GOLD PRICE CLOSED: UP $6.15 TO $1931.55

SILVER PRICE CLOSED: DOWN $0.05 AT $23.08

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1931.95

Silver ACCESS CLOSE: 23.10

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

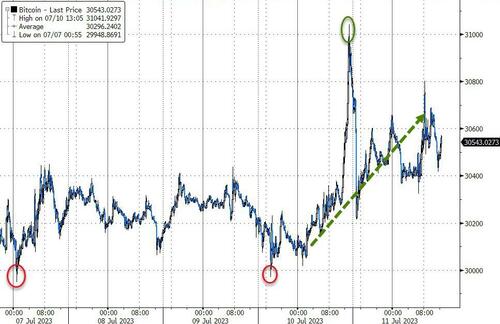

Bitcoin morning price:, $30,441 DOWN 448 Dollars

Bitcoin: afternoon price: $30,534 UP 355 dollars

Platinum price closing $929.00 DOWN $0.60

Palladium price; $1249.40 UP $5.55

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,556.45 UP 0.00 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1494.95 DOWN 2.12 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1753.4 UP 6,48 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JULY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,926.200000000 USD

INTENT DATE: 07/07/2023 DELIVERY DATE: 07/11/2023

FIRM ORG FIRM NAME ISSUED STOPPED

435 H SCOTIA CAPITAL 10

624 H BOFA SECURITIES 23

657 C MORGAN STANLEY 8

661 C JP MORGAN 2

661 H JP MORGAN 1

686 C STONEX FINANCIA 1

726 C CUNNINGHAM COM 1

737 C ADVANTAGE 32 6

905 C ADM 2

TOTAL: 43 43

JPMorgan stopped 0/128 contracts.

FOR JULY:

GOLD: NUMBER OF NOTICES FILED FOR JULY/2023. CONTRACT: 128 NOTICES FOR 12800 OZ or 0.3981 TONNES

total notices so far: 2287 contracts for 228,700 oz (7.1135 tonnes)

FOR JULY:

SILVER NOTICES: 108 NOTICE(S) FILED FOR 540,000 OZ/

total number of notices filed so far this month : 3538 for 17,690,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $6.15

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.00 TONNES OF GOLD FROM THE GLD/

INVENTORY RESTS AT 915.26 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 5 CENTS AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL DEPOSIT OF OF 0.020 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 464.822 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A VERY STRONG SIZED 1911 CONTRACTS TO 121,649 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS STRONG SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR TINY $0.02 GAIN IN SILVER PRICING AT THE COMEX ON MONDAY. TAS ISSUANCE WAS A SMALL SIZED 318 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH . CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON FRIDAY NIGHT: 318 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.02). AND WERE UNSUCCESSFUL IN KNOCKING ANY SPEC LONGS AS WE HAD A HUMONGOUS GAIN ON OUR TWO EXCHANGES OF 2,853 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 0 MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION.

WE MUST HAVE HAD:

A HUMONGOUS ISSUANCE OF EXCHANGE FOR PHYSICALS( 942 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 16.110 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S HUGE 485,000 OZ QUEUE JUMP.//NEW STANDING: 18.605 MILLION OZ/ // HUGE SIZED COMEX OI GAIN/ HUMONGOUS SIZED EFP ISSUANCE/VI) SMALL NUMBER OF T.A.S. CONTRACT ISSUANCE (318 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL + 1175 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTRACTS for 5 days, total 2297 contracts: OR 11.485 MILLION OZ (459 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 11.485 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 11.485 MILLION OZ

RESULT: WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1911 CONTRACTS DESPITE OUR GAIN IN PRICE OF $0.02 IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A HUMONGOUS EFP ISSUANCE CONTRACTS: 942 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JULY OF 16.110 MILLION OZ FOLLOWED BY TODAY’S 485,000 OZ QUEUE JUMP: TOTAL NOW STANDING 18.605 MILLION OZ///// .. WE HAVE A HUGE SIZED GAIN OF 2853 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A SMALL 318//NEGLIGIBLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION. THE NEW TAS ISSUANCE TODAY (318) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE.

WE HAD 108 NOTICE(S) FILED TODAY FOR 540,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GIGANTIC SIZED 22,841 CONTRACTS TO 485,952 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED 3,000 CONTRACTS

WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI ( 19,769 CONTRACTS) DESPITE OUR $1.35 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JULY. AT 5.1975 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0.3950 TONNE QUEUE JUMP: NEW TOTAL OF GOLD STANDING FOR JULY: 7.222 TONNES// + /AN UNBELIEVABLY HUGE (AND CRIMINAL) ISSUANCE OF 21,676 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH A $1.35 LOSS IN PRICE WITH RESPECT TO MONDAY’S TRADING.WE HAD AN ATMOSPHERIC SIZED GAIN OF 21,206 OI CONTRACTS (65.959 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1437 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 482,880

IN ESSENCE WE HAVE A GIGANTIC SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 24,278 CONTRACTS WITH 22,841 CONTRACTS INCREASED AT THE COMEX// AND A FAIR 1437 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 24,278 CONTRACTS OR 75,514 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A HUGE 21,676 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1437 CONTRACTS) ACCOMPANYING THE GIGANTIC SIZED GAIN IN COMEX OI (22,841) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 24,278 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JULY AT 5.1975 TONNES FOLLOWED BY TODAY’S 0.3950 TONNE QUEUE JUMP//NEW TOTAL 7.222 TONNES ///// /3) TINY LONG LIQUIDATION//4) HUMONGOUS SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: UNBELIEVABLY HUGE T.A.S. ISSUANCE: 21,676 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

TOTAL EFP CONTRACTS ISSUED: 10,160 CONTRACTS OR 1,016,000 OZ OR 31.601 TONNES IN 5 TRADING DAY(S) AND THUS AVERAGING: 2032 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAY(S) IN TONNES 31.601 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 31.601/3550 x 100% TONNES 0.890% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 31.601 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A STRONG SIZED 1911 CONTRACTS OI TO 120,474 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 942 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 942 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 942 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1911 CONTRACTS AND ADD TO THE 942 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A VERY STRONG SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2853 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 14.265 MILLION OZ

