GOLD PRICE CLOSED: DOWN $8.35 TO $1917.45

SILVER PRICE CLOSED: DOWN $0.07 AT $22.69

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1914,40

Silver ACCESS CLOSE: 22.65

Shanghai Gold Benchmark Price

USD oz  AM1961.08

AM1961.08

PM1961.39

Historical SGE Fix

New York price at the time: 1925.00

premium $36.00

xxxxxxxxxxxxxxxxxx

Bitcoin morning price:, $29,905 UP 838 Dollars

Bitcoin: afternoon price: $29,498 UP 431 dollars

Platinum price closing $894.25 DOWN $9.70

Palladium price; $1236,85 UP $12.75

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,570.00 DOWN 18.50 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1505,32 DOWN5,71 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1744.42 DOWN 15.37 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: AUGUST 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,924.100000000 USD

INTENT DATE: 08/08/2023 DELIVERY DATE: 08/10/2023

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 33

132 C SG AMERICAS 6

323 C HSBC 231

323 H HSBC 1

357 C WEDBUSH 1

363 H WELLS FARGO SEC 25

435 H SCOTIA CAPITAL 111

657 C MORGAN STANLEY 46

661 C JP MORGAN 1

690 C ABN AMRO 30 16

737 C ADVANTAGE 21

905 C ADM 38

TOTAL: 280 280

MONTH TO DATE: 10,240

JPMorgan stopped 16/280 contracts.

FOR AUGUST:

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2023. CONTRACT: 280 NOTICES FOR 28,000 OZ or 0.8709 TONNES

total notices so far: 10,240 contracts for 1,024,000 oz (31.850 tonnes)

FOR AUGUST:

SILVER NOTICES: 4 NOTICE(S) FILED FOR 20,000 OZ/

total number of notices filed so far this month : 896 for 4,480,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $8.35

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD//

NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 903.69 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 7 CENTS AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: WITHDRAWAL OF 1.193 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 450.180 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUMONGOUS SIZED 3886 CONTRACTS TO 137,631 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUMONGOUS SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.40 LOSS IN SILVER PRICING AT THE COMEX ON TUESDAY. TAS ISSUANCE WAS ANOTHER JUPITER SIZED 9444 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AND TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 9444 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.40). BUT WERE UNSUCCESSFUL IN KNOCKING OF ANY SILVER CONTRACTS AS WE HAD OUR SMALL GAIN OF 211 CONTRACTS ON BOTH EXCHANGES WITH CONSIDERABLE T.A.S.LIQUIDATION.

WE MUST HAVE HAD:

AN ULTRA GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICALS( 4097 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.105 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 15,000 OZ QUEUE JUMP //NEW STANDING RISES AT 4.480 MILLION OZ + OUR NEW CRIMINAL 0 CONTRACTS OF EXCHANGE FOR RISK FOR 0.00 MILLION OZ + 1.45 MILLION OZ EX. FOR RISK/PRIOR/// NEW TOTAL STANDING FOR SILVER: 5.930 MILLION OZ/// // // GIGANTIC SIZED COMEX OI GAIN/ ULTRA HUGE SIZED EFP ISSUANCE/VI) JUPITER SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE (9944 CONTRACTS)/ZERO EXCHANGE FOR RISK ISSUED

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL 659 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTRACTS for 7 days, total 10,556 contracts: OR 52.780 MILLION OZ (1508 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 52.780 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 52.780 MILLION OZ

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3886 CONTRACTS WITH OUR LOSS IN PRICE OF $0.40 IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD AN ULTRA HUGE EFP ISSUANCE CONTRACTS: 4097 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 3.105 MILLION OZ FOLLOWED BY TODAY’S 15,000 OZ QUEUE JUMP//NEW STANDING 4.480 MILLION OZ+ 1.45 MILLION OZ EXCHANGE FOR RISK NEW TOTALS 5.930 MILLION OZ//// WE HAVE A SMALL SIZED GAIN OF 211 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE 9944//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION . THE NEW TAS ISSUANCE TUESDAY NIGHT (9444) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., PROBABLY TOMORROW.

WE HAD 4 NOTICE(S) FILED TODAY FOR 20,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 3675 CONTRACTS TO 427,759 AND CLOSER TO TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED: 448 CONTRACTS

WE HAD A FAIR SIZED DECREASE IN COMEX OI ( 3675 CONTRACTS) WITH OUR $9.60 LOSS IN PRICE//TUESDAY. WE ALSO HAD A RATHER SMALL INITIAL STANDING IN GOLD TONNAGE FOR AUGUST. AT 30.656 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 28,000 OZ QUEUE.JUMP + PRIOR ISSUANCE OF EXCHANGE FOR RISK = (.684 TONNES) //NEW STANDING 32.510 TONNES + .684 EXCHANGE FOR RISK = 33.194/ + /A FAIR (AND CRIMINAL) ISSUANCE OF 1744 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH A $9.60 LOSS IN PRICE WITH RESPECT TO TUESDAY’S TRADING.WE HAD A SMALL SIZED LOSS OF 1253 OI CONTRACTS (3.897 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1744 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 427,759

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1253 CONTRACTS WITH 3657 CONTRACTS DECREASED AT THE COMEX// AND A FAIR 2422 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 1253 CONTRACTS OR 3.897 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 1744 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2422 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (3675) //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 1253 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR JULY AT 30.656 TONNES FOLLOWED BY TODAY’S 28,000 OZ QUEUE JUMP //NEW STANDING 32.510 TONNES + .684 TONNES (EXCHANGE FOR RISK//PRIOR) NEW TOTALS: 33.194 TONNES/// 3) ZERO LONG LIQUIDATION WITH HUGE TAS LIQUIDATION //4) FAIR SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 1744 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUG :

TOTAL EFP CONTRACTS ISSUED: 19,881 CONTRACTS OR 1,988,100 OZ OR 61.838 TONNES IN 7 TRADING DAY(S) AND THUS AVERAGING: 2840 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAY(S) IN TONNES 61.838 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 61.838/3550 x 100% TONNES 1.74% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH: 409.30 TONNES INITIAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 61.838 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (JUNE), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUGE SIZED 3886 CONTRACTS OI TO 137,431 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE AN ULTRA HUGE 4097 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 2062 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 4097 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3886 CONTRACTS AND ADD TO THE 4097 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 211 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 1.035 MILLION OZ

OCCURRED DESPITE OUR $0.40 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED DOWN 16.13 PTS OR 0.49% //Hang Seng CLOSED UP 61.86 PTS OR 0.32% /The Nikkei CLOSED DOWN 172.96 PTS OR 0.32% //Australia’s all ordinaries CLOSED UP 0.31 % /Chinese yuan (ONSHORE) closed UP 7.2056 /OFFSHORE CHINESE YUAN UP TO 7.2210 /Oil UP TO 83.86 dollars per barrel for WTI and BRENT UP AT 86.86 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 3675 CONTRACTS DOWN TO 427,759 WITH OUR LOSS IN PRICE OF $9.60 ON TUESDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF AUGUST… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2422 EFP CONTRACTS WERE ISSUED: : DEC 2422 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2422 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 1253 CONTRACTS IN THAT 2422 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED LOSS OF 3675 COMEX CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $9.60//TUESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A FAIR 1744 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//THE HUGE NUMBER OF T.A.S. CONTRACTS INITIATED OVER THE PAST SEVERAL WEEKS SPELLS TROUBLE FOR THE GOLD/SILVER MARKET AS RAIDS WILL SURELY BE UPON US TRYING TO CONTAIN OUR PRECIOUS METALS RISE IN PRICE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: AUGUST (33.194) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 33.194 TONNES (INCLUDING .6842 EXCHANGE FOR RISK)

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $9.60) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A SMALL LOSS OF 1253 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH ALL OF THE LOSS COMING FROM T.A.S. LIQUIDATION. THE T.A.S. ISSUED ON TUESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 3.897 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST. (30.656 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 28,000 OZ QUEUE JUMP//NEW STANDING ADVANCES TO 32.510 TONNES + .6842 (PRIOR EXCHANGE FOR RISK) //NEW TOTAL 33.194 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $9.60.

