GOLD PRICE CLOSED: UP $0.60 TO $1932.60

SILVER PRICE CLOSED: UP $0.0 AT $23.20

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1931.25

Silver ACCESS CLOSE: 23.21

Shanghai Gold Benchmark Price

USD oz  AM2007.42

AM2007.42

PM1995.91

Historical SGE Fix

New York price at the time: $1932.00

premium $63.00

xxxxxxxxxxxxxxxxxx

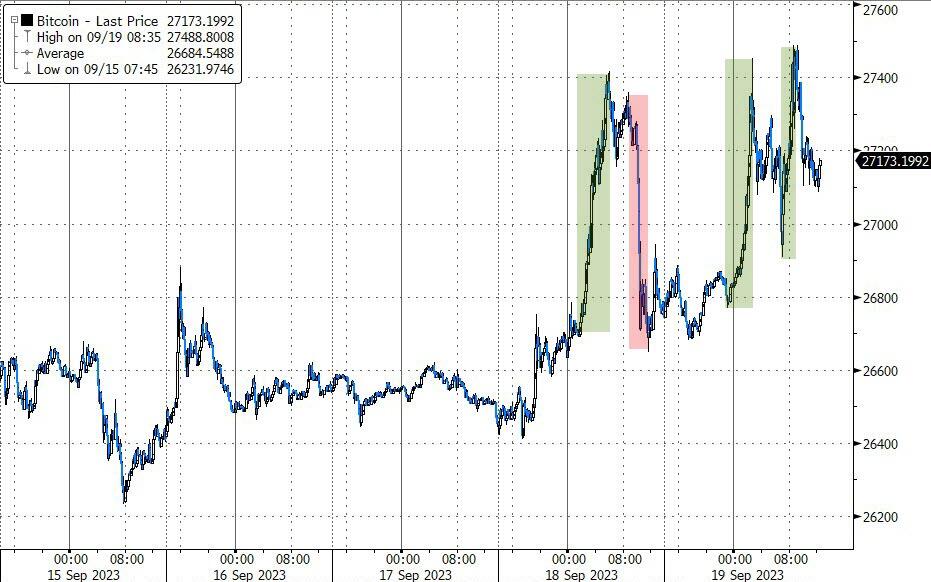

Bitcoin morning price:, $27,249 UP 545 Dollars

Bitcoin: afternoon price: $27,130 UP 426 dollars

Platinum price closing $966.65 UP $10.00

Palladium price; $1265.25 UP $16,80

END

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,696.26 DOWN 11.50 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1558,43 DOWN 3.45 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1808.26 DOWN .54 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,931.500000000 USD

INTENT DATE: 09/18/2023 DELIVERY DATE: 09/20/2023

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 3

323 H HSBC 4

435 H SCOTIA CAPITAL 5

624 H BOFA SECURITIES 6

661 C JP MORGAN 20

737 C ADVANTAGE 4

905 C ADM 2

TOTAL: 22 22

MONTH TO DATE: 3,864

JPMorgan stopped 0/22 contracts.

FOR SEPT.:

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2023. CONTRACT: 22 NOTICES FOR 2200 OZ or 0.0604 TONNES

total notices so far: 3864 contracts for 386,400 oz (12.018 tonnes)

FOR SEPT:

SILVER NOTICES: 5 NOTICE(S) FILED FOR 25,000 OZ/

total number of notices filed so far this month : 2616 for 13,080,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $0.60

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ NO CHANGES IN GOLD INVENTORY AT THE GLD: //

INVENTORY RESTS AT 880,27 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 0 CENTS AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV: WOW!! DEPOSIT OF 8.801 MILLION OZ FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 450.133 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A FAIR SIZED 93 CONTRACTS TO 125,340 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS FAIR SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.11 GAIN IN SILVER PRICING AT THE COMEX ON MONDAY. TAS ISSUANCE WAS A GOOD SIZED 535 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 535 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.11). AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A VERY STRONG GAIN OF 735 OI CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

A GOOD ISSUANCE OF EXCHANGE FOR PHYSICALS( 488 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 14.420 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S SMALL QUEUE JUMP OF 25,000 OZ//NEW TOTAL 13.410 MILLION OZ + OUR CRIMINAL ISSUANCE OF 0 EXCHANGE FOR RISK CONTRACTS//NEW TOTALS EXCHANGE FOR RISK: 3.0 MILLION OZ: NEW TOTALS SILVER STANDING: 16.410 MILLION OZ// /// / //FAIR SIZED COMEX OI GAIN/ GOOD SIZED EFP ISSUANCE/VI) GOOD SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 535 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -154 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTRACTS for 12 days, total 8877 contracts: OR 44.385 MILLION OZ (739 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 44.385 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 41.945 MILLION OZ (SMALLER THIS MONTH)

RESULT: WE HAD A FAIR SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 93 CONTRACTS WITH OUR GAIN IN PRICE OF $0.11 IN SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR EFP ISSUANCE CONTRACTS: 488 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR SEPT OF 14.2 MILLION OZ FOLLOWED BY TODAY’S 25,000 OZ QUEUE JUMP .+ 0 MILLION OZ EXCHANGE FOR RISK//PRIOR TOTAL FOR EXCHANGE FOR RISK = 3.0 MILLION OZ/TOTAL EXCH. FOR RISK /NEW TOTALS STANDING 16.410 MILLION OZ// /// WE HAVE A VERY STRONG SIZED GAIN OF 581 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A GOOD SIZED 535 CONTRACTS//ZERO FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION AS THE SHORTS CAPITULATED. THE NEW TAS ISSUANCE MONDAY NIGHT (535) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 5 NOTICE(S) FILED TODAY FOR 25,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 528 CONTRACTS TO 440,528 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED: –689 CONTRACTS

WE HAD A SMALL SIZED DECREASE IN COMEX OI ( 528 CONTRACTS) DESPITE OUR STRONG $8.40 GAIN IN PRICE//MONDAY. WE ALSO HAD A RATHER STRONG INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 12.656 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 100 OZ E.F.P. JUMP TO LONDON//NEW TOTAL STANDING 14.497 TONNES + /A FAIR (AND CRIMINAL) ISSUANCE OF 978 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH OUR $8.40 GAIN IN PRICE WITH RESPECT TO MONDAY’S TRADING.WE HAD A FAIR SIZED GAIN OF 1908 OI CONTRACTS (5.922 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2432 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 440,545

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1908 CONTRACTS WITH 528 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 2432 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1908 CONTRACTS OR 5.922 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 978 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2432 CONTRACTS) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI (528) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 1908 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 12.656 TONNES FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 100 OZ/// 3) ZERO LONG LIQUIDATION WITH SOME TAS LIQUIDATION COVERING THEIR SHORTFALL DURING THE COMEX SESSION //4) SMALL SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 978 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT :

TOTAL EFP CONTRACTS ISSUED: 28,545 CONTRACTS OR 2,854,500 OZ OR 88.87 TONNES IN 12 TRADING DAY(S) AND THUS AVERAGING: 2378 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES 88.87 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 88.87/3550 x 100% TONNES 2.50% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 88.87 TONNES (SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A SMALL SIZED 93 CONTRACTS OI TO 125,340 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A GOOD 488 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 488 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 488 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 93 CONTRACTS AND ADD TO THE 488 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A VERY STRONG SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 581 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 2.905 MILLION OZ

