GOLD PRICE CLOSED: UP $17.05 TO $1936.95

SILVER PRICE CLOSED: UP $0.49 AT $24.71

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1937.45

Silver ACCESS CLOSE: 24.74

Shanghai Gold Benchmark Price

USD oz  AM1960.45

AM1960.45

PM1957.97

Historical SGE Fix

New York price at the time: $1918.00

premium $40.00

xxxxxxxxxxxxxxxxxx

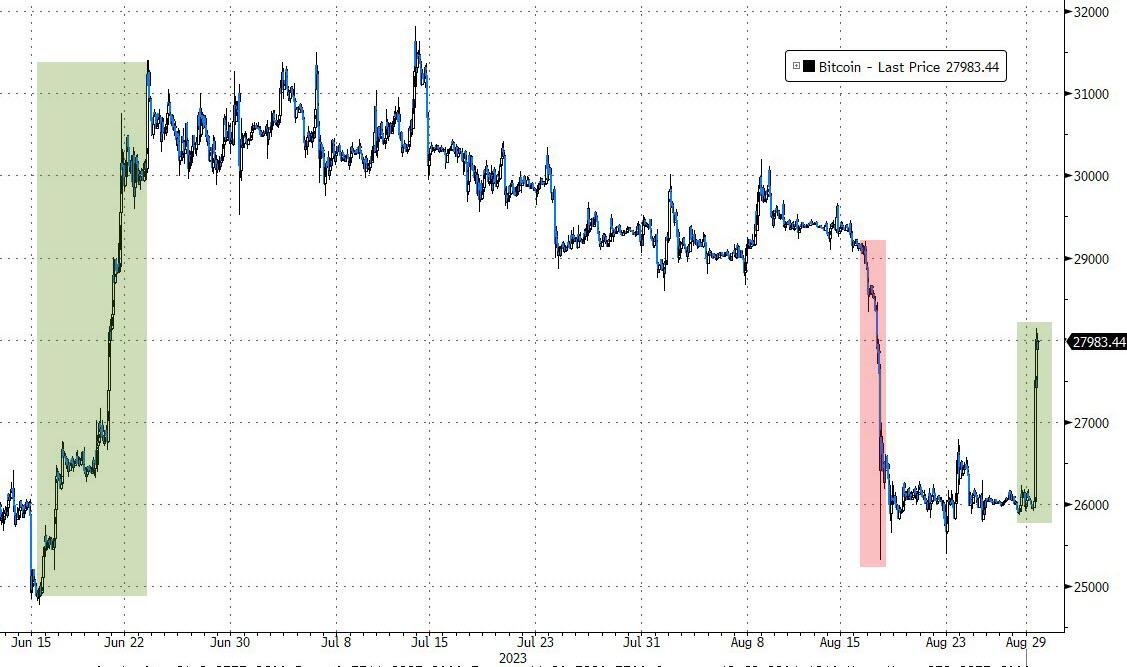

Bitcoin morning price:, $26,038 DOWN 70 Dollars

Bitcoin: afternoon price: $27,952 UP 1844 dollars

Platinum price closing $983,40 UP $15.60

Palladium price; $1257.70 DOWN $1.15

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,626.26 UP 15.25 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 131,72 UP 7.25 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1780.06 UP 5.32 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: AUGUST 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,917.900000000 USD

INTENT DATE: 08/28/2023 DELIVERY DATE: 08/30/2023

FIRM ORG FIRM NAME ISSUED STOPPED

435 H SCOTIA CAPITAL 20

624 H BOFA SECURITIES 57

661 C JP MORGAN 82

686 C STONEX FINANCIA 5

TOTAL: 82 82

MONTH TO DATE: 12,118

JPMorgan stopped 0 /82 contracts.

FOR AUGUST:

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2023. CONTRACT: 82 NOTICES FOR 8200 OZ or 0.2550 TONNES

total notices so far: 12,118 contracts for 1,211,800 oz (37.6992 tonnes)

FOR AUGUST:

SILVER NOTICES: 0 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month : 954 for 4,770,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $17.05

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/HUGE CHANGES IN GOLD INVENTORY AT THE GLD: /A DEPOSIT OF 2.60 TONNES OF GOLD INTO THE GLD.

INVENTORY RESTS AT 886,64 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 49 CENTS AT THE SLV// SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 183,000 OZ SILVER INTO THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 445.044 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 2019 CONTRACTS TO 133,507 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.03 GAIN IN SILVER PRICING AT THE COMEX ON MONDAY. TAS ISSUANCE WAS A FAIR SIZED 533 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 513 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.03). BUT WERE SUCCESSFUL IN KNOCKING SOME SILVER CONTRACTS AS WE HAD A STRONG SIZED LOSS OF 1162 CONTRACTS ON BOTH EXCHANGES ALONG WITH HUGE T.A.S.LIQUIDATION THROUGHOUT THE COMEX SESSION.

WE MUST HAVE HAD:

A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS( 482 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.105 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S NIL OZ QUEUE JUMP //NEW STANDING REMAINS AT 4.770 MILLION OZ + OUR NEW CRIMINAL 0 CONTRACTS OF EXCHANGE FOR RISK FOR 0 MILLION OZ + EXCHANGE FOR RISK//PRIOR 9.88 MILLION OZ/// : THUS NEW STANDING FOR SILVER IN OZ: 4.770 MILLION OZ + 9.88 MILLION EXCHANGE FOR RISK = 14.650 MILLION OZ/// // // HUGE SIZED COMEX OI LOSS/ FAIR SIZED EFP ISSUANCE/VI) FAIR SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE (533 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL 375 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTRACTS for 21 days, total 29,979 contracts: OR 149.895 MILLION OZ (1427 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 149.895 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 149.845 MILLION OZ (THIS MONTH IS GOING TO BE HUGE

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2019 CONTRACTS DESPITE OUR GAIN IN PRICE OF $0.03 IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR EFP ISSUANCE CONTRACTS: 482 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 3.105 MILLION OZ FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP//NEW STANDING 4.770 MILLION OZ+ 0 MILLION EX. FOR RISK //NEW TOTAL EXCH. FOR RISK 9.88 MILLION OZ EXCHANGE FOR RISK// NEW TOTALS STANDING FOR SILVER: 14.65 MILLION OZ//// WE HAVE A STRONG LOSS OF 1537 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A FAIR 533 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION WHICH EXPLAINS THE HUGE OI LOSS COMEX . THE NEW TAS ISSUANCE MONDAY NIGHT (533) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 0 NOTICE(S) FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 1078 CONTRACTS TO 433,537 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED: 994 CONTRACTS

WE HAD A SMALL SIZED DECREASE IN COMEX OI ( 1078 CONTRACTS) DESPITE OUR $6.90 GAIN IN PRICE//MONDAY. WE ALSO HAD A RATHER SMALL INITIAL STANDING IN GOLD TONNAGE FOR AUGUST. AT 30.656 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 8200 OZ QUEUE JUMP + PRIOR ISSUANCE OF EXCHANGE FOR RISK = (.684 TONNES) //NEW STANDING 38.171 TONNES + .684 EXCHANGE FOR RISK = 38.855/ + /A FAIR (AND CRIMINAL) ISSUANCE OF 685 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH OUR $6.90 GAIN IN PRICE WITH RESPECT TO MONDAY’S TRADING.WE HAD A SMALL SIZED loss OF 122 OI CONTRACTS (0.379 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 956 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 433,831

IN ESSENCE WE HAVE A SMALL SIZED deCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 122 CONTRACTS WITH 1078 CONTRACTS DECREASED AT THE COMEX// AND A SMALL 956 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI loss ON THE TWO EXCHANGES OF 122 CONTRACTS OR 0.379 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL 685 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (956 CONTRACTS) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (1078) //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 122 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR JULY AT 30.656 TONNES FOLLOWED BY TODAY’S 8200 OZ QUEUE JUMP //NEW STANDING 38.171 TONNES + .684 TONNES (EXCHANGE FOR RISK//PRIOR) NEW TOTALS: 38.855 TONNES/// 3) ZERO LONG LIQUIDATION WITH SOME TAS LIQUIDATION DURING THE COMEX SESSION //4) SMALL SIZED COMEX OPEN INTEREST LOSS/ 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 685 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUG :

TOTAL EFP CONTRACTS ISSUED: 58,248 CONTRACTS OR 5,824,800 OZ OR 181.17 TONNES IN 21 TRADING DAY(S) AND THUS AVERAGING: 2774 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 21 TRADING DAY(S) IN TONNES 181.17 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 181.17/3550 x 100% TONNES 5.09% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 181.17 TONNES (A STRONGER MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUGE SIZED 2019 CONTRACTS OI TO 133,509 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A FAIR 482 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 482 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 482 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2019 CONTRACTS AND ADD TO THE 482 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1537 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 7.685 MILLION OZ

OCCURRED DESPITE OUR $0.03 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED UP 37.25 PTS OR 1.20% //Hang Seng CLOSED UP 353.29 PTS OR 1.95% /The Nikkei CLOSED UP 56.98 PTS OR 0.18% //Australia’s all ordinaries CLOSED UP .69 % /Chinese yuan (ONSHORE) closed DOWN 7.2937 /OFFSHORE CHINESE YUAN DOWN TO 7.3053 /Oil UP TO 80.74 dollars per barrel for WTI and BRENT UP AT 85.19 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 1078 CONTRACTS TO 433,831 DESPITE OUR GAIN IN PRICE OF $6.05 ON MONDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF AUGUST… THE CME REPORTS THAT THE BANKERS ISSUED A SMALL SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 956 EFP CONTRACTS WERE ISSUED: : DEC 956 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 956 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL TOTAL OF 122 CONTRACTS IN THAT 956 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED LOSS OF 1078 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR GAIN IN PRICE OF $6.90//MONDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR FRIDAY NIGHT WAS A SMALL 685 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: AUGUST (38.855) ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES (INCLUDING .6842 EXCHANGE FOR RISK)

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $6.90) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A SMALL GAIN OF 872 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE T.A.S. LIQUIDATION ON THE FRONT END OF MONDAY’S TRADING. THE T.A.S. ISSUED ON MONDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 0.379 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST. (30.656 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 8300 OZ QUEUE JUMP //NEW STANDING ADVANCES QUITE A BIT TO 38.171 TONNES + .6842 (PRIOR EXCHANGE FOR RISK) //NEW TOTAL 38.855 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $6.90.

WE HAD – REMOVED 994 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 122 CONTRACTS OR 12,200 OZ OR 0.379 TONNES.

Estimated gold volume today:// 173,105 awful

final gold volumes/yesterday 124,614 really awful//speculators have left the gold arena

//AUGUST 29/ FOR THE AUGUST 2023 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 64.302 OZ Brinks 2 KILOBARS . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | nil oz |

| No of oz served (contracts) today | 82 notice(s) 8200 OZ 0.2550 TONNES |

| No of oz to be served (notices) | 154 contracts 15,400 oz 0.4790 TONNES |

| Total monthly oz gold served (contracts) so far this month | 12,118 notices 1,211,800 OZ 37.692 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: NIL oz

customer deposits: 0

nil oz

total customer deposits: nil oz

we had 1 customer withdrawals

i) Out of Brinks: 64.302 oz (2 kilobars)

total withdrawals 64.302 oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 236 contracts having LOST 80 contracts. We had 163 contracts filed

on MONDAY, so we gained 83 contracts or an additional 8300 oz will stand at the comex,

Sept LOST 61 contracts to 3937.

Oct LOST 3358 contracts to 29,749 contracts.

We had 82 contracts filed for today representing 8200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 82 notices were issued from their client or customer account. The total of all issuance by all participants equate to 82 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2023. contract month,

we take the total number of notices filed so far for the month (12,118 x 100 oz ), to which we add the difference between the open interest for the front month of AUGUST (236 CONTRACT) minus the number of notices served upon today 82 x 100 oz per contract equals 1,227,200 OZ OR 38.171 TONNES the number of TONNES standing in this active month of AUGUST. + .684 TONNES EXCHANGE FOR RISK/prior = 38.885 tonnes

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (12,118) x 100 oz + (236) {OI for the front month} minus the number of notices served upon today (82) x 100 oz) which equals 1,227,200 oz standing OR 38.171 TONNES + .684 TONNES OF EXCHANGE FOR RISK/prior = 38.885 TONNES

TOTAL COMEX GOLD STANDING: 38.885 TONNES WHICH IS SMALL FOR AN ACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,071,097.121 OZ 64.41 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,550,525.610 OZ

TOTAL REGISTERED GOLD: 10,907,962,556 (339.28 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,642,563.610 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,836,865 OZ (REG GOLD- PLEDGED GOLD) 274.86 tonnes//dropping like a stone

END

SILVER/COMEX

AUGUST 29

//2023// THE AUGUST 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 109,434.183 oz Delaware . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 1,071,379.410 oz Loomis |

| No of oz served today (contracts) | 0 CONTRACT(S) (nil OZ) |

| No of oz to be served (notices) | 0 contracts (NIL oz) |

| Total monthly oz silver served (contracts) | 954 Contracts (4,770,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposit customer account:

i) Into Loomis : 1071,379.410 oz

total customer deposits: 1,071,379.410 oz

JPMorgan has a total silver weight: 139.276 million oz/278.214 million = 49.96% of comex .//

Comex withdrawals 1

i) Out of Delaware: 109,434.185 oz

adjustments: 4 : all dealer to customer

i) HSBC 265,450.700 oz

ii) Out of Brinks: 29,228.190 oz

iii) Out of JPMorgan 5,237.100 oz

iv)Manfra: 29,664.810 oz

TOTAL REGISTERED SILVER: 42.102 MILLION OZ//.TOTAL REG + ELIGIBLE. 278.214 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR August:

silver open interest data:

FRONT MONTH OF AUGUST /2023 OI: 0 CONTRACTS HAVING GAINED 0 CONTRACT(S). WE HAD

0 NOTICE FILED ON MONDAY SO WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF AUGUST.

SEPT HAS A LOSS OF 7845 CONTRACTS DOWN TO 14,309 WITH 2 MORE READING DAYS BEFORE FIRST DAY NOTICE. WE WILL HAVE A LOW DELIVERY MONTH FOR SEPT.

OCT GAINED 195 CONTRACT TO STAND AT 885.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes// est. volume today 95,602 sthuge

Comex volume: confirmed yesterday: 71,691 large

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 954 x 5,000 oz = 4,770,000 oz

to which we add the difference between the open interest for the front month of AUGUST (0) and the number of notices served upon today 0x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST/2023 contract month: 954 (notices served so far) x 5000 oz + OI for the front month of AUGUST (0) – number of notices served upon today (0 )x 500 oz of silver standing for the AUGUST contract month equates to 4.770 million oz.+ 0 MILLION OZ EXCHANGE FOR RISK ISSUED TODAY+ //NEW TOTAL EXCHANGE FOR RISK: 9.88 MILLION OZ//NEW SILVER STANDING: 14.65 MILLION oz.

There are 42.102 million oz of registered silver.

Thus if we take today’s standing at 14.65 and add last month’s 30.9 million oz we have 44.540 million oz against only 42.432 million registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

AUGUST 29/WITH GOLD UP 17.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.6 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.64 TONNES

AUGUST 28/WITH GOLD UP $6.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / //INVENTORY RESTS AT 884.04 TONNES

AUGUST 25/WITH GOLD DOWN $6.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 884.04 TONNES

AUGUST 24/WITH GOLD UP $0.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //INVENTORY RESTS AT 884.91 TONNES

AUGUST 23/WITH GOLD UP $21.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 4.32 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 884.91 TONNES

AUGUST 22/WITH GOLD UP $2.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 0.87 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 889.23 TONNES

AUGUST 21/WITH GOLD UP $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.60 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 890.10 TONNES

AUGUST 18/WITH GOLD UP $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 6.92 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 887.50 TONNES

AUGUST 17/WITH GOLD DOWN $12.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 16/WITH GOLD DOWN $7.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 15/WITH GOLD DOWN $7,45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 895.87 TONNES

AUGUST 14/WITH GOLD DOWN $2.10 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.75 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 899.63 TONNES

AUGUST 11/WITH GOLD DOWN $2.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 903.31 TONNES

AUGUST 10/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 9/WITH GOLD DOWN $8.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 8/WITH GOLD DOWN $9.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES FORM THE GLD /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 7/WITH GOLD DOWN $5.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 906.00 TONNES

AUGUST 4/WITH GOLD UP $7.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.18 TONNES OF GOLD FROM THE GLD/// .///INVENTORY RESTS AT 906.00 TONNES

AUGUST 3/WITH GOLD DOWN $5.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 2/WITH GOLD DOWN $3.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.75 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 1/WITH GOLD DOWN $28.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 31/WITH GOLD UP $9.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 28/WITH GOLD UP $14.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 915,82 TONNES