WE HAD – REMOVED 448 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET LOSS ON THE TWO EXCHANGES 1253 CONTRACTS OR 125,300 OZ OR 3.897 TONNES.

Estimated gold volume today:// 132,005 awful

final gold volumes/yesterday 152,550 awful

//AUGUST 9/ FOR THE AUGUST 2023 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 53,663.338 Malca 1638 kilobars . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 57,488.988 OZ HSBC |

| No of oz served (contracts) today | 280 notice(s) 28000 OZ 0.8709TONNES |

| No of oz to be served (notices) | 212 contracts 21200 oz 0.6594 TONNES |

| Total monthly oz gold served (contracts) so far this month | 10,240 notices 1,024,000 OZ 31.850 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: NIL oz

customer deposits: 0

total customer deposits: nil oz

we had 1 customer withdrawals

i) Out of Malca 53,663.338 oz 1638 kilobars)

Adjustments; 1//dealer to customer JPMorgan:

385.812 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 492 contracts having LOST 1913 contracts. We had 2193 contracts filed

on Tuesday, so we gained 280 contracts or an additional 28,000 oz will stand at the comex

Sept gained 59 contracts to 2726.

Oct gained 40 contracts to 32,983 contracts.

We had 280 contracts filed for today representing 28000 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 1 notice was issued from their client or customer account. The total of all issuance by all participants equate to 280 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 16 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2023. contract month,

we take the total number of notices filed so far for the month (10,240 x 100 oz ), to which we add the difference between the open interest for the front month of AUGUST (492 CONTRACT) minus the number of notices served upon today 280 x 100 oz per contract equals 1,045,200 OZ OR 32.510 TONNES the number of TONNES standing in this active month of AUGUST. + .684 TONNES EXCHANGE FOR RISK/prior = 33.194 tonnes

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (10,240) x 100 oz + (492) {OI for the front month} minus the number of notices served upon today (280) x 100 oz) which equals 1,045,200 oz standing OR 32.510 TONNES + .684 TONNES OF EXCHANGE FOR RISK/prior = 33.194 TONNES

TOTAL COMEX GOLD STANDING: 33.194 TONNES WHICH IS SMALL FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,083,941.636 OZ 64.82 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 22,207,661.667 OZ

TOTAL REGISTERED GOLD: 12,037,550.164 (374,44 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,170,111.150 O Z

REGISTERED GOLD THAT CAN BE SERVED UPON: 9,953,609 OZ (REG GOLD- PLEDGED GOLD) 309.59 tonnes//

END

SILVER/COMEX

AUGUST 9

//2023// THE AUGUST 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 92,402,985 oz Brinks Loomis . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | nil |

| No of oz served today (contracts) | 4 CONTRACT(S) (20,000 OZ) |

| No of oz to be served (notices) | 0 contracts (nil oz) |

| Total monthly oz silver served (contracts) | 896 Contracts (4,480,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: 0 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0 deposits customer account:

total customer deposits: nil oz

JPMorgan has a total silver weight: 140.471 million oz/281.306 million =49.92% of comex .//

Comex withdrawals 2

i) Out of Loomis 19,178.843 oz

ii) Out of Brinks 73,229.150 oz

adjustments: 0

TOTAL REGISTERED SILVER: 31.066 MILLION OZ//.TOTAL REG + ELIGIBLE. 281.306 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF AUGUST /2023 OI: 4 CONTRACTS HAVING LOST 41 CONTRACT(S). WE HAD

44 NOTICES FILED ON TUESDAY SO WE GAINED 3 CONTRACTS OR AN ADDITIONAL 15,000 OZ WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF AUGUST.

SEPT HAS A LOSS OF 9063 CONTRACTS DOWN TO 83,452

OCT GAINED 101 CONTRACTS TO STAND AT 209.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 4 for 20,000 oz

Comex volumes// est. volume today 77,787 strong/t.a.s.induced /

Comex volume: confirmed yesterday: 104,783 strong/t.a.s induced

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 896 x 5,000 oz = 4,480,000 oz

to which we add the difference between the open interest for the front month of AUGUST (4) and the number of notices served upon today 4 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST/2023 contract month: 896 (notices served so far) x 5000 oz + OI for the front month of AUGUST (4) – number of notices served upon today (4 )x 500 oz of silver standing for the AUGUST contract month equates to 4.480 million oz.+ 0.0 MILLION OZ EXCHANGE FOR RISK ISSUED TODAY+ 1.45 MILLION OZ EXCHANGE FOR RISK PRIOR//NEW TOTALS: 5.930 MILLION oz.

There are 31.066 million oz of registered silver.

Thus if we take today’s standing at 5.930 and add last month’s 30.9 million oz we have 36.830 million oz against only 31.066 million registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

AUGUST 9/WITH GOLD DOWN $8.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 8/WITH GOLD DOWN $9.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES FORM THE GLD /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 7/WITH GOLD DOWN $5.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 906.00 TONNES

AUGUST 4/WITH GOLD UP $7.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.18 TONNES OF GOLD FROM THE GLD/// .///INVENTORY RESTS AT 906.00 TONNES

AUGUST 3/WITH GOLD DOWN $5.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 2/WITH GOLD DOWN $3.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.75 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 1/WITH GOLD DOWN $28.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 31/WITH GOLD UP $9.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 28/WITH GOLD UP $14.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 915,82 TONNES

JULY 27/WITH GOLD DOWN $21.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 917.26 TONNES

JULY 26/WITH GOLD UP $6.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 25/WITH GOLD UP $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 24/WITH GOLD DOWN $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.20 TONNES OF GOLD INTO THE GLD//: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 21/WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / .////INVENTORY RESTS AT 913.80 TONNES

JULY 20/WITH GOLD DOWN $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 913.80 TONNES

JULY 19/WITH GOLD UP $0.65 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .86 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 912.07 TONNES

JULY 18/WITH GOLD UP $23.45 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: .////INVENTORY RESTS AT 912.93 TONNES

JULY 17/WITH GOLD DOWN $6.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD.////INVENTORY RESTS AT 912.93 TONNES

JULY 14/WITH GOLD UP $0.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: ////INVENTORY RESTS AT 914.66 TONNES

JULY 13/WITH GOLD UP $3.30 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.29 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.66 TONNES

JULY 12/WITH GOLD UP $24.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.31 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 914.95 TONNES

JULY 11/WITH GOLD UP $6.15 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.0 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 915.26 TONNES

JULY 10 WITH GOLD DOWN $1.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.60 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 916.26 TONNES.

JULY 7 WITH GOLD UP $16.80 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 917.86 TONNES.

