GOLD PRICE CLOSED: DOWN $9.60 TO $1925,80

SILVER PRICE CLOSED: DOWN $0.40 AT $22.76

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1925.65

Silver ACCESS CLOSE: 22.76

Shanghai Gold Benchmark Price

USD oz gram kilo tola

AM1965.74

PM1964.19

New York price at the time: 1933.00

premium $32.00

xxxxxxxxxxxxxxxxxx

Bitcoin morning price:, $29,364 UP 297 Dollars

Bitcoin: afternoon price: $29,067 DOWN 22 dollars

Platinum price closing $903.95 DOWN $20.55

Palladium price; $1224,20 DOWN $17.35

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,584.68 DOWN 4.40 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1510.41 DOWN 4.86 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1756,98 DOWN 3.18 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: AUGUST 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,933.500000000 USD

INTENT DATE: 08/07/2023 DELIVERY DATE: 08/09/2023

FIRM ORG FIRM NAME ISSUED STOPPED

152 C DORMAN TRADING 4

190 H BMO CAPITAL 210

323 C HSBC 190

357 C WEDBUSH 1

363 H WELLS FARGO SEC 57

365 H MAREX CAPITAL M 1

435 H SCOTIA CAPITAL 153

624 H BOFA SECURITIES 455

661 C JP MORGAN 174 662

685 C RJ OBRIEN 1

690 C ABN AMRO 24

700 C UBS 2019

709 C BARCLAYS 48

726 C CUNNINGHAM COM 2

737 C ADVANTAGE 21

880 C CITIGROUP 2

991 H CME 362

TOTAL: 2,193 2,193

MONTH TO DATE: 9,960

JPMorgan stopped 662/2193 contracts.

FOR AUGUST:

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2023. CONTRACT: 2193 NOTICES FOR 219,300 OZ or 6.8211 TONNES

total notices so far: 9960 contracts for 996000 oz (30.979 tonnes)

FOR AUGUST:

SILVER NOTICES: 44 NOTICE(S) FILED FOR 220,000 OZ/

total number of notices filed so far this month : 892 for 4,460,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $9.60

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 906.00 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 40 CENTS AT THE SLV// NO CHANGES IN SILVER INVENTORY AT THE SLV:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 448.987 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUMONGOUS SIZED 3560 CONTRACTS TO 141,517 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUMONGOUS SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.46 LOSS IN SILVER PRICING AT THE COMEX ON MONDAY. TAS ISSUANCE WAS A JUPITER SIZED 8716 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 8716 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.46). BUT WERE UNSUCCESSFUL IN KNOCKING OF ANY SILVER CONTRACTS AS WE HAD OUR HUMONGOUS GAIN OF 5662 CONTRACTS ON BOTH EXCHANGES.

WE MUST HAVE HAD:

A GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICALS( 2062 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.105 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 225,000 OZ QUEUE JUMP //NEW STANDING RISES AT 4.465 MILLION OZ + OUR NEW CRIMINAL 0 CONTRACTS OF EXCHANGE FOR RISK FOR 0.00 MILLION OZ + 1.45 MILLION OZ EX. FOR RISK/PRIOR/// NEW TOTAL STANDING FOR SILVER: 5.940 MILLION OZ/// // // GIGANTIC SIZED COMEX OI GAIN/ HUGE SIZED EFP ISSUANCE/VI) JUPITER SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE (8716 CONTRACTS)/ZERO EXCHANGE FOR RISK ISSUED

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL 261 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTRACTS for 6 days, total 6459 contracts: OR 32.295 MILLION OZ (1076 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 32.295 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 32.295 MILLION OZ

RESULT: WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3560 CONTRACTS WITH OUR LOSS IN PRICE OF $0.46 IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 2062 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 3.105 MILLION OZ FOLLOWED BY TODAY’S 225,000 OZ QUEUE JUMP//NEW STANDING 4.465 MILLION OZ+ 1.45 MILLION OZ EXCHANGE FOR RISK NEW TOTALS 5.940 MILLION OZ//// .. WE HAVE A HUMONGOUS SIZED GAIN OF 5622 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE 8716//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION . THE NEW TAS ISSUANCE MONDAY NIGHT (8716) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE./

WE HAD 44 NOTICE(S) FILED TODAY FOR 220,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 1026 CONTRACTS TO 431,434 AND CLOSER TO TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED: 297 CONTRACTS

WE HAD A SMALL SIZED DECREASE IN COMEX OI ( 1026 CONTRACTS) WITH OUR $5.45 LOSS IN PRICE//MONDAY. WE ALSO HAD A RATHER SMALL INITIAL STANDING IN GOLD TONNAGE FOR AUGUST. AT 30.656 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 16,400 OZ QUEUE.JUMP + PRIOR ISSUANCE OF EXCHANGE FOR RISK = (.684 TONNES) //NEW STANDING 31.639 TONNES + .684 EXCHANGE FOR RISK = 32.323/ + /A FAIR (AND CRIMINAL) ISSUANCE OF 1757 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH A $5.45 LOSS IN PRICE WITH RESPECT TO MONDAY’S TRADING.WE HAD A SMALL SIZED GAIN OF 884 OI CONTRACTS (2.749 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1910 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 431,731

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 884 CONTRACTS WITH 1026 CONTRACTS DECREASED AT THE COMEX// AND A FAIR 1910 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 884 CONTRACTS OR 2.749 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 1657 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1910 CONTRACTS) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (1026) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 884 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR JULY AT 30.656 TONNES FOLLOWED BY TODAY’S 16,400 OZ QUEUE JUMP //NEW STANDING 31.639 TONNES + .684 TONNES (EXCHANGE FOR RISK//PRIOR) NEW TOTALS: 32.323 TONNES/// 3) ZERO LONG LIQUIDATION WITH SOME TAS LIQUIDATION //4) SMALL SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 1657 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUG :

TOTAL EFP CONTRACTS ISSUED: 17,459 CONTRACTS OR 1,745, 900 OZ OR 54.30 TONNES IN 6 TRADING DAY(S) AND THUS AVERAGING: 2909 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 6 TRADING DAY(S) IN TONNES 54.30 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 54.30/3550 x 100% TONNES 1.69% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 54.30 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 3560 CONTRACTS OI TO 141,517 AND CLOSER TO OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A HUGE 2062 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 2062 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2062 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 3560 CONTRACTS AND ADD TO THE 2062 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 5622 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 28.11 MILLION OZ

