GOLD PRICE CLOSED DOWN $32.10 TO $2389.60

SILVER PRICE DOWN $0.66 TO $31.23

Gold ACCESS CLOSED $2379.00

Silver ACCESS CLOSED: $30.88

Bitcoin morning price:$69,994 UP 784 DOLLARS.

Bitcoin: afternoon price: $69,545 UP 334 dollars

Platinum price closing DOWN $11.60 TO $1043.80

Palladium price; DOWN $25.30 AT $1004.65

END

FRBNY ORCHESTRATED RAID. YOU CAN BET THE FARM THAT CENTRAL BANKS WERE BUYERS OF NAKED GOLD SHORTS AND WLL BE TENDERING THESE CONTRACTS FOR PHYSICAL

SHANGHAI GOLD PREMIUM 31 DOLLARS/COMEX GOLD

SHANGHAI GOLD

SHANGHAI GOLD (USD) FUTURES – QUOTES

VENUE:

- GLOBEX

AUTO-REFRESH IS OFF

Last Updated 22 May 2024 01:52:50 PM CT.

Market data is delayed by at least 10 minutes.

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $3256.15 DOWN 47.09 CDN dollars per oz( * NEW ALL TIME HIGH 3,305.30 CDN DOLLARS PER OZ//MAY 20 2024)

*BRITISH GOLD: 187.70 DOWN 34.56 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2197.86 DOWN 33.21 Euros per oz //* (ALL TIME CLOSING HIGH: 2248.89 EUROS PER OZ//APRIL 16.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCH: COMEX

EXCHANGE: COMEX

CONTRACT: MAY 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,421.700000000 USD

INTENT DATE: 05/21/2024 DELIVERY DATE: 05/23/2024

FIRM ORG FIRM NAME ISSUED STOPPED

357 C WEDBUSH 4

435 H SCOTIA CAPITAL 1

624 H BOFA SECURITIES 4

657 H MORGAN STANLEY 1

TOTAL: 5 5

MONTH TO DATE: 2,2

JPMorgan stopped 0/5

FOR MAY2024

GOLD: NUMBER OF NOTICES FILED FOR MAY/2024. CONTRACT: 5 NOTICES FOR 500 OZ or 0.0155 TONNE

total notices so far: 2205 contracts for 220,500 Oz (6.858 tonnes)

FOR MAY:

SILVER NOTICES: 31 NOTICE(S) FILED FOR 155,000 OZ/

total number of notices filed so far this month : 6009 for 30.045 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $32.10

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

NO CHANGES IN GOLD INVENTORY AT THE GLD:

/ /INVENTORY RESTS AT 838.54TONNES

INVENTORY RESTS AT 838.54 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER DOWN $0.66 AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV:

// INVENTORY LOWERS TO 422.227 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 422.227 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY HUGE SIZED 1400 CONTRACTS TO 186,945 AND STALLING FROM ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS TINY SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR LOSS OF $0,41 IN SILVER PRICING AT THE COMEX ON TUESDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN SHORT COVERING BY OUR SPECS WITH THE LOSS IN PRICE. WE HAD ANOTHER HUMONGOUS SIZED 1013 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 1013 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0,41 BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A SMALL SIZED GAIN OF 238 CONTRACTS ON OUR TWO EXCHANGES WITH THE LOSS IN PRICE OF $0,41.

WE MUST HAVE HAD:

A HUGE SIZED 1638 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 28.130MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE JUMP OF 30,000 OZ

//NEW STANDING FOR SILVER//MAY IS THUS 30.250 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI LOSS //HUMONGOUS SIZED EFP ISSUANCE/ VI) HUMONGOUS SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1013 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED 1394 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY

TOTAL CONTRACTS for 16 DAYS, total 21,040 contracts: OR 105.200 MILLION OZ (1315 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 1315 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL PROBABLY BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 105.200 MILLION OZ //WILL BE A STRONG MONTH FOR EX FOR PHYSICAL ISSUANCE

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1400 CONTRACTS WITH OUR LOSS IN PRICE OF SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 1013 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAY OF 29.345 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 30,000 OZ QUEUE JUMP

//NEW TOTAL STANDING AT 30.250 MILLION OZ

WE HAVE A SMALL SIZED GAIN OF 238 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUMONGOUS SIZED 1013 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS

THE NEW TAS ISSUANCE TUESDAY NIGHT (1013) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 31 NOTICE(S) FILED TODAY FOR 155,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 2889 OI CONTRACTS TO 530,591 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 1933 CONTRACTS

WE HAD A FAIR SIZED INCREASE IN COMEX OI (2889 CONTRACTS) OCCURRED DESPITE OUR LOSS OF $12.00 IN PRICE/TUESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER TRYING TO CONTAIN GOLD’S PRICE RISE. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 4.684 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY;S 400 OZ QUEUE JUMP PLUS WE MUST ADD THAT DUBIOUS ISSUANCE OF 1084 OI EX FOR RISK CONTRACTS ISSUES ON FRIDAY WHEREBY THE BUYER ASSUMES RISK OF 3.3716 TONNES OF GOLD//NEW STANDING INCREASES TO 6.923 TONNES PLUS THE DUBIOUS 3.3716 ECH FOR RISK!

NEW STANDING 10.2946 TONNES// ALL OF THIS HAPPENED WITH OUR $12.00 LOSS IN PRICE WITH RESPECT TO TUESDAY’S TRADING. WE HAD A STRONG SIZED GAIN OF 5091 OI CONTRACTS (15.84 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 2202 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 530,591

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5091 CONTRACTS WITH 2889 CONTRACTS INCREASED AT THE COMEX// AND A STRONG SIZED 2202 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 5091 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 1122 CONTRACTS,,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2202 CONTRACTS) ACCOMPANYING THE FAIR GAIN IN COMEX OI 2889/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 5091 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 4.684 TONNES FOLLOWED BY TODAY;S 400 OZ QUEUE JUMP PLUS 3.3716 TONNES EX FOR RISK//PRIOR

//NEW STANDING /MAY 10.2946 TONNES.

/ 3) CONSIDERABLE LIQUIDATION OF CONTRACTS MOSTLY DUE TO SPREADERS WITH THE LARGE LOSS IN PRICE.

// 4) GOOD SIZED COMEX OPEN INTEREST GAIN 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1122 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY. :

TOTAL EFP CONTRACTS ISSUED: 64,532 CONTRACTS OR 6,453,200 OZ OR 200.72 TONNES IN 16 TRADING DAY(S) AND THUS AVERAGING: 4033 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES 200.72 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 200.72 DIVIDED BY 3550 x 100% TONNES = 5.66% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 200.72 TONNES (WILL BE ANOTHER STRONG MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 1400 CONTRACTS OI TO 186,945 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1638 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1638 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1638 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1400 CONTRACTS AND ADD TO THE 1638 E.FP. ISSUED

WE OBTAIN A SMALL SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 238 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 1.190 MILLION OZ

OCCURRED DESPITED OUR $0,41 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED UP 0,037 PTS OR 0.02% //Hang Seng CLOSED DOWN 25.02 PTS OR 0.13%// Nikkei CLOSED DOWN 329.83 OR 0.85%//Australia’s all ordinaries CLOSED DOWN 0.02%///Chinese yuan (ONSHORE) closed DOWN TO 7,2404 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2514/ Oil DOWN TO 77.88 dollars per barrel for WTI and BRENT UP AT 82.04 /Stocks in Europe OPENED MOSTLY GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 2889 CONTRACTS TO 530,591 DESPITE OUR LOSS IN PRICE OF $12.00 WITH RESPECT TO TUESDAY TRADING. WE HAD A CONSIDERABLE T.A.S. LIQUIDATION TUESDAY AS WELL AS SHORTS, DESPERATELY TRYING TO GET OUT OF THEIR NAKED SHORTS WITH GOLD’S RECENT RAPID RISE!

