GOLD PRICE CLOSED: UP $16,40 TO $2049.20

SILVER PRICE DOWN 8 CENTS TO $23.07

Access prices: closes 4: 15 PM

Gold ACCESS CLOSED 2037.70

Silver ACCESS CLOSED: 22.91

Bitcoin morning price:, 42,657 DOWN 1060 DOLLARS

Bitcoin: afternoon price: $42,770 DOWN 1173 dollars

Platinum price closing $925.70 DOWN $0.95

Palladium price; $988.95 UP $10.45

END

SHANGHAI GOLD (USD) FUTURES – QUOTES

SHANGHAI GOLD PREMIUM 45 DOLLARS/COMEX GOLD

Beginning Monday, April 1, 2024, CME Group settlement data will no longer be accessible through ftp.cmegroup.com and will have a delayed publication time of 12:00 a.m. CT on all cmegroup.com web pages. Learn about alternate ways to access the data in our FAQ.

AUTO-REFRESH IS OFF

Last Updated 31 Jan 2024 12:51:39 PM CT.

Market data is delayed by at least 10 minutes.

Due to the huge rise in the dollar, we must look at gold and silver in currencies other than the dollar to understand where we are heading

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $2,738.67 UP 11.03 CDN dollars per oz( * NEW ALL TIME HIGH 2,795.90 CDN DOLLARS PER OZ//DEC 1 272023)

*BRITISH GOLD: 1607.02 UP 2.97 pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1655.17 BRITISH POUNDS/OZ) OCT 2/2023

*EURO GOLD: 1884,83 UP 6.81 euros per oz //* (ALL TIME CLOSING HIGH: 1903.75 EUROS PER OZ//DEC 1.2023)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,031.500000000 USD

INTENT DATE: 01/30/2024 DELIVERY DATE: 02/01/2024

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 86

104 C MIZUHO 158

118 C MACQUARIE FUT 80

132 C SG AMERICAS 51

190 H BMO CAPITAL 836

323 C HSBC 1603 170

357 C WEDBUSH 8

363 H WELLS FARGO SEC 195

365 C MAREX CAPITAL M 60

407 C STRAITS FIN LLC 1

435 H SCOTIA CAPITAL 625

624 C BOFA SECURITIES 1

657 C MORGAN STANLEY 607

661 C JP MORGAN 1547 1277

661 H JP MORGAN 53

685 C RJ OBRIEN 7

686 C STONEX FINANCIA 3

690 C ABN AMRO 3

709 C BARCLAYS 4

737 C ADVANTAGE 12

880 C CITIGROUP 25

880 H CITIGROUP 109

DLV615-T CME CLEARING

BUSINESS DATE: 01/30/2024 DAILY DELIVERY NOTICES RUN DATE: 01/30/2024

PRODUCT GROUP: METALS RUN TIME: 20:31:12

905 C ADM 26 19

TOTAL: 3,783 3,783

MONTH TO DATE: 3,783

JPMorgan stopped 1277/3783 contracts.

FOR JAN.:

GOLD: NUMBER OF NOTICES FILED FOR FEB/2024. CONTRACT: 3783 NOTICES FOR 378,300 OZ or 11.7667 TONNES

total notices so far: 3783 contracts for 378,300 Oz (11.7667 tonnes)

FOR FEBRUARY:

SILVER NOTICES 547 NOTICE(S) FILED FOR 2,735,000 OZ/

total number of notices filed so far this month : 547 for 2,745,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES

GLD

WITH GOLD UP $16.40

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 2,01 TONNES OF GOLD FROM THE GLD

INVENTORY RESTS AT 852.88 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER DOWN 8 CENTS AT THE SLV//

MEGA CHANGES IN SILVER INVENTORY AT THE SLV AGAIN: A WITHDRAWAL OF 1.7438 MILLION OZ OF SILVER FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 440.137 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 485 CONTRACTS TO 136,855 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS STRONG SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR LOSS OF $0.05 IN SILVER PRICING AT THE COMEX ON TUESDAY. WE HAD A ZERO LONG LIQUIDATION AT THE COMEX SESSION BUT A CONSIDERABLE SHORT COVERING. WE HAD A FAIR 369 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 369 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.05), BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A FAIR SIZED GAIN OF 321 CONTRACTS GAIN ON OUR TWO EXCHANGES ACCOMPANYING CONSIDERABLE SHORT COVERING BUT AT HIGHER PRICES.

WE MUST HAVE HAD:

A VERY STRONG SIZED 809 ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.535 MILLION OZ (FIRST DAY NOTICE) ACCOMPANYING A STRANGE 89 CONTRACT ISSUANCE FOR EX. FOR RISK FOR 445,000 OZ//NEW TOTAL; 3.980 MILLION OZ

//NEW STANDING FOR SILVER IS THUS 3.980 MILLION OZ

/ STRONG SIZED COMEX OI GAIN/HUGE SIZED EFP ISSUANCE/ VI) FAIR SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 369 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED 886 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN

TOTAL CONTRACTS for 21 days, total 15,733 contracts: OR 78.665 MILLION OZ (749 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 78.655 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 485 CONTRACTS DESPITE OUR TINY LOSS IN PRICE OF SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 809 ISSUED FOR MARCH AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB. OF 3.535 MILLION OZ ACCOMPANIED BY TODAY’S 445,000 OZ EX. FOR RISK //NEW TOTAL 3.980 MILLION OZ

NEW STANDING 3.980 million OZ /// WE HAVE A HUMONGOUS GAIN OF 321 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE TINY LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A FAIR SIZED 369 CONTRACTS//SOME FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION/// WITH CONSIDERABLE SHORT COVERINGS FROM OUR SPEC SHORTS . THE NEW TAS ISSUANCE TUESDAY NIGHT (369) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 547 NOTICE(S) FILED TODAY FOR 2,735,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 4438 CONTRACTS TO 430,328 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED 1245 CONTRACTS

WE HAD A FAIR SIZED DECREASE IN COMEX OI ( 3193 CONTRACTS) DESPITE OUR $6.50 GAIN IN PRICE//TUESDAY. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR FEB. AT 49.773 TONNES ON FIRST DAY NOTICE ACCOMPANIED BY TODAY’S HUGE 55,400 OZ EX. FOR RISK //THUS INITIAL STANDING FOR FEB: 51.494 TONNES // ALL OF THIS HAPPENED WITH OUR $6.50 GAIN IN PRICE WITH RESPECT TO TUESDAY’S TRADING. WE HAD A FAIR SIZED LOSS OF 1062 OI CONTRACTS (.5692) PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3376 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 430,328

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1062 CONTRACTS WITH 4438 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 3376 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 1062 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 1374 CONTRACTS.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3376 CONTRACTS) ACCOMPANYING THE GOOD SIZED LOSS IN COMEX OI (4438) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 1062 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 49.773 TONNES PLUS TODAY’S 1.723 TONNE OZ EX. FOR RISK//NEW STANDING 51.496 TONNES. / 3) ZERO LONG LIQUIDATION // 4) FAIR SIZED COMEX OPEN INTEREST LOSS/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 1374 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JAN.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN. :

TOTAL EFP CONTRACTS ISSUED: 93,804 CONTRACTS OR 9,380,400 OZ OR 291.76 TONNES IN 21 TRADING DAY(S) AND THUS AVERAGING: 4466 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 21 TRADING DAY(S) IN TONNES 291.76 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 291.76/3550 x 100% TONNES 8,19% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EX FOR PHYSICAL)

FEB’24:

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A STRONG SIZED 485 CONTRACTS OI TO 137,433 AND CLOSER TO THE COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 809 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MARCH 809 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 809 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 485 CONTRACTS AND ADD TO THE 809 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A FAIR SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 321 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 1.605 MILLION OZ

OCCURRED WITH OUR $.05 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED DOWN 41.98 PTS OR 1.48% //Hang Seng CLOSED DOWN 218.38 PTS OR 1.39% /The Nikkei CLOSED UP 220.85 OR 0.61% //Australia’s all ordinaries CLOSED UP 0.99% /Chinese yuan (ONSHORE) closed UP AT 7.1779 /OFFSHORE CHINESE YUAN CLOSED UP TO 7.1890 /Oil UP TO 77.01 dollars per barrel for WTI and BRENT DOWN AT 81.67/ Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE STRONGER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 4438 CONTRACTS TO 430,328 DESPITE OUR GAIN IN PRICE OF $6.50 WITH RESPECT TO TUESDAY TRADING.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF FEB..… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3376 EFP CONTRACTS WERE ISSUED: : APRIL 3376 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3376 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1062 CONTRACTS IN THAT 3376 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A GOOD SIZED LOSS OF 4438 COMEX CONTRACTS..AND THIS TINY SIZED LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR GAIN IN PRICE OF $6.50 TUESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A FAIR SIZED 1374 CONTRACTS. THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: FEB (22.706 TONNES) ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 51.496 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $6.50 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR LOSS OF 1062 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD A FAIR T.A.S. LIQUIDATION ON THE FRONT END OF TUESDAY’S TRADING . THE T.A.S. ISSUED ON TUESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS. WE ALSO EXPERIENCED CONSIDERABLE SPECULATOR SHORT COVERING AT HIGHER PRICES AS WELL AS FINAL LIQUIDATION OF OUR SPREADERS.