OCCURRED DESPITE OUR $0.46 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED DOWN 8.21 PTS OR 0.25% //Hang Seng CLOSED DOWN 353.75 PTS OR 1.81% /The Nikkei CLOSED UP 122.73 PTS OR 0.38% //Australia’s all ordinaries CLOSED DOWN 0.01 % /Chinese yuan (ONSHORE) closed DOWN 7.2175 /OFFSHORE CHINESE YUAN DOWN TO 7.2447 /Oil UP TO 80.66 dollars per barrel for WTI and BRENT UP AT 83.65 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 1026 CONTRACTS DOWN TO 431,434 WITH OUR LOSS IN PRICE OF $5.45 ON MONDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF AUGUST… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 1910 EFP CONTRACTS WERE ISSUED: : DEC 1910 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1910 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 884 CONTRACTS IN THAT 1910 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED LOSS OF 729 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $5.45//MONDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS A FAIR 1657 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THE HUGE NUMBER OF T.A.S. CONTRACTS INITIATED OVER THE PAST SEVERAL WEEKS SPELLS TROUBLE FOR THE GOLD/SILVER MARKET AS RAIDS WILL SURELY BE UPON US TRYING TO CONTAIN OUR PRECIOUS METALS RISE IN PRICE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: AUGUST (32.323) (NON ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 32.323 TONNES (INCLUDING .6842 EXCHANGE FOR RISK)

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $5.45) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A SMALL GAIN OF 884 TOTAL CONTRACTS ON OUR TWO EXCHANGES. THE T.A.S. ISSUED ON MONDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 2.749 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST. (30.656 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 16,400 OZ QUEUE JUMP//NEW STANDING ADVANCES TO 31.639 TONNES + .6842 (PRIOR EXCHANGE FOR RISK) //NEW TOTAL 32.323 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $5.45.

WE HAD – REMOVED 297 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 884 CONTRACTS OR 88,400 OZ OR 2.749 TONNES.

Estimated gold volume today:// 141,372 awful

final gold volumes/yesterday 110,161 awful

//AUGUST 8/ FOR THE AUGUST 2023 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 32.151 Brinks 1 kilobar . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 57,488.988 OZ HSBC |

| No of oz served (contracts) today | 2193 notice(s) 219300 OZ 0.0653TONNES |

| No of oz to be served (notices) | 212 contracts 21200 oz 0.6594 TONNES |

| Total monthly oz gold served (contracts) so far this month | 9960 notices 996000 OZ 30.979 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: NIL oz

customer deposits: 0

total customer deposits: nil oz

we had 1 customer withdrawals

i) Out of Brinks 32.151 oz (one kilobar)

Adjustments; 0

/

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 2405 contracts having GAINED 143 contracts. We had 21 contracts filed

on Monday, so we gained 164 contracts or an additional 16,400 oz will stand at the comex

Sept gained 11 contracts to 2677.

Oct gained 84 contracts to 32,943 contracts.

We had 21 contracts filed for today representing 2100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 174 notices were issued from their client or customer account. The total of all issuance by all participants equate to 2193 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and662 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2023. contract month,

we take the total number of notices filed so far for the month (9960 x 100 oz ), to which we add the difference between the open interest for the front month of AUGUST (2405 CONTRACT) minus the number of notices served upon today 2193 x 100 oz per contract equals 1,017,200 OZ OR 31.639 TONNES the number of TONNES standing in this active month of AUGUST. + .684 TONNES EXCHANGE FOR RISK/prior = 32.323 tonnes

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (9960) x 100 oz + (2405) {OI for the front month} minus the number of notices served upon today (2193) x 100 oz) which equals 1,017,200 oz standing OR 30.639 TONNES + .684 TONNES OF EXCHANGE FOR RISK/prior = 32.323 TONNES

TOTAL COMEX GOLD STANDING: 32.323 TONNES WHICH IS SMALL FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,083,941.636 OZ 64.82 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,260,325.005 OZ

TOTAL REGISTERED GOLD: 12,039,935.976 (374,49 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,226,389.029 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,955,994 OZ (REG GOLD- PLEDGED GOLD) 309.67 tonnes//

END

SILVER/COMEX

AUGUST 8

//2023// THE AUGUST 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 525,905.873 oz CNT Brinks Loomis Delaware Manfra . |

| Deposits to the Dealer Inventory | N/A oz |

| Deposits to the Customer Inventory | 600,568.320 oz CNT |

| No of oz served today (contracts) | 44 CONTRACT(S) (220,000 OZ) |

| No of oz to be served (notices) | 1 contract (5,000 oz) |

| Total monthly oz silver served (contracts) | 892 Contracts (4,460,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i) Into CNT: 600,568.320 oz

total customer deposits: 600,568.320 oz

JPMorgan has a total silver weight: 140.471 million oz/281.399 million =49.92% of comex .//

Comex withdrawals 5

i) Out of CNT 126,326.375 oz

ii) Out of Loomis 28,868.340 oz

iii0 Out of Brinks 148,033.230 oz

iv) Out of Delaware 10,913.363 iz

v) Out of Manfra 211,764.564 oz

adjustments: 1 Brinks /dealer to customer:

615,493.04 oz

TOTAL REGISTERED SILVER: 31.066 MILLION OZ//.TOTAL REG + ELIGIBLE. 281.399 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF AUGUST /2023 OI: 45 CONTRACTS HAVING LOST 15 CONTRACT(S). WE HAD

60 NOTICES FILED ON MONDAY SO WE GAINED 45 CONTRACTS OR AN ADDITIONAL 225,000 OZ WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF AUGUST.

SEPT HAS A LOSS OF 2396 CONTRACTS DOWN TO 92,515

OCT GAINED 20 CONTRACTS TO STAND AT 108.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 44 for 220,000 oz

Comex volumes// est. volume today 87,473 strong/t.a.s.induced /

Comex volume: confirmed yesterday: 80,273 strong/t.a.s induced

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 892 x 5,000 oz = 4,460,000 oz

to which we add the difference between the open interest for the front month of AUGUST (45) and the number of notices served upon today 44 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST/2023 contract month: 892 (notices served so far) x 5000 oz + OI for the front month of AUGUST (45) – number of notices served upon today (44 )x 500 oz of silver standing for the AUGUST contract month equates to 4.465 million oz.+ 0.0 MILLION OZ EXCHANGE FOR RISK ISSUED TODAY+ 1.45 MILLION OZ EXCHANGE FOR RISK PRIOR//NEW TOTALS: 5.915 MILLION oz.

There are 31.066 million oz of registered silver.

