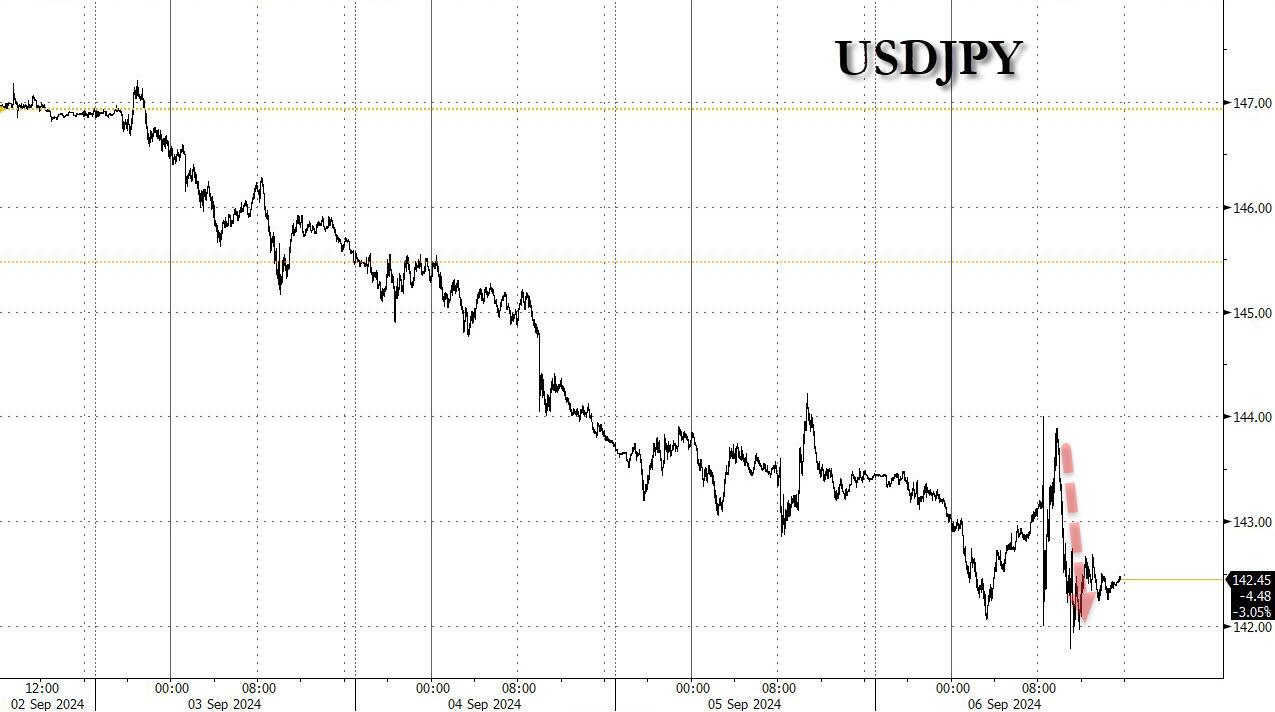

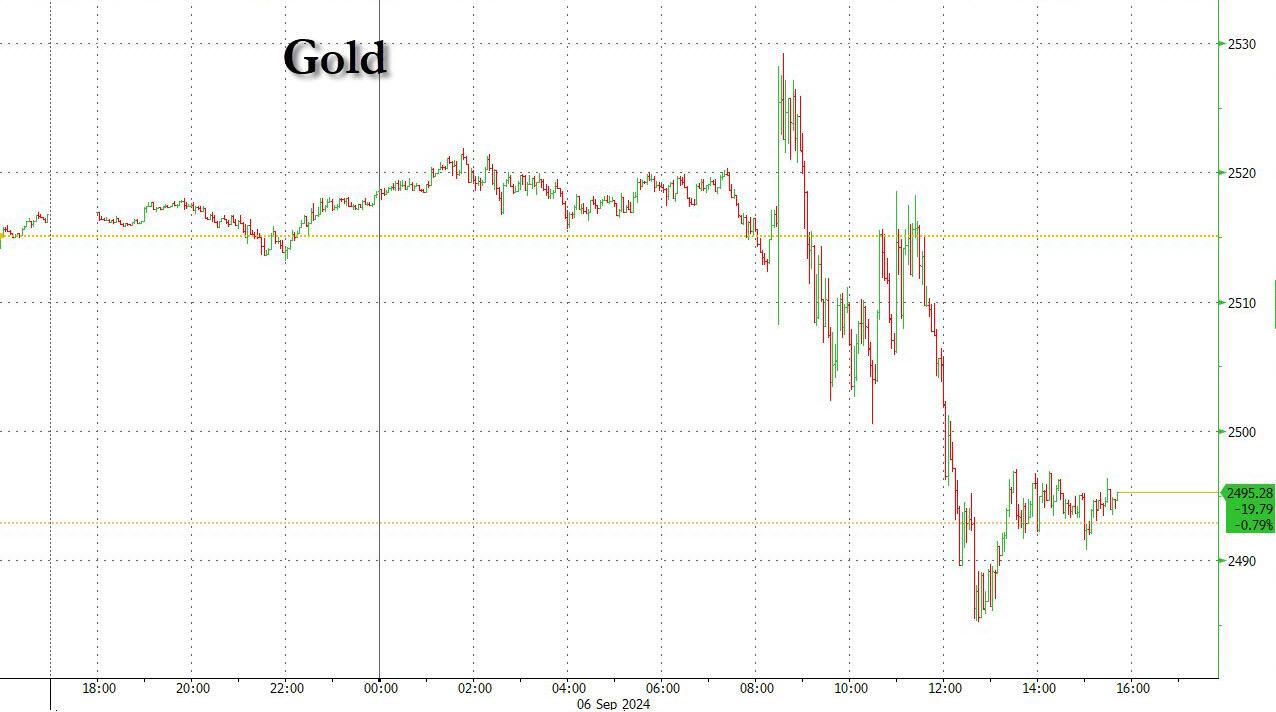

SEPT 6//GOLD CLOSED DOWN $1765 TO $2495.25/SILVER CLOSED DOWN 84 CENTS TO $27.89//PLATINUM CLSOED DOWN $5.60 TO $922.50 WHILE PALLADIUM CLOSED DOWN $24.90 TO $918.60//THE YEN CLOSED DRAMATICALLY UP TO 142.46 THUS BLOWING UP ALL REMAINING YEN CARRY TRADES: THIS FORCES INVESTORS TO BAIL OUT OF ASSETS//A MUST VIEW: ANDREW MAGUIRE LIVE FROM THE VAULT NO 189//JOBS REPORT A TOTAL PHONY BUT IT STILL WAS DISMAL//BUFFET IS UNLOADING MOST OF HIS BANK OF AMERICA STOCK/ ISRAEL VS HAMAS/RUSSIA VS UKRAINE/COVID UPDATES//HEALTHY FOOD ISEAS//COVID UPDATES/VACCINE INJURY/PAUL ALEXANDER//SWAMP STORIES FOR YOU TONIGHT//

323 C HSBC 102 363 H WELLS FARGO SEC 283 523 H INTERACTIVE BRO 8 657 C MORGAN STANLEY 35 661 C JP MORGAN 177 686 C STONEX FINANCIA 3 737 C ADVANTAGE 2 79 880 H CITIGROUP 700 905 C ADM 15

TOTAL: 702 702 MONTH TO DATE: 3,628

JPMorgan stopped 177/702

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2024. CONTRACT: 702 NOTICES FOR 70,200 OZ or 2.1835 TONNES

total notices so far: 3628 contracts for 362,800 Oz (11.284 tonnes)

FOR SEPT:

SILVER NOTICES: 10 NOTICE(S) FILED FOR 50,000 OZ/

total number of notices filed so far this month : 4,678 for 23,390,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $17.65 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ NO CHANGES IN GOLD INVENTORY AT THE GLD:

/ /INVENTORY RESTS AT 862.74 TONNES

INVENTORY RESTS AT 862.74 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $.84 AT THE SLV

NO CHANGES IN SILVER INVENTORY AT THE SLV: ..

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 466.234 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 1849 CONTRACTS TO 128,604 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR STRONG GAIN OF $0.55 IN SILVER PRICING AT THE COMEX ON THURSDAY’S TRADING. WE LOST ZERO NET LONGS WITH THE GAIN IN PRICE. WE HAD A HUGE LOSS OF 660 CONTRACTS ON OUR TWO EXCHANGES. WE HAD AGAIN A HUGE LIQUIDATION OF T.A.S. CONTRACTS DURING THURSDAY’S TRADING//. WE HAD CONSIDERABLE SHORT COVERING BY OUR SPECS WITH THE GAIN IN PRICE. WE HAD A HUMONGOUS 1130 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY ANOTHER HUGE 690 CONTRACT T.A.S ISSUANCE. IN ESSENCE WE LOST 660 CONTRACTS ON OUR TWO EXCHANGES DESPITE THE GAIN IN PRICE. ALL OF THE LOSS IN COMEX OI WAS DUE TO OUR SPREADER T.A.S. LIQUIDATION.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN YESTERDAY. THE ACCUMULATED T.A.S. IS BEING USED TO MANIPULATE PRICES AT THE COMEX NOW EVERY DAY..

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 690 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS BUT TO NO AVAIL. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.55) AND WERE UNSUCCESSFUL IN KNOCKING ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A HUGE LOSS OF 660 TOTAL OI CONTRACTS ON OUR TWO EXCHANGES, WITH ALL OF THE LOSS DUE TO TA.S. LIQUIDATION.

