GOLD PRICE CLOSED: UP $13.00 TO $1945.60

SILVER PRICE CLOSED: UP $0.35 AT $23.55

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1932.20

Silver ACCESS CLOSE: 23.25

Shanghai Gold Benchmark Price

USD oz  AM2001.82

AM2001.82

PM2006.49

Historical SGE Fix

NEW YORK PRICE AT THE SAME TIME: $1933.00

premium $73.00

xxxxxxxxxxxxxxxxxx

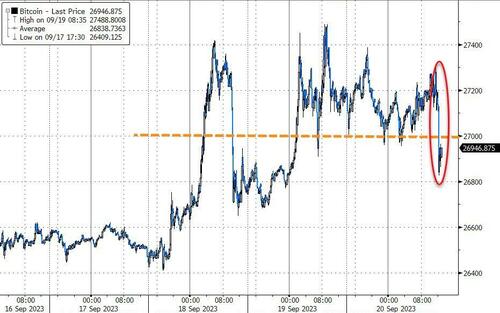

Bitcoin morning price:, $27,102 DOWN 28 Dollars

Bitcoin: afternoon price: $26,927 DOWN 209 dollars

Platinum price closing $937.35 DOWN $29.30

Palladium price; $1283.00 UP $17,80

END

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

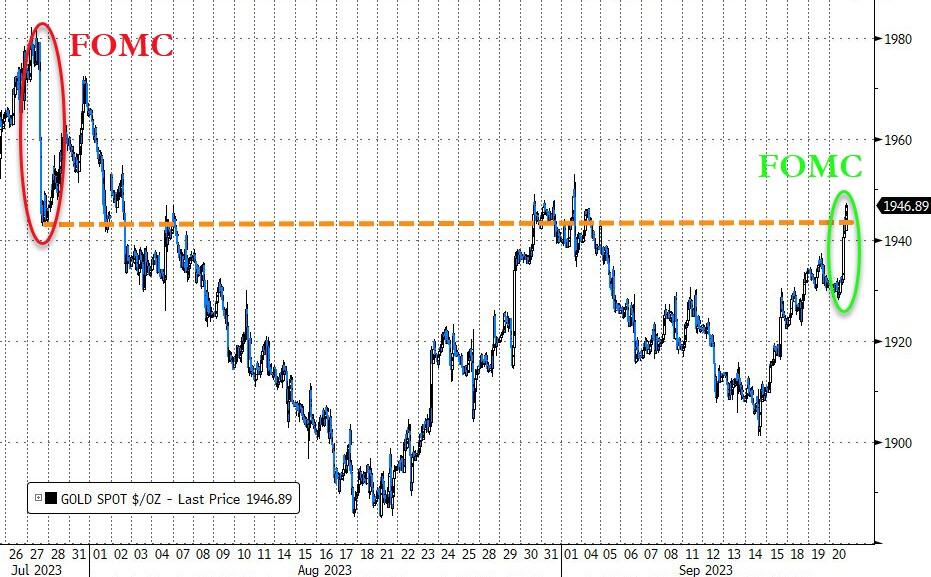

FOMC; today’s FOMC and resultant action was all pre ordained. The banker crooks wanted a much higher gold/silver smack than what they got. The reason: gold arbitrage through London-Shanghai and Moscow is killing them!

xxxxxxxx

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,703.78 UP 7,46 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1565,19 UP 6.78 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1812.26 UP 3.82 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,932.000000000 USD

INTENT DATE: 09/19/2023 DELIVERY DATE: 09/21/2023

FIRM ORG FIRM NAME ISSUED STOPPED

323 H HSBC 1

435 H SCOTIA CAPITAL 1

624 H BOFA SECURITIES 1

737 C ADVANTAGE 3

TOTAL: 3 3

MONTH TO DATE: 3,867

JPMorgan stopped 0/22 contracts.

FOR SEPT.:

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2023. CONTRACT: 3 NOTICES FOR 300 OZ or 0.00933 TONNES

total notices so far: 3867 contracts for 386,700 oz (12.027 tonnes)

FOR SEPT:

SILVER NOTICES: 1 NOTICE(S) FILED FOR 5,000 OZ/

total number of notices filed so far this month : 2617 for 13,085,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD UP $13.00

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: //A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/

INVENTORY RESTS AT 878.83 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER UP 35 CENTS AT THE SLV// NO CHANGES IN SILVER INVENTORY AT THE SLV:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 450.133 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A GOOD SIZED 409 CONTRACTS TO 125,749 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS GOOD SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR $0.0 GAIN IN SILVER PRICING AT THE COMEX ON TUESDAY. TAS ISSUANCE WAS A FAIR SIZED 393 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 395 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.00). AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A HUGE GAIN OF 1397 OI CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

A HUGE ISSUANCE OF EXCHANGE FOR PHYSICALS( 903 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 14.420 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S ZERO QUEUE JUMP OF NIL OZ//NEW TOTAL 13.410 MILLION OZ + OUR CRIMINAL ISSUANCE OF 0 EXCHANGE FOR RISK CONTRACTS//NEW TOTALS EXCHANGE FOR RISK: 3.0 MILLION OZ: NEW TOTALS SILVER STANDING: 16.410 MILLION OZ// /// / //FAIR SIZED COMEX OI GAIN/ GOOD SIZED EFP ISSUANCE/VI) FAIR SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 395 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -85 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTRACTS for 13 days, total 9780 contracts: OR 48.900 MILLION OZ (752 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 48.900 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 48.900 MILLION OZ (SMALLER THIS MONTH)

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 409 CONTRACTS DESPITE OUR GAIN IN PRICE OF $0.0 IN SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 903 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR SEPT OF 14.2 MILLION OZ FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP .+ 0 MILLION OZ EXCHANGE FOR RISK//PRIOR TOTAL FOR EXCHANGE FOR RISK = 3.0 MILLION OZ/TOTAL EXCH. FOR RISK /NEW TOTALS STANDING 16.410 MILLION OZ// /// WE HAVE A HUMONGOUS SIZED GAIN OF 1312 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A FAIR SIZED 395 CONTRACTS//SMALL FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION AS THE SHORTS CAPITULATED. THE NEW TAS ISSUANCE TUESDAY NIGHT (395) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 1 NOTICE(S) FILED TODAY FOR 5,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2467 CONTRACTS TO 438,078 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED: –0 CONTRACTS

WE HAD A FAIR SIZED DECREASE IN COMEX OI ( 2467 CONTRACTS) DESPITE OUR TINY $0.60 GAIN IN PRICE//TUESDAY. WE ALSO HAD A RATHER STRONG INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 12.656 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 400 OZ QUEUE JUMP //NEW TOTAL STANDING 14.510 TONNES + /A FAIR (AND CRIMINAL) ISSUANCE OF 862 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH OUR $0.60 GAIN IN PRICE WITH RESPECT TO TUESDAY’S TRADING.WE HAD A TINY SIZED GAIN OF 195 OI CONTRACTS (0.6065 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2662 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 440,545

IN ESSENCE WE HAVE A TINY SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 195 CONTRACTS WITH 2467 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 2662 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 195 CONTRACTS OR 0.6065 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 862 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2662 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI (2867) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 195 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 12.656 TONNES FOLLOWED BY TODAY’S QUEUE JUMP TO LONDON OF 400 OZ/// 3) ZERO LONG LIQUIDATION WITH SOME TAS LIQUIDATION COVERING THEIR SHORTFALL DURING THE COMEX SESSION //4) FAIR SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 862 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT :

TOTAL EFP CONTRACTS ISSUED: 31,207 CONTRACTS OR 3,120,700 OZ OR 97.06 TONNES IN 13 TRADING DAY(S) AND THUS AVERAGING: 2400 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAY(S) IN TONNES 97.06 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 97.07/3550 x 100% TONNES 2.73% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 97.07 TONNES (SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A GOOD SIZED 409 CONTRACTS OI TO 125,749 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A GOOD 395 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 903 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 903 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 494 CONTRACTS AND ADD TO THE 903 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1312 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 6.560 MILLION OZ

OCCURRED DESPITE OUR $0.00 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING//TUESDAY NIGHT

SHANGHAI CLOSED DOWN 16.39 PTS OR 0.52% //Hang Seng CLOSED DOWN 111.57 PTS OR 0.62%/ /The Nikkei CLOSED DOWN 218.81 PTS OR .66% //Australia’s all ordinaries CLOSED DOWN 0.45 % /Chinese yuan (ONSHORE) closed DOWN AT 7.2966 /OFFSHORE CHINESE YUAN DOWN TO 7.3032 /Oil DOWN TO 90.49 dollars per barrel for WTI and BRENT UP AT 93.62 / Stocks in Europe OPENED ALL GREEN// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 2497 CONTRACTS TO 438,078 DESPITE OUR TINY GAIN IN PRICE OF $0.60 ON TUESDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 2662 EFP CONTRACTS WERE ISSUED: : DEC 2662 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2662 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A TINY SIZED TOTAL OF 195 CONTRACTS IN THAT 2662 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED LOSS OF 2467 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR SMALL ADVANCE IN PRICE OF $0.60//TUESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR FRIDAY NIGHT WAS A FAIR 862 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: SEPT (14.510) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 14.510 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $0.60) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A TINY GAIN OF 195 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD A SOME T.A.S. LIQUIDATION ON THE FRONT END OF TUESDAY’S TRADING. THE T.A.S. ISSUED ON TUESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 0.6065 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPT. (12.656 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 400 OZ//NEW STANDING 14.510 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $0.60.

WE HAD – REMOVED 0 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 195 CONTRACTS OR 19500 OZ OR 0.6065 TONNES.

Estimated gold volume today:// 191,029 poor

final gold volumes/yesterday 139,618 awful

//speculators have left the gold arena

//SEPT 20/ /// THE SEPT. 2023 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 10,522.942 OZ ASAHI BRINKS . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | NIL |

| No of oz served (contracts) today | 3 notice(s) 300 OZ 0.00933 TONNES |

| No of oz to be served (notices) | 798 contracts 79800 oz 2.482 TONNES |

| Total monthly oz gold served (contracts) so far this month | 3867 notices 386700 OZ 12.027 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: NIL oz

customer deposits: 0

total customer deposits: NIL oz

we had 2 customer withdrawals

i) Out of ASAHI 8583.231 oz

ii) Out of Brinks 1739.711 oz

total withdrawals 10,322.942 oz oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPTEMBER.

For the front month of SEPTEMBER we have an oi of 801 contracts having LOST 18 contracts. We had

22 contracts were served on TUESDAY, so we GAINED an additional 4 CONTRACTS or AN ADDITIONAL 400 oz will stand for delivery in this non active delivery month of Sept

Oct LOST 435 contracts to 22,985 contracts.

NOV GAINED 74 CONTRACTS to stand at 98

December LOST 2733 contracts UP to 375,019 contracts.

We had 3 contracts filed for today representing 300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 3 notices were issued from their client or customer account. The total of all issuance by all participants equate to 22 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2023. contract month,

we take the total number of notices filed so far for the month (3867 x 100 oz ), to which we add the difference between the open interest for the front month of SEPT (801 CONTRACTS) minus the number of notices served upon today 3 x 100 oz per contract equals 466,500 OZ OR 14.510 TONNES the number of TONNES standing in this non active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month: No of notices filed so far (3867) x 100 oz + (xxx) {OI for the front month} minus the number of notices served upon today (3) x 100 oz) which equals 466,100 oz standing OR 14.500 TONNES

TOTAL COMEX GOLD STANDING: 14.510 TONNES WHICH IS HUGE FOR AN INACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,016,871.449 OZ 62.733 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 20,931,908.140 OZ

TOTAL REGISTERED GOLD 10,801,765.332 (335,98 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,130,142.808 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,784,894 OZ (REG GOLD- PLEDGED GOLD) 273.24 tonnes//dropping like a stone

END

SILVER/COMEX

SEPT 20

//2023// THE SEPT 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | nil oz . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 30,954.871 oz Delaware |

| No of oz served today (contracts) | 1 CONTRACT(S) (5,000 OZ) |

| No of oz to be served (notices) | 65 contracts (325,000 oz) |

| Total monthly oz silver served (contracts) | 2617 Contracts (13,085,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposit customer account:

i) Into Delaware: 30,954.871 oz

total customer deposit 30,954.891 oz

JPMorgan has a total silver weight: 136.901 million oz/274.079 million or 50.00%

Comex withdrawals 0

total: nil oz

adjustments: 2 dealer to customer

i)ASAHI 100,108.290 oz

ii) Malca 242,497.900 oz

TOTAL REGISTERED SILVER: 42.062 MILLION OZ//.TOTAL REG + ELIGIBLE. 274,074 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR August:

silver open interest data:

FRONT MONTH OF SEPT /2023 OI: 66 CONTRACTS HAVING LOST 5 CONTRACT(S). WE HAD 5

CONTRACT SERVED ON TUESDAY. SO WE GAINED 0 CONTRACTS OR NIL ADDITIONAL OZ WILL STAND FOR SILVER AT THE COMEX..

OCT LOST 8 CONTRACTS TO STAND AT 1017.

NOVEMBER GAINED 0 CONTRACTS TO STAND AT 140

DEC. GAINED 280 CONTRACTS TO STAND AT 113,253 .

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1 for 5,000 oz

Comex volumes// est. volume today 51,903 poor

Comex volume: confirmed yesterday 43,049 poor

To calculate the number of silver ounces that will stand for delivery in SEPT. we take the total number of notices filed for the month so far at 2617 x 5,000 oz = 13,085,000 oz

to which we add the difference between the open interest for the front month of SEPT (66) and the number of notices served upon today 1 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT/2023 contract month: 2617 (notices served so far) x 5000 oz + OI for the front month of SEPT (66) – number of notices served upon today (1 )x 500 oz of silver standing for the SEPT contract month equates to 13.410 million oz. + 0 MILLION EXCHANGE FOR RISK..NEW TOTALS EXCHANGE FOR RISK: 3.0 MILLION OZ//NEW TOTAL STANDING FOR SILVER: 16.410 MILLION OZ//

There are 42.062 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

SEPT 20/WITH GOLD UP $13.00 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/ : // //INVENTORY RESTS AT 878.83 TONNES

SEPT 19/WITH GOLD UP $0.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD : // //INVENTORY RESTS AT 880.217 TONNES

SEPT 18/WITH GOLD UP $8.40 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD : A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 880.217 TONNES

SEPT 15/WITH GOLD UP $13.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD : A WITHDRAWAL OF 1.055 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 879.70 TONNES

SEPT 14/WITH GOLD UP $1.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD : A WITHDRAWAL OF 4.63 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 882.01 TONNES

