FINALIZED///WE MOVED

GOLD PRICE CLOSED UP $5.40 TO $2335.60

SILVER PRICE DOWN $0.08 TO $27.24

Gold ACCESS CLOSED $2332.85

Silver ACCESS CLOSED: $27,43

The defense of $2300 gold is now upon us and surpassed. Next up $2400 gold//Silver’s next line is $28.42. Then $34.76

The Fed is trapped as they still have their huge shortfall in gold (owes at least 67 tonnes to the BIS), They hoped that they could extricate themselves from their mess with this coming options expiry. So far, they have failed

Bitcoin morning price:$64,119 DOWN 409 DOLLARS.

Bitcoin: afternoon price: $64,654 DOWN 940 dollars

Platinum price closing UP $0 TO $915.30

Palladium price; DOWN $24,40AT $957.60

END

SHANGHAI GOLD PREMIUM 25 DOLLARS/COMEX GOLD

SHANGHAI GOLD…

SHANGHAI GOLD (USD) FUTURES – QUOTES

Last Updated 26 Apr 2024 01:48:18 PM CT.

Market data is delayed by at least 10 minutes.

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $3184.20 UP 8.20 CDN dollars per oz( * NEW ALL TIME HIGH 3,301.52 CDN DOLLARS PER OZ//APRIL 16 2024)

*BRITISH GOLD: 18671.30UP 7.05 pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2185.70 UP 13.06 ros per oz //* (ALL TIME CLOSING HIGH: 2248.89 EUROS PER OZ//APRIL 16.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: APRIL 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,329.800000000 USD

INTENT DATE: 04/25/2024 DELIVERY DATE: 04/29/2024

FIRM ORG FIRM NAME ISSUED STOPPED

190 H BMO CAPITAL 1

435 H SCOTIA CAPITAL 792

624 H BOFA SECURITIES 975

657 C MORGAN STANLEY 26

661 C JP MORGAN 145

690 C ABN AMRO 7

737 C ADVANTAGE 9

905 C ADM 3

991 H CME 6

TOTAL: 982 982

MONTH TO DATE: 17,284

JPMORGAN STOPPED (RECEIVED) 0/982 CONTRACTS

FOR APRIL/2024

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2024. CONTRACT: 982 NOTICES FOR 982,000 OZ or 3.0544 TONNES

total notices so far: 17254 contracts for 1,725,400 Oz (53.7604 tonnes)

FOR APRIL:

SILVER NOTICES: 13NOTICE(S) FILED FOR 65,000 OZ/

total number of notices filed so far this month : 1649 for 8,245,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $5.40

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL 1.54 TONNES FROM THE GLD

/ /INVENTORY RESTS AT 832.19 TONNES

INVENTORY RESTS AT 832.19 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER DOWN$0.08 AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.097MILLION OZ OUT OF THE SLV/

// INVENTORY INCREASES T0 428.717MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 428.717MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUMONGOUS SIZED 2779 CONTRACTS TO 178,226 BUT STILL RAPIDLY CLOSING IN ON THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, DESPITE THE RAID AND THIS HUMONGOUS SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR SMALL GAIN OF $0,05 IN SILVER PRICING AT THE COMEX ON THURSDAY. WE HAD SOME LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN PANICKING SHORT COVERING BY OUR SPECS WITH THE SMALL PRICE GAIN IN PRICE. WE HAD A HUGE SIZED 733T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 733 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.05, BUT WERE SUCCESSFUL IN KNOCKING SOME SILVER LONGS AS WE HAD A HUGE SIZED LOSS OF 2279 CONTRACTS ON OUR TWO EXCHANGES DESPITE THE GAININ PRICE OF $0.05

WE MUST HAVE HAD:

A STRONG SIZED 500 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 2.465 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 65,000 OZ QUEUE JUMP //NEW STANDING REMAINS AT 8.260 MILLION OZ//

//NEW STANDING FOR SILVER IS THUS 8.260 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI LOSS/ STRONGSIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 8733CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED A STRONG 1470 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL

TOTAL CONTRACTS for 20DAYS, total 29,387 contracts: OR 146.935 MILLION OZ (1469CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 144.185 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 146.935 MILLION OZ (THIS MONTH WILL PROBABLY BE A WHOPPER OF ISSUANCE OF EFPS//4TH HIGHEST EVER RECORDED FOR A MONTH)

RESULT: WE HAD A HUMONGOUS SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1247 CONTRACTS DESPITE OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG EFP ISSUANCE CONTRACTS: 500 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL. OF 2.465 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAYS’ 65,000 QUEUE JUMP TO LONDON

//NEW TOTAL STANDING REMAINS AT 8.260 MILLION OZ

WE HAVE A HUGE SIZED LOSS OF 2279 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 733 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS

THE NEW TAS ISSUANCE THURSDAY NIGHT (733 WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 13 NOTICE(S) FILED TODAY FOR 65,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 1203 OI CONTRACTS TO 520914 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 1203CONTRACTS

WE HAD A GOODSIZED INCREASE IN COMEX OI (3224CONTRACTS) WITH OUR $5.05 GAIN IN PRICE//THURSDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER TO WHACK GOLD’S PRICE. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR APRIL. AT 44.8615 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUMONGOUS QUEUE JUMP OF 81,300 OZ.(2.528TONNES)

NEW STANDING 53.673 TONNES// ALL OF THIS HAPPENED WITH OUR $5.05 GAIN IN PRICE WITH RESPECT TO THURSDAY’S TRADING. WE HAD A STRONG SIZED GAIN OF 5788OI CONTRACTS (18.00 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2564 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 520,914

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5788 CONTRACTS WITH 3224 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 2564 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 6991 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED 2087CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2564 CONTRACTS) ACCOMPANYING THE GOOD SIZED GAIN IN COMEX OI 4427 TOTAL GAIN FOR OUR THE TWO EXCHANGES: 5788 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 44.8615 TONNES FOLLOWED BY TODAY’S MASSIVE QUEUE JUMP 2.528TONNES

//NEW STANDING 53.673TONNES.

/ 3) ZERO LONG LIQUIDATION WITHTHE GAIN IN PRICE.

// 4) GOOD SIZED COMEX OPEN INTEREST GAIN/ 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: STRONG T.A.S. ISSUANCE: 5826CONTRACTS/ HUGE SHORT COVERING BY OUR WRONG FOOTED SPECS WITH THE FED’S CONTINUAL RAID ON THE COMEX GOLD.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL. :

TOTAL EFP CONTRACTS ISSUED: 76,382 CONTRACTS OR 7,638,200 OZ OR 237.58TONNES IN 20TRADING DAY(S) AND THUS AVERAGING: 3968 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20TRADING DAY(S) IN TONNES 229.60 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 237.58DIVIDED BY 3550 x 100% TONNES = 6.69% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 237.58 TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A -HUGE SIZED 2779 CONTRACTS OI TO 178,266 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 500 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 800 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 500 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1247 CONTRACTS AND ADD TO THE 500 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2279 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 11.35 MILLION OZ

OCCURRED DESPITE OUR $0.05 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

REPORT THIS AD

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

Advertisements

REPORT THIS AD

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING/THURSDAY NIGHT

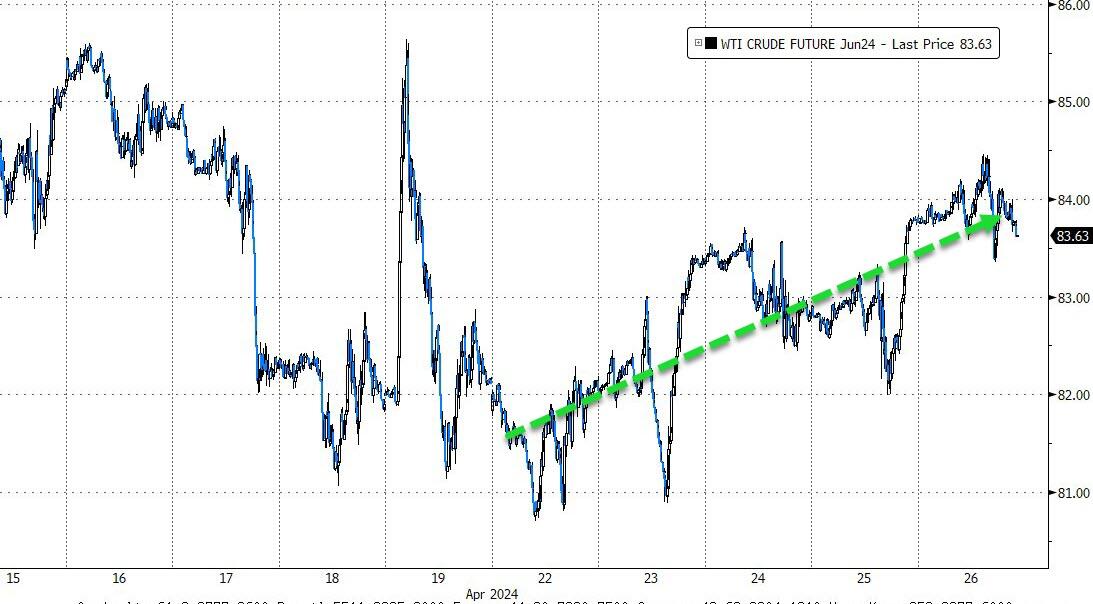

SHANGHAI CLOSED UP 35.74PTS OR 1.17% //Hang Seng CLOSED UP 366.61 PTS OR 2.12% / Nikkei CLOSED UP 306.28 PTS 0.81% //Australia’s all ordinaries CLOSED DOWN 1.29%///Chinese yuan (ONSHORE) closed UP 7.2464//OFFSHORE CHINESE YUAN CLOSED UP TO 7.2603 Oil UP TO 84.17dollars per barrel for WTI and BRENT UP AT 89.52Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GOOD SIZED 3224 CONTRACTS TO 522,017 WITH OUR GAIN IN PRICE OF $5.05 WITH RESPECT TO THURSDAY TRADING. WE HAD CONSIDERABLE A.S. LIQUIDATION AS WELL AS SHORTS, DESPERATELY TRYING TO GET OUT OF THEIR NAKED SHORTS.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF APRIL..… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG 2564 EFP CONTRACTS WERE ISSUED: : JUNE 2564 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2564CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 5788 CONTRACTS IN THAT 2564 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A GOOD SIZED GAIN OF 3234 COMEX CONTRACTS..AND THIS STRONG GAIN ON OUR TWO EXCHANGES HAPPENED WITHOUR GAIN IN PRICE OF $5.05 THURSDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT WAS A FAIR SIZED 2087 CONTRACTS. WE HAD 0 EX FOR RISK ISSUANCE. MOST OF THE TRADING AND SUPPLY OF CONTRACTS ON THURSDAY WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: APRIL (53.673 TONNES) ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNEES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $5.05 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG SIZED GAIN OF 6991 TOTAL CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR GAIN IN PRICE 0F $5.05

WE HAD A FAIR T.A.S. LIQUIDATION ON THE FRONT END OF WEDNESDAY’S TRADING ALONG. THE T.A.S. ISSUED ON THURSDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 21,744 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL. (44.8615 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE QUEUE.JUMP OF 81,300 OZ (2.528 TONNES)//NEW STANDING; 53.673 TONNES

NEW STANDING: 50.650ONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $5.05

WE HAD REMOVED 1203 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET GAIN ON THE TWO EXCHANGES 5788 CONTRACTS OR 578,800OZ (5.988ONNES)

confirmed volume THURSDAY 239,815 contracts//fair

//speculators have left the gold arena

APRIL 26INITIAL APRIL GOLD

/ /// THE APRIL 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 96,453oz Brinks 3 kilobars . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | NIL |

| No of oz served (contracts) today | 982notice(s) 98,200OZ 3.0544TONNES |

| No of oz to be served (notices) | 2 contracts 200 OZ 0.00622 ONNES |

| Total monthly oz gold served (contracts) so far this month | 17,254notices 1,725,400oz 53.7604 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: nil oz

we have 0 customer deposits:

total deposit 0 oz

total customer withdrawals: 1

i) Out of Brinks: 96.453 oz (3 kilobars)

Adjustments: 1

adjustment: 99,346.590oz dealer to customer//brinks

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of APRIL we have an oi of 984 contracts having GAINED 879 contracts. We had 66 contracts served on THURSDAY, so we GAINED 813 contracts or an additional WHOPPING 81,300 oz (2,528onnes) will stand at the comex

MAY LOST 138 CONTRACTS TO STAND AT 1869

JUNE DEREASED ITS OI BY 1366CONTRACTS DOWN TO 407,129CONTRACTS.

We had 982contracts filed for today representing 98,200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 145 notices were issued from their client or customer account. The total of all issuance by all participants equate to 982 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the APRIL. /2024. contract month, we take the total number of notices filed so far for the month (17,284x 100 oz ), to which we add the difference between the open interest for the front month of APRIL. (984CONTRACTS) minus the number of notices served upon today (982x 100 oz per contract( equals 1,725,600OZ OR 53.673TONNES.

thus the INITIAL standings for gold for the APRIL. contract month: No of notices filed so far (17,284) x 100 oz + (984{OI for the front month} minus the number of notices served upon today (982 x 100 oz which equals 1,725600 oz (53.67 7TONNES)

TOTAL COMEX GOLD STANDING FOR APRIL: 53.67 TONNES WHICH IS HUGE FOR THIS ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX84XXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,567,289.026 48.749tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,622,732.936OZ

TOTAL REGISTERED GOLD 7,532,908.295 (234.236 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,090,381.598OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 5,965,619 oz (REG GOLD- PLEDGED GOLD)

185.54tonnes/dropping like a stone

END

SILVER/COMEX

APRIL 26

INITIAL

//2024// THE APRIL 2025SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1090,885.745 oz Delaware Loomis . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | |

| No of oz served today (contracts) | 13 CONTRACT(S) (65,000 OZ) |

| No of oz to be served (notices) | 3 contracts (15,000 oz) |

| Total monthly oz silver served (contracts) | 1649 Contracts (8,245,000oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit :nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0 deposits customer account:

total customer deposits nil oz

JPMorgan has a total silver weight: 130.1709million oz/294.016million or 44.06%

adjustment: 1

manfra dealer to customer 628,810.09 oz

Comex withdrawals: 2

i) 556,146,615 oz Delaware

ii) Loomis: 514m739.110 oz

total withdrawal 1090,885,745oz

TOTAL REGISTERED SILVER: 47.602MILLION OZ//.TOTAL REG + ELIGIBLE. 294.016million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF APRIL /2023 OI: 16 CONTRACTS HAVING GAINED 11 CONTRACT(S).

WE HAD 2 CONTRACTS SERVED ON THURSDAY, SO WE GAINED 13 CONTRACTS OR ADDITIONAL 650000 OZ WILL STAND AT THE COMEX.

.

MAY SAW A LOSS OF 13,936 CONTRACTS DOWNTO 19,876

JUNE SAW A GAIN OF 164 CONTRACTS RISING TO 902

JULY SAW A GAIN OF 10,669 CONTRACTS UP TO 124,766

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 13for 65,000oz

CONFIRMED volume; ON MONDAY 134,446HUGE

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 1649 5,000 oz = 8,245,000 oz

to which we add the difference between the open interest for the front month of APRIL (16and the number of notices served upon today 13x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL/2024 contract month: 1649(notices served so far) x 5000 oz + OI for the front month of APRIL. (16)number of notices served upon today (13x 500 oz of silver standing for the APRIL contract month equates to 8.260 MILLION OZ.

New total standing: 8.260 million oz.

