GOLD PRICE CLOSED DOWN $1.00 TO $2033.30

SILVER PRICE DOWN $.07 TO $22.43

Gold ACCESS CLOSED 2033.80

Silver ACCESS CLOSED: 22.45

Bitcoin morning price:, $59,418 UP 2789 DOLLARS.

Bitcoin: afternoon price: $59,880 up 462 dollars

Platinum price closing DOWN $12.10 AT $882.15

Palladium price; DOWN $18.45 AT $928.55

END

SHANGHAI GOLD PREMIUM 50 DOLLARS/COMEX GOLD

SHANGHAI GOLD (USD) FUTURES – QUOTES

SHANGHAI GOLD (USD) FUTURES – QUOTES

Beginning Monday, April 1, 2024, CME Group settlement data will no longer be accessible through ftp.cmegroup.com and will have a delayed publication time of 12:00 a.m. CT on all cmegroup.com web pages. Learn about alternate ways to access the data in our FAQ.

Last Updated 28 Feb 2024 07:56:10 AM CT.

Market data is delayed by at least 10 minutes.

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $2,760.90 UP $14.90 CDN dollars per oz( * NEW ALL TIME HIGH 2,795.90 CDN DOLLARS PER OZ//DEC 1 2023)

*BRITISH GOLD: 1606.45 UP 6.40 pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1655.17 BRITISH POUNDS/OZ) OCT 2/2023

*EURO GOLD: 1876.51 UP 4.50 euros per oz //* (ALL TIME CLOSING HIGH: 1903.75 EUROS PER OZ//DEC 1.2023)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

EXCHANGE: COMEX

ACCESS MARKET:

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,034.000000000 USD

INTENT DATE: 02/27/2024 DELIVERY DATE: 02/29/2024

FIRM ORG FIRM NAME ISSUED STOPPED

323 C HSBC 9

363 H WELLS FARGO SEC 21

624 H BOFA SECURITIES 252

661 C JP MORGAN 470

686 H STONEX FINANCIA 3

880 H CITIGROUP 796

991 H CME 41

TOTAL: 796 796

MONTH TO DATE: 20,754

JPMorgan stopped 470/796 contracts.

FOR FEB/2024

GOLD: NUMBER OF NOTICES FILED FOR FEB/2024. CONTRACT: 796 NOTICES FOR 79,600 OZ or 2.4758 TONNES

total notices so far: 20,754 contracts for 2,075,400 Oz (64.552 tonnes)

FOR FEBRUARY:

SILVER NOTICES 0 NOTICE(S) FILED FOR NIL OZ/

total number of notices filed so far this month : 1308 for 6,540,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

GLD

WITH GOLD DOWN $1.00//

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 826.94 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER DOWN 7 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: HUGE DEPOSIT OF 5.123 MILLION OZ INTO THE SLV/.

THIS DATA IS JUST NOT BELIEVABLE.

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 433.086 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 1354 CONTRACTS TO 144,382 AND FURTHER FROM THE RECORD HIGH OI OF 244,710, SET FEB 25/2020 AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR RISE IN PRICE OF $0.03 IN SILVER PRICING AT THE COMEX ON TUESDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN SOME SHORT COVERING DESPITE THE PRICE OF SILVER RISING BY A SMALL AMOUNT. WE HAD A GOOD 431 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 431 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE NOW SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.03), AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A TINY SIZED GAIN OF 66 CONTRACTS ON OUR TWO EXCHANGES DESPITE A MUCH LOWER PRICE.

WE MUST HAVE HAD:

A MEGA HUMONGOUJS SIZED 1450 ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.535 MILLION OZ (FIRST DAY NOTICE) ACCOMPANYING A STRANGE 89 CONTRACT ISSUANCE FOR EX. FOR RISK FOR 445,000 OZ ON FIRST DAY NOTICE/ FOLLOWED BY TODAY’S 0 OZ E.F.P. JUMP TO LONDON//0 QUEUE JUMP //NEW TOTAL REMAINS AT ; 6.985 MILLION OZ

//NEW STANDING FOR SILVER IS THUS 6.985 MILLION OZ

/ HUGE SIZED COMEX OI LOSS/MEGA HJUMONGOUS SIZED EFP ISSUANCE/ VI) GOOD SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 431 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED A HUGE 359 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF FEB

TOTAL CONTRACTS for 19 days, total 12,627 contracts: OR 63.135 MILLION OZ (664 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 63,135 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 118.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 63.135 MILLION OZ.

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1384 CONTRACTS DESPITE OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A MEGA HUMONGOUS EFP ISSUANCE CONTRACTS: 1450 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR FEB. OF 3.535 MILLION OZ ACCOMPANIED BY FIRST DAY NOTICE OF 445,000 OZ EX. FOR RISK FOLLOWED BY TODAY’S 0 OZ E.F.P. JUMP//(0 OZ QUEUE JUMP) //NEW TOTAL REMAINS AT 6.985 MILLION OZ

NEW STANDING 6.985 MILLION OZ /// WE HAVE A TINY GAIN OF 66 OI CONTRACTS ON THE TWO EXCHANGES WITH THE GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG SIZED 3445 CONTRACTS//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION/// WITH SOME SHORT COVERING FROM OUR SPEC SHORTS ( WITH PRICE OF SILVER RISING) . THE NEW TAS ISSUANCE TUESDAY NIGHT (3445) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 0 NOTICE(S) FILED TODAY FOR NIL OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 871 CONTRACTS TO 411,195 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW CLOSER TO OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED 176 CONTRACTS

WE HAD A SMALL SIZED INCREASE IN COMEX OI ( 871 CONTRACTS) WITH OUR $4.40 GAIN IN PRICE//TUESDAY. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR FEB. AT 49.773 TONNES ON FIRST DAY NOTICE ACCOMPANIED BY FIRST DAY NOTICE : 55,400 OZ EX. FOR RISK //THUS INITIAL STANDING FOR FEB: 51.494 TONNES FOLLOWED BY TODAY’S HUGE 60,400 OZ QUEUE JUMP //NEW TOTAL OF GOLD STANDING ADVANCES TO: 66.276 TONNES // ALL OF THIS HAPPENED DESPITE OUR $4.40 GAIN IN PRICE WITH RESPECT TO TUESDAY’S TRADING. WE HAD A A GOOD SIZED GAIN OF 3876 OI CONTRACTS (12.055) PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 3005 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 411,195

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3896 CONTRACTS WITH 871 CONTRACTS INCREASED AT THE COMEX// AND A GOOD SIZED 3005 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3876 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): GOOD SIZED 3445 CONTRACTS.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3005 CONTRACTS) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI (871) //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 3876 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR FEB. AT 49.773 TONNES PLUS FIRST DAY NOTICE OF 1.723 TONNE OZ EX. FOR RISK FOLLOWED BY TODAY’S 60,400 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 66.276 TONNES. / 3) ZERO LONG LIQUIDATION // 4) SMALL SIZED COMEX OPEN INTEREST GAIN/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: STRONG T.A.S. ISSUANCE: 3445 CONTRACTS//CONSIDERABLE SHORT COVERING AGAIN

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

FEB.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEB. :

TOTAL EFP CONTRACTS ISSUED: 63,431 CONTRACTS OR 6,343,100 OZ OR 197.29. TONNES IN 19 TRADING DAY(S) AND THUS AVERAGING: 3357 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAY(S) IN TONNES 197.29 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 197.290/3550 x 100% TONNES 5.65% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EX FOR PHYSICAL)

FEB’24: 197.29 TONNES (SHOULD BE A WEAKER ISSUANCE MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (FEB), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUGE SIZED 1384 CONTRACTS OI TO 144,741 AND CLOSER TO THE COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1450 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 1450 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1450 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1025 CONTRACTS AND ADD TO THE 1450 OI TRANSFERRED TO LONDON THROUGH EFP’S,

WE OBTAIN A GOOD SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 66 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTAL 0.330 MILLION OZ

OCCURRED WITH OUR $.03 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED DOWN 57.63 PTS OR 1.91% //Hang Seng CLOSED DOWN 253.95 PTS OR 1.51% / Nikkei CLOSED DOWN 31.49 PTS OR .08%//Australia’s all ordinaries CLOSED DOWN 0.06% /Chinese yuan (ONSHORE) closed DOWN 7.1990 //OFFSHORE CHINESE YUAN CLOSED DOWN TO 7.2142 /Oil UP TO 78.14 dollars per barrel for WTI and BRENT UP AT 82.92/ Stocks in Europe OPENED MOSTLY ALL RED EXCEPPT GERMANY// ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 871 CONTRACTS TO 411,195 WITH OUR GAIN IN PRICE OF $4.40 WITH RESPECT TO TUESDAY TRADING. ACCORDING TO OUR EXPERT ANDREW MAGUIRE, THE LOW COMEX GOLD OI WAS DUE TO THE CRIMINAL BANKS LEAVING THE GOLD ARENA AND USING THEIR “SKILLS” ON THE NEW FUTURES OF BITCOIN. WITH CENTRAL BANK BUYING PHYSICAL GOLD IN RECORD NUMBERS, IT WOULD BE FUTILE TRYING TO SELL NAKED CALLS AGAINST GOLD AS CB’S WOULD JUST TURN AROUND AND TAKE DELIVERY.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF FEB..… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS 3005 EFP CONTRACTS WERE ISSUED: : APRIL 3005 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3005 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 3876 CONTRACTS IN THAT 3005 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A GOOD SIZED GAIN OF 871 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $4.40 TUESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A GOOD SIZED 3445 CONTRACTS. THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS SOLD OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: FEB (66.276 TONNES) ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT GAINED $4.40 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A GOOD SIZED GAIN OF 3876 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH OUR HIGHER PRICE. WE HAD TO HAVE HAD ANOTHER HUGE EPISODE OF STRONG SHORT COVERING. WE HAD A GOOD T.A.S. LIQUIDATION ON THE FRONT END OF TUESDAY’S TRADING . THE T.A.S. ISSUED ON TUESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 12.055 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR FEB. (49.773 TONNES) ON FIRST DAY NOTICE ALONG WITH AN EXCHANGE FOR RISK FOR 1.7235 TONNES. THIS WAS FOLLOWED WITH TODAY’S 60,400 OZ QUEUE JUMP (1.878 TONNES//NEW TOTAL STANDING 66.276: ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $4.40

WE HAD +ADDED 176 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET GAIN ON THE TWO EXCHANGES 3876 CONTRACTS OR 387,600 OZ OR 12.055 TONNES.

estimated volume today 131,775 poor

final gold volumes/yesterday 151,103 poor

//speculators have left the gold arena

FEB 28 INITIAL FEB GOLD

/ /// THE FEB 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 13,476.371 oz Brinks Delaware JPMorgan includes 3 kilobars . |

| Deposit to the Dealer Inventory in oz | 64,035.176 oz ASAHI |

| Deposits to the Customer Inventory, in oz | 89,315.478 oz Loomis |

| No of oz served (contracts) today | 796 notice(s) 79,600 OZ 2.47858 TONNES |

| No of oz to be served (notices) | 0 contracts 0 oz 0. TONNES |

| Total monthly oz gold served (contracts) so far this month | 20,754 notices 2,075,400 oz 64.553 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

1 dealer deposits:

i) Into ASAHI: 64,035.176 oz

total dealer deposits: nil oz

total customer withdrawals: 3

i) Out of Brinks: 9981.520 oz

ii)Out of Delaware 96.453 ooz

iii)Out of JPMorgan 3398.398 oz

total withdrawal: 13,476.371 oz

we had 1 customer deposit

i) Into Loomis: 89,315.478 oz

total deposit 89,315.478

Adjustments: 1 all dealer to customer//

i)Loomis: 3,279.402 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR FEB.