Thus if we take today’s standing at 5.915 and add last month’s 30.9 million oz we have 36.815 million oz against only 31.066 million registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

AUGUST 8/WITH GOLD DOWN $9.60 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 906.00 TONNES

AUGUST 7/WITH GOLD DOWN $5.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 906.00 TONNES

AUGUST 4/WITH GOLD UP $7.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.18 TONNES OF GOLD FROM THE GLD/// .///INVENTORY RESTS AT 906.00 TONNES

AUGUST 3/WITH GOLD DOWN $5.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 2/WITH GOLD DOWN $3.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.75 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 1/WITH GOLD DOWN $28.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 31/WITH GOLD UP $9.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 28/WITH GOLD UP $14.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 915,82 TONNES

JULY 27/WITH GOLD DOWN $21.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 917.26 TONNES

JULY 26/WITH GOLD UP $6.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 25/WITH GOLD UP $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 24/WITH GOLD DOWN $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.20 TONNES OF GOLD INTO THE GLD//: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 21/WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / .////INVENTORY RESTS AT 913.80 TONNES

JULY 20/WITH GOLD DOWN $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 913.80 TONNES

JULY 19/WITH GOLD UP $0.65 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 912.07 TONNES

JULY 18/WITH GOLD UP $23.45 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: .////INVENTORY RESTS AT 912.93 TONNES

JULY 17/WITH GOLD DOWN $6.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD.////INVENTORY RESTS AT 912.93 TONNES

JULY 14/WITH GOLD UP $0.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 914.66 TONNES

JULY 13/WITH GOLD UP $3.30 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.29 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.66 TONNES

JULY 12/WITH GOLD UP $24.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.95 TONNES

JULY 11/WITH GOLD UP $6.15 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.0 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 915.26 TONNES

JULY 10 WITH GOLD DOWN $1.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.60 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 916.26 TONNES.

JULY 7 WITH GOLD UP $16.80 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.86 TONNES.

JULY 6/WITH GOLD DOWN $9.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 917.86 TONNES

JULY 5/WITH GOLD DOWN $2.20 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 2.6 TONNES FROM THE GLD///INVENTORY RESTS AT 921.90 TONNES

JULY 3/WITH GOLD UP $1.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 924.50 TONNES//

JUNE 30/WITH GOLD UP $10.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 924.50 TONNES

JUNE 29/WITH GOLD DOWN $3.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.81 TONNES

GLD INVENTORY: 906.00 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 8/WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 7/WITH SILVER DOWN 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 4/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.294 MILLION OZ FROM THE SLV// OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 3/WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 189,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.281 MILLION OZ

AUGUST 2/WITH SILVER DOWN 43 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 275,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.471 MILLION OZ

AUGUST 1/WITH SILVER DOWN 61 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 31/WITH SILVER UP 45 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 28/WITH SILVER UP 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.930 MILLION OZ

JULY 27/WITH SILVER DOWN 59 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ

JULY 26/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 25/WITH SILVER UP 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 826,000 OZ FROM THE SLV..////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 24/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 21/WITH SILVER DOWN 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.101 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 20/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.468 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 454.107 MILLION OZ/

JULY 19/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 18/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 17/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 4.856 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 14/WITH SILVER UP 27 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.21 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 13/WITH SILVER UP 64 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 12/WITH SILVER UP $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.881 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 11/WITH SILVER DOWN 5 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .020 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 464.822 MILLION OZ/

JULY 10/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.672 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 464.802 MILLION OZ

JULY 7/WITH SILVER UP 42 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.474 MILLION OZ

JULY 6/WITH SILVER DOWN 50 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.667 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 466.474 MILLION OZ//

JULY5/WITH SILVER UP 30 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JULY 3/WITH SILVER UP 7 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

CLOSING INVENTORY 448.987 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

The Real Threat Is A Market-Driven Dollar-Downgrade

TUESDAY, AUG 08, 2023 – 05:00 AM

Last week, Fitch Ratings downgraded the US’s long-term credit rating from AAA to AA+. While the downgrade won’t significantly impact the US government’s ability to borrow, it should serve as a wake-up call because there is a much bigger problem looming on the horizon: a market-driven downgrade of the US dollar.

The bond market got pummeled last week with four losing days before a rally on Friday driven by a weaker-than-expected jobs report. That rally wasn’t enough to recover all the losses, and yields finished the week above 4% across the board.

We also saw a reversion in the 5-year and 30-year yields, with the 30-year closing above the 5-year for the first time in quite a while. The 5-year and 10-year yields remain inverted, still flashing recession.

The upward movement of yields on the long end of the curve could indicate that bond traders are starting to reckon with reality, but there is still a long way to go. Generally, investors still seem to think that the Fed will be able to push price inflation back to the low levels we saw during the decade preceding the pandemic. They haven’t figured out that this easing price inflation is transitory. So, the bond market remains priced for a fantasy, although it appeared the smoke might be clearing as yields move up.

Supply and demand dynamics are also driving yields higher. In just two months since Congress reached a deal and suspended the debt ceiling for two years, the national debt has surged by a staggering $1.2 trillion. And the borrowing isn’t going to slow down anytime soon. Last week, the Treasury Department upped its projection for third-quarter debt issuance to $1.01 trillion. That’s up from the $733 billion Q3 projection it imagined in May.

Rising interest rates make a “soft landing” (tackling inflation without a recession) less likely because they are problematic for everybody. Along with the US government, corporations and consumers are buried under debt. As rates rise, it becomes more and more difficult to service that debt or to continue propping up the bubble economy with additional borrowing.

Oil prices also continued their upward climb last week. Oil is up about 30% in this most recent run. The fact that the oil chart looks bullish and the bond chart looks bearish makes sense if the underlying problem in the economy is inflation.

The Fitch Downgrade and the Bigger Problem

With the current debt ceiling fight resolved, Fitch removed the US’s Issuer Default Rating from “watch negative” to “a stable outlook.” But the end of the debt ceiling standoff wasn’t enough to alleviate fears about America’s debt trajectory.

“The repeated debt-limit political standoffs and last-minute resolutions have eroded confidence in fiscal management.”

Nevertheless, the markets generally brushed off the Fitch downgrade. And in the big scheme of things, it is irrelevant.

It doesn’t even make sense to apply a credit rating on the US government. The point of a rating is to indicate the likelihood of default. Nobody is really worried about the US government defaulting because the Federal Reserve can always create more money.

But that doesn’t mean there is no risk in buying US Treasuries. And that risk applies to any bond you buy with US dollars. It doesn’t matter how credit-worthy the issuer of the bond happens to be. In fact, the same risk applies if you take your dollars and stuff them under the mattress.

That risk is inflation.

Every day, your dollar is losing its purchasing power.

Dollar depreciation is like a default. If a government has to resort to a printing press to pay off its bills, you still get your money back when a government bond matures, but you lose purchasing power. The dollars you get back won’t buy as much stuff.