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAY.… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 2202 EFP CONTRACTS WERE ISSUED: : JUNE 2202 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE:2202 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 5091 CONTRACTS IN THAT 2202 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A FAIR SIZED GAIN OF 2889 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $12.00// TUESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A FAIRT SIZED 1122 CONTRACTS. MOST OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (6.923 TONNES+ 3.3716 EX FOR RISK/PRIOR) = 10.2946 TONNES ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 6.923 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 10.2946

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A $12.00 //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG GAIN OF 7024 CONTRACTS ON TUESDAY DESPITE THE LOSDS IN PRICE. THE T.A.S. ISSUED ON MONDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS AND MOST LIKELY ON TODAY’S TRADING.

WE HAVE GAINED A TOTAL OI OF 21.85 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY (4.684 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 4 CONTRACTS OR 400 OZ ( .0124 TONNES) PLUS 3.3716 TONNES OF EX FOR RISK/PRIOR

NEW STANDING: 6.923 TONNES PLUS 3.1716 TONNES EX FOR RISK/PRIOR = 10.2946

ALL OF THIS WAS ACCOMPLISHED WITH OUR HUGE LOSS IN PRICE TO THE TUNE OF $12.00

WE HAVE REMOVED 1235 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES 7024 CONTRACTS OR 702,400 (21.85 TONNES)

confirmed volume TUESDAY 280,761 contracts// fair

//speculators have left the gold arena

MAY 22 MAY GOLD

/ /// THE MAY 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | nil OZ . |

| Deposit to the Dealer Inventory in oz | 00 oz |

| Deposits to the Customer Inventory, in oz | 64,018.917 oz Ashai |

| No of oz served (contracts) today | 5 notice(s) 500 OZ 0.0155 TONNES |

| No of oz to be served (notices) | 21 contracts 2100 OZ 0.0653 TONNES |

| Total monthly oz gold served (contracts) so far this month | 2205 notices 220,500 oz 6.858 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: 0 oz

we have 1 customer deposit:

i) into ASHAI: 64,018.917 oz

total deposit 64,018.917 oz

total customer withdrawals: 0

TOTAL WITHDRAWALS nil 0z

Adjustments: 1

brinks///dealer to customer; 5921.76 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY

For the front month of MAY we have an oi of 26 contracts having LOST 27 contracts.

We had 31 contracts served on TUESDAY, so we gained 4 contracts or 400 oz (0.0124 Tonnes).

JUNE DECREASED ITS OI BY 8164 CONTRACTS DOWN TO 199,098 CONTRACTS.

JULY GAINED 44 CONTRACTS TO STAND AT 586

We had 5 contracts filed for today representing 500 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 5 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the MAY /2024. contract month, we take the total number of notices filed so far for the month (2205) x 100 oz ) to which we add the difference between the open interest for the front month of MAY ( 26 CONTRACTS) minus the number of notices served upon today (5 x 100 oz per contract( equals 222200 OZ OR 6.911 TONNES. PLUS THE 3.3716 OF EX FOR RISK/PRIOR = 10.2826

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (2205x 100 oz + (26 OI for the front month} minus the number of notices served upon today (5 x 100 oz which equals 222200 oz (6.923 TONNES) PLUS 3.3716 EX FOR RISK/PRIOR = 10.2946 TONNES.

TOTAL COMEX GOLD STANDING FOR MAY: 10.2946 TONNES WHICH IS HUGE FOR THIS A NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX84XXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,548,842.069 48.17 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,555,512.794 OZ

TOTAL REGISTERED GOLD 7,314,436.355 ( 227.50 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,241,076.429 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 5,765,594 oz (REG GOLD- PLEDGED GOLD)= 179.33 tonnes //dropping like a stone

END

SILVER/COMEX

MAY 22

INITIAL

//2024// THE MAY 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | nil . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 64,018.917 oz Ashai |

| No of oz served today (contracts) | 31 CONTRACT(S) (155,000 OZ) |

| No of oz to be served (notices) | 41 contracts (0.205 million oz) |

| Total monthly oz silver served (contracts) | 6009 Contracts (30.045 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i) into Ashai 64,018.917 oz

total customer deposit 64,018.917 oz

JPMorgan has a total silver weight: 128.997million oz/297.746 million or 43.24%

adjustment: 0

Comex withdrawals: 0

TOTAL REGISTERED SILVER: 62.613MILLION OZ//.TOTAL REG + ELIGIBLE. 297.746 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF MAY/2024 OI: 72 CONTRACTS HAVING LOST 54 CONTRACT(S).

.

We had 60 notices served on TUESDAY so we GAINED 6 contracts or 30,000 oz underwent a STRONG QUEUE JUMP AS THEY WERE SET TO TAKE DELIVERY ON THIS SIDE OF THE POND.

JUNE SAW A GAIN OF 177 CONTRACTS RISING TO 1668

JULY SAW A LOSS OF 1448 CONTRACTS DOWN TO 149,926

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 31 for 155,000 oz

CONFIRMED volume; ON TUESDAY 123,886 mammoth

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 6009 x 5,000 oz = 30.045 MILLION oz

to which we add the difference between the open interest for the front month of MAY (72 and the number of notices served upon today 31x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2024 contract month: 6009 notices served so far) x 5000 oz + OI for the front month of MAY (72)x number of notices served upon today minus (31x 5000 oz of silver standing for the may contract month equates to 30.250 MILLION OZ.

New total standing: 30.250 million oz.

There are 62.613 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

MAY 22 WITH GOLD DOWN $32.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 21 WITH GOLD DOWN $12,00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 20 WITH GOLD UP $21.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.10 TONNES OF GOLD INTO THE GLD//NEW TOTAL 838.54 TONNES

MAY 17 WITH GOLD UP $31.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//NEW TOTAL 833.36 TONNES

MAY 16 WITH GOLD DOWN $7.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//NEW TOTAL 833.36 TONNES

MAY 15 WITH GOLD UP $34.90 ON THE DAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD

///INVENTORY RISES TO 831.93 TONNES

MAY 14 WITH GOLD DOWN $17.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//

///INVENTORY RISES TO 831.33 TONNES

MAY 13 WITH GOLD DOWN $31.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD////INVENTORY RISES TO 831.93 TONNES

MAY 10 WITH GOLD UP $34.65 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 9 WITH GOLD UP $18.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 8 WITH GOLD DOWN $0.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 830.47 TONNES

MAY 7 WITH GOLD DOWN $6.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 832.19 TONNES

MAY 6WITH GOLD UP $21.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .55 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 831.64 TONNES