For the front month of FEBRUARY we have an oi of 796 contracts having GAINED 554 contracts. We had 50 notices filed on Tuesday, so we GAINED 604 contracts or an additional 60,400 oz (1.878 tonnes) will stand for delivery at the comex.

We also had 554 notices filed under exchange for risk on first day notice for a total of 55,400 oz or 1.723 tonnes to which must be added to the delivery cycle.

Thus initial standing for gold for February is 50.136 tonnes + 1.723 tonnes = 51.859 tonnes. This was followed with today’s QUEUE jump of 60,400 oz//New standing 64.553 tonnes + 1.723 tonnes = 66.276 TONNES

March gained 71 contracts to stand at 3156

APRIL LOST 173 CONTRACTS FALLING TO 316,607.

We had 796 contracts filed for today representing 79,600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 796 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 470 notice(s) was (were) stopped ( (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the FEB. /2024. contract month, we take the total number of notices filed so far for the month (20754 x 100 oz ), to which we add the difference between the open interest for the front month of FEB. (796 CONTRACTS) minus the number of notices served upon today 796 x 100 oz per contract equals 2,015,000 OZ OR 62.675 TONNES + 1.723 Ex for Risk/prior = 64.261 tonnes

thus the INITIAL standings for gold for the FEB. contract month: No of notices filed so far (20,754) x 100 oz + (796) {OI for the front month} minus the number of notices served upon today (796) x 100 oz which equals 2,075,400 oz (64.553 TONNES) + 54,400 oz (1.723 TONNES) ex. for risk/prior// NEW total standing OR 66.276 TONNES

TOTAL COMEX GOLD STANDING FOR FEB: 66.276 TONNES WHICH IS GREAT FOR AN ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,354,385.502 42.127 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 18,259,880.491 OZ

TOTAL REGISTERED GOLD 8,088,671.657 (251.59 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,171,208.874 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,734,286 oz (REG GOLD- PLEDGED GOLD) 209.464 tonnes/dropping like a stone

END

SILVER/COMEX

FEB 28/INITIAL

//2024// THE FEB 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1020.561 oz Delaware . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 257,734.310 oz Brinks Loomis |

| No of oz served today (contracts) | 0 CONTRACT(S) (NIL OZ) |

| No of oz to be served (notices) | 0 contracts (NIL oz) |

| Total monthly oz silver served (contracts) | 1308 Contracts (6,550,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit: nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 deposits customer account:

i) Into Brinks 161,389.910 oz

ii) Into Loomis: 96,344.400 oz

total customer deposits 251,734.310 oz

JPMorgan has a total silver weight: 129.806 million oz/282.005 million or 46.26%

adjustment: customer to dealer/ASAHI 585,748.610 oz

dealer to customer JPM 315l,324.674 oz

Comex withdrawals: 0

i)Delaware 1020.561 oz

total withdrawal: 1020.561 oz

TOTAL REGISTERED SILVER: 49.378 MILLION OZ//.TOTAL REG + ELIGIBLE. 282.075 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF FEB. /2023 OI: 0 CONTRACTS HAVING LOST 4 CONTRACT(S). WE HAD 4 NOTICES FILED ON TUESDAY SO WE GAINED 0 CONTRACT OR AN ADDITIONAL NIL OZ OF SILVER CONTRACTS WILL STAND FOR DELIVERY AT THE COMEX

MARCH LOST 11,027 CONTRACTS TO 6773. WE HAVE 1 MORE READING DAYS BEFORE FIRST DAY NOTICE.

APRIL SAW A GAIN OF 196 CONTRACTS TO STAND AT 773

MAY SAW A GAIN OF 9232 CONTRACTS UP TO 113,923.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 10 for 50,000 oz

Comex volumes// est. volume today 49,805 poor

Comex volume: confirmed yesterday 89,189 excellent

To calculate the number of silver ounces that will stand for delivery in FEB. we take the total number of notices filed for the month so far at 1308 x 5,000 oz = 6,540,000 oz

to which we add the difference between the open interest for the front month of FEB. (0) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the FEB/2024 contract month: 1308 (notices served so far) x 5000 oz + OI for the front month of FEB. (0) – number of notices served upon today (0 )x 500 oz of silver standing for the FEB contract month equates to 6.540 MILLION OZ. + .445 MILLION OZ EX. FOR RISK PRIOR//NEW TOTAL 6.985 MILLION OZ

New total standing: 6.985 million oz.

There are 49.108 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

FEB28/WITH GOLD DOWN $1.00 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RESTS AT 826.94 TONNES

FEB27/WITH GOLD UP $4.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF .87 TONNES OF GOLD FROM THE GLD:/INVENTORY RESTS AT 826.94 TONNES

FEB26/WITH GOLD DOWN $8.90 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 827.81 TONNES

FEB23/WITH GOLD UP $17 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD.//INVENTORY RESTS AT 827.81 TONNES

FEB22/WITH GOLD DOWN $2.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD://INVENTORY RESTS AT 829.82 TONNES

FEB21/WITH GOLD DOWN $5.30 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 7.59 TONNES OF GOLD OUT OF THE GLD///INVENTORY RESTS AT 29.82 TONNES

FEB20/WITH GOLD UP $16.15 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 0.58 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 837.89 TONNES

FEB16/WITH GOLD UP $8,60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD///INVENTORY RESTS AT 837.31 TONNES

FEB15/WITH GOLD UP $11.70 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB14/WITH GOLD DOWN $2.75 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB13/WITH GOLD DOWN $20.15 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/INVENTORY RESTS AT 841.92 TONNES

FEB12/WITH GOLD DOWN $4.80 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG WITHDRAWAL OF 1.74 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 841.92 TONNES

FEB9/WITH GOLD DOWN $8.60 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A STRONG DEPOSIT OF 1.44 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 843.66 TONNES

FEB8/WITH GOLD DOWN $2.70 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 5.47 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 842.22 TONNES:

FEB7/WITH GOLD UP $0.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A MASSIVE WITHDRAWAL OF 4.04 TONNES OF GOLD FROM THE GLD. / //://INVENTORY RESTS AT 847.69 TONNES:

FEB6/WITH GOLD UP $8.50 TODAY NO CHANGES IN GOLD INVENTORY AT THE GLD:/ / //://INVENTORY RESTS AT 851.73 TONNES:

FEB5/WITH GOLD DOWN $9.85 TODAY SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF .58 TONNES OF GOLD INTO THE GLD// / //://INVENTORY RESTS AT 851.73 TONNES:

FEB 2/WITH GOLD DOWN $17.95 TODAY SMALL CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF .58 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 851.15 TONNES:

FEB 1/WITH GOLD UP $5.00 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.73 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 851.15 TONNES:

JAN 31/WITH GOLD UP $16.40 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 852.88 TONNES:

JAN 30/WITH GOLD UP $6.50 TODAY HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 1.16 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 854.89 TONNES:

TOTAL IN LAST 18 DAYS WITHDRAWAL OF 14.12 TONNES

JAN 29/WITH GOLD UP $8.70 TODAYHUGE CHANGES IN GOLD INVENTORY AT THE GLD:A WITHDRAWAL OF 2.88 TONNES OF GOLD FROM THE GLD// / //://INVENTORY RESTS AT 856.05 TONNES

JAN 26/WITH GOLD DOWN $0.10 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 25/WITH GOLD UP $2.50 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 24/WITH GOLD DOWN $9.75 TODAY:NO CHANGES IN GOLD INVENTORY AT THE GLD: / //://INVENTORY RESTS AT 858.93 TONNES

JAN 23/WITH GOLD UP $3.95 TODAY:HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 2.02 TONNES OF GOLD FROM THE GLD/ //://INVENTORY RESTS AT 858.93 TONNES

GLD INVENTORY: 826.04 TONNES

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

FEB 28/WITH SILVER DOWN 7 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 5.123 MILLION OZ INTO THE SLV//// : SLV INVENTORY RESTS AT 433.086 MILLION OZ

FEB 27/WITH SILVER UP 3 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.64 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 427.943 MILLION OZ

FEB 26/WITH SILVER DOWN 44 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.065 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 428.603 MILLION OZ

FEB 23/WITH SILVER DOWN 44 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.065 MILLION OZ FROM THE SLV//// : SLV INVENTORY RESTS AT 428.603 MILLION OZ

FEB 22/WITH SILVER DOWN 10 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV

// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 21/WITH SILVER DOWN 28 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 2.348 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 432.766 MILLION OZ

FEB 20/WITH SILVER DOWN 33 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 3.385 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 435.008 MILLION OZ

FEB 16/WITH SILVER UP 53 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.235 MILLION OZ OF SILVER FROM THE SLV// : SLV INVENTORY RESTS AT 438.393 MILLION OZ

FEB 15/WITH SILVER UP 56 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 14/WITH SILVER UP 24 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV : SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 13/WITH SILVER DOWN 60 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL WITHDRAWAL OF 0.504 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 437.615 MILLION OZ

FEB 12/WITH SILVER UP 14 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 1.921 MILLION OZ OZ OUT OF THE SLV: SLV INVENTORY RESTS AT 438.119 MILLION OZ

FEB 9/WITH SILVER DOWN 4 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV A SMALL DEPOSIT OF 600,000 OZ INTO THE SLV: SLV INVENTORY RESTS AT 440.040 MILLION OZ

FEB 8/WITH SILVER UP 29 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: SLV INVENTORY RESTS AT 439.994 MILLION OZ

FEB 7/WITH SILVER DOWN 18 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 4.04 MILLION OZ INTO THE SLV///INVENTORY RESTS AT 439.994 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 6/WITH SILVER UP 11 CENTS TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: /INVENTORY RESTS AT 435.144 MILLION OZ//LAST 9 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 5/WITH SILVER DOWN 32 CENTS TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.345 MILLION OZ FROM THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 435.144 MILLION OZ//LAST 8 DAYS: 10.7598 MILLION OZ WITHDRAWAL

FEB 2/WITH SILVER DOWN 50 CENTS TODAY SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.58 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 438.489 MILLION OZ//LAST 7 DAYS: 14.105 MILLION OZ WITHDRAWAL