OCCURRED WITH OUR $0.02 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED UP 17.67 PTS OR 0.22% //Hang Seng CLOSED UP 180.11 PTS OR 0.97% /The Nikkei closed UP 13.84 OR 0.04% //Australia’s all ordinaries CLOSED UP 1.51 % /Chinese yuan (ONSHORE) closed UP 7.2000 /OFFSHORE CHINESE YUAN UP TO 7.2078 /Oil UP TO 73.45 dollars per barrel for WTI and BRENT UP AT 78.16 / Stocks in Europe OPENED MOSTLY ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A HUMONGOUS SIZED 22,841 CONTRACTS UP TO 485,952 DESPITE OUR LOSS IN PRICE OF $1.35 ON MONDAY,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1437 EFP CONTRACTS WERE ISSUED: : AUGUST 1437 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1437 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: AN ATMOSPHERIC SIZED TOTAL OF 22,841 CONTRACTS IN THAT 1437 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A HUMONGOUS SIZED GAIN OF 22,841 COMEX CONTRACTS..AND THIS STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $1.35//MONDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS AN UNBELIEVABLY HUGE 21,676 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THE HUGE NUMBER OF T.A.S. CONTRACTS INITIATED OVER THE PAST SEVERAL WEEKS SPELLS TROUBLE FOR THE GOLD/SILVER MARKET AS RAIDS WILL SURELY BE UPON US.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JULY (7.222) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 7.222 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $1.35) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD AN ATMOSPHERIC SIZED GAIN OF 24,278 CONTRACTS ON OUR TWO EXCHANGES. WE HAD SOME TAS LIQUIDATION THROUGHOUT THE MONDAY COMEX SESSION . THE TAS ISSUED MONDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 75.51 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY. (5.11974 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 0.3950 TONNES//TOTAL STANDING FOR JULY GOLD: 7.222 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $1.35.

WE HAD + ADDED 3,000 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 24,275 CONTRACTS OR 2,427,500 OZ OR 75.51 TONNES.

Estimated gold volume today:// 202,672 FAIR

final gold volumes/yesterday 268,811 FAIR

//JULY 11/ FOR THE JULY 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | NIL OZ . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today | 128 notice(s) 12800 OZ 0.3981 TONNES |

| No of oz to be served (notices) | 35 contracts 3500 oz 0.10886 TONNES |

| Total monthly oz gold served (contracts) so far this month | 2287 notices 228,700 OZ 7.1135 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

Customer deposits: 0

total customer deposits: 0 oz

total dealer deposits: 0

we had 0 customer withdrawals:

total withdrawals: NIL oz

Adjustments; 1

I) out of JPM< 32,215.302 oz (1000 kilobars)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 143 contracts having GAINED 84 contracts. We had 43 contracts served on Monday. Thus we gained 127 contracts or an additional 12,700 oz of gold will stand at the comex.

AUGUST LOST 10,914 contracts DOWN to 328,853 contracts

SEPT gained 283 contracts to stand at 445

We had 108 contracts filed for today representing 10800 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 128 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2023. contract month,

we take the total number of notices filed so far for the month (2287 x 100 oz ), to which we add the difference between the open interest for the front month of JULY (143 CONTRACT) minus the number of notices served upon today 128 x 100 oz per contract equals 232,200 OZ OR 7.222 TONNES the number of TONNES standing in this NON active month of July.

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (2287) x 100 oz + (143) {OI for the front month} minus the number of notices served upon today (128) x 100 oz) which equals 232,200 oz standing OR 7.222 TONNES

TOTAL COMEX GOLD STANDING: 7.222 TONNES WHICH IS STRONG FOR A NON ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,812,828.645 OZ 56,38 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,285,232.943 OZ

TOTAL REGISTERED GOLD: 11,833,384.990 (368.06 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,451,8467,953 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,020,556 OZ (REG GOLD- PLEDGED GOLD) 311.681 tonnes//

END

SILVER/COMEX

JULY 11

//2023// THE JULY 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,168,835.112 oz CNT Loomis . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 3987.562 oz Delaware |

| No of oz served today (contracts) | 108 CONTRACT(S) (540,000 OZ) |

| No of oz to be served (notices) | 183 contracts (915,000 oz) |

| Total monthly oz silver served (contracts) | 3538 Contracts (17,690,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposits

total dealer deposit: 0 oz

total dealer deposits: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i) Into Delaware: 3987.562 oz

total customer deposits: 3987.562 oz

JPMorgan has a total silver weight: 139.982 million oz/277,238 million =50.54% of comex .//dropping fast

Comex withdrawals 2

i) Out of CNT 569,456.312 oz

ii) Out of Loomis: 599,378.800 oz

adjustments: dealer to customer

i) Brinks 118,961.454 oz

TOTAL REGISTERED SILVER: 34.553 MILLION OZ//.TOTAL REG + ELIGIBLE. 278.403 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF JULY /2023 OI: 291 CONTRACTS HAVING GAINED 63 CONTRACT(S). WE HAD 34 NOTICES FILED ON MONDAY SO WE GAINED A STRONG 97 CONTRACTS OR AN ADDITIONAL 485,000 OZ WILL STAND AT THE COMEX FOR DELIVERY IN JULY.

AUGUST GAINED 43 CONTRACTS TO STAND AT 558

SEPT HAS A GAIN OF 1028 CONTRACTS DOWN TO 105,104

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 108 for 540,000 oz

Comex volumes// est. volume today 35,683 poor /

Comex volume: confirmed yesterday: 40,654 fair

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 3538 x 5,000 oz = 17,690,000 oz

to which we add the difference between the open interest for the front month of JULY(291) and the number of notices served upon today 108 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY/2023 contract month: 3538 (notices served so far) x 5000 oz + OI for the front month of JULY (291) – number of notices served upon today (108 )x 500 oz of silver standing for the JULY contract month equates to 18.605 million oz +

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

JULY 11/WITH GOLD UP $6.15 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.0 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 915.26 TONNES

JULY 10 WITH GOLD DOWN $1.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.60 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 916.26 TONNES.

JULY 7 WITH GOLD UP $16.80 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.86 TONNES.

