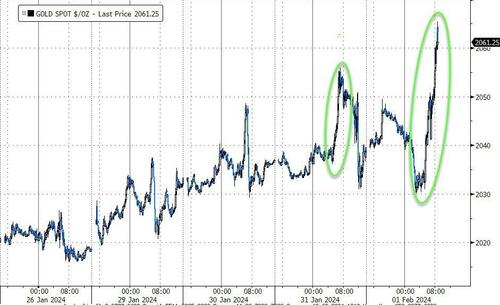

FEB 1//GOLD CLOSED UP $5,00 TO $2054.20//SILVER CLOSED UP 7 CENTS TO $23.14//PLATINUM CLOSED DOWN $10.20 TO $915.50 WHILE PALLADIUM CLOSED DOWN $15.45 TO $973.50//PANIC AT THE GOLD GOLD COMEX//ANOTHER BANK FAILURE IN THE MAKING IN JAPAN DUE TO HIGHER INTEREST RATES//EU HOLDS RATES STEADY//CHAOS CONTINUES THROUGHOUT EUROPE DUE TO GREEN POLICY BY THE EU//ISRAEL VS HAMAS: MAYBE A DEAL TO RELEASE THE HOSTAGES//ISRAEL CONTINUES TO CIRCLE KHAN YOUNIS// FAMILIES OF HOSTAGES SET TO SUE IRAN IN FEDERAL COURT IN NEW YORK//IRANIAN GUARD SEIZES A CARGO SHIP//COVID UPDATES//VACCINE INJURIES//DR PAUL ALEXANDER/SLAY NEWS/EVOL NEWS//NEWS ADDICTS//

072 C GOLDMAN 260 104 C MIZUHO 482 118 C MACQUARIE FUT 244 132 C SG AMERICAS 21 190 H BMO CAPITAL 2949 323 C HSBC 640 667 323 H HSBC 1711 357 C WEDBUSH 8 1 363 H WELLS FARGO SEC 762 365 C MAREX CAPITAL M 60 365 H MAREX CAPITAL M 1 407 C STRAITS FIN LLC 1 435 H SCOTIA CAPITAL 1905 624 C BOFA SECURITIES 1 624 H BOFA SECURITIES 3775 657 C MORGAN STANLEY 6 661 C JP MORGAN 5363 3850 685 C RJ OBRIEN 7 686 C STONEX FINANCIA 1 1 690 C ABN AMRO 7 33 709 C BARCLAYS 4 737 C ADVANTAGE 12 53 880 C CITIGROUP 74

DLV615-T CME CLEARING BUSINESS DATE: 01/31/2024 DAILY DELIVERY NOTICES RUN DATE: 01/31/2024 PRODUCT GROUP: METALS RUN TIME: 20:50:16 880 H CITIGROUP 369 905 C ADM 47 3

TOTAL: 11,659 11,659 MONTH TO DATE: 15,442

JPMorgan stopped 3850//11,659 contracts.

FOR FEB.:

GOLD: NUMBER OF NOTICES FILED FOR FEB/2024. CONTRACT: 11,659 NOTICES FOR 1,165,900 OZ or 36.264 TONNES

total notices so far: 15,442 contracts for 1,544,200 Oz (48.031 tonnes)

FOR FEBRUARY:

SILVER NOTICES 70 NOTICE(S) FILED FOR 350,000 OZ/

total number of notices filed so far this month : 617 for 3,085,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

GLD

WITH GOLD UP $5.00

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD

INVENTORY RESTS AT 851.15 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER UP 7 CENTS AT THE SLV//

MEGA CHANGES IN SILVER INVENTORY AT THE SLV AGAIN: A WITHDRAWAL OF 1.19 MILLION OZ OF SILVER FROM THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 438.947 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A FAIR SIZED 158 CONTRACTS TO 136,386 AND CLOSER TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS FAIR SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR LOSS OF $0.08 IN SILVER PRICING AT THE COMEX ON WEDNESDAY. WE HAD A ZERO LONG LIQUIDATION AT THE COMEX SESSION BUT A CONSIDERABLE SHORT COVERING. WE HAD A HUGE 728 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 728 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.08), BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A STRONG SIZED GAIN OF 609 CONTRACTS GAIN ON OUR TWO EXCHANGES ACCOMPANYING CONSIDERABLE SHORT

WE MUST HAVE HAD:

A FAIR SIZED 350 ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.535 MILLION OZ (FIRST DAY NOTICE) ACCOMPANYING A STRANGE 89 CONTRACT ISSUANCE FOR EX. FOR RISK FOR 445,000 OZ/ FOLLOWED BY TODAY’S 0 OZ QUEUE N=JUMP//NEW TOTAL; 3.980 MILLION OZ

//NEW STANDING FOR SILVER IS THUS 3.980 MILLION OZ

/ FAIR SIZED COMEX OI LOSS/GOOD SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 728 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED 417 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB

TOTAL CONTRACTS for 1 day, total 350 contracts: OR 17.50 MILLION OZ (350 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 17.50 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 17.50 MILLION OZ.

RESULT: WE HAD A FAIR SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 158CONTRACTS DESPITE OUR TINY LOSSIN PRICE OF SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 728 ISSUED FOR MARCH AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB. OF 3.535 MILLION OZ ACCOMPANIED BY YESTERDAY’S 445,000 OZ EX. FOR RISK //NEW TOTAL 3.980 MILLION OZ

NEW STANDING 3.980 million OZ /// WE HAVE A SMALL GAIN OF 192OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE TINY LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 728CONTRACTS//SOME FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION/// WITH CONSIDERABLE SHORT COVERINGS FROM OUR SPEC SHORTS . THE NEW TAS ISSUANCE WEDNESDAY NIGHT (728) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 70 NOTICE(S) FILED TODAY FOR 350,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 2465 CONTRACTS TO 432,793 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: – REMOVED 83 CONTRACTS

WE HAD A FAIR SIZED INCREASE IN COMEX OI ( 2465 CONTRACTS) WITH OUR $16.40 GAIN IN PRICE//WEDNESDAY. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR FEB. AT 49.773 TONNES ON FIRST DAY NOTICE ACCOMPANIED BY YESTERDAY’S HUGE 55,400 OZ EX. FOR RISK //THUS INITIAL STANDING FOR FEB: 51.494 TONNES FOLLOWED BY TODAY’S 12,900 OZ QUEUE JUMP//NEW TOTAL OF GOLD STANDING: 51.859 TONNES // ALL OF THIS HAPPENED WITH OUR $16.40 GAIN IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A HUGE SIZED GAIN OF 11,702 OI CONTRACTS (36.390) PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 9,237CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 432,876

IN ESSENCE WE HAVE A HUGE SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 11,702 CONTRACTS WITH 2548 CONTRACTS INCREASED AT THE COMEX// AND A HUGE SIZED 9,237EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 11,702 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 1299 CONTRACTS.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A HUGE SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (9237CONTRACTS) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (2548) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 11,702 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 49.773 TONNES PLUS YESTERDAY’S 1.723 TONNE OZ EX. FOR RISK FOLLOWED BY TODAY’S 12,900 OZ QUEUE JUMP//NEW STANDING 51.859 TONNES. / 3) ZERO LONG LIQUIDATION // 4) FAIR SIZED COMEX OPEN INTEREST GAIN/ 5) HUGE ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 1299CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

FEB.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB. :

TOTAL EFP CONTRACTS ISSUED: 9237 CONTRACTS OR 923,700OZ OR 28.730 TONNES IN 1 TRADING DAY(S) AND THUS AVERAGING: 9237 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY(S) IN TONNES 28.73 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 28.73/3550 x 100% TONNES 0.816% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EX FOR PHYSICAL)

FEB’24: 28.73 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A FAIR SIZED 158CONTRACTS OI TO 136,386 AND CLOSER TO THE COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 5 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 350 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MARCH 350 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 350 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 158 CONTRACTS AND ADD TO THE 350 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A FAIR SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 192CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 0.960 MILLION OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

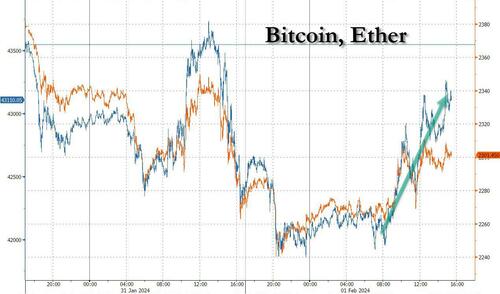

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 17,84 PTS OR 0.64% //Hang Seng CLOSED UP 81.14 PTS OR 0.52% /The Nikkei CLOSED DOWN 275.25 OR 0.76% //Australia’s all ordinaries CLOSED DOWN 1.19% /Chinese yuan (ONSHORE) closed DOWN AT 7.1822 /OFFSHORE CHINESE YUAN CLOSED DOWN TO 7.1952 /Oil DOWN TO 76.18 dollars per barrel for WTI and BRENT DOWN AT 80,93/ Stocks in Europe OPENED ALL MIXED// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 2465 CONTRACTS TO 432,793 WITH OUR GAIN IN PRICE OF $16.40 WITH RESPECT TO WEDNESDAY TRADING.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF FEB..… THE CME REPORTS THAT THE BANKERS ISSUED A HUGE SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 9237 EFP CONTRACTS WERE ISSUED: : APRIL 9237 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 9237CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A HUGE SIZED TOTAL OF 11,702 CONTRACTS IN THAT 9237 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE HAD A FAIR SIZED GAIN OF 2465 COMEX CONTRACTS..AND THIS HUGE SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $16.40 WEDNESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT WAS A FAIR SIZED 1299 CONTRACTS. THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: FEB (51.859 TONNES) ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 51.859 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $16.40 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A HUGE SIZED GAIN OF11,702 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD A FAIR T.A.S. LIQUIDATION ON THE FRONT END OF WEDNESDAY’S TRADING . THE T.A.S. ISSUED ON WEDNESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS. WE ALSO EXPERIENCED CONSIDERABLE SPECULATOR SHORT COVERING AT HIGHER PRICES AS WELL AS FINAL LIQUIDATION OF OUR SPREADERS.

