JULY 25/GOLD CLOSED UP $2.45 TO $1962.55 WHILE SILVER ALSO HAD A STRONG DAY UP 24 CENTS TO $24.65//PLATINUM WAS UP $6.05 TO $969.80 WHILE PALLADIUM WAS UP $6.05 TO $1295.00/CHINA TO INITIATE MORE STIMULUS TO SUPPORT THEIR PLUMMETING ECONOMY//CHINA REPLACES ITS VANISHING FOREIGN MINISTER//EU REPORTS ON PLUMMETING LOAN DEMAND//UKRAINE VS RUSSIA UPDATES//RUSSIA ATTACKS A DANUBE PORT WITHIN YARDS TO A BORDER WITH ROMANIA//TENSIONS ESCALATE//COVID/VACCINE UPDATES//DR PAUL ALEXANDER/SLAY NEWS/EVOL NEWS/NEWS ADDICTS//ISRAEL IN A STATE OF CHAOS AFTER THE AFFIRMATIVE VOTE AS DRS GO ON STRIKE//YELLOW CARRIERS AND FED EX UPDATES/SWAMP STORIES FOR YOU TONIGHT//

132 C SG AMERICAS 26 159 C MAREX CAPITAL M 117 123 190 H BMO CAPITAL 56 365 H MAREX CAPITAL M 12 8 657 C MORGAN STANLEY 8 661 C JP MORGAN 60 685 C RJ OBRIEN 3 686 C STONEX FINANCIA 40 30 732 C RBC CAP MARKETS 9 737 C ADVANTAGE 102 117 905 C ADM 13

TOTAL: 362 362 MONTH TO DATE: 4,347

JPMorgan stopped 0/0 contracts.

FOR JULY:

GOLD: NUMBER OF NOTICES FILED FOR JULY/2023. CONTRACT: 0 NOTICES FOR 0 OZ or 0 TONNES

total notices so far: 3275 contracts for 327,500 oz (10.1866 tonnes)

FOR JULY:

SILVER NOTICES: 10 NOTICE(S) FILED FOR 50,000 OZ/

total number of notices filed so far this month : 5065 for 25,345,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $2.45

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 919.00 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP $0.24 AT THE SLV// SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 826,000 OZ FORM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 452.480 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 2020 CONTRACTS TO 146,629 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS GIGANTIC SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.23 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. TAS ISSUANCE WAS A STRONG SIZED 734 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH . CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 734 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.23). AND WERE SUCCESSFUL IN KNOCKING SOME SPEC LONGS AS WE HAD A HUGE LOSS ON OUR TWO EXCHANGES OF 1450CONTRACTS. WE HAD A HUGE 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 5.25MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION.

WE MUST HAVE HAD:

A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS( 570 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 16.110 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S HUGE 45,000 QUEUE JUMP + 0 MILLION OZ EXCHANGE FOR RISK FOR TODAY//NEW STANDING: 25.450 MILLION OZ + 5.25 MILLION OZ EXCHANGE FOR RISK/PRIOR: NEW TOTAL 30.700 MILLION OZ// // GIGANTIC SIZED COMEX OI LOSS/ GOOD SIZED EFP ISSUANCE/VI) GOOD NUMBER OF T.A.S. CONTRACT ISSUANCE (734CONTRACTS)/ZERO EXCHANGE FOR RISK ISSUED/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –397 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTRACTS for 15 days, total 16,076 contracts: OR 80.380 MILLION OZ (1072 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 80.380 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 80.380 MILLION OZ (LARGER THAN LAST MONTH)

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2020 CONTRACTS WITH OUR LOSS IN PRICE OF $0.23 IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD EFP ISSUANCE CONTRACTS: 570 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JULY OF 16.110 MILLION OZ FOLLOWED BY TODAY’S MASSIVE 45,000 OZ QUEUE. JUMP + 0 MILLION OZ EXCHANGE FOR RISK TODAY + (PRIOR EXCHANGE FOR RISK : 5.25 MILLION OZ): TOTAL NOW STANDING 25.450 MILLION OZ NORMAL STANDING + 5.25 MILLION EXCHANGE FOR RISK = 30.700 MILLION OZ.///// .. WE HAVE A HUGE SIZED LOSS OF1450 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG 734//CONSIDERABLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION TO CONTAIN SILVER PRICE’S RISE. THE NEW TAS ISSUANCE TODAY (734) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE./

WE HAD 10 NOTICE(S) FILED TODAY FOR 50,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 7890 CONTRACTS TO 487,232 AND CLOSER TO TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED: 116 CONTRACTS

WE HAD A STRONG SIZED INCREASE IN COMEX OI ( 7890CONTRACTS) WITH OUR $4.65 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JULY. AT 5.1975 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0.0000 TONNE QUEUE JUMP: NEW TOTAL OF GOLD STANDING FOR JULY: 10.345 TONNES// + /A FAIR (AND CRIMINAL) ISSUANCE OF 2445 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH A $4.65 LOSS IN PRICEWITH RESPECT TO MONDAY’S TRADING.WE HAD A STRONG SIZED GAIN OF 10,035 OI CONTRACTS (31.213 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2145CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 487,232

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,035 CONTRACTS WITH 7890 CONTRACTS INCREASED AT THE COMEX// AND A FAIR 2145 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 10,035CONTRACTS OR 31.213 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 2445 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2145 CONTRACTS) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (7890) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 10,035 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JULY AT 5.1975 TONNES FOLLOWED BY TODAY’S 0.0000 TONNE QUEUE JUMP//NEW TOTAL 10.345 TONNES ///// /3) ZERO LONG LIQUIDATION WITH MINOR TAS LIQUIDATION TO CONTAIN GOLD’S PRICE//4) STRONG SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 2445 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

TOTAL EFP CONTRACTS ISSUED: 34,250 CONTRACTS OR 3,425,000 OZ OR 106.53 TONNES IN 15 TRADING DAY(S) AND THUS AVERAGING: 2283 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15 TRADING DAY(S) IN TONNES 106.53 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 106.53/3550 x 100% TONNES 3.00% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 106.53 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A LARGE SIZED 2020 CONTRACTS OI TO 149,974 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 570 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 570and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 570 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2020 CONTRACTS AND ADD TO THE 570 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1450 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 7.25 MILLION OZ

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED UP 67.36 PTS OR 2.13% //Hang Seng CLOSED UP 766.25 PTS OR 4.10% /The Nikkei CLOSED DOWN 18.43 PTS OR 0.06% //Australia’s all ordinaries CLOSED UP 0.50 % /Chinese yuan (ONSHORE) closed UP 7.1466 /OFFSHORE CHINESE YUAN UP TO 7.1412 /Oil UP TO 78.73 dollars per barrel for WTI and BRENT UP AT 82.65 / Stocks in Europe OPENED MOSTLY GREEN// ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 7890CONTRACTS UP TO 487,232 DESPITE OUR LOSS IN PRICE OF $4.65 ON MONDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2145 EFP CONTRACTS WERE ISSUED: : AUGUST 2145 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2145 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 10,035 CONTRACTS IN THAT 2145LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED GAIN OF 7890 COMEX CONTRACTS..AND THIS STRONG SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $4.65//MONDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS A FAIR 2445 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THE HUGE NUMBER OF T.A.S. CONTRACTS INITIATED OVER THE PAST SEVERAL WEEKS SPELLS TROUBLE FOR THE GOLD/SILVER MARKET AS RAIDS WILL SURELY BE UPON US TRYING TO CONTAIN OUR PRECIOUS METALS RISE IN PRICE. IT MAY BE TO NO AVAIL!!