WE HAD A HUGE 1130 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 22.765 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 30,000 OZ QUEUE JUMP//NEW STANDING ADVANCES TO 23.790 MILLION OZ

//NEW STANDING FOR SILVER//SEPT ADVANCES TO 23.790 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI LOSS //HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 690 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 59 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT

TOTAL CONTRACTS for 4 DAYS, total 2661 contracts: OR 13.305 MILLION OZ (665 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 13.305 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL PROBABLY BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 13.305 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1849 CONTRACTS DESPITE OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS:1130 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 22.765 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE 30,000 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR SEPT ADVANCES TO 23.790 MILLION OZ

WE HAVE A HUGE LOSS OF 660 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE GAIN IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 690 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX TRADING//// MASSIVE ATTEMPTED SHORT COVERING FROM OUR SPEC SHORTS WITH THE GAIN IN PRICE THURSDAY/ AND ZERO LIQUIDATION OF LONGS. ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER.

THE NEW TAS ISSUANCE THURSDAY NIGHT (690) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND FOR SURE TODAY., .

WE HAD 10 NOTICE(S) FILED TODAY FOR 50,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 561 OI CONTRACTS TO 520,152 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 9270 CONTRACTS//

WE HAD A small SIZED INCREASE IN COMEX OI (561 CONTRACTS) OCCURRED DESPITE OUR STRONG GAIN OF $18.00 IN PRICE //THURSDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT AT 12.885 TONNES ON FIRST DAY NOTICE FOLLOWED BY THURSDAYS STRONG 1,400 OZ E.F.P. JUMP TO LONDON WHERE THESE BOYS TOOK IMMEDIATE DELIVERY OVER IN LONDON ON A T + 1 BASIS.

NEW STANDING REDUCES TO 11.897 TONNES

/ ALL OF THIS HAPPENED WITH OUR $18.00 GAIN IN PRICE WITH RESPECT TO THURSDAY’S TRADING. WE HAD A VERY STRONG SIZED GAIN OF 12,633 OI CONTRACTS (39.293 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 3202 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 520,152

IN ESSENCE WE HAVE A VERY FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3763 CONTRACTS WITH 9431 CONTRACTS INCREASED AT THE COMEX// AND A GOOD SIZED 3202 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3763 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 1419 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3202 CONTRACTS) ACCOMPANYING THE SMALL SIZED INCREASE IN COMEX OI OF 561 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 3763 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT 12.885 TONNES FOLLOWED BY TODAY’S 1400 OZ E.F.P. JUMP TO LONDON

//NEW STANDING REDUCES TO: /SEPT 11.897 TONNES.