WE HAVE LOST A TOTAL OI OF 3.303 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR FEB. (49.773 TONNES) ON FIRST DAY NOTICE ALONG WITH ANOTHER STRANGE 554 CONTRACT EXCHANGE FOR RISK FOR 1.7235 TONNES. VERY UNUSUAL TO OBTAIN THIS ON OUR INITIAL FIRST DAY NOTICE. ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $6.50

WE HAD – REMOVED 1245 CONTRACT TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET LOSS ON THE TWO EXCHANGES 1062 CONTRACTS OR 106,200 OZ OR 3.303 TONNES.

Estimated gold volume today:// 189,183 poor

final gold volumes/yesterday 251,897 fair

//speculators have left the gold arena

JAN 31 INITIAL FEB GOLD

/ /// THE FEB 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 43,339.538 OZ Brinks Manfra . |

| Deposit to the Dealer Inventory in oz | 32,004.15 oz ASAHI |

| Deposits to the Customer Inventory, in oz | NIL oz |

| No of oz served (contracts) today | 3783 notice(s) 378,300 OZ 11.7667 TONNES |

| No of oz to be served (notices) | 12219 contracts 12,219 oz 38.006 TONNES |

| Total monthly oz gold served (contracts) so far this month | 378300 notices 378,300 oz 11.7667 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

1 dealer deposits:

i) Into ASAHI 32004,15 oz

total dealer deposits: 32,004.15 oz

total customer withdrawals: 2

i) Out of Brinks 41,796.290 oz (1300 kilobars)

ii) Out of Manfra: 1543.248 oz (48 kilobars)

total withdrawals 43,359.538 oz 1348 kilobars

we had 0 customer deposits

total customer deposits NIL oz

Adjustments; 3

a) dealer to customer JPMorgan: 123,263.795 oz

b) dealer to customer Malca: 482.265 oz

c) dealer to customer Manfra: 1253.889 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEB.

For the front month of FEBRUARY we have an oi of 16,002 contracts having LOST 14,282 contracts. Thus

by definition the initial amount of gold standing is as follows:

16,002 contracts x 100 oz per contract = 1,600,200 oz or 49.773 tonnes.

However for the first time ever, we received notice that we also had 554 notices filed under exchange for risk for a total of 55,400 oz or 1.723 tonnes.

Thus initial standing for gold for February is 49.773 tonnes + 1.723 tonnes = 51.494 tonnes which is pretty good.

March GAINED 345 contracts to stand at 2017.

APRIL GAINED 8929 CONTRACTS RISING TO 342,407.

We had 3783 contracts filed for today representing 378,300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 1547 notices were issued from their client or customer account. The total of all issuance by all participants equate to 3783 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1277 notice(s) was (were) stopped ( received) by J.P.Morgan//customer account and 0 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the FEB. /2024. contract month, we take the total number of notices filed so far for the month (3783 x 100 oz ), to which we add the difference between the open interest for the front month of FEB. (16,002 CONTRACTS) minus the number of notices served upon today 3783 x 100 oz per contract equals 1,600,200 OZ OR 49.773 TONNES + 1.723 Ex for Risk = 51.496 tonnes

thus the INITIAL standings for gold for the FEB. contract month: No of notices filed so far (3783) x 100 oz + (16,002) {OI for the front month} minus the number of notices served upon today (3783) x 100 oz) which equals 1,600,200 oz + 55,400 oz ex. for risk//total standing OR 51.494 TONNES

TOTAL COMEX GOLD STANDING FOR FEB: 51.494 TONNES WHICH IS GREAT FOR AN ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,350,186.829 41.99 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 19,576,936.516 OZ

TOTAL REGISTERED GOLD 9,034,198,687 (281,00 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,542,737.829 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 7,684012 oz (REG GOLD- PLEDGED GOLD) 239,00tonnes

END

SILVER/COMEX

JAN 31/INITIAL

//2024// THE FEB 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 915,626.280 oz CNT BRINKS MANRA . |

| Deposits to the Dealer Inventory | 606,851.75OZ asahi |

| Deposits to the Customer Inventory | 554,583.434 oz DELAWARE CNT |

| No of oz served today (contracts) | 547 CONTRACT(S) (2,735,000 OZ) |

| No of oz to be served (notices) | 160 contracts (800,000 oz) |

| Total monthly oz silver served (contracts) | 547 Contracts (2,735,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 1 dealer deposit

i) Into ASAHI: 606,851.75 oz

total dealer deposit: 606,851.75 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 deposits customer account:

i) Out of Delaware 3874.600 oz

ii) Out of CNT 550,788.834 oz

total customer deposits 554,583.434 oz

JPMorgan has a total silver weight: 130.806 million oz/275.229 million or 47.63%

adjustment: 4

a) dealer to customer Asahi 874,200.840 oz

b) customer to dealer

i) Brinks 34,910.550 oz

ii) CNT 605,981.450 oz

iii) Manfra 546,575.035 oz

Comex withdrawals: 3

i) Out of CNT 286,296.800 oz

ii) Out of Brinks 433,162,960 oz

iii) Out of Manfra; 196,166.528 oz

total withdrawal: 915,626.280 oz

TOTAL REGISTERED SILVER: 42.54 MILLION OZ//.TOTAL REG + ELIGIBLE. 275.229 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF FRB. /2023 OI: 707 CONTRACTS HAVING LOST 7 CONTRACT(S).

THUS BY DEFINITION, WE HAVE THE FOLLOWING INITIAL STANDING FOR SILVER AT THE COMEX:

707 NOTICES X 5000 OZ PER NOTICE = 3,535,000 OZ. HOWEVER FOR THE FIRST TIME FOR SILVER WE

RECEIVED NOTICE THAT WE HAVE AN ADDITIONAL 89 NOTICES SERVED UPON FOR EXCHANGE FOR RISK FOR A TOTAL OF 445,000 OZ.

THUS THE INITIAL SILVER STANDING FOR THIS NON ACTIVE MONTH OF FEB IS 3.535 MILLION OZ + .445 MILLION EX FOR RISK = 3.980 MILLION OZ.

WHEN YOU SEE EXCHANGE FOR RISK VERY EARLY, OBVIOUSLY THEY ARE HAVING DIFFICULTY FINDING NEEDED SILVER FOR THE DELIVERIES.

MARCH LOST 2706 CONTRACTS TO 97,275

APRIL SAW A GAIN OF 1425 CONTRACTS UP TO 25,202

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 547 for 2,735,000 oz

Comex volumes// est. volume today 55,645 good

Comex volume: confirmed yesterday 59,462 good

To calculate the number of silver ounces that will stand for delivery in FEB. we take the total number of notices filed for the month so far at 547 x 5,000 oz = 2,735,000 oz

to which we add the difference between the open interest for the front month of FEB. (707) and the number of notices served upon today 547 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB/2024 contract month: 707 (notices served so far) x 5000 oz + OI for the front month of FEB. (547) – number of notices served upon today (83 )x 500 oz of silver standing for the FEB contract month equates to 3.535 MILLION OZ. + .445 MILLION OZ EX. FOR RISK//NEW TOTAL 3.980 MILLION OZ

New total standing: 3.980 million oz.