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JULY (10.345) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.345 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $4.65) //// BUT WERE SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD A STRONG SIZED GAIN OF 10,035 CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE TAS LIQUIDATION THROUGHOUT THE MONDAY COMEX SESSION TRYING DESPERATELY TO CONTAIN GOLD’S RISE. THE TAS ISSUED MONDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS. THE MASSIVE T.A.S. ISSUED LAST MONDAY WAS USED THROUGHOUT THE WEEK CONTAINING GOLD’S RISE.

WE HAVE GAINED A TOTAL OI OF 31.261 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY. (5.11974 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 0.0000 TONNES//TOTAL STANDING FOR JULY GOLD: 10.345 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $4.65.

WE HAD + ADDED 116 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST AFTER TRADING ENDED LAST NIGHT

NET GAIN ON THE TWO EXCHANGES 10,035 CONTRACTS OR 1,003,500 OZ OR 31.213 TONNES.

Total monthly oz gold served (contracts) so far this month

3275 notices 327500 OZ 10.1866 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

1 dealer deposit:

i) Into brinks: 31,805.675 oz

total dealer deposits: 31,805.675 oz

total customer deposits: 0 oz

we had 1 customer withdrawals:

i) Out of Brinks 128.604 oz (4 kilobars)

total withdrawals: 128.604 oz

Adjustments; 0/

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 51 contracts having LOST 5 contracts. We had 5 contracts served on Monday. Thus we gained 0 contracts or an additional nil oz of gold will stand at the comex.

AUGUST LOST 30,811 contracts DOWN to 129,559 contracts. We have 4 more reading days before the big August contract delivery month.

SEPT gained 154 contracts to stand at 869

We had 0 contracts filed for today representing nil oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2023. contract month,

we take the total number of notices filed so far for the month (3275 x 100 oz ), to which we add the difference between the open interest for the front month of JULY (51 CONTRACT) minus the number of notices served upon today 0 x 100 oz per contract equals 332,600 OZ OR 10.345 TONNES the number of TONNES standing in this NON active month of July.

thus the INITIAL standings for gold for the JULYcontract month: No of notices filed so far (3275) x 100 oz + (51) {OI for the front month} minus the number of notices served upon today (0) x 100 oz) which equals 332,600oz standing OR 10.345 TONNES

TOTAL COMEX GOLD STANDING: 10.345 TONNES WHICH IS STRONG FOR A NON ACTIVE DELIVERY MONTH.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,274,188.234 OZ

TOTAL REGISTERED GOLD: 11,673,156.913 (363.08 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,601,031.316 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,654,315 OZ (REG GOLD- PLEDGED GOLD) 300.289 tonnes//

END

SILVER/COMEX

JULY 25

//2023// THE JULY 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

687,989.620 oz CNT Delaware JPMorgan Loomis

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

1227,955.463 oz Brinks CNT Delaware

No of oz served today (contracts)

10 CONTRACT(S) (50,000 OZ)

No of oz to be served (notices)

25 contracts (125,000 oz)

Total monthly oz silver served (contracts)

5065 Contracts (25.345,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposit: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 3 deposits customer account:

i) Into Brinks 600,394.340 oz

ii) Into CNT 600,570.608 oz

iii) Into Delaware 26,990.515 oz

total customer deposits: 1,227,915.463 oz

JPMorgan has a total silver weight: 139.331 million oz/277.172 million =50.16% of comex .//

Comex withdrawals 4

i) Out of CNT 1001.11 oz

ii) Out of Delaware 999.800 oz

iii) Our od JPMorgan: 605,660.310 oz

iv) Out of Loomis 80,328.400 oz

total: 687,989.620 oz

adjustments: 1 dealer to customer Brinks

9760.400 oz

TOTAL REGISTERED SILVER: 35.564 MILLION OZ//.TOTAL REG + ELIGIBLE. 277.172 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF JULY /2023 OI: 35 CONTRACTS HAVING GAINED 9 CONTRACT(S). WE HAD 0 NOTICES FILED ON MONDAY SO WE GAINED 9 CONTRACTS OR AN ADDITIONAL 45,000 OZ WILL STAND AT THE COMEX FOR DELIVERY IN JULY,

AUGUST GAINED 2 CONTRACTS TO STAND AT 831

SEPT HAS A LOSS OF 2624 CONTRACTS DOWN TO 122,502

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 10 for 50,000 oz

Comex volumes// est. volume today 52,048 fair /

Comex volume: confirmed yesterday: 58,249 fair

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 5065 x 5,000 oz = 25,345,000 oz

to which we add the difference between the open interest for the front month of JULY(35) and the number of notices served upon today 10 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY/2023 contract month: 5065 (notices served so far) x 5000 oz + OI for the front month of JULY (35) – number of notices served upon today (10 )x 500 oz of silver standing for the JULY contract month equates to 25.450 million oz + 0.0 MILLION OZ EXCHANGE FOR RISK TODAY//PRIOR EXCHANGE FOR RISK TOTALS 5.25 MILLION OZ /NEW TOTAL STANDING FOR DELIVERY: 30.700 MILLION OZ..WE HAVE 35 MILLION OZ OF REGISTERED SILVER AT THE COMEX//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

JULY 25/WITH GOLD UP $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 24/WITH GOLD DOWN $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.20 TONNES OF GOLD INTO THE GLD//: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 21/WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / .////INVENTORY RESTS AT 913.80 TONNES

JULY 20/WITH GOLD DOWN $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 913.80 TONNES

JULY 19/WITH GOLD UP $0.65 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 912.07 TONNES

JULY 18/WITH GOLD UP $23.45 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: .////INVENTORY RESTS AT 912.93 TONNES

JULY 17/WITH GOLD DOWN $6.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD.////INVENTORY RESTS AT 912.93 TONNES

JULY 14/WITH GOLD UP $0.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 914.66 TONNES

JULY 13/WITH GOLD UP $3.30 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.29 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.66 TONNES

JULY 12/WITH GOLD UP $24.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.95 TONNES

JULY 11/WITH GOLD UP $6.15 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.0 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 915.26 TONNES

JULY 10 WITH GOLD DOWN $1.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.60 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 916.26 TONNES.

JULY 7 WITH GOLD UP $16.80 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.86 TONNES.