/ 3) SMALL T.A.S. LIQUIDATION WITH ZERO NET LONG SPECS BEING CLIPPED,

4) SMALL SIZED COMEX OPEN INTEREST GAIN 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1419 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

TOTAL EFP CONTRACTS ISSUED: 22,468 CONTRACTS OF 2,246,800 OZ OR 69.88 TONNES IN 4 TRADING DAY(S) AND THUS AVERAGING: 6422 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 4 TRADING DAY(S) IN TONNES 69.88 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 69.88 DIVIDED BY 3550 x 100% TONNES = 1.97% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 69.88 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPTEMBER. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 1849 CONTRACTS OI TO 128,663 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1130 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 1130 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1130 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1849 CONTRACTS AND ADD TO THE 1130 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 719 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 3.30 MILLION OZ OCCURRED WITH OUR $0.55 GAIN IN PRICE WITH ALL OF THE LOSS DUE TO T.A.S. SPREADER LIQUIDATION.

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

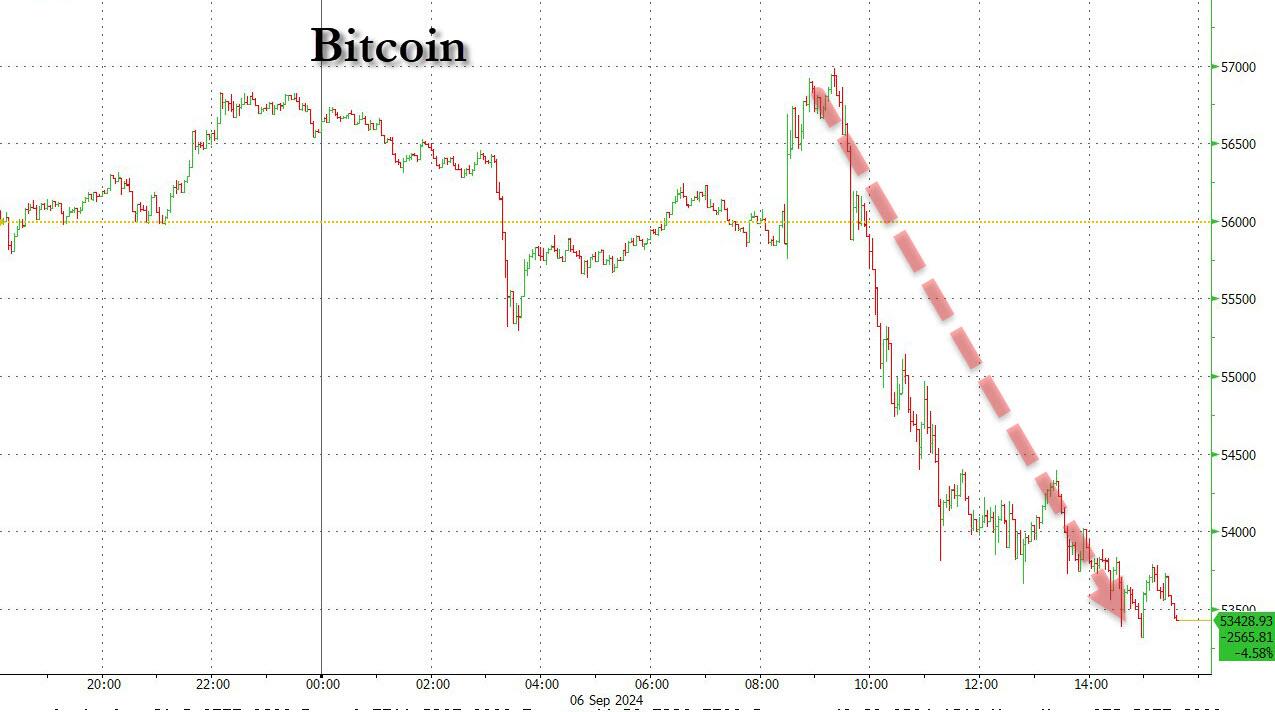

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING/THURSDAY NIGHT

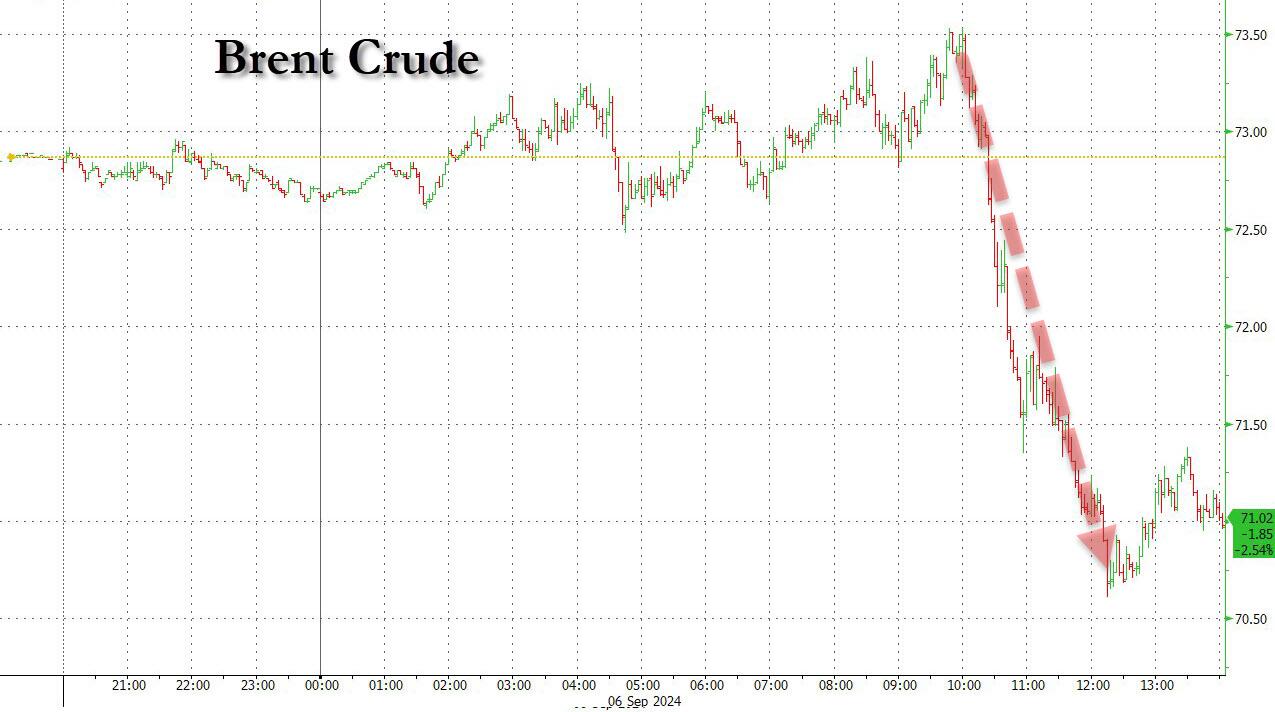

SHANGHAI CLOSED DOWN 22.51 PTS OR 0.81% //Hang Seng CLOSED DOWN 13.04 PTS OR 0.07% // Nikkei CLOSED DOWN 265.62 OR 0.72%//Australia’s all ordinaries CLOSED UP 0.33%///Chinese yuan (ONSHORE) CLOSED UP TO 7,0883 CHINESE YUAN OFFSHORE CLOSED UP TO 7.0938/ Oil UP TO 69.48 dollars per barrel for WTI and BRENT DOWN AT 72.42 Stocks in Europe OPENED ALL RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 561 CONTRACTS TO 511,282 WITH OUR GAIN IN PRICE OF $18.00 WITH RESPECT TO THURSDAY’S TRADING. WE LOST ZERO IN NUMBER OF /T.A.S. CONTRACTS AS SHORTS TRIED TO, THROUGHOUT THE SESSION, COVER WHAT THEY COULD AT MUCH HIGHER PRICES.

THE FED IS THE MAJOR SHORT OF AROUND 148+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS IS SCHEDULED TO HAPPEN LATE SEPT 2024/BEGINNING OF OCTOBER. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER CONTAINMENT.

OUR PHYSICAL LONDONERS ALSO BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT THESE PRICES AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD ZERO T.A.S. LIQUIDATION ON THURSDAY’S HUGE GAIN IN PRICE WITH ZERO LONGS WERE CLIPPED (AS YOU WILL SEE BELOW) BUT WE DID HAVE MAJOR SHORT COVERING. THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF THE SPREADERS // T.A.S DURING THE WEEK IS SURELY DISTORTING COMEX OPEN INTEREST.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE NON ACTIVE DELIVERY MONTH OF SEPTEMBER.… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A GOOD SIZED 3202 EFP CONTRACTS WERE ISSUED: : OCT/DEC3202 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3202 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 3763 CONTRACTS IN THAT 7761 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A SMALL GAIN OF 561 COMEX CONTRACTS..AND THIS VERY FAIR GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR HUGE GAIN IN PRICE OF $18.00/THURSDAY COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AS MENTIONED ABOVE. THE RAIDS ON LAST WEDNESDAY, FRIDAY AND THIS PAST TUESDAY WERE ORCHESTRATED BY THE FRBNY AS WE ARE NOW FINISHED WITH OPTIONS EXPIRY FOR THE OTC/LONDON LBMA BETS ENDING FRIDAY AFTERNOON. DESPITE THE FED’S HUGE SHORT PREDICAMENT THEY STILL HAVE TIME AND ENERGY TO RAID OUR PRECIOUS METALS. SUCH CROOKS!

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT A FAIR SIZED 1419 CONTRACTS. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE (AND SPREADERS LATE IN THE MONTH). THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S AND THIS WEEK’S TRADING//RAIDS

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: SEPT (11.897 TONNES) WHICH IS HUGE FOR A NON DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 44 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 11.897 TONNES.

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $18.00 ////AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE DID HAVE A FAIR GAIN IN OUR TWO EXCHANGES. WE HAD ZERO T.A.S. SPREADER LIQUIDATION. BUT CENTRAL BANK LONGS, SEIZING THE MOMENT, EXERCISED FOR PHYSICAL IN A BIG WAY.

WE HAVE GAINED A TOTAL OI OF 11.703 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPT (12.885 TONNES) ON FIRST DAY NOTICE FOLLOWED BY THURSDAY’S E..F.P. JUMP TO LONDON OF A GOOD SIZED 1400 OZ AS THESE BOYS WERE IN IMMEDIATE NEED OF PHYSICAL GOLD AND THUS TOOK DELIVERY ON THAT SIDE OF THE POND.

//NEW STANDING FOR SEPT REDUCES TO: 11.897 TONNES.

NEW STANDING FOR SEPT: 11.897 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $18.00

WE HAVE REMOVED 9270 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. THIS IS THE LARGEST ADJUSTMENT TO DATE.

NET GAIN ON THE TWO EXCHANGES 3763 CONTRACTS OR 376,300 OZ (11.70

Total monthly oz gold served (contracts) so far this month

3628 notices 362800 oz 11.284 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: nil oz

we have 1 customer deposits

i) Into JPMorgan: 81,226.710 oz oz

total deposits 81,226.710 oz

withdrawals:1

i) Out of Brinks 55,402.961 oz

TOTAL WITHDRAWALS 55,402.961 oz 1.723 tonnes

adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPTEMBER

For the front month of SEPT. we have an oi of 899 contracts having LOST 28 contracts. We had 14 notices filed on Thursday so we LOST 14 contracts or 1400 oz will NOT stand at the comex as these boys were ferried over to London where they are taking immediate delivery of physical gold over there. This is a considerable amount of gold and our bankers must be in trouble.

OCTOBER LOST 543 CONTRACTS DOWN TO 42,159 CONTRACTS

NOVEMBER GAINED another 51 CONTRACTS TO STAND AT 82

DECEMBER, THE BIGGEST DELIVERY MONTH GAINED 460 CONTRACTS TO 410,804.

