GOLD PRICE CLOSED: DOWN $25.60 TO $1920.00

SILVER PRICE CLOSED: DOWN $0.13 AT $23.42

Access prices: closes 4: 15 PM

Gold ACCESS CLOSE 1920.00

Silver ACCESS CLOSE: 23.39

Shanghai Gold Benchmark Price

USD oz  AM2001.82

AM2001.82

PM2006.49

Historical SGE Fi

NEW YORK PRICE AT THE SAME TIME: $1932.60

premium $73.90

xxxxxxxxxxxxxxxxxx

Bitcoin morning price:, $26,768 DOWN 159 Dollars

Bitcoin: afternoon price: $26,602 DOWN 325 dollars

Platinum price closing $924.70 DOWN $12.65

Palladium price; $1269.00 DOWN $14.00

END

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros/4: 15 PM ACCESS

CANADIAN GOLD: $2,588.87 DOWN 11.,46 CDN dollars per oz (ALL TIME HIGH 2,775.35)

BRITISH GOLD: 1561,74 DOWN 3.42 pounds per oz//(ALL TIME HIGH//CLOSING///1630.29)

EURO GOLD: 1800.82 DOWN 10.82 euros per oz //(ALL TIME HIGH/CLOSING//1861.21)//

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2023 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,945.600000000 USD

INTENT DATE: 09/20/2023 DELIVERY DATE: 09/22/2023

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 10

323 H HSBC 15

435 H SCOTIA CAPITAL 22

624 H BOFA SECURITIES 25

657 C MORGAN STANLEY 6

661 C JP MORGAN 100 7

686 C STONEX FINANCIA 1

690 C ABN AMRO 1

732 C RBC CAP MARKETS 1

737 C ADVANTAGE 1 13

TOTAL: 101 101

MONTH TO DATE: 3,96

JPMorgan stopped 7/101 contracts.

FOR SEPT.:

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2023. CONTRACT: 101 NOTICES FOR 10,100 OZ or 0.3141 TONNES

total notices so far: 3968 contracts for 396,800 oz (12.342 tonnes)

FOR SEPT:

SILVER NOTICES: 1 NOTICE(S) FILED FOR 5,000 OZ/

total number of notices filed so far this month : 2618 for 13,090,000 oz

XXXXXXXXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD

WITH GOLD DOWN $25.60

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: / SMALL CHANGES/A WITHDRAWAL OF 0.58 TONNES OF GOLD FROM THE GLD/

INVENTORY RESTS AT 878.25 TONNES

Silver//

WITH NO SILVER AROUND AND SILVER DOWN 13 CENTS AT THE SLV// HUGE CHANGES IN SILVER INVENTORY AT THE SLV:HUGE CHANGES : A WITHDRAWAL OF 1.1 MILLION OZ OF SILVER FROM THE SLV/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 449.033 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A GOOD SIZED 486 CONTRACTS TO 125,263 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS TINY SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR $0.35 GAIN IN SILVER PRICING AT THE COMEX ON WEDNESDAY. TAS ISSUANCE WAS A FAIR SIZED 491 CONTRACTS. THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 491 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.35). AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A STRONG GAIN OF 590 OI CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

A STRONG ISSUANCE OF EXCHANGE FOR PHYSICALS( 609 CONTRACTS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 14.420 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S ZERO QUEUE JUMP OF NIL OZ//NEW TOTAL 13.410 MILLION OZ + OUR CRIMINAL ISSUANCE OF 0 EXCHANGE FOR RISK CONTRACTS//NEW TOTALS EXCHANGE FOR RISK: 3.0 MILLION OZ: NEW TOTALS SILVER STANDING: 16.410 MILLION OZ// /// / //FAIR SIZED COMEX OI GAIN/ GOOD SIZED EFP ISSUANCE/VI) FAIR SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 491 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -467 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT:

TOTAL CONTRACTS for 14 days, total 10,395 contracts: OR 51.945 MILLION OZ (742 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 48.900 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 51.945 MILLION OZ (SMALLER THIS MONTH)

RESULT: WE HAD A GOOD SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 486 CONTRACTS DESPITE OUR GAIN IN PRICE OF $0.35 IN SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG EFP ISSUANCE CONTRACTS: 609 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS./ WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR SEPT OF 14.2 MILLION OZ FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP .+ 0 MILLION OZ EXCHANGE FOR RISK//PRIOR TOTAL FOR EXCHANGE FOR RISK = 3.0 MILLION OZ/TOTAL EXCH. FOR RISK /NEW TOTALS STANDING 16.410 MILLION OZ// /// WE HAVE A SMALL SIZED GAIN OF 123 OI CONTRACTS ON THE TWO EXCHANGES. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A FAIR SIZED 491 CONTRACTS//ZERO FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION. THE NEW TAS ISSUANCE WEDNESDAY NIGHT (491) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE., .

WE HAD 1 NOTICE(S) FILED TODAY FOR 5,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A VERY STRONG SIZED 7783 CONTRACTS TO 445,861 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,541 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED: –2159 CONTRACTS

WE HAD A VERY STRONG SIZED INCREASE IN COMEX OI ( 7783 CONTRACTS) WITH OUR STRONG $13.00 GAIN IN PRICE//WEDNESDAY. WE ALSO HAD A RATHER STRONG INITIAL STANDING IN GOLD TONNAGE FOR SEPT. AT 12.656 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 10,000 OZ QUEUE JUMP //NEW TOTAL STANDING 14.8211 TONNES + /A FAIR (AND CRIMINAL) ISSUANCE OF 1237 T.A.S. CONTRACTS /// ALL OF..THIS HAPPENED WITH OUR $13.00 GAIN IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING.WE HAD A GIGANTIC SIZED GAIN OF 13,963 OI CONTRACTS (43.43 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6180 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 445,861

IN ESSENCE WE HAVE A GIGANTIC SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 13,963 CONTRACTS WITH 9942 CONTRACTS INCREASED AT THE COMEX// AND A STRONG SIZED 6180 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 13,963 CONTRACTS OR 43.43 TONNES. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 1237 CONTRACTS)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (6180 CONTRACTS) ACCOMPANYING THE VERY STRONG SIZED GAIN IN COMEX OI (7783) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 13,963 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR NORMAL FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) FAIR INITIAL STANDING AT THE GOLD COMEX FOR SEPT. AT 12.656 TONNES FOLLOWED BY TODAY’S QUEUE JUMP TO LONDON OF 10,000 OZ/// 3) ZERO LONG LIQUIDATION WITH ZERO TAS LIQUIDATION C DURING THE COMEX SESSION //4) VERY STRONG SIZED COMEX OPEN INTEREST GAIN/ 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 1237 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023 INCLUDING TODAY

SEPT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT :

TOTAL EFP CONTRACTS ISSUED: 37,387 CONTRACTS OR 3,738,700 OZ OR 116.28 TONNES IN 14 TRADING DAY(S) AND THUS AVERAGING: 2670 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 14 TRADING DAY(S) IN TONNES 116.28 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 116.28/3550 x 100% TONNES 3.26% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 116.28 TONNES (SMALLER THAN LAST MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF MAY HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF JUNE., FOR BOTH GOLD:

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (SEPT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A GOOD SIZED 486 CONTRACTS OI TO 125,263 AND FURTHER FROM OUR COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A STRONG 609 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 609 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 609 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 486 CONTRACTS AND ADD TO THE 609 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A SMALL SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 123 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 0.615 MILLION OZ

OCCURRED DESPITE OUR $0.35 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING//WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 23.87 PTS OR 0.77% //Hang Seng CLOSED DOWN 230.19 PTS OR 1.29%/ /The Nikkei CLOSED DOWN 452.75 PTS OR 1.37% //Australia’s all ordinaries CLOSED DOWN 1.30 % /Chinese yuan (ONSHORE) closed DOWN AT 7.3056 /OFFSHORE CHINESE YUAN DOWN TO 7.3132 /Oil DOWN TO 89.26 dollars per barrel for WTI and BRENT UP AT 92.98 / Stocks in Europe OPENED ALL RED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

a)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 7783 CONTRACTS TO 445,861 WITH OUR STRONG GAIN IN PRICE OF $13.00 ON WEDNESDAY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF SEPT.… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 6180 EFP CONTRACTS WERE ISSUED: : DEC 6180 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 6180 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GIGANTIC SIZED TOTAL OF 13,963 CONTRACTS IN THAT 6180 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A STRONG SIZED GAIN OF 7783 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR STRONG ADVANCE IN PRICE OF $13.00//WEDNESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT WAS A FAIR 1237 CONTRACTS. THROUGHOUT THE PAST WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR SPREAD WHICH WILL BE LIQUIDATED TWO MONTHS HENCE)//

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: SEPT (14.8211) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 12 MONTHS OF 2021-2022:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 14.8211 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $13.00) //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A GIGANTIC GAIN OF 16,122 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD A ZERO T.A.S. LIQUIDATION ON THE FRONT END OF WEDNESDAY’S TRADING. THE T.A.S. ISSUED ON WEDNESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 43.43 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPT. (12.656 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 10,000 OZ//NEW STANDING 14.8211 TONNES // ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $13.00.