JULY 6/WITH GOLD DOWN $9.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 917.86 TONNES

JULY 5/WITH GOLD DOWN $2.20 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 2.6 TONNES FROM THE GLD///INVENTORY RESTS AT 921.90 TONNES

JULY 3/WITH GOLD UP $1.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 924.50 TONNES//

JUNE 30/WITH GOLD UP $10.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 924.50 TONNES

JUNE 29/WITH GOLD DOWN $3.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.81 TONNES

JUNE 28/WITH GOLD DOWN $1.15 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 925.65 TONNES

JUNE 27/WITH GOLD DOWN $9.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD./INVENTORY RESTS AT 925.65 TONNES

JUNE 26/WITH GOLD UP $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD/////INVENTORY RESTS AT 927.10 TONNES

JUNE 23/WITH GOLD UP $5.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: WITHDRAWALS OF 4.33 TONNES OF GOLD OVER THE PAST TWO DAYS. /INVENTORY RESTS AT 929.70 TONNES

JUNE 21/WITH GOLD DOWN $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 934.03 TONNES

JUNE 20/WITH GOLD DOWN $22.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.03 TONNES

JUNE 16/WITH GOLD UP $0.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.33 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.03 TONNES

JUNE 15/WITH GOLD UP $2.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 929.70 TONNES

JUNE 14/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 931.44 TONNES

JUNE 13/WITH GOLD DOWN $10.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.01 TONNES FORM THE GLD///INVENTORY RESTS AT 931.44

GLD INVENTORY: 919.00 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 25/WITH SILVER UP 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 826,000 OZ FROM THE SLV..////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 24/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 21/WITH SILVER DOWN 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.101 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 20/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.468 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 454.107 MILLION OZ/

JULY 19/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 18/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 17/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 4.856 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 14/WITH SILVER UP 27 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.21 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 13/WITH SILVER UP 64 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 12/WITH SILVER UP $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.881 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 11/WITH SILVER DOWN 5 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .020 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 464.822 MILLION OZ/

JULY 10/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.672 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 464.802 MILLION OZ

JULY 7/WITH SILVER UP 42 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.474 MILLION OZ

JULY 6/WITH SILVER DOWN 50 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.667 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 466.474 MILLION OZ//

JULY5/WITH SILVER UP 30 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JULY 3/WITH SILVER UP 7 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JUNE 30/WITH SILVER UP 19 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.377 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT468.141 MILLION OZ//

JUNE 29/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.763 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 466.764 MILLION OZ//

JUNE 28/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.527 MILLION OZ//

JUNE 27/WILVER SILVER UP 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 734,000 OZ INTO THE SLV////INVENTORY RESTS AT 470.527 MILLION OZ

JUNE 26/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 469.793 MILLION OZ.

JUNE 23/WITH SILVER DOWN 9 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A NET DEPOSIT OF 6.61 MILLION OZ INTO THE SLV OVER THESE PAST TWO DAYS//INVENTORY RESTS AT 469.793 MILLION OZ//

JUNE 21/WITH SILVER DOWN $.40 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.784 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 20/WITH SILVER DOWN 89 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 16/WITH SILVER UP 23 CENTS TODAY :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 463.183 MILLION OZ

JUNE 15/WITH SILVER DOWN 17 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.377 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 463.642 MILLION OZ//

JUNE 14/WITH SILVER UP 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 735,000 OZ FROM THE SLV///INVENTORY RESTS AT 465.019 MILLION OZ//

JUNE 13/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.515 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 465.754 MILLION OZ//

JUNE 12/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.269 MILLION OZ//

3,Chris Powell of GATA provides to us very important physical commentaries

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES/SILVER

BIX WEIR

very unusual for Newmont to default because of a strike. This is dangerous to our bankers who have massive derivatives (short positions) on silver. There are 100 to one paper to physical silver contracts out there. So let’s watch this one carefully

(Bix Weir)

ALERT! Largest Silver Mine in the World Declares “FORCE MAJEURE!” GOT PHYSICAL SILVER?! (Bix Weir)

The largest Silver mine in the world, Mexico’s Penasquito Mine, has been shut down for 2 months forcing it’s owner, Newmont Mining, to DEFAULT on Silver Deliveries and declare a “Force Majeure!”

A huge story by itself but the FACT that Newmont Mining chose to default on the forward delivery contracts instead of supplementing silver from other operations gives us a glimpse into just how scarce physical silver is!!

BUY! BUY! BUY!

ALERT! Largest Silver Mine in the World Declares “FORCE MAJEURE!” GOT PHYSICAL SILVER?! (Bix Weir)

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1466

OFFSHORE YUAN: UP TO 7.1412

SHANGHAI CLOSED UP 67.36 PTS OR 2.13%

HANG SENG CLOSED UP 766.25 PTS OR 4.10%

2. Nikkei closed DOWN 18.43 PTS OR 0.06%

3. Europe stocks SO FAR: ALL MOSTLY GREEN

USA dollar INDEX UP TO 101.19 EURO FALLS TO 1.1048 DOWN 15 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.466 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 141.43/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ON SHORE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.2423***/Italian 10 Yr bond yield RISES to 4.072*** /SPAIN 10 YR BOND YIELD RISES TO 3.468…**

3i Greek 10 year bond yield RISES TO 3.723

3j Gold at $1961.05 silver at: 24.66 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 32 /100 roubles/dollar; ROUBLE AT 90.14//

3m oil into the 78 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 141.48// 10 YEAR YIELD AFTER BREAKING .54%, RISES TO 0.466% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8687 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9566 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.903 UP 5 BASIS PTS…

USA 30 YR BOND YIELD: 3.957 UP 4 BASIS PTS/

USA 2 YR BOND YIELD: 4.879 UP 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.96…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 7 BASIS PTS AT 4.3115

end

2.a Overnight: Newsquawk and Zero hedge:

US Futures Rise, Chinese Stocks Soar As Politburo Vows Support, FOMC Meeting Begins

TUESDAY, JUL 25, 2023 – 08:16 AM

US futures are higher with bond yields also rising higher in quiet, cautious trade ahead of a barrage of earnings including MSFT and GOOGL later today, as well as central bank announcements tomorrow (the FOMC meeting begins today) and Thursday from the ECB and BOJ. S&P futures were fractionally higher, rising 0.1%, as a surge in Chinese stocks spilled over; Nasdaq 100 futures rose as much as 0.4%, after a weak session Monday, with Microsoft Corp. and Alphabet Inc. due to report their first earnings since artificial-intelligence fever broke out. Shares in both companies were about 0.5% higher in New York pre-market trading as investors waited to see if the results justify the companies’ hefty year-to-date share gains. Treasury yields climbed across the curve, while the dollar and oil both reversed earlier losses; iron ore prices climbed while gold reversed modest gains. Today focus will be on MSFT and GOOGL earnings after the close. On macro, we get Case Shiller, Consumer Confidence and Richmond Fed at 10am ET.

In premarket trading, megacap stocks again lead higher. Shares in General Motors and General Electric gained in premarket trading as both companies raised their earnings guidance, while NXP Semiconductors NV advanced as its results beat expectations. China stock traded in the US rallied after China’s Politburo was far more dovish than expected: HSI and CSI added 4.1% and 2.9% today; FXI closed with a 2.1% gain yesterday. Here are the most notable premarket movers:

Goldman Sachs Group shares slipped as Citi cut its rating on the stock to neutral from buy, saying that the company’s targets are achievable, but it will take time and a better investment banking environment to attain them.

Walmart rises 1.2% in premarket trading after being upgraded to overweight from neutral at Piper Sandler, which said the retailer has a chance to further extend market share gains as grocery inflation subsides. The broker also raises its price target on Walmart to a Street high.

Rackspace Technology falls as much as 4.3% in premarket trading on Tuesday as Citigroup downgrades the infrastructure software company’s stock to sell from neutral, saying the valuation does not reflect the estimated downside potential.