We had 702 contracts filed for today representing 70,200 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notice issued from their client or customer account. The total of all issuance by all participants equate to 702 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 177 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for SEPT /2024. contract month, we take the total number of notices filed so far for the month (3628) x 100 oz ) to which we add the difference between the open interest for the front month of SEPT 899( CONTRACTS) minus the number of notices served upon today (702 x 100 oz per contract( equals 382,500 OZ OR 11.897 TONNES.

thus the INITIAL standings for gold for the SEPTEMBER contract month: No of notices filed so far (3628 x 100 oz +we add the difference for front month of SEPT (899 X// , OI} minus the number of notices served upon today (702) x 100 oz which equals 382,500 oz (11.897 TONNES)

TOTAL COMEX GOLD STANDING FOR SEPT.: 11.897 TONNES WHICH IS HUGE FOR THIS NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

total pledged gold: 1,780,327.447 oz 55.375 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,037,284.269 OZ

TOTAL REGISTERED GOLD 7,425,642.244 ( 230.96 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,611,592.025 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 5,645,315 oz (REG GOLD- PLEDGED GOLD)= 175.59 tonnes //

END

SILVER/COMEX

SEPT 6/2024

INITIAL

//2024// THE SEPT 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

1022.16 OZ

Delaware

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

nil oz

No of oz served today (contracts)

10 CONTRACT(S) (50,000 OZ)

No of oz to be served (notices)

80 contracts (0.400 million oz)

Total monthly oz silver served (contracts)

4678 Contracts (23.390 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit/

total dealer deposit : NIL oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0 customer deposits:

total customer deposit nil oz

JPMorgan has a total silver weight: 134.996million oz/306.007 million or 44.08%

adjustment:5

a) dealer to customer Asahi 128,720.400 oz

b) dealer to customer Brinks 9827.940 oz

c) dealer to customer CNT 64,203.370 oz

d) dealer to customer Loomis 10,032.35 oz

e) customer tp dealer Manfra: 107,240.400 oz

withdrawals: 1

i) Out of Delaware 1022.12 oz

total customer withdrawals: 1022.12 oz

TOTAL REGISTERED SILVER: 77.637 MILLION OZ//.TOTAL REG + ELIGIBLE. 306.016 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR SEPTEMBER:

silver open interest data:

FRONT MONTH OF SEPT/2024 OI: 90 CONTRACTS HAVING LOST 241 CONTRACT(S).

WE HAD 247 NOTICES FILED ON THURSDAY, SO WE GAINED 6 CONTRACTS OR 30,000 OZ

UNDERWENT A QUEUE JUMP TO TAKE DELIVERY OF SILVER OVER ON THIS SIDE OF THE POND..

THERE MUST BE ENOUGH SILVER OVER HERE.

OCTOBER SAW ANOTHER LOSS OF 40 OF OPEN INTEREST CONTRACTS AND THUS WE HAVE 1371 OPEN INTEREST CONTRACTS FOR OCTOBER.

NOVEMBER SAW ITS ANOTHER GAIN OF 13 CONTRACTS TO STAND AT 22.

DECEMBER SAW A LOSS OF 2042 CONTRACTS UP TO 114,125.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 10 for 50,000 oz

CONFIRMED volume; ON THURSDAY 67,871 strong

To calculate the number of silver ounces that will stand for delivery in SEPT. we take the total number of notices filed for the month so far at 4678 x 5,000 oz = 23.390 MILLION oz

to which we add the difference between the open interest for the front month of SEPT(899) and the number of notices served upon today 10 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT/2024 contract month: 4678 notices served so far) x 5000 oz + OI for the front month of SEPT (899)x number of notices served upon today minus (10)x 5000 oz of silver standing for the SEPT contract month equates to 23.790 MILLION OZ.

New total standing: 23.790 million oz.

There are 77,743 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS//

GLD

SEPT 6 WITH GOLD DOWN $17.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 5 WITH GOLD UP $18.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 4 WITH GOLD UP $3.45 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 3 WITH GOLD DOWN $4.25 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 5,47 TONNES OF GOLD INTO THE GLD/:/ //////INVENTORY RESTS AT 862.74 TONNES

AUGUST 30 WITH GOLD DOWN $31.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD/:/ //////INVENTORY RESTS AT 857.27 TONNES

AUGUST 29 WITH GOLD UP $23.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 28 WITH GOLD DOWN $14.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 27 WITH GOLD DOWN $1.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 26 WITH GOLD UP $9.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD VAPOUR GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 23 WITH GOLD UP $29.70 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER WITHDRAWAL OF 8.88 TONNES OF GOLD VAPOUR GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 857.85 TONNES

AUGUST 22 WITH GOLD DOWN $28.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 9.43 TONNES OF GOLD VAPOUR GOLD INTO THE GLD./ //////INVENTORY RESTS AT 866.70 TONNES

AUGUST 21 WITH GOLD DOWN $1.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER WITHDRAWAL OF 1.73 TONNES OF GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 857.27 TONNES

AUGUST 20 WITH GOLD UP $9.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 4.03 TONNES OF GOLD VAPOUR INTO THE GLD./ //////INVENTORY RESTS AT 859.00 TONNES

AUGUST 19 WITH GOLD UP $3.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 7.19 TONNES OF GOLD VAPOUR INTO THE GLD./ //////INVENTORY RESTS AT 854.97 TONNES

AUGUST 16 WITH GOLD UP $44.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: //////INVENTORY RESTS AT 847.78 TONNES

AUGUST 15 WITH GOLD UP $13,70 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD OUT OF THE GLD//////INVENTORY RESTS AT 847.78 TONNES

AUGUST 14 WITH GOLD DOWN $26.20 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.03 TONNES OF GOLD OUT OF THE GLD//////INVENTORY RESTS AT 845.76 TONNES

AUGUST 13 WITH GOLD UP $3.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//////INVENTORY RESTS AT 849.79 TONNES

AUGUST 12 WITH GOLD UP $30.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ////INVENTORY RESTS AT 846.91 TONNES

AUGUST 9 WITH GOLD UP $10.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 846.91 TONNES

AUGUST 8 WITH GOLD UP $31.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.02 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 844.04 TONNES