JULY 6/WITH GOLD DOWN $9.90 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD//INVENTORY RESTS AT 917.86 TONNES

JULY 5/WITH GOLD DOWN $2.20 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 2.6 TONNES FROM THE GLD///INVENTORY RESTS AT 921.90 TONNES

JULY 3/WITH GOLD UP $1.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 924.50 TONNES//

JUNE 30/WITH GOLD UP $10.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 924.50 TONNES

JUNE 29/WITH GOLD DOWN $3.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.26 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 926.81 TONNES

GLD INVENTORY: 903.69 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 9/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 8/WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 7/WITH SILVER DOWN 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 4/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.294 MILLION OZ FROM THE SLV// OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 3/WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 189,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.281 MILLION OZ

AUGUST 2/WITH SILVER DOWN 43 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 275,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.471 MILLION OZ

AUGUST 1/WITH SILVER DOWN 61 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 31/WITH SILVER UP 45 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 28/WITH SILVER UP 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.930 MILLION OZ

JULY 27/WITH SILVER DOWN 59 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ

JULY 26/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 25/WITH SILVER UP 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 826,000 OZ FROM THE SLV..////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 24/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 21/WITH SILVER DOWN 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.101 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 20/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.468 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 454.107 MILLION OZ/

JULY 19/WITH SILVER UP 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 18/WITH SILVER DOWN 19 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:A ////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 17/WITH SILVER UP 25 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 4.856 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 14/WITH SILVER UP 27 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.21 MILLION OZ OF SILVER FROM THE SLV////////INVENTORY RESTS AT 455.875 MILLION OZ/

JULY 13/WITH SILVER UP 64 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 12/WITH SILVER UP $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.881 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 462.941 MILLION OZ/

JULY 11/WITH SILVER DOWN 5 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .020 MILLION OZ INTO THE SLV////INVENTORY RESTS AT 464.822 MILLION OZ/

JULY 10/WITH SILVER UP 2 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.672 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 464.802 MILLION OZ

JULY 7/WITH SILVER UP 42 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 466.474 MILLION OZ

JULY 6/WITH SILVER DOWN 50 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.667 MILLION OZ FROM THE SLV///INVENTORY RESTS AT 466.474 MILLION OZ//

JULY5/WITH SILVER UP 30 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

JULY 3/WITH SILVER UP 7 CENTS TODAY; NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY RESTS AT 468.141 MILLION OZ//

CLOSING INVENTORY 450.180 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

RUSS AND PAM MARTENS:

Jamie Dimon Faces an Uphill Battle Convincing a Jury He Didn’t Know that Child Sex-Trafficker, Jeffrey Epstein, Was Financing His Operation Out of JPMorgan JPMorgan Chase and Jeffrey Epstein

By Pam Martens and Russ Martens: August 9, 2023 ~

Jamie Dimon is between a rock and a hard place. He is either going to have to convince a jury come October that he was left in the dark by the bank’s general counsel, his compliance and money laundering executives, and the heads of his investment bank and asset and wealth division about the fact that notorious child molester Jeffrey Epstein was a client at the bank for more than a decade – which would make Dimon sound so isolated as to be unfit to be running the bank – or Dimon is going to have to admit that he lied under oath in his federal court deposition. Neither is a comfortable proposition to be facing for a jury trial currently scheduled for October 23.

JPMorgan Chase is currently facing off against three federal lawsuits before Judge Jed Rakoff in the Southern District of New York that charge the bank with facilitating Epstein’s sex trafficking operation, which included dozens of underage school girls. One lawsuit was brought by Epstein’s victims; another by the Attorney General of the U.S. Virgin Islands where Epstein owned an island compound; and a third by shareholders of the bank, which name the bank, Dimon, another bank executive and specific Board Members as defendants.

It is the lawsuit brought by the Attorney General of the U.S. Virgin Islands that is currently scheduled for trial on October 23 that poses a significant amount of legal peril for Dimon. That lawsuit alleges that JPMorgan Chase not only “facilitated” Epstein’s crimes against women and girls but “actively participated in Epstein’s sex trafficking venture.”

According to the transcript of Dimon’s deposition conducted on May 26, his position is this:

“I don’t recall knowing anything about Jeffrey Epstein until the stories broke sometime in 2019. And I was surprised that I didn’t even — had never even heard of the guy, pretty much, and how involved he was with so many people.”

Dimon’s reference to stories breaking in 2019 is because the U.S. Department of Justice, which had cut Epstein a notorious sweetheart deal in 2007 that provided him a non prosecution agreement and allowed him to plead to two counts of procuring prostitution (instead of multiple counts of rape and sexual assaults of underage schoolgirls) finally got around to bringing federal sex trafficking charges against Epstein in 2019 – after Epstein and his wealthy pals had raped and sexually assaulted hundreds of other girls.

The details of that 2007-2008 sweetheart deal had been making headlines for years – headlines that Dimon somehow missed, despite testifying in his deposition that he read multiple newspapers daily. In addition to newspaper headlines, bestselling author, James Patterson’s book, “Filthy Rich,” covering Epstein’s sexual assaults of young girls had been released in 2016 and Julie Brown’s blockbuster series on Epstein’s crimes in the Miami Herald in 2018 had caused a viral media storm. But Dimon somehow missed it all.

Dimon’s general counsel from 2007 to 2015 was Stephen Cutler, the former Director of the Division of Enforcement at the Securities and Exchange Commission. Cutler stepped down as General Counsel in 2015 to become Vice Chairman at JPMorgan Chase and a senior advisor to Dimon and the bank’s Board of Directors. He served in that position until 2018 when he left the bank to join the law firm Simpson Thacher & Bartlett. It is almost inconceivable that in all those years Cutler would not have brought the reputational risk that Epstein posed to the bank to the attention of Dimon or the Board.

According to emails obtained by the U.S. Virgin Islands in discovery, Cutler was aware of Epstein’s history and the existence of his accounts at the bank from at least 2011. Cutler reported directly to Dimon and his office was located next door to Dimon’s office. The emails show that Cutler was against keeping Epstein as a client. It is only common sense that someone higher up than Cutler would have had to overrule him. That suggests some interference by Dimon or the Board of Directors to keep Epstein and his accounts at the bank.

In addition, dozens of internal emails show that a multitude of the bank’s compliance personnel and anti-money laundering staff were holding “Rapid Response” team meetings as each scandalous newspaper article about Epstein appeared.

The U.S. Virgin Islands has produced extensive evidence that the motive for keeping Epstein as a client at JPMorgan Chase, despite his ongoing sex trafficking, was the revenues his accounts were generating for the bank and the ultra wealthy clients he was referring to the bank.

In a court filing on July 26, the U.S. Virgin Islands lists the following individuals as people Epstein referred as clients to the bank: Microsoft co-founder and billionaire Bill Gates; Google co-founder and billionaire Sergey Brin; the Sultan of Dubai, Sultan Ahmed bin Sulayem; media and real estate billionaire Mort Zuckerman; former U.S. Treasury Secretary and former Harvard President Larry Summers, and numerous others.

Another big hurdle for Dimon before a jury is a smoking gun email raised during Dimon’s deposition by well-known attorney, David Boies, of law firm Boies, Schiller & Flexner LLP. (Dimon’s deposition was conducted jointly by lawyers for the U.S. Virgin Islands and lawyers for Epstein’s victims. Boies is representing the victims.)