JULY 6/WITH GOLD DOWN $9.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 917.86 TONNES

JULY 5/WITH GOLD DOWN $2.20 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 2.6 TONNES FROM THE GLD///INVENTORY RESTS AT 921.90 TONNES

JULY 3/WITH GOLD UP $1.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 924.50 TONNES//

JUNE 30/WITH GOLD UP $10.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 924.50 TONNES

JUNE 29/WITH GOLD DOWN $3.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.81 TONNES

JUNE 28/WITH GOLD DOWN $1.15 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 925.65 TONNES

JUNE 27/WITH GOLD DOWN $9.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD./INVENTORY RESTS AT 925.65 TONNES

JUNE 26/WITH GOLD UP $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD/////INVENTORY RESTS AT 927.10 TONNES

JUNE 23/WITH GOLD UP $5.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: WITHDRAWALS OF 4.33 TONNES OF GOLD OVER THE PAST TWO DAYS. /INVENTORY RESTS AT 929.70 TONNES

JUNE 21/WITH GOLD DOWN $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 934.03 TONNES

JUNE 20/WITH GOLD DOWN $22.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.03 TONNES

JUNE 16/WITH GOLD UP $0.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.33 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.03 TONNES

JUNE 15/WITH GOLD UP $2.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 929.70 TONNES

JUNE 14/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 931.44 TONNES

JUNE 13/WITH GOLD DOWN $10.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.01 TONNES FORM THE GLD///INVENTORY RESTS AT 931.44

GLD INVENTORY: 915.26 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 11/WITH SILVER DOWN 5 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .020 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 464.822 MILLION OZ/

JULY 10/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.672 MILLLION OZ FROM THE SLV///INVENTORY RESTS AT 464.802 MILLION OZ

JULY 7/WITH SILVER UP 42 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.474 MILLION OZ

JULY 6/WITH SILVER DOWN 50 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.667 MILLION OZ FORM THE SLV///INVENTORY RESTS AT 466.474 MILLION OZ//

JULY5/WITH SILVER UP 30 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JULY 3/WITH SILVER UP 7 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JUNE 30/WITH SILVER UP 19 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.377 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT468.141 MILLION OZ//

JUNE 29/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.763 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 466.764 MILLION OZ//

JUNE 28/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.527 MILLION OZ//

JUNE 27/WILVER SILVER UP 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 734,000 OZ INTO THE SLV////INVENTORY RESTS AT 470.527 MILLION OZ

JUNE 26/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 469.793 MILLION OZ.

JUNE 23/WITH SILVER DOWN 9 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A NET DEPOSIT OF 6.61 MILLION OZ INTO THE SLV OVER THESE PAST TWO DAYS//INVENTORY RESTS AT 469.793 MILLION OZ//

JUNE 21/WITH SILVER DOWN $.40 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.784 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 20/WITH SILVER DOWN 89 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 16/WITH SILVER UP 23 CENTS TODAY :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 463.183 MILLION OZ

JUNE 15/WITH SILVER DOWN 17 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.377 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 463.642 MILLION OZ//

JUNE 14/WITH SILVER UP 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 735,000 OZ FROM THE SLV///INVENTORY RESTS AT 465.019 MILLION OZ//

JUNE 13/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.515 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 465.754 MILLION OZ//

JUNE 12/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.269 MILLION OZ//

JUNE 9/

CLOSING INVENTORY 464.822 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

Peter Schiff: Bond Bear Will Maul Stocks And The Dollar

TUESDAY, JUL 11, 2023 – 02:00 PM

Stocks and bonds had a tough week last week. In his podcast, Peter Schiff talked about the market moves in the context of Fed rhetoric and the jobs reports. He concluded that we could be heading toward another big leg down in bonds, and this bond bear will maul stocks and the dollar.

Peter said called last week “decisive” and “telling” in the markets. The stock market and the bond market both showed weakness, along with the dollar. But gold finished last week with a small gain.

Given the fact that everything else went down, I think the fact that gold managed to go up could indicate we’ve kind of come to the end of this trend where we’ve had this bear market rally and stocks and the pullback in gold.”

https://www.zerohedge.com/markets/peter-schiff-bond-bear-will-maul-stocks-and-dollar

Bonds got clobbered last week driving yield across the spectrum to over 4%. We also had a complete inversion of the yield curve from the 6-month note to the 30-year bond.

The yield curve is clearly flashing recession. Now, you can argue that we’re in a recession even though the statistics don’t reflect that. But what the yield curve is telling you is we’re going to be in a recession. The question is when is it going to start, if it isn’t already here.”

Peter said the yield curve also indicates that price inflation expectations are still anchored, but they may be on the verge of coming unanchored.

If that is the case, I expect to see a sharper increase in yields in the 30-year, and I expect that inversion to reverse. Because as investors begin to have a more realistic outlook on inflation, they’re going to sell bonds, particularly the 30-year bonds. And the fact that the dollar went down and gold went up, may be a reflection of the fact that investors are starting to think this way.”

Peter said he thinks the weakness in the bond market caused the stock market to fall. So, what caused the carnage in the bond market?

For one thing, last week the Fed released the minutes from the June FOMC meeting. That reinforced the notion that more rate hikes are coming. In fact, most of the FOMC members indicated they expected additional hikes.

So, they’re just slowing down the pace of the rate hikes, but they’re not stopping the rate hikes. And of course, a lot of people are betting that the Fed is finished, that the reason they paused is because they’re done. I think there is a good chance that that is the case. But, you know, the Fed is certainly talking like that’s not the case. They’re acknowledging that inflation is still a threat. And it’s actually a bigger threat than what they acknowledge. But they’re not proclaiming victory, and they’re talking about more hikes. So, I think that hurt the market.”

But what really clobbered the bond market and drug down stocks was the much stronger than expected ADP private sector job numbers. In fact, they more than doubled the forecast. This threw fuel on the idea that the Fed is going to have to get even more aggressive in its inflation fight.

The Fed is still under the false impression that inflation is the byproduct of people working, and if more people are working, then we’re going to have more inflation. That is not the case. In fact, it’s the opposite. When people are productively employed, they make more things. You have more stuff. It costs less.

When you have a lot of people who aren’t working and who aren’t producing, but they’re spending because they’re getting unemployment checks, or food stamps, or other forms of welfare, all of that is inflationary, because you have less stuff being produced but more money being printed to buy that stuff. And so, the markets and the Fed still haven’t come to terms with that reality.”

But on Friday, the Bureau of Labor Statistics non-farm payroll report came out, and it was a miss. Not only that, the BLS revised the job numbers downward for every month this year. In all, 196,00 jobs disappeared from the numbers.

I’ve been saying all along that I don’t believe these job numbers. I think they’re overstated. And I think that despite this downward revision, they’re probably still overstated.”

Peter noted the big increase in corporate bankruptcies.

The government is still assuming all these new companies are being formed and creating all these jobs. All these bankruptcies would indicate that it’s more companies that are dying.

The birth-death model needs to be adjusted to have more deaths. Because that’s what’s happening. These companies are dying, and these dying companies are obviously laying off workers.