So, an honest rating of US government debt would be junk status — not because of the default risk but because of the high likelihood that it will continue to inflate away the dollar’s value.

In fact, we’re insulting to junk status. You are guaranteed to lose with a long-term US Treasury. There is no chance that you will buy a 30-year Treasury with a yield of just over 4% today and break even at the end of that term. Sure, you’ll get all of your dollars back (most likely), but those dollars won’t have anywhere near the value that they had when you loaned them out.

That raises a key question: if you’re guaranteed to lose with a bond, what should the rating be?

At some point, people need to realize that the fact the US government will have to print money in order to pay its debts is a reason not to buy Treasuries. Keep in mind, Treasuries are just future payments of US dollars. So, you should really be looking at the rating of the currency and consider what the dollar will be worth in 30 years. Will that 4% interest cover what you lose through inflation over that period of time and give you some kind of positive return?

The bottom line is the rating is meaningless. All US government debt is junk. People need to get out of all dollar-denominated debt as quickly as they can.

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

3,Chris Powell of GATA provides to us very important physical commentaries

China officially adds 740,000 oz (2.302) tonnes. However it purchases a lot more than that and puts the yellow stuff in their investment banks

(Bloomberg)

China’s central bank adds gold for ninth straight month

Submitted by admin on Mon, 2023-08-07 09:57Section: Daily Dispatches

Or announces an addition anyway. No official gold data is very complete or reliable.

* * *

By Sybilla Gross

Bloomberg News

via Yahoo News, Sunnyvale, California

Monday, August 7, 2023

China raised its gold reserves for a ninth straight month in July as central bank purchases continue to underpin prices of the precious metal.

Bullion held by the People’s Bank of China rose by 740,000 troy ounces, the central bank said today. That’s equivalent to about 23 tons. Total stockpiles now sit at 2,137 tons, with around 188 tons added in a run of purchases that began in November.

China has led central bank buying in recent months as it continues to diversify its reserves. That has helped keep prices buoyant despite rising interest rates around the world, which typically sap demand for non-interest bearing bullion. …

… For the remainder of the report:

https://finance.yahoo.com/news/china-central-bank-adds-more-081837343.html

end

Demand for gold is still red hot in Turkey because of their declining Lira. Now they plan to restrict gold import quotas toprotect its FX balances

(Reuters)

Turkey said to plan gold import quota to protect FX balance

Submitted by admin on Mon, 2023-08-07 10:05Section: Daily Dispatches

From Reuters

Monday, August 7, 2023

ANKARA — Turkey plans to impose a quota on imports of unprocessed gold in order to reduce the negative impact on the current account balance, according to a source familiar with the matter and state-owned Anadolu Agency.

Anadolu reported today that the Treasury had decided to introduce the quota in a bid to both relieve the deficit and boost foreign exchange reserves.

It said legislative work on the measure would be completed soon by the Treasury and the Trade Ministry and that the quotas will apply to unprocessed gold imports carried out by precious metals brokers who are members of Borsa Istanbul.

Imports of unprocessed gold in the first seven months of the year increased by 180% from the same period a year earlier to $19.4 billion, Trade Ministry data shows.

After February’s devastating earthquakes, restrictions were imposed on gold imports. But domestic demand for gold nonetheless became stronger, with negative returns on the lira being the main factor boosting demand. …

… For the remainder of the report:

END

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES/SILVER

5 a. IMPORTANT COMMENTARIES ON COMMODITIES: Lithium batteries

Lithium Batteries//GREEN NEW DEAL

Robert H

Re: Lithium battereis, billions of our tax dollars pumped into it, another huge gov’t scam.

>

> FOOD FOR THOUGHT

>

>

>

> A machine like this is required to move 500 tons of earth/ ore which

> will be refined into one lithium car battery. It burns 900-1000

> gallons of fuel in a 12 hour shift.

>

> Lithium is refined from ore using sulfuric acid. The proposed lithium

> mine at Thacker Pass, Nevada is estimated to require up to 75

> semi-loads of sulfuric acid a day! The acid does not turn into unicorn

> food as AOC believes.

>

> Refining lithium has created several EPA SUPERFUND SITES. IT IS VERY

> TOXIC TO THE ENVIRONMENT!

>

> A battery in an electric car, let’s say an average Tesla, is made of :

>

> 25 pounds of lithium,

>

> 60 pounds of nickel,

>

> 44 pounds of manganese,

>

> 30 pounds of cobalt,

>

> 200 pounds of copper,

>

> And 400 pounds of aluminum, steel, and plastic, etc……averaging

> 750-1,000 pounds of minerals, that had to be mined and processed into

> a battery that merely stores electricity… Electricity which is

> generated by oil, gas, coal, or water ( and a tiny fraction of wind

> and solar )…

>

> That is the truth, about the lie, of “green” energy.

>

> There’s nothing green about the “Green New Deal”.

>

> people better learn how to vote or this nonsense will continue to

> flow down on top of you from the throne of government upon of which

> you put these people.

>

> Stop drinking the Green New Deal’s sulfuric acid Kool-Aid!

>

> “Woke — a Synonym for Stupid”

>

> Dr. Phillip A. Fields

>

> Scientist / Researcher

>

> SE Labs

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS MONDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2175

OFFSHORE YUAN: DOWN TO 7.2447

SHANGHAI CLOSED DOWN 8.21 PTS OR 0.25%

HANG SENG CLOSED DOWN 353,75 PTS OR 1.81%

2. Nikkei closed UP 122.73 PTS OR 0.38%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 102.48 EURO FALLS TO 1.0942 DOWN 62 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.591 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 142.97/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ON SHORE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.4225***/Italian 10 Yr bond yield FALLS to 4.120*** /SPAIN 10 YR BOND YIELD FALLS TO 3.486…**

3i Greek 10 year bond yield FALLS TO 3.740

3j Gold at $1929.00 silver at: 22.96 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 10 /100 roubles/dollar; ROUBLE AT 96.38//

3m oil into the 80 dollar handle for WTI and 83 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 142.97// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.591% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8774 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9600 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.995 DOWN 8 BASIS PTS…

USA 30 YR BOND YIELD: 4.160 DOWN 10 BASIS PTS/

USA 2 YR BOND YIELD: 4.730 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 27.02…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 10 BASIS PTS AT 4.3935

end

2.a Overnight: Newsquawk and Zero hedge:

Futures And Yields Slide, Global Markets Tumble As Mood Sours After Trifecta Of Dismal News

BY TYLER DURDEN

TUESDAY, AUG 08, 2023 – 08:40 AM

Global stocks slid, US equity futures slumped and bond yields tumbled as a raft of news on collapsing Chinese trade, Italian banks hit with an unexpected windfall tax, and a downgrade of US banks by Moodys (on increasing funding costs/CRE exposure) sparked a fresh round of fears about the financial system and global economy. At 7:45am, S&P futures were down 0.7% trading as low as 4,502 while Nasdaq futures dropped 0.8% amid a broad flight to safety across markets which sent yields on the 10-year Treasury 10 basis points lower and the equivalent rates in Germany fell 15 basis points. The Bloomberg dollar index climbed 0.5% while oil resumed its slide following ugly oil import data by China. Today’s macro data includes Small Biz Optimism, Trade Balance, and Wholesales Sales/Inventories … nothing market-moving as we await Thursday’s CPI print.

