GOLD PRICE CLOSED UP $5.05 TO $2329.80

SILVER PRICE UP $0.05 TO $27.32

Gold ACCESS CLOSED $2332.85

Silver ACCESS CLOSED: $27,43

The defense of $2300 gold is now upon us and surpassed. Next up $2400 gold//Silver’s next line is $28.42. Then $34.76

The Fed is trapped as they still have their huge shortfall in gold (owes at least 67 tonnes to the BIS), They hoped that they could extricate themselves from their mess with this coming options expiry. So far, they have failed

Bitcoin morning price:$63,929 DOWN 30 DOLLARS.

Bitcoin: afternoon price: $64,654 UP 699 dollars

Platinum price closing UP $6.50TO $915.30

Palladium price; DOWN $24,05AT $982.00

END

SHANGHAI GOLD PREMIUM 34 DOLLARS/COMEX GOLD

SHANGHAI GOLD…

SHANGHAI GOLD (USD) FUTURES – QUOTES

Last Updated 25 Apr 2024 02:58:30 PM CT.

Market data is delayed by at least 10 minutes.

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $3185.41 UP 14.20 CDN dollars per oz( * NEW ALL TIME HIGH 3,301.52 CDN DOLLARS PER OZ//APRIL 16 2024)

*BRITISH GOLD: 1864.16 UP 7.05 pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2174,09 UP 7.13uros per oz //* (ALL TIME CLOSING HIGH: 2248.89 EUROS PER OZ//APRIL 16.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: APRIL 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,324.500000000 USD

INTENT DATE: 04/24/2024 DELIVERY DATE: 04/26/2024

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 46

190 H BMO CAPITAL 9

435 H SCOTIA CAPITAL 3

624 H BOFA SECURITIES 40

737 C ADVANTAGE 15

905 C ADM 5

991 H CME 14

TOTAL: 66 66

JPMORGAN STOPPED (RECEIVED) 0/66CONTRACTS

FOR APRIL/2024

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2024. CONTRACT: 66 NOTICES FOR 6600 OZ or 0.2053 TONNES

total notices so far: 16,302 contracts for 1,630,200 Oz (50.919 tonnes)

FOR APRIL:

SILVER NOTICES: 2 NOTICE(S) FILED FOR 10,000 OZ/

total number of notices filed so far this month : 1636 for 8,180,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $5.05

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

NO CHANGES IN GOLD INVENTORY AT THE GLD:

/ /INVENTORY RESTS AT 833.63 TONNES

INVENTORY RESTS AT 833,63 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER UP $0.05 AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 1.534MILLION OZ INTO THE SLV/

// INVENTORY INCREASES T0 429.814 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 429.814MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A MEGA HUMONGOUS SIZED 2695 CONTRACTS TO 173,045 BUT STILL RAPIDLY CLOSING IN ON THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, DESPITE THE RAID AND THIS HUMONGOUS SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR SMALL LOSS OF $0,05 IN SILVER PRICING AT THE COMEX ON WEDNESDAY. WE HAD SOME LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN PANICKING SHORT COVERING BY OUR SPECS WITH THE HUGE PRICE LOSS IN PRICE. WE HAD A HUGE SIZED 831 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 831 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.05, AND WERE SUCCESSFUL IN KNOCKING SOME SILVER LONGS AS WE HAD A HUGE SIZED LOSS OF 1470 CONTRACTS ON OUR TWO EXCHANGES WITH THE LOSS IN PRICE OF $0.05

WE MUST HAVE HAD:

A HUGE SIZED 1225 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 2.465 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S NIL OZ E.F.P.JUMP TO LONDON //NEW STANDING REMAINS AT 8.195 MILLION OZ//

//NEW STANDING FOR SILVER IS THUS 8.195 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI LOSS/ HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 823 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED A STRONG 1470 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL

TOTAL CONTRACTS for 19 DAYS, total 28,837 contracts: OR 144.185MILLION OZ (1518 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 144.185 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 144.815 MILLION OZ (THIS MONTH WILL PROBABLY BE A WHOPPER OF ISSUANCE OF EFPS)

RESULT: WE HAD A HUMONGOUS SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2695 CONTRACTS WITH OUR LOSS IN PRICE OF SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUMONGOUS EFP ISSUANCE CONTRACTS: 831 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL. OF 2.465 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAYS’ 10,000 OZ E.F.P JUMP TO LONDON

//NEW TOTAL STANDING REMAINS AT 8.195 MILLION OZ

WE HAVE A HUGE SIZED LOSS OF 2695 OI CONTRACTS ON THE TWO EXCHANGES WITH THE LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 831 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (831 WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 2 NOTICE(S) FILED TODAY FOR 10,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 1341 OI CONTRACTS TO 517,590 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 872 CONTRACTS

WE HAD A FAIR SIZED INCREASE IN COMEX OI (1341 CONTRACTS) DESPITE OUR $4.60 LOSS IN PRICE//WEDNESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER TO WHACK GOLD’S PRICE. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR APRIL. AT 44.8615 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S TINY QUEUE JUMP OF 600 OZ.(0.0186TONNES)

NEW STANDING 50.827 TONNES// ALL OF THIS HAPPENED WITH OUR $3.75 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A STRONG SIZED GAIN OF 3532 OI CONTRACTS (14.09 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2191 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 518,462

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3532 CONTRACTS WITH 1341CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 2191 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3532 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED 5826 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2191 CONTRACTS) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI 1341/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 3532 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 44.8615 TONNES FOLLOWED BY TODAY’S TINY 0.0186TONNES QUEUE JUMP

//NEW STANDING 50.827 TONNES.

/ 3) ZERO LONG LIQUIDATION DESPITE THE LOSS IN PRICE.

// 4) FAIR SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: STRONG T.A.S. ISSUANCE: 5826CONTRACTS/ HUGE SHORT COVERING BY OUR WRONG FOOTED SPECS WITH THE FED’S CONTINUAL RAID ON THE COMEX GOLD.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL. :

TOTAL EFP CONTRACTS ISSUED: 73,818 CONTRACTS OR 7,381,800 OZ OR 229.60TONNES IN 19TRADING DAY(S) AND THUS AVERAGING: 3968 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19TRADING DAY(S) IN TONNES 229.60 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 229.60 DIVIDED BY 3550 x 100% TONNES = 6.46% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

Advertisements

REPORT THIS AD

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 229.60 TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A MEGA-HUGE SIZED 2695 CONTRACTS OI TO 173,045AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 831 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 800 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 831 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2695 CONTRACTS AND ADD TO THE 831 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1470 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 7.35MILLION OZ

OCCURRED WITH OUR $0.05 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

Advertisements

REPORT THIS AD

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED UP 8.08 PTS OR 0.27% //Hang Seng CLOSED UP 83,27PTS OR 0.48% / Nikkei CLOSED DOWN 831,60PTS OR 2.16% //Australia’s all ordinaries CLOSED DOWN 0.01%///Chinese yuan (ONSHORE) closed UP 7.2460//OFFSHORE CHINESE YUAN CLOSED UP TO 7.26750 Oil UP TO 82.97dollars per barrel for WTI and BRENT UP AT 88.18 Stocks in Europe OPENED ALL MOSTLY MIXED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1341 CONTRACTS TO 517,590 DESPITE OUR LOSS IN PRICE OF $3.75 WITH RESPECT TO WEDNESDAY TRADING. WE HAD CONSIDERABLE A.S. LIQUIDATION AS WELL AS SHORTS, DESPERATELY TRYING TO GET OUT OF THEIR NAKED SHORTS.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF APRIL..… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG 2191 EFP CONTRACTS WERE ISSUED: : JUNE 2191 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2191 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 3532 CONTRACTS IN THAT 2191 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A FAIR SIZED GAIN OF 1341 COMEX CONTRACTS..AND THIS GOOD GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $3.75 WEDNESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A STRONG SIZED 4157 CONTRACTS. WE HAD 0 EX FOR RISK ISSUANCE. MOST OF THE TRADING AND SUPPLY OF CONTRACTS ON TUESDAY WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: APRIL (50.827 TONNES) ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNEES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 50.827TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $3.75 //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A GOOD SIZED GAIN OF 3532 TOTAL CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR LOSS IN PRICE 0F $3.75

WE HAD A STRONG T.A.S. LIQUIDATION ON THE FRONT END OF WEDNESDAY’S TRADING ALONG. THE T.A.S. ISSUED ON WEDNESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 10.98 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL. (44.8615 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S SMALL QUEUE.JUMP OF 600 OZ (0.0186TONNES)//NEW STANDING; 50.827TONNES

NEW STANDING: 50.650ONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $3.75

WE HAD REMOVED 872 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET GAIN ON THE TWO EXCHANGES 3532 CONTRACTS OR 353,200 OZ (10.98TONNES)

confirmed volume WEDNESDAY 197m049 contracts//fair

//speculators have left the gold arena

APRIL 25 INITIAL APRIL GOLD

/ /// THE APRIL 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 21.151oz Brinks one kilobar . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | 32,,246.041oz asahi Delaware 1002 kilobars and 1 kilobar |

| No of oz served (contracts) today | 39 notice(s) 3900 OZ 0.1213 TONNES |

| No of oz to be served (notices) | 53 contracts 5300 OZ 0.1648ONNES |

| Total monthly oz gold served (contracts) so far this month | 16,302 notices 1,630,200 oz 50.919 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: nil oz

we have 2 customer deposits:

i) Into Asahi 32,213,890 oz (1002 kilobars)

ii) Into Delaware 32,151 oz (1 kilobar)

total deposit 32m246,041 oz

total customer withdrawals: 1

i) Out of Brinks: 32,15 oz (1 kilobars)

Adjustments: 1

adjustment: 1553.919oz customer to dealer //brinks

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of APRIL we have an oi of 105 contracts having GAINED 29 contracts. We had 23 contracts served on WEDNESDAY, so we GAINED 6 contracts or an additional 600 oz (0.0186tonnes) will stand at the comex

MAY LOST 134 CONTRACTS TO STAND AT 1999

JUNE DEREASED ITS OI BY 484CONTRACTS UP TO 408,495CONTRACTS.

We had 66 contracts filed for today representing 6600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 66 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the APRIL. /2024. contract month, we take the total number of notices filed so far for the month (16,302x 100 oz ), to which we add the difference between the open interest for the front month of APRIL. (105CONTRACTS) minus the number of notices served upon today (66x 100 oz per contract( equals 1,634,100OZ OR 50.827 TONNES.

thus the INITIAL standings for gold for the APRIL. contract month: No of notices filed so far (16,302) x 100 oz + (105 {OI for the front month} minus the number of notices served upon today (66 x 100 oz which equals 1,634,100 oz (50.827TONNES)

TOTAL COMEX GOLD STANDING FOR APRIL: 50.827 TONNES WHICH IS HUGE FOR THIS ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,567,289.026 48.749tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,622,656.483OZ

TOTAL REGISTERED GOLD 7,532,254.885 (234.236 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,090,381.598OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 5,964,965 oz (REG GOLD- PLEDGED GOLD)

185.54tonnes/dropping like a stone

END

SILVER/COMEX

APRIL 24

INITIAL

//2024// THE APRIL 2025SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 3173.900 oz CNT . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,136,625.460 oz Brinks ASAHI |

| No of oz served today (contracts) | 2CONTRACT(S) (10,000 OZ) |

| No of oz to be served (notices) | 3 contracts (15,000 oz) |

| Total monthly oz silver served (contracts) | 1636Contracts (8,180,000oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit :nil oz

Advertisements

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 deposits customer account:

i) Into Brinks 597,216.000oz

ii) Into ASAHI 597,216.000 oz

total customer deposits 1,136,625.460oz

JPMorgan has a total silver weight: 130.1709million oz/295.107million or 44.06%

adjustment: 6 ALL DEALER TO CUSTOMER

I) asahi 720,932,140 OZ

II) cnt 89,734,000 OZ

III) hsbc 24M521,100 OZ

IV) Int Delaware 9663.000 oz

v) JPMorgan 20,501.010 oz

vi) Manfra: 99,333.812.0z

Comex withdrawals: 1

i0 CNT 3,173.900 oz

total withdrawal 3173.000oz

TOTAL REGISTERED SILVER: 46m231MILLION OZ//.TOTAL REG + ELIGIBLE. 295m107million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF APRIL /2023 OI: 5 CONTRACTS HAVING LOST 6 CONTRACT(S).

WE HAD 8 CONTRACTS SERVED ON WEDNESDAY, SO WE LOST 2 CONTRACTS OR ADDITIONAL 10,0000 OZ WILL NOT STAND AT THE COMEX AS THEY WERE E.F.P.;d TO LONDON FOR DELIVERY OVER ON THAT SIDE OF THE POND,

.

MAY SAW A LOSS OF 10,611CONTRACTS DOWNTO 33,912

JUNE SAW A GAIN OF 40 CONTRACTS RISING TO 738

JULY SAW A GAIN OF 7338CONTRACTS UP TO 114,097

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 8 for 40,000 oz

CONFIRMED volume; ON MONDAY 106,172/HUGE

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 1636 5,000 oz = 8,180,000 oz

to which we add the difference between the open interest for the front month of APRIL (5)and the number of notices served upon today 2x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL/2024 contract month: 1636(notices served so far) x 5000 oz + OI for the front month of APRIL. (5)number of notices served upon today (2x 500 oz of silver standing for the APRIL contract month equates to 8.195 MILLION OZ.

New total standing: 8.195 million oz.

There are 46,231 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

APRIL 25WITH GOLD UP $5.05 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD /INVENTORY RISES AT 833,63 TONNES

APRIL 19 WITH GOLD UP $15.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 4.32 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 831.91 TONNES

APRIL 18 WITH GOLD UP $11.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE WITHDRAWAL OF 2.59 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 827.59 TONNES

APRIL 17 WITH GOLD DOWN $17.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 830;18 TONNES

APRIL 16 WITH GOLD UP $23.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 828.45 TONNES

APRIL 15 WITH GOLD UP $9.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE WITHDRAWAL OF 4.03 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 826.72 TONNES

APRIL 12 WITH GOLD UP $2.80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD/ INVENTORY RISESS AT 830.75 TONN

APRIL 10 WITH GOLD DOWN $14.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 828.71 TONNES

APRIL 9 WITH GOLD UP $11.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 827,85 TONNES

APRIL 8 WITH GOLD UP $7.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A WITHDRAWAL OF 6.02 TONNES OF GOLD INTO THE GLD/ INVENTORY REMAINS AT 826.41 TONNES

APRIL 5 WITH GOLD UP $38.65 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/ INVENTORY REMAINS AT 832.45 TONNES

APRIL 4 WITH GOLD DOWN $3.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD/ INVENTORY REMAINS AT 830.73 TONNES

APRIL 3 WITH GOLD UP $33,85 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD // INVENTORY REMAINS AT 829.00 TONNES

APRIL 2 WITH GOLD UP $23.90 TODAY; HUG CHANGES IN GOLD INVENTORY AT THE GLD A WITH DRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD.:// INVENTORY REMAINS AT 829.00 TONNES

APRIL 1 WITH GOLD UP $18.70 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:// INVENTORY REMAINS AT 830.15 TONNES

MARCH 28 WITH GOLD UP $26.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:// INVENTORY REMAINS AT 830.15 TONNES

MARCH 27 WITH GOLD UP $15.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// INVENTORY FALLS TO 830.15 TONNES

MARCH 26 WITH GOLD UP $1.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 835.33 TONNES

MARCH 25 WITH GOLD UP $17.05 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 838.50 TONNES

MARCH 22 WITH GOLD DOWN $23.75 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 838.50 TONNES

GLD INVENTORY: 833,63 TONNES,

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 25WITH SILVER UP $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 1.534 MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 24/WITH SILVER DOWN $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 11.904MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 428.280 MILLION OZ

APRIL 23/WITH SILVER UP $0.11TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV / :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 22/WITH SILVER DOWN $1.51 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.194 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 19/WITH SILVER UP 42 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.657 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 418.570 MILLION OZ

APRIL 18/WITH SILVER DOWN $.04TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.977 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 422.227 MILLION OZ

APRIL 17/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF .868 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 426/204 MILLION OZ

APRIL 16/WITH SILVER DOWN $0.46 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF NON EXISTENT SILVER// :SLV INVENTORY RESTS AT 427.072 MILLION OZ

APRIL 15/WITH SILVER UP $0.46 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 12/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 4.069 MILLION OZ FROM THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 11/WITH SILVER UP $0.23 TODAY: STRANGE INDEED! HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.931 MILLION OZ :SLV INVENTORY RESTS AT 437.998 MILLION OZ

APRIL 10/WITH SILVER UP $0.04 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:SLV INVENTORY RESTS AT 441.929 MILLION OZ

APRIL 9/WITH SILVER UP $0.15 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.549 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 441.929 MILLION OZ

APRIL 8/WITH SILVER UP $0.33 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.320 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 441.328 MILLION OZ

APRIL 5/WITH SILVER UP $0.61 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.748 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 441.060 MILLION OZ

APRIL 4/WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.671 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 437.312 MILLION OZ

APRIL 3/WITH SILVER UP $1.14 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.835 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 433.641 MILLION OZ

APRIL 2/WITH SILVER UP 84 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6.721 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 430.806 MILLION OZ

APRIL 1/WITH SILVER UP 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// SLV INVENTORY RESTS AT 424.085 MILLION OZ

MARCH 28/WITH SILVER UP 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.005 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 424.085 MILLION OZ

REPORT THIS AD

MARCH 27/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A A DEPOSIT OF 1.691 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 423.079 MILLION OZ

MARCH 26/WITH SILVER DOWN 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A A DEPOSIT OF 0.366 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 421.388 MILLION OZ

MARCH 25/WITH SILVER UP 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 3.887 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 421.022 MILLION OZ

MARCH 22/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE DEPOSIT OF 1.1899 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 424.909 MILLION OZ

CLOSING INVENTORY 429.814 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

PETER SCHIFF/SCHIFFGOLD/MIKE MAHARRAY

END

2.Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens/…

Jim Rickards…

This “Emperor” Has No Clothes

THURSDAY, APR 25, 2024 – 09:35 AM

Authored by James Rickards via DailyReckoning.com,

Does the Fed even matter that much to the real economy and investor portfolios?

