GOLD PRICE CLOSED: UP $14.15 TO $1961.25

SILVER PRICE CLOSED: UP $0.15 AT $24.36

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1958/85

Silver ACCESS CLOSE: 24.33

SHANGHAI FIXES MORNING AND NIGHT JULY 27: $2001.20 AND $1997.00 (IN DOLLARS CONVERTED FROM CNY)

USA CLOSING PRICE; 1947.10//

PREMIUM TO NY: $53.90

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Bitcoin morning price:, $29,194 UP 6 Dollars

Bitcoin: afternoon price: $29,335 UP 147 dollars

Platinum price closing $938.10 DOWN $0.90

Palladium price; $1244,25 DOWN $0.70

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,592.37 UP 21.40 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1523,74 UP 4.57 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1777,22 UP 3.36 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: JULY 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,945.400000000 USD

INTENT DATE: 07/27/2023 DELIVERY DATE: 07/31/2023

FIRM ORG FIRM NAME ISSUED STOPPED

435 H SCOTIA CAPITAL 1657 C MORGAN STANLEY 1

690 C ABN AMRO 1

737 C ADVANTAGE 1

JPMorgan stopped 0/2 contracts.

FOR JULY:

GOLD: NUMBER OF NOTICES FILED FOR JULY/2023. CONTRACT: 2 NOTICES FOR 2400 OZ or 0.00622 TONNES

total notices so far: 3308 contracts for 330,800 oz (10.2892 tonnes)

FOR JULY:

SILVER NOTICES: 4 NOTICE(S) FILED FOR 20,000 OZ/

total number of notices filed so far this month : 5131 for 25,655,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $14.15

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//

INVENTORY RESTS AT 915.82 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP $0.15 AT THE SLV// small CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 550,000 OZ FROM THE SLV..

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 451.93 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 985 CONTRACTS TO 145,266 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS STRONG SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.59 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. TAS ISSUANCE WAS A STRONG SIZED 510 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 510 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.59). AND WERE SUCCESSFUL IN KNOCKING SOME SPEC LONGS AS WE HAD A STRONG LOSS ON OUR TWO EXCHANGES OF 572 CONTRACTS. WE HAD 0 CRIMINAL NOTICES FILED IN THE CATEGORY OF EXCHANGE FOR RISK TRANSFER FOR 0 MILLION OZ// ( THE TOTAL ISSUED IN THIS CATEGORY SO FAR THIS MONTH TOTAL 5.25 MILLION OZ.). WE HAVE NOW RETURNED TO OUR USUAL AND CUSTOMARY SCENARIO: BANKERS SHORT AND SPECS LONG WITH MANIPULATION NOW MID MONTH AND BEYOND, DUE TO TAS MANIPULATION.

WE MUST HAVE HAD:

A SMALL ISSUANCE OF EXCHANGE FOR PHYSICALS( 230 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 16.110 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 10,000 QUEUE JUMP + 0 MILLION OZ EXCHANGE FOR RISK FOR TODAY//NEW STANDING: 25.680 MILLION OZ + 5.25 MILLION OZ EXCHANGE FOR RISK/PRIOR: NEW TOTAL 30.94 MILLION OZ// // STRONG SIZED COMEX OI LOSS/ SMALL SIZED EFP ISSUANCE/VI) GOOD NUMBER OF T.A.S. CONTRACT ISSUANCE (510 CONTRACTS)/ZERO EXCHANGE FOR RISK ISSUED/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL –183 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JULY. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY:

TOTAL CONTRACTS for 18 days, total 17,070 contracts: OR 85.350 MILLION OZ (948 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 85.35 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.35 MILLION OZ (SMALLER THAN LAST MONTH)

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 985 CONTRACTS WITH OUR LOSS IN PRICE OF $0.59 IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL EFP ISSUANCE CONTRACTS: 230 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JULY OF 16.110 MILLION OZ FOLLOWED BY TODAY’S 10,000 OZ QUEUE. JUMP + 0 MILLION OZ EXCHANGE FOR RISK TODAY + (PRIOR EXCHANGE FOR RISK : 5.25 MILLION OZ): TOTAL NOW STANDING 25.690 MILLION OZ NORMAL STANDING + 5.25 MILLION EXCHANGE FOR RISK = 30.94 MILLION OZ.///// .. WE HAVE A GOOD SIZED LOSS OF 572 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A GOOD 510//CONSIDERABLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION AND WAS INSTRUMENTAL IN YESTERDAY’S HUGE RAID. THE NEW TAS ISSUANCE TODAY (510) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE./

WE HAD 2 NOTICE(S) FILED TODAY FOR 20,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A VERY STRONG SIZED 14,571 CONTRACTS TO 459,036 AND CLOSER TO TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED: 1377 CONTRACTS

WE HAD A STRONG SIZED DECREASE IN COMEX OI ( 14,571 CONTRACTS) WITH OUR STRONG $21.80 LOSS IN PRICE. WE ALSO HAD A STRONG INITIAL STANDING IN GOLD TONNAGE FOR JULY. AT 5.1975 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0.00311 TONNE QUEUE JUMP : NEW TOTAL OF GOLD STANDING FOR JULY: 10.2890 TONNES// + /A FAIR (AND CRIMINAL) ISSUANCE OF 1516 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH A $21.80 LOSS IN PRICE WITH RESPECT TO THURSDAY’S TRADING.WE HAD A STRONG SIZED LOSS OF 10,761 OI CONTRACTS (33.471 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 3810 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 459,036

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,761 CONTRACTS WITH 14,571 CONTRACTS DECREASED AT THE COMEX// AND A GOOD 3810 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 10,761 CONTRACTS OR 33.471 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 1516 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3810 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (14,571) //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 10,761 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) GOOD INITIAL STANDING AT THE GOLD COMEX FOR JULY AT 5.1975 TONNES FOLLOWED BY TODAY’S 0.00311 TONNE QUEUE JUMP //NEW TOTAL ADVANCES TO 10.2890 TONNES ///// /3) SOME LONG LIQUIDATION WITH HUGE TAS LIQUIDATION AND SPREADER LIQUIDATION TO AID IN GOLD’S RAID YESTERDAY//4) STRONG SIZED COMEX OPEN INTEREST LOSS/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 1516 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY :

TOTAL EFP CONTRACTS ISSUED: 46,997 CONTRACTS OR 4,699,700 OZ OR 146.18 TONNES IN 18 TRADING DAY(S) AND THUS AVERAGING: 2610 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAY(S) IN TONNES 146.18 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 146.18/3550 x 100% TONNES 4.11% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 146.18 TONNES (WEAKER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A STRONG SIZED 985 CONTRACTS OI TO 145,266 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 230 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 230 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 230 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 802 CONTRACTS AND ADD TO THE 230 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 755 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 3.775MILLION OZ