FEB 1/WITH SILVER UP 7 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.19 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 438.947 MILLION OZ//LAST 6 DAYS: 10.3018 MILLION OZ WITHDRAWAL

JAN 31/WITH SILVER DOWN 8 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.7438 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 440.137 MILLION OZ//LAST 5 DAYS: 9.1118 MILLION OZ WITHDRAWAL

JAN 30/WITH SILVER DOWN 5 CENTS TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.876 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 442.699 MILLION OZ//LAST 4 DAYS: 7.368 MILLION OZ WITHDRAWAL

JAN 29/WITH SILVER UP $.37 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.105 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 444.575 MILLION OZ

JAN 26/WITH SILVER DOWN $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.556 MILLION OZ INTO THE SLV(FAIRY TALES) // /INVENTORY RESTS AT 446.680 MILLION OZ

JAN 25/WITH SILVER UP $0.03 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.831 MILLION OZ INTO THE SLV(FAIRY TALES) // /NVENTORY RESTS AT 448.236 MILLION OZ

JAN 24/WITH SILVER UP $0.44 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: ANOTHER DEPOSIT OF 1.375 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 450.067 MILLION OZ

JAN 23/WITH SILVER UP $0.21 TODAY MEGA CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 16.201 MILLION OZ INTO THE SLV(FAIRY TALES) // //INVENTORY RESTS AT 448.694 MILLION OZ

JAN 22/WITH SILVER DOWN $0.45 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 19/WITH SILVER DOWN $0.11 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 458,000 OZ OUT OF THE SLV // //INVENTORY RESTS AT 432.493 MILLION OZ

JAN 18/WITH SILVER UP $0.13 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 432.951 MILLION OZ

JAN 17/WITH SILVER DOWN $0.38 TODAY HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 779,000 OZ FROM THE SLV.: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 16/WITH SILVER DOWN $0.08 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

JAN 12/WITH SILVER UP $0.62 TODAY NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY RESTS AT 433.500 MILLION OZ

CLOSING INVENTORY 433.086 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1:Peter Schiff/Mike Maharrey

end

2.Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens/ CLAUDIO GLASS

END

3. CHRIS POWELL//GATA GOLD COMMENTARIES: daily Dispatches

German financial magazine interviews GATA secretary on gold price suppression

Submitted by admin on Tue, 2024-02-27 17:19 Section: Daily Dispatches

5:17p ET Monday, February 27, 2024

Dear Friend of GATA and Gold:

Rainer Kromarek of the German financial magazine Smart Investor has just interviewed your secretary/treasurer about gold price suppression and what it will take for the monetary metal to break free of its central bank chains.

The interview can be found at the Smart Investor internet site —

— and is easily translated to English by modern internet browsers.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Why? what are they afraid of?

(GATA)

Fed chairman Powell refuses to answer congressman’s questions on gold repatriation

Submitted by admin on Wed, 2024-02-28 13:42 Section: Daily Dispatches

By Ken Silva

HeadlineUSA, Charlotte, North Carolina

Wednesday, February 28, 2024

Concerned about a weaponized financial system, many countries have signaled plans to remove their gold and other assets from the United States in the wake of the unprecedented Western sanctions imposed on Russia over its invasion of Ukraine.

And at least one congressman is demanding answers from the Federal Reserve as to how much foreign gold has actually been removed from U.S. shores so far.

According to a 2023 Invesco survey, a “substantial percentage” of central banks expressed concern about how the U.S. and its allies froze nearly half of Russia’s $650 billion gold and forex reserves. One anonymous central banker told Invesco that his country quietly repatriated its gold from London, and some 68% of the banks surveyed said they are keeping their gold reserve within their country’s borders—up from 50% in 2020. …

… For the remainder of the report:

https://headlineusa.com/fed-chair-tight-lipped-on-foreign-nations-evacuation-of-gold-from-u-s

4. OTHER GOLD COMMENTARIES/PODCASTS/

END

5 a. IMPORTANT COMMENTARIES ON COMMODITIES /

END

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.1991

OFFSHORE YUAN: DOWN TO 7.2142

SHANGHAI CLOSED DOWN 57.63 PPTS OR 1.91%

HANG SENG CLOSED DOWN 253.95 PTS OR 1.51%

2. Nikkei closed DOWN 31.49 PTS OR .08%

3. Europe stocks SO FAR: MOSTLY ALL RED EXCEPT GERMANY

USA dollar INDEX UP TO 104.05 EURO FALLS TO 1.0812 DOWN 29 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.692 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 150.65/JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN/ OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund UP TO +2.4495***/Italian 10 Yr bond yield UP to 3.896* /SPAIN 10 YR BOND YIELD UP TO 3.339…**

3i Greek 10 year bond yield UP TO 3.389

3j Gold at $2030.20 silver at: 22.39 1 am est) SILVER NEXT RESISTANCE LEVEL AT $30.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 42 /100 roubles/dollar; ROUBLE AT 91.63//

3m oil into the 78 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 150.65// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.692% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8801 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9518 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

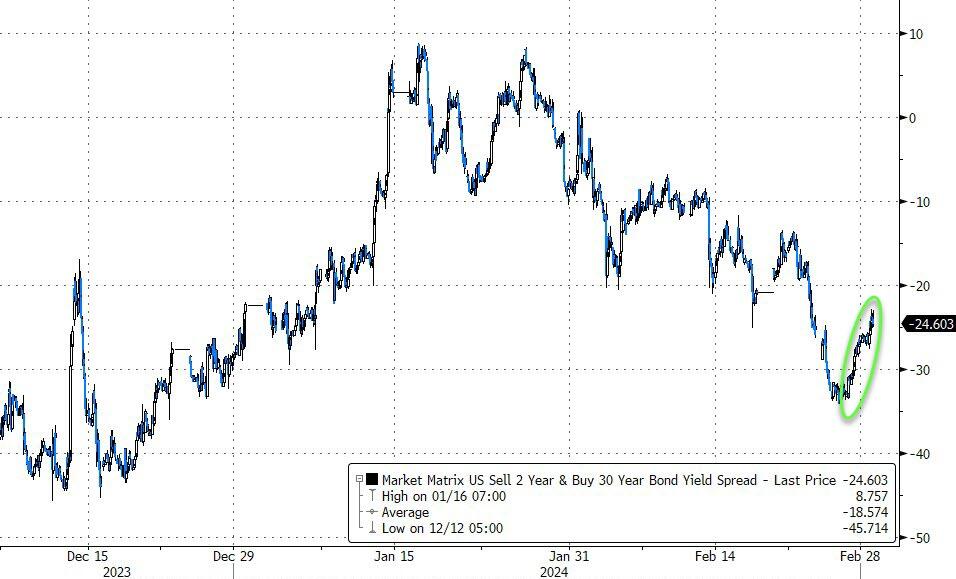

USA 10 YR BOND YIELD: 4.287 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.417 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.683 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 31.19…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 4 BASIS PTS AT 4.220

end

2.a Overnight: Newsquawk and Zero hedge

Future Slide As Hawkish Fed Concerns Return

WEDNESDAY, FEB 28, 2024 – 08:16 AM

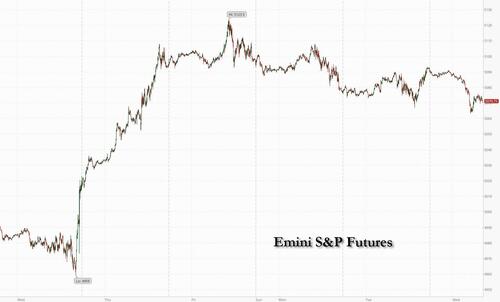

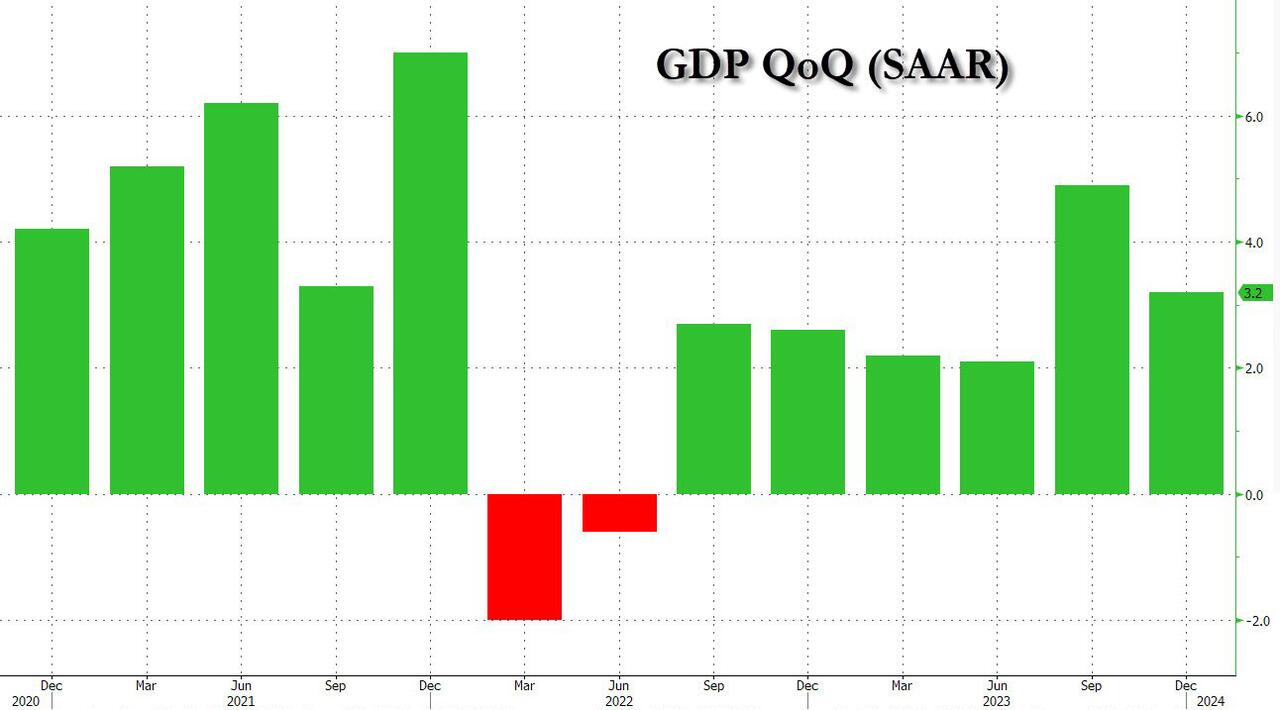

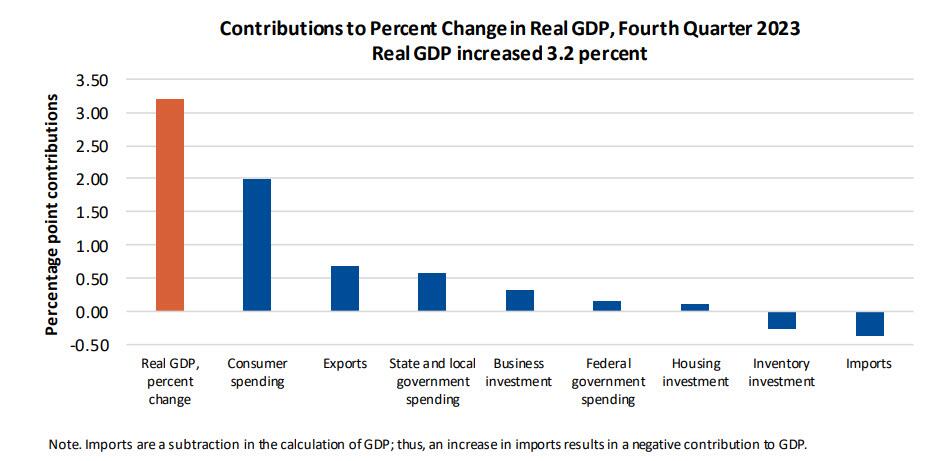

US stock futures slumped, pointing to a weak open on Wall Street with both Tech and small-caps underperforming, as traders braced for today’s revised GDP print and tomorrow’s core PCE report which whisper sees coming in hotter than expected and may further push back on expectations for rate cuts.