AUGUST 7 WITH GOLD UP $1.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.16 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 848.06 TONNES

AUGUST 6 WITH GOLD DOWN $13.10 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD” A WITHDRAWAL OF .57 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 844.90 TONNES

AUGUST 2 WITH GOLD DOWN $9.95 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.58 TONNES OF GOLD OUT OF THE GLD//INVENTORY RESTS AT 845.47 TONNES

AUGUST 1 WITH GOLD UP $9.15 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 846.05 TONNES

GLD INVENTORY: 862.74 TONNES, TONIGHTS TOTAL

SILVER

SEPT 6//WITH SILVER DOWN $.84//NO CHANGES IN SILVER INVENTORY /: .///./// /INVENTORY AT 466.234 MILLION OZ

SEPT 5//WITH SILVER UP $.55//SMALL CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 0.193 MILLION OZ OF SILVER INTO THE SLV/: .///./// /INVENTORY AT 466.234 MILLION OZ

SEPT 4//WITH SILVER UP $.17//SMALL CHANGES IN SILVER INVENTORY A DEPOSIT OF 0.456 MILLION OZ OF SILVER INTO THE SLV/: .///./// /INVENTORY AT 466.427 MILLION OZ

SEPT 3//WITH SILVER DOWN $.74//HUGE CHANGES IN SILVER INVENTORY A DEPOSIT OF 1.278 MILLION OZ OF SILVER INTO THE SLV/: .///./// /INVENTORY AT 465.971 MILLION OZ

AUGUST30//WITH SILVER DOWN $.42//NO CHANGES IN SILVER INVENTORY: .///./// /INVENTORY AT 464.693 MILLION OZ

AUGUST 29//WITH SILVER UP $.37//SMALL CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 0.558 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 464.693 MILLION OZ

AUGUST 28//WITH SILVER DOWN $0.76//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 2.301 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 465.281 MILLION OZ

AUGUST 27//WITH SILVER DOWN $0.03//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 2.921 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 462.959 MILLION OZ

AUGUST 26//WITH SILVER UP $0.23//SMALL CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 45,000 OZ OUT OF THE SLV. .///./// /INVENTORY AT 465.880 MILLION OZ

AUGUST 23//WITH SILVER UP $0.72//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 1.506 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 465.925 MILLION OZ

AUGUST 22//WITH SILVER DOWN $0.44//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 0.943 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 468.344 MILLION OZ

AUGUST 21//WITH SILVER $0.03//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 1..552 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 468.344 MILLION OZ

AUGUST 20//WITH SILVER $0.24//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 1.369 MILLION OZ FROM THE SLV. .///./// /INVENTORY AT 466.792 MILLION OZ

AUGUST 19//WITH SILVER $0.39//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 1.506 MILLION OZ FROM THE SLV. .///./// /INVENTORY AT 465.423 MILLION OZ

AUGUST 16//WITH SILVER $0.49//NO CHANGES IN SILVER INVENTORY: .///./// /INVENTORY AT 466.929 MILLION OZ

AUGUST 15//WITH SILVER $1.14//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.186 MILLION ON INTO THE SLV.///./// /INVENTORY AT 466.929 MILLION OZ

AUGUST 14//WITH SILVER DOWN $0.40//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 13//WITH SILVER DOWN $0.19//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 12//WITH SILVER UP $.37//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 9//WITH SILVER DOWN $.03//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 8//WITH SILVER UP $.70//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 3.241 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 7//WITH SILVER DOWN $0.27//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.552 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 6//WITH SILVER UP $0.05//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 458.851 MILLION OZ

AUGUST 2//WITH SILVER DOWN $0.01//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 1.243 MILLION OZ OF SILVER OUT OF THE SLV ///./// /INVENTORY AT 460.961 MILLION OZ

AUGUST 1//WITH SILVER DOWN $0.46//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.608 MILLION OZ OF SILVER VAPOUR INTO THE SLV///./// /INVENTORY AT 462.204 MILLION OZ

CLOSING INVENTORY 466.243 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

end

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY//BILL HOLTER:

While the resilience of gold and silver prices puzzles western investors, the Asian hegemons take a different view and Russia is now investing her surplus oil revenue in gold

While gold and silver are yet to break into new high ground, the resilience of gold this week has been remarkable for its firm undertone, just under its all-time high. And silver is showing signs of bottoming out after a decent correction. In European trade this morning, gold was $2518, up $15 from last Friday. At $28.80, silver was down just 5 cents. Volumes in both Comex contracts were moderate.

Comex Open Interest declined in gold to little more than its long-time average, a healthy development. In silver, Open Interest is considerably below the long-term average. These are our next charts.

In both cases, when Open Interest declines, prices don’t decline much with it. Clearly, attempts by the shorts to reduce their liabilities are failing, as the next chart for the financial position of the Swap category in the gold contract demonstrates:

Despite the fall in Open Interest from a recent high of 598,013 contracts on 18 July, the Swaps (mostly bullion bank trading desks) have record gross and net liabilities, shouldered between 19 longs and 26 shorts. That’s a combined loss on the short side averaging $77.4 billion between 26 traders, averaging nearly $3bn each. This is why I think that a higher gold price could lead to one or more traders needing rescuing.

Asian and central bank demand continues apace, keeping London and Comex short of physical liquidity. Comex was never intended to be a delivery market, yet according to my records, since late November 2020 when stand-for-deliveries became a common occurrence having been rare, some 2,136 tonnes of gold have been stood for delivery, and 24,072 tonnes of silver. These are staggering figures, and do not include exchanges for physical, a significant but unknown portion of which were swapped for London forward contracts and then delivery taken.

The premium on gold in Shanghai today is minimal. But this is not where the big buyers in the form of banks operate, only buying in Shanghai when there is a discount. The banks back their gold account liabilities by buying physical gold in western markets, or by not withdrawing purchased bullion from the Shanghai Gold Exchange.