OCCURRED WITH OUR $0.59 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED UP 59.26 PTS OR 1.84% //Hang Seng CLOSED UP 277.45 PTS OR 1.41% /The Nikkei CLOSED DOWN 131.93 PTS OR 0.40% //Australia’s all ordinaries CLOSED DOWN 0.74 % /Chinese yuan (ONSHORE) closed DOWN 7.1555 /OFFSHORE CHINESE YUAN DOWN TO 7.1580 /Oil UP TO 79.84 dollars per barrel for WTI and BRENT UP AT 83.88 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A VERY STRONG SIZED 14,571 CONTRACTS DOWN TO 459,036 WITH OUR STRONG LOSS IN PRICE OF $21.80 ON THURSDAY. MOST OF THE LOSS WAS DUE TO SPREADER LIQUIDATION AND T.A.S. LIQUIDATION.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF JULY… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3810 EFP CONTRACTS WERE ISSUED: : AUGUST 3810 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3810 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 10,761 CONTRACTS IN THAT 3810 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A VERY STRONG SIZED LOSS OF 14,571 COMEX CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR STRONG LOSS IN PRICE OF $21.80//THURSDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT WAS A FAIR 1516 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THE HUGE NUMBER OF T.A.S. CONTRACTS INITIATED OVER THE PAST SEVERAL WEEKS SPELLS TROUBLE FOR THE GOLD/SILVER MARKET AS RAIDS WILL SURELY BE UPON US TRYING TO CONTAIN OUR PRECIOUS METALS RISE IN PRICE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JULY (10.2861) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $21.80) //// AND WERE SUCCESSFUL IN KNOCKING FEW SPECULATOR LONGS AS WE HAD A STRONG SIZED LOSS OF 10,761 CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE SPREADER LIQUIDATION THROUGHOUT THE THURSDAY COMEX SESSION AS WELL AS T.A.S. LIQUIDATION, WHICH BOTH PLAYED OUR MAJOR ROLE IN THURSDAY’S RAID KNOCKING THE PRICE OF GOLD SOUTHBOUND. THE TAS ISSUED THURSDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 33.471 PAPER TONNES OF TOTAL OI FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY. (5.11974 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 0.00311 TONNES//TOTAL STANDING FOR JULY GOLD ADVANCES TO: 10.2890 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR STRONG LOSS IN PRICE TO THE TUNE OF $21.80.

WE HAD – REMOVED 1377 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET LOSS ON THE TWO EXCHANGES 10,761 CONTRACTS OR 1,076,100 OZ OR 33.471 TONNES.

Estimated gold volume today:// 190,391 poor

final gold volumes/yesterday 407,623//tas and spreader liquidation//huge volume

//JULY 28/ FOR THE JULY 2023 CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | nil OZ . |

| Deposit to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today | 2 notice(s) 200 OZ 0.00622 TONNES |

| No of oz to be served (notices) | 0 contracts 0 oz 0.0 TONNES |

| Total monthly oz gold served (contracts) so far this month | 3308 notices 330800 OZ 10.2892 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: NIL

total customer deposits: 0 oz

we had 0 customer withdrawals:

total withdrawals: nil

Adjustments; 0 /

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY.

For the front month of JULY we have an oi of 2 contracts having LOST 23 contracts. We had 24 contracts served on Thursday. Thus we gained 1 contract or an additional 100 oz of gold will stand at the comex.

AUGUST LOST 35,225 contracts DOWN to 21,315 contracts. We have 1 more reading day before the big August contract delivery month. We will probably have a rather small 34-40 tonnes of gold standing for delivery.

SEPT gained 403 contracts to stand at 1567

We had 2 contracts filed for today representing 200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 2 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the JULY /2023. contract month,

we take the total number of notices filed so far for the month (3308 x 100 oz ), to which we add the difference between the open interest for the front month of JULY (2 CONTRACT) minus the number of notices served upon today 2 x 100 oz per contract equals 330,800 OZ OR 10.2890 TONNES the number of TONNES standing in this NON active month of July.

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (3308) x 100 oz + (2) {OI for the front month} minus the number of notices served upon today (2) x 100 oz) which equals 330,700 oz standing OR 10.2890 TONNES

TOTAL COMEX GOLD STANDING: 10.2890 TONNES WHICH IS STRONG FOR A NON ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,030,421.032 OZ 63,15 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,337,753.171 OZ

TOTAL REGISTERED GOLD: 12,122,919.622 (377.07 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,214,833.549 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 10,092,498 OZ (REG GOLD- PLEDGED GOLD) 313.92 tonnes//

END

SILVER/COMEX

JULY 28

//2023// THE JULY 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 638,929.157 oz Delaware Brinks CNT . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 601,769.580 oz CNT |

| No of oz served today (contracts) | 4 CONTRACT(S) (20,000 OZ) |

| No of oz to be served (notices) | 7 contracts (35,000 oz) |

| Total monthly oz silver served (contracts) | 5131 Contracts (25,655,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i) Into CNT: 601,769.580 oz

total customer deposits:601,769.580 oz

JPMorgan has a total silver weight: 139.331 million oz/278.535 million =49.91% of comex .//

Comex withdrawals 3

i) Out of Delaware 19,934.623 oz

ii) Out of Brinks 604,680.680 oz

iii) Out of CNT: 23,313.834 oz

total: 638,929.157 oz

TOTAL REGISTERED SILVER: 32.272 MILLION OZ//.TOTAL REG + ELIGIBLE. 278.535 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF JULY /2023 OI: 11 CONTRACTS HAVING LOST 30 CONTRACT(S). WE HAD 32 NOTICES FILED ON THURSDAY SO WE GAINED 2 CONTRACTS OR AN ADDITIONAL 10,000 OZ WILL STAND AT THE COMEX FOR DELIVERY IN JULY,

AUGUST LOST 26 CONTRACTS TO STAND AT 788. WE WILL PROBABLY HAVE AROUND 3.0 MILLION OZ STANDING FOR DELIVERY IN AUGUST.

SEPT HAS A LOSS OF 2419 CONTRACTS DOWN TO 116,276

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 32 for 160,000 oz

Comex volumes// est. volume today 40,677 poor /

Comex volume: confirmed yesterday: 87,823 strong/raid

To calculate the number of silver ounces that will stand for delivery in JULY. we take the total number of notices filed for the month so far at 5131 x 5,000 oz = 25,655,000 oz

to which we add the difference between the open interest for the front month of JULY(11) and the number of notices served upon today 4 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY/2023 contract month: 5131 (notices served so far) x 5000 oz + OI for the front month of JULY (11) – number of notices served upon today (4 )x 500 oz of silver standing for the JULY contract month equates to 25.690 million oz + 0.0 MILLION OZ EXCHANGE FOR RISK TODAY//PRIOR EXCHANGE FOR RISK TOTALS 5.25 MILLION OZ /NEW TOTAL STANDING FOR DELIVERY: 30.94 MILLION OZ..WE HAVE 32 MILLION OZ OF REGISTERED SILVER AT THE COMEX//

the record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

JULY 28/WITH GOLD UP $14.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 915,82 TONNES

JULY 27/WITH GOLD DOWN $21.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 917.26 TONNES

JULY 26/WITH GOLD UP $6.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 25/WITH GOLD UP $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 24/WITH GOLD DOWN $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.20 TONNES OF GOLD INTO THE GLD//: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 21/WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / .////INVENTORY RESTS AT 913.80 TONNES

JULY 20/WITH GOLD DOWN $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 913.80 TONNES

JULY 19/WITH GOLD UP $0.65 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 912.07 TONNES

JULY 18/WITH GOLD UP $23.45 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: .////INVENTORY RESTS AT 912.93 TONNES

JULY 17/WITH GOLD DOWN $6.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD.////INVENTORY RESTS AT 912.93 TONNES

JULY 14/WITH GOLD UP $0.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 914.66 TONNES

JULY 13/WITH GOLD UP $3.30 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.29 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.66 TONNES

JULY 12/WITH GOLD UP $24.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.95 TONNES

JULY 11/WITH GOLD UP $6.15 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.0 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 915.26 TONNES

JULY 10 WITH GOLD DOWN $1.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.60 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 916.26 TONNES.

