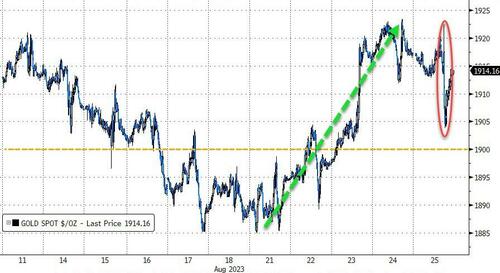

GOLD PRICE CLOSED: DOWN $6.05 TO $1912.60

SILVER PRICE CLOSED: UP $0.01 AT $24.19

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1913.60

Silver ACCESS CLOSE: 24.21

Shanghai Gold Benchmark Price

USD oz  AM1963.25

AM1963.25

PM1965.74

Historical SGE Fix

New York price at the time: $1917.00

premium $48.00

xxxxxxxxxxxxxxxxxx

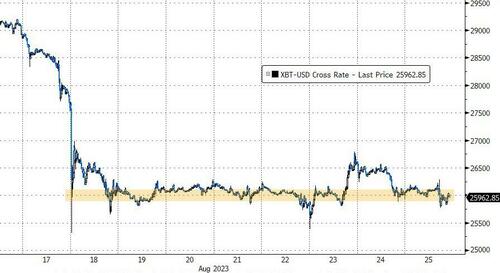

Bitcoin morning price:, $26,131 UP 75 Dollars

Bitcoin: afternoon price: $26,000 DOWN 56 dollars

Platinum price closing $946.40 UP $6.10

Palladium price; $1228.95 DOWN $7.75

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,603.44 DOWN .80 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1520.56 DOWN .80 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1772.54 DOWN 1.50 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: AUGUST 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,918.200000000 USD

INTENT DATE: 08/24/2023 DELIVERY DATE: 08/28/2023

FIRM ORG FIRM NAME ISSUED STOPPED

152 C DORMAN TRADING 12

435 H SCOTIA CAPITAL 302

624 H BOFA SECURITIES 310

657 C MORGAN STANLEY 2

905 C ADM 2

TOTAL: 314 314

MONTH TO DATE: 11,873

JPMorgan stopped 0 /319 contracts.

FOR AUGUST:

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2023. CONTRACT: 314 NOTICES FOR 31,400 OZ or 0.9766 TONNES

total notices so far: 11,873 contracts for 1,187,300 oz (36.930 tonnes)

FOR AUGUST:

SILVER NOTICES: 1 NOTICE(S) FILED FOR 5,000 OZ/

total number of notices filed so far this month : 952 for 4,760,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $6.05

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD/

INVENTORY RESTS AT 884.04 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 1 CENT AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.751 MILLION OZ FROM THE SLV// OZ OF SILVER FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 446.145 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 2651 CONTRACTS TO 136,150 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.16 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. TAS ISSUANCE WAS A HUGE SIZED 1485 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 1485 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.16). AND WERE SUCCESSFUL IN KNOCKING OF A FEW SILVER CONTRACTS AS WE HAD A STRONG SIZED LOSS OF 751 CONTRACTS ON BOTH EXCHANGES ALONG WITH SOME T.A.S.LIQUIDATION THROUGHOUT THE COMEX SESSION.

WE MUST HAVE HAD:

A HUMONGOUS ISSUANCE OF EXCHANGE FOR PHYSICALS( 1900 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.105 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 5,000 OZ QUEUE JUMP //NEW STANDING REMAINS AT 4.760 MILLION OZ + OUR NEW CRIMINAL 0 CONTRACTS OF EXCHANGE FOR RISK FOR NIL OZ + EXCHANGE FOR RISK//PRIOR = 8.88 MILLION OZ/// N: THUS NEW STANDING FOR SILVER IN OZ: 4.760 MILLION OZ + 8.88 MILLION EXCHANGE FOR RISK = 13.640 MILLION OZ/// // // HUGE SIZED COMEX OI LOSS/ HUGE SIZED EFP ISSUANCE/VI) MEGA HUMONGOUS SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE (1485 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -359 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTRACTS for 19 days, total 28,367 contracts: OR 141,835 MILLION OZ (1493 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 141.835 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 141.835 MILLION OZ (THIS MONTH IS GOING TO BE VERY STRONG

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2651 CONTRACTS WITH OUR LOSS IN PRICE OF $0.16 IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 1900 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 3.105 MILLION OZ FOLLOWED BY TODAY’S 5000 OZ QUEUE JUMP//NEW STANDING 4.760 MILLION OZ+ 8.88 MILLION OZ EXCHANGE FOR RISK// NEW TOTALS STANDING FOR SILVER: 13.64 MILLION OZ//// WE HAVE A SMALL LOSS OF 392 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A GIGANTIC 1485 CONTRACTS//SOME FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION . THE NEW TAS ISSUANCE THURSDAY NIGHT (1485) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 1 NOTICE(S) FILED TODAY FOR 5,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 407 CONTRACTS TO 435,344 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED: 1376 CONTRACTS

WE HAD A SMALL SIZED DECREASE IN COMEX OI ( 407 CONTRACTS) WITH OUR $0.65 GAIN IN PRICE//THURSDAY. WE ALSO HAD A RATHER SMALL INITIAL STANDING IN GOLD TONNAGE FOR AUGUST. AT 30.656 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 31,400 OZ QUEUE JUMP + PRIOR ISSUANCE OF EXCHANGE FOR RISK = (.684 TONNES) //NEW STANDING 37.440 TONNES + .684 EXCHANGE FOR RISK = 38.124/ + /A FAIR (AND CRIMINAL) ISSUANCE OF 654 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH OUR $0.65 GAIN IN PRICE WITH RESPECT TO THURSDAY’S TRADING.WE HAD A FAIR SIZED GAIN OF 2491 OI CONTRACTS (7.748 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2898 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 436,720

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2491 CONTRACTS WITH 407 CONTRACTS DECREASED AT THE COMEX// AND A FAIR 2898 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2491 CONTRACTS OR 7.748 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL 654 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2898 CONTRACTS) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (407) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 2491 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR JULY AT 30.656 TONNES FOLLOWED BY TODAY’S 31,400 OZ QUEUE JUMP //NEW STANDING 37,440 TONNES + .684 TONNES (EXCHANGE FOR RISK//PRIOR) NEW TOTALS: 38.124 TONNES/// 3) ZERO LONG LIQUIDATION WITH SOME TAS LIQUIDATION DURING THE COMEX SESSION //4) SMALL SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: SMALL T.A.S. ISSUANCE: 654 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUG :

TOTAL EFP CONTRACTS ISSUED: 55,134 CONTRACTS OR 5,513,400 OZ OR 171.48 TONNES IN 19 TRADING DAY(S) AND THUS AVERAGING: 2902 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAY(S) IN TONNES 171.48 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 171.48/3550 x 100% TONNES 4.84% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 171.48 TONNES (A STRONGER MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A GIGANTIC SIZED 2651 CONTRACTS OI TO 136,150 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A HUMONGOUS 1900 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 1900 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1900 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2651 CONTRACTS AND ADD TO THE 1900 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A STRONG LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 751 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 3.755 MILLION OZ

OCCURRED DESPITE OUR $0.16 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED DOWN 18.17 PTS OR 0.59% //Hang Seng CLOSED DOWN 255.79 PTS OR 1.40% /The Nikkei CLOSED DOWN 662.93 PTS OR 2.05% //Australia’s all ordinaries CLOSED DOWN .92 % /Chinese yuan (ONSHORE) closed DOWN 7.2828 /OFFSHORE CHINESE YUAN DOWN TO 7.2928 /Oil UP TO 80.12 dollars per barrel for WTI and BRENT UP AT 84.33 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 407 CONTRACTS UP TO 435,344 WITH OUR GAIN IN PRICE OF $0.65 ON THURSDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF AUGUST… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2898 EFP CONTRACTS WERE ISSUED: : DEC 2898 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2898 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR TOTAL OF 2491 CONTRACTS IN THAT 2898 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED LOSS OF 407 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $0.65//THURSDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT WAS A SMALL 664 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: AUGUST (38,124) ( ACTIVE MONTH)

TONNES),

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.440 TONNES (INCLUDING .6842 EXCHANGE FOR RISK)

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $0.65) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR GAIN OF 2491 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD SOME T.A.S. LIQUIDATION ON THE FRONT END OF YESTERDAY’S TRADING. THE T.A.S. ISSUED ON THURSDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 7.748 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST. (30.656 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 31,400 OZ QUEUE JUMP //NEW STANDING ADVANCES QUITE A BIT TO 37.440 TONNES + .6842 (PRIOR EXCHANGE FOR RISK) //NEW TOTAL 38.124 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $0.65.

WE HAD – REMOVED 1376 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 2491 CONTRACTS OR 249,100 OZ OR 7.748 TONNES.

Estimated gold volume today:// 163,899 awful

final gold volumes/yesterday 147,225 awful//speculators have left the gold arena

//AUGUST 25/ FOR THE AUGUST 2023 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 12,603.309 OZ Manfra 392 KILOBARS . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 314 notice(s) 31,400 OZ 0.9766 TONNES |

| No of oz to be served (notices) | 164 contracts 16,400 oz 0.510 TONNES |

| Total monthly oz gold served (contracts) so far this month | 11,873 notices 1,187,300 OZ 36,9300 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: NIL oz

customer deposits: 0

total customer deposits: nil oz

we had 1 customer withdrawals

i) Out of Manfra 12,603.309 oz (392 kilobars)

total withdrawals 12,603.309 oz

Adjustments; dealer to customer: 96,549.453 oz (3003 kilobars)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 478 contracts having LOST 5 contracts. We had 319 contracts filed

on Thursday, so we gained 314 contracts or an additional 31400 oz will stand at the comex,

Sept GAINED 517 contracts to 4030.

Oct GAINED 595 contracts to 32,599 contracts.

We had 314 contracts filed for today representing 31400 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 314 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2023. contract month,

we take the total number of notices filed so far for the month (11,873 x 100 oz ), to which we add the difference between the open interest for the front month of AUGUST (438 CONTRACT) minus the number of notices served upon today 314 x 100 oz per contract equals 1,203,700 OZ OR 37.440 TONNES the number of TONNES standing in this active month of AUGUST. + .684 TONNES EXCHANGE FOR RISK/prior = 38.124 tonnes

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (11,873) x 100 oz + (438) {OI for the front month} minus the number of notices served upon today (314) x 100 oz) which equals 1,203,700 oz standing OR 37.440 TONNES + .684 TONNES OF EXCHANGE FOR RISK/prior = 38.124 TONNES

TOTAL COMEX GOLD STANDING: 38.124 TONNES WHICH IS SMALL FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,071,097.121 OZ 64.41 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,608,596.142 OZ

TOTAL REGISTERED GOLD: 10,907,962,556 (339.28 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,700,633.586 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,836,865 OZ (REG GOLD- PLEDGED GOLD) 274.86 tonnes//dropping like a stone

END

SILVER/COMEX

AUGUST 25

//2023// THE AUGUST 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 938,933.795 oz Brinks CNT Delaware HSBC Loomis . |

| Deposits to the Dealer Inventory | 577,377.460 oz Brinks |

| Deposits to the Customer Inventory | nil |

| No of oz served today (contracts) | 1 CONTRACT(S) (5,000 OZ) |

| No of oz to be served (notices) | 0 contracts (NIL oz) |

| Total monthly oz silver served (contracts) | 952 Contracts (4,760,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: 1

i) Into Brinks: 577,377.460 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0 deposits customer account:

total customer deposits: nil oz

JPMorgan has a total silver weight: 139.276 million oz/276.160 million =50.36% of comex .//

Comex withdrawals 5

i) Out of Brinks 128,911.500 oz

ii) Out of CNT: 5028.210 oz

iii) Out of Delaware 4057.025 oz

iv) Out of HSBC 600,692.440 oz

v) Out of Loomis 200,244.600 oz

total: 938,933.795 oz

adjustments: 1 and a doozy: JPMorgan customer to dealer; 7,419,135.200 oz

TOTAL REGISTERED SILVER: 35.601 MILLION OZ//.TOTAL REG + ELIGIBLE. 276.160 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF AUGUST /2023 OI: 1 CONTRACTS HAVING GAINED 1 CONTRACT(S). WE HAD

0 NOTICES FILED ON THURSDAY SO WE GAINED 1 CONTRACT OR AN ADDITIONAL 5,000 OZ WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF AUGUST.