There are 47.602 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

APRIL 26WITH GOLD UP $5.40TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.54 TONNES FROM THE GLD /INVENTORY RISES AT 832.19 TONNES

APRIL 25WITH GOLD UP $5.05 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD /INVENTORY RISES AT 833,63 TONNES

APRIL 19 WITH GOLD UP $15.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 4.32 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 831.91 TONNES

APRIL 18 WITH GOLD UP $11.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE WITHDRAWAL OF 2.59 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 827.59 TONNES

APRIL 17 WITH GOLD DOWN $17.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 830;18 TONNES

REPORT

APRIL 16 WITH GOLD UP $23.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 828.45 TONNES

APRIL 15 WITH GOLD UP $9.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE WITHDRAWAL OF 4.03 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 826.72 TONNES

APRIL 12 WITH GOLD UP $2.80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD/ INVENTORY RISESS AT 830.75 TONN

APRIL 10 WITH GOLD DOWN $14.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 828.71 TONNES

APRIL 9 WITH GOLD UP $11.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 827,85 TONNES

APRIL 8 WITH GOLD UP $7.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A WITHDRAWAL OF 6.02 TONNES OF GOLD INTO THE GLD/ INVENTORY REMAINS AT 826.41 TONNES

APRIL 5 WITH GOLD UP $38.65 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/ INVENTORY REMAINS AT 832.45 TONNES

APRIL 4 WITH GOLD DOWN $3.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD/ INVENTORY REMAINS AT 830.73 TONNES

APRIL 3 WITH GOLD UP $33,85 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD // INVENTORY REMAINS AT 829.00 TONNES

APRIL 2 WITH GOLD UP $23.90 TODAY; HUG CHANGES IN GOLD INVENTORY AT THE GLD A WITH DRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD.:// INVENTORY REMAINS AT 829.00 TONNES

APRIL 1 WITH GOLD UP $18.70 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:// INVENTORY REMAINS AT 830.15 TONNES

MARCH 28 WITH GOLD UP $26.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:// INVENTORY REMAINS AT 830.15 TONNES

MARCH 27 WITH GOLD UP $15.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// INVENTORY FALLS TO 830.15 TONNES

MARCH 26 WITH GOLD UP $1.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 835.33 TONNES

MARCH 25 WITH GOLD UP $17.05 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 838.50 TONNES

MARCH 22 WITH GOLD DOWN $23.75 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 838.50 TONNES

GLD INVENTORY: 832.17 TONNES,

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 26WITH SILVER DOWN .08 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.097 MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 25WITH SILVER UP $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 1.534 MILLION OF SILVER OUT OF THE SLV// :SLV INVENTORY RESTS AT 428.717 MILLION OZ

APRIL 24/WITH SILVER DOWN $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 11.904MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 428.280 MILLION OZ

APRIL 23/WITH SILVER UP $0.11TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV / :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 22/WITH SILVER DOWN $1.51 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.194 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 19/WITH SILVER UP 42 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.657 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 418.570 MILLION OZ

APRIL 18/WITH SILVER DOWN $.04TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.977 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 422.227 MILLION OZ

APRIL 17/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF .868 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 426/204 MILLION OZ

APRIL 16/WITH SILVER DOWN $0.46 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF NON EXISTENT SILVER// :SLV INVENTORY RESTS AT 427.072 MILLION OZ

APRIL 15/WITH SILVER UP $0.46 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 12/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 4.069 MILLION OZ FROM THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 11/WITH SILVER UP $0.23 TODAY: STRANGE INDEED! HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.931 MILLION OZ :SLV INVENTORY RESTS AT 437.998 MILLION OZ

APRIL 10/WITH SILVER UP $0.04 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:SLV INVENTORY RESTS AT 441.929 MILLION OZ

APRIL 9/WITH SILVER UP $0.15 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.549 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 441.929 MILLION OZ

APRIL 8/WITH SILVER UP $0.33 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.320 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 441.328 MILLION OZ

APRIL 5/WITH SILVER UP $0.61 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.748 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 441.060 MILLION OZ

APRIL 4/WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.671 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 437.312 MILLION OZ

APRIL 3/WITH SILVER UP $1.14 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.835 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 433.641 MILLION OZ

APRIL 2/WITH SILVER UP 84 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6.721 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 430.806 MILLION OZ

APRIL 1/WITH SILVER UP 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// SLV INVENTORY RESTS AT 424.085 MILLION OZ

MARCH 28/WITH SILVER UP 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.005 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 424.085 MILLION OZ

REPORT THIS AD

MARCH 27/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A A DEPOSIT OF 1.691 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 423.079 MILLION OZ

MARCH 26/WITH SILVER DOWN 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A A DEPOSIT OF 0.366 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 421.388 MILLION OZ

MARCH 25/WITH SILVER UP 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 3.887 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 421.022 MILLION OZ

MARCH 22/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE DEPOSIT OF 1.1899 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 424.909 MILLION OZ

CLOSING INVENTORY 428.717 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

PETER SCHIFF/SCHIFFGOLD/MIKE MAHARRAY

END

2.Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens/…

e

END

3. CHRIS POWELL//GATA DISPATCHES

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS

end

5 a. IMPORTANT COMMENTARIES ON COMMODITIES/

REPORT THIS AD

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP 7.2464

OFFSHORE YUAN: UP TO 7.2603

SHANGHAI CLOSED UP 35.74PTS OR 1.17%

HANG SENG CLOSED UP 366.61PTS OR 2.12%

2. Nikkei closed UP 306.28OR 0.81%

3. Europe stocks SO FAR: ALL GREEN

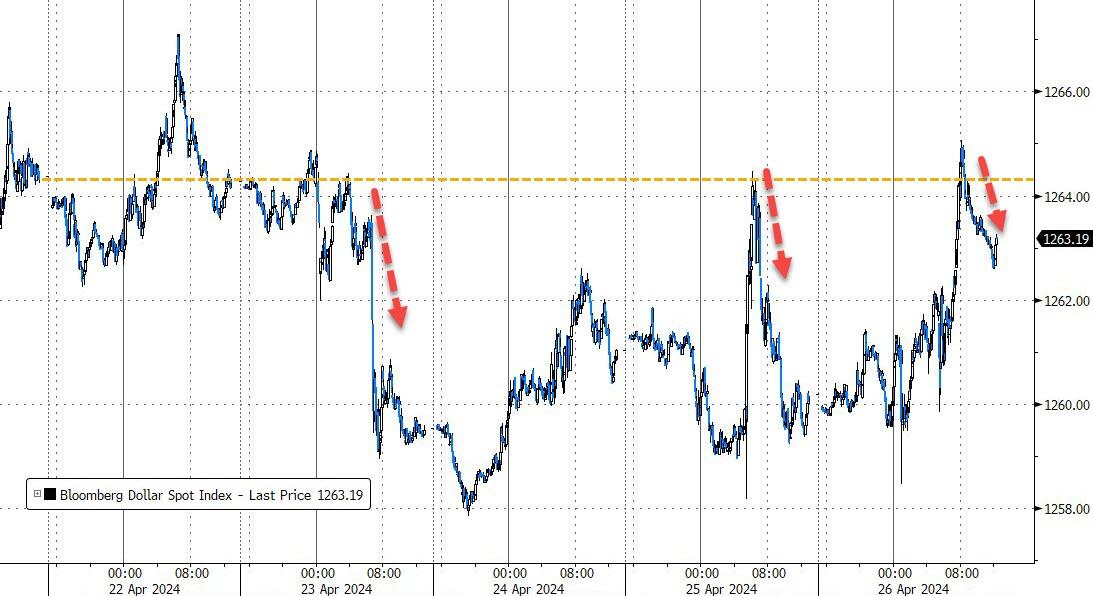

USA dollar INDEX UP TO 105.55 EURO RISES TO 1.0730 UP 3 BASIS PTS

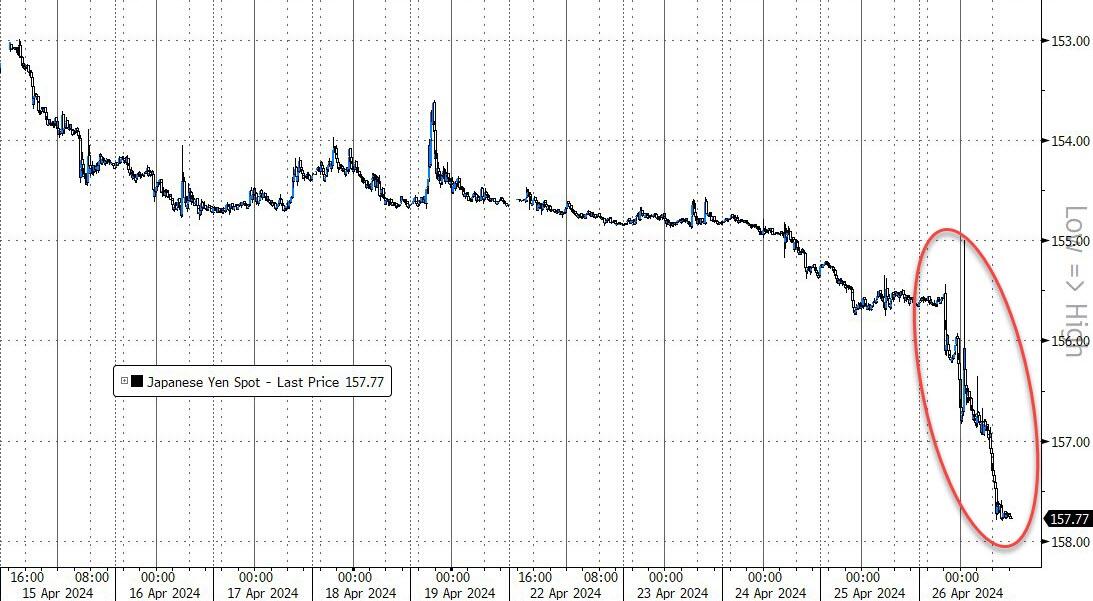

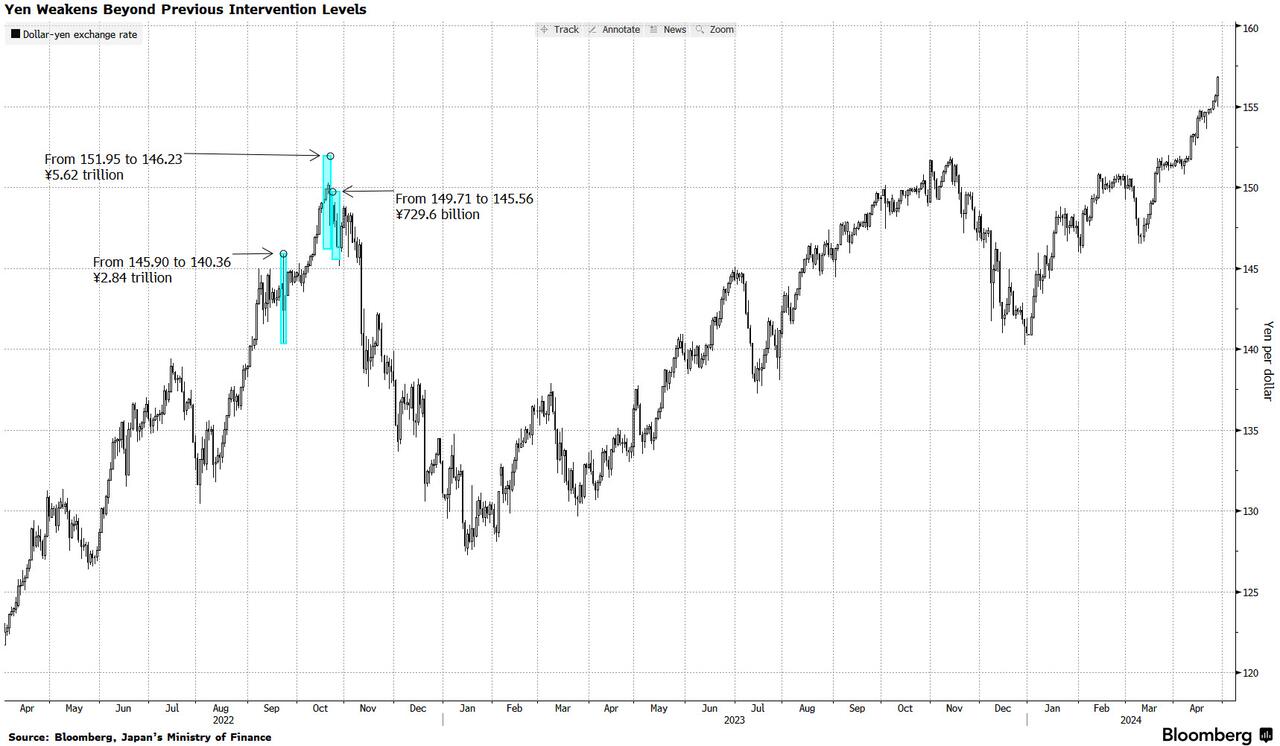

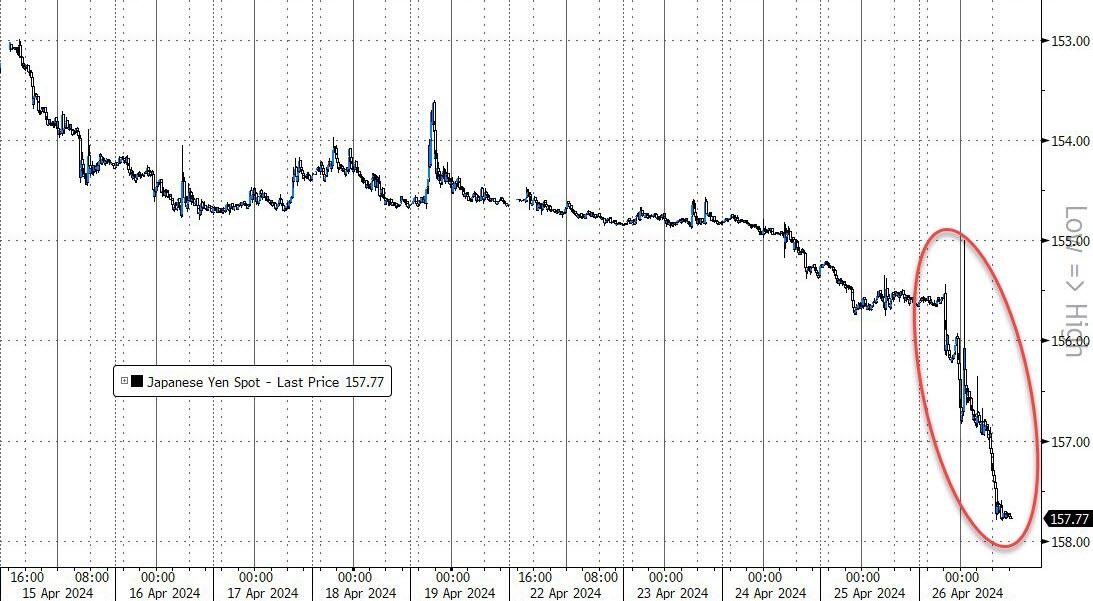

3b Japan 10 YR bond yield: FALL TO. +.883apan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 156.72JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN:UP/ OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