JULY 7 WITH GOLD UP $16.80 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.86 TONNES.

JULY 6/WITH GOLD DOWN $9.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 917.86 TONNES

JULY 5/WITH GOLD DOWN $2.20 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 2.6 TONNES FROM THE GLD///INVENTORY RESTS AT 921.90 TONNES

JULY 3/WITH GOLD UP $1.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 924.50 TONNES//

JUNE 30/WITH GOLD UP $10.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 924.50 TONNES

JUNE 29/WITH GOLD DOWN $3.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.81 TONNES

JUNE 28/WITH GOLD DOWN $1.15 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 925.65 TONNES

JUNE 27/WITH GOLD DOWN $9.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.45 TONNES OF GOLD FROM THE GLD./INVENTORY RESTS AT 925.65 TONNES

JUNE 26/WITH GOLD UP $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.6 TONNES OF GOLD FROM THE GLD/////INVENTORY RESTS AT 927.10 TONNES

JUNE 23/WITH GOLD UP $5.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: WITHDRAWALS OF 4.33 TONNES OF GOLD OVER THE PAST TWO DAYS. /INVENTORY RESTS AT 929.70 TONNES

JUNE 21/WITH GOLD DOWN $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY REST AT 934.03 TONNES

JUNE 20/WITH GOLD DOWN $22.40 TODAY: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 934.03 TONNES

JUNE 16/WITH GOLD UP $0.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 4.33 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 934.03 TONNES

JUNE 15/WITH GOLD UP $2.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 929.70 TONNES

JUNE 14/WITH GOLD UP $10.30 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 931.44 TONNES

JUNE 13/WITH GOLD DOWN $10.30 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.01 TONNES FORM THE GLD///INVENTORY RESTS AT 931.44

GLD INVENTORY: 915.82 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JULY 28/WITH SILVER UP 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.930 MILLION OZ

JULY 27/WITH SILVER DOWN 59 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ

JULY 26/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 25/WITH SILVER UP 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 826,000 OZ FROM THE SLV..////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 24/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 21/WITH SILVER DOWN 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.101 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 20/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.468 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 454.107 MILLION OZ/

JULY 19/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 18/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 17/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 4.856 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 14/WITH SILVER UP 27 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.21 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 13/WITH SILVER UP 64 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 12/WITH SILVER UP $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.881 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 11/WITH SILVER DOWN 5 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .020 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 464.822 MILLION OZ/

JULY 10/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.672 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 464.802 MILLION OZ

JULY 7/WITH SILVER UP 42 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.474 MILLION OZ

JULY 6/WITH SILVER DOWN 50 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.667 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 466.474 MILLION OZ//

JULY5/WITH SILVER UP 30 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JULY 3/WITH SILVER UP 7 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JUNE 30/WITH SILVER UP 19 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.377 MILLION OZ INTO THE SLV/////INVENTORY RESTS AT468.141 MILLION OZ//

JUNE 29/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.763 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 466.764 MILLION OZ//

JUNE 28/WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 470.527 MILLION OZ//

JUNE 27/WILVER SILVER UP 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 734,000 OZ INTO THE SLV////INVENTORY RESTS AT 470.527 MILLION OZ

JUNE 26/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY REST AT 469.793 MILLION OZ.

JUNE 23/WITH SILVER DOWN 9 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A NET DEPOSIT OF 6.61 MILLION OZ INTO THE SLV OVER THESE PAST TWO DAYS//INVENTORY RESTS AT 469.793 MILLION OZ//

JUNE 21/WITH SILVER DOWN $.40 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.784 MILLION OZ OF SILVER INTO THE SLV////INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 20/WITH SILVER DOWN 89 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 463.183 MILLION OZ//

JUNE 16/WITH SILVER UP 23 CENTS TODAY :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 459,000 OZ FROM THE SLV///INVENTORY RESTS AT 463.183 MILLION OZ

JUNE 15/WITH SILVER DOWN 17 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.377 MILLION OZ OF SILVER FROM THE SLV////INVENTORY RESTS AT 463.642 MILLION OZ//

JUNE 14/WITH SILVER UP 29 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 735,000 OZ FROM THE SLV///INVENTORY RESTS AT 465.019 MILLION OZ//

JUNE 13/WITH SILVER DOWN 25 CENTS TODAY; HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.515 MILLION OZ OF SILVER FROM THE SLV///INVENTORY RESTS AT 465.754 MILLION OZ//

JUNE 12/WITH SILVER DOWN 26 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 467.269 MILLION OZ//

CLOSING INVENTORY 41.930 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

END

3,Chris Powell of GATA provides to us very important physical commentaries

A good read: how the banks $118 billion capital buffer will be wiped out by Basel iii

(Bloomberg News)

Banks’ $118 billion capital buffer likely to be wiped out by Basel III rules

Submitted by admin on Wed, 2023-07-26 11:47Section: Daily Dispatches

By Jennifer Surane,and Katanga Johnson

Bloomberg News

Wednesday, July 26, 2023

Wall Street’s biggest banks are preparing for new regulations that could erase almost all of the $118 billion in excess capital they squirreled away over the past decade, likely crimping shareholder buybacks for years to come.

The Federal Reserve and the Federal Deposit Insurance Corp. will vote Thursday to propose the measures during two separate open meetings, marking the first hurdle in putting the United States on track to adopt its final version of international banking standards known as the Basel III endgame.

Ahead of the meetings, both regulators, along with the Office of the Comptroller of the Currency, plan to release hundreds of pages of documents detailing the changes.

“There’s certainly a great deal of angst from investors around these expected proposals,” Jason Goldberg, an analyst at Barclays, said in an interview. “Share repurchases could be lower than desired in the near term. Ultimately we would expect the group to adapt and move forward.” …

… For the remainder of the report:

END

Your weekend reading material

(Alasdair Macleod)

Alasdair Macleod: Inflation will return

Submitted by admin on Thu, 2023-07-27 13:15Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Thursday, July 27, 2023

It is an error to expect inflation to continue to fall in America. All financial market values in the United States and elsewhere are predicated on this hope.

The misunderstanding is to assume that the widely expected recession will lead to further falls in consumer price inflation, and that therefore interest rates and bond yields will decline. These hopes are based on Keynes’ rejection of Say’s Law, which simply points out there is no such thing as Keynes’ general glut because the unemployed stop producing.

A further point is that banks are increasingly scared of lending risk, which is leading to a credit squeeze. This raises the question: How can interest rates fall when there is a worsening shortage of credit?

The current economic setup for the U.S., the Eurozone, and the U.K. seems set to increase central bank credit to replace commercial bank lending, which will undermine their currencies. Additionally, government funding requirements will increase materially at a time when cross-border investment flows are threatened by financial bear markets.

The timing of a new BRICS gold-backed settlement currency and China’s determination to consolidate the BRICS and Shanghai Cooperation Organisation’s sphere of influence have the potential to offer alternatives for capital flows escaping from the collapsing finances of the Western alliance led by America.

Above all, we are witnessing the death of fiat, because it is increasingly difficult to see how the current currency regime based on the dollar will survive. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/inflation-will-return-july-2023?gmrefcode=gata

END

Kinesis joins Valaurum to put gold in those bills

(Kinesis London)

Kinesis joins Valaurum to put practical amounts of gold in circulation

Submitted by admin on Thu, 2023-07-27 13:24Section: Daily Dispatches

Kinesis to Produce Physical Gold Bills in Partnership with Valaurum

By Sean Dickens

Kinesis, London

Thursday, July 27, 2023

Kinesis has established a global collaborative partnership with Valaurum, the manufacturer of the patented Aurum gold bill, to produce a series of Kinesis gold bills containing small, practical amounts of physical gold for investment and global spending.

