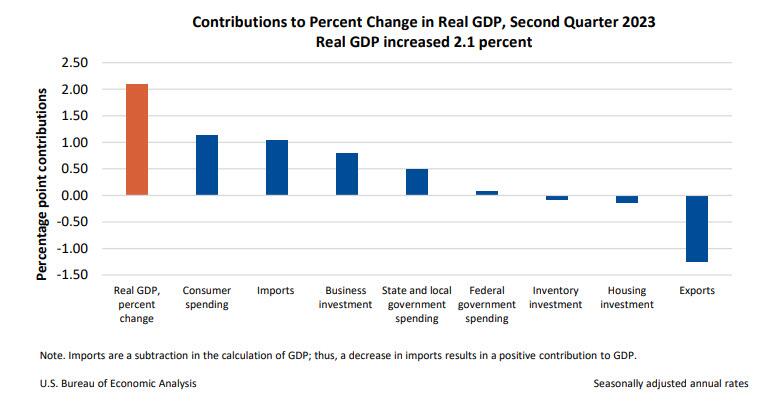

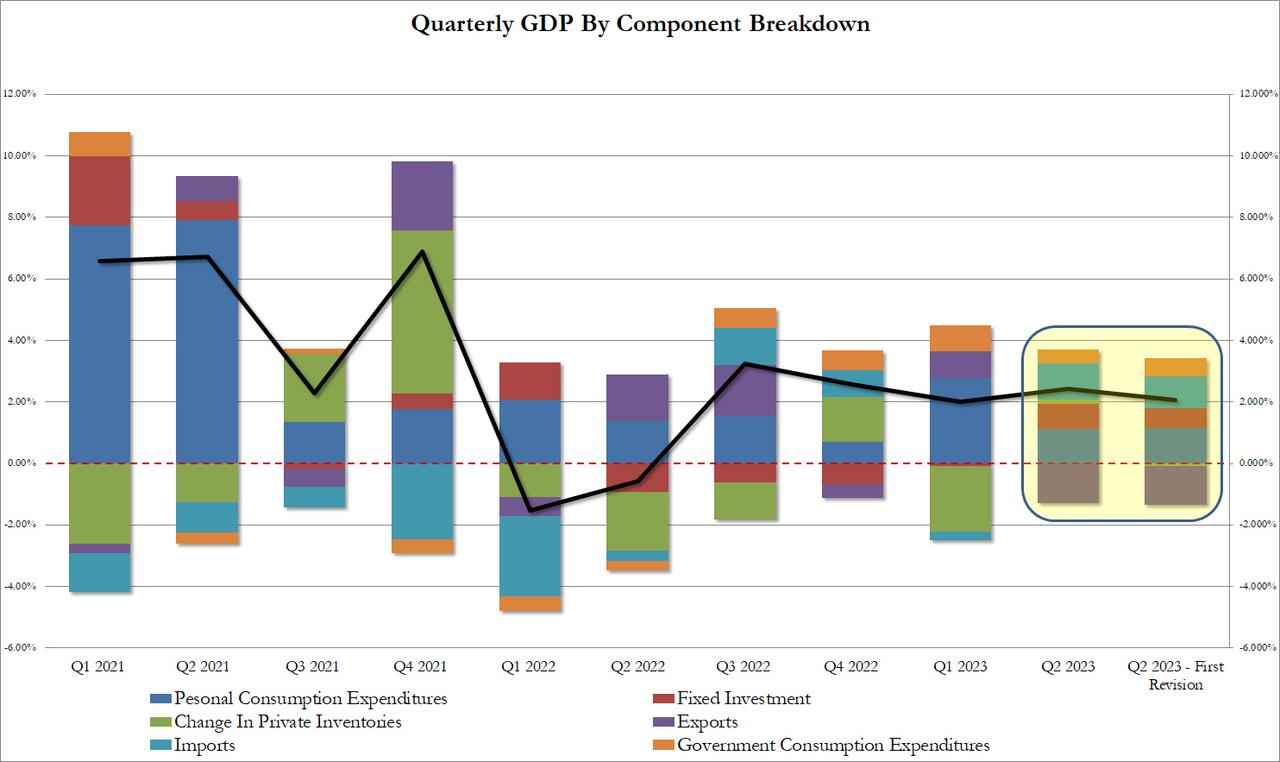

AUGUST 30/FIRST DAY NOTICE TOMORROW/WEST CLOSING CONTROL OVER GOLD/SILVER PRICING: GOLD CLOSED UP $8.15 TO $ 1944.90//SILVER CLOSED DOWN 2 CENTS TO $24.69//PLATINUM CLOSED DOWN $2.95 TO $980.45, WHEREAS PALLADIUM WAS DOWN $30.10 TO $1227.60// CHINA CUTS MORTGAGE RATES TRYING TO STIMULATE ITS HOUSING SECTOR//BRITAIN’S CLIMATE CONTROL COMMITTEE WANTS ALL CITIZENS TO SHUT OFF HEAT DURING THE NIGHT//RUSSIA VS UKRAINE UPDATES//COVID AND VACCINE UPDATES//DR PAUL ALEXANDER/SLAY NEWS/EWOL NEWS//NEWS ADDICTS//ANOTHER MILITARY COUP IN AFRICA THIS TIME IN OIL RICH GABON//THE NORMALLY FROTHY ADP REPORT SHOWS EMPLOYMENT FALTERING//Q2 GDP FIRST REVISION LOWERED TO 2.1%//IDALIA HITS THE FLORIDA COAST NEAR TALLAHASSEE//SWAMP STORIES FOR YOU TONIGHT///

435 H SCOTIA CAPITAL 28 624 H BOFA SECURITIES 84 661 C JP MORGAN 154 686 C STONEX FINANCIA 28 905 C ADM 1 991 H CME 13

TOTAL: 154 154 MONTH TO DATE: 12,272

JPMorgan stopped 0 /154 contracts.

FOR AUGUST:

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2023. CONTRACT: 154 NOTICES FOR 15400 OZ or 0.4790 TONNES

total notices so far: 12,272 contracts for 1,227,200 oz (38.171 tonnes)

FOR AUGUST:

SILVER NOTICES: 0 NOTICE(S) FILED FOR nil OZ/

total number of notices filed so far this month : 954 for 4,770,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $8.15

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/HUGE CHANGES IN GOLD INVENTORY AT THE GLD: /A DEPOSIT OF 2.59 TONNES OF GOLD INTO THE GLD.

INVENTORY RESTS AT 889,23 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 2 CENTS AT THE SLV// SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.834 MILLION OZ OZ SILVER OUT OF THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 443,210 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 1486 CONTRACTS TO 134,993 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.49 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. TAS ISSUANCE WAS A GIGANTIC SIZED 1169 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 1169 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.49). BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER CONTRACTS AS WE HAD A HUMONGOUS SIZED GAIN OF 4080 CONTRACTS ON BOTH EXCHANGES ALONG WITH LITTLE T.A.S.LIQUIDATION THROUGHOUT THE COMEX SESSION.

WE MUST HAVE HAD:

A GIGANTIC ISSUANCE OF EXCHANGE FOR PHYSICALS( 2162 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.105 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S NIL OZ QUEUE JUMP //NEW STANDING REMAINS AT 4.770 MILLION OZ + OUR NEW CRIMINAL 0 CONTRACTS OF EXCHANGE FOR RISK FOR 0 MILLION OZ + EXCHANGE FOR RISK//PRIOR 9.88 MILLION OZ/// : THUS NEW STANDING FOR SILVER IN OZ: 4.770 MILLION OZ + 9.88 MILLION EXCHANGE FOR RISK = 14.650 MILLION OZ/// // // HUGE SIZED COMEX OI GAIN/ GIGANTIC SIZED EFP ISSUANCE/VI) GIGANTIC SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE (1169CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL 469 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTRACTS for 22 days, total 32,141 contracts: OR 160.705 MILLION OZ (1460 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 160.705MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 160.705 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1486 CONTRACTS WITH OUR GAIN IN PRICE OF $0.49 IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A GIGANTIC EFP ISSUANCE CONTRACTS: 2162 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 3.105 MILLION OZ FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP//NEW STANDING 4.770 MILLION OZ+ 0 MILLION EX. FOR RISK //NEW TOTAL EXCH. FOR RISK 9.88 MILLION OZ EXCHANGE FOR RISK// NEW TOTALS STANDING FOR SILVER: 14.65 MILLION OZ//// WE HAVE A GIGANTIC GAIN OF 3648 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A GIGANTIC 1169 CONTRACTS//LITTLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION . THE NEW TAS ISSUANCE TUESDAY NIGHT (1169) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 0 NOTICE(S) FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 9275 CONTRACTS TO 442,806 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED: 452 CONTRACTS

WE HAD A STRONG SIZED INCREASE IN COMEX OI ( 9275 CONTRACTS) WITH OUR $17.05 GAIN IN PRICE//TUESDAY. WE ALSO HAD A RATHER SMALL INITIAL STANDING IN GOLD TONNAGE FOR AUGUST. AT 30.656 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP + PRIOR ISSUANCE OF EXCHANGE FOR RISK = (.684 TONNES) // STANDING REMAINS AT 38.171 TONNES + .684 EXCHANGE FOR RISK = 38.855/ + /A FAIR (AND CRIMINAL) ISSUANCE OF 1515 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH OUR$17.65 GAIN IN PRICEWITH RESPECT TO TUESDAY’S TRADING.WE HAD A VERY STRONG SIZED GAIN OF 11,715 OI CONTRACTS (36.414 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2440CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 442,806

