imports into China hit a four-year high in August 2022.

In the East, many people use gold as their primary form of savings and wealth preservation. An article published by Seeking Alpha summarizes this dynamic.

For millions of people in Asia gold still is the ‘basic form of saving.’ In contrast to the West, where financialization started decades ago, and gold has slowly been removed from people their day-to-day lives. Until a financial crisis emerges, that is. In the West, people own little or no physical gold when they feel financially confident. People in the East have retained a long-term view concerning gold. Their ancestors saved in gold, and so have they been taught. With the knowledge that ultimately, gold doesn’t lose its purchasing power.”

Trying to get gold when a crisis rears its ugly head is a little like trying to get insurance when your house is on fire.

Western investors spurn gold to their own detriment.

Between March 10 and May 1 of this year, three of the largest bank failures in U.S. history occurred.

On March 10 the Federal Deposit Insurance Corporation (FDIC) seized Silicon Valley Bank after $42 billion in deposits had exited the bank the day prior with another $100 billion queued up to leave the next day – meaning it was possible for a federally-insured bank to lose 85 percent of its deposits in the span of 48 hours in the digital age. (For a closer look at what was going on at Silicon Valley Bank, see our report: Silicon Valley Bank Was a Wall Street IPO Pipeline in Drag as a Federally-Insured Bank; FHLB of San Francisco Was Quietly Bailing It Out.)

Two more bank failures followed in short order: Signature Bank on March 12 and First Republic Bank on May 1. Both banks were experiencing bank runs as a result of a loss of confidence by their customers.

First Republic Bank, Silicon Valley Bank, and Signature Bank were the second, third and fourth largest bank failures in U.S. history, respectively. (The largest failure was Washington Mutual during the financial crisis of 2008.)

The Fed’s answer to this crisis of confidence was to allow JPMorgan Chase, officially the riskiest U.S. bank with a string of felonies, to buy the failed First Republic Bank. At the time, First Republic was the 14th largest bank in the U.S. and JPMorgan Chase was the number 1 largest bank with $3.3 trillion in consolidated assets. (Is there any logic, whatsoever, in allowing the riskiest bank in the United States to get even larger? The only possible explanation is regulatory capture.)

So here we are today. The banking crisis has pretty much disappeared from the headlines but the smoldering remnants of the crisis are very much still with us.

The Federal Reserve has released a listing of the largest banks in the United States by assets as of March 31, 2023. We decided to check to see how much the 15 largest banks by assets have lost in market value in the past year and a half – from their closing price on December 31, 2021 to their closing price yesterday, June 26, 2023.

Per the chart above, among the 15 largest banks, the following five banks have performed the worst in terms of share price declines since December 31, 2021: Truist Bank (ticker TFC), Citizens Bank (CFG), U.S. Bank (USB), PNC Bank (PNC), and Bank of America (ticker BAC).

Bank of America is the second largest bank in the United States with $2.5 trillion in consolidated assets and 3,804 domestic bank branches. It has lost 37 percent of its market value (market capitalization) in a year and a half.

But by far, the worst performer in the above group is Truist Bank – a name that grew out of the merger of SunTrust and BB&T banks in 2019. Truist Bank has lost 49 percent of its market value in a year and a half.

As of March 31, Truist was the sixth largest bank in the United States with consolidated assets of $565 billion and a whopping 2,006 branches. According to its regulatory filing of March 31, it held a total of $416.9 billion in deposits, of which $176 billion were uninsured deposits, or 42 percent.

Uninsured deposits, those exceeding the FDIC’s $250,000 insurance cap per depositor/per bank, were one of the key problems in the run on the banks earlier this year.

As we reported in January, in the past decade and a half, the Fed has rarely seen a bank merger it couldn’t wrap its arms around. (See In 16 Years, the Fed Has Approved 4,506 Bank Mergers and Denied One.) But there was one regulator’s voice that did speak out boldly regarding the SunTrust and BB&T merger in 2019.

At the time, Martin Gruenberg was a member of the Board of Directors of the FDIC. (Today, he is the Chairman of the FDIC.) This is a portion of his stated concerns on the merger that created today’s Truist:

“Based on September 30, 2019 Call Report data, BB&T and SunTrust together hold approximately $150 billion in deposits in excess of the deposit insurance limit. The combined institution is expected to hold approximately $331 billion in deposits, indicating that about 45 percent of the deposits would be uninsured. In addition, the combined institution is expected to have over 14 million deposit accounts based on recent Call Report data from the individual institutions.

