SEPT 18/GOLD CLOSED UP $8.40 TO $1932.00 SILVER CLOSED UP 11 CENTS TO $23.20 //PLATINUM CLOSED UP $26.10 TO $936.65 WHILE PALLADIUM CLOSED DOWN $2.65 TO $1248.45/GOOD GOLD COMMENTARY TODAY FROM MATHEW PIEPENBURG//CHINA EXPERIENCES HUGE OUTFLOWS OF DOLLARS AS ITS ECONOMY IS IMPLODING//ITALY OVERWHELMED WITH MIGRANT INFLUX///IRAN AND USA EXCHANGE PRISONERS IN A RANSOM DEAL//COVID UPDATES/VACCINE UPDATES/DR PAUL ALEXANDER/NEW ADDICTS/EVOL NEWS//UAW STILL FAR APART IN THEIR NEGOTIATIONS WITH THE 3 CAR COMPANIES//SWAMP STORIES FOR YOU TONIGHT//

435 H SCOTIA CAPITAL 1 624 H BOFA SECURITIES 1 737 C ADVANTAGE 2

TOTAL: 2 2 MONTH TO DATE: 3,842

JPMorgan stopped 0/2 contracts.

FOR SEPT.:

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2023. CONTRACT: 2 NOTICES FOR 200 OZ or 0.0622 TONNES

total notices so far: 3842 contracts for 384,200 oz (11.9502 tonnes)

FOR SEPT:

SILVER NOTICES: 7 NOTICE(S) FILED FOR 35,000 OZ/

total number of notices filed so far this month : 2611 for 13,055,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $8.40

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD//

INVENTORY RESTS AT 880,27 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 11 CENTS AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.651 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 441.332 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GIGANTIC SIZED 1088 CONTRACTS TO 125,698 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.16 GAIN IN SILVER PRICING AT THE COMEX ON FRIDAY. TAS ISSUANCE WAS A HUGE SIZED 917 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON FRIDAY NIGHT: 917 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.16). BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS DESPITE HAVING A HUMONGOUS SIZED LOSS OF 2677 CONTRACTS ON BOTH EXCHANGES WE HAD WITH CONSIDERABLE T.A.S.LIQUIDATION AT HIGHER PRICES THROUGHOUT THE FRIDAY COMEX SESSION AS OUR SHORT SPECULATORS CAPITULATED AND COVERED WITH RECKLESS ABANDON.

WE MUST HAVE HAD:

A FAIR ISSUANCE OF EXCHANGE FOR PHYSICALS( 355 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 14.420 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S SMALL QUEUE JUMP OF 20,000 OZ//NEW TOTAL 13.385 MILLION OZ + OUR CRIMINAL ISSUANCE OF 0 EXCHANGE FOR RISK CONTRACTS//NEW TOTALS EXCHANGE FOR RISK: 3.0 MILLION OZ: NEW TOTALS SILVER STANDING: 16.385 MILLION OZ// /// / //HUGE SIZED COMEX OI LOSS/ FAIR SIZED EFP ISSUANCE/VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 917CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -20 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTRACTS for 11 days, total 8389 contracts: OR 41.945 MILLION OZ (762 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 41.945 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 41.945 MILLION OZ (SMALLER THIS MONTH)

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1088 CONTRACTS DESPITE OUR STRONG GAIN IN PRICE OF $0.16 IN SILVER PRICING AT THE COMEX//FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR EFP ISSUANCE CONTRACTS: 355 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR SEPT OF 14.2 MILLION OZ FOLLOWED BY TODAY’S 20,000 OZ QUEUE JUMP .+ 0 MILLION OZ EXCHANGE FOR RISK//PRIOR TOTAL FOR EXCHANGE FOR RISK = 3.0 MILLION OZ/TOTAL EXCH. FOR RISK /NEW TOTALS STANDING 16.385 MILLION OZ// /// WE HAVE A HUGE SIZED LOSS OF 753 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 917 CONTRACTS//CONSIDERABLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE FRIDAY COMEX SESSION AS THE SHORTS CAPITULATED. THE NEW TAS ISSUANCE FRIDAY NIGHT (917) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 7 NOTICE(S) FILED TODAY FOR 35,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 424 CONTRACTS TO 441,073 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED: 411 CONTRACTS

WE HAD A SMALL SIZED INCREASE IN COMEX OI ( 424 CONTRACTS) DESPITE OUR STRONG $13.20 GAIN IN PRICE//FRIDAY. WE ALSO HAD A RATHER STRONG INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 12.656 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 200 OZ QUEUE JUMP//NEW TOTAL STANDING 14.495 TONNES + /A FAIR (AND CRIMINAL) ISSUANCE OF 1133 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH OUR$13.20 GAIN IN PRICEWITH RESPECT TO FRIDAY’S TRADING.WE HAD A FAIR SIZED GAIN OF 3268 OI CONTRACTS (10.164 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2844CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 441,484

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3268 CONTRACTS WITH 424 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 2844 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3268CONTRACTS OR 10.164 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 1133 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2844 CONTRACTS) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (424) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 3268 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 12.656 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 200 OZ/// 3) ZERO LONG LIQUIDATION WITH STRONG TAS LIQUIDATION COVERING THEIR SHORTFALL DURING THE COMEX SESSION //4) SMALL SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 1133 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT :

TOTAL EFP CONTRACTS ISSUED: 26,113 CONTRACTS OR 2,611,300 OZ OR 81.222 TONNES IN 11 TRADING DAY(S) AND THUS AVERAGING: 2373 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAY(S) IN TONNES 81.222 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 81.222/3550 x 100% TONNES 2.28% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 81.222 TONNES (SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUGE SIZED 1088 CONTRACTS OI TO 125,698 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A FAIR 355 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 335and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 355 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1088 CONTRACTS AND ADD TO THE 355 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 753 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTAL 3.765 MILLION OZ

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

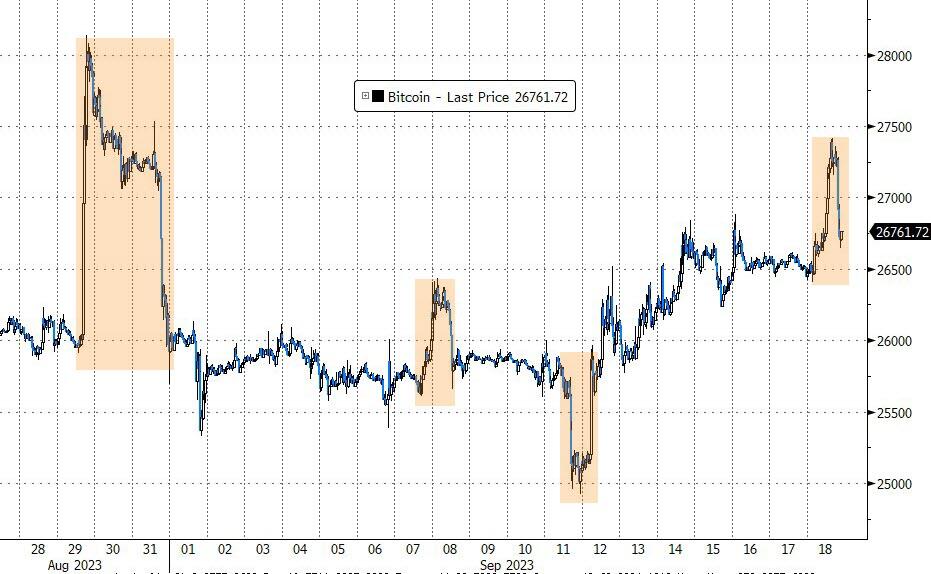

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

MONDAY MORNING//SUNDAY NIGHT

SHANGHAI CLOSED UP 8,19 PTS OR 0.26% //Hang Seng CLOSED DOWN 252.34 PTS OR 1.39%/ /The Nikkei CLOSED //Australia’s all ordinaries CLOSED DOWN 0.73 % /Chinese yuan (ONSHORE) closed DOWN AT 7.2956 /OFFSHORE CHINESE YUAN DOWN TO 7.2975 /Oil UP TO 91.37 dollars per barrel for WTI and BRENT UP AT 94.35 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 424CONTRACTS TO 441,073 DESPITE OUR STRONG GAIN IN PRICE OF $13.20 ON FRIDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2844 EFP CONTRACTS WERE ISSUED: : DEC 2844 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2844 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 3268 CONTRACTS IN THAT 2844LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED GAIN OF 424 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $13.20//FRIDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR FRIDAY NIGHT WAS A FAIR 1133 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: SEPT (14.500) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 14.500 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $13.20) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR GAIN OF 3268 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD A ZERO T.A.S. LIQUIDATION ON THE FRONT END OF FRIDAY’S TRADING. THE T.A.S. ISSUED ON FRIDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 11.443 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPT. (12.656 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 200 OZ//NEW STANDING 14.500 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $13.20.

WE HAD – REMOVED 411 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 3268 CONTRACTS OR 326,800 OZ OR 10.164 TONNES.

Estimated gold volume today:// 135,347 awful

final gold volumes/yesterday 207,824 poor//speculators have left the gold arena

Total monthly oz gold served (contracts) so far this month

3842 notices 384200 OZ 11.9502 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposit:

total dealer deposits: NIL oz

customer deposits: 0

total customer deposits: nil oz

we had 0 customer withdrawal

total withdrawals NIL oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPTEMBER.

For the front month of SEPTEMBER we have an oi of 822 contracts having LOST 12 contracts. We had

14 contracts were served on FRIDAY, so we gained an additional 2 CONTRACTS or AN ADDITIONAL 200 oz will stand for delivery in this non active delivery month of Sept.

Oct LOST 883 contracts to 24,544 contracts.

NOV GAINED 3 CONTRACTS to stand at 23

December GAINED 860 contracts UP to 377,415 contracts.

We had 2 contracts filed for today representing 200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 2 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2023. contract month,

we take the total number of notices filed so far for the month (3842 x 100 oz ), to which we add the difference between the open interest for the front month of SEPT (822 CONTRACTS) minus the number of notices served upon today 2 x 100 oz per contract equals 466,200 OZ OR 14.500 TONNES the number of TONNES standing in this non active month of SEPT.

thus the INITIAL standings for gold for the SEPTcontract month: No of notices filed so far (3842) x 100 oz + (822) {OI for the front month} minus the number of notices served upon today (2) x 100 oz) which equals 466,200 oz standing OR 14.500 TONNES

TOTAL COMEX GOLD STANDING: 14.500 TONNES WHICH IS HUGE FOR AN INACTIVE DELIVERY MONTH.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 20,878,273.020 OZ

TOTAL REGISTERED GOLD 10,801,765.332 (335,98 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,076,507.688 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,747,673 OZ (REG GOLD- PLEDGED GOLD) 272.08 tonnes//dropping like a stone

END

SILVER/COMEX

SEPT 18

//2023// THE SEPT 2023 SILVER CONTRACT

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

399,684.870 oz CNT

.