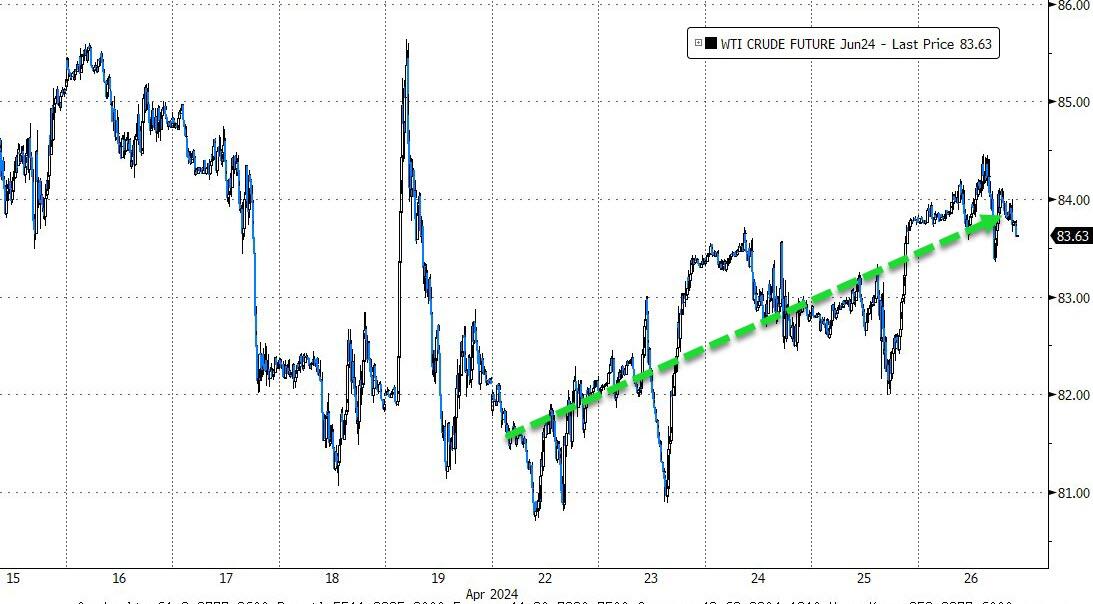

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UPTO +2.5900/Italian 10 Yr bond yield UP to 3..9140SPAIN 10 YR BOND YIELD UP TO 3.379

3i Greek 10 year bond yield DOWNTO 3.489

3j Gold at $2344.60 //Silver at: 27.58 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 13/100 roubles/dollar; ROUBLE AT 91.80/

3m oil into the 84dollar handle for WTI and 89 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 156.72/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.887% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9115as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9781well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

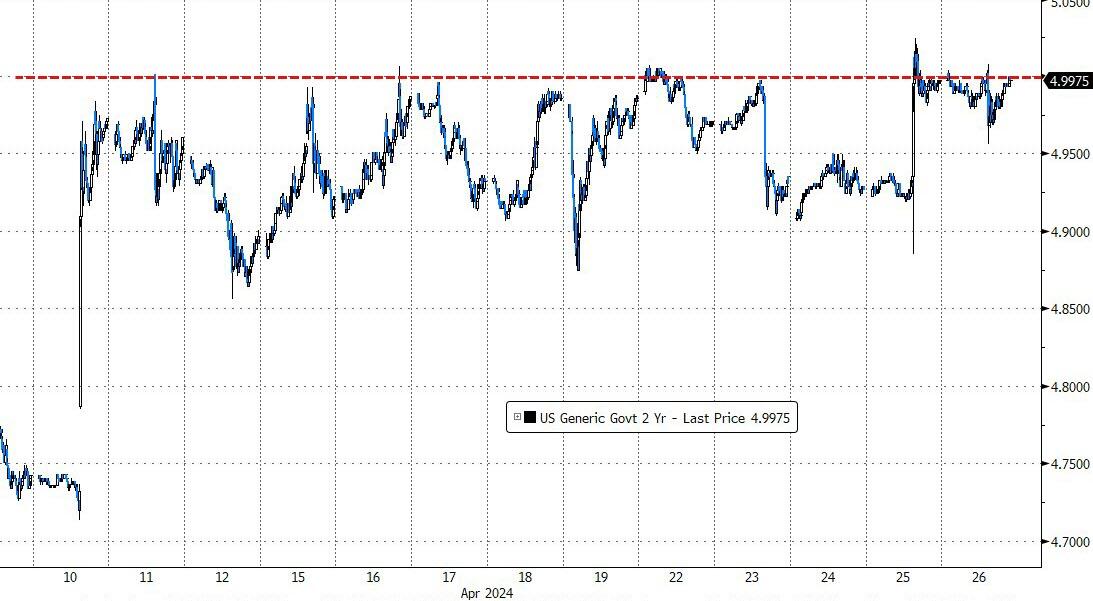

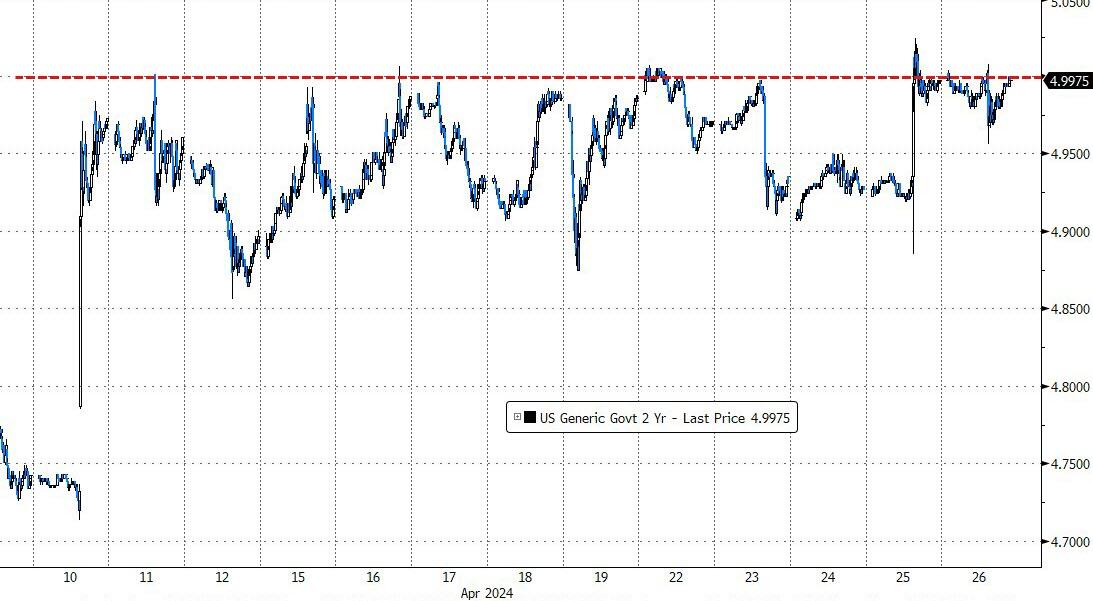

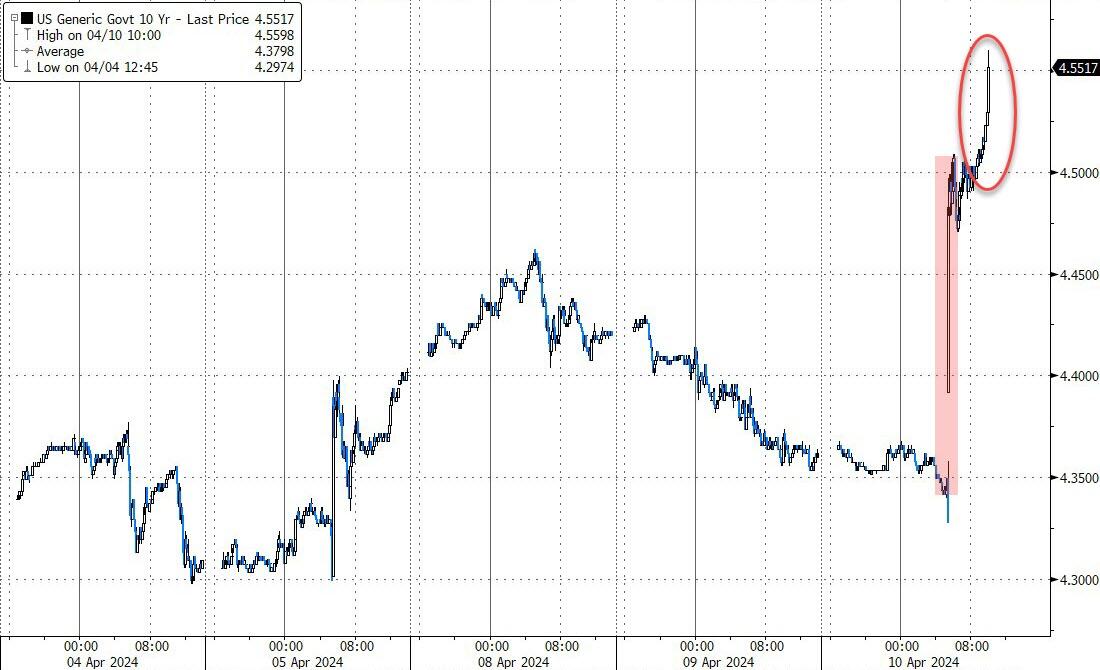

USA 10 YR BOND YIELD: 4.685 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.791 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.993 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.54…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 2 BASIS PTS AT 4.3885

end

2.a Overnight: Newsquawk and Zero hedge

Japan refuses to prop us the yen as it falls to 156.87 to the dollar

(zerohedge)

Futures Jump As Tech Giants Soar, Yen Plummets After BOJ Refuses To Prop Up Crashing Currency

FRIDAY, APR 26, 2024 – 08:18 AM

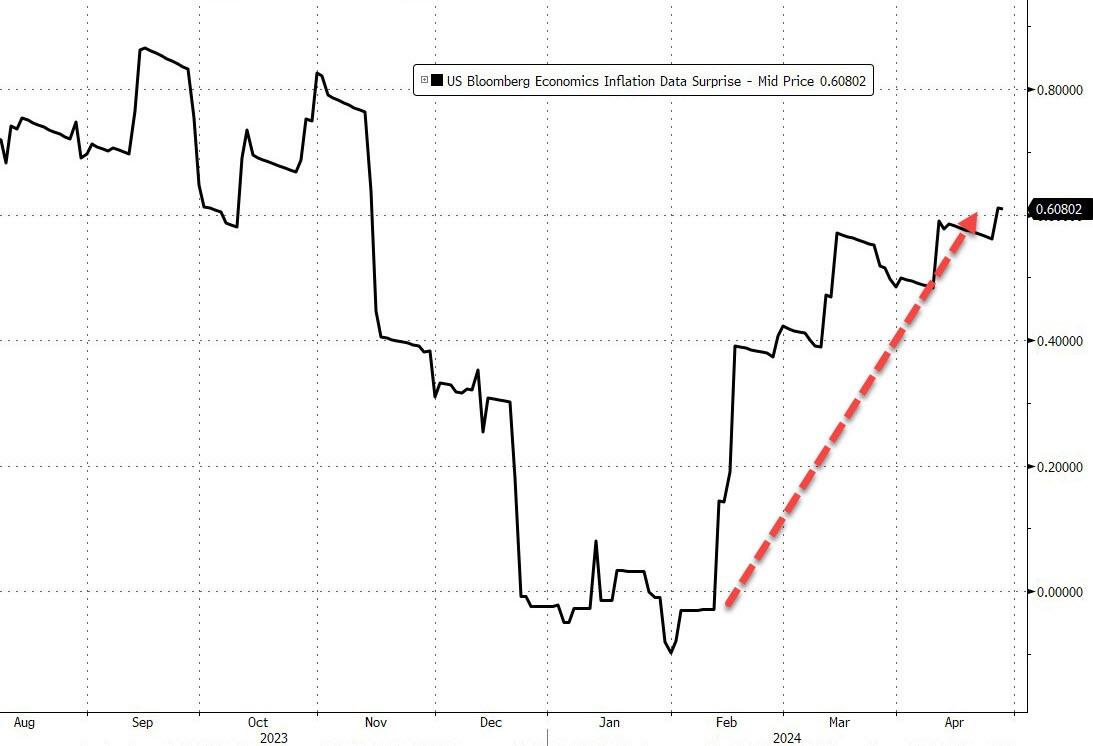

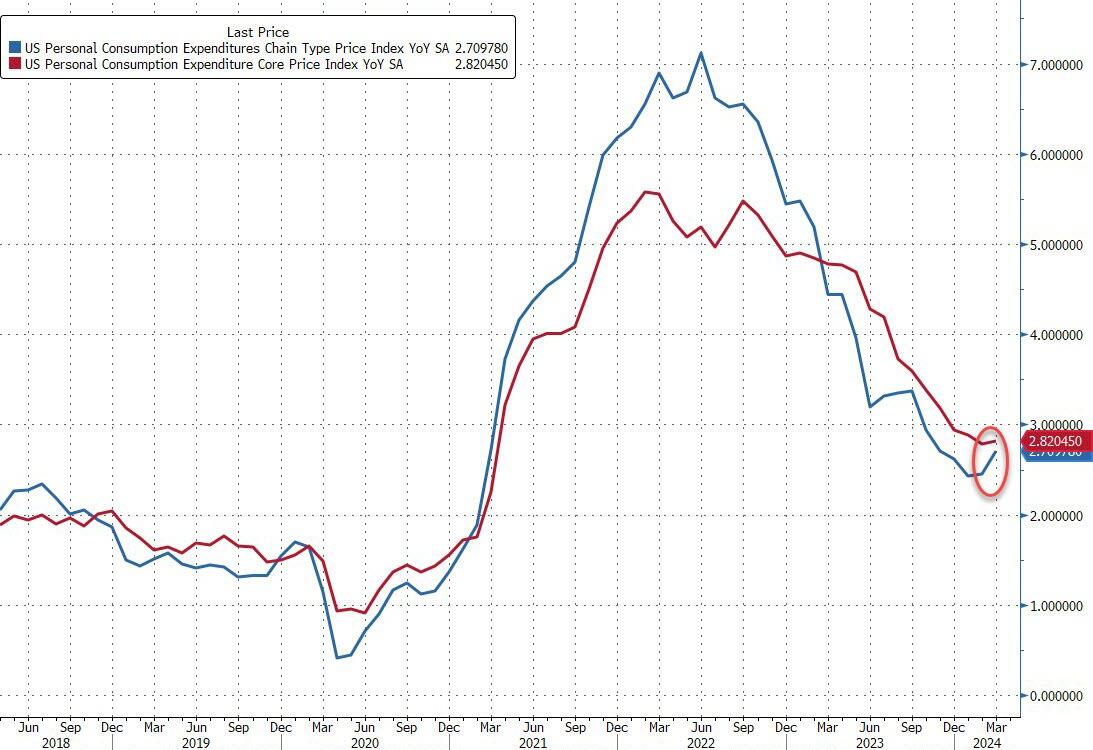

In a rollercoaster 48 hours to close the week, yesterday’s early market slump (after the disappointing Meta guidance) has been fully reversed and stock futures are now pointing sharply higher after blockbuster earnings from Microsoft and Alphabet with attention now turning to the release of US personal consumption data – the Fed’s preferred measure of inflation, where a hotter-than-expected reading after Thursday’s weaker GDP figures may signal US rates will remain higher for longer. As of 7:40am, S&P futures are 0.7% higher while Nasdaq futures gain 1.1%. The positive sentiment carried into European trading, with tech stocks leading equity gains, with miners outperforming as copper hit $10,000 a ton for the first time in two years. Traders are also speculating as to whether Japan will intervene to support the Yen after the currency slid to a 34-year low before rebounding after the central bank kept rates on hold and Ueda said nothing to prop up the currency in what Deutsche Bank has called a policy of “benign neglect.” Later in the day, attention will shift. Elsewhere, the USD is higher and bond yields are slightly lower. In commodities, oil and precious metals are higher; base metals and Ags are mixed. Today, key focus will be the March PCE release at 8.30am ET, where consensus expects headline PCE and core PCE to both rise +0.3% MoM.