SEPT 13/WITH GOLD DOWN $2.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 12/WITH GOLD DOWN $11.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 11/WITH GOLD UP $4.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 8/WITH GOLD UP $0.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 7/WITH GOLD DOWN $0.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.22 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.69 TONNES

SEPT 6/WITH GOLD DOWN $8.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.81 TONNES

SEPT 5/WITH GOLD DOWN $13.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.97 TONNES

SEPT 1/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 31/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 30/WITH GOLD UP $8.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.59 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.23 TONNES

AUGUST 29/WITH GOLD UP 17.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.6 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.64 TONNES

AUGUST 28/WITH GOLD UP $6.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / //INVENTORY RESTS AT 884.04 TONNES

AUGUST 25/WITH GOLD DOWN $6.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 884.04 TONNES

AUGUST 24/WITH GOLD UP $0.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //INVENTORY RESTS AT 884.91 TONNES

AUGUST 23/WITH GOLD UP $21.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 4.32 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 884.91 TONNES

AUGUST 22/WITH GOLD UP $2.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 0.87 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 889.23 TONNES

AUGUST 21/WITH GOLD UP $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.60 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 890.10 TONNES

AUGUST 18/WITH GOLD UP $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 6.92 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 887.50 TONNES

AUGUST 17/WITH GOLD DOWN $12.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: /// //INVENTORY RESTS AT 894.42 TONNES

GLD INVENTORY: 878.83 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 19/WITH SILVER UP 35 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 450.133 MILLION OZ

SEPT 19/WITH SILVER UP 0 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 8.801 MILLION OZ INTO THE SLV. : // /.////INVENTORY RESTS AT 450.133 MILLION OZ

SEPT 18/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 1.651 MILLION OZ INTO THE SLV. : // /.////INVENTORY RESTS AT 441.332 MILLION OZ

SEPT 15/WITH SILVER UP 37 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.31 MILLION OZ FROM THE SLV. : // /.////INVENTORY RESTS AT 439.681 MILLION OZ

SEPT 14/WITH SILVER DOWN 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: : // /.////INVENTORY RESTS AT 440.736 MILLION OZ

SEPT 13/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1,009 MILLION OZ INTO THE SLV//: // /.////INVENTORY RESTS AT 440.736 MILLION OZ

SEPT 12/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.209 MILLION OZ INTO TEH SLV//: // /.////INVENTORY RESTS AT 439.727 MILLION OZ

SEPT 11/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.209 MILLION OZ INTO TEH SLV//: // /.////INVENTORY RESTS AT 439.727 MILLION OZ

SEPT 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 7/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 6/WITH SILVER DOWN 36 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.373 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 5/WITH SILVER DOWN 69 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 734,000 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 437.891 MILLION OZ

SEPT 1/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 440.00 MILLION OZ

AUGUST 31/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 438.625 MILLION OZ

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.834 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 443.210 MILLION OZ

AUGUST 29/WITH SILVER UP 49 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 183,000 OF SILVER INTO THE THE SLV// /.////INVENTORY RESTS AT 445.044 MILLION OZ

AUGUST 28/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.281 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 444.861 MILLION OZ

AUGUST 25/WITH SILVER UP ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.751 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 446.145 MILLION OZ

AUGUST 24/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.651 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 448.896 MILLION OZ

AUGUST 23/WITH SILVER UP 94 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 826,000 OZ FROM THE SLV// /.////INVENTORY RESTS AT 450.547 MILLION OZ

AUGUST 22/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: /.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 21/WITH SILVER UP 59 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 917,0000 OZ FROM THE SLV//.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 18/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 17/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

CLOSING INVENTORY 450.133 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

Peter Schiff: The Inflation War Is Over; Inflation Won!

https://WWW.ZEROHEDGE.COM/MARKETS/PETER-SCHIFF-INFLATION-WAR-OVER-INFLATION-WON

WEDNESDAY, SEP 20, 2023 – 12:05 PM

After the August CPI data came out, Paul Krugman declared that the inflation war was over. The Biden administration and the Fed won the fight. In his podcast, Peter Schiff said he actually agrees with Krugman, at least in part. The inflation war is over. But who really won?

Last week’s CPI data showed price inflation heating up again, driven by climbing oil prices. Despite CPI rising to 3.7% in August after dipping to 3.2% a month earlier, Peter said most people still think everything is fine.

I think the more important aspect of the inflation data was how few people seem to comprehend what it means. Most of the talk I hear by the talking heads on the financial media is that everything is great. The inflation threat is pretty much behind us. Yeah, there are a few more bumps in the road, but we’re on the road to 2%. No problem. We’ll be there. The Fed is going to be cutting interest rates by next year, so these high rates aren’t really a problem. It’s just a temporary nuisance until we get back to low rates.”

Peter mentioned one pundit who proclaimed inflation has topped out and it’s coming down.

How can he say that when if you actually look at what’s happening, it’s the reverse? Inflation has bottomed out and now it’s rising.”

We had a long run of low inflation as the government measures it. (Not necessarily how people live it.) We enjoyed more than a decade with CPI averaging less than 2%. That all changed in 2021. Peter called it the “breakout year” for inflation. Then in 2022, it got even worse.

If you think of inflation like a stock, this was a massive breakout. You had a 10-year consolidation, kind of below this 2% resistance, and now it’s a massive breakout above 2%.”

Peter said it looks like 2023 will be a bit of a pullback.

If you were a trader, you would want to buy inflation. Inflation looks very bullish on a chart. It broke out and now you got a little bit of a pullback, and it’s an opportunity to buy the pullback following the breakout. All the evidence is inflation is heading a lot higher.”

Oil prices closed above $90 last week. They are up 8% in September already. Meanwhile, interest rates continue to climb. Americans have a lot of debt and they use a lot of energy. In other words, two important inputs in the US economy continue to get more expensive. At least some of those costs will be passed on to consumers and that will ultimately be reflected in the CPI.

It’s obvious to anybody who opens their eyes that inflation is not topped out and coming down. It’s bottomed out and going up. And the people who are blind to this, who are asleep, they are in for a rude awakening. That is a lot of investors.”

Peter said the thinks we’ll see much worse price inflation in 2024.

All of these rosy Goldilocks scenarios that are out there, they’re all going to fall apart in 2024.”

Nevertheless, after the August CPI data came out, Paul Krugman loudly declared the inflation war was over and the Fed won.

According to Paul Krugman, the economy is great, and we’ve won the war on inflation, and there’s no recession. I mean, how wrong can one guy be?”

Peter said he does think Krugman is right about one thing though.

I agree with Krugman that the inflation war is over. I just disagree on who won. I think inflation won!”

Of course, the Federal Reserve hasn’t officially surrendered, but Peter said when it does, gold is going to go ballistic.

You don’t want to wait for that to buy it. You want to head over to SchiffGold and buy your gold now, and your silver, before this next breakout. Because when it moves, I am convinced it’s going ot be fast.”

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

3,Chris Powell of GATA provides to us very important physical commentaries

Bullion fund founder and Canadian Nick Barisheff dies

(GATA)

Bullion fund founder, monetary metals advocate Nick Barisheff dies

Submitted by admin on Tue, 2023-09-19 08:59Section: Daily Dispatches

Board of Directors of BMG Group Inc., Announces the Passing of Industry Icon Nick Barisheff

Company Announcement

Monday, September 18, 2023

MARKHAM, Ontario, Canada — The Board of Directors at BMG Group Inc. sadly informs the public of the passing of Nick Barisheff on Friday, September 15.