That’s an important question that doesn’t get nearly enough scrutiny. It’s possible that neither the Fed nor the reporters who cover the Fed want to ask hard questions about what the Fed really does.

Could it be the case that the emperor has no clothes?

Financial journalists often refer to a Goldilocks economy (“not too hot, not too cold, just right!”) as a tribute to the Fed’s finesse in handling rates. It’s also called the “soft landing” scenario because the Fed supposedly tamed inflation without causing a recession.

These narratives have no factual foundations; they’re just stories designed to get you to buy stocks and pump up stock prices.

The truth is the Fed is always behind the curve and doesn’t finesse the economy. And there’s no such thing as a soft landing; the economy does not gradually shift gears. It’s either growing fast or going into recession.

So where does the Fed stand today? Will it start cutting rates as Wall Street keeps (wrongly) predicting?

Wall Street Keeps Getting It Wrong

The Fed will not cut rates at its May or June meetings. Wall Street’s been predicting rate cuts for almost two years and they’ve been wrong every time. They’re predicting a June rate cut, and they’ll be wrong again.

A rate cut at the July 31 meeting is possible but is in jeopardy now due to inflation going up again in the latest report. We’ll have three more months of inflation, unemployment and GDP data between now and then.

If the Fed does cut rates in late July, it won’t be for good reasons. It’ll be because the economy has fallen into a recession. But given the boost to U.S. growth from out-of-control government spending in an election year, the recession may be postponed. So don’t count on a July rate cut either.

There’s no Fed meeting in August. The next meeting after that is Sept. 18. The Fed may be ready for a rate cut by then but here’s the problem: The Sept. 18 date is just seven weeks before the election on Nov. 5. The Fed pretends it’s non-political but in fact, it is highly political.

A rate cut in September will be viewed as helping Biden by boosting the economy and hurting Trump. At the same time, Trump is the likely winner based on currently available polling data and trends.

The Fed won’t want to be in the position of appearing to boost Biden and hurt Trump if Trump is going to win. Trump will make the Fed Public Enemy No. 1 and that’s the last thing they want. So the Fed will take a pass in September.

There’s no Fed meeting in October. The next two Fed meetings after that are on Nov. 7 and Dec. 18, both safely after the election. The Fed could cut rates at both meetings. But the Fed has painted itself into a corner on that.

The Fed’s Running out of Time

Beginning at the FOMC meeting on March 20, the Fed promoted the narrative that there would be three rate cuts before the end of the year. If they don’t cut in May, June, July or September (for reasons noted above) and there are no meetings in August or October, then the Fed would have at most two rate cuts this year, in November and December.

In short, the Fed is running out of meetings in which to conduct three rate cuts and may have to settle for two.

The Fed’s reckless promise and the dictates of the calendar are what are driving the stock market. The stock market’s fixated on the Fed, but the Fed doesn’t know what they’re doing. That’s a recipe for volatility and a sharp reversal of the first-quarter gains.

So why doesn’t the Fed just get on with it and start cutting rates in May? They could make an announcement and hire a band to play “Happy Days Are Here Again.”

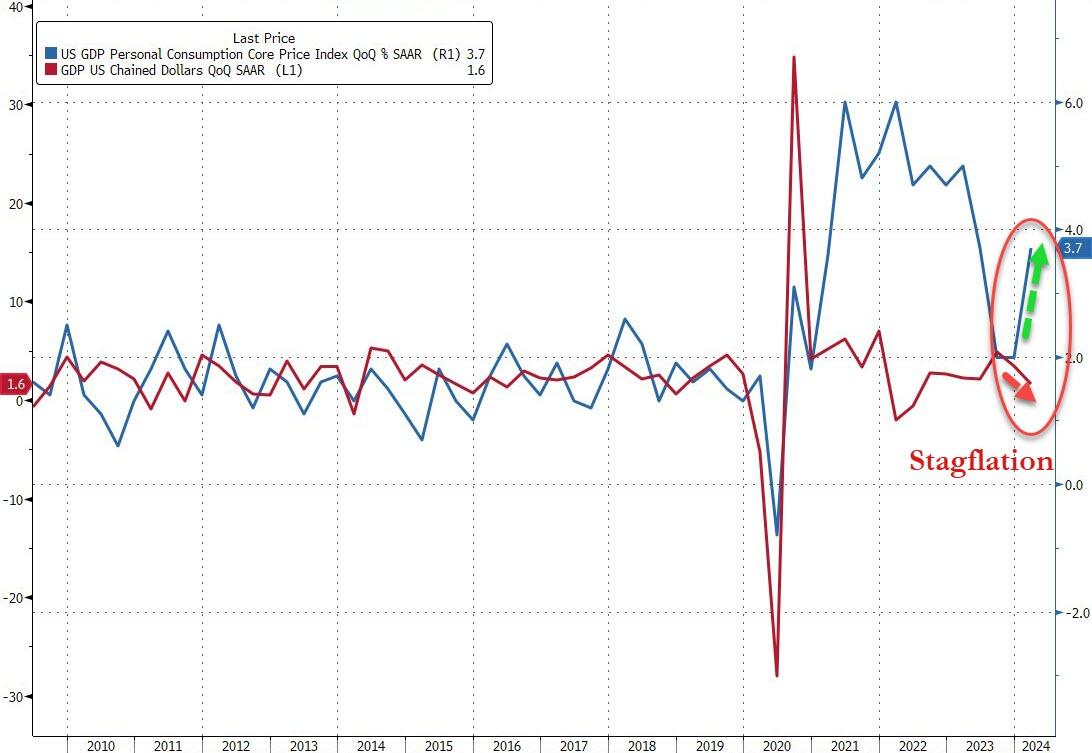

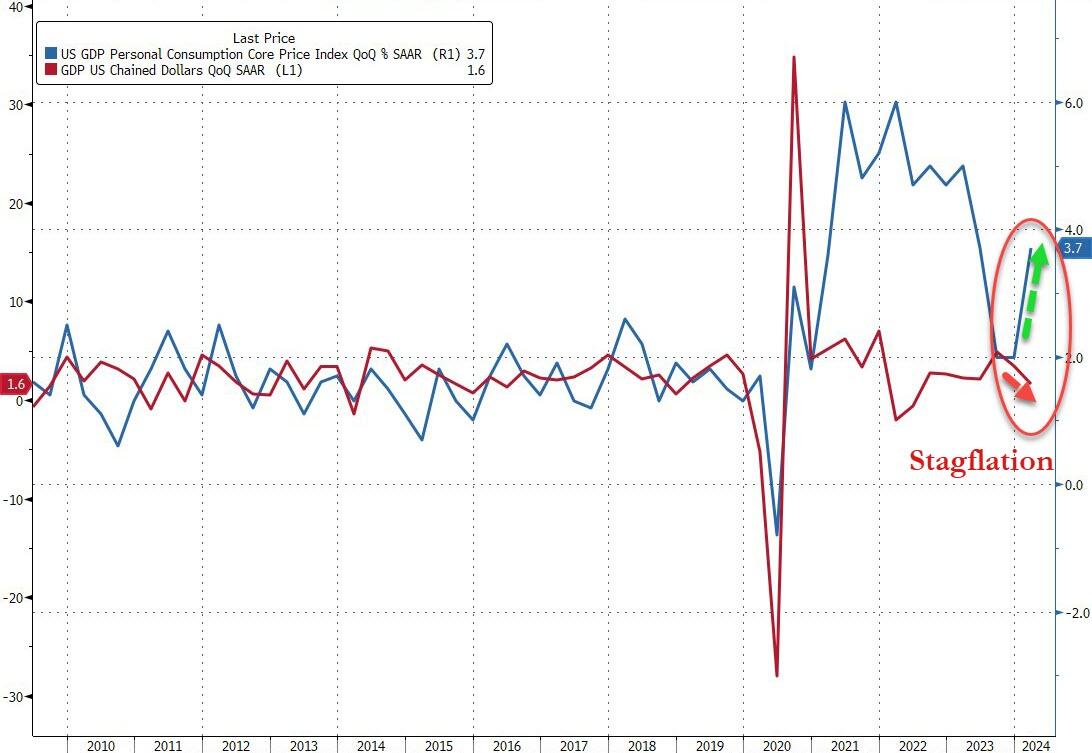

The Fed thought they had won the battle when inflation dropped from 9.1% (CPI year-over-year) in June 2022 to 3.0% in June 2023. Nice job, Fed. It was when that June 2023 reading came out in July 2023 that the Fed put in one last rate hike, and then stopped dead. Since then, it’s been a countdown to rate cuts.

The problem is that inflation isn’t done. From the 3.0% in June 2023, inflation rose to 3.7% in August, and 3.7% again in September 2023. Inflation fluctuated between 3.1% and 3.4% until recently. March inflation came in at 3.5%, a full 0.3 percentage points higher than in February.

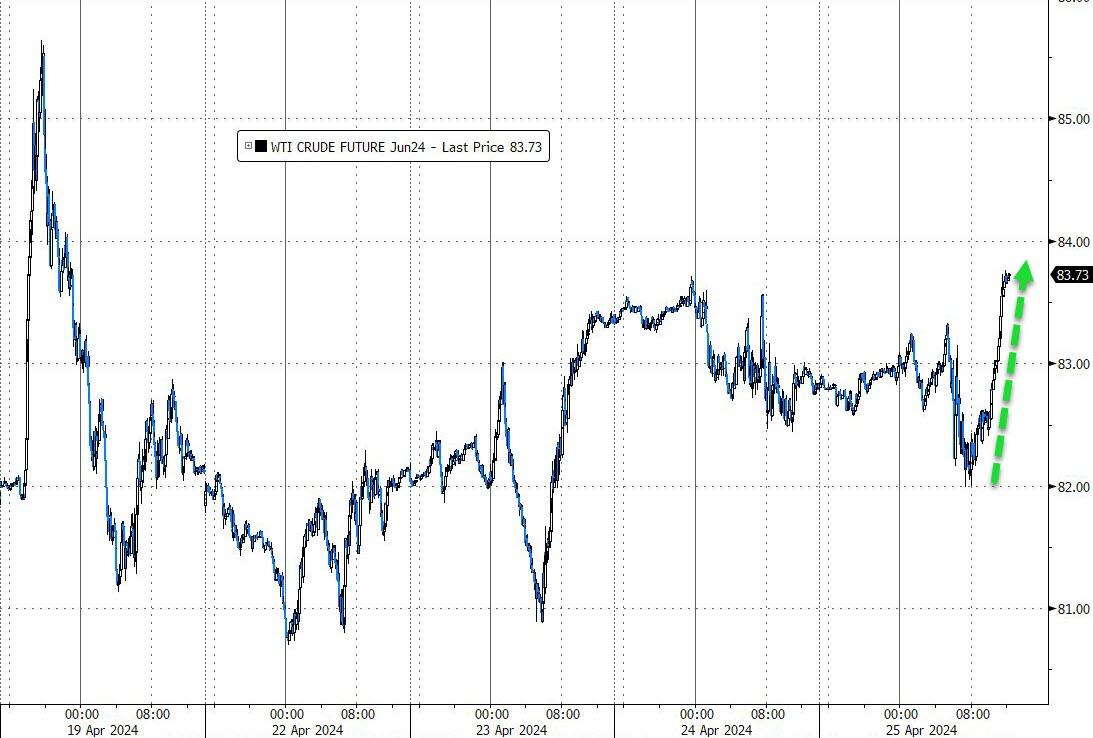

Oil’s up 24% in 4 Months

That’s not all that’s going up. The price of oil was $68.50 per barrel last Dec. 12 and is over $83.00 per barrel today. That’s about a 21% increase in just four months.

That oil price shock hasn’t worked its way through the supply chain yet. It has resulted in some price increases, but more are in the pipeline. This oil price spike will keep inflation at current levels or higher in the months ahead. The Fed is looking for signs that inflation is coming down but they’re not going to get them, as shown in the latest inflation report.

The price of one gallon of regular gasoline (regular, national average) was $3.64 as of yesterday, April 22. It was $3.57 on April 4, $3.55 on April 3, $3.54 on March 28, $3.52 on March 4 and $3.51 on April 4, 2023.

Put differently, gas prices are higher than they were last week, last month and last year.

That’s a bad sign for Biden politically, but it’s a worse sign for the Fed in terms of inflation. That gas price rise isn’t over because the wholesale price of oil is still on the rise. And oil prices affect far more than the price of gas at the pump.

Higher oil prices mean higher transportation costs whether by truck, train, plane or ship since all goods have to be transported to market. That means the price of everything is going up.

Other factors driving inflation from the supply side include the Key Bridge collapse in Baltimore, the closing of the Red Sea/Suez Canal shipping route and continued fallout from Ukraine war sanctions. Some of these supply side constraints may be deflationary in the long run, but they are definitely inflationary in the short run.

Running on Fed Happy Talk

The stock market has been running on Fed Happy Talk. That situation may end abruptly on June 12 if the Fed doesn’t cut rates and signals that rate cuts are not to be expected in the near future and perhaps not before the end of the year.