Deposits to the Dealer Inventory

nil

Deposits to the Customer Inventory

2983.10 oz

No of oz served today (contracts)

7 CONTRACT(S) (35,000 OZ)

No of oz to be served (notices)

66 contracts (330,000 oz)

Total monthly oz silver served (contracts)

2611 Contracts (13,055,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposit: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposit customer account:

i) Into Delaware 2983.10 oz

total customer deposit 2983.10 oz

JPMorgan has a total silver weight: 136.901 million oz/272.385 million or 50.36%

Comex withdrawals 1

i) Out of CNT: 399,684.874 oz

total: 399,684.874 oz

adjustments: 0

TOTAL REGISTERED SILVER: 42.405 MILLION OZ//.TOTAL REG + ELIGIBLE. 272.385 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR August:

silver open interest data:

FRONT MONTH OF SEPT /2023 OI: 73 CONTRACTS HAVING LOST 9 CONTRACT(S). WE HAD 13

CONTRACT SERVED ON FRIDAY. SO WE GAINED 4 CONTRACTS OR 20,000 OZ WILL STAND FOR SILVER AT THE COMEX..

OCT LOST 60 CONTRACTS TO STAND AT 1083.

NOVEMBER GAINED 2 CONTRACTS TO STAND AT 136

DEC. LOST 1935 CONTRACTS TO STAND AT 113,251 .

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 7 for 35,000 oz

Comex volumes// est. volume today 45,226 poor

Comex volume: confirmed yesterday 68,706 fair

To calculate the number of silver ounces that will stand for delivery in SEPT. we take the total number of notices filed for the month so far at 2611 x 5,000 oz = 13,055,000 oz

to which we add the difference between the open interest for the front month of SEPT (73) and the number of notices served upon today 7 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT/2023 contract month: 2611 (notices served so far) x 5000 oz + OI for the front month of SEPT (73) – number of notices served upon today (7 )x 500 oz of silver standing for the SEPT contract month equates to 13.3850 million oz. + 0 MILLION EXCHANGE FOR RISK..NEW TOTALS EXCHANGE FOR RISK: 3.0 MILLION OZ//NEW TOTAL STANDING FOR SILVER: 16.385 MILLION OZ//

There are 42.145 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

SEPT 18/WITH GOLD UP $8.40 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD : A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 880.217 TONNES

SEPT 15/WITH GOLD UP $13.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD : A WITHDRAWAL OF 1.055 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 879.70 TONNES

SEPT 14/WITH GOLD UP $1.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD : A WITHDRAWAL OF 4.63 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 882.01 TONNES

SEPT 13/WITH GOLD DOWN $2.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 12/WITH GOLD DOWN $11.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 11/WITH GOLD UP $4.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 8/WITH GOLD UP $0.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 7/WITH GOLD DOWN $0.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.22 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.69 TONNES

SEPT 6/WITH GOLD DOWN $8.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.81 TONNES

SEPT 5/WITH GOLD DOWN $13.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.97 TONNES

SEPT 1/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 31/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 30/WITH GOLD UP $8.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.59 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.23 TONNES

AUGUST 29/WITH GOLD UP 17.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.6 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.64 TONNES

AUGUST 28/WITH GOLD UP $6.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / //INVENTORY RESTS AT 884.04 TONNES

AUGUST 25/WITH GOLD DOWN $6.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 884.04 TONNES

AUGUST 24/WITH GOLD UP $0.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //INVENTORY RESTS AT 884.91 TONNES

AUGUST 23/WITH GOLD UP $21.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 4.32 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 884.91 TONNES

AUGUST 22/WITH GOLD UP $2.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 0.87 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 889.23 TONNES

AUGUST 21/WITH GOLD UP $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.60 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 890.10 TONNES

AUGUST 18/WITH GOLD UP $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 6.92 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 887.50 TONNES

AUGUST 17/WITH GOLD DOWN $12.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: /// //INVENTORY RESTS AT 894.42 TONNES

GLD INVENTORY: 880.217 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 18/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 1.651 MILLION OZ INTO THE SLV. : // /.////INVENTORY RESTS AT 441.332 MILLION OZ

SEPT 15/WITH SILVER UP 37 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.31 MILLION OZ FROM THE SLV. : // /.////INVENTORY RESTS AT 439.681 MILLION OZ

SEPT 14/WITH SILVER DOWN 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: : // /.////INVENTORY RESTS AT 440.736 MILLION OZ

SEPT 13/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1,009 MILLION OZ INTO THE SLV//: // /.////INVENTORY RESTS AT 440.736 MILLION OZ

SEPT 12/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.209 MILLION OZ INTO TEH SLV//: // /.////INVENTORY RESTS AT 439.727 MILLION OZ

SEPT 11/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.209 MILLION OZ INTO TEH SLV//: // /.////INVENTORY RESTS AT 439.727 MILLION OZ

SEPT 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 7/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 6/WITH SILVER DOWN 36 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.373 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 5/WITH SILVER DOWN 69 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 734,000 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 437.891 MILLION OZ

SEPT 1/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 440.00 MILLION OZ

AUGUST 31/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 438.625 MILLION OZ

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.834 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 443.210 MILLION OZ

AUGUST 29/WITH SILVER UP 49 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 183,000 OF SILVER INTO THE THE SLV// /.////INVENTORY RESTS AT 445.044 MILLION OZ

AUGUST 28/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.281 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 444.861 MILLION OZ

AUGUST 25/WITH SILVER UP ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.751 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 446.145 MILLION OZ

AUGUST 24/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.651 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 448.896 MILLION OZ

AUGUST 23/WITH SILVER UP 94 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 826,000 OZ FROM THE SLV// /.////INVENTORY RESTS AT 450.547 MILLION OZ

AUGUST 22/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: /.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 21/WITH SILVER UP 59 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 917,0000 OZ FROM THE SLV//.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 18/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 17/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

CLOSING INVENTORY 441.332 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

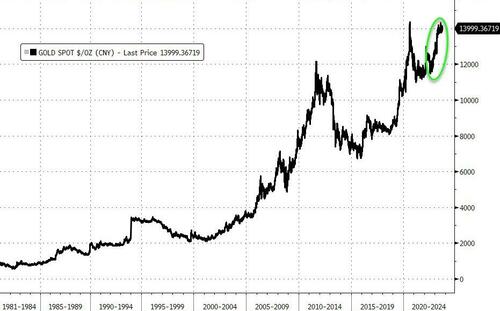

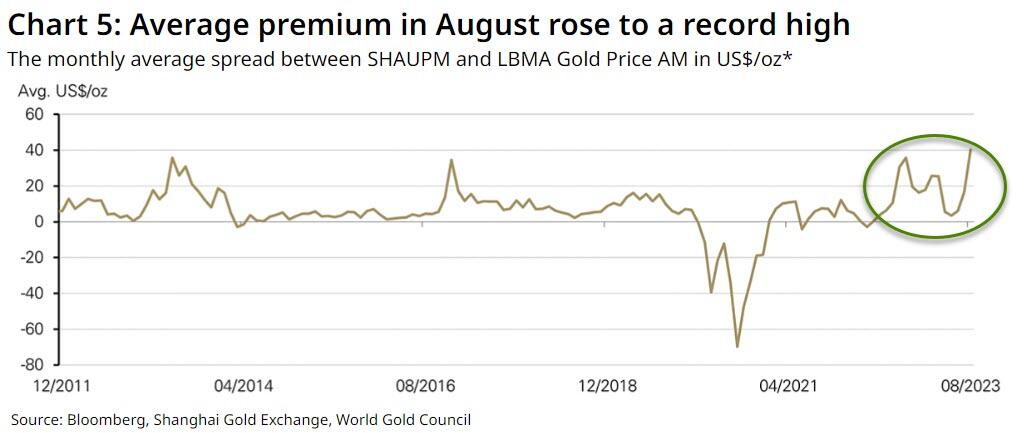

As Gold Hit New Record High In Yuan, Chinese Demand Improved In August

MONDAY, SEP 18, 2023 – 03:30 AM

Via SchiffGold.com,

Chinese gold demand improved on multiple fronts in August.

China ranks as the world’s biggest gold market.

While the price of gold declined in dollar terms last month, it was up 1.8% in yuan due to Chinese currency weakness.

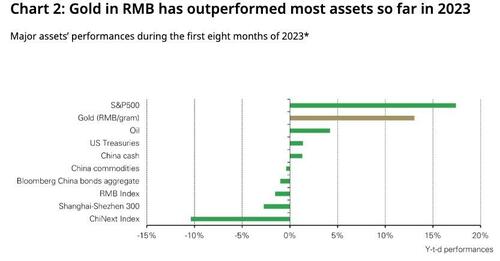

With prices rising, gold has outperformed most other assets in China, according to data from the World Gold Council.

Gold withdrawals from the Shanghai Gold Exchange (SGE) totaled 161 tons last month, reflecting strong wholesale demand for gold. This represented a 46-ton month-on-month increase.

Year-on-year, withdrawals from the SGE were down a modest 5 tons. According to the World Gold Council, this was “mainly due to 2022’s distorted seasonality amid COVID-related restrictions and a lower local gold price.”

Chinese Valentine’s Day and various jewelry fairs are scheduled in September. This will likely boost retail demand this month.

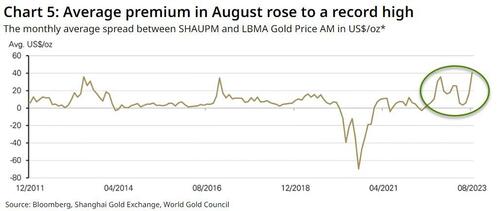

Also reflecting strong domestic gold demand, the Shanghai-London gold price spread averaged $40/oz in August, a new record high. This was a $23 per ounce month-on-month increase.

According to the WGC, “We believe improving gold demand and relatively tepid imports in recent months may have led to local demand and supply conditions tightening, pushing up the local gold price premium.”

Chinese gold import data lags by one month, so the July data is the most recent. China imported 107 tons of gold in July, 9 tons higher than June’s total. Compared to last year, imports were down 69 tons.

Chinese investors appear to be turning to gold. Metal flowed into Chinese gold-backed ETFs for the third straight month in August. Funds based in the country added 4.6 tons of metal, raising the total AUM to $3.6 billion.