MAY 2 WITH GOLD UP $0.20 ON THE DAY; SMAKK CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 830.47 TONNES

MAY 1 WITH GOLD UP $7.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

APRIL 29WITH GOLD UP $10,55TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

APRIL 26WITH GOLD UP $5.40TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.54 TONNES FROM THE GLD /INVENTORY RISES AT 832.19 TONNES

APRIL 25WITH GOLD UP $5.05 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD /INVENTORY RISES AT 833,63 TONNES

APRIL 19 WITH GOLD UP $15.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 4.32 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 831.91 TONNES

APRIL 18 WITH GOLD UP $11.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE WITHDRAWAL OF 2.59 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 827.59 TONNES

APRIL 17 WITH GOLD DOWN $17.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 830;18 TONNES

APRIL 16 WITH GOLD UP $23.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 828.45 TONNES

APRIL 15 WITH GOLD DOWN $. 80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A HUGE WITHDRAWAL OF 1.80 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 824.84 TONNES

APRIL 12 WITH GOLD UP $2.80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD/ INVENTORY RISESS AT 830.75 TONN

GLD INVENTORY: 838.54 TONNES, TONIGHTS TOTAL

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 22 WITH SILVER DOWN $0.66 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 21 WITH SILVER DOWN $0.41 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A DEPOSIT OF 3.792 MILLION OZ FROM THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 20 WITH SILVER UP $1.28 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 1.005 MILLION OZ FROM THE SLV// INVENTORY LOWERS TO 418.435 MILLION OZ

MAY 17 WITH SILVER UP $1.37 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 868,000 OZ FROM THE SLV// INVENTORY LOWERS TO 419.440 MILLION OZ

MAY 16 WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY REMAINS AT 420.308 MILLION OZ

MAY 15 WITH SILVER UP 101 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A WITHDRAWAL OF 1.919 MILLION OZ FROM THE SLV

INVENTORY RESTS AT 420.308 MILLION OZ

MAY 14 WITH SILVER UP 25 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;

INVENTORY RESTS AT 422.227 MILLION OZ

MAY 13 WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;NVENTORY RESTS AT 422.227 MILLION OZ

MAY 10 WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A HUGE WITHDRAWAL OF 1.,828 MILLION OZ//INVENTORY RESTS AT 422.227 MILLION OZ

MAY 9 WITH SILVER UP 78 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 8 WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 7WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 6 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.055 MILLION OZ

MAY 3 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 2WITH SILVER UP 0.12 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ A WITHDRAWALOF 4.471 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 1 WITH SILVER UP 0.09 TODAY: SMALLCHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF ,457 MILLION OZ INTO THE SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 29WITH SILVER UP $0.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 26WITH SILVER DOWN 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.097 MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 25WITH SILVER UP $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 1.534 MILLION OF SILVER OUT OF THE SLV// :SLV INVENTORY RESTS AT 428.717 MILLION OZ

APRIL 24/WITH SILVER DOWN $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 11.904MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 428.280 MILLION OZ

APRIL 23/WITH SILVER UP $0.11TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV / :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 22/WITH SILVER DOWN $1.51 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.194 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 19/WITH SILVER UP 42 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.657 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 418.570 MILLION OZ

APRIL 18/WITH SILVER DOWN $.04TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.977 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 422.227 MILLION OZ

APRIL 17/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF .868 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 426/204 MILLION OZ

APRIL 16/WITH SILVER DOWN $0.46 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF NON EXISTENT SILVER// :SLV INVENTORY RESTS AT 427.072 MILLION OZ

APRIL 15/WITH SILVER UP $0.88 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 12/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 4.069 MILLION OZ FROM THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 11/WITH SILVER UP $0.23 TODAY: STRANGE INDEED! HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.931 MILLION OZ :SLV INVENTORY RESTS AT 437.998 MILLION OZ

CLOSING INVENTORY 422.227 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

“Inflation Creates An Illusion Of Wealth” – Peter Schiff Blasts Biden’s Brags About Raising Taxes

WEDNESDAY, MAY 22, 2024 – 11:25 AM

This week Peter’s back to discuss new economic data, Powell’s recent remarks in the Netherlands, and the Biden administration’s new tariffs. More and more signs point to economic stagflation, but Biden, Powell, and their cronies continue to deflect the blame and increase everyday Americans’ taxes.

The Dow may have traded above 40,000 this week, but that doesn’t necessarily mean Americans are wealthier:

“Inflation creates an illusion of prosperity, an illusion of wealth. That’s another reason that government loves inflation so much. They’re really partners. The government derives all sorts of hidden benefits from inflation, but it never wants to admit this. It never wants to say this out loud. But everything the government does is supported by inflation...

They kind of worship inflation, but they never speak its name— not in the context of what they’re using it for, right? And so when the public gets upset that prices are rising a lot and their living standards are falling, then the government will talk about inflation. But it’ll talk about it as if it’s this exogenous event that is completely beyond their control.”

Contrary to what progressives believe, inflation is not a result of capitalism:

“Everything is more expensive because of the government debasement of our money. That’s why we have inflation. It’s not an accident, and it’s not a natural byproduct of capitalism.

Capitalism does the reverse! I’ve pointed this out, but the CPI from 1800 to 1900 lost 50% of its value. Prices fell for a hundred years! That’s what capitalism does.

Now in the following hundred years, prices skyrocketed. That’s what socialism does. That’s what government does. That’s what central banking does.”

Wednesday’s inflation report was not as bad as expected, although rising prices in industrial metals beg to differ:

“As everybody is talking about, ‘Hey, we got this great inflation news,’ copper is telling you that inflation is not good. It’s bad. So I’d rather believe the market than the Fed telling us inflation is under control. … Look at copper— “Dr. Copper”— it’s telling you that inflation is anything but under control.”

New data on retail sales, manufacturing, and housing permits all point towards a slowdown in the economy:

“That’s the sign of a weaker economy. Why are they building fewer homes? Because Americans can’t afford to buy them. They don’t have the purchasing power, and mortgage rates have gone up. But of course, if we’re not going to be adding to the supply of houses, then the housing shortage is going to continue.”

Peter pivots to tariffs, the big political news of the week:

“[Biden’s] announcing them like he’s delivering good news, like, ‘Hey, I got great news, everybody! We’ve got these tariffs.’ The tariffs are taxes! Higher tariffs mean higher taxes…

Who wants to hear that? And these are not, ‘Oh, we’re going to tax the rich.’ No, no, these are not the taxes that fall on the rich. In fact, the rich couldn’t care less about these tariffs. It’s the middle class or the poor that are going to pay these tariffs. And that’s Biden’s base, right? That’s who he’s playing to. That’s the votes that he wants. And he’s telling his own people of raising your taxes, except he’s not putting it in those words. He’s lying.”

The new tariffs are a textbook case of government regulation contradicting other government regulations. None of it makes any sense:

“Biden likes to pretend, ‘Oh, we’re all about the environment. We want people to go solar.’ 50% tariffs on solar panels— 50% percent! People are supposed to be converting to solar. You know, there’s all kinds of tax credits. You invest in solar panels, you get a tax credit. So the government is subsidizing people for using solar power. Tesla gets subsidies for selling battery powered cars.