OCCURRED DESPITE OUR $0.11 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED DOWN 0.97 PTS OR 0.03% //Hang Seng CLOSED UP 66.62 PTS OR 0.37%/ /The Nikkei CLOSED DOWN 290.50 PTS OR .87% //Australia’s all ordinaries CLOSED DOWN 0.45 % /Chinese yuan (ONSHORE) closed UP AT 7.2913 /OFFSHORE CHINESE YUAN UP TO 7.2933 /Oil UP TO 92.45 dollars per barrel for WTI and BRENT UP AT 95.02 / Stocks in Europe OPENED ALL MOSTLY GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 528 CONTRACTS TO 440,545 DESPITE OUR STRONG GAIN IN PRICE OF $8.40 ON MONDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2432 EFP CONTRACTS WERE ISSUED: : DEC 2432 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2432 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2593 CONTRACTS IN THAT 2432 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A SMALL SIZED LOSS OF 528 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $8,40//MONDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR FRIDAY NIGHT WAS A FAIR 978 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: SEPT (14.497) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 14.497 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $8.40) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR GAIN OF 1908 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD A ZERO T.A.S. LIQUIDATION ON THE FRONT END OF MONDAY’S TRADING. THE T.A.S. ISSUED ON MONDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 5.922 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPT. (12.656 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S EFP JUMP OF 100 OZ//NEW STANDING 14.497 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $8.40.

WE HAD – REMOVED 689 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 1908 CONTRACTS OR 190,800 OZ OR 5.922 TONNES.

Estimated gold volume today:// 127,937 awful

final gold volumes/yesterday 145,476//speculators have left the gold arena

//SEPT 19/ /// THE SEPT. 2023 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | NIL OZ . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 63,958.062 oz ASAHI |

| No of oz served (contracts) today | 22 notice(s) 2200 OZ 0.0604 TONNES |

| No of oz to be served (notices) | 797 contracts 79700 oz 2.479 TONNES |

| Total monthly oz gold served (contracts) so far this month | 3864 notices 386400 OZ 12.018 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: NIL oz

customer deposits: 1

i) Into ASAHI: 63,958.062 oz

total customer deposits: 63,958.062 oz

we had 0 customer withdrawal

total withdrawals NIL oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPTEMBER.

For the front month of SEPTEMBER we have an oi of 819 contracts having LOST 3 contracts. We had

2 contracts were served on MONDAY, so we LOST an additional 1 CONTRACT or AN ADDITIONAL 100 oz will NOT stand for delivery in this non active delivery month of Sept this guy was EFP’d to London to take delivery over there.

Oct LOST1134 contracts to 23,420 contracts.

NOV GAINED 1 CONTRACTS to stand at 24

December GAINED 337 contracts UP to 377,752 contracts.

We had 22 contracts filed for today representing 2200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 20 notices were issued from their client or customer account. The total of all issuance by all participants equate to 22 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2023. contract month,

we take the total number of notices filed so far for the month (3864 x 100 oz ), to which we add the difference between the open interest for the front month of SEPT (819 CONTRACTS) minus the number of notices served upon today 22 x 100 oz per contract equals 466,100 OZ OR 14.497 TONNES the number of TONNES standing in this non active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month: No of notices filed so far (3864) x 100 oz + (819) {OI for the front month} minus the number of notices served upon today (22) x 100 oz) which equals 466,100 oz standing OR 14.497 TONNES

TOTAL COMEX GOLD STANDING: 14.500 TONNES WHICH IS HUGE FOR AN INACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,065,097.949 OZ 64.233 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 20,942,231.082 OZ

TOTAL REGISTERED GOLD 10,801,765.332 (335,98 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,140,465.750 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,736,668 OZ (REG GOLD- PLEDGED GOLD) 272.08 tonnes//dropping like a stone

END

SILVER/COMEX

SEPT 19

//2023// THE SEPT 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1934.600 oz Delaware . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 1,665,229.878 oz CNT HSBC Loomis |

| No of oz served today (contracts) | 5 CONTRACT(S) (25,000 OZ) |

| No of oz to be served (notices) | 66 contracts (330,000 oz) |

| Total monthly oz silver served (contracts) | 2616 Contracts (13,080,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 deposit customer account:

i) Into CNT: 600,184.538 oz

ii) Into HSBC 577,684.800 oz

iii) Into Loomis: 487,390.540 oz

total customer deposit 1,665,229.878 oz

JPMorgan has a total silver weight: 136.901 million oz/274.048 million or 50.00%

Comex withdrawals 1

i) Out of Delaware: 1934.600 oz

total: 1934.600 oz

adjustments: 0

TOTAL REGISTERED SILVER: 42.405 MILLION OZ//.TOTAL REG + ELIGIBLE. 272.385 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR August:

silver open interest data:

FRONT MONTH OF SEPT /2023 OI: 71 CONTRACTS HAVING LOST 2 CONTRACT(S). WE HAD 7

CONTRACT SERVED ON MONDAY. SO WE GAINED 5 CONTRACTS OR 25,000 OZ WILL STAND FOR SILVER AT THE COMEX..

OCT LOST 57 CONTRACTS TO STAND AT 1025.

NOVEMBER GAINED 4 CONTRACTS TO STAND AT 140

DEC. GAINED 165 CONTRACTS TO STAND AT 112,973 .

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 5 for 25,000 oz

Comex volumes// est. volume today 40,443 poor

Comex volume: confirmed yesterday 48,045 poor

To calculate the number of silver ounces that will stand for delivery in SEPT. we take the total number of notices filed for the month so far at 2616 x 5,000 oz = 13,080,000 oz

to which we add the difference between the open interest for the front month of SEPT (71) and the number of notices served upon today 5 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT/2023 contract month: 2616 (notices served so far) x 5000 oz + OI for the front month of SEPT (71) – number of notices served upon today (5 )x 500 oz of silver standing for the SEPT contract month equates to 13.410 million oz. + 0 MILLION EXCHANGE FOR RISK..NEW TOTALS EXCHANGE FOR RISK: 3.0 MILLION OZ//NEW TOTAL STANDING FOR SILVER: 16.410 MILLION OZ//

There are 42.145 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

SEPT 19/WITH GOLD UP $0.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD : // //INVENTORY RESTS AT 880.217 TONNES

SEPT 18/WITH GOLD UP $8.40 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD : A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 880.217 TONNES

SEPT 15/WITH GOLD UP $13.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD : A WITHDRAWAL OF 1.055 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 879.70 TONNES

SEPT 14/WITH GOLD UP $1.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD : A WITHDRAWAL OF 4.63 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 882.01 TONNES

SEPT 13/WITH GOLD DOWN $2.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 12/WITH GOLD DOWN $11.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 11/WITH GOLD UP $4.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 8/WITH GOLD UP $0.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 7/WITH GOLD DOWN $0.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.22 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.69 TONNES

SEPT 6/WITH GOLD DOWN $8.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.81 TONNES

SEPT 5/WITH GOLD DOWN $13.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.97 TONNES

SEPT 1/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 31/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 30/WITH GOLD UP $8.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.59 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.23 TONNES

AUGUST 29/WITH GOLD UP 17.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.6 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.64 TONNES

AUGUST 28/WITH GOLD UP $6.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / //INVENTORY RESTS AT 884.04 TONNES

AUGUST 25/WITH GOLD DOWN $6.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 884.04 TONNES

AUGUST 24/WITH GOLD UP $0.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //INVENTORY RESTS AT 884.91 TONNES

AUGUST 23/WITH GOLD UP $21.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 4.32 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 884.91 TONNES

AUGUST 22/WITH GOLD UP $2.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 0.87 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 889.23 TONNES