During the month, poor equity market performance (CSI300: -6%) and continued local currency weakness drove many to safe-haven assets such as gold, which has delivered attractive returns so far in 2023.”

Meanwhile, the People’s Bank of China added more gold to its reserves in August. It was the 10th straight month of gold buying for the Chinese central bank with an addition of 29 tons. The PBoC now officially holds 2,165 tons of gold.

You can read more about central bank gold buying HERE.

Looking ahead, the World Gold Council said an improved outlook for China’s economy could provide some support for local gold demand.

Also, various jewelry fairs and industry events may spur both manufacturers’ and retailers’ replenishing demand. Furthermore, with the National Day Holiday and Mid-Autumn Festival approaching, retailers’ inventory restocking is likely to continue.”

However, high gold prices could create some headwinds for the Chinese gold market.

Real BRICS Threat + The Worst Macros I’ve Ever Seen

Matthew Piepenburg September 17, 2023

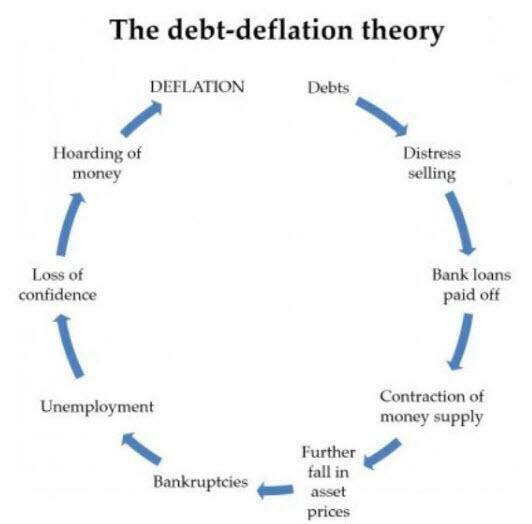

In many recent articles and interviews, I’ve warned that Powell’s “higher for longer” war against inflation will actually (and ironically) lead to, well… greater inflation.

That is, the rising interest expense (nod to Powell) on Uncle Sam’s fatally rising 33T bar tab will inevitably need to be paid with an inflationary mouse-clicker at the Eccles Building.

I’ve also consistently maintained that Powell’s war on inflation is mostly just optics, as he secretly seeks inflation to help pay down that bar tab with an increasingly inflated/debased USD.

As John Williams recently argued, true inflation using an honest (rather than the openly bogus BLS) measure is now closer to 11.5% rather than the officially reported headline rate of 3.7%.

This should come as very little surprise to those whose eyes are open to the Modis Operandi of debt-soaked/failed regimes. As former European Commission President, Jean-Claude Juncker confessed: “When the data is too bad, we just lie.”

But even for those who still believe the current Truman Show inflation (and “soft landing”) narrative out of DC, the Bezos Post or legacy media A, B, or C, there’s more fire adding to the inflationary flames than just bogus narratives and calming platitudes.

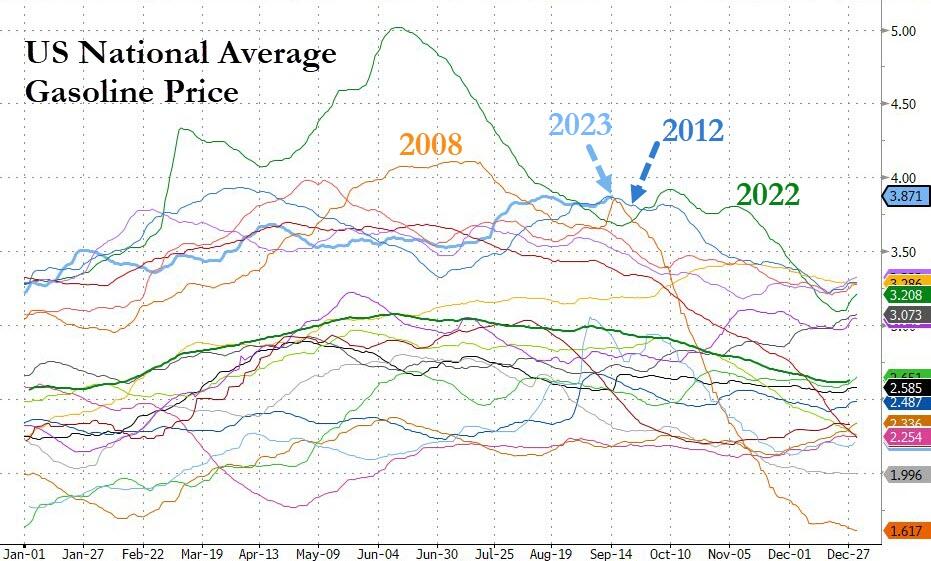

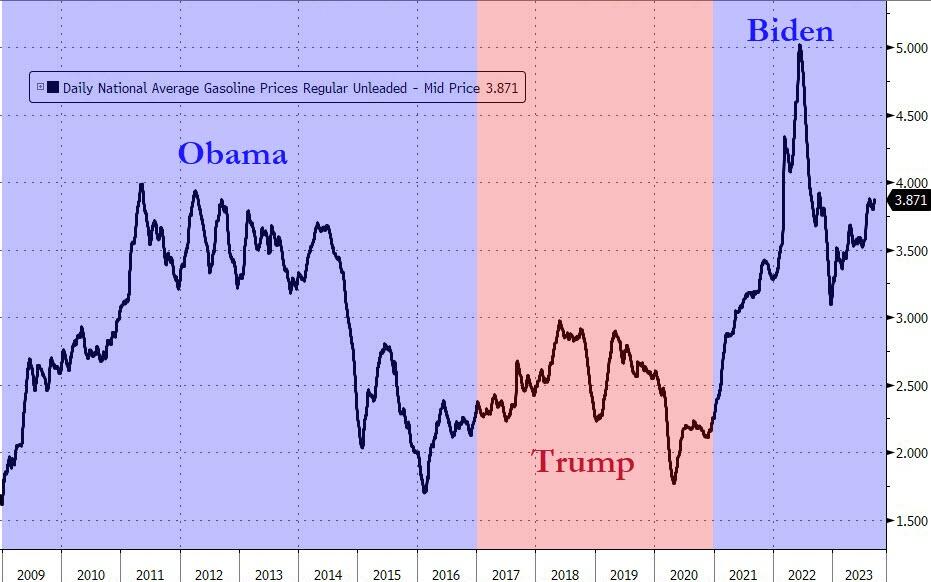

In particular, I’m talking about oil-driven inflation, and nothing burns faster.

Scary Flames in the Oil Supply

Left or right, the dumb out of DC just keeps getting dumber.

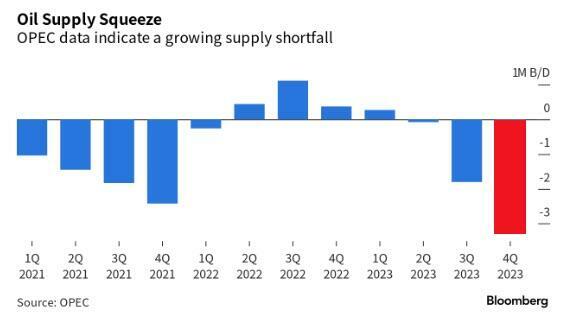

Between rising rates (nod to Powell), which make capex investing untenable for US oil producers, and a Weekend at Bernie’s White House, which has spent years effectively legislating US oil into oblivion, US energy supply is falling, and we all know that weakening supply leads to higher prices—and inflation.

Meanwhile, Saudi Arabia, whom that same White House called a “pariah state,” has not been warming to Biden’s awkward fist-pumps and increased production pleas, but rather joining other OPEC leaders in cutting, rather than expanding, oil production.

Gee, what a geopolitical shocker…

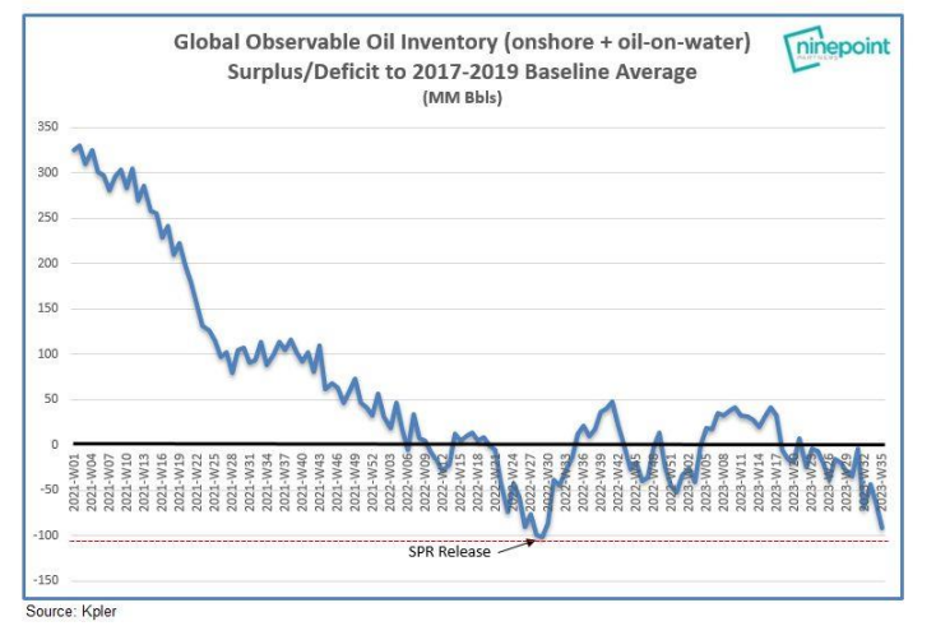

Net result, both national and global oil inventories are falling, and falling hard.

The Awkward Oil Two-Step

The once “go green” White House realized that the world, and inflation scales, still revolves around oil, especially after sanctioning Western Europe’s former energy supplier in one of the most short-sighted (i.e., stupid) policy decisions since the Iraq war.

This may explain why Biden changed his stripes and why there was a sudden pivot toward allowing greater US shale output in 2023 by pumping more cash into those shale fields at a pace not seen in 3 years.

Unfortunately, however, this may be too little too late (like Powell’s QT) to prevent oil price shocks and higher inflation into year end, thus adding insult to an already injured (and rising) US CPI measure of inflation.

As oil supply tightens, oil prices, and hence inflation rates, rise together with bond yields and interest rates—a perfect storm for over-inflated bond, stock, and real estate markets.

Those prices and inflation rates would be even worse if Chinese oil demand rises—which is why current Western headlines are literally praying for China to implode first. This might explain why The Economist has had two consecutive cover stories about an imploding China.

See how big media and big government sleep together?