WE HAD – REMOVED 2159 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST

NET GAIN ON THE TWO EXCHANGES 13,963 CONTRACTS OR 1,396,300 OZ OR 43.43 TONNES.

Estimated gold volume today:// 220,970 fair

final gold volumes/yesterday 233,663 fair

//speculators have left the gold arena

//SEPT 21/ /// THE SEPT. 2023 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | nil OZ . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | NIL |

| No of oz served (contracts) today | 101 notice(s) 10,100 OZ 0.3141 TONNES |

| No of oz to be served (notices) | 797 contracts 79700 oz 2.479 TONNES |

| Total monthly oz gold served (contracts) so far this month | 3968 notices 396,800 OZ 12.342 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposit:

total dealer deposits: NIL oz

customer deposits: 0

total customer deposits: NIL oz

we had 0 customer withdrawals

total withdrawals nil oz

Adjustments; 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPTEMBER.

For the front month of SEPTEMBER we have an oi of 898 contracts having GAINED 97 contracts. We had

3 contracts were served on WEDNESDAY, so we GAINED an additional 100 CONTRACTS or AN ADDITIONAL 10,000 oz will stand for delivery in this non active delivery month of Sept

Oct LOST 770 contracts to 22,215 contracts.

NOV GAINED 238 CONTRACTS to stand at 336

December GAINED 7387 contracts UP to 382,406 contracts.

We had 101 contracts filed for today representing 10,100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 100 notices were issued from their client or customer account. The total of all issuance by all participants equate to 101 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 7 notice(s) was (were) stopped received by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the SEPT /2023. contract month,

we take the total number of notices filed so far for the month (3968 x 100 oz ), to which we add the difference between the open interest for the front month of SEPT (898 CONTRACTS) minus the number of notices served upon today 101 x 100 oz per contract equals 476,500 OZ OR 14.8211 TONNES the number of TONNES standing in this non active month of SEPT.

thus the INITIAL standings for gold for the SEPT contract month: No of notices filed so far (3968) x 100 oz + (898) {OI for the front month} minus the number of notices served upon today (101) x 100 oz) which equals 476,500 oz standing OR 14.8211 TONNES

TOTAL COMEX GOLD STANDING: 14.8211 TONNES WHICH IS HUGE FOR AN INACTIVE DELIVERY MONTH.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,016,871.449 OZ 62.733 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED: 20,931,908.140 OZ

TOTAL REGISTERED GOLD 10,801,765.332 (335,98 tonnes)..

TOTAL OF ALL ELIGIBLE GOLD: 10,130,142.808 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 8,784,894 OZ (REG GOLD- PLEDGED GOLD) 273.24 tonnes//dropping like a stone

END

SILVER/COMEX

SEPT 21

//2023// THE SEPT 2023 SILVER CONTRACT

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,542,376.127 oz Brinks CNT Delaware JPMorgan . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 1 CONTRACT(S) (5,000 OZ) |

| No of oz to be served (notices) | 64 contracts (320,000 oz) |

| Total monthly oz silver served (contracts) | 2618 Contracts (13,090,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: 0

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0 deposit customer account:

total customer deposit nil oz

JPMorgan has a total silver weight: 136.312 million oz/272.537 million or 50.01%

Comex withdrawals 4

i) Out of Brinks 530,071.900 oz

ii) Out of CNT 420,438.600 oz

iii) Out of Delaware: 2954.875 oz

iv) Out of JPMorgan 588,910.752 oz

total: 1,542,376.127 oz

adjustments: 0

TOTAL REGISTERED SILVER: 42.062 MILLION OZ//.TOTAL REG + ELIGIBLE. 272.537 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR August:

silver open interest data:

FRONT MONTH OF SEPT /2023 OI: 65 CONTRACTS HAVING LOST 1 CONTRACT(S). WE HAD 1

CONTRACT SERVED ON WEDNESDAY. SO WE GAINED 0 CONTRACTS OR NIL ADDITIONAL OZ WILL STAND FOR SILVER AT THE COMEX..

OCT LOST 40 CONTRACTS TO STAND AT 975.

NOVEMBER GAINED 0 CONTRACTS TO STAND AT 140

DEC. LOST 616 CONTRACTS TO STAND AT 112,637 .

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1 for 5,000 oz

Comex volumes// est. volume today 72,654 good

Comex volume: confirmed yesterday 60,667 fair

To calculate the number of silver ounces that will stand for delivery in SEPT. we take the total number of notices filed for the month so far at 2618 x 5,000 oz = 13,090,000 oz

to which we add the difference between the open interest for the front month of SEPT (65) and the number of notices served upon today 1 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT/2023 contract month: 2618 (notices served so far) x 5000 oz + OI for the front month of SEPT (65) – number of notices served upon today (1 )x 500 oz of silver standing for the SEPT contract month equates to 13.410 million oz. + 0 MILLION EXCHANGE FOR RISK..NEW TOTALS EXCHANGE FOR RISK: 3.0 MILLION OZ//NEW TOTAL STANDING FOR SILVER: 16.410 MILLION OZ//

There are 42.062 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS

SEPT 21/WITH GOLD DOWN $25.60 TODAY:SMALL CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 0.58 TONNES OF GOLD FROM THE GLD/ : // //INVENTORY RESTS AT 878.25 TONNES

SEPT 19/WITH GOLD UP $0.60 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD : // //INVENTORY RESTS AT 880.217 TONNES

SEPT 18/WITH GOLD UP $8.40 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD : A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD// //INVENTORY RESTS AT 880.217 TONNES

SEPT 15/WITH GOLD UP $13.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD : A WITHDRAWAL OF 1.055 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 879.70 TONNES

SEPT 14/WITH GOLD UP $1.00 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD : A WITHDRAWAL OF 4.63 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 882.01 TONNES

SEPT 13/WITH GOLD DOWN $2.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 12/WITH GOLD DOWN $11.20 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 11/WITH GOLD UP $4.45 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 8/WITH GOLD UP $0.35 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD : / //INVENTORY RESTS AT 886.64 TONNES

SEPT 7/WITH GOLD DOWN $0.20 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 3.22 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.69 TONNES

SEPT 6/WITH GOLD DOWN $8.80 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.16 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.81 TONNES

SEPT 5/WITH GOLD DOWN $13.50 TODAY: SMALL CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.97 TONNES

SEPT 1/WITH GOLD UP $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 31/WITH GOLD DOWN $1.00 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 0.87 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 890.10 TONNES

AUGUST 30/WITH GOLD UP $8.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.59 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 889.23 TONNES

AUGUST 29/WITH GOLD UP 17.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.6 TONNES OF GOLD INTO THE GLD.: / //INVENTORY RESTS AT 886.64 TONNES

AUGUST 28/WITH GOLD UP $6.90 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: / //INVENTORY RESTS AT 884.04 TONNES

AUGUST 25/WITH GOLD DOWN $6.05 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD// //INVENTORY RESTS AT 884.04 TONNES

AUGUST 24/WITH GOLD UP $0.65 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD //INVENTORY RESTS AT 884.91 TONNES

AUGUST 23/WITH GOLD UP $21.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 4.32 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 884.91 TONNES

AUGUST 22/WITH GOLD UP $2.95 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 0.87 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 889.23 TONNES

AUGUST 21/WITH GOLD UP $7.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 2.60 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 890.10 TONNES