US-listed Chinese stocks extend their rally in premarket trading Tuesday, after Beijing’s pledge to support the economy spurred fresh bets that more stimulus measures could be on the way. Alibaba (BABA US) +1.6%, Baidu +1.8%.

Zevia is downgraded to neutral from buy at Goldman Sachs after the beverage producer reported preliminary 2Q revenue that missed estimates due to supply chain interruptions. The broker said it now sees a balanced risk/reward ratio, and therefore moves to the sidelines.

AMC drops as much as 15% in premarket trading — narrowing the spread between its common and preferred shares — after a Delaware court judge sent a new letter to the company and its shareholders about the movie-theater chain’s stock-conversion plan.

Some 48% of the S&P by market cap, or companies with a market value of $16.3 trillion, are reporting earnings this week. Despite stocks trading near 2023 highs, investors seem unwilling to place big bets, given uncertainty over what signals Federal Reserve and European Central Bank policymakers might send, with the Fed’s potential policy path, especially, crucial for global markets.

“Investors are unlikely to feel safe enough to get into the equities water before such an eventful week,” Mizuho International Plc strategists Evelyne Gomez-Liechti and Helen Rodriguez wrote in a note.

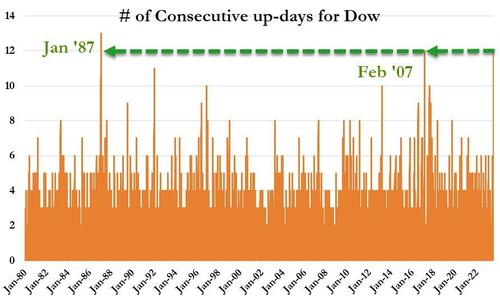

Despite the listless mood, hopes have grown that the US economy will be able to escape a sharp recession. That’s lifted the Dow Jones Industrial Average 5% so far this month, as investors price a better outlook for companies making industrial equipment and heavy machinery. That’s put the Dow index in the midst of its longest winning streak in more than six years.

European shares also edged higher, lifted by resources firms such as Anglo American Plc and Rio Tinto Plc that benefited after China’s Politburo signaled more support. The Stoxx 600 is up 0.2% after the Hang Seng finished with gains of 4.1%. Mining stocks have outperformed while Adidas and Bayer are all higher post-earnings. Among individual movers, consumer-goods giant Unilever Plc stood out, gaining as much as 5.7% after beating sales estimates, while spirits group Remy Cointreau SA surged after Chinese sales helped it surpass forecasts.European market sentiment was dampened by a euro-area bank lending survey which showed a record plunge in loan demand from the bloc’s companies. Alongside a dismal business outlook reading from Germany, the data raise questions over the ECB’s capacity to hike interest rates much beyond the 25 basis points priced for this Thursday’s meeting. Here are some of the most notable European movers:

Unilever shares rise about 5.7% after the consumer-staples company reported better-than-expected second-quarter sales. The beat showed continued volume resilience, according to Morgan Stanley

Adidas shares gained as much as 6.6% in Frankfurt trading after the sale of the sportswear retailer’s inventory of Yeezy sneakers from a canceled partnership with the rapper Kanye West

Randstad rises as much as 4.2%, reversing a decline in early trading, as investors digested a set of results showing second- quarter underlying Ebita beat estimates while the Dutch staffing firm missed on revenue and gross profits

Bayer gained 1.8%, reversing an initial drop of as much as 3.2%, as investors look beyond an expected cut to 2023 guidance following a slew of warnings from chemical companies

Logitech shares gain as much as 6.3% in Zurich after the Swiss maker of computer peripherals boosted its outlook for the first half of fiscal 2024. Sales for gaming and pointing devices beat estimates

Compass shares fall as much as 4.7% after the catering company reported 3Q earnings. Tuesday’s update is “fine,” but “investors may have been looking for slightly more,” according to Barclays

DSV shares decline as much as 6.3%. While the transport and logistics company’s second-quarter Ebit before significant items came in ahead of expectations, the Air & Sea segment missed estimates

Dassault Systemes shares fall as much as 6.1%, their biggest drop since April, after the software firm reported slower growth in key areas from its cloud-based design platform

Elior sinks as much as 10%, biggest intraday drop since May 17, after the French catering company cuts its FY profit margin forecast for the second time this year, citing higher costs due to inflation and new contracts

Thales shares fall as much as 2.7% after the French defense group reached an agreement with Thoma Bravo for the acquisition of 100% of Imperva based on an enterprise value of $3.6 billion

Babcock shares drop as much as 3.9% on Tuesday, snapping an 11-day winning run, as Liberum restarts coverage with a hold rating and says last week’s results were “not as good as they looked”

Idorsia shares tumble as much as 17%, touching an all-time low, after the Swiss pharmaceuticals producer reported an operating loss for 2Q and suspended its 2025 profitability target

Attention is now turning to LVMH, Europe’s biggest company on what it says about Chinese consumer trends in its report later in the day.

Earlier in the session, Asian stocks advanced, lifted by Chinese shares after the country’s top leadership signaled fresh support for the ailing economy, while investors braced for key central bank meetings this week. The MSCI Asia Pacific Index rose as much as 1%, led by material and communication services shares. Most regional markets rallied, with technology and property shares propelling mainland Chinese and Hong Kong benchmarks. Chinese stocks drive Asian equity gains following an ADR rally in New York on Politburo’s pro-growth message. Hang Seng Tech index surges as much as 5.3% and H shares jump more than 4%. The CSI 300 rallied 2.6% – poised for its best day in five months – as developer shares soar the most in seven months.

China’s top leaders on Monday pledged to boost consumption and offer more support for the troubled property sector to help revive a slowing economy. The statement from the Politburo meeting was taken positively by investors, who say the outcome was better than expected. “The Politburo met earlier and was more dovish than expected, promising housing easing, local debt resolution, and a boost to capital markets. It could be a defining moment, akin to October 2018,” Morgan Stanley economists including Robin Xing wrote in a note. “We expect a meaningful growth rebound in 4Q, keeping full-year growth at the government’s target of 5%.”

Other Asian markets are narrowly mixed: Japanese stocks traded in a narrow range as investors awaited policy decisions from the Federal Reserve and the Bank of Japan. The Fed is expected to further raise interest rates, while the BOJ is projected to stand pat as it waits for sustainable inflation. Kospi nudged higher while the ASX 200 was positive with the index led by gains in the mining and energy sectors amid recent strength in underlying commodity prices owing to the Chinese stimulus hopes. Key stock gauges in India closed flat on Tuesday while small and mid-sized companies continued their rally to new peaks as ongoing earnings season unfolds. The S&P BSE Sensex was little changed at 66,355.71 in Mumbai, while the NSE Nifty 50 Index was also flat at 19,680.60. BSE Ltd.’s small- and mid-cap stocks rallied more than 0.3% each.

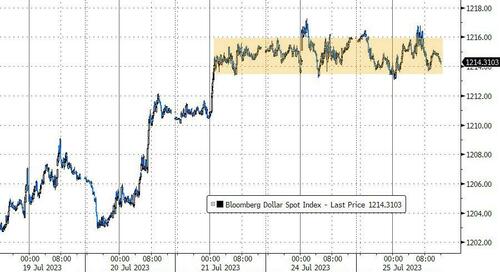

In FX, the Bloomberg’s Dollar Spot Index traded in the red, on track to snap five sessions of gains, while the euro touched a two-week high against the greenback after China signaled renewed support for its struggling economy.

