JULY 27/SPREADER AND TAS INDUCED RAID ON OUR PRECIOUS METALS: GOLD CLOSED DOWN $21.80 TO $1947.10//SILVER CLOSED DOWN 59 CENTS TO $24.21//PLATINUM CLOSED DOWN $25.80 TO $939.00//PALLADIUM CLOSED DOWN $50.05 TO $1244.95//ECB HIKES BY 25 BASIS POINTS AS EXPECTED//UPDATES ON UKRAINE VS RUSSIA//COVID UPDATES//DR PAUL ALEXANDER//HOUSING PERMIT DATA FROM THE USA//YELLOW TO SEEK BANKRUPTCY PROTECTION ON MONDAY///SWAMP STORIES FOR YOU TONIGHT…

190 H BMO CAPITAL 6 435 H SCOTIA CAPITAL 3 624 H BOFA SECURITIES 23 690 C ABN AMRO 15 737 C ADVANTAGE 1

TOTAL: 24 24 MONTH TO DATE: 3,306

JPMorgan stopped 0/24 contracts.

FOR JULY:

GOLD: NUMBER OF NOTICES FILED FOR JULY/2023. CONTRACT: 24 NOTICES FOR 2400 OZ or 0.07465 TONNES

total notices so far: 3306 contracts for 330,600 oz (10.2830 tonnes)

FOR JULY:

SILVER NOTICES: 32 NOTICE(S) FILED FOR 160,000 OZ/

total number of notices filed so far this month : 5127 for 25,635,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $21.80

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//

INVENTORY RESTS AT 917.26 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN $0.59 AT THE SLV// NO CHANGES IN SILVER INVENTORY AT THE SLV:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 452.480 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 647 CONTRACTS TO 146M281 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS STRONG SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.15 GAIN IN SILVER PRICING AT THE COMEX ON THURSDAY. TAS ISSUANCE WAS A STRONG SIZED 422 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 422 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.15). BUT WERE UNSUCCESSFUL IN KNOCKING SOME SPEC LONGS AS WE HAD A STRONG LOSS ON OUR TWO EXCHANGES OF 583CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 5.25MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO (TAS) MANIPULATION.

WE MUST HAVE HAD:

A TINY ISSUANCE OF EXCHANGE FOR PHYSICALS( 64 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 16.110 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 80,000 QUEUE JUMP + 0 MILLION OZ EXCHANGE FOR RISK FOR TODAY//NEW STANDING: 25.680 MILLION OZ + 5.25 MILLION OZ EXCHANGE FOR RISK/PRIOR: NEW TOTAL 30.93 MILLION OZ// // GOOD SIZED COMEX OI GAIN/ TINY SIZED EFP ISSUANCE/VI) GOOD NUMBER OF T.A.S. CONTRACT ISSUANCE (422CONTRACTS)/ZERO EXCHANGE FOR RISK ISSUED/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –1064 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTRACTS for 17 days, total 16,840 contracts: OR 84.200 MILLION OZ (990 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 84.200 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 84.200 MILLION OZ (SMALLER THAN LAST MONTH)

RESULT: WE HAD A GOOD SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 647 CONTRACTS DESPITE OUR GAIN IN PRICE OF $0.15 IN SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A TINY EFP ISSUANCE CONTRACTS: 64 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JULY OF 16.110 MILLION OZ FOLLOWED BY TODAY’S HUGE 80,000 OZ QUEUE. JUMP + 0 MILLION OZ EXCHANGE FOR RISK TODAY + (PRIOR EXCHANGE FOR RISK : 5.25 MILLION OZ): TOTAL NOW STANDING 25.680 MILLION OZ NORMAL STANDING + 5.25 MILLION EXCHANGE FOR RISK = 30.93 MILLION OZ.///// .. WE HAVE A GOOD SIZED LOSS OF583 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A GOOD 422//CONSIDERABLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION TO CONTAIN SILVER PRICE’S RISE. THE NEW TAS ISSUANCE TODAY (422) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE./

WE HAD 32 NOTICE(S) FILED TODAY FOR 160,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2569 CONTRACTS TO 473,607 AND CLOSER TO TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED: 2569 CONTRACTS

WE HAD A FAIR SIZED DECREASE IN COMEX OI ( 2569CONTRACTS) DESPITE OUR STRONG $6.35 GAIN IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JULY. AT 5.1975 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0.09953 TONNE E.F.P. JUMP TO LONDON: NEW TOTAL OF GOLD STANDING FOR JULY: 10.2861 TONNES// + /A FAIR (AND CRIMINAL) ISSUANCE OF 2354 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH A $6.35 GAIN IN PRICEWITH RESPECT TO WEDNESDAY’S TRADING.WE HAD A FAIR SIZED LOSS OF 1780 OI CONTRACTS (5.537 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4349CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 473,607

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1780 CONTRACTS WITH 2569 CONTRACTS DECREASED AT THE COMEX// AND A GOOD 4349 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1780CONTRACTS OR 5.537 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 2354 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4349 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (2569) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 1780 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JULY AT 5.1975 TONNES FOLLOWED BY TODAY’S 0.09953 TONNE E.F.P. JUMP TO LONDON//NEW TOTAL REDUCES TO 10.2861 TONNES ///// /3) ZERO LONG LIQUIDATION WITH STRONG TAS LIQUIDATION AND SPREADER LIQUIDATION TO CONTAIN GOLD’S PRICE//4) TINY SIZED COMEX OPEN INTEREST GAIN/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 2354 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

TOTAL EFP CONTRACTS ISSUED: 43,187 CONTRACTS OR 4,318,700 OZ OR 134.32 TONNES IN 17 TRADING DAY(S) AND THUS AVERAGING: 2540 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAY(S) IN TONNES 134.32 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 134.32/3550 x 100% TONNES 3.77% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 134.32 TONNES (WEAKER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A FAIR SIZED 647 CONTRACTS OI TO 146,251 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 64 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 64and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 64 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 647 CONTRACTS AND ADD TO THE 64 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A FAIR SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 583 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 2.915 MILLION OZ

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING//WEDNESDAY NIGHT

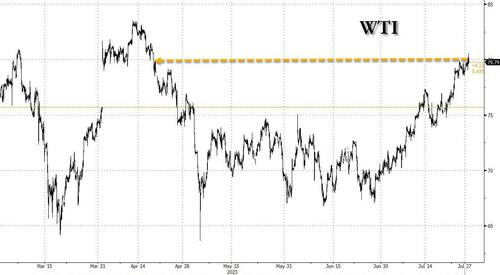

SHANGHAI CLOSED DOWN 6.36 PTS OR 0.20% //Hang Seng CLOSED UP 273.97 PTS OR 1.41% /The Nikkei CLOSED UP 222.82 PTS OR 0.68% //Australia’s all ordinaries CLOSED UP 0.72 % /Chinese yuan (ONSHORE) closed UP 7.1475 /OFFSHORE CHINESE YUAN UP TO 7.1534 /Oil UP TO 79.65 dollars per barrel for WTI and BRENT UP AT 83.70 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 2569CONTRACTS UP TO 473,607 DESPITE OUR STRONG GAIN IN PRICE OF $6.35 ON WEDNESDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4349 EFP CONTRACTS WERE ISSUED: : AUGUST 4349 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4349 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1780 CONTRACTS IN THAT 4349LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED LOSS OF 2569 COMEX CONTRACTS..AND THIS GOOD SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR STRONG GAIN IN PRICE OF $6.35//WEDNESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT WAS A FAIR 2354 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THE HUGE NUMBER OF T.A.S. CONTRACTS INITIATED OVER THE PAST SEVERAL WEEKS SPELLS TROUBLE FOR THE GOLD/SILVER MARKET AS RAIDS WILL SURELY BE UPON US TRYING TO CONTAIN OUR PRECIOUS METALS RISE IN PRICE. IT MAY BE TO NO AVAIL!!