SEPT HAS A LOSS OF 11,363 CONTRACTS DOWN TO 27,720

OCT GAINED 26 CONTRACT TO STAND AT 638.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1 for 5,000 oz

Comex volumes// est. volume today 85,357 very strong

Comex volume: confirmed yesterday: 110,309 huge

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 952 x 5,000 oz = 4,760,000 oz

to which we add the difference between the open interest for the front month of AUGUST (1) and the number of notices served upon today 1x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST/2023 contract month: 952 (notices served so far) x 5000 oz + OI for the front month of AUGUST (1) – number of notices served upon today (1 )x 500 oz of silver standing for the AUGUST contract month equates to 4.760 million oz.+ 0.0 MILLION OZ EXCHANGE FOR RISK ISSUED TODAY+ 8.80 MILLION OZ EXCHANGE FOR RISK PRIOR//NEW TOTAL EXCHANGE FOR RISK: 8.88 MILLION OZ//NEW SILVER STANDING: 13.64 MILLION oz.

There are 35.601 million oz of registered silver.

Thus if we take today’s standing at 13.64 and add last month’s 30.9 million oz we have 44.540 million oz against only 35.601 million registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

AUGUST 25/WITH GOLD DOWN $6.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 884.04 TONNES

AUGUST 24/WITH GOLD UP $0.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //INVENTORY RESTS AT 884.91 TONNES

AUGUST 23/WITH GOLD UP $21.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 4.32 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 884.91 TONNES

AUGUST 22/WITH GOLD UP $2.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 0.87 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 889.23 TONNES

AUGUST 21/WITH GOLD UP $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.60 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 890.10 TONNES

AUGUST 18/WITH GOLD UP $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 6.92 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 887.50 TONNES

AUGUST 17/WITH GOLD DOWN $12.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 16/WITH GOLD DOWN $7.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 15/WITH GOLD DOWN $7,45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 895.87 TONNES

AUGUST 14/WITH GOLD DOWN $2.10 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.75 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 899.63 TONNES

AUGUST 11/WITH GOLD DOWN $2.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 903.31 TONNES

AUGUST 10/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 9/WITH GOLD DOWN $8.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 8/WITH GOLD DOWN $9.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES FORM THE GLD /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 7/WITH GOLD DOWN $5.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 906.00 TONNES

AUGUST 4/WITH GOLD UP $7.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.18 TONNES OF GOLD FROM THE GLD/// .///INVENTORY RESTS AT 906.00 TONNES

AUGUST 3/WITH GOLD DOWN $5.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 2/WITH GOLD DOWN $3.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.75 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 1/WITH GOLD DOWN $28.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 31/WITH GOLD UP $9.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 28/WITH GOLD UP $14.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 915,82 TONNES

JULY 27/WITH GOLD DOWN $21.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 917.26 TONNES

JULY 26/WITH GOLD UP $6.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 25/WITH GOLD UP $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 24/WITH GOLD DOWN $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.20 TONNES OF GOLD INTO THE GLD//: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 21/WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / .////INVENTORY RESTS AT 913.80 TONNES

JULY 20/WITH GOLD DOWN $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 913.80 TONNES

GLD INVENTORY: 884.04 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 25/WITH SILVER UP ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.751 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 446.145 MILLION OZ

AUGUST 24/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.651 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 448.896 MILLION OZ

AUGUST 23/WITH SILVER UP 94 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 826,000 OZ FROM THE SLV// /.////INVENTORY RESTS AT 450.547 MILLION OZ

AUGUST 22/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: /.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 21/WITH SILVER UP 59 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 917,0000 OZ FROM THE SLV//.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 18/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 17/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 16/WITH SILVER DOWN 13 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 15/WITH SILVER DOWN 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 14/WITH SILVER DOWN 3 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.459 MILLION OZ INTOTHE SLV/: //////INVENTORY RESTS AT 452.565 MILLION OZ

AUGUST 11/WITH SILVER DOWN 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.926 MILLION OZ INTOTHE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 452.106 MILLION OZ

AUGUST 10/WITH SILVER UP 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 9/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 8/WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 7/WITH SILVER DOWN 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 4/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.294 MILLION OZ FROM THE SLV// OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 3/WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 189,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.281 MILLION OZ

AUGUST 2/WITH SILVER DOWN 43 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 275,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.471 MILLION OZ

AUGUST 1/WITH SILVER DOWN 61 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 31/WITH SILVER UP 45 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 28/WITH SILVER UP 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.930 MILLION OZ

JULY 27/WITH SILVER DOWN 59 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ

JULY 26/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 25/WITH SILVER UP 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 826,000 OZ FROM THE SLV..////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 24/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 21/WITH SILVER DOWN 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.101 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 20/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.468 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 454.107 MILLION OZ/

CLOSING INVENTORY 446.145 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

Good commentary from Mike Maharrey on credit card debt

(Mike Maharrey)

More Americans Are Having A Hard Time Paying Their Big Credit Card Bills

FRIDAY, AUG 25, 2023 – 07:20 AM

Authored by Michael Maharrey via SchiffGold.com,

Since price inflation took off in the wake of pandemic-era stimulus, Americans have blown through their savings and run up their credit cards to make ends meet. Now they’re starting to have a hard time paying those credit card bills.

The number of Americans rolling credit card debt from month to month is now higher than the number of people paying their bills in full for the first time ever.

Americans are buried under more than $1 trillion in credit card debt. Credit card balances increased by $45 billion between April and June alone. Meanwhile, credit card interest rates have climbed to 20.6%. With both balances and interest expenses rising, more and more people are struggling to pay the bills.

According to a JD Power survey, 51% of US credit cardholders now carry revolving debt. To put that into perspective, from 2018 to 2022, the percentage of those rolling over balances ranged from 40% to 50%.

The average balance on a credit card was $2,573 in June. That represents a 6.5% increase from a year ago.

What we have not seen in the past is there are more revolvers than transactors,” JD Power managing director of payments intelligence John Cabell told Yahoo Finance. “It’s inflation, it’s savings dwindling, we’re also seeing rising interest rates, which makes it harder to pay off that balance because it’s getting bigger.”

The rising number of delinquent accounts also indicates people are having a hard time keeping up with credit card payments. The number of accounts past due by one cycle has increased 42.6% over the last two years. Delinquencies have crept up to the highest level since 2017.

The pandemic-era savings cushions are gone, the economy is shaky and consumers are leaning more heavily than ever on their credit cards to cover day-to-day expenses,” Cabell said. “Consumers are using their cards for a lot of everyday purchases. Grocery shopping is the lead purchase type that consumers say they are making.”

This raises an important question: what happens when consumers max out their credit cards?

There is some indication we may be close to that point.