Tying it Together

Regardless, we need to tie all this together.

If, as I see it, inflation (however misreported) becomes obviously more real and felt, the consequent rising bond yields will make the USD stronger and Uncle Sam’s bar tab more expensive, which hardy bodes well for America’s twin deficit black-hole of unpayable debt unless…

…Unless the Fed starts printing more fake and inflationary money to buy its own IOUs and weaken its export-killing, and BRICS-ignoring, USD.

Again, no matter how I turn the macros, the Fed will eventually have no choice but to pivot toward more instant liquidity and hence more inflationary policies to save/monetize its broke(n) bond markets.

Once this inevitability becomes a headline, the temporarily rising USD will be seen for what most of the informed world already recognizes—just another fiat monster backing a world reserve currency in the hands of a nation whose debt to GDP and deficit to GDP ratios mirror that of any other banana republic.

Reality is Hard to Look at Directly, But not for the BRICS

Many in the US or EU may not wish to see this. Bad news, like death and the sun, is hard to stare into.

But the BRICS nations, no strangers themselves to embarrassing balance sheets, are seeing this clearly.

Although I never bought into the gold-backed BRICS currency hype, I have zero doubt that this amalgam of commodity-heavy nations has a common enemy in the current US-dominated (and USD-driven) international trade system, whose hegemonic days are now numbered and whose alliances, as we warned from day-1 of the Putin sanctions (economic suicide), are forever de-dollarizing away from DC.

Moreover, the BRICS don’t need an “official” gold backed currency to trade their real assets in gold rather than Dollars. All they have to do, as Marcus Krall and I recently discussed, is request payment for their exports in gold.

The BRICS+ nations are hardly the perfect marriage of unlimited trust and efficient coordination. Nevertheless, they share an existential threat from an over-priced USD and negative-returning UST.

Never has the phrase the “enemy of my enemy is my friend” found a better home than among the rising list of BRICS+ actors who recognize that their very survival hinges upon escaping the suffocating death of paying > $14T of USD-dominated debts whose rising costs (rates) they can no longer afford lest they become vassals of DC.

As Luke Gromen recently observed, from the perspective of the BRICS nations, it’s “either hang together or hang separately.”

A Changing Petrodollar?

China, for example, can not abide forever by a petrodollar system of oil purchases. As the world’s largest oil importer, it mathematically recognizes that it will eventually run out of dollars to buy that oil.

In short, China needs to come up with a better plan—outside the Greenback.

And they will.

By the way, have you noticed the next BRIC in the wall? It’s Saudi Arabia.

See a trend? See a looming change in oil currencies?

Just saying…

As I warned months ago, this Saudi trend away from DC and closer to Shanghai could eventually be a key driver in slowly unwinding the current petrodollar system between a once “friendly” US-Saudi relationship toward a now weakening relationship which hitherto ensured the global demand (and hence the survival) of an otherwise debased paper Dollar.

If the petrodollar system radically or even slowly unwinds, this will do far more to destroy demand and the inherent purchasing power of the USD (and send gold skyrocketing) than any gold-backed BRICS trade currency.

And yet with all the recent sensationalism preceding the BRICS summit in South Africa, almost no one saw this—at least not in the legacy media.

Imagine that…

Other Tricks Up the BRICS Sleeve: More USD Assets than Liabilities

Aside from knee-capping the USD via a shift (gradual or sudden) in the petrodollar trade, it’s worth noting that but for South Africa, the remaining BRICS nations have more USD assets than liabilities, which means they can start dumping USTs to the detriment of Uncle Sam in order to raise USDs.

Many idealogues and US-thinktankers still think the US has all the power over these silly little BRICS nations who allegedly suffer from a dollar shortage.

The chest-puffers still see the USD as all-powerful and all-controlling, after all, just ask Iraq or Libya…

But the dollar-forever crowd is missing the forest for the trees or the basic math of fantasy debt.

If you haven’t noticed, the US just added an extra $1.9 trillion of insane borrowing to the back end of 2023.

And they did this as rates are rising and with the Fed still in full QT/suicide mode.

This mathematically places downward price pressure on bonds and hence upward cost pressure on yields, a scenario America simply can’t play out for much longer at $95T+ in combined public, household and corporate debt.

If the BRICS nations chose to add a layer of US asset dumping to this toxic mix, the ramifications for Uncle Sam would be even more staggering/painful for a debt-based system already on the cliff’s edge.

This is Bad, Really Bad

To repeat: The macros, no matter how I turn them, have never been this bad, this vulnerable and this foreseeable.

The US is now trapped in a vicious circle of debt for which there is no way out other than a currency-destroying return to more artificial, QE “stimulus” and the mother of all inflationary waves.

The horizon is now clear: Yields are up, twin deficits are up, inflation, even the mis-reported kind, is up, and yes, GDP is up too, but as I recently wrote, debt-driven GDP growth is not growth, but just debt.

Unless DC cuts spending at record levels (which kills election results for political opportunists and thus won’t happen), the only tool Washington DC has is more fake money and more real inflation, which means the Dollar in your wallet, checking account or portfolio is about to insult you.

3,Chris Powell of GATA provides to us very important physical commentaries

Chris Powell…

Another admission from the BIS that central banks rig the gold market

Submitted by admin on Sat, 2023-09-16 11:02Section: Daily Dispatches

11:08a Saturday, September 16, 2023

Dear Friend of GATA and Gold:

While central bank trading is a primary determinant of the price of gold and other currencies, gold market analysis seldom makes any reference to the broker that provides much camouflage for central bank gold trading: the Bank for International Settlements.

Of course over many years GATA has amassed much documentation of BIS interventions in the gold market. Among our favorites are a BIS PowerPoint presentation, made at a BIS conference for prospective BIS members, actually advertising that the bank’s services to members include gold market interventions —

— and a speech by a leading BIS official declaring that to “influence” the price of certain assets, “especially gold and foreign exchange,” is a big objective of central bank cooperation through the BIS:

This week GATA’s consultant about the BIS, Robert Lambourne, who — apparently alone among financial analysts outside central banking — calculates and reports the monthly changes in the bank’s gold swap positions, called attention to another confirmation of the bank’s major but largely surreptitious role in rigging the gold and currency markets. It is a pamphlet in which the bank profiles itself. The pamphlet is posted at the BIS’ internet site here —

On Page 3, under the heading “Banking Services,” the BIS says:

“We offer financial services exclusively to central banks, monetary authorities, and international organisations, mainly to assist them in the management of their foreign exchange assets. As an institution owned and governed by central banks, we are well placed to understand the needs of reserve managers — their primary focus on safety and liquidity, as well as the evolving need to diversify their exposures and obtain a competitive return.

“To meet those needs, we provide credit, gold and foreign exchange intermediation, and asset management services, while administering our own capital. An integrated risk management function ensures that financial and operational risks are properly measured and controlled.”

But this measuring and controlling are done in secret, the better to deceive and cheat the markets that are being measured and controlled. This measuring and controlling, the BIS suggests, are actually for the benefit of those who are deceived and cheated, particularly those using gold to try to protect themselves against rampant inflation, which has become the main product of modern central banking.

How good central banks are, determining the value of all capital, labor, goods, and services in the world so that mere free markets needn’t bother!

Gold market analysis that doesn’t incorporate the work of the BIS is largely a waste of time — that is, nearly all gold market analysis.

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

Swiss propose a referendum partially nationalizing UBS

(Bloomberg)

Swiss propose referendum on nationalizing UBS

Submitted by admin on Sun, 2023-09-17 11:01Section: Daily Dispatches

By Bastian Benrath Bloomberg News Sunday, September 17, 2023

A popular initiative in Switzerland wants to hold a vote on partially nationalizing UBS Group, the initiators wrote on their website.

The so-called banks initiative proposes to amend the Swiss constitution to say that “large banks of systemic importance are to be managed as joint stock companies with the confederation as majority shareholder in terms of share capital,” according to the website.

The text is currently under review by federal authorities. If they greenlight it, the initiators have 18 months to collect 100,000 signatures for their cause.

Parliament and cabinet ministers would then need to weigh in before the issue could be put to a national vote, a process that would likely take several years. …

In dollars: 1923.85. There is 3.75 riyals to the dollar.

Gold prices soar to record highs in Saudi market

Submitted by admin on Sun, 2023-09-17 18:09Section: Daily Dispatches

From Sammaa TV, Karachi, Pakistan Sunday, September 17, 2023

In a remarkable turn of events, the Saudi Arabian gold market witnessed a substantial surge in gold prices, with the price of 24-karat gold per gram reaching an unprecedented high of 231.98 riyals.

This astonishing increase has left both experts and investors astounded, as the global economic landscape continues to evolve.

According to reports from the Saudi Press Agency, the surge in gold prices took place yesterday, setting a new benchmark for precious metal enthusiasts.

The substantial increase in gold prices also extended to bulk purchases, with one kilogram of gold commanding a staggering 233,604.13 riyals.

The factors contributing to this remarkable surge in gold prices are multifaceted and remain a topic of discussion among market analysts. …

5 a. IMPORTANT COMMENTARIES ON COMMODITIES: DIAMONDS

G7 Prepares Russian Diamond Ban, Potentially Reshaping Global Rough Stone Supply Chain

FRIDAY, SEP 15, 2023 – 08:40 PM

While Western sanctions haven’t led to the collapse of Russia’s economy, the Group of Seven (G7) nations remain determined to roll out the next round of sanctions in a matter of weeks. According to Reuters, this round aims to reshape the global diamond supply chain, shifting it away from Moscow’s influence.

Reuters said, “The plan could transform the global diamond supply chain, but implementation will depend heavily on India, whose diamond industry employs millions of people who cut and polish 90% of the world’s diamonds.”

A Belgian official told reporters the new trade restriction will go into effect on Jan. 1. They said the ban was proposed by Belgium, where Antwerp, home to all major diamond mining companies, is located.

Reuters noted the restriction would fracture the global consumer diamond market in half as G7 countries would no longer be able to accept diamonds from Russia, the world’s largest producer of rough diamonds.

“We’re talking about restructuring a global market,” the official said, admitting trade restrictions won’t perfectly work right away.

The official continued, “Russia is the biggest supplier globally. With this system, we are cutting them out, leaving them in an inferior market with lower prices. We are slashing the financial flows from this sector.”

We pointed out last year that Russian mining giant Alrosa PJSC’s diamonds were still flowing onto global markets despite the US Department of the Treasury’s Office of Foreign Assets Control hitting the company with sanctions.

Anglo American Plc’s De Beers said the diamond industry supports G7 efforts:

“The question is how we can do this collectively and effectively so that all parts of the industry – large and small – are represented.”