AUGUST 21/WITH GOLD UP $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.60 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 890.10 TONNES

AUGUST 18/WITH GOLD UP $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 6.92 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 887.50 TONNES

AUGUST 17/WITH GOLD DOWN $12.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: /// //INVENTORY RESTS AT 894.42 TONNES

GLD INVENTORY: 880.217 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 19/WITH SILVER UP 0 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 8.801 MILLION OZ INTO THE SLV. : // /.////INVENTORY RESTS AT 450.133 MILLION OZ

SEPT 18/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 1.651 MILLION OZ INTO THE SLV. : // /.////INVENTORY RESTS AT 441.332 MILLION OZ

SEPT 15/WITH SILVER UP 37 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.31 MILLION OZ FROM THE SLV. : // /.////INVENTORY RESTS AT 439.681 MILLION OZ

SEPT 14/WITH SILVER DOWN 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: : // /.////INVENTORY RESTS AT 440.736 MILLION OZ

SEPT 13/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1,009 MILLION OZ INTO THE SLV//: // /.////INVENTORY RESTS AT 440.736 MILLION OZ

SEPT 12/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.209 MILLION OZ INTO TEH SLV//: // /.////INVENTORY RESTS AT 439.727 MILLION OZ

SEPT 11/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.209 MILLION OZ INTO TEH SLV//: // /.////INVENTORY RESTS AT 439.727 MILLION OZ

SEPT 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 7/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 6/WITH SILVER DOWN 36 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.373 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 5/WITH SILVER DOWN 69 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 734,000 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 437.891 MILLION OZ

SEPT 1/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 440.00 MILLION OZ

AUGUST 31/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 438.625 MILLION OZ

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.834 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 443.210 MILLION OZ

AUGUST 29/WITH SILVER UP 49 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 183,000 OF SILVER INTO THE THE SLV// /.////INVENTORY RESTS AT 445.044 MILLION OZ

AUGUST 28/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.281 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 444.861 MILLION OZ

AUGUST 25/WITH SILVER UP ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.751 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 446.145 MILLION OZ

AUGUST 24/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.651 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 448.896 MILLION OZ

AUGUST 23/WITH SILVER UP 94 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 826,000 OZ FROM THE SLV// /.////INVENTORY RESTS AT 450.547 MILLION OZ

AUGUST 22/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: /.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 21/WITH SILVER UP 59 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 917,0000 OZ FROM THE SLV//.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 18/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 17/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

CLOSING INVENTORY 450.133 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

3,Chris Powell of GATA provides to us very important physical commentaries

China relaxes temporary curbs on gold imports. The premium is now $77.00

(London Financial Times)

China lifts temporary curbs on gold imports as renminbi recovers

Submitted by admin on Mon, 2023-09-18 08:41Section: Daily Dispatches

By Cheng Leng and Harry Dempsey

Financial Times, London

Monday, September 18, 2023

China’s central bank has lifted temporary curbs on gold imports that were imposed on some lenders in a bid to defend the renminbi but caused the price of the precious metal to rise in the country.

The spread between the Shanghai gold price and London hit a record $121 per troy ounce last Thursday, according to calculations based on public traded prices.

The spread narrowed to $76 today after the People’s Bank of China relaxed curbs on imports of the precious metal last week, said people familiar with the informal order given to some state and midsized commercial banks.

China in August had reduced and stopped granting quotas for international gold imports by banks to ease a rush in purchases to hedge against a weaker domestic currency. The renminbi fell to its lowest point against the dollar in 16 years in early September after the release of disappointing economic data. …

… For the remainder of the report:

https://www.ft.com/content/b8406698-b98f-444b-b1a7-03c29f6f5779

END

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES//CHINA==LONDON GOLD ARBITRATION

this is the death knell of our western bankers

(zerohedge)

Shanghai Arb Gives Dollar Gold Price ‘More Room to Rise’ as Yen Gold Hits Record

Tuesday, 9/19/2023 14:23

The GOLD PRICE in London’s bullion market rose to new 2- week highs against the US Dollar on Tuesday, trading above $1935 per Troy ounce as global stock markets slipped and government bond yields rose ahead of tomorrow’s September interest-rate decision from the Federal Reserve.

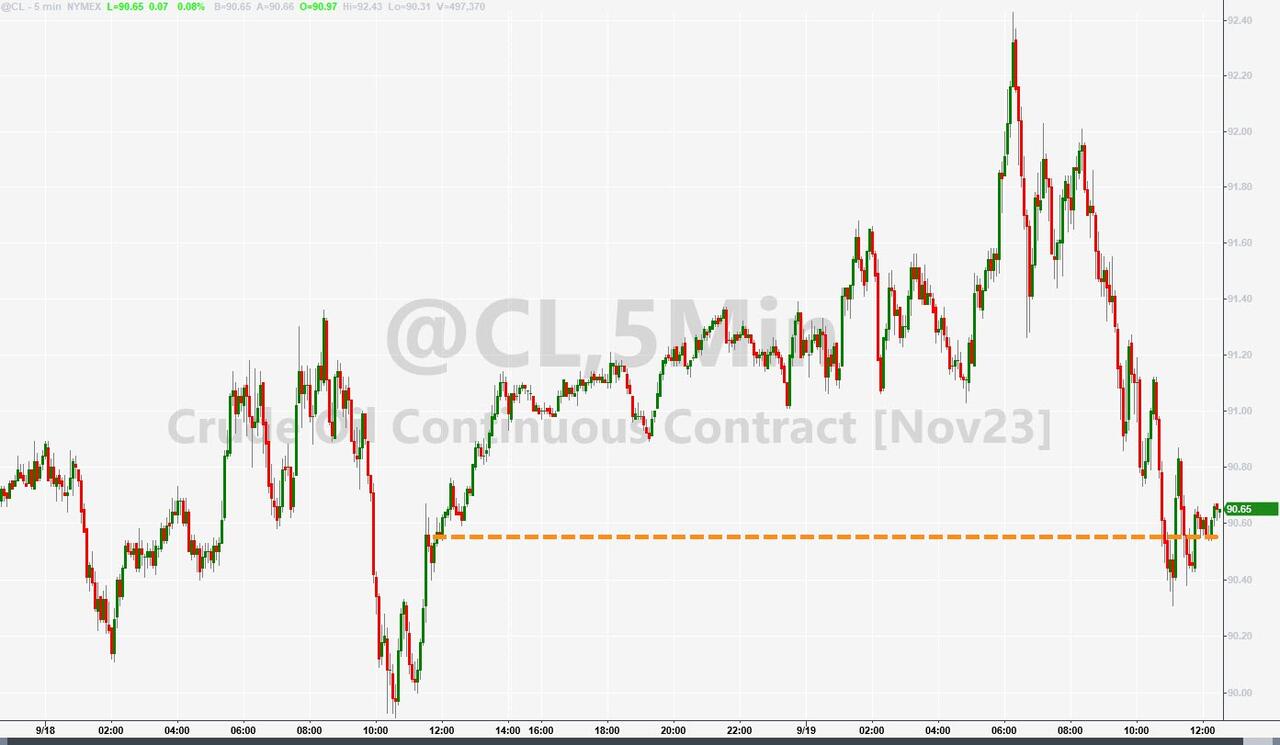

Crude oil rose again, hitting fresh 2023 highs above $95 per barrel of European benchmark Brent.