There are 41.579 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

JAN 31/WITH GOLD UP $16.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 852.88 TONNES:

JAN 30/WITH GOLD UP $6.50 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 854.89 TONNES:

TOTAL IN LAST 18 DAYS WITHDRAWAL OF 14.12 TONNES

JAN 29/WITH GOLD UP $8.70 TODAYHUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.88 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 856.05 TONNES

JAN 26/WITH GOLD DOWN $0.10 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 25/WITH GOLD UP $2.50 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 24/WITH GOLD DOWN $9.75 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 23/WITH GOLD UP $3.95 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD/ //://INVENTORY RESTS AT 858.93 TONNES

JAN 22/WITH GOLD DOWN $6.00 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD/ //://INVENTORY RESTS AT 860.95 TONNES

JAN 19/WITH GOLD UP $8.15 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD //://INVENTORY RESTS AT 862.10 TONNES

JAN 18/WITH GOLD UP $14.85 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.30 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 862.10 TONNES

JAN 17/WITH GOLD DOWN $23.25 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .549 TONNES OF GOLD INTO THE GLD.;//://INVENTORY RESTS AT 864.40 TONNES

JAN 12/WITH GOLD UP $31.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A MASSIVE WITHDRAWAL OF 4.61 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 864.99 TONNES

JAN 11/WITH GOLD DOWN $7.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A MASSIVE WITHDRAWAL OF 4.61 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 864.99 TONNES

JAN 10/WITH GOLD DOWN $4.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 869.60 TONNES

JAN 9/WITH GOLD UP $0.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 869.60 TONNES

JAN 8/WITH GOLD DOWN $16.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 4.61 TONNES FROM THE GLD. INVENTORY RESTS AT 869.60 TONNES

JAN 5/WITH GOLD UP $0.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD:///. // INVENTORY RESTS AT 874.21 TONNES

JAN 4/WITH GOLD UP $7.60 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD:///. // INVENTORY RESTS AT 874.21 TONNES

JAN 3/WITH GOLD DOWN $29.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.90 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 874.21 TONNES

JAN 2/WITH GOLD UP $1.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 879.11 TONNES

DEC 29/WITH GOLD DOWN $10.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.16 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 880.55 TONNES

DEC 28/WITH GOLD DOWN $8.35 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.45 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 881.71 TONNES

DEC 27/WITH GOLD UP $23.25 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.01 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 880.26 TONNES

DEC 26/WITH GOLD UP $1.25 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD:/. // INVENTORY RESTS AT 878.25 TONNES

DEC 22/WITH GOLD UP $17,85 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD:/. // INVENTORY RESTS AT 878.25 TONNES

DEC 21/WITH GOLD UP $5.10 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT .58 TONNES OF 2.02 TONNES OF GOLD INTO THE GLD//. // INVENTORY RESTS AT 878.25 TONNES

DEC 20/WITH GOLD DOWN $3.60 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD//. // INVENTORY RESTS AT 877.67 TONNES

GLD INVENTORY: 852.88 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JAN 31/WITH SILVER DOWN 8 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7438 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 440.137 MILLION OZ//LAST 5 DAYS: 9.1118 MILLION OZ WITHDRAWAL

JAN 30/WITH SILVER DOWN 5 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.876 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 442.699 MILLION OZ//LAST 4 DAYS: 7.368 MILLION OZ WITHDRAWAL

JAN 29/WITH SILVER UP $.37 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.105 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 444.575 MILLION OZ

JAN 26/WITH SILVER DOWN $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.556 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 446.680 MILLION OZ

JAN 25/WITH SILVER UP $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.831 MILLION OZ INTO THE SLV(FAIRY TALES) // /

INVENTORY RESTS AT 448.236 MILLION OZ

JAN 24/WITH SILVER UP $0.44 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER DEPOSIT OF 1.375 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 450.067 MILLION OZ

JAN 23/WITH SILVER UP $0.21 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 16.201 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 448.694 MILLION OZ

JAN 22/WITH SILVER DOWN $0.45 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 19/WITH SILVER DOWN $0.11 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 18/WITH SILVER UP $0.13 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 432.951 MILLION OZ

JAN 17/WITH SILVER DOWN $0.38 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 779,000 OZ FROM THE SLV.: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 16/WITH SILVER DOWN $0.08 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 12/WITH SILVER UP $0.62 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 11/WITH SILVER DOWN 34 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.912 MILLION OZ

JAN 10/WITH SILVER DOWN 3 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 450,000 OZ FROM THE SLV// //INVENTORY RESTS AT 433.912 MILLION OZ

JAN 9/WITH SILVER DOWN 20 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV //INVENTORY RESTS AT 434.370 MILLION OZ

JAN 8/WITH SILVER DOWN 8 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1,602,000 OZ INTO THE SLV//:././/////INVENTORY RESTS AT 434.370 MILLION OZ

JAN 5/WITH SILVER UP 20 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 916,000 OZ INTO THE SLV//:././/////INVENTORY RESTS AT 435.972 MILLION OZ

JAN 4/WITH SILVER UP 5 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV/:././/////INVENTORY RESTS AT 435.056 MILLION OZ

JAN 3/WITH SILVER DOWN 78 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWALOF 2.294 MILLION OZ OZ FROM THE SLV././/////INVENTORY RESTS AT 435.056 MILLION OZ

JAN 2/WITH SILVER DOWN 9 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWALOF 915,000 OZ FORM THE SLV././/////INVENTORY RESTS AT 437.35 MILLION OZ

DEC 29/WITH SILVER DOWN 29 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV/: //////INVENTORY RESTS AT 438.265 MILLION OZ

DEC 28/WITH SILVER DOWN 25 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV/: //////INVENTORY RESTS AT 438.265 MILLION OZ

DEC 27/WITH SILVER UP 20 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 1.374 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 438.265 MILLION OZ

THIS IS THE 3RD STRAIGHT DAY THAT THE SLV HAS ENGAGED IN WITHDRAWALS

DEC 26/WITH SILVER DOWN 14 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 1.465 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 439.639 MILLION OZ

DEC 22/WITH SILVER UP 0 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 2.289 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 441.104 MILLION OZ

DEC 21/WITH SILVER DOWN 2 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV/: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 443.393 MILLION OZ

DEC 20/WITH SILVER UP 28 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV/: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 443.393 MILLION OZ

CLOSING INVENTORY 440.137 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

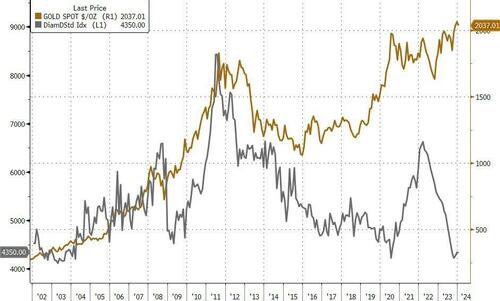

The Value Of Diamonds Sinks As Gold Stays Strong

WEDNESDAY, JAN 31, 2024 – 07:20 AM

Valentine’s Day is here and you might find yourself buying (or wishing you had remembered to buy) a Valentine’s Day present. A classic romantic present involves gold, diamonds, and sometimes both. And both diamonds and gold seem at first blush to have a lot in common.

Both are or at least can be beautiful. Diamonds are one of the shiniest gemstones (high refractive index if you’re science-minded) and can be perfectly clear or come in a wide range of colors. Gold is of course famously appealing to look at. Both diamonds and gold convey luxury and wealth, and both are regularly used to make luxury products such as rings, bracelets, watches, and earrings.

The expense of both diamonds and gold is one reason why it’s so common for both diamonds and gold to be part of an engagement ring- the expense of these materials makes engagement rings expensive which helps them serve as a costly sign of commitment.

Some have argued that the similarities between diamonds and gold are even greater, given that some are turning to diamonds as a store of value and as an investment. But this overlooks why gold has historically been preferred as a store of value to diamonds, and how new technological developments have made the differences between diamond and gold even greater.

First, diamonds lack the history of gold. While gold has spontaneously emerged as a treasured metal and as a store of value or as a currency from civilization to civilization, the emergence of diamonds as a valuable commodity is much more recent and historically contingent. While diamonds were always recognized as gemstones, broad-based demand for diamonds did not emerge in the West until the 1800s and their famous role as the central stone in an engagement ring did not emerge until the mid 1900’s due to savvy marketing campaigns.