Boies introduced an email directly referring to a planned Epstein meeting with Dimon in 2010. The exchange between Boies and Dimon went as follows:

Boies: “On February 26, 2010, Lesley Groff [Epstein’s assistant] writes Mr. Epstein on the subject of, Jes [Staley] and Jamie. ‘Shall I have Lynn prepare heavy snacks for your evening appointments with [redacted], Jes Staley and Jamie Dimon? Or is this to be a nice, sit-down dinner at 9 p.m.?’ And Mr. Epstein replies, ‘Snacks.’ “

Dimon responds:

“I have never had an appointment with Jeff Epstein. I’ve never met Jeff Epstein. I never knew Jeff Epstein. I never went to Jeff Epstein’s house. I never had a meal with Jeff Epstein. I have no idea what they’re referring to here.”

Boies points out that there is no followup email between Epstein and Groff where Epstein tells her she is misinformed and Dimon is not going to be at the meeting.

Jes Staley testified in his deposition that he had discussions with Dimon about Epstein in 2006, thus refuting Dimon’s narrative of what he knew and when he knew it.

There is no dispute that Epstein had accounts at JPMorgan and its successor, JPMorgan Chase, from at least 1998 to 2013. (A former FBI agent retained as an expert witness by the U.S. Virgin Islands is prepared to testify that the account relationship dates back to 1985.) According to transaction documents obtained in discovery by the U.S. Virgin Islands, JPMorgan Chase handled 9,000 transactions payable to Epstein-related individuals (which included his accomplices and recruiters of underage girls) between 2005 and 2019, and “had a combined value of over $2.4 billion.”

In addition, without filing the legally-required Suspicious Activity Reports for a Level 3 Registered Sex Offender who had been chronicled in dozens of newspaper reports as paying his victims in cash, JPMorgan Chase allowed Epstein or his representative to withdraw the following sums in hard cash from his accounts at the bank according to a court filing made by the U.S. Virgin Islands:

“In the year 2003, Epstein was able to withdraw highly suspicious amounts of cash totaling $175,311. In 2004, he withdrew $840,000. In 2005, he withdrew $904,337. In 2006, he withdrew $938,625. In 2007, he withdrew $526,000. In 2008, he withdrew $469,000. In 2009, he withdrew $165,011. In 2010, he withdrew $253,397. In 2011, he withdrew $260,000. In 2012, he withdrew $290,000. In 2013, he withdrew $197,152.”

According to internal documents produced in discovery, Epstein was allowed to withdraw in hard cash as much as $40,000 to $80,000 per month in some years without the mandated filings of Suspicious Activity Reports by the bank.

Adding to the stench around Epstein’s long-term relationship with JPMorgan Chase is the question as to how the U.S. Department of Justice and the FBI investigated this case from 2007 to at least 2019 and never discovered that JPMorgan Chase was at the center of handling the financing for this international sex ring with 9,000 transactions of over $2.4 billion.

When the U.S. Department of Justice learned in 2014 that JPMorgan Chase had been the bank handling Bernie Madoff’s Ponzi account for decades, it charged the bank with two felony counts and imposed massive fines. Why aren’t we hearing a peep from the U.S. Department of Justice now about JPMorgan Chase – especially after its disgrace in letting Epstein off the hook in 2007-2008?

Equally troubling, the Epstein-related lawsuits before Judge Rakoff against JPMorgan Chase have been making headlines in major U.S. newspapers for months now. Why hasn’t the U.S. Senate Banking Committee or the Senate Finance Committee convened hearings?

On August 11 of last year, President Biden’s Attorney General at the U.S. Department of Justice, Merrick Garland, told the American people this:

“Faithful adherence to the rule of law is the bedrock principle of the Justice Department and of our democracy. Upholding the rule of law means applying the rule of law evenly, without fear or favor.”

Garland’s credibility on that issue hinges on how JPMorgan Chase, the largest bank in the United States, and its billionaire Chairman and CEO, Jamie Dimon, are treated in the Epstein matter.

3,Chris Powell of GATA provides to us very important physical commentaries

Turkey continues to import high amounts of gold (and silver) in the form of bullion and jewelry. Now the Turkish authorities want to impose extra charges on gold that arrives from countries that do not have a free trade agreement with it

(Reuters)

Turkey imposes extra charge on some gold imports

Submitted by admin on Tue, 2023-08-08 14:26Section: Daily Dispatches

By Ezgi Erkoyun

Reuters

Tuesday, August 8, 2023

ISTANBUL — Turkey has introduced a 20% additional charge for some gold imports, according to a decision published in the Official Gazette early today, in an effort to curb the negative impact on the current account balance.

The decision said that gold imports originating from countries that are without a free trade agreement and not in the European Union will be charged an additional fee on top of existing import and other duties.

The gold imports that will be charged the extra fee as part of the decision include gold jewellery products and parts, and some base metal products plated with precious metals.

Turkey’s current account deficit widened mainly due to high gold and energy imports and stood at $37.7 billion in the first five months of the year, widening some 44% when compared to the same period last year.

On Monday the state-owned Anadolu news agency reported citing an unnamed source that Turkey plans to impose a quota on imports of unprocessed gold.

end

END

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES/SILVER

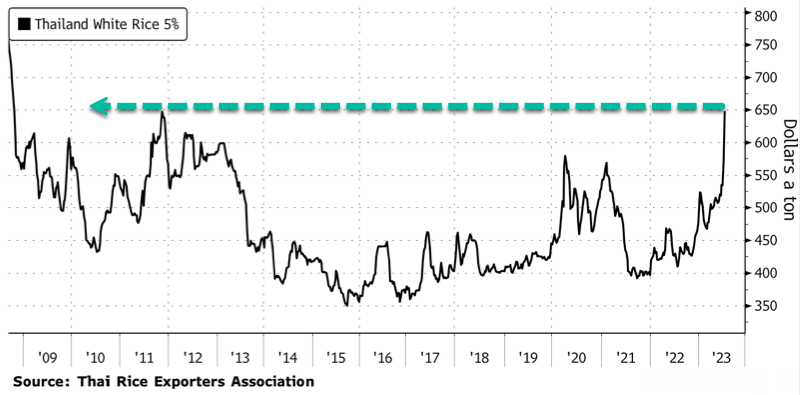

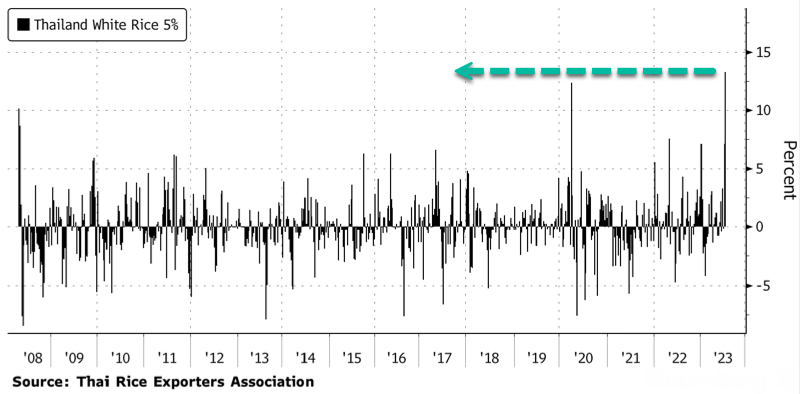

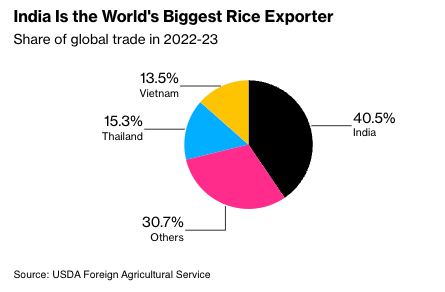

5 a. IMPORTANT COMMENTARIES ON COMMODITIES: RICE

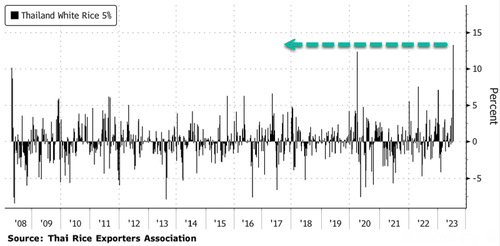

Thai rice up a huge 13% this week and over 50% since 2022, hitting 648 dollars per ton, its highest level since Oct 2008