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JULY (10.2861) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $6.35) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED LOSS OF 1780 CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE TAS LIQUIDATION THROUGHOUT THE WEDNESDAY COMEX SESSION TRYING DESPERATELY TO CONTAIN GOLD’S RISE. THE TAS ISSUED WEDNESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS. WE ALSO HAD SOME SPREADER COMEX LIQUIDATION TODAY TOGETHER WITH THE T.A.S. LIQUIDATION CONTAINING GOLD’S RISE A BIT.

WE HAVE GAINED A TOTAL OI OF 5.537 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY. (5.11974 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 0.09953 TONNES//TOTAL STANDING FOR JULY GOLD REDUCES TO: 10.2861 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR STRONG GAIN IN PRICE TO THE TUNE OF $6.35.

WE HAD – REMOVED 2429 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 1780 CONTRACTS OR 178,000 OZ OR 5.537 TONNES.

Total monthly oz gold served (contracts) so far this month

3306 notices 330600 OZ 10.2830 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

1 dealer deposit:

i) Into ASAHI: 31,940.900 oz

total dealer deposits: 31,940.900 oz

total customer deposits: 0 oz

we had 0 customer withdrawals:

total withdrawals: nil

Adjustments; 1 / customer to dealer//JPMorgan: 385,811.955 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 25 contracts having LOST 39 contracts. We had 7 contracts served on Wednesday. Thus we lost 32 contracts or an additional 3200 oz of gold will not stand at the comex as these guys were EFP’d through a transfer to take delivery over in England.

AUGUST LOST 34,012 contracts DOWN to 56,540 contracts. We have 2 more reading days before the big August contract delivery month.

SEPT gained 168 contracts to stand at 1164

We had 24 contracts filed for today representing 2400 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 24 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2023. contract month,

we take the total number of notices filed so far for the month (3306 x 100 oz ), to which we add the difference between the open interest for the front month of JULY (25 CONTRACT) minus the number of notices served upon today 24 x 100 oz per contract equals 330,700 OZ OR 10.2861 TONNES the number of TONNES standing in this NON active month of July.

thus the INITIAL standings for gold for the JULYcontract month: No of notices filed so far (3306) x 100 oz + (xx) {OI for the front month} minus the number of notices served upon today (24) x 100 oz) which equals 330,700oz standing OR 10.2861 TONNES

TOTAL COMEX GOLD STANDING: 10.2861 TONNES WHICH IS STRONG FOR A NON ACTIVE DELIVERY MONTH.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,337,753.171 OZ

TOTAL REGISTERED GOLD: 12,122,919.622 (377.07 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,214,833.549 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,092,498 OZ (REG GOLD- PLEDGED GOLD) 313.92 tonnes//

END

SILVER/COMEX

JULY 27

//2023// THE JULY 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

8245.420 oz

Delaware

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

2017.200 oz Delaware

No of oz served today (contracts)

32 CONTRACT(S) (160,000 OZ)

No of oz to be served (notices)

9 contracts (45,000 oz)

Total monthly oz silver served (contracts)

5127 Contracts (25,635,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposit: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i) Into Delaware: 2017.200 oz

total customer deposits: 2017.200 oz

JPMorgan has a total silver weight: 139.331 million oz/278.572 million =49.91% of comex .//

Comex withdrawals 1

i) Out of Delaware 8245.420 oz

total: 8245.42 oz

TOTAL REGISTERED SILVER: 32.272 MILLION OZ//.TOTAL REG + ELIGIBLE. 278.572 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF JULY /2023 OI: 41 CONTRACTS HAVING LOST 11 CONTRACT(S). WE HAD 26 NOTICES FILED ON WEDNESDAY SO WE GAINED 16 CONTRACTS OR AN ADDITIONAL 80,000 OZ WILL STAND AT THE COMEX FOR DELIVERY IN JULY,

AUGUST LOST 12 CONTRACTS TO STAND AT 814

SEPT HAS A LOSS OF 1339 CONTRACTS DOWN TO 118,767

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 32 for 160,000 oz

Comex volumes// est. volume today 83,353 strong/raid /

Comex volume: confirmed yesterday: 59,768 fair

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 5127 x 5,000 oz = 25,635,000 oz

to which we add the difference between the open interest for the front month of JULY(41) and the number of notices served upon today 32 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY/2023 contract month: 5127 (notices served so far) x 5000 oz + OI for the front month of JULY (41) – number of notices served upon today (32 )x 500 oz of silver standing for the JULY contract month equates to 25.680 million oz + 0.0 MILLION OZ EXCHANGE FOR RISK TODAY//PRIOR EXCHANGE FOR RISK TOTALS 5.25 MILLION OZ /NEW TOTAL STANDING FOR DELIVERY: 30.93 MILLION OZ..WE HAVE 32 MILLION OZ OF REGISTERED SILVER AT THE COMEX//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

JULY 27/WITH GOLD DOWN $21.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 917.26 TONNES

JULY 26/WITH GOLD UP $6.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 25/WITH GOLD UP $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 24/WITH GOLD DOWN $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.20 TONNES OF GOLD INTO THE GLD//: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 21/WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / .////INVENTORY RESTS AT 913.80 TONNES

JULY 20/WITH GOLD DOWN $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 913.80 TONNES

JULY 19/WITH GOLD UP $0.65 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 912.07 TONNES

JULY 18/WITH GOLD UP $23.45 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: .////INVENTORY RESTS AT 912.93 TONNES

JULY 17/WITH GOLD DOWN $6.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD.////INVENTORY RESTS AT 912.93 TONNES

JULY 14/WITH GOLD UP $0.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 914.66 TONNES

JULY 13/WITH GOLD UP $3.30 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.29 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.66 TONNES

JULY 12/WITH GOLD UP $24.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.95 TONNES

JULY 11/WITH GOLD UP $6.15 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.0 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 915.26 TONNES

JULY 10 WITH GOLD DOWN $1.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.60 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 916.26 TONNES.

JULY 7 WITH GOLD UP $16.80 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.86 TONNES.