The offshore yuan jumped to its strongest level in more than a week after the People’s Bank of China continued its support for the currency.

The euro dropped and German bonds briefly recovered losses after a bank lending survey released by the European Central Bank showed a bigger-than-expected fall in demand for loans due to higher interest rates. A soft reading for the German business outlook also weighed on the currency.

EUR/GBP declined as much as 0.3% to 0.8603, lowest in a week: The pound rose, on course to end its longest losing streak since March 2020 against the US dollar; GBP/USD rose as much as 0.3% to $1.2865

The Australian dollar led the advance among the Group-of-10 currencies, gaining 0.5% as optimism on China spurred exporters to get some hedging on board before Wednesday’s local inflation data, according to Asia-based FX traders

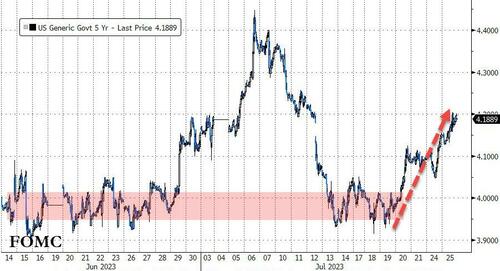

In rates, treasury yields are higher by 2bp-3bp across the curve as the Bloomberg Dollar Spot Index falls 0.1%; 2s10s curve is optically steeper after switch to new 2-year note sold at auction Monday. The new 2-year trades around 4.87% after drawing 4.823% in the auction, highest yield for an auction of the tenor since 2007. Still, vs the 10-year at 3.89% its 98bp spread is tighter than the old 2-year note’s; the higher-yielding old 2-year traded nearly 106bp cheap to the 10- year Monday. Bunds are in the red although they briefly pared declines after German IFO missed expectations. German 10-year yields are up 2bps. Auction cycle continues with $43b 5-year. Apart from new 2-year, benchmark yields are highest since July 12 as wagers that the Fed will raise rates again this year after an expected quarter-point hike at the meeting that concludes Wednesday have increased somewhat. Ahead of auction at 1pm New York time, WI 5-year yield at around 4.15% is higher than 5-year auction stops since October; last month’s drew 4.019%.

Commodity prices were mostly on the rise after Chinese leaders used this week’s Politburo meeting to flag more aid to the economy. Oil prices held near three-month highs, with brent futures trading near $83 while copper and steel-making staple iron ore both rose, given their importance for China’s property sector. US-listed Chinese stocks also extended their rally in premarket trading.

In Crypto, Binance and CEO Zhao are planning to seek a dismissal of the CFTC complaint, according to Bloomberg. Crypto exchange Kraken says it is investigating reports that some clients are experiencing funding delays. UK Information Commission will examine Worldcoin (WDC), a project by OpenAI CEO Sam Altman, according to a spokesperson cited by CoinDesk.

Looking ahead, the US economic calendar includes July Philadelphia Fed non- manufacturing activity at 8:30am, May FHFA house price index and S&P CoreLogic home prices at 9am, and July Conference Board consumer confidence and Richmond Fed manufacturing at 10am; Fed speakers are in self-imposed quiet period ahead of Wednesday’s rate decision

Market Snapshot

S&P 500 futures up 0.2% to 4,591.50

MXAP up 1.3% to 168.30

MXAPJ up 1.9% to 532.87

Nikkei little changed at 32,682.51

Topix up 0.2% to 2,285.38

Hang Seng Index up 4.1% to 19,434.40

Shanghai Composite up 2.1% to 3,231.52

Sensex little changed at 66,334.14

Australia S&P/ASX 200 up 0.5% to 7,339.67

Kospi up 0.3% to 2,636.46

STOXX Europe 600 up 0.2% to 466.57

German 10Y yield little changed at 2.45%

Euro little changed at $1.1063

Brent Futures down 0.3% to $82.46/bbl

Gold spot up 0.3% to $1,960.69

U.S. Dollar Index little changed at 101.33

Top Overnight News

US national security officials are scrutinizing an Abu Dhabi sovereign wealth fund’s planned $3bn takeover of New York-based Fortress Investment Group amid concerns in Washington over the United Arab Emirates’ ties to China. FT

Unilever reported higher than expected underlying sales growth in the first half of the year driven by continued price rises, but sales volumes were flat as the cost of living crisis squeezed consumers. The company said “we have passed peak inflation”, adding that it had moderated its price rises. Prices rose 9.4 per cent in the first half, compared to 13.3 per cent in the fourth quarter of 2022. FT

The slow pace of Ukraine’s counteroffensive against entrenched Russian invaders is dimming hopes that negotiations for an end to the fighting could come this year and raising the specter of an open-ended conflict, according to Western officials. WSJ

Corporate loan demand in the euro area fell the most on record in the second quarter as rate hikes started to bite, an ECB survey showed. Demand for mortgages and other consumer borrowing declined, and lenders expect more tightening to come. Germany is probably still stuck in a recession, Ifo’s head said, as its business outlook worsened in July. BBG

Chipmakers warned that shortages of technicians, engineers and computer scientists are threatening US plans for rapid expansion of the sector. About 115,000 new jobs are expected by 2030 but current graduation rates imply more than half may remain unfilled, an industry body said. BBG

McCarthy says House probes into the foreign business activities of the Biden family rose to the level of an impeachment inquiry. The Hill

DeSantis is no longer Trump’s main rival as the Florida governor’s campaign continues to falter. London Times

The FDIC hit out at some US banks for incorrectly reporting the amount of their uninsured deposits, after dozens of lenders restated their figures downward earlier this year. The regulator said banks were wrong to exclude deposits that were collateralized by pledged assets. The level of uninsured deposits at banks came into focus after the collapse of SVB and Signature Bank. BBG

General Motors has raised its guidance for the second time this year, citing strong customer demand. The Detroit carmaker predicted it will earn between $12bn and $14bn this year, having raised the bar in April when it said it would bring in $12.5bn at most. FT

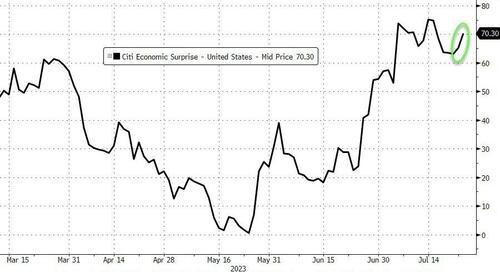

US data surprises have been positive in the last couple of months, while European and China data have undershot…

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mostly higher amid a rally in Chinese stocks after the Politburo’s support pledges, although gains for the rest of the region were capped after soft global PMIs and with some cautiousness heading into risk events. ASX 200 was positive with the index led by gains in the mining and energy sectors amid recent strength in underlying commodity prices owing to the Chinese stimulus hopes. Nikkei 225 lagged as speculation remained rife regarding this week’s BoJ meeting with source reports noting the central bank is to consider a large increase in its 2023 inflation outlook and could raise its forecast to around 2.5%. Hang Seng and Shanghai Comp were boosted with gains led by a surge in property and tech stocks after the Politburo’s support pledges which lifted the Hang Seng Tech Index by around 5%, while the Hang Seng Mainland Properties Index rose by a double-digit percentage from early on as the Politburo’s statement omitted the language that homes are not for speculation.