Nick Barisheff was the founder, chair, and CEO of BMG Group Inc.

The company extends its sincerest condolences to Nick’s family and friends and mourns the loss of a great Canadian.

Nick was an industry icon in the bullion bars business and the acclaimed author of the book titled “$10,000 Gold: Why Gold’s Inevitable Rise Is the Investor’s Safe Haven.” Nick was also the author of a weekly BMG eNewsletter, “The BullionBuzz,” where he shared his expert insights with investors and curated the top must-read news items related to the financial markets and precious metals.

Over multiple decades, Nick was deeply involved in the precious metals sector, staunchly advocating for the many benefits that investors can realize through the ownership of physical gold, silver, and platinum bullion. Leveraging his profound comprehension of the precious metals market, Nick prepared various strategies, offerings, and solutions tailored to clients seeking to incorporate bullion assets into their investment portfolios. …

… For the remainder of the announcement:

END

China and India big recipients of Swiss gold exports. Russia’s big gold arbitrage scheme has a lot to do with this

(Reuters)

Swiss gold exports up in August due to higher shipments to India and China

Submitted by admin on Tue, 2023-09-19 16:16Section: Daily Dispatches

From Reuters

Tuesday, September 19, 2023

LONDON — Swiss gold exports rose by 7.3% in August from July as higher deliveries to India and China offset lower supplies to Turkey, customs data showed today.

Switzerland is the world’s biggest bullion refining and transit hub, while China and India are the largest consumer markets with local demand sensitive to high prices and time of the season.

Supplies to India, where jewellers usually make purchases for the October-November festival season, jumped by almost threefold to their highest since May, while shipments to China rose 1%, the data showed.

China’s physical gold premiums soared to a new high last week, amid strong demand to shore up a depreciating yuan and a lack of fresh import quotas. …

… For the remainder of the report:

end

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES//CHINA==LONDON GOLD ARBITRATION

-END-

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:NICKEL

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2966

OFFSHORE YUAN: DOWN TO 7.3032

SHANGHAI CLOSED DOWN 16.39 PTS OR 0.52%

HANG SENG CLOSED DOWN 111,57PTS OR 0.62%

2. Nikkei closed DOWN 218.81 PTS OR .66 %

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 104.68 EURO RISES TO 1.0703 UP 21 BASIS PT

3b Japan 10 YR bond yield: RISES TO. +.711 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.91/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN// OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.7190***/Italian 10 Yr bond yield UP to 4.495*** /SPAIN 10 YR BOND YIELD UP TO 3.776…**

3i Greek 10 year bond yield FALLS TO 4.065

3j Gold at $1933.25 silver at: 23.32 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 29 /100 roubles/dollar; ROUBLE AT 96.55//

3m oil into the 90 dollar handle for WTI and 93 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.91// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.711% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8972 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9602well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.348 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.418 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 5.075 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 27.04…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 14 BASIS PTS AT 4.2965

end

2.a Overnight: Newsquawk and Zero hedge:

USA EARLY MORNING REPORT

Futures Rise, Dollar And Yields Slide Ahead Of Fed Decision

WEDNESDAY, SEP 20, 2023 – 08:14 AM

US equity futures rose, alongside European markets, as traders awaited the Fed’s rate decision that will be scrutinized for the policy outlook and “dots” rather than the widely expected pause in hikes. As of 7:45am ET, contracts on the S&P 500 and the Nasdaq 100 both added about 0.2%, with spoos trading up to 4,500. Treasury yields fell across the board, taking their cue from sliding UK rates after inflation unexpectedly slowed and printed far below expectations (CPI core 6.2%, Exp. 6.8%, CPI MoM 0.3%, Exp. 0.7%). The Bloomberg Dollar Spot Index traded near the lows of the day, lifting most Group-of-10 currencies. Brent crude reversed earlier losses after it retreated from $95. Gold was little changed, while Bitcoin declined for the first time in three days.

In premarket trading, major technology and internet stocks were mostly higher. Instacart slipped as much as 5%, one day after surging following one of the year’s biggest US initial public offerings but closing at session lows. Intel shares pared an earlier decline as analysts said that the chipmaker showed some progress in its Innovation conference. However, there was disappointment that the event lacked a new customer announcement for the firm’s 18A semiconductor manufacturing process. Here are some other notable premarket movers:

- ARS Pharmaceuticals shares drop as much as 47% in US premarket trading, set for their biggest fall on record if the move holds, after the biotech said that the FDA has issued a letter requesting additional study for neffy — an epinephrine nasal spray to treat allergic reactions — in order to support drug approval, according to a statement.

- Pinterest shares rise 3.4%. Analysts were impressed by Tuesday’s investor day, saying that the social networking company was upbeat and that the long-term targets look achievable.

- Taysha Gene Therapies shares drop as much as 5.8%, after the biotech scrapped the development of its TSHA-120 gene therapy program to treat a rare neurodegenerative disorder following feedback from the FDA. Analysts cut their price targets on the stock, saying that while the update was disappointing, investors were focused on the company’s development of a treatment for Rett syndrome.

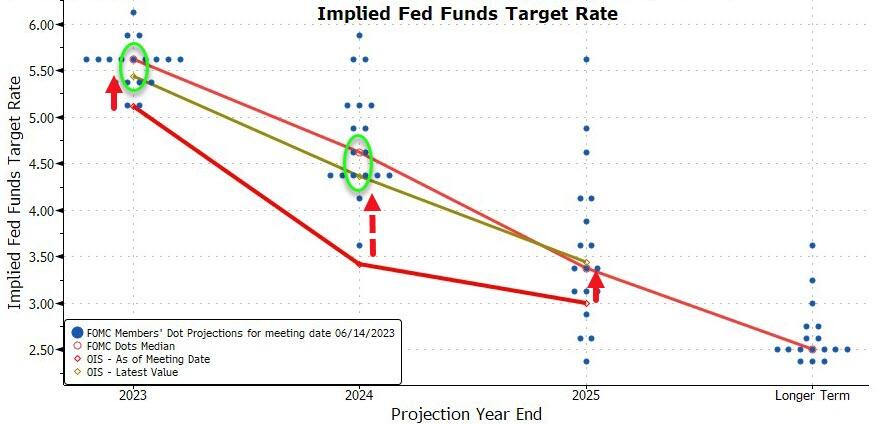

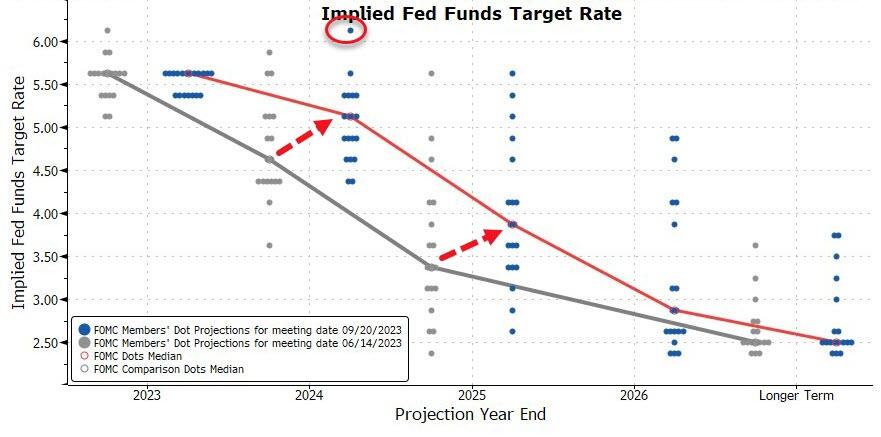

As previewed overnight, today all eyes will be on the Fed’s 2pm decision (and Powell’s presser) which is expected to hold for the second time this year following a slowing in inflation, while leaving the door open for another increase as early as November. Wall Street will be focused on whether Fed officials’ forecasts for interest rates, the so-called dot plot, show whether they seem determined to hike again.More here

“While rates should remain steady, a question mark remains over the longer-term outlook,” said Richard Flynn, UK Managing Director at Charles Schwab. “Now that inflation has peaked, we are likely to see the Fed shift to a more surgical approach. There continues to be a possibility of a hike later this year as central bankers target remaining sticky areas, but one more boost is unlikely to trouble the market.”