“Total assets of the combined institution are expected to be about $450 billion. The individual institutions each report some long-term unsecured debt, which if combined would amount to approximately 3.6 percent of total assets at the time of the merger.

“In the event of failure of the merged institution, the universe of potential acquirers would be quite limited for an institution of this size. It is likely that only a Global Systemically Important Bank, or GSIB, would have the capacity to make such an acquisition. Even then, based on the experiences in the financial crisis, interest in, and support for, such acquisitions may be limited among the GSIBs. Absent a viable purchase and assumption bid, the FDIC would likely have to establish a bridge bank to manage an orderly failure of the institution.

“The large branch network, substantial IT systems, and millions of account holders would make the management of a bridge bank a significant operational challenge. The volume of accounts, combined with the estimates of uninsured deposits, would also pose a challenge to an orderly resolution with a rapid deposit insurance determination over the course of a weekend.”

There was also this from Gruenberg:

“Given the limited availability of potential acquirers if the merged institution were to fail, the heavy reliance on uninsured depositors, and the lack of an unsecured debt requirement, the failure could well pose a ‘risk to the stability of the United States banking or financial systems.’ ”

Despite these grave warnings, the merger went through.

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS/TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2164

OFFSHORE YUAN: DOWN TO 7.2188

SHANGHAI CLOSED UP 38.82 PTS OR 1.23%

HANG SENG CLOSED UP 354.00 PTS OR 1.88%

2. Nikkei closed DOWN 160.48 PTS OR 0.49%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 102.19 EURO RISES TO 1.0947 UP 37 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.371 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 143.62/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ON SHORE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.297***/Italian 10 Yr bond yield RISES to 3.935*** /SPAIN 10 YR BOND YIELD RISES TO 3.272…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 3.498

3j Gold at $1924.50 silver at: 22.87 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 1 /100 roubles/dollar; ROUBLE AT 85.09//

3m oil into the 68 dollar handle for WTI and 72 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 143.62// 10 YEAR YIELD AFTER BREAKING .54%, RISES TO .371% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8943 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9789 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.721 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 3.810 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.679 UP 0 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.04…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.3515 UP 5 BASIS PTS

end

2. Overnight: Newsquawk and Zero hedge:

Futures Rally Fizzles After Lagarde Dashes Hopes Of End To ECB Rate Hikes

TUESDAY, JUN 27, 2023 – 08:22 AM

After starting off strong, US equity futures have again faded a modest attempt to rally, and are back to unchanged as they revert to the declining trendline from the 2023 high hit on June 16 but followed by the worst week since March amid rising recession fears. At 7:45am ET, S&P futures were just barely in the green. Nasdaq 100 futures added 0.4%, as traders positioned for a rebound after the tech benchmark sank 1.4% on Monday.

In Europe, the Stoxx 600 Index also ceded its opening gains after ECB President Christine Lagarde dashed hopes of an imminent end to the interest-rate hiking cycle in her opening remarks to the ECB retreat in Sintra; global equity markets are attempting to shake off recent weakness amid renewed expectations for China stimulus which helped push HK/Mainland stocks higher after Premier Li reiterated the 5% GDP target remains on track. This optimism is pushing base metals higher ex-copper; the moves are aided by a slightly weaker USD while 10-year Treasury bond yields rose; crude dropped more than 1% and copper followed. Today, we have a 5Y bond auction which JPM says should be well digest given yield levels. IMF’s Gopinath says central banks may need to tolerate higher inflation to avoid financial crises, indicating once again that the Fed will inevitably have to raise its inflation target. Today’s macro data focus includes Durable/Cap Goods, Home Price data, regional Fed mfg indicators, and Consumer Confidence.

In premarket trading, Tesla shares rebounded by 1.7% after the electric-vehicle maker slid over 6% Monday following a downgrade from Goldman Sachs on a difficult pricing environment; Advanced Micro Devices and Meta Platforms advanced. Here are some other notable premarket movers:

Lordstown Motors more than halved after the electric-vehicle maker, once hailed by former US President Donald Trump for saving automaking jobs, filed for bankruptcy.

Snowflake shares rise as much as 4.4% in US premarket trading, set to reverse the previous session’s losses, after the software company announced an AI-related partnership with Nvidia.

US-listed Chinese stocks rise in premarket trading, set to bounce back from recent declines as Beijing regulators firm up control over Chinese markets. Alibaba (BABA US) rises 1.8%, Baidu (BIDU US) +1.7%.