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 11,715 CONTRACTS WITH 9275 CONTRACTS INCREASED AT THE COMEX// AND A FAIR 2440 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 11,715CONTRACTS OR 36.414 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 1515 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2440 CONTRACTS) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI (9275) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 11,715 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR JULY AT 30.656 TONNES FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP //NEW STANDING 38.171 TONNES + .684 TONNES (EXCHANGE FOR RISK//PRIOR) NEW TOTALS: 38.855 TONNES/// 3) ZERO LONG LIQUIDATION WITH LITTLE TAS LIQUIDATION DURING THE COMEX SESSION //4) STRONG SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 1515 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUG :

TOTAL EFP CONTRACTS ISSUED: 60,688 CONTRACTS OR 6,068,800 OZ OR 188.765 TONNES IN 22 TRADING DAY(S) AND THUS AVERAGING: 2750 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 22 TRADING DAY(S) IN TONNES 188.765 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 188.765/3550 x 100% TONNES 5.21% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 188.765 TONNES (A STRONGER MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A HUGE SIZED 1486 CONTRACTS OI TO 135,425 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A GIGANTIC 2162 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 2162and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2162 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1486 CONTRACTS AND ADD TO THE 2162 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 3648 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 18.240 MILLION OZ

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED UP 1.25 PTS OR 0.04% //Hang Seng CLOSED DOWN 1.17 PTS OR 0.01% /The Nikkei CLOSED UP 10.30 PTS OR 0.35% //Australia’s all ordinaries CLOSED UP 1.22 % /Chinese yuan (ONSHORE) closed UP 7.2888 /OFFSHORE CHINESE YUAN UP TO 7.2988 /Oil UP TO 81.70 dollars per barrel for WTI and BRENT UP AT 85.98 / Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 9275CONTRACTS TO 442,806 WITH OUR GAIN IN PRICE OF $17.65 ON TUESDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF AUGUST… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2440 EFP CONTRACTS WERE ISSUED: : DEC 2440 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2440 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG TOTAL OF 11,715 CONTRACTS IN THAT 2440LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED GAIN OF 9275 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $17.65//MONDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A FAIR 1515 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: AUGUST (38.855) ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES (INCLUDING .6842 EXCHANGE FOR RISK)

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $17.65) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A VERY STRONG GAIN OF 12,412 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD LITTLE T.A.S. LIQUIDATION ON THE FRONT END OF TUESDAY’S TRADING. THE T.A.S. ISSUED ON TUESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 36.414 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST. (30.656 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP //NEW STANDING REMAINS AT 38.171 TONNES + .6842 (PRIOR EXCHANGE FOR RISK) // TOTAL REMAINS AT 38.855 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $17.65.

WE HAD – REMOVED 652 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 11,715 CONTRACTS OR 1,171,500 OZ OR 36.414 TONNES.

Total monthly oz gold served (contracts) so far this month

12,272 notices 1,227,200 OZ 38.171 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposit:

total dealer deposits: NIL oz

customer deposits: 0

total customer deposits: nil oz

we had 1 customer withdrawals

i) Out of JPMorgan 160,755.000(5,000 kilobars)

total withdrawals 160,755,000 oz

Adjustments; 2 dealer TO CUSTOMER

i) Out of HSBC 3,279.402 oz

ii) Out of Brinks 36,748.593 ozoz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST.

For the front month of AUGUST we have an oi of 154 contracts having LOST 82 contracts. We had 82 contracts filed

on TUESDAY, so we gained 0 contracts or an additional NIL oz will stand at the comex,

Sept GAINED 12 contracts to 3949. We have one more reading day before first day notice. It looks like we will have close to 10 tonnes of gold standing which is huge for a non delivery month.

Oct GAINED 9869 contracts to 28,791 contracts.

We had 0 contracts filed for today representing oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 154 notices were issued from their client or customer account. The total of all issuance by all participants equate to 154 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the AUGUST /2023. contract month,

we take the total number of notices filed so far for the month (12,272 x 100 oz ), to which we add the difference between the open interest for the front month of AUGUST (154 CONTRACT) minus the number of notices served upon today 154 x 100 oz per contract equals 1,227,200 OZ OR 38.171 TONNES the number of TONNES standing in this active month of AUGUST. + .684 TONNES EXCHANGE FOR RISK/prior = 38.885 tonnes

thus the INITIAL standings for gold for the AUGUSTcontract month: No of notices filed so far (12,272) x 100 oz + (154) {OI for the front month} minus the number of notices served upon today (154) x 100 oz) which equals 1,227,200 oz standing OR 38.171 TONNES + .684 TONNES OF EXCHANGE FOR RISK/prior = 38.885 TONNES

TOTAL COMEX GOLD STANDING: 38.885 TONNES WHICH IS SMALL FOR AN ACTIVE DELIVERY MONTH.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,389,770.610 OZ

TOTAL REGISTERED GOLD 10 ,867,934.561 (338.03 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,521,836.049 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,796,837 OZ (REG GOLD- PLEDGED GOLD) 273,618 tonnes//dropping like a stone

END

SILVER/COMEX

AUGUST 30

//2023// THE AUGUST 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

609,948.670 oz Delaware CNT

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

nil oz

No of oz served today (contracts)

0 CONTRACT(S) (nil OZ)

No of oz to be served (notices)

0 contracts (NIL oz)

Total monthly oz silver served (contracts)

954 Contracts (4,770,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposit: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0 deposit customer account:

total customer deposits: nil oz

JPMorgan has a total silver weight: 139.276 million oz/277.604 million = 50.18% of comex .//

Comex withdrawals 2

i) Out of Delaware: 9759.1000 oz

ii) Out of CNT: 599,989.570 oz

adjustments: 1 : customer to dealer

592,572.7000 oz

TOTAL REGISTERED SILVER: 42.695 MILLION OZ//.TOTAL REG + ELIGIBLE. 277,604 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR August:

silver open interest data:

FRONT MONTH OF AUGUST /2023 OI: 0 CONTRACTS HAVING GAINED 0 CONTRACT(S). WE HAD

0 NOTICE FILED ON TUESDAY SO WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF AUGUST.

SEPT HAS A LOSS OF 8162 CONTRACTS DOWN TO 6147 WITH 1 MORE READING DAYS BEFORE FIRST DAY NOTICE. WE WILL HAVE A LOW DELIVERY MONTH FOR SEPT OF AROUND 15 MILLION OZ//

OCT GAINED 118 CONTRACT TO STAND AT 1003.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

Comex volumes// est. volume today 71,696 strong

Comex volume: confirmed yesterday 106,407 huge

To calculate the number of silver ounces that will stand for delivery in AUGUST. we take the total number of notices filed for the month so far at 954 x 5,000 oz = 4,770,000 oz

to which we add the difference between the open interest for the front month of AUGUST (0) and the number of notices served upon today 0x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST/2023 contract month: 954 (notices served so far) x 5000 oz + OI for the front month of AUGUST (0) – number of notices served upon today (0 )x 500 oz of silver standing for the AUGUST contract month equates to 4.770 million oz.+ 0 MILLION OZ EXCHANGE FOR RISK ISSUED TODAY+ //NEW TOTAL EXCHANGE FOR RISK: 9.88 MILLION OZ//NEW SILVER STANDING: 14.65 MILLION oz.

There are 42.102 million oz of registered silver.

Thus if we take today’s standing at 14.65 and add last month’s 30.9 million oz we have 44.540 million oz against only 42.432 million registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

AUGUST 30/WITH GOLD UP $8.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.59 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.23 TONNES

AUGUST 29/WITH GOLD UP 17.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.6 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.64 TONNES

AUGUST 28/WITH GOLD UP $6.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / //INVENTORY RESTS AT 884.04 TONNES

AUGUST 25/WITH GOLD DOWN $6.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 884.04 TONNES

AUGUST 24/WITH GOLD UP $0.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //INVENTORY RESTS AT 884.91 TONNES

AUGUST 23/WITH GOLD UP $21.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 4.32 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 884.91 TONNES

AUGUST 22/WITH GOLD UP $2.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 0.87 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 889.23 TONNES

AUGUST 21/WITH GOLD UP $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.60 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 890.10 TONNES

AUGUST 18/WITH GOLD UP $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 6.92 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 887.50 TONNES

AUGUST 17/WITH GOLD DOWN $12.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 16/WITH GOLD DOWN $7.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 15/WITH GOLD DOWN $7,45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 895.87 TONNES

AUGUST 14/WITH GOLD DOWN $2.10 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.75 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 899.63 TONNES

AUGUST 11/WITH GOLD DOWN $2.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 903.31 TONNES

AUGUST 10/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 9/WITH GOLD DOWN $8.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 8/WITH GOLD DOWN $9.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES FORM THE GLD /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 7/WITH GOLD DOWN $5.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 906.00 TONNES

AUGUST 4/WITH GOLD UP $7.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.18 TONNES OF GOLD FROM THE GLD/// .///INVENTORY RESTS AT 906.00 TONNES

AUGUST 3/WITH GOLD DOWN $5.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 2/WITH GOLD DOWN $3.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.75 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 1/WITH GOLD DOWN $28.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 31/WITH GOLD UP $9.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 28/WITH GOLD UP $14.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 915,82 TONNES

JULY 27/WITH GOLD DOWN $21.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 917.26 TONNES

JULY 26/WITH GOLD UP $6.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 25/WITH GOLD UP $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 24/WITH GOLD DOWN $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.20 TONNES OF GOLD INTO THE GLD//: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 21/WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / .////INVENTORY RESTS AT 913.80 TONNES