Top Asian News

China’s NDRC held a meeting with private firms including ANTA (2020 HK), NIO (9866 HK) and TCL where it listened to the companies’ opinions and suggestions on the current economic situation, according to Reuters.

European bourses are managing to eke out marginal gains, Euro Stoxx 50 +0.1%, with macro drivers downbeat since the APAC upside seen on Chinese stimulus. Mining names outperform given Politburo stimulus while Unilever +5.0% is supporting the FTSE 100 and AEX post-earnings; on that point, European heavyweight LVMH reports after the Paris close. Stateside, futures are in the green but only modestly so with specific drivers somewhat light ahead of tomorrow’s FOMC and with numerous large-cap earnings due in- and after-hours today; ES +0.1%.

Top European News

ECB Euro area bank lending survey: net 14% of EZ banks tightened credit standards in Q2 vs. 27% in Q1. Banks expect more moderate net tightening on loans to firms in Q3. The cumulated net tightening since the beginning of 2022 has been substantial. Firms’ net demand for loans fell strongly in the second quarter of 2023, dropping to an all-time low since the start of the survey in 2003.

EU ministers have given the final approval to the EU chips, according to the European Council.

UK pensions regulator warned that pension fund trustees must consider widening the range of their investments including in start-ups and other illiquid assets or face “robust intervention”, according to FT.

5.7 magnitude earthquake occurred in central Turkey, via EMSC.

FX

DXY slips within 101.430-180 range before another boost from the Euro after weak German Ifo.

EUR/USD tests Fib support at 1.1055 from 1.1086 peak near 1bln option expiry interest.

Aussie rebounds alongside Yuan ahead of CPI data, AUD/USD probes 0.6770 expiries from 0.6726 base, USD/CNY and USD/CNH both sub-7.1400 from 7.1600+ and 7.1900 respective highs.

Yen retains recovery momentum vs Dollar between 141.62-21 bounds amidst demand at the overnight Tokyo fix.

Pound holds onto the 1.2800 handle against Buck amidst supportive EUR/GBP tailwinds within 0.8637-03 range.

PBoC set USD/CNY mid-point at 7.1406 vs exp. 7.2044 (prev. 7.1451)

China’s major state-owned banks were seen selling dollars in the offshore and onshore spot FX markets in early Asian trades, according to sources cited by Reuters.

Fixed Income

Bond bears back in the driving seat as post-EU PMI momentum wanes and EGBs only bounce partially after dire German Ifo survey.

Bunds back below par within 133.77-14 range, Gilts remain soft between 96.78-38 parameters irrespective of decent demand for 2038 DMO issuance and T-note nearer 111-23+ trough than 112-01+ peak ahead of US data, consumer confidence and 5 year supply.

BTPs also on the back foot following mixed Italian auctions.

Commodities

WTI and Brent are now mostly softer intraday as the complex came off the best levels seen overnight with added pressure from the German Ifo Survey which, in fitting with yesterday’s PMIs, underscored a worsening economic situation in Germany.

Spot gold continues to oscillate on either side of its 100 DMA (1,962.91/oz) ahead of a triple-threat of central banks including the likes of the FOMC tomorrow, ECB on Thursday, and BoJ on Friday.

Base metals have been underpinned this week by the Chinese Politburo meeting which reignited some optimism in industrials via the hint of further stimulus, albeit the upside is currently capped by the German economic woes telegraphed by the Ifo data.

Agriculture remains a theme as supply risks grow with Chicago Wheat rallying some 10% overnight at one point, whilst corn prices were also supported.

Kremlin says it is impossible to return to lapsed Black Sea Grain deal.

Russian Finance Ministry plans to cut the discount it uses to set taxes on the country’s crude oil exports to USD 20/bbl from USD 25/bbl currently, according to Finance Minister Siluanov cited by Reuters.

Kazakh Energy Minister said there are no issues with shipping Kazakh crude via Russia amid Black Sea tensions.

Kazakhstan’s Tengizchevroil has reduced daily output by 12-13k/T due to unscheduled maintenance, via Deputy Energy Minister.

China’s H1 gold output rose 2.2% Y/Y to 178.6 metric tons and gold consumption rose 16.4% Y/Y to 554.9 metric tons, according to Reuters citing state media.

Geopolitics

White House said the US does not support attacks inside of Russia when asked about the drone strikes in Moscow.

Japan launched a protest against North Korea over its missile launch, while it noted that North Korea’s missile launch is unacceptable and threatens not only Japan but also the regional and international society’s peace and stability.

China’s government said a delegation led by Politburo member Li Hongzhong is to visit North Korea from July 26th. Subsequently, a Russian delegation is to visit North Korea this week, led by the Russian Minister of Defence, via KCNA. Additionally, the Russian Defence Ministry says Defence Minister Shoigu ‘s visit to North Korea will contribute to strengthening military relations between the two countries, via Al Arabiya.

Russian authorities have announced the suspension of navigation within the Gulf of Sevastopol, via Al Arabiya.

China’s Foreign Ministry said a senior official of the Japanese defense ministry has grossly interfered in China’s internal affairs, and China is firmly opposed to this and has lodged stern representations with Japan, via Global Times.

Japan and Italy to hold joint fighter jet drills at Komatsu Base Aug 2-10; Japan and Australia to hold joint fighter jet drills at the Base Aug 23-September 15.

US event calendar

08:30: July Philadelphia Fed Non-Manufactu, prior -16.6

09:00: May S&P CS Composite-20 YoY, est. -2.35%, prior -1.70%

09:00: May S&P/Case-Shiller US HPI YoY, prior -0.24%

09:00: May S&P/CS 20 City MoM SA, est. 0.70%, prior 0.91%

10:00: July Conf. Board Consumer Confidenc, est. 112.0, prior 109.7

July Conf. Board Present Situation, prior 155.3

July Conf. Board Expectations, prior 79.3

10:00: July Richmond Fed Business Conditio, prior -12

July Richmond Fed Index, est. -10, prior -7

DB’s Jim reid concludes the overnight wrap

Sentiment has been a bit more negative than markets over the last 24 hours, as weak data from the flash PMIs for July was a bit worrying. However, DM equities just about shrugged it off and US bonds sold off after a weak 2yr Treasury auction, and traded in completely the opposite direction to the way European bonds did after the weak PMIs. The Chinese stimulus announcement yesterday has turned momentum overnight in their bourses, with Chinese real estate stocks up c.+7%, reducing YTD losses to c.-13.7%, so there’s some interesting global push/pull factors going on at the moment. Markets are now awaiting this week’s round of central bank decisions, multiple data releases, and a raft of earnings over the rest of the week.

As you’ll see in the day ahead, there’s lots to look forward to today including earnings from Microsoft and Alphabet after the bell; however, the one I’m most intrigued about is the latest quarterly ECB bank lending survey. The last survey, conducted in the weeks after the March banking stress, saw our aggregate indicator of BLS credit conditions decline to its weakest since the GFC amid a sharp fall in demand for loans and tightening credit standards. Banks did expect a partial rebound in credit conditions in Q2 so we’ll see if that materialised. It’s tough to disentangle recent shocks (energy spike and regional bank/Credit Suisse crisis) and their recovery, from the cyclical (400bps of hikes in a year). As well as a steer on Europe it might also give us clues as to the all important Fed SLOOS next week.