WE HAVE GAINED A TOTAL OI OF 36.39 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR FEB. (49.773 TONNES) ON FIRST DAY NOTICE ALONG AN EXCHANGE FOR RISK FOR 1.7235 TONNES. THIS WAS FOLLOWED WITH TODAY’S 12,900 OZ QUEUE JUMP .4012 TONNES//NEW TOTAL STANDING 51.859: ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $16.40

WE HAD – REMOVED 83 CONTRACT TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET GAIN ON THE TWO EXCHANGES 11,702 CONTRACTS OR 1,170,200 OZ OR 36.39 TONNES.

452,557.431 OZ Brinks JPMorgan 14,076 kilobars 14.076 tonnes of gold withdrawn

.

Deposit to the Dealer Inventory in oz

nil oz

Deposits to the Customer Inventory, in oz

NIL oz

No of oz served (contracts) today

11,659 notice(s) 1,165,900 OZ 36.264 TONNES

No of oz to be served (notices)

677 contracts 67700 oz 2.105 TONNES

Total monthly oz gold served (contracts) so far this month

15442 notices 1,544,200 oz 48.031 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: nil oz

total customer withdrawals: 2

i) Out of Brinks 225,057 oz (7000 kilobars)

ii) Out of JPMorgan: 227,500.431 (7076 kilobars)

total withdrawals 452,557.431 oz 14,076 kilobars (14.076 tonnes)

we had 0 customer deposits

total customer deposits NIL oz

Adjustments; 1

a customer to dealer HSBC 172,256.534 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEB.

For the front month of FEBRUARY we have an oi of 12,326 contracts having LOST 3654 contracts. We had 3783 notices filed yesterday, so we gained 129 contracts or an additional 12900 oz will stand in this active delivery month of February.

However for the first time ever, on first day notice we also had 554 notices filed under exchange for risk for a total of 55,400 oz or 1.723 tonnes to which must be added to the delivery cycle.

Thus initial standing for gold for February is 50.136 tonnes + 1.723 tonnes = 51.859 tonnes which is pretty good.

March GAINED 74 contracts to stand at 2068.

APRIL GAINED 5006 CONTRACTS RISING TO 347,413.

We had 11,659 contracts filed for today representing 1,165,900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 5363 notices were issued from their client or customer account. The total of all issuance by all participants equate to 11,659 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 3850 notice(s) was (were) stopped ( received) by J.P.Morgan//customer account and 260 notice(s) received (stopped) by the squid (Goldman Sachs)

To calculate the INITIAL total number of gold ounces standing for the FEB. /2024. contract month, we take the total number of notices filed so far for the month (15,442 x 100 oz ), to which we add the difference between the open interest for the front month of FEB. (12,326 CONTRACTS) minus the number of notices served upon today 11,659 x 100 oz per contract equals 1,611,900 OZ OR 50.136 TONNES + 1.723 Ex for Risk/prior = 51.859 tonnes

thus the INITIAL standings for gold for the FEB.contract month: No of notices filed so far (15,442) x 100 oz + (12,326) {OI for the front month} minus the number of notices served upon today (11,659) x 100 oz) which equals 1,611,900 oz + 55,400 oz ex. for risk/prior//total standing OR 51.859 TONNES

TOTAL COMEX GOLD STANDING FOR FEB: 51.859 TONNES WHICH IS GREAT FOR AN ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 19,124,379.085 OZ

TOTAL REGISTERED GOLD 9,206,455.221 (286.33 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9917,923.864 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 7,856,269 oz (REG GOLD- PLEDGED GOLD) 244,36 tonnes

END

SILVER/COMEX

FEB 1/INITIAL

//2024// THE FEB 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

619,852.100 oz

delaware JPMorgan

.

Deposits to the Dealer Inventory

nil OZ

Deposits to the Customer Inventory

321,796.100 oz Manfra

No of oz served today (contracts)

70 CONTRACT(S) (350,000 OZ)

No of oz to be served (notices)

90 contracts (450,000 oz)

Total monthly oz silver served (contracts)

617 Contracts (3,085,000 oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposit: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i) Into Manfra: 321,796.100 oz

total customer deposits 321,796.100 oz

JPMorgan has a total silver weight: 130.199 million oz/274,781 million or 47.44%

adjustment: 2

a) dealer to customer

i) Asahi 9872.804 oz

ii) Manfra 323,726.100 oz

Comex withdrawals: 2

i) Out of Delaware: 12,584.200 oz

ii) Out of JPMorgan 607,267.900 oz

total withdrawal: 691,852.100 oz

TOTAL REGISTERED SILVER: 42.873 MILLION OZ//.TOTAL REG + ELIGIBLE. 274.931 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF FRB. /2023 OI: 160 CONTRACTS HAVING LOST 547 CONTRACT(S). WE HAD 547 NOTICES FILED YESTERDAY SO WE NEITHER GAINED NOR LOST ANY SILVER CONTRACTS STANDING FOR DELIVERY.

MARCH LOST 788 CONTRACTS TO 96,487

APRIL SAW A GAIN OF 2 CONTRACTS UP TO 2

MAY SAW A GAIN OF 860 CONTRACTS UP TO 26,062

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 70 for 350,000 oz

Comex volumes// est. volume today 86,955 huge

Comex volume: confirmed yesterday 72,581 strong

To calculate the number of silver ounces that will stand for delivery in FEB. we take the total number of notices filed for the month so far at 617 x 5,000 oz = 3,085,000 oz

to which we add the difference between the open interest for the front month of FEB. (160) and the number of notices served upon today 70 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB/2024 contract month: 617 (notices served so far) x 5000 oz + OI for the front month of FEB. (160) – number of notices served upon today (70 )x 500 oz of silver standing for the FEB contract month equates to 3.535 MILLION OZ. + .445 MILLION OZ EX. FOR RISK PRIOR//NEW TOTAL 3.980 MILLION OZ

New total standing: 3.980 million oz.

There are 42.873 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

FEB 1/WITH GOLD UP $5.00 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 851.15 TONNES:

JAN 31/WITH GOLD UP $16.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 852.88 TONNES:

JAN 30/WITH GOLD UP $6.50 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 854.89 TONNES:

TOTAL IN LAST 18 DAYS WITHDRAWAL OF 14.12 TONNES

JAN 29/WITH GOLD UP $8.70 TODAYHUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.88 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 856.05 TONNES

JAN 26/WITH GOLD DOWN $0.10 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 25/WITH GOLD UP $2.50 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 24/WITH GOLD DOWN $9.75 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 23/WITH GOLD UP $3.95 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD/ //://INVENTORY RESTS AT 858.93 TONNES

JAN 22/WITH GOLD DOWN $6.00 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD/ //://INVENTORY RESTS AT 860.95 TONNES

JAN 19/WITH GOLD UP $8.15 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD //://INVENTORY RESTS AT 862.10 TONNES

JAN 18/WITH GOLD UP $14.85 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 2.30 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 862.10 TONNES

JAN 17/WITH GOLD DOWN $23.25 TODAY: BIG CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .549 TONNES OF GOLD INTO THE GLD.;//://INVENTORY RESTS AT 864.40 TONNES

JAN 12/WITH GOLD UP $31.65 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A MASSIVE WITHDRAWAL OF 4.61 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 864.99 TONNES

JAN 11/WITH GOLD DOWN $7.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD; A MASSIVE WITHDRAWAL OF 4.61 TONNES OF GOLD FROM THE GLD//://INVENTORY RESTS AT 864.99 TONNES

JAN 10/WITH GOLD DOWN $4.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 869.60 TONNES

JAN 9/WITH GOLD UP $0.95 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 869.60 TONNES

JAN 8/WITH GOLD DOWN $16.85 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 4.61 TONNES FROM THE GLD. INVENTORY RESTS AT 869.60 TONNES

JAN 5/WITH GOLD UP $0.80 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD:///. // INVENTORY RESTS AT 874.21 TONNES

JAN 4/WITH GOLD UP $7.60 TODAY: NO CHANGES IN GOLD INVENTORY AT THE GLD:///. // INVENTORY RESTS AT 874.21 TONNES

JAN 3/WITH GOLD DOWN $29.40 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.90 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 874.21 TONNES

JAN 2/WITH GOLD UP $1.50 TODAY: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD INTO THE GLD///. // INVENTORY RESTS AT 879.11 TONNES

GLD INVENTORY: 851.15 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

FEB 1/WITH SILVER UP 7 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.19 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 438.947 MILLION OZ//LAST 6 DAYS: 10.3018 MILLION OZ WITHDRAWAL

JAN 31/WITH SILVER DOWN 8 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7438 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 440.137 MILLION OZ//LAST 5 DAYS: 9.1118 MILLION OZ WITHDRAWAL

JAN 30/WITH SILVER DOWN 5 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.876 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 442.699 MILLION OZ//LAST 4 DAYS: 7.368 MILLION OZ WITHDRAWAL

JAN 29/WITH SILVER UP $.37 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.105 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 444.575 MILLION OZ