In premarket trading, Google parent Alphabet surged as much as 12%, poised to add more than $230 billion to its market capitalization and exceed $2 trillion in valuation. Microsoft rose 4% after the software giant reported third-quarter results that beat expectations, a sign that AI is fueling growth and demand. The companies trounced Wall Street estimates with their latest quarterly results, fueled in part by demand for AI services. In other earnings-related moves, Exxon fell 1.2% after missing EPS but smashing revenue estimates, while Intel slumped more than 7% after providing weaker-than-anticipated guidance. Here are some other notable movers:

- Atlassian shares slide 5.3% after the application software company said co-founder Scott Farquhar is stepping down as co-CEO after 23 years.

- Boyd Gaming shares fall 14% after the regional casino operator reported adjusted earnings per share for the first quarter that missed the average analyst estimate.

- Chinese stocks listed in the US rise, reflecting a rally in Hong Kong as Asian big tech names get a boost following robust earnings from Alphabet and Microsoft. Alibaba +2.0%, Baidu +2.6%, PDD Holdings +2.5%, JD.com +5.0%, NetEase +1.7%, Trip.com +3.1%, KE Holdings +3.3%, Bilibili +5.4%

- Cloud software stocks rise following better-than-expected sales in Microsoft and Google’s cloud divisions. Datadog +4.9%, Snowflake +3.5%, MongoDB +3.8%, Cloudflare +2.3%

- Enphase Energy (ENPH US) shares rise 2.9% as Barclays upgrades its recommendation to overweight from equal-weight, saying the solar-equipment manufacturer is nearing an inflection point.

- Intel shares drop 7.3% after the chipmaker’s second-quarter outlook was weaker than anticipated, underlining the difficulties the company has had in executing a turnaround.

- KLA Corp shares rise TKTK after the semiconductor equipment supplier’s third-quarter earnings beat estimates and outlook for the fourth quarter was strong, prompting analysts to raise their price targets.

- Marathon Digital shares rise 3.3% after the company increases year-end hash rate target to 50 EH/s from 35-37 EH/s.

- Mobileye shares fall 3.0% after a downgrade to underweight at Morgan Stanley in the wake of the company’s results.

- Roku shares fall 4.8% as the streaming-video platform company said it expects adjusted Ebitda to moderate in the second half of the year, after reporting first-quarter results that beat expectations.

- Snap shares surge 24% after the social-media company reported first-quarter results that beat expectations and gave an outlook that is stronger than forecast, helping to ease concerns about its growth.

- T-Mobile shares waver after the carrier’s results received a mixed reception from analysts, who said that the earnings were overall solid, but were disappointed that the company didn’t raise its guidance for postpaid phone subscribers as it looks raise prices.

- Teladoc Health shares drop 4.4% after a second-quarter forecast missed estimates. The healthcare services company also reported a first-quarter gross margin that fell short of expectations.

While earnings remain center stage, the focus Friday will also be on US data, with the Fed’s preferred measure of inflation of particular interest. Treasury yields dipped following yesterday’s bond-market losses when stagflationary GDP data pushed back expectations for policy easing. A gauge of the dollar was steady.

“We have a precarious situation where the earnings of a few big companies are driving sentiment on the entire market,” said Justin Onuekwusi, chief investment officer St James Place Management. “We have seen a bit of volatility driven by earnings as well as rate decreases being priced out and that’s likely to continue.”

Almost 80% of S&P 500 firms that have reported so far have beaten analysts’ earnings estimates, according to JPMorgan strategists. Still, stock price reactions have been underwhelming, with better-than-expected results seeing below average upside, while those missing estimates are being penalized by more than usual, the strategists wrote. More than 50% of S&P 500 companies have yet to report.

A big highliight of the overnight session was the latest collapse in the Japanese yen which fell to a fresh cycle low near 157 versus the dollar after the Bank of Japan stood pat on interest rates and Governor Ueda did little to push back against recent weakness in the press conference. The yen’s slump to a record low versus the dollar has left traders on guard for any hints of intervention from Japan. The yen swung sharply from the day’s low to near its high amid jittery trading in the wake of the Bank of Japan’s decision to keep monetary policy unchanged.

“Should the yen fall further from here, like after the BOJ decision in September 2022, the possibility of intervention will increase,” said Hirofumi Suzuki, chief currency strategist at Sumitomo Mitsui Banking Corp. “It is not the level but it’s the speed that will trigger the action.”

European stocks rose along with US equity futures: the Stoxx 600 is up 0.6%, with technology and construction sectors leading gains, while chemicals and insurance subgroups are the biggest losers. Thyssenkrupp shares jumped after Czech billionaire Daniel Kretinsky’s EP Corporate Group agreed to buy a fifth of the German manufacturer’s troubled steel unit. Miners outperformed as copper hit $10,000 a ton for the first time in two years. Here are the biggest movers Friday:

- Saint-Gobain shares gain as much as 6.3% after the French building-materials producer reported first-quarter sales that were slightly above expectations, according to Oddo. Separately, management is seeing signs of bottoming out for new build markets in Europe

- NatWest rises as much as 5.2% after net interest income and pretax operating profit for the first quarter beat the average analyst estimate

- Amundi soars 7%, most in two years, after the French asset manager reported net inflows for the first quarter that beat the average estimate. Citi analysts expect mid-single digit consensus upgrades. KBW called the results “solid.”

- Electrolux shares gain as much as 7%, the most since December, after first-quarter figures from the Swedish maker of domestic appliances weren’t as bad as feared, with an operating loss of SEK720 million, versus an expected SEK809 million

- Jeronimo Martins soars most in six months after Ebitda margin erosion in 1Q was smaller than analysts expected, showing that Portuguese retailer can withstand competition pressure in Poland as well as negative impact from slowing inflation

- Airbus shares fall as much as 3% to the lowest since early March after its first-quarter results were significantly below estimates, even as the planemaker reiterated its full-year targets

- IMCD’s shares sink as much as 10%, the most since March 2020, after the specialty chemicals and ingredients company reported first-quarter operating Ebita that missed estimates. ING says the story was “underlying quite weak.”

- Hexagon shares fall as much as 4.4% after the software firm reported sales and operating profit that missed estimates, while saying that demand will remain mixed in the near term

- ConvaTec Group shares decline as much as 7.2% after the medical equipment maker was downgraded to reduce by analysts at Peel Hunt, which has growing concerns about its wound care products in the US

- Yara shares fall as much as 6.9%, the lowest intraday since May 2020, after the Norwegian agricultural chemicals firm reported adjusted Ebitda below estimates

Earlier in the session, Asian stocks rose, headed for their best week since November, as investors cheered upbeat earnings from technology firms and sentiment on China continued to improve. Japanese stocks rose as the Bank of Japan left interest rates unchanged. The MSCI Asia Pacific Index rose 0.8%, with TSMC and Tencent among the biggest boosts. The gauge extended its weekly gains to more than 3%. Stocks rose in mainland China and Hong Kong, with the Hang Seng China Enterprises Index poised for its best week since April 2015. Signs of an improving Chinese economy, better corporate earnings and Bejing’s support measures have spurred inflows from global funds.

- Hang Seng and Shanghai Comp. were underpinned by strength in tech and property, while the constructive mood was also facilitated by a meeting between US Secretary of State Blinken and Chinese Foreign Minister Wang where it was stated that the US-China relationship has stabilised although negative factors are building.

- ASX 200 underperformed after the prior day’s losses caught up with the index on return from holiday.

- Nikkei 225 was initially choppy and briefly dipped into negative territory as participants braced for the BoJ policy announcement and whether the central bank flags a reduction in bond buying, but then surged as the central bank kept policy settings unchanged and refrained from any major hawkish surprises.

In FX, the dollar was slightly lower, as all the action was in the Japanese yen which cratered to a fresh 34 year low near 157 versus the dollar after the Bank of Japan stood pat on interest rates and Governor Ueda did little to push back against recent weakness in the press conference. USD/JPY did swing sharply lower to sub-155 before swiftly rebounding in jittery trading amid heightened speculation that authorities may intervene in the market.

In rates, treasuries climbed, paring some of Thursday’s post-data drop. US yields are richer by up to 2bp across long-end of the curve with 5s30s spread around 8bp, tighter by around 1bp on the day; 10-year yields around 4.685%, down 1.5bp on the day with bunds outperforming by 1bp in the sector.

In commodities, oil prices advance, with WTI rising 0.4% to trade near $83.90 a barrel. Spot gold rises 0.7% to around $2,350/oz. Copper hit $10,000 a ton for the first time in two years.

Looking at today’s calendar, the US session highlight is the March personal income/spending (8:30am); we algo get the April revised University of Michigan sentiment (10am) and April Kansas City Fed services activity (11am). Fed members are in self-imposed quiet period ahead of May 1 policy announcement

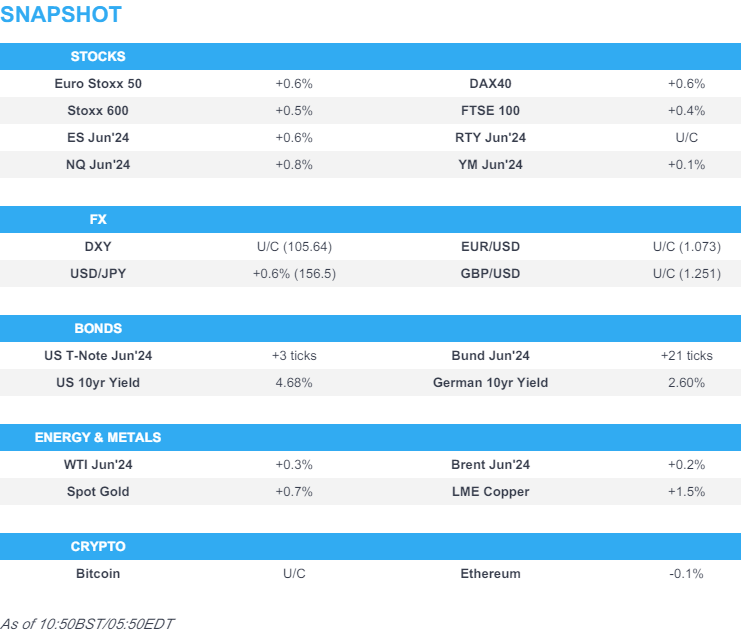

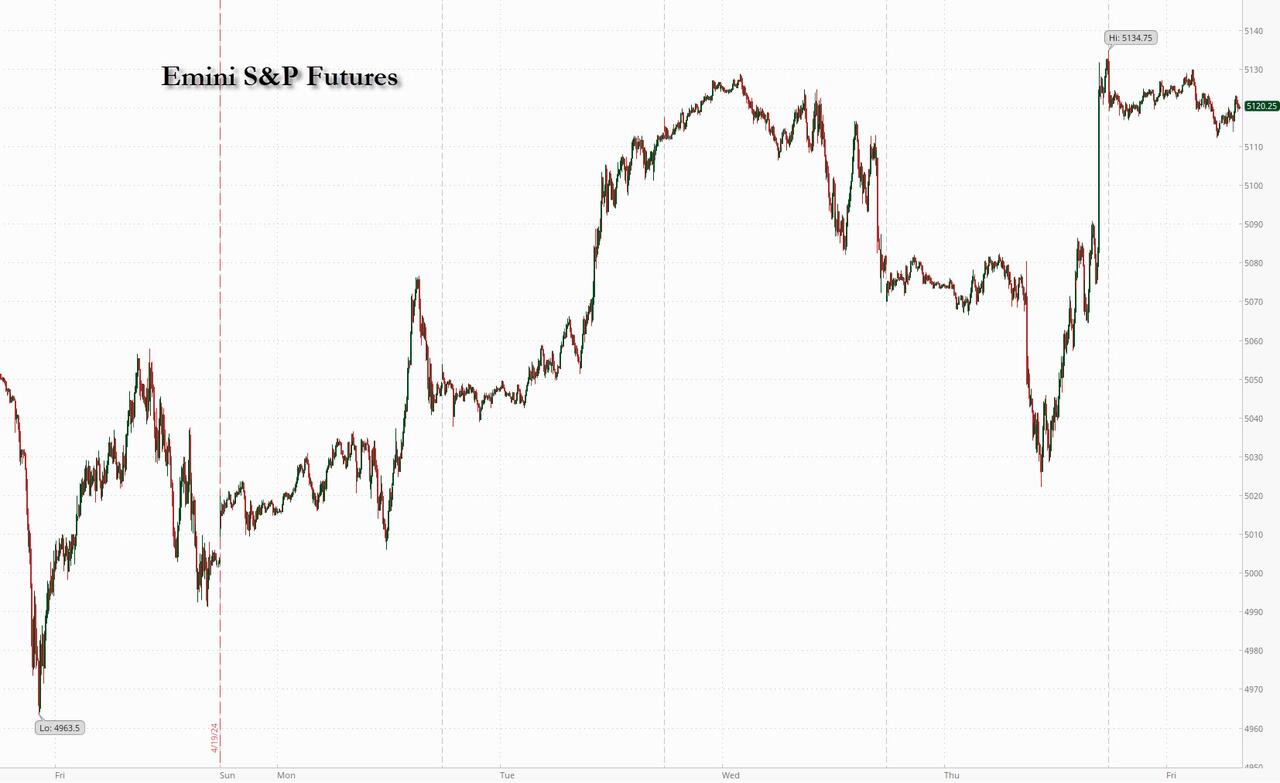

Market Snapshot

- S&P 500 futures up 0.8% to 5,121.00

- STOXX Europe 600 up 0.6% to 505.47

- MXAP up 0.7% to 172.65

- MXAPJ up 0.8% to 536.04

- Nikkei up 0.8% to 37,934.76

- Topix up 0.9% to 2,686.48

- Hang Seng Index up 2.1% to 17,651.15

- Shanghai Composite up 1.2% to 3,088.64

- Sensex down 0.7% to 73,833.99

- Australia S&P/ASX 200 down 1.4% to 7,575.91

- Kospi up 1.1% to 2,656.33

- German 10Y yield little changed at 2.60%

- Euro up 0.2% to $1.0748

- Brent Futures up 0.2% to $89.21/bbl

- Brent Futures up 0.2% to $89.21/bbl

- Gold spot up 0.6% to $2,347.56

- US Dollar Index down 0.10% to 105.49

Top Overnight News

- BOJ leaves rates unchanged, as expected, and retained its guidance from Mar about purchasing gov’t bonds (there had been some speculation of a taper or a hint of one). WSJ

- Japan’s Tokyo CPI for April cools far more than anticipated, coming in +1.8% ex-food/energy vs. the Street +2.7% and down from +2.9% in March. BBG

- China’s foreign minister says the relationship w/the US was starting to stabilize but that “negative factors” were increasing. NBC News

- Eurozone inflation expectations over the next 12 months ticked down to 3% (from 3.1%), hitting the lowest level since Dec 2021. ECB

- The ECB is likely to need extra interest rate cuts if global borrowing costs are pushed up by the US Federal Reserve maintaining its restrictive monetary policy stance, a top eurozone policymaker has said. Fabio Panetta, head of Italy’s central bank, said that if the Fed keeps rates on hold longer than markets expect, or even raises them, it would be “likely to reinforce the case for a rate cut [by the ECB] rather than weakening it”. FT

- Donald Trump’s allies are quietly drafting proposals that would attempt to erode the Federal Reserve’s independence if the former president wins a second term, in the midst of a deepening divide among his advisers over how aggressively to challenge the central bank’s authority. WSJ

- Walmart’s CEO says inflation continues to cool: “At Walmart, we are now seeing prices that are in line with where they were 12 months ago. I haven’t been able to say that for a few years now. The last few weeks, we’ve taken even more prices down in areas like produce and meat and fresh food”. ABC News