JULY 27/WITH GOLD DOWN $21.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 917.26 TONNES

JULY 26/WITH GOLD UP $6.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 25/WITH GOLD UP $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 24/WITH GOLD DOWN $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.20 TONNES OF GOLD INTO THE GLD//: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 21/WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / .////INVENTORY RESTS AT 913.80 TONNES

JULY 20/WITH GOLD DOWN $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 913.80 TONNES

GLD INVENTORY: 886.64 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 29/WITH SILVER UP 49 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 183,000 OF SILVER INTO THE THE SLV// /.////INVENTORY RESTS AT 445.044 MILLION OZ

AUGUST 28/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.281 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 444.861 MILLION OZ

AUGUST 25/WITH SILVER UP ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.751 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 446.145 MILLION OZ

AUGUST 24/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.651 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 448.896 MILLION OZ

AUGUST 23/WITH SILVER UP 94 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 826,000 OZ FROM THE SLV// /.////INVENTORY RESTS AT 450.547 MILLION OZ

AUGUST 22/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: /.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 21/WITH SILVER UP 59 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 917,0000 OZ FROM THE SLV//.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 18/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 17/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 16/WITH SILVER DOWN 13 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 15/WITH SILVER DOWN 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 14/WITH SILVER DOWN 3 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.459 MILLION OZ INTOTHE SLV/: //////INVENTORY RESTS AT 452.565 MILLION OZ

AUGUST 11/WITH SILVER DOWN 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.926 MILLION OZ INTOTHE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 452.106 MILLION OZ

AUGUST 10/WITH SILVER UP 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 9/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 8/WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 7/WITH SILVER DOWN 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 4/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.294 MILLION OZ FROM THE SLV// OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 3/WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 189,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.281 MILLION OZ

AUGUST 2/WITH SILVER DOWN 43 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 275,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.471 MILLION OZ

AUGUST 1/WITH SILVER DOWN 61 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 31/WITH SILVER UP 45 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 28/WITH SILVER UP 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.930 MILLION OZ

JULY 27/WITH SILVER DOWN 59 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ

JULY 26/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 25/WITH SILVER UP 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 826,000 OZ FROM THE SLV..////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 24/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 21/WITH SILVER DOWN 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.101 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 20/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.468 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 454.107 MILLION OZ/

CLOSING INVENTORY 445.044 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

EGON VON GREYERZ..

Von Greyerz: Will This Be The Fall Of Falls?

TUESDAY, AUG 29, 2023 – 06:30 AM

Authored by Egon von Greyerz via GoldSwitzerland.com,

This 25 minute video with Matthew Piepenburg and myself is probably one of the most important discussions that we have had.

For years we have both warned investors about the consequences of a system based on unlimited money printing, debt creation and money debasement.

The world economy and the financial system is now on the cusp of a precipice.

No one can forecast when the coming violent turn will come.

It can take years or it can happen tomorrow.

Future historians will tell us when it happened.

In the meantime investors have one duty to themselves and their dependents which is to protect their wealth from total destruction.

Money printing and debt creation have taken markets to dizzy and unsustainable levels.

Since Nixon closed the gold window in 1971, both global and US debt is up over 80X!

And asset markets have been inflated by this fake money with the Nasdaq up 120X and the S&P up 44X since 1971.

But the bubbles are not just in stocks but also in bonds, property, art, other collectibles etc, etc.

In our view, the time to pay the Piper is here and now. The consequences will be costly, even very costly for the investors who ignore this major risk.

Just as bubble assets can go up exponentially they can implode even faster.

RISK OF MARKETS FALLING 50-90%

Sustained corrections of 50% to 90% in stocks and bonds are very possible and when the bubble bursts it will go so fast that there won’t be time to get out or to buy insurance.

Whether the Everything Bubble turns to the Everything Collapse today or tomorrow, the time to protect your assets is before it happens which means NOW.

Forecasting the gold price is a Mug’s game . But understanding the significance of gold for protecting against unprecedented risk is not. We had the Ides of March in mid March this year when 4 US banks, led by Silicon Valley Bank and Credit Suisse, Switzerland’s second biggest bank all went under in a matter of days.

That was a rehearsal. Bad debts and rising interest rates are a timebomb for the banking system. So is the $2-3 quadrillion derivatives risk. This gargantuan risks are before us now and could materialise at any time starting this autumn.

The risk of A Catastrophic Debt Implosion is just too big to ignore.

In our video discussion below Matt and I discuss these risks and most importantly, the best way to protect or insure against this risk.

Owning physical gold outside the banking system is by far the superior method to preserve wealth.

But it is not just about buying physical gold but how you own it, where you store it, in what jurisdictions etc.

This is an area which MAM/GoldSwitzerland has focused on for a quarter of a century and has developed a superior system for HNWIs.

Please watch this important discussion…https://www.zerohedge.com/markets/von-greyerz-will-be-fall-falls

END

3,Chris Powell of GATA provides to us very important physical commentaries

Tonight’s reading material

Alasdair Macleod..

Alasdair Macleod: Hedging the end of fiat

Submitted by admin on Mon, 2023-08-28 13:03Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Monday, August 28, 2023

It is slowly coming clear that the fiat dollar’s hegemony is drawing to a close. That’s what the BRICS summit in Johannesburg is all about — rats, if you like, deserting the dollar’s ship. With the dollar’s backing being no more than a precarious faith in it, it is bound to be sold down by foreign holders.

Being only fiat, it could even become valueless, threatening to take down the other Western alliance fiat currencies as well.

How do you protect your paper wealth from this outcome? Some swear by bitcoin and others by gold.

This article looks at what is likely to emerge as a replacement currency system, and concludes that from practical and legal aspects, bitcoin and the entire cryptocurrency industry will fail with fiat, while mankind will return to gold, as it has always done in the past when state control over currency fails. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/hedging-the-end-of-fiat?gmrefcode=gata

END

A summary of events related to the BRICS summit

(New York/Insider)

BRICS summit ended with no new currency and contradictory comments about it

Submitted by admin on Mon, 2023-08-28 09:46Section: Daily Dispatches

By Huileng Tan

Insider, New York

Monday, August 28, 2023

A group of major emerging economies wrapped up a summit in South Africa last Thursday by welcoming six new members — but without a new dollar-challenging currency.

The summit of Brazil, Russia, India, China, and South Africa or BRICS nations added Saudi Arabia, Iran, Ethiopia, Egypt, Argentina, and the United Arab Emirates to its fold. It is the bloc’s first expansion in 13 years as it seeks to be an alternative to Western-led groupings.

While there was talk about the bloc’s possible creation of a common currency to rival the U.S. dollar, that didn’t happen — in fact, chatter from the BRICS nations on the issue was divided, pointing to different opinions that may delay any such development.

As this dollar alternative was being discussed, data from SWIFT showed the greenback was used for a record 46% of foreign-exchange payments via the communications system in July.

Here’s what the leaders of five BRICS members said about de-dollarization: …

… For the remainder of the report:

END

This is the big result from the BRICS summit: big oil exporters joining the group. Local currency settlements for now may replace the dollar

(Global Times/Beijing)

As big oil exporters join BRICS, local currency settlements may replace dollar

Submitted by admin on Fri, 2023-08-25 20:06Section: Daily Dispatches

From Global Times, Beijing

Friday, August 25, 2023

With Iran, Saudi Arabia, and the United Arab Emirates joining BRICS, the multilateral mechanism now includes major global oil producers and importers. Analysts said that a wider adoption of local currencies for trade among BRICS countries, rather than using the U.S. dollar, seems more natural.

Six candidates — Argentina, Egypt, Ethiopia, Iran, Saudi Arabia, and the United Arab Emirates — will be admitted as BRICS members on January 1, 2024, South African president announced on Thursday at the BRICS summit. Currently, BRICS members include Brazil, Russia, India, China and South Africa.

A Shanghai-based oil industry insider told the Global Times today on the condition of anonymity that having oil producers and consumers as members will set a foundation for BRICS members to use local currencies in settlement, which can definitely reduce transaction costs, adding that people are witnessing the twilight of the petrodollar. …

… For the remainder of the report:

https://www.globaltimes.cn/page/202308/1296990.shtml

END

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

Bitcoin Spikes After ETF Court Ruling

TUESDAY, AUG 29, 2023 – 10:41 AM

With Bitcoin languishing back at pre-ETF excitement levels – despite hashrates reaching record highs – the news this morning has re-awakened those animal spirits in crypto.