Before the Russian invasion of Ukraine, De Beers and Alrosa were responsible for nearly 60% of all rough diamond sales worldwide, with De Beers accounting for 33% and Alrosa for 24%.

The challenging part will be getting India, the mecca of diamond cutting and polishing, on board with trade restrictions.

Another Belgian official said:

“The Indian polishers can polish whatever they want but (Russian gems) need to be segregated … At the point when the polished diamond is offered for export, the reference will be made to the original rough, again using a combination of physical inspection and traceability data.”

Despite all the sanctions that Western officials, US and European corporate media outlets, and neoconservative think tanks said would implode the Russian economy, the International Monetary Fund expects the Russian economy to grow by 1.5% this year. Remember, President Biden once vowed to “turn the ruble into rubble.”

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS MONDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2958

OFFSHORE YUAN: UP TO 7.2975

SHANGHAI CLOSED UP 8.19 PTS OR 0.26%

HANG SENG CLOSED DOWN 252.34PTS OR 1.39%

2. Nikkei closed

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 104.95 EURO RISES TO 1.0665 UP 18 BASIS PT

3b Japan 10 YR bond yield: FALLS TO. +.701 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.61/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ON SHORE YUAN: DOWN// OFF- SHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN’S worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

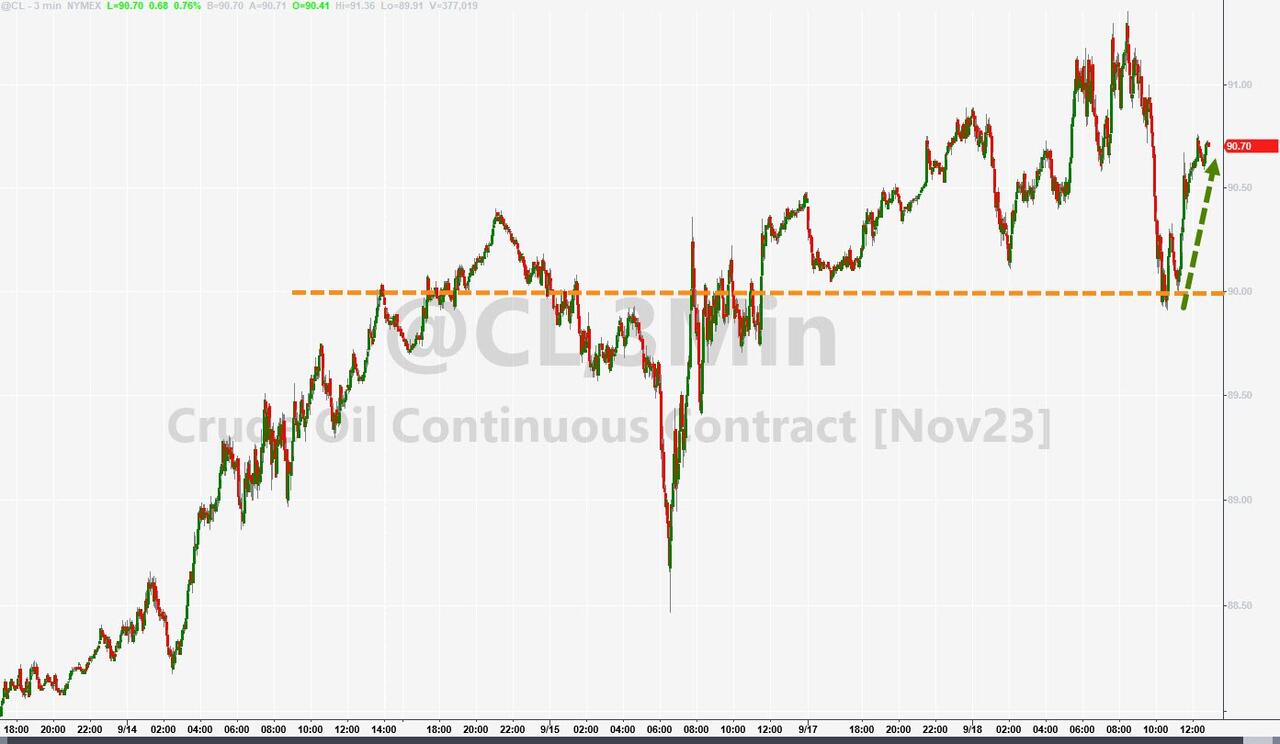

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.6900***/Italian 10 Yr bond yield UP to 4.475*** /SPAIN 10 YR BOND YIELD UP TO 3.751…**

3i Greek 10 year bond yield RISES TO 4.113

3j Gold at $1926.85 silver at: 23.12 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 25 /100 roubles/dollar; ROUBLE AT 96.56//

3m oil into the 91 dollar handle for WTI and 94 handle for Brent/

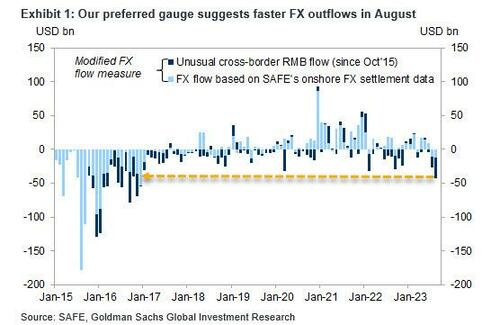

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.61// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.701% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8961 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9557well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.343 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.419 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 5.058 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 27.02…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 7 BASIS PTS AT 4.4315

end

2.a Overnight: Newsquawk and Zero hedge:

USA EARLY MORNING REPORT

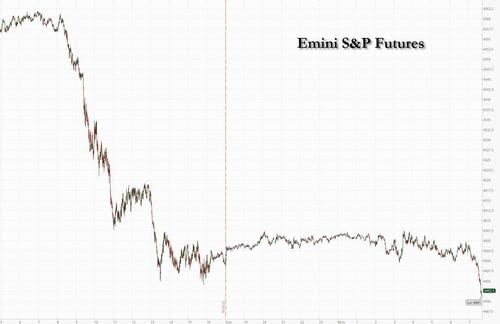

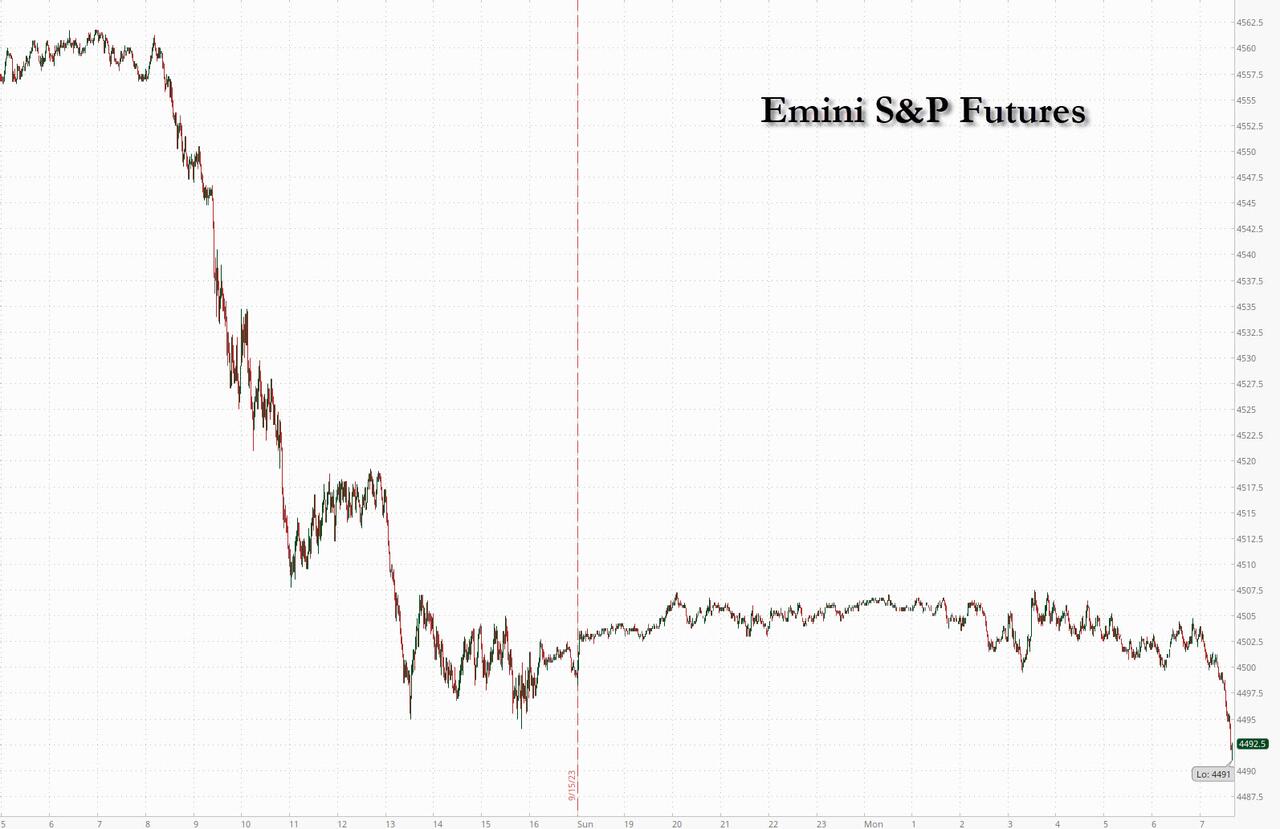

“This Week Will Be Bumpy”: S&P Futures Slide, Europe & Asia Slump With Brent At $95 Ahead Of Central Bank Barrage

MONDAY, SEP 18, 2023 – 08:12 AM

US equity futures were flat for much of the session before taking leg lower into the red with Treasury yields ticking higher, the USD flat, oil near $95, highlighting inflationary pressures just as policymakers prepare for interest-rate meetings, and bitcoin is surging as traders start pricing in the coming easing tidal wave. As of 7:45am, S&P and Nasdaq 100 futures were down -0.2%. In commodities, WTI and ags are the best performers with base metals and natgas the biggest laggards. Stocks in Europe and Asia dropped sharply, mirroring the decline that took the S&P 500 down more than 1% last Friday.

This week is a filled with multiple central bank decisions, including the Fed. JPM’s market intel desk writes that with BBG reporting options markets are betting on faster than expected rate cuts in 2024; “let’s see the update from the DOTS” says JPM’s Andrew Tyler. This week, the UAW strike may dominate headlines with about 10% of the 150k person union on strike, and the Biden admin may get involved. Meanwhile, the US government shutdown looms after Sep 30, currently a bi-partisan deal in the House has yet to materialize.