American Equity shares surged 9.5% in postmarket trading after Bloomberg News reported that Canadian investment giant Brookfield has made a cash and stock offer that’s set to be recommended by the insurer’s board.

Applied Digital Corp. fell 4.5% postmarket after the datacenter designer and operator posted preliminary fiscal 4Q revenue that fell shy of estimates.

Markets are coming to terms with the view that the Federal Reserve won’t cut interest rates this year and other central banks will continue raising rates to quell inflation. Morgan Stanley economists said in research note on Tuesday that they see the Fed hiking by 25 basis points next month. On the positive side, there’s also growing speculation among investors that any recession may be shallow and less damaging to earnings than expected.

“Growth has held up well thus far,” said Mark Dowding, chief investment officer at BlueBay Asset Management. “With central banks nearing the end of their rate hiking cycles, this has fed hopes of a relatively soft landing in economic terms, without a more severe recession.”

Earlier in the session, Asian stocks were mostly positive as the risk tone improved following a weak US session, encouraged by a fresh round of China stimulus hopes.

Hang Seng and Shanghai Comp were firmer with Hong Kong led by gains in tech and property after the PBoC’s continued liquidity efforts, while Premier Li pledged to roll out effective policy measures during his speech at the WEF in Tianjin and it was also reported that US Treasury Secretary Yellen is planning a trip to China in July.

ASX 200 gained as strength in financials and cyclicals picked up the slack from the losses in tech and telecoms.

Nikkei 225 was pressured in a continued pullback from the 33,000 level amid increasing speculation that the recent currency weakness could force the BoJ’s hand regarding YCC.

In Europe, the Stoxx 600 Index dipped 0.1%, marking a seventh day of declines and the longest losing streak since February 2018. Among individual stock movers, Amsterdam-listed Prosus NV jumped 6% after winning regulatory approval to remove its cross-holding structure with Naspers Ltd. Volkswagen AG dragged autos stocks down following a report that it’s planning to cut back production of one of its electric SUV models due to weak sales.

Lenders were the best performing sector in Europe as ECB officials reiterated their view that interest rates hikes will continue. ECB President Christine Lagarde said the central bank probably won’t be able to declare the end of its historic cycle of interest- rate increases anytime soon and reiterated plan for another hike at the next meeting in July. Lagarde speech kicked off annual ECB retreat in Sintra, Portugal. The Stoxx 600 Banks Index was 0.5% higher as of 11:20am in London vs a 0.2% decline in the Stoxx 600 Index. Santander +2.8%, CaixaBank +2.5%, Banco BPM, +1.5%, Commerzbank +1.5%. Here are some other notable European movers:

Wise rises as much as 21% after after the money-transfer firm boosted its 2024 outlook. It is the strongest stock on the Stoxx 600 on Tuesday, with the shares turning positive year-to- date.

Prosus gains as much as 10% in Amsterdam after the tech investor and its parent Naspers said they received South African approval to remove their cross-holding structure.

Telecom Plus rises as much as 13% after the multi-utilities firm’s full-year results, with Peel Hunt describing the update as “reassuring and encouraging,” saying FY23 has been “stellar.”

SES-imagotag climbs as much as 21%, on course for a second session of recovery, as the French company seeks to reassure investors after Friday’s critical short-seller report.

Carnival rises as much as 7.3% in London, recovering part of the previous day’s slump, after Morgan Stanley raised its price target. The stock fell 12% on Monday after disappointing 2Q results.

JD Sports drops as much as 6.4% to the lowest in more than five months after the sportswear retailer gave a trading update. Peel Hunt says the US market slowed more than expected in 2Q.

Fresenius Medical Care drops as much as 5.1% after a proposal for US medicare payments for dialysis payments disappointed analysts. Separately-listed parent company Fresenius SE falls as much as 2%.

Volkswagen drops as much as 3% after newspaper Nordwest-Zeitung reported that the carmaker will cut back production of the electric ID.4 compact SUV and ID.7 at its factory in Emden, Germany.

Xior falls as much as 7.4% after shareholder ESHF offered shares worth €25.5 million in the student-housing operator at an around 8% discount to their last close. JPMorgan priced the deal.

Persimmon falls as much as 2% as Barclays (equalweight) says consensus earnings estimates for the UK’s largest listed homebuilder no longer look as conservative as previously thought.