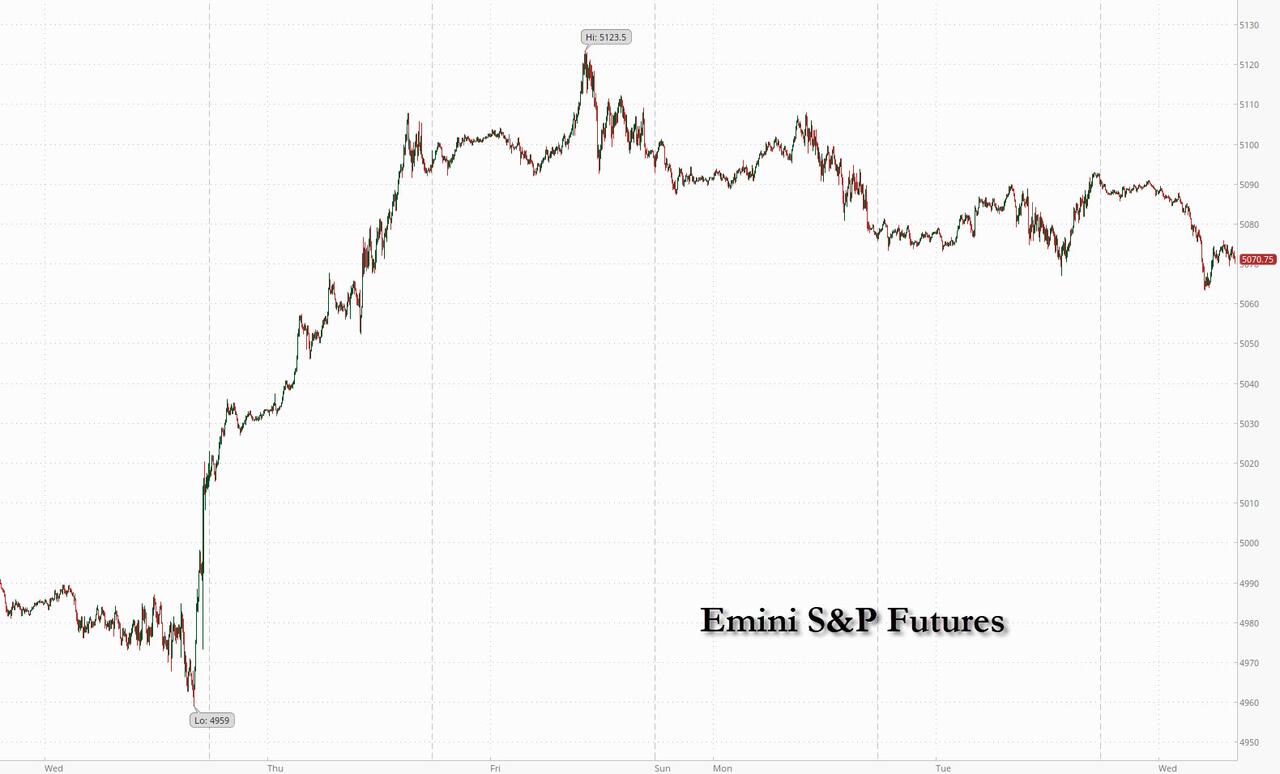

As of 7:50am, contracts on the Nasdaq 100 drop 0.5%, while S&P 500 futures down 0.4% as European stocks hovered below record high while Asia was dragged lower by Chinawhere regulators are taking steps to shrink the size of a popular quantitative trading strategy “Direct Market Access” that contributed to turmoil in the nation’s stock market this month. Bond yields are lower, and the USD is stronger, while commodities are mixed with base metals higher and energy lower. Bitcoin surged again rising just shy of $60K following record inflows into the Blackrock bitcoin ETF. The macro data focus will be on details surrounding the second estimate of Q4 GDP, as well as the latest inventory data (the more important data kicks off tomorrow with PCE and then Friday’s ISM number). Today’s price action may be more about month-end rebalancing where JPM’s Quant & Derivs Strategy team thinks that we could see stocks lose as much as 1.5% on the rebalance and that rebalancing moves can occur before month-end.

In premarket trading, Nvidia dropped 1.3% in premarket trading, dragging the megacap sector lower. Here are some other notable premarket movers:

- Ambarella (AMBA) gains 7% after the company projected revenue for the first quarter that topped the average analyst estimate at the midpoint.

- Array (ARRY) slips 6% following its earnings, which prompted BNP Paribas to downgrade the renewable energy equipment maker and give the stock its only negative analyst rating.

- Beyond Meat (BYND) soars 61% after it reported fourth-quarter sales that surpassed expectations.

- Bumble (BMBL) falls 10% after the online dating company issued first-quarter guidance that was weaker than forecast. The company is cutting about one-third of its workforce after a recent executive shakeup.

- Coupang (CPNG) jumps 8% after South Korea’s largest online retailer reported its fastest revenue growth since 2021.

- Credo Technology (CRDO) gains 7% after the communications equipment company reported earnings that prompted a price target raise at Cowen, which said the results signal the company is “well past the bottom”