JAN 26/WITH SILVER DOWN $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.556 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 446.680 MILLION OZ

JAN 25/WITH SILVER UP $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.831 MILLION OZ INTO THE SLV(FAIRY TALES) // /

INVENTORY RESTS AT 448.236 MILLION OZ

JAN 24/WITH SILVER UP $0.44 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER DEPOSIT OF 1.375 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 450.067 MILLION OZ

JAN 23/WITH SILVER UP $0.21 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 16.201 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 448.694 MILLION OZ

JAN 22/WITH SILVER DOWN $0.45 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 19/WITH SILVER DOWN $0.11 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 18/WITH SILVER UP $0.13 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 432.951 MILLION OZ

JAN 17/WITH SILVER DOWN $0.38 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 779,000 OZ FROM THE SLV.: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 16/WITH SILVER DOWN $0.08 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 12/WITH SILVER UP $0.62 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 11/WITH SILVER DOWN 34 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.912 MILLION OZ

JAN 10/WITH SILVER DOWN 3 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 450,000 OZ FROM THE SLV// //INVENTORY RESTS AT 433.912 MILLION OZ

JAN 9/WITH SILVER DOWN 20 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV //INVENTORY RESTS AT 434.370 MILLION OZ

JAN 8/WITH SILVER DOWN 8 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1,602,000 OZ INTO THE SLV//:././/////INVENTORY RESTS AT 434.370 MILLION OZ

JAN 5/WITH SILVER UP 20 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 916,000 OZ INTO THE SLV//:././/////INVENTORY RESTS AT 435.972 MILLION OZ

JAN 4/WITH SILVER UP 5 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV/:././/////INVENTORY RESTS AT 435.056 MILLION OZ

JAN 3/WITH SILVER DOWN 78 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWALOF 2.294 MILLION OZ OZ FROM THE SLV././/////INVENTORY RESTS AT 435.056 MILLION OZ

JAN 2/WITH SILVER DOWN 9 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWALOF 915,000 OZ FORM THE SLV././/////INVENTORY RESTS AT 437.35 MILLION OZ

DEC 29/WITH SILVER DOWN 29 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV/: //////INVENTORY RESTS AT 438.265 MILLION OZ

DEC 28/WITH SILVER DOWN 25 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV/: //////INVENTORY RESTS AT 438.265 MILLION OZ

DEC 27/WITH SILVER UP 20 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 1.374 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 438.265 MILLION OZ

THIS IS THE 3RD STRAIGHT DAY THAT THE SLV HAS ENGAGED IN WITHDRAWALS

DEC 26/WITH SILVER DOWN 14 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 1.465 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 439.639 MILLION OZ

DEC 22/WITH SILVER UP 0 CENTS TODAY:HUGE CHANGES IN SILVER INVENTORY AT THE SLV/: A WITHDRAWAL OF 2.289 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 441.104 MILLION OZ

DEC 21/WITH SILVER DOWN 2 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV/: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 443.393 MILLION OZ

DEC 20/WITH SILVER UP 28 CENTS TODAY:NO CHANGES IN SILVER INVENTORY AT THE SLV/: NO CHANGES IN SILVER INVENTORY AT THE SLV//////INVENTORY RESTS AT 443.393 MILLION OZ

CLOSING INVENTORY 438.947 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

Peter Schiff: The Economy May Already Be In Recession

Recent data have many cheerful about the economy. But according to Peter in his latest podcast, the economy may already be in recession. Here are some of Peter’s biggest causes for concern:

The recipe for GDP growth is a recipe for disaster

The big factor driving the GDP was the increase in government spending. Well, where’s the government getting this money? It’s borrowing it! That’s not a recipe for economic growth – that’s a recipe for disaster!”

Spending increases caused massive increases in national debt and liabilities.

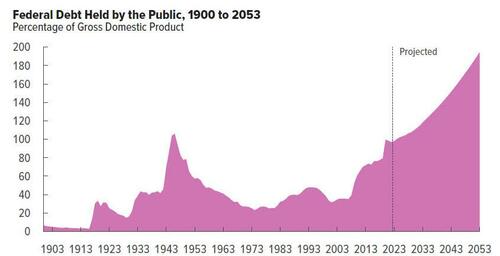

The US national debt currently stands at $34.1 trillion. Total unfunded liabilities tower in the hundreds of trillions, mostly from Social Security and Medicare.

Peter states that this used to be a priority, but is no longer:

Back in the 1980s, 1990s we were still pretending we were going to do something about entitlements —about Social Security, about Medicare, that there was going to be some effort to fix the problem before it blew up… Nobody at this point believes that we’re going to do anything about stopping the bomb from going off. In fact, it’s already gone off. We’ve already passed the point.”

Social Security is officially broke

Social Security trust funds are now liquidating their treasury holdings, putting a massive net drain on the US treasury.

And it’s getting worse:

[The] drain is getting bigger every day as more people retire whether voluntarily or involuntarily and more people just drop out of the labor force and stop paying taxes.”

Peter explains that many roles are being replaced by AI and automation tools, which don’t help the Social Security fund:

They’re not going to be paying Social Security taxes. Computer programs don’t have to pay into FICA. This this is going to get bigger but given the fact that we have this huge hole in Social Security, we’re bleeding — we’ve got a massive deficit that’s running out of control.”

Peter projects a total depletion of Social Security reserves within the next few years.

Making matters worse, manufacturing has been in recession

This confounds the administration’s narrative of a healthy economy:

They keep talking about a “Manufacturing Renaissance.” They got the “r” right, except it’s a recession instead of a renaissance.”

The Fed Philly Manufacturing Index has been negative for 18 out of the past 20 months, a manufacturing dark age.

This all begs the question:

How can you talk about a great economy? How healthy can the economy be when a vitally important part, the goods-producing sector, has been in a recession for almost two years?”

There are signs of higher inflation to come

Peter points out that just this week, oil prices rose $5 a barrel and the M2 money supply increased a whopping $100 billion, a significant expansion.

I’m correct that inflation is going to be picking up, it’s going to be weakening the economy. We could see a more meaningful turnaround. Maybe we’ll even get the government to come back and officially acknowledge that we’re in a recession.”

END

2) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

MATHEW PIEPENBURG

END

3. CHRIS POWELL//GATA GOLD COMMENTARIES:

Your weekend reading material

Alasdair Macleod….

Alasdair Macleod: Tides of change in gold paper markets

Submitted by admin on Wed, 2024-01-31 15:02 Section: Daily Dispatches

3p ET Wednesday, January 31, 2024

Dear Friend of GATA and Gold:

Market analyst and GoldMoney research director Alasdair Macleod writes today that open interest in the gold futures contract on the New York Commodities Exchange has fallen sharply in recent days.

He concludes that the decline in the contract’s liquidity will make prices more volatile and market rigging more difficult.

Macleod’s analysis is headlined “Tides of Change in Gold Paper Markets” and it’s posted at his internet site here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

END

Another rising gold hub!

(Swiss Infor.GATA)

Can the UAE outshine Switzerland with gold?

Submitted by admin on Wed, 2024-01-31 15:16 Section: Daily Dispatches

By Dominique Soguel and Pauline Turuban Swiss Info / Swiss Broadcasting Corp., Bern Wednesday, January 31, 2024

Switzerland sits at the heart of Europe and has for decades been the dominant player in the global gold industry both in terms of refining capacity and trading. But the United Arab Emirates, which lies at the crossroads of the West and an increasingly affluent East, is threatening that supremacy, having built its position quietly over the past two decades.

..

These dramatically different worlds are intertwined yet also increasingly competitive.

The UAE, particularly Dubai, is on the rise as an international gold hub. Since 2012 it has leveraged its strategic location, modern infrastructure, and business-friendly policies to attract global players.

While Switzerland offers a well-established financial system and an orderly, regulated market, the UAE provides a dynamic and forward-looking environment with a strong emphasis on innovation — in architecture, digital technology and the business environment.

Sanctions on Russia over its war against Ukraine have also helped shift global gold trading to Dubai and Hong Kong. …

Silver miners now realize that silver and gold are being manipulated..so they are urging at least the silver metal to be added to Canada/s critical mineral list.

(GATA)

.

Silver miners urge adding the metal to Canada’s critical minerals list

Submitted by admin on Wed, 2024-01-31 14:50 Section: Daily Dispatches

2:50p ET Wednesday, January 31, 2024

Dear Friend of GATA and Gold (and that other monetary metal, Silver):

Twenty executives of Canadian silver mining companies today sent a letter to Canada’s minister of energy and natural resources, Jonathan Wilkinson, asking that silver be added to the country’s official list of critrical minerals.

Along with gold, silver already seems to be on the U.S. government’s list of critical currencies whose markets must be manipulated and their prices suppressed lest they resume their historic competition with the U.S. dollar.

The letter from the Canadian mining executives is posted in PDF format here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

END

Record high gold demand due to central bank purchases

(Bloomberg)

Gold demand to hit record with central bank buying, gold council says

Submitted by admin on Wed, 2024-01-31 14:17 Section: Daily Dispatches

Will price suppression hit a record too? The council didn’t say.

* * *

By Yvonne Yue Li Bloomberg News Wednesday, January 31, 2024

Total gold demand hit a record last year and is expected to expand again in 2024 as the U.S. Federal Reserve moves toward cutting interest rates, potentially aiding prices, according to the World Gold Council.

Overall consumption climbed by about 3% to 4,899 tons last year, supported by strong demand in the opaque over-the-counter market, as well as from sustained central-bank buying, according to the WGC’s full-year report. That’s the highest total figure in data going back to 2010.