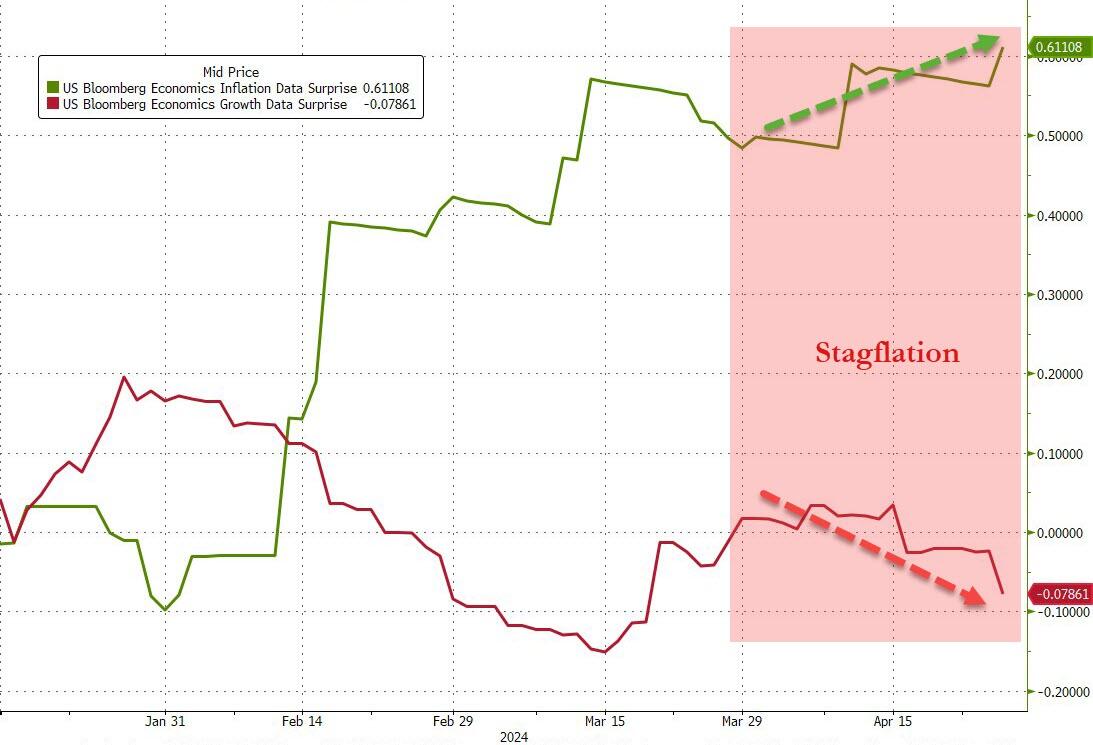

By then, we may be facing one of the worst economic outcomes possible: recession + inflation = stagflation.

Anyone under the age of 60 probably has no acquaintance with stagflation.

The U.S. last experienced this in 1977–1981. I remember that period well. It was great for leveraged holders of hard assets such as gold and real estate.

It was a nightmare for holders of stocks. (The long-term bull market in stocks did not start until August 1982.)

Investors might keep that winning hard asset portfolio allocation in mind as events unfold between now and June.

END

3. CHRIS POWELL//GATA DISPATCHES

Silver Bullion TV reviews the success of the Sound Money Defense League

Submitted by admin on Tue, 2024-04-23 22:43 Section: Daily Dispatches

10:42p ET Tuesday, April 23, 2024

Dear Friend of GATA and Gold:

Interviewed this week by Patrick Vierra of Silver Bullion TV in Singapore, Money Metals Exchange CEO Stefan Gleason explains the work of the Sound Money Defense League in the United States. The league lately has assisted passage of legislation in 45 of the 50 states to exempt monetary metals coin and bullion from sales taxes.

The league also has been encouraging states to hold some of their cash reserves in monetary metal to hedge their exposure to the U.S. dollar.

The interview is 40 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS

Gold Prices: Beyond Inflation And Real Yields

(courtesy Robert Burrows)

THURSDAY, APR 25, 2024 – 12:25 PM

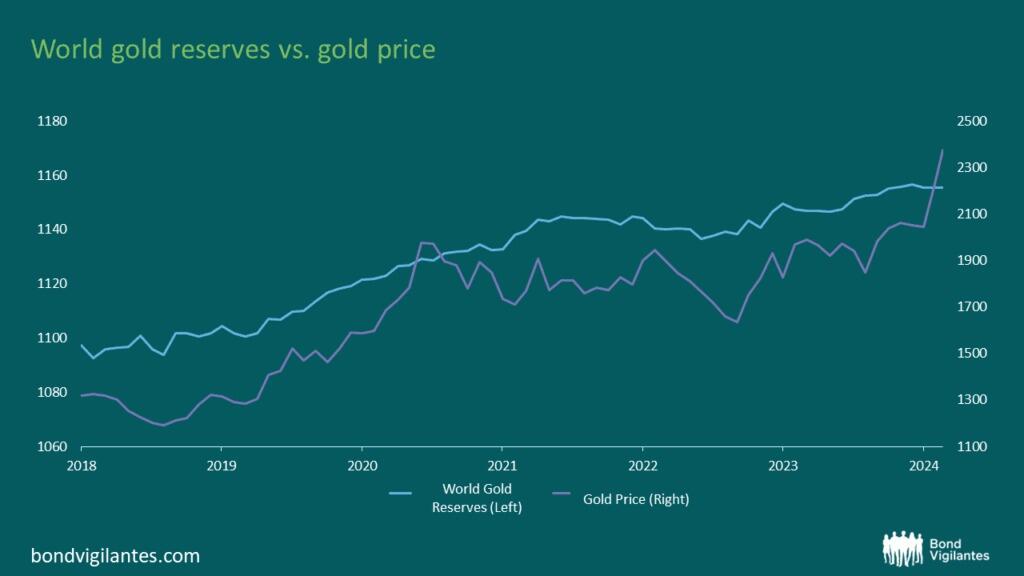

Authored Robert Burrows via BondVigilantes.com,

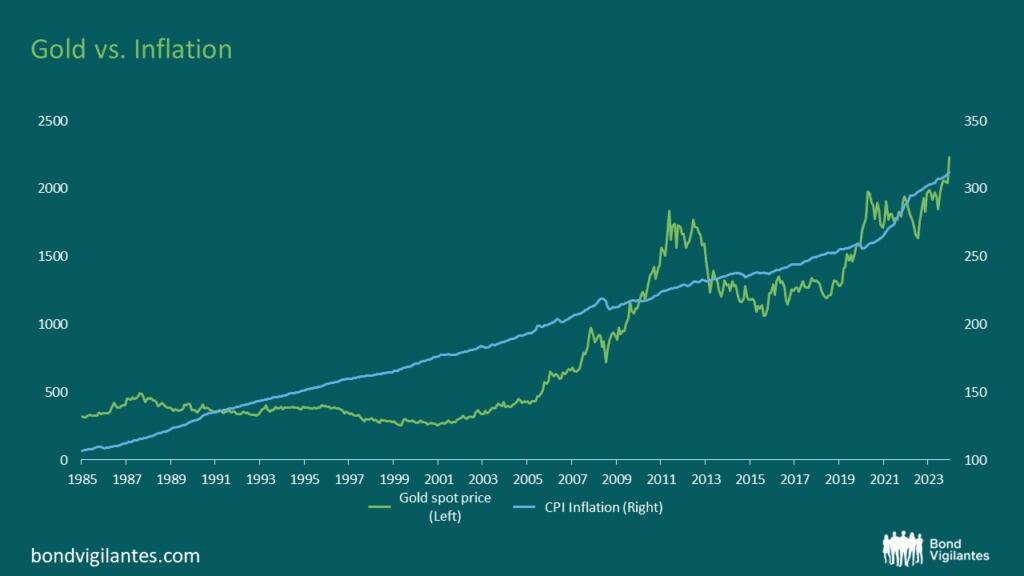

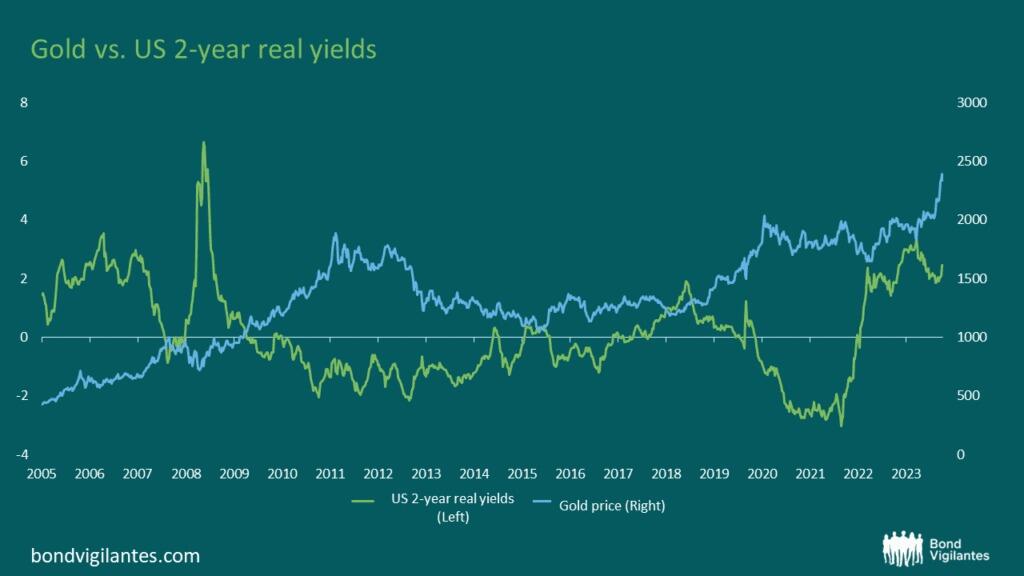

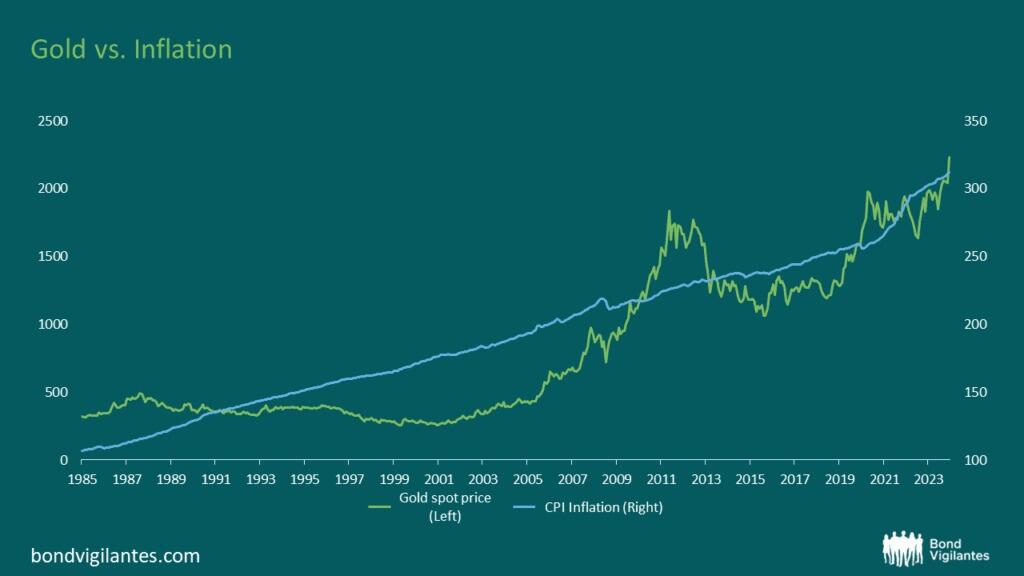

Renowned for its role as a hedge against economic uncertainty and inflation, gold has long captivated investors. One key factor influencing gold’s price is the relationship between real yields and inflation. Over the long term, gold has protected one against the pernicious effects of inflation and remains a powerful diversifier within an investment portfolio:

ource: M&G, Bloomberg, 23 April 2024

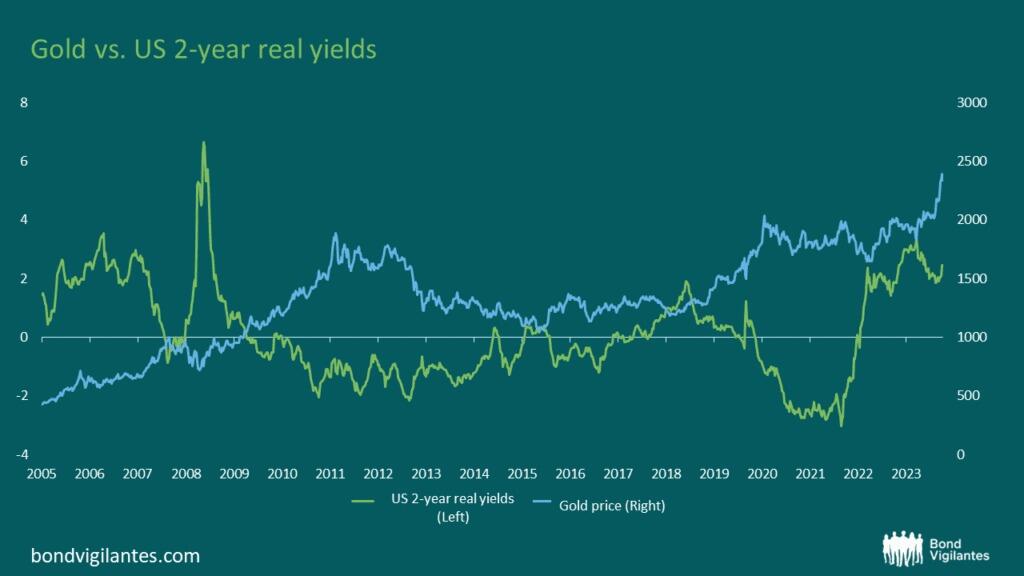

Real yields, also known as inflation-adjusted yields, represent the return on an investment after accounting for inflation. They are calculated by subtracting the inflation rate from the nominal yield of a financial instrument, such as a government bond. Real yields provide a more accurate measure of an investor’s purchasing power and the true return on their investment. Historically, gold prices have exhibited an inverse correlation with real yields. When real yields are low or negative, indicating that inflation-adjusted returns on fixed-income investments are meagre or eroded by inflation, investors seek alternative stores of value, such as gold. Conversely, when real yields are high, offering attractive returns relative to inflation, the opportunity cost of holding gold increases, leading to downward pressure on the gold price.

The below chart demonstrates this general trend:

Source: M&G, Bloomberg, 23 April 2024

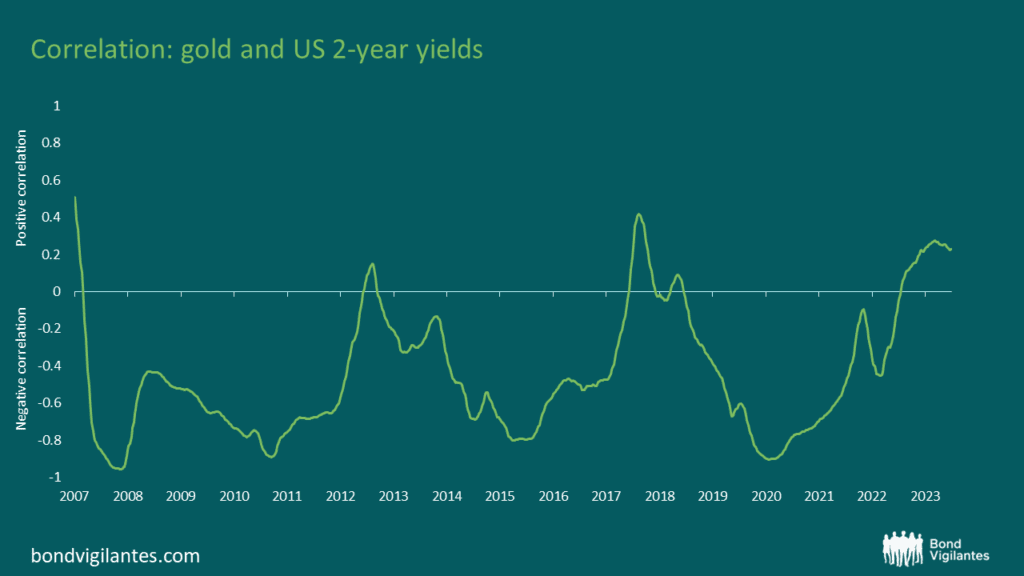

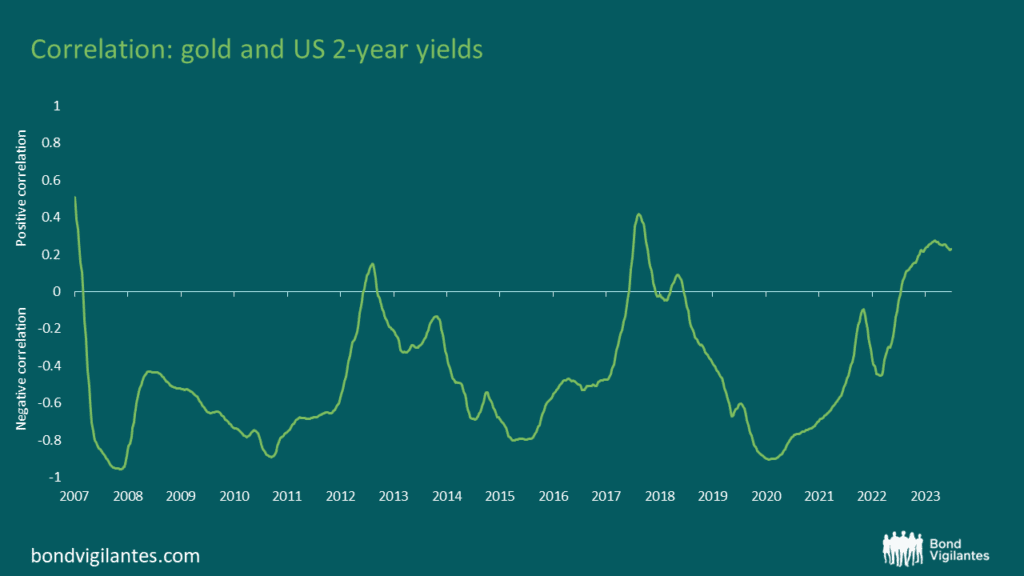

While the trend is not perfect, the following chart demonstrates that correlations have been negative for the bulk of the time:

Source: M&G, Bloomberg, 23 April 2024

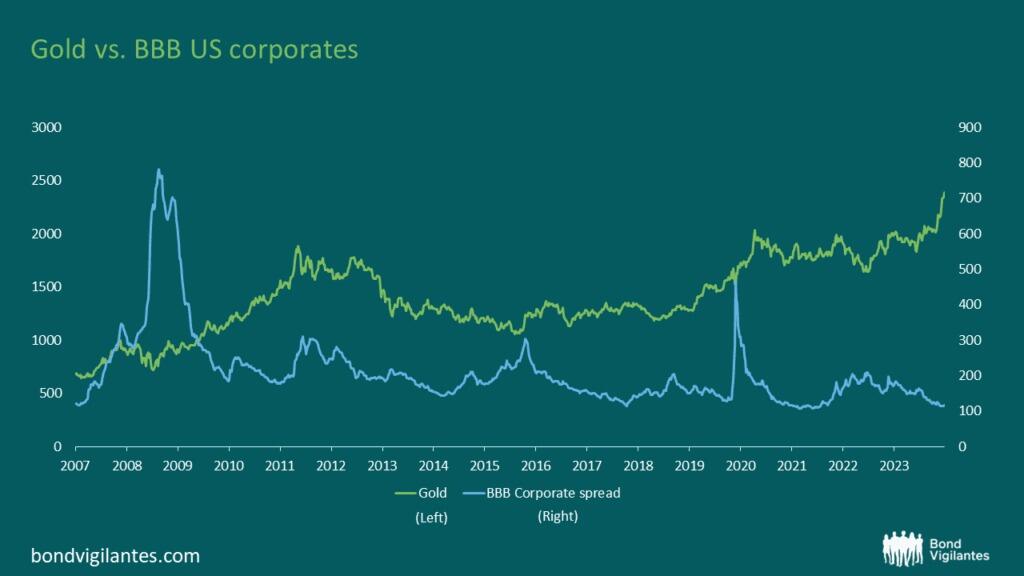

So why is gold going up? If these correlations hold and real yields are moving higher, the gold price should be trending lower. There is something else at play. Investors will generally point to global instability, with geopolitical concerns being obvious. The other would be the challenging fiscal backdrop of many major economies, which I have written about. These concerns are well founded; however, they do not seem to be showing up in other risk assets.

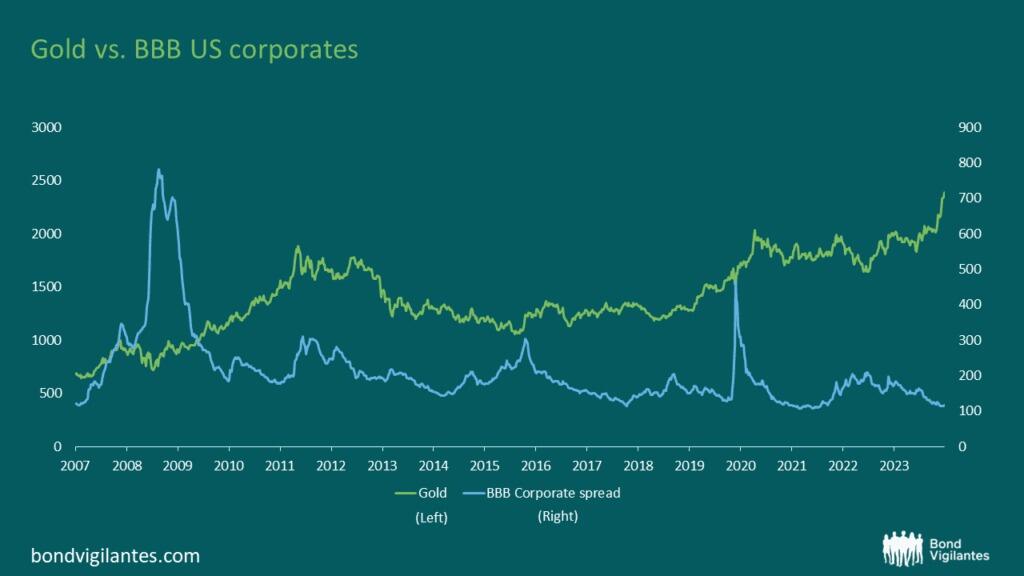

BBB US corporates are trading at their all-time tights, so there is nothing to see here:

Source: M&G, Bloomberg, 23 April 2024

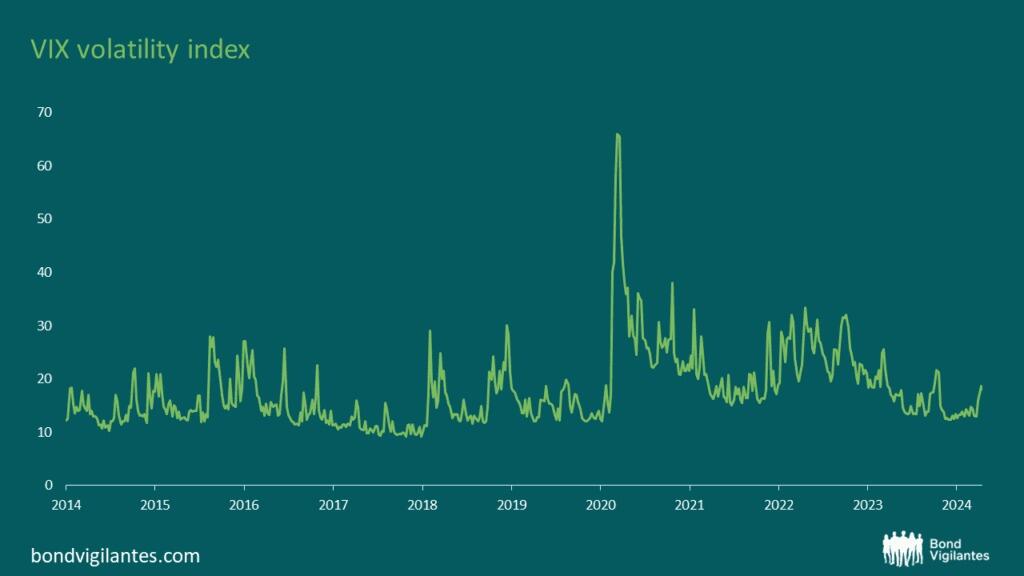

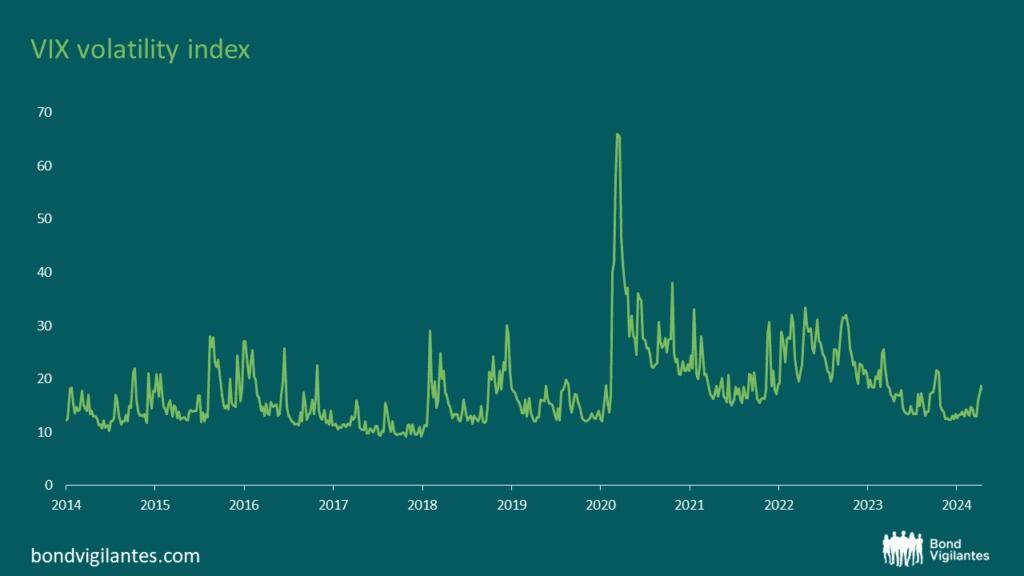

Volatility is not exploding, as shown by the volatility index VIX:

Source: M&G, Bloomberg, 23 April 2024

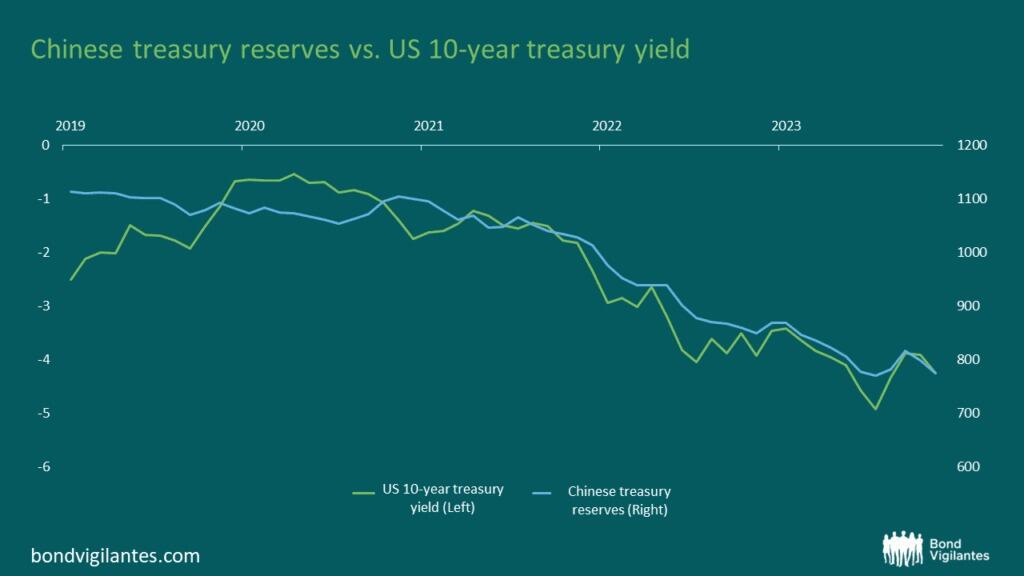

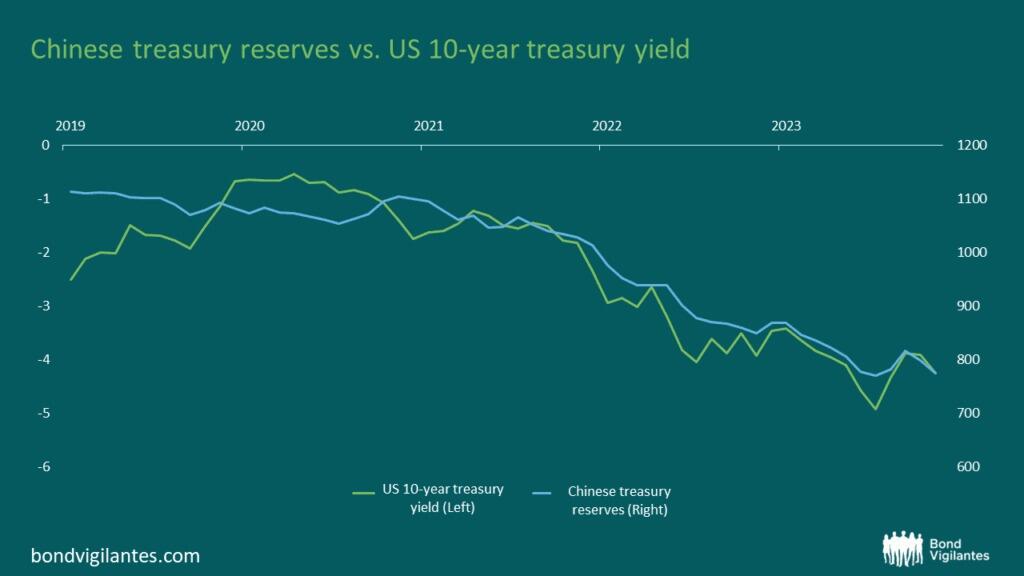

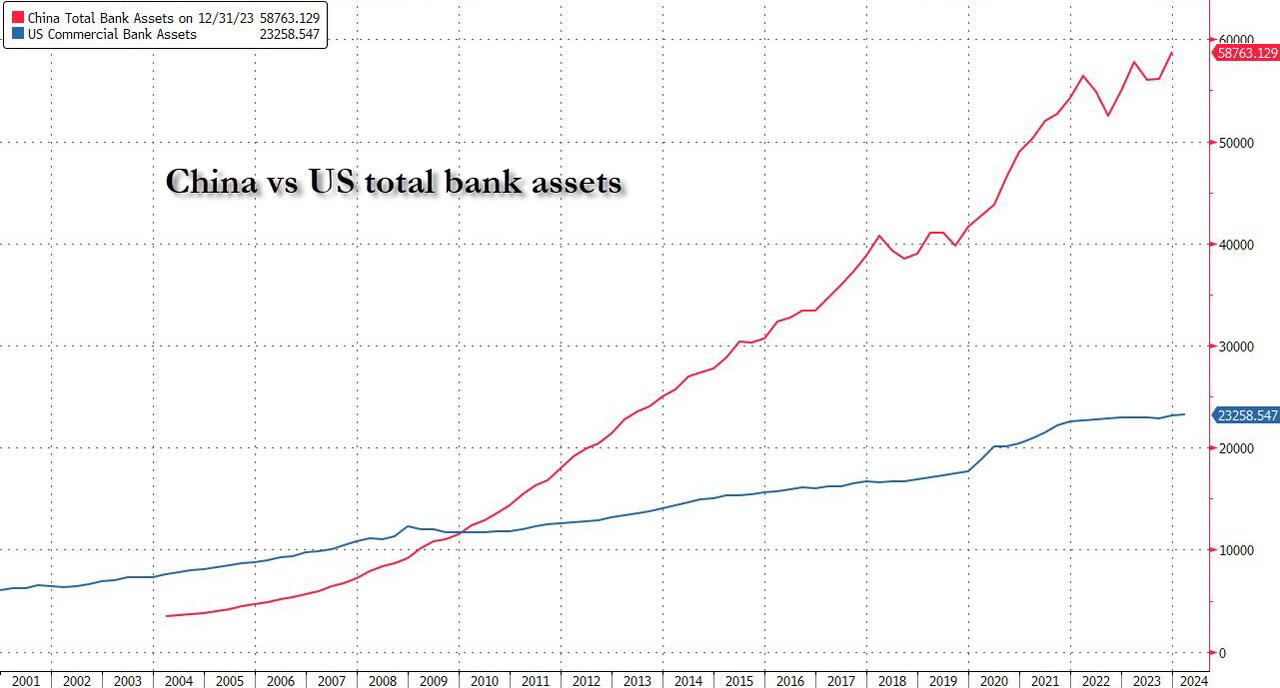

A quick look at China shows some interesting developments. We know why interest rates have gone up: to combat inflation. However, yields may still be pressured higher due to countries selling down their treasury reserves. China, for example, has been reducing its treasury reserves for some years. This is not the sole reason for higher yields but will be a contributory factor. The below chart shows Chinese treasury reserves falling plotted against the 10-year treasury yield (inverted):