(zerohedge)

Rice Crisis Sends Prices To Highest Levels Since 2008

WEDNESDAY, AUG 09, 2023 – 06:55 AM

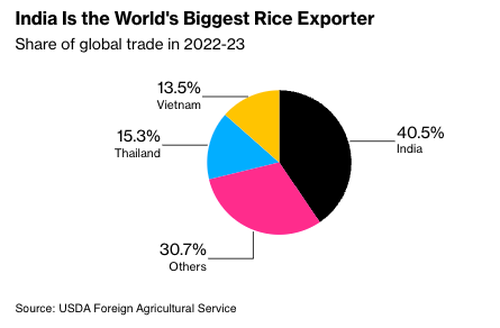

On Wednesday, the Thai Rice Exporters Association revealed that the price of Thai white rice 5% broken, a key Asian benchmark, reached the highest level since Great Financial Crisis. This surge is mainly attributed to increasing fears of a global shortage due to the damaging effects of the El Nino weather phenomenon on Asian farmlands and India’s recent decision to restrict certain rice exports.

Thai white rice 5% broken hit $648 per ton this week, the highest level since October 2008. Prices are up over 50% since the start of 2022.

The weekly change in rice prices is about a 13% surge, the largest since the index began in the summer of 2008.

We provided readers with enough understanding that rice, which is critical to the diets of billions of people worldwide, was headed for a shortage:

- Sept. 2022: The Stage Is Being Set For A Massive Global Rice Shortage

- May 2023: Global Rice Shortage Looms, Set To Be The Biggest In Decades

- May 2023: Thai Rice Crop In Crosshairs Of El Nino As Farmers Are Warned About Water Shortages

And now comes the panic:

India’s move to ban some rice exports sent shockwaves worldwide and was to ensure domestic supplies were adequate to prevent a hyperinflationary spike in food prices that would ultimately spark social unrest. Also, Thailand, the second-biggest shipper, has asked farmers to switch to crops that use less water due to arid conditions.

India’s export restriction applies to shipments of non-basmati white rice.

The latest report on global food prices from the Food and Agriculture Organization of the United Nations showed the global food index, which tracks monthly changes in the international prices of globally-traded food commodities, jumped the most in 18 months.

Last month, Bloomberg quoted Peter Timmer, Professor Emeritus at Harvard University, who warned: “There is considerably more reason for concern now that rice prices in Asia could spiral out of control pretty quickly.”

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2010

OFFSHORE YUAN: UP TO 7.2256

SHANGHAI CLOSED DOWN 16.13 PTS OR 0.49%

HANG SENG CLOSED UP 61,86 PTS OR 0.32%

2. Nikkei closed DOWN 172,96 PTS OR 0.53%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 102.31 EURO RISES TO 1.0973 UP 14 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.562 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 142.97/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ON SHORE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.4614***/Italian 10 Yr bond yield RISES to 4.120*** /SPAIN 10 YR BOND YIELD RISES TO 3.510…**

3i Greek 10 year bond yield RISES TO 3.769

3j Gold at $1923.30 silver at: 22.68 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 10 /100 roubles/dollar; ROUBLE AT 96.38//

3m oil into the 83 dollar handle for WTI and 85 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 143.42// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.562% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8773 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9626 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.027 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.192 UP 0 BASIS PTS/

USA 2 YR BOND YIELD: 4.781 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 27.03…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 5 BASIS PTS AT 4.4375

end

2.a Overnight: Newsquawk and Zero hedge:

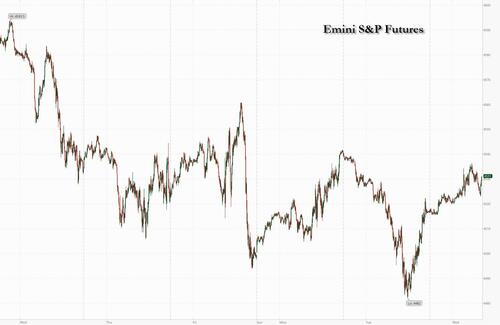

Futures Rise On Hope China’s Deflation Will Lead To More Policy Easing

WEDNESDAY, AUG 09, 2023 – 08:18 AM

S&P futures point to a higher open after China officially entered into deflation with -0.4% CPI print, continuing the buying momentum from the second half of yesterday’s session while European stocks rebound sharply from yesterday’s rout led by a rebound in Italian banks after the government backtracked on part of its new windfall tax on lenders. As of 7:45am ET, both S&P and Nasdaq 100 futures are 0.2% higher with other global markets also in risk-on mode, with the euro strengthening, copper rebounding, 10Y TSY yields rising to 4.03% ahead of another closely watched bond auction later today (US government is selling $38 billion of new 10-year notes, $3 billion larger than the last 10-year note debut in May) and oil rising by $1, just inches away from 2023 highs. Rice in Asia soared to its highest level since 2008.

China’s CPI – coming one day before the US inflation number – printed negatively for the first time in two years which is likely to produce a deflationary impulse on core goods inflation, and which according to JPM’s trading desk could prove useful to the Fed (and markets) if we see the US Consumer shift back from Services demand to Goods demand this year (more in the full JPM trading desk note this morning available to pro subs). Today’s macro data and earnings focus is on mortgage applications (down 3.1% after sliding 3.0% last week) and DIS earnings. Homebuilders have outperformed the SPX by 23% YTD.

In premarket trading, all the megacap techs are higher, with both KRE and XLF indicated marginally higher. Commodities are higher led by Energy, which also saw a late day rally. WeWork shares crashed 17% after the co-working business said there is “substantial doubt” about its ability to continue operating. Here are some other notable premarket movers:

- Lyft falls as much as 8% after the ride-hailing company reported its slowest revenue growth since the pandemic.

- Penn Entertainment shares rise 9.6% after the sports-entertainment company announced a long-term exclusive partnership with Disney’s ESPN.

- DraftKings fell as much as 6.7% on concern the tie-up between Penn Entertainment and Disney’s ESPN will increase competition.

- Rivian shares rise as much as 2.2% after the electric-vehicle startup raised its full-year production forecast to 52,000 vehicles from 50,000. The company also reported better-than-expected second-quarter results.

- Twilio shares rise as much as 7.9% after the software company reported second-quarter results that beat analysts’ expectations and raised its profit outlook for the year.

- Marqeta jumps 17% after second-quarter revenue at the commerce payments platform beat analyst estimates and analysts flagged the renewal of the Cash App contract with Block (SQ US) as a positive.