The bullion price in Yen meanwhile rose to a yet another new all-time JPY gold high, very nearly touching ¥9,200 per gram as the Japanese currency sank yet again ahead of Wednesday’s Fed announcement – expected to leave Dollar interest rates unchanged at the current 16-year high of 5.5% per annum, but with new GDP and inflation forecasts expected to accompany a prediction of one more rate-rise by Christmas.

“The Yuan and Yen need the Fed’s help,” says an opinion column in the Wall Street Journal, pointing to tomorrow’s US interest-rate decision as the 2 giant Asian currencies extend their summer 2023 slide, dropping to the lowest since 2007 and re-testing last fall’s 3-decade lows respectively.

With most major economies continuing to hike borrowing costs, “Being a loose monetary policy outlier is an uncomfortable place [for Beijing and Tokyo] to be these days,” the WSJ says.

Gold in China also rose overnight, setting its highest- ever Shanghai afternoon benchmark price outside of last Thursday’s Chinese gold price record, with a rise of 22.4% from this time last year.

“Banks who have now been issued with import licenses are buying gold in London and selling in Shanghai,” says Bruce Ikemizu of the Japan Bullion Market Association, analyzing the “import arbitrage” which the People’s Bank of China has finally enabled after weeks of restricting new import quotas in the No.1 gold consumer market.

“The recent spike in gold premiums versus London prices has been accompanied by Shanghai trading volumes also skyrocketing…A large amount of gold was actually being bought.”

Chart of Shanghai Gold Exchange price and trading volume (bottom, purple). Source: JBMA via Bloomberg

Looking ahead, “The fact that the premium is still over $60 per ounce means London buying and Shanghai selling will continue,” Ikemizu says. “So there is still room for Dollar- denominated gold to be bought on that basis.”

Gold prices for Eurozone investors today touched the highest since mid-June at €1811 per ounce after new data said consumer-price inflation across the 20-nation currency area slowed for the 4th month running in August, dropping to 5.2% per year – the weakest since January 2022.

Back then, deposit interest rates at the European Central Bank were held at minus 0.5% per annum.

Last week the ECB raised its deposit rate to a Eurozone- union record of 4.0%.

“Governments should maintain restrictive monetary policy to combat inflation,” says the Paris-based OECD think tank today, echoing last week’s comments from the Washington- based IMF while raising its global economic growth forecast for 2023 from 2.7% to 3.0% per year, led by India and with the forecast for the USA revised up from 1.6% to 2.2%.

Euro-area GDP growth will slow however on the OECD’s new analysis, dropping to 0.6% from the 0.9% forecast for the 340-million citizen single currency zone in June, led by a 0.2% annual decline in Germany.

“German economic output is likely to shrink slightly in the third quarter of 2023,” says the Bundesbank – national central bank of the Eurozone’s largest economy – in its latest monthly report.

“Despite slowing inflation, strong wage growth and a good labor market, German households are still holding back on spending [while] continuing weakness in the industrial sector also puts pressure on economic performance.”

Germany’s manufacturing activity shrank last month at the worst pace since the Covid Crisis according to the HCOB PMI survey. Its preliminary reading for September will be published Friday.

Today’s new OECD outlook also cuts half-a-point off its 2023 and 2024 growth forecasts for China, with GDP in the world’s No.2 economy set to expand by 5.1%, the slowest pace since 1990.

Across the entire G20 group of leading economies, real GDP growth will slow next year to 2.7% from 3.1%, the OECD predicts, while inflation slows over 1 percentage point from 2023’s pace of 6.0% per annum.

With the OECD leaving its 2023 GDP growth forecast for the United Kingdom unchanged at just 0.3% while cutting its 2024 forecast below Germany’s at 0.8%, the UK gold price in Pounds per ounce today hit 3-month highs above £1560 ahead of tomorrow’s Bank of England decision, widely expected to bring another interest-rate rise, up to a 15-year high of 5.5% per annum.

-END-

Gold SWOT: Gold Imports by India Surged 40% in August

(courtesy Frank HOLMES/SWOT)

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:NICKEL

Is The LME Losing Its Grip On Global Nickel Pricing?

TUESDAY, SEP 19, 2023 – 05:00 AM

Authored by Metal Miner’s Nichole Bastin via OilPrice.com,

- Nickel prices experience a significant decline, erasing gains from H2 2022, and the Stainless Monthly Metals Index drops by 3.1%.

- The stainless steel market is oversupplied, leading to limited demand and historically short 304 mill lead times, though base prices remain unchanged.

- In the aftermath of the March 2022 nickel squeeze, trading volumes on the LME remain low, prompting potential new futures contracts from competitors like the Shanghai Futures Exchange and Abaxx Commodities Exchange.

The nickel price index continued to trend downward, as it fell to its lowest level since July 2022 by mid-September. Following an over 7% decline during August, prices fell nearly 3% during the first two weeks of September. As prices drop toward historical support zones, they come close to wiping out nearly all gains from the last major uptrend in H2 2022. While the LME nickel contract remains plagued by low liquidity, the continued creation of lower highs and lower lows suggests bearish momentum within the market.

Overall, the Stainless Monthly Metals Index (MMI) returned downward from last month, with a 3.1% decline from August to September.

Stainless Inventories Reportedly “Supplied to Over-Supplied”

The stainless steel market remains decidedly bearish as the final quarter of 2023 nears. Suppliers described current inventory levels among both service centers and end users as “supplied to oversupplied.” While 304 and 430 grades account for the majority of the market, oversupply is apparently indicative through much of the stainless market.

Numerous end users reportedly intend to sit out of the market for the remainder of the year, which will pressure service center pricing as they work to reduce inventories at the end of the year. Competitive import prices tempted some OEMs back into the market, as witnessed by a jump in cold rolled import licenses during August. However, imports throughout the year remain muted from 2022 amid the shift in market dynamics. View MetalMiner’s track record of forecasting where industrial metal prices are headed.

Stainless Mill Lead Times Remain Short, Base Prices Hold Firm

Amid limited demand, 304 mill lead times remain historically short. Lead times continue to average around 4.5 weeks. Under normal conditions, mill lead times typically extend from 6 to 8 weeks.

In spite of the bearish market, base prices have remained unchanged since January 2022. Domestic mills are expected to hold firm on base prices during the remainder of the year to mitigate the impact of lower demand. While greater market pressure could change this, the effective duopoly between NAS and Outokumpu and long lead times for imports will allow domestic producers greater control over market pricing.

Impress your executive team and lead like a procurement pro. Decode nickel market volatility’s impact on earnings with the Monthly Metals Outlook report. Start with a free sample, then subscribe.

Broken Nickel Market Still Ripe For Challengers

September marked the year-and-a-half anniversary of the March 2022 nickel squeeze, which caused liquidity within its 3M nickel contract to plunge. While trading volumes picked up slightly throughout the summer, they sit far beneath their averages from previous years. This leaves the LME nickel contract ripe for the picking.

In addition to Global Commodity Holdings, the Shanghai Futures Exchange (SHFE) is reportedly considering the creation of its own international nickel futures contract. According to Reuters, the exchange “has been studying the structure of the nickel market and supply and demand at the instigation of industry participants looking for alternatives.”

It remains unclear whether a viable alternative contract would bring traders back to the market. The impact of the March 2022 squeeze reverberated across exchanges, as open participation on the SHFE’s own active nickel contract dropped amid the nickel market exodus. How exactly these factors will impact 2024 nickel prices and market volatility are all covered in MetalMiner’s 2024 Annual Metals Outlook.