JULY 6/WITH GOLD DOWN $9.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 917.86 TONNES

JULY 5/WITH GOLD DOWN $2.20 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 2.6 TONNES FROM THE GLD///INVENTORY RESTS AT 921.90 TONNES

JULY 3/WITH GOLD UP $1.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 924.50 TONNES//

JUNE 30/WITH GOLD UP $10.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 924.50 TONNES

JUNE 29/WITH GOLD DOWN $3.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.81 TONNES

JUNE 28/WITH GOLD DOWN $1.15 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 925.65 TONNES

JUNE 27/WITH GOLD DOWN $9.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD./INVENTORY RESTS AT 925.65 TONNES

JUNE 26/WITH GOLD UP $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD/////INVENTORY RESTS AT 927.10 TONNES

JUNE 23/WITH GOLD UP $5.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: WITHDRAWALS OF 4.33 TONNES OF GOLD OVER THE PAST TWO DAYS. /INVENTORY RESTS AT 929.70 TONNES

JUNE 21/WITH GOLD DOWN $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 934.03 TONNES

JUNE 20/WITH GOLD DOWN $22.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.03 TONNES

JUNE 16/WITH GOLD UP $0.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.33 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.03 TONNES

JUNE 15/WITH GOLD UP $2.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 929.70 TONNES

JUNE 14/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 931.44 TONNES

JUNE 13/WITH GOLD DOWN $10.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.01 TONNES FORM THE GLD///INVENTORY RESTS AT 931.44

GLD INVENTORY: 917.26 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 27/WITH SILVER DOWN 59 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ

JULY 26/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 25/WITH SILVER UP 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 826,000 OZ FROM THE SLV..////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 24/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 21/WITH SILVER DOWN 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.101 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 20/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.468 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 454.107 MILLION OZ/

JULY 19/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 18/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 17/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 4.856 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 14/WITH SILVER UP 27 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.21 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 13/WITH SILVER UP 64 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 12/WITH SILVER UP $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.881 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 11/WITH SILVER DOWN 5 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .020 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 464.822 MILLION OZ/

JULY 10/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.672 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 464.802 MILLION OZ

JULY 7/WITH SILVER UP 42 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.474 MILLION OZ

JULY 6/WITH SILVER DOWN 50 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.667 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 466.474 MILLION OZ//

JULY5/WITH SILVER UP 30 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JULY 3/WITH SILVER UP 7 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JUNE 30/WITH SILVER UP 19 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.377 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT468.141 MILLION OZ//

JUNE 29/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.763 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 466.764 MILLION OZ//

JUNE 28/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.527 MILLION OZ//

JUNE 27/WILVER SILVER UP 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 734,000 OZ INTO THE SLV////INVENTORY RESTS AT 470.527 MILLION OZ

JUNE 26/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 469.793 MILLION OZ.

JUNE 23/WITH SILVER DOWN 9 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A NET DEPOSIT OF 6.61 MILLION OZ INTO THE SLV OVER THESE PAST TWO DAYS//INVENTORY RESTS AT 469.793 MILLION OZ//

JUNE 21/WITH SILVER DOWN $.40 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.784 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 20/WITH SILVER DOWN 89 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 16/WITH SILVER UP 23 CENTS TODAY :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 463.183 MILLION OZ

JUNE 15/WITH SILVER DOWN 17 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.377 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 463.642 MILLION OZ//

JUNE 14/WITH SILVER UP 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 735,000 OZ FROM THE SLV///INVENTORY RESTS AT 465.019 MILLION OZ//

JUNE 13/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.515 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 465.754 MILLION OZ//

JUNE 12/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.269 MILLION OZ//

CLOSING INVENTORY 452.480 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

(Schiff Gold)

Millennials Investing In More Gold Than Boomers Or X-ers

Millennials are buying more gold than Boomers or Gen-X, according to a recent survey. But there’s a catch. Millennials are also more likely to invest in paper gold instead of physical metal.

According to the report by State Street, on average, Millennials have 17% of their portfolios allocated to gold. Boomers and X-ers lag with a 10% allocation on average.

About 88% of the investors surveyed who hold gold called it a long-term investment. More than 70% reported that gold boosted the overall performance of their portfolios.

More than half of the respondents who currently invest in gold said they plan to increase their allocation in the next six to 12 months.

But digging a little deeper, we find that Millennials are also more likely to invest in gold Exchange Traded Funds (ETFs) instead of gold bars or gold coins.

Sixty-five percent of Millennials said ETFs were the best way to invest in gold compared to Boomers at 55%. X-ers are far more likely to invest in physical gold. Only 35% of Gen-X respondents said they thought ETFs were the best way to hold gold.

While ETFs provide exposure to the price of gold and can serve a similar role in a portfolio, owning shares of a gold ETF is not the same as owning gold.

ETFs are backed by physical gold held by the issuer and are traded on the market like stocks. They allow investors to play gold without having to buy full ounces of gold at spot price. Since their purchase is just a number in a computer, they can trade their investment into another stock or cash pretty much whenever they want, even multiple times on the same day. Many speculative investors appreciate this liquidity.

There are also gold mining ETFs that track the value of gold mining companies and also generally follow the price of gold. These are very popular with speculative commodity investors.

There are good reasons to invest in ETFs, but they aren’t a substitute for owning physical metal. In an overall investment strategy, SchiffGold recommends buying gold bullion first.

When considering gold-backed ETFs, you should always keep in mind that you don’t own the gold. Buying the most common ETFs does not entitle you to any actual amount of the precious metal.

Having physical metal in your possession is particularly important in the event of an economic meltdown. Think about it: what would you rather have in your possession during a crisis – a piece of paper, or a physical asset recognized as real money all over the world?

Gold-backed ETFs are prized for their liquidity and ease of transfer, but during a period of economic chaos, those characteristics would likely vanish. Crisis creates uncertainty. Panicked people won’t value paper that may or may not represent a tangible asset. But they will value physical metal that they can hold in their hands.

In the event of an economic collapse, barter could become an important means of conducting business. That’s exactly what happened in Greece during its economic meltdown. You can use gold coins and easily barter in an emergency. People all over the world recognize gold as money. It’s much less certain that you would be able to liquidate an ETF during a time of crisis.

Consider a case of a dollar collapse or hyperinflation. The rapidly rising price of consumer goods, from groceries to gasoline, would make day-to-day living very difficult. Even if you managed to liquidate your gold-backed ETF, the currency you pull out would rapidly lose value. Physical gold, in your hand, would be immune to the government’s printing press. In all likelihood, your gold would buy you the same basket of goods and services a month, or even a year later. The cash you pulled from your gold-backed ETF would likely purchase far less as time goes on.

Although gold-backed ETFs offer an easy way to invest in gold, you always have to remember that you don’t own what you can’t hold in your own hands. There is always “counterparty risk.” The fact you possess an ETF does not give you the right to redeem it for actual gold. The owner of the gold is backing your investment, and promising to pay you dollars.

Physical gold offers stability and certainty in your investment. You can put a gold coin in your pocket. With a gold-backed ETF, all you have is a piece of paper representing a legal promise. That’s well and good in normal market conditions – but in a real emergency, promises are easily broken.

Gold-backed ETFs have a place in an overall investment scheme. But for security in the event of a crisis, they simply cannot replace physical gold.

Below we separate the hype from the sad reality of the USD in the face of a new “BRICS currency.”

Net conclusion: The real death of the USD will be domestic not foreign.

The Bell Has Been Tolling for Years

When it comes to the “bell tolling for fiat,” we can all hear its loud chimes, but that bell has been tolling since 1971 (or frankly 1968), when the US leadership decoupled the world reserve currency from its golden chaperone.

Like any teenager throwing a house party, the lack of a parental chaperone leads to lots of crazy events and lots of broken furniture.

The same is true of post-71 politicians and central bankers suddenly freed of a gold-backed chaperone and thus suddenly loaded with drunken power to mouse-click currencies and expand deficits.