The U.S. Court of Appeals for the DC Circuit issued its opinion in Grayscale v. SEC this morning, ruling that the agency was unreasonable to deny the crypto giant permission to launch a Bitcoin ETF.

The win by Grayscale on Tuesday comes after the firm sued the SEC in June 2022 – when the US securities regulator blocked the crypto-focused asset manager from converting its Bitcoin Trust (GBTC) to an ETF.

The firm had argued that the SEC’s approval of ETFs investing in bitcoin futures contracts, but not proposed products that would hold bitcoin directly, is “arbitrary and capricious.”

“The denial of Grayscale’s proposal was arbitrary and capricious because the Commission failed to explain its different treatment of similar products,” wrote Judge Neomi Rao.

Grayscale CEO Michael Sonnenshein said in a Tuesday tweet that the company’s legal team is “actively reviewing” the court’s decision.

Bitcoin is up from $26,000 to $27,000 on the headline.

Grayscale says converting to an ETF would help it unlock about $5.7 billion in value from the $16.2 billion trust by making it easier to create and redeem shares.

GBTC itself is up around 17% on the news, compressing its discount to NAV even more dramatically…

As Fortune.com reports, the ruling does not mean the SEC has to immediately implement the ruling.

The SEC has 45 days to appeal the decision, which could then go either to the U.S. Supreme Court or a so-called ‘en banc’ review, a legal procedure used when a team of judges handles a case deemed to be extremely complex.

While it could appeal the decision, it is also facing applications for Bitcoin ETFs from traditional financial firms like BlackRock and Fidelity, which makes it more likely the agency will simply accept the court ruling and approve applications in coming weeks.

Of course, the SEC will likely not take this denial well and, as some industry participants have noted, will now seek another means to stop this ETF leading top more widespread adoption of crypto.

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2937

OFFSHORE YUAN: DOWN TO 7.3053

SHANGHAI CLOSED UP 37.25 PTS OR 1.20%

HANG SENG CLOSED UP 353,29 PTS OR 1.95%

2. Nikkei closed UP 56.98 OR 0.18%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 104.08 EURO FALLS TO 1.0809 DOWN 16 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.641 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 146.98/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ON SHORE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.5605***/Italian 10 Yr bond yield DOWN to 4.214*** /SPAIN 10 YR BOND YIELD FALLS TO 3.569…**

3i Greek 10 year bond yield RISES TO 3.83

3j Gold at $1917.90 silver at: 24.21 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 62 /100 roubles/dollar; ROUBLE AT 95.93//

3m oil into the 80 dollar handle for WTI and 85 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 146.98// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.641% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8848 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9565well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

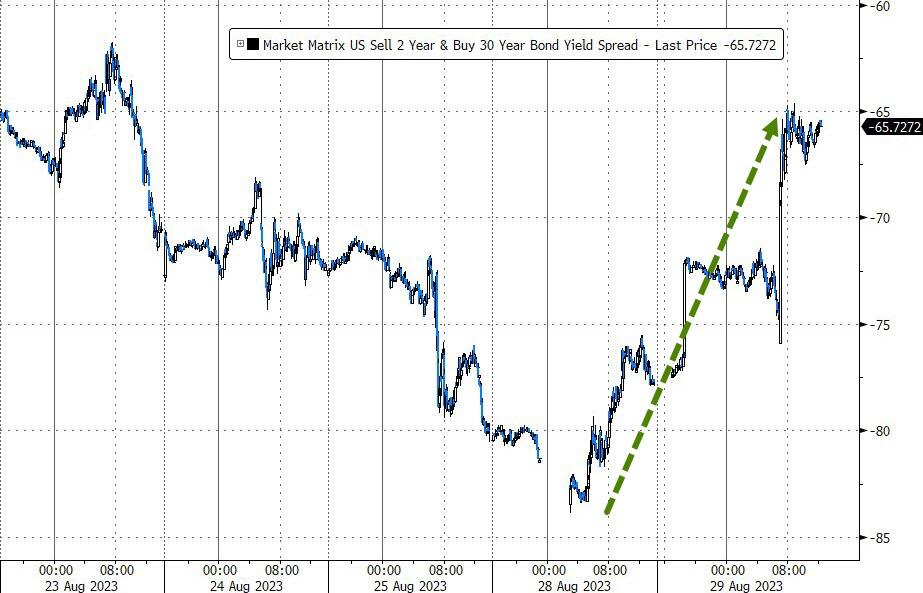

USA 10 YR BOND YIELD: 4.217 DOWN 0 BASIS PTS…

USA 30 YR BOND YIELD: 4.292 DOWN 0 BASIS PTS/

USA 2 YR BOND YIELD: 5.012 DOWN 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.61…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.5012

end

2.a Overnight: Newsquawk and Zero hedge:

USA EARLY MORNING REPORT

Futures Flat Ahead Of Data Dumpfest

TUESDAY, AUG 29, 2023 – 08:14 AM

US stock futures erased gains of as much as 0.3% following another parade of modest China stimuli as investors monitored the outlook for interest rates ahead of key inflation and jobs data later this week, with the Federal Reserve’s data dependence in firmly mind. Contracts on the Nasdaq 100 and S&P 500 traded flat by 7:30 a.m. in New York after gaining as much as 0.4% and 0.3%, respectively. In Europe, the Stoxx 600 rises for a second day while Asian stocks closed at the highest level in two weeks, as Chinese equities extended their gains following the country’s market-boosting measures. A fall in Treasury yields also helped sentiment. Treasury yields and the dollar were steady; the USDJPY rose to 146.97, the highest level since November, and a red line for imminent BOJ intervention.

In premarket trading, retailer Best Buy climbed 3.3% ahead of its second-quarter earnings report, while Verizon and AT&T rose after Citigroup upgraded the stocks to buy, saying it sees a more constructive investment case for large-cap telecommunications firms. Here are some other notable premarket movers:

- BigBear.ai Holdings Inc. climbs 2.9% after HC Wainwright & Co LLC started coverage on the application software company with a buy rating and $4 price target.

- Emergent BioSolutions slips 2% after Benchmark Company LLC downgraded it to hold from buy, with the analyst citing restructuring plans that are expected to “slow share price rebound.”

- Jackson Financial rises as much as 7.8% after S&P Dow Jones said the stock is set to join S&P SmallCap 600 index prior to the opening of trading on Sept. 1.

- Nio falls as much as 3.8% after the Chinese electric-vehicle maker reported bigger-than-expected losses in 2Q as competition heated up. Vehicle sales and margins also missed estimates, while guidance for 3Q deliveries was ahead.

- Noco-Noco rises as much as 90%, on track to recoup some of its Monday losses when it slid 53% after the Japanese advanced electric battery technology company made its debut on the Nasdaq.

- PDD Holdings shares surge as much as 13% after the Chinese e-commerce company reported quarterly revenue and earnings well above estimates. Operating and marketing expenses were higher than expected as the company competes with rivals over pricing at home and abroad.

- Verizon and AT&T rise as Citi upgrades to buy, saying it sees a more constructive investment case for large-cap telecommunications firms.

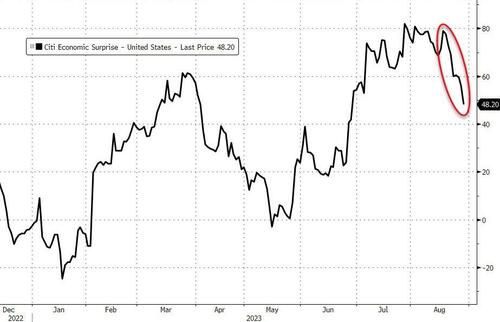

Despite modest gains so far in the final week of August, global stocks are on track for their worst month in almost a year as policy makers remain determined to stifle inflation. Economic reports are assuming even more importance than usual after Federal Reserve Chair Jerome Powell reiterated at Jackson Hole last week that the central bank is ready to raise rates further if the data suggests that is appropriate.

“August has been a challenging month for markets, with investor sentiment cautiously picking up again,” said Victoria Scholar, head of investment at Interactive Investor. “Focus will be on key economic data from the US this week, with hopes that this will fuel expectations that the economy stateside is heading for a soft landing.”

While it’s a bumper week for data releases, including payrolls and GDP, today traders will be monitoring the latest job openings and US consumer confidence data. Other reports this week include US employment growth, the core PCE deflator and August’s payrolls and wages data. Euro-area inflation readings will be in focus this week as well.