The government is paying Americans, and they’re trying to encourage them to use solar power. Yet we now want to impose taxes on them when they do it. You want to buy solar panels? Now the government is going to drive up the price of the very panels it’s subsidizing you to buy. … Government has two policies at cross purposes.”

Jerome Powell spoke in Amsterdam this week and gave an alarming look into his naivete:

“Powell basically said, ‘No, I have no regrets, nothing. I wouldn’t change anything. We did everything right.’ ..

If that’s truly what Powell believes, then there’s no hope of them solving any problems that they clearly don’t understand. Powell has no idea where inflation comes from. So how is he going to get rid of it?”

The simple fact is that the economy is too complicated for any man or institution to plan. Tariffs, central banking, and tax credits only serve to distort and manipulate economic incentives for the interests of those in power. Powell and Biden illustrate this perfectly.

3. CHRIS POWELL//GATA DISPATCHES

CHRIS POWELL…

Jan Nieuwenhuijs: Strong PBoC and Chinese private-sector buying continues to boost gold

Submitted by admin on Wed, 2024-05-22 11:15 Section: Daily Dispatches

By Jan Nieuwenhuijs

Gainesville Coins, Lutz, Florida

Wednesday, May 22, 2024

Chinese private-sector gold imports accounted for 543 tonnes in the first quarter, while the People’s Bank of China added 189 tonnes to its reserves over this time.

Most of the PBoC’s purchases are “unreported.”

China continues to be the marginal buyer in the gold market, driving up the price. I expect that China will remain a robust buyer of gold going forward

In my latest article on global gold flows from March 2024, “China Has Taken Over Gold Price Control from the West,” I showed that in 2022 China broke the peg between the U.S. dollar gold price and “real yields.”

Instead of being price-sensitive, China had become a driving force of the gold price.

The data at my disposal ran until December 2023 which made me hesitant to conclude the sharp increase in the gold price since late February was also caused by the Chinese. However, as new data has been released, I can confidently say that China initiated the current bull market. …

… For the remainder of the analysis:

https://www.gainesvillecoins.com/blog/strong-pboc-chinese-private-sector-buying-boosts-gold-price

END

Alabama abolishes income taxes on gold and silver

Submitted by admin on Mon, 2024-05-20 12:52 Section: Daily Dispatches

From Money Metals News Service

Saturday, May 18, 2024

Alabama Governor Kay Ivey today signed a bill that removes all income taxes on capital gains from the sale of gold and silver, enabling the state to take an important step forward in reinforcing sound-money principles.

With this move, Alabama joins a growing number of states prioritizing the protection of citizens against the deleterious effects of inflation, currency debasement, and mounting federal debt.

Enactment of Senate Bill 297 makes Alabama the 13th state in the nation that does not impose capital gains taxes on sales of gold and silver. …

… For the remainder of the report:

END

Jim Rickards: Trump aims not for currency war but currency peace

Submitted by admin on Tue, 2024-05-21 11:17 Section: Daily Dispatches

By James G. Rickards

The Daily Reckoning, Baltimore

Tuesday, May 14, 2024

There has been a lot reported in recent days about the return of currency wars. This story arises in the context of a likely Trump election victory in the November presidential elections.

Trump badly bungled his transition after being elected president in 2016. He wasn’t ready with a long list of loyal appointees

Many of his senior appointments, such as Rex Tillerson as secretary of state, James Mattis as secretary of defense, and John Kelly as chief of staff, secretly disliked Trump but accepted their roles as so-called “adult supervision” around the supposedly reckless Trump.

They thwarted his agenda. That backstabbing came on top of the large number of Obama holdovers in the deep state who saw themselves as a “resistance” movement.

Trump is doing a better job of preparing for a second term as president, but the resistance isn’t sitting still either. They’re moving to disable a new Trump administration even before the election.

The currency wars stories are part of that effort. …

… For the remainder of the commentary:

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS /

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT//aluminum

Aluminum Jumps To 23-Month High Amid Ongoing Aussie Production Issues

TUESDAY, MAY 21, 2024 – 08:40 PM

From coffee to cocoa, orange juice to gold, and silver to copper, commodity prices are spiking across the board (we outlined this on Monday). The latest surge occurred Tuesday when aluminum tagged 23-month highs due to ongoing production issues emerging from Australia. The broad-based commodity rally signals the inflation storm central bankers are battling is not over.

Rio Tinto, one of the largest aluminum producers, declared force majeure on third-party contracts for exporting alumina from its refineries in Queensland, Australia. This is due to a broken natural gas pipeline operated by Queensland Gas Pipeline.

A spokesperson for the company told Dow Jones that NatGas supplies will return to capacity at a much later date than previously anticipated:

“The pipeline operator’s current estimate [is] for a return to normal levels in the second half of 2024.

“Until then, Yarwun and QAL [Queensland Alumina Limited] will continue to operate at lower capacities.”

On the London Metal Exchange, aluminum contracts settled up 3.6% at $2,725.50 a metric ton, the highest level since early summer 2022.

Colin Hamilton, managing director for commodities research at BMO Capital Markets, told Bloomberg that today’s price action in aluminum markets suggests mounting fears about “dwindling aluminum output” — a situation he views as “unlikely.”

Hamilton noted that industrial metal could be “part of the digital and electrical revolution we know is coming … is going to benefit.” We call this “The Next AI Trade.”

One base metal that has been on everyone’s radars is copper. Comex prices have squeezed to record highs and continue on Tuesday.

Since February, industrial metals tracked by Bloomberg have soared 30%.

Precious metals tracked by Bloomberg have also broken out.

Commodities as a whole, tracked by Bloomberg, have soared.

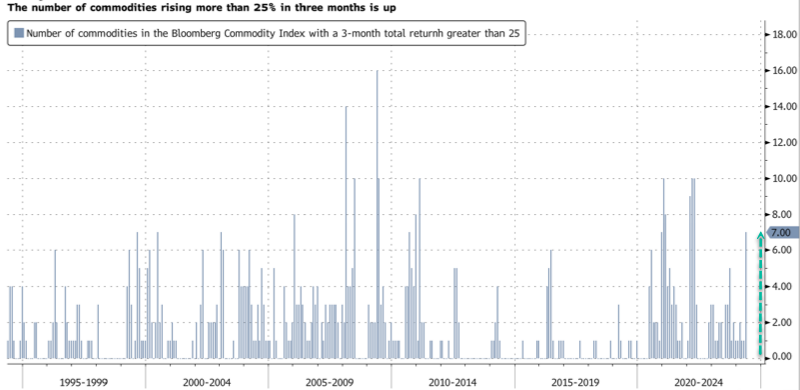

Bloomberg’s Cameron Crise pointed out that the number of commodities in the Bloomberg Commodity Index that are up by at least 25% over the three month period have risen to seven.

Crise continues:

Currently, there are seven: cocoa, copper, nickel, orange juice, silver, tin, and zinc. Clearly industrial metals are a theme in that list, which itself raises the question of how valid some of the global growth concerns might be. Anyhow, the current total of seven is the highest since the middle of 2022; coincidentally (or not), the industrial metals subindex total return is also the highest since the same point in time.