The launch of Kinesis Aurum gold bills is set to provide the Kinesis community — as well as gold investors, collectors, and enthusiasts across the world — with a new way to spend and store physical gold.

Central to the partnership, Kinesis and Valaurum will be releasing a series of co-branded bills, titled “Kinesis Aurum,” featuring unique custom designs and beginning with two bills containing one-tenth of a gram (100 milligrams) and 1 gram of gold, respectively. The precise, micro-layer of gold enshrined within the Kinesis Aurum will be visible from edge to edge throughout each bill.

Outside of the digital solution of Kinesis, the weight and indivisibility of gold has made the metal impractical as everyday money. Through encasing smaller denominations of gold within bills, Kinesis Aurum is reintroducing physical gold as a circulating currency. …

… For the remainder of the announcement:

END

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES/SILVER

Andrew Maguire: Live from the vault 133

UAE India partnership to trigger a surge in Indian SILVER demand – LFTV Ep: 133

•

1.4K views • 2 hours ago

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1555

OFFSHORE YUAN: DOWN TO 7.1580

SHANGHAI CLOSED UP 59.26 PTS OR 1.84%

HANG SENG CLOSED UP 277.45 PTS OR 1.41%

2. Nikkei closed DOWN 131.93 PTS OR 0.40%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 101.22 EURO RISES TO 1.1107 UP 30 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.558 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 139.13/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ON SHORE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.433***/Italian 10 Yr bond yield RISES to 4.067*** /SPAIN 10 YR BOND YIELD RISES TO 3.471…**

3i Greek 10 year bond yield RISES TO 3.750

3j Gold at $1955.85 silver at: 24.28 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 43 /100 roubles/dollar; ROUBLE AT 91.02//

3m oil into the 79 dollar handle for WTI and 83 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 139.13// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.558% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8679 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9555 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

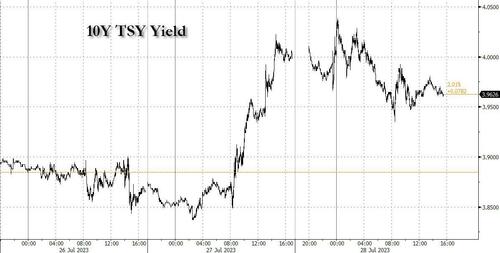

USA 10 YR BOND YIELD: 3.961 DOWN 5 BASIS PTS…

USA 30 YR BOND YIELD: 4.018 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.877 DOWN 7 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.96…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 5 BASIS PTS AT 4.350

end

2.a Overnight: Newsquawk and Zero hedge:

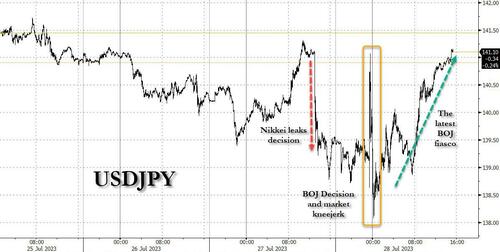

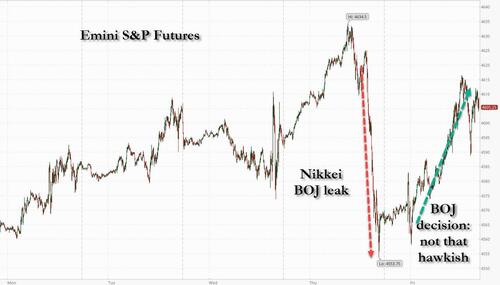

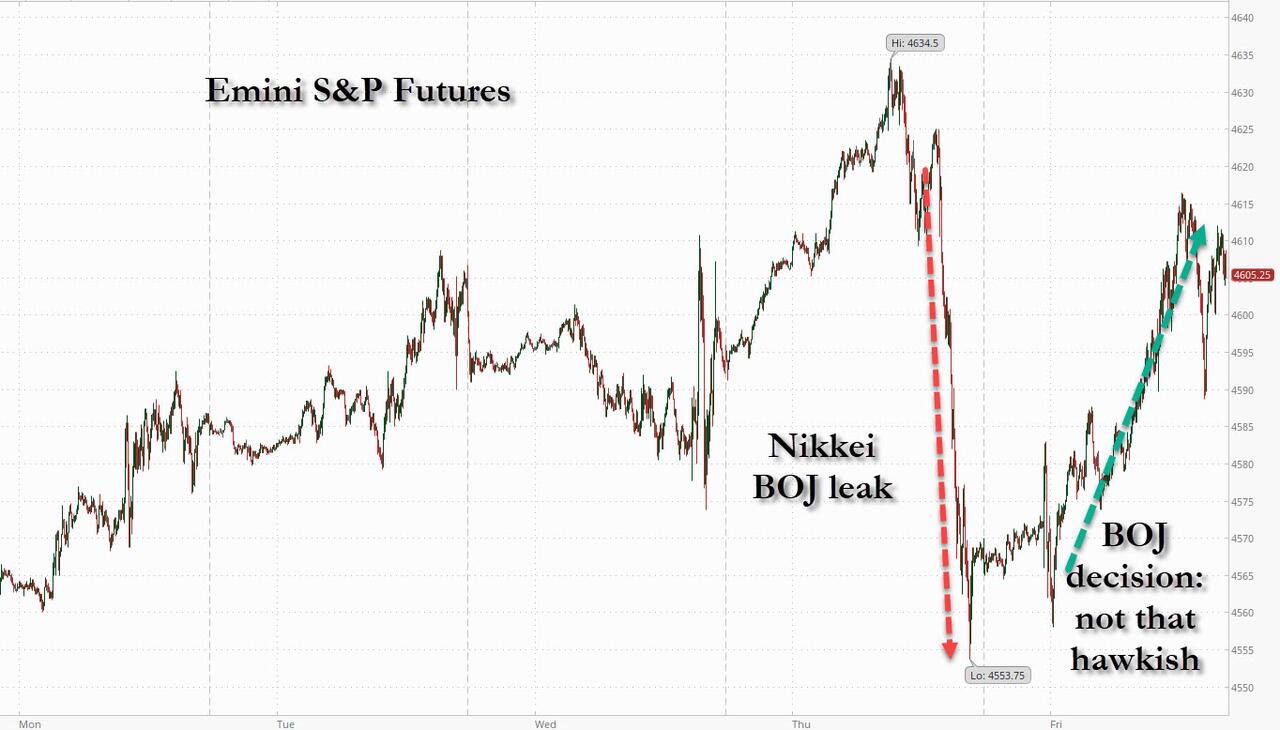

Futures Rebound After BOJ YCC “Tweak” Turns Out To Be Less Hawkish Than Some Feared