In June, credit card spending suddenly fell off a cliff. According to the latest Federal Reserve data, revolving credit, primarily reflecting credit card debt, shrank by $600 million in June, a -0.6% decrease.

The big drop in credit card spending isn’t good news for the US economy. An ING economist called declining credit card spending “a troubling sign” given that consumer spending makes up two-thirds of the US economy.

With savings exhausted and credit cards maxed out, consumers have little choice but to stop spending.

This undercuts the notion that the Fed can slay price inflation while simultaneously bringing the economy to a “soft landing.”

The bottom line is that Americans turned to credit cards because they didn’t have any other way to make ends meet. People don’t run up their Visa balance month after month to buy groceries when they are in “very strong” financial shape.

The stimulus checks are long gone. Savings are being depleted. The average person had no choice but to pull out the plastic if they wanted to maintain their standard of living. Of course, this wasn’t a sustainable trajectory. A credit card has this inconvenient thing called a limit. We might be close to hitting it.

end

Ron Paul and Schiff gold on the growing national debt

(Ron Paul/SchiffGold)

Ron Paul: Growing National Debt Menaces Our Prosperity & Our Liberty

FRIDAY, AUG 25, 2023 – 06:30 AM

The national debt has climbed to a staggering $32.7 trillion. In just the first two months after Congress reached a deal and suspended the debt ceiling for two years, the national debt surged by $1.2 trillion.

And there is no end in sight.

The US government continues to run massive deficits month after month. In fact, the federal government is running budget shortfalls you would expect to see during a deep recession. With two months left, the fiscal 2023 budget deficit has already eclipsed the massive 2022 shortfall.

You might be thinking that with the spending cuts in the Fiscal Responsibility Act, Congress fixed this problem. But we live in an upside-down world where spending cuts mean spending keeps going up.

And we are on the cusp of another budget battle that will almost certainly mean even more spending coming down the pike.

Most people just shrug at these numbers, but as Ron Paul explains, the growing debt menaces both our prosperity and our liberty.

The following was originally published by the Ron Paul Institute. The opinions expressed are Ron Paul’s and do not necessarily reflect those of Peter Schiff or SchiffGold.

Congress’ top priority this fall will be passing legislation funding the government and avoiding a “shutdown.” As of this writing, it appears unlikely that the Republican-controlled House will be able to make a deal with President Biden and the Senate Democrats on a long-term spending bill. Instead, they will likely pass a short-term funding bill to give themselves more time to reach an agreement on a longer-term bill.

Any bipartisan agreement is unlikely to reduce government spending or begin to pay down, or stop the growth of, the over $32 trillion national debt, which the Congressional Budget Office projects will grow by at least $115 trillion over the next thirty years. Instead, Congress and the administration will continue to pretend they are addressing the spending problem by “reducing the projected rate of spending growth,” and other gimmicks.

The sad fact is both parties, along with a majority of the American people, are addicted to welfare-warfare spending. What little resistance there is to big government within the Republican party is likely to be further weakened by the rise of a new form of “conservatism” that advocates the use of government power—including deficit spending and increasing the federal debt — to advance conservative political and social goals.

The failure to take seriously the threat to the American economy caused by reckless federal spending is illustrated by the reactions to the credit rating agency Fitch’s downgrade of the US government’s credit rating. Instead of treating it as a wake-up call, government officials like current Treasury Secretary (and former Federal Reserve Chair) Janet Yellen dismissed the downgrade as “arbitrary and based on outdated data.”

One reason Yellen and others may be so blasé about the federal debt is that they believe the Federal Reserve will bail the government out by holding interest rates low enough to keep the federal government’s interest payments to manageable levels.

This is why, even though the Fed has been raising interest rates, the rates remain well below what they would likely be in a free market. However, the Fed knows it cannot go back to keeping rates at or below zero without causing price inflation.

Therefore the Fed will likely continue to raise rates for the next several months. The Fed will likely pause its rate increase next year in the hope of boosting economic activity to help President Biden’s reelection campaign. Former President Trump gave Powell an additional incentive to keep rates low next year by promising not to re-appoint him if he returns to the Oval Office.

Despite the Fed’s repeated interest rate increases, Americans are paying an average of $709 more per month for basic living expenses than they were two years ago. This is why credit card debt is over one trillion dollars. Adding more in private and public debt will increase pressure on the Fed to “do the impossible” – keep interest rates relatively low without creating price inflation. Eventually, the Fed-created debt-based economy will collapse as the dollar loses its reserve currency status. This will increase political divisions and may even lead to political violence.

Those of us who know the truth must make preparations to ensure the safety of ourselves and our loved ones and do all we can to spread the ideas of liberty. Creating a critical mass of people to reject the false promises of the welfare-warfare state is the only way to regain liberty without first suffering political and economic upheaval.

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

JOHN RUBINO..

The big news: Saudi Arabia and UAE joining the BRICS. This would kill the dollar

(John Rubino)

BRICS Summit Ends With a Bang — And a Tease

Saudi Arabia, UAE, and Iran join the bloc. So much for the Petrodollar

| JOHN RUBINOAUG 24 |

In a nice bit of misdirection, the BRICS countries distracted the West with hints of a “gold-backed currency” at their August 22 – 24 meeting. Then, while everyone was looking over there, they did something potentially even bigger by admitting Saudi Arabia and the United Arab Emirates as members, with Iran, Argentina, Egypt, and Ethiopia scheduled for the following year.

Along the way, they of course threatened to bypass the dollar by cutting more bi-lateral trade deals:

“The objective, irreversible process of de-dollarization of our economic ties is gaining momentum, and efforts are being made to work out effective mechanisms for mutual settlements and monetary and financial control,” Putin said. “As a result, the share of the dollar in export-import transactions within the BRICS is declining: last year it amounted to only 28.7 percent.”

The former president of Nigeria reportedly got a standing ovation for this:

I want to buy from India. Why should I use dollars? It’s a payment and settlement system that will allow me to buy whatever I want to buy in India, whatever I want to buy in Brazil, without looking for dollars.

And they tossed off another currency tease:

“The creation of a currency for commercial transactions and investments between BRICS members improves our payment conditions and reduces our vulnerabilities,” said Brazilian President Luiz Inacio Lula da Silva, who has been the most vocal proponent of the common currency project among the five leaders.

Going forward, the one BRICS certainty is that the world’s second and third-largest oil producers (Saudi Arabia and Russia) will be operating at least partially outside the dollar-centric financial system and within an aspirationally dollar-free system.