JULY 20/WITH GOLD DOWN $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 913.80 TONNES

GLD INVENTORY: 889.23 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.834 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 443.210 MILLION OZ

AUGUST 29/WITH SILVER UP 49 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 183,000 OF SILVER INTO THE THE SLV// /.////INVENTORY RESTS AT 445.044 MILLION OZ

AUGUST 28/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.281 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 444.861 MILLION OZ

AUGUST 25/WITH SILVER UP ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.751 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 446.145 MILLION OZ

AUGUST 24/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.651 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 448.896 MILLION OZ

AUGUST 23/WITH SILVER UP 94 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 826,000 OZ FROM THE SLV// /.////INVENTORY RESTS AT 450.547 MILLION OZ

AUGUST 22/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: /.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 21/WITH SILVER UP 59 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 917,0000 OZ FROM THE SLV//.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 18/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 17/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 16/WITH SILVER DOWN 13 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 15/WITH SILVER DOWN 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 14/WITH SILVER DOWN 3 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.459 MILLION OZ INTOTHE SLV/: //////INVENTORY RESTS AT 452.565 MILLION OZ

AUGUST 11/WITH SILVER DOWN 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.926 MILLION OZ INTOTHE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 452.106 MILLION OZ

AUGUST 10/WITH SILVER UP 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 9/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 8/WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 7/WITH SILVER DOWN 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 4/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.294 MILLION OZ FROM THE SLV// OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 3/WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 189,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.281 MILLION OZ

AUGUST 2/WITH SILVER DOWN 43 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 275,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.471 MILLION OZ

AUGUST 1/WITH SILVER DOWN 61 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 31/WITH SILVER UP 45 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 28/WITH SILVER UP 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.930 MILLION OZ

JULY 27/WITH SILVER DOWN 59 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ

JULY 26/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 25/WITH SILVER UP 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 826,000 OZ FROM THE SLV..////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 24/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 21/WITH SILVER DOWN 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.101 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 20/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.468 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 454.107 MILLION OZ/

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2888

OFFSHORE YUAN: DOWN TO 7.2988

SHANGHAI CLOSED UP 1.25 PTS OR 0.04%

HANG SENG CLOSED DOWN 1.17 PTS OR 0.01%

2. Nikkei closed UP 10.30 OR 0.35%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 103.42 EURO FALLS TO 1.0885 UP 16 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.641 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 146.35/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ON SHORE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.5710***/Italian 10 Yr bond yield UP to 4.225*** /SPAIN 10 YR BOND YIELD RISES TO 3.589…**

3i Greek 10 year bond yield RISES TO 3.859

3j Gold at $1939.05 silver at: 24.62 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 55 /100 roubles/dollar; ROUBLE AT 96.00//

3m oil into the 81 dollar handle for WTI and 87 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 146.35// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.641% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8790 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9569well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.149 UP 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.2580 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.907 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.75…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.4930

end

2.a Overnight: Newsquawk and Zero hedge:

USA EARLY MORNING REPORT

Futures, Bonds Dip As German Inflation Comes In Hotter Than Expected

WEDNESDAY, AUG 30, 2023 – 08:11 AM

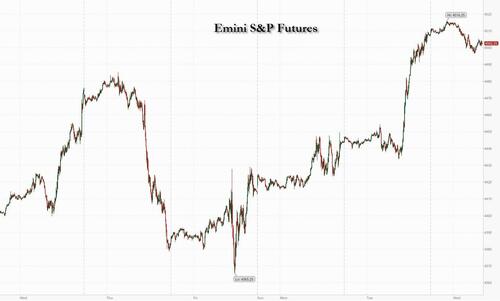

US equity futures are lower, following most European bourses and bonds in the red European after the latest round of German regional data suggested inflation may not yet be fully on the retreat in the euro region. As of 7:45am ET, S&P and Nasdaq 100 futures were both down about 0.1% after the S&P 500 jumped by the most since June on Tuesday after unexpectedly weak JOLTS jobs and consumer-confidence readings in the US raised hopes the Federal Reserve may be nearing the end of its tightening cycle.

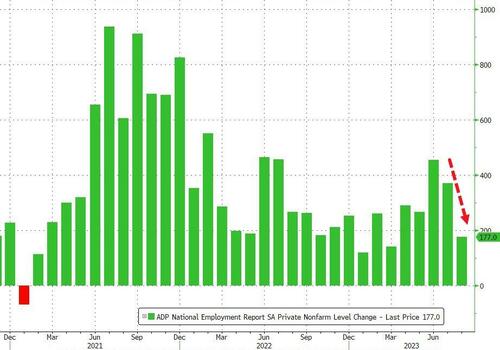

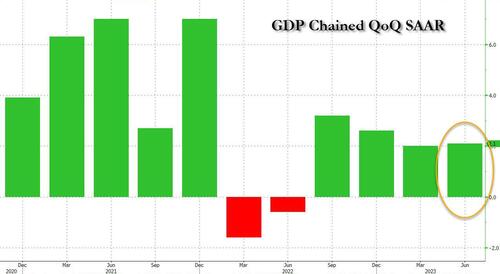

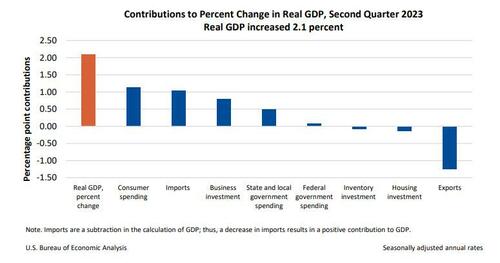

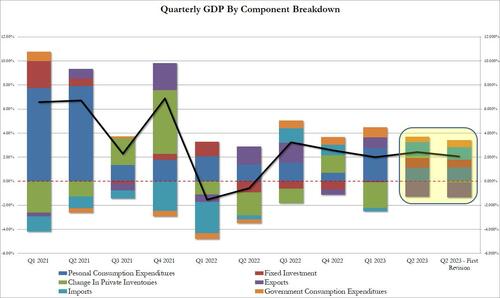

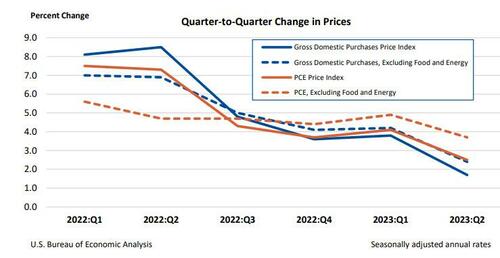

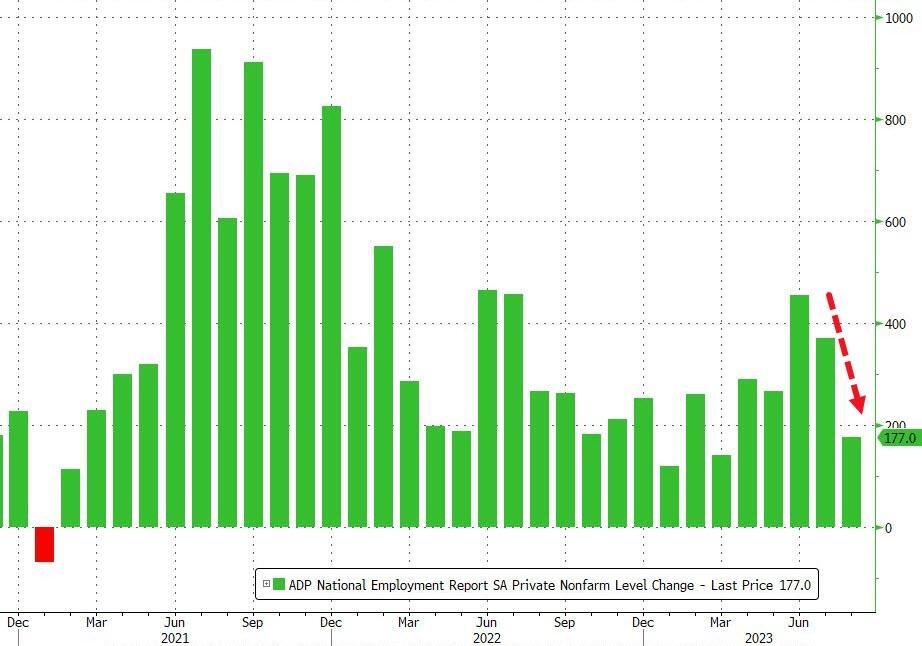

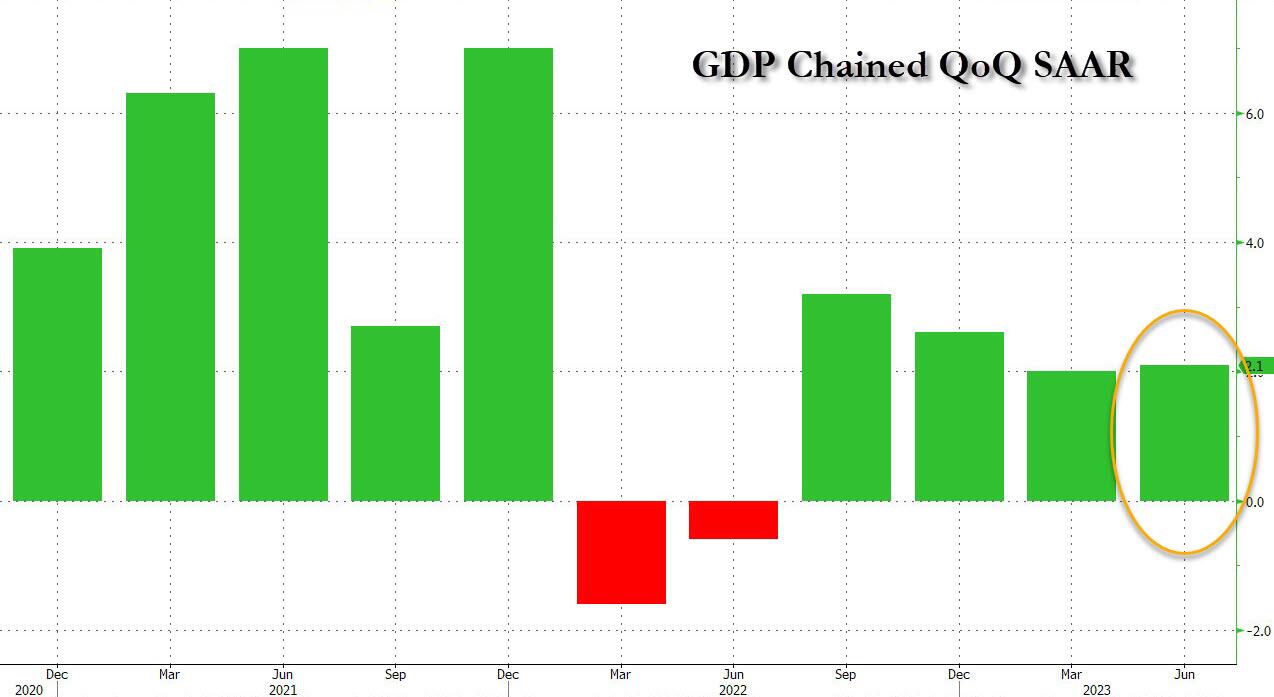

German 10-year bund yields jumped as much as 7bps points to 2.58% after regional reports showed inflation accelerated in four of six German states in August, ahead of figures for the overall German economy due later Wednesday. A separate report showed Spanish inflation also quickened. The dollar weakened as the session has progressed and is trading lower against most G-10 currencies. Oil prices remain higher but metals are mixed, with copper slightly lower. Today, we get the latest ADP (which has been a terrible predictor of NFP numbers) and GDP revision which JPM expects to be revised down to 2.0% from 2.4%, below the consensus of no revision. China will release PMI-Mfg. and PMI-Srvcs tonight at 9.30pm ET.

In premarket trading, megacap tech names are mostly lower; with NVDA dropping -0.8% after closing at an all time high yesterday. HP Inc. slumped 10% after the technology hardware company cut its full-year cash flow and profit outlook. Treasury yields ticked higher and a gauge of the dollar was steady. Chinese stocks listed in the US fell in premarket trading, paring gains following a 6% rally in the Nasdaq Golden Dragon China Index in the previous two sessions. Alibaba -1.6%, Baidu -1.3%, PDD Holdings unchanged, JD.com -1.9%, NetEase -1.3%, Trip.com -2.3%, KE Holdings -2.4%, ZTO Express -4.8%. EV stocks lead losses; Nio falls 3.8%, extending a decline since reporting on Tuesday; Li Auto -3.9%, Xpeng -2.8%. Here are other notable premarket movers:

Alphabet analysts were positive about the company’s artificial intelligence updates at its Google Cloud Next event. The tech giant also announced a new AI infrastructure and software as part of an expanded partnership with Nvidia. Shares fluctuate.

Ambarella drops 21% after its forecast for third-quarter revenue fell short of Wall Street expectations, prompting a slew of price target cuts from analysts.

Box falls 9.1% after the infrastructure software company cut its full-year revenue forecast, with analysts flagging pressure on the firm’s clients against a tough macroeconomic backdrop.

FibroGen tumbles 22% after the biotech company’s Phase 3 LELANTOS-2 trial of pamrevlumab for the treatment of ambulatory patients with Duchenne muscular dystrophy did not meet the primary endpoint.

Globalstar rises 6.1% as the company named former CEO and executive chairman of Qualcomm, Paul Jacobs, as its new CEO.

Investors will monitor reports on US economic growth and private-sector employment later Wednesday, as well as key non-farm payrolls numbers on Friday, to further ascertain the economy’s resilience amid high interest rates. “Data is king right now in terms of market sentiment,” said Susannah Streeter, an analyst at Hargreaves Lansdown Plc. “The non-farm payroll snapshot on Friday will crown the week, and if it points to a fresh slowdown in hiring, we could see another spurt in stock prices.”

Meanwhile, stronger than expected German and Spanish inflation data muddied the waters for European policy makers as they approach the September rates decision. Market pricing implies roughly even odds of a quarter-point increase by the European Central Bank to 4%. Further clouding the outlook was data showing that euro-area economic confidence slowed more than anticipated this month.

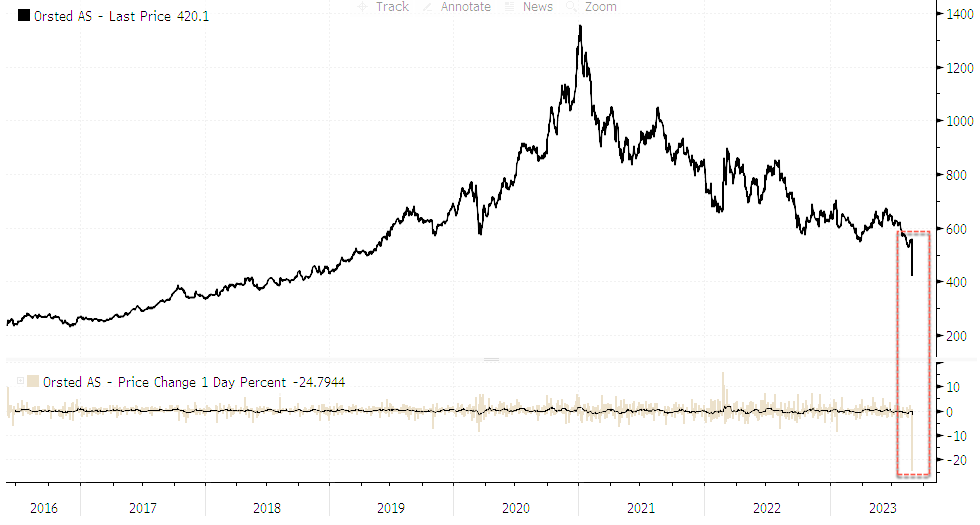

European stocks and bund futures are in the red after Spanish and German inflation data kept the possibility of another ECB rate hike firmly on the table. The Stoxx 600 is down 0.3%, led by declines in the utility, technology and consumer sectors. Banks and basis resources gained while utilities led the decline as Orsted A/S plunged more than 20% after the Danish power generator forecast potential impairments of up to $2.3 billion relating to its US portfolio. Among other individual movers, Prudential Plc climbed more than 4% after posting a rise in new business profit. Here are the most notable European movers:

Orsted slumps as much as 21%, the most on record, after the Danish power generator forecast potential impairments of up to $2.3b relating to its US portfolio. Jefferies called the update a “clear negative”

Delivery Hero shares fall as much as 7.3% to the lowest level since June. Analysts say the food delivery company’s first-half gross margins were slightly below estimates

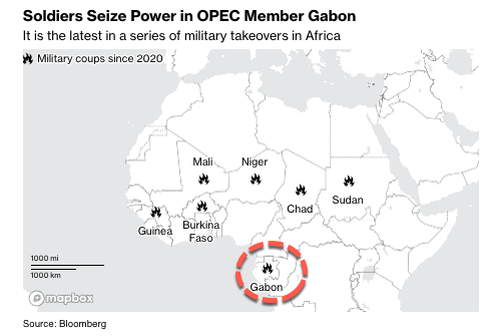

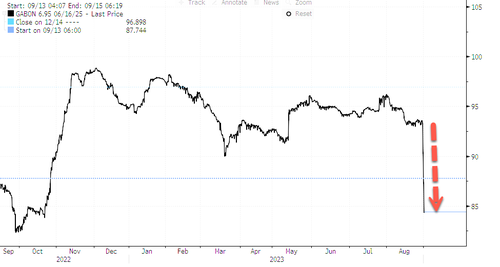

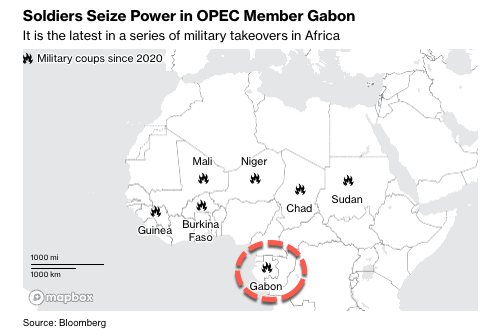

Mining group Eramet SA, oil and gas producer Maurel & Prom and a listed unit of TotalEnergies SE all sank after soldiers seized power in OPEC member Gabon, where the companies have operations

Brunello Cucinelli gains as much as 6.2%, the most intraday since March 16, as the Italian luxury company said it expects full-year revenue to rise by about 19%, at the top end of previous guidance

Aroundtown rises as much as 8.9% after the German landlord raises its full-year guidance for funds from operations (FFO). Berenberg says aiming for a higher earnings level was a “positive surprise”

Prudential rises as much as 4.6% after the insurer reports improved new business profit from its insurance operation. Analysts highlight the company’s strong performance in Hong Kong

Opus Global, a Hungarian holding company, fell as much as 12% after announcing it will suspend its share buyback program and may resume purchases after Oct. 2, when it’s due to publish 2Q results

In Asia, the MSCI Asia Pacific Index came off its highs after earlier rising as much as 1%, as the strong rally in Chinese equity markets gradually evaporated. Tech stocks such as TSMC and Samsung were the top contributors to the gauge’s gains. Benchmarks had earlier rallied, with the Hang Seng Index rising as much as 1.4%, after Chinese state-owned lenders were reported to prepare to reduce rates on the majority of outstanding mortgages, as well as on deposits.

Hang Seng and Shanghai Comp both opened with gains as the region conformed to the global risk appetite, with the Shanghai Comp on a more cautious footing after US Commerce Secretary Raimondo suggested US firms complain that China is “un-investable”, while participants also awaited the speculated mortgage rates cuts. In other news, China is reportedly exploring ways to make its own AI memory chips despite US sanctions, according to SCMP sources.

Australia’s ASX 200 led the gain in the region, rising more than 1% as a slide in the country’s inflation data bolstered prospects for the rate freeze next week.

Nikkei 225 saw its machinery sector leading the gains, although the index’s upside is hampered by the recent gains in the JPY.

Indian stocks ended flat on Wednesday as banks and utilities declined while technology shares were among gainers. The S&P BSE Sensex Index was little changed at 65,087.25 in Mumbai, while the NSE Nifty 50 Index was flat at 19,347.45. Out of 31 stocks in the index, 17 rose and 14 fell. The Nifty has traded below its 20-day moving average for the fourth session in a row despite positive global cues.

“These little piecemeal policy shifts are probably very good in the short term for sentiment, but they don’t necessarily create this sort of surge in terms of the local economy,” Dwyfor Evans, head of APAC macro strategy at State Street Global Markets, said on Bloomberg Television. “There are still bigger issues at play here that I think are holding investors back still at this particular point.”

In FX, the Bloomberg Dollar Spot Index rose 0.1%; it dropped 0.4% on Tuesday as bets for a Federal Reserve hike by year-end were pared back significantly following weak US consumer confidence and JOLTS data

EUR/USD strengthened after data showed inflation in Germany and Spain accelerated, bolstering possibility that ECB may have to raise rates further. Euro bearish sentiment in options over the next month eases following the latest data out of the US and the euro area.

Australia’s dollar fell after weaker-than-expected inflation bolstered prospects that the RBA will stand pat on rates next week. AUD/USD slipped 0.1% after adding 0.8% on Tuesday. The pair briefly fell to 0.6450 earlier Wednesday. Bids for exporters remain layered 0.6440/50, according to traders. Reserve Bank pricing sees an implied rate of 4.164% by the December meeting from 4.175% yesterday

In rates, treasuries were under pressure as the US trading day begins, paced by bunds, where bear-flattening ensued after German inflation rose more than forecast. US yields remain inside Tuesday’s bull-steepening ranges. German 10-year yields rise 6bps to 2.57% while Treasuries also declined, paring some of Tuesday’s rally: yields were higher by 1bp-3bp across the maturity spectrum with the curve steeper, following short-end-led declines of more than 10bp Tuesday. Market-implied expectations for Fed policy are little changed, pricing in just over 50% odds of a quarter-point rate increase in November. Treasuries may draw support from expectations that month-end index rebalancing late Thursday, estimated to extend its duration by 0.12 year, will spur buying. Focal points of US session include August ADP employment change ahead of broader jobs report Friday, and the second estimate of 2Q GDP, a month after the first one exceeded economist estimates, sparking a bond market selloff.

In commodities, crude futures advance, with WTI rising 0.6% to trade near $81.70. Spot gold rises 0.1%.

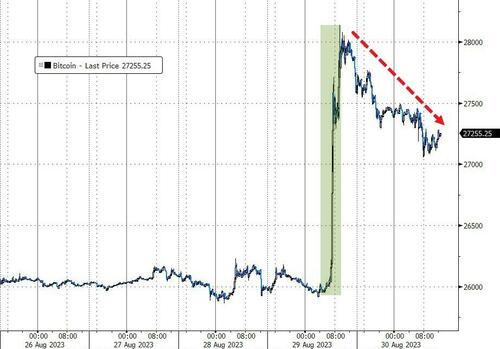

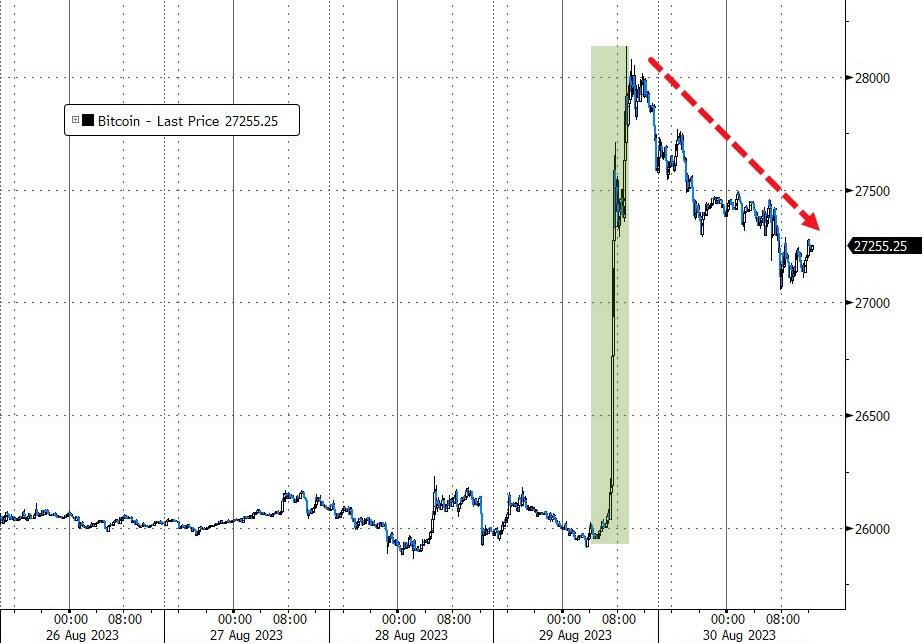

Bitcoin is under modest pressure despite the relatively directionless USD action. Currently, BTC resides at the low end of USD 27.29-27.75k parameters, which are well within Tuesday’s more pronounced USD 26-28.14k bounds.

To the day ahead now, and data releases include the German and Spanish CPI readings for August, UK mortgage approvals for July, whilst in the US there’s the ADP’s report of private payrolls for August, the second estimate of Q2 GDP, along with pending home sales for July. Today’s earnings releases include Salesforce.

Market Snapshot

S&P 500 futures down 0.1% to 4,501.00

MXAP up 0.3% to 161.60

MXAPJ up 0.3% to 508.58

Nikkei up 0.3% to 32,333.46

Topix up 0.4% to 2,313.38

Hang Seng Index little changed at 18,482.86

Shanghai Composite little changed at 3,137.14

Sensex up 0.4% to 65,352.93

Australia S&P/ASX 200 up 1.2% to 7,297.75

Kospi up 0.4% to 2,561.22

STOXX Europe 600 down 0.1% to 459.35

German 10Y yield little changed at 2.56%

Euro down 0.1% to $1.0865

Brent Futures up 0.2% to $85.70/bbl

Gold spot down 0.1% to $1,936.26

U.S. Dollar Index up 0.11% to 103.64

Top Overnight News

Leading BOJ hawk Naoki Tamura hinted that the central bank may attain its long sought-after goal of 2% inflation on a stable basis by early 2024, which may pave the way for higher rates. He hopes the bank will have a “higher resolution” picture around January to March. Economists surveyed by Bloomberg still see April as the most likely month for a policy change. BBG

China has asked two of the nation’s biggest financial firms to examine the books of Zhongrong International Trust Co., potentially paving the way for a state-led rescue of the troubled shadow lender. BBG

Australia’s CPI in Jul moved down to +4.9% from +5.4% in June and below the Street’s +5.2% forecast. BBG

Spain’s CPI for Aug ran slightly hot, with the core number coming in at +6.1% (down from +6.2% in Jul but ahead of the Street’s +6% forecast) and headline +2.4% (up from +2.1% in Jul and inline w/the Street’s +2.4% forecast). BBG

Ukrainian drones struck seven Russian regions overnight, destroying several military cargo planes, in Kyiv’s most sweeping unmanned aerial attack inside enemy territory since Moscow invaded last year. FT

Soldiers seized power in OPEC member Gabon, canceling an Aug. 26 presidential election that was set to extend the Bongo family’s 56-year hold on power. The military takeover is the ninth in sub-Saharan Africa since 2020 and follows a coup in Niger last month, raising concerns of further regional instability. BBG

US oil stockpiles slumped by 11.5 million barrels last week, the API is said to have reported. That would cut total holdings to the lowest this year if confirmed by the EIA. Supplies at Cushing dropped 2.24 million to the least since early January. BBG

Founders and venture capitalists who flocked to artificial-intelligence startups are learning that turning the chatbot buzz into successful businesses is harder than it seems. Almost a year into the boom ignited by the November launch of ChatGPT, some startups that epitomized the zeal for so-called generative AI are now navigating layoffs and reduced user interest. WSJ

Amazon is being threatened with legal action from the US medicines watchdog over the sales of “unapproved” drugs on its online site, as the tech giant faces scrutiny while seeking to break further into the $4tn American healthcare industry. FT

A more detailed look at global markets courtesy of Newsuawk

APAC stocks traded positively across the board following the JOLTS-induced gains seen on Wall Street and in the run-up to month end. ASX 200 saw its upside driven by the industrial sector and closely followed by its gold sector, with a further boost seen from the softer-than-expected Aussie CPI data. Nikkei 225 saw its machinery sector leading the gains, although the index’s upside is hampered by the recent gains in the JPY. Hang Seng and Shanghai Comp both opened with gains as the region conformed to the global risk appetite, with the Shanghai Comp on a more cautious footing after US Commerce Secretary Raimondo suggested US firms complain that China is “un-investable”, while participants also awaited the speculated mortgage rates cuts. In other news, China is reportedly exploring ways to make its own AI memory chips despite US sanctions, according to SCMP sources.