And since then, all kinds of things have been breaking, from banks to bonds to currencies.

And now, with all the extreme hype (and, yes, some genuine reality) behind the headlines of a revolutionary gold-backed BRICS trade currency, many are making sensational claims that the World Reserve Currency (i.e., USD) is nearing its end and that fiat money from DC to Tokyo is effectively toast.

Hmmm…

Don’t Bury the Dollar Just Yet

Before we start tossing red roses over the shallow grave of an admittedly grotesque US Greenback in general, or fiat fantasy money in general, let’s all take a deep breath.

That is, let’s re-think through this inevitable funeral with a bit more, well, realism, mathematics and even geopolitical common sense before we turn our backs on the USD, and this is coming from an author who has never thought highly of that Dollar, be it fiat, politicized and now weaponized.

So, let’s take a deep breath and engage open, informed and critical minds when it comes to debating many of the still open, un-known and critical issues surrounding the so-called “game changer” event when the BRICS+ nations convene this August in S. Africa.

Needed Context for the “BRICS New Currency” Debate

As made clear literally from Day 1 of the Western sanctions against Putin, the West may have been aiming for Putin’s (or the Ruble’s) chest, but it then shot itself in the foot.

After decades of DC exporting USD inflation from Argentina to Moscow, a large swath of the developing countries of the world who owe greater than $14T in USD-denominated debt were already reeling under the pain of rate-hike gyrations which made their own debt and currency markets flip and flop like a dying fish on the dock.

Needless to say, a 500-basis-point spike in the cost of that debt under Powell didn’t help. In fact, it did little good (or goodwill) for USD friends and enemies alike, from the gilt markets in London to the fruit markets in Santiago.

Adding insult to injury, DC coupled this strong-Dollar policy with a now weaponized-Dollar policy in which a nuclear and economic power like Russia had its FX reserves frozen and access to SDRs and SWIFT transactions blocked.

Like Napoleon at Moscow, this was going a step too far…

The net result was an obvious and immediate distrust of that once neutral world reserve currency, an outcome which economists like Robert Triffin warned our congress against in 1960, and even John Maynard Keyes warned the world against long before.

Heck, even Obama warned against such weaponization of a reserve currency as recently as 2015.

Thus, and as I (and many others) warned from Day 1 of the sanctions, the distrust for the USD unleashed by the sanctions in early 2022 was “a genie that can never go back in the bottle.”

Or more simply stated, the trend toward de-dollarization was now going to come at greater speed and with greater force.

This force, of course, is now being seen, as well as debated, under the highly symbolic as well as substantive example of the BRICS+ nations seeking to usher in a gold-backed trade currency to move openly away from the USD, a move which some maintain will soon de-throne the USD as a world reserve currency and send its value immediately to the ocean floor.

The Trend Away from the USD Is Clear, But It’s Pace Is Not

For me, the trajectory of this de-dollarization trend is fairly obvious; but the speed and knowable magnitude of these changes are where I take a more realistic (i.e., less sensational) stance.

But before I argue why, let’s agree on what we do know.

The BRICS New Currency Is Very Real

We know, for example, that Russian finance experts like Sergei Glasyev have real motives and sound reasons for planning a new (anti-Dollar) financial system which not only seeks a Eurasian Economic Union for cross boarder trade settlements backed by local currencies and commodities, but to which gold will likely be added as a “backer” to the same.

Glasyev has also made headlines with plans regarding the Moscow World Standard as a far more fair-playing and fair-priced gold exchange alternative to the Western LBMA exchange.

If we take his gold backing plans seriously, we must also take seriously the plan to expand such gold-backed trade currency plans into the Shanghai Cooperation Organization which would make the final tally of BRICS+ nations “going gold” as high as 41 country codes.

This could ostensibly mean greater than 50% of the world’s population and GDP would be trading in a gold-backed settlement currency outside of the USD, and that, well, matters to both the demand and strength of that Dollar…

China’s Motives Are Also Anti-Dollar

China, moreover, has invested heavily in the Belt & Road Initiative (152 countries) as well as in massive infrastructure projects in Africa and South America, areas of the world that are all too familiar with America’s intentional (or at least cyclical) modus operandi of developing nations enjoying low US rates and cheaper Dollars to create local credit booms which later crash and burn into a local debt crisis whenever those US rates and Dollars rise.

China therefore has a vested interest in protecting its EM investments as well as EM export markets in a currency outside of a USD monopoly.

Meanwhile, as the US is making less and less friends with EM markets, Crown Princes, French Presidents and EU and UK bond markets, China has been busy brokering peace between Saudi Arabia and Iran, as well as building a literal bridge between the latter and Iraq while simultaneously making Yuan-trade deals with Argentina.

Other Reasons to Take the BRICS+ Currency Seriously

Tag on the fact that Brazil, China and Iran are trading outside the USD-denominated SWIFT payment system, and it seems fairly clear that much of the world is leaning toward what Zoltan Poszar described as a “commodity rather that debt-based trade settlement currency” for which Charles Gave (and the BRICS+ nations) see gold as an “essential element” to that global new trend.

Finally, with a strong Greenback making USD energy and other commodity prices painfully (if not fatally) too expensive for large swaths of the globe, it’s no secret to those same large swaths of the globe (including petrodollar nations…) that gold holds its value far better than a USD.

Given this fact, it’s easy to see why BRICS+ nations wish to settle trades in a gold-backed local currency in order to ease the pressure on commodity prices. This gives them the opportunity, as Luke Gromen reminds, to buy time to pay down their other USD-denominated debt obligations.

In addition to the foregoing arguments, the fact that the BRICS+ nations are cloning IMF and World Bank swing loan and “contingency reserve asset” infrastructure programs under their own Asian Monetary Fund and New Development Bank, it becomes more than clear that a new BRICS+ world, trade currency and institutionalized infrastructure is as real as the trend away from a monopolar hegemony of the USD.

In short, and to repeat: There are many, many reasons to both see and trust the obvious and current trend/trajectory away from the USD as warned over a year ago, all of which, no matter what the slope and degree, will be good, very good for gold (see below).

But here’s the rub: The speed, scope, efficiency and ramifications of this trend in general, and the “BRICS August Game Changer” in particular, are far too complex, fluid and unknown to make any immediate (or “sensational”) funeral plans for the USD today.

And here’s a few reasons as to why.

Why the BRICS New Currency Is No Immediate Threat to the USD

First, we have to ask the very preliminary question as to whether the August BRICS summit will even involve an actual announcement of a new, gold-backed trading currency.

So far, all we have to go on is a leak from a Russian embassy in Kenya, not an official communication from the Kremlin or CCP.

Meanwhile, India, a key BRICS member, has openly denied such a new trade currency as a fixed agenda item for this August.

But notwithstanding such media noise, we must also look a bit deeper into the mechanics, economics and politics of a sudden “game-changer” new currency.

The BRICS New Currency: Many Operational Questions Still Open

Mechanically speaking, for example, who will indeed be the issuing entity of this new currency?

The new BRICS Bank?

What will be the actual gold coverage ratio? 10% 15% 20%?

Will BRICS+ member nations/central banks need to deposit their physical gold in a central depository, or will they enjoy (most likely) the flexibility of pledging their domestically-held gold as an accounting-only-unit?