If we have all these bankruptcies, does it makes sense that we have strong job gains?”

In other words, the government formula is overstating job creation and understating layoffs.

Peter said the market reaction to these contradictory job reports was telling. Bonds got clobbered when the ADP number came out stronger than expected and then bonds sold off again with the weaker-than-expected BLS job report. You would have expected the bond market to enjoy a relief rally.

To me, that was very negative for the markets. Because I’ve been looking for and waiting for a breakdown in the bond market. I’ve been thinking that we’re just going sideways, but that we have another big move down in bonds, meaning a big move up in yields. And that could be happening — where we start to see the movement on the 10 to the 30 from a four-handle to a five-handle. Remember, we’ve already got the shorter maturities in the fives. The longer-term bonds should be up there too. If that happens, if we start moving toward 5% on the 10-year through the 30-year, that is going to be a huge problem. Because that is going to put a lot more downward pressure on the portfolios of banks, and all of their underwater mortgage-backed securities and Treasury portfolios are about to get hammered.”

This will also put more pressure on the stock market.

It’s also notable that even with the selloff in stocks last week, the dollar fell too.

Peter said all of these trends are a negative for American markets but a positive for gold.

In this podcast, Peter also covers some of the negative economic data that recently came out.

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

De-Dollarization Just Got Real, Part 2: BRICS To Introduce Gold-Backed Currency In August

We now have both the event and the date

JUL 10, 2023

There’s an old saying about predictions: It’s okay to forecast an event or a date, but not both. But lately, Jim Rickards has been predicting both the introduction by the BRICS coalition of gold-backed currency and the date, August 22. Here’s a short video where he lays it out.

https://rubino.substack.com/p/de-dollarization-just-got-real-part

Based on subsequent headlines, it seems that Rickards’ gamble paid off, with him nailing both parts of the story:

Russia confirms BRICS will create a gold-backed currency

(Kitco News) – Friday, according to state-run RT, the Russian government has confirmed that Brazil, Russia, India, China and South Africa, also known as BRICS nations, will introduce a new trading currency backed by gold. The official announcement is expected to be made during the BRICS summit in August in South Africa.

The latest news is adding new momentum to the ongoing de-dollarization trend unfolding in the global economy. Since mid-2022, central banks worldwide have been buying gold at a historic pace in part to diversify their reserve away from the U.S. dollar.

For many analysts, a gold-backed currency is the next evolution in this process. Many analysts have seen China’s recent gold purchases as an attempt to bring international credibility to the yuan.At the same time, the U.S. government’s weaponization of the U.S. dollar against Russia for invading Ukraine has created some geopolitical uncertainty among some nations allied with Russia.

What does this mean?

There’s a lot to consider here, including:

- The introduction of a gold-backed BRICS currency is the beginning, not the end, of a long journey. It will have to survive the inevitable growing pains as technical questions are (sometimes very messily) worked out, and people will have to be convinced to use it. On the latter point, Rickards predicts that each BRICS country will issue bonds denominated in the new currency and encourage citizens to buy them, thus jumpstarting a bond market that will then go global.

- We’ll have to see what exactly “gold-backed” means. Will the currency be convertible into gold at government offices or via bank accounts? Will participants settle trade imbalances by shipping physical gold from vault to vault? Will there be some kind of blockchain-like ledger that accounts for who owns what? Will China be in charge of everything or will decision-making be distributed?

- The BRICS countries will have to prove they can play nice with each other, something that, based on past history and current governance styles, is not at all guaranteed. Picture the eurozone with eight different flavors of dictatorship.

- How will the existing fiat monetary powers react to such a challenge? The US tends to respond violently to countries that nationalize their resources or otherwise deviate from dollar hegemony. A gold-backed BRICS currency would be orders of magnitude more threatening than, say, a couple of random countries trading oil in yuan. So it’s possible that the US response would be commensurately extreme. Since we’re already on the verge of WWIII in two separate theaters, any escalation from here would take the world into “inconceivable” territory.

- Last but least, the BRICS currency is emerging at the exact time that central banks around the world — including some of the BRICS — are rolling out central bank digital currencies (CBDCs) that appear to be designed more as tools for social control than as improvements in national monetary systems. The new BRICS currency seems like a separate issue. But could it be part of the same overarching plan? Stay tuned.

Good for gold

Assuming the world manages to avoid a nuclear war, gold probably wins in two ways if a gold-backed BRICS currency gains traction in global trade.

- The participants will need more gold to back a rising amount of currency in circulation, increasing demand for limited supplies of available metal.

- The existence of a major gold-backed currency would lead to a public debate over the difference between and relative merits of fiat currency and sound money. Millions of newly minted gold bugs will result (since that’s just what happens when normal people actually consider these issues) leading to a big jump in retail gold demand.

To sum up, many things have to go right for the BRICS currency to launch successfully and gain traction, and a smooth introduction is probably the least likely scenario. But there’s a decent chance that it’s good for gold. In any event, it’s nice to have both an event and a date to look forward to.

end

end

3,Chris Powell of GATA provides to us very important physical commentaries

Two commentaries on the same subject: many countries repatriating their gold in response to Russian sanctions

(Reuters and National Post Toronto)

Countries are repatriating gold in response to sanctions against Russia, study finds

Submitted by admin on Sun, 2023-07-09 22:51Section: Daily Dispatches

By Marc Jones

Reuters

Monday, July 10, 2023

LONDON — More countries are repatriating gold reserves as protection against the sort of sanctions imposed by the West on Russia, according to an Invesco survey of central bank and sovereign wealth funds published today.

The financial market rout last year caused widespread losses for sovereign money managers who are “fundamentally” rethinking their strategies on the belief that higher inflation and geopolitical tensions are here to stay.

Over 85% of the 85 sovereign wealth funds and 57 central banks that took part in the annual Invesco Global Sovereign Asset Management Study believe that inflation will now be higher in the coming decade than in the last.

Gold and emerging market bonds are seen as good bets in that environment, but last year’s freezing of almost half of Russia’s $640 billion of gold and forex reserves by the West in response to the invasion of Ukraine also appears to have triggered a shift.

The survey showed a “substantial share” of central banks were concerned by the precedent that had been set. Almost 60% of respondents said it had made gold more attractive, while 68% were keeping reserves at home compared to 50% in 2020.

One central bank, quoted anonymously, said of gold: “We did have it held in London … but now we have transferred it back to own country to hold as a safe haven asset and to keep it safe.”