Back to those flash PMI numbers, it became clear things were surprising on the downside from the get-go in the European session. For instance, the French composite PMI hit a 32-month low of 46.6 (vs. 47.7 expected), whilst the manufacturing PMI hit a 38-month low of 44.5 (vs. 46.0 expected). Then in Germany, the composite PMI fell to an 8-month low of 48.3 (vs. 49.8 expected), with the manufacturing PMI diving deeper into contractionary territory, falling to a 38-month low of 38.8 (vs. 41.0 expected). That was then followed up by the Euro Area-wide numbers, where the composite PMI also hit an 8-month low of 48.9 (vs. 49.6 expected).

Outside of the Euro Area the picture was a bit brighter, but to be frank it still wasn’t great. In the US, the composite PMI fell to a 5-month low of 52.0 (vs. 53.0 expected), which added to the signs from other indicators that the economy is decelerating. Likewise in the UK, the composite PMI hit a 6-month low of 50.7 (vs. 52.3 expected). So in both cases the composite PMI was still above the 50-mark that separates expansion from contraction, but the numbers were weaker than expected.

Those prints led to a decent sovereign bond rally across Europe, with yields on 10yr bunds (-4.9bps), OATs (-4.7bps) and BTPs (-4.6bps) all moving lower. In part, that was because of growing doubts that the ECB would deliver another hike in September after their move this week. For example, expectations of a second hike by September were down from 65% on Friday to 58% by the close yesterday, so it’s becoming increasingly balanced in terms of market pricing.

For US Treasuries however, it was a somewhat different story ahead of the Fed’s decision tomorrow. 2yr yields were up an impressive +7.7bps to 4.92% given the global data. The sell-off accelerated after the European close as we saw a $42bn auction of 2-year notes issued at 4.823%, the highest interest rate since 2007. The move in the 10yr was more moderate, with a +3.5bps sell-off to 3.87%. Higher inflation breakevens drove things, with the 10yr breakeven up +4.7bps to 2.40%, marking its highest level since SVB’s collapse in early March. The bond sell-off came as investors raised their Fed funds expectations, with the December 2024 pricing up +11.0bps on Monday to 4.145%.

That shift in inflation expectations came against the backdrop of significant commodity price moves yesterday. For instance, wheat (+8.60%) hit a 5-month high, following a Russian attack in Ukrainian ports of Reni and Izmail on the Danube river, which have been used for grain exports. Other agricultural goods have also been affected, with corn (+5.97%) and soybeans (+1.62%) both rising in trading yesterday. Energy prices also moved higher, with Brent crude oil prices (+2.06%) at a 3-month high of $82.74/bbl, while WTI oil prices (+2.17% to $78.74/bbl) outperformed following news of a refinery outage in the US. In aggregate, it’s clear that we’re experiencing one of the strongest commodity advances of the last year now.

Those commodity price moves were helpful for energy stocks, which lifted a broader rally across several equity indices. Among others, the S&P 500 rose +0.40% to close just shy of its 15-month high last week. And there was a particular milestone for the Dow Jones (+0.52%), which rose for an 11th consecutive session for the first time since February 2017. That run of advances in 2017 lasted for 12 consecutive sessions, so another positive day today would match that. And if there were a 13th gain tomorrow, that would match a record last set in January 1987. Meanwhile in Europe, the STOXX 600 (+0.06%) still posted a very modest gain despite the disappointing PMI data.

In other economic news on Monday, we got a readout from a key economic policy meeting of China’s Politburo, which showed an increased focus on the “new difficulties and challenges” facing the economy. The meeting did not offer immediate stimulus measures but our China economists see the meeting as setting an encouraging tone for stronger policy easing down the road. See their reaction note here for more details.

Asian equity markets are mostly higher this morning as a result. The Hang Seng (+3.17%) is leading gains buoyed by locally-listed Chinese stocks while the CSI (+2.49%) and the Shanghai Composite (+1.87%) are also trading sharply higher with property leading the gains. Elsewhere, the KOSPI (+0.09%) is swinging between gains and losses with the Nikkei (-0.43%) bucking the regional trend. US stock futures are fairly flat.

Early morning data showed that South Korea’s seasonally adjusted GDP expanded +0.6% in April-June on a quarterly basis (v/s +0.5% expected) following a +0.3% increase in the preceding three months, despite a decline in exports.

To the day ahead now, and data releases from the US include the Conference Board’s consumer confidence measure and the Richmond Fed’s manufacturing index for July. Alongside that, there’s the FHFA house price index for May. Over in Germany, there’s the Ifo business climate indicator for July. From central banks, we’ll get the Euro Area bank lending survey. Finally, today’s earnings releases include Microsoft, Alphabet, Visa, General Motors, General Electric and Spotify

2 b) NOW NEWSQUAWK (EUROPE/REPORT)/ASIA REPORT

EUROPE

US futures positive ahead of key US earnings, EUR lags post-Ifo & Fixed pressured – Newsquawk US Market Open

TUESDAY, JUL 25, 2023 – 05:47 AM

European bourses & US futures are incrementally positive ahead of numerous key earnings from both sides of the pond

DXY slipped to 101.18 before deriving support from an Ifo/ECB BLS driven hit to the Euro, AUD leads pre-CPI

Core benchmarks are modestly pressured as earlier upside dissipates despite a strong DMO sale, US 5yr due

German Ifo shows a return to growth contraction in Q3 while the ECB survey illustrates the ongoing impact of policy tightening

Crude trims APAC gains on German growth concerns while metals welcome Chinese stimulus, XAU near the 100-DMA

Looking ahead, highlights include US Consumer Confidence, Supply from the US, Earnings from EssilorLuxottica, Kering, LVMH, Microsoft, Alphabet, Visa, Moody’s & GE.

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

European bourses are managing to eke out marginal gains, Euro Stoxx 50 +0.1%, with macro drivers downbeat since the APAC upside seen on Chinese stimulus.

Mining names outperform given Politburo stimulus while Unilever +5.0% is supporting the FTSE 100 and AEX post-earnings; on that point, European heavyweight LVMH reports after the Paris close.

Stateside, futures are in the green but only modestly so with specific drivers somewhat light ahead of tomorrow’s FOMC and with numerous large-cap earnings due in- and after-hours today; ES +0.1%.

Click here and here for a recap of the main European equity updates.

FX

DXY slips within 101.430-180 range before another boost from the Euro after weak German Ifo.

EUR/USD tests Fib support at 1.1055 from 1.1086 peak near 1bln option expiry interest.

Aussie rebounds alongside Yuan ahead of CPI data, AUD/USD probes 0.6770 expiries from 0.6726 base, USD/CNY and USD/CNH both sub-7.1400 from 7.1600+ and 7.1900 respective highs.

Yen retains recovery momentum vs Dollar between 141.62-21 bounds amidst demand at the overnight Tokyo fix.

Pound holds onto the 1.2800 handle against Buck amidst supportive EUR/GBP tailwinds within 0.8637-03 range.

PBoC set USD/CNY mid-point at 7.1406 vs exp. 7.2044 (prev. 7.1451)

China’s major state-owned banks were seen selling dollars in the offshore and onshore spot FX markets in early Asian trades, according to sources cited by Reuters.