- Tango Therapeutics jumps as much as 80%, on track for its biggest rise on record if gains hold, after data was published on competitor Mirati Therapeutics Inc.’s cancer drug candidate MRTX1719.

- Coupang gains 4% after the online retailer reported second-quarter earnings per share that beat estimates. Citi said the company had a “solid” beat on the top-line and Ebitda.

The tentative improvement in sentiment faces a test on Thursday when the latest US CPI data is published. It takes place as a closely watched bond-market gauge of inflation expectations is rising back toward a nine-year high, signaling elevated price pressures for years. The US five-year inflation breakeven – which basically is a proxy for oil prices – has risen to around 2.5%, just shy of the peak in April 2022, when it reached the highest since 2014.

The “inflation report will be key if today’s rally is to be sustained.” said Lewis Grant, a senior portfolio manager at Federated Hermes. “Investor risk aversion has started to wane but remains volatile and investors are anxiously searching for the next signal.”

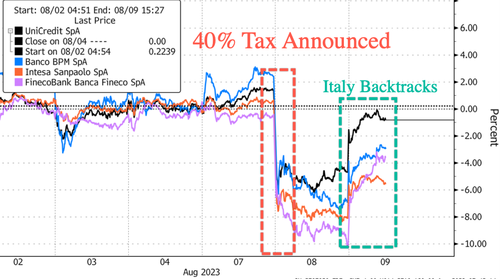

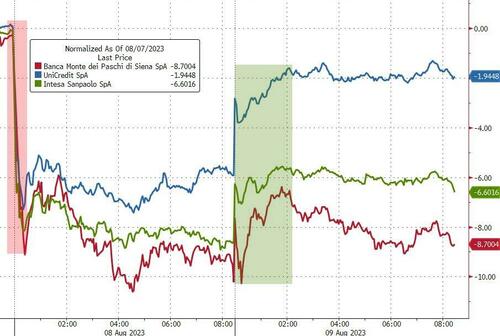

European stocks are ahead, led by a rebound in Italian banks after the government backtracked on part of its new windfall tax on lenders. The Stoxx 600 is up 1% while the Euro Stoxx Banks Index adds 1.7% after falling 3.5% on Tuesday. UniCredit SpA and Intesa Sanpaolo SpA, at the center of Tuesday’s declines when the new tax was unveiled, became some of Wednesday’s biggest gainers, boosting the Stoxx Europe 600 as much as 1% Wednesday. Here are some of Europe’s top movers:

- Delivery Hero gains as much as 10% after the food delivery company demonstrated its path to profitability with a positive adj. Ebitda in the first half

- Vestas Wind Systems rises as much as 3.8% after it published earnings analysts said showed a stronger-than-expected performance for the firm’s Services business

- Sampo shares rise as much as 5.9%, the most since March 2022, after the insurance company owner’s second-quarter earnings came in better than feared

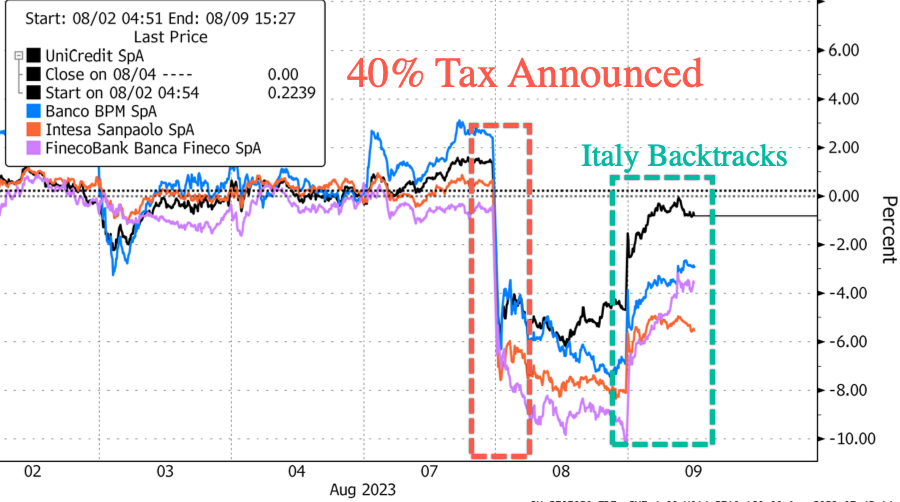

- Italian banks rebound from Tuesday’s slump after the government issued a clarification of its new tax on banks’ windfall profits, saying it will be capped

- Fraport rises as much as 5.2% after Morgan Stanley boosted its price target for the German airport operator as second- quarter earnings provided much-wanted relief

- E.On gain as much as 2.3% after the German energy networks operator reported first- half results in line with an earlier update

- TP ICAP surges as much as 16%, the most since 2020, after the financial services firm delivered results which Canaccord says “give comfort,” and announced a buyback

- Hill & Smith rises as much as 10% as analysts highlights good first-half results and balance sheet strength for the infrastructure and transport company

- Flutter Entertainment drops as much as 6.1% as a new partnership between Penn Entertainment and Disney’s ESPN stoked concern over rising competition

- Ahold Delhaize shares slip as much as 3.6% in early trading after revenue and adjusted operating profit in the US came in below expectations

Asian stocks were mixed after two days of declines, weighed by losses in some Chinese stocks as latest economic data showed further acceleration of deflationary pressures in the economy. The MSCI Asia Pacific Index was up 0.1% for the day. “Investors are clamoring for broad-based stimulus in China. I don’t think we are going to get that,” David Chao, strategist at Investec Asset Management, said on Bloomberg Television. Chao sees China moving ahead with piecemeal measures to support consumption and private investment that may result in “a pop in Chinese equities later this year.”

- Chinese stocks in Hong Kong erased a drop of as much as 0.9%, while the CSI-300 was down about 0.2%, as markets reflected on the mixed inflation data from China which showed CPI Y/Y slipped into deflation territory, albeit at a narrower-than-expected drop in prices, while factory gate prices continued to fall at a steeper than forecast pace. Property stocks in the mainland rebounded after a report said that tier-1 cities are discussing potential measures to ease the malaise in the sector. Property stocks have taken a beating this week over potential default at Country Garden Holdings.

- Japan’s Nikkei 225 weakened with trade initially indecisive amid an influx of earnings releases and with the biggest winners and losers all driven by corporate results including SoftBank which was near the bottom end of the spectrum after its surprise loss.

- Meanwhile, Korean stocks were set to snap a five-day selling spree, with retail and foreign investors nibbling in the market. An EV-led selloff in the market has sapped risk sentiment this week, but technology stocks are leading the rebound.

- Indian stocks reversed earlier losses and closed higher on Wednesday, helped by advances in shares of automobile and metal producers. The S&P BSE Sensex rose 0.2% to 65,995.81 in Mumbai, while the NSE Nifty 50 Index advanced 0.3% to 19,632.55. Technology stocks and Reliance Industries also helped benchmarks reverse earlier losses as they recovered in late buying by investors. The BSE IT index closed 0.3% higher.

In FX, the Bloomberg Dollar Index falls 0.1%. The Swedish krona and Norwegian krone are the best performers among the G-10 currencies. The Aussie climbed as much as 0.3% to 65.64 US cents after the People’s Bank of China set the dollar-yuan rate at 548 pips below traders’ estimate, signaling it’s in no rush to withdraw support for the currency. China’s state-owned banks were also seen selling dollars, according to Asia-based FX traders.