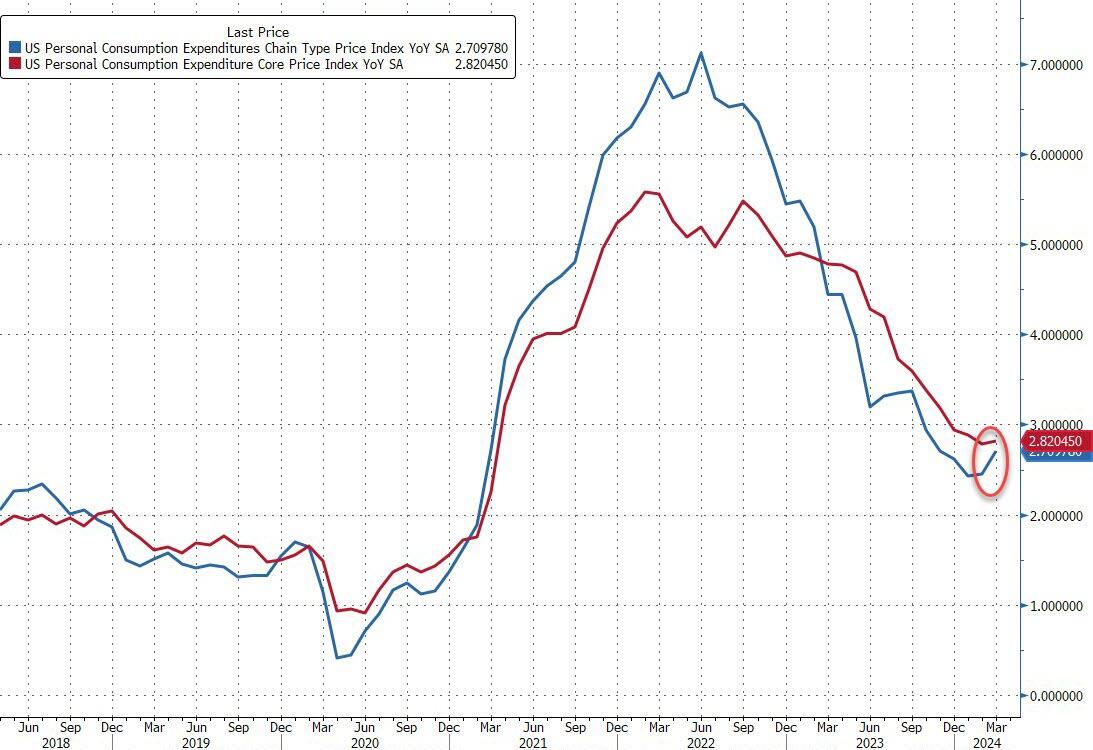

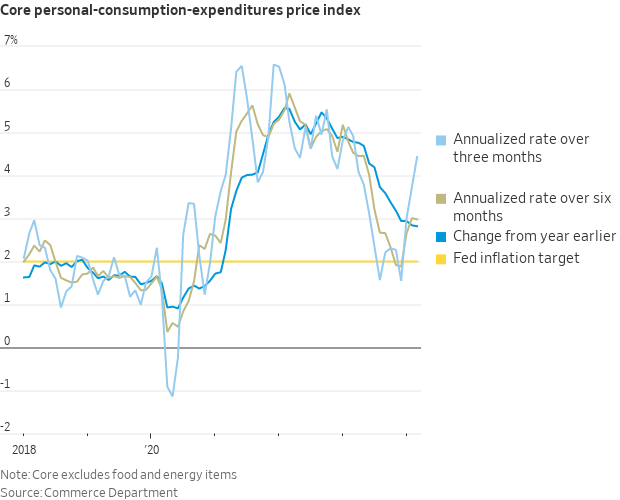

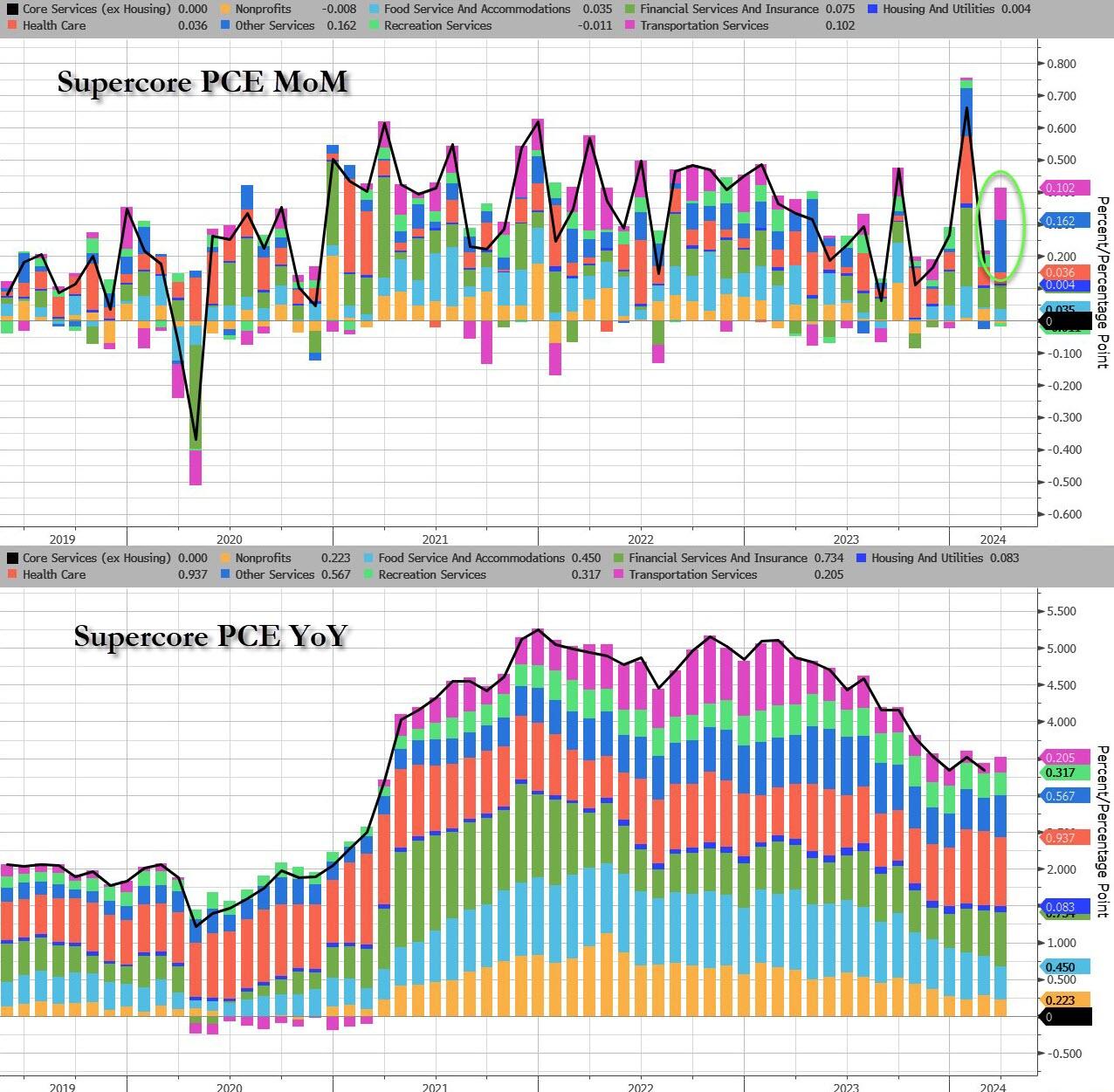

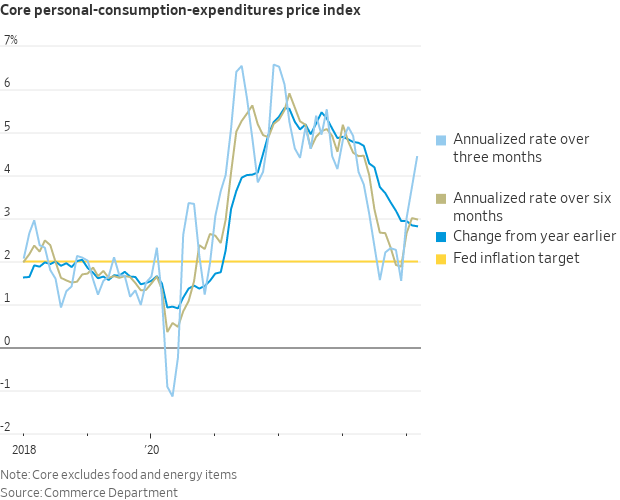

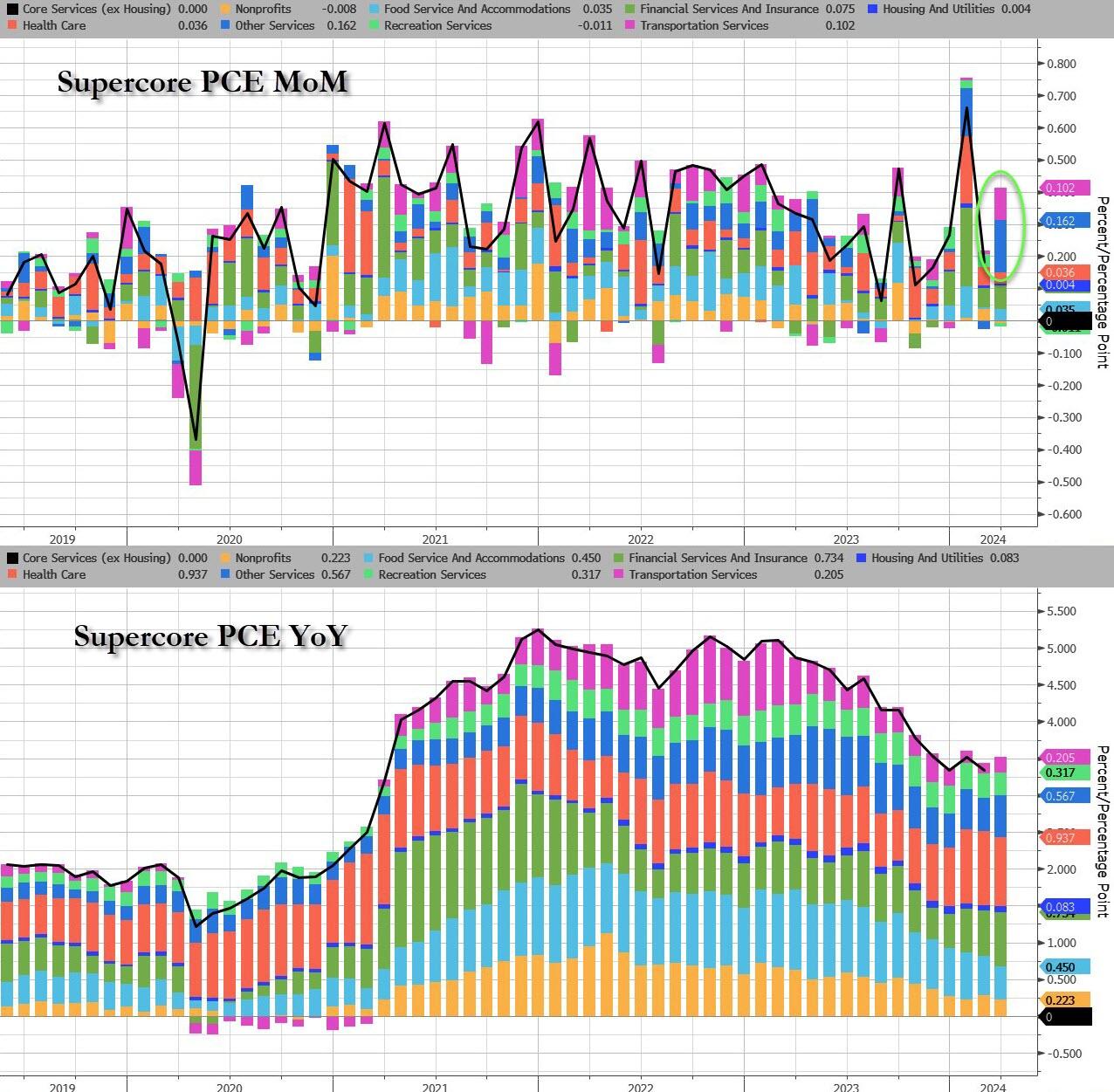

- Annualized US core PCE inflation accelerated to 4.5% over the last three months, but underlying trends are less alarming. The Q1 acceleration mostly reflected one-off surprises in acyclical categories where costs pass-through with long lags, and forward-looking indicators are at target-consistent levels. Progress therefore appears delayed but not reversed, and we forecast that core PCE inflation will slow to 2.2% on a sequential annualized basis in 2024Q2-Q4. GIR

- Microsoft and Alphabet jumped premarket after stellar earnings and expectations for a surge in cloud revenue fueled by AI demand. Execs at both companies said they plan to spend more on AI. BBG

Earnings

- Alphabet Inc (GOOGL) Q1 2024 (USD): EPS 1.89 (exp. 1.51), Revenue 80.54bln (exp. 78.59bln); board authorised Co. to repurchase up to an additional 70bln and declared a cash dividend of 0.20/shr. Shares +11.5% in pre-market trade

- Microsoft Corp (MSFT) Q3 2024 (USD): EPS 2.94 (exp. 2.82), Revenue 61.86bln (exp. 60.8bln). Shares +4.1% in pre-market trade

- Intel Corp (INTC) Q1 2024 (USD): Adj. EPS 0.18 (exp. 0.14), Revenue 12.70bln (exp. 12.78bln). Shares -7.5% in pre-market trade

- Snap Inc (SNAP) Q1 2024 (USD): Adj. EPS 0.03 (exp. -0.05), Revenue 1.19bln (exp. 1.12bln). Shares +23.5% in pre-market trade

- TotalEnergies (TTE FP) Q1 (USD): Adj. Net 5.11bln (exp. 5bln). Adj. EBITDA 11.5bln (exp. 11.1bln). Plans a USD 2bln share buyback Q2; Cash flow from operating activities 2.2bln (prev. 5.1bln Y/Y); Dividend +7% Y/Y

- Airbus (AIR FP) Q1 24 (USD): Adj. EBIT 600mln (exp. 789mln), Revenue 12.80bln (exp. 12.87bln), Gross Orders 170 (prev. 156), Net Orders 170 (prev. 142), Deliveries 142. Reaffirms 2024 guidance.

A recap of overnight news courtesy of Newsquawk

APAC stocks were mostly higher as the region digested recent market themes including disappointing US data, strong big tech earnings and the BoJ policy announcement. ASX 200 underperformed after the prior day’s losses caught up with the index on return from holiday. Nikkei 225 was initially choppy and briefly dipped into negative territory as participants braced for the BoJ policy announcement and whether the central bank flags a reduction in bond buying, but then surged as the central bank kept policy settings unchanged and refrained from any major hawkish surprises. Hang Seng and Shanghai Comp. were underpinned by strength in tech and property, while the constructive mood was also facilitated by a meeting between US Secretary of State Blinken and Chinese Foreign Minister Wang where it was stated that the US-China relationship has stabilised although negative factors are building.

Top Asian News

- Chinese Foreign Minister Wang said in a meeting with US Secretary of State Blinken that the China-US relationship has stabilised but negative factors are building, while he added that sliding into conflict with the US would be a lose-lose situation that they ask the US not to interfere with China’s internal affairs. Furthermore, Blinken said there is no substitute for face-to-face diplomacy and they need to avoid miscalculations, while he hopes the US and China can make progress on agreements, citing fentanyl, military-to-military ties and AI risks.