For Chinese banks and investors, the strength in the yuan has been keeping the gold price down, and lower yuan interest rates make gold even more attractive. The yuan’s chart (invested scale) is below:

It appears that Russia is adding to her gold holdings as well. According to the Russian news agency Interfax, Russia is increasing her purchases of gold to RUB 8.2bn daily, the equivalent of over 36,000 ounces financed by a surplus in oil revenues. This is a clear signal that Russia prefers holding gold to fiat currencies, a view echoed by China with respect to the dollar.

And lastly, an update on the technical chart, which has gold consolidating at the upper trend line of a bullish flag

:

3.CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

Russia is going to buy gold exponentially and sell lots of oil

(Jerusalem post)

* * *

end

4. OTHER GOLD COMMENTARIES/LIVE FROM THE VAULT: TODAY ANDREW MAGUIRE live from the vault

no 189

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES: DIAMONDS

the cost of collectibles, wines, watches diamonds collapse as these goods are just too great for everybody

The downturn in the diamond market is nothing short of breathtaking. Prices are in free fall as cash-strapped consumers have been shunning luxury goods, grappling with failed Bidenomics that unleashed an inflation storm and resulted in high interest rates. Compounding the issue, the rising demand for lab-grown diamonds has pressured the prices of natural stones.

According to Bloomberg data, citing the Diamond Standard Index, diamond prices have plunged to the lowest on record, with data going back to early 2002. The index has lost 45% of its value since March 2022.

Since diamonds are a consumer-driven market, the fierce bear market in prices signals that the industry is in trouble, as well as signals that low/mid-tier consumers are in trouble. In less than a week, Dollar General and Dollar Tree, with tens of thousands of stores nationwide, have warned that their core customer bases are under pressure. These discount retailers offer a unique glimpse into consumer sentiment that is not manipulated by government statisticians at the BLS.

De Beers, the world’s largest diamond producer by value, recorded its worst year in two decades earlier this summer. Its parent company, Anglo American, recently announced plans to divest and spin off its 85% stake in the diamond subsidiary.

CEO Duncan Wanblad acknowledged the challenges De Beers has faced. In May, he said, “It is sitting at the bottom of a cycle. That cycle is more macroeconomic than fundamental.”

The diamond and luxury goods industry was a major beneficiary of the helicopter money the US government dished out during the Covid era. However, as soon as pandemic savings dried up and the Biden-Harris team ignited an inflation storm through failed Bidenomics, consumers had to quickly dial back spending on diamonds, Rolexes, handbags, and Gucci loafers.

There has also been downward pressure from Gen Z’s distaste for marriage. Some millennials are too broke to afford natural stones and have gravitated to lab-grown diamonds. In recent years, the rapid growth of artificial stones has pressured natural stone prices.

In addition to a collapse in diamond prices, the Bloomberg Subdial Watch Index, which tracks prices for the 50 most-traded watches by value on the secondary market, has sunk nearly 18% in 24 months.

Looking at wine prices on the London International Vintners Exchange, the Live-ex Fine Wine 50 index has plunged below Covid lows, with a 5-year return of around 8.4%.

Let’s not forget that classic automobiles, such as Packard Roadsters and Ford Thunderbirds, or mainly classics before the 1960s, are not selling well at auctions. Baby boomers overpaid for these vehicles, while GenXers and millennials instead seek cars from the 1980s, 1990s, and 2000s, such as 911 Turbos. So much for the old folks trying to dump their 1930s Packards at auction bought a decade or two ago. The market is no longer there.

Overall, this note offers a view into consumer health. Low—and mid-tier households are certainly feeling recession-like pressures. Next up, a pullback in spending from higher income households?

END

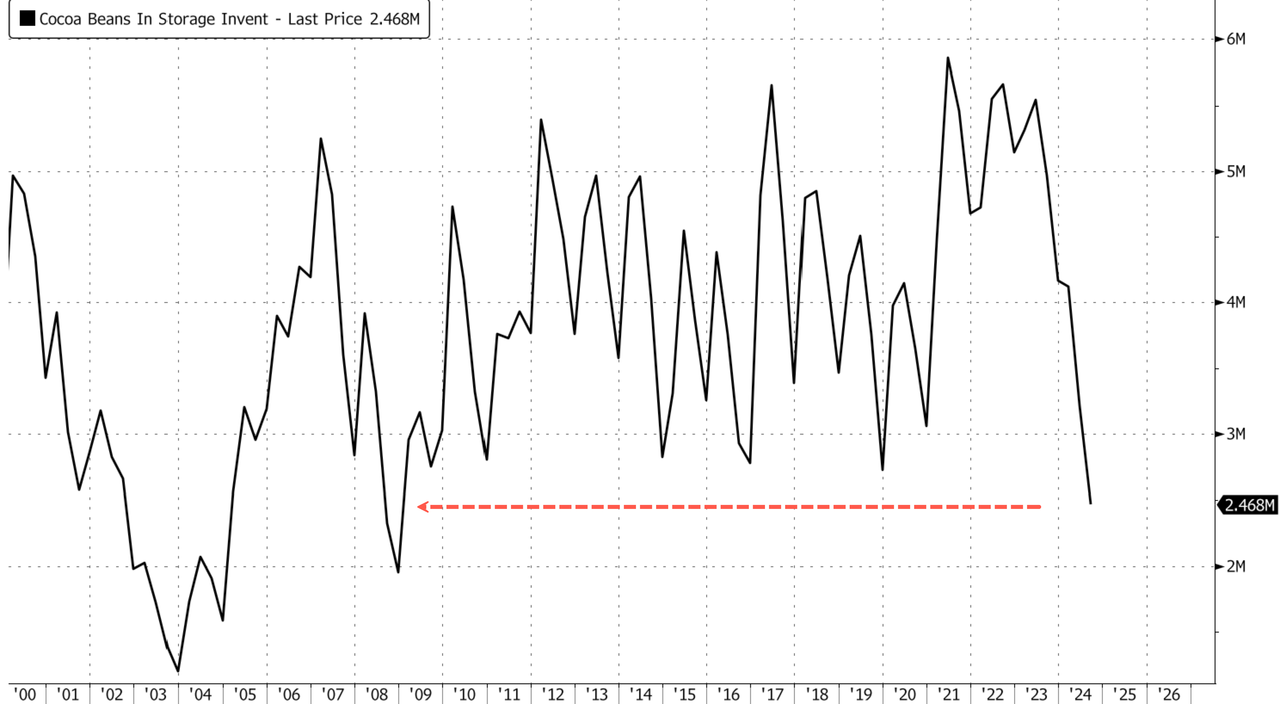

Global Cocoa Deficit Deeper Than Expected, US Stockpiles Hit 2009 Lows

Thursday, Sep 05, 2024 – 09:55 PM

Following a massive price surge in cocoa prices in New York earlier this year, where prices topped nearly $12,000 per ton before bottoming out in the low $7,000s and resulting in what technical analysts say is a triangle pattern, prices are expected to stay rangebound as compression indicates a major move nears.