Britain’s CPI rose 6.7% from a year earlier in August, the slowest pace in 18 months, and less than the 7% expected by economists. The probability of a quarter-point rate increase by the BOE at its meeting on Thursday — almost guaranteed earlier this week — fell to less than 50%, according to swap pricing. Gilt yields tumbled, and US Treasury yields dipped in sympathy after rates on both the five- and 10-year notes hit the highest levels since 2007 on Tuesday.

In Europe, stocks rose and the pound weakened after British inflation slowed unexpectedly. The Stoxx 600 rose 0.6%, with retail and real estate leading gains. Sterling fell as much as 0.5% against the dollar to its lowest level since May as traders bet that the Bank of England is nearing the end of its hiking cycle. UK bonds soared. Here are Europe’s top movers

- Delivery Hero shares gain as much as 8.2% as Hauck & Aufhaeuser starts coverage of the food-delivery company with a buy rating, while two other analysts reiterated their bullish stance after the stock dropped to the lowest since May following first-half earnings last month.

- UK stocks outperform, with midcaps leading the charge, after data showed that inflation fell unexpectedly to the lowest level in 18 months, easing pressure for further interest-rate increases from the Bank of England.

- Ypsomed shares rise as much as 5.3% to a record high after the Swiss pharmaceutical company announced a long-term supply agreement with Novo Nordisk for large quantities of auto injectors. The pact has “very significant” earnings potential for Ypsomed, according to ZKB.

- M&G shares gain as much as 4.6% after the UK fund manager reports forecast-beating operating profits for the first half-year of 2023.

- Clariant shares rise as much as 3.6% after Jefferies raised the recommendation on the stock to buy from hold, saying the Swiss specialty chemical company’s increased urgency to resolve the performance of its Sunliquid biofuel unit is a “key positive.”

- Self Storage shares soar as much as 66% to NOK39.9, as T-C Storage HoldCo, an indirect subsidiary of Teachers Insurance and Annuity Association, agrees to launch a recommended voluntary cash tender offer for 100% of the company at NOK40 per share.

- Finsbury Food shares rise as much as 23% to 109.5p after Dbay agrees to buy the UK specialty bakery company in a deal valuing the company’s share capital at about £143.4 million.

- Baloise shares drop as much as 9.9% after the Swiss insurer’s profit figures came in somewhat below expectations, according to analysts, and Vontobel says higher claims in non-life will hit earnings in 2H.

- Talanx shares fall as much as 7.6% after an offering of 4.88m shares by the German reinsurance company priced at €61.50 apiece, representing about a 6.5% discount to Tuesday’s close.

- Air Liquide shares decline as much as 3.4% after Stifel cites comments from CEO, CFO in a London sell-side meeting late Tuesday, saying trading might be more difficult in second half than 1H, especially in Electronics and Industrial Merchant units.

Earlier in the session, Asian stocks fell for a third day as caution prevailed ahead of the Federal Reserve’s policy decision, with surging oil prices driving inflation and raising the possibility of higher-for-longer interest rates. The MSCI Asia Pacific Index dropped as much as 0.6% on Wednesday, led by health-care and energy shares. Japanese and Australian stocks slipped. Brent held close to $94 per barrel, setting the stage for another interest-rate hike by the Fed this year.

- Chinese equities dipped after the nation’s lenders kept their benchmark lending rates unchanged, following the central bank’s move last week to hold policy rates steady as officials assess the economic impact of existing stimulus. The CSI 300 Index is edging closer to the lowest level this year.

- Japan’s Nikkei 225 gradually weakened after the latest trade data showed Japanese exports and imports remained in contraction territory, albeit not as bad as feared.

- Indian stocks declined the most in two months and were the worst performers in the region led by a selloff in index majors including HDFC Bank and Reliance Industries. The S&P BSE Sensex fell 1.2% to 66,800.88 on Wednesday, while the NSE Nifty 50 Index declined by the same magnitude. The MSCI Asia Pacific Index was down 0.7%. HDFC Bank contributed the most to the Sensex’s decline, decreasing 4%, following a downgrade by Nomura on rising concerns over private sector lender’s margins post merger with parent HDFC. All but one sectoral index on the BSE closed with losses amid a broad selloff in the market as traders exercised caution ahead of Federal Reserve’s rate-setting meeting. Out of 30 shares in the Sensex index, seven rose and 23 fell.

- Australia’s ASX 200 was dragged lower by the commodity-related sectors including energy after oil prices eased back from YTD highs although losses were cushioned by resilience in consumer stocks.

In FX, the Bloomberg Dollar Spot Index is flat ahead of the Fed decision later on Wednesday. the yen touched the psychological level of 148 per dollar, the lowest in more than 10 months. The pound traded as much as 0.5% lower to $1.2334 after UK inflation report; money markets price a 52% chance of a quarter-point hike on Thursday, compared with about 90% yesterday.

In commodities, crude futures decline, with WTI falling 1.4% to trade near $89.90. Spot gold drops 0.1%. Goldman analysts raised their forecast for crude back to triple digits as worldwide demand hits unprecedented levels and OPEC+ supply curbs continue to tighten the market. The Wall Street bank pushed up its 12-month forecast for Brent to $100 a barrel from $93. However, most of the rally “is behind us,” the bank said in a note.

Bitcoin is under modest pressure but resides in particularly narrow parameters and is yet to meaningfully deviate away from the USD 27k handle pre-FOMC.

In rates, treasuries were underpinned by gilts, with futures paring portion of Tuesday’s losses led by belly of the curve. US yields are lower by as much as 3bp in belly of the curve with 5s30s steeper and 2s5s30s fly richer by ~2bp on the day; 10-year yields near 4.34% trail gilts by ~7bp in the sector. UK 2s richer by 14.5bp on the day, lowest yield since July. FOMC expected to keep rates unchanged at the 2pm announcement; the dot-plot update is expected to indicate another hike before year-end in a close call. Gilts outperform in an aggressive bull-steepening move after an unexpected drop in UK inflation opened the door for Bank of England to pause rate hikes in Thursday’s decision. US session includes Fed rate decision at 2pm New York time, released with latest staff projections.

Looking to the day ahead now, and the main highlight will be the Fed’s latest policy decision and Chair Powell’s press conference. Other central bank speakers include the ECB’s Elderson. Data releases include the UK CPI and German PPI for August. Lastly, today’s earnings releases include FedEx.