Miners led an advance in the Stoxx Europe 600 index after China signaled further measures to support its economy. NN Group NV jumped as much as 11% after the financial-services company reported results that beat analysts’ expectations. European bonds gained, with the German 10-year yield falling three basis points to 2.54%. UK stocks outperformed when they reopened after Monday’s holiday. Here are the biggest European movers:

- NN Group surges as much as 11%, the most since March 2020, after the Dutch insurance and investment management firm delivered results that analysts say were ahead of expectations

- Bunzl shares rise as much as 4.8% after the UK distribution and business services company reported a stronger-than-expected margin performance and raised its full-year guidance

- Vestas climbs as much as 3.3% after Nordea raised the the wind-turbine-maker’s recommendation to buy, citing easing headwinds, flattening inflation, stabilizing supply chains and higher US orders

- Heineken rises as much as 2.1% as JPMorgan upgrades the Dutch brewer to overweight from neutral. Share price weakness post first-half results presents an attractive entry point, the broker says

- Britvic shares gain as much as 4%, the most since Nov. 23, after Barclays upgraded its rating on the UK soft-drinks maker to overweight citing multiple top-line and earnings growth drivers

- Zurich Airport rises as much as 3.1% after the Swiss airport operator reported Ebitda for 1H that beat the average analyst estimate. ZKB says the company benefited from a “true travel boom”

- Telecom Italia gains as much as 3% after Italy approved a decree which empowers it to take a stake in the phone company’s network business of as much as a 20%

- NHOA fell as much as 23%, the most on record, after the French maker of renewable-energy equipment launched a €250m capital increase with shareholders’ preferential subscription rights

Earlier in the session, Asian stocks rose 0.8%, climbing for the second day to the highest level in two weeks, as Chinese equities extended their gains following the country’s market-boosting measures. The Hang Seng Index extended its increase into a second day and China’s stocks outperformed, with the Hang Seng China Enterprises Index rising more than 2%. Chinese internet firms Tencent and Alibaba provided the biggest support to the gauge, with a measure of tech firms listed in Hong Kong rising as much as 3%.

In its latest stimulus step, China is poised to cut interest rates on trillions of yuan of outstanding home mortgages for the first time since the global financial crisis, as policymakers dig deeper into their toolkit to shore up growth in the world’s second-largest economy.

“If policy measures continue to be unveiled in the coming weeks, the market narrative may shift from ‘too little, too late’ to a more confident stance as policymakers regain credibility,” UBS Global Wealth Management strategists including Solita Marcelli and Mark Haefele wrote in a note.

In rates, Treasury futures were lower in early US session, paring small gains amassed during Asia session and London morning. US 10-year yield around 4.22%, 2bps cheaper on the day, outperforming gilts in the sector while trailing bunds, stronger following German 5-year note auction. The week’s coupon auction cycle concludes with $36b 7-year note sale, following decent demand for Monday’s 2- and 5-year notes.

In FX, the Bloomberg Dollar Spot Index rose to 1244, strengthening against EUR, GBP and CHF, and especially the yen, with the USDJPY surging above 147 for the first time since Nov 2022 and guaranteeing that a BOJ intervention is now inevitable. Meanwhile looking at the BBDXY, Sean Callow, strategist at Westpac Banking said that a move in the index toward 1250 “is still achievable over multi-days or week, but will probably require substantial upside surprises on both NFP and CPI.” The British pound edged higher after the slowest increase in grocery bills in almost a year drove down inflation in shops in August, relieving some of the pressure on the Bank of England to keep raising interest rate hikes.

In commodities, oil climbed toward $81 per barrel as traders waited for the next set of clues on the outlook for crude demand in the US and China. Gold was little changed.

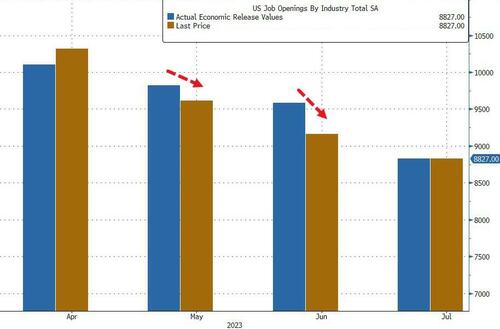

Looking at today’s calendar, we get the August Conference Board consumer confidence read (116.0 survey vs. 117.0 prior), July’s JOLTS job openings (exp. down to 9.5MM from 9.588MM), and the June FHFA house price index; FDIC will propose new guideline for regional banks today; 7yr auction at 1pm.

Market Snapshot

- S&P 500 futures little changed at 4,442.25

- STOXX Europe 600 up 0.6% to 458.20

- MXAP up 0.7% to 160.84

- MXAPJ up 1.0% to 506.27

- Nikkei up 0.2% to 32,226.97

- Topix up 0.2% to 2,303.41

- Hang Seng Index up 1.9% to 18,484.03

- Shanghai Composite up 1.2% to 3,135.89

- Sensex up 0.2% to 65,106.00

- Australia S&P/ASX 200 up 0.7% to 7,210.46

- Kospi up 0.3% to 2,552.16

- German 10Y yield little changed at 2.54%

- Euro little changed at $1.0811

- Brent Futures up 0.3% to $84.68/bbl

- Gold spot up 0.1% to $1,922.94

- US Dollar Index little changed at 104.05

Top Overnight News

- Japan may be at an inflection point in its 25-year battle with deflation as price and wage rises show signs of broadening, the government said on Tuesday, signaling its conviction the economy was nearing an end to prolonged stagnation. RTRS

- Toyota will halt all 14 plants in Japan tonight due to a systems problem, though it doesn’t suspect a cyberattack. It’s not clear when operations will resume. BBG

- Hong Kong’s lived-in home prices declined for a third straight month in July to a six-month low, reflecting the prevailing sentiment in the city’s property market amid an elevated interest-rate environment. Prices fell 1.1% month on month in July, the biggest drop this year. The widely watched gauge slipped to 343.4 from 347.3 in June, the lowest level since 346.8 in February. SCMP

- China’s biggest state-owned banks are considering lowering deposit rates for at least the third time in a year, according to people familiar with the matter, as they ramp up efforts to boost the economy and protect margins. BBG

- The slowest increase in grocery bills in almost a year drove down inflation in British shops in August, relieving some of the pressure on the BOE to keep raising interest rates. The British Retail Consortium said that shop price inflation fell sharply again to 6.9% in August from 7.6% the month before. Food price led the decline, particularly for meat, potatoes and cooking oils. BBG

- AI technology is actually quite labor-intensive, relying on an army of workers scrubbing the data on which models are being trained. Washington Post

- Today the FDIC will vote on five separate proposals at a meeting, all aimed at ensuring banks with over $100 billion in assets are prepared for their own potential failures, and can be taken apart smoothly and quickly. RTRS

- The Biden administration and its European allies are laying plans for long-term military assistance to Ukraine to ensure Russia won’t be able to win on the battlefield and persuade the Kremlin that Western support for Kyiv won’t waver. WSJ

- Homeowners are increasingly forgoing home insurance, gambling that the likelihood of a disaster isn’t high enough to justify the cost of a policy. Some skipping insurance say they are doing so because they can no longer afford the rising premiums. The national average for home insurance based on $250,000 in dwelling coverage increased this year to $1,428 annually, up 20% from 2022, according to Bankrate. WSJ

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded with an upward bias following the positive lead from Wall Street, with little in terms of fresh catalysts to dictate price action heading into month-end. ASX 200 was supported by its gold, mining, and materials sectors but with the gains modest intraday, with the upside hampered by the index’s IT and Healthcare sectors. Nikkei 225 was caged after opening higher, with the index supported by its machinery sector, while Toyota shares waned after reports it is to suspend operations at all of its 14 Japanese assembly plants amid system failures. Hang Seng and Shanghai Comp saw another session in the green, with the gains in the former more pronounced as index heavyweights are again buoyed by the recent stock support measures.

Top Asian News

- Chinese State media reports PBoC may cut banks’ RRR earlier than expected to maintain reasonable ample liquidity, according to reports.

- Chinese banks are considering additional deposit rate cuts to boost growth, according to Bloomberg; Major lenders could lower rates across key tenors by 5-20bps, the plan has been signed off by regulators and the cut could come as soon as Friday.

- China to cut rates on existing mortgages as soon as today, via Bloomberg.

- PBoC sold CNY 385bln via 7-day reverse repos with the rate at 1.80% for a CNY 274bln net injection.

- South Korea plans government spending of KRW 656.9tln (+2.8% from 2023); and sees debt-to-GDP ratio at 51% in 2024 (vs 50.4% in 2023), according to the Finance Ministry.