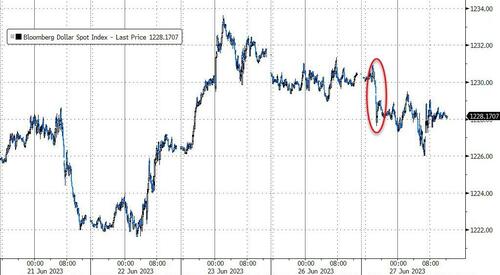

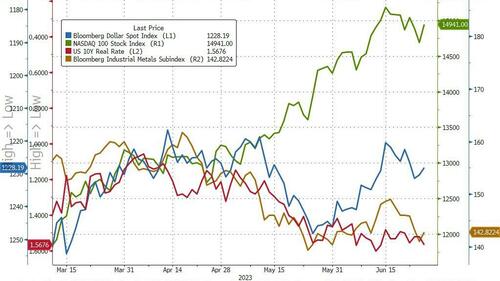

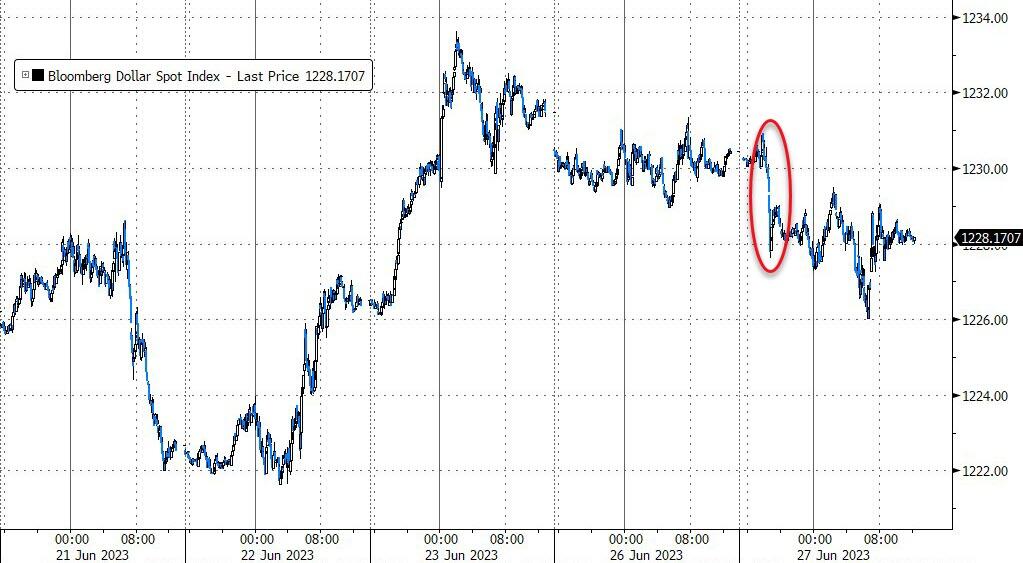

In FX, the euro is sitting atop the intraday G10 rankings, rising 0.2% versus the greenback following Lagarde’s hawkish comments. The Bloomberg Dollar Spot Index is down 0.1%. AUD/USD leads gains rising as much as 0.7%. USD/JPY falls 0.2% as investors mull future yen intervention potential.

In rates, Treasuries are lower with the US 10-year yield adding 1bps to 3.73%. The long-end of the curve underperforms, pushing 5s30s spread toward steepest levels of the day into early US session. Bigger losses hit gilts, where front-end and belly yields are cheaper by more than 3bp on the day. US session has busy economic data slate and a 5-year note auction, following strong reception for Monday’s 2-year sale. Treasury yields are cheaper by ~1.5bp across long-end of the curve with 5s30s spread steeper by 0.5bp on the day; 10-year yields around 3.73% with gilts trading 2.5bp cheaper vs Treasuries in the sector. 2-year treasury yields rise two basis points to 4.67% after yesterday’s auction narrowly missed being the most expensive since 2007. Longer-dated treasuries remain little changed; focus turns to the five-year note auction later Tuesday. US auction cycle continues with $43 billion 5- year notes at 1pm, and concludes with $35 billion 7-year notes Wednesday; Monday’s 2-year note auction stopped 0.8bp through the WI yield in a strong reception.

In commodities, crude futures decline with WTI falling 0.6% to trade near $68.95. Spot gold is little changed around $1,925. Bitcoin rises 0.7%.

To the day ahead now, and US data releases include the Conference Board’s consumer confidence for June, the preliminary reading of durable goods orders for May, new home sales for May, the Richmond Fed’s manufacturing index for June, and the FHFA’s house price index for April. Elsewhere, we’ll get the Canadian CPI reading for May, and Italian consumer confidence for June. Otherwise from central banks, we’ll hear from ECB President Lagarde, as well as the BoE’s Dhingra and Tenreyro.