AUGUST 18/WITH GOLD UP $1.15 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 6.92 TONNES OF GOLD FROM THE GLD//: //: /// //INVENTORY RESTS AT 887.50 TONNES

AUGUST 17/WITH GOLD DOWN $12.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD: //: /// //INVENTORY RESTS AT 894.42 TONNES

GLD INVENTORY: 878.25 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

SEPT 21/WITH SILVER DOWN 13 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:. : // /.////INVENTORY RESTS AT 450.133 MILLION OZ

SEPT 19/WITH SILVER UP 0 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.1 MILLION OZ INTO THE SLV. : // /.////INVENTORY RESTS AT 449.033 MILLION OZ

SEPT 18/WITH SILVER UP 11 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 1.651 MILLION OZ INTO THE SLV. : // /.////INVENTORY RESTS AT 441.332 MILLION OZ

SEPT 15/WITH SILVER UP 37 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.31 MILLION OZ FROM THE SLV. : // /.////INVENTORY RESTS AT 439.681 MILLION OZ

SEPT 14/WITH SILVER DOWN 16 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: : // /.////INVENTORY RESTS AT 440.736 MILLION OZ

SEPT 13/WITH SILVER DOWN 23 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1,009 MILLION OZ INTO THE SLV//: // /.////INVENTORY RESTS AT 440.736 MILLION OZ

SEPT 12/WITH SILVER UP 1 CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.209 MILLION OZ INTO TEH SLV//: // /.////INVENTORY RESTS AT 439.727 MILLION OZ

SEPT 11/WITH SILVER UP 19 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.209 MILLION OZ INTO TEH SLV//: // /.////INVENTORY RESTS AT 439.727 MILLION OZ

SEPT 8/WITH SILVER DOWN 8 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 7/WITH SILVER DOWN 21 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: // /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 6/WITH SILVER DOWN 36 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.373 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 436.518 MILLION OZ

SEPT 5/WITH SILVER DOWN 69 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 734,000 OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 437.891 MILLION OZ

SEPT 1/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 440.00 MILLION OZ

AUGUST 31/WITH SILVER DOWN 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.375 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 438.625 MILLION OZ

AUGUST 30/WITH SILVER DOWN 2 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.834 MILLION OZ OF SILVER OUT OF THE THE SLV// /.////INVENTORY RESTS AT 443.210 MILLION OZ

AUGUST 29/WITH SILVER UP 49 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 183,000 OF SILVER INTO THE THE SLV// /.////INVENTORY RESTS AT 445.044 MILLION OZ

AUGUST 28/WITH SILVER UP 3 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.281 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 444.861 MILLION OZ

AUGUST 25/WITH SILVER UP ONE CENT TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.751 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 446.145 MILLION OZ

AUGUST 24/WITH SILVER DOWN 16 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.651 MILLION OZ OZ FROM THE SLV// /.////INVENTORY RESTS AT 448.896 MILLION OZ

AUGUST 23/WITH SILVER UP 94 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 826,000 OZ FROM THE SLV// /.////INVENTORY RESTS AT 450.547 MILLION OZ

AUGUST 22/WITH SILVER UP 12 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV: /.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 21/WITH SILVER UP 59 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 917,0000 OZ FROM THE SLV//.////INVENTORY RESTS AT 451.373 MILLION OZ

AUGUST 18/WITH SILVER UP 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

AUGUST 17/WITH SILVER UP 15 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV//.////INVENTORY RESTS AT 452.290 MILLION OZ

CLOSING INVENTORY 449.033 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

Fed Talk & Dot Plots: There’s A Big Difference Between Saying And Doing

THURSDAY, SEP 21, 2023 – 11:05 AM

Authored by Michael Maharrey via SchiffGold.com,

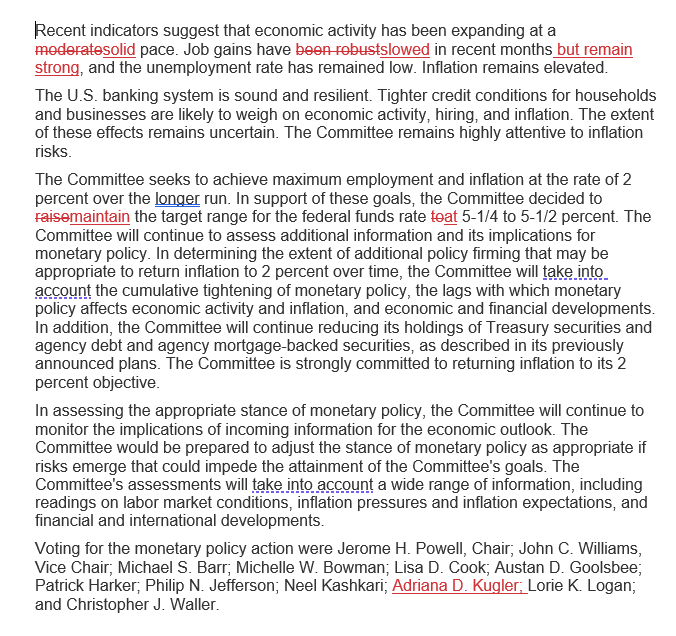

The Federal Reserve held interest rates steady at the September FOMC meeting, but the committee indicated that it plans to hold rates higher for longer than originally projected.

As you digest the Fed meeting, it’s important to remember that there is a big difference between “saying” and “doing.”

While the Fed didn’t raise rates this month, it indicated that it plans to hike one more time this year.

The FOMC was widely expected to stand pat this month. The question was how will the central bankers proceed in the months ahead. Based on projections released after the meeting, the Fed is leaning toward keeping monetary policy restrictive for longer.

As a Reuters article put it, the Fed “stiffened its hawkish stance.”

The official FOMC statement was virtually identical to the one issued after the July meeting.

“The Committee will continue to assess additional information and its implications for monetary policy. In determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.”

The committee also stuck to its “data dependent” mantra, saying it will “continue to monitor the implications of incoming information for the economic outlook” and adjust monetary policy if “risks emerge that could impede the attainment of the Committee’s goals.”

The Committee’s assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.”

In a nutshell, the Fed continued to give itself plenty of wiggle room to justify any action it takes in the future.

During his post-meeting press conference, Federal Reserve Chairman Jerome Powell said the committee is “in a position to proceed carefully in determining the extent of additional policy firming.” But he also said the committee members would like to see more progress in its inflation fight.

We want to see convincing evidence really that we have reached the appropriate level, and we’re seeing progress and we welcome that. But, you know, we need to see more progress before we’ll be willing to reach that conclusion.”

The CPI came in hotter than expected in August, throwing some cold water on the disinflation narrative.

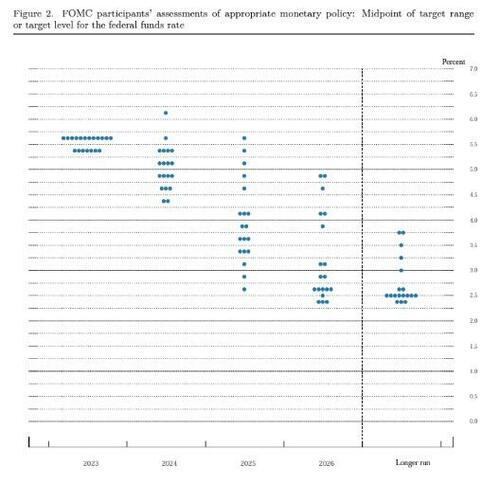

While there were no surprises in policy or official rhetoric, the so-called “dot-plot” released by the committee was slightly more hawkish than the one released after the June meeting.

Twelve FOMC members indicated that they expect one additional hike this year while seven opposed it.

Meanwhile, committee members projected two rate cuts in 2024. That’s two fewer than the June forecast and would put rates around 5.1% at the end of 2024. Over the longer term, FOMC members projected rates to come in around 2.9% in 2026.

Powell indicated that optimism about the economy was driving the anticipation of fewer cuts next year more than worry about persistent price inflation.

The FOMC statement said, “The committee characterized economic activity as “expanding at a solid pace,” and the Fed upped its economic forecast significantly, projecting GDP to increase 2.1% this year. That’s more than double the 1% estimate from June. They expect growth to slow to 1.5% next year, up from June’s 1.1% projection. Any talk of a recession is completely out of the discussion.