Source: M&G, Bloomberg, 23 April 2024

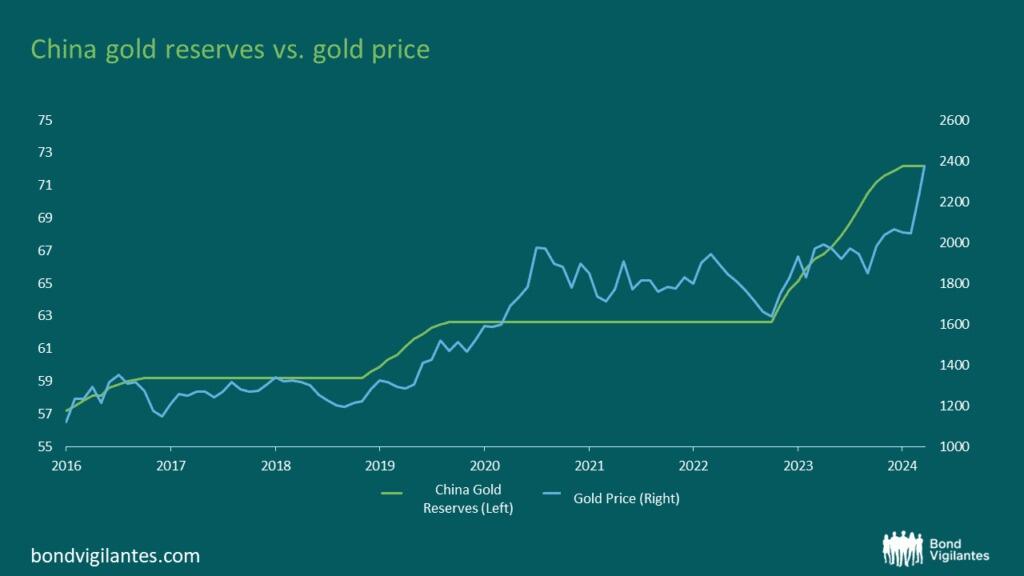

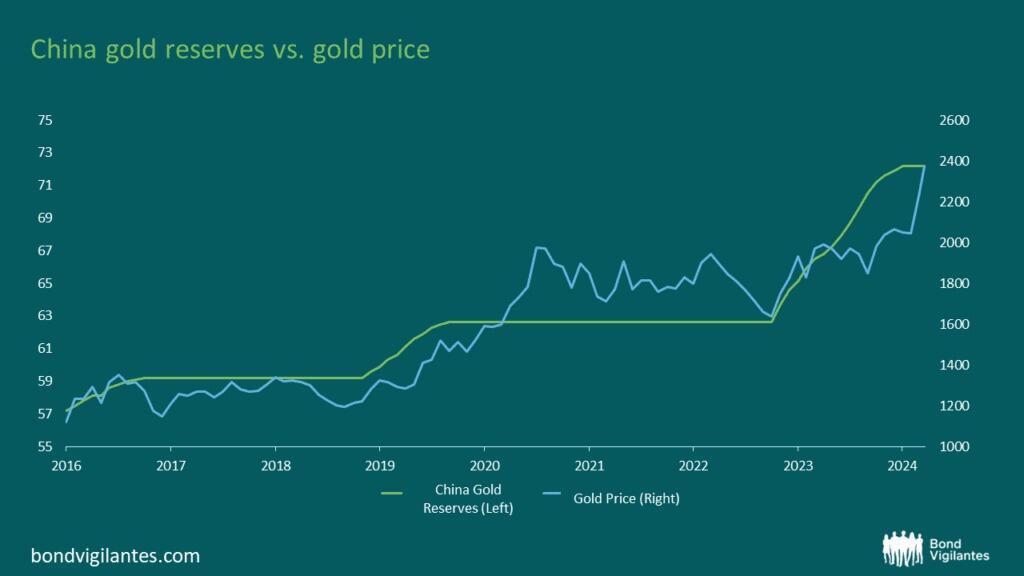

Where are these funds going? Bolstering gold reserves it would seem…

Source: M&G, Bloomberg, 23 April 2024

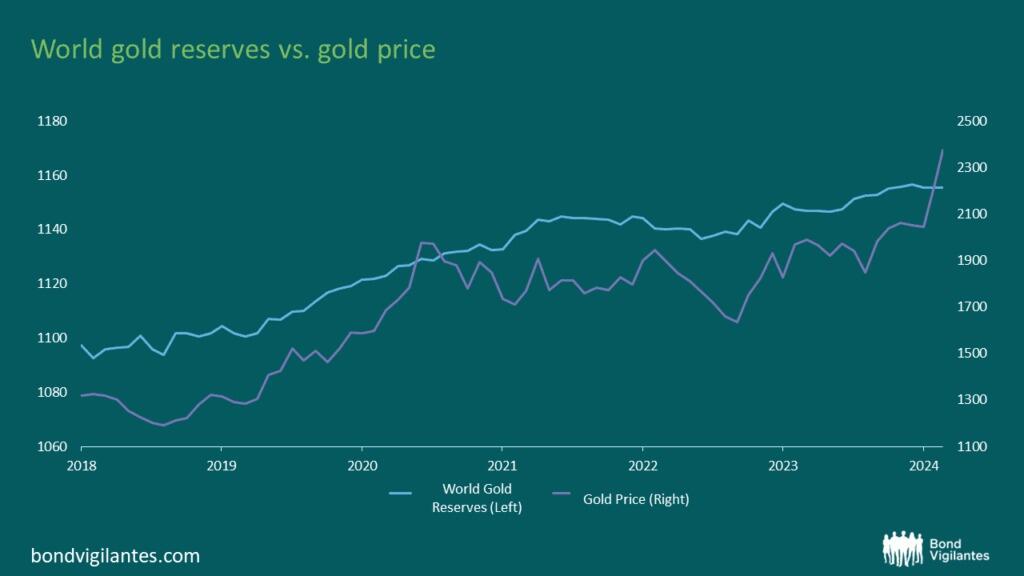

…, and China is not alone in this thinking:

Source: M&G, Bloomberg, 23 April 2024

We have witnessed many responses with the onset of the war in Ukraine, one of which is sanctions. The sanctions have attempted to lock out a country from its reserves. The West’s freezing of Russia’s gold and forex reserves in response to the conflict appears to have triggered this shift. More recently, there have been threats to confiscate Russian reserves and use these funds to support Ukraine’s efforts. This will undoubtedly make other countries somewhat nervous, especially those not 100% aligned with the West’s worldview.

Clearly, the Gold price is influenced by a multitude of factors, and one cannot point to any one single issue. However, it doesn’t seem as though gold is currently being bought for its safe-haven appeal at this stage. Where would the gold price be if the Fed starts cutting and the geopolitics worsen?

end

5 a. IMPORTANT COMMENTARIES ON COMMODITIES/

REPORT THIS AD

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP 7.2460

OFFSHORE YUAN: UP TO 7.2650

SHANGHAI CLOSED UP 8.08PTS OR 0.27%

HANG SENG CLOSED UP 83.07 PTS OR 0.48%

2. Nikkei closed DOWN 831,60 OR 2.16%

3. Europe stocks SO FAR: ALL MOSTLY MIXED

USA dollar INDEX DOWN TO 105.62 EURO RISES TO 1.0712 UP 19 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.889Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 155,55 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN:UP/ OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UPTO +2.5765*/Italian 10 Yr bond yield UP to 3..936 SPAIN 10 YR BOND YIELD UP TO 3.373

3i Greek 10 year bond yield UP TO 3.4999

3j Gold at $2329,20silver at: 27.41 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 16 /100 roubles/dollar; ROUBLE AT 92.08/

3m oil into the 82dollar handle for WTI and 88 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 155.55/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.889% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9134as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9791well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

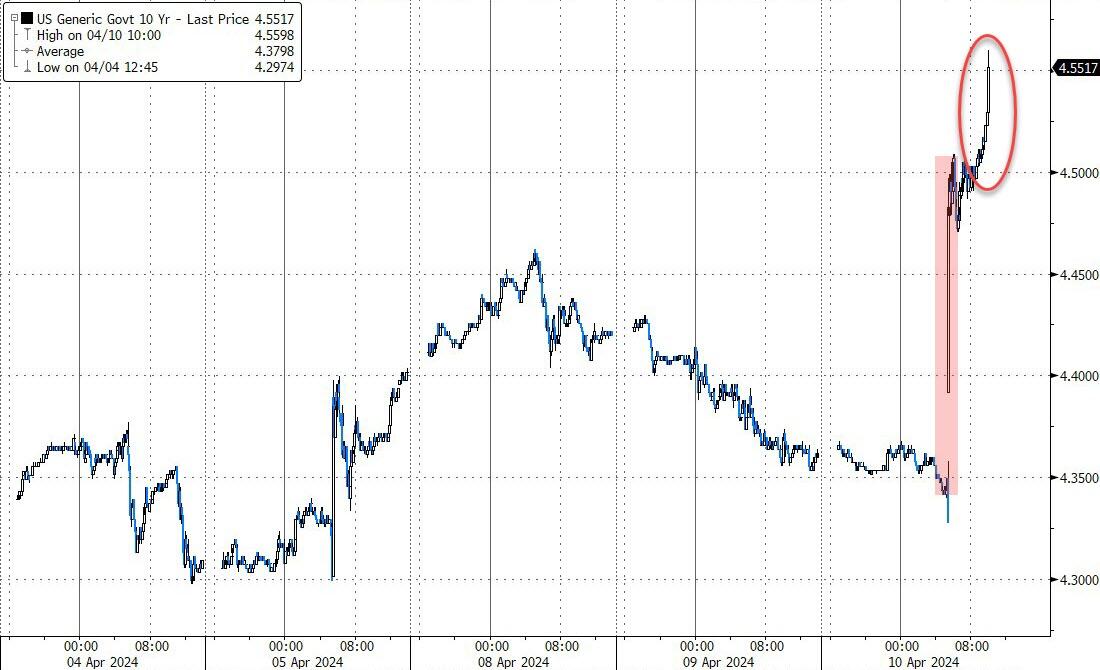

USA 10 YR BOND YIELD: 4.653UP 0 BASIS PTS…

USA 30 YR BOND YIELD: 4.787 UP 0BASIS PTS/

USA 2 YR BOND YIELD: 4.927DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.51…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.3620