Market Snapshot

S&P 500 futures up 0.2% to 4,379.25

MXAP up 0.4% to 163.13

MXAPJ up 0.7% to 515.99

Nikkei down 0.5% to 32,538.33

Topix down 0.3% to 2,253.81

Hang Seng Index up 1.9% to 19,148.13

Shanghai Composite up 1.2% to 3,189.44

Sensex up 0.4% to 63,213.14

Australia S&P/ASX 200 up 0.6% to 7,118.21

Kospi little changed at 2,581.39

STOXX Europe 600 little changed at 452.59

German 10Y yield little changed at 2.32%

Euro up 0.3% to $1.0940

Brent Futures up 0.7% to $74.69/bbl

Gold spot up 0.1% to $1,925.27

U.S. Dollar Index down 0.14% to 102.54

Top Overnight News

China’s Premier said the country would take steps to boost the economy while Q2 GDP will be higher than Q1, with the country on track to achieve its full-year growth target of around 5%. RTRS

China cracks down on market commentators it feels are speaking too negatively about the country’s financial prospects. FT

US Treasury Secretary Janet Yellen plans to visit Beijing in early July for the first high-level economic talks with her new Chinese counterpart, people familiar with the scheduling said. BBG

ECB’s Lagarde warns that inflation remains too high and persistent, which will require further policy tightening in response (another hike is coming in July, and “it is unlikely that in the near future the central bank will be able to state with full confidence that the peak rates have been reached”), although she acknowledges that price pressures are starting to ease. ECB

UK food price inflation cools to +14.6% in June (vs. +15.4% in May and +15.7% in April) while overall shop price inflation also eased. London Times

IMF warns countries may need to tolerate a period of inflation above their 2% targets in order to avoid a financial crisis. FT

Western powers are considering contingencies in case Putin’s grip on power is compromised to such a degree that the country’s nuclear weapons are compromised. FT

Russia closed a criminal probe into Yevgeny Prigozhin and his Wagner group for mutiny, and preparations have begun to transfer heavy weaponry to Russian army units, Interfax reported. Prigozhin’s jet reportedly landed in Belarus, though it’s not clear if he was on board. BBG

Lordstown filed for bankruptcy and sued Foxconn after the EV startup’s $170 million investment deal with the Taiwanese firm unraveled. It listed as much as $500 million of assets and liabilities, and accused Foxconn of fraud and breach of contract. BBG

One of the questions we hear most frequently from clients is ‘where are we in the cycle’? Of course, no two cycles are the same given that their drivers, and the structural factors that influence them, can vary significantly between one cycle and another. That said, we find that most cycles go through four phases, starting with ‘Despair’ (a bear market) and followed by ‘Hope’ – the strongest and shortest phase, where markets and valuations rise in anticipation of a future profit growth recovery. Next, there is usually a ‘Growth’ phase, where profits recover and grow but valuations fall back and returns moderate. The final phase, which we describe as ‘Optimism’, is generally associated with increasing valuations even as interest rates rise. GIR

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mostly positive as the risk tone improved following the predominantly negative handover from the US where the major indices were subdued heading into quarter-end and the Nasdaq underperformed amid weakness in tech and communications. ASX 200 gained as strength in financials and cyclicals picked up the slack from the losses in tech and telecoms. Nikkei 225 was pressured in a continued pullback from the 33,000 level amid increasing speculation that the recent currency weakness could force the BoJ’s hand regarding YCC. Hang Seng and Shanghai Comp were firmer with Hong Kong led by gains in tech and property after the PBoC’s continued liquidity efforts, while Premier Li pledged to roll out effective policy measures during his speech at the WEF in Tianjin and it was also reported that US Treasury Secretary Yellen is planning a trip to China in July

Top Asian News

PBoC set USD/CNY mid-point at 7.2098 vs exp. 7.2194 (prev. 7.2056)

China state banks were spotted selling dollars in offshore currency markets to prop up the yuan, according to sources cited by Reuters.

Chinese Premier Li said the pandemic will be over and both visible and invisible barriers will disappear, while he added that countries should strengthen dialogue and communications to avoid misunderstanding with no country able to resolve all problems and unity is the right answer. Premier Li also commented that China will continue to provide a strong driving force for the global economy and roll out more effective policy measures to expand domestic demand and opening up. Furthermore, Li stated that Q2 economic growth will be higher than Q1 growth and China is expected to achieve its growth target of around 5% for 2023, according to Reuters.