Market snapshot

- S&P 500 futures up 0.1% to 4,496.25

- STOXX Europe 600 up 0.6% to 459.08

- MXAP down 0.8% to 161.48

- MXAPJ down 0.6% to 500.28

- Nikkei down 0.7% to 33,023.78

- Topix down 1.0% to 2,406.00

- Hang Seng Index down 0.6% to 17,885.60

- Shanghai Composite down 0.5% to 3,108.57

- Sensex down 1.2% to 66,775.50

- Australia S&P/ASX 200 down 0.5% to 7,163.33

- Kospi little changed at 2,559.74

- Brent Futures down 1.2% to $93.21/bbl

- Gold spot down 0.1% to $1,929.80

- U.S. Dollar Index little changed at 105.09

- German 10Y yield little changed at 2.74%

- Euro up 0.1% to $1.0695

Top Overnight News from Bloomberg

- The PBOC said it has sufficient policy space to support the Chinese economy, adding to expectations there may be more easing to come, including rate cuts, after this month’s pause. The comments came shortly after Chinese banks left their benchmark loan rates unchanged. BBG

- The European Union is “very far” from imposing new tariffs on Chinese electric cars, a top official told CNBC, just days after the bloc launched an investigation into subsidies given by Beijing. CNBC

- UK inflation undershoots the Street by a wide margin, w/headline coming in at +6.7% (down from +6.8% in Jul and below the Street’s +7% forecast) and core at +6.2% (down from +6.9% in Jul and below the Street’s +6.8% forecast). BBG

- The UAW weighed an expansion of its strikes against Detroit’s automakers on, after union President Shawn Fain said more plants faced walkouts if carmakers didn’t sweeten their offers. The union will have a Facebook Live event today at 10 a.m. local time in Detroit, where it will likely discuss whether more plants will join the strike. BBG

- The United States is discussing terms of a mutual defense treaty with Saudi Arabia that would resemble military pacts with Japan and South Korea, according to American officials. The move is at the center of President Biden’s high-stakes diplomacy to get the kingdom to normalize relations with Israel. NYT

- Republicans are working on Plan Bs to avoid to a shutdown after days of chaos (some of those Plan Bs involve asking Democrats for help), but time is of the essence and there is still enormous division within the caucus. The Hill

- At today’s meeting Fed officials are likely to make fairly straightforward revisions to their economic projections. For 2023, we expect a substantial upward revision to GDP growth (+1.1pp to +2.1%) and moderate downward revisions to the unemployment rate (-0.2pp to 3.9%) and core inflation (-0.4pp to 3.5%). For November, we think that further labor market rebalancing, better news on inflation, and the likely upcoming Q4 growth pothole will convince more participants that the FOMC can forgo a final hike this year, as we think it ultimately will. On neutral, we expect the median longer run rate dot to finally rise a bit to 2.75%. GIR

- Pimco warned markets may be underestimating the risks of both one more Fed hike and a US recession, making haven assets a preferred play. Money manager Geraldine Sundstrom recommends sticking to assets that offer a pickup in yields, including US agency mortgages and some financial credits. BBG

- US stockpiles fell by 5.25 million barrels last week, the API is said to have reported. That would bring holdings to the lowest in more than nine months if confirmed by the EIA today. Inventories at Cushing also slid. BBG

- We have nudged up our 12-month ahead Brent forecast from $93/bbl to $100/bbl as we now expect modestly sharper inventory draws. The key reason is that significantly lower OPEC supply and higher demand more than offset significantly higher US supply. Overall, we believe that OPEC will be able to sustain Brent in an $80-$105 range in 2024 by leveraging robust Asia-centric global demand growth (1.8mb/d) and by exercising its pricing power assertively. GIR

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly lower with risk appetite dampened ahead of the incoming deluge of central bank policy announcements including the latest FOMC rate decision and dot plot projections. ASX 200 was dragged lower by the commodity-related sectors including energy after oil prices eased back from YTD highs although losses were cushioned by resilience in consumer stocks. Nikkei 225 gradually weakened after the latest trade data showed Japanese exports and imports remained in contraction territory, albeit not as bad as feared. Hang Seng and Shanghai Comp conformed to the subdued mood after the PBoC unsurprisingly maintained its benchmark 1-year and 5-year Loan Prime Rates at 3.45% and 4.20%, respectively, while Country Garden’s dollar bondholders have been left in the dark regarding a coupon payment which was due on Monday although the developer still has a 30-day grace period.

Top Asian News

- Chinese Loan Prime Rate 1Y (Sep) 3.45% vs. Exp. 3.45% (Prev. 3.45%); 5Y (Sep) 4.20% vs. Exp. 4.20% (Prev. 4.20%)

- PBoC official said China’s monetary policy still has ample policy room to respond to unexpected challenges and changes, while they will continue to implement prudent monetary policy and step up counter-cyclical adjustments. Furthermore, the PBoC will keep liquidity reasonably ample and enhance the stability of credit growth, according to Reuters.

- NDRC Vice Chairman Cong Liang said China’s macroeconomic policies have been effective and that China’s economy faces a lot of difficulties and challenges, while he added that economic positives are increasing and those shorting China will surely be proven wrong.

- US State Department said Climate Envoy Kerry met with Chinese Vice President Han and emphasised the need for China to raise ambition in efforts to accelerate decarbonisation and reduce emissions of methane, according to Reuters.

- China exported zero germanium and gallium products in August which are materials key to the semiconductor industry, according to customs data.

European bourses are in the green, Euro Stoxx 50 +0.5%, with the FTSE 100 +0.7% outperforming after sub-forecast inflation data and associated GBP softness. Sectors are primarily firmer, Real Estate and Banking names are outperforming on the UK data while Energy and Basic Resources lag with benchmarks mixed/softer. Stateside, futures are essentially flat across the board ahead of the FOMC, ES +0.1%, NQ +0.1%;

Top European News

- ECB’s Schnabel says new supply-side shocks may pose upside risks to inflation; Dynamics in wage growth remain strong, while labour shortages persist; Energy shock threatens to leave permanent scars in the euro area. via a slide release

- The Times’ Shadow MPC voted 7-2 in favour of a 25bps hike to the Bank Rate to “ensure inflation is finally under control”.

- Swedish Finance Ministry says new spending in the 2024 budget totals SEK 39bln (exp. ~40bln); prioritising fighting inflation and supporting households/welfare.

- Swiss Government Forecasts (SECO): downgrades 2023 CPI (2.2%), upgrades 2024 CPI (1.9%); upgrades 2023 GDP, downgrades 2024 GDP; says global economy likely to take longer to recover from challenges assumed in the June forecast. Click here for more detail.

- UK PM Sunak has reportedly summoned his cabinet, according to Sun reporter Cole; “Looks like we may be hearing the new Net Zero plan today”.

FX

- Sterling undermined by softer than forecast UK CPI metrics pre-BoE as casts doubt over 25 bp rate hike, Cable retreats from 1.2397 to 1.2335 before recovering.

- Yen finally relents in battle to say above 148.00 vs. Dollar regardless of verbal intervention from a top Japanese FX diplomat.

- DXY regroups, but remains cautious within the 105.00-260 range awaiting Fed guidance.

- Euro retains sight of 1.0700 against Greenback and is flanked by option expiries.

- Loonie loses post-Canadian inflation data thrust as crude prices retreat, Usd/Cad straddles 1.3450 ahead of BoC minutes and conscious of 1.1 bn expiry interest nearby.