end

2.a Overnight: Newsquawk and Zero hedge

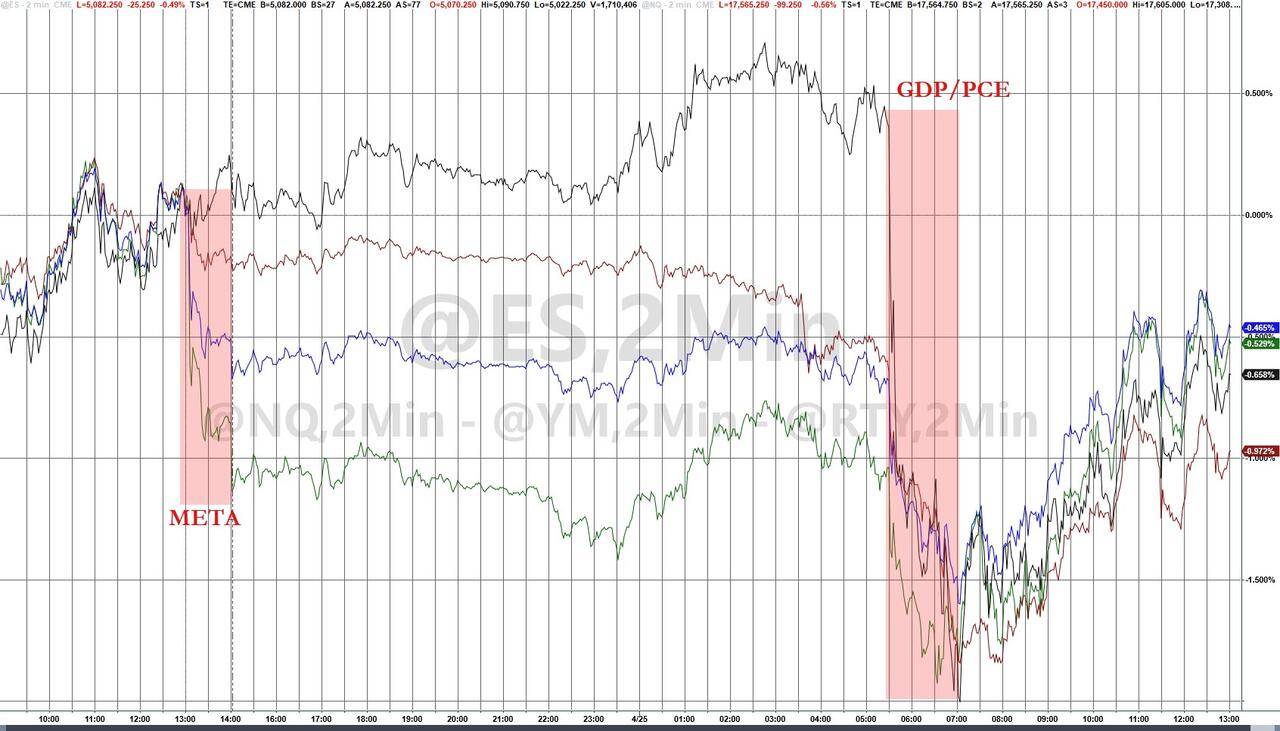

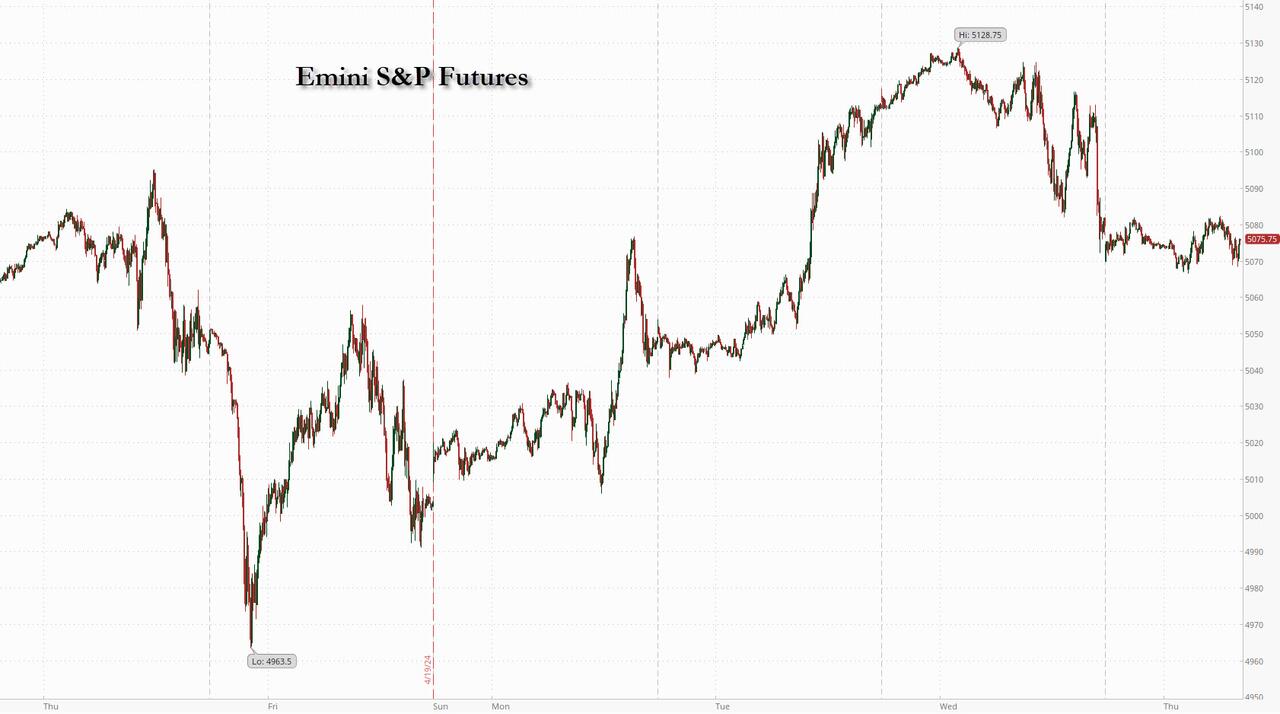

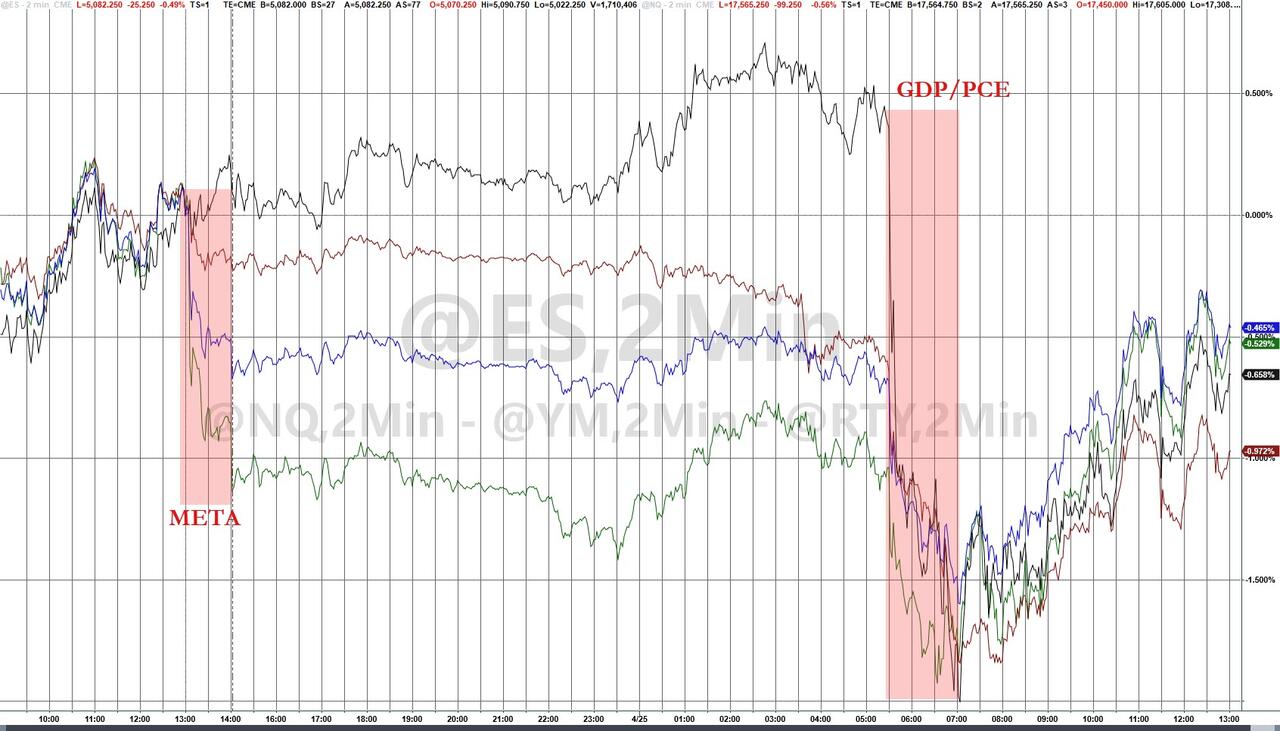

US Futures Tumble After Facebook Implodes; GDP Data On Deck

THURSDAY, APR 25, 2024 – 08:09 AM

The three-day rebound from last week’s rout ended with a thud after the close yesterday when Meta imploded, plunging as much as 17% and losing $200 billion in market cap, after the company revealed disappointing revenue guidance coupled with higher capex projections. The report sent US futures lower, and as of 7:50am, S&P futures are down 0.6% with Nasdaq futures sliding 1% (Meta accountied for more than half of the decline) dragged by Mag7 names (META -12.6%, AMZN -2.2%, MSFT -1.5%, GOOGL -2.8% but Semis are broadly stronger, buoyed by META’s capex spend (at least $70bn over next 2 years). Bond yields are flattish with the 10Y trading at 4.65% and the curve slightly steeper as the USD is moving lower but not for the yen which continues its historic implosion as the hopeless BOJ sits in shock and watches its currency collapse (there is a BOJ meeting tonight where we expect nothing from the headless chickens). Commodites are rising today with strength in Energy and Metals. In macro, we get Q1 GDP numbers today with an update on March inventories and the normal jobless claims, but tomorrow’s s PCE is the more impactful number. After the close we get earnings from GOOG/MSFT which take on heightened importance given META’s price reaction.

In premarket trading, Meta tumbled as much as 15% after it projected second-quarter sales below analyst expectations and increased spending estimates for the year (JPM tech trader Jack Atherton says he would buy the dip with META). Alphabet Inc., which reports earnings later along with Microsoft Corp., also dropped. IBM shares are also down over 8% following weak demand for the company’s consulting unit. Here are the most notable US premarket movers:

- Arista Networks (ANET US) shares rise 2.7% as analysts note that the cloud-networking company could benefit from Meta’s increased spending plans.

- Ford (F US) shares gain 3.0% after the automaker reported first-quarter adjusted earnings per share that came ahead of consensus estimates. Citi said the results were an “encouraging outcome.”

- International Business Machines (IBM US) shares slip as much as 9.0% after the company reported results that showed weak demand for the company’s consulting unit. It also confirmed the acquisition of software firm HashiCorp Inc.

- Meta Platforms (META US) shares slump 13% after the Facebook parent gave a revenue forecast that was seen as weak and increased its spending estimates for the year amid an ongoing push into AI.

- Social media and online advertising companies trade lower following disappointing results from Facebook parent Meta. Snap (SNAP US) -5.1%, Pinterest (PINS US) -4.5%, Alphabet (GOOGL US) -2.9%, Trade Desk (TTD US) -3.3%

- ServiceNow (NOW US) shares fall 4.9% after the software company gave a full-year subscription revenue forecast that was slightly weaker than expected. Analysts are broadly positive on the report.

- Silicon Laboratories (SLAB US) shares rise 2.3% as Needham & Co. upgrades rating to buy from hold. The broker says the semiconductor device company “is well positioned for the semiconductor cyclical recovery.”

Hopes for tech megacaps have been red hot after the frenzy around artificial intelligence powered Wall Street’s record-breaking rally. But gains at the start of the week are flagging, suggesting wagers on an AI-driven profit boost may be overdone. US data due Thursday could turn the focus back to the timing of Federal Reserve policy easing.

“I think we are just hitting a little bit of a reality check,” Sonja Laud, chief investment officer at Legal & General Investment Management, said on Bloomberg Television. “This doesn’t take away the excitement around the potential going forward, but it’s probably valuation coming back to a more realistic pathway.”

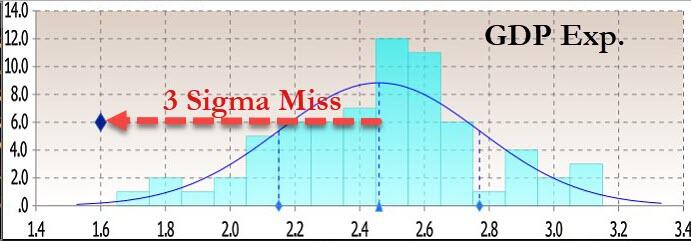

Beyond corporate results, traders are also bracing for US economic growth figures after scaling back expectations for Fed interest-rate cuts for weeks. Economists predict GDP cooled to around 2.5% in the first quarter from 3.4%, with the figures still potentially suggesting persistent inflationary pressures.

“Any downside surprises could see markets bringing expected Fed interest rate cuts earlier — after having been pushed out to much later this year,” economists at Rand Merchant Bank in Johannesburg said. “However, upside surprises could see continued market volatility as the market tries to ascertain the risk that a hotter-than-expected economy poses to anticipated interest-rate cuts.”

Meanwhile, Secretary of State Antony Blinken said the world’s largest economies must “lay out our differences,” as he began two days of talks in China, with the threat of US sanctions targeting Beijing over its support of Russia’s war in Ukraine looming over his visit.

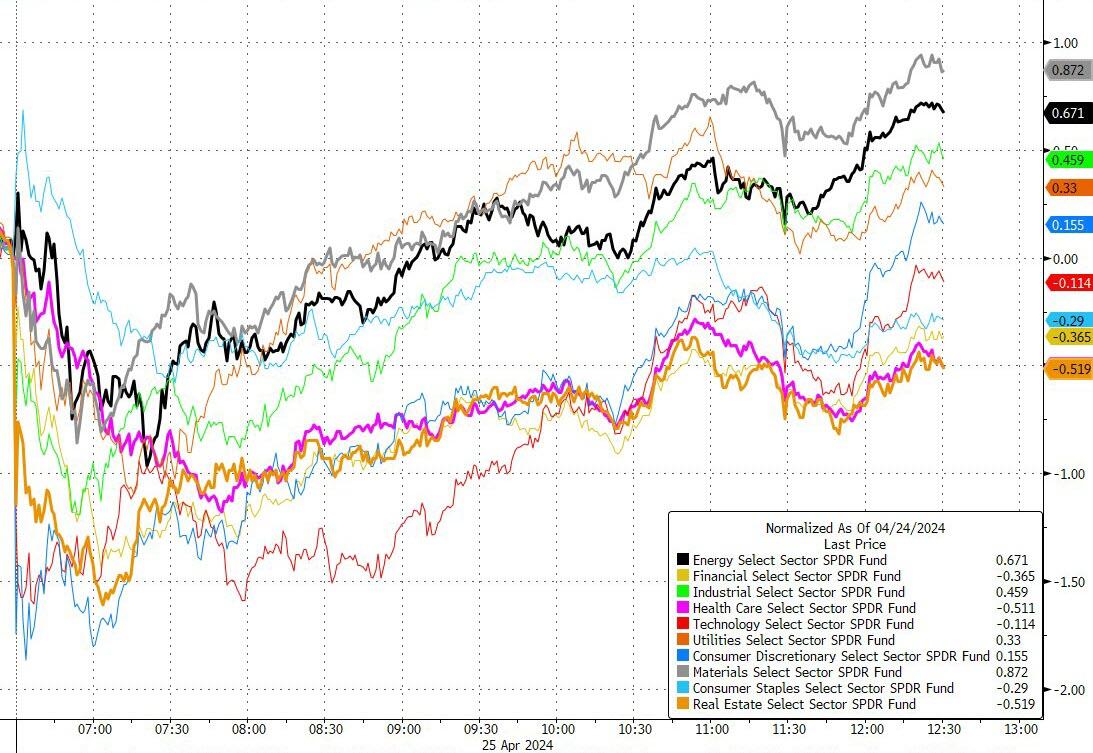

Europe’s Stoxx 600 Index edged lower with food beverage and industrial goods sectors leading declines, while mining and personal care drug shares are the biggest outperformers as traders processed a deluge of corporate updates on the busiest day of the earnings season. Anglo American Plc soared 14% after rival BHP Group made an all-share takeover proposal valuing it at £31.1 billion ($38.8 billion) in a deal that would create the world’s largest copper miner. Here are the biggest movers Thursday:

- Anglo American soars as much as 14%, hitting the highest level since July, after the miner received an all-share takeover approach worth $39 billion from global industry leader BHP

- AstraZeneca jump as much as 6.5%, the most since November 2020, after the drugmaker reported better-than-expected results for the first quarter

- Unilever gains as much as 5.3%, the most in over a month, after the consumer goods giant delivered a strong sales beat in the first quarter and showed volumes are improving

- Barclays rises as much as 5.2% to the highest since Feb. 2022, after investment banking revenue for the first quarter met the average analyst estimate

- Sanofi advances as much as 4.5%, the most since March 2023, after the French drugmaker reported first-quarter results that beat expectations, helped by new drug products Beyfortus and Altuviiio

- Adyen slumps as much as 15% after the Dutch payment firm’s 1Q report showed a decline in take rates, offsetting stronger-than-expected growth in processing volumes

- Pernod Ricard shares drop as much as 3.1% after the spirits maker reported fiscal 3Q results. Organic sales missed estimates as US buyers work through high inventories and the Chinese market remains slow

- Telia shares fall as much as 9.6% after reporting free cash flow well below estimates, with the Swedish telecom operator blaming higher interest costs and different timing of pension refund this year, among others

- Kesko slides as much as 6.5%, the most since June, after the Finnish home goods and improvement retailer reports weaker-than-expected earnings and cuts 2024 guidance, with its construction arm dragging on growth

- Neste declines as much as 11% to their lowest since 2020 after Finnish refiner reports adjusted 1Q Ebitda for the first quarter that missed estimates, driven by a weaker renewable diesel market, RBC says

In FX, the Bloomberg Dollar Spot Index falls 0.1% while the pound is among the best performing G-10 currencies, rising 0.4% versus the greenback. The yen extended losses after weakening beyond 155 per dollar for the first time in more than three decades on Wednesday, heightening the chances of intervention ahead of Bank of Japan’s policy decision Friday. The Japanese currency weakened to 155.74 per dollar on Thursday, a new 34-year low. The BOJ is forecast to keep its interest rate settings unchanged, while the yen’s plunge makes it more likely the bank will tone down its stance on keeping policy easy. Governor Kazuo Ueda’s press conference “is expected to take a hawkish tone, and even if depreciation in the yen doesn’t accelerate, the government is likely to intervene at the same time and swing the yen stronger by about 5 yen,” said Eiji Dohke, a strategist at SBI Securities. The first intervention would probably be for trillions of yen, followed by smaller long-term purchases, he said.