Rod Ringrow, Invesco’s head of official institutions, who oversaw the report, said that is a broadly-held view.

“‘If it’s my gold then I want it in my country’ has been the mantra we have seen in the last year or so,” he said. …

… For the remainder of the report:

end

Gold swaps and Bank of England’s custodial gold inventory decline

Submitted by admin on Mon, 2023-07-10 10:45Section: Daily Dispatches

A little more journalism would ask the New York Fed about any changes in its own custodial gold inventory — not that any answer would necessarily be truthful.

* * *

Central Banks Move Gold Back Home After Freeze on Russian Assets

By Arjun Neil Alim and Harry Dempsey

Financial Times, London

Monday, July 10, 2023

A growing number of countries are bringing their physical gold reserves back home to avoid Russian-style sanctions on their foreign assets, while increasing their purchases of the precious metal as a hedge against high levels of inflation.

Central banks globally made record purchases of gold in 2022 and into the first quarter of this year, as they hunted for safe havens from high inflation and volatile bond prices, according to a survey of sovereign investors by asset manager Invesco. China and Turkey together accounted for almost one-fifth of these purchases

Concerned by the decision by the US and others to freeze Russian assets, central banks opted to buy physical gold rather than derivatives or exchange traded funds that track the metal’s price.

They also preferred to hold it in their own country as global tensions increased. Invesco’s survey found that 68% of central banks held part of their gold reserves domestically, up from 50% in 2020. In five years that figure is expected to rise to 74%, the survey showed.

“Until this year central banks were willing to buy or sell gold through ETFs and gold swaps,” said Invesco’s head of official institutions, Rod Ringrow. “This year it has been much more physical gold and the desire to hold gold in country rather than overseas with other central banks. … It’s part of the reaction to the freezing of the Bank of Russia’s reserves.” …

In a sign of the move to repatriate gold, holdings at the Bank of England, one of the main storage hubs for official financial institutions globally, have slipped 12% from their 2021 peak to 164 million troy ounces at the start of June.

The attraction of holding gold in large liquid hubs such as London has also been reduced by the fact that hedging by gold miners peaked at the turn of the millennium and has since fallen. That has limited the ability for central banks to earn a yield by swapping out bullion stored overseas.

… For the remainder of the report:

https://www.ft.com/content/76bddb74-4ddb-4e36-b70c-c0e26d8bf557

END

This is quite a find!!

More than 700 Civil War-era gold coins discovered in Kentucky cornfield

Submitted by admin on Mon, 2023-07-10 19:47Section: Daily Dispatches

By Chris Knight

National Post, Toronto

Monday, July 10, 2023

A man in Kentucky has harvested a fortune in gold from his cornfield, after stumbling across a cache of more than 700 gold coins dating back to the U.S. Civil War era.

The man, whose name and location have not been revealed, can be heard on a short video breathlessly exclaiming “this is the most insane thing ever” while digging the coins out of the dirt.

The treasure, which has already been dubbed “The Great Kentucky Hoard,” has not been precisely valued, but just one of the coins, an 1863 $20 Gold Liberty coin, has in the past sold at auction for more than $100,000. The cache includes 18 of those, as well as more than 600 gold dollar coins, dating from 1854 to 1862.

Kentucky was a border state during the Civil War and declared itself neutral when hostilities broke out. It was the site of several fierce battles, and its uncertain future led to many wealthy inhabitants hiding their valuables from one side or the other. Legends persist of buried treasure left behind by Daniel Boone, Jesse James, and others. …

… For the remainder of the report:

end

More nations cut their ties with the USA dollar

(Daily Star/Bangladesh)

Bangladesh and India to begin bilateral trade in rupees tomorrow

Submitted by admin on Mon, 2023-07-10 20:12Section: Daily Dispatches

By AKM Zamir Uddin

The Daily Star, Dhaka, Bangladesh

Sunday, July 9, 2023

Bangladesh is set to join a global effort that is seeking to cut over-dependence on the U.S. dollar when it comes to settling foreign trades as the country commences to use the rupee to carry out bilateral transactions with India from July 11.

The move may extend some respite to importers since they will be able to open letters of credit in the rupee to source a portion of the products from the neighbouring country, thus cutting the use of the U.S. dollar to some extent.

The government has toughened import rules due to the shortage of American greenback, driven by higher import bills, with a view to stopping further depletion of the foreign currency reserve, which has fallen by nearly 30% from a year ago.

Both the Bangladesh Bank and the Indian High Commission are expected to announce the move toward the Indian currency at an event at Le Méridien Hotel in Dhaka on Tuesday. …

… For the remainder of the report:

https://www.thedailystar.net/business/global-economy/news/new-era-dawns-trade-india-3364336

end

The Sound Money Defense league’s successes discussed on Palisades Gold radio

(Stefan Gleason)

Sound Money Defense League’s successes discussed on Palisades Gold Radio

Submitted by admin on Fri, 2023-07-07 19:10Section: Daily Dispatches

7:10p ET Friday, July 7, 2023

Dear Friend of GATA and Gold:

Stefan Gleason of the Sound Money Defense League (and coin and bullion dealer Money Metals Exchange) today explains to Tom Bodrovics of Palisades Gold Radio the league’s increasingly successful work to exempt the purchase and sale of the monetary metals from state taxes in the United States.

Gleason and Bodrovics also discuss legislation introduced in Congress by U.S. Rep. Alex X. Mooney, R-West Virginia, to return the United States to a gold standard, after first determining whether the U.S. gold reserve has been encumbered by gold leases, swaps, and similar mechanisms

In 2009 a member of the Federal Reserve’s Board of Governors, Kevin M. Warsh, admitted to GATA that the Fed has secret gold swap agreements with foreign banks:

https://www.gata.org/node/7819

Other topics of the discussion include the totalitarian implication of central bank digital currencies.