In rates, 10-year Treasury yields ticked up ahead of another closely watched bond auction later today, while the treasuries curve was flatter with front-end yields modestly cheaper and long-end little changed vs Tuesday’s closing levels, outperforming bunds and gilts. The US government is expected to sell $38 billion of new 10-year notes, $3 billion larger than the last 10-year note debut in May. Treasury 10-year yields around 4.03%, marginally cheaper on the day with bunds and gilts lagging by additional 2.5bp and 1.5bp in the sector; long-end outperforms ahead of 10- and 30-year supply over Wednesday and Thursday, with 2s10s and 5s30s spreads flatter by 1bp and 1.5bp on the day. Japan bonds drew support during Asia session from data showing China experiencing deflation. Focal point of US session is upsized 10-year note auction, following strong demand for Tuesday’s 3-year note sale. The Treasury auction cycle resumes with $38b 10-year new issue at 1pm New York time and concludes with $23b 30-year bond sale Thursday. WI 10-year at around 4.03% is ~17bp cheaper than July’s stop-out and above auction stops since November.

The week’s debt auctions will gauge how concerned investors are about a rising US budget deficit, a week after Fitch Ratings decided to strip the US of its top credit rating. Tuesday’s $42 billion sale of three-year notes had a lower-than-expected yield, a sign that demand was stronger than anticipated.

In crypto, the Fed announced the creation of an activities supervision program to oversee bank tech initiatives which will focus on activities related to crypto, blockchain tech and non-bank tech partnerships, while the Fed said state member banks should receive written non-objection from the Fed before issuing, holding or transacting in dollar tokens, according to Reuters.

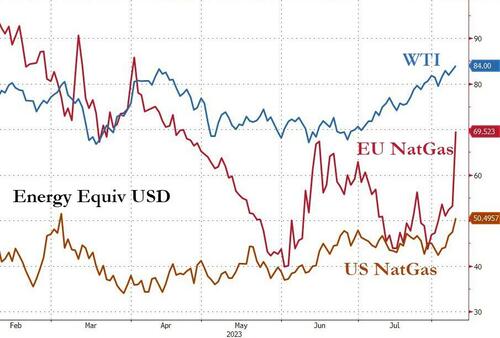

In commodities, US crude futures advance, with WTI rising 1% to trade near $83.70. Spot gold adds 0.1%. Bitcoin is down 0.6%.

Looking ahead to today, it will be quiet in terms of data, with weekly mortgage applications in the US and Canada’s monthly building permits. Meanwhile, as the earnings season starts to wind down, we will hear from the likes of Walt Disney, Sony, Vestas and Illumina.

Market Snapshot

- S&P 500 futures up 0.3% to 4,533.75

- MXAP up 0.1% to 165.09

- MXAPJ up 0.5% to 522.35

- Nikkei down 0.5% to 32,204.33

- Topix down 0.4% to 2,282.57

- Hang Seng Index up 0.3% to 19,246.03

- Shanghai Composite down 0.5% to 3,244.49

- Sensex down 0.3% to 65,640.89

- Australia S&P/ASX 200 up 0.4% to 7,337.96

- Kospi up 1.2% to 2,605.12

- STOXX Europe 600 up 0.9% to 462.95

- German 10Y yield little changed at 2.47%

- Euro up 0.2% to $1.0975

- Brent Futures up 0.3% to $86.41/bbl

- Gold spot up 0.2% to $1,929.02

- U.S. Dollar Index down 0.12% to 102.40

Top Overnight News

- A US plan to restrict investment in China will probably only apply to companies that get at least half their revenue from sectors such as quantum computing and AI, people familiar said, allowing PE and VC firms to still put money into bigger conglomerates. The proposal, expected in coming days, will take about a year to go into force. BBG

- China’s CPI falls into deflation in Jul (it came in at -0.3% vs. flat in June but not as bad as the Street’s -0.4% forecast) while the PPI sank 4.4% (better than -5.4% in June, but worse than the Street’s -4% forecast). BBG

- Italy backtracks on its planned bank windfall tax as the gov’t looks to calm market jitters, stating that the levy would be capped at 0.1% of RWAs, much smaller than some analysts had feared (the tax will only raise about EU1.8B). FT

- Talks are ongoing to restart the deal that allowed Ukraine to export grain via a safe corridor on the Black Sea, Turkish President Recep Tayyip Erdogan said late Tuesday after speaking with Russian leader Vladimir Putin. BBG

- US banks suffered almost $19bn of losses on soured loans in the second quarter, the highest level in more than three years as lenders contend with rising defaults among credit card and commercial real estate borrowers. FT

- The CBO paints a challenging fiscal picture for the US and now expects that the total deficit for 2023 will be $1.7 trillion, or about $200 billion larger than the estimate it published in May. CBO

- New contract demands made by the United Auto Workers union would add more than $80 billion to each of the biggest US automakers’ labor costs, according to people familiar with the companies’ estimates. BBG

- WeWork on Tuesday raised doubt about its ability to stay in business as the co-working space provider faces losses and a dwindling cash pile amid major changes in the way people work. WSJ

- Amazon is in talks to join other tech companies as an anchor investor in the Arm IPO, a person familiar said. The offering is expected next month and may raise $10 billion. Amazon is already one of Arm’s biggest clients. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed as participants digested a deluge of earnings releases and the latest inflation data from China which was mixed but showed consumer prices in deflationary territory for the first time in more than two years. ASX 200 was just about kept afloat by the outperformance in its top-weighted financial sector after Australia’s largest lender CBA posted a record FY profit. Nikkei 225 ultimately weakened with trade initially indecisive amid an influx of earnings releases and with the biggest winners and losers all driven by corporate results including SoftBank which was near the bottom end of the spectrum after its surprise loss. Hang Seng and Shanghai Comp were subdued as markets reflected on the mixed inflation data from China which showed CPI Y/Y slipped into deflation territory, albeit at a narrower-than-expected drop in prices, while factory gate prices continued to fall at a steeper than forecast pace.

Top Asian News

- US is set to limit the scope of the China investment ban with a revenue rule and the order limiting investments is expected in the approaching days, according to Bloomberg.

- US lawmakers asked the FCC to address potential threats from Chinese cellular Internet of Things modules in US networks.

- China’s National Bureau of Statistics said the Y/Y decline in consumer prices is only temporary.

- China government considering holding leaders with Japan on the sidelines of the ASEAN meeting in Indonesia, according to Kyodo.

European bourses are firmer across the board, Euro Stoxx 50 +1.4%, with newsflow light and the main mover being banks clawing back downside from the Italian windfall tax following an adjustment. As such, the FTSE MIB +1.9% outperforms while the OMX Copenhagen +0.4% is the relatively underperformer as Novo Nordisk pares some of Tuesday’s pronounced gains. Stateside, futures are on the front foot and making up for some of the prior session’s downside, ES +0.3%, as risk sentiment improves and was further assisted by Fed’s Harker.

Top European News

- UK government is pushing back against attempts by some members of the House of Lords for tighter corporate transparency and warned that publishing all trust data could be problematic, according to FT.

- Cap on Italy bank windfall tax halves the estimated hit on average CET1 to 30bps with Fineco (FBK IM) and Bper (BPE IM) among banks benefiting the most, according to Jefferies; elsewhere, cap at 0.1% of assets for new Italian bank tax equates into an aggregate total impact of EUR 1.9bln for banks/asset gatherers, via UBS.