In premarket trading, mega cap Tech names are mostly in the green. Apple shares rise as much as 0.5% with analysts positive on the tech company’s pre-orders for the latest iPhone 15, saying data so far is surpassing expectations and could bode well for the shares if momentum is sustained. Societe Generale plunged as much as 11% after cutting profitability targets. Here are some other notable premarket movers:

Alteryx shares jump 5.3% after the computer-software company was upgraded to overweight from equal-weight at Morgan Stanley, which said the current valuation undervalues its growth and profit potential.

Micron shares gained 2.5% after the chipmaker was raised to buy from hold at Deutsche Bank, with the broker noting that prices for DRAM chips have started to improve faster than expected.

Disney and Warner Bros Discovery (WBD US) rise after the two media and entertainment companies were initiated with outperform recommendations at Raymond James, which noted compelling cash-flow growth expectations. Paramount Global was rated new market perform.

L3Harris Technologies shares rose 1.8% after the defense company was upgraded to overweight from equal-weight at Wells Fargo, which said the risk-reward has become more balanced.

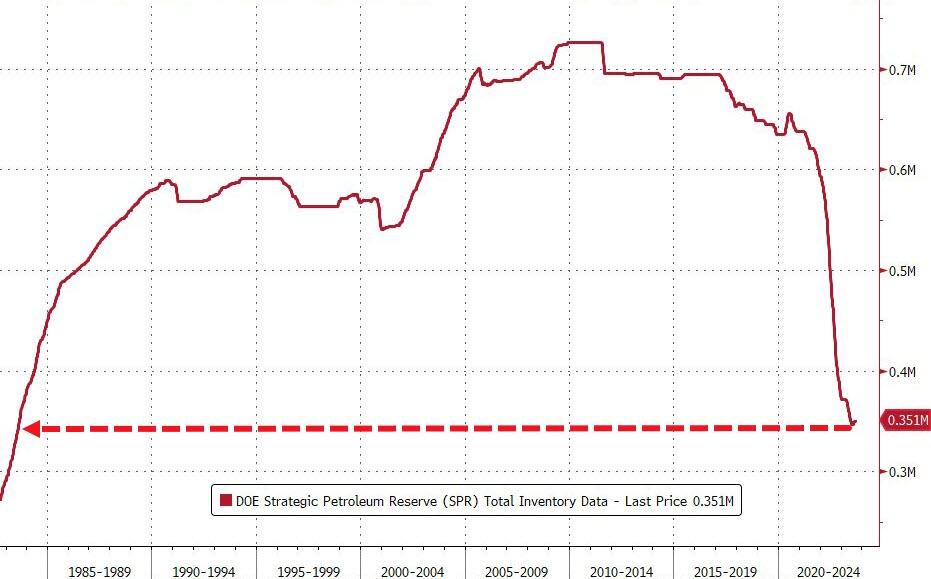

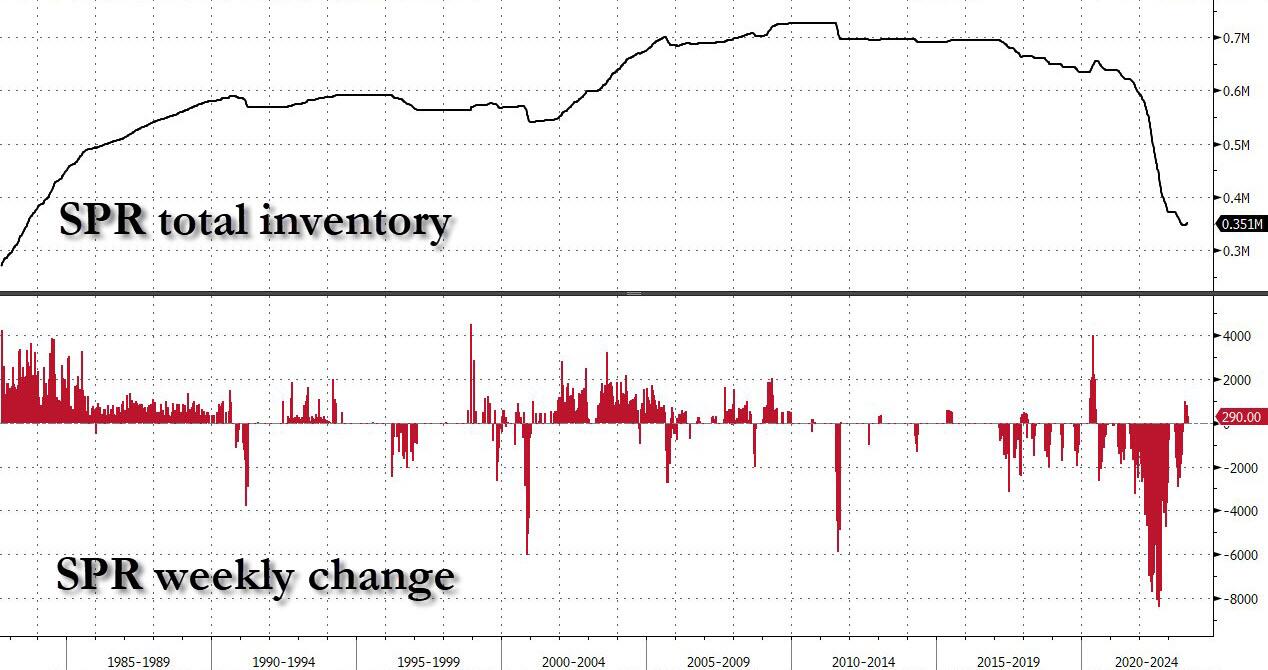

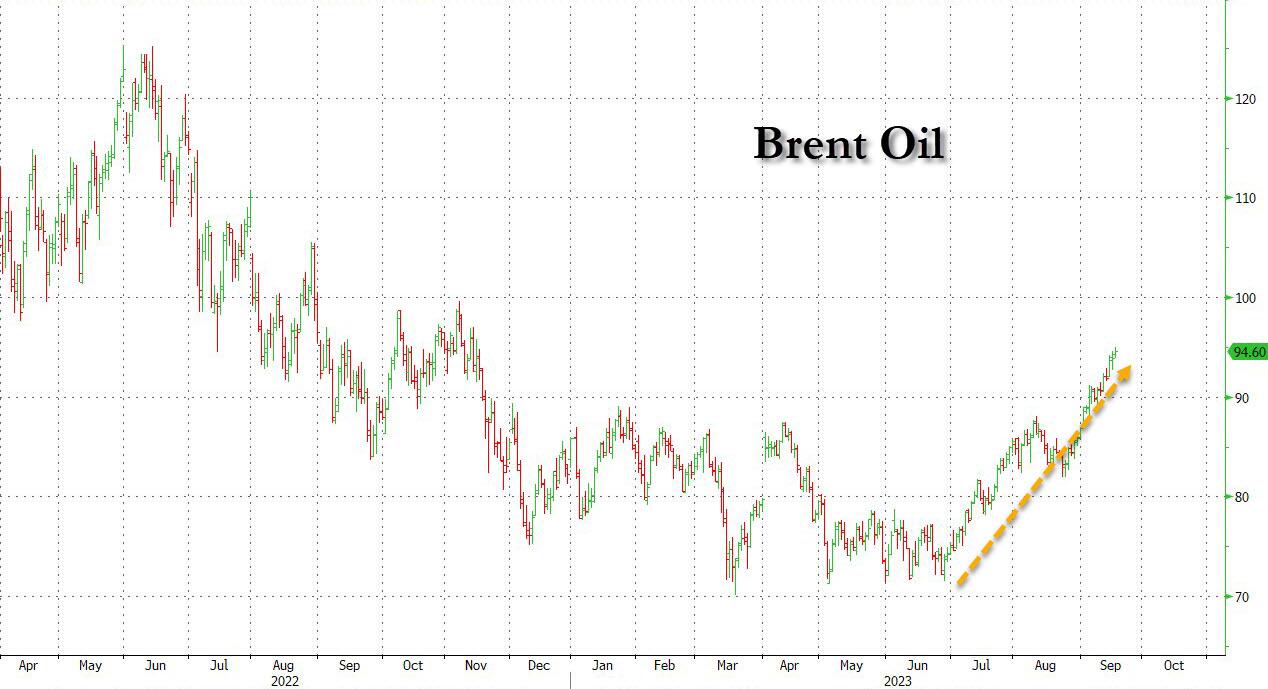

A three-week rally in oil prices has pushed benchmark Brent higher by 11%, and back to the average price at which Joe Biden drained almost 200 million barrels from the SPR, complicating the task of central bankers around the world in their fight against inflation. The Federal Reserve’s policy announcement on Wednesday will be followed by those from the Bank of England on Thursday and the Bank of Japan a day later.

“This week will be bumpy,” said Francois Rimeu, a fund manager at La Francaise Asset Management in Paris. “Pretty tough messages are expected from central bankers.”

Monday’s subdued mood in stock markets matched the relentless bearish tone of a note from Morgan Stanley’s Mike Wilson, who said investors have turned more cautious (which is amusing since he has been talling them to short the S&P since 3900 last December). “The majority of investors we’ve spoken with are in the ‘pushed out’ camp and are of the view that 2024 is now looking like a more challenging year for risk assets relative to 2023,” Wilson wrote in a note.

Other disagree: according to economists surveyed by Bloomberg News, a resilient US economy will prompt the Fed to pencil in one more interest-rate hike this year and stay at the peak level next year for longer than previously expected,

“A number of Fed speakers have taken a slightly more cautious tone recently, mentioning that risks have become more two-sided and talking of the ability to ‘proceed carefully,’” said Credit Agricole strategists led by Jean-François Paren. “That said, it is far too early to declare victory, and the Fed will want to keep the possibility of further tightening on the table.”

European stocks slumped; the Stoxx 600 is down 0.6%, led by declines in the construction and consumer product sectors. Major European markets are all lower with France the biggest laggard. UK rents increases 12% YoY in Aug, the largest increase on record. In EMEA, 3M Momentum is leading, Cyclicals are lagging; Value over Growth. UKX -0.2%, SX5E -0.7%, SXXP -0.5%, DAX -0.5%. Here are the most notable movers:

Pendragon shares rise as much as 32% after the new and used car seller agreed to sell its UK motor and leasing business to Lithia Motors Inc. and form a strategic partnership with the US company in a deal that promises a cash dividend of about £240 million to its shareholders.

PGS shares rise as much as 16% after the Norwegian geophysical data company’s sector peer TGS agreed to an all-share merger. TGS shares slide as much as 7%, with DNB analysts seeing the deal as less favorable to its shareholders.