In purchasing power parity terms, the BRICS now account for a bigger share of global GDP than the G7 countries.

Geographically, they control a big part of the total landmass:

They also represent a significant share of the world’s population (led by people who are, for now, mostly unfamiliar to Westerners):

Meanwhile, the 2024 BRICS chairmanship will pass to Russia, which guarantees a lot of trash-talk before, during, and after the next meeting.

International bank ING was quick to post an analysis of the “Saudi surprise”. Here’s an excerpt:

BRICS expansion: The Saudi surprise adds momentum to the de-dollarisation debate

The big surprise from the BRICS summit in South Africa is that Saudi Arabia has been invited to join the group of major emerging countries. And that’s adding fresh impetus to the de-dollarisation debate, which is a potential challenge to the dominance of the US dollar in global trade

Accelerated expansion

We knew that the expansion of the BRICS grouping was top of the agenda at this 15th BRICS summit in South Africa. We had thought that the United Arab Emirates (UAE), Egypt and Bangladesh would be invited to join given they were already part of the BRICS’s New Development Bank. In the end, it was not only the UAE and Egypt invited to join, but also Saudi Arabia, Iran, Argentina and Ethiopia.

The biggest surprise is Saudi Arabia. It had been rumoured that the country wanted to enter the group, but the geo-political situation – given tense relations with the West – raised doubts about whether Saudi Arabia would formalise political and economic ties with the BRICS.

Together with fellow oil and gas exporters Iran and the UAE, the admission of Saudi Arabia to the BRICS grouping will inevitably focus debate on the use of non-dollar currencies in trade. As an aside, at this conference, Brazil proposed to Argentina that Brazil would guarantee Argentine payments for Brazilian exports in renminbi. This is perhaps a reflection of Argentina’s ability to tap renminbi swap lines and expose the scarcity of dollars. Additionally, Argentina remains in dire financial straits as it struggles to source hard currency to service largely dollar-denominated debt.Saudi switch to non-dollar invoicing?

The recently-announced news that a handful of countries, including Saudi Arabia, the UAE and Iran have been invited to join BRICS increases the energy dominance of the group, specifically when it comes to crude oil. As it stands, BRICS members make up around 20% of global oil output. The addition of Saudi, the UAE and Iran would see the BRICS group make up almost 42% of global crude oil output.

As for Saudi Arabia, it is the largest crude oil exporter. In 2022, the Kingdom exported around 7.3m b/d of crude oil, which makes up a little more than 17% of global crude oil exports. The bulk of these exports (76%) go to Asia, of which 35% go to BRICS members China and India.

Therefore, given the ambitions of the BRICS to de-dollarise, there certainly will be increased speculation that this latest move could see Saudi Arabia increasingly switching to non-dollar-denominated currencies for oil trade. To some, it might make sense that Saudi Arabia starts accepting the Chinese yuan and Indian rupee from China and India for its crude oil. And there has been plenty of noise and reportedly discussions between Saudi Arabia and China on the matter. However, up until now, it does not appear as though the Saudis have been willing. The fact that the Saudi riyal is pegged to the US dollar might mean that the Saudis are reluctant to start making the shift.

However, where we have seen a shift is obviously in relation to Iran. Given sanctions, any buyers of its crude will be paying in non-dollar currencies. China is the largest buyer of Iranian oil at the moment and is reportedly paying in yuan.

Some thoughts

None of this should come as a surprise. Numerous mistakes by the West — led by the US — have led countries with half the global population and 40+% of GDP to want out of the current system. Our two biggest mistakes are:

- Accumulating insane amounts of debt that can only be resolved through a brutal financial crisis and global currency reset. What sane developing country would volunteer for such a thing?

- Weaponizing the world’s reserve currency and related systems to the point that emerging nations see themselves as either current or future victims of US predation. Again, who wants to sit around waiting for the inevitable sanctions/asset theft/CIA coup?

The BRICS are, in short, a threat made in the USA. But today it went global.

END

3,Chris Powell of GATA provides to us very important physical commentaries

Why the dollar scheme ends and the new BRICS currency will begin shortly.

(Ambrose Evans Pritchard)

Ambrose Evans-Pritchard: The BRICs currency ignores the traumatic lessons of the half-baked euro

Submitted by admin on Thu, 2023-08-24 19:45Section: Daily Dispatches

By Ambrose Evans-Pritchard

The Telegraph, London

Thursday, August 24, 2023

Dollar hegemony has become a curse for the global economy. It serves the interests of no country, least of all the United States itself.

The frenetic monetary lurches of the U.S. Federal Reserve are transmitted worldwide in disruptive cycles of dollar liquidity, and amplified through the $12 trillion market for offshore dollar loans and a vast nexus of debt contracts linked to U.S. borrowing costs.

When the Fed giveth by means of zero rates and money creation (QE), it floods the international system with cheap funding and sets off destabilising credit booms.

When the Fed taketh by driving real rates through the roof and destroying money (QT), it drains global liquidity and tortures dollar debtors everywhere. It overwhelms other central banks trying to navigate the reefs — even in Europe or China — and imposes a de-facto monetary policy on countries whether they want it or not.

The effects can be violently pro-cyclical and malign. Ultimately it “blows back” into the U.S. economy. That is the risk we face now as the Fed pushes half the world into a credit crunch by the most aggressive monetary tightening in 40 years.

We badly need other currencies to step up to the plate. None is fit for purpose. As the saying goes, Europe is a museum; Japan is a nursing home; and China is a prison. …

… For the remainder of the analysis:

END

Another metal trader gets dinged with rocks instead of nickel

(Bloomberg)

Another metals trader says it has been hit by a nickel fraud

Submitted by admin on Thu, 2023-08-24 10:27Section: Daily Dispatches

By Archie Hunter, Alfred Cang, and Jonathan Browning

Bloomberg News

Thursday, August 24, 2023

Another trading house has been stung after buying a cargo supposedly containing nickel that turned out to be full of near-worthless rubble.

The latest example, detailed in lawsuits in London and Singapore, is separate from the $600 million alleged fraud against Trafigura Group that shocked the trading industry earlier this year, but it involves several of the same companies.

The revelation that the problem of non-existent nickel is more widespread will be another blow to confidence in the scandal-prone metals trading industry.