Broadly, stronger activity means we have to do more with rates, and that’s what that meeting is telling you.”

Saying Isn’t Doing

Powell and Company say they will raise rates one more time. And they say they will leave rates higher for longer. But saying and doing are two different things.

In fact, the Fed’s track record at projecting the trajectory of interest rates is abysmal. The central bankers would likely offer more accurate projections if they just threw darts at a dart board.

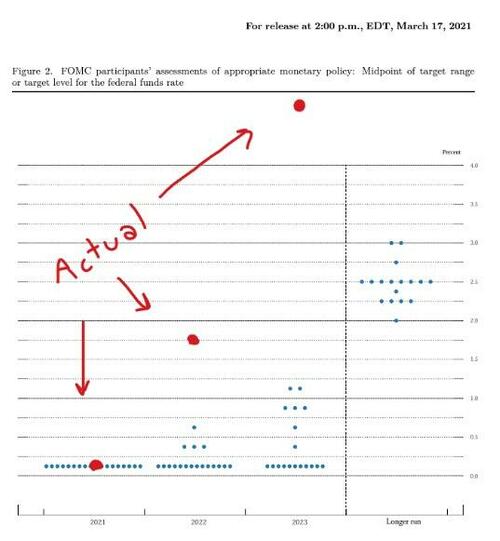

According to fund manager David Hay, the Fed has only gotten interest rate projections right 37% of the time. And as Hay pointed out, “They control interest rates!”

Just consider that in March 2021, the FOMC projected the interest rate would still be zero in 2022. The actual 2022 rate was 1.75%. And in 2023, the vast majority of FOMC members thought the rate would still be zero percent. The actual rate – over 5%.

This is just one example of how horribly wrong the Fed has been. I can cite other examples.

Remember back in 2006 when the central bankers insisted there was no housing bubble? Then when things started to unravel, they promised the problem was contained to subprime.

In 2008, Ben Bernanke launched quantitative easing and swore that it wasn’t debt monetization. He said the Fed would sell all of the bonds it planned to buy once the emergency was over. Today, virtually all of those bonds remain on the Fed’s balance sheet.

It’s almost like the Fed people are wrong about everything.

So, why should we put any stock at all in the most recent dot-plot or the Fed’s economic projections?

The problem is the central bankers are disconnected from reality. This also seems typical. Remember “transitory” inflation?

The point here is there is no reason to believe anything Powell and Company said today or to think their musings will aid in projecting the central bank’s next moves. Given the Fed’s track record, it’s more likely that rates will be at zero by the end of next year and the US economy will be in the clutches of a deep recession.

The fact is the Fed can afford to be hawkish as long as the economy is limping along with no obvious hiccups. The real test will come when something breaks in the economy.

And something will break with interest rates at 5.5%. It’s just a matter of time.

As the saying goes, things happen slowly and then all at once.

Interest rates are higher than they were in June 2006, the peak of that hiking cycle that burst the housing bubble. The Fed held them there until Bernanke cut rates in September 2007 when home sales started to collapse. In other words, rates are currently at levels that set off the 2008 financial crisis and the Great Recession. The difference is today we have even more debt and malinvestments in the economy. One has to wonder why anybody thinks things will turn out differently this time.

Consider this; the last time rates were this high, the national debt was a mere $5.6 trillion. Today the debt stands at over $33 trillion and the federal government is running huge deficits month after month.

Meanwhile, there were more corporate defaults through the first six months of 2023 than we had in all of ’22, and “healthy” American consumers have blown through their savings and have turned to using credit cards with 20 percent-plus interest rates to make ends meet.

The fact is the Federal Reserve has screwed up everything that is a function of interest rates. Rate hikes have already precipitated a financial crisis. Despite the Fed’s insistence that “the US banking system is sound and resilient,” we’ve already witnessed three major bank failures. The Fed’s bank bailout papered over those problems and plugged that hole in the dam (Banks are still getting bailout money.), but it’s only a matter of time before something else breaks. (Commercial real estate is a good candidate.)

Cuts are coming, no matter how tough Powell talks today, or what the rest of his crew put on a dot plot. It doesn’t matter what they say. It’s all about what they do.

end

2 Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens//JAMES RICKARDS//JOHN RUBINO

3,Chris Powell of GATA provides to us very important physical commentaries

Seems that London is too afraid of sanctions so Russia sells its gold production to the UAE. This begins the loop in that India (and others) buys this gold for discounted Russian oil and pays gold for it. Thus gold for oil and Russia accumulates gold.

(Bloomberg)

Russia becomes UAE’s top gold source after being shut out of West

Submitted by admin on Wed, 2023-09-20 13:25Section: Daily Dispatches

By Eddie Spence

Bloomberg News

Wednesday, September 20, 2023

Russia became the United Arab Emirates’ top source of gold last year after Western countries imposed sanctions on supplies following the Kremlin’s invasion of Ukraine.

The UAE last year imported 96.4 tons of gold from Russia, more than any other country, according to the United Nations’ Comtrade database. That’s roughly a third of Russia’s annual mine production, and a more than 15-fold increase year-on-year in the UAE’s gold imports from the country.

The UAE has long been a key hub for precious metals, particularly from Africa and India, but last year was the first time it played a major role in trading Russian gold. Before the war, almost all of Russia’s bullion was shipped to London, the world’s top market, but it rapidly became taboo among the banks that used to handle it. …

… For the remainder of the report:

end

4, OTHER IMPORTANT GOLD/SILVER COMMENTARIES//CHINA==LONDON GOLD ARBITRATION

-END-

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES:IRON ORE//CARBON OFFSETS

Congratulations to these guys: these figured out this carbon nonsense

(zerohedge)

Backfire: World’s Fourth Largest Iron Ore Producer Stops Purchasing Carbon Offsets

THURSDAY, SEP 21, 2023 – 04:15 AM

About three weeks after Shell, Europe’s largest oil company, quietly shelved the world’s largest corporate plan to develop carbon offsets, the world’s number four iron ore producer, Fortescue Metals Group Ltd., has decided to end purchases of voluntary carbon offsets. This comes as at least one major study has revealed carbon offsets are prone to ‘greenwashing’ and most credits don’t actually benefit the climate.

Billionaire Andrew Forrest’s Fortescue Metals produced about 2.55 million tons of scope 1 and 2 carbon dioxide emissions in the year leading up to June 30. Bloomberg said the company has implemented a new policy to halt purchases of carbon offset credits from the current fiscal year.

“We are the only heavy emitter in the world to stop purchasing voluntary offsets,” Dino Otranto, chief executive officer of Fortescue’s metals business, said in a statement.

The move by Fortescue comes after Shell laid out an updated strategy for the company that included cutting costs and doubling down on profit centers (oil and gas) – which notably shelved the world’s largest corporate plan to develop carbon offsets.

According to Bloomberg Green’s investigations, many offset programs don’t deliver the promised environmental benefits.

A study by the University of California, Berkeley’s Goldman School of Public Policy found that REDD+ credits account for a quarter of the carbon offset market. And according to researchers, “Most credits probably don’t represent any climate benefit.”

The Berkeley findings raise serious questions about the carbon offsets market come months after the world’s leading carbon credit certifier, Verra, sold worthless offsets to major corporations.

Recall Elon Musk tweeted one year ago, “ESG is a scam. It has been weaponized by phony social justice warriors.”

As we noted earlier this year, “Carbon Credits Are The Biggest Scam Since Indulgences… How You Can Avoid Being Fleeced.”