- Xiaomi (1810 HK) Q2 (CNY): Revenue 67.35bln (exp. 65.84bln), Net 5.14bln (prev. 2.08bln). Smartphone revenue 36.6bln. Will not declare an interim dividend for 6 months.

- Fitch affirms New Zealand at “AA+”; outlook Stable

European bourses are in the green, Euro Stoxx 50 +0.4%, after a constructive open with catalysts light at the time. Following the open, both cash and futures pared some of this move before reverting back towards initial bests on subsequent Chinese source reports. FTSE 100 +1.5% outperforms as it plays catch up to gains elsewhere on Monday’s UK Bank Holiday. As mentioned, sentiment saw some modest upside on the sources with ADRs for Chinese stocks seeing upside. Within Europe, sectors are all in the green featuring outperformance in Basic Resources given benchmark and above factors, Real Estate is firmer after pressure in Monday’s session while Tech has made its way into the green despite initial marginal pressure. Stateside, futures are in the green though only modestly so with the ES and NQ posting gains of circa. +0.1%; upside which began before the Chinese rate reports, but has picked up further since those aired. Agricultural Bank of China (1288 HK) – H1 (CNY): net profit 133.234bln vs. prev. 128.945bln, net interest income 290.421bln vs. prev. 300.219bln, NIM 1.66%

Top European News

- Riksbank’s Bunge says prices are still rising much too fast, right now it looks like the fight against inflation is not over yet. Says the Swedish Crown is undervalued.

FX

- DXY continues to rotate around 104.000 as demand for month-end rebalancing counters softer rates and renewed risk appetite.

- Aussie and Kiwi marginally outperform on 0.6400 and 0.5900 handles against the Buck respectively.

- Yen off worst levels vs. Dollar, but still vulnerable within a 146.60-32 range after an unexpected rise in Japanese unemployment.

- Euro wanes against Greenback and eyes big expiry at 1.0800 plus 200 DMA for support.

- The Yuan saw some two-way action before coming under pressure on source reports that Chinese banks are considering additional deposit rate cuts to support growth, subsequent reports saw some of this briefly pare-back.

- PBoC set USD/CNY mid-point at 7.1851 vs exp. 7.2854 (prev. 7.1856)

- RBA’s Bullock says the impact of climate change on the neutral interest rate is not clear cut; could put upward and downward pressure on the neutral rate. Inflation is still too high, and that will be my first priority as Governor.

Fixed Income

- Debt futures pare gains after extending to the upside in early EU trade awaiting a relatively busy PM agenda.

- Bunds retain bid tone within 132.48-13 range amidst decent Bobl sale and demand for 2053 German tap.

- Gilts pullback further between 94.79-24 parameters after return from 3-day UK weekend.

- T-note holding middle ground within 109-28+/21+ bounds.

Commodities

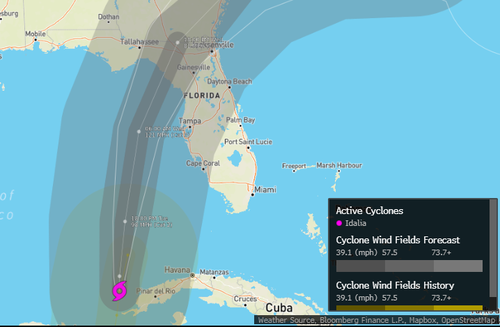

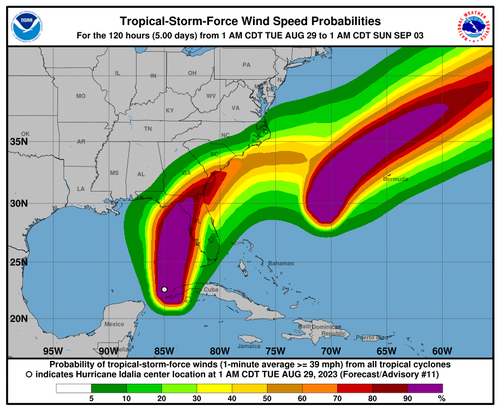

- WTI and Brent Oct’23 are at the top-end of USD 79.79-80.75/bbl and USD 84.11-85.11/bbl parameters. The respective peaks printed following Bloomberg source reports with support via the bullish catalysts of Hurricane Idalia as it continues to intensify as it enters the Gulf.

- Dutch TTF pulls back modestly after Monday’s pronounced strike-notice-driven gains, developments since have detailed the potential action workers will take from the 7th.

- Spot gold is in narrow bounds but just about retains a positive bias as the USD picks up, while base metals were already gleaning support from the firmer APAC handover but have extended since.

- NHC says Idalia is now a hurricane and is expected to rapidly intensify into an extremely dangerous major hurricane before making landfall on Wednesday.

- Australian union said workers at Chevron’s (CVX) LNG facilities to participate in rolling stoppages, bans and limitations; Industrial action will escalate each week until Chevron agrees to bargaining claims, according to Reuters. Workers at Chevron’s Australian LNG facilities plan work stoppages of as long as ten hours from next week, according to Reuters

- Chilean copper miner Codelco makes further staff cuts, according to a statement cited by Reuters.

- Australian Agriculture Minister said the first shipment of Australian barley has been dispatched to China, according to Reuters.

- Ukraine’s First Deputy Agriculture Minister says Ukraine’s winter wheat sowing area will likely remain unchanged despite the export crisis, according to Reuters.

Geopolitics

- North Korean Leader Kim says the US has turned waters near the Korean Peninsula into the most unstable region with the danger of nuclear war, reported via KCNA. Will deliver new weapons to military units under the policy of expanding tactical nuclear weapons operations.

- US President Biden is to meet with Brazilian President Lula on September 19th, according to Reuters.

- Veteran US diplomat Mark Lambert likely to be named as Assistant Secretary for China and Taiwan, according to Reuters sources; appointment unlikely to change US’ China stance.

- Taiwan’s Defence Ministry says 12 Chinese military craft entered the ADIZ on Tuesday, seven craft crossed the median line.