Other Nickel Price Factors at Work

Meanwhile, as Class 2 nickel supply becomes increasingly important amid the rise of EVs, Singapore’s Abaxx Commodities Exchange is currently working on a physically settled nickel sulfate futures contract it hopes to have available by the end of the year. Abaxx’s contract would not compete with the LME or SHFE, which reflect the Class 1 nickel price. Should it become liquid enough to use as a pricing benchmark, however, it would provide an important reference point within the increasingly bifurcated nickel market between Class 1 and 2 material.

As the LME fights to retain its dominant position as the global pricing benchmark, the beleaguered exchange’s continued struggles to regain market participants begs the question as to why stainless producers use LME nickel prices to begin with. Outokumpo boasts using an average of 90% recycled material content within its melt mixes. This would suggest scrap prices hold a far more important position in the actual cost of stainless steel.

Beyond that, there remains a considerable margin between scrap prices and LME prices, a notable benefit to mills. Low liquidity on the LME contract exacerbates this delta, as it has led to a lack of momentum within price action causing slow overall price movement. This, in turn,has led to slow declines within the stainless surcharge.

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

FTX Sues Bankman-Fried’s Law Professor Parents To Recover “Fraudulently Transferred And Misappropriated Funds”

BY TYLER DURDEN

TUESDAY, SEP 19, 2023 – 01:45 PM

Bankrupt crypto exchange FTX has sued the parents of founder Sam Bankman-Fried, who were just profiled by Bloomberg in “How Sam Bankman-Fried’s Elite Parents Enabled His Crypto Empire“, even as the article forgot to mention all the others who enabled SBF’s criminal spree…

… to recover millions of dollars in “fraudulently transferred and misappropriated funds,” the company said in a court filing late Monday alleging the “effectively altruist” parents were instead complicit in their son’s crime, and spent illicit money on hotels, real estate and others.Allan Joseph Bankman, left, and Barbara Fried, right, leave after a bail hearing for their son, along with lawyers, at Manhattan Federal Court in New York, on Aug. 11.

The company, operated in bankruptcy by new management, alleged that Joseph Bankman and Barbara Fried, both Stanford Law School professors, “exploited their access and influence within the FTX enterprise to enrich themselves, directly and indirectly by millions of dollars,” at the expense of the debtors and creditors, the company said.

Hilariously, when the cryptocurrency exchange collapsed last November, Bankman-Fried’s parents remained by his side as his legal advisers, the Journal had reported. Which may explain why their son had his bail stripped from him and is now rotting away in prison ahead of his trial.

Worse, Bankman had been a paid employee of FTX for almost a year. He joined his son in meetings with Washington policy makers and expanded the company’s “philanthropic” endeavors.

“Bankman played a key role in perpetuating the culture of misrepresentations and gross mismanagement and helped cover up allegations that would have exposed the fraud committed by the FTX Insiders,” the company estate alleged.

It gets better: Bankman and Fried are “renowned”, in Bloomberg’s parlance, legal scholars and taught at Stanford Law School. Bankman is an expert on taxes, while Fried’s specialty is ethics.

“This is a dangerous attempt to intimidate Joe and Barbara and undermine the jury process just days before their child’s trial begins,” attorneys representing Bankman and Fried said in a statement. “These claims are completely false.”

Despite “knowing or blatantly ignoring” that FTX was insolvent or on the brink of insolvency, Bankman and Fried discussed with Bankman-Fried the transfer to them of a $10 million cash gift and a $16.4 million luxury property in the Bahamas, the filing said. The pair also “pushed for tens of millions of dollars in political and charitable contributions.”

Bankman seemed keenly aware of the company’s risk of downfall, according to the filing. He started conversations about how to ensure that assets — including primary residences — were safe from bankruptcy a year before FTX collapsed into Chapter 11.

The filing includes details of spending escapades, particularly by Bankman, who was employed by FTX Philanthropy starting in 2021, according to court papers. In one instance, he gave a former law student a “free trip to France,” which included tickets to the Formula 1 Grand Prix, which cost several thousand dollars.

Although Fried was not formally employed by the crypto exchange, she too wielded influence over the company’s finances. The lawsuit describes her as the “single most influential advisor” over her son and FTX’s political contributions. As evidence of that, she had Bankman-Fried give millions to a political action group that she co-founded, court papers show.

While Bankman-Fried has claimed that his parents “weren’t involved in any of the relevant parts” of the business, the FTX Group was self-described over the years as a “family business,” according to the filing. And in the months leading to the company’s insolvency, Bankman’s role appeared to become only more involved.

FTX asked for the court to award damages whose value would be determined at a trial. Bankman-Fried’s own trial on fraud charges will start on Oct. 3.

Finally, in the latest vivid example how lawyers always win, SBF’s parents are being sued for tens of millions, while the FTX lawyers are taking in about $1 million in fees every day. It remains unclear how many billions SBF himself managed to stash away in various crypto and offshore accounts, which will wait for him when he emerges from prison.

The adversary proceeding is Alameda Research LLC, et al. v. Allan Joseph Bankman and Barbara Fried, 22-110678, U.S. Bankruptcy Court for the District of Delaware.

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2913

OFFSHORE YUAN: UP TO 7.2933

SHANGHAI CLOSED DOWN 0.97 PTS OR 0.45%

HANG SENG CLOSED DOWN 66.62PTS OR 0.37%

2. Nikkei closed DOWN 290.30 PTS OR .87 %

3. Europe stocks SO FAR: ALL MOSTLY GREEN

USA dollar INDEX DOWN TO 104535 EURO RISES TO 1.0712 UP 20 BASIS PT

3b Japan 10 YR bond yield: RISES TO. +.705 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.70/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP// OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.7105***/Italian 10 Yr bond yield UP to 4.495*** /SPAIN 10 YR BOND YIELD UP TO 3.773…**

3i Greek 10 year bond yield RISES TO 4.096

3j Gold at $1936.60 silver at: 23.36 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 29 /100 roubles/dollar; ROUBLE AT 96.25//

3m oil into the 92 dollar handle for WTI and 95 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.61// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.705% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8955 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9594well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

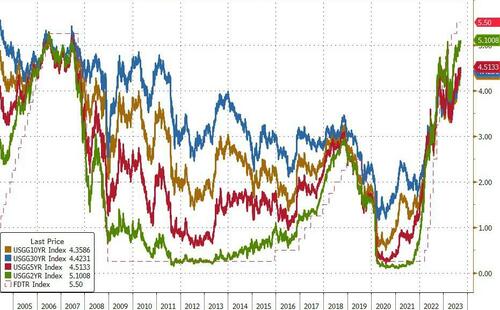

USA 10 YR BOND YIELD: 4.336 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.406 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 5.060 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 27.03…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 4 BASIS PTS AT 4.43905

end

2.a Overnight: Newsquawk and Zero hedge:

USA EARLY MORNING REPORT

Futures Flat As Traders Brace For Central Bank Deluge, Watch Surging Oil

TUESDAY, SEP 19, 2023 – 08:16 AM

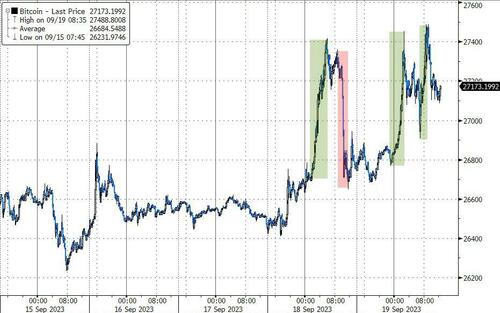

US futures were modestly in the green, reversing an earlier drop in Asian markets as traders awaited signals from central banks in a week full of monetary policy decisions. Europe’s Stoxx 600 benchmark climbed 0.3%, lifted by energy names with oil majors TotalEnergies, BP and Shell among the biggest contributors. As of 7:45am, S&P 500 futures and Nasdaq contracts were both up around 0.1%; crude rallied to a new 10 month high with Brent surpassing $95. The dollar and gold were flat while Bitcoin rose.