END

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.3056

OFFSHORE YUAN: DOWN TO 7.3132

SHANGHAI CLOSED DOWN 23.87 PTS OR 0.77%

HANG SENG CLOSED DOWN 452.75PTS OR 1.37%

2. Nikkei closed DOWN 218.81 PTS OR .66 %

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 105.30 EURO FALLS TO 1.0530 UP 52 BASIS PT

3b Japan 10 YR bond yield: RISES TO. +.737 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.93/JAPANESE YEN FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN// OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.7495***/Italian 10 Yr bond yield UP to 4.542*** /SPAIN 10 YR BOND YIELD UP TO 3.800…**

3i Greek 10 year bond yield FALLS TO 4.095

3j Gold at $1918.95 silver at: 23.09 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 60 /100 roubles/dollar; ROUBLE AT 95.55//

3m oil into the 89 dollar handle for WTI and 92 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.93// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.737% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9049 as the Swiss Franc is still rising against most currencies. Euro vs SF 0.9627well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

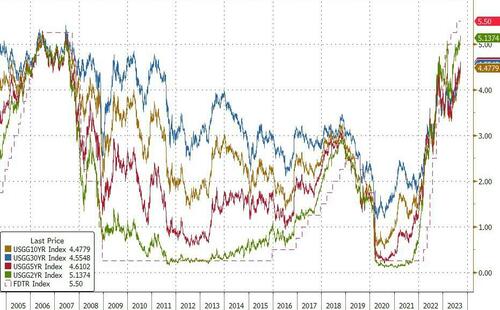

USA 10 YR BOND YIELD: 4.4444 UP 10 BASIS PTS…

USA 30 YR BOND YIELD: 4.486 UP 8 BASIS PTS/

USA 2 YR BOND YIELD: 5.165 UP 8 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 27.12…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 6 BASIS PTS AT 4.3650

end

2.a Overnight: Newsquawk and Zero hedge:

USA EARLY MORNING REPORT

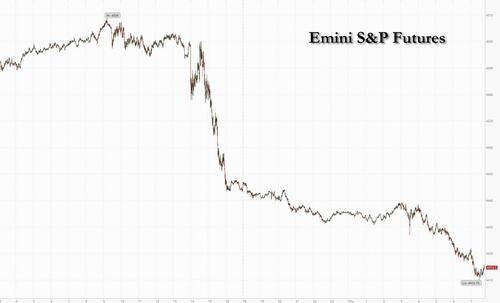

Futures, Global Stocks Tumble As Markets Reel After Fed’s Hawkish Pause

THURSDAY, SEP 21, 2023 – 08:13 AM

Futures are sharply lower, extending yesterday’s steep losses after the Fed’s hawkish pause. The Fed wasn’t alone in keeping rates unchanged: it was followed by both the SNB and BOE, both of which surprised markets by not raising rates and sending the franc and sterling sliding. On the other hand, the inflation-ridden Riksbank and Norges both hiked, telling investors to expect more such moves. Hyperinflating basket case Turkey hiked by 500bps, in line with expectations. As of 7:45am, S&P futures tumbled 0.7% to 4,415, while Nasdaq 100 futures were down 1% briefly dipping below the key 15,000 level. Most Treasury yields climbed apart from two-year rates, which edged lower. The Bloomberg Dollar Spot Index traded near the day’s highs, pressuring most other Group-of-10 currencies. Brent crude fell for a third-straight day, trading below $93. Gold slid and Bitcoin declined 1%. Today’s macro data focus is on Jobless Claims, Existing Home Sales, Leading Index, and Philly Fed.

In premarket trading, Splunk was set to open sharply higher after Cisco announced it would purchase the company for $157/share (it closed just below $120). Broadcom slumped after a report by The Information that Google has discussed dropping the company as an AI chips supplier as early as 2027. FedEx shares rise as much as 5.4% after the courier raised the lower end of its fiscal 2024 adjusted EPS forecast, thanks to cost cutting, strong pricing and customers who switched to the courier from its main rival on concern over a potential strike, and prompting analysts to hike their price targets on the stock. Analysts were positive on the company’s cost reduction progress and highlighted the strong performance at its Ground unit and said that guidance is still conservative. Here are the other notable premarket movers:

- ARM Holdings shares fall 2.3%, with the chip designer nearing its $51 IPO price, as rising bond yields put pressure on growth stocks, with tech peers down too.

- Broadcom shares drop as much as 4.6%, following a report from The Information that Google executives “extensively” discussed dropping the semiconductor maker as an AI chips supplier as early as 2027, citing a person familiar with the matter.

- CrowdStrike shares rise as much as 3.4%, as analysts hike their price targets on the stock following the Fal.Con cybersecurity conference and investor briefing, at which it set out new targets. Analysts said the company’s margin outlook was especially strong, and new products such should help boost growth.

- Film and entertainment stocks rise, after Hollywood Studios and writers came a step closer to reaching a deal to end months of strikes. Warner Bros (WBD US) +3.1% and Paramount (PARA US) +3%.

The Fed on Wednesday held its target range, while updated quarterly projections showed most officials favored another rate hike in 2023. Policymakers also see less easing next year, with the median forecast for the federal funds rate at 5.1% by year-end, up from 4.6% when projections were last updated in June.

“People did expect a hawkish hold from the Fed, but it’s the extent of the hawkishness that surprised,” said Lee Hardman, a strategist at MUFG Bank Ltd. “We thought they may take one cut out of next year’s forecasts — instead they took two out. So it was much more hawkish than markets were pricing in.”

Some non-Fed headlines came from BAC’s CFO who says, “It’s difficult to see a US recession when the consumer is spending 4% more year-over year.” Axios reported that the US Chamber of Commerce’s Small Business Index, a confidence indicator, has reached its highest level since COVID struck US markets in early 2020. The survey includes 751 business, each that have fewer than 500 people; 71% say they expect revenue to increase next year. Spoiler alert: it won’t.