In the premarket, tech and small-caps underperformed while defensives were the green. Investors are also closely watching US financials after Moody’s lowered credit ratings for 10 small and midsized lenders and warned about the risks tied to commercial real estate: the XLF was indicated -67bps and KRE -1.3% lower in premarket trading. Eli Lilly extended gains to 8.6%, after the drugmaker boosted its revenue guidance for the full year; the guidance beat the average analyst estimate. Earlier, Lilly shares jumped following Novo Nordisk’s Wegovy update. Here are some other notable premarket movers:

- Hims & Hers Health shares surge 17% after the telehealth company boosted its full- year adjusted Ebitda outlook. Overall, analysts said the print was better than expected, with Citi highlighting the better average order value being a key driver for the beat.

- Home Depot and Lowe’s are downgraded to market perform from outperform at Telsey Advisory Group. Home Depot falls 1.3%, while Lowe’s slides 1.4%.

- Lucid gains as much as 4.5% on Tuesday after the EV startup said it still believes it will produce at least 10,000 vehicles this year.

- Maravai LifeSciences shares slide 15% after the biotech firm cut its full-year outlook for adjusted earnings per share, adjusted Ebitda and total revenue.

- Olaplex tumbles as much as 27%, after cutting its full-year projections for net sales, adjusted Ebitda and adjusted net income.

- Palantir Technologies shares edge higher 2.6% after the data-analysis software company reported second-quarter results and raised its full-year adjusted operating profit forecast.

- Paramount Global rises as much as 4.4% after the media company reported revenue for the second quarter that beat the average analyst estimate, driven by a jump in its streaming-TV business.

- Proterra Inc. which makes heavy-duty electric vehicle components like chargers and batteries, filed for bankruptcy on Monday. Shares fall 66%.

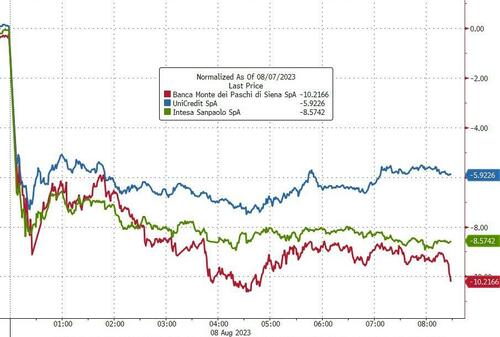

In Europe, the Stoxx 600 dropped 0.7% with banks posting the steepest losses after Italy announced an unexpected tax on windfall profits, sending shares of UniCredit SpA and Intesa Sanpaolo SpA down more than 7%. The euro-area banks index slumped as much as 3.4%. BPER Banca, Banco BPM, Intesa Sanpaolo and UniCredit all fell at least 7%. In the UK, banks also fall as BNP Paribas Exane says that while lenders in Britain are cheap, it is staying relatively cautious, downgrading Barclays to neutral and Virgin Money UK to underperform. Here are the most notable European movers:

- Novo Nordisk jumps as much as 16%, the most since 2002, after results from the SELECT cardiovascular outcomes trial for Wegovy, where the obesity drug achieved its primary objective.

- Glencore shares drop as much as 4.4% after the miner reported a 50% drop in first-half adjusted Ebitda. Analysts said profits were weaker than expected amid a drop in commodity prices

- Abrdn falls as much as 9.6% after the investment company posted 1H operating profit and net outflows that missed expectations. RBC says the results signal a further delay of return to growth

- InterContinental Hotels shares rise as much as 2.2% after the hotel operator reported estimate- beating results and said there’s no sign of cooling in leisure demand

- Fraport rises as much as 8.6% after the German airport operator produced second-quarter earnings that beat analysts’ estimates and showed a continued recovery toward pre-pandemic levels

- Norma shares advance as much as 9.4%, the most in more than six months, after the tech hardware firm provided guidance that Baader Helvea says looks “reasonable”

- TI Fluid shares rose as much as 22%, the most intra-day on record, after the UK car- fluid-storage manufacturer delivered what the analysts saw as a strong trading update with a significant EBIT beat

Earlier in the session, Asian stocks slumped as the early optimism following the positive lead from Wall St was soured as Chinese markets entered the fray, while the region also digested disappointing Chinese trade data.

- Hang Seng and Shanghai Comp spooked markets with the Hong Kong benchmark heavily pressured as tech and property stocks lead the broad declines across sectors, while sentiment was also not helped by the wider-than-expected contraction in Chinese exports and imports data.

- ASX 200 traded rangebound after mixed consumer sentiment and business confidence surveys.

- Nikkei 225 was initially lifted by a weaker currency and earnings release but then wiped out nearly all of its gains as markets were spooked by selling in Chinese stocks.

Investor sentiment took a big hit after China released more data that showed its economic engine is sputtering. Exports plunged by the most since early 2020, the beginning of the Covid pandemic, and imports contracted last month. The Hang Seng China Enterprises Index and a gauge of European mining shares fell about 2%. Commodities prices retreated, with oil and copper losing almost 2%. Sentiment was further dented after two missed coupon payments by Country Garden.

As Bloomberg notes, China’s disappointing economic recovery is being felt acutely among exporting nations in the developing world. The MSCI Emerging Market Index of stocks headed for the lowest close in almost four weeks and looked to breach the support level at its 50-day moving average. Its currency-index counterpart also traded at the weakest level since July 10, with the South Korean won and Malaysian ringgit among the worst performers.

“Reduced demand for raw materials and commodities due to its economic slowdown is likely to lead to a decrease in global commodity prices,” according to Nigel Green, CEO of DeVere Group. “Those countries heavily reliant on commodity exports would then experience economic hardships as their revenues decline.”