The discussion is 51 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES/

end

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//COCOA

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2000

OFFSHORE YUAN: UP TO 7.2078

SHANGHAI CLOSED UP 17.67 PTS OR 0.55%

HANG SENG CLOSED UP 180.11 PTS OR 0.97%

2. Nikkei closed DOWN 13.84 PTS OR 0.04%

3. Europe stocks SO FAR: MOSTLY ALL GREEN

USA dollar INDEX DOWN TO 101.53 EURO FALLS TO 1.0991 DOWN 14 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.447 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 140.36/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ON SHORE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.6145***/Italian 10 Yr bond yield FALLS to 4.367*** /SPAIN 10 YR BOND YIELD FALLS TO 3.674…** DANGEROUS//

3i Greek 10 year bond yield FALLS TO 4.011

3j Gold at $1936.50 silver at: 23.15 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 25 /100 roubles/dollar; ROUBLE AT 90.17//

3m oil into the 73 dollar handle for WTI and 78 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 142.25// 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO 0.447% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8815 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9689 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.963 DOWN 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.002 DOWN 4 BASIS PTS/

USA 2 YR BOND YIELD: 4.843 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.11…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 0 BASIS PTS AT 4.688 UP 1 PTS

end

2. Overnight: Newsquawk and Zero hedge:

Futures Rise After Latest China Stimulus Report, Looming CPI Keeps Gains In Check

TUESDAY, JUL 11, 2023 – 08:15 AM

For the second day in a row, S&P futures are largely unchanged following a muted overnight session, reversing an earlier loss around the start of the European session and trading around session highs. In a reversal of yesterday’s tech/small cap drubbing sparked by fears about the upcoming Nasdaq special rebalance (see here). As of 7:30am, S&P futures were up 0.2%, trading at 4,450, and building on Monday’s modest gains with sentiment boosted after China signaled that more economic aid measures will come to support its ailing property market along with measures to boost business confidence; Nasdaq futures were also in the green as tech stocks see a lift while bond yields fall ahead of growing expectation that tomorrow’s CPI will surprise dovishly (in large part on the back of yesterday’s Manheim used car index collapse).

Treasury yields fell with the 10Y yield trading below 4% as USD weakness continued for a third day. NY Fed’s consumer survey shows inflation expectations continuing to decline; 1Y expectations are now 3.8%, the lowest reading since Apr 2021. The perceived probability of job loss moved up to 12.9%, highest since Nov 2021, which may feed into a reduced job quits rate. Meanwhile, Fedspeak remained hawkish, continuing the recent narrative with all of Monday’s Fed speakers indicating they are looking for higher rates. As such rate hike expectations for July remain ~90%. With all eyes on Wednesday’s CPI print, we may see another quiet (from a news/catalyst perspective) session with activity mostly position squaring ahead of the CPI print. Yesterday saw another strong series of short covering, which in turn led to the third worst day of 2023 for hedge funds according to Goldman prime brokerage.

In premarket trading, Iovance Biotherapeutics shares fall 11% after the biotechnology company announced the pricing of an underwritten public offering of 20 million shares of its common stock at $7.50 per share, a nearly 15% discount to last close. JPMorgan gaines more than 1% after it was raised to buy from hold at Jefferies, which highlights the big US investment bank’s “stable” earnings outlook and better revenue diversity. Here are some other premarket movers:

- Nio’s US-listed shares rise 1% in premarket trading following a 7.9% rally on Monday. Morgan Stanley said the EV maker’s sales momentum showed a big improvement last month and is likely to register further gains through September.

- Viridian Therapeutics Inc. reported preliminary data from an ongoing trial of its eye disease drug on Monday. Shares slumped 14% in premarket trading Tuesday.

- Zillowis raised to overweight from neutral at Piper Sandler, which sees share gains and improving housing macro conditions setting up a better 2H23 and FY24 for the tech real estate marketplace. The broker also boosted its price target. Shares gain 3.8% in premarket trading

“Last week’s surge in government bond yields put some pressure on equities – and highlights that companies will need to deliver on the market’s earnings expectations as the Q2 reporting season gets underway,” BlackRock Investment Institute analysts including Jean Boivin wrote in a note. “Resilient consumers have helped support earnings, but we see them exhausting the savings built up during the pandemic this year.”

While central bank officials in Europe and the US are increasingly suggesting they’ve reached a turning point in the battle against inflation, they’re also warning that higher rates for longer are needed to ensure price stability. That’s a mixed blessing for stock bulls who have had to endure a disappointing start to the second half after stellar gains in the first six months of the year. The approaching second-quarter earnings season will give them more food for thought: it kicks off in earnest on Friday, when JPMorgan, Citigroup and Wells Fargo all report their numbers.

“US equity markets have priced in a soft landing, or a more friendly recession, but actually the risk is for the recession to come in harder than expected,” Cecilia Chan, chief investment officer for APAC at HSBC Asset Management, said on Bloomberg TV. “For developed markets we expect a choppy-waters kind of scenario where it will be more difficult from now on, and we are more conscious of valuations that are on the expensive side.”

On Wednesday, the latest US CPI data will give further insight into outlook for prices and interest rates. Most Fed policymakers expect to increase rates by a further half percentage point by the end of the year, according to projections released after their June gathering. The ECB, meanwhile, is all but certain to raise rates by a quarter point on July 27. Policymakers are debating whether to raise borrowing costs again at their subsequent meeting in September.

In the UK, data showed that wage growth held at a level that BOE Governor Andrew Bailey said is fueling inflation. The data is crucial to shaping the central bank’s next decision on rates in August. The pound rose to the highest versus the dollar since April 2022.

In Europe, the Stoxx 600 index was on track for a third day of gains with construction, consumer and mining stocks leading gains after Governing Council member Francois Villeroy de Galhau said the European Central Bank is nearly finished hiking, but added that interest rates will stay at “high plateau” for some time. The UK’s benchmark fell as the latest wage data added pressure on the Bank of England to keep raising rates. Bonds rose, with the German 10-year yield falling five basis points to 2.59%. Here are the other notable European movers:

- Kingspan Group shares rise as much as 13% after the building materials company issued an unscheduled trading update, saying it expects to report record 1H23 trading profit in the region of €435m

- Nordic Semiconductor shares climb as much as 8.8% higher in volatile trading. The Norwegian chipmaker gave tepid 3Q sales guidance and said it’s intentionally skipping any guidance for 4Q amid a chip sector slowdown

- Forterra drops as much as 12%, the steepest decline since March 2020, after the British building materials firm issued a pre-close update which analysts say implies significant downside to current consensus

- Saab gains as much as 6.5% after Citi says the denfese company’s shares don’t yet reflect the positives from Turkey agreeing not to block Sweden’s bid to join the NATO defense alliance

- Nordex shares rose as much as 5.4% in Frankfurt on Tuesday after the company announced it received further orders for several wind farms in the Mediterranean region at the end of 2Q, according to statement

- British Land shares rise as much as 3.1%, among the top performers in the Stoxx 600 Real Estate Index, after the commercial property landlord said momentum continues to be strong

- BMW falls as much as 2.2% after Bankhaus Metzler cut to hold from buy, which sees the market environment for demand and pricing becoming more challenging in the second half of the year, while margins could soften slightly

- Dowlais, the automotive technology business spun off from Melrose, drops as much as 7.4%, most since May 24, as Citi starts coverage with a sell rating. The broker opens a pair trade, with an overweight on Melrose

- Tryg dropped as much as 5.8%, the most since October, after the Danish insurer reported gross premiums for the second quarter that missed the average analyst estimate

- Sensirion shares tumble as much as 20%, the most ever, after the Swiss maker of gas and liquid flow sensors issued a profit warning on the back of a more pronounced inventory correction and weaker consumer demand.