The Trafigura case has spawned several lawsuits, while in March the London Metal Exchange discovered that 54 tons of “nickel” held at a warehouse in Rotterdam and owned by JPMorgan Chase & Co. was actually just bags of stones. …

… For the remainder of the report:

END

END

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES

Live from the vault: Episode 137

Episode 137

1 day ago

No Coincidence – Indonesian VP Endorses Sharia Gold Launch During BRICS Summit

In this week’s episode of Live from the Vault, Andrew Maguire covers the latest developments on the intensifying paper versus physical battle and the ongoing central bank gold-buying sprees as Kinesis powers gold adoption in Indonesia.

The precious metals expert and whistleblower provides an update for silver stackers before revealing the global ramifications of the BRICS summit and their upcoming commodity-backed currency poised to compete with the US dollar.

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2828

OFFSHORE YUAN: UP TO 7.2928

SHANGHAI CLOSED DOWN 18.17 PTS OR 0.59%

HANG SENG CLOSED DOWN 255.79 PTS OR 1.40%

2. Nikkei closed DOWN 662.93 OR 2.05%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 103.98 EURO RISES TO 1.0803 UP 5 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.650 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 146.01/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ON SHORE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.5619***/Italian 10 Yr bond yield UP to 4.235*** /SPAIN 10 YR BOND YIELD RISES TO 3.590…**

3i Greek 10 year bond yield RISES TO 3.842

3j Gold at $1918.60 silver at: 24.22 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 22 /100 roubles/dollar; ROUBLE AT 94.65//

3m oil into the 80 dollar handle for WTI and 84 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 146.01// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.650% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8856 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9568well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.252 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.313 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 5.031 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.46…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 8 BASIS PTS AT 4.511

end

2.a Overnight: Newsquawk and Zero hedge:

Futures Climb Tentatively Ahead Of Powell’s J-Hole Speech

FRIDAY, AUG 25, 2023 – 08:12 AM

Futures are slightly higher ahead of today’s Jackson Hole main event, with tech flat following yesterday’s violent Nvidia “sell the news” dump even as yields ticked modestly higher again. At 8:00 am, S&P futures were higher by 0.3% on the day, trading just around 4,400 and paring a portion of Thursday’s session losses while Nasdaq 100 futures are flat after the index sank more than 2% yesterday. Europe’s Stoxx 50 rises 0.6%, extending its first weekly advance in four as commodity shares led gains as oil and iron ore prices climbed; Asian equities slumped Friday, paring their first weekly gain since July, as Chinese stocks slid and technology shares were sold off. Quality is leading, Growth is lagging; Cyclicals flat vs. Defensives.

Powell kicks off 10:05 am ET and this year’s theme “structural changes in the global economy” appears to have roiled bond markets with some thinking >5% Fed Funds is the new normal or perhaps a higher inflation target. The bond market reaction may result in lower yields as we turn the page to Sept as JPM does not think Powell tips his hand on future policy at this event. Treasury yields ticked higher, with two-year notes holding above 5%. The dollar was little changed; commodities are mixed with Energy leading and metals lagging.

In premarket trading, Digital World Acquisition Corp. the special-purpose acquisition company that’s seeking to take Donald Trump’s media company public, falls 4.4% after the former President posted his own mug shot in a return to Elon Musk’s X. Affirm Holdings jumped 7.5% after fourth-quarter revenue at the financial technology company beat expectations, helped by an increase in transactions on its platforms. Here are some other notable premarket movers:

- Ardelyx rises 2.8% after the biotech was upgraded to overweight from neutral at Cantor Fitzgerald, saying that the Street is underappreciating the peak sales potential of Xphozah, Ardelyx’s flagship drug.

- Clarivate Plc dips 1.8% after RBC Capital Markets downgraded the information services company to sector perform from outperform.

- Domo (DOMO) tumbles 33% after the application software company cut its full-year forecast. Cowen cut its rating on the firm in the wake of the report, citing the significantly lower guidance.

- Hawaiian Electric (HE) sinks 21% as the utility’s woes deepened following the wildfires in Maui, suspending its dividend while S&P cut its credit rating.

- Marvell Technology (MRVL) falls 3.1% after the semiconductor company gave a forecast for the current quarter that was largely line with Wall Street estimates. Analysts noted that its AI business was continuing to grow while KeyBanc said its networking and consumer segments were still weak.

- Olaplex (OLPX) drops 5.0% as Piper Sandler cuts its recommendation on the hair-care company to underweight from neutral, citing margin pressures.

Equities have struggled for direction this week, gaining strongly one day only to wipe out the advance the next, as the focus swung from Nvidia earnings to the trajectory of interest rates. As previewed yesterday, Powell, who is scheduled to deliver a speech at 10:05 a.m. Washington time, will likely outline how officials will assess whether rates should go higher and determine when it’s time to start cutting them.

“There could be another phase of uncertainty and a broad-based selloff is possible depending on the magnitude of the hawkishness” at Jackson Hole, said Carlos von Hardenberg, portfolio manager at Mobius Capital Partners. “But the market is differentiating relatively radically between companies that are in the pole position to show very strong earnings growth in the near and medium term.”

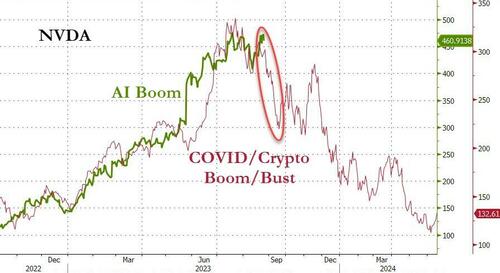

The effects of higher-for-longer interest rates will overshadow the buzz around artificial intelligence, spelling trouble for tech stocks, according to Bank of America Corp. strategists. On Thursday, even a blowout sales forecast from Nvidia wasn’t enough to stem the Nasdaq 100’s slump amid a rise in bond yields.

Elsewhere, China eased its mortgage policies further in a push to support its economy, although the boost to stocks on the mainland from the news proved to last just a few minutes.

Europe’s Stoxx 600 is up 0.3% and set to log its first weekly rise in four. Mining, retail and energy stocks are leading gains while health care creates a drag. Here are the biggest European movers:

- Tesco shares gain as much as 1.9%, among the top performers in the FTSE 100 Index, after Barclays lifted its price target on the UK grocer and said there’s scope for a guidance boost.

- JCDecaux shares gain as much as 4.5%, the most since May, after Deutsche Bank raises the advertising company to buy from hold, saying risks related to the firm’s China exposure may have been priced in.