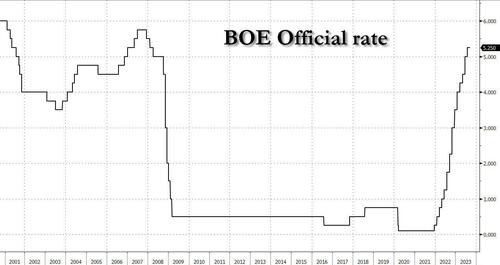

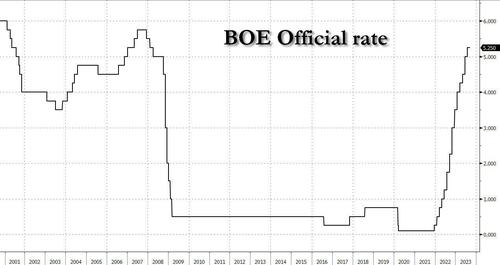

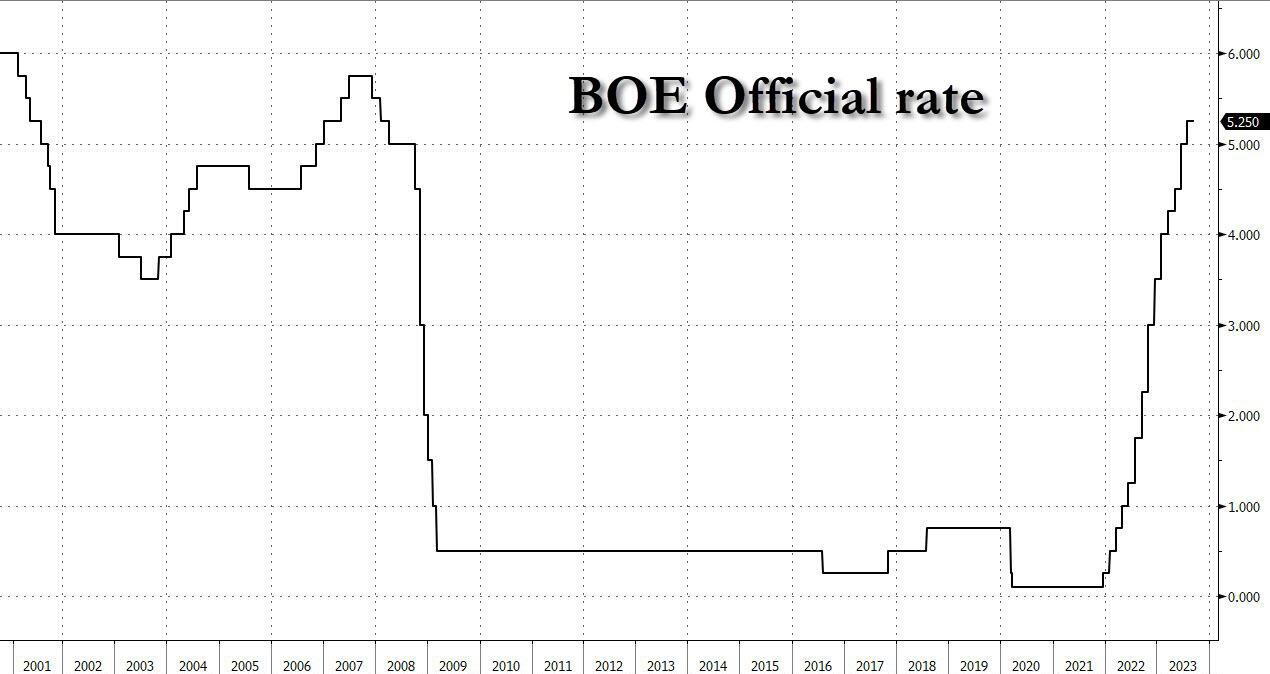

Europe’s Stoxx 600 Index declined 1% but was off session lows, with all sectors in the red, as traders digested the Fed’s higher-for-longer message. Travel and leisure stocks fell the most, while miners and industrial stocks also underperformed. Swiss equities were higher after the SNB unexpectedly paused rate hikes, while the BOE is due to announce its rate decision later Shares in UK banks and home builders rose as traders slashed their bets on further rate hikes with UBS saying the BOE hiking cycle is now over. The central bank held its key rate at 5.25%, ending a series of 14 successive hikes since December 2021, after a surprise drop in August inflation this week.

“Inflation has fallen a lot in recent months and we think it will continue to do so,” BOE Governor Andrew Bailey said in a written statement. “That’s welcome news. But there is no room for complacency. We need to be sure inflation returns to normal and we will continue to take the decisions necessary to do just that.”

A day after the Federal Reserve’s meeting, Europe had its own frenetic flurry of central bank decisions. Before the BOE, Swiss National Bank surprised investors by holding interest rates, causing the franc’s steepest drop since May against the euro. Sweden’s Riksbank increased its key rate as expected and said more hikes were possible, while Norway’s central bank said more tightening may come in December after raising rates to the highest in more than 14 years. Here are Europe’s top movers:

- Merck shares gain as much as 2.2% after Citi raised its recommendation on the German biotech group to buy, predicting performance in the firm’s Life Science and Semiconductor segments will recover in the near future.

- JD Sports shares rise as much as 8.6% after reporting results that Peel Hunt analysts said reflected a “surprisingly strong” performance in the US following recent guidance cuts from peers Foot Locker and Dick’s Sporting Goods.

- Next shares gain as much as 2.5% after the UK retailer boosted its pretax profit outlook for the full year, following other guidance raises in August and June. The third guidance update in three months is impressive, with the sales outlook suggesting resilience in the first half, Jefferies said.

- Safilo shares rise as much as 8.1%, the most intraday since August 2022, after the Italian eyewear company said it’s launching its Carrera Smart Glasses with Amazon.com’s Alexa technology, according to a statement late on Wednesday.

- Valneva shares rise as much as 4.7% after the French pharmaceutical firm reported better-than-expected first-half earnings. Van Lanschot Kempen sees a “strong set” of figures with beats across the board.

- CVS Group shares gain as much as 4.4% after the veterinary services firm reports better-than-expected profit. The stock plummeted earlier this month as UK antitrust regulators announced a probe of the sector.

- Delivery Hero rises as much as 2%, adding to Wednesday’s 7.1% gain, as the food delivery company confirmed that it’s mulling a sale of some businesses in Southeast Asia. Analysts said a potential deal could boost the company’s balance sheet and profit by shaking off some unprofitable operations that are currently involved in intensive competition.

- Ocado shares drop as much as 9.3% after being downgraded to underperform from neutral at BNP Paribas Exane, which cited the British online grocer’s share price rally in recent months.

- SSP Group shares fall as much as 8.7% after the food services company gave a trading update saying it expects full-year EPS toward the lower end of its guidance range. Analysts at Goodbody and Shore Capital noted the FX headwinds apparent in the update, but were encouraged by the opportunity from new business.

- Engcon shares drop as much as 8.9% after an editorial column on Swedish retail-trading website Placera.se recommended its users sell the Swedish industrial firm’s shares, citing a high valuation and slowing growth prospects.

- Quadient shares fall as much as 8.7% after the French postal- and document-services company reported first-half results that Oddo said were slightly below estimates.

Earlier in the session, Asian stocks fell the most in nearly a month after the Fed signaled that interest rates will remain higher for longer amid renewed economic strength, while Chinese equities slumped on persistent pessimism. The MSCI Asia Pacific Index dropped as much as 1.4%, set for a fourth day of losses, led by health-care and technology shares. Most markets in the region were down, with South Korea’s Kospi Index slumping more than 1% as large-cap chip and battery stocks dragged. The Fed left its benchmark interest rate unchanged as expected, while indicating that borrowing costs will likely stay higher for longer after one more hike this year. The message triggered overnight losses in Wall Street, gains in Treasury yields and strength in the dollar.

- Hang Seng and Shanghai Comp declined alongside the downbeat mood across regional peers, although the losses in the mainland were initially cushioned following the Chinese Cabinet’s pledge to speed up the development of the advanced manufacturing sector and amid resilience in developers after Guangzhou adjust purchase rules for several districts.

- Japan’s Nikkei 225 retreated below the 33,000 level as Japanese yields climbed to decade highs and with the BoJ kickstarting its 2-day policy meeting.

- Australia’s ASX 200 was lower with the top-weighted financial industry leading the broad declines.

- India’s benchmark stocks gauge dropped for a third consecutive session to its two-week low as US Federal Reserve’s signal to keep interest rates higher for longer spooked equities in Asia. The S&P BSE Sensex fell 0.9% to 66,230.24 in Mumbai, its lowest close since Sept. 6. The NSE Nifty 50 Index declined 0.8% to 19,742.35. ICICI Bank contributed the most to the Sensex’s decline, decreasing 2.8%. Out of 30 shares in the Sensex index, 6 rose and 20 fell, while 4 were unchanged.

In FX, the dollar gained against most major currencies, aside from the yen, which traded around 148 per dollar after weakening on Wednesday to the lowest level since November.

- EUR/CHF rises as much as 0.8% to 0.9656, the biggest daily jump since June

- EUR/SEK drops as much as 0.9% to 11.7687; it rose earlier to 11.9381 after the Riskbank announced a quarter-point interest rate increase

- EUR/NOK drops as much as 0.4% to 11.4573 before halving losses; Wednesday’s low is 11.4560

- GBP/USD falls as much as 0.4% to 1.2265, after the BOE unexpectedly ended its hiking cycle

With most central banks out of the way, attention now turns to Friday’s BOJ announcement. There are heightened prospects of official support for the Japanese currency, said John Vail, chief global strategist for Nikko Asset Management Co. in Tokyo. “Japan’s Ministry of Finance is likely to intervene in large fashion at 150 per dollar because it is hard to tolerate more inflationary pressure.”

The value of the yen has slumped to the lowest on record, as measured against a broad basket of its peers and adjusted for inflation, according to data from the Bank for International Settlements. This underscores the pressure to address yen weakness at the Bank of Japan, which is where this week’s series of central bank policy meetings wraps up on Friday.

In rates, treasury yields were broadly higher after the rate on the two-year note, which is more sensitive to imminent Fed moves, hit the highest since 2006 on Wednesday. After resuming post-Fed selloff in early Asia session, front-end of the Treasuries curve trades richer on the day into early US, outperforming belly and long-end as steepening move extends. US yields richer by 2bp across front-end of the curve while belly out to long-end trades cheaper by 1.5bp to 4bp on the day; 10-year yields around 4.45% the highest level since 2007, underperforming bunds and gilts by 1.5bp and 5bp in the sector. Gilts were supported after Bank of England keeps rates unchanged. Long-end Treasury yields also reach new cycle highs, joining rest of the curve after Wednesday’s Fed decision. Dollar IG issuance slate includes IBK 5Y; issuance paused Wednesday for the Fed decision and is expected to remain quiet for Thursday. US economic data slate includes 2Q current account balance, September Philadelphia Fed business outlook and weekly initial jobless claims (8:30am), August existing home sales and leading index (10am); no Fed speakers scheduled.

In commodities, oil’s breakneck rally is taking a breather as a smaller-than-expected drop in US crude stockpiles bolstered technical resistance to further gains; crude futures declined with WTI falling 1% to trade near $88.80. Spot gold drops 0.4%.