Earlier, a gauge of Asian equities climbed more than 1% and snapped a four-day losing streak, boosted by gains in semiconductor-related shares and China’s latest moves to support its flagging economy and property sector. The MSCI Asia Pacific Index climbed 1.2%, with Taiwan Semiconductor the biggest contributor after a better-than-expected sales report amid the boom in artificial intelligence. South Korea, Hong Kong, Taiwan and Australia were among the best-performing markets in the region, while Japanese stocks halted their longest losing run of the year as a result of a recent surge in the yen following months of carry-trade driven weakness.

Stock gauges in Hong Kong and mainland China extended gains from Monday as Chinese authorities signaled further policy support for the economy following minor steps to support the weak property market. The Hang Seng Index is still down 17% from a January high. “Valuations have been cheap but earnings revision seems to be bottoming out,” Rupal Agarwal, Asia quantitative strategist at Bernstein told Bloomberg Television explaining her constructive view on China. “Some of the policy-led support that the market could start receiving is also one of the key catalysts we are looking for,” she added. Japan’s Nikkei 225 was the laggard and gave back most of its early gains with the upside capped by a firmer currency. ASX 200 traded higher with the index led by the tech and mining-related industries, while risk sentiment was also facilitated by an improvement in Westpac consumer confidence and NAB business surveys.

In FX, the Bloomberg Dollar Spot Index saw another day of broad-based weakening as the Japanese yen outperformed most major peers. USD/JPY fell as much as 0.63% as traders sold out of long dollar positions; NZD/USD slipped 0.4% and AUD/USD fell 0.1% after China’s economic stimulus signal did little to support the currencies.

“We do not expect big FX moves today, but DXY could continue drifting toward the 101.50 area,” wrote Chris Turner, head of fx strategy at ING, in a note. “The push factor of the Fed/US interest rate story versus the pull factor of overseas asset markets is slightly working against the dollar.”

In rates, treasuries advanced across the curve with yields on the two-year falling three basis points to 4.83% and yields on the 10-year down three basis points to 3.965%, outperforming bunds and gilts by 1bp and 2bp; euro bonds also saw broad.

Governing Council member Francois Villeroy de Galhau said the European Central Bank is nearly finished hiking, but interest rates will stay at “high plateau” for some time. Treasury’s $40 billion 3-year new-issue auction closes at 1pm New York time; $32 billion 10-year and $18 billion 30-year reopenings are Wednesday and Thursday. Gilts are higher after the UK unemployment rate unexpectedly rose in May although wages did top estimates. UK two-year yields are down 3bps at 5.34%. The pound is up 0.3%.

In commodities, crude futures advanced, with WTI gaining 0.2% to trade near $73.20. Spot gold adds 0.6%. Bitcoin falls 1.3%.

Looking To the day ahead, and data releases include UK employment and Italian industrial production for May, along with the German ZEW survey for July. In the US, there’s also the NFIB’s small business optimism index for June which came in stronger at 91.0 from 89.4 last month, above the 89.9 expectation. From central banks, we’ll hear from the ECB’s Villeroy. Finally, NATO leaders will be gathering for a summit in Vilnius.

Market Snapshot

- S&P 500 futures up 0.2% at 4,455

- MXAP up 1.2% to 163.48

- MXAPJ up 1.5% to 514.40

- Nikkei little changed at 32,203.57

- Topix down 0.3% to 2,236.40

- Hang Seng Index up 1.0% to 18,659.83

- Shanghai Composite up 0.6% to 3,221.37

- Sensex up 0.6% to 65,748.95

- Australia S&P/ASX 200 up 1.5% to 7,108.85

- Kospi up 1.7% to 2,562.49

- STOXX Europe 600 up 0.2% to 449.22

- German 10Y yield little changed at 2.61%

- Euro little changed at $1.1012

- Brent Futures up 0.9% to $78.36/bbl

- Gold spot up 0.6% to $1,936.90

- US Dollar Index down 0.23% to 101.74

Top Overnight News

- Japanese consumers may finally be shedding their decades-old frugal mindset, spending more on items that retailers were once too afraid to raise prices on and paving the way for the central bank to finally unwind its massive monetary stimulus. The world’s third-largest economy is seeing early signs of demand-driven inflation with an increasing number of hotels, restaurants and retailers now charging more for services – without losing consumers who are willing to pay more on prospects of higher wages. RTRS

- China signaled more economic support measures are imminent after authorities took a small step toward supporting the ailing property market by extending loan relief for developers. BBG

- Sales of homegrown passenger-car brands in China are consistently eclipsing those of their Western rivals, signaling the growing influence of the country’s electric-vehicle makers—and a triumph for Beijing’s industrial policy. WSJ

- France will send its long-range SCALP missiles to Ukraine to help it defend its territory against Russia, the latest step-up of western military support. FT

- The US will transfer F-16 fighter jets to Turkey in consultation with Congress, the US national security adviser said on Tuesday, hours after Turkey’s president agreed to drop his veto on Sweden joining Nato. FT

- The Fed’s John Williams said the US jobs market remains strong, but he sees signs of slowing in the direction of labor demand. An increase in unemployment and a further easing of demand will be needed to bring inflation back to target. He also said officials “have some ways to go to get the policy to this sufficiently restrictive stance.” BBG

- A growing number of countries are bringing their physical gold reserves back home to avoid Russian-style sanctions on their foreign assets, while increasing their purchases of the precious metal as a hedge against high levels of inflation. FT

- House Republicans threaten to block bills that don’t contain what they believe are adequate spending cuts, raising the risk of a gov’t shutdown later in the year. The Hill

- The restart of federal student loan payments this fall will be a renewed burden for millions of borrowers and another headwind for a US economy that’s losing momentum. BBG

- Alternative financing options for businesses unable to borrow from banks are likely more expensive. Academic research suggests that, after controlling for firm and loan characteristics, nonbank loans for mid-sized public companies typically carry interest rates that are roughly 200 basis points higher than those of bank loans. GIR

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly positive following the tailwinds from the US where cyclicals benefitted from encouraging inflation proxies ahead of this week’s US CPI data, while participants also reflected on China’s support efforts. ASX 200 traded higher with the index led by the tech and mining-related industries, while risk sentiment was also facilitated by an improvement in Westpac consumer confidence and NAB business surveys. Nikkei 225 was the laggard and gave back most of its early gains with the upside capped by a firmer currency. Hang Seng and Shanghai Comp conformed to the upbeat mood as developers benefitted after China extended two financial policies to support the stable and healthy development of the real estate market to the end of 2024.