- Aston Martin shares rise as much as 5.7% after Jefferies raised its recommendation on the luxury sports carmaker to buy from hold, saying it sees scope for the company to build on the re-positioning begun by Chairman Lawrence Stroll.

- European tech stocks miss out on any artificial intelligence buzz generated by Nvidia’s blowout sales forecasts, as they languish on the fringes of the global AI race.

- Watches of Switzerland plunges as much as 29%, the most on record, after Rolex said it plans to buy luxury retailer Bucherer.

- CMC Markets shares drop as much as 20% at the open to their lowest level in nearly four years after the online trading platform said in a trading update that its annual net operating income would be lower than last year due to “subdued” market conditions.

Earlier in the session, Asian equities slumped paring their first weekly gain since July, as Chinese stocks slid and technology shares were sold off on risk aversion ahead of a speech from Federal Reserve Chair Jerome Powell. The MSCI Asia Pacific Index declined as much as 1.2%, trimming its advance for the week to 0.6%, with chipmakers TSMC and Samsung among the biggest drags. A gauge off Chinese technology stocks in Hong Kong slumped more than 2% after Meituan warned of slower orders, while NetEase dropped on a revenue miss as the widespread tech selling clouded over their earnings results, while losses in the mainland were limited following a firm liquidity injection by the PBoC and after the securities regulator met with financial industry firms and urged longer-term funds to help steady the stock market.

- Japan’s Nikkei 225 fell by as much as 2% after it gapped below 32,000 with tech stocks hit by the broad sector recoil.

- ASX 200 was pressured by heavy losses in tech and the commodity sectors, while consumer stocks showed some resilience after stronger earnings from Wesfarmers.

- Indian markets closed at their lowest level since June 30 on Friday, marking their fifth straight week of losses, on broad risk aversion ahead of Federal Reserve Chair Jerome Powell’s speech. The S&P BSE Sensex fell 0.6% to 64,886.51 in Mumbai, while the NSE Nifty 50 Index declined by the same magnitude.

Risk appetite in Asia remains fragile amid concerns on China’s economy and expectations of higher-for-longer US interest rates. After a tech-led rally Thursday on Nvidia’s strong results, investor attention has shifted to the Jackson Hole Symposium where Powell’s speech may provide clues on the Fed’s policy path.

In FX, the greenback is supported with the Dollar Index rising 0.2% to its highest since the start of June.

- The euro extends recent losses and heads for its sixth weekly decline. EUR/USD drops as much as 0.4% to 1.0766, breaches 200-DMA support on an intraday basis; technically, there is little support until 1.0635, the May lows

- USD/JPY pares a 0.3% advance to trade 0.1% higher on the day at 146.04; the pair heads for its fourth weekly advance for the first time since Feb.

- GBP/USD down 0.3% to 1.2560, lowest since June 13; the pound was sold for dollars by momentum funds as concerns of a hawkish Powell spurred broad greenback strength, according to traders

In rates, treasuries were slightly cheaper across the curve, following losses seen in core European rates over the early London session. 10-year TSY yields are around 4.245%, cheaper by 1bp on the day with bunds and gilts lagging by additional 3bp and 1.5bp in the sector; belly slightly lags on the Treasuries curve, flattening 5s30s spread by 1.2bp vs. Thursday close. Treasury futures are near lows of the day, adding to losses seen Thursday although price action broadly remains within Wednesday’s session range. US session focus is on Jackson Hole economic policy symposium, where Fed Chair Powell is expected to speak at 10:05am New York. Investors will be focused on Fed speakers at Jackson Hole and the FOMC’s view on the long-term neutral interest rate, which has been in focus extensively this week

In commodities, iron ore was set for its biggest weekly gain since June ahead of China’s traditional peak season for construction activity from next month. Oil trimmed a weekly loss.

Bitcoin is contained in narrow parameters with specific catalysts light as we await Central Bank impetus from the ECB and Fed. JPM sees limited downside for crypto markets in the near term, via CoinDesk.

To the day ahead now, and there are several central bank speakers today, including Fed Chair Powell, the Fed’s Harker, Mester and Goolsbee, along with ECB President Lagarde. Data releases include the Germany’s Ifo business climate indicator for August, and in the US we’ll get the University of Michigan’s final consumer sentiment index for August.

Market Snapshot

- S&P 500 futures up 0.2% to 4,396.25

- STOXX Europe 600 up 0.3% to 452.93

- German 10Y yield little changed at 2.55%

- Euro down 0.3% to $1.0782

- MXAP down 1.3% to 158.38

- MXAPJ down 1.2% to 498.03

- Nikkei down 2.1% to 31,624.28

- Topix down 0.9% to 2,266.40

- Hang Seng Index down 1.4% to 17,956.38

- Shanghai Composite down 0.6% to 3,064.08

- Sensex down 0.4% to 64,978.04

- Australia S&P/ASX 200 down 0.9% to 7,115.18

- Kospi down 0.7% to 2,519.14

- Brent Futures up 1.1% to $84.27/bbl

- Gold spot down 0.2% to $1,913.99

- U.S. Dollar Index up 0.20% to 104.20

Top Overnight News from Bloomberg

- An abstract interest-rate metric is dominating discussions across trading desks ahead of the Jackson Hole symposium, with investors wondering if Federal Reserve Chair Jerome Powell will weigh in, and bracing for further declines in US Treasuries if he does.

- European Central Bank Governing Council member Joachim Nagel said that he’s not convinced inflation is under control enough for a halt in interest rate hikes, with his decision hinging on additional data in the coming weeks.

- Business confidence in Germany took another hit in August, despite the economy just exiting a recession in the second quarter.

- The yen has eclipsed bond market liquidity as a potential catalyst for a further adjustment to the Bank of Japan’s monetary policy.

- American politicians are keener than ever to juice the economy with government cash, a shift that’s already helping to drive up borrowing costs and looks likely to keep them high long after the inflation emergency is over.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded lower following the weak handover from global counterparts after the Nvidia-related euphoria wore off and with markets bracing for Fed Chair Powell’s speech at Jackson Hole. ASX 200 was pressured by heavy losses in tech and the commodity sectors, while consumer stocks showed some resilience after stronger earnings from Wesfarmers. Nikkei 225 fell by as much as 2% after it gapped below 32,000 with tech stocks hit by the broad sector recoil. Hang Seng and Shanghai Comp declined with NetEase and Meituan among the worst performers in Hong Kong as the widespread tech selling clouded over their earnings results, while losses in the mainland were limited following a firm liquidity injection by the PBoC and after the securities regulator met with financial industry firms and urged longer-term funds to help steady the stock market.