“The landscape is appropriate for emerging central banks to continue to be net buyers,” Joseph Cavatoni, chief market strategist at the WGC, said in an interview.

The council sees a strong case for record buying by countries such as China and Poland, he said. …

The USA increases its gold loans to 121 tonnes and thus the reason for the continual raids on gold

(Robert Lambourne/GATA)

Robert Lambourne: Gold intervention via BIS rose 21% in December

Submitted by admin on Thu, 2024-02-01 14:28 Section: Daily Dispatches

By Robert Lambourne Thursday, February 1, 2024

Trading in gold swaps by the Bank for International Settlements, the central bank of the central banks, continued in December. From information in the BIS statement of account for December, published this week —

— it is estimated that the volume of the bank’s gold swaps increased in December by 21 tonnes, from 100 tonnes at the end of November to 121 tonnes, up 21%. In the last two months the estimated level of gold swaps is up by 78%

The BIS’ gold swaps had fallen to zero as of December 31, 2022, and reached a peak for 2023 of 188 tonnes as of May 31.

Hence trading in gold swaps via the BIS remains active and is still large in volume.

There seem to be no new reasons to alter the assumption that the BIS is continuing to enter these swaps on behalf of the U.S. Federal Reserve. There is no evidence to suggest that any other major central bank is actively trading this much gold, and it remains clear that many central banks are accumulating record levels of physical gold.

The basic transaction that the BIS is believed to undertake is to swap dollars for gold that is transferred from a bullion bank, then to deposit this gold in a gold sight account at a central bank, presumed to be the Fed but almost certainly being the central bank that is using the BIS to execute the gold swap on its behalf.

Given the recent volatility in the level of BIS gold swaps, it seems likely that most are of a short duration. Why a central bank needs the BIS to undertake gold swaps isn’t clear. The swaps are likely connected with short-term trading needs — perhaps being used to aid suppression the gold price via the futures markets.

The volatility in the volume of swaps is clear from a review of Table B below. Volumes of swaps in 2023 were well below the average seen in the preceding four years but remained significant.

The gold price increased from $2,040 at November 30 to $2,063 at December 29 (per USAGold.com).

Using the December 29 gold price of $2,063, the 121 tonnes of gold swaps carried out via the BIS are valued at about $8 billion. (The corresponding value of the swaps in place at November 30 was around $6.5 billion.) So the recent trading in BIS gold swaps has high dollar value and shows that gold remains a significant monetary asset still actively traded on behalf of at least one central bank, assumed to be the Fed.

As ever with the BIS, it remains unlikely that more information about why it undertakes these transactions will be provided. This secrecy implies that central bank gold policy involves much deception — that it could be currency or gold market intervention for one or more central banks for which the BIS provides camouflage.

For example, the most recent published BIS annual report does not provide any information on the gold swaps other than confirming that swaps covering 77 tonnes of gold were in place as of March 31, 2023, and the subsequent interim report for the six months to September 30 has no disclosures about the gold swaps in place at that date.

GATA’s research on gold price suppression indicates that an active policy of price suppression was implemented around 30 years ago and was primarily intended to suppress interest rates. Recent updates on this research are provided in the following links to presentations Chris Powell and Bill Murphy made last November at the New Orleans Investment Conference.

An even more recent lament by GATA Secretary/Treasurer Chris Powell is at the link below. Powell remarks that so much of the recent bullish commentary on the prospects for gold fails to highlight the regular and repeated efforts to suppress the gold price during the past 30 years. He argues that this results in an incomplete picture of the risks as well as the rewards of gold ownership even as the financial outlook for the U.S. government seems fraught amid so much debt built up.

The highly influential report below from 2005 abput “Gibson’s paradox” remains relevant and highlights work in this area by former U.S. Treasury Secretary and Harvard University President Lawrence Summers:

It also remains relevant to highlight the following remarks made in a speech by Summers on September 8, 1999, as reported in the book “The Wealth of Progressive Nations: The Collected Lectures of Lawrence Summers.” The remarks below are an extract of a section of the speech titled “A New Economic Paradigm.”

“Most important of all, the Clinton-Gore administration has established a new paradigm for the management of our nation’s budget, with enormous cumulative benefits for our economy and our citizens. It has become a commonplace to remark on how exceptional today’s 4.2% unemployment rate is relative to any expectation at the beginning of the decade. It is no less remarkable that today, after 8.5 years of expansion, long-term interest rates are around 2 percentage points lower than they were at its start.”

From this it is reasonable to conclude that keeping interest rates “lower” was considered a priority and succeeding at it was “remarkable.” While this is not proof that gold price suppression was undertaken specifically to reduce interest rates, it shows that reducing interest rates was a priority.

Further evidence of this priority is provided by the following link to an interview with Robert Rubin about his time working in the Clinton administration after January 1993. In answer to a question on the initial decision to prioritize deficit reduction, Rubin remarks: “On the other hand, if interest rates go down as a result, then that will stimulate growth, and we thought that the beneficial effect of lower interest rates would outweigh the contractionary impact of the deficit reduction.”

Hence there is plenty of evidence that keeping interest rates low was a key priority during the Clinton presidency.

In the context of gold price suppression being used to assist efforts to reduce interest rates, the following report issued by GATA in 2007 with an analysis of the gold market by Frank Veneroso is a notable reference as it confirms that GATA’s primary assertions about gold price suppression were plausible:

Reading the remarks of Rubin and Summers on the priorities in the 1990s is a reminder of how far the the fiscal positions of Western nations have worsened since then.

This worsening trend for Western nations, especially the United States, probably reduces the appeal to the BIS of undertaking gold swaps on behalf of any central bank where the liability is to return gold. The trend possibly reduces the appeal of any such swaps to the central bank or banks for which the BIS has been acting. So a report issued by GATA in 2012 is worth revisiting as it highlights the acknowledgment of gold price suppression by a former chairman of the BIS, Jelle Zijlstra, a Dutch politician, economist, and central banker. It seems likely, therefore, that BIS management understands what the swaps are being used for and why they require camouflage:

The continuing conundrum facing the Federal Reserve about raising dollar interest rates has seemingly been resolved for now with the recent announcement of no change to rates and no reference to increases being considered.

Despite its regularly opaque rhetoric, the Fed needs to bolster confidence in the U.S. Treasuries market when the U.S. government’s ever-increasing debt has been so controversial recently. Forthcoming new debt issuance is going to be monitored closely by investors.

The Treasury Department’s monthly report on December revenue and expenditure points toward at best a similar level of cash outflows in the current fiscal year to the underlying deficit of about $2.1trillion in the year to September 30, 2023.

See Appendix A in the following link for an explanation of the $2.1 trillion deficit in fiscal 2023:

The trends behind the deficit are not positive, with higher expenditures and much-reported higher interest costs in the December monthly statement. It seems that the run rate of gross interest costs reported in the last 12 months should now be passing $1 trillion, but a surprising reduction in the annual interest payments on the $7 trillion of Treasury debt held by federal government-sponsored trust funds has been reported.

On a rolling 12-month basis the gross interest cost reported in the monthly statements is $957 billion. On the face of it the reduced interest charge on the Treasury debt held by the trust funds is counterintuitive and perhaps is indicative of the pressure to keep a lid on interest costs.

The December monthly report on the federal government’s finances is here:

In these circumstances the room for the Fed to raise interest rates in the next few years seems restricted and hence it seems likely as noted above that the BIS and some of its members might be questioning the role of the bank in these swaps and the obligation to make future deliveries of gold, since the Fed may be unable to move interest rates high enough to contain inflation.

In this context the relatively stable price of oil is relevant as it seems that strong forces want to keep oil prices subdued despite developments that might be expected to result in higher prices, such as production cuts by major producers and the dangers to shipments through the Red Sea.

With 2024 being a presidential election year in the United States there appear to be strong political incentives to contain oil prices and that even recent moves to consolidate the number of oil producers in the U.S. might be tacitly encouraged in return for commitments to keep production high.

The success or otherwise of such efforts might be a clue to the timing of a gold price reset as there appears to be little effort by the Fed and Treasury Department to accept that federal debt levels may be dangerously high now.

The report at the following link, which reviews the possible connection between hedge funds’ basis trades in U.S. Treasuries and the Fed’s program of quantitative tightening could be read as another sign of how difficult it is to find purchasers of U.S. Treasuries at current prices:

The link below contains a commentary on the apparent enrichment of certain hedge funds and the individuals involved as a result of the apparent support from the Fed to the hedge fund basis trade used to effect “quantitative tightening”:

Again, it seems appropriate to note that a report titled “Living with High Public Debt” authored by Serkan Arslanalp and Barry Eichengreen was published in August 2023 by the Federal Reserve Bank of Kansas City. This report reinforces just how difficult it is to handle high federal government debt with spending far in excess of revenue.

The report can be found at the Kansas City Fed’s internet site and at GATA’s:

“Looking forward, the challenges are daunting. Given aging populations, governments will have to find additional finance for healthcare and pensions. They will have to finance spending on defense, climate change abatement, and adaptation, and the digital transition. A growing number of low-income countries are already in debt distress.

“Living with high public debt therefore means avoiding steps that make a bad situation worse. This means minimizing unproductive public spending. It means targeting social transfers as a way of limiting pressures on the expenditure side. It means limiting contingent liabilities by, inter alia, adequately regulating banks and avoiding recapitalization costs.

“It means contemplating tax increases where revenues are low by international standards. It means further developing financial markets where markets are underdeveloped and where a diverse population of local investors in debt securities is absent. It means embracing legal and procedural changes that streamline and speed restructuring for countries whose debts are unsustainable.