- US is pushing allies in Europe and Asia to tighten restrictions on exports of chip-related technology and tools to China amid rising concerns about Huawei’s development of advanced semiconductors, according to FT sources. US wants Japan, South Korea, and the Netherlands to use existing export controls more aggressively, including stopping engineers from their countries servicing chipmaking tools at fabs in China.

- ByteDance reportedly prefers shutting down the app rather than a sale if it exhausts all legal options and the algorithms TikTok relies on are deemed core to ByteDance’s overall operations, making the sale of the app unlikely, according to Reuters sources.

European bourses, Stoxx 600 (+0.5%) are entirely in the green, though trade has been contained at session highs, as participants await March’s US PCE at 13:30 BST. European sectors are almost entirely in the green, with the exception of Chemicals, following poor IMCD (-9.1%) results. Tech tops the pile, with optimism lifted following strong large-cap Tech earnings in the US. US Equity Futures (ES +0.7%, NQ +0.9%, RTY +0.1%) are entirely in the green, with the NQ outperforming, benefitting from significant pre-market strength in both Google (+11.1%) and Microsoft (+3.6%), after reporting strong earnings after-market.

Top European News

- ECB’s Panetta said they must weigh the risk of monetary policy becoming too tight, while he added that timely and small rate cuts would counter weak demand and could be paused. Furthermore, he stated that hesitations in adjusting rates would hurt investment and productivity, while large rate cuts could create a credibility issue.

- ECB Consumer Inflation Expectations survey (Mar) – 12-months ahead 3.0% (prev. 3.1%); 3-year ahead 2.5% (prev. 2.5%). Economic growth expectations for the next 12 months 1.1% (prev. -1.1%)

- SNB Chair Jordan said SNB has been successful in fight against inflation; uncertainty remains elevated and shocks can occur at and time

BOJ

- BoJ kept its policy settings unchanged with the short-term interest rate target at 0.0%-0.1%, as expected, with the decision made unanimously, while it dropped the reference from the statement that it currently buys about JPY 6tln worth of JGBs per month but stated that it will conduct JGB, commercial paper and corporate bond buying in line with the decision in March. BoJ said it must be vigilant to FX and market moves and their impact on the economy and prices but noted no excessive behaviour is seen in Japan’s asset market and financial institutions’ practices. Furthermore, it stated that if trend inflation rises, the BoJ will likely adjust the degree of monetary easing but also added to expect accommodative monetary conditions to continue for the time being. In terms of the latest Outlook Report, Board Members’ Real GDP median forecast for Fiscal 2024 was cut to 0.8% from 1.2% but the Fiscal 2025 median forecast was maintained at 1.0%, while the Core CPI Fiscal 2024 median forecast was raised to 2.8% from 2.4% and Fiscal 2025 median forecast was raised to 1.9% from 1.8%.

- PRESS CONFERENCE: BoJ Governor Ueda said easy financial conditions will be maintained for the time being; Weak JPY so far is not having a big impact on trend inflation. Difficult to gauge timing of future rate hikes. Weak JPY so far is not having a big impact on trend inflation. Reduction in JGB buying in the future is in sight. Will not comment on FX moves

FX

- USD is around flat, and holding within a 105.40-71 range. USD was initially being propped up by JPY softness post-BoJ, although that has abated somewhat, amid Yen intervention speculation.

- JPY is the clear laggard across the majors following the BoJ policy announcement overnight, which provided no hawkish surprise. USD/JPY took another leg higher amid BoJ Ueda’s press conference, before being slapped down to sub-155 levels, a few hours later. Some will likely view the move as intervention but we are yet to see any official confirmation of this.

- EUR is flat vs. the USD and breached yesterday’s 1.0740 best. If the pair ventures higher, 1.0756 from April 11th is the next potential target.

- Antipodeans are firmer vs. the USD and outmuscling peers alongside the favourable risk environment. AUD/USD has gained a firmer footing above its 200 and 50DMAs at 0.6526 and 0.6532 respectively with focus now on a potential approach of 0.66

- PBoC set USD/CNY mid-point at 7.1056 vs exp. 7.2449 (prev. 7.1058).

Fixed Income

- USTs are a touch firmer after yesterday’s data induced losses, which sent the Jun’24 UST to a contract low of 107.04. Today’s trade has been contained within a 107.04-108.01 range, with all eyes on March’s US PCE metrics later.

- Bund price action has been following USTs and attempting to recoup recently lost ground which has been inspired this week by a combination of better data and speak from hawkish ECB members. Bunds are so far respecting yesterday’s 129.53-130.38 range.

- Gilts are firmer and in-fitting with global peers in an attempt to claw back recent losses. However, with a lack of UK-specific drivers, UK paper will likely remain at the whim of global peers.

Commodities

- A relatively tame session thus far for the crude complex following Thursday’s choppy trade, as participants await monthly US PCE metrics; Brent Jun’24 range between 89.08-69/bbl.

- Precious metals are firmer amid the softer Dollar and ahead of the US PCE data, with spot silver narrowly leading vs spot gold. XAU topped yesterday’s peak (USD 2,344.93/oz) to trade in a current intraday range between USD 2,326.36-2,352.30/oz.

- Base metals are stronger across the board amid bullish momentum after copper crossed key levels, with the broader complex underpinned by the softer Dollar and broader risk appetite; 3M LME copper is posting gains of over USD 100/t at the time of writing after mounting the key USD 10,000/t mark to levels last seen in 2022.

- India Oil Minister said cartel of oil producers are responsible for current volatility in the market; oil producers are cutting down and holding back production, according to ETNow.

Geopolitics: Middle East

- “US Secretary of State Blinken to visit Israel on Tuesday”, according to Sky News Arabia

- Hezbollah said it shelled an Israeli force with artillery at the site of Al-Malikiyah and achieved a direct hit, according to Al Jazeera.

Geopolitics: Other

- US official said the US could announce as soon as Friday USD 6bln in new weapon purchases for Ukraine.

- North Korean leader Kim supervised the test-firing of multiple launch rockets, according to KCNA.

- China’s Defence Ministry said Chinese and French militaries established a dialogue mechanism for cooperation between theatre commands, according to Reuters.