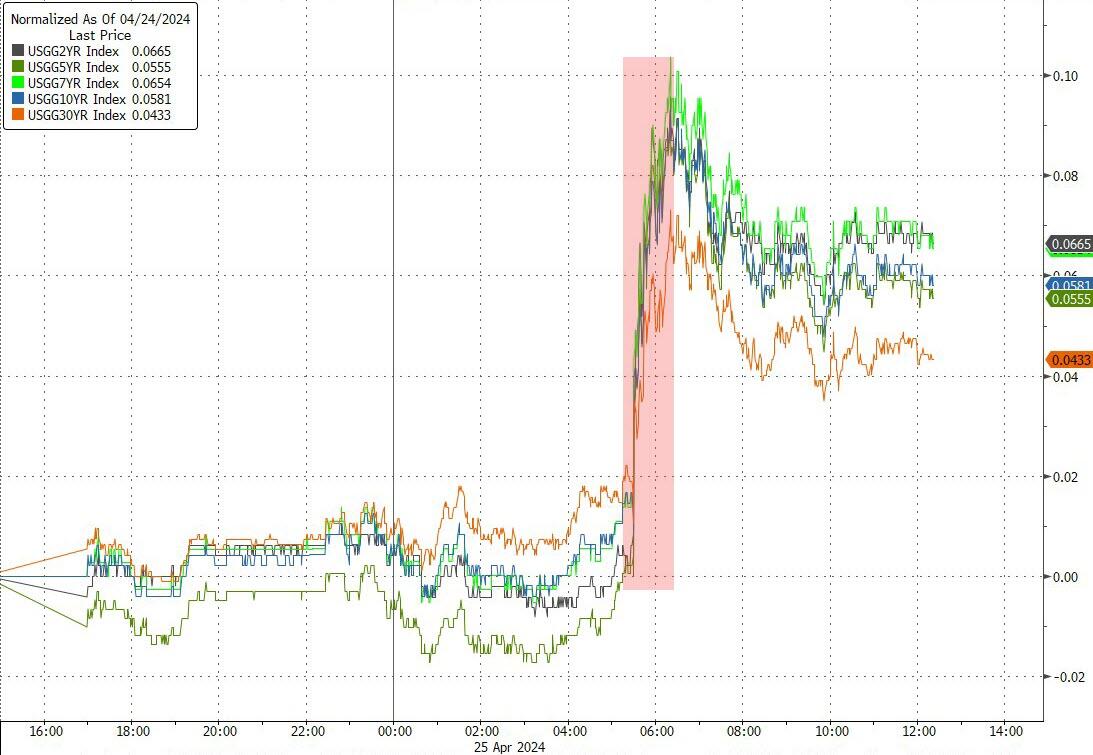

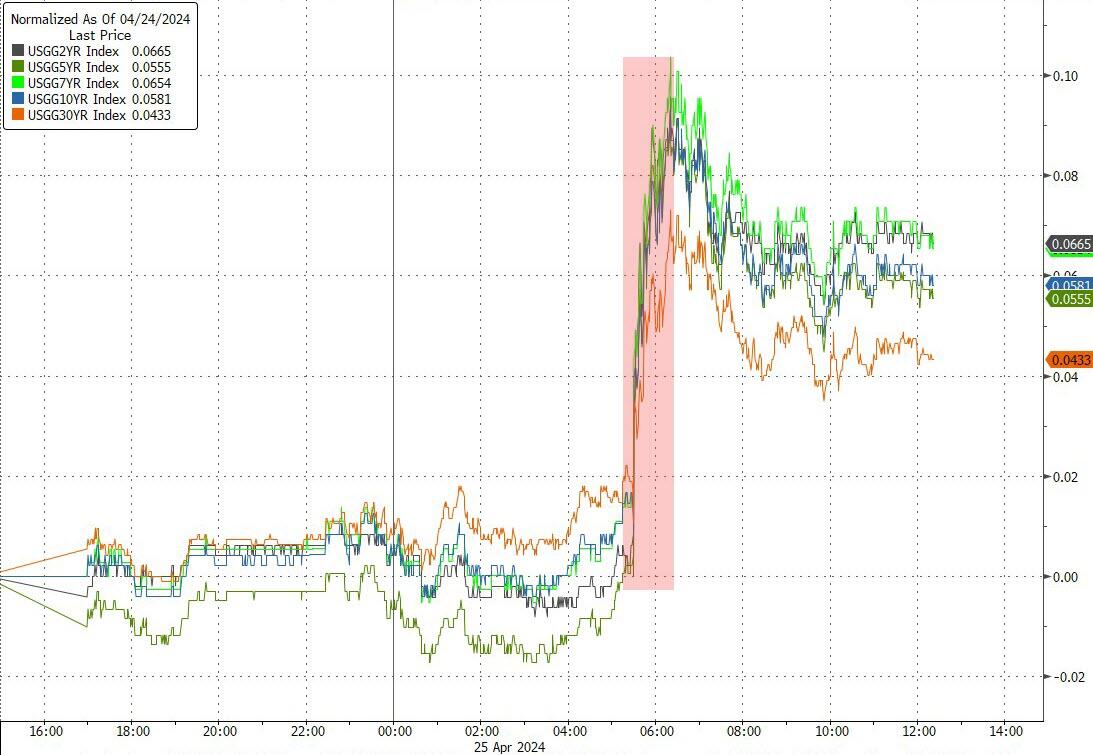

In rates, treasuries were little changed after yields rose in the previous session. US 10-year yields around 4.64% are near flat on the day with bunds and gilts outperforming by 1.5bp and 2.5bp in the sector. Core European rates outperform Treasuries, with little reaction in Spanish short-end bonds to Prime Minister Pedro Sanchez’s threat to resign, made after European markets closed on Wednesday. The week’s treasury coupon auction cycle concludes with $44b 7-year note sale at 1pm New York time, following solid results for both 2- and 5-year sales earlier this week; WI 7-year yield at ~4.652% is roughly 47bp cheaper than last month’s, which stopped 0.8bp through in a strong result.

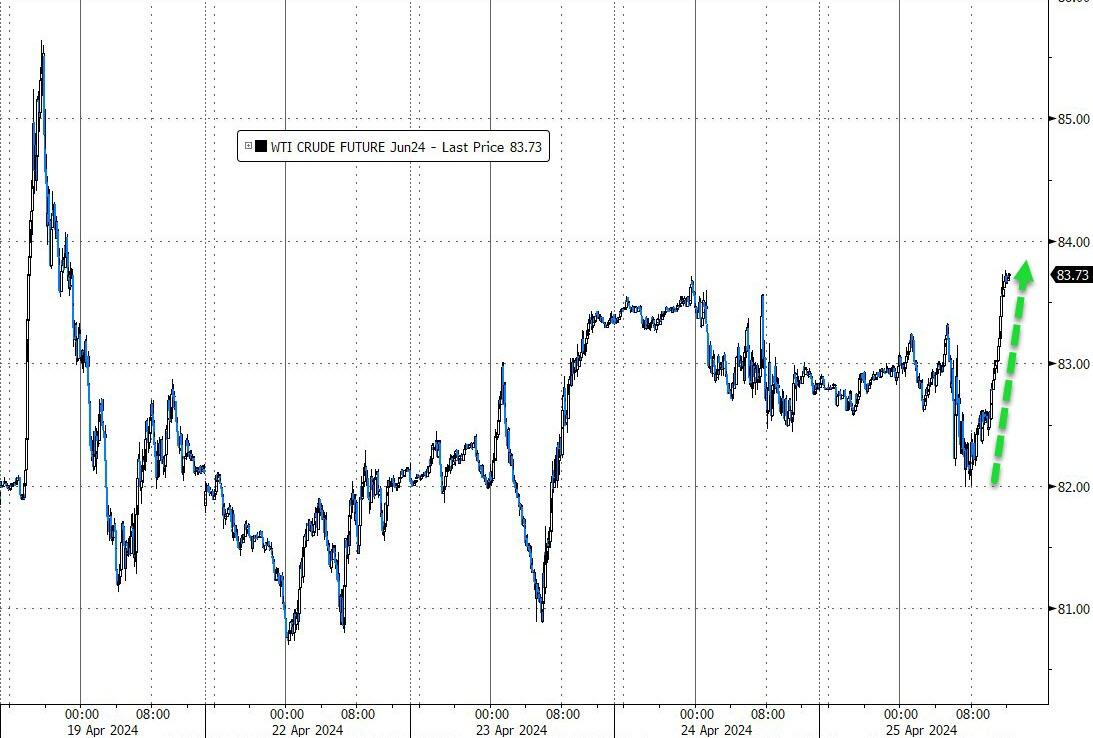

In commodities, oil prices are little changed, with WTI trading near $82.80 a barrel. Spot gold rises 0.4% to around $2,325/oz.

Bitcoin was flat in choppy trade and briefly approached the $64,000 level before fading back.

Looking at the calendar, US data releases include the initial Q1 GDP reading from the US, along with the weekly initial jobless claims, pending home sales for March, and the Kansas City Fed’s manufacturing index for April. Meanwhile from central banks, we’ll hear from ECB President Lagarde, the ECB’s Schnabel, Vujcic, Nagel and Panetta. And we’ll also get the ECB’s latest Economic Bulletin. Finally, today’s earnings releases include Microsoft, Alphabet, Caterpillar and Intel.

Corporate Highlights:

- Caterpillar Inc. reported first-quarter results that showed machinery sales dipping from a year earlier and warned its second-quarter figures are also expected to be lower.

- Lazard Inc. posted its best first-quarter revenue on record as the investment bank jostles for position among boutiques to take advantage of the rebound in mergers and acquisitions.

- Southwest Airlines Co. is slowing growth, ending service at four airports and offering voluntary leaves to address “significant challenges” in 2024 and 2025 created after Boeing Co. again reduced the number of aircraft the carrier will receive this year.

- Barclays Plc posted first-quarter revenue that topped analyst estimates after its stock traders collected a surprise windfall from tumultuous global markets.

- Deutsche Bank AG relied on its traders and investment bankers to make up for a slowdown in income from lending, as Chief Executive Officer Christian Sewing seeks to deliver on an ambitious revenue goal.

- BNP Paribas SA’s fixed-income traders trailed all of the large Wall Street banks in the first quarter, taking the shine off a strong performance in other parts of the investment bank.

- Unilever Plc sales jumped more than expected in the first quarter as Chief Executive Officer Hein Schumacher pushes ahead with his turnaround plan.

- Nestle SA sales growth sputtered in the first quarter as the maker of Nespresso coffee was hit by cooler demand in North America and supply constraints at its vitamins unit.

- STMicroelectronics NV reported weaker sales than analysts expected, exacerbated by a slowdown in chip demand from the automotive sector.

Earnings

- Meta Platforms Inc (META) Q1 2024 (USD): EPS 4.71 (exp. 4.32), Revenue 36.46bln (exp. 36.16bln), Q2 24 revenue view 36.5-39bln (exp. 38.38bln), FY24 capex view 35-40bln (exp. 34.73bln), also expects capex to increase in FY25 (exp. 37.73bln). Shares are down -12.9% pre-market.

- International Business Machines Corp (IBM) Q1 2024 (USD): Adj. EPS 1.68 (exp. 1.60), Revenue 14.46bln (exp. 14.55bln). Shares are down 8.5% pre-market

- Ford Motor Co (F) Q1 2024 (USD): Adj. EPS 0.49 (exp. 0.42), Revenue 42.8bln (exp. 40.1bln). Shares are up 3.2% pre-market

- Barclays (BARC LN) Q1 (GBP): Investment Bank Revenue 3.33bln (exp. 3.35bln). FICC Revenue 1.4bln (exp. 1.52bln); affirms FY24 NII guidance. CEO said seeing an uptick in deals flow and equity markets

- AstraZeneca (AZN LN) Q1 (USD): Core EPS 2.06 (exp. 1.89). Revenue 12.7bln (exp. 11.9bln); Confirms a 7% increase in the annual dividend announced at AGM.

- Unilever (ULVR LN) Q1 (GBP) Revenue 15bln (exp. 14.7bln). Underlying Sales +4.4% (exp. +3.6%). Co. is increasingly confident in its ability to deliver sustained volume growth and positive mix; affirms FY24 underlying sales growth.

- Nestle (NESN SW) Q1 (CHF): Organic Revenue +1.4% (Exp. 2.9%); Revenue 22.1bln (prev. 23.5bln Y/Y). CEO said “We had expected a slow start and see a strong rebound in Q2 with reliable delivery for the remainder of the year.”

- STMicroelectronics (STM FP) Q1 (USD): Revenue 3.47bln (exp. 3.63bln). Guides Q2 Revenue 3.2bln (exp. 3.8bln) and gross margin 40% (exp. 42.4%). Cuts FY24 Revenue guidance amid slower than expected Auto chip demand, now between 14-15bln (exp. 16.2bln). (Newswires)

Market Snapshot

- S&P 500 futures down 0.6% to 5,079.25

- STOXX Europe 600 down 0.1% to 504.95

- MXAP down 1.0% to 171.56

- MXAPJ down 0.4% to 531.90

- Nikkei down 2.2% to 37,628.48

- Topix down 1.7% to 2,663.53

- Hang Seng Index up 0.5% to 17,284.54

- Shanghai Composite up 0.3% to 3,052.90

- Sensex up 0.6% to 74,269.03

- Australia S&P/ASX 200 little changed at 7,683.00

- Kospi down 1.8% to 2,628.62

- German 10Y yield little changed at 2.58%

- Euro up 0.3% to $1.0726

- Brent Futures up 0.4% to $88.40/bbl

- Gold spot up 0.4% to $2,326.48

- US Dollar Index down 0.25% to 105.60

Top Overnight News

- The South Korean economy grew at the fastest pace in more than two years in the first quarter beating all estimates with a pick-up in domestic consumption and robust exports, but the market questioned if the recovery was sustainable. GDP for the January-March quarter was 1.3% higher than the preceding three months on a seasonally adjusted basis, the sharpest expansion since the fourth quarter of 2021. RTRS

- French President Emmanuel Macron, who was instrumental in making Ursula von der Leyen the European Commission president five years ago, is now in talks with fellow EU leaders to find a different candidate — such as Mario Draghi — to fill the top job. BBG

- BHP has proposed a £31bn takeover of Anglo American that would bring together two global mining companies and rank as one of the industry’s largest transactions in years. FT

- Ukraine is set to increase long-range attacks inside Russia as an influx of western military aid aims to help Kyiv shape the war “in much stronger ways”, the head of the UK military has said. FT

- Israel will no longer pursue an all-out assault on Rafah but instead proceed gradually and in a more targeted fashion so as to limit civilian casualties. WSJ

- Pivotal GDP data looks set to confirm an ongoing economic boom last quarter, adding to pressure on the Fed to keep rates steady. GDP probably rose at a 2.5% annualized rate, with consumer spending seen advancing 3%. That would mean the fastest growth on a four-quarter basis in two years. BBG

- White-collar hiring is stalling out across much of the US. Hiring in professional services, finance and tech is running at one-third the rate of the overall labor market. Wage growth for high-paid workers has also cooled. BBG

- Micron is poised to receive $6.1 billion in grants and as much as $7.5 billion in loans from the US government, to build new American factories. BBG

- Mark Zuckerberg rekindled investor fears that he would not control costs at Meta after vowing to increase spending and turn the social media group into “the leading AI company in the world”, sending its shares tumbling more than 12 per cent in pre-market trading on Thursday. FT

- Boeing DoJ aims to determine by late May if Boeing breached an agreement shielding it from criminal prosecution over 2018 and 2019 fatal crashes, Reuters reports. Families of victims urged prosecution in five-hour meetings on Wednesday. Separately, Boeing said it was disappointed at not advancing in the US Air Force’s Collaborative Combat Aircraft programme, but remains committed to delivering next-gen autonomous combat aircraft, including MQ-25 Stingray, MQ-28 Ghost Bat, and undisclosed proprietary programmes.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly subdued after the uninspiring handover from the US where futures were pressured after-hours following Meta’s underwhelming guidance, while the region also digested several earnings releases and markets in both Australia and New Zealand markets were closed for ANZAC Day. Nikkei 225 underperforms and retreated beneath the 38,000 level amid tech weakness and with earnings releases influencing price action, while the BoJ also kick-started its 2-day policy meeting. KOSPI was dragged lower amid losses in tech heavyweights despite stronger-than-expected GDP data and a blockbuster earnings report from SK Hynix. Hang Seng and Shanghai Comp. were positive with the Hong Kong benchmark underpinned amid resilience in the property industry, while the mainland eked slight gains after Premier Li noted China seeks to enhance development momentum and with US Secretary of State Blinken calling for the US and China to manage differences responsibly during a trip to China.

Top Asian News

- China is to speed up the local government special bond offer and is expected to accelerate special bond issuance in Q2 and Q3, according to PBoC-backed Financial News.

- China’s mission to the EU said if the European side suspects the existence of so-called subsidies, it is entirely possible to verify and resolve the situation through communication with the firm or a government department, after Chinese security equipment company Nuctech’s Dutch and Polish offices were raided by EU competition regulators.

- US Secretary of State Blinken called for the US and China to manage differences responsibly, according to AFP.

- Japanese Chief Cabinet Secretary Hayashi said won’t comment on forex levels or intervention but reiterated it is important for currencies to move in a stable manner reflecting fundamentals and rapid FX moves are undesirable, while he added they are closely watching FX moves and will be ready to take full response.

- Japanese Finance Minister Suzuki said closely watching FX markets and will handle it appropriately.

- South Korea’s market watchdog is preparing a new monitoring system to detect illegal stock short selling with the new mechanism to be implemented in a speedy manner, according to Reuters.