Cohesion Among the Distrusting?

As important, just how much trust and cohesion is there among the BRICS+ nations?

Sure, this collection of nations may trust gold more than they trust each other or the US (which is why such a gold-backed trade currency may work, as it can’t be “inflated away”), but if a BRICS member country wishes to redeem its gold from say, Russia, years down the road, can it realistically assume it will happen?

What if Russia (or any other trade partner) is in a nastier mood tomorrow than they are today?

Basic Math

In addition, there are certain economic/mathematical issues to consider.

We know, for example, that the collective BRICS+ gold reserve (as of Q1 2023) is just over 5452 tones, valued today at approximately $350B.

Enough, yes to stake a new currency.

But measured against a net global amount of $13T in total physical gold, are the BRICS+ gold reserves enough to make a sizable dent (even at a partial coverage ratio) to tilt the world away from the USD overnight, when the USA, at least officially, has much, much more gold than the BRICS+?

That said, we can’t deny that the actual gold stores in places like Russia and China are far, far higher than officially reported by the World Gold Council.

Additionally, the historically unprecedented rate of central bank gold stacking in 2022-23 seems to suggest that the enemies of the USD are indeed “loading their guns” for a reason.

Expecting, however, all of the BRICS+ members to maintain the discipline to continue to purchase and store more physical gold despite the political temptations to redeem the same for later or unexpected domestic spending needs may be a naive assumption in a real world of ever-shifting national behaviors.

Geopolitical Considerations & the BRICS New Currency

Speaking of such shifting behaviors, we also can’t ignore the various pro and con forces within a geopolitical backdrop wherein much of the world, whether it loves or hates the US, still needs its USDs and USTs.

China, for example, may be letting maturities run and even dumping the USTs it now owns at a fast pace (only years away from total UST liquidation), but for now, China needs to keep the USD from growing too weak to buy all the Chinese exports of those American products made, in well…China.

That said, if the trend is indeed a new world of currency wars, rather than currency cooperation, which is a more than fair assumption, then all such liberal economic cooperation/trade arguments fall to the floor.

Nevertheless, with over $30T worth of USDs held by non-US parties in the form of bonds, stocks, and checking accounts, the collective desire (common interest) to keep those USDs alive and at least relatively strong is a major counter-force to the notion that the world and USD are coming to a sudden change this August.

Furthermore, in such an uncertain world of competing currencies as well as national and individual self-interests, the trillions and trillions of off-shored USTs/USDs tangled up within the foreign as well as US banking and derivative markets is important.

Why?

Because any massive dislocation in risk asset (and even currency) markets emanating from South Africa or elsewhere, in August or much later, would more than likely (and ironically) cause a disruption in foreign markets so dramatic that we could easily see a flow into, rather than away from, USDs for the simple (and again ironic) reason that the mean and ugly Greenback is still the best/most-demanded horse in the global fiat slaughter house.

In other words, even if all the BRICS+ plans for a gold-backed trading currency go flawlessly, the time gap between the accepted rise of such a settlement currency and the open fall of the USD is likely to be long, wide and unknown enough to see the USD actually get stronger rather than weaker before we experience any final fall in the USD as a global reserve currency.

The USD: Supremacy (Still) vs. Hegemony (Gone)

So, no, I don’t think that the USD will fall entirely from grace or even supremacy in August of 2023, even if the trend away from its prior hegemony is becoming increasingly undeniable.

It will take more than sensational BRICS headlines to make such a rapid change, but yes, and as the Sam Cooke song says, “change is gonna come.”

My only point is that for now, and for all the reasons cited above, the trajectory and speed of those changes are likely not as sensational as the trajectory and speed of the current headlines.

No Matter What: Gold Wins

The case for gold, of course, does not change just because the debate about the speed and scope of the new BRICS+ trade currency rages today.

No matter what, the very fact that such a gold-backed trade settlement unit will inevitably come to play will be an equally inevitable tailwind for global gold demand and hence global gold pricing in all currencies, including the USD.

The Dollar Will Die from Within, Not from Without

Furthermore, and despite all the hype as well as substance behind the BRICS headlines, I see the evolution of such a gold-backed trade currency as a reaction to, rather than attack upon, the USD, whose real and ultimate threat comes from within, rather than outside, its borders.

The world is losing trust in the USD because US policy makers killed it from within.

Ever since Nixon took the gold chaperone away, politicians and central bankers have been deficit spending like drunken high school seniors in a room filled with beer but absent of parental consent.

The entire world has long known what many Americans are finally seeing from inside their own walls, namely: The US will never, ever be able to put its fiscal house in order.

Uncle Sam is simply too far in debt and there’s simply no way out as it approaches a wall of open and obvious fiscal dominance in which fighting inflation will only (and again, ironically) cause more inflation.

Or stated simply, Uncle Sam can’t afford his own ever-increasing and entirely unpayable deficit spending habits without having to resort to trillions and trillions of more mouse-clicked Dollars to keep yields in check and IOUs from defaulting.

And that, far more than a BRICS new currency, is what will put the final rose on a fiat system (and Dollar) that is already openly but slowly dying—first slowly, then all at once.

But I don’t think that day will be August 22.

END

3,Chris Powell of GATA provides to us very important physical commentaries

A good read: how the banks $118 billion capital buffer will be wiped out by Basel iii

(Bloomberg News)

Banks’ $118 billion capital buffer likely to be wiped out by Basel III rules

Submitted by admin on Wed, 2023-07-26 11:47Section: Daily Dispatches

By Jennifer Surane,and Katanga Johnson Bloomberg News Wednesday, July 26, 2023

Wall Street’s biggest banks are preparing for new regulations that could erase almost all of the $118 billion in excess capital they squirreled away over the past decade, likely crimping shareholder buybacks for years to come.

The Federal Reserve and the Federal Deposit Insurance Corp. will vote Thursday to propose the measures during two separate open meetings, marking the first hurdle in putting the United States on track to adopt its final version of international banking standards known as the Basel III endgame.

Ahead of the meetings, both regulators, along with the Office of the Comptroller of the Currency, plan to release hundreds of pages of documents detailing the changes.

“There’s certainly a great deal of angst from investors around these expected proposals,” Jason Goldberg, an analyst at Barclays, said in an interview. “Share repurchases could be lower than desired in the near term. Ultimately we would expect the group to adapt and move forward.” …

Record quarterly gold production and solid cost performance – Record quarterly gold production reflects 100% ownership of Canadian Malartic for the full quarter, combined with a strong operational performance at all producing sites. Payable gold production1 in the second quarter of 2023 was 873,204 ounces at production costs per ounce of $851, total cash costs per ounce2 of $840 and all-in sustaining costs (“AISC”) per ounce3 of $1,150

Operational performance drives strong quarterly financial results – The Company reported quarterly net income of $0.66 per share in the second quarter of 2023, with adjusted net income4 of $0.65 per share. Operating cash flow was $1.46 per share

Strong operating and safety performance at all mine sites – Gold production and costs in the second quarter of 2023 were better than anticipated, reflecting strong operating performance across the Company’s mines, despite the challenges related to wildfires in northern Ontario and Quebec and the caribou migration in Nunavut. Lower than expected costs reflect a strong operating performance, favourable foreign exchange rates and the easing of certain inflationary pressures