He added:

Obviously, over long periods of time the link between the series above and inflation isn’t necessarily that great; the highest-ever reading came in 2009 with the correction of the GFC downside overshoot in commodity prices. Still, the relatively broad-based rise in industrial metals is noteworthy and raises another question about just how benign the inflation outlook might be moving forwards.

The hot commodity market is posing new challenges for Fed chair Jerome Powell and his friends in the White House…

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

ASIA TRADING//WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED UP 0,037 PTS OR 0.02% //Hang Seng CLOSED DOWN 25.02 PTS OR 0.13%// Nikkei CLOSED DOWN 329.83 OR 0.85%//Australia’s all ordinaries CLOSED DOWN 0.02%///Chinese yuan (ONSHORE) closed DOWN TO 7,2404 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2514/ Oil DOWN TO 77.88 dollars per barrel for WTI and BRENT UP AT 82.04 /Stocks in Europe OPENED MOSTLY GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2405

OFFSHORE YUAN: DOWN TO 7.2514

SHANGHAI CLOSED DOWN 0.37 PTS OR 0.02 %

HANG SENG CLOSED DOWN 25.01 PTS OR 0.13%

2. Nikkei closed DOWN 329.83 PTS OR 0.85 %

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 104.81 EURO FALLS TO 1.0822 DOWN 32 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.994 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 156.60 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.536/Italian 10 Yr bond yield UP to 3.851 SPAIN 10 YR BOND YIELD UP TO 3.300%

3i Greek 10 year bond yield UP TO 3.536

3j Gold at $2412.25//Silver at: 31.61 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 8 100 roubles/dollar; ROUBLE AT 90.17

3m oil into the 77 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 156.60/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.994% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9153 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9903well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.455 UP 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.582 UP 4 BASIS PTS/

USA 2 YR BOND YIELD: 4.871 UP 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.18…(TURKEY)

10 YR UK BOND YIELD: 4.2740 UP 14 PTS

2a New York OPENING REPORT

Futures Drop, Yields Jump On Red-Hot UK Inflation, Nvidia Earnings On Deck

WEDNESDAY, MAY 22, 2024 – 07:57 AM

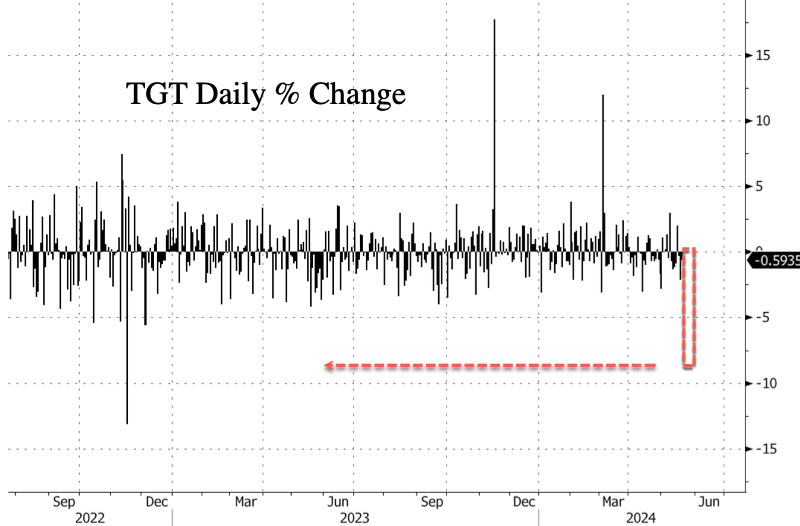

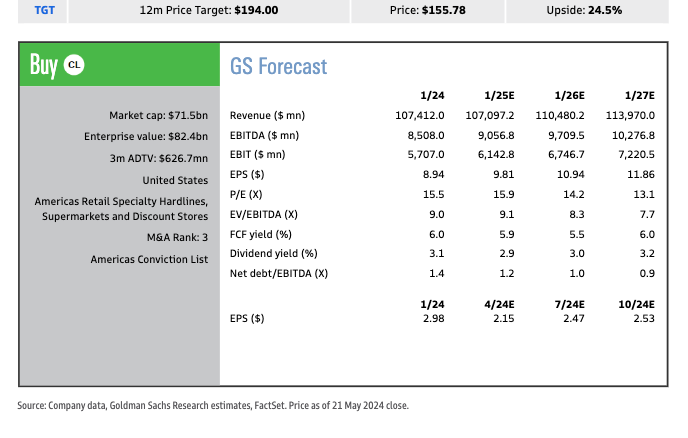

US futures are lower on Nvidia day; with the stock down 56bps in premarket trading, while Mag7 and semis are also all lower pre-mkt. As of 7:20am, S&P futures are down 0.1%, just off session lows amid signs of sticky inflation that dampened bets on early interest-rate cuts; Nasdaq futures drop 0.2% while Europe’s Stoxx 600 gauge slipped 0.3%, with energy shares among the big losers amid an earlier drop in crude prices. Bond yields are higher by 2-3bps in sympathy with Gilts where yields jumped on much hotter than expected inflation, or rather less than expected disinflation. The USD is higher and commodities are mixed: energy is higher, reversing earlier losses, while precious metals are lower with Ags outperforming. Aside from NVDA, the latest Fed Minutes are also released today, which should align with recent Fedspeak (hikes unlikely in 2024 and need more data to support cuts), as well as some consumer-sector earnings (Target tumbled 8% after guidance disappointed) which, in total, show a still solid aggregate consumer but continued deterioration in the lower income consumers.

In premarket trading, Tesla slid after disclosing European sales fell to a 15-month low in April while Lululemon shares dropped 4.6% after the athleisure brand announced organizational changes, including the departure of chief product officer Sun Choe. Raymond James said Choe leaving the company added to the “wall of worry” in the near term, while Jefferies noted that the adjustments could indicate future issues with top-line growth. Here are some other notable premarket movers:

- Bentley Systems shares fall 3.8% after Schneider Electric says talks with the software firm regarding a potential strategic transaction have been mutually terminated, according to an emailed statement. No transaction was agreed upon.

- Edwards Life shares climb 1.7% after an upgrade to buy at Citi.

- Kraft Heinz shares tick 0.9% higher after an upgrade to overweight from neutral at Piper Sandler, which said there is better visibility on the packaged-food company’s upside in food service, aided by a new innovation in time-saving dispensers.

- Lululemon shares decline 4.6% after the athleisure brand announced organizational changes, including the departure of chief product officer Sun Choe. Raymond James said Choe leaving the company added to the “wall of worry” in the near term, while Jefferies noted that the adjustments could indicate future issues with top-line growth.

- Middleby shares slip 2.2% after a downgrade to underweight at JPMorgan.

- Modine shares decline 9.1% after the maker of heating and air conditioning products provided a fiscal 2025 earnings forecast range with a midpoint that’s short of estimates.

- Rezolute shares jump 31% after the clinical-stage biopharmaceutical company said the Phase 2 study of RZ402 for certain patients with diabetic macular edema met both primary endpoints.

- Urban Outfitters shares jump 5.5% after the clothing retailer reported 1Q net sales that beat the average analyst estimate. Barclays highlighted the performance of Anthropologie, Free People, Free People Movement and Nuuly, which more than made up for the underperformance of its Urban Outfitters banner.