In FX, the Bloomberg Dollar Spot Index rises 0.4% with the world’s reserve currency advancing against all of its of Group-of-10 peers. The yen slid the most against the US currency after falling as much as 0.7%. The People’s Bank of China set Tuesday’s yuan reference rate at 7.1565 per dollar, revising an earlier fixing in the morning when it had indicated a stronger fixing of 7.1365. The latest fixing was set at the weakest level in nearly a month. “A clearly visible CNY depreciation trend might further strengthen the tendency of private domestic capital to leave China,” said Ulrich Leuchtmann, head of currency strategy at Commerzbank AG in Frankfurt. “The Chinese authorities have to be very certain that their capital controls work well if they want to risk that.”

In rates, treasuries hoeld gains into early US session with yields lower by up to 10bp across long-end of the curve. Treasury yields are down 3bp to 10bp across the curve with 2s10s, 5s30s spreads flatter by 5.5bp and 2.5bp on the day; 10- year yields just under 4% are richer by 10bp on the day with bunds and gilts outperforming by 4.5bp and 1bp in the sector. Treasuries drew support during Asia session following disappointing China trade data. Today’s bull-flattening move is led by bunds, drawing flight-to-quality flows with Italian banks slumping after the government introduced a surprise tax on “extra profits” this year. US regional banks are also in focus after Moody’s Investors Service lowered credit ratings for 10 small and midsize lenders based on mounting funding costs. Treasury auction cycle begins with 3-year note sale at 1pm New York time. The treasury auction cycle includes $42b 3-year note followed by $38b 10-year Wednesday and $23b 30-year bond Thursday in upsized auction amounts. WI 3-year yield around 4.38% is ~15bp richer than last month’s, which stopped 0.2bp through the WI yield.

In commodities, crude futures declined with WTI falling 2% to trade near $80. Spot gold drops 1%

Looking to the day ahead, on the data side in the US we will get the July NFIB small business optimism, June wholesale trade sales and June trade balance releases. Over in Europe, we have the final Germany inflation print for July as well as the releases of the ECB’s latest consumer expectations survey. Our economists’ dbDIG survey suggests that the ECB survey should show a further slight easing of inflation expectations – see their earlier note here. Among central bank speakers, we will hear from the Fed’s Harker and Barkin. Finally, earning releases include Eli Lilly, UPS, Glencore, Bayer, Coupang, Barrick Gold, Take-Two Interactive, Rivian and Lyft.

Market Snapshot

- S&P 500 futures down 0.3% to 4,522.00

- MXAP down 0.8% to 165.03

- MXAPJ down 1.1% to 520.05

- Nikkei up 0.4% to 32,377.29

- Topix up 0.3% to 2,291.73

- Hang Seng Index down 1.8% to 19,184.17

- Shanghai Composite down 0.3% to 3,260.62

- Sensex down 0.1% to 65,876.04

- Australia S&P/ASX 200 little changed at 7,311.14

- Kospi down 0.3% to 2,573.98

- STOXX Europe 600 down 0.4% to 457.83

- German 10Y yield little changed at 2.49%

- Euro down 0.2% to $1.0979

- Brent Futures down 1.2% to $84.28/bbl

- Gold spot down 0.2% to $1,932.35

- U.S. Dollar Index up 0.31% to 102.37

Top Overnight News

- China’s trade plunged in July as slowing global demand clouded the outlook for exports, while domestic pressures weighed on imports in a hit to the economic recovery. Overseas shipments dropped 14.5% in dollar terms last month from a year earlier — the worst decline since February 2020 — while imports contracted 12.4%, the customs administration said Tuesday. That left a trade surplus of $80.6 billion for the month. BBG

- Country Garden (2007.HK) said it has not paid two dollar bond coupons due on Aug. 6 totaling $22.5 million, confirming market fears that the biggest privately owned developer in China is slipping into repayment troubles. The bonds in question are notes due in Feb 2026 and Aug 2030 , the firm told Reuters. Both payments have 30-day grace periods, according to investors citing prospectuses. RTRS

- Chinese firms forced to cut prices amid tepid demand, raising the risk of a Japan-like slide into sustained deflation. BBG

- Eurozone inflation expectations sink further according to the latest ECB survey (“median expectations for inflation over the next 12 months decreased further to 3.4%, from 3.9% in May, and those for inflation three years ahead also declined, easing to 2.3% from 2.5% in May”) (ECB)

- Italy’s right-wing government shocked markets with an unexpected tax on banks’ windfall profits, wiping out around $10 billion from the market value of the country’s lenders. Deputy Prime Minister Matteo Salvini announced a 40% levy on the extra profits of lenders for 2023 late Monday night, as part of a wide-ranging decree approved at a cabinet meeting. BBG

- Apartment buildings, long considered a real-estate haven, are emerging as the next major trouble spot in the beleaguered commercial-property world. Investors bid up the prices of multifamily buildings for years, attracted by steadily rising rents and the prospect of outsize returns. Many took on too much debt, expecting they could raise rents fast enough to pay it down. WSJ

- Moody’s cut its rating on 10 small and midsize banks including MTB, WBS, BOKF, ONB, PNFP, FULT, ASB, and PB. and adopted a negative outlook for 11 lenders including PNC, COF, CFG, FITB, RF, ALLY, OZK, and HBAN. In addition, the agency said that it may downgrade major lenders including USB, BK, STT, TFC, and NTRS. The action came as part of a review driven by the challenges facing the industry including higher funding costs, potential regulatory capital weaknesses, and rising risks tied to commercial real estate loans amid weakening demand for office space “which have collectively lowered the credit profile of a number of US banks, though not all equally”. BBG

- Some of the biggest names in commercial real-estate lending have all but turned off the spigot. Blackstone Mortgage Trust and KKR Real Estate Finance Trust, two of the biggest mortgage real-estate investment trusts, have halted loans to any new borrowers. WSJ

- UPS (-7% pre mkt) reported small EPS upside at 2.54 (vs. the Street’s 2.50 forecast) as very healthy operating margins (13.2% vs. the Street’s 12.4% forecast) helped to offset a revenue shortfall (-10.9% to $22.055B vs. the Street’s $22.99B forecast). However, the company is cutting its guidance, with revenue getting hit by the macro environment (they now see $93B vs. the prior $97B) and op. margins pressured by the new Teamsters deal. RTRS

- Booming oil prices last year powered U.S. inflation to 40-year highs. That trend was reversing in 2023—until now. Benchmark crude prices are up 21% over the past six weeks, driving up the cost of American workers’ commutes and freight haulers’ trips.