Top Asian News

BoJ Board Member Tamura said BoJ will take steps to curb an excessive rise in interest rates, such as increasing bond buying if BoJ sees speculative and sharp moves that deviate from fundamentals. BoJ Board Member Tamura said he personally feels that sustained and stable achievement of the 2% inflation target is in sight, and it is appropriate to keep easy policy now given uncertainty on hitting the price goal; does not expect 10yr JGB yield to rise to 1.0%. There is a good chance Japan’s economic growth will exceed expectations, he said.

China is reportedly exploring ways to make its own AI memory chips despite US sanctions, SCMP sources said; “China’s top DRAM maker, ChangXin Memory Technologies, is the country’s best hope for specialist chips, but it may take up to four years to deliver products”.

Country Garden (2007 HK) will raise HKD 270mln via new share issues at HKD 0.77 each, according to Reuters.

Chinese regulators urge money brokers to ensure data security, according to Reuters.

PBoC injected CNY 382bln via 7-day reverse repos with the maintained rate at 1.80% for a CNY 81bln net injection.

PBoC holds a meeting with private firms in order to promote their financing, according to Yicai.

European bourses are in the red, Euro Stoxx 50 -0.6%, with stocks generally soft after yesterday’s upside. The current session’s pressure is a function of more hawkish ECB expectations for September after German-state and Spanish metrics. Sectors are mostly in the red with Tech underperforming as yields rise, a narrative which is supporting Banking/Insurance names. Stateside, futures are modestly softer, ES -0.2% ahead of a busy US agenda; NQ -0.3% lags incrementally given the mentioned yield moves.

Top European News

EU Chamber of Commerce President says “uninvestable” is not a term that we would use to describe China; China is under-invested in terms of the FDI it has been able to attract for Europe.

ECB’s Centeno says EZ economic growth indicators have been surprising on the downside recently, downside risks for growth outlined in June projections are materialising. Not seeing de-anchoring of inflation expectations. Seeing a degree of flexibility in the labour market that was not evident in the past.

FX

Greenback steadier after a collapse on lower job openings and loss of consumer confidence.

DXY attempts to form a base around 103.50 – Kiwi cedes ground to Buck along with Yen and Aussie following weak Antipodean data and somewhat mixed BoJ rhetoric

NZD/USD pivots 0.5950, USD/JPY reclaims 146.00+ status and AUD/USD tests 0.6450 from a peak above 21 DMA.

Euro underpinned as German state CPIs imply upside bias to national outturn.

EUR/USD approaches 1.0900 and the top of the band of expiries.

PBoC sets USD/CNY mid-point at 7.1816 vs exp. 7.2773 (prev. 7.1851)

Fixed Income

Broad debt retracement from Tuesday’s US data-inspired highs, with EGBs leading the way and peers down in sympathy.

Bunds below the prior session low within 131.83-132.56 range.

T-note towards base of 110-18+/28 bounds and Gilts trying to stay afloat between 94.35-91 parameters.

Australia sells AUD 700mln 2.75% 2028 Bonds: b/c 3.25x (prev. 5.70x), average yield 3.8331% (prev. 3.5188%)

UK DMO intends to schedule 11 conventional Gilt auctions and four I/L in the October-December period.

Commodities

Currently, WTI Oct’23 and Brent Nov’23 are at the top-end of sub-USD 1/bbl parameters, a peak which printed in proximity to Idalia getting upgraded to a category four hurricane.

Spot gold is unchanged in extremely narrow circa. USD 3/oz bounds as the DXY struggles to meaningfully deviate from the neutral point ahead of a packed afternoon agenda; base metals mixed.

US Energy Inventory Data (bbls): Crude -11.5mln (exp. -2.9mln), Gasoline +1.4mln (exp. -1.4mln), Distillate +2.5mln (exp. +0.1mln), Cushing -2.2mln.

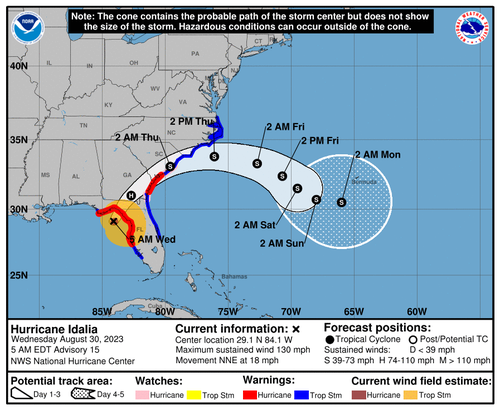

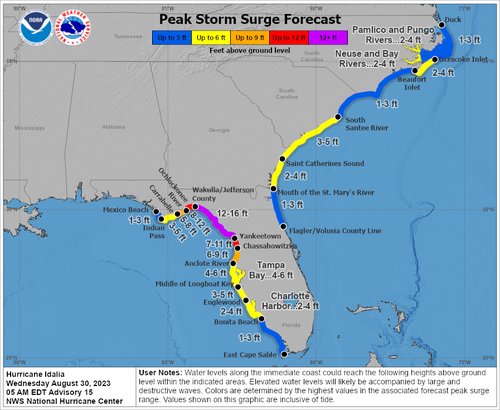

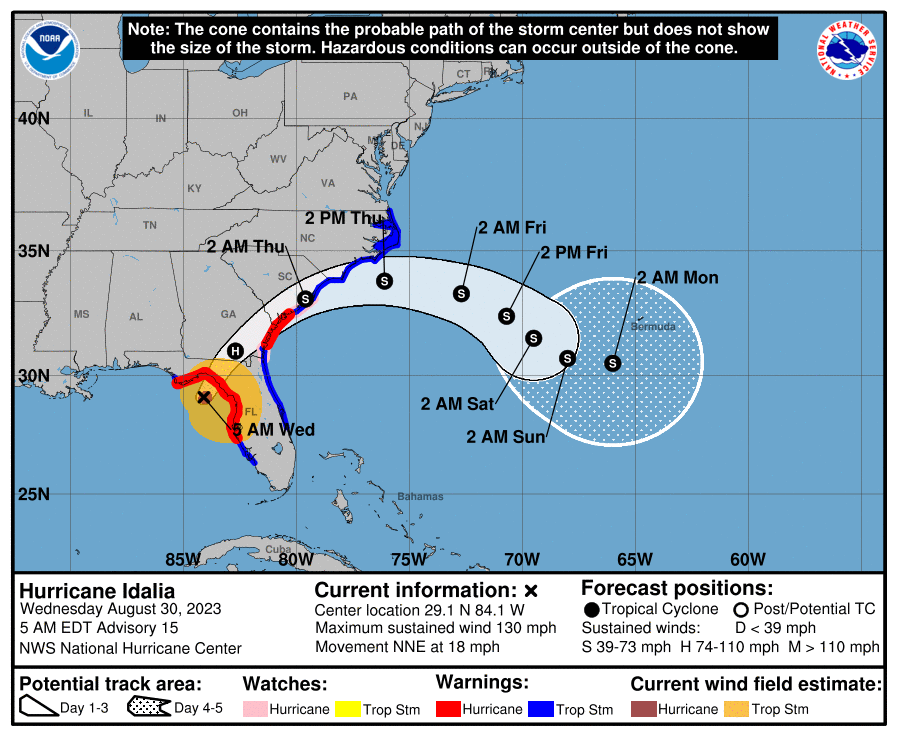

NHC says Idalia rapidly intensifies into a Category 4 Hurricane, catastrophic storm surge and destructive winds are nearing Florida Big Bend region. “Idalia could continue to strengthen before it reaches the Big Bend coast of Florida in a few hours. While Idalia should weaken after landfall, it is likely to still be a hurricane while moving across southern Georgia, and near the coast of Georgia or southern South Carolina late today. Idalia should emerge off the southeastern United States coast early on Thursday and move eastward through late week.”

Japanese PM Kishida says aims to bring down retail gasoline prices to around JPY 175/litre in October (currently JPY 185/litre).

Geopolitics

Explosions were reported at Pskov Airport in western Russia, near the border with Estonia, according to BNO Newsroom.

The Chinese Embassy in the US said China is working to ease market access further and treat foreign firms in the same manner as domestic firms, and added that China will only open its doors wider to the outside world. The embassy noted cyber security review on Micron (MU) is necessary for safeguarding national security, according to Reuters.

Senior Gabonese military officers appear on television and claim they have taken power and borders are closed until further notice; Gabon soldiers announce the cancellation of elections, and the dissolution of institutions on TV, via AFP.