US Event Calendar

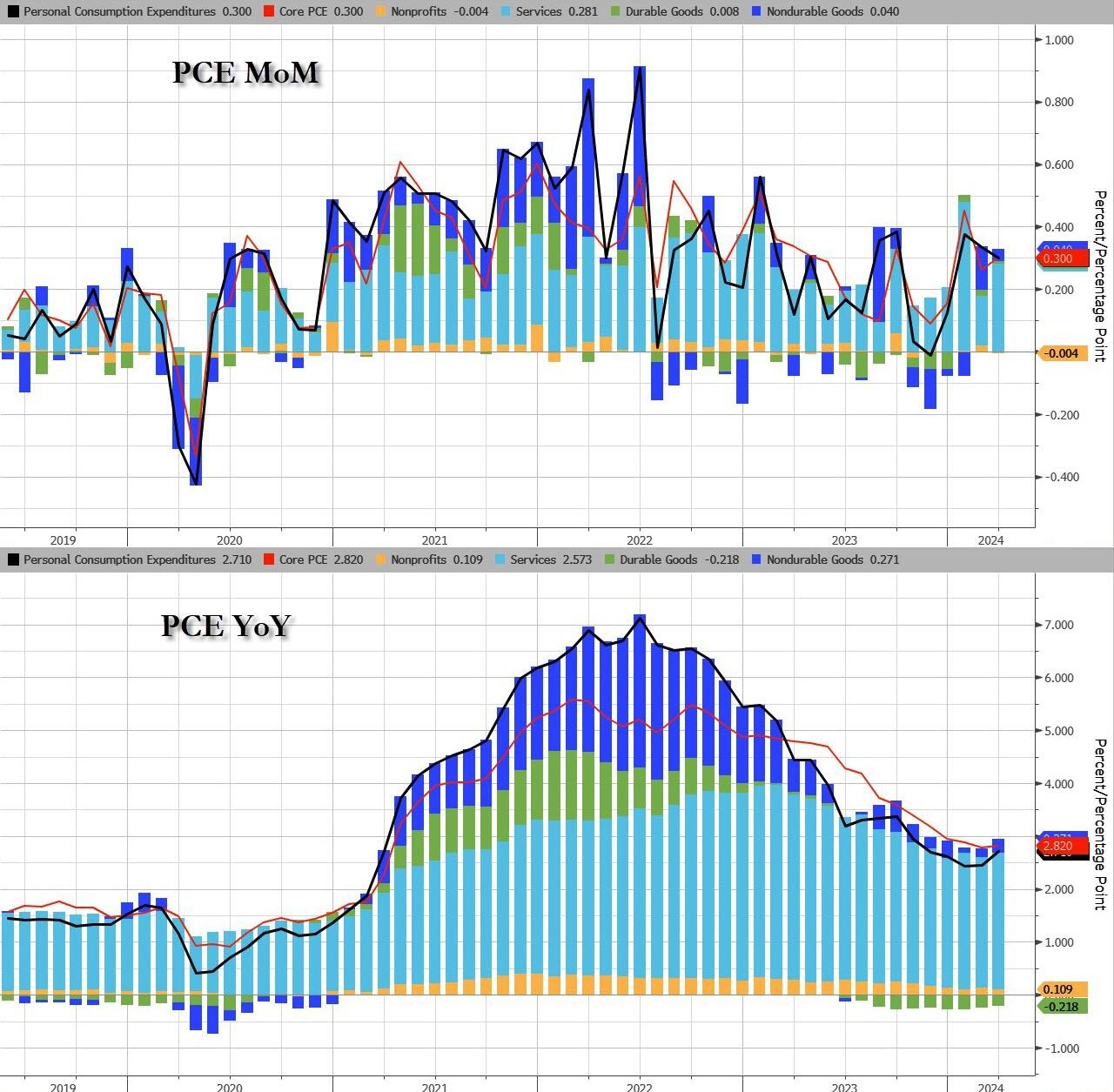

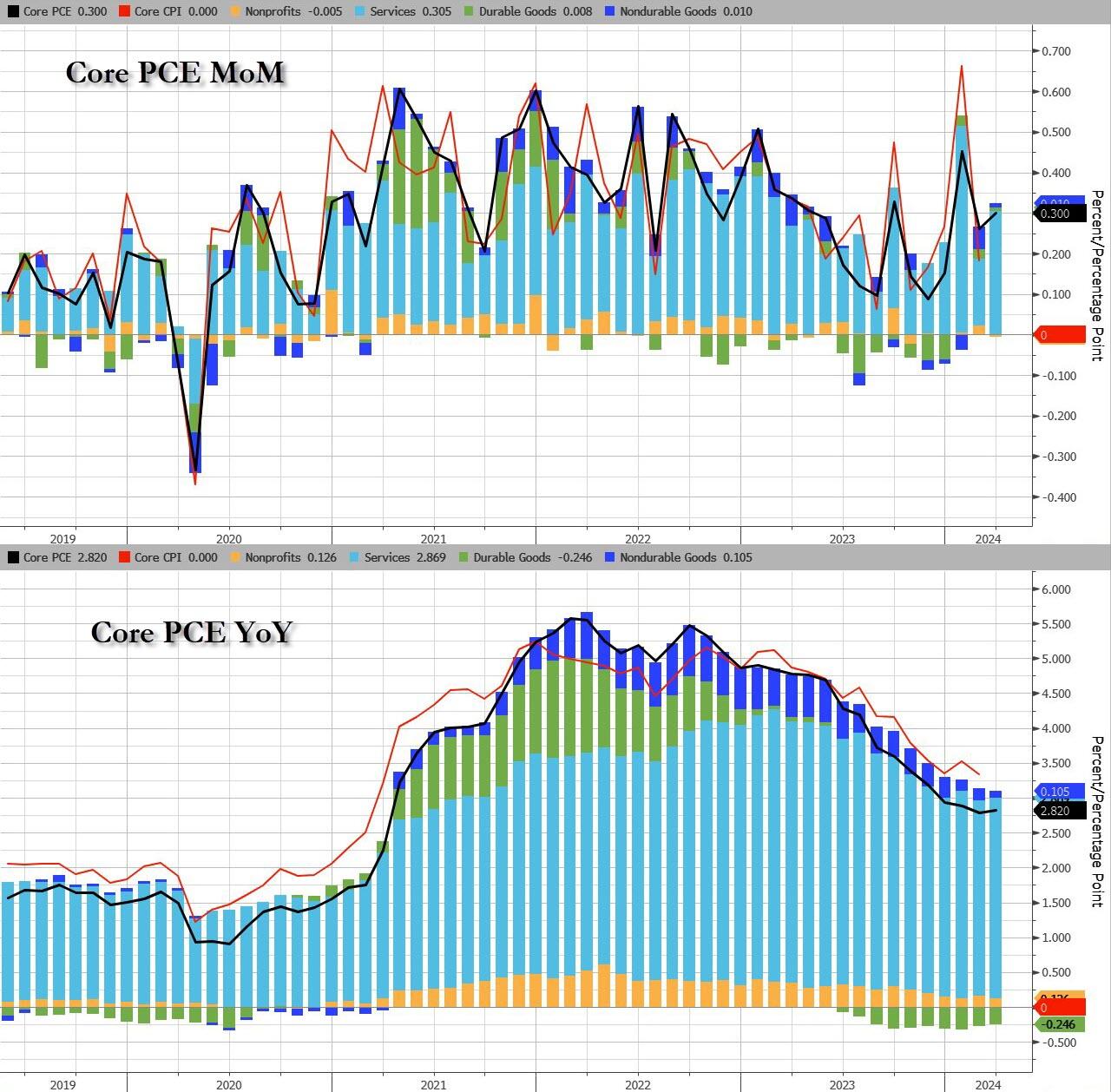

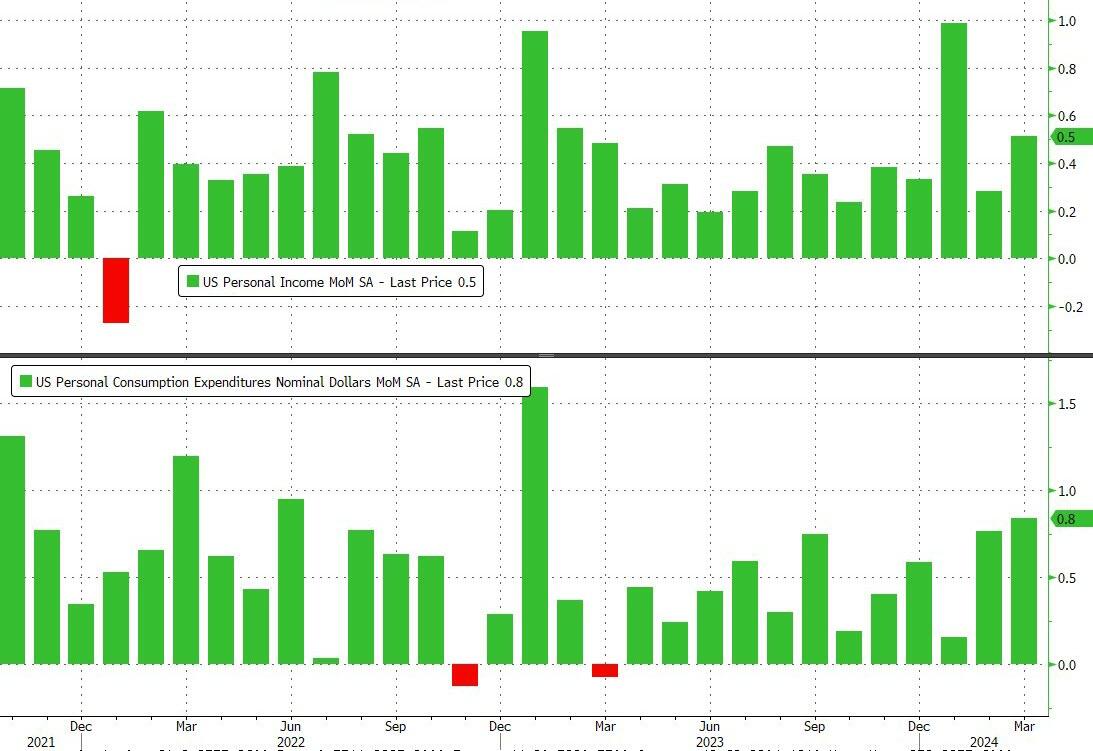

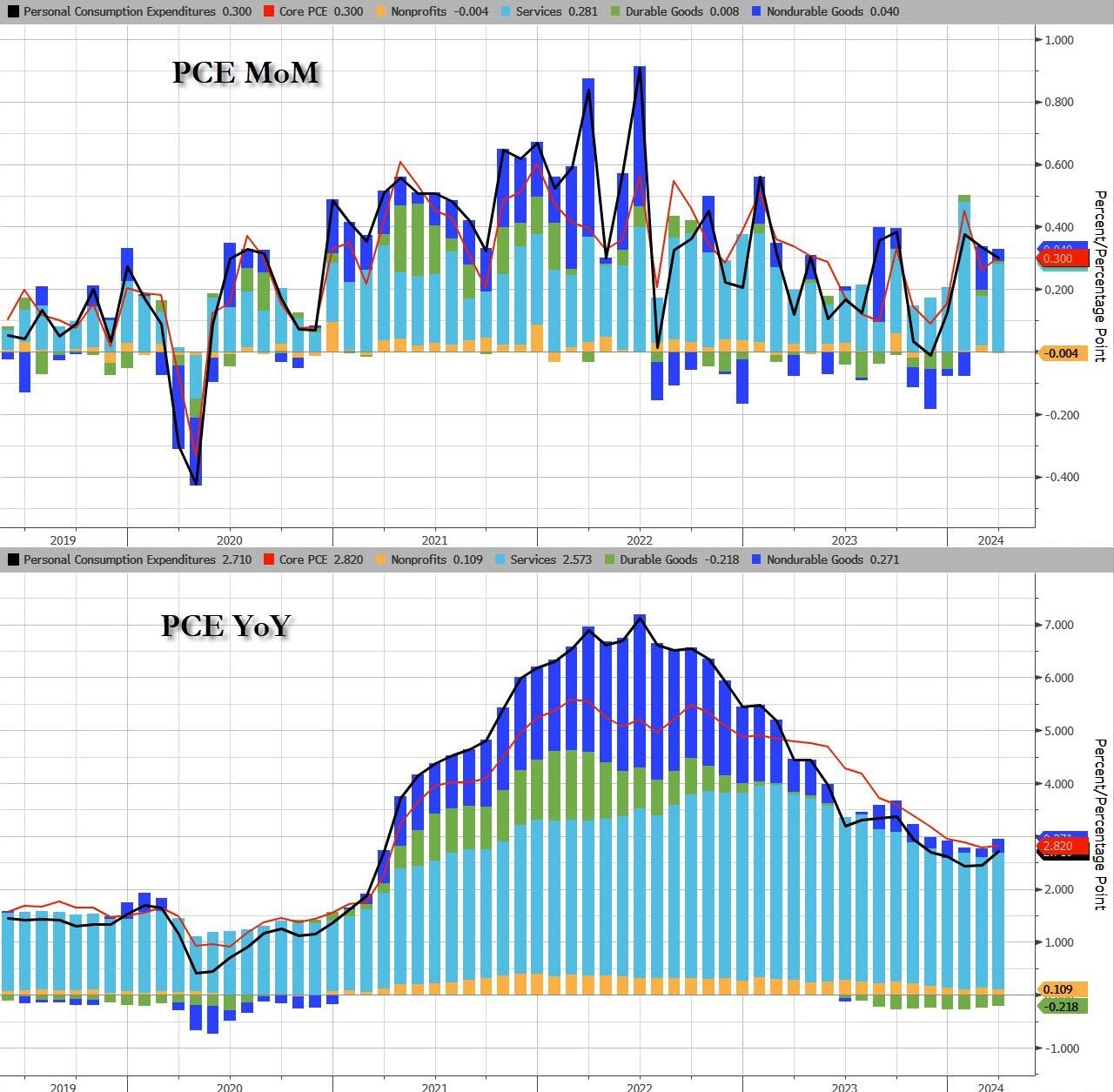

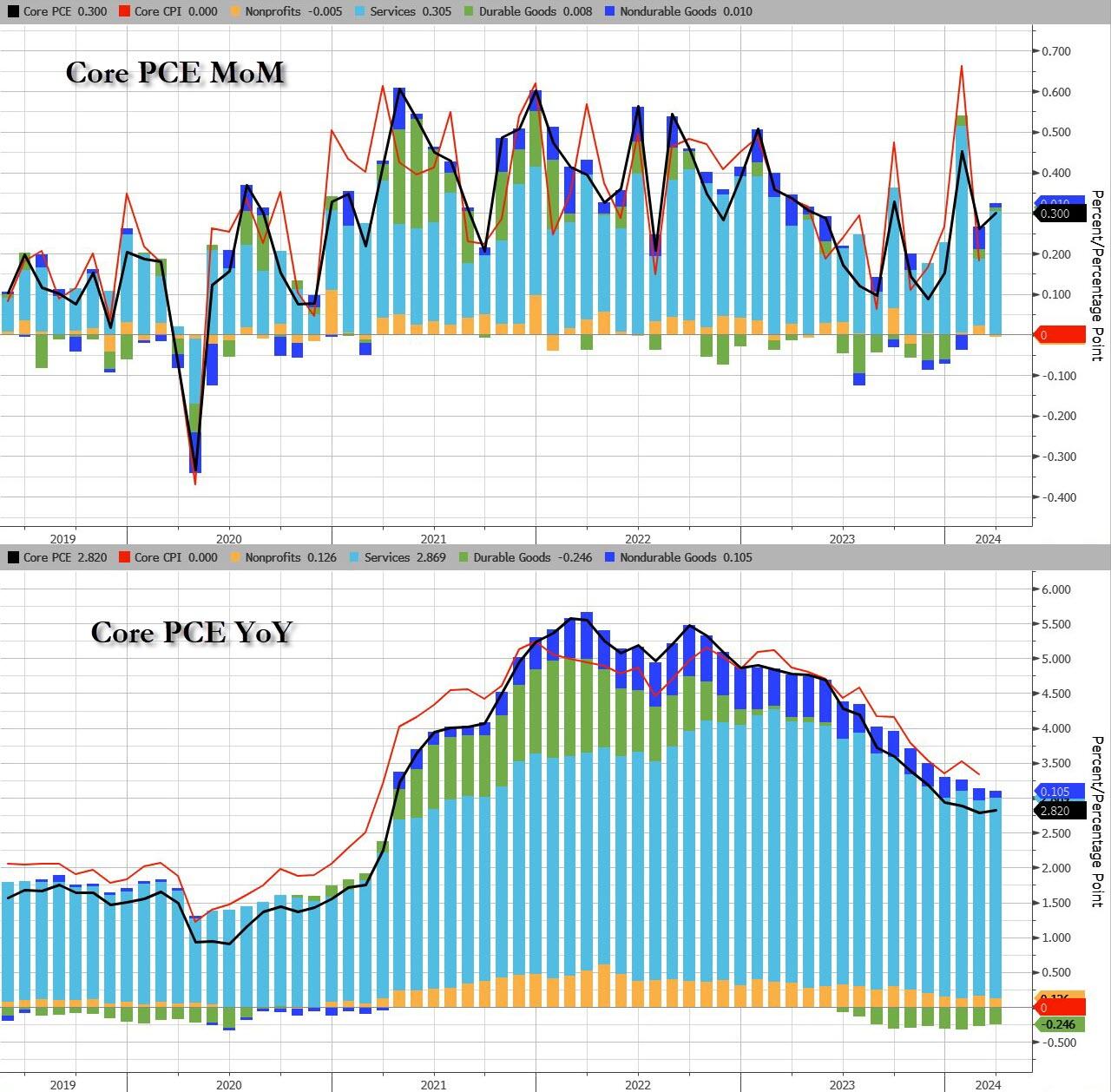

- 08:30: March PCE Deflator MoM, est. 0.3%, prior 0.3%

- March PCE Core Deflator MoM, est. 0.3%, prior 0.3%

- March PCE Deflator YoY, est. 2.6%, prior 2.5%

- March PCE Core Deflator YoY, est. 2.7%, prior 2.8%

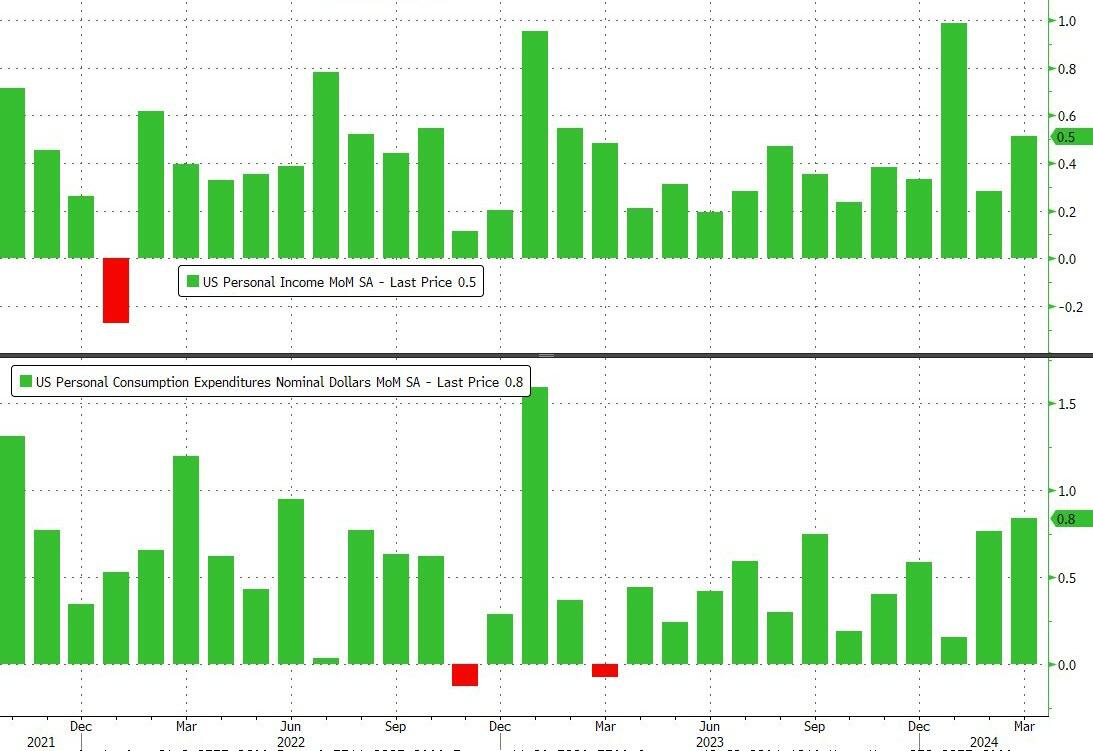

- 08:30: March Personal Income, est. 0.5%, prior 0.3%

- March Personal Spending, est. 0.6%, prior 0.8%

- March Real Personal Spending, est. 0.3%, prior 0.4%

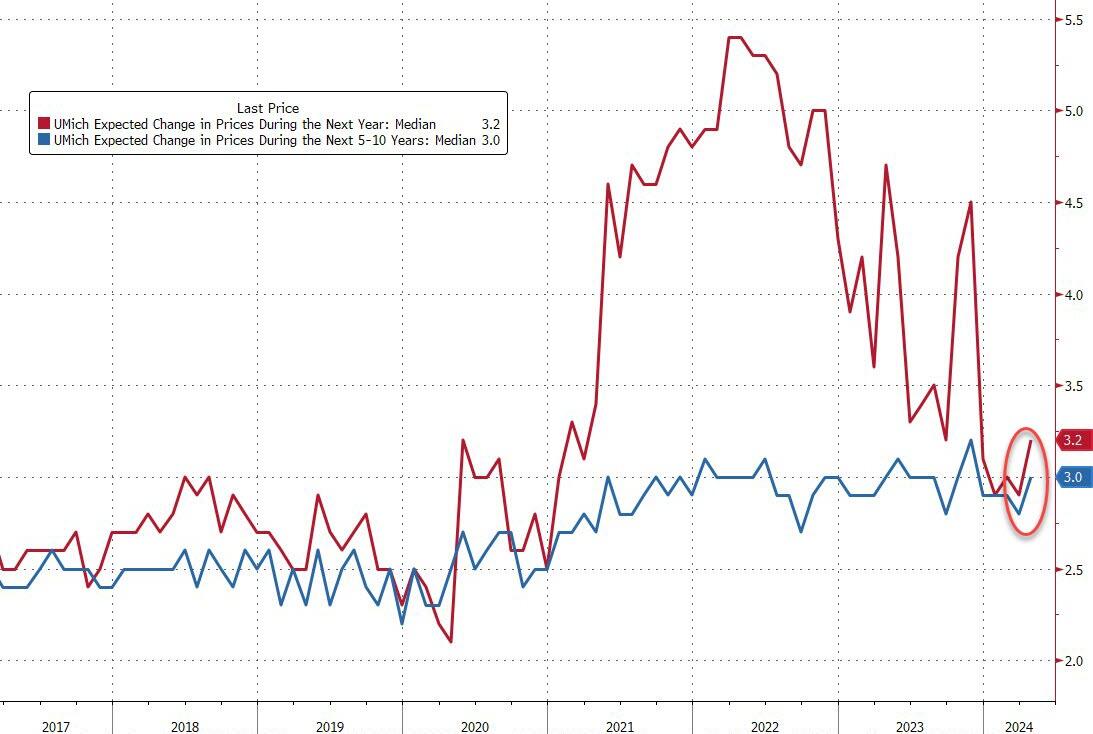

- 10:00: April U. of Mich. Sentiment, est. 77.9, prior 77.9

- April U. of Mich. Current Conditions, prior 79.3

- April U. of Mich. Expectations, prior 77.0

- April U. of Mich. 1 Yr Inflation, prior 3.1%

- April U. of Mich. 5-10 Yr Inflation, est. 3.0%, prior 3.0%

- 11:00: April Kansas City Fed Services Activ, prior 7

DB’s Jim Reid concludes the overnight wrap

It’s been a volatile 24 hours in markets, but in spite of a selloff yesterday, there’s increasing positivity this morning thanks to strong results from Microsoft and Alphabet after last night’s close. Both companies exceeded revenue and earnings expectations, with Alphabet seeing the larger beat on profitability, as their growth was boosted by demand for cloud computing and AI-related offerings. That’s seen Alphabet rise by over 11% in after-hours trading, while Microsoft is up more than -4%, having both been down in the main session yesterday. In turn, futures on the S&P 500 are currently up +0.81%, which is a significant turnaround from yesterday, as the index closed -0.46% lower, and that was only after recovering from initial losses that had pushed it down -1.60%.

That positivity has continued into Asian markets overnight, which comes as the Bank of Japan left their interest rates unchanged at their latest meeting. That’s seen the Japanese Yen weaken further, and it’s currently trading at 156.11 per dollar, which is its weakest level since 1990. Front-end government bond yields have also fallen overnight in Japan, with the 2yr yield down -0.7bps to 0.29%. And for equities, all the major indices have risen, including the Nikkei (+0.74%), the KOSPI (+1.10%), the Hang Seng (+1.98%), the CSI 300 (+1.03%) and the Shanghai Comp (+0.79%).