Top Asian News

- Australian PM Albanese is reportedly considering delaying a trip to Beijing until next year as the government prepares the appointment of a new ambassador to China, while turning down an invitation would be seen by China as a snub, according to Sydney Morning Herald.

European bourses are firmer but off of best levels, Euro Stoxx 50 +0.4%, as sentiment has gradually deteriorated throughout the morning from initial APAC performance and as ZEW remains glum. Sectors are primarily in the green, though shy of best levels given the above; Autos lag with Volkswagen dragging after a Handelsblatt piece. Stateside, futures are directionally in-fitting but have been much closer to unchanged throughout the morning ahead of a relatively thin US agenda, ES +0.1%. German Cartel Office says, following the European Court Ruling, see scope for further actions against Big Tech names.. Reminder, On July 4th, the EU’s Top Court said the German Antitrust Agency can asses privacy in its investigations.

Top European News

- UK PM Sunak considers delaying cabinet reshuffle until September, according to The Telegraph.

- Barclays said UK consumer spending in June rose 5.4% Y/Y which was boosted by warm weather and noted that food price inflation pushed the annual increase in grocery spending in June to the highest since February 2021, according to Reuters.

- ECB’s Villeroy says we are starting to see good news on inflation; inflation will continue to decline and will be back at 2% by 2025; inflation should be at 2.5% on average next year.

FX

- Yen and Franc outperform amidst retreat in US Treasury yields, USD/JPY extends reversal through 141.00 and a Fib to just under 140.50, USD/CHF towards 0.8800 from 0.8850+ and DXY depressed within 101.960-670 range as a result.

- Pound perks up as UK average earnings exceed expectations, Cable probes 1.2900 briefly and EUR/GBP pivots 0.8550.

- Euro fades between 1.1026-1.0998 parameters vs Buck after downbeat ZEW survey.

- Kiwi lags awaiting RBNZ and confirmation that OCR has peaked at 5.5%, NZD/USD reverses from 0.6225 and AUD/NZD rebounds from just under 1.0750.

- PBoC set USD/CNY mid-point at 7.1886 vs exp. 7.2177 (prev. 7.1926)

Fixed Income

- Bonds bounce further from recent lows, with Bunds at best levels since last Thursday at 131.58 and Bobls underpinned near 115.00 following a decent 5 year German auction.

- Gilts lag within 93.31-92.78 range after another UK average earnings beat, but T-note closer to 111-16 peak than 111-04 trough amidst soft US inflation vibes ahead of CPI.

Commodities

- Crude benchmarks spent much of the European morning resilient to the gradual downtick in broader risk appetite. However, the complex has most recently moved in-line and is now essentially flat and echoing the price action of European/US equity futures.

- Spot gold remains firmer given the lessening risk appetite and as the USD fails to derive any significant benefit from this.

- Base metals are hanging onto their APAC gains spurred by further Chinese stimulus hopes, despite the broader dip in risk appetite.

- Indonesia seized an Iranian-flagged tanker due to alleged illegal transhipment of oil, according to Reuters.

Geopolitics

- US President Biden is to meet with Ukrainian President Zelensky during the NATO summit on Wednesday, while Japanese PM Kishida also plans to meet with Zelensky at the NATO summit, according to CNN and Nikkei.

- US National Security Advisor Sullivan says allies will send a positive signal on Ukraine’s future membership at the NATO summit; Biden intends to move forward with the transfer of F16s to Turkey in consultation with Congress.

- North Korean leader Kim’s sister said the US spy plane entered its economic water zone eight times on July 10th and warned US forces will face critical flight in case of repeated illegal intrusion, according to KCNA.

- Azerbaijani border guards suspend transport between Armenia and the Nagorno-Karabakh region, according to Al Arabiya.

Asia Pacific

- APAC stocks were mostly positive following the tailwinds from the US where cyclicals benefitted from encouraging inflation proxies ahead of this week’s US CPI data, while participants also reflected on China’s support efforts.

- ASX 200 traded higher with the index led by the tech and mining-related industries, while risk sentiment was also facilitated by an improvement in Westpac consumer confidence and NAB business surveys.

- Nikkei 225 was the laggard and gave back most of its early gains with the upside capped by a firmer currency.

- Hang Seng and Shanghai Comp conformed to the upbeat mood as developers benefitted after China extended two financial policies to support the stable and healthy development of the real estate market to the end of 2024.

US Event Calendar

- 06:00: June Small Business Optimism, 91.0 est. 89.9, prior 89.4

DB’s Jim Reid concludes the overnight wrap

Markets had started the week in a holding pattern, but a rates rally in the US emerged as the main theme on Monday that sent the 10yr Treasury yield back beneath 4% again. The decline in yields followed some dovish tones in usually second-tier US data, which comes ahead of tomorrow’s all-important US CPI print. For equities it was a slow moving day, but the major indices like the S&P 500 (+0.24%) and Europe’s STOXX 600 (+0.18%) did see muted gains ahead of the start of earnings season later this week.

Earlier in the day 10yr US Treasury yields briefly looked like they might move above the pre-SVB peak, reaching as high as 4.088% shortly before the US open. But yields closed materially lower in the end, with the 2yr down -8.8bps to 4.86% and the 10yr down -6.8bps to 3.99%. The latter was the sharpest daily fall since the first half of June, and overnight we’ve seen the 10yr move another basis point lower to 3.98%. The rally came as investors grew more confident that the Fed would cut rates in H1 2024 (with June 2024 Fed pricing down -11.0bps from Friday). However, investors only marginally dialled back their expectations for rate hikes this year, with no change in the 89% likelihood of a hike this month and with the terminal rate priced for November down just -1.0bps to 5.42%.