- CNOOC (883 HK) Q1 (CNY): Net 39.7bln (+24% Y/Y). Oil & Gas sales revenue CNY 89.98bln. Total net production -9.9% Y/Y

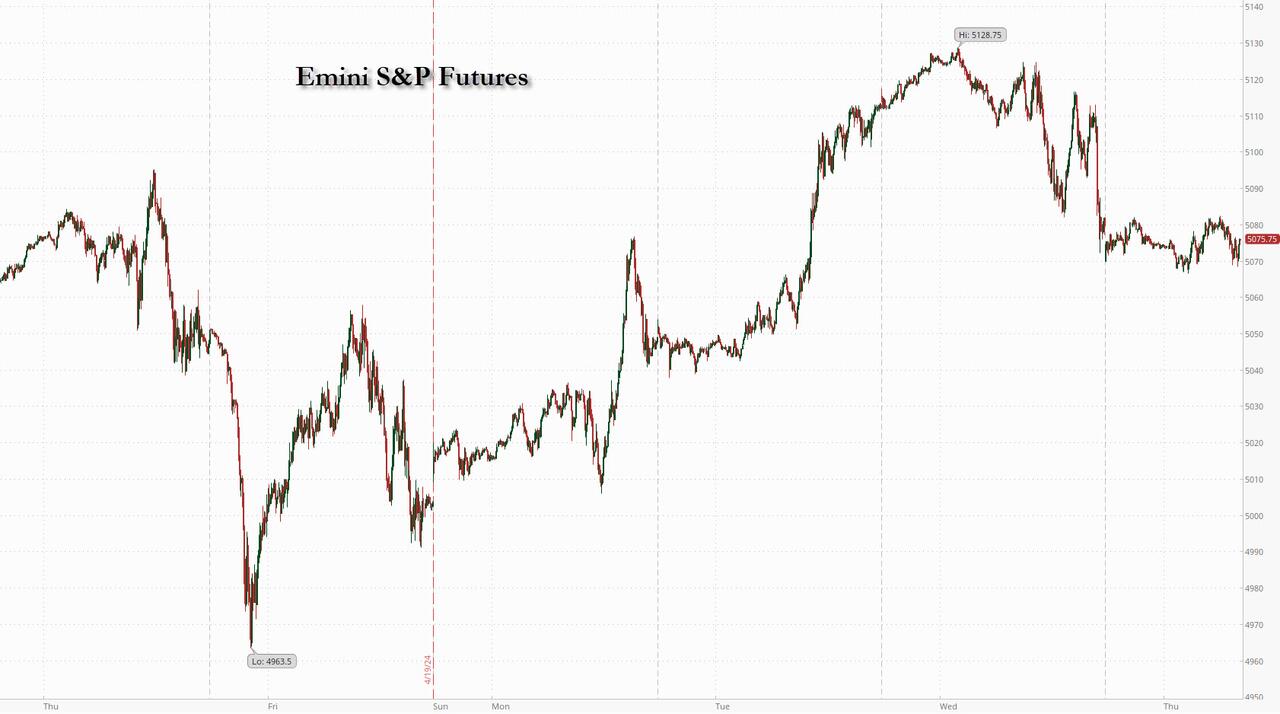

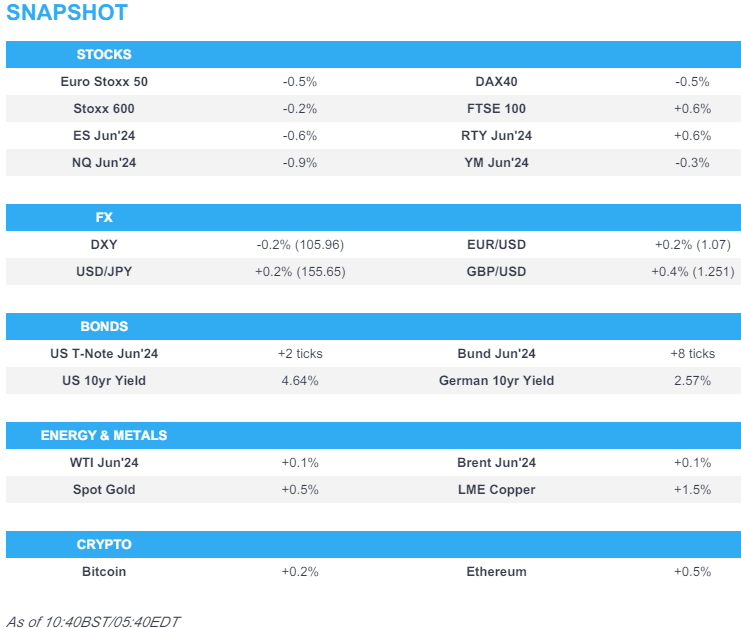

European bourses, Stoxx600 (-0.1%) initially opened mixed, though sentiment quickly soured and indices now hold a negative bias. European sectors hold a negative tilt; Basic Resources is the clear outperformer, with Anglo American (+11.5%) taking the lion’s share of the gains on BHP takeover reports; positive price action in the metals complex is also helping. Food Beverage & Tobacco is found at the foot of the pile, following post-earning losses in Nestle (-3.9%) and Pernod Ricard (-2.9%). US Equity Futures (ES -0.5%, NQ -0.9%, RTY +0.5%) are mixed, with clear underperformance in the tech-heavy NQ, dragged down by Meta (-13%) post-earnings, with IBM (-8%) also fuelling the downside.

Top European News

- ECB’s Schnabel said may face bumpy last mile of disinflation; wage growth seems to be easing in line with projections.

- ECB’s Muller said not comfortable starting with back-to-back cuts, via Bloomberg.

- BHP (BHP AT) confirmed that on the 16th April, it made an offer to Anglo America (AAL LN) regarding a potential combination; valuing Anglo American’s share capital at GBP 31.1bln (vs GBP 25.75bln market cap on Wednesday’s close)

FX

- Dollar is losing ground vs. peers (ex-JPY) with no obvious driver. DXY dipped under yesterday’s 105.59 trough but it remains to be seen how much the dollar is sold ahead of upcoming tier 1 US data.

- EUR is benefiting from the broad softness in USD with EUR/USD eclipsing yesterday’s 1.0714 peak and eyeing the 12th April high at 1.0729.

- GBP is enjoying a session of gains vs. the USD and to a lesser extent the EUR. Cable is back on a 1.25 handle for the first time since April 12th; 1.2558 was the high that day, which roughly coincides with the 200DMA at 1.2557.

- JPY is the only of the majors losing ground to the USD as USD/JPY’s ascent above 155.50 overnight is sustained. Intervention speculation remains. However, comments from an LDP lawmaker yesterday that 160 could be the line of the sand has given USD/JPY bulls confidence to chase prices higher.

- Antipodeans are at the top of the leaderboard for the majors vs. the USD. AUD/USD breached its 200DMA at 0.6526 alongside strength in copper and iron prices.

Fixed Income

- USTs are in consolidation mode below the 108 mark as traders brace for today and tomorrow’s tier 1 US data. For today’s quarterly PCE data, ING notes that a 0.4% MoM reading tomorrow could see Fed easing expectations cut back to just 25bp. Currently USTs remain contained within yesterday’s 107.20-108.02.

- Steady trade for Bunds with macro drivers on the light side, and unreactive to typical hawkish-leaning commentary from ECB’s Muller; Bunds are contained within yesterday’s range with greater attention to the downside with the 10yr just circa 20 ticks above the recent contract low.

- Gilts are marginally firmer in quiet UK trade. However, the modest gains need to be taken in the context of recent selling pressure post-Pill. 96.18 is the high for today but is a far cry from Wednesday’s 96.67 peak.

Commodities

- Choppy sideways trade for the crude complex; initial gains in the morning have now faded, with oil prices now lower on the session; Brent June in a USD 87.80-88.49/bbl parameter.

- Firm bias across precious metals amid a weaker Dollar and as geopolitical risks remain. Price action is more contained ahead of US GDP and PCE. XAU found support at USD overnight support at 2,305/oz before rising to a USD 2,328.88/oz intraday peak.

- Base metals are mostly firmer with clear outperformance in copper prices this morning and gains in iron overnight, with desks citing robust Chinese demand prospects. Elsewhere, mining giant BHP made a takeover offer for peer Anglo American.

Geopolitics

- Russian Foreign Ministry said the appearance of NATO nuclear facilities in Poland makes it a military target for Russia, according to Al Arabiya.

- Belarusian President Lukashenko said probability of incidents on the Belarusian-Ukrainian border is quite high; around 120k Ukrainian servicemen deployed near the border; Belarus has moved several battalions of fully operational readiness to the border.

US Event Calendar

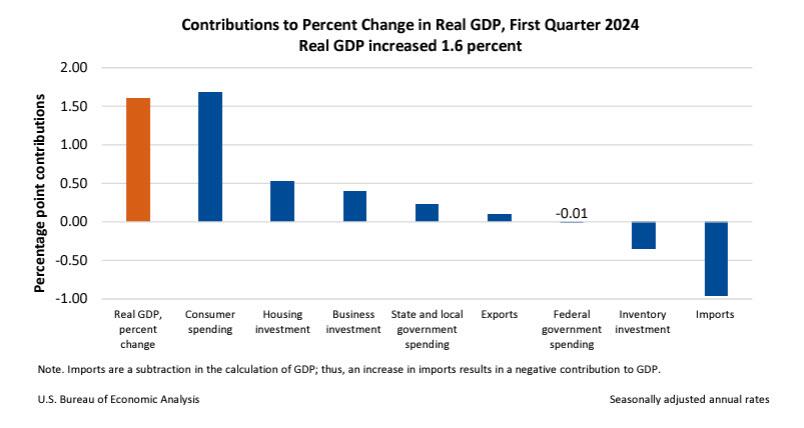

- 08:30: 1Q GDP Annualized QoQ, est. 2.5%, prior 3.4%

- 1Q Personal Consumption, est. 3.0%, prior 3.3%

- 1Q GDP Price Index, est. 3.0%, prior 1.6%

- 1Q Core PCE Price Index QoQ, est. 3.4%, prior 2.0%

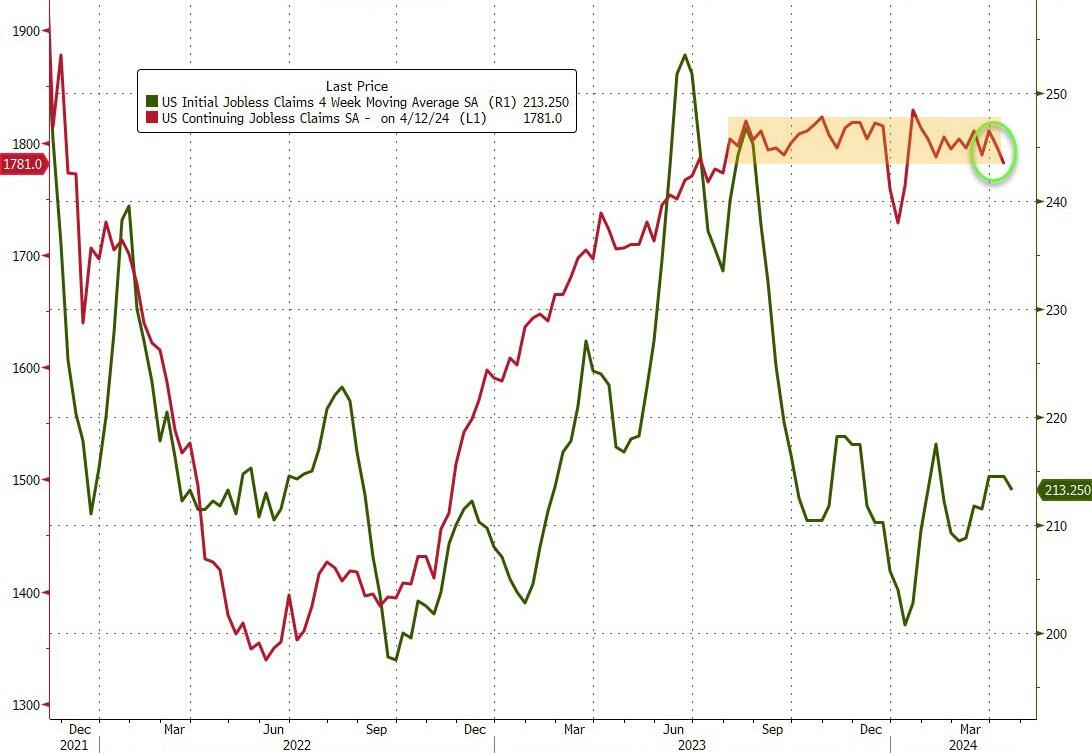

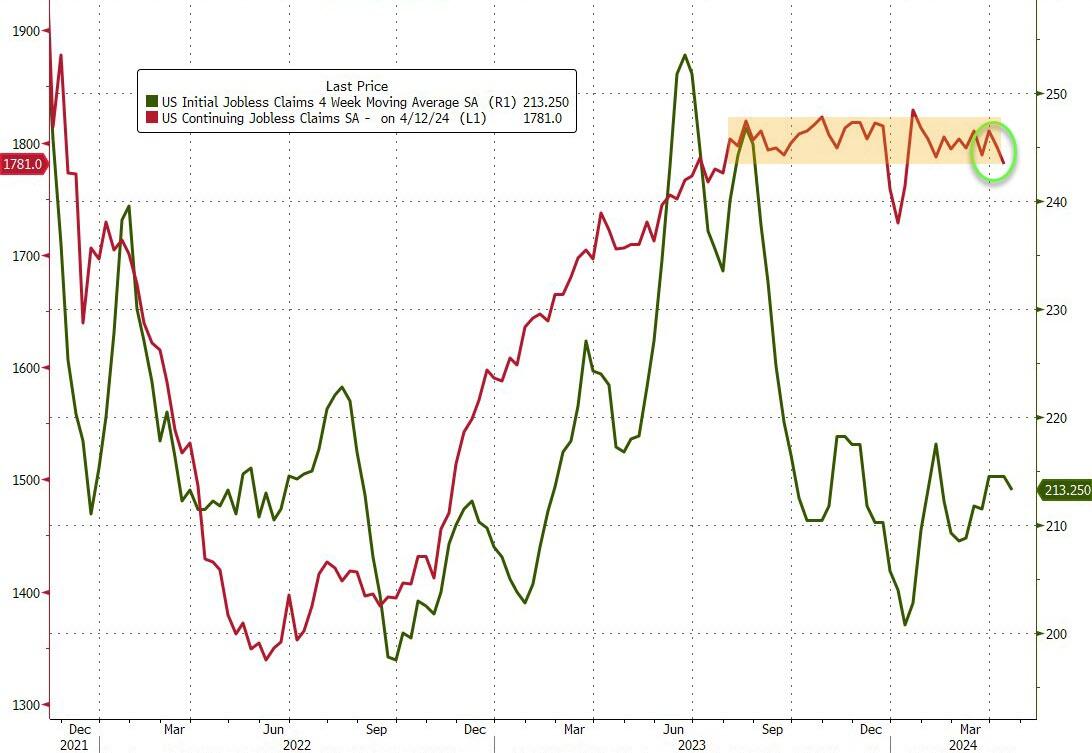

- 08:30: April Initial Jobless Claims, est. 215,000, prior 212,000

- April Continuing Claims, est. 1.81m, prior 1.81m

- 08:30: March Wholesale Inventories MoM, est. 0.3%, prior 0.5%

- March Retail Inventories MoM, est. 0.5%, prior 0.5%, revised 0.6%

- 08:30: March Advance Goods Trade Balance, est. -$91b, prior -$91.8b, revised -$90.3b

- 10:00: March Pending Home Sales (MoM), est. 0.4%, prior 1.6%

- March Pending Home Sales YoY, est. -3.0%, prior -2.2%

- 11:00: April Kansas City Fed Manf. Activity, est. -5, prior -7

DB’s Jim Reid concludes the overnight wrap

Markets have had a challenging 24 hours, and futures on the S&P 500 are down -0.66% overnight after Meta reported a disappointing outlook after the market close. Ahead of that, risk assets had already experienced a mediocre session yesterday, with equities flat in the US but down in Europe, as a bond selloff and geopolitical tensions weighed on sentiment. The losses for bonds didn’t have a single catalyst, but they gathered pace throughout the day, and in Europe it left 10yr yields at their highest levels of 2024 so far. To be honest, there were few assets that did particularly well, with the dollar index (+0.17%) the notable exception. Today will see more tech results come out as well, with Microsoft and Alphabet reporting after the US close.

Kicking off with Meta, its shares fell -15% in after-hours trading yesterday, as even though its Q1 results slightly exceeded revenue and earnings estimates, revenue guidance for Q2 came towards the lower end of analysts’ expectations. The company also raised its cost expectations for 2024, seeing capex spending totalling $35-40bn (vs. $30-37bn earlier guidance). All this led to what was in many ways a mirror image of the reaction to Tesla’s results the day before, with Meta’s outlook disappointing relative to lofty expectations that had seen its shares rise +39.4% year-to-date. Adding to more negative tech sentiment overnight, IBM slumped -8.5% after-market after its own results.