FRIDAY, JUL 28, 2023 – 08:09 AM

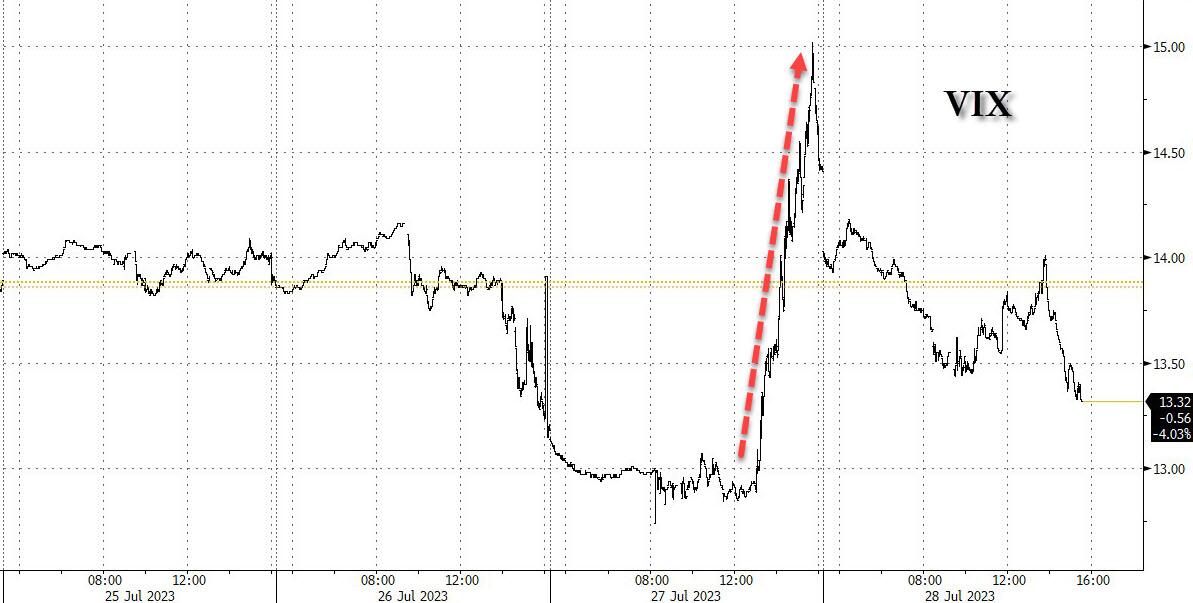

US equity futures reversed an earlier loss and traded at session highs even as bonds around the world fell, briefly sending the 10Y Treasury to 4.04% and JGBs to 0.57%, well above the previous 0.5% cap and the highest since 2014, after the Bank of Japan – the only major central bank not to have begun reversing ultra-easy monetary policy – surprised investors by tweaking its control of market rates, in a market test to how far it can go without explicitly starting normalization. But in the end, the tweak ended up being less hawkish than some feared and as a result, futures are now reversing much of yesterday’s sharpo losses.

Having previously capped bond yields at 0.5% in a bid to stoke borrowing and its economy, the central bank said today it now regarded that level as a reference point rather than a rigid limit, and instead of intervening to keep rates capped at 0.5% it would only do so firmly at 1.0%, while deciding whether and where to intervene in the 0.5% to 1.0% band (the BOJ graphic explaining the change is below).

The BOJ pledged to show more flexibility over its yield curve control policy, though governor Kazuo Ueda insisted the bank was still far from the point where it could raise rates, and by then global deflation will have returned anyway.

In stock markets, the busiest week in the earnings calendar was drawing to a close, with sentiment supported by forecast-beating results and conviction that interest rates in the US and euro zone are near their peak. As of 7:30am ET, S&P futures traded 0.5% higher, reversing some of yesterday dump which was sparked, ironically, by a planted story in the Nikkei previewing the BOJ’s action, which however turned out to be less hawkish than expected, and thus the equity market overreacted on Thursday, and rebounded today as 10Y yields traded down to 3.96% after rising as high as 4.04%

In premarket trading, Enphase Energy shares plunged 15% after the solar-equipment manufacturer reported second-quarter revenue that missed estimates. Analysts found the results to be disappointing, and noted that the third-quarter revenue outlook also failed to meet expectations. On the other end, First Solar shares jumped as much as 9% after the solar technology company results beat estimates and announced plans for a new manufacturing facility in the US, which analysts took as a sign of confidence in demand. Brokers also highlighted strong bookings and average selling prices. Here are some other notable premarket mover:

Ford shares drop 2% after the automaker said it now expects to see losses from electric vehicles hit $4.5 billion this year. While Ford’s other segments performed well, Morgan Stanley sees major changes to the EV strategy possibly being necessary.

- Homology Medicines shares surge 17% after the biotech said it will evaluate strategic alternatives and cut 87% of its workforce, citing the current financing environment and Homology’s anticipated clinical development timelines. RBC said that the decision to preserve cash was “pragmatic.”

- Intel shares are rise as much as 8% in premarket trading on Friday after the chipmaker reported second-quarter results that beat expectations as its PC business was starting to recover. The company’s CEO says Intel remains on track to meet its of target of regaining manufacturing leadership by 2025.

- Roku shares rise nearly 10% after the streaming-video platform company reported second-quarter revenue that was much stronger than expected. While analysts were positive about the results, they warned that Hollywood strikes would turn into a headwind if they prolong.

- Solar stocks fell in US premarket trading after Enphase Energy reported second-quarter revenue that missed the average analyst estimate, and gave lower-than-anticipated third-quarter revenue guidance.

The BOJ move also sparked speculation it marked the first step towards the end of extraordinary stimulus after the recent surge in inflation. It also triggered big swings in the yen, sending it as much as 1% lower and higher at one point against the dollar, before trading largely unchanged compared to the pre-BOJ announcement. Despite the rollercoaster move, the yen was still headed for its best month since March, with gains of almost 3.5%.

“The BOJ decision is an invitation to short dollar-yen,” said Kenneth Broux, currency strategist at Societe Generale SA. “Higher Japanese yields reduce the spread versus US Treasuries and German bunds.” He added however that dollar downside could be limited, given Thursday’s strong US data that could imply further Fed tightening; furthermore sticky rate differentials mean that those who are stuck in a short USDJPY will suffer brutal bleeding thanks to the 5.50% difference between the BOJ and the Fed, a difference which will remain for a long time.

Markets elsewhere reacted to the possibility that higher yields at home will persuade Japanese investors, who own sizable amounts of US, European and Australian bonds, to reduce overseas debt holdings. As noted above, US Treasury yields rocked as high as 4.04% – first after a Nikkei news report that Japan was poised to tweak its yield-curve control policy, and then after the BOJ indeed tweaked it – but then yields dipped back down to 3.96% after markets digested the announcement realizing that it is not as hawkish as some had feared.

Elsewhere, the German 10Y Bund increased as much as 5 basis points, and Australia’s climbed 20 basis points at one point.

“This is a big week as it signals we are pretty much at the end of hiking cycles globally,” said Peter Kinsella, head of currency strategy at asset manager Union Bancaire Privee UBP SA. The “BOJ is effectively saying the top of the yield range is now 1% so that implies 50 basis points in potential steepening. So it’s slow gradual normalization, but yes, it’s normalization BOJ style,” he added.