In premarket trading, mega-cap Tech names were mostly higher. Keep an eye on AAPL which is reportedly seeing better than expected iPhone demand despite a tepid reception to its announcement a week ago. Block, formerly known as Square, shares fall as much as 1.7% after the digital payments firm said that Alyssa Henry, the CEO of its Square business, is leaving, with Jack Dorsey to take over. Analysts said that the development was a surprise and may add to other concerns about the company, but welcomed Dorsey stepping in to the role. Here are some other notable premarket movers:

- Equinox Gold shares fall 10% after the company agrees to sell $150 million of 4.75% unsecured convertible senior notes due 2028.

- Nio falls 4.4% after reporting proposed offering of $500m of convertible senior notes due 2029 and $500m of convertible senior notes due 2030.

- Rackspace Technology shares are indicated higher after Raymond James upgraded the infrastructure-software company to outperform from market perform, saying its turnaround plan is gaining traction.

- Rocket Lab USA shares fall as much as 19%, after the spacecraft maker said its rocket had experienced an issue shortly after launch, forcing it to end the mission. It also postponed an upcoming mission.

In other news, the UAW set a Friday at 12pm ET deadline for a deal before expanding the strike. Macy’s is said to hire 38k holiday workers vs. 41k in 2022 and 76k in 2021. Today’s macro data focus is on Housing Starts and Building Permits; we’ll see if the hard data matches yesterday’s soft data which showed the NAHB Housing Index fall to the lowest level since April.

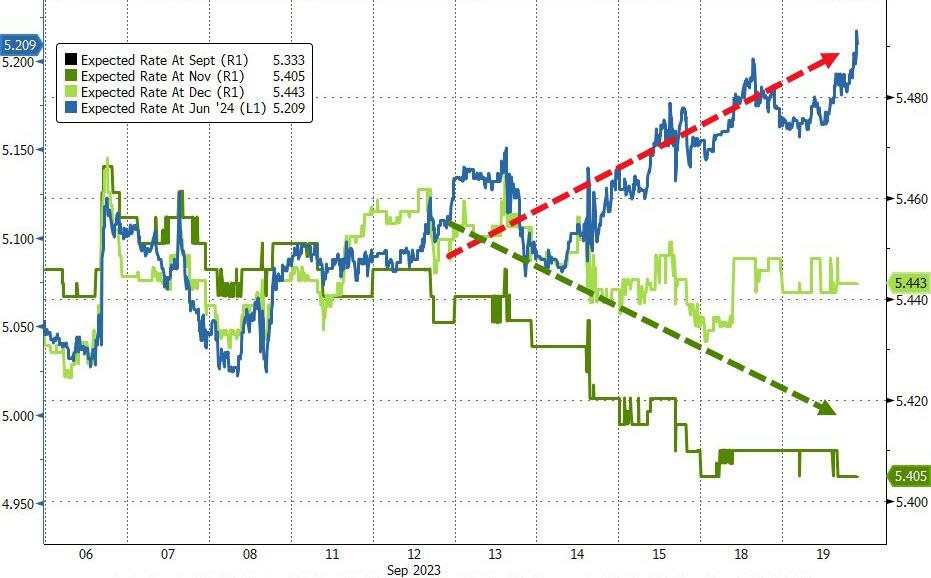

With the Fed forecast to keep interest rates on hold this week, traders will be focused on the so-called dot plot summary of economic forecasts. The two main questions are whether policymakers will retain their projections for one more 25 basis-point hike by year-end, and how much easing they are penciling in for 2024. In June, they projected one percentage point of cuts.

“The Fed is likely to highlight that in its collective view the fight against inflation has not yet been won and that the FOMC will be highly data-dependent in terms of future rate decisions, leaving the door open for a possible rate hike later in the year,” said Richard Flax, chief investment officer at European digital wealth manager Moneyfarm. “If the Fed sounds a more hawkish tone, we could see a continuation of the higher-for-longer trend that we’ve seen recently, with lower probability of significant rate cuts in 2024.”

Meanwhile, as reported yesterday, crude has soared by about a third since mid-June as Saudi Arabia and Russia joined hands to curb supplies and drive a rebound in prices. That has sustained the pressure on central bankers as they seek to cool inflation, while managing risks to their economies. The Federal Reserve sets policy Wednesday, the Bank of England Thursday and the Bank of Japan Friday.

“Central banks have done a rather good job so far, but there’s little room for manoeuvre now,” said David Kalfon, chief executive officer of Sanso Investment Solutions. “They made clear since the start of the cycle that beating inflation is the key, not growth.”

The prospect of rates staying higher for longer has not only drained some of the enthusiasm toward tech shares, after they led the rally in US stocks earlier this year, but may have popped the AI bubble. Flows suggest investors are positioning for more losses in the Nasdaq 100, according to Citigroup’s Chris Montagu who said that Nasdaq futures continued to attract bearish flows last week, leaving positioning heavier on short bets rather than long. That suggests “few investors are comfortable taking a bullish view on the possibility of a near-term reversal for the growth/tech related index,” they wrote in a note dated Sept. 18. The Nasdaq 100 is down about 3.9% from a peak on July 18.

European stocks managed to shrug off opening declines to trade slightly higher. The Stoxx 600 is up 0.2% with real estate, financial services and autos the best performing sectors. Oil majors TotalEnergies SE, BP Plc and Shell Plc were among the biggest contributors as Europe’s Stoxx 600 benchmark climbed 0.3%. Here are Europe’s biggest movers:

- Billerud shares gain as much as 9.4%, the most since 2020, after Jefferies upgraded its view on the Swedish paper and packaging firm to buy from hold, quoting year-to-date underperformance and easing wood costs heading into 2024.

- TUI shares rise as much as 6.6% after the package tour operator confirmed it expects underlying Ebit to grow significantly in 4Q and the full fiscal year, as holiday bookings continue to defy the cost-of-living squeeze.

- Ocado shares gain as much as 5% after the UK online grocer reported sales growth in the third quarter. Bernstein said the update shows good progress toward the company’s full-year guidance of mid-single-digit revenue growth.

- Volkswagen rises as much as 3.4%, the best performer in Germany’s DAX index, after Jefferies double-upgrades the shares to buy from underperform, citing the potential for improvements and cost cuts in 2024, as well as the stock’s attractive valuation.

- Avacta shares rise as much as 15% after the UK biotech provided an update to its key AVA6000 trial, saying the “excellent safety profile” of the chemotherapy candidate “continues to be observed in the sixth dose escalation cohort.”

- British Land shares gain as much as 2.6% after UK landlord upgrades retail park ERV growth guidance for FY2024 to 3%-5% from 2%-4% on the back of continued “significant leasing momentum,” according to a statement.

- Kion shares fall as much as 4.1% after an offering of shares from Invesco via Goldman Sachs priced at €35.20 apiece, representing an approximately 5.8% discount to the last close.

- SocGen shares fall as much as 3.3% after the co. suffered rating downgrades from BNP Paribas Exane and HSBC after the French lender’s new CEO failed to win over investors with a new strategic plan on Monday.