- PBoC set USD/CNY mid-point at 7.1732 vs exp. 7.2926 (prev. 7.1733)

- PBoC official Zou said the global FX market has seen great volatility this year and said more attention will be paid to changes in the yuan exchange rate against a basket of currencies. Zou added there is a solid foundation to keep the yuan exchange rate basically stable and said they will resolutely correct one-sided pro-cyclical behaviour for the yuan exchange rate, while they will resolutely curb disruptions to market order and guard against exchange rate overshooting risks.

- US Treasury Secretary Yellen said the Treasury generally understands the need to smooth out volatility in exchange rates but not to influence forex levels, while she added that the view on any Japanese yen intervention would depend on the circumstances, according to Reuters.

- Japan’s top FX diplomat Kanda says excessive yen moves are not desirable and watching FX with a high level of urgency, while they will take appropriate steps on FX as needed and are closely communicating with US and overseas FX

Fixed Income

- Gilts front-run debt recovery before Central Bank cavalry arrives as softer than consensus UK inflation data calls 25 bp BoE hike into question.

- 10-year bond extends to 96.49 from 95.99, Bunds and T-note tag along within 127.74-30 and 109-10/03+ respective ranges awaiting FOMC.

Commodities

- Crude benchmarks pressured after seven consecutive sessions of upside and ahead of multiple days of broader macro risk events, with pressure potentially also emanating from the downbeat APAC tone.

- Dutch TTF has trimmed initial upside and has reverted back to the sub-37.50/MWh trough, as participants continue to focus on Australian updates. Most recently, downside came alongside Offshore saying negotiations resulted in some concession on both sides.

- Spot gold is flat with numerous technicals in close proximity, Palladium outperforms potentially on EU auto registration numbers while base peers have managed to lift off of initial lows.

- US Energy Inventory Data (bbls): Crude -5.3mln (exp. -2.2mln), Gasoline +0.7mln (exp. +0.3mln), Distillate -0.3mln (exp. +0.2mln), Cushing -2.6mln.

- Goldman Sachs raises its 12-month ahead Brent forecast to USD 100/bbl (prev. USD 93/bbl), expects modestly sharper inventory draws. Click here for more detail.

- Chevron (CVX) says no agreement has been reached with unions following further consultation sessions held this week with the Fair Work Commission. Ongoing lack of agreement reinforces the view that there is “no reasonable prospect of an agreement between the parties”. Engaged in meaningful negotiations to finalise enterprise agreements with market competitive remuneration and conditions. However, unions continue to ask for terms significantly higher than the market.

- Australia’s Offshore Alliance says negotiations before the commissioner were useful and resulted in some concessions on both sides; adds that members remain open to compromise but Chevron must table a viable offer.

- China’s state planner NDRC to increase retail prices of gasoline and diesel by CNY 385/t and CNY 370/t respectively from September 21st.

Geopolitics

- Gulf Cooperation Council Countries and the US called for the completion of the demarcation of Kuwaiti-Iraqi maritime borders and urged Iraq to settle its internal legal status to ensure regulation of maritime in the Khor Abdallah Waterway, while they also urged Iran to fully cooperate with the IAEA, according to a joint statement.

- Iranian President Raisi said Washington should prove its goodwill and determination for the revival of the 2015 nuclear pact, while he reportedly demanded that the US end its sanctions on Iran.

- US military official says the joint military exercises with Armenia will begin today on time.

- Ceasefire has reportedly been announced in Karabakh, according to Sputnik Armenia and Ifax; Karabakh Armenians to meet with Azeri authorities on September 21st, Ifax reports; Armenian Deputy Foreign Minister says Yerevan could theoretically live under Azerbaijan but dialogue is crucial.

- Russia’s Kremlin says Russian President Putin is to meet China’s top diplomat Wang Yi.

US Event Calendar

- 07:00: Sept. MBA Mortgage Applications, prior -0.8%

- 14:00: Sept. Interest on Reserve Balances R, est. 5.40%, prior 5.40%

- 14:00: Sept. FOMC Rate Decision (Lower Boun, est. 5.25%, prior 5.25%

- 14:00: Sept. FOMC Rate Decision (Upper Boun, est. 5.50%, prior 5.50%

DB’s Jim Reid concludes the overnight wrap

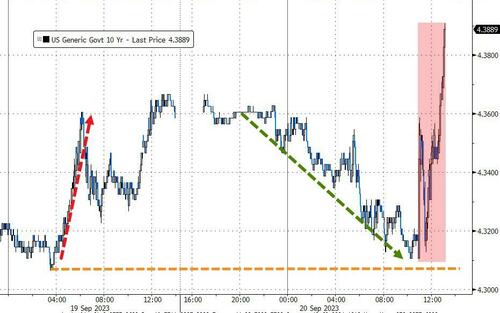

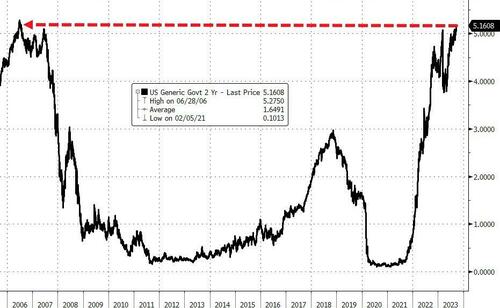

The long-term study shows how this has been the worst start to a decade for US Treasuries since our data begins in 1800 and yesterday incrementally added to this as 10yr US yields hit 15-plus year highs, with 2yrs at 16-year highs, just as we approach an important trio of central bank meetings. That starts with the Federal Reserve tonight, before we hear from the Bank of England tomorrow, and then the Bank of Japan on Friday morning. But despite all the recent speculation that central banks are near the end of their tightening cycles, the backdrop this week has been a much more hawkish one. For instance, oil prices hit new 10-month highs intra-day though they were marginally lower on the day by the close. We also had an upside surprise from Canada’s CPI, which added to the sense that rate cuts weren’t coming anytime soon.

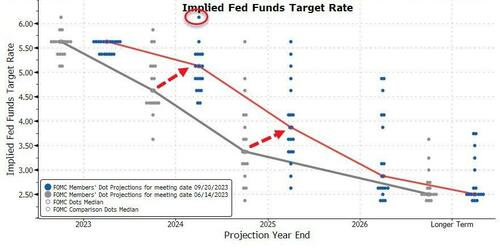

Of course, the main focus today will be on the Federal Reserve’s decision tonight, along with Chair Powell’s subsequent press conference. In terms of the actual decision, they’re widely expected to leave rates unchanged, so the bigger focus is likely to be on their latest Summary of Economic Projections, which includes the dot plot for where officials see rates over the years ahead. At the last quarterly release in June, the dot plot pointed to two further rate hikes by year-end, and we got one of them at the most recent meeting in July. Our US economists still expect the Fed to signal one further hike this year, but they think Powell will leave open the question of when that tightening could occur, and will lean heavily on a message of data dependency. And even though they expect the Fed’s forecasts to show softer inflation, they think that stronger growth and lower unemployment should counterbalance that, meaning that the 2024 dot will show one less rate cut in 2024 as well. See their full preview here.

We’ll see where things stand after the Fed’s decision, but a key story for much of yesterday was the continued rise in oil prices. Brent Crude almost reached $96/bl yesterday morning but it retreated to close a touch below Monday’s 10-month high (-0.10% to $94.34/bbl) and this morning is trading at $93.23/bbl as we go to print. So a big correction in the last 15 hours from the peaks.