Chinese Premier Li said we will support the development of foreign companies in China; will not abuse security checks on foreign firms, according to Reuters.

Chinese Premier Li said China will improve government procurement policies on medicines, according to Reuters.

US Treasury Secretary Yellen reportedly plans a China trip in July to speak with her Chinese counterpart while the US prepares investment curbs, according to Bloomberg.

New Zealand Finance Minister Robertson said the RBNZ Monetary Policy Committee Remit and Charter were renewed with only minor changes to the monetary policy framework, while he added that the MPC is now required to ‘achieve and maintain’ rather than ‘keep’ inflation between 1%-3% and the MPC should communicate key considerations of its decisions with regard to financial risks.

European bourses have been edging lower throughout the morning despite the enthusiasm seen ahead of the cash open, with the ECB Sintra Forum underway. US equity futures are seeing modest gains with the NQ attempting to recoup some of its tech-driven losses on Monday. Equity sectors in Europe are mixed with Banks top of the leaderboard whilst Autos and Parts lag.

Top European News

FX

DXY is on a softer footing intraday with the range on either side of 102.50, whilst prelim rebalancing models tilt Dollar-negative.

EUR now stands as the modest outperformer amid more hawkish-leaning ECB commentary.

CNH is firmer amid a stronger-than-expected PBoC Yuan fixing overnight alongside reports that Chinese state banks were said to be selling USD/CNH.

Antipodeans initially outperformed amid Chinese optimism before waning alongside risk sentiment.

Credit Agricole on month-end rebalancing: flows are likely to be mild USD selling across the board with the strongest sell signal in the case of the USD vs the SEK.

Citi’s prelim Month-end FX rebalancing: expectations Dollar negative. The model suggests FX rebalancing needs are tilted toward USD selling. Hedge and asset FX rebalancing needs are coinciding Negative US equity rebalancing flow estimated to dominate equity rebalancing.

Fixed Income

Debt futures have extended their pull-back from yesterday’s best levels to deeper lows.

Bunds initially experienced some impetus from a lower German Q3 refunding remit before ECB President Lagarde stressed that the war against inflation is still not over.

Gilts were unfazed by a solid DMO linker sale.

BTPs remain below par as they weigh up decent demand for short-dated Italian issuance.

T-note also nudged up to the top end of its intraday parameter at one point before trimming gains, with the contract contained to a tight range.

Commodities

WTI and Brent contracts have given up the mild gains seen in early European hours alongside a deterioration in risk sentiment.

Spot gold as been constrained to a tight range amidst a light European data calendar but a busy speakers slate.

Base metals relinquished most of their mild APAC gains which emanated from the aforementioned economic commentary from Chinese Premier Li, with prices recently hit amid a turn in the risk sentiment.

Central Banks

ECB’s Lagarde said “We have made significant progress but – faced with a more persistent inflation process – we cannot waver, and we cannot declare victory yet”. “Inflation in the euro area is too high and is set to remain so for too long”. “We have not yet seen the full impact of the cumulative rate hikes we have decided on since last July.” “Barring a material change to the outlook, we will continue to increase rates in July.” “…it is unlikely that in the near future the central bank will be able to state with full confidence that the peak rates have been reached”, according to the ECB.

ECB’s Kazaks said market bets on rate cuts in early 2024 are wrong; sees rate hikes past July, “but when and by how much will be data dependent”, according to Reuters. ECB’s Kazaks said further rate hikes are necessary to tame inflation, and the risk of doing too little is bigger than the risk of doing too much, via CNBC. He added he cannot say at the moment how high rates will go and markets are making a mistake in predicting rate cuts.

ECB’s Simkus said we shouldn’t rule out the option of a September hike, according to Bloomberg

BoE’s Dhingra said the external shock has not totally worn off; Wages are responding to inflation with a lag; Medium-term economic forecasts are not good at picking up turning points, according to Reuters.

Morgan Stanley now expects Fed to deliver a 25bps rate hike in July, taking the terminal rate to 5.375% (prev. 5.1%), according to Reuters.

Geopolitics

Russia’s Kremlin said it sees no grounds right now to launch peace talks with Ukraine over Russia’s “special military operation”, according to Reuters.

Belarusian President said all orders were given to the army to remain on full combat readiness; our country has the necessary capabilities to the Western threat, according to Sky News Arabia.

Belarusian border guards monitor daily provocations on the borders with NATO countries, according to Belarusian President cited by Al Jazeera. Lukashenko added that if Russia falls, we will all fall, according to Al Arabiya.