To the day ahead, and we’ll get the Bank of England’s latest policy decision, and also hear remarks from the ECB’s Schnabel and Lane. Otherwise, data releases include the US weekly initial jobless claims, existing home sales for August, the Conference Board’s leading index for August, and the Philadelphia Fed’s business outlook for September. In the Euro Area, we’ll get the preliminary consumer confidence reading for September, whilst in the UK there’s the public finances for August.

Market Snapshot

- S&P 500 futures down 0.4% to 4,430.50

- Brent Futures down 1.3% to $92.35/bbl

- Gold spot down 0.2% to $1,926.07

- U.S. Dollar Index up 0.13% to 105.46

- STOXX Europe 600 down 0.7% to 457.60

- MXAP down 1.5% to 159.24

- MXAPJ down 1.6% to 492.56

- Nikkei down 1.4% to 32,571.03

- Topix down 0.9% to 2,383.41

- Hang Seng Index down 1.3% to 17,655.41

- Shanghai Composite down 0.8% to 3,084.70

- Sensex down 0.9% to 66,197.17

- Australia S&P/ASX 200 down 1.4% to 7,065.23

- Kospi down 1.7% to 2,514.97

- German 10Y yield little changed at 2.73%

- Euro little changed at $1.0657

- Brent Futures down 1.3% to $92.35/bbl

Top Overnight News

- Japan may be nearing a point where it can declare victory in its battle against deflation, paving the way for further BOJ policy normalization. Nikkei

- As China’s stock market struggles to recover, regulators have started to probe some hedge funds and brokerages on quantitative trading strategies amid a growing outcry against a sector able to profit from share price falls and volatility. RTRS

- Natural gas prices sink in Europe as Chevron seems close to resolving a strike in Australia while flows recover in Norway. BBG

- Norway’s central bank hikes rates by 25bp to 4.25%, as expected, and provides hawkish forward guidance by signaling another increase in Dec (most assumed today’s hike would be the last one). Switzerland’s SNB surprises markets by leaving rates unchanged (economists were anticipating a 25bp hike). BBG

- Poland looks to downplay remarks from its PM about no longer supplying weapons to Ukraine, insisting that the country remains a committed to helping Kyiv achieve victory. FT

- Google has talked “extensively” about dropping Broadcom as its AI chip supplier as soon as 2027 as the internet giant looks to cut costs and utilize proprietary silicon (in addition, Google is working to replace Broadcom with Marvell for network interface chips). The Information

- House Republicans reported major progress charting a path forward on a partisan bill to avert a government shutdown and a Department of Defense spending bill — two measures that suffered public setbacks just a day before — after Speaker Kevin McCarthy (R-Calif.) hashed out a new framework for a GOP-only stopgap proposal in a House Republican conference meeting that lasted more than two hours on Wednesday. The Hill

- AMZN is abandoning plans to impose a new fee on merchants that don’t use its shipping services amid increased regulatory/antitrust scrutiny on the company from the gov’t. BBG

- FDX reported very strong FQ1 earnings, with EPS of 4.55 (vs. the Street 3.73), thanks to aggressive cost cutting, and the full-year EPS outlook was increased (although by less than the Q1 beat). RTRS

A more detailed look at global markets courtesy of Newquawk

Asia-Pac stocks were pressured in the aftermath of the FOMC’s hawkish pause. ASX 200 was lower with the top-weighted financial industry leading the broad declines. Nikkei 225 retreated below the 33,000 level as Japanese yields climbed to decade highs and with the BoJ kickstarting its 2-day policy meeting. Hang Seng and Shanghai Comp declined alongside the downbeat mood across regional peers, although the losses in the mainland were initially cushioned following the Chinese Cabinet’s pledge to speed up the development of the advanced manufacturing sector and amid resilience in developers after Guangzhou adjust purchase rules for several districts.

Top Asian News

- Japanese PM Kishida said he will instruct people to pull together the pillars of an economic package early next week, while they will include measures to counter inflation and social measures to counter declining population, according to Reuters.

- Chinese Commerce Ministry says some firms have obtained export licenses for gallium and germanium; willing to seek a basket of solutions for the Australian wine dispute.

- China’s 2023 nat gas demand seen at 396.4BCM, +8% Y, via CNOOC; LNG imports 70.79mln/T, +10.9% YY. Nat gas demand from China seen peaking in 2040 at 700BCM.

European bourses are pressured as the region reacts to Wednesday’s FOMC where a hawkish hold was delivered, Euro Stoxx 50 -1.1%. Action which continues the tone of APAC trade but with the region conscious of a Chinese cabinet pledge around manufacturing and also beginning to look ahead to Friday’s BoJ. Sectors are primarily in the red with the exception of Retail post-earnings from JD Sports and Next which reside towards the top of the Stoxx 600; Travel/Leisure and Basic Resources lag, latter on benchmark activity and numerous price target cuts. US futures are lower across the board but with action slightly more contained when compared to European peers, ES -0.4%, NQ -0.6%; today’s docket has a handful of data points before Friday’s Fed speak resumption with Cook, Daly & Kashkari. Google (GOOG) reportedly wants to ditch Broadcom (AVGO) as its TPU sever chip supplier to reduce AI costs, according to The Information; Since last year has been working to replace Broadcom with Marvell Technology (MRVL). Pre-market: GOOG -0.7%, AVGO -5.2%, MRVL +3.5%

Top European News

- Sunak Gambles on Voters Focusing More on Costs Than Climate

- Next Raises Guidance Again as Wage Gains Boost Shoppers

- SNB Surprises With Rate Pause as Tightening Tames Inflation

- Riksbank Hikes Swedish Rate With Door Kept Open to Act Again

- Norway Raises Rate Again and Signals Another Move in December

- Swiss Stocks Outshine Peers as SNB Pauses; Fed Weighs on Region

FX

- The Fed revives Greenback fortunes via more hawkish dot plots, DXY firmly back above 105.000 within a 105.400-680 range.

- Franc collapses as SNB defies expectations for a 25bp hike and bases new forecasts on steady 1.75% rate, EUR/CHF and USD/CHF spike circa 100 pips to 0.9677 and 0.9078 respectively.

- Pound flounders in the dark about BoE prospects for midday as markets remain split between pause and 1/4 point rate rise, Cable sub-1.2300 from just over 1.2350 at best.

- Yen and Euro pare declines vs. Dollar ahead of 148.50 and 1.0600, with EUR/USD propped up by a Fib and option expiries.

- Norwegian Crown underpinned around 11.5000 vs. Euro after hawkish Norges Bank hike, Swedish Krona choppy on either side of 11.9000 as Riksbank reaches a peak and hedges 25% FX reserves.

- PBoC set USD/CNY mid-point at 7.1730 vs exp. 7.3052 (prev. 7.1732)

- The European Commission has sent a letter to Poland listing 11 questions to determine the scope of the visa-for-bribes scandal and the EU security impact, via Politico; the letter warns that Poland could be violating EU law

Fixed Income

- Bonds off worst levels, but still heavy in wake of hawkish FOMC and through slew of other Central Bank pronouncements.

- Bunds below par between 129.69-23 parameters, Gilts sub-96.00 within 96.41-95.81 range and T-note nearer base of 108-16/25+ bounds pre-BoE, IJC, Philly Fed and ECB speakers

Commodities

- Crude benchmarks are softer intraday given broader risk sentiment post-Fed, WTI below USD 89.00/bbl and Brent down to a test of USD 92.00/bbl respectively at worst; currently off these lows.

- Dutch TTF pressured as Offshore Alliance members at Woodside have overwhelmingly voted to endorse a deal with the company.

- Spot gold is under modest pressure as the USD remains bid with base metals similarly pressured on the broader risk tone.

- Saudi Crown Prince MBS responded that output reductions are purely based on supply and demand to the market when asked about criticism that oil output cuts help Russia.

- Australian industrial arbitrator said Chevron (CVX) and unions are on the precipice of achieving the first enterprise agreements for LNG facilities and discussions have resulted in widespread agreement on the majority of provisions of proposals. The arbitrator made recommendations on pay and working conditions for Chevron and unions to consider but noted that a failure to settle all outstanding issues would result in the agreed provisions simply evaporating, while parties are required to advise the commission of their acceptance or rejection of recommendations by 09:00 Sydney time on Friday.