Cofina shares gain as much as 13% after the Portuguese company said on Friday night that it’s analyzing the two offers it received for its Cofina Media unit; no decision has been taken about whether it will sell Cofina Media or not.

Drax shares rise as much as 5.3%, rebounding from a 10% drop on Friday that came after the UK’s National Audit Office said it will produce a report about the nation’s current biomass strategy and the fuel’s contribution to the UK’s net zero target.

International Distributions Services shares gain as much as 5.2% after JPMorgan upgraded its recommendation on the the Royal Mail owner to overweight from neutral, citing an attractive entry point.

Societe Generale shares drop as much as 7.9% after the lender announced a new strategic plan. KBW called the strategy “disappointing,” while Bloomberg Intelligence said it lacked major proposals to restructure its struggling investment banking division.

S4 Capital shares tumble as much as 28% to a record low after the digital advertising agency reduced full-year guidance for a second time in two months. The company said its clients are cautious in spending due to fears of a recession, and its current client activity levels are weaker than expected. Jefferies and Peel Hunt cut price targets.

Nordic Semiconductor shares slide as much as 16% after the chipmaker reduced quarterly revenue and margin forecasts, citing weak demand across its core markets and no signs of improvement amid an industry downturn.

ALD LeasePlan shares slump as much as 15%, the most since March 2020, after the operational leasing and fleet management company that’s majority owned by Societe Generale announced a new strategic plan for 2023-2026.

Lonza shares fall as much as 10.5%, the most since July, after the Swiss bioprocessing company announced the departure of CEO Pierre-Alain Ruffieux. The uncertainty will lead shares to underperform ahead of capital markets day next month, according to Morgan Stanley.

Earlier in the session, Asian stocks fell, with the tech sector leading the declines in a busy week for central bank decisions. A lack of positive developments from China also kept sentiment in check. The MSCI Asia Pacific ex-Japan Index dropped as much as 0.9%, dragged lower by information tech and financials. Among individual stocks, TSMC and Samsung Electronics contributed the most to the benchmark’s loss. Japanese markets were closed for a holiday, while the central bank there is due to meet later this week. Optimism spurred by nascent signs of stabilization in China’s economy has been offset by lingering concerns over the property crisis, with some distressed developers facing more debt payment deadlines.

A gauge of Chinese stocks traded in Hong Kong fell about 1%, while the onshore CSI 300 Index touched its lowest level this year before trading higher. Hang Seng and Shanghai Comp retreated at the open with the declines in Hong Kong led by tech and property stocks including Evergrande shares which slumped by more than 20% in early trade after some of its wealth management employees were detained by Chinese authorities. Conversely, the losses in the mainland were later reversed in the aftermath of the PBoC’s firm liquidity efforts and the previously unannounced meeting between Chinese Foreign Minister Wang Yi and US National Security Adviser Sullivan.

Australia’s ASX 200 was pressured with underperformance in tech and telecoms and with the handover of leadership at the RBA met with little fanfare.

The Nikkei 225 remained closed as Japanese participants observed the Respect for the Aged Day holiday.

In FX, the Bloomberg Dollar Spot was is down 0.1%. The Norwegian krone is the worst performer among the G-10’s, falling 0.6% versus the greenback. Spot gold rises 0.1%.

In rates, treasuries drop, with US 10-year yields rising 1bps to 4.34%. Bunds and gilts are also lower; regional yields are higher in this heavy central bank week, which sees decisions from the Fed (pause), BOJ (no change but may hint at tightening) and BoE, which is expected to hike 25bps to 5.5%, ending the hiking cycle; The ECB warns on additional hikes, but market expects the CB to have already completed.

In commodities, oil prices gained with US crude futures rising 0.6% to trade near $91.30. On the outlook for oil, traders will be monitoring clues on prospects for global supply when Saudi Energy Minister Prince Abdulaziz bin Salman addresses an industry conference later Monday. Hedge funds last week boosted their bullish wagers on Brent and US crude to a 15-month high. Brent has gained 11% in three weeks.

Looking at today’s calendar, it’s a slow start to the week, with the New York Fed Services Business index due, followed by the NAHB Housing Market Index, and the latest TIC data after the close.

Market Snapshot

S&P 500 futures up 0.1% to 4,504.00

MXAP down 0.6% to 162.97

MXAPJ down 0.9% to 504.11

Nikkei up 1.1% to 33,533.09

Topix up 0.9% to 2,428.38

Hang Seng Index down 1.4% to 17,930.55

Shanghai Composite up 0.3% to 3,125.93

Sensex down 0.2% to 67,671.61

Australia S&P/ASX 200 down 0.7% to 7,230.37

Kospi down 1.0% to 2,574.72

STOXX Europe 600 down 0.5% to 459.72

German 10Y yield little changed at 2.68%

Euro little changed at $1.0658

Brent Futures up 0.3% to $94.17/bbl

Brent Futures up 0.2% to $94.16/bbl

Gold spot up 0.1% to $1,926.10

U.S. Dollar Index little changed at 105.34

Top Overnight News

Biden’s national security advisor secretly met with China’s foreign minister in Europe over the weekend, a “significant step” toward stabilizing relations between the two countries (the weekend discussion could pave the way for Biden and Xi to meet later this year on the sidelines of the APEC summit in November). NBC News

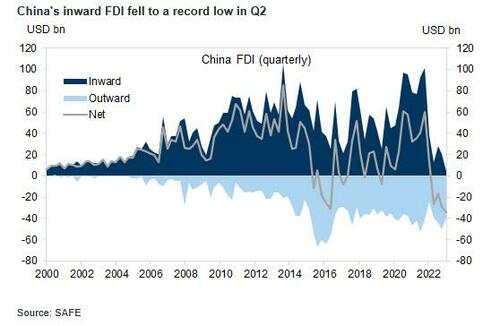

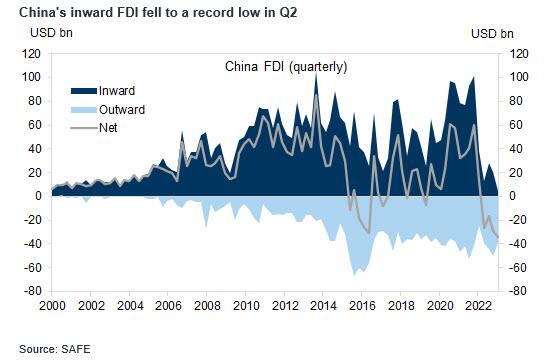

China’s economy is showing some green shoots (the latest evidence being Aug retail sales and industrial production Thurs night), but FDI (foreign direct investment) remains a big problem (FDI slumped 5.1% YTD through Aug, a larger drop than the -4% YTD as of Jul). SCMP

SoftBank is on the hunt for deals in artificial intelligence, including a potential investment in OpenAI, after the blockbuster listing of UK chip designer Arm bolstered Masayoshi Son’s multibillion-dollar war chest. FT

Brent edged closer to $95 for the first time since November after a three-week run of gains. Growing supply tightness and eroding inventories suggest the rally may have further to run after hedge funds boosted bullish bets to a 15-month high last week. Saudi Energy Minister Prince Abdulaziz bin Salman speaks at the World Petroleum Congress in Calgary later. BBG

The US and Iran are set to complete an exchange of prisoners after months of negotiations, a breakthrough that Washington hopes will open the door to a de-escalation of tensions between the arch-foes. In a carefully sequenced process, five American-Iranian dual nationals will be released on Monday by the Islamic republic and flown to Qatar, while the US will also free five Iranians from American prisons. FT

U.S. COVID infections are hovering near levels of the pandemic’s first peak in 2020, and approaching the Delta peak of late 2021, according to wastewater surveillance and modeling by forecasters. It’s yet another sign that while the official pandemic state may be over, the days of COVID are far from it. Fortune

The restart of student-loan payments could divert up to $100 billion from Americans’ pockets over the coming year, leaving consumers squeezed and some of the nation’s largest retailers fearing a spending slowdown. WSJ

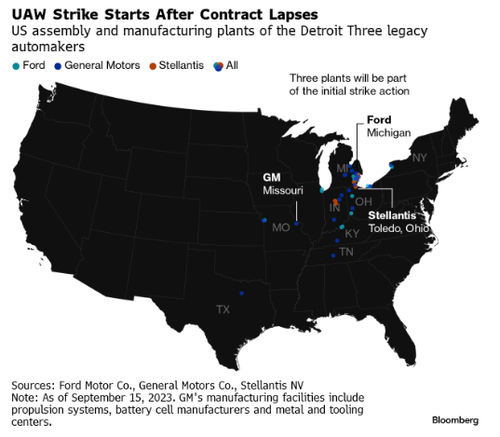

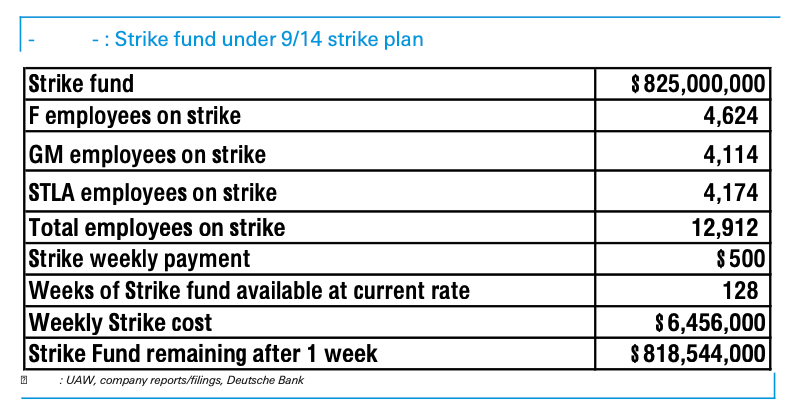

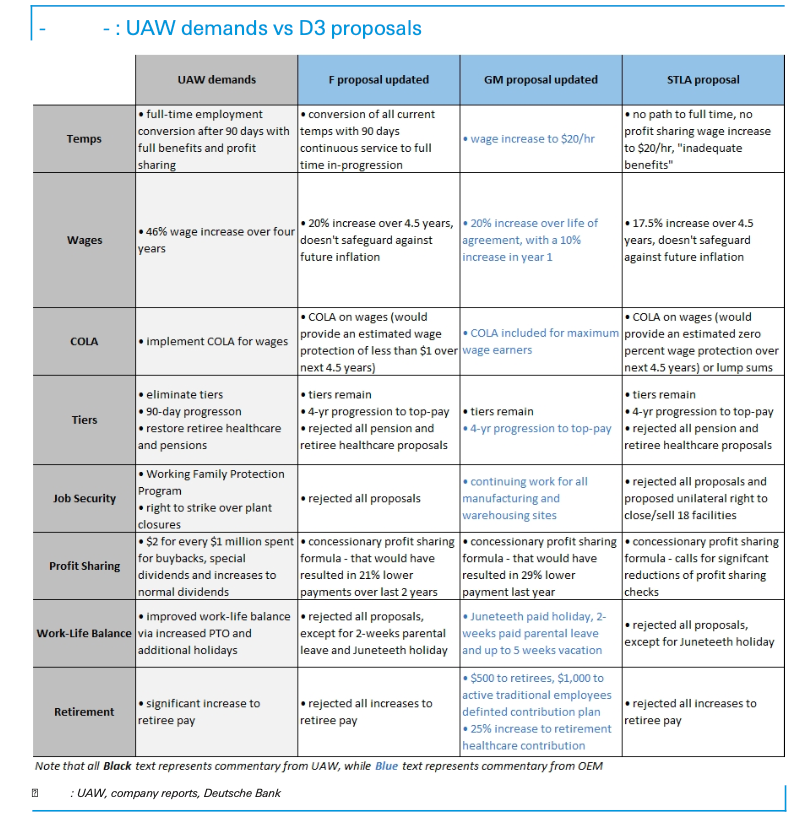

Auto strike latest: The UAW’s Shawn Fain rejected an offer of a 21% raise from Stellantis. “It’s definitely a no-go,” Fain told CBS. His comments signal the union and Detroit execs are still far apart. The union also rejected what Stellantis called a “compelling offer” that would protect jobs at an idled Jeep plant in Illinois. BBG