Top Asian News

- PBoC was said to ask some banks to limit southbound bond connect investments with the guidance said to be aimed at outflows and limiting yuan offshore supply, according to Reuters sources.

- China reportedly plans to cut stamp duty on domestic stock trading by up to 50%, via Reuters citing sources; could be announced as soon as Friday.

- China is issuing nationwide guidance on the easing of mortgage rules; issuing detailed rules for conditions to qualify for first-home mortgage rates.

- Reuters polls shows 55% of economists say the BoJ will not start unwinding ultra-easy policy until at least July 2024, while 73% of economists think BoJ will end YCC control in 2024 (prev. 50%) and 41% expect BoJ to end NIRP in 2024 (prev. 54%)

European bourses are modestly firmer, Euro Stoxx 50 +0.4%, with the overall tone a tentative one ahead of Jackson Hole. Limited equity reaction was seen to German Ifo, GDP revisions or an ECB sources piece that had a dovish headline message. Sectors are primarily in the green with outperformance in Energy and Basic Resources while Health Care languishes in the red. Stateside, futures are more contained than their above peers but retain a similar positive skew, ES +0.2% as attention turns to Chair Powell.

Top European News

- ECB’s Nagel it is much too early to think about a rate-hike pause, while he stated they have to be stubborn on policy and more stubborn than inflation, according to an interview with Bloomberg TV.

- ECB’s Vujcic said the Eurozone economy is basically stagnating and inflation has most likely peaked, while he added that it is to be seen whether rates are restrictive enough, according to an interview on Bloomberg TV.

- Momentum is growing for a pause in ECB rate hikes as recession fears increase, debate still open, via Reuters citing sources; Policymakers agree that any decision to pause would need to make clear the job is not done and future hikes could still be needed. Several of the sources said they saw chances evenly split between hike/pause, smaller number saw a pause as more likely. Re. August Flash PMIs, several policymakers cautioned against reading too much into such surveys as there is a growing gap between hard data and sentiment readings. All sources agreed that even in the scenario of a pause, ECB would need to make clear its job was not done and more policy tightening could still be needed. Those arguing for tightening want solid evidence that inflation is heading back to target without the risk of getting stuck above 2%, say a meaningful decline in underlying inflation would be needed for a pause.

- UK Ofgem Energy Price Cap (GBP): 1923 (prev. 2074), -7.3% for dual-fuel households, for the October-December. The first time the average energy bill has gone below 2k since April 2022.

FX

- Greenback elevated before Fed Chair Powell emerges from Jackson Hole with the DXY holding above 104.000.

- Euro lags after losing 200 DMA and 1.0800+ status vs Dollar even before dovish-leaning ECB sources and downbeat German Ifo survey.

- Yen back below 146.00 as yields remain lofty and Tokyo CPI metrics come in mostly softer than expected.

- Kiwi faces stronger AUD/NZD headwinds as Aussie derives support from base metals.

- NZD/USD towards the bottom of the 0.5928-0.5895 range and AUD/USD vice-versa between 0.6427-03 parameters.

- Pound flounders sub-1.2600 against Buck irrespective of improvement in UK consumer confidence per GfK.

- PBoC set USD/CNY mid-point at 7.1883 vs exp. 7.2923 (prev. 7.1886)

Fixed Income

- Deeper retreat in debt before Fed Chair Powell and ECB President Lagarde deliver remarks at the JH symposium.

- Bunds back down towards 132.20 low from 132.57 peak set post-ECB sources and Ifo survey.

- Gilts and T-note both depressed within 94.48-24 and 109-20/12+ respective ranges.

- BTPs remain under par and sub-115.00 in the wake of a mixed 2-year Italian auction.

Commodities

- Crude benchmarks are trending higher despite the modest USD upside and tentative tone overall, action which comes in relatively limited specific fundamentals as we await developments around Australian LNG.

- Currently, the benchmarks are towards session highs with WTI Oct’23 above USD 80.00/bbl and Brent Oct’23 around USD 84.50/bbl.

- Spot gold is little changed given the incrementally firmer USD and tentative tone overall while spot silver has resumed its advance with technicals assisting.

- Base metals benefit from the latest support measures out of China, targeting the property sector.

- Offshore Alliance members at Woodside Energy (WDS AT) endorsed the in-principle agreement.

- Chevron (CVX) says it has not received any notice of intent to strike from Australian LNG unions.

- China’s Industry Ministry said it aims to increase the output of 10 non-ferrous metals by 5% in 2023-2024 and will promote companies cooperating in overseas iron ore exploration, especially in neighbouring countries.

- Trader sources cited by Reuters suggest rising prices of a popular Russian crude sold in China are set to peak soon as independent refiners are likely to switch to cheaper Iranian crude as Iran boosts exports to four-and-a-half-year highs.

Geopolitics

- White House said US President Biden and Ukrainian President Zelensky discussed the start of training Ukrainian fighter pilots and the expedited approval of other nations to transfer their F-16s, according to Reuters.

- Russian military said it intercepted a Ukrainian S-200 missile over Russian territory, while the Russian Defence Ministry said a Ukrainian attack on Crimea involving 42 drones was thwarted, according to Reuters and AFP.

- Taiwan Defence Ministry said 13 Chinese military aircraft entered Taiwan’s ‘response zone’ and 5 Chinese naval ships engaged in combat readiness patrols on Friday morning, according to Reuters.

US Event Calendar

- 10:00: Aug. U. of Mich. Sentiment, est. 71.2, prior 71.2

- Current Conditions, prior 77.4

- Expectations, prior 67.3

- 1 Yr Inflation, est. 3.3%, prior 3.3%

- 5-10 Yr Inflation, est. 2.9%, prior 2.9%

- 11:00: Aug. Kansas City Fed Services Activ, prior -1

Central Banks

- 10:05: Fed’s Powell Speaks at Jackson Hole Economic Policy Symposium

- 11:00: Fed’s Harker Interview With Bloomberg TV

- 11:30: Fed’s Mester Speaks on CNBC

- 11:30: Fed’s Harker Interview With Yahoo Finance Live

- 12:30: Fed’s Goolsbee Speaks on CNBC

- 14:00: Fed’s Goolsbee Speaks on Bloomberg TV

- 14:30: Fed’s Mester Speaks on Bloomberg TV

DB’s Henry Allen concludes the overnight wrap