All eyes now turn to AI bellwether Nvidia, which is down 0.6% in thin premarket New York trading. It’s projected to report a 243% gain in revenue, according to Wall Street estimates, but its 90% year-to-date share rally sets a high bar for further gains. Shares have hit a fresh record high this week ahead of the result, seen as the grand finale for a robust US earnings season.

“Nvidia remains the focal point,” Pepperstone Group Ltd. strategist Chris Weston said, noting that options markets are pricing a 7% to 9% swing in the stock after the result. And while Nvidia’s sales and gross margins will grab the initial spotlight, “it’s the guidance on the earnings landscape and product roll-out from CEO Jensen Huang that could dictate if the market really wants to push this one along for a more sustained period,” Weston said.

Markets are also growing jittery about the prospect of stubbornly high inflation that could prevent central banks from easing policy as early as currently anticipated. The latest UK CPI figures lifted the pound and knocked bond prices across Europe as traders pushed back their expected timing for the first Bank of England rate cut. Earlier on Wednesday, the Reserve Bank of New Zealand kept interest rates unchanged and signaled policy will stay tight for longer, while Federal Reserve Governor Waller said on Tuesday he needs to see several more good inflation numbers to begin interest-rate cuts.

“Both the RBNZ and the UK inflation data highlight the fraught nature of the current juncture, with investors struggling to gauge both the timing and extent of long-awaited central bank easing cycles,” Rabobank’s head of rates strategy, Richard McGuire, said.

Meanwhile, two more Fed officials again reinforced a higher-for-longer message on rates. On Tuesday, Loretta Mester and Susan Collins said they need more evidence of slowing inflation before cutting. In response, traders dialed down expectatons for Fed interest rate cuts this year, currently seeing around 40 basis points of rate cuts in 2024, versus the 50 basis-point reduction priced last week. Minutes of the last Fed policy meeting, due later Wednesday, could offer further clues on rate-setters’ thinking.

European stocks dropped, with the Stoxx 600 index slipped 0.3%; travel and leisure stocks lead gains while the autos sector have the largest declines. Among individual stock movers, shares in Anglo American Plc weakened as investors waited to see if rival BHP Group Ltd. would launch its takeover bid to create a global copper behemoth. BHP has a deadline of 5 p.m. London time to announce a firm intention to make an offer for what could be among the world’s biggest takeover deals this year. Here are some of the biggest European movers Wednesday:

- Evotec climbs as much as 2.6% after first-quarter sales beat market expectations. Still, analysts flag risks to the firm’s reiterated 2024 guidance amid a broader slowdown

- Marks & Spencer jumps as much as 8.3% after reporting adjusted pretax profit that came ahead of estimates, saying it’s in the strongest financial health since 1997

- Swiss Life falls as third-party asset management net inflows came in “much weaker than expected,” and overshadow fee income growth, according to Citi

- SSE falls as much as 2.5% as the lack of EPS guidance by the UK power company disappoints alongside weaker performance in its renewables unit

- RS Group falls as much as 13% after reporting lower sales and profits in the recently-ended financial year, warning that demand remains subdued

- Ypsomed jumps 7.1% after its guidance beat expectations, according to ZKB. The Swiss supplier of auto-injectors also plans to separate its Diabetes Care operations

- Mytilineos drops as much as 6.3% after a shareholder launched an offer to sell shares in the Greek energy company at a discount to yesterday’s closing price

- Close Brothers falls as much as 7.9% after a trading update that saw downgrades to net interest margins and loan book growth

- Eutelsat drops following a downgrade to neutral at Citi, which says the satellite company’s risk profile is currently “heightened”

Earlier, Asian stocks traded in a narrow range as investors awaited new catalysts. The MSCI Asia Pacific Index dropped as much as 0.3% before erasing some losses. Toyota Motor and Alibaba Group dragged on the gauge, while chipmaker TSMC, a top Nvidia supplier, was among the biggest boosts. Stocks rose in Taiwan and New Zealand while benchmarks fell in Japan. Markets were closed for holidays in Singapore, Malaysia and Thailand. The key MSCI Asia stock gauge is trading close to its highest level in more than two years after a recent rally in Chinese stocks and hopes of US rate cuts. Strong gains in Hong Kong have raised some concerns of overheating, however, while two Federal Reserve officials reinforced a higher-for-longer message on interest rates Tuesday.

In FX, the Bloomberg dollar index rose to sessoon highs, tracking the rise in yields. The pound rose to the strongest level in two months against the euro as traders pared UK rate-cut bets after inflation cooled at a slower-than-expected pace. “UK services inflation remains high and suggests the BOE can wait before cutting the policy rate,” said Elias Haddad, a senior strategist at Brown Brothers Harriman & Co. in London. “The upward adjustment to UK interest rate expectations supports a firmer GBP particularly versus EUR.”

- EUR/GBP fell as much as 0.3% to 0.8512, crossing the April low to hit the weakest since March 11

- GBP/USD rose as much as 0.4% to 1.2761, extending a four-day rally to 0.7%; pair continued to trade at the highest since March

- EUR/CHF rose 0.3% to 0.9916, on its longest winning streak since October 2022

Treasuries were pressured lower over early London session, following wider losses seen across gilts which aggressively bear flattened with yields at highest in weeks after inflation slowed far less than expected. Following the UK April CPI, the UK 2-year year yield remains cheaper by around 12bp on the day into early US session with UK 2s10s spread flatter by 3bp and 5s30s by 4bp on the day. Subsequently, UK markets no longer fully priced two Bank of England rate cuts for this year. US yields are also cheaper by 3bp to 5bp across the curve with belly-led losses on the day flattening 5s30s spread by around 1bp; 10-year yields around 4.45%, cheaper by 4bp vs. Tuesday close with UK 10-year underperforming by around 6.5bp in the sector

US session focus also includes supply pressure with $16 billion 20-year bond sale scheduled for 1pm New York, while Fed release latest policy minutes at 2pm. Treasury auctions resume with $16b 20-year bond sale at 1pm, before $16b 10-year TIPS reopening Thursday. The WI 20-year yield at ~4.66% is roughly 16bp richer than April’s stop-out, which traded 2.5bp through the WI in a strong auction result

In commodities, crude reversed earlier losses, when prices were pressured by the surprise build in private inventories (Crude +2.5mln vs exp. -2.5mln) ahead of today’s DoEs; Brent traded as low as $81.50 before rebounding over $82. Precious metals are softer with spot gold subdued amid a lack of notable geopolitical developments in recent days and ahead of FOMC minutes; XAU resides within a USD 2,410.69-2,426.62/oz range. A pullback is seen across most base metals following the recent rally, with profit-taking not to be discounted, with 3M LME copper towards the bottom end of a 10,636.50-10,857.50 intraday range.

In crypto, Bitcoin stabilized around $70K, with Ethereum holding just above $3.7k.

To the day ahead now, and the main highlight will be Nvidia’s earnings after the close. Otherwise, data releases include the aforementioned red hot UK CPI print for April and US existing home sales for April. We’ll get the FOMC minutes from the May meeting, and hear from ECB President Lagarde, BoE Deputy Governor Breeden, and the Fed’s Goolsbee.