Important milestones achieved across the portfolio – At the Canadian Malartic complex, the team celebrated production of its seventh million ounce in June. In addition, Detour Lake, Goldex and Macassa each achieved record quarterly mill throughput rates, while Meliadine recorded its best ever monthly mill throughput in May 2023

Gold production, cost and capital expenditure guidance reiterated for 2023 – Expected payable gold production in 2023 remains unchanged at approximately 3.24 to 3.44 million ounces with total cash costs per ounce expected to be between $840 and $890 and AISC per ounce expected to be between $1,140 and $1,190. Total capital expenditures (excluding capitalized exploration) for 2023 are still estimated to be approximately $1.42 billion. The Company’s 2023 production guidance assumes Kittila operates at an annual rate of 1.6 million tonnes per annum (“Mtpa”). A decision by the Supreme Court of Finland (the “SAC”) to either maintain the 1.6 Mtpa permit or revert to the 2.0 Mtpa permit is expected in the third quarter of 2023

Solid cash flow generation strengthens the Company’s balance sheet and liquidity position – During the second quarter of 2023, the Company repaid $900 million of the amounts drawn on its unsecured revolving bank credit facility. The amount repaid on the unsecured revolving bank credit facility was repaid using $300 million in cash on hand and $600 million drawn on an unsecured term loan facility (the “Term Loan Facility”) which the Company entered into in the quarter. Additionally on June 30, 2023, the Company repaid the $100 million 4.54% Series A senior notes at maturity. As at June 30, 2023, the Company’s long term debt was $1,942.0 million and its net debt5 was $1,509.5 million.

Update on key value drivers and pipeline projects

Odyssey mine at the Canadian Malartic complex – In June 2023, the Company released the results of a new internal study reflecting significant project advancements, an improved valuation and opportunities to further enhance value (see the news release dated June 20, 2023). Shaft sinking activities ramped up through the quarter, with approximately 60 metres sunk as at June 30, 2023. Production via the ramp at the Odyssey South deposit increased through the quarter and remains on schedule to reach a planned rate of 3,500 tonnes per day (“tpd”) in 2024. Drilling activities focused on infilling the internal zones at the Odyssey South deposit and mineral resource expansion of the East Gouldie deposit to the east and west

Detour Lake – In the second quarter of 2023, the mill set a record for quarterly throughput, with an improved mill availability of 92.8%. The continued focus on mill process optimization and mill availability is tracking well to reach and potentially exceed, throughput of 28.0 Mtpa. The Company is advancing the underground mining scenario study based on a revised mineral resource model and expects to report the results of this study in the first half of 2024

Optimization of assets and infrastructure in the Abitibi Gold Belt – The Company continued to advance several internal evaluations to assess potential production opportunities at the Macassa Near Surface and the Amalgamated Kirkland (“AK”) deposits, and at the Upper Beaver and Wasamac projects. These evaluations include an assessment of ore transportation via rail or truck to the Company’s existing processing facilities in the region, with a goal of increasing future gold production at lower capital costs and with a reduced environmental footprint. The results of these evaluations are expected to be reported in the first half of 2024

Positive exploration results at Detour, Meliadine, Kittila and Hope Bay

Based on exploration success in the first half of 2023, a supplemental exploration budget of $32 million has been approved – The Company’s exploration program returned positive results in the first half of 2023 at several key operating sites and projects, showing excellent potential to identify additional mineral resources and replace mineral reserves. These results support the focused addition of supplemental budgets. An update on selected exploration programs and budgets is set out in the sections below

Detour – Drilling continues to investigate the deposit below the West Pit mineral reserve and the western plunge extension of the mineralization to confirm the mineralized zones potentially amenable to underground mining. Drill results below the West pit reserve continue to demonstrate potential for a higher grade envelope with a recent intercept yielding 12.9 grams per tonne (“g/t”) gold over 12.9 metres at 400 metres depth, while two kilometres west of the open pit mineral reserves mineralization remains open with a recent intercept returning 2.8 g/t gold over 14.4 metres at 1,061 metres depth

Meliadine – Drilling continues to investigate the vertical extensions of the mineralized zones in the central part of the Tiriganiaq, Wesmeg and Wesmeg North deposits. At Wesmeg North, a recent intercept yielded 6.3 g/t gold over 7.4 metres at 558 metres depth. Approximately 1.5 kilometres southeast of Tiriganiaq at the F-Zone deposit, a recent intercept yielded 6.4 g/t gold over 16.0 metres at 167 metres depth in the upper portion of the deposit

Kittila – Drilling has extended the Rimpi Main Zone to the north, outside of the current mineral resources, with a recent intercept yielding 7.2 g/t gold over 4.5 metres at 1,102 metres depth. In the Roura area close to the shaft bottom, a recent intercept in the Main Zone yielded 7.7 g/t gold over 7.3 metres at 1,152 metres depth. At shallow depth in the Rimpi area, the Parallel / Sisar Zone was identified in an area that has received limited drilling to date, yielding 3.1 g/t gold over 4.5 metres at 142 metres depth and opening a new near-surface target area for future exploration

Hope Bay project – A total of nine exploration drill rigs were operating at the Doris and Madrid deposits and regionally during the second quarter. At Doris, drilling in the BCO Zone continued to return good grades and thicknesses to further confirm the potential to expand the zone along strike. At Madrid, drilling focused on a two-kilometre long, previously untested gap between the Suluk and Patch 7 zones, with new highlight intercepts of 10.0 g/t gold over 14.0 metres at 677 metres depth and 13.7 g/t gold over 4.6 metres at 697 metres depth. This drilling confirms the potential of Madrid/Suluk/Patch 7 as it extends the high-grade Patch 7 Zone by 500 metres vertically and by 900 metres laterally at depth

A quarterly dividend of $0.40 per share has been declared

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1475

OFFSHORE YUAN: UP TO 7.1534

SHANGHAI CLOSED DOWN 6,36 PTS OR 0.20%

HANG SENG CLOSED UP 273.97 PTS OR 1.41%

2. Nikkei closed UP 222.82 PTS OR 0.68%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 100.61 EURO RISES TO 1.1125 UP 47 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.441 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 140.61/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ON SHORE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.401***/Italian 10 Yr bond yield FALLS to 4.062*** /SPAIN 10 YR BOND YIELD FALLS TO 3.455…**

3i Greek 10 year bond yield RISES TO 3.724

3j Gold at $1968.20 silver at: 24.93 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 4 /100 roubles/dollar; ROUBLE AT 90.19//

3m oil into the 79 dollar handle for WTI and 83 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 140.21// 10 YEAR YIELD AFTER BREAKING .54%, FALLS TO 0.441% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8574 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9537 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.865 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 3.944 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.833 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.95…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 1 BASIS PTS AT 4.3040

end

2.a Overnight: Newsquawk and Zero hedge:

S&P Futures Soar To 2023 High After Dovish Fed, Meta Earnings

THURSDAY, JUL 27, 2023 – 07:55 AM

US futures and global stocks soared, and the dollar slumped as investors wagered that the Fed has reached the end of its 16-month long policy-tightening cycle. A barrage of earnings beats (sorry Mike Wilson) from high-profile companies added to the bullish momentum, propelling the Stoxx Europe 600 index 1% higher to a two-month high, while US futures pointed to a strong Wall Street session after Fed Chair Powell failed to dent market optimism during his press conference. At 7:30am Nasdaq 100 futures were up 1.3%, led by an 9% premarket surge in Facebook parent Meta Platforms which reported blowout guidance for Q3; S&P futures rose 0.6% to a fresh 2023 high at 4,623. Treasury yields dropped on the short end, while the dollar pushed lower. Oil and gold prices are up. Iron ore, meanwhile, is trading lower. Today, we will receive a slew of growth and inflation data. As Fed staff now dropped US recession forecast, today’s growth data will be important to assess the soft-landing scenario. Keep an eye on banks stocks as Fed will hold meeting at 1pm ET today to implement Basel 3 endgame agreement.