So demand for gold is more stable and organic than the demand for diamonds. When central banks look to preserve the value of their currency, they often increase strategic gold reserves, not strategic diamond reserves.

While diamonds and gold might be seen as similar because both have industrial uses as well as usage in jewelry and investment, that overlooks the fact almost all gold is used for jewelry or as an investment while 80% of diamonds are used by industry. While every single ounce of gold could be used in industry, jewelry, or as an investment, because gold is fungible and divisible, the opposite is true for diamonds. Diamond value varies dramatically between individual stones. The value of a diamond depends on its size, its color, its clarity, and its cut. Many diamonds are worthless for any non-industrial purposes. While gold can be used as bullion converted to jewelry then melted back into bullion, cutting a diamond over and over would destroy its value. Demand for gold is driven by every sector. Demand for small industrial diamonds is not driven by demand for large diamonds that could feature in jewelry, and vice versa.

Both gold and (gemstone quality) diamonds are valuable because of their relative rarity compared to demand. Gold is rare because the element, gold, is genuinely rare. Diamonds have been rare, because while they are made of carbon, a common element, the specific arrangement of carbon atoms that make up a diamond is rarely produced in nature, at least not in the form of large diamonds.

But advances in technology have changed that. It is now much cheaper to buy a lab-grown diamond for an engagement ring than to buy a diamond mined out of the earth. And these lab-grown diamonds are not stones that happen to resemble diamonds such as cubic zirconia, they are genuine diamonds created in a lab. Advances in technology have driven down the prices of both lab-grown and naturally mined diamonds. The value of lab-grown diamonds is down by over 70% since the start of 2016 and even natural mined diamonds have fallen by over 25%. It is unlikely that technological improvements in creating lab-grown diamonds will stop improving meaning lab-grown diamonds will be able to supply diamonds to both the industrial market and the jewelry market.

If you think diamonds are prettier than gold, I wouldn’t argue. But I know which one I would rather have as part of my investment portfolio.

END

Four States Consider Lifting Taxes On Precious Metals

WEDNESDAY, JAN 31, 2024 – 03:45 PM

Citizens of Georgia, Kentucky, Wisconsin, and Kansas may soon enjoy lower taxes on precious metals if recently introduced pro-metal bills are made law in 2024.

Earlier this month, all four states introduced or reintroduced bills that would exempt precious metals from either state sales tax (in Kentucky and Wisconsin) or state income tax (in Georgia and Kansas).

Kentucky lawmakers will vote on House Bill 101 and Senate Bill 105 in this year’s legislative session. If passed, the bills would end state sales tax on gold, silver, platinum, and palladium bullion starting in August of this year. Wisconsin’s Assembly Bill 29 and Senate Bill 33 would both enact similar provisions while also lifting sales tax on the purchase of copper bullion.

Proponents of these bills point out that gold and silver are one of the only asset classes that have sales taxes; investors don’t have to pay sales tax on more common investments, like stocks and bonds. The Sound Money Defense League recently elaborated on this point:

“Sales taxes are typically levied on final consumer goods. Computers, shirts, and shoes carry sales taxes because the consumer is ‘consuming’ the good. Precious metals are inherently held for resale, not ‘consumption,’ making the imposition of sales taxes on precious metals illogical from the start.”

Both Kansas and Georgia eliminated sales taxes on bullion in the past and are now taking the next logical step in facilitating the use of sound money. House Bill 895 in Georgia and House Bill 2405 and Senate Bill 303 in Kansas would lift state capital gains taxes on precious metals, leaving only the federal capital gains tax on income earned from holding gold or silver.

Kansas’ two bills also explicitly reaffirm that gold and silver are legal tender in the state and ensure physical metal can be used voluntarily as currency, establishing a relatively free market in money:

“The purchase, sale or exchange of any type or form of specie shall not give rise to any tax liability of any kind… Unless expressly provided by statute or by contract, no person shall have the right to compel any other person to tender specie or to accept specie as tender.”

Many argue income tax on precious metals constitutes a second tax on top of inflation. As Peter Schiff says, “Printing money is merely taxation in another form.” This implicit inflation tax affects everyone’s cash holdings, whether they invest in precious metals or not. Depending on where they live, anyone who earns a nominal capital gain on gold and silver can incur a second, explicit tax liability, even if their gain is only nominal.

By considering these bills, these states join the long and growing list of jurisdictions in the United States that offer some sort of tax relief for precious metals. Missouri and Oklahoma, for example, filed bills last month that would also exempt precious metals from state income tax. Oklahoma and Florida went a step further and also considered bills that would establish bullion depositories in each state, which would promote sound monetary policy at the state level.

It’s no surprise that more states are taking steps to protect their citizens from wealth-destroying monetary policy carried out by the Federal Reserve. The recent stretch of high inflation serves as a stark reminder of the centrality of money in advanced economies. When the value of money is eroded by inflationary spending and out-of-control public debt, ordinary people pay the price. Thankfully, as state laws reduce the costs of investing in precious metals, holding physical gold and silver increasingly provides a hedge against this hidden tax.

Should the bills in Kansas, Kentucky, Georgia, and Wisconsin be enacted, state lawmakers will have offered their citizens a more secure financial future.

END

2) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

MATHEW PIEPENBURG

END

3. CHRIS POWELL//GATA GOLD COMMENTARIES:

4. OTHER GOLD/SILVER //COMMENTARIES//

Global Silver Demand Forecasted to Rise to 1.2 Billion Ounces in 2024 |

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES /

END

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

end

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP 7.1779

OFFSHORE YUAN: UP TO 7.1890

SHANGHAI CLOSED DOWN 41.98 PTS OR 1.48%

HANG SENG CLOSED DOWN 218.38 PTS OR 1.39%

2. Nikkei closed UP 220.85 PTS OR 0.61%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 103.36 EURO FALLS TO 1.0836 DOWN 7 BASIS PTS

3b Japan 10 YR bond yield:RISES TO. +.726 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.83/JAPANESE YEN NOW RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP// OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.2385***/Italian 10 Yr bond yield UP to 3.786** /SPAIN 10 YR BOND YIELD UP TO 3.157…**

3i Greek 10 year bond yield UP TO 3.242

3j Gold at $2039.00 silver at: 23.12 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 1 /100 roubles/dollar; ROUBLE AT 89.72//

3m oil into the 77 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147,83// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.726% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8635 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9357 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

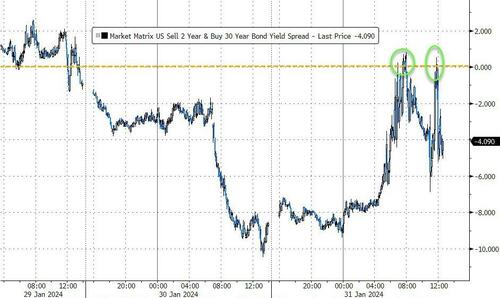

USA 10 YR BOND YIELD: 4.036 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.252 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.322 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 30.36…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 4 BASIS PTS AT 3.9239

end

2.a Overnight: Newsquawk and Zero hedge

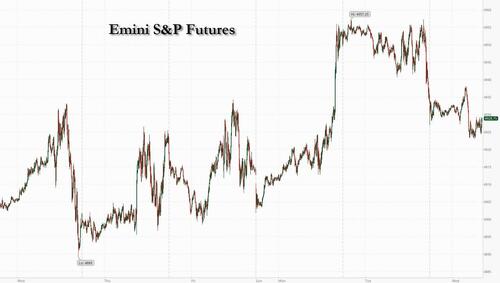

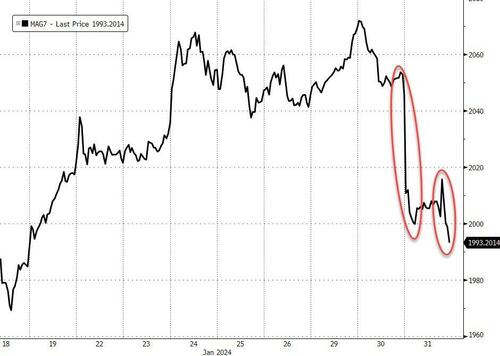

Futures Slide Dragged by Tech Giants Ahead Of Fed Decision

WEDNESDAY, JAN 31, 2024 – 08:16 AM

US equity futures slumped after earnings from tech giants GOOGL, MSFT and AMD fell short of Wall Street’s lofty expectations and as investors prepared for the first interest-rate decision of the year from the Fed (full preview here).