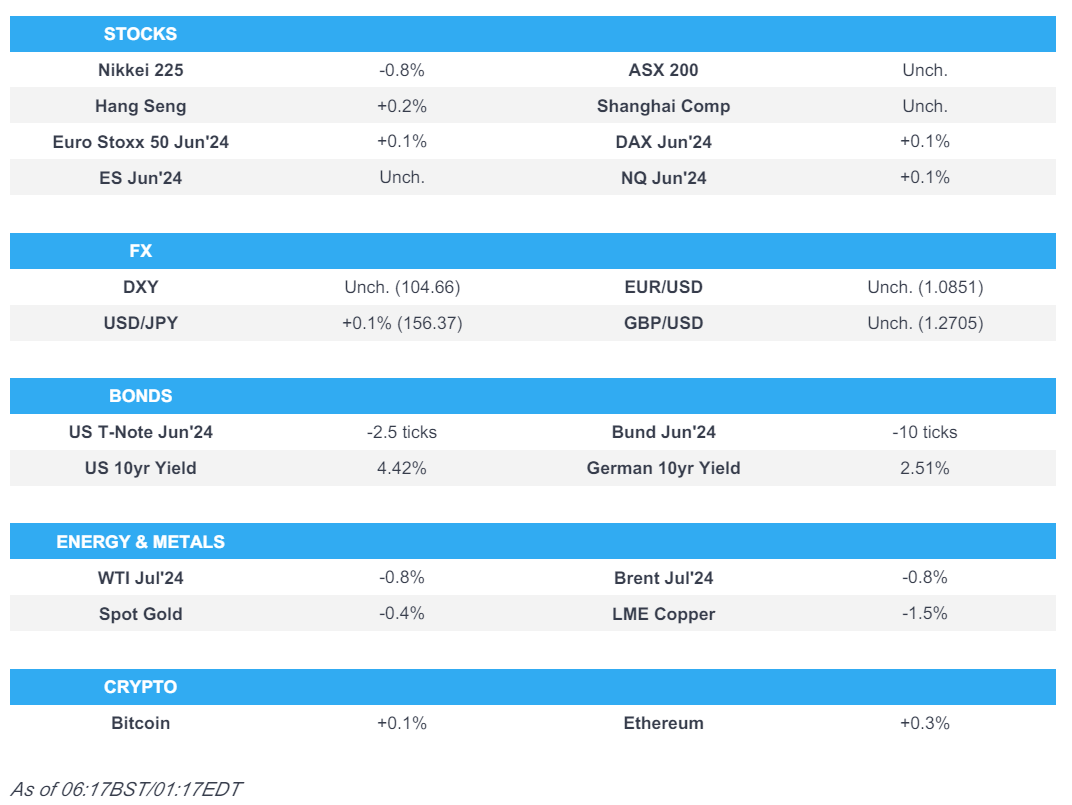

Market Snapshot

- S&P 500 futures little changed at 5,340.75

- MXAP down 0.2% to 180.88

- MXAPJ up 0.3% to 568.56

- Nikkei down 0.8% to 38,617.10

- Topix down 0.8% to 2,737.36

- Hang Seng Index down 0.1% to 19,195.60

- Shanghai Composite little changed at 3,158.54

- Sensex up 0.3% to 74,199.82

- Australia S&P/ASX 200 little changed at 7,848.14

- Kospi little changed at 2,723.46

- STOXX Europe 600 down 0.3% to 521.14

- German 10Y yield little changed at 2.53%

- Euro little changed at $1.0849

- Brent Futures down 1.5% to $81.66/bbl

- Gold spot down 0.3% to $2,413.00

- US Dollar Index little changed at 104.70

Top Overnight News

- China’s mega banks are urging branch managers to lend to state-owned companies that buy unsold homes, offering a quick show of support for the government’s housing rescue package unveiled last week. BBG

- China signaled it’s ready to unleash tariffs as high as 25% on imported cars with large engines, as trade tensions escalate with the US and European Union. BBG

- New Zealand’s central bank makes a hawkish tweak to its statement, warning that rates may need to stay at present levels for longer than previously envisioned. WSJ

- UK inflation falls by less than anticipated in April, causing markets to dial back expectations for a June BOE rate cut (headline CPI was +2.3% in Apr, a steep fall from +3.2% in Mar but ahead of the Street’s +2.1% forecast. Core came in at +3.9%, down from +4.2% in Mar but above the Street’s +3.6% forecast). RTRS

- White House says a deal to normalize relations between Saudi Arabia and Israel is within reach, but its not clear if Netanyahu will agree to Riyadh’s demands (which include committing to the creation of a Palestinian state and a halt to the war in Gaza). Politico

- The US should lift its “absolutely unfair” ban on the Ukrainian army using American-supplied weapons to strike targets inside Russia, in order to help thwart Moscow’s new offensive, Ukraine’s top national security official has said. FT

- Biden’s approval rating falls to the lowest level in nearly two years (the rating sank to 36%, down from 38% in Apr). RTRS

- US gasoline supplies gained by more than 2 million barrels last week, API data is said to show. That would take total holdings to the highest in eight weeks if confirmed by the EIA today. Crude inventories also rose. BBG

- Fed’s Mester (voter) said expect above-trend growth for the year and keeping rates restrictive is not that big of a risk right now given job market strength. Mester said she raised her estimate of the long-run neutral rate in the last projection and the current level of policy may not be “as restrictive” as it might otherwise have been, while she needs to see a few more months of inflation coming down and is also watching expectations.

- Fed’s Collins (non-voter) said elevated uncertainty continues to be a feature of the economy and cannot overreact to any data point, while she added this is a period when patience really matters and uncertainty is a key factor at this point. Furthermore, she said there are a lot of reasons to think Fed policy is “moderately” restrictive with some impacts still in the pipeline and the neutral rate may be higher at least in the medium term

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly rangebound as global markets brace for the FOMC Minutes and Nvidia earnings. ASX 200 just about kept afloat as strength in the heavy industries picked up the slack from the sluggish consumer and tech sectors. Nikkei 225 underperformed following a retreat beneath the 39,000 level and amid mixed data releases as trade data disappointed but machinery orders topped forecasts and showed a surprise M/M expansion. Hang Seng and Shanghai Comp were somewhat varied as the former mildly resumed its advances with XPeng among the notable gainers in Hong Kong due to its Q2 delivery guidance, while the mainland was contained amid a lack of drivers and lingering trade frictions.

Top Asian News

- RBNZ kept the OCR unchanged at 5.50% as expected, while it noted that monetary policy needs to be restricted and it raised its OCR projections with the OCR seen at 5.61% in September 2024 (prev. 5.60%), 5.54% in June 2025 (prev. 5.33%), 5.40% in September 2025 (prev. 5.15%) and at 2.99% in June 2027. RBNZ said restrictive monetary policy has reduced capacity pressures in the New Zealand economy and lowered consumer price inflation, as well as noted that annual consumer price inflation is expected to return to within the committee’s 1%-3% target range by the end of 2024. RBNZ Minutes noted the committee agreed that interest rates need to remain at a restrictive level for a sustained period to ensure annual headline CPI inflation returns to the 1%-3% target range, while the committee agreed that interest rates may have to remain at a restrictive level for longer than anticipated in the February Monetary Policy Statement to ensure the inflation target is met. Furthermore, the committee discussed the possibility of increasing the OCR at this meeting.