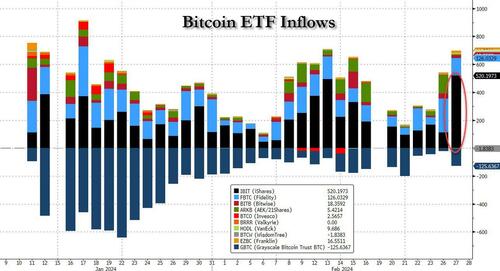

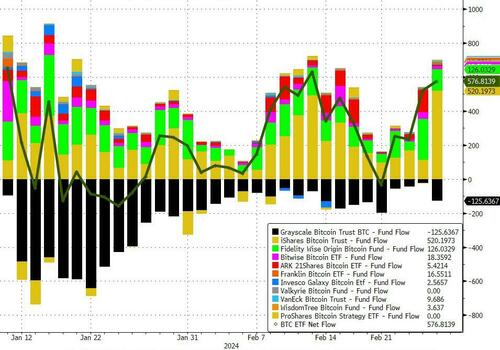

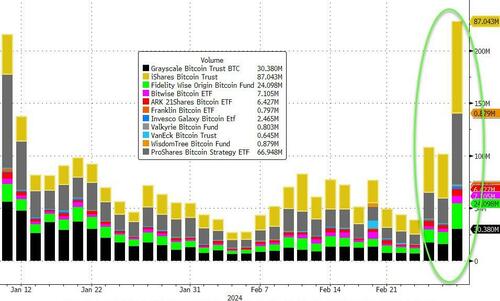

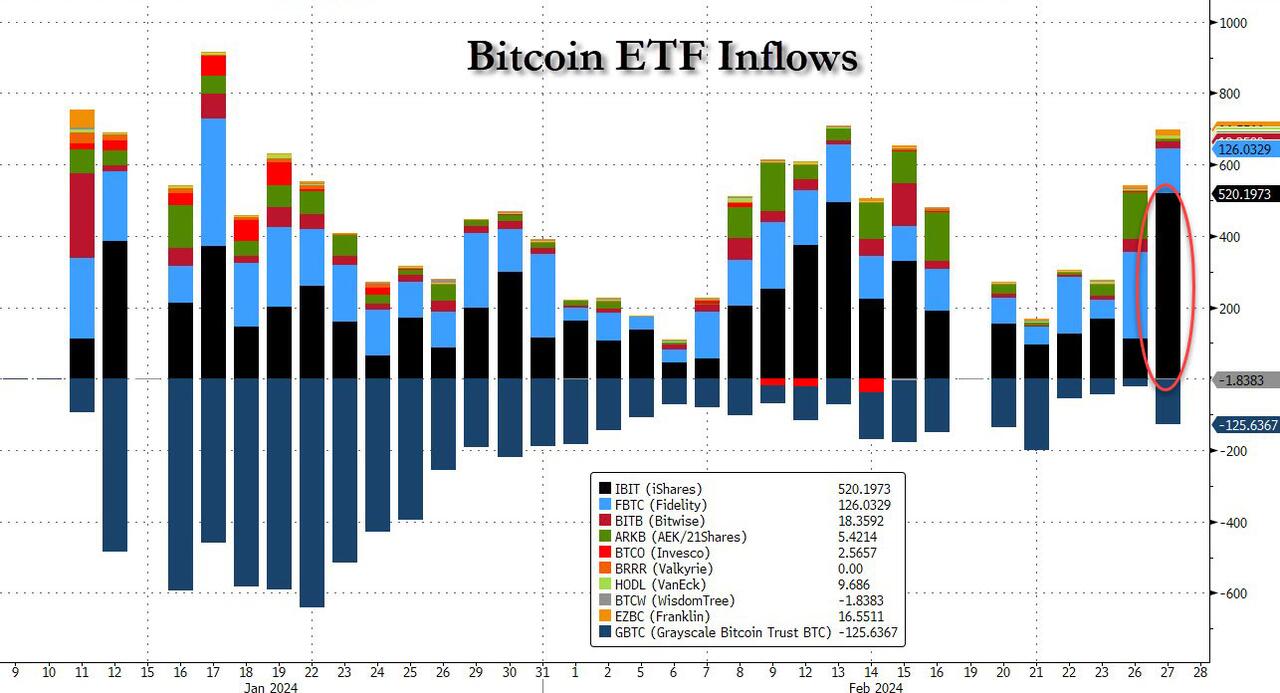

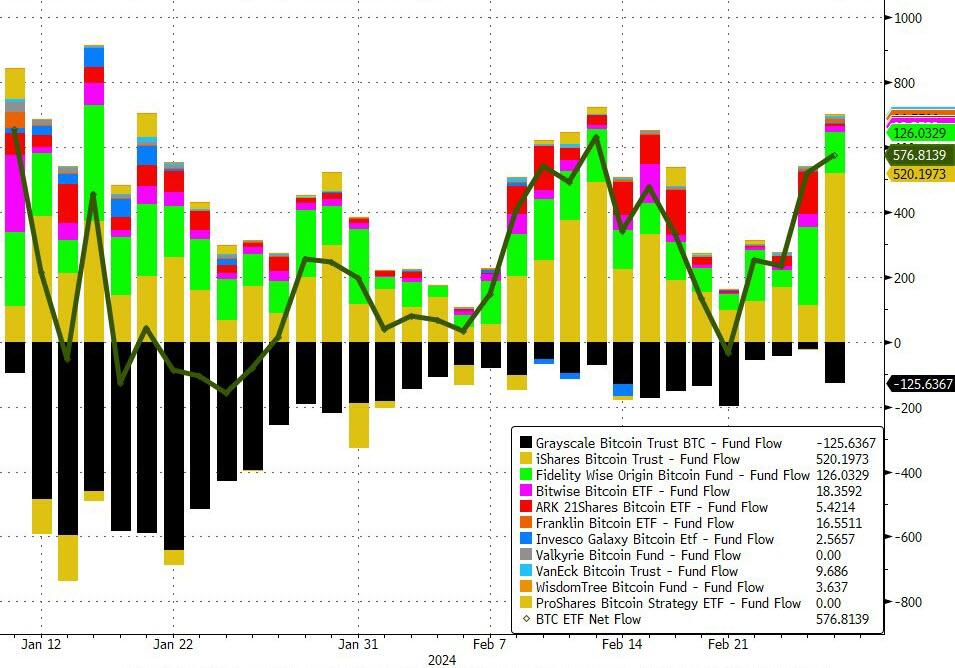

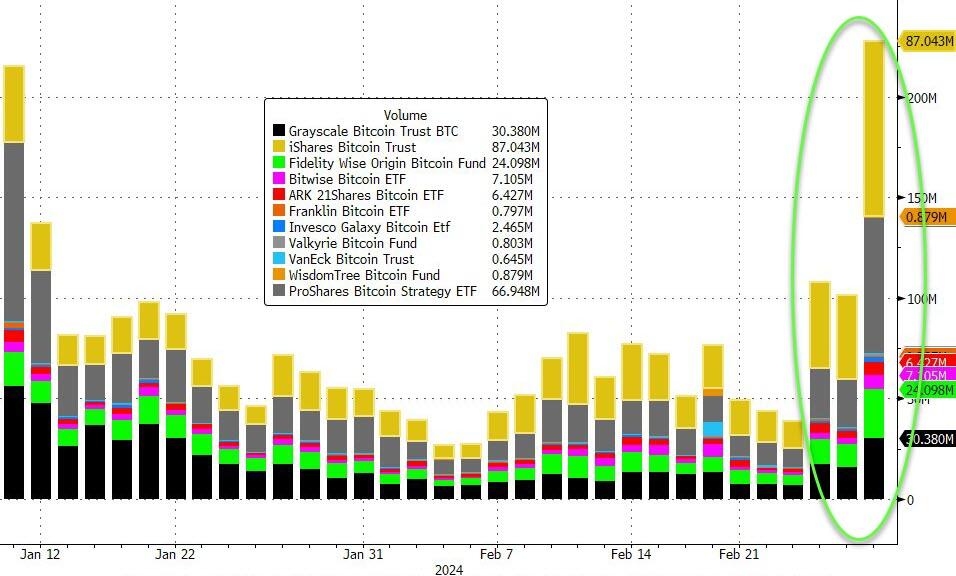

Cryptocurrency-linked stocks gained as Bitcoin advanced for a fifth day, on track for its biggest monthly increased since October 2021. The launch of spot Bitcoin exchange-traded funds in the US in early January has driven a surge in buying, overcoming concerns over slower Fed rate cuts. Bitcoin climbed above $59,000 Wednesday, up almost 40% in the month.

Aside from earnings, attention will be on the latest US GDP print and tomorrow’s inflation numbers and a strong line-up of central bank speakers. Investors are contending with an erosion in expectations for how much the Federal Reserve and European Central Bank will lower rates.

“In December, markets priced sizeable rate cuts in 2024, but what’s happened is we have had slightly problematic inflation prints in most parts of the world,” said Guy Miller, chief market strategist at Zurich Insurance Co. “The US economy has done better than what many people expected, the labor market remains tight and wage gains have been higher than what central bankers are comfortable with.”

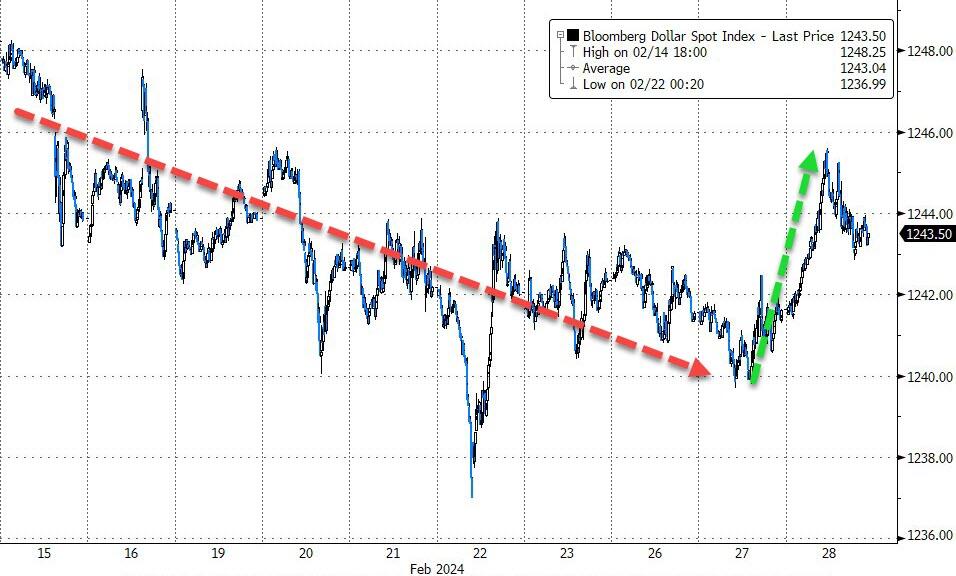

Meanwhile, traders have moved to price only 75 basis points of US easing by year-end, in line with what Fed policymakers in December indicated is the likeliest outcome. Treasury yields dipped Wednesday, while a gauge of the dollar strengthened to the highest since Feb. 20.

In Europe, the Stoxx 600 index edged 0.2% lower as investors digested the latest earnings; telecoms and insurance stocks outperforme while personal care stocks are the worst performers, led lower by Reckitt Benckiser, whose sales missed expectations and its shares tumbled 12%, the most since 2008, after the consumer goods company said its sales fell. Tech was also hit after Dutch chip gear firm ASM International slipped as it projected revenue for this quarter that fell far below market expectations. Here are the biggest movers Wednesday:

- Glanbia rose as much as 7.2% on the Irish stock exchange, the most in almost a year, after publishing strong full-year results and announcing a share buyback program.

- Alcon rose as much as 6% after releasing results after the market close on Tuesday that were seen as positive by analysts. Highlights include the Swiss eye-care producer’s above-consensus guidance.

- UCB shares gained as much as 5.1%, to the highest since May 2022, after the biopharmaceutical company reported earnings for the year that beat analysts’ estimates. Citigroup noted the profit share of its Evenity osteoporosis drug is “under-appreciated.”

- Reckitt Benckiser shares drop as much as 10%, hitting their lowest level since March 2020, after the household-goods maker reported a surprise fall in like-for-like sales in the final quarter of 2023, missing expectations across the board.

- St James’s Place plunged as much as 33% after the wealth management firm reported an adjusted pretax loss for the full year, with analysts flagging an ongoing service charge issue and a sharp dividend cut.

- ASM International declined as much as 6.1% in Amsterdam after the chip equipment maker gave a weaker-than-expected forecast for the current quarter, showcasing the challenge in near-term demand before an expected improvement later this year.

- Worldline plunged as much as 17% after the French payment processor reported a net loss of €817 million for 2023 due to goodwill impairments. The results and guidance met lowered expectations, yet investors are still cautious.

- Just Eat Takeaway falls as much as 7.6% in Amsterdam after the food delivery firm issued guidance for 2024 revenue growth which analyst considered cautious.

Earlier in the session, Asian stocks closed lower, dragged by China where the CSI 300 Index dropped as much as 1.3% to touch session low following a report that regulators are taking steps to gradually shrink the size of a popular quantitative trading strategy. Some quantitative funds that manage money for external clients were told to stop accepting new inflows and phase out existing products for “Direct Market Access.” Small-cap indexes fall more: CSI 1000 Index drops as much as 4.5% and CSI 2000 Index -6.8%. Meanwhile, Hong Kong stocks slumped more than 1% as the city’s budget report failed to impress investors. Chinese stocks fell after a recent rally took gauges to resistance levels, with traders looking to this week’s manufacturing report and a key political meeting in Beijing next week for momentum.

“This move to deleverage could lead to an extended drop and might be a replay of the slump in January. This is hits across all gauges, as quants usually hold thousands of stocks at once, and the unexpected move leads to a wave of selling,” says Chen Zunde, fund manager ate Guangdong Fund Investment Co.

- Hang Seng and Shanghai Comp. were pressured amid initial developer-related concerns after a wind-up petition was filed against Country Garden, although the property sector in Hong Kong then recovered after the government announced the cancellation of all demand-side property tightening measures for residential.

- ASX 200 was indecisive with tech strength offset by weakness in telecoms, consumer stocks and financials, while data showed softer-than-expected monthly CPI in January and a miss on Construction Work Done for Q4.

- Nikkei 225 lacked conviction but remained above the 39,000 level in the absence of any pertinent catalysts.

In FX, the dollar has benefited from the risk-off mood. The Bloomberg Dollar Spot Index rises 0.2% as the greenback gains versus all its G-10 rivals. The kiwi is the weakest, falling 1.2% versus the dollar after the RBNZ softened its threat of a hike amid signs inflation pressures are waning. Elsewhere, the New Zealand dollar slid more than 1% after the Reserve Bank of New Zealand delivered less hawkish comments on inflation, citing how most measures of price expectations have fallen. Meanwhile, Nigeria’s naira weakened to a fresh low after a much-bigger-than-expected 400 basis point interest rate increase by the central bank on Tuesday failed to support the currency. The naira has been sapped by a local scarcity of dollars and an outstanding backlog of demand for the greenback

In rates, treasury futures hold small gains accumulated during early London session as bunds and gilts advanced, with yields richer by 1bp-2bp across the curve. Weakness in US technology shares pressures S&P 500 futures, further supporting Treasuries. 10-year Treasury yields at 4.29% are ~2bp richer on the day with bunds slightly outperforming and gilts lagging by less than 1bp in the sector; Tuesday’s notable curve-steepening move remains intact with 2s10s and 5s30s trading near top of Tuesday range. IG dollar issuance slate already includes a few names; seven issuers priced $8.5b Tuesday, leaving weekly total already above the $35b expected. Borrowers paid concessions of less than 2bps driven by order books said to be 3.3 times oversubscribed. US session highlights include 4Q GDP revision, and corporate issuance slate is expected to remain busy.