Bond bears back in the driving seat as post-EU PMI momentum wanes and EGBs only bounce partially after dire German Ifo survey.

Bunds back below par within 133.77-14 range, Gilts remain soft between 96.78-38 parameters irrespective of decent demand for 2038 DMO issuance and T-note nearer 111-23+ trough than 112-01+ peak ahead of US data, consumer confidence and 5 year supply.

BTPs also on the back foot following mixed Italian auctions.

WTI and Brent are now mostly softer intraday as the complex came off the best levels seen overnight with added pressure from the German Ifo Survey which, in fitting with yesterday’s PMIs, underscored a worsening economic situation in Germany.

Spot gold continues to oscillate on either side of its 100 DMA (1,962.91/oz) ahead of a triple-threat of central banks including the likes of the FOMC tomorrow, ECB on Thursday, and BoJ on Friday.

Base metals have been underpinned this week by the Chinese Politburo meeting which reignited some optimism in industrials via the hint of further stimulus, albeit the upside is currently capped by the German economic woes telegraphed by the Ifo data.

Agriculture remains a theme as supply risks grow with Chicago Wheat rallying some 10% overnight at one point, whilst corn prices were also supported.

Kremlin says it is impossible to return to lapsed Black Sea Grain deal.

Russian Finance Ministry plans to cut the discount it uses to set taxes on the country’s crude oil exports to USD 20/bbl from USD 25/bbl currently, according to Finance Minister Siluanov cited by Reuters.

Kazakh Energy Minister said there are no issues with shipping Kazakh crude via Russia amid Black Sea tensions.

Kazakhstan’s Tengizchevroil has reduced daily output by 12-13k/T due to unscheduled maintenance, via Deputy Energy Minister.

China’s H1 gold output rose 2.2% Y/Y to 178.6 metric tons and gold consumption rose 16.4% Y/Y to 554.9 metric tons, according to Reuters citing state media.

ECB Euro area bank lending survey: net 14% of EZ banks tightened credit standards in Q2 vs. 27% in Q1. Banks expect more moderate net tightening on loans to firms in Q3. The cumulated net tightening since the beginning of 2022 has been substantial. Firms’ net demand for loans fell strongly in the second quarter of 2023, dropping to an all-time low since the start of the survey in 2003. Click here for more detail.

EU ministers have given the final approval to the EU chips, according to the European Council.

UK pensions regulator warned that pension fund trustees must consider widening the range of their investments including in start-ups and other illiquid assets or face “robust intervention”, according to FT.

5.7 magnitude earthquake occurred in central Turkey, via EMSC.

DATA RECAP

German Ifo Business Climate New (Jul) 87.3 vs. Exp. 88.0 (Prev. 88.5); German GDP is likely to shrink in Q3.

German Ifo Expectations New (Jul) 83.5 vs. Exp. 83.0 (Prev. 83.6); Current Conditions New (Jul) 91.3 vs. Exp. 93.0 (Prev. 93.7)

GEOPOLITICS

White House said the US does not support attacks inside of Russia when asked about the drone strikes in Moscow.

Japan launched a protest against North Korea over its missile launch, while it noted that North Korea’s missile launch is unacceptable and threatens not only Japan but also the regional and international society’s peace and stability.

China’s government said a delegation led by Politburo member Li Hongzhong is to visit North Korea from July 26th. Subsequently, a Russian delegation is to visit North Korea this week, led by the Russian Minister of Defence, via KCNA. Additionally, the Russian Defence Ministry says Defence Minister Shoigu ‘s visit to North Korea will contribute to strengthening military relations between the two countries, via Al Arabiya.

Russian authorities have announced the suspension of navigation within the Gulf of Sevastopol, via Al Arabiya.

China’s Foreign Ministry said a senior official of the Japanese defense ministry has grossly interfered in China’s internal affairs, and China is firmly opposed to this and has lodged stern representations with Japan, via Global Times.

Japan and Italy to hold joint fighter jet drills at Komatsu Base Aug 2-10; Japan and Australia to hold joint fighter jet drills at the Base Aug 23-September 15.

CRYPTO

Binance and CEO Zhao are planning to seek a dismissal of the CFTC complaint, according to Bloomberg.

Crypto exchange Kraken says it is investigating reports that some clients are experiencing funding delays.

UK Information Commission will examine Worldcoin (WDC), a project by OpenAI CEO Sam Altman, according to a spokesperson cited by CoinDesk.

APAC TRADE

APAC stocks traded mostly higher amid a rally in Chinese stocks after the Politburo’s support pledges, although gains for the rest of the region were capped after soft global PMIs and with some cautiousness heading into risk events.

ASX 200 was positive with the index led by gains in the mining and energy sectors amid recent strength in underlying commodity prices owing to the Chinese stimulus hopes.

Nikkei 225 lagged as speculation remained rife regarding this week’s BoJ meeting with source reports noting the central bank is to consider a large increase in its 2023 inflation outlook and could raise its forecast to around 2.5%.

Hang Seng and Shanghai Comp were boosted with gains led by a surge in property and tech stocks after the Politburo’s support pledges which lifted the Hang Seng Tech Index by around 5%, while the Hang Seng Mainland Properties Index rose by a double-digit percentage from early on as the Politburo’s statement omitted the language that homes are not for speculation.

NOTABLE ASIA-PAC HEADLINES

China’s NDRC held a meeting with private firms including ANTA (2020 HK), NIO (9866 HK) and TCL where it listened to the companies’ opinions and suggestions on the current economic situation, according to Reuters.

DATA RECAP

South Korean GDP QQ (Q2 A) 0.6% vs. Exp. 0.5% (Prev. 0.3%); YY (Q2 A) 0.9% vs. Exp. 0.8% (Prev. 0.9%)

2 c. ASIAN AFFAIRS

ASIAN AND AUSTRALIAN CLOSINGS//EUROPE OPENING TRADING:

TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED UP 67.36 PTS OR 2.13% //Hang Seng CLOSED UP 766.25 PTS OR 4.10% /The Nikkei CLOSED DOWN 18.43 PTS OR 0.06% //Australia’s all ordinaries CLOSED UP 0.50 % /Chinese yuan (ONSHORE) closed UP 7.1466 /OFFSHORE CHINESE YUAN UP TO 7.1412 /Oil UP TO 78.73 dollars per barrel for WTI and BRENT UP AT 82.65 / Stocks in Europe OPENED MOSTLY GREEN// ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

2 d./NORTH KOREA/ SOUTH KOREA/

////SOUTH KOREA/CHINA

END

2e) JAPAN

JAPAN/

END

3 CHINA /

CHINA/

China stocks surge after its Politburo meeting where they are targeting more stimulus. The meeting was more dovish than expected

(zerohedge)

China Stocks Surge After Politburo Meeting More Dovish Than Expected

MONDAY, JUL 24, 2023 – 05:20 PM

The Politburo of the Chinese Communist Party held its July meeting today, and according to the statement, policymakers acknowledged the insufficient domestic demand and economic growth difficulties, and in particular highlighted the new developments related to supply and demand of the housing market: “Housing is for living in, not for speculation” was deleted from today’s statement. The authority pledged to strengthen countercyclical policy adjustment, and push forward high-quality development.

Main points: