SEPT 1//GOLD CLOSED UP $1.00 TO $1940.70 //SILVER WAS DOWN 20 CENTS TO $24.23//PLATINUM CLOSED DOWN $14.85 TO $965.60 WHILE PALLADIUM WAS UP $2.60 TO $1230,20//GOLD COMMENTARY TODAY: MIKE MAHARRAY//BIG NEWS TODAY: THE JOBS REPORT //A TOTAL PHONY//DETAILS ON THE JOBS REPORT PROVIDED//UKRAINE VS RUSSIA UPDATE//COVID/VACCINE UPDATES//DR PAUL ALEXANDER/EVOL NEWS/NEWS ADDICTS//TUCKER CARLSON INTERVIEWING DAVE PARTNOY//SWAMP STORIES FOR YOU TONIGHT//

118 C MACQUARIE FUT 416 132 C SG AMERICAS 176 323 H HSBC 174 363 H WELLS FARGO SEC 116 365 H MAREX CAPITAL M 1 435 H SCOTIA CAPITAL 93 624 H BOFA SECURITIES 252 661 C JP MORGAN 11 686 C STONEX FINANCIA 7 690 C ABN AMRO 44 726 C CUNNINGHAM COM 5 1 732 C RBC CAP MARKETS 1 737 C ADVANTAGE 39 26

TOTAL: 681 681 MONTH TO DATE: 3,415

JPMorgan stopped 11 /681 contracts.

FOR SEPT.:

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2023. CONTRACT: 681 NOTICES FOR 68,100 OZ or 2.1181 TONNES

total notices so far: 3415 contracts for 341,500 oz (10.672 tonnes)

FOR SEPT:

SILVER NOTICES: 288 NOTICE(S) FILED FOR 1,440,000 OZ/

total number of notices filed so far this month : 2151 for 10,755,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP 1.00

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/NO CHANGES IN GOLD INVENTORY AT THE GLD: /

INVENTORY RESTS AT 890.10 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 20 CENTS AT THE SLV// SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OZ SILVER OUT OF THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 438.625 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 1057 CONTRACTS TO 130,756 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS STRONG SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.26 LOSS IN SILVER PRICING AT THE COMEX ON THURSDAY. TAS ISSUANCE WAS A STRONG SIZED 727 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 727 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.26). AND WERE SUCCESSFUL IN KNOCKING SOME SILVER CONTRACTS AS WE HAD A SMALL SIZED LOSS OF 150 CONTRACTS ON BOTH EXCHANGES ALONG WITH HUGE T.A.S.LIQUIDATION//AND SPREADER LIQUIDATION THROUGHOUT THE COMEX SESSION.

WE MUST HAVE HAD:

A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 770 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 14.420 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 2.0 MILLION OZ//NEW TOTAL 12.420 MILLION OZ/// / //STRONG SIZED COMEX OI LOSS/ STRONG SIZED EFP ISSUANCE/VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE (727CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL 231 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST:

TOTAL CONTRACTS for 1 days, total 770 contracts: OR 3.850 MILLION OZ (770 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 3.850 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 3.85 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1051 CONTRACTS WITH OUR LOSS IN PRICE OF $0.26 IN SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG EFP ISSUANCE CONTRACTS: 770 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR SEPT OF 14.420 MILLION OZ FOLLOWED BY TODAY’S 2.0 MILLION OZ E.F.P. TO LONDON /// WE HAVE A SMALL LOSS OF 281 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG 727 CONTRACTS//CONSIDERABLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED ALONG WITH COMEX SPREADER LIQUIDATION, DURING THE THURSDAY COMEX SESSION . THE NEW TAS ISSUANCE THURSDAY NIGHT (727) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 288 NOTICE(S) FILED TODAY FOR 1,440,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 5263 CONTRACTS TO 442,643 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED: 947 CONTRACTS

WE HAD A STRONG SIZED DECREASE IN COMEX OI ( 5263 CONTRACTS) WITH OUR $5.20 LOSS IN PRICE//THURSDAY. WE ALSO HAD A RATHER STRONG INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 12.656 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 23,700 OZ QUEUE JUMP//NEW TOTAL STANDING 13.393 TONNES + /A FAIR (AND CRIMINAL) ISSUANCE OF 2428 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH OUR$5.20 LOSS IN PRICEWITH RESPECT TO THURSDAY’S TRADING.WE HAD A VERY SMALL SIZED LOSS OF 564 OI CONTRACTS (1.754 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4699CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 442,643

IN ESSENCE WE HAVE A VERY SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 564 CONTRACTS WITH 5263 CONTRACTS DECREASED AT THE COMEX// AND A STRONG 4699 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 564CONTRACTS OR 1.754 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 2478 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4699 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI (5263) //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 564 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING SHORT AND SPECULATORS GOING LONG ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 12.656 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 23,700 OZ/// 3) ZERO LONG LIQUIDATION WITH CONSIDERABLE TAS LIQUIDATION DURING THE COMEX SESSION //4) STRONG SIZED COMEX OPEN INTEREST LOSS/ 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 2428 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUG :

TOTAL EFP CONTRACTS ISSUED: 4699 CONTRACTS OR 469,900 OZ OR 15.107 TONNES IN 1TRADING DAY(S) AND THUS AVERAGING: 4699 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY(S) IN TONNES 15.107 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 15.107/3550 x 100% TONNES 0.422% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 15.107 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A STRONG SIZED 1051 CONTRACTS OI TO 130,756 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A STRONG 770 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 770and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 770 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 920 CONTRACTS AND ADD TO THE 770 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 281 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 1.405 MILLION OZ

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING//THURSDAY NIGHT

SHANGHAI CLOSED UP 13.37 PTS OR 0.43% //Hang Seng CLOSED /The Nikkei CLOSED UP 91.28 PTS OR 0.28% //Australia’s all ordinaries CLOSED DOWN 0.37 % /Chinese yuan (ONSHORE) closed UP 7.2555 /OFFSHORE CHINESE YUAN UP TO 7.2569 /Oil UP TO 84.84 dollars per barrel for WTI and BRENT UP AT 87.69 / Stocks in Europe OPENED ALL MOSTLY MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 5263CONTRACTS TO 442,643 WITH OUR LOSS IN PRICE OF $5.30 ON THURSDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 4699 EFP CONTRACTS WERE ISSUED: : DEC 4699 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4699 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY SMALL TOTAL OF 564 CONTRACTS IN THAT 4699LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 5263 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR FALL IN PRICE OF $5.20//THURSDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT WAS A FAIR 1239 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: SEPT (13.393) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 13.393 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT LOST $5.20) //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A TINY GAIN OF 383 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD CONSIDERABLE T.A.S. LIQUIDATION ON THE FRONT END OF THURSDAY’S TRADING. THE T.A.S. ISSUED ON THURSDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 1.754 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPT. (12.656 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 23,700 OZ // ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $5.20.

WE HAD – REMOVED 947 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET LOSS ON THE TWO EXCHANGES 564 CONTRACTS OR 56400 OZ OR 1.754 TONNES.

Estimated gold volume today:// 161,150 awful

final gold volumes/yesterday 140,526 awful//speculators have left the gold arena

Total monthly oz gold served (contracts) so far this month

3415 notices 341,500 OZ 10.622 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposit:

total dealer deposits: NIL oz

customer deposits: 0

total customer deposits: nil oz

we had 1 customer withdrawals

i) Out of JPMorgan: 482,245 15 KILOBARS

total withdrawals 482.245 oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPTEMBER.

For the front month of SEPTEMBER we have an oi of 1572 contracts having LOST 2497 contracts. We had

2734 contracts were served upon yesterday, so we gained an additional 237 or 23700 oz will stand for delivery in this non active

delivery month of Sept.

Oct lost 342 contracts to 29,060 contracts.

December LOST 2808 contracts down to 380,027 contracts.

We had 681 contracts filed for today representing 68,100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 681 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 11 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2023. contract month,

we take the total number of notices filed so far for the month (3415 x 100 oz ), to which we add the difference between the open interest for the front month of SEPT (1572 CONTRACT) minus the number of notices served upon today 681 x 100 oz per contract equals 430,600 OZ OR 13.393 TONNES the number of TONNES standing in this non active month of SEPT.

thus the INITIAL standings for gold for the SEPTcontract month: No of notices filed so far (341,500) x 100 oz + (1572) {OI for the front month} minus the number of notices served upon today (681) x 100 oz) which equals 430,600 oz standing OR 12.656 TONNES

TOTAL COMEX GOLD STANDING: 13.393 TONNES WHICH IS HUGE FOR AN INACTIVE DELIVERY MONTH.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 21,389,738,459 OZ

TOTAL REGISTERED GOLD 10 ,854.431 (337.61 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,535,307.318 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,843355 OZ (REG GOLD- PLEDGED GOLD) 275.06 tonnes//dropping like a stone

END

SILVER/COMEX

SEPT 1

//2023// THE SEPT 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

9989.83 oz Delaware

.

Deposits to the Dealer Inventory

nil

Deposits to the Customer Inventory

581,787.109oz Loomis

No of oz served today (contracts)

288 CONTRACT(S) (1,440,000 OZ)

No of oz to be served (notices)

333 contracts (1,665,000 oz)

Total monthly oz silver served (contracts)

2151 Contracts (10,755,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposit: 1

i)Into ASAHI 586,113.500 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposit customer account:

i) Into Loomis: 581,787.109 oz

total customer deposits: 581,787.109 oz

JPMorgan has a total silver weight: 138.666 million oz/278.305 million = 49,80% of comex .//

Comex withdrawals 1

i) Out of Delaware 9989.83 oz

total 9989.83 oz

adjustments: 0

TOTAL REGISTERED SILVER: 44.350 MILLION OZ//.TOTAL REG + ELIGIBLE. 278.305 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR August:

silver open interest data:

FRONT MONTH OF SEPT /2023 OI: 621 CONTRACTS HAVING LOST 2293 CONTRACT(S). WE HAD 1893

CONTRACTS SERVED UPON YESTERDAY. SO WE LOST 400 CONTRACTS OR 2.0 MILLION OZ WERE IMMEDIATELY E.F.P’d TO LONDON AS THERE WAS NO METAL OVER HERE FOR THESE GUYS.

OCT LOST 2 CONTRACTS TO STAND AT 1145.

DEC. GAINED 1169 CONTRACTS TO STAND AT 118,590 .

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 288 for 1,440,000 oz

Comex volumes// est. volume today 60,406 strong

Comex volume: confirmed yesterday 49,696 poor

To calculate the number of silver ounces that will stand for delivery in SEPT. we take the total number of notices filed for the month so far at 2151 x 5,000 oz = 10,755,000 oz

to which we add the difference between the open interest for the front month of SEPT (621) and the number of notices served upon today 288x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT/2023 contract month: 2151 (notices served so far) x 5000 oz + OI for the front month of SEPT (621) – number of notices served upon today (288 )x 500 oz of silver standing for the SEPT contract month equates to 12.420 million oz.

There are 44.350 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

SEPT1/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD .: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 31/WITH GOLD DOWN $1.00 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 30/WITH GOLD UP $8.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.59 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.23 TONNES

AUGUST 29/WITH GOLD UP 17.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.6 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.64 TONNES

AUGUST 28/WITH GOLD UP $6.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / //INVENTORY RESTS AT 884.04 TONNES

AUGUST 25/WITH GOLD DOWN $6.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 884.04 TONNES

AUGUST 24/WITH GOLD UP $0.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //INVENTORY RESTS AT 884.91 TONNES

AUGUST 23/WITH GOLD UP $21.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 4.32 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 884.91 TONNES

AUGUST 22/WITH GOLD UP $2.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 0.87 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 889.23 TONNES

AUGUST 21/WITH GOLD UP $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.60 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 890.10 TONNES

AUGUST 18/WITH GOLD UP $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 6.92 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 887.50 TONNES

AUGUST 17/WITH GOLD DOWN $12.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 16/WITH GOLD DOWN $7.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 894.42 TONNES

AUGUST 15/WITH GOLD DOWN $7,45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.76 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 895.87 TONNES

AUGUST 14/WITH GOLD DOWN $2.10 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.75 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 899.63 TONNES

AUGUST 11/WITH GOLD DOWN $2.10 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .31 TONNES FORM THE GLD//: /// //INVENTORY RESTS AT 903.31 TONNES

AUGUST 10/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 9/WITH GOLD DOWN $8.75 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 8/WITH GOLD DOWN $9.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.31 TONNES FORM THE GLD /// //INVENTORY RESTS AT 903.69 TONNES

AUGUST 7/WITH GOLD DOWN $5.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: /// //INVENTORY RESTS AT 906.00 TONNES

AUGUST 4/WITH GOLD UP $7.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.18 TONNES OF GOLD FROM THE GLD/// .///INVENTORY RESTS AT 906.00 TONNES

AUGUST 3/WITH GOLD DOWN $5.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 2/WITH GOLD DOWN $3.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.75 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 909.18 TONNES

AUGUST 1/WITH GOLD DOWN $28.45 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 31/WITH GOLD UP $9.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.89 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 912.93 TONNES

JULY 28/WITH GOLD UP $14.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 915,82 TONNES

JULY 27/WITH GOLD DOWN $21.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD//: //: / .////INVENTORY RESTS AT 917.26 TONNES

JULY 26/WITH GOLD UP $6.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 25/WITH GOLD UP $2.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 24/WITH GOLD DOWN $4.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.20 TONNES OF GOLD INTO THE GLD//: / .////INVENTORY RESTS AT 919.00 TONNES

JULY 21/WITH GOLD DOWN $3.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / .////INVENTORY RESTS AT 913.80 TONNES

JULY 20/WITH GOLD DOWN $8.70 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.73 TONNES FROM THE GLD/ .////INVENTORY RESTS AT 913.80 TONNES

GLD INVENTORY: 890.10 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT1/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 438,625 MILLION OZ

AUGUST 31/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 440.00 MILLION OZ

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.834 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 443.210 MILLION OZ

AUGUST 29/WITH SILVER UP 49 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 183,000 OF SILVER INTO THE THE SLV// /.////INVENTORY RESTS AT 445.044 MILLION OZ

AUGUST 28/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.281 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 444.861 MILLION OZ

AUGUST 25/WITH SILVER UP ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.751 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 446.145 MILLION OZ

AUGUST 24/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.651 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 448.896 MILLION OZ

AUGUST 23/WITH SILVER UP 94 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 826,000 OZ FROM THE SLV// /.////INVENTORY RESTS AT 450.547 MILLION OZ

AUGUST 22/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: /.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 21/WITH SILVER UP 59 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 917,0000 OZ FROM THE SLV//.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 18/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 17/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 16/WITH SILVER DOWN 13 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 15/WITH SILVER DOWN 6 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.275 MILLION OZ INTOTHE SLV/: / .////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 14/WITH SILVER DOWN 3 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.459 MILLION OZ INTOTHE SLV/: //////INVENTORY RESTS AT 452.565 MILLION OZ

AUGUST 11/WITH SILVER DOWN 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.926 MILLION OZ INTOTHE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 452.106 MILLION OZ

AUGUST 10/WITH SILVER UP 6 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 9/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 8,807 MILLION OZ OUT OF THE SLV/: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 450.180 MILLION OZ

AUGUST 8/WITH SILVER DOWN 40 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 7/WITH SILVER DOWN 46 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 4/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.294 MILLION OZ FROM THE SLV// OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 458.987 MILLION OZ

AUGUST 3/WITH SILVER DOWN 16 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 189,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.281 MILLION OZ

AUGUST 2/WITH SILVER DOWN 43 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 275,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.471 MILLION OZ

AUGUST 1/WITH SILVER DOWN 61 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 31/WITH SILVER UP 45 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 184,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.746 MILLION OZ

JULY 28/WITH SILVER UP 15 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 550,000 OZ OF SILVER FROM THE SLV// .////INVENTORY RESTS AT 451.930 MILLION OZ

JULY 27/WITH SILVER DOWN 59 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ

JULY 26/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: .////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 25/WITH SILVER UP 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A SMALL WITHDRAWAL OF 826,000 OZ FROM THE SLV..////INVENTORY RESTS AT 452.480 MILLION OZ/

JULY 24/WITH SILVER DOWN 23 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 21/WITH SILVER DOWN 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.101 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 453.306 MILLION OZ/

JULY 20/WITH SILVER DOWN 38 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.468 MILLION OZ OF SILVER FROM THE SLV ////INVENTORY RESTS AT 454.107 MILLION OZ/

Aristotle listed four characteristics of sound money: it must be durable, portable, divisible, and have intrinsic value. Gold possesses all of these characteristics, which is why gold has served as money for thousands of years.

Every natural element with which the earth has been endowed has a usefulness—a purpose. If we listen to gold, its message is loud and clear—gold is money. To serve as natural money is gold’s highest purpose.”

Modern financial systems spurn gold. Governments need central banks to create money (inflation) and manipulate interest rates (the cost of money) to prop up their borrowing and spending. The kind of spending and accompanying budget deficits we see in the US wouldn’t be possible if the Federal Reserve was not keeping interest rates lower than they otherwise would and monetizing the debt through QE.

But even as governments devalue their fiat currencies, gold maintains its purchasing power over time. Consider this: an ounce of gold buys the same amount of oil as it did 70 years ago.

As Turk put it, “Gold preserves purchasing power, which is one of the key requisites of money. As illustrated by the above chart, it is an outcome that no national currency can match.”

Sound money also enables sound economic calculation. As Turk explains, this is only possible “using a consistent, unchanging unit of account to measure prices over time.”

Gold serves this role perfectly because it is the only element in the known universe that is eternal and not subject to decay or degradation. A gram of gold today is identical to a gram of gold mined by the Romans.”

One important characteristic of sound money is that its stock remains relatively constant. Somewhat surprisingly, Turk asserts, “Gold is not valuable because it is rare.”

Plenty of gold exists that has yet to be mined on land, under the oceans, and even extracted from ocean water when the technologies become available to make that mining possible. Gold is valuable because it is useful but mined—produced—only when it is profitable to do so, which depends on how gold has been dispersed in the earth’s crust when combined with humanity’s ability, financial capacity, and available technology needed to discover, mine, and refine it.”

The amount of mined gold has grown over the years, but it has expanded at a relatively consistent rate. According to Turk, the average annual rate over the last 529 years is 1.2%. Since 1960 the average growth in the gold stock is 1.8%, ranging from 1.4% to 2.2%.

Compare that to the stock of dollars. Since 1960, money supply growth varied from a low of 1% in 1993 to a high of 19.1% in 2020. As a result, “this inconsistency results in swings in the dollar stock that in turn causes volatility in prices expressed in dollars because there are not enough or too many dollars circulating relative to the prevailing level of economic activity.”

Economist Milton Friedman developed the k-percent rule. In a nutshell, he postulated that the quantity of currency should increase by a constant percentage rate every year, irrespective of bank credit cycles. As Turk explains, gold comes closer than any central bank-managed currency to fulfilling this rule.

The gold stock grows at approximately the same rate as world population and new wealth creation. Consequently, the purchasing power arising from the interaction of gold’s supply—its aboveground stock—and the unfailing inelastic demand for gold that exists because it is money, make gold uniquely useful to accurately calculate the price of goods and services throughout time. It is a feature that the dollar and other national currencies fail to match because their annual growth rates are not consistent, causing fluctuations in their “aboveground” stock. Since 1950 the weight of the gold stock has grown 3.5 times, but a gram of gold still purchases the same amount of crude oil.”

Significantly, gold doesn’t require “management” by central bankers. Experience teaches us that currency management always creates artificial booms rife with malinvestments and misallocations. This inevitably leads to busts.

Recurring bank and currency crises throughout history result from human error and other human frailties that inevitably destroy fiat currency, like the unwillingness to “take away the punchbowl” after a period of prolonged credit expansion. Gold is different. Gold does not need management by a central bank or government. Gold is money that manages itself because growth in the gold stock is controlled by two immutable forces—nature and profitable mining. Together they impose discipline on the production of gold that prevents the money punchbowl from overflowing, which is a key factor explaining why gold preserves purchasing power over time.”

Turk goes on to assert that “the timeless reliability in the interconnection of gold’s supply and demand sets gold apart from national currencies as does its essential nature.”

Gold is tangible; national currencies are intangible financial promises with counterparty risk. This risk arises because promises do get broken, as was demonstrated in the 2008 financial crisis and countless other banking and fiat currency crises. Gold is natural money that has served humanity well throughout history by enabling people to achieve an ever-higher standard of living. We can ponder whether this outcome results from fortuitous chance or from the intelligent design of a creator endowing the earth’s resources providentially to equip humanity with natural money. Regardless of gold’s origin, which is unknowable, it cannot be denied that gold is money and is as useful today as at any time in history.”

3,Chris Powell of GATA provides to us very important physical commentaries

Very surprising: Singapore becomes more open about its gold reserves

(Ronan Manly)

Ronan Manly: Singapore becomes more open about its gold reserves

Submitted by admin on Thu, 2023-08-31 09:12Section: Daily Dispatches

9:12a ET Thursday, August 31, 2023

Dear Friend of GATA and Gold:

Bullion Star gold researcher Ronan Manly this week examines the recent candor of Singapore’s central bank, the Monetary Authority of Singapore, about the nation’s rapidly increasing gold reserves.

Manly’s analysis is headlined “First-Ever Filming of Singapore’s Gold Reserves in Super-Secret Gold Vault” and it’s posted at Bullion Star here:

5 a. IMPORTANT COMMENTARIES ON COMMODITIES: COPPER

First, we had a few years back a nickel fraud. Now its copper

(zerohedge)

EU’s Top Copper Producer Warns Of Massive Theft, Shares Plunge

FRIDAY, SEP 01, 2023 – 06:55 AM

Shares of Europe’s top copper producer in Frankfurt trading plummeted following an announcement that it might have fallen victim to a massive theft, potentially leading to losses of several hundred million euros –adding to the series of turbulence to rock the global metals sector in recent years.

Bloomberg reported that Hamburg-based Aurubis ‘found discrepancies’ in its metal inventories. It said suppliers had manipulated details about the scrap metal shipments, with even its employees in the sampling department covering up the scam.

“What we currently know is that some of our recycling suppliers appear to have manipulated details about the raw materials they deliver to us, and they have been working with employees in our sampling department to hide the shortfall from us,” Angela Seidler, vice president for investor relations and corporate communications, told Bloomberg by phone.

Seidler continued, “Then, in the production process, we have found that the metal is missing, but it is something we have discovered over time because in the case of copper, for example, it takes four weeks for the material to be processed.”

Aurubis expects a detailed report will be completed by the end of September. It said preliminary figures show losses could be in “the low, three-digit-million-euro range.”

The news of the metal theft forced the company to admit its previously forecast operating earnings before taxes of 450 to 550 million euros for this fiscal year is no longer attainable.

“It’s a very serious incident, but the impact of it will be digested within our current fiscal year, and it will not have an impact on our expansion plans and our strategic priorities,” Seidler said.

Shares of Aurubis crashed as much as 17% in Frankfurt trading. Salzgitter, which has a 30% stake in Aurubis, sank 7.3% as it slashed guidance.

Morgan Stanley analyst Ioannis Masvoulas told clients the revelation of the scam is a “negative surprise, which raises uncertainties around inventory management.”

More from Masvoulas’ note (breakdown courtesy of Bloomberg):

Shows a more extensive impact related to alleged criminal activities than previously anticipated

While suggests an inventory writedown in the order of about 3% of market cap, the impact may be bigger on market sentiment toward the company

This setback follows a weaker operating performance that translates to a soft exit rate for FY23

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2555

OFFSHORE YUAN: UP TO 7.2569

SHANGHAI CLOSED UP 13.37 PTS OR 0.43%

HANG SENG CLOSED

2. Nikkei closed UP 81.28 OR 0.28%

3. Europe stocks SO FAR: ALL MOSTLY MIXED

USA dollar INDEX UP TO 103.52 EURO FALLS TO 1.0841 DOWN 1 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.619 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 145.37/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ON SHORE YUAN: UP// OFF- SHORE: UP

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.4725***/Italian 10 Yr bond yield UP to 4.136*** /SPAIN 10 YR BOND YIELD FALLS TO 3.493…**

3i Greek 10 year bond yield FALLS TO 3.691

3j Gold at $1945.10 silver at: 24.63 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 35 /100 roubles/dollar; ROUBLE AT 96.38//

3m oil into the 84 dollar handle for WTI and 87 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 146.35// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.618% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8831 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9573well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.097 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.219 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.837 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 26.71…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 0 BASIS PTS AT 4.4055

end

2.a Overnight: Newsquawk and Zero hedge:

USA EARLY MORNING REPORT

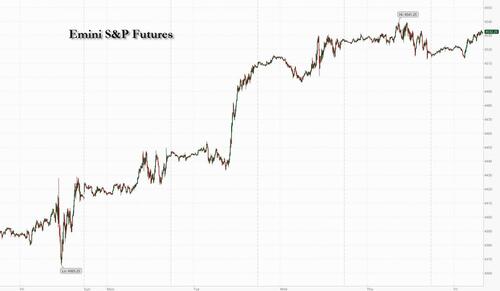

Futures Rise, Yields Dip Ahead Of August Jobs Data

FRIDAY, SEP 01, 2023 – 08:09 AM

Futures and global markets are higher ahead of the NFP today at 8:30am ET (full preview here). At 7:40am ET, S&P futures rose 0.3% to 4,531 with Nasdaq futures up 0.2%. Major global markets are also higher, led by the UK (UKX +0.5%, SX5E +0.4%, SXXP +0.4%, DAX +0.1%), with the final Eurozone Mfg PMI is revised lower to 43.5 from 43.7, further boosting odds the ECB is done. On September ECB, Greg Fuzesi thinks that the July minutes and Isabel Schnabel’s comments yesterday (“growth had “moderated visibly”) both consistent with a pause in September ECB. He expects the final hike to happen in October after a pause in September. China reduced banks’ reserve requirement of foreign currency deposits, boosting the yuan, while China’s Caixin Mfg PMIsurprised to the upside: 51.0 vs. 49.0 survey vs. 49.2 prior. Bond yields are lower and the Bloomberg dollar index is flat. Commodities are mostly stronger led by oil. Key macro focus will be the labor data release today (NFP, Unemployment Rate, Avg. Hourly Earnings, Labor Force Participation) at 8.30am ET and the Mfg ISM at 10am ET.

In premarket trading, Broadcom dropped as much as 4.6% after its revenue forecast disappointed, signaling that demand for electronic components remains sluggish. Dell Technologies jumped 10% after it reported better-than-expected second-quarter revenue, driven by personal computers and data center hardware sales. US-listed Chinese stocks advanced in premarket trading after Beijing and Shanghai both eased housing rules, a sign of further government support toward the economy. Here are some other notable premarket movers:

23andMe jumps 19% after it received FDA 510(k) clearance to report an additional 41 genetic variants in the BRCA1 and BRCA2 genes that increase risk for breast, ovarian, prostate and pancreatic cancer.

Elastic rises 17% after its first-quarter results beat expectations and full-year forecast was raised.

Eos Energy Enterprises soars 50% after announcing that the Department of Energy’s Loan Programs Office has issued an up to $398.6 million conditional commitment to the battery startup.

Lululemon gains 3% as analysts lift their price targets on the the athleisure firm that boosted its net revenue guidance after the close on Thursday.

MongoDB rallies 6.4% after a 55% boost to full-year EPS guidance at mid-point of the outlook range, prompting analysts to raise price targets.

Nutanix jumps 18% as guidance beat expectations. Analysts noted a strong performance in renewals and a share buyback worth $350 million.

SentinelOne gains 2% after estimate-beating results and raised guidance eased investor fears over competition.

Shares in marijuana companies advanced as the Drug Enforcement Agency said Wednesday it would review its classification of cannabis. Canopy Growth gains 12%, Tilray Brands (TLRY) rises 3%, Aurora Cannabis (ACB) is up 2.5%.

Tingo Group falls 14% as short seller Hindenburg Research posted a message about the agri-fintech firm on X.

Friday’s payrolls report (previewed here) should provide further evidence of cooling in the still-tight US labor market. The question is whether that will be enough to stall the Federal Reserve’s tightening cycle or even lead to early rate cuts. Meanwhile, a rapidly weakening economy is likely to tilt the European Central Bank in favor of a pause this month, with no further hikes beyond the current rate of 3.75%, according to Morgan Stanley economists.

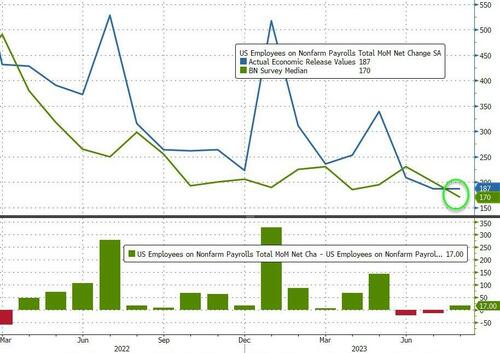

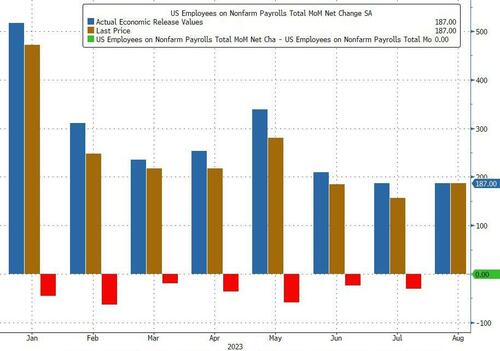

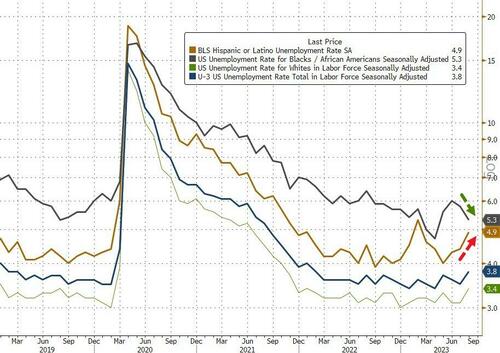

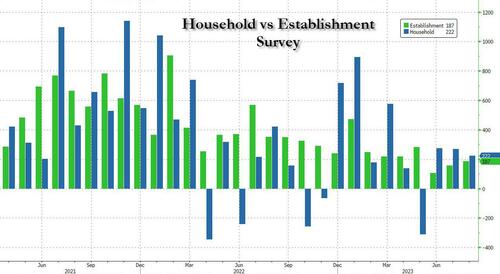

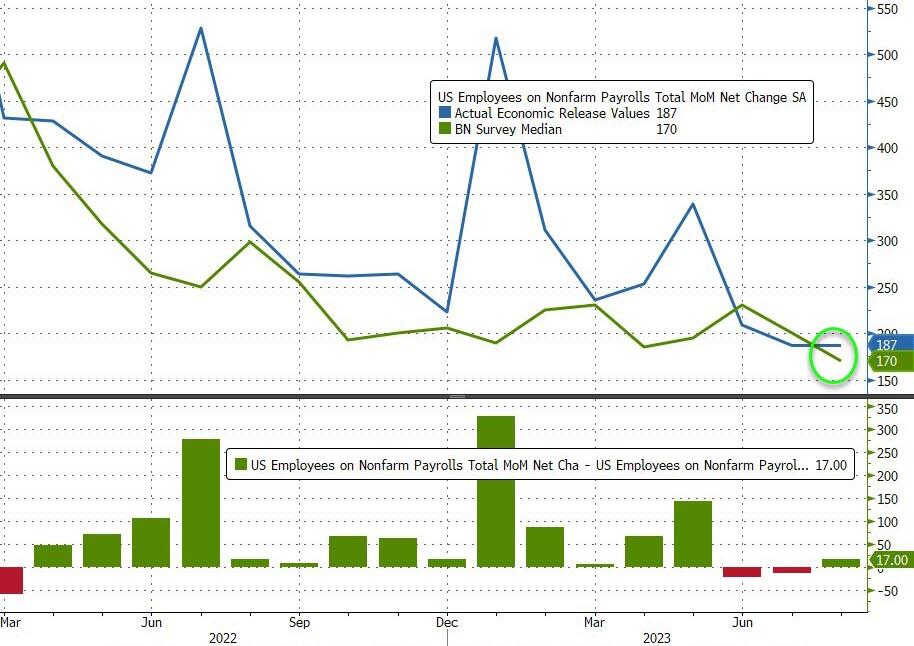

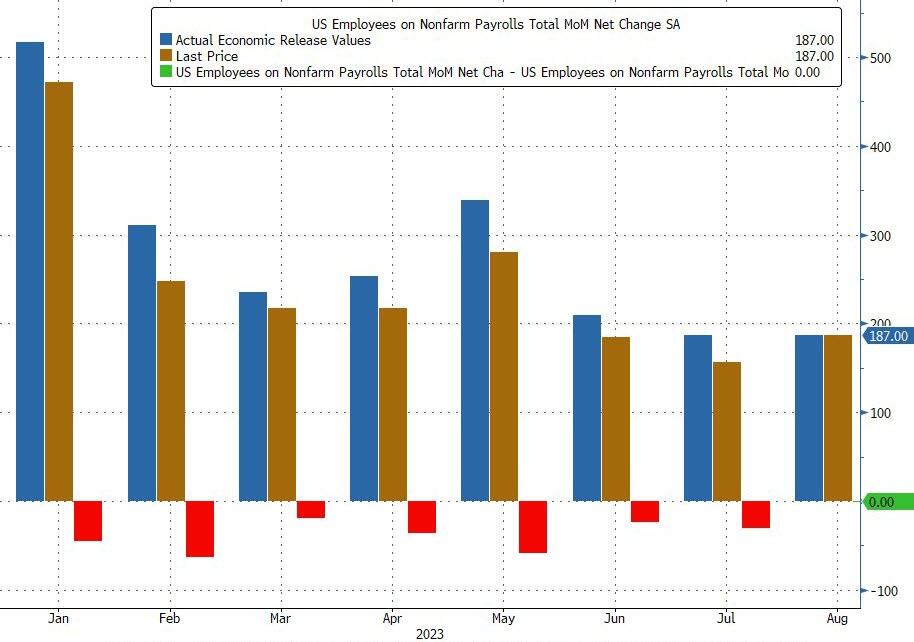

Consensus expects a 170K NFP print with unemployment unchanged at 3.5%, and average hourly earnings dropping to 4.3% YoY from 4.4%. Here is a breakdown of payrolls forecasts by bank:

215,000 – Societe Generale

200,000 – Barclays

200,000 – UBS

175,000 – HSBC

170,000 – Credit Suisse

160,000 – Wells Fargo

155,000 – Morgan Stanley

150,000 – Deutsche Bank

149,000 – Goldman Sachs

130,000 – Citigroup

125,000 – JP Morgan Chase

“I’m personally more inclined toward the soft landing scenario given the resilience of the labor market and inflation slowing down, so I’m not expecting any catastrophic numbers this afternoon,” said Harry Wolhandler, head of equities at Meeschaert Asset Management in Paris. “In any event, should there be bad surprises, the Fed now has room for maneuver to lower rates.”

The Stoxx Europe 600 index rose 0.3%, trimming a bigger gain earlier in the session, with energy majors outperforming as crude oil headed for the biggest weekly advance since April. Miners jumped as China’s latest stimulus measures boosted prices of some industrial metals. Car makers declined, with Renault SA and Volkswagen AG falling more than 3% each after being downgraded to sell by UBS Group AG on increasing competition from Asia. Aurubis AG slumped as much as 18% after Europe’s top copper producer said it faces large losses due to a massive metal theft. Here are the other notable European movers:

Johnson Matthey jumps as much as 14% after Standard Investments, the investment arm of US company Standard Industries, doubles its stake in the British chemicals maker

Vestas gains as much as 3.8% after the wind-turbine manufacturer announced it is close to landing a large order to deliver turbines for a US wind park, a potential respite for the beleaguered industry

European energy stocks outperform after the sector is double-upgraded to overweight at Morgan Stanley, predicting an extended period of strong free cash flow, buybacks and dividend growth

WH Smith gains as much as 4.3% after Goodbody upgraded its recommendation on the UK newsagent and bookstore chain to buy, citing “encouraging momentum” going into the new fiscal year

Boohoo shares rise as much as 10% on Friday, on track for their biggest weekly advance since Nov. 11, after Frasers increases its stake in the online fast fashion retailer

Fielmann Group rises as much as 6.3% after the eyewear company raised its full-year guidance after its recent acquisition of SVS Vision amid what AlsterResearch sees as an attractive market.

AmRest Holdings rise as much as 3.5% after the Polish restaurant operator reported better-than-expected 2Q earnings and gave positive outlook on current trading

Aurubis slumps as much as 18% after Europe’s top copper producer releases an update identifying a large metal theft. Salzgitter, which has a 30% stake in Aurubis, drops 7.3% as it suspends guidance

Renault and Volkswagen decline after both carmakers were cut to sell and given Street-low price targets by UBS, which cites the impact from factors including the rise of Chinese automakers

BioMerieux falls as much as 7.7% after the French diagnostics firm’s second-quarter Ebit slightly missed estimates due to negative currency and M&A effects, overshadowing a beat on overall sales

Earlier in the session, Asian stocks advanced and headed for their second weekly gain, as Chinese equities climbed following more stimulus measures from Beijing. Japan’s benchmark also rose, eyeing an historic milestone. The MSCI Asia Pacific Index rose as much as 0.5%, led higher by Samsung and several Japanese firms.

China shares traded higher and metals looked set to extend this week’s advances after China’s government allowed the nation’s largest cities to cut down payments for home buyers and encouraged lenders to lower rates on existing mortgages as well as on deposits. Meanwhile, Shanghai and Beijing eased home-buying mortgage rules for residents. Hong Kong’s market was shut as the city braced for what may be the strongest storm to hit in at least five years.

The yuan also strengthened after China’s central bank reduced the foreign exchange reserve requirement ratio for financial institutions in a bid to support the currency. The currency has since pared its gains. Sentiment was further buoyed by an unexpected rise in manufacturing data that advanced to 51 in August, the highest reading since February, according to a Caixin survey.

Japan’s Topix benchmark gained nearly 1%, boosted by Sony, putting it on course for its highest close since 1990. The index posted its eighth consecutive month of increase in August — the longest winning streak since 2013 — and the gauge was now set for the best weekly advance since October. Data earlier showed companies’ profits rose 11.6% on an annual basis in the second quarter.

Australia’s ASX 200 declined further under 7,300 and was weighted by its metals names as Fortescue Metals slumped after its CFO left three days after the CEO’s departure. Korea’s KOSPI was underpinned by the South Korean trade data which printed better than feared.

Indian stocks posted their biggest advance in two months on Friday as metals and utilities led the rally across sectors after strong economic data boosted investor sentiment. The S&P BSE Sensex Index rose 0.9% to 65,387.16 in Mumbai, while the NSE Nifty 50 Index advanced by a similar measure as both gauges surged the most since June 30. The sharp move pushed the benchmarks by at least 0.7% higher for the week, snapping their retreat for preceding five weeks. Stocks in India have been receiving a chunk of foreign flows coming to emerging markets. For August, foreigners bought $1.6 billion of local shares while selling Taiwan, South Korea and Indonesia, and extending a selloff in China.

In FX, the Bloomberg Dollar Spot Index was little changed on Friday but down 0.2% this week, set to halt six straight weeks of gains after data showed the Federal Reserve’s preferred measure of underlying inflation posted the smallest back-to-back increases since late 2020. Focus now is on US payrolls data later on Friday, which is expected to show the US labor market likely cooled in August

Further dollar declines could be limited. “The path to more pronounced dollar depreciation — further moderation in the US economic data, including nonfarm payrolls report, combined with less negativity abroad — has been narrowing lately,” wrote Goldman Sachs strategist Karen Fishman, and since Goldman’s sellside desk is always wrong, it means the dollar is about to crater.

EUR/USD recouped some lost ground ahead of the key US data. The common currency fell yesterday after bearish comments from European Central Bank officials fueled concern the euro region may be heading for stagflation.

USD/JPY little changed at 145.49. The pair recovered from an intraday low of 145.24 after Japanese Finance Minister Shunichi Suzuki said sudden moves in the foreign currency market aren’t desirable, and he will closely watch movements

A 0.3% rise in the Aussie dollar on China’s FX RRR cut was reversed in part by leveraged selling shortly after by weak domestic home loan data. Move extended under weight of early London names selling to partially fill in option and exporter related bids under 0.6450 strikes, according to traders

In rates, treasuries were mixed in early US trading ahead of the August employment report, with the curve steeper. With Fed swaps pricing in about 50% odds of another rate hike this year, report is anticipated to show 170k nonfarm payrolls increase, smallest in more than two years; crowd-sourced whisper number is 155k. Yields remain within 2bp of Thursday’s closing levels; Thursday’s ranges included weekly lows for 10-year to 30-year tenors. 2s10s and 5s30s spreads are wider by 2bp-3bp, paced by curve-steepening in most euro-zone bond markets. The economic calendar also includes August final S&P Global US Manufacturing PMI at 9:45am, July construction spending and August ISM manufacturing at 10am and August vehicle sales throughout the day.

In commodities, oil is set for a weekly gain after Russia signaled that it would extend export curbs and US inventories dropped further. Gold headed for the second weekly advance.

Looking to the day ahead now, and the main highlight will be the US jobs report for August. Otherwise, we’ll get the global manufacturing PMIs for August and the ISM manufacturing reading from the US. From central banks, we’ll hear from the Fed’s Bostic and Mester.

Market Snapshot

S&P 500 futures up 0.2% to 4,526.00

MXAP up 0.4% to 162.78

MXAPJ up 0.3% to 508.53

Nikkei up 0.3% to 32,710.62

Topix up 0.8% to 2,349.75

Hang Seng Index down 0.5% to 18,382.06

Shanghai Composite up 0.4% to 3,133.25

Sensex up 0.8% to 65,348.50

Australia S&P/ASX 200 down 0.4% to 7,278.30

Kospi up 0.3% to 2,563.71

STOXX Europe 600 up 0.2% to 459.33

German 10Y yield little changed at 2.49%

Euro little changed at $1.0852

Brent Futures up 0.3% to $87.13/bbl

Gold spot up 0.1% to $1,942.47

US Dollar Index little changed at 103.57

Top Overnight News from Bloomberg

Markets settled into a holding pattern ahead of Friday’s key US jobs data, with European stocks and American equity-index futures edging higher, Treasury yields flat and a gauge of the dollar steady.

China intensified efforts to stimulate the economy and support its currency, as investor concerns over the growth outlook persist. The central bank will trim the amount of foreign currency deposits banks are required to hold as reserves for the first time this year, the People’s Bank of China said Friday.

Dollar General Corp., already on track for its first annual share decline, fell again after cutting its profit forecast for the second straight quarter amid rising labor costs and “softer sales trends.”

US and other Group of Seven nations increasingly see evidence of deep-seated structural problems in China that ultimately will strengthen the West’s hand against a weakening geopolitical competitor. The view emerging from officials in Washington, Rome, Tokyo and other capitals, who spoke with Bloomberg News mostly on condition of anonymity in recent days, is that the dominant economic narrative that has guided the flows of capital around the globe for decades is flipping fast.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed following a similar lead from Wall Street, whilst Hong Kong markets were closed due to Typhoon Saola. ASX 200 declined further under 7,300 and was weighted by its metals names as Fortescue Metals slumped after its CFO left three days after the CEO’s departure. Nikkei 225 opened in the red but quickly trimmed losses with the rebound spearheaded by the energy sector. KOSPI was underpinned by the South Korean trade data which printed better than feared. Shanghai Comp opened firmer after large Chinese banks cut their deposit rates, while the PBoC also lowered down payment for first and second-time home buyers and announced a cut to the FX RRR. Modest upticks were seen after the Caixin PMI Finals were surprisingly revised into expansion territory.

Top Asian News

PBoC is to cut FX RRR by 2ppts to 4% (prev. 6%) from September 15th, according to the central bank. China’s Global Times, on the PBoC FX RRR cut, said “This move aims to enhance the ability of financial institutions to utilize foreign exchange capital.”

Several major Chinese banks lowered their deposit rates, including ICBC, China Construction Bank, Bank of Communications, and Bank of China.

China’s Shenzhen City will suspend work, businesses, transportation, and markets from Friday afternoon amid Typhoon Saola, according to the Shenzhen Government.

PBoC sold CNY 101bln via 7-day reverse repos with the rate at 1.80% for a CNY 120bln net injection.

China to take additional action to revive the property sector, via Reuters citing sources; incl. relaxing home purchase curbs and removing caps on new homes.

Softbank’s (9984 JT) Arm Holdings is expected to set a price range for its IPO next week, with plans to price its shares on September 13th and trading to start the following day, according to Reuters sources.

Japanese Finance Minister Suzuki said FX moves should be set by the market and should reflect fundamentals; sudden FX moves are undesirable, according to Reuters.

European bourses are in the green, Euro Stoxx 50 +0.3%, as modest upside creeps in following a tentative/slightly subdued open with fundamentals light ahead of key US data. Sectors are primarily positive, Energy the clear outperformer after an MS upgrade and broader benchmark action while Autos lag following a negative Volkswagen broker move and as Tesla cuts prices in China for some models. Stateside, futures are in-fitting with Europe and are slightly firmer, ES +0.2%. with the tone equally as tentative before NFP & ISM Manufacturing.

Top European News

ECB’s de Guindos said the latest data from July and August point towards economic deceleration in Q3 and probably in Q4, and the ECB needs to keep working to bring inflation back to the 2% target. He said the latest data from inflation in August has been very similar to July, and the rate decision in September is still up for debate. He said data in the next few days is key to the September ECB decision, according to Reuters.

ECB’s Villeroy says after overall inflation peaked and underlying inflation has also peaked since April and appears to have begun its decline. This encouraging sign is still far from sufficient. Options are open at the next and upcoming meetings. Very close to a peak in rates, far from the point where we could consider cuts. Keeping rates high for long enough matters more than the level. Will slightly revise up France’s 2023 GDP forecast.