In premarket trading, megacap techs are higher led by META which has soared 9% post earnings after the Facebook parent gave a revenue forecast ahead of consensus, driven by a recovery in advertising sales. Analysts note that AI-powered tools are boosting engagement and advertiser return, with several upping their price targets. Chipmakers also advanced, led by Micron Technology which highlighted its development of high-bandwidth memory products. Here are some other notable premarket movers:

US airline stocks drop in US premarket trading after results from peer Southwest Air showed that rising costs weighed even as demand for travel over the summer was strong, sending its shares as much as 7.4% lower in premarket trading.

American Airlines -2%, United Airlines -1.3%, Delta Air Lines -1.2%, JetBlue Airways -3.2%

Comcast gained more than 4% after beating profit estimates.

EBay shares drop 5.9% after the online marketplace’s third-quarter earnings outlook missed estimates. Analysts said the beat in the company’s second-quarter results was overshadowed by the guidance, with Jefferies expressing concern that growth initiatives could result in reduced margins without an uplift in gross merchandise volume and profit.

Estee Lauder shares fall 0.8%, after Jefferies downgraded the beauty products maker to hold from buy, along with peer Coty, on worries over a recovery in China.

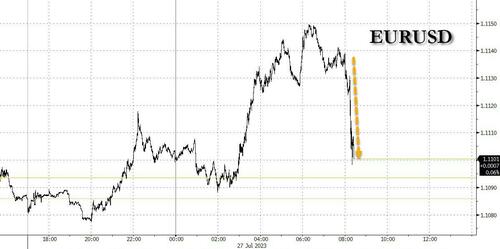

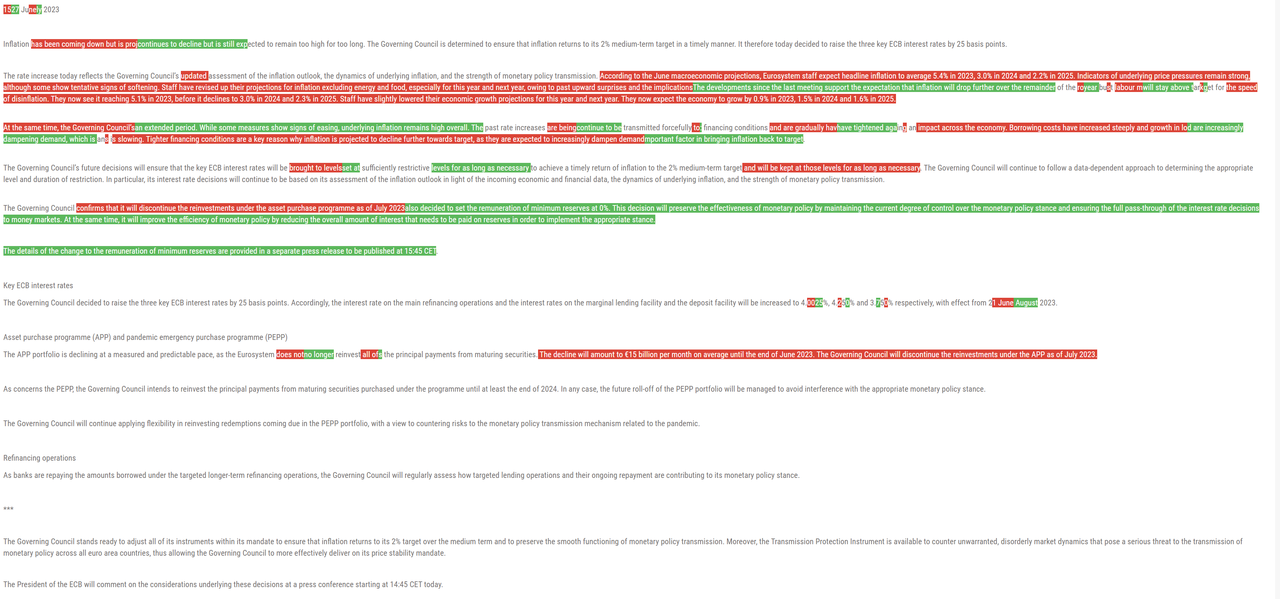

The move higher came after the Fed raised the federal funds rate to a 22-year high and while it signaled further hikes would be data dependent, many investors concluded that it’s done hiking interest rates (just tell them not to look at the soaring price of gasoline and food). They have trimmed bets on more increases this year, as Fed Chair Jerome Powell pointed to signs that higher borrowing costs are working to curb price pressures. Meanwhile, a predicted 25-basis-point rate rise later Thursday from the European Central Bank could be one of its last moves this cycle.

“There is belief that the Fed is probably done,” said Timothy Graf, head of EMEA macro strategy at State Street Bank & Trust Co. “Markets are also seeing a US economy that’s held up far better than the consensus outlook. They are pricing that we have achieved a landing that everyone thought would be impossible to achieve.”

What’s more, gloomy forecasts for an earnings recession have failed to materialise, according to Graf, with equity moves showing “people were under-invested in a lot of the big themes that generated returns this year.” Indeed, surprisingly strong earnings have shattered views that the US is in an earnings recession. More than half of all companies have beat analyst estimates so far, and today stands to be the busiest of the second-quarter calendar.

European stocks followed US equity futures and Asian counterparts higher ahead of the ECB decision today. The Stoxx 600 is up 1% after snapping a six-session win streak on Wednesday, with the media, technology and construction sectors leading gains. Among individual European movers, BNP Paribas SA, Nestle SA and Carrefour SA all rallied after topping estimates. On the downside, Shell Plc retreated despite pledging more buybacks as its profits fell from last year’s highs. Barclays Plc slumped on back of a 41% decline in quarterly trading revenue. Here are the most notable European movers:

Nestle shares rise as much 2%, the most in six weeks, after the food giant lifted the lower end of its forecast range for full- year sales growth

Universal Music Group gains as much as 12%, biggest increase on record, as its second-quarter revenue beat estimates driven by growth from its recorded music and merchandising segments

BNP Paribas shares advance as much as 4.3%, second-best performer in the Stoxx 600 Banks Index, after it reported what Morgan Stanley says are a strong set of results, while RBC also notes “reassuring” cost control

RELX shares jump as much as 4.3%, the biggest intraday gain since Feb. 16, after the information and analytics company reported adjusted operating profit that beat estimates

Inchcape shares rise as much as 14%, the most since 2009, after the UK car dealer reported strong revenue growth for the first half, boosted by its recent acquisition of US distributor Derco