- Swedish NIER Forecasts (July): economy heading for a downturn. Riksbank Rate, end-2023: 4.0% (prev. 3.75%)

FX

- DXY dips under 102.50 to a 102.29 session trough, but price action overall remains contained in quiet trade and newsflow.

- Yuan was in focus during APAC hours given Chinese inflation, with the CNH benefitting post-release and spurred further by reports China’s major state-owned banks are seen selling dollars to buy Yuan.

- Antipodeans are the relative outperformers given the week’s hefty losses thus far, as sentiment improves slightly and the USD pulls back as mentioned.

- EUR and GBP are both benefiting from the tone/broader USD action, with specifics limited and EUR perhaps deriving support from the Italian government altering its windfall tax.

- PBoC set USD/CNY mid-point at 7.1588 vs exp. 7.2198 (prev. 7.1565)

- China’s major state-owned banks were seen selling dollars to buy yuan in the onshore spot FX market.

Fixed Income

- Core benchmarks are relatively contained and yet to deviate much from the unchanged mark in limited newsflow ex-supply; though, there is a minor discrepancy between the performance of core and periphery EGBs.

- Gilts have been the relative outperformers throughout the session with specifics limited though it is worth highlighting that UK debt didn’t benefit quite as much from the week’s initial bullish price action; the 10yr DMO outing was well received and spurred a fresh session high.

- Bunds have been in-fitting but came under some pressure following a relatively tepid German sale, though it is worth caveating that summer conditions apply and desks point out the timing coincided with large volumes going through, which are likely sell orders.

- Stateside, USTs are in-fitting and given the action, there is little of note occurring across the curve where yields are under very modest pressure.

Commodities

- Energy tilts firmer after an overnight session of sideways trade, complex continuing to derive support from Saudi commentary earlier in the week.

- Crude benchmarks are currently above the USD 83.00/bbl and USD 86.50/bbl marks for WTI Sep’23 and Brent Oct’23 respectively.

- Spot gold sees marginal gains, albeit as a function of the softer USD with the yellow metal in a tight range.

- LME copper trades with modest gains but remains under the USD 8,500/t mark in a USD 8,487.50-347.50/t range.

- Iranian oil official says Iran is to produce an extra 250k BPD of oil by the end of summer, according to Tasim.

- India Food Secretary says India has adequate stocks of rice and wheat. Follows on from rice prices within Asia lifting to their highest since 2008.

Geopolitics

- Russia’s Defence Minister says Russia is to build up forces at the Western borders, according to Tass.

- Russia shot down two combat drones that were headed towards its capital, according to AFP News Agency citing the Moscow Mayor.

- Polish Deputy Interior Minister says 2k troops to be sent to the Belarus border, via PAP.

US Event Calendar

- 07:00: Aug. MBA Mortgage Applications -3.1%, prior -3.0%

DB’s Jim Reid concludes the overnight wrap

In what is proving to be a volatile August so far, with negative headlines outpacing positive ones, yesterday saw a return to risk-off leaving the S&P 500 down -0.42% on the day, and -1.95% for the month so far. This occurred on the back of weaker Chinese trade data we reported yesterday coupled with negative news on both sides of the Atlantic for the banking sector. However, sentiment improved during the US session, with S&P 500 recovering after being -1.2% down at the lows, in part following a strong 3yr Treasury auction. China has slipped into deflation this morning as expected but the data was broadly inline so there been no additional sell-off momentum so far, with fresh stimulus hopes still in the background.

In the US, the regional banking story reappeared in the headlines after Moody’s downgraded ten small and midsize banks and put a number of larger firms on review or negative outlook. 29 banks in total saw some kind of action. The US regional bank index traded more than -4% lower following the news but recovered to close at -1.38%. The broader banking sector also underperformed, with S&P 500 banks down -1.07%. The regional banking index had reached a post-SVB high the previous day, with a +34% increase since its low in mid-May, having reversed about two thirds of the post-SVB decline. Moody’s cited higher funding costs, potential regulatory capital weakness and increasing commercial real estate risks. In my mind, until we truly know where CRE will bottom its impossible to call the all clear for this cycle. This story won’t fully play out for some time though.

Over in Europe, Italian banks saw a sharp decline (-8.27%) after the Italian government announced a one-off windfall tax of banks that will amount to 40% of the excess net interest margin earned in 2023 (or 2022 if that is higher). However, in the evening the government issued a clarification that the levy would not exceed 0.1% of a firm’s assets. In an update published overnight, our European bank analysts estimate that such a cap would reduce the overall size of the tax by over 40%, though it would still take more than 10% from 2023 profits. See here for more. So this adjustment should improve sentiment today. The broader European banking index had declined -3.54% yesterday, though it is still up +13.6% year-to-date (versus + 7.93% ytd for the broader STOXX 600). The Italian FTSE-MIB (-2.12%) led the declines in Europe with the DAX and CAC -1.10% and -0.69% respectively. Beyond the immediate market impact, the story is a reminder that the burden-sharing of the costs and benefits from higher rates has a habit of becoming a political issue.

The risk-off mood led a decline in long-term yields, with 10yr treasuries down -6.7bps and 30yr -6.3bp (4-5bps up from the day’s lows though). The 2yr had seen a modest sell-off earlier in the day, but ended up closing -1.3bp lower, falling a few bps after a strong 3yr Treasury auction. This saw $42bn of 3yr notes issued at 4.398%, nearly 2bps below its pre-auction trading, with strong indirect demand and record low primary dealer take down. So a successful start to the increased refunding supply of Treasuries. This will be tested more with the 10yr auction today and 30yr auction tomorrow. Yesterday, our US rates strategists published a chart that nicely visualises the large increase in supply that’s due in the coming months – see here for more.

Back in Europe, yields saw an even stronger bull flattening rally. 2yr bund yields were down -6.9bps, while the 10yr yield declined by -13.3bps, its sharpest daily fall since mid-June as the China and banking story dominated.

As discussed earlier, it was a bad day for US equities, but better than it might have been, with the S&P 500 closing -0.42% down. Financials (-0.88%) led the decline. Tech also had a bad day, with the NASDAQ down -0.79% and tech mega caps underperforming, although Apple managed to stem its losses (+0.53%) after five days of decline. A notable outperformer was healthcare, led by a positive reaction to Eli Lilly & Co results the previous evening, which saw its shares jump up by +14.9%. Energy also gained (+0.49%), as oil moved higher during the day (WTI crude +1.20% to $82.92/bl). Comments by Ukraine’s President Zelensky warning that it could target Russian ports if Russia continues to block Ukrainian waters added to oil supply concerns.

In Fed speak, we heard from Philadelphia Fed President Harker. For someone generally perceived to be around the median on the FOMC (and a voter this year), his comments leaned dovish, noting that “we may be at the point where we can be patient and hold rates steady and let the monetary policy actions we have taken do their work”. He also spoke in favour of a soft landing path, saying that “I expect only a modest slowdown in economic activity to go along with a slow but sure disinflation”. Meanwhile, Richmond Fed President Thomas Barkin (non-voter) gave little colour on the policy front, saying he was “leaning toward waiting until September to decide” if another hike is appropriate. In terms of Fed fund expectations, the market continued to see a 34% chance of a hike across the next two meeting but moved to price slightly more cuts for 2024, with end-24 pricing down -2.6bps to 3.97%, its lowest in nearly three weeks.