European stocks are in the red with technology leading declines while banks rise. While the Stoxx 600 is down 0.3%, European bourses were still set for their third straight weekly gain. Here are the most notable European movers:

- AstraZeneca gains as much as 4.8% after reporting second-quarter sales and profit that beat estimates and announcing the $1 billion acquisition of a portfolio of rare disease gene therapies from Pfizer

- Hermes shares jumped as much as 4.3% after the French luxury group outperformed its rivals during the second quarter with unabated demand for its high-end purses, notably in the US and China

- Standard Chartered shares rise as much as 6.7% in London, the most since March, after the bank reported better-than-expected pretax profit for the second quarter

- Eni shares rise as much as 1.8% after the Italian oil and gas giant’s second-quarter profit beat consensus estimates, with the analysts flagging a strong performance at its Global Gas & Lng Portfolio (GGP) unit

- Euronext shares jump as much as 7.1%, most since March, after the exchange operator reported revenue for the second quarter that beat the average analyst estimate and announced a €200m buyback

- Ams-OSRAM shares rally as much as 19%, their biggest one-day climb since 2020. The company says it will exit non-core and lower-performing semiconductor businesses, a move that analysts say will help facilitate a turnaround and its debt refinancing

- Sanofi falls as much as 4.1%, the most since May 30, after the French drugmaker reported its latest earnings, which analysts say is a mixed bag, as overall sales missed slightly and growth for its key drug Dupixent only arrived in line

- Air France-KLM shares fall as much as 6% after analysts noted headwinds including elusive profit guidance and a higher unit-cost forecast, even as the company posted a strong 2Q operating income beat

- Signify shares fell as much as 5.1%, the biggest drop since May 18, after the lighting maker cut its adjusted Ebita margin forecast for the full year and reported revenue for the second quarter that missed the average analyst estimate

- Atos shares sink as much as 20% after the French IT firm recorded a negative free cash flow of €969m in the first half, a figure that is well below analyst estimates and is about three quarters of the stock’s market value

- Vanquis Banking shares slumped as much as 29% to their lowest level in over 30 years, after the specialist lender reported a loss and a decrease in its net interest margin

- Evotec falls as much as 11%, the most since November, after the German biotech cut its full-year forecast as the effects from the cyberattack earlier this year continues to impact the firm’s earnings

Earlier in the session, Asia’s equity benchmark held steady as a rally in Chinese stocks was offset by losses in Japan, where the central bank jolted markets by loosening its grip on bond yields. The MSCI Asia Pacific Index was little changed on Friday, but headed for a 2% weekly gain as Chinese shares extended this week’s rally on emerging signs that Beijing is acting on its policy pledges. Meanwhile, the Nikkei 225 slid as much as 2.6%, the worst performance in Asia, on concern the Bank of Japan’s adjustment paves the way for a stronger currency, potentially hurting exporters, however the Nikkei eventually rallied sharply, closing down just 0.4% led by Japan’s lenders who rallied on optimism their profitability will improve.

Regional stocks have climbed this week on hopes of stimulus measures in China following the Politburo meeting. A gauge of the nation’s equities listed in Hong Kong jumped as much as 1.7% on Friday after regulators were said to have signaled additional support for the technology sector and on speculation that authorities may lower stamp duties to bolster trading. Tencent and Meituan were among the top positive contributors in the MSCI Asia gauge, while Japan’s Sony and Toyota Motor were among the biggest drags.

Asia’s stock benchmark climbed for a fourth straight day on Thursday after the US central bank raised interest rates to a 22-year high and said further tightening would be data dependent. The gauge is approaching this year’s high seen in January though its gain of 9% so far in 2023 compares poorly with the S&P 500 Index’s 18% advance. Optimism over earnings, gains in China and rising speculation that the Federal Reserve is nearing the end of its policy tightening have boosted sentiment toward Asia’s emerging-market equities in recent weeks.

The MSCI Asia gauge is on track for a second straight month of gains, with its 3.7% rally in July set to be the best since January. An index of Southeast Asian stocks has jumped close to 6% this month, heading for the best performance since November. “There is enormous potential for emerging-market equities to play catch up on emerging market debt in a world where the Fed stops tightening and the dollar weakens,” Christopher Wood, global head of equity strategy at Jefferies, wrote in a note.

Australia’s ASX 200 was pressured amid weakness in the property sector and miners, with sentiment also not helped by the surprise contraction in Retail Sales

The record-breaking India stock market ended the week among the worst performing markets in the region as sentiment was hit by weaker-than-expected earnings from some index heavyweights. The S&P BSE Sensex fell 0.2% on Friday to 66,160.20 in Mumbai, while the NSE Nifty 50 Index was little changed at 19,646.05. The MSCI Asia Pacific Index was up 0.5% for the day. For the week, benchmark indexes lost 0.8% as compared to the regional benchmark’s 2.6% gains. Indian equities underperformed their peers in China, Hong Kong and Taiwan. The losses in the benchmarks during the week were limited by continued net buying of stocks by global funds, who look set to mark their fifth consecutive month of net purchases in July. Global funds have net bought over $19 billion since end of February. HDFC Bank contributed the most to the Sensex’s decline, decreasing 1.7%. Out of 31 shares in the Sensex index, 15 rose and 15 fell, while 1 was unchanged

In FX, the Bloomberg Dollar Spot Index slipped, while Treasury yields fell led by the short-end of the curve. USD/JPY fell more than 1% after the BOJ decision before gaining by a similar amount. It was down 0.1% at 139.30 at 10:30 a.m. London. Dollar sell-stops are building below 137.25, the July 14 low and buy stops above 142, according to Asia-based FX traders. European short-end bonds gained following dovish comments by ECB policymakers; Money markets ease ECB tightening wagers for a second day.

In rates, treasuries held gains in early US trading, led by the short end, steepening the curve. Curves are steeper globally led by UK and Japan, where 10-year yields jumped to highest level in nearly a decade after BOJ effectively adopted a higher target, a move previewed during US trading hours Thursday. US yields lower across the curve by as much as 5bp-6bp at short end with long end little changed; however 30-year earlier climbed to within 0.1bp of its July 10 YTD high 4.082%.

Yields remain higher on the week with the curve steeper, as focus began shifting from Fed policy stance — which Chair Powell this week said was evenhanded with respect to another interest-rate hike in September — to strong economic growth indicators and expectations that Treasury auction size increases will be announced next week for the August-to-October financing period. Also ahead next week, month-end Treasury index rebalancing is projected to extend its duration by 0.07 year, and first major economic indicators for July including ISM manufacturing and services gauges and employment report are slated.

In commodities, crude futures decline with WTi falling 0.3%. Spot gold adds 0.2%.

Bitcoin prices are relatively stable just above the USD 29,000 level.

To the day ahead now, and data releases from the US include the Q2 employment cost index, June’s PCE inflation, personal income and personal spending, and the final University of Michigan consumer sentiment index for July. Over in Europe, we’ll get the French and German CPI readings for July. Central bank speakers include the ECB’s Simkus. Finally, earnings releases include Exxon Mobil and Procter & Gamble.

Market Snapshot

- S&P 500 futures up 0.3% to 4,578.25

- MXAP up 0.3% to 169.86

- MXAPJ up 0.1% to 536.74

- Nikkei down 0.4% to 32,759.23

- Topix down 0.2% to 2,290.61

- Hang Seng Index up 1.4% to 19,916.56

- Shanghai Composite up 1.8% to 3,275.93

- Sensex down 0.5% to 65,953.22

- Australia S&P/ASX 200 down 0.7% to 7,403.65

- Kospi up 0.2% to 2,608.32

- STOXX Europe 600 down 0.4% to 470.02

- German 10Y yield little changed at 2.52%

- Euro down 0.1% to $1.0963

- Brent Futures down 0.2% to $84.03/bbl

- Gold spot up 0.2% to $1,949.96

- U.S. Dollar Index up 0.12% to 101.90

Top Overnight News from Bloomberg

- China’s markets regulator has consulted securities firms for possible measures to boost stocks amid growing signs Beijing is seeking to restore investor confidence, people familiar with the matter said. BBG

- China has asked its largest technology companies to provide case studies of their most successful startup investments in consumer, telecom and media companies, a sign authorities are ready to grant them broader leeway in backing such deals after a crackdown brought them to a virtual halt two years ago. BBG