In commodities, oil fell after a two-day gain as signs of higher US inventories vied with expectations that OPEC+ will extend supply cuts. WTI fell 1.1% to trade near $78. Iron ore resumed its slide, as investors remained undecided about the strength of China’s demand for steel ahead of the nation’s usual peak construction season. Spot gold falls 0.2%.

Bitcoin continues to soar and currently holds just shy of the $60k mark less than $10k away from a new all time high, boosted by a record inflow into the IBIT ETF.

Looking at today’s calendar, US economic data includes second estimate of 4Q GDP, January advance goods trade balance and wholesale inventories (8:30am). Fed speakers scheduled include Bostic (12pm), Collins (12:15pm) and Williams (12:45pm).

Market Snapshot

- S&P 500 futures down 0.4% to 5,071.50

- STOXX Europe 600 down 0.2% to 495.55

- MXAP down 0.7% to 172.05

- MXAPJ down 0.8% to 523.37

- Nikkei little changed at 39,208.03

- Topix down 0.1% to 2,674.95

- Hang Seng Index down 1.5% to 16,536.85

- Shanghai Composite down 1.9% to 2,957.85

- Sensex down 0.8% to 72,478.32

- Australia S&P/ASX 200 little changed at 7,660.42

- Kospi up 1.0% to 2,652.29

- German 10Y yield little changed at 2.45%

- Euro down 0.4% to $1.0803

- Brent Futures down 0.9% to $82.92/bbl

- Brent Futures down 0.9% to $82.92/bbl

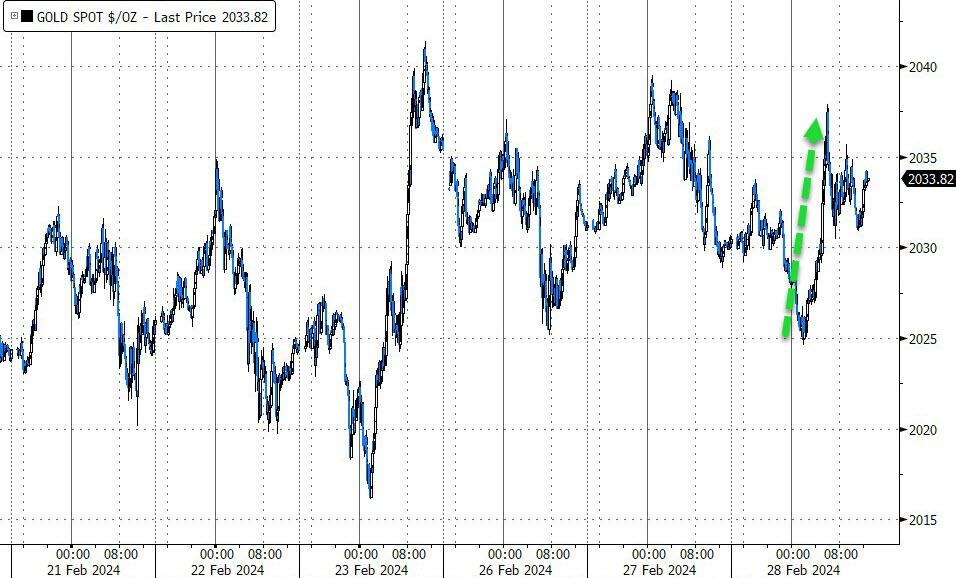

- Gold spot down 0.2% to $2,025.50

- U.S. Dollar Index up 0.35% to 104.20

Top Overnight News

- European stocks struggled for traction and US futures slipped as traders brace for a slew of economic data in the second half of the week that will help determine the path of monetary policy.

- Goldman Sachs Group Inc. Chief Executive Officer David Solomon said softer spending by consumers calls into question expectations that the US economy will avoid a recession.

- US President Joe Biden and Republican frontrunner Donald Trump both cruised to victory in their party’s Michigan primary elections Tuesday, with results for the two candidates indicating discontent among Democrats and Republicans for the likely nominees.

- Bond traders no longer expect the Federal Reserve to lower interest rates by more than 75 basis points this year, bringing their view in line with what Fed policy makers have indicated is the likeliest outcome.

- Europe’s biggest asset manager is joining a chorus of investors who are turning bearish on Switzerland’s franc after slowing inflation has eliminated the need for the central bank to prop up the currency.

- Chinese regulators are taking steps to gradually shrink the size of a popular quantitative trading strategy that contributed to turmoil in the nation’s stock market this month, according to people familiar with the matter.

Earnings

- Baidu Inc (BIDU) Q4 2023 (USD): EPS 3.08 (exp. 2.48), Revenue 4.92bln (exp. 4.86bln) Shares -1.2% in pre-market trade

- eBay Inc (EBAY) – Q4 2023 (USD): Adj. EPS 1.07 (exp. 1.03), Revenue 2.56bln (exp. 2.51bln); authorised additional 2bln share repurchase programme and raises quarterly cash dividend 8% to 0.27/shr. Shares +3.2% in pre-market trade

- Beyond Meat (BYND) Q4 2023 (USD): Revenue 73.7mln (exp. 66.8mln), Adj. EBITDA loss 125mln (exp. loss 47mln); FY revenue view 315-345mln (exp. 344mln) Shares +55% in pre-market trade

- ASM International (ASM NA) – Q4 (EUR): Normalised Net 100mln (exp. 137mln, prev. 142mln Y/Y), Normalised Op. 141mln (prev. 190mln Y/Y), Revenue 633mln (exp. 647mln, prev. 725mln Y/Y), Launches 150mln share buyback. Raises dividend to 2.75/shr (prev. 2.50/shr). Guides Q1 Revenue 600-640mln. (Newswires) Shares -3.7% in European trade / peer Nvidia (-1.2% pre-market) lags

- Reckitt (RKT LN) – Q4 (GBP): LFL Sales -1.2% (exp. 1.75%), FY LFL Sales +3.5% (exp. 4.15%), Revenue 3.56bln (exp. 3.6bln). Sees 2024 capital expenditure to be 3-3.5% of Net Revenue. Sees 2024 adj. operating profit to grow ahead of net revenue growth. Shares -10.1% in European trade

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded cautiously and followed suit to the rangebound performance seen on Wall St where stocks largely ignored weak US data ahead of key events, while the region also digested a couple of data releases and the RBNZ policy announcement. ASX 200 was indecisive with tech strength offset by weakness in telecoms, consumer stocks and financials, while data showed softer-than-expected monthly CPI in January and a miss on Construction Work Done for Q4. Nikkei 225 lacked conviction but remained above the 39,000 level in the absence of any pertinent catalysts. Hang Seng and Shanghai Comp. were pressured amid initial developer-related concerns after a wind-up petition was filed against Country Garden, although the property sector in Hong Kong then recovered after the government announced the cancellation of all demand-side property tightening measures for residential.

Top Asian News

- Hong Kong Financial Secretary Chan said in the budget address that momentum for economic recovery needs to be improved amid global challenges. Chan announced the government is to cancel all demand-side property tightening measures for residential and noted there is room to further adjust measures for the property market, while it will waive stamp duties payable on transfer of REIT units.

- HKMA said the maximum loan-to-value ratios will be adjusted to 70% for self-occupation residential properties valued at HKD 30mln or less, while the maximum LTV ratio will be adjusted from 50% to 60% for non-self-use residential properties.

- RBNZ kept the OCR unchanged at 5.50% as expected, while it slightly lowered its OCR projections and said the OCR needs to remain at a restrictive level for a sustained period. The committee remains confident that the current level of the OCR is restricting demand but also noted that headline inflation remains above the 1%-3% target band, limiting the committee’s ability to tolerate upside inflation surprises. Furthermore, the RBNZ reduced its OCR forecast with the June 2024 view lowered to 5.59% from 5.67% and the March 2025 view lowered to 5.47% from 5.56%.

- RBNZ Governor Orr said during the press conference Q&A that they did discuss a hike in rates and there was strong consensus that the current level of rates was sufficient, while he added that many variables have given them confidence that policy is working and noted that underlying inflation is still a concern, but headline inflation is easing.

- China reportedly tells quants to phase out Direct Market Access (DMA) products blamed for turmoil, according to Bloomberg sources; Chinese markets extended losses following this news.

- PBoC governor and Shanghai party chief held a seminar on Tuesday; PBoC supports Shanghai’s high-level opening up financially

European bourses, (Stoxx600 -0.1%), are mixed, but with clear underperformance in the AEX (-0.7%), after poor results from chip-maker ASM International (-3.8%). European sectors hold a negative tilt; Optimised Personal Care Drug and Grocery is dragged down by Reckitt (-8.9%) post-earnings, whilst Mercedes-Benz (+1.7%) drives Autos higher. US Equity Futures (ES -0.5%, NQ -0.9%, RTY -0.8%) are entirely in the red, paring back most of the gains seen in the prior session, with underperformance in the NQ hampered by Nvidia (-1.9% pre-market).

Top European News

- ECB’s de Guindos says recent inflation outlook has been very positive and prices will continue to decline; we need to be sure that prices will move towards our 2% target

FX

- USD is making gains vs. all peers with January PCE data tomorrow expected to come in hot. DXY has reclaimed 104 status and taken out its 100, 10 and 21DMAs as well as a cluster of highs from last week. Current high today at 104.24.

- EUR is hampered by the broadly firmer USD with EUR/USD oscillating around the 1.08 mark after taking out yesterday’s low of 1.0812.

- GBP is dragged lower by the USD after yesterday’s failure to test 1.27 to the upside. Session low currently sits at 1.2622 with the 22nd Feb low at 1.2612.

- USD/JPY remains arguably the most important pair to watch after printing a high of 150.79 with the YTD peak just above at 150.88. The further the pair climbs, the more likely is jawboning from Japanese officials and speculation over intervention.

- NZD is the standout laggard across the majors as the RBNZ stood pat on rates vs. a 30% chance of a hike accompanied by dovish tweaks to the OCR projections. NZD/USD has erased all of last week’s gains and slipped below the 0.61 mark with the next downside support via its 100DMA at 0.6091. AUD lower in sympathy as well as the region’s soft inflation metrics overnight.

- PBoC set USD/CNY mid-point at 7.1075 vs exp. 7.2023 (prev. 7.1057).

Fixed Income

- USTs are marginally firmer with specifics light and perhaps some follow-through from the dovish RBNZ OCR projections in the absence of other drivers. Action which comes after Tuesday’s bear-steepening.

- Bunds are modestly firmer with specifics light and the focus once again on supply. Bunds are eking out marginal new highs of 132.41 seemingly as US equity futures deteriorate further, but ultimately remains comfortably within yesterday’s 132.02-71 range.