As of 7:45am ET, contracts on the Nasdaq 100 slid 1.1%, while those on the S&P 500 retreated 0.5% with Microsoft, Alphabet and Advanced Micro Devices all sliding in premarket after their updates failed to match the market hype around tech megacaps and artificial intelligence that has helped drive the recent record-setting rally in US stocks. The balance of MegaCaps are also lower as we await the Fed. Bond yields are modestly lower as part of a bull steepening; the US dollar is stronger despite consensus expecting more dovish signaling from Powell, and commodities are mixed. JPM asks if with Russell futs positive, will we see the pain trade (+Value/-Growth with MegaCap underperformance) come to fruition near-term? The macro data focus is on ADP, ECI (Fed’s preferred measure of wage inflation), Chicago PMIs, Trsy Refunding Announcement, and then Fed meeting later today.

As noted above, the biggest premarket movers were the tech giants as Microsoft, Alphabet and chipmaker Advanced Micro Devices all fell short of the bonanza required to satisfy. Microsoft’s revenue growth was the strongest since 2022 and AI products helped with that, but there were hopes for even more given the run in its shares in recent weeks that took its market value over $3 trillion. Alphabet, meanwhile, was hit by a miss in its core Google search advertising business, and AMD’s lackluster outlook overshadowed its AI chip prospects. All three are lower in premarket trading. In other individual stock moves, Paramount Global soared 21% after Bloomberg reported that media mogul Byron Allen made a $14.3 billion offer for the company. Tesla fell as much as 3.4% after Elon Musk’s $55 billion pay package at the electric automaker was struck down by a Delaware judge. Here are all the notable premarket movers:

- Advanced Micro Devices slips 5% after the chipmaker gave a revenue forecast that was weaker than expected.

- Alphabet falls 5.6% reporting fourth-quarter revenue from its core search advertising business that fell short of analysts’ estimates.

- Boston Scientific jumps 3% after the company reported adjusted earnings per share for the fourth quarter that beat the average analyst estimate.

- Mondelez falls 4% after the maker of Oreo cookies issued weaker-than-expected guidance for full-year organic net revenue growth.

- Paramount Global soars 17% after Bloomberg reported that media mogul Byron Allen has made a $14.3 billion offer to buy all of the outstanding shares of the company.

- Rockwell Automation slides 7.9% after reporting first-quarter sales and adjusted earnings per share that trailed the average analyst estimates.

- SoFi Technologies slips 3% as Morgan Stanley issued a downgrade, flagging near-term revenue headwinds.

- Starbucks gains 3% as management maintained confidence in the company’s 2024 profit goal, predicting that greater efficiency, new stores and a core of loyal customers will offset a dip in revenue growth.

- Stryker climbs 5% after the medical-device manufacturer forecast for 2024 that beat the average analyst estimate.

- Tesla shares fall 2.6% after top boss Elon Musk’s $55 billion pay package at the electric automaker was struck down by a Delaware judge.

Attention now turns later to the Fed, with the Federal Open Market Committee poised to keep rates unchanged but indicated no more tightening bias (see our preview here). The rate decision and accompanying statement will be released at 2 p.m. in Washington, with Chair Jerome Powell holding a press conference 30 minutes later. Traders see a roughly 40% chance the central bank will lower rates for the first time in March, but most Fed officials have said it’s too soon to speculate on such a pivot. While Powell may say that recent declines in inflation are encouraging, he may still show little urgency to ease, given resilience in the labor market and growth in the economy.

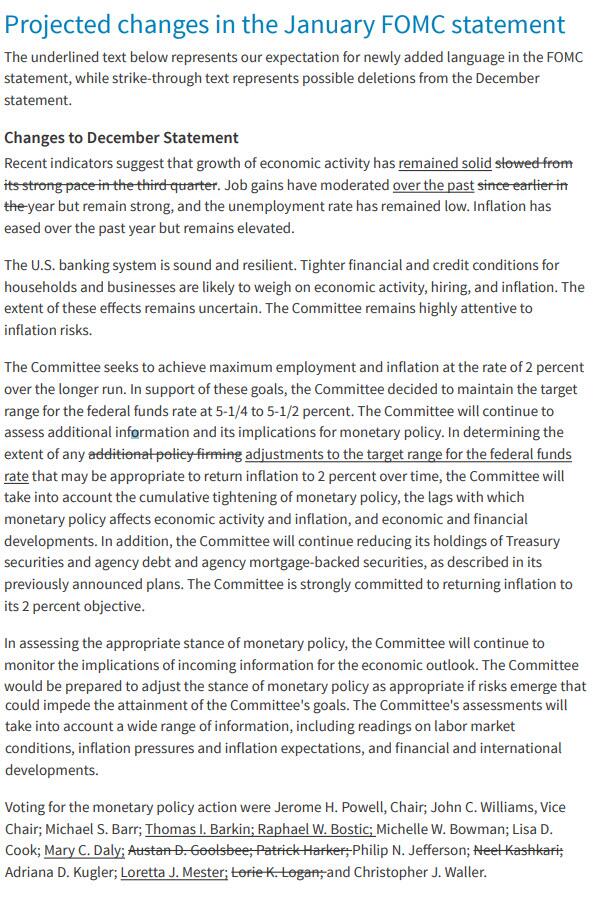

“Even if it’s not our scenario, we expect the Fed to keep the door open for a possible rate cut in March, without sending a firm and definitive signal,” said Alexandre Hezez, chief investment officer at Group Richelieu in Paris. A proposed redline statement from Barclays is shown below.

While we have more US megacap earnings after the close today and tomorrow, it’s a busy day of earnings in Europe too: Novo Nordisk A/S became only the second European company to reach a market value of $500 billion after it said sales and profit will surge again this year thanks to its blockbuster obesity shot Wegovy. Shares in Hennes & Mauritz AB plunged as much as 11% after the retailer missed profit estimates and its chief executive officer stepped down. Europe’s Stoxx 600 index edged higher with the insurance and real estate sectors rising most, while retailers fall after fast fashion giant H&M reported poor 4Q results. Here are the biggest European movers:

- Novo Nordisk climbs as much as 4.1%, taking the Danish drugmaker’s market value to $500 billion for the first time after announcing fresh guidance for 2024 and strong 4Q results

- Beijer Ref gains as much as 11% after the Swedish industrial ventilation firm reported 4Q earnings that Jefferies say were solid, with upbeat outlook commentary the key positive

- Wartsila rises as much as 7.2% to hit its highest level in four-and-a-half years after the company, which serves the marine and energy markets, said it expects demand to improve in 2024

- SEB shares jump as much as 7.9%, the most since October, after the French appliances maker forecast a full-year operating result of more than 15%, compared the previous 10% prediction

- Borregaard climbs as much as 9.4% to highest since June after Norwegian supplier of specialized biochemicals posted fourth-quarter Ebitda that Carnegie said showed strong results

- KPN climbs after raising FY free cash flow guidance and beating analyst estimates on the metric for 4Q. Service revenue growth was seen as steady, hinting at a healthy Dutch market

- Hennes & Mauritz drops as much as 10% after the clothing retailer reported 4Q operating profit that missed estimates; Bernstein says results showed weakness across the board

- Novartis shares fall as much as 5.3%, most since March 2022, after the Swiss pharma giant’s sales came in lower than analysts’ expectations, with key drugs missing estimates

- Raiffeisen Bank bank drops as much as 8.4% after fourth quarter net income missed expectations as the lender continued to reduce the volume of customer loans in Russia

- Vodafone shares drop as much as 4.1%, the most in two months, after its talks with Iliad to merge Italian operations fell through. Vodafone said it’s still in discussions with other bidders

Earlier in the session, in Asia, Japanese bond yields rose as a summary of the Bank of Japan’s meeting signaled it’s getting closer to raising its interest rate for the first time since 2007. Japanese stocks also gained, as signs that the BOJ may move to end negative rates boosted optimism over lenders’ profitability. Stocks in China and Hong Kong extended losses after data showed another month of contraction in China’s factory activity. Mainland shares wiped out all the gains spurred by hopes of stronger support measures by the authorities.