- The White House has decided it will bar Hong Kong’s top government official from attending a major economic summit in the United States this fall, according to three U.S. officials familiar with the matter, in the latest test of President Biden’s bid to reset relations with China. Washington Post

- The Tokyo CPI for Jul overshoots the Street, with core (ex-food/energy) coming in at +4% Y/Y (up from +3.8% in June and ahead of the Street’s +3.7% forecast). RTRS

- The BOJ surprised markets by loosening its grip on bond yields. It kept the target for 10-year yields at around 0% but said its 0.5% ceiling was now a reference point — not a rigid limit. It will manage the curve “flexibly” and buy benchmark bonds at 1% every business day, effectively capping it at that level. BBG

- Donald Trump has been accused of attempting to have surveillance video footage at his Mar-a-Lago estate deleted ahead of an FBI search, as federal prosecutors added more criminal counts to a case over the former US president’s handling of classified documents. FT

- Office space set to shrink for the first time on record – the lack of new supply coupled with existing buildings being repurposed or destroyed means the total square footage available to be used as office space will shrink this year for the first time on record. BBG

- Tech investment giant Sequoia Capital pared back the size of two major venture funds, part of a dramatic downsizing the venture firm is undertaking amid a startup downturn. WSJ

- Facebook removed content related to Covid-19 in response to pressure from the Biden administration, including posts claiming the virus was man-made, according to internal company communications viewed by The Wall Street Journal. WSJ

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed with the region cautious as all attention was on the BoJ policy decision in which the central bank kept monetary policy settings unchanged but announced to guide YCC more flexibly with fixed rate operations for 10yr JGB to be conducted at 1.0% (prev. 50bps). ASX 200 was pressured amid weakness in the property sector and miners, with sentiment also not helped by the surprise contraction in Retail Sales. Nikkei 225 underperformed with yields higher and markets spooked by the latest BoJ developments. Hang Seng and Shanghai Comp shrugged off early weakness and gained after further calls and efforts for China to support the housing market and tech industry. US equity futures were rangebound overnight although slumped during US trade as markets faltered stateside following source reporting by the Nikkei on the BoJ. European equity futures are indicative of a lower open with the Euro Stoxx 50 -0.4% after the cash market closed up by 2.3% yesterday.

Top Asian News

- Chinese market watchdog has reportedly asked brokers for advice to boost stocks, according to Bloomberg; brokers reportedly proposed stamp duty reduction.

- Italian PM Meloni said she plans to go to China in one of her next diplomatic missions and the decision on leaving China’s Belt and Road Initiative will be made by December.

- China reportedly urges improved mortgage rules to support the housing market, while it also asked tech giants to showcase investments in a sign of easing, according to Bloomberg.

- US is to ban Hong Kong Chief Executive Lee from the APEC Economic Summit, according to Washington Post.

European equities are a mixed bag as the dust settles on yesterday’s ECB announcement and the overnight BoJ release. The Stoxx 600 index is on track to close the week out with gains over just over 1% with discrepancies between regional bourses stemming from various heavyweight earnings releases. Equity sectors in Europe have a negative tilt with Tech, Real Estate and Travel & Leisure names lagging peers. US equity futures are trading on the front foot, as positivity seemingly returns following a sell-off in stocks yesterday, after a slew of hot data prints ahead of today’s top-tier data.

Top European News

- ECB’s Simkus says the choice for September is between 25bps hike and unchanged rate; rate cut unlikely in H1’24; would not call a situation a recession, it is more a soft landing scenario, according to Reuters.

- ECB’s Villeroy says French data showing inflation is falling without a recession; Pragmatism also needed as decisions at upcoming rate meetings will be open and entirely data drivenPerseverance is now the prime key virtue given the time needed for full transmission of monetary policy. Our growing confidence in the fall in inflation towards 2% is based on the good transmission of monetary policy, according to Reuters.

- ECB’s Kazimir says ECB is nearing the completion of policy tightening; he is still waiting for an answer for what is coming in September; says ECB’s mission is still not fulfilled and “we should take firm step further”. He noted if ECB was to take a break in September, it would be premature to consider it the end, and added the ECB looking for the right place to stay for a large part of next year, according to Reuters.

- ECB Survey of Professional Forecasters (SBF): expectations for headline HICP inflation were broadly unchanged compared to the previous survey

FX

- XY briefly topped 102.00 earlier in the European morning. Dollar paused for breath after Thursday’s sharp rebound on bullish US data and Euro depreciation on the back of a dovish ECB hike, but retained a firm underlying bid.

- The Buck faced strong competition from the Yen following the BoJ’s hawkish “surprise” as this hammered USD/JPY down to within single digit pips of 138.00 at one stage from 141.05

- Antipodeans lag with the Aussie underperforming as Australian Retail Sales were downwardly revised, while market pricing was already tilting heavily in favour of no change in rates from the RBA next week.

Fixed Income

- Debt futures have settled down following several bouts of fast market moves and high volatility amidst somewhat mixed data and further reaction to or reflection on Central Bank meetings that threw several surprises.

- Bunds and Gilts have regained poise within wider 132.96-81 and 95.62-11 respective ranges, while OATs and Bonos lag in wake of French and Spain inflation data.

- The T-note remains above parity between 110-10+/110-25+ parameters in consolidative trade after yesterday’s mostly stellar US macro releases and turning attention to another busy agenda to end a hectic week.

Commodities

- WTI and Brent front-month futures continue with the choppy but horizontal performance seen overnight with prices moving in tandem with the broader risk sentiment. Complex-specific newsflow has been light this morning aside from the release of overall mixed GDP from various EZ nations.

- Spot gold was dragged back under its 100 DMA (USD 1,966.76/oz) to levels near USD 1,950/oz yesterday following the hot US economic data, with prices today meandering around the half-round figure and on both sides of the 50 DMA and 21 DMA.

- Base metals meanwhile are mostly firmer despite the stronger Dollar amid continued tailwinds from Chinese stimulus.

Geopolitics

- Russia prevented a Ukrainian drone attack on targets in Moscow, according to RIA citing the Defence Ministry.

- US President Biden and Italian PM Meloni’s joint statement said the US and Italy will continue to provide political, military, financial and humanitarian assistance to Ukraine for as long as it takes. US and Italy are firmly committed to a free, open, prosperous, inclusive and secure Indo-Pacific, while they reiterated the vital importance of maintaining peace and stability across the Taiwan Strait. Furthermore, they commit to strengthening the bilateral and multilateral consultation on the opportunities and challenges posed by China.

- US is expected to announce a weapons package for Taiwan worth more than USD 300mln, according to US officials cited by Reuters.

- North Korea staged a military parade in celebration of the 70th anniversary of the end of the Korean War, while the Chinese delegation attended the parade and North Korea displayed an ICBM at the parade, according to KCNA.

- North Korean leader Kim had a formal lunch with Russian Defence Minister Shoigu and exchanged views on the political situation around the Korean peninsula, as well as discussed issues to advance strategic cooperation on military and security. Furthermore, North Korea said it will fight on the side of countries challenging US hegemony, according to KCNA.

- Russian President Putin said North Korea’s support for the military operation against Ukraine emboldens the two countries’ determination to cope with Western organisations, according to KCNA.

- Russia’s Putin says we will discuss peace plan today, according ot Reuters.

- China declares a large no-sail zone in the South China Sea for military exercises from July 29 to August 2nd, according to a journalist on Twitter.