- SMCP Shares in France’s SMCP plunged as much as 29% amid huge trading volumes on Monday after the owner of fashion brands Sandro, Maje, Claudie Pierlot and Fursac, cut its 2023 guidance, citing a slowdown in Europe and lower-than-expected Chinese consumption.

- Naked Wines shares drop as much as 10%, the most since July 4, after the online wine merchant said sales fell in the first quarter of the current fiscal year and predicted a decline in revenue for the year. Higher profits have come at the expense of sales, according to Stifel.

- Kingfisher shares fall as much as 7.2% after the home improvement retailer reported first-half results that missed estimates and provided an outlook for the year which was also below expectations. Analysts flagged weakness in Poland during the first half.

Earlier in the session, Asian stocks fell for a second day as traders awaited a slew of major central bank decisions, with rising inflationary pressure from higher oil prices keeping the door open for hawkish messages. The MSCI Asia Pacific Index dropped as much as 0.4% on Tuesday before closing almost flat, led by technology and health-care shares.

- Hong Kong and mainland Chinese benchmarks traded in a tight range as investors weighed the recent green shoots in economic data against ongoing property sector woes. They are closely monitoring headlines from distressed developers for further clues on their financial health. Sentiment was driven by pressure in tech and mixed fortunes among the property stocks but downside stemmed following further US-China talks and the PBoC’s continued liquidity efforts.

- Japan’s Nikkei 225 underperformed as recent losses in the region caught up to the index on return from the holiday closure and with sentiment also dampened with participants second-guessing if BoJ Governor Ueda will lay the groundwork this week for a future exit.

- Australia also slid as traders parsed minutes from the central bank’s September meeting. The ASX 200 was pressured as weakness in real estate and financials led the declines from early on, while the RBA minutes from the September meeting provided very little in the way of new information.

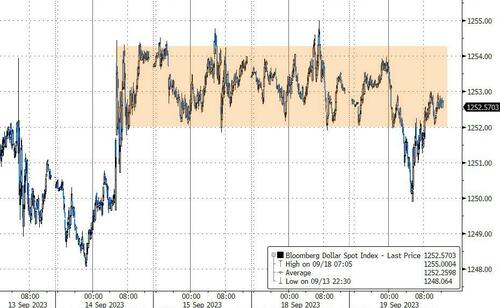

In FX, the Bloomberg Dollar Spot Index is down 0.1%, the Norwegian krone and the Swedish krona were among the best performers in the Group-of-10 ahead of central bank decisions in both countries on Thursday The pound and euro are flat with the latter showing little reaction to a downward revision to euro area CPI.

- The Australian dollar gained; the Reserve Bank of Australia considered the case for raising borrowing costs this month, according to minutes of the Sept. 5 meeting

- The euro fell for a first day in three after hitting its lowest level since March last week; common currency could be already in mean-reversion mode according to options.

In rates, treasuries are little changed as US trading day begins, with futures near high end of Monday’s ranges, after plying narrow ranges during Asia session and London morning. Volumes and flows remain thin ahead of Wednesday’s Fed policy announcement. Tuesday session includes 20-year bond reopening and housing starts data. Yields across the curve are higher on the day by less than 2bp, 10-year near 4.32%, rising 2bps from Monday’s close with bunds and gilts outperforming by 1.5bp and 6bp in the sector; UK bonds outperform in Europe ahead of domestic August CPI due Wednesday. Dollar IG issuance slate includes World Bank 5Y and is expected to grow; 10 issuers sold almost $15b Monday and at least one issuer stood down. Treasury coupon auctions resume with $13b 20-year bond reopening at 1pm New York time; this week also includes a $15b 10-year TIPS reopening Thursday.

In commodities, oil continues to climb with WTI futures up 1.1% at YTD high and approaching $93/bbl while Brent briefly rose above $95 for the first time this year.

Looking to the day ahead now, and data releases include US housing starts and building permits for August, as well as Canada’s CPI for August. Otherwise, central bank speakers include the ECB’s Elderson.

Market Snapshot

- S&P 500 futures little changed at 4,505.25

- MXAP down 0.1% to 162.78

- MXAPJ down 0.2% to 503.25

- Nikkei down 0.9% to 33,242.59

- Topix little changed at 2,430.30

- Hang Seng Index up 0.4% to 17,997.17

- Shanghai Composite little changed at 3,124.96

- Sensex down 0.4% to 67,596.84

- Australia S&P/ASX 200 down 0.5% to 7,196.63

- Kospi down 0.6% to 2,559.21

- STOXX Europe 600 up 0.2% to 457.69

- German 10Y yield little changed at 2.70%

- Euro little changed at $1.0688

- Brent Futures up 0.7% to $95.13/bbl

- Gold spot up 0.0% to $1,934.08

- U.S. Dollar Index down 0.12% to 105.07

Top Overnight News

- Secretary of State Blinken and Chinese Vice resident Han Zheng sounded conciliatory following a meeting Monday at the UN, the latest sign that relations between the two countries may be modestly thawing. SCMP

- The world economy is set for a slowdown as interest-rate increases weigh on activity and China’s rebound disappoints, the OECD said. Growth will ease to 2.7% in 2024 after an already “sub-par” expansion of 3% this year, according to its latest forecasts. BBG

- Senior Chinese officials were told that an internal Communist Party investigation found ex-Foreign Minister Qin Gang to have engaged in an extramarital affair that lasted throughout his tenure as Beijing’s top envoy to Washington. Qin, once considered a trusted aide to leader Xi Jinping, was stripped of his foreign minister title in July—without explanation—after he disappeared from public view a month earlier. At one point leading up to his ouster, the Foreign Ministry said the absence of 57-year-old Qin was due to health reasons. WSJ

- Japan’s BOJ isn’t expected to make any changes Thurs night, but Ueda will continue to lay the rhetorical groundwork for a further normalization of policy. BBG

- India rejected allegations by Justin Trudeau that its agents were behind the June 18 assassination of a prominent Sikh leader in British Columbia, calling them “absurd and motivated,” and moved to expel a Canadian diplomat. The festering ties threaten to derail plans for an early-stage trade deal. BBG

- The UAW warned it will expand its auto workers’ strike from noon Friday if “serious progress” isn’t made in talks with Ford, GM and Stellantis. The Chrysler parent described resumed negotiations as “constructive,” but union leader Shawn Fain told NPR they have a “long way to go.” BBG

- Trump plans to skip the next GOP debate on Sept 27 and instead address a crowd in Detroit as the former president looks to inject himself into the UAW strikes. NYT

- McCarthy’s fiscal blueprint, unveiled over the weekend, doesn’t have enough Republican support to make it out of the House (and it was already DOA in the Senate and White House), raising the odds of a shutdown at the end of the month. NYT

- Crude rallied, with Brent tipping over $95. Rising energy costs may cause a significant reversal in US headline inflation, forcing the Fed to act more aggressively. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly lower following the flat performance stateside amid a lack of catalysts and with risk appetite sapped as markets brace for the approaching flurry of central bank meetings. ASX 200 was pressured as weakness in real estate and financials led the declines from early on, while the RBA minutes from the September meeting provided very little in the way of new information. Nikkei 225 underperformed as recent losses in the region caught up to the index on return from the holiday closure and with sentiment also dampened with participants second-guessing if BoJ Governor Ueda will lay the groundwork this week for a future exit. Hang Seng and Shanghai Comp were choppy owing to the pressure in tech and mixed fortunes among the property stocks but with downside stemmed following further US-China talks and the PBoC’s continued liquidity efforts.