- Gilt price action is similar to that seen in EGBs with Gilts also able to eke out some very marginal gains but well within Tuesday’s 97.22-98.15 bounds; a UK outing produced a wide 2.2bps tail, resulting in modest pressure in Gilts.

- UK sells GBP 4.0bln 4.00% 2031 Gilt: b/c 3.0x, average yield 4.085%, tail 2.2bps.

- Italy sells EUR 8.25bln vs exp. EUR 7.50-8.25bln 3.35% 2029 & 3.85% 2034 BTP and EUR 1.5bln vs exp. EUR 1.00-1.50bln 2031 CCTeu.

- Orders for Italy’s new 6yr BTP Valore retail bond reaches 12bln since the start of the odder, according to bourse data cited by Reuters

Commodities

- A downbeat session for the broader crude complex in what is seemingly a function of a firmer Dollar and a subdued risk tone. Brent May futures have slipped below USD 82.00/bbl.

- The firmer Dollar exerts broader pressure on precious metals, although losses are capped ahead of key US data alongside a number of Fed speakers; XAU approaches USD 2,025/oz to the downside after falling under its 50 DMA at 2,032.15/oz.

- Base metals are softer across the board amid the aforementioned pressure from the stronger Greenback, whilst Chinese markets overnight continued to tumble despite intervention from regulators.

- US Private Energy Inventory (bbls): Crude +8.4mln (exp. +2.7mln), Cushing +1.8mln, Gasoline -3.3mln (exp. -1.5mln), Distillate -0.5mln (exp. -2.1mln)

- Trafigura Chief Economist says oil market talk has shifted to upside risk; oil spreads show a relatively tight market, via Bloomberg TV.

- Citi upgrades 0-3m Palladium price targe price forecast to USD 1200/oz (prev. 950/oz) on the prospect of imminent supply cuts; bounce would present a tactical opportunity for spec selling and producer hedging; sees structural long-term downtrend.

Geopolitics: Middle East

- US Central Command said a US aircraft and a coalition warship shot down five Houthi one-way attack unmanned aerial vehicles in the Red Sea on Tuesday, according to Reuters.

- “Israeli sources: The Israeli delegation returned from Doha after two days of negotiations on the detainee deal without progress”, according to Sky News Arabia

Geopolitics: Other

- China’s Vice Foreign Minister Sun Weidong conducted consultations in Moscow where he met with his counterpart and the Russian Foreign Minister, while he stated that China supports Russia’s BRICS presidency and stands ready to continuously strengthen strategic coordination between both sides in international multilateral platforms. Furthermore, Sun said both sides should strengthen communication and coordination in Asia-Pacific affairs, as well as jointly safeguard regional security and stability.

- South Korea and the US are to conduct annual military drills from March 4th-14th.

US Event Calendar

- 07:00: Feb. MBA Mortgage Applications -5.6, prior -10.6%

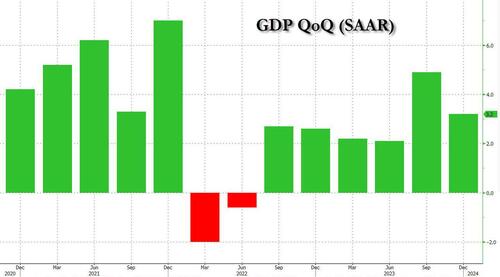

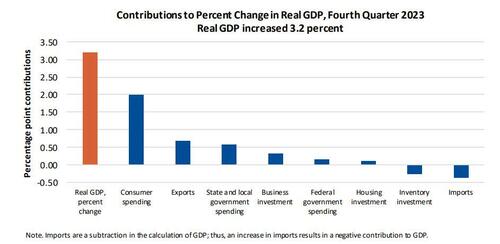

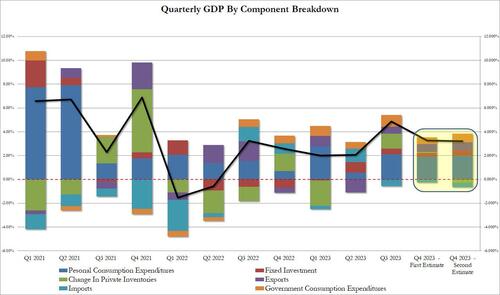

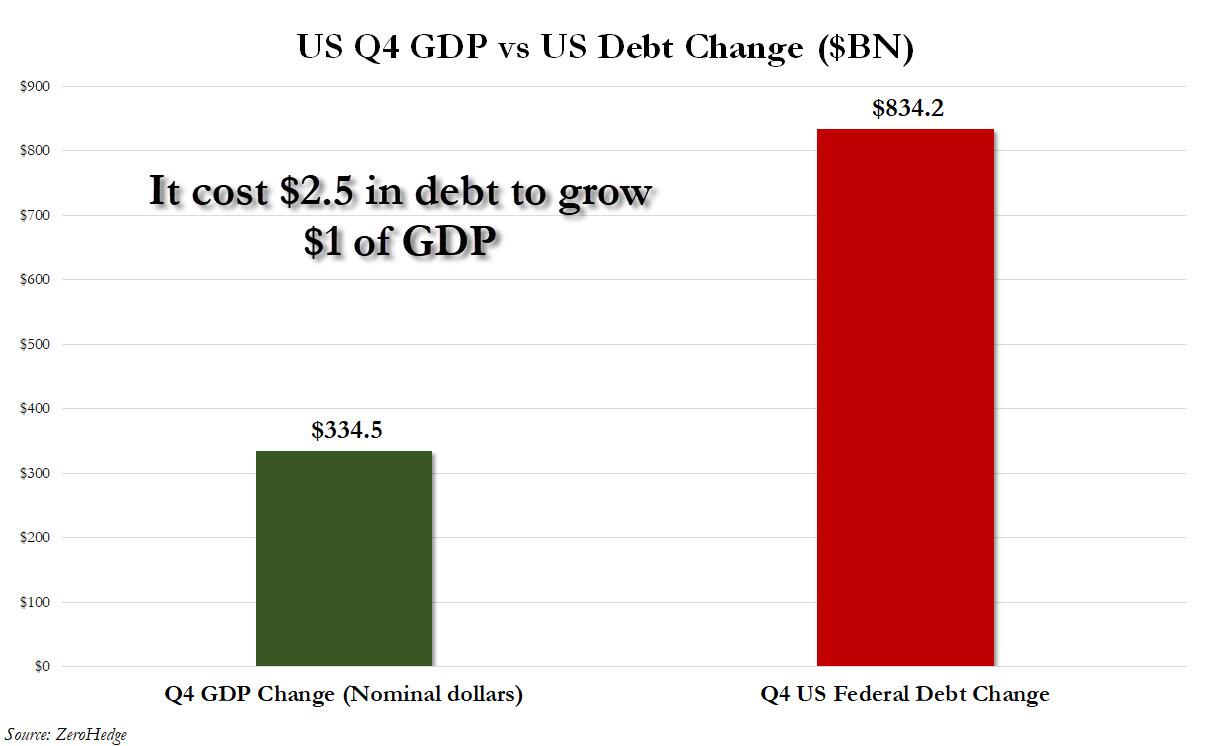

- 08:30: 4Q GDP Annualized QoQ, est. 3.3%, prior 3.3%

- 4Q Personal Consumption, est. 2.7%, prior 2.8%

- 4Q GDP Price Index, est. 1.5%, prior 1.5%

- 4Q Core PCE Price Index QoQ, est. 2.0%, prior 2.0%

- 08:30: Jan. Retail Inventories MoM, est. 0.4%, prior 0.8%

- Jan. Wholesale Inventories MoM, est. 0.2%, prior 0.4%

- 08:30: Jan. Advance Goods Trade Balance, est. -$88.5b, prior -$88.5b, revised -$87.9b

Central Bank Speakers

- 12:00: Fed’s Bostic Participates in Fireside Chat

- 12:15: Fed’s Collins Gives Remarks, Fireside Chat

- 12:45: Fed’s Williams Delivers Keynote Remarks

DB’s Jim Reid concludes the overnight wrap

Henry is on duty tomorrow but given it will be a leap day I wanted to wish all those EMR readers who were born on February 29th a very happy birthday for tomorrow! The last time it fell on a workday was in 2016 so make sure your workmates shower you with 8 years’ worth of gifts.

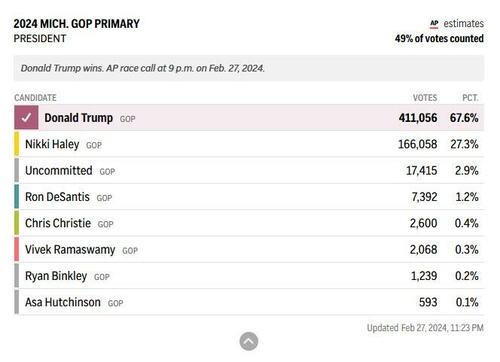

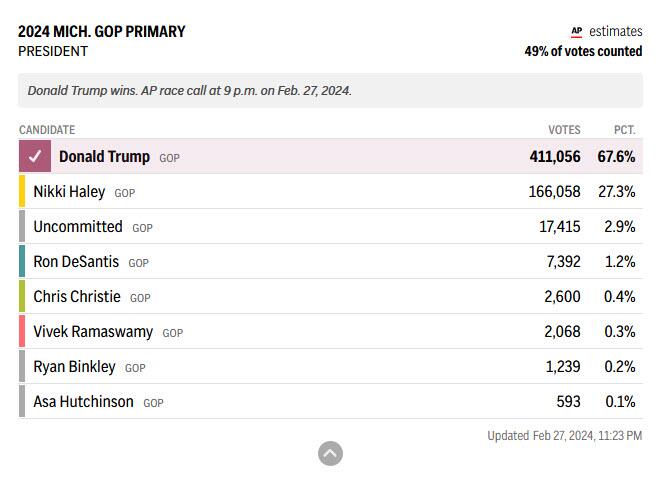

The week so far has been a bit of a crawl and not the leaps of last week as we await the all important core PCE print tomorrow. Yesterday saw equities post marginal gains (S&P 500 +0.17%), with bond yields edging up across the globe. Despite the subdued tone in markets, there’ve been some important headlines on the political side overnight, as former President Donald Trump seems to be on track to record another primary victory in Michigan. Current estimates are pointing to a big winning margin for Trump (68%) against Nikki Haley (26.8%) with 70% of the vote in, and that comes ahead of Super Tuesday next week, when 15 states will be holding votes on the Republican side. So if Trump is able to keep winning those contests, then he’ll soon have a very substantial delegate lead on the way to the nomination.

Overnight, the Reserve Bank of New Zealand held its official cash rate (OCR) unchanged at 5.5% – a 15-year high but on a day where there was a small chance of a hike delivered a relatively dovish stance. The central bank in its statement highlighted that “core inflation and most measures of inflation expectations have declined and the risks to the inflation outlook have become more balanced”. Following the decision, t he kiwi (-0.94%) is trading at $0.6113, after being one of the best performers in the last month with some hiking probabilities priced in. Bonds rallied with yields on the 10yr government bonds dropping -9.2bps to trade at 4.71% as we go to print.