US Event Calendar

- 09:00: June S&P/Case-Shiller US HPI YoY, prior -0.46%

- 2Q House Price Purchase Index QoQ, prior 0.5%

- June FHFA House Price Index MoM, est. 0.6%, prior 0.7%

- June S&P/CS 20 City MoM SA, est. 0.80%, prior 0.99%

- June S&P CS Composite-20 YoY, est. -1.60%, prior -1.70%

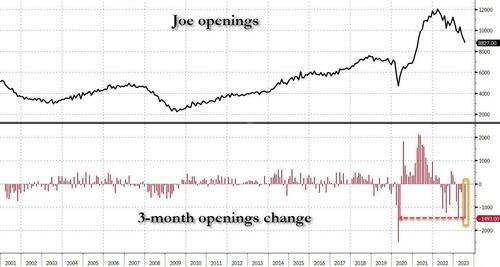

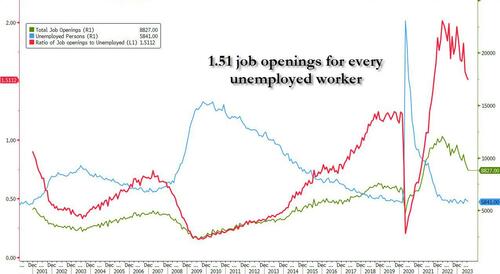

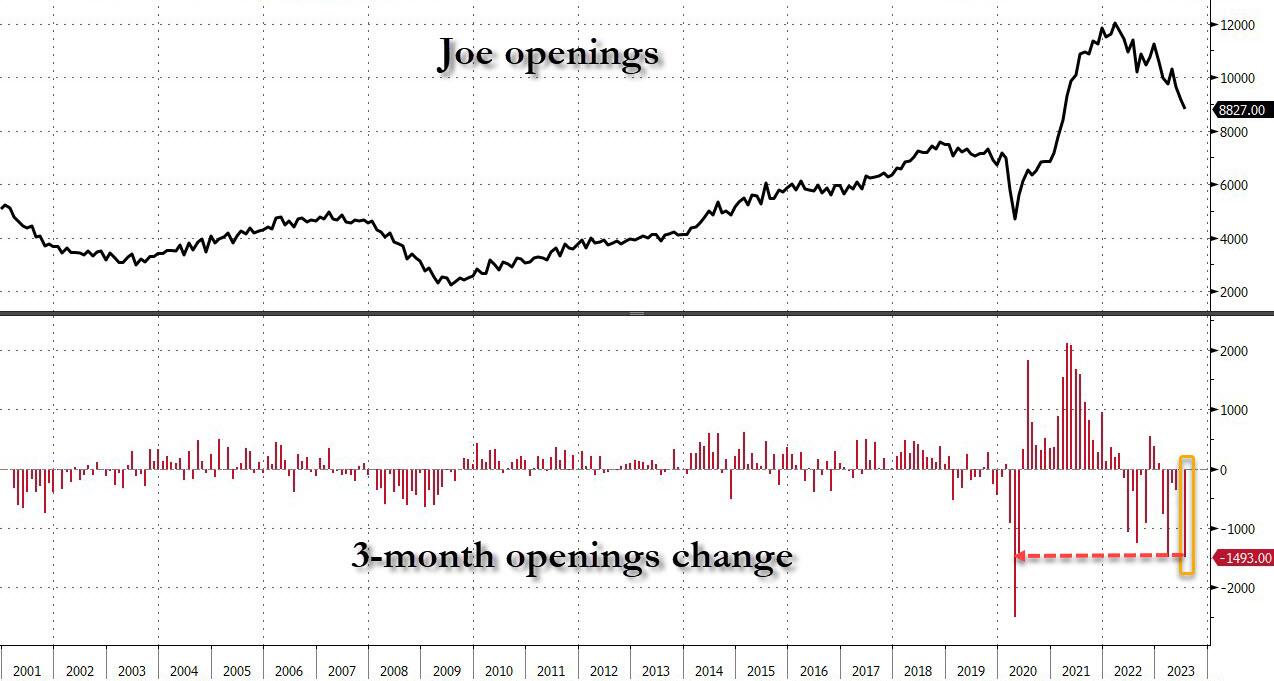

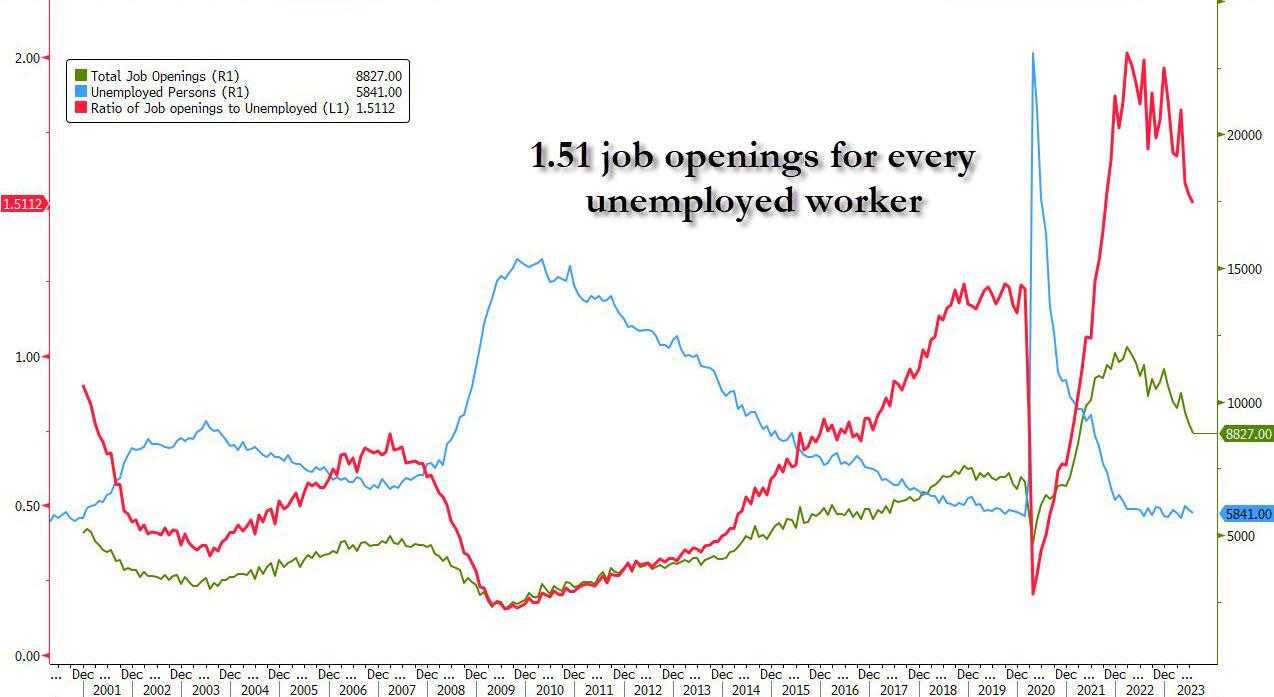

- 10:00: July JOLTs Job Openings, est. 9.5m, prior 9.58m

- 10:00: Aug. Conf. Board Consumer Confidence, est. 116.0, prior 117.0

- Aug. Conf. Board Present Situation, prior 160.0

- Aug. Conf. Board Expectations, prior 88.3

- Aug. Dallas Fed Services Activity, prior -4.2

DB’s Jim Reid concludes the overnight wrap

As the UK returns from the holiday weekend, it’s clear that markets have taken last week’s speeches at Jackson Hole in their stride. That will come as a relief to many, since last year saw the S&P 500 plunge -3.37% on the day of Powell’s hawkish remarks, and we also had a relentless bond selloff that continued into late-October. But this time around, the S&P 500 has advanced on Friday (+0.67%) and again yesterday (+0.63%), just as yields on 10yr Treasuries have kept falling after last week’s highs to trade at 4.19% this morning.

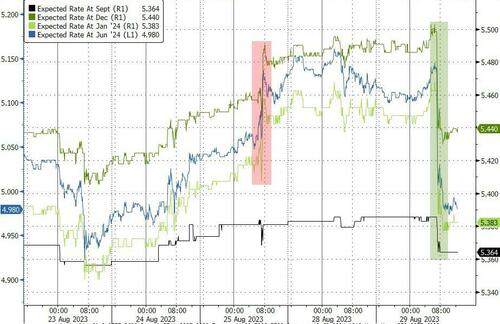

In several respects, Powell’s speech on Friday had quite a few hawkish lines in it. For instance, he reiterated that inflation “remains too high”, and that the Fed was “prepared to raise rates further if appropriate”. He also said that they would be keeping policy “at a restrictive level until we are confident that inflation is moving sustainably down toward our objective.” But on the dovish side, he also acknowledged that inflation had moved lower, and pointed out that there was uncertainty about monetary policy lags. Indeed, Powell said that “there may be significant further drag in the pipeline” from those lags, and he weighed up that there were risks from tightening too little and tightening too much. So it was quite a different tone to last year, when it was abundantly clear that Powell’s message was that the Fed wasn’t about to let-up on inflation.

The most obvious takeaway from this year’s speech is that markets now consider another hike this year as increasingly likely, with futures pricing in a 67% chance of a hike by November. That’s been reflected in front-end yields, with the 2yr Treasury yield closing at a post-2007 high of 5.08% on Friday. Furthermore, the 3m T-bill yield rose to another post-2001 high yesterday of 5.484%. In the meantime, the recent pattern of rate cuts being pushed into the future has continued, and the first full 25bp cut now isn’t priced in until the June 2024 meeting.

Over at the ECB, the debate is also continuing about whether there’ll be another hike at their meeting in two weeks’ time. Currently, markets are considering the decision to be finely balanced, with a 42% chance of a move priced in. This is up from 34% on Friday, as markets took a slightly hawkish interpretation to the lack of a reaction in ECB commentary to last week’s underwhelming PMIs. In her own speech at Jackson Hole, President Lagarde avoided giving a clear signal as well, focusing instead on structural shifts such as changing labour markets, geopolitical divisions and the energy transition. Meanwhile, yesterday saw Austria’s Holzmann push for another hike next month, saying that if “there aren’t any big surprises, I see a case for pushing on with rate increases without taking a pause.”