Taiwanese Deputy Chief of Staff says we will destroy China’s ships and planes that are approaching 22 km from the island, according to Al Arabiya.

d

Economic Data

08:30: May Durable Goods Orders, est. -0.8%, prior 1.1%

Durables -Less Transportation, est. 0%, prior -0.3%

May Cap Goods Ship Nondef Ex Air, est. 0.2%, prior 0.5%

May Cap Goods Orders Nondef Ex Air, est. 0%, prior 1.3%

09:00: April S&P CS Composite-20 YoY, est. -2.60%, prior -1.15%

April S&P/CS 20 City MoM SA, est. 0.35%, prior 0.45%

10:00: June Conf. Board Consumer Confidenc, est. 103.9, prior 102.3

June Conf. Board Expectations, prior 71.5

June Conf. Board Present Situation, prior 148.6

10:00: June Richmond Fed Index, est. -12, prior -15

10:00: May New Home Sales MoM, est. -1.2%, prior 4.1%

May New Home Sales, est. 675,000, prior 683,000

10:30: June Dallas Fed Services Activity, prior -17.3

DB’s Jim Reid concludes the overnight wrap

If you’re reading this in the UK, and large parts of Europe, this might be the first day in a few weeks that you’re not waking up feeling like you’ve slept in a sauna. Never has a drop in temperature and a touch of wind been so well received. On Sunday evening we had a rare 5 minutes of rain and I took my glasses off and sat outside in it and soaked in every drop.

Talking of the seasons, this morning we’re launching our summer survey aimed at market participants (link here). The survey will be open until Thursday and all responses are anonymous. In this edition, we’re interested in your thoughts on when the next US recession will occur, and how severe that might be. We’re also curious if you think central banks are making a policy error, and if so whether they’re being too dovish or hawkish. Finally, we have several questions on ChatGPT and the impact of AI on markets and economies. So do you think this is a short-lived fad or a game-changer for human productivity. All responses very much appreciated.

Of course, the biggest international news right now has come from Russia, but when it came to global markets over the last 24 hours, there weren’t many implications outside of a few specific assets. For example, European natural gas prices initially saw a strong uptick at the open of more than +13%, but more than reversed this gain by the end of the session to close -3.0% lower. Oil prices similarly posted initial gains, and after an up-and-down day, ended closing slightly higher, with Brent crude up +0.5% from its levels on Friday. Prices of wheat (for which Russia is a big exporter) had been on course to close at a 4-month high, but ended up closing -1.24% lower.

To be honest, one of the few areas where the impact was clearly obvious was for Russian assets themselves. The country’s equity indices, which these days are largely separated from international markets, underperformed but even they recovered from their initial losses, with the MOEX Russia index shedding -1.92% at its intraday low, before partially recovering to close -1.36% lower. The Russian ruble also lost a bit of ground, but had likewise recovered by the end of the session and was only -0.04% weaker against the US Dollar (in the offshore market). Conversely, investors became a lot more optimistic about Ukraine’s economic prospects yesterday. It’s worth noting that these are pretty illiquid markets, but the country’s GDP-linked dollar bond due in 2041 hit its highest level since Russia’s invasion began.

The aftermath of the dramatic weekend events in Russia continued to draw headlines. We heard from both President Putin and Wagner group’s Prigozhin for the first time since Saturday night’s apparent compromise, but there was little new in these comments. Putin decried the “mutiny” but said that Wagner group fighters “who did not shed blood” could “sign a contract with the Defence Ministry or move to Belarus”, while Wagner’s Prigozhin denied that Wagner’s “march for justice” was ever aimed at regime change. So plenty of head scratching as to the motivation for the actions and the wider implications. Our EM strategists yesterday published a note outlining their initial takeaways on the weekend’s developments here.

Away from Russia, markets generally had a risk-off tone yesterday as fears continued to rise about a potential recession. In fact, the classic leading indicator, namely the 2s10s yield curve inverted a further -1.2bps to -102.7bps, which is just shy of the -108.7bps level right before SVB collapsed. Indeed, if that level is breached over the coming days, then the curve would be more inverted than at any time since 1981, back when Paul Volcker was Fed Chair and holding rates at very restrictive levels. This flattening was evident across the curve, and the 1s30s curve (-1.4bps) is now at its most inverted since available data begins in 2002, having now reached -148.9bps.