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks traded mixed after the early optimism following the positive lead from Wall St was soured as Chinese markets entered the fray, while the region also digested disappointing Chinese trade data. ASX 200 traded rangebound after mixed consumer sentiment and business confidence surveys. Nikkei 225 was initially lifted by a weaker currency and earnings release but then wiped out nearly all of its gains as markets were spooked by selling in Chinese stocks. Hang Seng and Shanghai Comp spooked markets as they entered the fray with the Hong Kong benchmark heavily pressured as tech and property stocks lead the broad declines across sectors, while sentiment was also not helped by the wider-than-expected contraction in Chinese exports and imports data.

Top Asian News

- China’s Ambassador to the Philippines said the Philippines took unilateral actions to undermine the existing management status quo on Second Thomas Shoal and China had no choice but to make necessary responses. Furthermore, China hopes the Philippines meets China halfway and said third-party forces will not help the situation, while China is waiting for feedback from the Philippine side and hopes to start talks ASAP, according to Reuters.

- Major Chinese property developer Country Garden Holdings (2007 HK) said it has not paid two USD bond coupons due Aug 6th worth some USD 22.5mln, according to Reuters.

European bourses are lower across the board, Euro Stoxx 50 -1.20%, risk tone hit by Chinese trade and reports around a property developer. Within Europe, the FTSE MIB -2.2% lags following Italy approving a 40% windfall tax on banks, pressuring the broader banking index, -2.7%. Elsewhere, sectors are more mixed; Banking lags as mentioned while Basic Resources are dented by the trade data and a poorly-received update from Glencore. Stateside, futures are in the red, ES -0.5% and feature continued modest underperformance in the RTY -0.8%. Elsewhere, the risk tone around banks was soured further by Moody’s downgrading several US banks.

Top European News

- BoE’s Pill said inflation remains much too high and they have seen a lot of news on inflation persistence. Pill added that there are risks on both sides on UK inflation and risks that the UK hasn’t raised rates enough but also noted that a lot of rate hikes have yet to hit the economy.

- Barclaycard UK July consumer spending rose 4.0% Y/Y vs. prev. 5.4% growth in June, while it noted that supermarket spending growth slowed sharply, according to Reuters.

- Italy’s Deputy PM said the Cabinet approved a 40% windfall tax on banks, limited to 2023. Subsequently, it was reported that Italy expects to collect last than EUR 3bln from windfall tax on banks, according to Reuters citing sources. Note, Italian banks have been under marked pressure in European trade, SX7E -2.7%

- ECB Consumer Inflation Expectations survey (Jun) – 12-months ahead 3.4% (prev. 3.9%); 3-year ahead 2.3% (prev. 2.5%)

FX

- A firm session thus far for the DXY, to a 102.47 peak irrespective of downside in yields in what is seemingly a flight to safety against the backdrop of the soured risk sentiment.

- Antipodeans are the marked laggards in early European hours amid the aforementioned downbeat risk tone and concerning Chinese trade data, whilst Australia also saw a decline in consumer confidence and sentiment data overnight.

- Traditional havens are softer on the back of the firmer Dollar, but losses are cushioned by the haven statuses, whilst a decline in US yields could also be providing some padding against the Buck.

- EUR and GBP are subdued given the USD’s upside, single currency saw little reaction to the latest consumer expectation survey while drivers for GBP have been limited and action largely USD-driven.

- The NOK is among the G10 laggards given its sensitivity to risk.

- PBoC set USD/CNY mid-point at 7.1565 vs exp. 7.1869 (prev. 7.1380)

Fixed Income

- Core benchmarks are firmer across the board given the deterioration in broader risk sentiment that took hold during APAC trade.

- Bund lifted to a 133.17 peak following a particularly strong Bobl auction, surpassing the July 31st/August 1st virtual double-top at 133.05/06. A move which brings into play 133.34 and thereafter 133.92, from the 28th and 27th of July respectively.

- A slight widening of the BTP-Bund yield spread to just above the 170bp mark, incrementally higher than the last few weeks but shy of the mid-July wides at circa. 175bp.

- Gilts are similarly bid with their own specifics light and action seemingly a function of the broader risk tone and aforementioned factors.

- Stateside, the picture is much the same as EGBs and Gilts with Treasuries posting gains of circa. 15 ticks in relative proximity to the high point of 110.31 to 111.18+ parameters, ahead of Fed speak and 3yr supply.

Commodities

- WTI and Brent futures are on the backfoot as a function of a firmer Dollar, broader risk aversion, and headwinds from downbeat Chinese trade data.

- Spot gold is subdued by the Buck and trades under its 50 DMA (USD 1,944.27/oz) around the USD 1,932/oz mark in a relatively tight USD 1,938-30/oz intraday range; yellow metal hit by the USD, but somewhat cushioned by the overall tone given its haven allure.

- Base metals have continued to dip following the commencement of the European session, initial pressure from APAC factors was further fanned by the release from Glencore. Though, internal commentary noted of a more positive macro backdrop in H2 and above-average real-term prices ahead.

- UBS retains a positive outlook for oil prices and forecasts Brent at USD 90/bbl by end-2023; Oil demand is set to breach 103mln BPD in August for the first time, due to China, India and the Middle East. See a market deficit of circa. 2mln BPD in July and August, vs around 0.7mln BPD in June.

- Turkey imposed a 20% extra fee for some gold imports, according to the Official Gazette.

Geopolitics

- Japan ruling LDP’s Aso said in Taipei that ‘we’ are moving from peacetime to times of turbulence and believe that issues that were hidden beneath the surface are coming to the fore, while he added that Taiwan is an important partner and friend. Furthermore, Aso said Japan has continued to say that peace in the Taiwan Strait is important for regional stability and the most important thing is to make sure war doesn’t break out in the Taiwan Strait.

- Polish Defence Ministry to send additional troops to Belarus border following request from border guard, according to PAP.

- Economic Community of West African States (ECOWAS) plans to mobilise 25,000 troops for possible intervention in Niger, according to Al Arabiya citing French Press.

US Event Calendar

- 06:00: July SMALL BUSINESS OPTIMISM, est. 91.3, prior 91.0

- 08:30: June Trade Balance, est. -$65b, prior -$69b

- 10:00: June Wholesale Trade Sales MoM, est. -0.2%, prior -0.2%

- 10:00: June Wholesale Inventories MoM, est. -0.3%, prior -0.3%

DB’s Jim Reid concludes the overnight wrap

As we approach the dog days of summer, and my holiday in a few days, it sometimes gets harder to explain moves in markets in both direction but as I’ve been doing this daily for nearly 17 years I’ve learnt to try to come up with rationales or I’ll have a blank piece of paper. We’ve had some big moves in rates in the last week following the US Treasury announcement last Monday, the Fitch US downgrade, the Treasury refunding announcement and then the reverse move after payrolls. All others things being equal I thought the extent of the rates rally after payrolls was strange given how 2-way the release was, and yesterday a 10bps intra-day rally in 2yrs from an earlier sell-off was also difficult to explain. All in all, 2yr US yields were flat (-0.1bp) at the close, with 10yr and 30yr yields up +5.6bps and +6.9bps. The S&P 500 (+0.90%) did rise after four days of losses though. Overnight, US 10yrs and 30yr yields are back -4bps and -5bps lower as I type so we are seeing some decent sized moves in these thin markets at the moment.