Elsewhere on the energy front, we saw a sizeable spike in European natural gas prices. One month TTF gas futures were up +9.84% to EUR 37.4/MWh, their highest level in three weeks, amid delays to production at Norwegian gas fields.

In other inflationary news, we had another upside inflation surprise out of Canada, as CPI hit +4.0% in August (vs. +3.8% expected). That led investors to price in a much higher likelihood that the Bank of Canada would hike rates next month, with the likelihood up from 25% on Monday to 51% after the close yesterday. In turn, Canadian sovereign bonds significantly underperformed, with the 10yr yield up +11.4bps yesterday to a new post-2008 high.

Those inflationary developments led investors to price in higher rates for longer. Indeed, the rate priced in for the Fed’s December 2024 meeting hit a new high for the cycle at 4.63%. That means less than three 25bp cuts are now priced in by end-2024. That helped boost yields across the curve, with the 2yr Treasury yield (+3.7bps) closing at a new high for this cycle at 5.09%, and the 10yr yield (+5.6bps) also closed at a new cycle high of 4.36%. It was much the same story in Europe, where yields on 10yr bunds (+3.0bps) and BTPs (+0.7bps) hit a 6-month high, whilst yields on 10yr French OATs (+2.8bps) closed at their highest since 2012. The only exception to this pattern were yields on 10yr gilts (-4.9bps), which fell ahead of this morning’s CPI report for August. That’ll be released shortly after we go to press, and will be the last big data release ahead of the Bank of England’s decision tomorrow. Headline is expected to pick up two tenths to 7% YoY with core down a tenth to 6.8% YoY.

The prospect of higher rates provided a tough backdrop for equities, though the S&P 500 crept back up in the last few hours of trading from being down -0.8% at the early session lows to close ‘only’ -0.22% lower, albeit to a 3-week low. The moderate decline was a broad-based one, with 8 of 10 S&P 500 sector groups down on the day. The other major US indices saw similar declines, including the Dow Jones (-0.31%) and the NASDAQ (-0.23%), whilst the small-cap Russell 2000 (-0.42%) fell to its lowest level since late-June. In Europe the picture was a bit more positive, but the STOXX 600 still fell -0.04%.

In Asia, the Nikkei (-0.36%), Hang Seng (-0.58%), CSI (-0.31%), Shanghai Composite (-0.34%) and the KOSPI (-0.05%) are all slightly lower alongside S&P 500 (-0.11%) and NASDAQ 100 (-0.16%) futures.

Early morning data showed that Japan’s exports dropped -0.8% y/y in August (v/s -2.1% expected) and against a -0.3% in July, making it the second month of declines (even if better than expected) mainly due to weak exports to China (-11.0% y/y). Meanwhile, imports weakened -17.8% y/y in August less than the expected fall of -20.0% as against a revised decline of -13.6%.

In FX, the Japanese yen pared its initial gains against the dollar to trade at 147.81 (+0.03%) after US Treasury Secretary Janet Yellen stated that the US would show understanding over Japan’s intervention to support its currency if the measures are aimed at smoothing out undue volatility. You’re unlikely to see anything ahead of the FOMC and BoJ (Friday) but this maybe makes intervention a bit easier going forward. Elsewhere, the People’s Bank of China (PBOC) left its 1-yr and 5-yr loan prime rates unchanged at 3.45% and 4.2%, respectively.

When it came to yesterday’s other data, US housing starts fell significantly more than expected in August, with an annualised rate of 1.283m (vs. 1.439m expected). That’s their lowest level since May 2020, when the economy was still affected by the initial wave of Covid-19. However, building permits moved up to an annualised 1.543m (vs. 1.440m expected), which is their highest level since October. Permits tend to be the more reliable data point so the uncertainty around housing continues after Monday’s poor NAHB. Separately in the Euro Area, the final August CPI reading was revised down to +5.2%, compared with the initial flash reading at +5.3%.

To the day ahead now, and the main highlight will be the Fed’s latest policy decision and Chair Powell’s press conference. Other central bank speakers include the ECB’s Elderson. Data releases include the UK CPI and German PPI for August. Lastly, today’s earnings releases include FedEx.

END

2 B) NOW NEWSQUAWK (EUROPE/REPORT)

Odds of a BoE hike /PAUSE to 50/50 post-CPI, FOMC looms – Newsquawk US Market Open

WEDNESDAY, SEP 20, 2023 – 06:23 AM

- FTSE 100 outperforms after sub-forecast UK inflation data, Real Estate and Banking leading

- Stateside, futures are essentially flat pre-FOMC

- GBP undermined as market pricing pivots to 50/50 for pause/hike by the BoE, DXY at 105.00, USD/JPY over 148.00

- EGBs & USTs rise on significant Gilt upside, US yields lower with the short-end leading

- Crude benchmarks pressured after seven sessions of upside, XAU flat while Palladium outperforms

- Looking ahead, highlights include US MBAs, FOMC & Fed Chair Powell’s Press Conference, BCB Policy Announcement, BoC Minutes, ECB’s Elderson.

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EQUITIES

- European bourses are in the green, Euro Stoxx 50 +0.5%, with the FTSE 100 +0.7% outperforming after sub-forecast inflation data and associated GBP softness.

- Sectors are primarily firmer, Real Estate and Banking names are outperforming on the UK data while Energy and Basic Resources lag with benchmarks mixed/softer.

- Stateside, futures are essentially flat across the board ahead of the FOMC, ES +0.1%, NQ +0.1%; Newsquawk preview available here.

- Click here for more detail.

FX

- Sterling undermined by softer than forecast UK CPI metrics pre-BoE as casts doubt over 25 bp rate hike, Cable retreats from 1.2397 to 1.2335 before recovering.

- Yen finally relents in battle to say above 148.00 vs. Dollar regardless of verbal intervention from a top Japanese FX diplomat.

- DXY regroups, but remains cautious within the 105.00-260 range awaiting Fed guidance.

- Euro retains sight of 1.0700 against Greenback and is flanked by option expiries.

- Loonie loses post-Canadian inflation data thrust as crude prices retreat, Usd/Cad straddles 1.3450 ahead of BoC minutes and conscious of 1.1 bn expiry interest nearby.

- PBoC set USD/CNY mid-point at 7.1732 vs exp. 7.2926 (prev. 7.1733)

- PBoC official Zou said the global FX market has seen great volatility this year and said more attention will be paid to changes in the yuan exchange rate against a basket of currencies. Zou added there is a solid foundation to keep the yuan exchange rate basically stable and said they will resolutely correct one-sided pro-cyclical behaviour for the yuan exchange rate, while they will resolutely curb disruptions to market order and guard against exchange rate overshooting risks.

- US Treasury Secretary Yellen said the Treasury generally understands the need to smooth out volatility in exchange rates but not to influence forex levels, while she added that the view on any Japanese yen intervention would depend on the circumstances, according to Reuters.

- Japan’s top FX diplomat Kanda says excessive yen moves are not desirable and watching FX with a high level of urgency, while they will take appropriate steps on FX as needed and are closely communicating with US and overseas FX

- Click here for more detail.

- Click here for the Option Expires for the NY Cut.

FIXED INCOME

- Gilts front-run debt recovery before Central Bank cavalry arrives as softer than consensus UK inflation data calls 25 bp BoE hike into question.