“This modest medicine does not make for a happy diagnosis. But it makes for a realistic one.”

In the circumstances vividly described in the report it seems ridiculous that the price of gold was relatively subdued during 2023. The report offers yet more reason to suspect that gold swaps undertaken by the BIS, probably on behalf of the Fed, are being used to suppress the dollar gold price.

Table A below highlights the level of gold swaps reported in the annual reports of the BIS back to 2010, when the bank’s use of gold swaps appears to have begun. At only one year-end since then, in March 2016, has the swap level been zero.

The BIS’s recently published interim report as of September 30, 2023, discloses that the BIS still holds 102 tonnes of its own gold and that few of its activities in derivatives involve central banks. An assumption that the gold held by the BIS remains at 102 tonnes has been used in this note to make the estimate of the bank’s gold swap level. The low level of derivatives reported by the BIS using central banks as counterparties at the year-end seems a sensible reason to assume that the swaps are almost certainly done with gold bullion banks rather than central banks. Historically, the first swaps described below were done with bullion banks.

* * *

… Historical context …

The BIS rarely comments publicly on its gold activities, but its first use of gold swaps was considered important enough to cause the bank to give some background information to the Financial Times for an article published July 29, 2010, coinciding with publication of the bank’s 2009-10 annual report.

The general manager of the BIS at the time, Jaime Caruana, said the gold swaps were “regular commercial activities” for the bank, and he confirmed that they were carried out with commercial banks and so did not involve central banks. It also seems highly likely that the BIS’ remaining swaps are still all made with commercial banks, because the BIS annual report has never disclosed a gold swap between the BIS and a major central bank.

The swap transactions potentially created a mismatch at the BIS, which may have ended up being long unallocated gold (the gold held in BIS sight accounts at major central banks) and short allocated gold (the gold required to be returned to swap counterparties). This possible mismatch has not been reported by the BIS.

The gold banking activities of the BIS have been a regular part of the services it offers to central banks since the bank’s establishment 90 years ago. The first annual report of the BIS explains these activities in some detail:

A June 2008 presentation made by the BIS to potential central bank members at its headquarters in Basel, Switzerland, noted that the bank’s services to its members include secret interventions in the gold and foreign exchange markets:

The use of gold swaps to take gold held by commercial banks and then deposit it in gold sight accounts held in the name of the BIS at major central banks doesn’t appear ever to have been as large a part of the BIS’ gold banking business as it has been in recent years, although the recent declines suggest this is changing.

As of March 31, 2010, excluding gold owned by the BIS, there were 1,706 tonnes held in the name of the BIS in gold sight accounts at major central banks, of which 346 tonnes or 20% were sourced from gold swaps from commercial banks.

If the BIS was adopting the level of disclosure made by publicly held companies, such as commercial banks, some explanation of these changes probably would have been required by the accounting regulators. This irony may not be lost on those dealing with regulatory activities at the BIS. Presumably the shrinkage of the BIS’ gold banking business shows that even central banks now prefer to hold their own gold or hold it in earmarked form — that is, as allocated gold.

A review of Table B below highlights recent BIS activity with gold swaps, and despite the recent declines, the recent positions estimated from the BIS monthly statements have regularly been large, especially in early 2022, and the volume of trading has been significant.

No explanation for this continuing use of swaps has been published by the BIS. Indeed, no comment on the bank’s use of gold swaps has been offered since 2010.

This gold is supplied by bullion banks via the swaps to the BIS. The gold is then deposited in BIS gold sight accounts (unallocated gold accounts) at major central banks such as the Federal Reserve.

The reasons for this activity have never been fully explained by the BIS and various conjectures have been made as to why the BIS has facilitated it. One conjecture is that the swaps are a mechanism for the return of gold secretly supplied by central banks to cover shortfalls in the gold markets. The use of the BIS to facilitate this trade suggests of a desire to conceal the rationale for the transactions.

As can be seen in Table A below, the BIS has used gold swaps extensively since its financial year 2009-10. No use of swaps is reported in the bank’s annual reports for at least 10 years prior to the year ended March 2010.

The February 2021 estimate of the bank’s gold swaps (552 tonnes) was higher than any level of swaps reported by the BIS at its March year-end since March 2010. The swaps reported at March 2021 were at the highest year-end level reported, as is clear from Table A.

—–

Table A — Swaps reported in BIS annual reports

March 2010: 346 tonnes. March 2011: 409 tonnes. March 2012: 355 tonnes. March 2013: 404 tonnes. March 2014: 236 tonnes. March 2015: 47 tonnes. March 2016: 0 tonnes. March 2017: 438 tonnes. March 2018: 361 tonnes. March 2019: 175 tonnes March 2020: 326 tonnes March 2021: 490 tonnes March 2022: 358 tonnes March 2023: 77 tonnes

—–

The table below reports the estimated swap levels since August 2018. It can be seen that the BIS is actively involved in trading gold swaps and other gold derivatives with changes from month to month reported in excess of 100 tonnes in this period.

—–

Table B — Swaps estimated by GATA from BIS monthly statements of account

* The estimate originally reported by GATA was 78 tonnes, but the BIS annual report states 77 tonnes. It is believed that slightly different gold prices account for the difference.

± The estimate originally reported by GATA was 487 tonnes, but the BIS annual report states 490 tonnes, It is believed that slightly different gold prices account for the difference.

** The estimate originally reported by GATA was 332 tonnes, but the BIS annual report states 326 tonnes. It is believed that slightly different gold prices account for the difference.

GATA uses gold prices quoted by USAGold.com to estimate the level of gold swaps held by the BIS at month-ends.

– – – – –

As noted already, the BIS in recent times has refused to explain its activities in the gold market, nor for whom the bank is acting:

Despite this reticence the BIS has almost certainly acted on behalf of central banks in taking out these swaps, as they are the BIS’ owners and control its Board of Directors. Historically, the BIS has often acted on behalf of the Federal Reserve.

This refusal to explain prompts some observers to believe that the BIS acts as an agent for central banks intervening surreptitiously in the gold and currency markets, providing those central banks with access to gold as well as protection from exposure of their interventions.

As mentioned above, it is possible that the swaps provide a mechanism for bullion banks to return gold originally lent to them by central banks to cover bullion bank shortfalls of gold. Some commentators have suggested that a portion of the gold held by exchange-traded funds and managed by bullion banks is sourced directly from central banks.

——

Robert Lambourne is a retired business executive in the United Kingdom who consults for GATA about the involvement of the Bank for International Settlements in the gold market.

* * *

4. OTHER GOLD/SILVER //COMMENTARIES//

Global Silver Demand Forecasted to Rise to 1.2 Billion Ounces in 2024 |

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.1822

OFFSHORE YUAN: UP TO 7.1952

SHANGHAI CLOSED DOWN 17,84 PTS OR 0.64%

HANG SENG CLOSED UP 81,14 PTS OR 0.52%

2. Nikkei closed DOWN 275.25 PTS OR 0.61%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 103.49 EURO RISES TO 1.0811 UP 6 BASIS PTS

3b Japan 10 YR bond yield:FALLS TO. +.688 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.07/JAPANESE YEN NOW RISING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN// OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund DOWN TO +2.2000***/Italian 10 Yr bond yield DOWN to 3.754** /SPAIN 10 YR BOND YIELD DOWN TO 3.126…**

3i Greek 10 year bond yield DOWN TO 3.242

3j Gold at $2033.80 silver at: 22.66 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 34 /100 roubles/dollar; ROUBLE AT 90.36//

3m oil into the 76 dollar handle for WTI and 80 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147,07// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.688% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8634 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9340 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

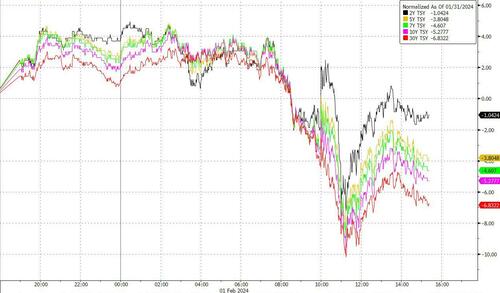

USA 10 YR BOND YIELD: 3.940 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.188 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.242 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 30.37…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: DOWN 7 BASIS PTS AT 3.854