On the monetary policy front in Europe, data out Wednesday showed cooling price pressures in France, adding to optimism that the ECB may begin trimming rates as soon as April. The 10-year yield on German debt dropped as much as eight basis points, while the euro weakened. Meanwhile, the dollar strengthened against most of its Group-of-10 peers, while Treasury yields were slightly richer on the day, with futures off highs reached after steep gains for Australian bonds on domestic inflation data and gains for bunds during London morning on retail sales data. US session features ADP employment, quarterly refunding announcement and Fed rate decision. US yields remain within 1bp-2bp of Tuesday’s closing levels, off session lows; 10-year around 4.03% after briefly dropping below 4% during London morning; bunds outperform by 2.5bp in the 10-year sector, gilts by 1.5bp. Dollar issuance slate light so far; just one deal priced Tuesday, and muted activity is expected Wednesday ahead of Fed rate announcement; dealers are calling for around $150b of new supply in February. At 8:30am US Treasury is slated to announce sizes of note and bond auctions during the February-to-April quarter.

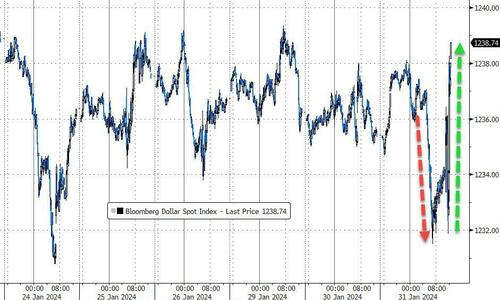

In FX, the Bloomberg Dollar Spot Index rose 0.1%, reversing three sessions of losses, as traders braced for the Federal Reserve to avoid signaling an imminent rate cut; Treasury yields fell 1-2bps across the curve.

- USD/JPY traded 0.1% higher at 147.78 after dropping 0.3% to 147.19; A summary of the BOJ’s meeting signaled the central bank is moving closer to raising rates.

- AUD/USD fell as much as 0.7% to 0.6559, the lowest level in a week, as Australian inflation eased more than expecting boosting bets on a pivot to rate cuts.

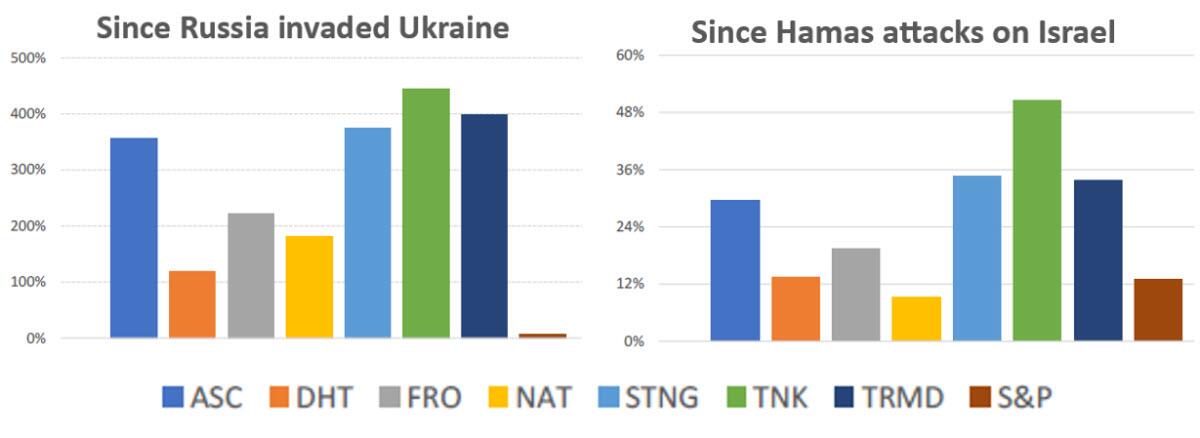

- EUR/USD dropped as much as 0.4% to 1.0806 before paring losses after French inflation dropped to its lowest level since before Russia invaded Ukraine; German unemployment unexpectedly decreased in January pointing to labor market resilience.

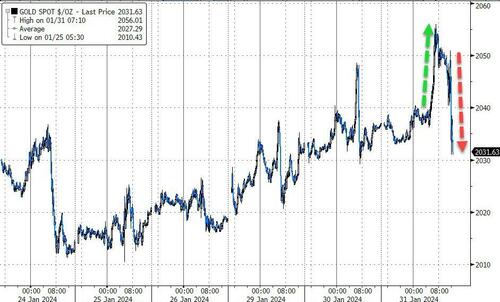

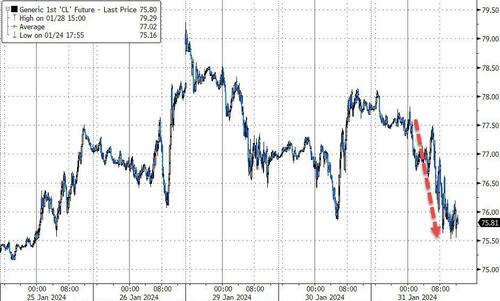

In commodities, oil headed for its first monthly gain since September as an escalation of attacks on ships in the Red Sea spurred a diversion of tanker traffic and raised fears about a wider conflict in the Middle East. On Wednesday, WTI fell 1.3% to trade near $76.80. Gold was flat, trading around $2,037.

To the day ahead now, and the main highlights will be the Federal Reserve’s policy decision and Chair Powell’s subsequent press conference, along with the quarterly refunding announcement from the US Treasury. On the data side, we’ll get the flash CPI releases for January from Germany and France, and in the US, there’s the ADP’s report of private payrolls for January and the Q4 Employment Cost Index. Finally, earnings releases include Boeing and Mastercard.

Market Snapshot

- S&P 500 futures down 0.5% to 4,925.25

- MXAP up 0.2% to 165.91

- MXAPJ down 0.4% to 502.98

- Nikkei up 0.6% to 36,286.71

- Topix up 1.0% to 2,551.10

- Hang Seng Index down 1.4% to 15,485.07

- Shanghai Composite down 1.5% to 2,788.55

- Sensex up 0.8% to 71,701.22

- Australia S&P/ASX 200 up 1.1% to 7,680.72

- Kospi little changed at 2,497.09

- STOXX Europe 600 little changed at 486.07

- German 10Y yield little changed at 2.21%

- Euro little changed at $1.0835

- Brent Futures down 1.0% to $82.04/bbl

- Gold spot up 0.1% to $2,039.51

- U.S. Dollar Index little changed at 103.47

Top Overnight News

- Australia’s CPI for Q4 undershoots the Street consensus at +4.1% Y/Y (vs. the Street’s +4.3% forecast). RTRS

- China’s NBS PMIs are mixed for Jan, with manufacturing coming in at 49.2 (up from 49 in Dec, but below the Street’s 49.3 forecast) and non-manufacturing at 50.7 (up from 50.4 in Dec and above the Street’s 50.6 forecast). WSJ

- A BOJ rate hike is getting closer, according to the summary of opinions from last week’s meeting. One member said there’s a “golden opportunity” to end negative rates before a Fed and ECB pivot. The yen rose and JGBs edged lower. BBG

- France’s CPI cools by more than anticipated in Jan, coming in +3.1% Y/Y (down from +3.7% in Dec and below the Street’s +3.3% forecast). BBG

- Iran signaled it’s prepared to hit back against any US strike on its soil or assets abroad, as the White House readies a response to a drone attack that killed three American soldiers over the weekend. BBG

- Paramount soared about 15% premarket after Byron Allen was said to have offered $14.3 billion for all of the outstanding shares. His plan is to sell the film studio, real estate and some intellectual property, while keeping the TV channels including the Paramount+ streaming service. He’s said to have banks and other investors lined up. BBG

- January FOMC Preview: Keeping a March Cut on the Table (Mericle): FOMC will likely aim to keep a March cut on the table without sending a decisive signal by removing the outdated hiking bias from its statement and noting that future policy changes will depend on upcoming inflation and other data. We continue to expect the FOMC to deliver a first cut in March and 5 cuts in total in 2024. The main reason is that progress on inflation has already surpassed the threshold the FOMC has given. GIR