US Event Calendar

07:00: Aug. MBA Mortgage Applications, prior -4.2%

08:15: Aug. ADP Employment Change, est. 195,000, prior 324,000

08:30: 2Q GDP Annualized QoQ, est. 2.4%, prior 2.4%

2Q GDP Price Index, est. 2.2%, prior 2.2%

2Q Core PCE Price Index QoQ, est. 3.8%, prior 3.8%

2Q Personal Consumption, est. 1.8%, prior 1.6%

08:30: July Retail Inventories MoM, est. 0.5%, prior 0.7%

08:30: July Advance Goods Trade Balance, est. -$90b, prior -$87.8b, revised -$88.8b

08:30: July Wholesale Inventories MoM, est. -0.3%, prior -0.5%

10:00: July Pending Home Sales (MoM), est. -1.0%, prior 0.3%

July Pending Home Sales YoY, est. -15.7%, prior -14.8%

DB’s Jim Reid concludes the morning wrap

I was back in the office yesterday after two weeks high up in the French Alps. For our entire trip it was mostly over 30 degrees even at altitude. However the day after we got back it snowed there. I think it would have blown the kids’ mind to have seen that after the weather we had. Talking of the kids, my twins were 6 yesterday. The biggest problem with that is that we bought them new bikes, plus one for Maisie. However this is the first ones we’ve bought that have not come preassembled. So last night my wife and I cursed, swore, and injured ourselves in the pursuit of building three bikes. If you happen to see me in the next few days I guarantee if you look closely enough you’ll see oil somewhere on me that I haven’t been able to get out.

It’s certainly not been a dull second half of August in my absense. To be fair the first half when I was around wasn’t dull either. Markets have swung from narrative to narrative with the soft landing one winning out handsomely yesterday or as a minimum the narrative that the Fed is more likely than not to be done hiking. Although with two whole days left of this choppy month, there’s plenty of time for that to change again.

The big driver yesterday was the latest JOLTS report which showed a further, and large, softening in the US labour market. That came alongside a weak consumer confidence print from the Conference Board, where the present situation component fell to a 9-month low. Together, those two releases led to growing hopes that the Fed would call it a day on their rate hikes, which sent yields on 10yr Treasuries down -8.2bps on the day to 4.12% with 2yrs falling a sizeable -15.4bps, the largest yield decline in nearly 4 months. Equities also rallied strongly on the back of those headlines, with the S&P 500 having its best day since early June (+1.45%) as it advanced for a third day in a row to 2-week highs.

In terms of the details of the JOLTS report, the main headline was that job openings fell to 8.827m in July (vs. 9.5m expected), which was the lowest it had been since March 2021. That meant that the ratio of job openings per unemployed individuals fell back to 1.51 as well, which is the lowest since September 2021, although above the levels around 1.2 seen before the Covid-19 pandemic. The other big story from the release was the decline in the quits rate of those voluntarily leaving their jobs, which is also a good metric for how confident workers are feeling about their prospects. That fell back to 2.3% in July, which is the first time it’s been back at its pre-pandemic level since the current surge in inflation began.

So far at least, this decline in job openings has occurred even as unemployment has remained at historically low levels. Or in other words, the fall in job openings doesn’t appear to have been at the expense of jobs, which is exactly what the Fed are wanting to see. But once these metrics have started falling in the past, it can be hard to know when they’re going to stop, not least since monetary policy operates with time lags that make it hard to feel your way through in real time. So outside of a sudden shock, any path to a hard landing will almost certainly be via signs of a soft landing first.

If you have that concern it would have been heightened by the Conference Board’s latest consumer confidence print. It showed a decline in the headline measure to 106.1 (vs. 116.0 expected), with drops in the present situation and expectations components as well. On top of that, there was another signal that the labour market was weakening, since the gap between the number saying jobs were “plentiful” compared to those saying they were “hard to get” fell to the narrowest since April 2021. So this print and the JOLTS numbers set the stage nicely for Friday’s payrolls.

For now the data put an abrupt stop to the growing narrative that the Fed would still deliver another rate hike in the current cycle. Indeed, the chance of another rate hike by November fell from 71% immediately before the JOLTS report to 51% by yesterday’s close.

For equities, the prospect of fewer rate hikes outweighed any concerns around the data being weak. The S&P 500 saw a near-continuous rally during the day to rise by +1.45%, its strongest gain since 2 June, ironically the last time we saw a strong US payrolls beat. So for a completely opposite reason. All 24 industry groups of the S&P 500 gained, with tech stocks leading the advance. This helped the NASDAQ (+1.74%) to hit a 3-week high, whilst the FANG+ Index rose +3.10% (its largest gain since late May).

Back in Europe, there was also a decent market rally following the releases, with yields on 10yr bunds (-5.3bps), OATs (-5.6bps) and BTPs (-7.2bps) all falling back. Likewise for equities, the STOXX 600 (+0.97%) posted a strong advance, although that was helped by the UK’s return from holiday, since the FTSE 100 (+1.72%) caught up with the previous day’s gains. Today however, attention will turn to the flash CPI numbers for August, with the country releases from Spain and Germany out today ahead of the Euro Area-wide release tomorrow. That’s the biggest remaining input for the ECB’s next decision in a couple of weeks’ time, with markets still narrowly expecting that the ECB will finally pause their hiking cycle after 9 consecutive increases.

In the cryptocurrency space, Bitcoin saw its strongest gain in two months, up +7.15% to $28,005, as the prospects for a first spot Bitcoin ETF improved after a court ruling in the US. It was also a positive day for commodities, with Brent crude (+1.27% to $85.49/bl) moving back above $85 for the first time in two weeks. Across asset classes, the US dollar was the one notable loser of the day, with the broad dollar index (-0.51%) having its weakest day in over three weeks.

Asian equity markets are also trading higher with the S&P/ASX 200 (+1.36%) leading gains across the region as Australia’s inflation softened in July (more below) with the Nikkei on track for its third consecutive day of gains (+0.94%), with the KOSPI (+0.62%) and the Hang Seng (+0.47%) also trading in positive territory. Elsewhere, stocks in mainland China are struggling to gain traction with the CSI (+0.04%) and the Shanghai Composite (+0.03%) both just above flat after losing earlier gains. S&P 500 (+0.17%) and NASDAQ 100 (+0.27%) futures are edging higher again. 10yr USTs (+1.37 bps) yields have edged back up a bit after the big rally yesterday.

Coming back to Australia, data showed that the inflation rate moderated to +4.9% y/y in July (v/s +5.2% expected), its lowest level in 17 months as against a level of +5.4% in June thus reducing the possibility of the Reserve Bank of Australia (RBA) raising interest rates again. Following the release, the Australian dollar lost ground against what has been a weak 24 hours for the US dollar and is down -0.14% at $0.6472 as I type.

News from various sources (like Bloomberg) are indicating that some Chinese state-owned banks are preparing to slash interest rates on existing mortgages and deposits very soon as Beijing is ramping up its efforts to revive growth in the world’s second-largest economy. So watch for headlines there.

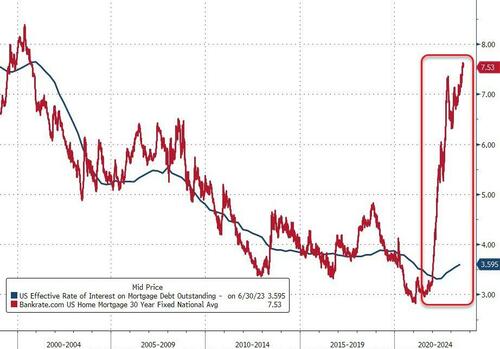

Back to yesterday and the other US data release was on housing for June. According to the 20-City index from S&P CoreLogic Case-Shiller, prices were up another +0.92% that month (vs. +0.80% expected), which is the third consecutive month that prices grew by at least +0.9%. Clearly, housing is only one sector of the economy, but it’s highly sensitive to interest rates, and this is a further sign that it’s picking back up again. On a year-on-year basis, the 20-city index is now only down by -1.17% (vs. -1.60% expected). That said, the house price resilience may be as much about the drag from higher rates on supply of housing in a still solid economy as it as sign of resilient demand.

To the day ahead now, and data releases include the German and Spanish CPI readings for August, UK mortgage approvals for July, whilst in the US there’s the ADP’s report of private payrolls for August, the second estimate of Q2 GDP, along with pending home sales for July. Today’s earnings releases include Salesforce.

2 B) NOW NEWSQUAWK (EUROPE/REPORT)/

Hawkish price action after Spanish & German State CPIs; US ADP, GDP Estimates due – Newsquawk US Market Open

WEDNESDAY, AUG 30, 2023 – 06:33 AM

European bourses are in the red as expectations for the ECB September meeting turns more hawkish

Stateside, futures are in the red with the NQ lagging slightly as yields lift

German regional & Spanish Flash CPIs spurred ECB pricing to a circa. 60% chance of 25bp in Sep., vs 50/50 recently

Broad debt retracement after Tuesday’s US-data inspired highs with EGBs leading post-data

Crude benchmarks at highs as Idalia intensifies into a category four hurricane, expected to intensify as it nears Florida

US Commerce Secretary Raimondo said some Chinese gov’t actions are positive, US businesses want to do business in China

Looking ahead, highlights include US ADP National Employment, US GDP Estimates (Prelim) & PCE Prices Prelim (Q2), German HICP (Flash).

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

European bourses are in the red, Euro Stoxx 50 -0.6%, with stocks generally soft after yesterday’s upside. The current session’s pressure is a function of more hawkish ECB expectations for September after German-state and Spanish metrics.

Sectors are mostly in the red with Tech underperforming as yields rise, a narrative which is supporting Banking/Insurance names.