Asian equity markets are slightly lower as I type with the Nikkei (-0.10%), Hang Seng (-0.27%), CSI (-0.30%) and the Shanghai Composite (-0.67%) declining. Shares of embattled developer Country Garden fell more than -12.0% after it received a liquidation petition in a Hong Kong court over its inability to repay a HK$1.6 billion ($204 million) loan and complicating its debt revamp prospects. On the flip side the HK budget is ongoing and restrictions on the property market have been lifted and boosts to tourism have been announced. Elsewhere, the KOSPI is nearly +1.0% higher this morning after two days of declines. US equity futures are just below flat with yields on 10yr USTs down -0.98bps, standing at 4.29%.

In early morning data, Australia’s CPI unexpectedly remained steady at +3.4% y/y in January (v/s +3.6% expected). YoY Core-CPI was +4.1% in January down from the +4.2% increase seen in December.

When it came to yesterday, the main story was more that there wasn’t much of a story, with little movement across the major asset classes. Among equities, there were some modest movements, with the S&P 500 (+0.17%) closing just below its all-time high, having basically been in a narrow band since the Nvidia results last week. Currently it’s down -0.21% for the week, meaning it still needs to recover a bit in order to achieve a joint record of 16 weekly advances in the last 18 (currently on 15/17 for first time since 1989). Small-cap stocks continued to outperform, with the Russell 2000 up +1.34%, in contrast to the Dow Jones, which was down -0.25%. Tech stocks saw a marginal outperformance, with the NASDAQ up +0.37% and Magnificent 7 up +0.22%. It shows the signs of the times that Apple yesterday announced the closure of its electric car unit which it set up in 2014 that at one point promised autonomous driving within a reasonable timeframe. The fact that they did this partly to divert resources to AI shows how trends can change.

Over in Europe the aggregate equity move was very similar, with the STOXX 600 up +0.18%, whilst the DAX (+0.76%) posted a 5th consecutive gain to reach a fresh all-time high.

On the rates side, Treasuries saw a mild sell off despite a fairly well digested 7yr auction. By the close, the 10yr Treasury yield was up +2.4bps to 4.30%. That said, there were some interesting trends on inflation expectations, which have continued to move higher over recent days. For instance, while the nominal 2yr yield was down -2.6bps, the 2yr breakeven was up a further +3.6bps to 2.75%, which is its highest level since March last year. Bear in mind that the 2yr breakeven began the year at 2.02%, so we’ve seen a pretty substantial move in just two months, which goes some way to explain why investors now don’t expect the rapid rate cuts that were priced at the start of the year. The amount of Fed cuts priced in 2024 inched down to 77bps, so now essentially in line with the 75bps of cuts penciled in by the median FOMC dot back in December. Patience on rates cuts continued to be visible in the latest Fed comments, with Fed Governor Bowman (hawk) noting that the latest inflation data “suggest slower progress in bringing inflation down toward our 2 percent target”.

Over in Europe, gilts saw some of the largest moves, which followed comments from BoE Deputy Governor Ramsden that “key indicators of inflation persistence remain elevated”. So 2 yr gilt yields were up +4.0bps to 4.33%, and 10yr gilt yields ended the session up +3.4bps at 4.19%, which is their highest level since late November. Elsewhere in Europe there was a similar pattern, with yields on 10yr bunds (+2.5bps) also hitting their highest level since November, at 2.46%.

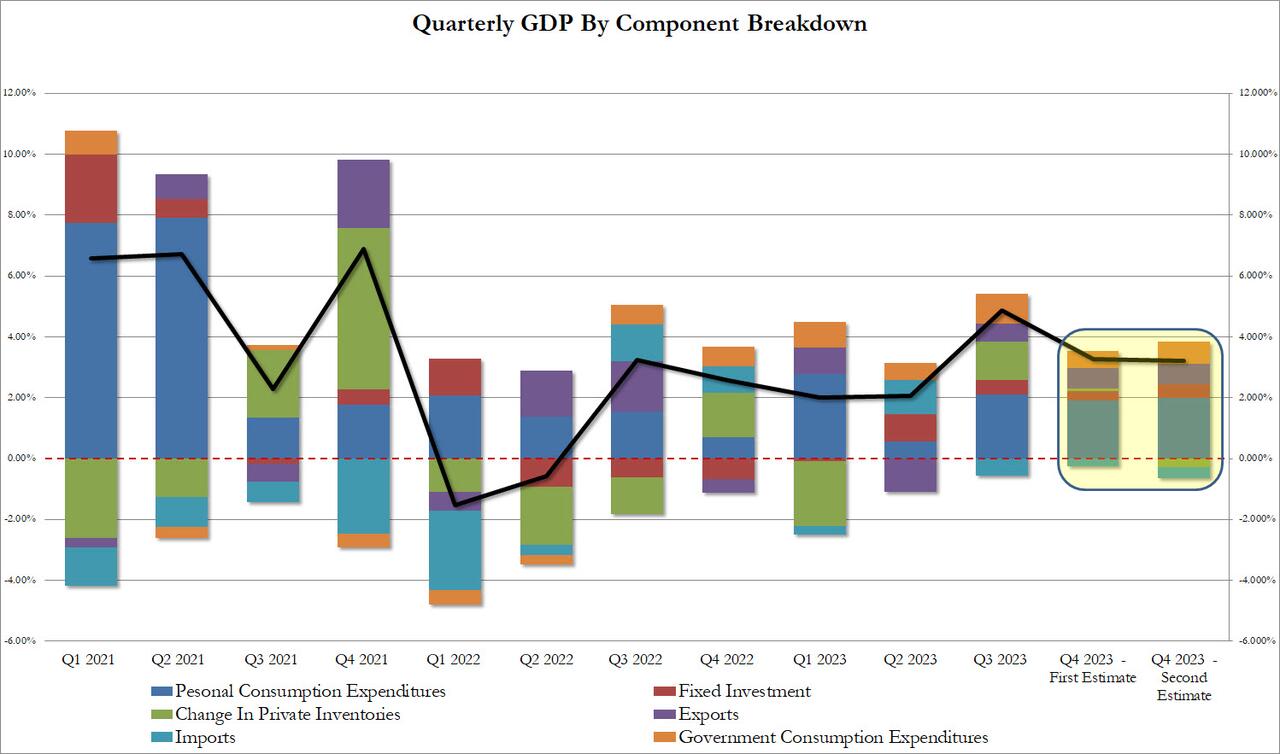

Elsewhere yesterday, there was a mixed tone from the latest US data. On the negative side, the Conference Board’s latest consumer confidence reading for February was down to 106.7 (vs. 115.0 expected), which is the first decline in four months. Moreover, the preliminary durable goods orders for January were down -6.1% (vs. -5.0% expected). Core capital goods orders were in line at +0.1%, but with the previous month revised down by four-tenths. That said, it wasn’t all bad news, with core capital goods shipments up +0.8% (vs. +0.1% exp) in January and the Richmond Fed’s manufacturing index up to -5 in February (vs. -9 expected), ending a run of 4 consecutive monthly declines. The stronger shipments data saw the Atlanta Fed’s GDPNow model marginally upgrade its estimate for Q1 growth to an annualised 3.25%. If realised, that would be a third consecutive quarter with growth above 3%.

To the day ahead now, and data releases include the second estimate of US GDP in Q4, along with the European Commission’s economic sentiment indicator for the Euro Area in February. From central banks, we’ll hear from the Fed’s Bostic, Collins and Williams, the ECB’s Muller and the BoE’s Mann.

end

From Europe

2 B) NOW NEWSQUAWK (EUROPE/REPORT)

US equities lower, Dollar bid and Kiwi slumped post-RBNZ as attention turns to US GDP and Fed speak – Newsquawk US Market Open

WEDNESDAY, FEB 28, 2024 – 06:06 AM

- European equities are mixed, whilst US futures are entirely in the red, with Nvidia weighing on the NQ

- Dollar is firmer and reclaims 104 status, focus remains on USD/JPY with YTD high in sights; Kiwi underperforms following a dovish hold at the RBNZ

- Bonds are incrementally firmer with specifics light and supply heavy, awaiting US GDP 2nd estimate

- Crude and base metals are hampered by the firmer Dollar

- Looking ahead, US GDP (2nd), PCE Prices Prelim. (Q4), Japanese Retail Sales, Comments from Fed’s Bostic, Collins, Williams & BoE’s Mann.

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses, (Stoxx600 -0.1%), are mixed, but with clear underperformance in the AEX (-0.7%), after poor results from chip-maker ASM International (-3.8%).

- European sectors hold a negative tilt; Optimised Personal Care Drug and Grocery is dragged down by Reckitt (-8.9%) post-earnings, whilst Mercedes-Benz (+1.7%) drives Autos higher.

- US Equity Futures (ES -0.5%, NQ -0.9%, RTY -0.8%) are entirely in the red, paring back most of the gains seen in the prior session, with underperformance in the NQ hampered by Nvidia (-1.9% pre-market).

- Click here and here for the sessions European pre-market equity newsflow, including earnings from Reckitt, ASM International, Holcim & more.

- Click here for more details.

FX

- USD is making gains vs. all peers with January PCE data tomorrow expected to come in hot. DXY has reclaimed 104 status and taken out its 100, 10 and 21DMAs as well as a cluster of highs from last week. Current high today at 104.24.

- EUR is hampered by the broadly firmer USD with EUR/USD oscillating around the 1.08 mark after taking out yesterday’s low of 1.0812.

- GBP is dragged lower by the USD after yesterday’s failure to test 1.27 to the upside. Session low currently sits at 1.2622 with the 22nd Feb low at 1.2612.

- USD/JPY remains arguably the most important pair to watch after printing a high of 150.79 with the YTD peak just above at 150.88. The further the pair climbs, the more likely is jawboning from Japanese officials and speculation over intervention.

- NZD is the standout laggard across the majors as the RBNZ stood pat on rates vs. a 30% chance of a hike accompanied by dovish tweaks to the OCR projections. NZD/USD has erased all of last week’s gains and slipped below the 0.61 mark with the next downside support via its 100DMA at 0.6091. AUD lower in sympathy as well as the region’s soft inflation metrics overnight.

- PBoC set USD/CNY mid-point at 7.1075 vs exp. 7.2023 (prev. 7.1057).

- Click here for more details.

FIXED INCOME

- USTs are marginally firmer with specifics light and perhaps some follow-through from the dovish RBNZ OCR projections in the absence of other drivers. Action which comes after Tuesday’s bear-steepening.

- Bunds are modestly firmer with specifics light and the focus once again on supply. Bunds are eking out marginal new highs of 132.41 seemingly as US equity futures deteriorate further, but ultimately remains comfortably within yesterday’s 132.02-71 range.