- GOOGL -4% .. Solid topline, miss on headline OI (search OI beat though) ….Total Revs $86.31 (+13% y/ cc) vs cons $85.34bn .. Search $48.02bn (+13% y/y) vs cons $48.1bn … YouTube $9.2bn (+15.5% y/y) vs cons $9.2bn … Google Cloud $9.19bn vs cons $8.94bn. Total Op Income $23.68bn vs cons $23.8bn … Google Services OI $26.73bn vs cons $25.78bn … Google Cloud OI $864mn vs cons $357mn. EPS $1.64 vs cons $1.59. Employees up small q/q to 182,502(+121 q/q). GS GBM

- Heading into January month-end, the Goldman desk’s model estimates $10 billion of US equities to sell from US pensions given the moves in equities and bonds over the month. Note, we saw one trigger event on Jan 10th in which $12bn of US equities were sold, bringing aggregate selling in January to -$22bn by month-end. GS GBM

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly subdued amid a deluge of earnings releases and key data releases at month-end. ASX 200 shrugged off early weakness and printed record highs as yields fell after softer-than-expected inflation. Nikkei 225 initially retreated following disappointing Industrial Production and Retail Sales data, while hawkish-leaning comments from the BoJ Summary of Opinions also provided a headwind for stocks. However, the index then gradually recovered all of its losses. KOSPI was subdued after results from Samsung Electronics which topped estimates but its profits declined. Hang Seng and Shanghai Comp underperformed following the latest Chinese PMI data in which Manufacturing PMI matched estimates and remained in contraction territory for a 4th consecutive month.

Top Asian News

- BoJ Summary of Opinions from the January meeting stated a member said that the BoJ must patiently maintain monetary easing under YCC, while the positive wage-inflation spiral must strengthen further and wage growth must exceed 2% to reach the price target. A member said the prerequisite for policy change including ending negative rates, appears to be falling into place given improvements in the economy and prices, while a member said they are now likely at a phase where they need to confirm through specific data the likelihood of achieving 2% inflation. Furthermore, a member said there is a strong chance they can judge that policy normalisation is possible once they can confirm the impact of the quake on the economy in the coming 1-2 months, while a member stated they must deepen the exit debate as the likelihood of achieving the price target has heightened and it was also stated that BoJ could be forced to sharply tighten monetary policy if its decision to end the negative rate comes too late.

- Chinese President Xi promised US President Biden that China wouldn’t interfere in the 2024 US presidential election, when they met last November, which China’s Foreign Minister reiterated to the US National Security Adviser over the weekend, according to CNN.

- IMF senior official said Chinese authorities need to give a consistent and clear set of messages to address property sector woes and need to separate viable from non-viable while protecting homebuyers, while the official added that going forward, they would prefer if there were more policy rate cuts than bank reserve cuts in China.

- China’s major state-owned banks seen selling dollars in onshore foreign exchange market on Wednesday, according to Reuters sources

- Joint Saudi-Kuwaiti statement: Acknowledges the close cooperation between the two sides in the field of energy, and acknowledges the successful efforts of the OPEC+ countries in enhancing the stability of global oil markets, according to Asharq News.

- Saudi Arabia’s decision on capacity was reportedly at least six months in the making based on uncertainty around the need for additional spare capacity, according to industry sources cited by Reuters.

- United Microelectronics Corporation (2303 TT) Q4 (TWD): Consolidated revenue 54.96bln (prev. 67.84bln Y/Y). Gross margin 32.4% (prev. 42.9% Y/Y). “We anticipate overall wafer demand will increase mildly, however, customers maintain a cautious approach”

European bourses are generally lower, with clear underperformance in the SMI, post-Novartis earnings. European sectors hold a positive tilt; Retail lags hampered by losses in H&M (-8.8%) post-earnings; Insurance tops the pile. US equity futures (ES -0.5%, NQ -1.3%, RTY +0.4%) is on a mixed footing; with clear underperformance in the tech-heavy NQ following after-hours earnings from MSFT (-1.5%), GOOG (-5.5%) and AMD (-6.6%), detailed below. Click here and here for the sessions European pre-market equity newsflow, including earnings from Novartis, Novo Nordisk, GSK & more.

Top European News

- The Times shadow MPC voted 8-1 in favour of keeping the base rate unchanged at 5.25% with the lone dissenter voting for a 25bps hike, while it said the BoE should avoid signalling to investors where it intends to shift monetary policy over the coming months.

- UK Chancellor Hunt has reportedly warned his cabinet that tax cuts in the Spring budget could be smaller than expected amid “major structural weaknesses” in the UK economy, according to The Times. Hunt reportedly said there is likely to be less headroom for tax cuts than in the Autumn statement.

- Hapag-Lloyd (HLAG GY) CEO says freight rates are rising in Q1 2024 vs Q4 2023; better profit prospects for current quarter; “We do not believe the Red Sea crisis will be over soon, will probably take months”

Earnings

- Alphabet Inc (GOOGL) – Q4 2023 (USD): EPS 1.64 (exp. 1.59), Revenue 86.31bln (exp. 85.33bln). Google advertising revenue USD 65.52bln (exp. 65.8bln). YouTube ads revenue USD 9.20bln (exp. 9.16bln). Google Services revenue USD 76.31bln (exp. 75.97bln). Google Cloud revenue USD 9.19bln (exp. 8.95bln). Other Bets revenue USD 657mln (exp. 298.6mln). Co. is taking action to optimise global office space. Executive says Co. saw ad strength in retail, while CFO says search remained the biggest contributor to revenue growth and operating cost increase primarily reflected by growing R&D expenses. (Newswires) Shares -5.5% pre-market

- Advanced Micro Devices Inc (AMD) – Q4 2023 (USD): Adj. EPS 0.77 (exp. 0.77), Revenue 6.17bln (exp. 6.12bln). Data centre revenue USD 2.28bln (exp. 2.3bln).Gaming revenue USD 1.37bln (exp. 1.25bln). Client revenue USD 1.46bln (exp. 1.51bln). Embedded revenue USD 1.06bln (exp. 1.06bln). Sees Q1 rev. USD of approximately USD 5.4bln +/- USD 300mln (exp. 5.77bln). Sees Q1 adj. gross margin about 52% (exp. 51.8%). (Newswires) Shares -6.7% pre-market

- Microsoft Corp (MSFT) – Q2 2024 (USD): EPS 2.93 (exp. 2.78), Revenue 62.02bln (exp. 61.1bln). Cloud revenue 33.7bln (exp. 32.31bln). Revenue breakdown (USD): Intelligent Cloud revenue 25.88bln (exp. 25.29bln). Productivity and Business Processes revenue 19.25bln (exp. 19.03bln). More Personal Computing revenue 16.89bln (exp. 16.8bln). Other metrics: (USD) Capital expenditure 9.74bln. Operating income 27.03bln. Says 6 points of Azure revenue growth is attributable to AI, up from 3 points growth in the prior quarter, via co. exec in an interview. Office Commercial paid seats rose to 400mln from 382mln in Q3 23. CEO says now 53,000 Azure AI customers and one-third were new to Azure in the past 12 months, adds over half of Fortune 500 companies use Azure’s OpenAI AI services, seeing an increase in billion-dollar-plus Azure commitments. Q3 Guidance (via earnings call). Sees Q3 rev. USD 60bln-61bln (exp. 60.86bln) .Sees Productivity and Business Processes rev. 19.3bln-19.6bln (exp. 19.5bln).Sees Intelligent Cloud rev. 26.0bln-26.3bln (exp. 25.9bln). Sees More Personal Computing rev. 14.7bln-15.1bln (exp. 15.4bln). Sees Operating Expenses 15.8bln-15.9bln (exp. 16.5bln).Sees COGS 18.6bln-18.8bln (exp. 19.5bln)Shares -1.3% pre-market