TSLA has already won, regardless of how the UAW talks turn out – the company’s manufacturing lead is only widening vs. the legacy OEMs as the firm drives down the cost of building an EV. WSJ

Utilities was among the most net sold sectors on the Goldman Prime Book last week, driven by long sales and to a much lesser extent short sales (~8 to 1). Last week’s net selling in US Utilities was the largest in 11 weeks and ranks in the 92nd percentile vs. the past five years. The US Utilities long/short ratio fell -4.9% on the week and now stands at 1.44, in the 12th percentile vs. the past year and in the 9th percentile vs. the past five years. GSPB

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly lower following last Friday’s declines on Wall St and with the region cautious in a holiday-thinned start to a busy week of central bank policy announcements. ASX 200 was pressured with underperformance in tech and telecoms and with the handover of leadership at the RBA met with little fanfare. Nikkei 225 remained closed as Japanese participants observed the Respect for the Aged Day holiday. Hang Seng and Shanghai Comp retreated at the open with the declines in Hong Kong led by tech and property stocks including Evergrande shares which slumped by more than 20% in early trade after some of its wealth management employees were detained by Chinese authorities. Conversely, the losses in the mainland were later reversed in the aftermath of the PBoC’s firm liquidity efforts and the previously unannounced meeting between Chinese Foreign Minister Wang Yi and US National Security Adviser Sullivan.

Top Asian News

US National Security Adviser Sullivan and Chinese Foreign Minister Wang Yi met in Malta over the weekend in an unannounced meeting to maintain open lines of communication with the discussions said to be candid, substantive and constructive, while they discussed security issues, Russia’s war in Ukraine and cross-Taiwan-Strait issues, according to the White House. Furthermore, a US official said the US sees some limited signs China may re-establish military communications with the US and the US raised concerns about Chinese assistance to Russia, as well as expressed concerns about China crossing the median line in the Taiwan Strait, according to Reuters.

China’s Foreign Ministry said following the meeting between Chinese Foreign Minister Wang and White House’s Sullivan that both sides agreed to continue to maintain high-level exchanges and hold consultations on Asia-Pacific affairs, maritime affairs and foreign policy, while it added that the Taiwan issue is the first insurmountable line on Sino-US relations, according to Reuters.

China’s Foreign Minister Wang Yi said in a meeting with Malta’s Foreign Minister that the two sides will work together to promote China-EU cooperation and China hopes Malta would continue to play a positive role in the development of China-EU relations. Furthermore, he said China-EU cooperation outweighs differences and China has consistently supported the EU’s strategic independence and European integration, according to Reuters.

Chinese Foreign Minister Wang Yi will visit Russia from September 18th-21st for the China-Russia strategic security consultations.

IMF’s Georgieva said China’s ageing population and declining productivity are suppressing growth and Beijing should work to boost domestic consumption, while she urged China to address the weakness in the real estate sector and build-up of local government debt. Furthermore, she stated the IMF must carefully monitor the outflow of investments from China and said that some sectors still offer opportunities, according to Reuters.

German Foreign Minister Baerbock said Europe must reduce its dependence on China and the EU should de-risk from China but not decouple, according to Bloomberg.

European bourses are in the red, Euro Stoxx 50 -0.8%, with participants cautious ahead of a Central Bank frenzy. Sectors have Health Care at the bottom weighed on by Lonza while pressure on LVMH’s Champagne brands has put Consumer Products & Services on the backfoot. Stateside, futures are essentially unchanged on the session after Friday’s pressure, ES +0.1%, with the US docket light until Wednesday’s FOMC. JP Morgan on EZ Equity Strategy: stays cautious on the region and expects defensive sectors to trade better into year-end.

Top European News

UK opposition Labour Party leader Keir Starmer pledged to seek a major rewrite of the Brexit deal in 2025 if the party wins the next general election, according to FT.

ECB’s Holzmann said that they definitely cannot say this was the final hike but the likelihood of another hike is not that big and noted that inflation risks haven’t receded lately. Furthermore, he stated that there is a risk more tightening will be needed and it wasn’t an easy decision at the last meeting where they had to weigh all arguments very carefully in order to come to an agreement.

ECB’s Muller sees a good case that no further rate hikes are needed and noted a strong case to quicken the balance sheet roll-off, while he added that the ECB should discuss an earlier end of PEPP reinvestment.

ECB’s Stournaras said governments must do their part in reining in consumer prices after borrowing costs reached a level that could be their peak, while he stated that monetary policy has done its part to fight inflation and it is up to fiscal policy to take off some of the heat, according to Bloomberg.

ECB’s Kazimir said he wishes the September rate hike was the last but cannot rule out further rate increases; only the March forecast can confirm that ECB is heading towards inflation goal; end of rate hikes to open debate on how to adjust PEPP and APP. Once clear that no more rate hikes are needed, debate should start on speeding up QT. Premature to place bets on the first-rate cut.

ECB’s de Guindos says parts of underlying inflation are moderating.

Bundesbank Monthly Report (September): expects the German economy to shrink in Q3 on weak industry and muted private consumption.

Moody’s raised Greece’s sovereign rating by two notches from Ba3; Outlook Stable from BA1; Outlook Positive and S&P affirmed Spain at A; Outlook Stable, while Fitch affirmed Germany at AAA; Outlook Stable and affirmed Malta at A+; Outlook Stable.

FX

DXY sits on a 105.000 handle within tight range ahead of NAHB on a quiet agenda before this week’s Central Bank-fest.

Kiwi and Aussie marginally outperform against Greenback above 0.5900 and 0.6400 respectively in the absence of anything specific.

Other majors relatively contained vs Buck as Franc, Yen, Pound, Loonie and Euro keep afloat of 0.9000, 148.00, 1.2350, 1.3550 and 1.0650.

PBoC set USD/CNY mid-point at 7.1736 vs exp. 7.2707 (prev. 7.1786)

Czech Central Bank Governor Michl said let’s forget about near-term rate cuts and that there will be no rate cuts in September and October, while they expect higher rates in the longer term and want to be a hawkish central bank. Furthermore, Michl said core inflation does not allow a rate cut now and they will wait for data in November and January, according to Reuters.

Fixed Income

Debt futures remain depressed and defensive awaiting inflation data, a swathe of September policy meetings and flash PMIs.

Bunds and Gilts teeter mostly above 130.00 and 95.00 between 130.24-129.97 and 95.23-94.96 respective parameters.

T-note hovers within 109-09/16 range pre-NAHB.

Commodities

WTI October and Brent November futures are firmer intraday, although off best levels with support emanating from Central Bank expectation, demand side support via China and ongoing Saudi/Russia curbs.

WTI trades around USD 91.30/bbl and towards the top end of a 90.86-91.70/bbl parameter thus far, while its Brent counterpart oscillates around USD 94.30/bbl in a USD 93.93-94.78/bbl band.

TTF is softer intraday despite Offshore Alliance members starting another 24-hour stoppage while Norway’s Troll field has begun to increase output after its prolonged shutdown.

Spot gold is rangebound between the 50- and 200-DMAs while base metals are more mixed given the cautious tone.

Australia’s Offshore Alliance union said members began another 24-hour stoppage on Sunday at Chevron’s (CVX) Australian LNG facilities.

French PM Borne said the government plans to permit gas stations to sell fuel at a loss for a limited period of a few months to help contain inflation.

Troll field in Norway to start ramping up output on Monday following the prolonged shutdown, according to Bloomberg’s Stapczynski.

Kuwait KNPC says power was cut at the Al Ahmadi (25k BPD) and Abdallah (270k BPD) refineries last night but work continues; working towards full production capacity, exports remain unaffected, according to a KNPC statement.

Kazakhstan raised its daily oil and gas condensate production by 10% on Sunday from Saturday to 250.4k tons following the completion of maintenance at the Karachagnak and Tengiz fields.

China August refined copper output +16.4% Y/Y to 1.12mln metric tons; Lead output +5.5% Y/Y to 619k tons, according to the stats bureau.

Ukraine intends to sue Hungary, Poland and Slovakia due to their refusal to drop a ban on Ukrainian agricultural products, via Politico.

Geopolitics

Ukraine’s general in command of ground forces announced that Ukrainian forces recaptured the eastern village of Klishchiivka on the southern flank of Bakhmut, according to a Telegram post cited by Reuters.

North Korean leader Kim met with Russian Defence Minister Shoigu in Vladivostok who showed Kim Russia’s hypersonic Kinzhal missiles and three nuclear-capable strategic aircraft, according to Russian media.

IAEA said Tehran took a disproportionate and unprecedented measure in barring a third of IAEA’s most experienced inspectors in Iran and noted that these inspectors are among the most experienced energy experts with unique knowledge of enrichment technology, according to Reuters.

Israel PM Netanyahu said Iran is violating all its commitments to the international community after Tehran moved to ban multiple inspectors, according to Reuters.

Saudi Arabia reportedly informed the Biden admin of its decision to halt all discussions of normalising ties with Israel on Sunday, citing Israeli PM Netanyahu’s “extremist” government, according to unconfirmed reports cited by The Jerusalem Post.