- RBNZ Governor Orr said during the press conference that it would take time for domestic inflation to decline, while he added the economy has a lower potential growth rate and he is unsure if that is temporary. Orr also commented that they have limited upside room for inflation surprises and the OCR track is a central projection not an absolute prediction, as well as noted that they had a real consideration on raising rates at this meeting.

European bourses, (Stoxx 600 -0.3%), are subdued across the board, but within recent ranges as the tone from APAC reverberated into Europe. European sectors are mostly lower, with the breadth of the market fairly narrow; Autos are found at the foot of the pile, after EU car registrations showed a fall in EV market share. Energy is also hampered by broader weakness in the crude complex. US equity futures (ES -0.1%, NQ U/C, RTY -0.2%) are trading tentatively in a catalyst-thin session, with focus on the FOMC Minutes and after-market earnings from Nvidia.

Top European News

- EU New car registrations: +13.7% in April 2024; battery electric 11.9% market share (vs 13% in March), according to acea. EU New Car Registrations by company in April Y/Y: Volkswagen (VOW3 GY) +15.5%. Stellantis (STLAP FP/ STLAM IM) +1.7%. Renault (RNO FP) +11.0%. BMW (BMW GY) +11.5%. Mercedes-Benz (MBG GY) +4.2%. Toyota (7203 JT) +47.3%. Nissan (7201 JT) +14.3%. Ford (F) -9.1%. Tesla (TSLA) +3.0%.

- UK ONS House Price Index (Mar) +1.8% (vs -0.2% in Feb).

- Barclays removed its expectations that the BoE will conduct the first rate cut in June.

FX

- DXY is slightly firmer but is showing mixed performance vs. peers (softer vs. NZD and GBP but firmer vs. CHF and JPY). DXY has caught a recent bid and currently trades near session highs at 104.77.

- EUR is marginally softer vs the Dollar but a session of losses vs. the GBP; In terms of price action for EUR/USD, the pair is currently respecting yesterday’s 1.0842-74 range.

- GBP is firmer in the wake of an unambiguously disappointing inflation report for the BoE. Y/Y measures fell from their priors but came in hotter-than-expected, as such the first full cut is now priced in November vs September pre-release. Accordingly, Cable vaulted to a high of 1.2761, though has since pared almost the entire move amid the recent Dollar strength, although EUR/GBP holds onto losses.

- Antipodeans are mixed vs. the USD with NZD the best performer across the majors post-RBNZ rate decision. The hawkish lean of the release saw NZD/USD spike higher to 0.6152. AUD/USD is a touch softer vs. the USD in quiet newsflow and as copper prices pull back.

- PBoC set USD/CNY mid-point at 7.1077 vs exp. 7.2376 (prev. 7.1069).

Fixed Income

- USTs are softer following the broader dynamics in fixed income markets but to a lesser extent than peers. Today’s FOMC minutes will be parsed for details on what lies ahead for the Fed. Trough thus far at 108.31+ low matched that of yesterday’s but failed to make any headway below that level.

- Gilts are notably lagging peers in the wake of the latest UK inflation release whereby Y/Y measures fell from their priors but came in hotter-than-expected. Gilts gapped lower by over a point, printing a low at 96.83, before stabilising on a 97 handle.

- Bunds were already on the backfoot before subsequently being dragged lower by UK inflation metrics. Jun’24 Bund contract went as low as 130.30, tripping below yesterday’s trough at 130.53.

- UK sells GBP 4bln 4.125% 2029 Gilt: b/c 3.2x (prev. 3.21x), average yield 4.199% (prev. 4.251%), tail 0.6bps (prev. 0.8bps).

- Germany sells EUR 3.283bln vs exp. EUR 4bln 2.20% 2034 Bund: b/c 2.8x (prev. 2.5x), average yield 2.53% (prev. 2.54%) & retention 17.9% (prev. 19.03%)

Commodities

- Crude is lower in a continuation of the recent trend, with prices also pressured by the surprise build in private inventories (Crude +2.5mln vs exp. -2.5mln) ahead of today’s DoEs; Brent July closer to the bottom end of a 81.57-82.63/bbl parameter.

- Precious metals are softer with spot gold subdued amid a lack of notable geopolitical developments in recent days and ahead of FOMC minutes; XAU resides within a USD 2,410.69-2,426.62/oz range.

- A pullback is seen across most base metals following the recent rally, with profit-taking not to be discounted, with 3M LME copper towards the bottom end of a 10,636.50-10,857.50 intraday parameter

- Global crude steel output -5.0% Y/Y; Chinse crude steel output -7.2% Y/Y

- Norway’s April Prelim oil production 1.854mln BPD (vs 1.84mln BPD in March), gas output 10.4bcm (vs 364.5mcm/day in March), according to the Oil Directorate

- China’s Coal Group said that China’s May coal imports are likely to be lower than April’s 42.5mln metric tons

- US Private Energy Inventory Data (bbls): Crude +2.5mln (exp. -2.5mln), Cushing +1.8mln, Gasoline +2.1mln (exp. -0.7mln), Distillate -0.3mln (exp. -0.4mln).

- Commerzbank said it expects Gold price to fall to USD 2300/toz in H2’24; raises forecast for Silver to USD 30/toz (prev. USD 29)

Geopolitics

- US senior official said negotiators are nearing a final set of arrangements for the US-Saudi defence deal and it is ‘pretty much there to do’, while the deal includes a security component and nuclear agreement but the deal is not done and requires more work. The official said elements such as a credible pathway to Palestinian statehood still have to be completed, while the US talked with Israeli officials and reinforced President Biden’s concerns about a Rafah ground invasion. Furthermore, the official said they had a very detailed discussion with Israelis about how to transition to a stabilisation phase in Gaza.

- China’s Foreign Minister Wang said in talks with Iran’s Deputy Foreign Minister that China will continue to strengthen strategic cooperation with Iran, safeguard common interests, and make endeavours for regional and world peace, according to Reuters.

- Russian Foreign Ministry said Russia’s response will not only be political if France sends troops to Ukraine, according to RIA.

- Russian Defence Ministry proposed to change external border of Russian territorial waters in Baltic Sea, via Interfax citing draft bill

US Event Calendar

- 07:00: May MBA Mortgage Applications, prior 0.5%

- 10:00: April Existing Home Sales MoM, est. 0.8%, prior -4.3%

- 10:00: April Home Resales with Condos, est. 4.22m, prior 4.19m

- 14:00: May FOMC Meeting Minutes

Fed speakers

- 09:40: Fed’s Goolsbee Gives Opening Remarks

DB’s Jim Reid concludes the overnight wrap

Markets continued to inch higher yesterday, with the S&P 500 (+0.25%) closing at another all-time high. But even with the new record, there were still clear signs of investor caution ahead of Nvidia’s earnings announcement later today, which is now the main focus for investors. It might seem strange that markets are hanging on the results of a single company, but over recent quarters, the release has become one of the most important events on the macro calendar. Moreover, that status has been justified by the massive moves afterwards, and Nvidia’s previous results in February saw the S&P 500 surge by +2.11% the next day, marking its strongest daily performance in over a year. So this is a pivotal event, and the recent releases have seen reactions that rival the sort of moves taking place after a surprise US jobs report or CPI release.