end

2.a Overnight: Newsquawk and Zero hedge

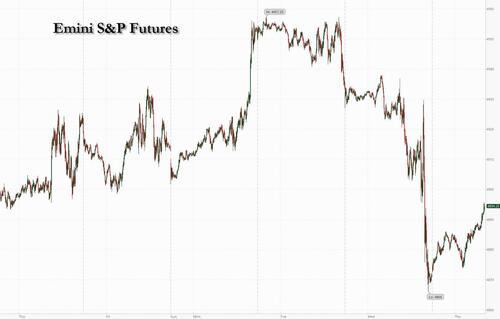

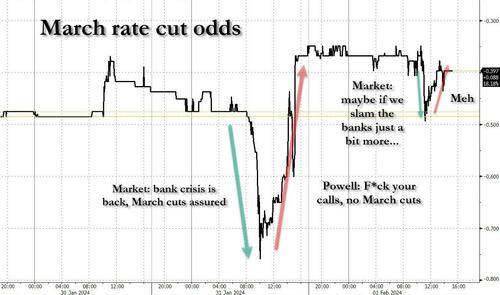

Stocks Rebound After Powell Hawkamania Sparks Worst Market Rout In Months

THURSDAY, FEB 01, 2024 – 08:14 AM

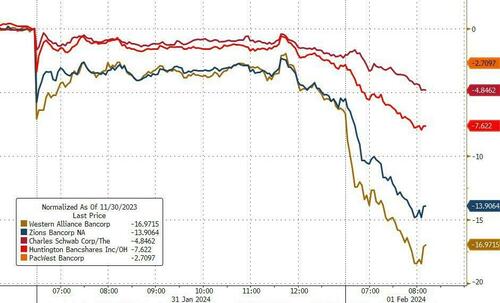

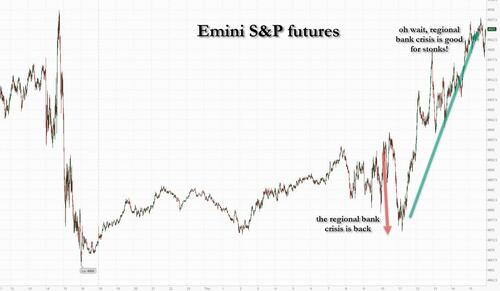

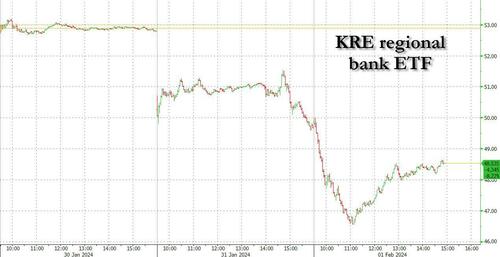

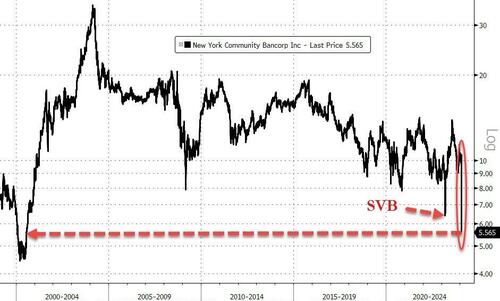

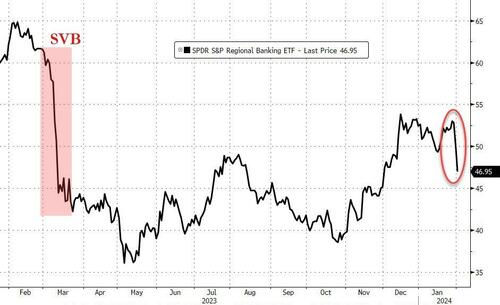

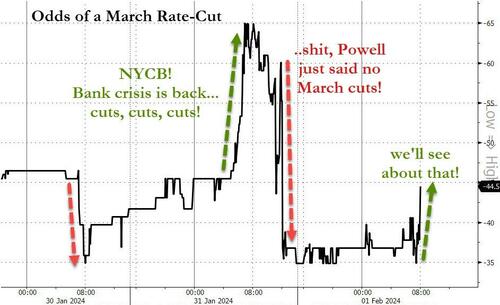

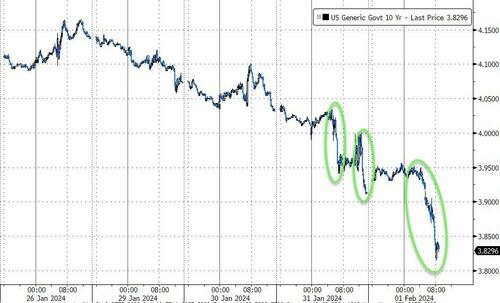

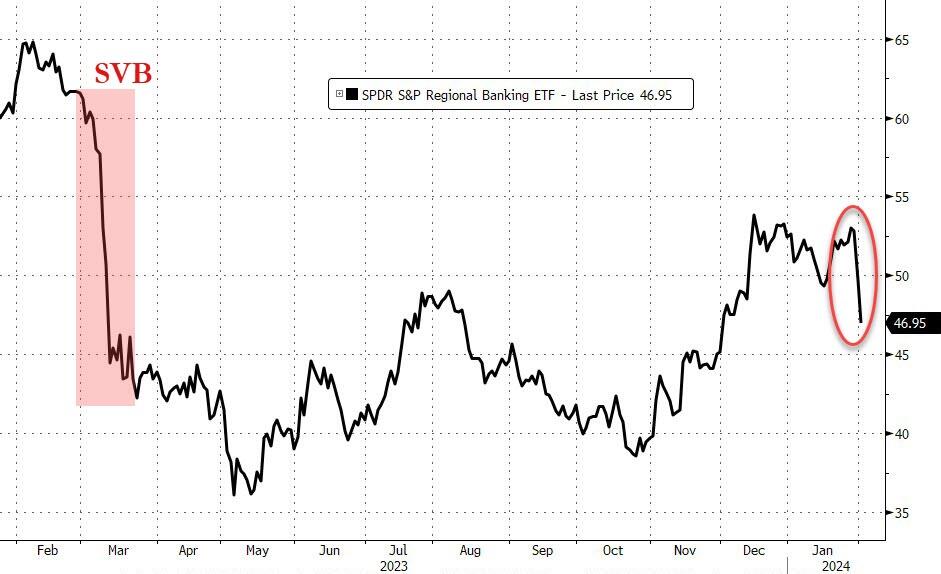

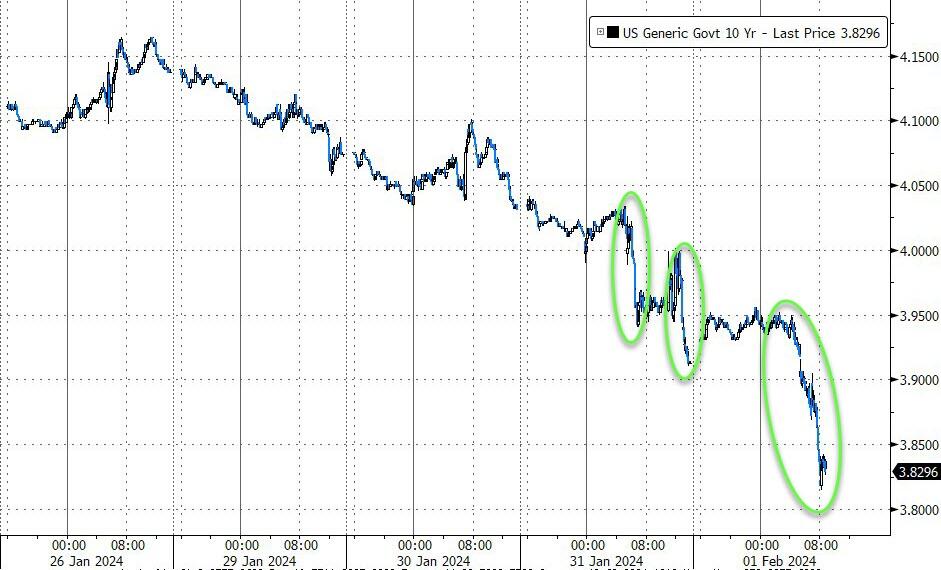

US equity futures rebounded after the worst day for stocks since September, as investors prepared for the next wave of megacap tech earnings while resetting expectations for the timing of Fed rate cuts, which have been pushed back from March to May at the earliest (unless of course there is a new banking crisis). As of 7:50am, S&P 500 futures gained 0.5% following a 1.6% plunge on Wednesday after Powell unleashed Hawkamania on the market during his press conference. Nasdaq 100 climbed 0.6% and awaiting earnings from Apple, Amazon and Meta.It’s the latest update from members of the “Magnificent Seven” stocks that have soared amid aggressive expectations from investors for earnings growth fueled by artificial intelligence applications and easier policy from the Fed. Meanwhile, the epicenter of the new banking crisis, New York Community Bancorp rallied following its record plunge. Interest rates reversed some of Wednesday’s losses with 10Y yields rising 2bps to 3.93% while the dollar was flat, reversing earlier gains.

In premarket trading, Qualcomm shares slipped 1.5% after the chipmaker reported first-quarter results that beat expectations, and provided an outlook for the year. While analysts see signs of a recovery in key markets, the company also warned about high inventory levels. Here are some other notable premarket movers:

Align Technology (ALGN) jumps 12% after the dental equipment firm reported fourth-quarter results and first-quarter guidance which beat estimates.

Amplitude (AMPL) slips 3% after Morgan Stanley downgraded the stock, saying the valuation doesn’t reflect the increasingly competitive landscape.

Arcutis Biotherapeutics (ARQT) drops 6% after the drugmaker filed for a $300m mixed-securities shelf.

Canada Goose (GOOS) rises 11% after the parka retailer’s fiscal fourth-quarter revenue outlook exceeded the average analyst estimate.

Cardinal Health (CAH) falls 3% after posting quarterly results.

MaxLinear (MXL) declines 11% after the semiconductor device company gave a disappointing revenue forecast.

Nextracker (NXT) surges 21% after the maker of measuring machines for the solar industry boosted its revenue guidance.

Wolfspeed (WOLF) falls 5% after providing a disappointing revenue forecast.