Before that overnight reversal, markets had struggled yesterday, as challenging data and poor earnings led to a notable selloff. That meant investors pushed back the timing of rate cuts yet again, and the 2yr Treasury yield (+7.1bps) closed at 4.998%, so almost at 5% for the first time since mid-November. That was mainly driven by the Q1 US GDP release, which had the unfortunate combination of a downside surprise on growth, and an upside surprise on inflation. As we found out in 2022, that stagflationary mix can potentially be a bad recipe for markets, so it wasn’t a surprise to see equities and bonds lose ground simultaneously even if equities have since been busy making up their initial losses.

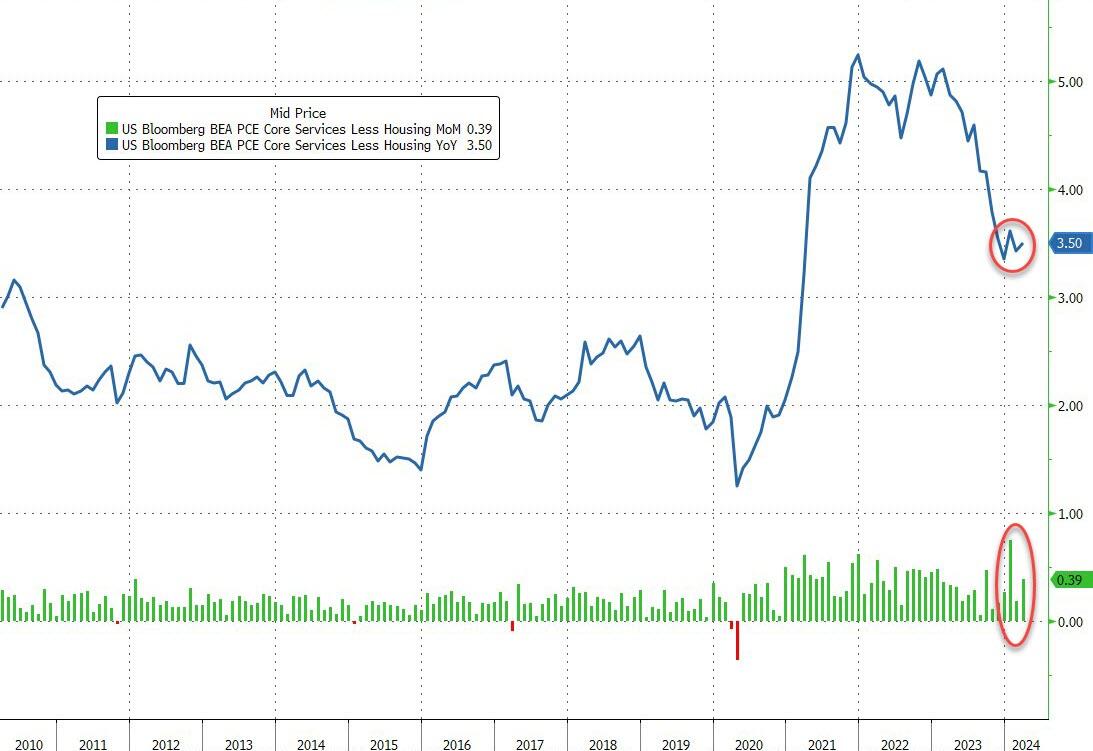

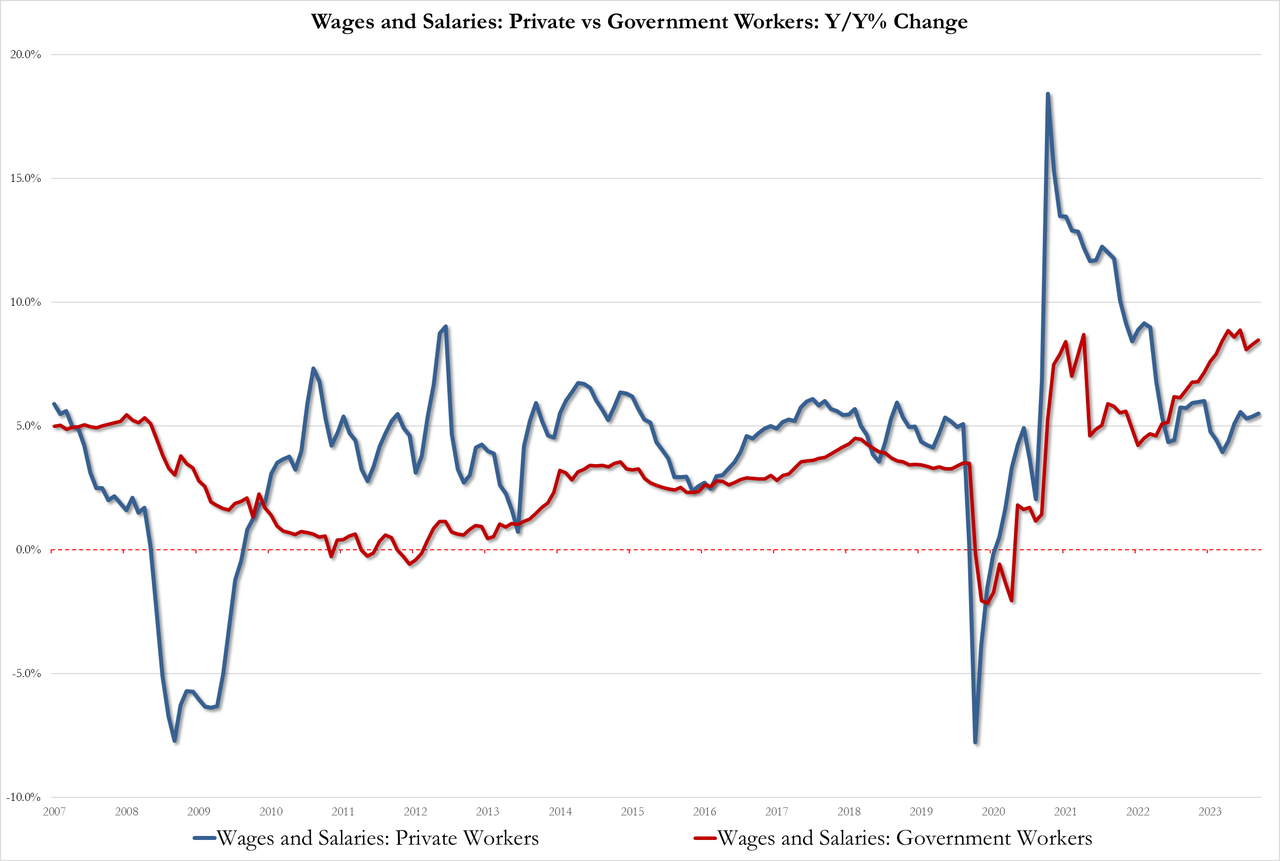

In terms of the details, growth came in at an annualised rate of +1.6% (vs. +2.5% expected), which is the slowest growth since Q2 2022. But more alarmingly for markets, core PCE surprised on the upside, with an annualised rate of +3.7% in Q1 (vs. +3.4% expected). Headline PCE was also strong, at +3.4% in Q1, and core services ex housing (a measure Fed Chair Powell has cited in the past) was at +5.1%. So whichever way you crunch the numbers, this clearly isn’t the sort of inflation momentum where the Fed could be comfortable cutting rates. We’ll get the monthly US PCE numbers for March today within the spending report as well. If you’re looking for positives on growth, final private domestic sales came in at 3.1%, with the slowing in headline GDP growth coming from net exports, inventories and government spending. So domestic demand still holding up well. However you could argue that just ties in with the strong inflation component.

Unsurprisingly, that release meant markets dialled back the odds of rate cuts anytime soon. For instance, the chance of a rate cut by the July meeting fell from 50% the previous day to 34% afterwards. And for the year as a whole, futures are now pricing in just 34bps of cuts by the December meeting, down from 43bps the previous day and 67bps at the start of the month. So futures are now pricing the most hawkish profile we’ve seen to date in this hiking cycle, at least in terms of where rates are set to be by the end of 2024. Indeed for the first time, the first 25bp cut isn’t fully priced in until the December 2024 meeting.

With investors pricing out rate cuts, US Treasuries slumped and yields hit their highest levels of 2024 so far. In particular, the 2yr Treasury yield (+7.1bps) saw a closing value of 4.998%, having reached 5.02% intra-day. And similarly, the 10yr yield was up +6.2bps to 4.70%, although this morning it’s since come down -1.0bps to 4.69%. Bear in mind that just after Christmas, the 10yr yield hit an intraday low of 3.78%, so it’s moved up by almost 100bps from that point now. At the same time, there was a decent spike in real yields, with the 10yr real yield (+4.4bps) reaching a post-November high of 2.28%.

That trend was echoed in Europe, where investors lowered their expectations for ECB rate cuts this year, and now see just 68bps of cuts by December’s meeting, down -5.5bps on the day. As in the US, that meant 10yr yields hit new YTD highs, with those on 10yr bunds (+4.1bps) up to 2.63%, 10yr OATs (+3.7bps) up to 3.13%, and 10yr gilts (+2.8bps) up to 4.36%. For now at least, a June rate cut from the ECB is still seen as an 84% probability, but from Monday we’ll start to get the flash CPI prints for April, so it’ll be interesting to see if that changes anything.

For equities, this backdrop meant it was a tough day across the board even if the recovery was steady as the US session progressed. All the major indices fell, including the S&P 500 (-0.46%), the NASDAQ (-0.64%) and the Dow Jones (-0.98%). Rebounds by Nvidia (+3.71%) and Tesla (+4.97%) helped limit and reverse the earlier larger losses. But Meta (-10.56%) was the worst performer in the entire S&P 500 following its earnings release the previous day, meaning that the Magnificent 7 (-1.19%) underperformed despite the gains for Nvidia and Tesla. IBM (-8.25%) lost significant ground after its release the previous evening as well.

Over in Europe, the STOXX 600 (-0.64%) also saw a decent decline, although the FTSE 100 (+0.48%) was again an exception as it hit another record high, aided by a surge in Anglo American (+16.10%), which was the index’s best performer after BHP proposed a takeover. The proposed deal would bring together two of the world’s largest mining companies and create a clear number one globally. Our mining team think the deal rationale is about global scale and growth in copper, a structurally tight commodity which is key to future global electrification. Copper prices have risen by +17.6% so far this year, and overnight they’re trading at their highest level since April 2022. The mining team’s note (link here) runs through the deal terms and other talking points.

Looking at yesterday’s other data, the US weekly initial jobless claims fell to 207k in the week ending April 20 (vs. 215k expected), which is their lowest level in a couple of months. Otherwise, pending home sales grew by +3.4% in March (vs. +0.4% expected), reaching a 13-month high.

To the day ahead now, and data releases include US PCE inflation for March, along with personal income and personal spending. In addition, there the University of Michigan’s final consumer sentiment index for April, and in the Euro Area, we’ll get the M3 money supply for March. Finally, earnings releases include Exxon Mobil and Chevron.

2 B) NOW NEWSQUAWK (EUROPE/REPORT)

Strong Big Tech earnings prop up equities, JPY lower post-BoJ & Dollar flat ahead of US PCE – Newsquawk US Market Open

FRIDAY, APR 26, 2024 – 05:57 AM

- Equities are firmer, benefiting from strong Big Tech earnings; Google (+11.7%), Microsoft (+3.6%)

- Dollar is flat, USD/JPY moved lower in quick succession before paring back, Aussie outperforms given the risk tone and higher metal prices

- Bonds are modestly firmer, though very much contained ahead of US PCE

- Crude within recent ranges, XAU trudges higher and base metals entirely in the green; 3M LME topped USD 10,000/t

- Looking ahead, US PCE, Personal Income, Earnings from Colgate, Exxon, Chevron & Phillips 66.

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses, Stoxx 600 (+0.5%) are entirely in the green, though trade has been contained at session highs, as participants await March’s US PCE at 13:30 BST.

- European sectors are almost entirely in the green, with the exception of Chemicals, following poor IMCD (-9.1%) results. Tech tops the pile, with optimism lifted following strong large-cap Tech earnings in the US.

- US Equity Futures (ES +0.7%, NQ +0.9%, RTY +0.1%) are entirely in the green, with the NQ outperforming, benefitting from significant pre-market strength in both Google (+11.1%) and Microsoft (+3.6%), after reporting strong earnings after-market.

- Click here and here for the sessions European pre-market equity newsflow.

- Click here for more details.

FX

- USD is around flat, and holding within a 105.40-71 range. USD was initially being propped up by JPY softness post-BoJ, although that has abated somewhat, amid Yen intervention speculation.

- JPY is the clear laggard across the majors following the BoJ policy announcement overnight, which provided no hawkish surprise. USD/JPY took another leg higher amid BoJ Ueda’s press conference, before being slapped down to sub-155 levels, a few hours later. Some will likely view the move as intervention but we are yet to see any official confirmation of this.

- EUR is flat vs. the USD and breached yesterday’s 1.0740 best. If the pair ventures higher, 1.0756 from April 11th is the next potential target.

- Antipodeans are firmer vs. the USD and outmuscling peers alongside the favourable risk environment. AUD/USD has gained a firmer footing above its 200 and 50DMAs at 0.6526 and 0.6532 respectively with focus now on a potential approach of 0.66

- PBoC set USD/CNY mid-point at 7.1056 vs exp. 7.2449 (prev. 7.1058).

- Click here for more details.

FIXED INCOME

- USTs are a touch firmer after yesterday’s data induced losses, which sent the Jun’24 UST to a contract low of 107.04. Today’s trade has been contained within a 107.04-108.01 range, with all eyes on March’s US PCE metrics later.

- Bund price action has been following USTs and attempting to recoup recently lost ground which has been inspired this week by a combination of better data and speak from hawkish ECB members. Bunds are so far respecting yesterday’s 129.53-130.38 range.

- Gilts are firmer and in-fitting with global peers in an attempt to claw back recent losses. However, with a lack of UK-specific drivers, UK paper will likely remain at the whim of global peers.

- Click here for more details.

COMMODITIES

- A relatively tame session thus far for the crude complex following Thursday’s choppy trade, as participants await monthly US PCE metrics; Brent Jun’24 range between 89.08-69/bbl.

- Precious metals are firmer amid the softer Dollar and ahead of the US PCE data, with spot silver narrowly leading vs spot gold. XAU topped yesterday’s peak (USD 2,344.93/oz) to trade in a current intraday range between USD 2,326.36-2,352.30/oz.

- Base metals are stronger across the board amid bullish momentum after copper crossed key levels, with the broader complex underpinned by the softer Dollar and broader risk appetite; 3M LME copper is posting gains of over USD 100/t at the time of writing after mounting the key USD 10,000/t mark to levels last seen in 2022.

- India Oil Minister said cartel of oil producers are responsible for current volatility in the market; oil producers are cutting down and holding back production, according to ETNow.

- Click here for more details.

NOTABLE EUROPEAN HEADLINES

- ECB’s Panetta said they must weigh the risk of monetary policy becoming too tight, while he added that timely and small rate cuts would counter weak demand and could be paused. Furthermore, he stated that hesitations in adjusting rates would hurt investment and productivity, while large rate cuts could create a credibility issue.

- ECB Consumer Inflation Expectations survey (Mar) – 12-months ahead 3.0% (prev. 3.1%); 3-year ahead 2.5% (prev. 2.5%). Economic growth expectations for the next 12 months 1.1% (prev. -1.1%)