We did hear contrasting comments from FOMC members yesterday on the potential for further hikes. Federal Reserve Governor Bowman, who typically leans hawkish, emphasised the potential for further hikes, saying she expects that “additional increases will likely be needed to lower inflation to the FOMC’s goal”. By contrast, in an interview published by the New York Times, New York Fed President Williams said that “monetary policy is in a good place” and “whether we need to adjust it in terms of that peak rate — but also how long we need to keep a restrictive stance — is going to depend on the data”. To be fair, Bowman also stressed data dependence but she focused more on still high inflation and tight labour market. Williams did dangle a rate cutting carrot for 2024 if inflation continued to behave.

An ongoing theme in US rates has been that the sizable US yield moves have continued with only minor changes in near-term Fed pricing though. Rate pricing for end-23 rose by 1.5bps on Monday to 5.38%, while end-24 pricing retreated -2.0bps to 4.00%. So that is five and a half 25bp cuts priced for 2024. On the topic of 2024 rate cuts, yesterday our US economists published a report in which they consider what policy rules would imply for the timing and pace of rate cuts in 2024 under different economic scenarios. See their note here.

Meanwhile, short-end yields in Europe rallied on Monday following news late on Friday that the Bundesbank will from October stop paying interest on domestic government deposits. Back in September 2022, the ECB had lifted the zero ceiling on such deposits to rise in line with policy rates amid fears of a negative impact on the repo market, before reducing this ceiling to ESTR minus 20bp in the spring. A decline in government deposits at the central bank and reduced collateral scarcity may have made the Bundesbank less concerned about the risks, though it is rather unusual for it to take this step unilaterally (without other euro area national central banks). Together with the recent ECB move to pay zero interest on banks’ minimum reserves, central banks might be looking for ways to reduce their high interest costs, at least if this can be done without hindering policy effectiveness.

The yield on 6m German bills thus fell by -4.7bps on Monday, while the 2yr yield declined by -2.7bps. The German curve notably twisted and steepened as 10yr Bund yields were +3.9bps higher. An additional notable feature in European rates has been the ongoing gradual rise in long-term inflation breakevens. The 5y5y rose for the seventh session in a row yesterday to 2.67%, its highest level since 2009. So the market is not giving a strong vote of confidence in the 2% inflation target. This is similar to the US where a similar measure is up over 10bps in the past week and at levels less than a handful of basis points from 10yr highs. Elsewhere, 10yr UK yields were the biggest underperformer yesterday and +8.1bps higher, largely reversing their Friday decline.

A risk-on mode returned to equity markets on Monday, with the S&P 500 rising +0.90%, ending a run of four declines in a row. A broad rally was led by communication services (+1.88%) and financials (+1.36%). Energy stocks underperformed (+0.15%) as oil prices retreated from their 3-month high reached on Friday (Brent -1.04% to $85.34/bl). Tech stocks were a slight underperformer, although the NASDAQ still posted a solid +0.61% gain. Within the megacaps, Apple (-1.73%) and Amazon (+1.90%) saw continued contrasting moves. Meanwhile, Berkshire Hathaway gained +3.60% after its results, further cementing its position as the largest US company by market cap outside the tech mega caps. Over in Europe, equities were near flat on the day. The STOXX 600 eked out a +0.09% rise, after being weighed down initially by the weak US session last Friday.

Asian equity markets are mixed this morning despite a strong handover from Wall Street overnight. Across the region, the Hang Seng (-1.15%) is leading losses with the KOSPI (-0.12%), the CSI (-0.02%) and the Shanghai Composite (-0.04%) inching lower. Otherwise, the Nikkei (+0.32%) is bucking the regional trend. S&P 500 (-0.22%) and NASDAQ 100 (-0.34%) futures are moving a bit lower.

Early morning data from China showed that exports dropped for the third consecutive month, sliding -14.5% y/y in July (v/s -13.2% expected; -12.4% in June) and recording its biggest drop since July 2020, highlighting that the world’s second biggest economy is being dragged lower by weakness in global demand and a domestic slowdown. At the same time, imports contracted -12.4% y/y in July (-5.6% expected) compared to a -6.8% drop in the previous month. Elsewhere, household spending in Japan fell -4.2% y/y in June (v/s -3.8% expected), a steeper fall than the prior month’s -4.0% drop while recording a fourth straight month of decline. Meanwhile, real wages declined for a 15th straight month, easing -1.6% y/y in June (v/s -0.9% expected) and against May’s downwardly revised drop of -0.9%. Nominal pay growth in June (+2.3% y/y) came in lower than a revised +2.9% rise in May (v/s +3.0% expected).

It was fairly quite day on the data front yesterday. A highlight was Germany’s industrial production print, which saw a larger-than-expected -1.5% mom decline in June (-0.5% exp). Also in Europe, French private sector labour market data showed a slowing in Q2. Employment grew 0.1% qoq, the slowest pace since Q4 2020, while wage growth was +1.0% qoq, down from +1.9% in Q1. So some evidence to argue against the risks of a wage-price spiral emerging in the euro area.

Looking to the day ahead, on the data side in the US we will get the July NFIB small business optimism, June wholesale trade sales and June trade balance releases. Over in Europe, we have the final Germany inflation print for July as well as the releases of the ECB’s latest consumer expectations survey. Our economists’ dbDIG survey suggests that the ECB survey should show a further slight easing of inflation expectations – see their earlier note here. Among central bank speakers, we will hear from the Fed’s Harker and Barkin. Finally, earning releases include Eli Lilly, UPS, Glencore, Bayer, Coupang, Barrick Gold, Take-Two Interactive, Rivian and Lyft.

2 b) NOW NEWSQUAWK (EUROPE/REPORT)/ASIA REPORT

EUROPE

Risk off sentiment after weak Chinese trade, Bunds bid; Fed speak & US supply due – Newsquawk US Market Open

TUESDAY, AUG 08, 2023 – 05:53 AM

- European bourses are lower given the risk tone post-China trade, banking names lag after an Italian windfall tax

- Stateside, futures are also in the red and feature continued underperformance in the RTY

- Given the tone after downbeat Chinese trade the DXY continues to lift with Antipodeans lagging