ECB’s Vujcic says inflation data in August was in-line with expectations, economic activity is slowing faster than forecast. Will not know in September, October or November where the terminal is. Inflation will ease in the coming months but there is a risk that disinflation will stall above the target.

BoE’s Pill says BoE needs to be particularly wary about letting an inflation persistence dynamic to set in; we have not yet seen a downturn in core inflation which would reassure us.

FX

Buck bounces from overnight lows, but is contained overall ahead of US payrolls, DXY sits within 103.480-770 range.

Franc a tad firmer in line with Swiss YY CPI vs consensus, USD/CHF towards base of 0.8813-46 parameters.

Euro, Pound, Yen and Loonie all rangy pre-NFP and Canadian GDP, EUR/USD around 1.0850 and surrounded by hefty expiries, Cable hovering below 1.2700, USD/JPY pivoting 145.00 and USD/CAD straddling 1.3500.

Yuan underpinned by multiple factors including 200 bp RRR cut and surprise upgrade to Caixin Chinese manufacturing PMI to growth from contraction, USD/CNY close to 7.2450 and USD/CNH sub-7.2400 at one stage.

PBoC set USD/CNY mid-point at 7.1788 vs exp. 7.2967 (prev. 7.1811)

Fixed Income

Debt succumbs to some consolidation as the turn of the month comes with key US macro releases via NFP and the manufacturing ISM.

Bunds, Gilts and T-note all in negative territory after Thursday’s rallies and within 133.13-132.76, 95.49-14 and 110-31+/27 respective ranges.

Commodities

Crude benchmarks are in the green but only modestly so and taking impetus from the USD rather than any specific crude driver with the overall tone tentative pre-NFP.

Dutch TTF has pared back to near the unchanged mark after initial gains as Chevron workers rejected the first mediation package ahead of potential strikes on September 7th.

Spot gold is at the top-end of parameters but as above this is relatively modest with specifics light while base metals have returned firmly to the green as China unveils further stimulus.

Crude futures were on a slightly firmer footing and extended on the prior session’s gains, with Brent testing 87/bbl to the upside as it takes aim at the August high of USD 87.37/bbl.

Spot gold saw an uptick as the DXY pulled back but price action remains within yesterday’s range and under USD 1,950/oz ahead of NFPs.

Copper futures were lifted on the aforementioned China announcement, with 3M LME copper briefly topping USD 8,500/t to the upside.

Chevron’s (CVX) Australia LNG workers reject the Co’s bargaining offer, according to unions; less than 1% of the Wheatstone and Gorgon downstream workforce voted in support of the offer, according to Reuters. Subsequently, sources report that CVX and unions will meet for talks next week.

Russia introduced a 7% export duty on a number of fertilisers from September 1st, according to Interfax.

Geopolitics

Japan imposed additional sanctions against North Korea, according to Reuters.

US Event Calendar

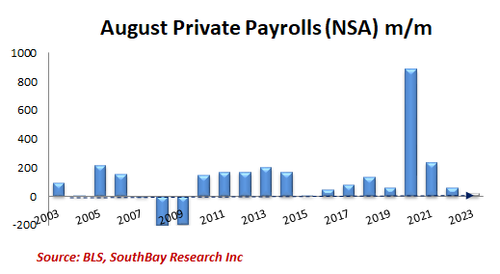

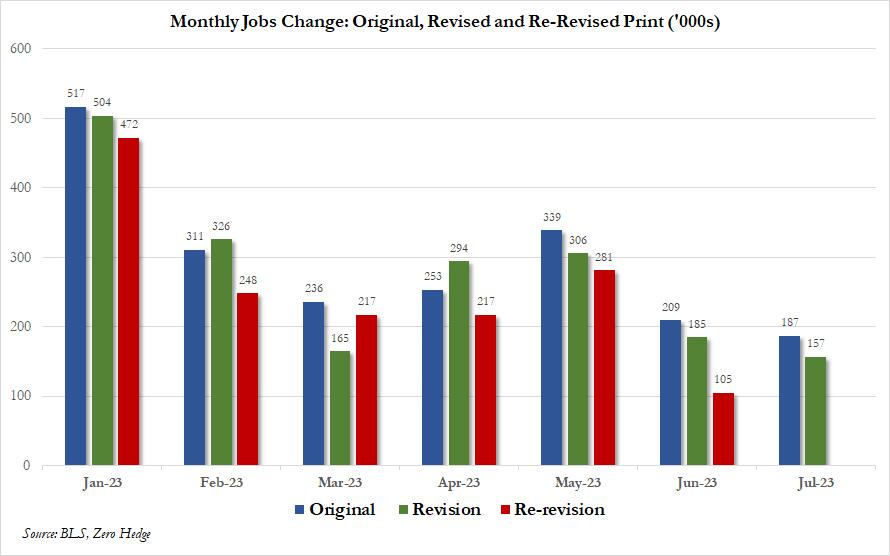

08:30: Aug. Change in Nonfarm Payrolls, est. 170,000, prior 187,000

Change in Private Payrolls, est. 148,000, prior 172,000

Change in Manufact. Payrolls, est. zero, prior -2,000

08:30: Aug. Average Hourly Earnings MoM, est. 0.3%, prior 0.4%

Average Hourly Earnings YoY, est. 4.3%, prior 4.4%

Average Weekly Hours All Emplo, est. 34.3, prior 34.3

08:30: Aug. Unemployment Rate, est. 3.5%, prior 3.5%

Underemployment Rate, prior 6.7%

Labor Force Participation Rate, est. 62.6%, prior 62.6%

09:45: Aug. S&P Global US Manufacturing PM, est. 47.0, prior 47.0

10:00: July Construction Spending MoM, est. 0.5%, prior 0.5%

10:00: Aug. ISM Manufacturing, est. 47.0, prior 46.4

Central Bank Speakers

06:00: FEd’s Bostic Speaks on US Monetary Policy

09:45: Fed’s Mester Speaks on Inflation

DB’s Jim Reid concludes the overnight wrap

Welcome to September and to an early month payrolls Friday. Spare a thought for me this weekend as I’ll be refereeing 40 plus over excited 6 year olds playing Laser Quest as our twins have their birthday party on Sunday. My advice to all the graduates just joining the industry and reading this is to have your kids young while you have lots of energy. Then when you get to my age you can have easy paced relaxing weekends rather than the ones I have. I’m going to be especially exhausted by Monday.

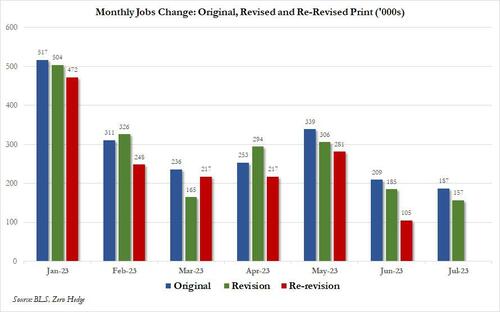

Since it’s the start of the month, we’ll shortly be releasing our monthly performance review for August, which has been a pretty challenging one for financial markets albeit one where markets had a much better last week or so. In the month we had a further softening in the economic data, particularly in Europe and China, which has led to growing concern about the near-term outlook. At the same time, there’s been rising speculation that interest rates are set to remain higher for longer, and earlier in the month we even saw the 10yr Treasury yield hit a post-GFC high after both a US government debt downgrade and a much higher Treasury issuance profile announced than expected. So a lot going on in a holiday heavy month. See the full report in your inboxes shortly.

August might not have been a great month overall, but since Jackson Hole last week, we’ve actually had a decent market rally though one that lost a little momentum in the last 24 hours. Yesterday saw the S&P 500 (-0.16%) end a four-day winning streak after a sell off late in the US session, whilst the 10yr Treasury yield (-0.7bps) retreated for a 5th day running. Fresh China stimulus overnight (more below) has restored a little momentum as we start September.