Top Asian News

- Chinese Foreign Minister Wang said China and Russia pursue an independent foreign policy and the cooperation between the sides is not aimed at a third party and will not be influenced by a third party. Wang also stated that China and Russia should follow the trend of progress of the times, show their responsibilities as major countries, fulfil their international obligations and strengthen strategic cooperation.

- China summoned the German envoy after German Foreign Minister Baerbock’s recently described Chinese President Xi as a dictator on US television, according to SCMP.

- European Commission Vice President Vera Jourova said it is important that China and EU keep communications open including in various degrees where they disagree, while she added China is a partner, competitor and systemic rival for Europe. Furthermore, she added that China’s continued economic success requires an attractive investment environment for foreign companies and that the EU does not seek to decouple from China.

- RBA Minutes from the September 5th meeting stated they considered raising rates by 25bps or holding steady and the case for holding steady was stronger, while it added that recent data did not materially alter the economic outlook. Furthermore, it reiterated that some further tightening of monetary policy may be required should inflation prove more persistent than expected.

- Japan ruling LDP senior official Seko says economic stimulus of a minimum of JPY 15tln is needed, and desirably JPY 20tln, according to Jiji press; size of economic stimulus must be around 3% of GDP.

European bourses are in the green, Euro Stoxx 50 +0.2%, though only modestly so with the space struggling to reclaim lost ground from Monday. Sectors are primarily in the green, with outperformance seen in Autos following a double-upgrade to Volkswagen while Retail lags in the red amid pressure in Kingfisher who cut FY guidance. Stateside, futures are in-fitting with European peers in posting a slight positive bias but generally struggling for direction as we await the Fed to kick off a blockbuster week of Central Bank activity; ES +0.2%.

Top European News

- OECD: The world economy is expected to grow by 3.0% in 2023, before slowing down to 2.7% in 2024. A disproportionate share of global growth in 2023-24 is expected to continue to come from Asia, despite the weaker-than-expected recovery in China.

- BoE’s Woods (FPC/PRC) says we are seeing a pick-up in impairments across the financial sector from a very low base, interested in banks’ exposure to the Chinese property sector.

FX

- Buck continues to buckle in the build-up to FOMC and a host of other Central Bank confabs, DXY edges closer to 105.000 within incrementally lower 105.210-010 range.

- Kiwi, Loonie and Aussie elevated amidst strength in underlying commodities, NZD/USD comfortably above 0.5900 pre-NZ current account data, AUD/USD probing 0.6450 post-hawkish RBA minutes and USD/CAD sub-200 DMA awaiting Canadian CPI.

- Sterling, Euro and Yen all hovering near big figures vs. Dollar, at 1.2400, 1.0700 and 148.00 respectively.

- PBoC set USD/CNY mid-point at 7.1733 vs exp. 7.2839 (prev. 7.1736)

Fixed Income

- Bonds bounce broadly, but not uniformly as the countdown to Central Bank-fest continues.

- Gilts outperform mainstream peers within 95.46-94.94 range pre and post-well received 2053 DMO sale.

- Bunds toppy above 130.00 between 130.10-129.80 parameters and T-note lags in tight 109-20/14 band awaiting US housing data, 20 year supply and the start 2-day Fed meeting.

Commodities

- WTI and Brent November futures remain on a positive footing after settling firmer on Monday with known fundamentals keeping the complex underpinned.

- However, following the OECD downgrades to 2024 growth views for numerous key economies including the EZ, Germany, UK & China some pressure has been seen across the commodity space; currently, WTI and Brent are firmer by circa. USD 0.50/bbl, having trimmed by a similar magnitude from earlier highs which saw Brent eclipse USD 95.00/bbl.

- Spot gold is essentially unchanged on the session given the USD remains contained overall but has been somewhat choppy within the current bounds, yellow metal continues to trade on either side of the 50-DMA at USD 1931/oz.

- Base metals are pressured given APAC losses and with further pressure emanating from the mentioned OECD forecasts.

Geopolitics

- G7 Foreign Ministers meeting chair Japan said Russia must withdraw its troops and military equipment from the internationally recognised territory of Ukraine immediately, completely and unconditionally, while G7 members condemned Russia for staging sham elections in illegally occupied territories of Ukraine and will never recognise Russia’s illegitimate claims. G7 reiterated the call on third parties to cease any and all assistance to Russia’s war of aggression or face severe costs and it called on China to press Russia to stop its military aggression and immediately withdraw its troops from Ukraine.

- Russian and Chinese Foreign Ministers noted the ‘futility’ of attempts to resolve the Ukraine crisis without due account for Russian interest and participation, while they also noted the closeness of their positions on the anti-Russian and anti-Chinese character of US actions in international affairs, according to Reuters.

- US State Department said following a meeting between Secretary of State Blinken and Chinese Vice President Han that the sides had a candid and constructive discussion. Furthermore, they exchanged views on Russia’s war in Ukraine and North Korea’s provocative actions, while Blinken underscored the importance of peace across the Taiwan Strait, according to Reuters.

- US, Japan and South Korea officials shared concerns that Russia-North Korea cooperation may have a negative impact on peace and stability in the Indo-Pacific, according to Japan’s Foreign Ministry.

- South Korean Foreign Ministry announced the successful transfer of Iran’s frozen funds to a third country and hopes that this will lead to the development of bilateral ties, according to Reuters.

- White House said it was deeply concerned about allegations made by Canadian PM Trudeau regarding the killing of a Sikh leader and it is critical that Canada’s investigation proceed and perpetrators are brought to justice. Furthermore, India’s government said allegations of Indian government involvement in any act of violence in Canada are absurd and motivated, while it added that allegations made by Canadian PM Trudeau to PM Modi regarding India’s involvement in any act of violence in Canada were completely rejected, according to Reuters.

- IAEA says negotiations with Iran are not progressing as quickly as required, according to Al Arabiya.

- Azerbaijan’s Defence Ministry has started “anti-terrorist” operations in Karabakh, according to Tass; “Large fighting begins near Stepanakert in Nagorno-Karabakh as Azerbaijan announces start of operation”, according to ELINT News.

US Event Calendar

- 08:30: Aug. Housing Starts MoM, est. -0.9%, prior 3.9%

- 08:30: Aug. Housing Starts, est. 1.44m, prior 1.45m

- 08:30: Aug. Building Permits MoM, est. -0.2%, prior 0.1%

- 08:30: Aug. Building Permits, est. 1.44m, prior 1.44m, revised 1.44m

DB’s Jim Reid concludes the overnight wrap

The overarching narrative behind the trilogy is that the financial world experienced a unique golden era during 1980-2020, but that the trends that enabled this super-cycle are set to reverse going forward. The pandemic accelerated this process, but we think those forces would likely have arisen in the 2020s regardless. For instance, inflation is back in a way we haven’t experienced in a generation, and there’s been a rapid rise in real yields over the last couple of years as well. All this is going to severely constrain the ability of policymakers to manage the business cycle. As a result, we think there’s going to be a higher frequency of recessions over the coming years and decades.

The second half of the study includes our updated multi-asset class returns across numerous DM and EM countries going back over 200 years where possible. We review the decade so far, which for bonds and 60/40 portfolios is up there with the worst on record. Commodities are outperforming, whilst equities are mixed depending on the country. For instance, US, Japanese and Indian bourses are outperforming history and leading the way. But others are still down over the 2020s in real terms.