US Event Calendar

- 08:30: June PCE Deflator MoM, est. 0.2%, prior 0.1%

- June PCE Core Deflator MoM, est. 0.2%, prior 0.3%

- June PCE Core Deflator YoY, est. 4.2%, prior 4.6%

- June PCE Deflator YoY, est. 3.0%, prior 3.8%

- June Personal Income, est. 0.5%, prior 0.4%

- June Personal Spending, est. 0.4%, prior 0.1%

- June Real Personal Spending, est. 0.3%, prior 0%

- 10:00: July U. of Mich. Sentiment, est. 72.6, prior 72.6

- July U. of Mich. Current Conditions, prior 77.5

- July U. of Mich. Expectations, prior 69.4

- July U. of Mich. 5-10 Yr Inflation, est. 3.0%, prior 3.1%

- July U. of Mich. 1 Yr Inflation, prior 3.4%

- 11:00: July Kansas City Fed Services Activ, prior 14

DB’s Jim Reid concludes the overnight wrap

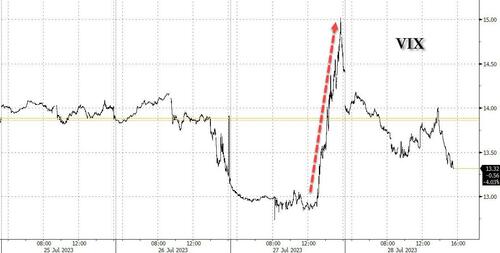

It was originally another great day for the fictitious soft-landing ETF yesterday until markets started to break down around 6pm London time last night after a softish 7-year Treasury auction and more importantly, a report from Nikkei suggesting the BoJ would discuss tweaks to YCC at this morning’s meeting, something they’ve followed through on as we’ll see immediately below. This turned an +8bps sell-off in 10yr US yields into a +13.1bps one by the close and turned the S&P 500 from a +0.7% gain to a -0.64% loss, with the NASDAQ moving from c.+1.3% to -0.22% over the same 3 hour late session period. It all overshadowed a relatively dovish ECB meeting, within the context of the expected +25bps hike, afterwhich European yields moved notably lower for the day (e.g. 2yr bunds -5.1bps).

So the last international hold out on ultra low yields has turned with the BoJ tweaking it’s YCC policy in the last couple of hours. In a slightly complicated message the BoJ kept their target for 10yr JGBs at 0% but effectively widened the band to +1% from 0.5% even if they’ve kept the original bands as reference points. It confused me a bit this early in the morning but they won’t be able to defend 0.5% now absent a macro development that structurally lowers yields. 10yr JGBs have increased +12bps as we type to 0.56bps, their highest since 2014 and all other things being equal this should continue to creep up in the days and weeks to come and removes an anchor for global yields. It’s going to be an interesting press conference just after we go to print.

Initially, the Japanese yen strangely fell on the news to 141 but now trades +0.6% higher at 138.6. Elsewhere the Nikkei (-2.24%) is sharply lower with the KOSPI (-0.26%) also trading in the red. Chinese stocks are bucking the trend with the CSI (+1.79%) leading gains followed by the Shanghai Composite (+1.38%) and the Hang Seng (+0.89%). US stock futures are edging slightly higher with those tied to the S&P 500 +0.18%. Meanwhile, yields on 10yr USTs (+3.01bps) are at 4.02% as we go to press.

Coming back to Japan, Tokyo’s consumer price index (CPI) rose +3.2% y/y in July (v/s +2.9% expected). This is the 14th consecutive month that the inflation rate in the capital came in above the BOJ’s 2% target. At the same time, core inflation (excluding fresh food) advanced +3.0% y/y in July, higher than Bloomberg estimates of +2.9% but lower than prior month’s reading of 3.2%. More surprising was the core-core inflation (excluding fresh food and energy) which climbed to +4.0% y/y in July (v/s +3.7% expected, +3.8% in June) and provided more justification for the move today. Elsewhere, Australia’s retail sales sharply declined by -0.8% m/m in June, recording its biggest decline this year, versus expectations of a flat outcome.

Before the 6pm London headline markets were riding high on optimism and shrugging off higher US yields. This all stemmed from another round of strong US data that added to investors’ optimism. At one point the Dow Jones was comfortably on track to record a 14th consecutive daily advance for the first time since the index’s creation in 1896. So a 1-in-a-127 year event. Blame the Nikkei article for that streak being over and only equally the record run.

Even before the late rate moves investors were growing increasingly sceptical about Fed rate cuts anytime soon, with the 2yr real yield (+6.3bps) hitting another post-GFC high of 3.058% with 2yr nominal yields up +7.7bps. The rate priced in for the December 2024 meeting rose by +15.3bps on the day to 4.23%. This moved US rates in the opposite direction to European yields (2yr bunds -5.1bps) after a slight dovish bias to the ECB meeting. All these moves will be put to the test today, or reinforced, by US core PCE, US ECI (important to see if labour costs can fall organicallly), alongside German and French CPI.

The main catalyst for the early move higher in US rates, and the earlier risk on yesterday, was a robust GDP print from the US, which showed growth accelerated in Q2 to an annualised pace of +2.4% (vs. +1.8% expected). The report also came with several positive details, including that core PCE inflation was only at +3.8% in Q2 (vs. +4.0% expected), which added to the recent theme of better-than-expected growth and softer-than-expected inflation. As well as the GDP release, the weekly jobless claims fell for a third week running to 221k over the week ending July 22 (vs. 235k expected), which is their lowest level since February. And the continuing claims print for the previous week came in at a post-January low of 1.69m (vs. 1.75m expected). So lots of good news all round from an economic standpoint maybe before the full impact of the monetary policy lag starts to bite.

So as discussed at the top equities faded into the close with tech stocks seeing the biggest beta to the move with the FANG+ index falling from c.+2.3% to -0.24% in the last 3 hours of trading. Meta (+4.40%) outperformed thanks to its strong Q2 results after the previous day’s close. This helped lift the communication services sector into the green for the day (+0.85%) while the rest of the top level S&P sectors declined, most notably real estate (-2.13%) and utilities (-1.73%). In Europe markets closed before the sell-off and neatly encapsulated the earlier bullish sentiment, with the STOXX 600 (+1.35%) hitting a 17-month high, whilst France’s CAC 40 (+2.05%) and Italy’s FTSE MIB (+2.13%) saw significant advances of their own.

Before all this excitement, the ECB delivered their own 25bp rate hike as expected, which took the deposit rate up to 3.75%. However, unlike recent meetings, there wasn’t a strong steer about what they’re going to do next, and President Lagarde said that “we have an open mind as to what the decisions will be in September and in subsequent meetings”. She avoided signalling a specific outcome, and said that if they did pause, then it “would not necessarily be for an extended period.” At the same time, the language in the statement was also softened, since it said that future decisions would ensure rates “will be set at sufficiently restrictive levels”. That’s a change from last time, when it said they “will be brought to levels sufficiently restrictive”. See our economists’ review here.

When it comes to the ECB’s next decision, we should start to get some more signals today, as the flash CPI releases from France, Spain and Germany are coming out ahead of the Euro Area-wide release on Monday. Obviously the data will go a long way to determining the likelihood of another move, but markets are still pricing in a 71.7% chance of another 25bp hike in September anyway. Nevertheless, sovereign bonds rallied yesterday after the decision, with yields on 10yr bunds (-1.0bps), OATs (-1.6bps) and BTPs (-3.0bps) all coming down. That divergence between Europe and the US also meant that the spread of 10yr Treasury yields over 10yr bunds reached its widest level of 2023 so far, at 153.4bps.