- Offshore Alliance members at Woodside (WDS AT) have overwhelmingly voted to endorse a deal with the company while members at Chevron (CVX) will meet tonight to consider a recommendation made by the Fair Work Commission, according to a statement.

- Natural Gas Pipeline Co. declared a force majeure on the M&M line near compressor station 158 located in Dewey County, Oklahoma.

- Russia is mulling an additional tax on exports for some commodities including metals, according to sources cited by Reuters.

Geopolitics

- Russian Foreign Ministry said NATO drills near Russian borders are increasingly provocative and aggressive in nature, as well increase risks of incidents, according to RIA.

- Saudi Arabia said solving the Palestinian issue is critical to a deal with Israel, according to FT. In relevant news, Saudi Crown Prince MBS said he is prepared to work with whoever is leading Israel if there is a breakthrough in negotiations for normalisation with Israel, while he had also commented that Saudis will get a nuclear weapon if Iran does first, according to AFP and Fox News.

- Iranian President Raisi said Iran has no problem with IAEA inspections of its nuclear sites.

- Qatar held separate bilateral meetings with the US and Iran this week, touching on nuclear and drone issues, according to sources cited by Reuters.

- Kuwait’s PM said the Iraqi ruling on regulating navigation in Khor Abdullah Waterway includes historical fallacies and Iraq needs to take concrete, decisive and urgent measures to address the ruling, according to Reuters.

- Nagorno-Karabakh ethnic Armenians say Azerbaijani forces have violated the ceasefire; Azerbaijan denies its forces violated the ceasefire.

US Event Calendar

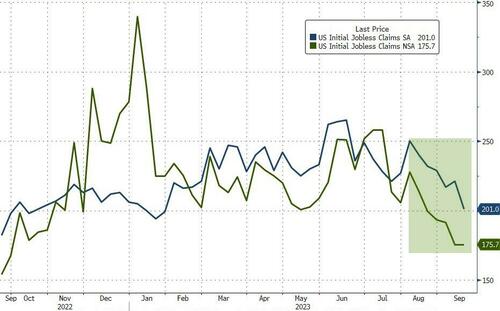

- 08:30: Sept. Initial Jobless Claims, est. 225,000, prior 220,000

- 08:30: Sept. Continuing Claims, est. 1.69m, prior 1.69m

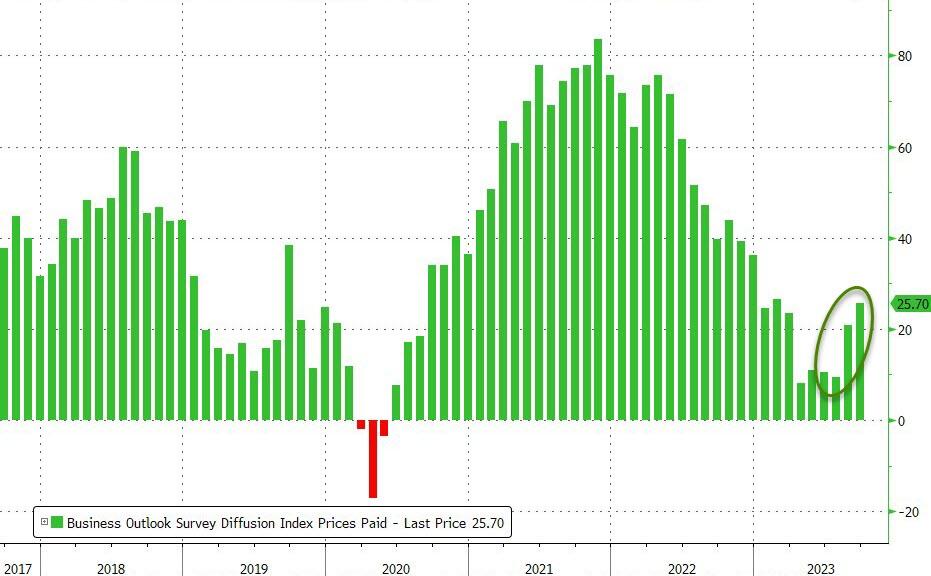

- 08:30: Sept. Philadelphia Fed Business Outl, est. -1.0, prior 12.0

- 08:30: 2Q Current Account Balance, est. -$220b, prior -$219.3b

- 10:00: Aug. Existing Home Sales MoM, est. 0.7%, prior -2.2%

- 10:00: Aug. Leading Index, est. -0.5%, prior -0.4%

DB’s Jim Reid concludes the overnight wrap

As widely expected, the FOMC kept the fed funds rate on hold yesterday, but this pause was accompanied by clear hawkish undertones and both bonds and equities sold off notably in the aftermath. 10yr US yields are at 4.43% as I type this morning, +12bps above where they were prior to the meeting. The starting point for the hawkishness came from the updated dot plot in the new Summary of Economic Projections. The end-2023 median dot was unchanged at 5.6%, but the median dot for 2024 moved 50bps higher to 5.1% (our US economists had expected 2024 to move up by 25bps). So the median FOMC member is pencilling in only two rate cuts in 2024, after one more hike this year. Interestingly, the newly published projections for 2026 showed the median dot at 2.9%, still above the long-term projection of 2.5%, so pointing to a persistently “tight” policy stance. The higher 2024-25 dot plot came as the SEP moved further towards a soft landing view, lowering unemployment projections for both 2024 and 2025 by 0.4pp to 4.1%. That would be only a slight uptick from the latest 3.8% level.

In the press conference Powell actually said that he “would not” have a soft landing as a baseline expectation, though later adding that soft landing is a primary objective for the FOMC. A little bit of a confusing message but overall, Powell reinforced a higher-for-longer message. Echoing the dot plot, he noted that the neutral rate may have risen and it was “certainly possible that the neutral rate…at this moment is higher than (the long-run rate)”. He also downplayed the prospects of cuts, saying that the FOMC was “never intending to send a signal” about timing of rate cuts with its dot plot and that “there’s so much uncertainty around” this.

Powell’s comments did see some moderation of the near-term tightening bias. He noted several times that the Fed is now in a position to “proceed carefully”. The prepared remarks struck a softer tone on labour market tightness and Powell highlighted that the last three inflation prints were “very good” readings, though not yet enough for the Fed to be confident they have reached a “sufficiently restrictive” stance. Our US economists note that with the FOMC end-2023 projections being likely too high on inflation and too low on unemployment, these set a relatively low bar for skipping the final projected hike. Correspondingly, our economists continue to expect no further rate increases – see the reaction note here for their full take.

So overall, the Fed sent a clear message that they think rates will stay high for longer, and the markets took this on board. Fed fund futures saw the chances of another hike by the end of the year move up to 54% from 45% the day before, with the peak rate now priced for January 2024 (with a 58% chance of a hike by then). Fed funds pricing for end-24 rose by +13.3bps on the day, and 20bps from its earlier intra-day lows, to a new cycle high of 4.76% (this is still more than 30bps below the Fed’s new median dot). My CoTD yesterday looked the implications of this pricing. Although it reflects the market pricing in a soft landing, the high levels probably increase the risk of a hard one. See the short note here.

In the bond market, the 2yr Treasury yield had been trading a few bps lower prior to the Fed decision but spiked by nearly 10bps in its immediate aftermath and closed +8.5bps up on the day at 5.18%, the highest level since 2006. The 10yr yield was up by +4.9bps to 4.41%, a new post-2007 high and is above 4.43% as I type. Meanwhile, the 10yr real yield closed above 2% for the first time since early 2009 (+6.6bps to 2.05%). Equities also lost ground in response to the Fed’s hawkish signal. The S&P 500 was down -0.94% by the close, with the decline coming during and after Powell’s press conference. Tech stocks lagged, with the NASDAQ down -1.53% and the Magnificent Seven mega caps down -2.20%. In FX, the dollar index gained about half a percent following the Fed event, closing up +0.19% on the day after trading lower earlier on. This morning in Asia, the trend continues with the dollar index rising another +0.2% and to fresh 14-year highs. The Yen has drifted to the lowest level since last November since the FOMC with this being an interesting set up ahead of the BoJ tomorrow morning.