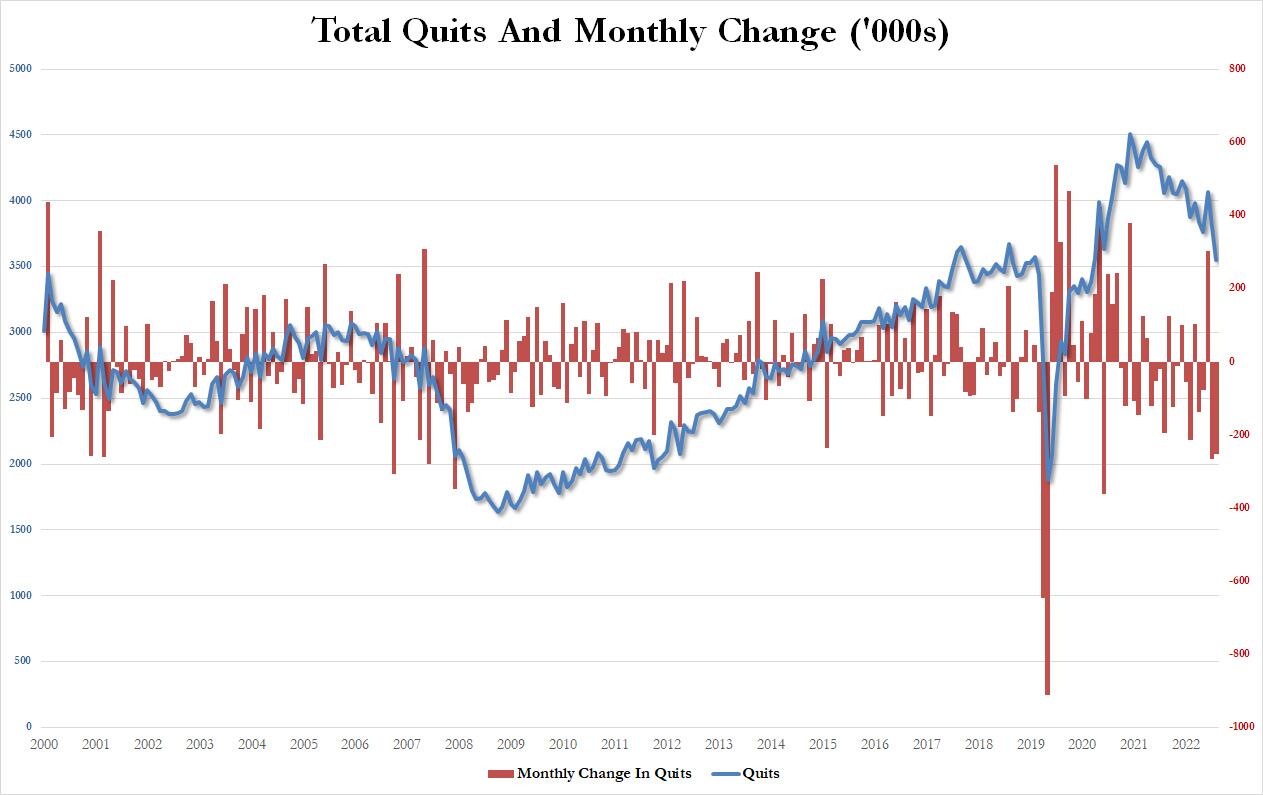

Looking forward, the question of whether we get more hikes will partly be determined by this week’s data, with several important releases coming up. In the US, the main highlight will be the jobs report on Friday, where our US economists expect nonfarm payrolls to have slowed further to +150k in August. That would be the slowest growth since December 2020, and they see that pushing the unemployment rate up a tenth to 3.6%. One category we’ve been following closely is Temporary Help Services, because that has traditionally been a strong leading indicator in previous cycles, turning down ahead of the overall number. It’s fallen for 6 months in a row now, so one to keep an eye on.

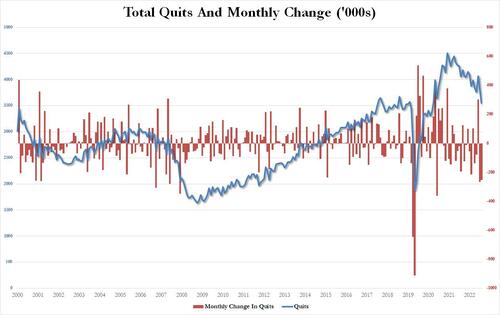

Staying on the US, an important release today will be the JOLTS report for July, which has been closely followed by the Fed to see if the tightness in the labour market is easing. Recent months have seen job openings come down to a 2-year low, albeit to a point that’s still well above pre-pandemic levels. The quits rate will also be an important measure in that release as well, since that’s strongly correlated with wage growth. Otherwise this week, look out for the July PCE inflation report on Thursday, which is the Fed’s preferred measure, along with the ISM manufacturing report for August on Friday, which will be out 90 minutes after the jobs report.

Over in the Euro Area, the main focus will be the flash CPI reading for August, which is out on Thursday. Our European economists see the headline print coming in at +5.5% year-on-year, up two-tenths from July, and they see core inflation at +5.4%. So both headline and core would still be more than twice the ECB’s 2% target, hence there’s still pressure for further rate hikes. Tomorrow we should get an initial indication of where the number might be from the country releases in Germany and Spain. At the same time, we found out yesterday that the Euro Area M3 money supply had seen an annual contraction for the first time since 2010, with a -0.4% year-on-year decline in June. So a fresh sign of how the ECB’s rapid monetary tightening is having an effect.

With all that to look forward to, markets put in a solid performance yesterday, with both the S&P 500 (+0.63%) and Europe’s STOXX 600 (+0.89%) posting steady gains. This makes it the first time in August that the S&P 500 managed to post two consecutive rises (after +0.67% on Friday). It was a similar story for sovereign bonds as well, with yields on 10yr Treasuries coming down -3.3bps to 4.20%. Yields on 10yr bunds were virtually unchanged at +0.2bps, while OAT (-0.4bps) and BTP (-1.9bps) yields saw a slight decline.

That positive mood has continued overnight in Asia, with solid gains for the major indices. Since we weren’t around yesterday, it’s worth mentioning that China announced on Sunday that there would be a cut in the stamp duty on stock trades from 0.1% to 0.05%. That helped trigger an initial surge in the CSI 300 of +5.46% on Monday, although the index pared back those gains through the session to only close up +1.17%. And this morning those gains have continued, with the CSI 300 up another +1.45%.

Other indices across the region seen a consistently positive performance this morning as well, with gains for the Hang Seng (+2.02%), the Shanghai Comp (+1.39%), the Nikkei (+0.31%) and the KOSPI (+0.22%). That’s extended to the US, where futures on the S&P 500 are up another +0.08% this morning. The main negative signal overnight has come from Japan, where the unemployment rate unexpectedly rose to 2.7% in July (vs. 2.5% expected), whilst the jobs-to-applicants ratio slipped further to 1.29.

2 B) NOW NEWSQUAWK (EUROPE/REPORT)/

Equities firmer, boosted after Chinese sources, Crude bid on Idalia news; JOLTS due – Newsquawk US Market Open

TUESDAY, AUG 29, 2023 – 06:09 AM

- Equities are in the green despite fading just after the European open, further upside seen on Chinese sources

- Multiple reports via State Media and BBG that China is considering rate-related action to bolster growth

- Crude benchmarks print fresh highs on the above and as Idalia intensifies into a hurricane, gas deflates slightly after marked Monday upside

- DXY continues to rotate around 104.00 with Antipodeans outperforming while the EUR fades towards marked 1.08 OpEx

- Debt futures pare gains after an initial extension in early trade, though Bunds remain in the green after a decent Bobl outing

- Looking ahead, highlights include US JOLTS, NBH Policy Announcement, Speeches from Fed’s Barr & RBA’s Bullock, and Supply from the US

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses are in the green, Euro Stoxx 50 +0.4%, after a constructive open with catalysts light at the time. Following the open, both cash and futures pared some of this move before reverting back towards initial bests on subsequent Chinese source reports.

- FTSE 100 +1.5% outperforms as it plays catch up to gains elsewhere on Monday’s UK Bank Holiday.

- As mentioned, sentiment saw some modest upside on the sources with ADRs for Chinese stocks seeing upside.

- Within Europe, sectors are all in the green featuring outperformance in Basic Resources given benchmark and above factors, Real Estate is firmer after pressure in Monday’s session while Tech has made its way into the green despite initial marginal pressure.

- Stateside, futures are in the green though only modestly so with the ES and NQ posting gains of circa. +0.1%; upside which began before the Chinese rate reports, but has picked up further since those aired.

- Agricultural Bank of China (1288 HK) – H1 (CNY): net profit 133.234bln vs. prev. 128.945bln, net interest income 290.421bln vs. prev. 300.219bln, NIM 1.66%

- Click here for more detail.

- Click here and here for a recap of the main European equity updates.

FX

- DXY continues to rotate around 104.000 as demand for month-end rebalancing counters softer rates and renewed risk appetite.

- Aussie and Kiwi marginally outperform on 0.6400 and 0.5900 handles against the Buck respectively.

- Yen off worst levels vs. Dollar, but still vulnerable within a 146.60-32 range after an unexpected rise in Japanese unemployment.