For much of the final day of the month yesterday, markets were supported by the data alongside several central bank speakers who sounded cautious about further rate hikes. For instance in the US, the weekly initial jobless claims fell back to 228k over the week ending August 26 (vs. 235k expected), which is their third consecutive decline. Furthermore, the PCE inflation numbers for July were also in decent shape, and that’s the number the Fed officially targets. The important takeaway was that the year-on-year number for core PCE only rose a tenth to 4.2%, which is beneath the 4.3% estimate that Chair Powell cited in his speech last week. So things are running a bit better than the Fed was expecting even a week ago. Slightly concerningly, the supercore services measure often referred to by the Fed was up a strong +0.45% on the month. But more encouragingly, our US economists noted that the 1-month annualised rate of trimmed mean PCE was only +2.4%, its lowest since spring 2021. So take your pick.

In conjunction with the inflation data, we had several remarks from central bank officials that added to hopes they might be done with their rate hikes. That included Atlanta Fed President Bostic, who said that “I feel policy is appropriately restrictive”, and that “we should be cautious and patient and let the restrictive policy continue to influence the economy, lest we risk tightening too much and inflicting unnecessary economic pain.” Meanwhile at the ECB, Isabel Schnabel of the Executive Board said that recent developments “point to growth prospects being weaker than foreseen in the baseline scenario” in the June projections. She also said that whilst further rate hikes could be warranted, there was also an acknowledgement that “should our assessment of the transmission of monetary policy suggest that the pace of disinflation is proceeding as desired, we may afford to wait until our next meeting”. We also got the accounts of the ECB’s July meeting, which showed a moderation of the ECB’s hawkish bias. See our European economists’ reaction note here.

When it comes to the ECB’s decision in a couple of weeks, yesterday brought another piece of the jigsaw with the flash CPI print for August. That showed headline inflation remaining at +5.3%, whilst core inflation fell back two-tenths to +5.3%. While the core print was in line with consensus, our economists note that the underlying momentum was more encouraging, with services inflation easing slightly despite upside in volatile package holidays. The global trend, the inflation data, and the Schnabel remarks helped dial back the chances of a rate hike in September, with market pricing moving from a 55% chance at the previous close, down to 40% immediately prior to the CPI print (after Schnabel’s comments) and to 24% by the close. That’s the lowest chance the market has given a September hike since May, so as it stands we’re getting to the point where it would actively be a surprise if the ECB didn’t pause. In turn, those expectations of a pause led to a significant rally among European sovereign bonds, with yields on 10yr bunds (-8.1bps), OATs (-8.3bps) and BTPs (-7.7bps) seeing big declines.

Looking forward, we’ve got a couple of important releases today that might give us extra clues on the hard vs soft landing debate. The most important will be the US jobs report for August, which is out at 13:30 London time. Our US economists expect nonfarm payrolls growth to slow to +150k (consensus at +170k). That would be the slowest print since December 2020, and they see that causing the unemployment rate to move up a tenth to 3.6%. The other release of note will be the ISM manufacturing, which has now been in contractionary territory for 9 months in a row.

With another round of data to look forward to, US equities were in something of a holding pattern. Having started the day up by nearly +0.4% in the morning, the S&P 500 ended up closing -0.16% down after a late sell-off. Healthcare services (-2.65%) and banks (-0.73%) were among the underperformers. Meanwhile, tech stocks outperformed, with the NASDAQ (+0.11%) hitting a 4-week high as it eked out a fifth consecutive gain. Over in Europe, equities saw a subdued performance, with the STOXX 600 down -0.20%.

Asian equity markets are trading higher this morning as China ramped up its efforts to support the economy after the People’s Bank of China (PBOC) reduced the amount of foreign exchange that financial institutions must hold as reserves for the first time this year. Starting from September 15, the central bank will lower the forex reserve ratio to 4% from the current level of 6%, a move aimed at reining in yuan weakness. The offshore yuan did spike +0.5% on the news but has settled only +0.1% higher as we type. Additionally, China’s Caixin manufacturing PMI rose to 51.0 in August, the highest reading since February compared to a level of 49.2 in July.

In terms of equity market moves, the Nikkei (+0.53%) is leading gains overnight, while the CSI (+0.51%), the Shanghai Composite (+0.25%), and the KOSPI (+0.17%) are also trading in positive territory. Elsewhere, trading in Hong Kong has been suspended for today as the city is bracing itself for super Typhoon Saola. S&P 500 (+0.10%) and NASDAQ 100 (+0.07%) futures are trading slightly higher.

Looking back at yesterday’s other data, there was a decent +0.8% jump in US personal spending in July (vs. +0.7% expected) supporting the evidence of strong start to the quarter. However, the savings rate fell back to an 8-month low of 3.5% and incomes were a tenth below expectations at +0.2%. Otherwise, the MNI Chicago PMI for August rose to a one-year high of 48.7 (vs. 44.2 expected) and 42.8 last month. Earlier in the day, German retail sales for July disappointed (-0.8% vs +0.3% expected) in a latest sign of growth struggles for Europe’s largest economy.

To the day ahead now, and the main highlight will be the US jobs report for August. Otherwise, we’ll get the global manufacturing PMIs for August and the ISM manufacturing reading from the US. From central banks, we’ll hear from the Fed’s Bostic and Mester.

2 B) NOW NEWSQUAWK (EUROPE/REPORT)/

2 c. ASIAN AFFAIRS

FRIDAY MORNING/THURSDAY NIGHT

SHANGHAI CLOSED UP 13.37 PTS OR 0.43% //Hang Seng CLOSED /The Nikkei CLOSED UP 91.28 PTS OR 0.28% //Australia’s all ordinaries CLOSED DOWN 0.37 % /Chinese yuan (ONSHORE) closed UP 7.2555 /OFFSHORE CHINESE YUAN UP TO 7.2569 /Oil UP TO 84.84 dollars per barrel for WTI and BRENT UP AT 87.69 / Stocks in Europe OPENED ALL MOSTLY MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

2 d./NORTH KOREA/ SOUTH KOREA/

////SOUTH KOREA/NORTH KOREA/

END

2e) JAPAN

JAPAN

3 CHINA /

CHINA/

China cuts its foreign exchange reserves to 4% from 6% to free up dollars. This will be a temporary fix as the yuan should again next week to falter

(zerohedge)

China Cuts FX Reserve Ratio To 4%, Unlocking $19BN, In Most “Visible” Step Yet To Prop Up Slumping Yuan

THURSDAY, AUG 31, 2023 – 10:18 PM

Following the news two weeks ago that China had suffered the largest FX outflow in a year…

… when in July, China suffered $25BN in net outflows via onshore outright spot transactions, offset by $14BN inflows via freshly entered and canceled forward transactions and further outflows via the SAFE dataset on “cross-border RMB flows” which amounted to another $16BN in the month, resulting in net total of $26BN in July outflows, the most since Sept 22, Beijing started taking the accelerating collapse in the yuan very seriously.

So seriously that it not only declared war on yuan bears with the first ever 1000+ pip gap between the yuan fix and estimates, one which has persisted for the past two weeks culminating with a near record gap of 1,092 moments ago…

… but a few days later, the PBOC orchestrated the biggest offshore liquidity crunch in hopes of sparking a short squeeze, when the Hong Kong’s offshore yuan interbank rate climbed to the highest since 2018, making holding on to a short yuan position extremely painful.

Neither did much, and the yuan continued to drift not too far from its lowest level on record, just as Citi strategists Philip Yin and Gaurav Garg correctly predicted:

“A CNH funding squeeze could be a tactical tool and a signaling device, but unlikely the go-to tool in isolation. Overall, the combination of rate cut and other FX tools suggest that fundamental-driven yuan weakness is allowed but the pace is managed.”