Those fears about a recession were given support by several factors. One was the latest Ifo business climate indicator from Germany, which fell to 88.5 in June (vs. 90.7 expected). That’s the second consecutive decline in that indicator, and now leaves it at its lowest level since November last year. In addition, the expectations component fell to 83.6 from 88.3 in May, which is the largest one-month decline in 11 months, and further adds to the picture that last month’s decline wasn’t just a blip. This backdrop meant that sovereign bonds put in a strong performance in Europe with 10yr bunds (-4.4bps), OATs (-3.9bps) and BTPs (-2.9bps) rallying, although a partial sell-off later in the day saw yields on 10yr Treasuries down by a more modest -1.4bps to 3.721%.

Given the general risk-off tone, equities struggled to gain traction, and the S&P 500 (-0.45%) and the STOXX 600 (-0.10%) both posted declines. Tech stocks also continued to slip, with the NASDAQ (-1.16%) and the FANG+ index (-2.98%) both falling to a 2-week low and with the latter seeing its sharpest daily fall since February. The FANG+ decline came as all 10 stocks were lower with Tesla down -6.0% and Nvidia down -3.7%. On the other hand, small-cap stocks were one of the outperformers, and the Russell 2000 (+0.09%) eked out a gain after a run of 5 consecutive declines. With the pullback in equities the VIX index rose 0.8pts to over 14.0 once again, but at that same time EURUSD vol was still subdued as the currency pair traded in just a 32pips range yesterday. That is the tightest range of the year, with the last day of such little volatility coming back in November 2021.

Asian equity markets are mixed this morning. As I check my screens, the Hang Seng (+1.53%) is sharply higher, rebounding from a five-day losing streak while mainland Chinese stocks are also in the green with the Shanghai Composite (+0.93%) and the CSI (+0.52%) moving higher. Otherwise, the Nikkei (-0.77%) is extending its losses for a third consecutive session with the KOSPI (-0.36%) also lower at the moment. Outside of Asia, US stock futures are shrugging off overnight weakness with those on the S&P 500 (+0.23%) and NASDAQ 100 (+0.19%) trading modestly higher.

Early this morning China’s Premier Li Qiang stated that the nation is still on course to reach its growth target of around 5% for 2023, set by the administration earlier this year while highlighting that Q2 growth is expected to be faster than it was in the first quarter.

In FX, the People’s Bank of China (PBOC) stepped up its efforts to slow the slide in the yuan after the central bank set the daily fixing stronger than market expectations for the second day in a row. The move is the PBOC’s biggest upward deviation that the central bank has made since May when the current selloff began. As we go to press, the onshore yuan (+0.35%) is trading at 7.215 versus the dollar.

To the day ahead now, and US data releases include the Conference Board’s consumer confidence for June, the preliminary reading of durable goods orders for May, new home sales for May, the Richmond Fed’s manufacturing index for June, and the FHFA’s house price index for April. Elsewhere, we’ll get the Canadian CPI reading for May, and Italian consumer confidence for June. Otherwise from central banks, we’ll hear from ECB President Lagarde, as well as the BoE’s Dhingra and Tenreyro.

end

2 b) NOW NEWSQUAWK (EUROPE/REPORT)/ASIA REPORT

European bourses choppy and EUR boosted amid hawkish vibes at ECB Sintra – Newsquawk US Market Open

TUESDAY, JUN 27, 2023 – 05:45 AM

European bourses have been edging lower throughout the morning despite the enthusiasm seen ahead of the cash open, with the ECB Sintra Forum underway.

DXY is on a softer footing intraday with the range on either side of 102.50, whilst prelim rebalancing models tilt Dollar-negative.

Debt futures have extended their pull-back from yesterday’s best levels to deeper lows.

WTI and Brent futures have given up the mild gains seen in early European hours alongside a deterioration in risk sentiment.

Overnight, Chinese state banks were spotted selling dollars in offshore currency markets to prop up the yuan, according to sources cited by Reuters.

Looking ahead, highlights include US Durable Goods, Consumer Confidence, New Home Sales-Units, Canadian CPI, and supply from US.

DXY is on a softer footing intraday with the range on either side of 102.50, whilst prelim rebalancing models tilt Dollar-negative.

EUR now stands as the modest outperformer amid more hawkish-leaning ECB commentary.

CNH is firmer amid a stronger-than-expected PBoC Yuan fixing overnight alongside reports that Chinese state banks were said to be selling USD/CNH.

Antipodeans initially outperformed amid Chinese optimism before waning alongside risk sentiment.

Credit Agricole on month-end rebalancing: flows are likely to be mild USD selling across the board with the strongest sell signal in the case of the USD vs the SEK.