Air Liquide rises as much as 1.6% after the gas company reported first-half Ebit and margins that exceeded estimates. Performance in the Americas was supported by higher prices in Industrial Merchant and strength in Healthcare, says Morgan Stanley

Shell drops as much as 2.3% after the oil company’s second-quarter profit missed estimates as commodity prices trended down

Neste shares plunge as much as 13%, most since March 2020, after the Finnish refiner reported adjusted Ebitda for the second quarter that missed the average analyst estimate. RBC says the company’s outlook and sales were underwhelming

Airbus shares slump 2.5% as analysts voice caution over the company’s decision to remove its target for raising aircraft production past pre-Covid levels and shift the focus to a longer-term goal

Barclays shares dropped as much as 6.7% as the announcement of a buyback failed to lift the mood after the UK bank’s corporate and investment bank revenues fell short of expectations for the second quarter

Teleperformance shares slump as much as 12%, the most in three months, after the provider of customer-relationship management services cut its revenue growth forecast for the year, saying it expects economic challenges to continue in the second half

St James’s Place shares slide as much as 12%, the biggest intraday decline since March 2020, after the investment management company reported first- half net inflows that missed estimates. Citi said the company’s flows were pressured by the macroeconomic backdrop

Earlier in the session, Asian stocks climbed, with a rally in Chinese technology stocks and speculation that the Federal Reserve is nearing the end of its rate-hike cycle helping drive the regional benchmark toward its 2023 high. The MSCI Asia Pacific Index jumped as much as 1%, set for a fourth day of gains and approaching this year’s peak seen in late January. Chinese tech companies provided the biggest boost as electric-vehicle shares surged on plans by Volkswagen AG to invest in XPeng. The EV maker’s stock soared 33%, leading the rally in Hong Kong’s Hang Seng Tech Index and putting it on track for a technical bull market. Equities in most of Asia’s emerging markets rose as the dollar slid following the Fed’s meeting. A weaker greenback is seen as beneficial for growth in the region’s developing economies, many of which rely on imports priced in dollars.

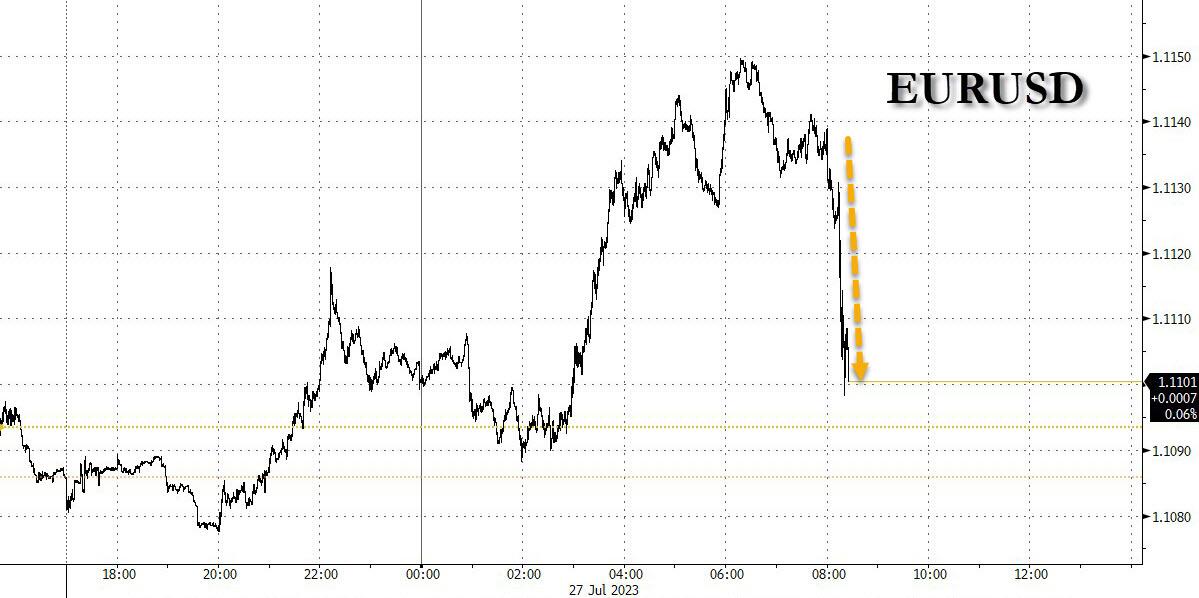

Japanese stocks also edged higher ahead of a monetary policy decision on Friday. KOSPI gained with the spotlight on earnings including Samsung Electronics which topped estimates.

The MSCI Asia Pacific gauge is up 2.6% so far this week, boosted by a rebound in Chinese shares after authorities signaled further property easing and a consumption boost to revive a struggling economy. The regional benchmark is up 9.3% this year, versus a gain of almost 19% in the S&P 500 Index. “The near-term outlook for Asian equities is improving, with some of the macro headwinds facing the market in the past 18 months likely to turn into tailwinds,” said Soo Hai Lim, head of Asia ex-China equities at Barings. “If the second half of the year sees central-bank tightening efforts wind down and earnings to guide higher, investor sentiment toward Asian equities should also improve.”

Australia’s stock market was led by strength in real estate and tech. The S&P/ASX 200 index rose 0.7% to 7,455.90, its highest close since Feb. 9, in a rally led by property and tech shares. The advance comes amid optimism the Fed is close to the end of its tightening cycle after the central bank said any further tightening would be data dependent. Read: Fed Raises Rates as Powell Keeps Options Open for Future Hikes In New Zealand, the S&P/NZX 50 index was little changed at 11,954.11

Stocks in India declined Thursday as fast-moving consumer goods firms dropped on worries over volume growth, and Mahindra led a retreat in automakers after its surprise stake disclosure in a small-sized lender. The S&P BSE Sensex fell 0.7% to 66,266.82 in Mumbai, posting a fourth drop in five sessions, while the NSE Nifty 50 Index slid 0.6%. They gauges rose 0.5% each on Wednesday. HDFC Bank contributed the most to the index decline, while Mahindra was the top decliner. The automaker closed 6.3% lower after analysts were surprised by its stake purchase in RBL Bank. The company’s market value dropped by $1.5 billion to $21.9 billion, wiping off its gains since start of the month. Out of 31 shares in the Sensex index, 9 rose and 20 fell, while 2 were unchanged.

In FX, The Bloomberg dollar index fell for the third day, extending Wednesday’s 0.3% drop, when Federal Reserve Chief Jerome Powell’s comments bolstered bets that the US tightening cycle is near an end. The Swedish krona and Norwegian krone are the best performers. EUR/USD climbed as much as 0.5% to 1.1144 ahead of the European Central Bank’s policy decision later on Thursday, where it’s set to announce a 25 basis-point rate increase. GBP/USD rose for a third day, but weakened slightly against the euro. Traders trimmed wagers on further rate hikes after a report that advisers to the Treasury are increasingly concerned over the extent of UK rate hikes. Market pricing now favors a quarter-point increase in August, which on a closing basis would the first time that’s happened since last month’s half-point hike. They also continued to pare bets on how high interest rates would rise this cycle, with pricing for the terminal rate edging back below 6%. That’s down from more than 6.5% expected earlier this month. AUD/USD rose as much as 0.9% to 0.6821 as yuan gains fueled leveraged demand for the currency and put large buy stops above 0.6850 into play.