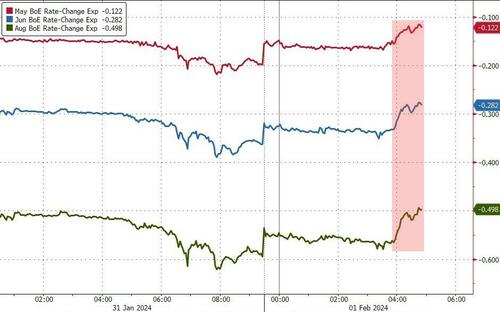

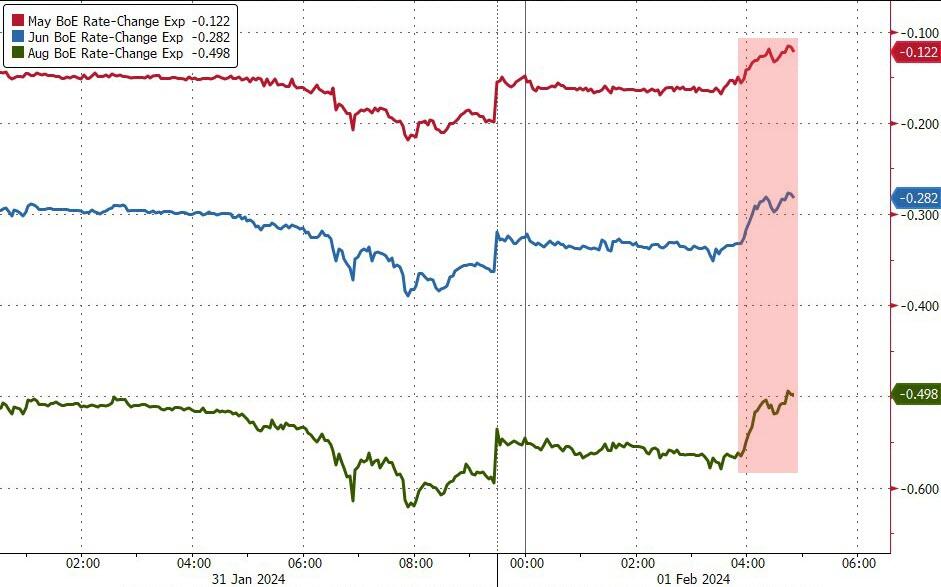

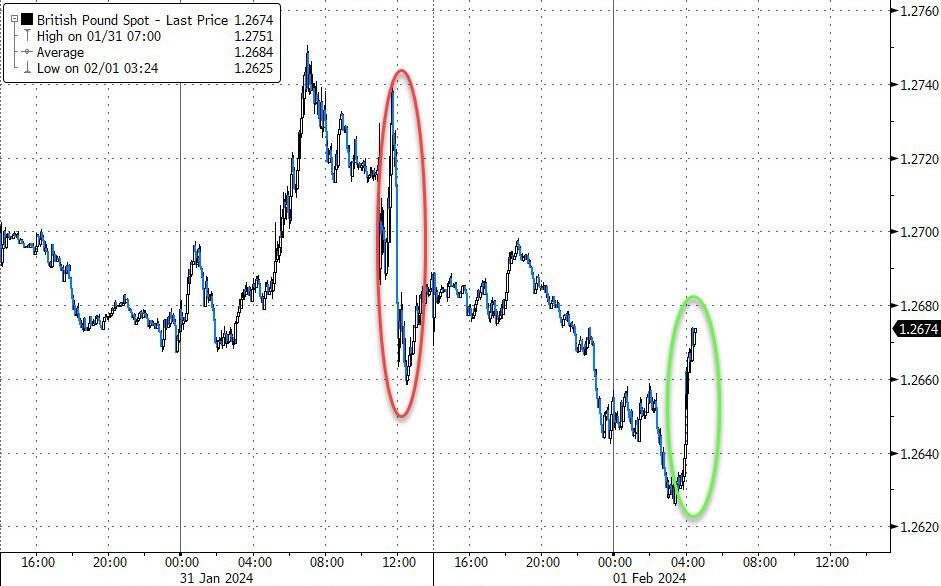

Stocks tumbled on Wednesday after Fed officials signaled they are in no rush to cut rates as they target lower inflation, with Chair Powell saying after Wednesday’s decision he doesn’t think a cut in March is likely. The Bank of England also said more evidence of moderating inflation was needed before it could ease policy, as it decided to keep rates at a 16-year high on Thursday.

“The market got ahead of itself in the last few months and it feels like we will get a respite as rate decreases start to get priced out and we see more rhetoric from central banks pushing back on rate cuts,” said Justin Onuekwusi, chief investment officer at wealth manager St James Place Management Svs Ltd.

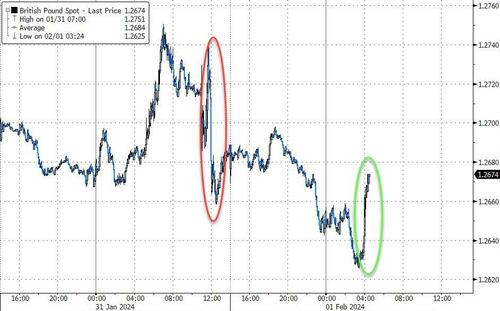

Central banks also dominated markets on Thursday where the pound pared its drop against the dollar and UK bonds fell after the BOE announcement. The central bank slashed its outlook for inflation this year and dropped its guidance that borrowing costs may have to rise again. Its decision to hold was a split view among policymakers, with two voting for a hike, six to keep rates unchanged and the first rate cut vote.

Sweden’s Riksbank earlier held rates steady and said it may lower borrowing costs as soon as the first half of the year, pivoting from a tightening campaign. The Swedish krona fell after the decision.

Meanwhile, European stocks are on the back foot as bank shares slide after some disappointing earnings reports from BNP Paribas and ING. The Stoxx 600 is down 0.1%. Adidas AG slumped on lower-than-expected profit guidance. Deutsche Bank AG rallied after announcing a share buyback and higher revenue goal. Ferrari NV rose after the supercar builder beat estimates. While strong numbers from Shell buoyed the energy sector, poor reports from BNP Paribas and ING weigh on bank shares. Here are the biggest movers Thursday:

Volvo Car soars as much as 32% after the Swedish firm said it will no longer extend funding to Polestar and is evaluating a restructuring of its holdings in the struggling electric vehicle maker

Shell gains as much as 2.8% after the oil major reported results that beat estimates and kept up the pace of buybacks, with analysts positive on the performance of the gas and upstream businesses

Evolution shares jump as much as 7% after the Swedish live casino operator reported in-line fourth-quarter trading. Morgan Stanley describes management commentary as “upbeat”

Deutsche Bank advances as much as 5.1% after it announced plans for a €675 million buyback in the first half and raised its mid-term revenue target, offsetting an otherwise disappointing 4Q

Julius Baer extend gains as much as 8.5%, most since July, amid a call with analysts in which the chairman said meaningful inflows were seen at the end of last year

Axfood climbs as much as 9% following its fourth-quarter earnings report, with DNB seeing a positive report with results ahead for all segments apart from its Dagab logistics unit

Hexagon rises as much as 6.5%, the most since Dec. 8, after the Swedish industrial software group delivered what DNB Markets describes as a strong print

Straumann gains as much as 5.3%, the most intraday since Dec. 14, after the Swiss dental equipment firm’s US rival Align reported estimate-beating results

BNP Paribas shares drop as much as 9.8%, the most intraday since March 2023, after the French bank reported 4Q results that missed estimates and lowered its performance targets

ING falls as much as 9.6% after the bank reported net interest income for the fourth quarter that missed the average analyst estimate; ING and BNP’s poor reports pull the wider sector downwards, too

Roche falls as much as 4.5% after the Swiss pharma giant gave a very weak outlook for 2024. Analysts attribute the softness to significant headwinds from the strong Swiss franc

Adidas slumps as much as 9%, the biggest intraday decline since February 2023, after the sportswear maker forecast operating profit for 2024 of about €500m, well below estimates

Earlier in the session, Asian stocks also declined, as Japan and Australia followed the US market lower, while Chinese stocks surged on the government’s latest policy support efforts. The MSCI Asia Pacific Index declined as much as 0.7% before paring the drop. TSMC, Toyota Motor and Commonwealth Bank of Australia were among the biggest drags. Japanese stocks slid as yen strengthened and Australian shares retreated from Wednesday’s record close after the Federal Reserve pushed back on expectations for US interest rate cuts.

Hang Seng and Shanghai Comp were mixed with early upside from stronger-than-expected Caixin PMI data and further support pledges although the gains were limited after the substantial PBoC liquidity drain and the mainland index gradually reversed course.

Nikkei 225 retreated amid recent currency strength and with a slew of earnings influencing price action.

ASX 200 pulled back from record highs amid weakness in tech and financials, as well as softer data.

In FX, the Bloomberg Dollar Spot Index is up 0.1% while the yen tops the G-10 FX pile, rising 0.1% versus the greenback. The Swedish krona falls 0.8% after the Riksbank left rates on hold and said it may lower borrowing costs as soon as in the first half of the year. The pound falls 0.4% ahead of the BOE decision while the yen was the only gainer against the greenback among its Group-of-10 peers.