- Novo Nordisk (NOVOB DC) – FY (DKK): Revenue 232.26bln (exp. 229.24bln), EPS 18.62 (exp. 18.32). New share buyback programme of up to DKK 20bln. The outlook reflects the gradual roll-out of Wegovy with capped volumes in international operations. Started increasing lower strength Wegovy within the US during January. Sees continued periodic supply constraints and related drug shortage notifications across a number of products and geographies. Q4: Wegovy Sales 9.62bln (prev. 2.45bln). Revenue 65.86bln (exp. 62.27bln). EBIT 26.7bln (exp. 24.9bln). FY24 Guidance: Sales: 18-26% (exp. 23.3%). Capex 45bln. adj. FCF 64-74bln. Co. has around a 2.8% weighting in the Stoxx Europe 600 (the largest in the index). Shares +1.1% in European trade

- Novartis (NOVN SW) – Q4 (USD): Revenue 11.4bln (exp. 11.7bln), Core EPS 1.53 (exp. 1.67), Core Net Income 3.12bln (exp. 3.34bln), Operating Income 3.8bln. FY23 dividend 3.30/shr, +3.1% (exp. 3.60). Net sales growth was driven primarily by strong performance for Entresto +31%, Kesimpta +99%, Kisqali +75%, Pluvicto +261% & Semblix +179%. Expect sales growth of 5% per annum until 2028, core operating margin at circa. 40% by 2027. (Newswires) Co. has around a 2% weighting in the Stoxx Europe 600 & and around a 16% weight in the SMI. Shares -3.5% in European trade

- GSK (GSK LN) – FY (GBP): Sales 30.33bln (exp. 29.81bln), adj. EPS 1.55 (exp. 1.52), adj. Operating Profit 8.78bln (exp. 8.77bln), Dividend 0.58/shr (exp. 0.57/shr). FY (continued): Shingrix sales 3.4bln, +17% (exp. increase mid-teen %) Arexvy sales 1.2bln (exp. 0.9-1.0bln). Vaccine sales +25% (exp. around 20%). adj. Speciality Medicine sales +15% (exp. increase low double-digit). Q4: adj. EPS 0.289 (exp. 0.299). Revenue 8.05bln (exp. 7.29bln). FY24 Guidance Dividend 0.60/shr (exp. 0.61/shr). Adverse impact of lower COVID-19 sales seen at 1pp of growth in sales. Commentary/CEO: 2031 sales outlook increased to over 38bln (upgraded). 2021-2026 outlook increased to sales more than +7% CAGR and Adjusted operating profit more than +11% CAGR. 2028-2030 is expected to see stable operating margins; given the likely loss of exclusivity for Dolutegravir during the period within the EU & US. Planning for at least 12 major launches from 2025. Strong pipeline progress, with 4 major product approvals: Arexvy RSV vaccine; Apretude for HIV prevention; Ojjaara for myelofibrosis and Jemperli in 1L endometrial cancer. (Newswires) Shares -0.9% in European trade

FX

- The Dollar Index is marginally firmer but once again finds itself pivoting around the 103.50 mark as has been the case in recent sessions. For now it is contained within yesterday’s 103.31-82 range with impetus expected from the FOMC.

- The EUR is a touch softer vs. the USD as the single-currency digests a soft French CPI and hawkishly-viewed German State CPI; EUR/USD is holding onto a 1.08 handle but a breach would see the YTD low at 1.0769 come into view.

- JPY is the marginal outperformer vs. the USD; still contained within yesterday’s 147.10-92 range with techs highlighting 10DMA at 147.86 and 100DMA at 147.47.

- AUD is the laggard within the antipodes as soft CPI metrics drag the currency lower. AUD ventured to a low of 0.6560 and further Downside sees 23rd Jan low at 0.6551. NZD steady on a 0.61 handle in what has been dull trade for the pair in recent sessions.

- PBoC set USD/CNY mid-point at 7.1039 vs exp. 7.1727 (prev. 7.1055).

Fied Income

- USTs are currently bid and the yield curve is marginally steeper, benchmark up to a 112-02 high. The docket is dominated by Quarterly Refunding (Monday’s estimates point to a smaller increase than forecast) and thereafter the FOMC/Powell.

- Bunds were initially bullish and shrugged off a hawkish handover from JGBs after the BoJ SOO; however, the deluge of German State CPIs were hotter Y/Y than consensus for the mainland implies and spurred a hawkish move down to 135.19.

- Gilt price action has largely taken impetus from EGBs awaiting the BoE on Thursday.

- Italy opens books to sell 15-year EUR benchmark; guidance seen +13bps to BTPs; pricing today

Commodities

- Softer trade across crude amid the overall downbeat risk tone in the market and the firmer Dollar. Sentiment for the complex is weighed on by Chinese Manufacturing PMI remaining in contraction whilst bullish Private Inventories, geopolitics, and energy commentary this morning are largely overlooked.

- Contained trade in spot gold ahead of the FOMC policy decision; XAU sees its 21 DMA (USD 2,030.10/oz) and 50 DMA (2,029.83/oz) converge.

- Chinese PMIs weighed on base metals overnight as Manufacturing PMI remained in contraction territory for a fourth consecutive month.

- US Energy Inventory Data (bbls): Crude -2.5mln (exp. -0.2mln), Gasoline +0.6mln (exp. +1.5mln), Distillate -2.1mln (exp. -0.4mln), Cushing -2.0mln.

- US seeks to buy about 3mln bbls of US-produced sour crude for the SPR for a June delivery.

Geopolitics

- Iran’s envoy to the UN said any attack on Iran, its interests or its nationals outside of its borders will be met with a definitive response, according to IRNA.

- US military said it shot down an anti-ship cruise missile fired by Yemen Houthis into the Red Sea, according to Reuters.

- Houthis say they fired missiles at US warship Greifley, and say they will target US, UK warships in ‘self-defence’, according to Al Arabiya

US Event Calendar

- 07:00: Jan. MBA Mortgage Applications -7.2%, prior 3.7%

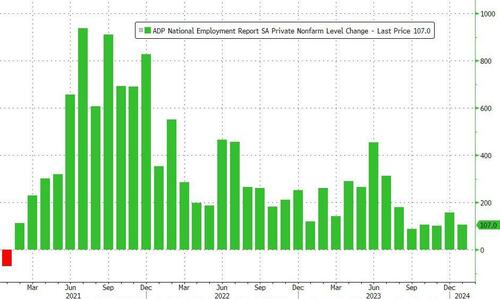

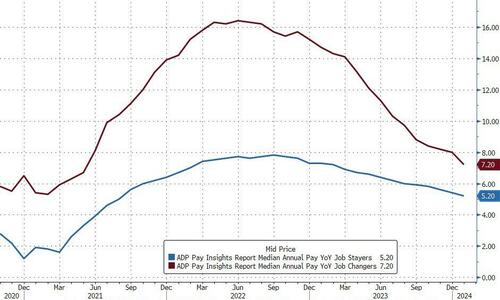

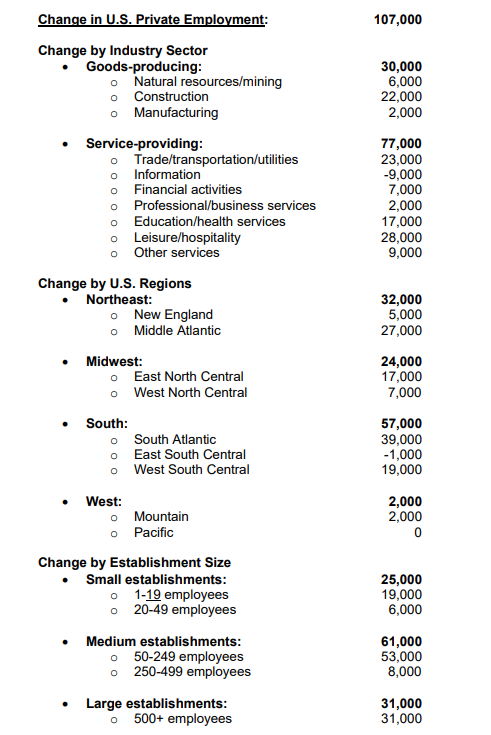

- 08:15: Jan. ADP Employment Change, est. 150,000, prior 164,000

- 08:30: 4Q Employment Cost Index, est. 1.0%, prior 1.1%

- 09:45: Jan. MNI Chicago PMI, est. 48.0, prior 46.9, revised 47.2

- 14:00: Jan. FOMC Rate Decision

DB’s Jim Reid concludes the overnight wrap