Stateside, futures are modestly softer, ES -0.2% ahead of a busy US agenda; NQ -0.3% lags incrementally given the mentioned yield moves.

Click here and here for a recap of the main European equity updates.

FX

Greenback steadier after a collapse on lower job openings and loss of consumer confidence.

DXY attempts to form a base around 103.50 – Kiwi cedes ground to Buck along with Yen and Aussie following weak Antipodean data and somewhat mixed BoJ rhetoric

NZD/USD pivots 0.5950, USD/JPY reclaims 146.00+ status and AUD/USD tests 0.6450 from a peak above 21 DMA.

Euro underpinned as German state CPIs imply upside bias to national outturn.

EUR/USD approaches 1.0900 and the top of the band of expiries.

PBoC sets USD/CNY mid-point at 7.1816 vs exp. 7.2773 (prev. 7.1851)

Currently, WTI Oct’23 and Brent Nov’23 are at the top-end of sub-USD 1/bbl parameters, a peak which printed in proximity to Idalia getting upgraded to a category four hurricane.

Spot gold is unchanged in extremely narrow circa. USD 3/oz bounds as the DXY struggles to meaningfully deviate from the neutral point ahead of a packed afternoon agenda; base metals mixed.

US Energy Inventory Data (bbls): Crude -11.5mln (exp. -2.9mln), Gasoline +1.4mln (exp. -1.4mln), Distillate +2.5mln (exp. +0.1mln), Cushing -2.2mln.

NHC says Idalia rapidly intensifies into a Category 4 Hurricane, catastrophic storm surge and destructive winds are nearing Florida Big Bend region. “Idalia could continue to strengthen before it reaches the Big Bend coast of Florida in a few hours. While Idalia should weaken after landfall, it is likely to still be a hurricane while moving across southern Georgia, and near the coast of Georgia or southern South Carolina late today. Idalia should emerge off the southeastern United States coast early on Thursday and move eastward through late week.”

Japanese PM Kishida says aims to bring down retail gasoline prices to around JPY 175/litre in October (currently JPY 185/litre).

US Commerce Secretary Raimondo says US businesses want to do business in China; hopes in next few months to “see some results” after China meetings, US told China in an export control meeting this week we are not targeting China. Had no expectation in the first meetings the US would suddenly resolve specific issues involving companies like Intel (INTC), Micron (MU) or Boeing (BA). Brought up Visa (V) and Mastercard (MA) China business issues in meetings. Some actions of the Chinese government are positive, but the US needs to see the situation on the ground match the rhetoric.

Cleveland-Cliffs (CLF) has reached a tentative agreement with the United Steelworkers (USW) on a new 3-year labour agreement, according to Reuters.

Goldman Sachs (GS) bought UK and US companies using Chinese state funds, according to FT.

EU Chamber of Commerce President says “uninvestable” is not a term that we would use to describe China; China is under-invested in terms of the FDI it has been able to attract for Europe.

ECB’s Centeno says EZ economic growth indicators have been surprising on the downside recently, downside risks for growth outlined in June projections are materialising. Not seeing de-anchoring of inflation expectations. Seeing a degree of flexibility in the labour market that was not evident in the past.

NOTABLE EUROPEAN DATA

German North Rhine-Westphalia State CPI YY (Aug 2023) 5.9% (Prev. 5.8%); Core 5.3% (prev. 5.4%); Bavaria State CPI YY (Aug 2023) 5.9% (Prev. 6.1%); Saxony State CPI YY (Aug 2023) 6.8% (Prev. 6.7%). The initial skew of the data was hawkish vs. mainland consensus, more recent metrics have been slightly dovish but the overall bias is now leaning towards the forecast/slightly above.

UK Mortgage Approvals (Jul 2023) 49.444k vs. Exp. 51.0k (Prev. 54.662k); Lending (Jul 2023) 0.23B GB (Prev. 0.136B GB)

GEOPOLITICS

Explosions were reported at Pskov Airport in western Russia, near the border with Estonia, according to BNO Newsroom.

The Chinese Embassy in the US said China is working to ease market access further and treat foreign firms in the same manner as domestic firms, and added that China will only open its doors wider to the outside world. The embassy noted cyber security review on Micron (MU) is necessary for safeguarding national security, according to Reuters.

Senior Gabonese military officers appear on television and claim they have taken power and borders are closed until further notice; Gabon soldiers announce the cancellation of elections, and the dissolution of institutions on TV, via AFP.

CRYPTO

Bitcoin is under modest pressure despite the relatively directionless USD action. Currently, BTC resides at the low end of USD 27.29-27.75k parameters, which are well within Tuesday’s more pronounced USD 26-28.14k bounds.

APAC TRADE

APAC stocks traded positively across the board following the JOLTS-induced gains seen on Wall Street and in the run-up to month end.

ASX 200 saw its upside driven by the industrial sector and closely followed by its gold sector, with a further boost seen from the softer-than-expected Aussie CPI data.

Nikkei 225 saw its machinery sector leading the gains, although the index’s upside is hampered by the recent gains in the JPY.

Hang Seng and Shanghai Comp both opened with gains as the region conformed to the global risk appetite, with the Shanghai Comp on a more cautious footing after US Commerce Secretary Raimondo suggested US firms complain that China is “un-investable”, while participants also awaited the speculated mortgage rates cuts. In other news, China is reportedly exploring ways to make its own AI memory chips despite US sanctions, according to SCMP sources.

NOTABLE ASIA-PAC HEADLINES

BoJ Board Member Tamura said BoJ will take steps to curb an excessive rise in interest rates, such as increasing bond buying if BoJ sees speculative and sharp moves that deviate from fundamentals. BoJ Board Member Tamura said he personally feels that sustained and stable achievement of the 2% inflation target is in sight, and it is appropriate to keep easy policy now given uncertainty on hitting the price goal; does not expect 10yr JGB yield to rise to 1.0%. There is a good chance Japan’s economic growth will exceed expectations, he said.

China is reportedly exploring ways to make its own AI memory chips despite US sanctions, SCMP sources said; “China’s top DRAM maker, ChangXin Memory Technologies, is the country’s best hope for specialist chips, but it may take up to four years to deliver products”.

Country Garden (2007 HK) will raise HKD 270mln via new share issues at HKD 0.77 each, according to Reuters.

Chinese regulators urge money brokers to ensure data security, according to Reuters.

PBoC injected CNY 382bln via 7-day reverse repos with the maintained rate at 1.80% for a CNY 81bln net injection.

PBoC holds a meeting with private firms in order to promote their financing, according to Yicai.

DATA RECAP

Australian Weighted CPI YY (Jul) 4.9% vs. Exp. 5.2% (Prev. 5.4%)

Australian Construction Work Done (Q2 2023) 0.4% vs. Exp. 0.8% (Prev. 1.8%)

Australian Building Approvals (Jul 2023) -8.1% vs. Exp. -0.8% (Prev. -7.7%); Private House Approvals (Jul 2023) 0.1% (Prev. -1.3%)

2 c. ASIAN AFFAIRS

WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED UP 1.25 PTS OR 0.04% //Hang Seng CLOSED DOWN 1.17 PTS OR 0.01% /The Nikkei CLOSED UP 10.30 PTS OR 0.35% //Australia’s all ordinaries CLOSED UP 1.22 % /Chinese yuan (ONSHORE) closed UP 7.2888 /OFFSHORE CHINESE YUAN UP TO 7.2988 /Oil UP TO 81.70 dollars per barrel for WTI and BRENT UP AT 85.98 / Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

2 d./NORTH KOREA/ SOUTH KOREA/

////SOUTH KOREA/NORTH KOREA/

END

2e) JAPAN

JAPAN

3 CHINA /

CHINA/

China cuts mortgage rates for the first time in 14 years trying to boost housing

(zerohedge)

In Desperate Attempt To Boost Housing, China Cuts Mortgage Rates For First Time Since 2009

TUESDAY, AUG 29, 2023 – 07:45 PM

With the market urgently demanding a bazooka or some other “whatever-it-takes“ policy reaction from Beijing in response to China’s slow-motion economic and housing sector trainwreck, Xi’s regime continues to play cat and mouse with traders and continues to trickle down tiny, piecemeal stimmies on a daily basis and this morning was no different when Bloomberg reported that China’s largest banks are set to cut interest rates on trillions of yuan of outstanding home mortgages (and deposits) for the first time since the global financial crisis, as policymakers dig deeper into their toolkit to shore up growth in the world’s second-largest economy.

And indeed, shortly after the report, China – which one year ago suffered through a crippling mortgage payment boycott which brought many of the country’s property developers to the brink of ruin – confirmed that its big (state-owned of course) lenders are reducing rates on the majority of the nation’s 38.6 trillion yuan ($5.3 trillion) of outstanding mortgages, with the reductions only affecting loans on first homes, two of the people said.

At the same time, lenders such as ICBC (Industrial & Commercial Bank of China) and China Construction Bank are poised to cut deposit rates later this week for the third time in a year, people familiar said.

The moves are part of a targeted push by Beijing to spur consumer spending, drive more funds into the stock market and alleviate pressure on lenders’ profit margins. The moves will also achieve none of that since nobody will allocate capital to – and in – a country where the largest asset, real estate, remains in freefall and where everyone is expecting some form of helicopter money to eventually emerge and contain the collapse.

The cuts to mortgage rates were highly anticipated by investors after the central bank hinted at support in mid-July. While China has reduced benchmark rates and pushed the average mortgage cost to a record low, most Chinese households didn’t benefit as banks won’t reprice existing loans until the beginning of next year.