AUD/USD sank 0.9% to 0.6511, the lowest level since November, on reduced risk appetite; Australia’s stock market tumbled from a record high

USD/SEK rose as much as 0.9% and EUR/SEK jumped 0.6%, after the Riksbank said it may lower borrowing costs as soon as in the first half of the year

EUR/USD pared a 0.4% loss to trade 0.2% lower at 1.0796 as euro-zone inflation eased less than anticipated at the start of the year

GBP/USD fell as much as 0.5% to 1.2627 as traders braced for the BOE decision later Thursday; The central bank is likely to deliver a brighter outlook for the UK economy and reduce its forecast for inflation

In rates, US 10-year yields first rose 3bps to 3.95% but have since erased much of the rise which followed Powell’s comments and the fresh concerns about regional lenders. Bunds are lower as data showed euro-zone CPI slowed less than expected in January. German 10-year yields rise 5bps to 2.21%. The dollar issuance slate includes four names so far; dealers are calling for around $150b of supply in February. US economic data includes January Challenger job cuts (7:30am), 4Q nonfarm productivity and weekly jobless claims (8:30am), January S&P US manufacturing PMI (9:45am), December construction spending and January ISM manufacturing (10am)

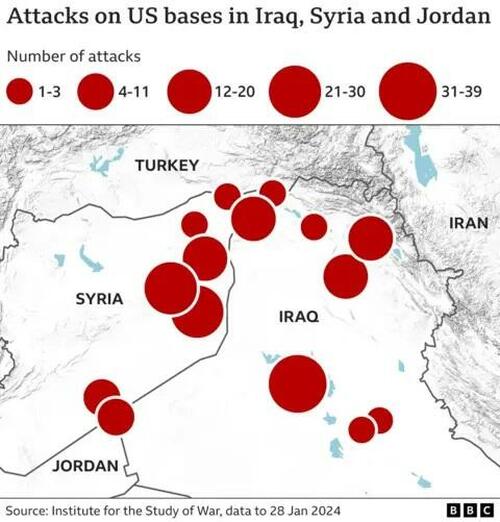

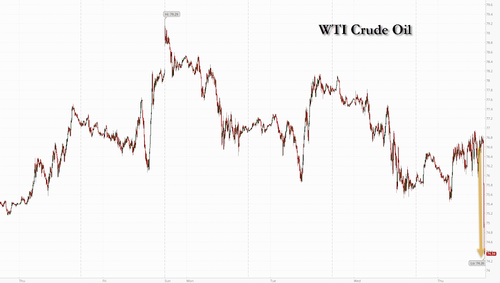

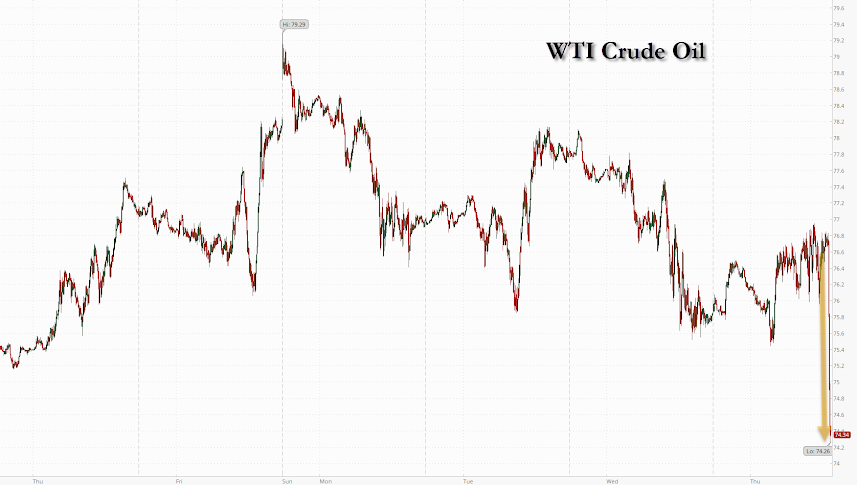

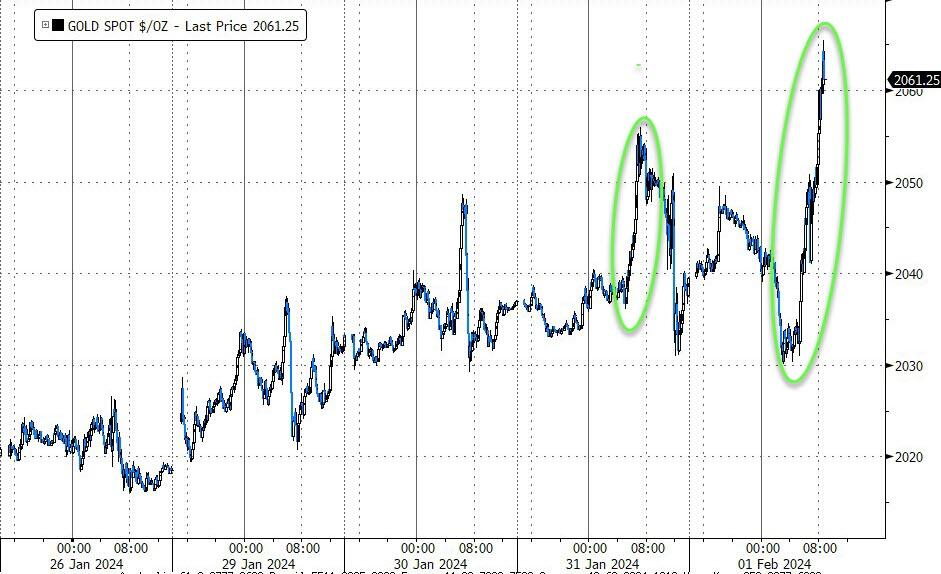

In commodities, oil rebounded after the biggest decline in three weeks on Wednesday as investors weighed the risks from any US retaliation to a deadly attack in Jordan against signs of robust American supply. WTI rose 0.8% to trade near $76.50, gold dropped to trade near session lows around $2,033.

To the day ahead now, and data releases include the global manufacturing PMIs for January, along with the ISM manufacturing reading from the US. In the Euro Area, there’s also the flash CPI print for January, and in the US there’s the weekly initial jobless claims. From central banks, the Bank of England will announce their latest policy decision, and we’ll also hear from the ECB’s Centeno and Lane. Finally, today’s earnings releases include Apple, Amazon and Meta.

Market Snapshot

S&P 500 futures up 0.3% to 4,885.75

STOXX Europe 600 little changed at 485.24

MXAP down 0.4% to 165.84

MXAPJ little changed at 503.50

Nikkei down 0.8% to 36,011.46

Topix down 0.7% to 2,534.04

Hang Seng Index up 0.5% to 15,566.21

Shanghai Composite down 0.6% to 2,770.74

Sensex little changed at 71,687.82

Australia S&P/ASX 200 down 1.2% to 7,588.19

Kospi up 1.8% to 2,542.46

German 10Y yield little changed at 2.20%

Euro down 0.2% to $1.0798

Brent Futures up 0.7% to $81.09/bbl

Gold spot up 0.1% to $2,042.31

U.S. Dollar Index up 0.39% to 103.68

Top Overnight News

Stocks fell in Asia and Europe as investors reset their expectations of when the Federal Reserve will start cutting interest rates and assessed a deluge of corporate earnings.

Jerome Powell delivered a clear message to traders eager for the central bank to start slashing interest rates: Not so fast.

Euro-zone inflation eased less than anticipated at the start of the year — testing investor expectations that the European Central Bank will begin lowering interest rates as soon as the spring.

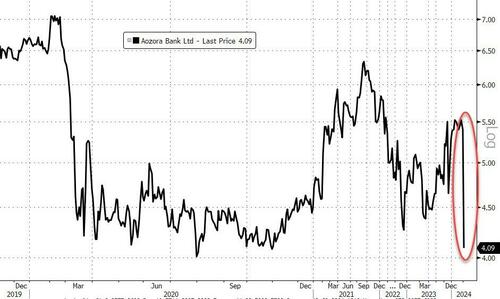

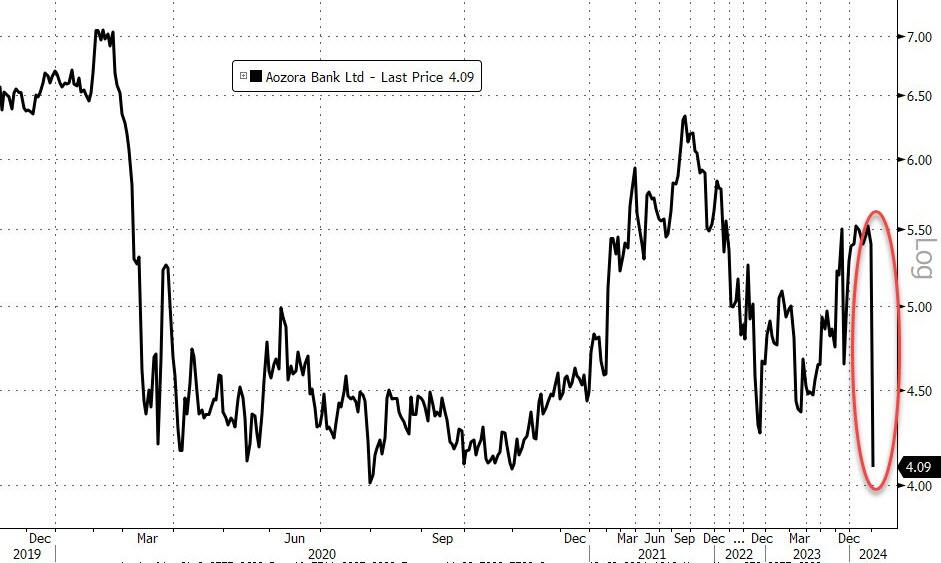

The US commercial real estate market has been in turmoil since the onset of the Covid-19 pandemic. But New York Community Bancorp and Japan’s Aozora Bank Ltd. delivered a reminder that some lenders are only just beginning to see the pain.

The Riksbank held rates steady and said it may lower borrowing costs as soon as in the first half of the year, pivoting from a tightening campaign that tipped the Swedish economy into recession.

Donald Trump’s legal troubles have helped him raise millions of dollars from supporters, but paying to defend himself has siphoned $51.2 million from his White House comeback effort in the past year.

A more detailed look at global markets courtesy of Newsquawk