Bloomberg cites new data from the International Cocoa Organization that says demand will exceed production by 462,000 metric tons. That’s about 5.2% more than the ICCO’s May forecast of a 439,000-ton deficit. This is a muchlarger shortage than the initial outlook published in February.

In the Friday report, ICCO wrote that global cocoa supplies remain depressed due to “adverse weather conditions, aged trees, pests and diseases that affected production in major cocoa areas during the season under review.”

Global cocoa production this season is 4.33 million tons, 2.9% below ICCO’s previous forecast. Grinding estimates are expected to be 2.1% lower, at 4.75 million tons.

Bloomberg noted, “New York futures are up around 80% this year as poor harvests in West Africa curbed supplies, though prices have pared back from record highs. The region’s cocoa industry is still grappling with lasting issues like crop disease, and new trees take at least three years to reach fruit-bearing maturity. That’s constraining how quickly production can ramp up to ease the shortage.”

New York bean prices are locked in a triangle formation of compressing price action, indicating that a big move might be on the horizon.

New data from ICE exchange-monitored warehouses shows US cocoa stockpiles have slumped to the lowest levels since early 2009.

Meanwhile, candy companies such as Hershey have been pushing higher cocoa costs to customers. The PA-based company has already slashed its sales and earnings outlook for the year as shoppers have decreased purchases of higher-priced chocolates and candies. In other words, demand destruction has emerged.

Let’s not forget that oil trader Pierre Andurand remains bullish on the view that the stocks-to-grinding ratio for the world at the end of the year will be at its lowest ever “and potentially run out of inventories late in the year.”

6 CRYPTOCURRENCY NEWS

END

ASIA TRADING/FRIDAY MORNING/THURSDAY NIGHT

SHANGHAI CLOSED DOWN 22.51 PTS OR 0.81% //Hang Seng CLOSED DOWN 13.04 PTS OR 0.07% // Nikkei CLOSED DOWN 265.62 OR 0.72%//Australia’s all ordinaries CLOSED UP 0.33%///Chinese yuan (ONSHORE) CLOSED UP TO 7,0883 CHINESE YUAN OFFSHORE CLOSED UP TO 7.0938/ Oil UP TO 69.48 dollars per barrel for WTI and BRENT DOWN AT 72.42 Stocks in Europe OPENED ALL RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.0883

OFFSHORE YUAN: UP TO 7.0938

SHANGHAI CLOSED DOWN 22.81 PTS OR 0.81 %

HANG SENG CLOSED DOWN 13.04 PTS OR 0.07%

2. Nikkei closed DOWN 265.62 PTS OR 0.72%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 101.02 EURO FALLS TO 1.1103 DOWN 7 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +0.851 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 143.06…… JAPANESE YEN NOW RISING AS WE HAVE NOW REACHED THE COLLAPSING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.1648/Italian 10 Yr bond yield DOWN to 3.5723 SPAIN 10 YR BOND YIELD DOWN TO 2.973%

3i Greek 10 year bond yield DOWN TO 3.179

3j Gold at $2515.40//Silver at: 28.77 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 69/ 100 roubles/dollar; ROUBLE AT 89.90

3m oil into the 69 dollar handle for WTI and 72 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 143.06/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.851 % STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8427 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9357 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.703 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 3.990 DOWN 4 BASIS PTS/

USA 2 YR BOND YIELD: 3.727 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 33.99…

10 YR UK BOND YIELD: 3.910 DOWN 4 PTS

10 YR CANADA BOND YIELD: 2.971 DOWN 4 BASIS PTS

5 YR CANADA BOND YIELD: 2.819 DOWN 2 PTS.

2a New York OPENING REPORT

Futures Slide Ahead Of Critical Jobs Report

Friday, Sep 06, 2024 – 08:12 AM

Futures are set to end a dismal first week of September lower, with tech again under pressure ahead of a very important jobs report. As of 8:00am, S&P futures are down 0.6% set for a 4th straight day of declines following a sudden dump around the European open; Nasdaq futures slide 1% as NVDA slides more than 2% pre-market while Broadcom also weighed on tech stocks after falling 9% after delivering a disappointing sales forecast. Bond yields are also lower, with the 10Y at 3.70%, the lowest since June 2023 as 2-, 5-, 10- yr yields are 3bp, 3bp, 3bp lower. The Bloomberg dollar index was lower for third day while the yen continues to surge on expectations today’s NFP will come in below expectations and greenlight a 50bps rate cut. Commodities are mixed with base metals higher and oil flat. Today, all eyes on the NFP print at 8.30am ET. Consensus expects 165k jobs being added, with unemployment dropping to 4.2% (our full preview is here). Fed’s Williams and Waller will speak this afternoon before the blackout period begins.

In premarket trading, Broadcom weighed on tech stocks as it falls 7% after the chipmaker gave a revenue forecast that’s seen as disappointing. Other chip stocks are down in sympathy (NVDA -1.3%, AMD -0.9%). US Steel is up 2% after Cleveland-Cliffs’s top executive said he’s still in the market for his rival’s assets. Here are other notable premarket movers:

Bowlero jumps 12% after the operator of bowling centers reported revenue for the fourth quarter that came in above the average analyst estimate.

DocuSign ticks 1% lower after the e-signature company reported billings growth that analysts viewed as weak.

Mobileye slips 2% after Bloomberg reported Intel is considering options for its stake in the automated driving systems provider.

Planet Labs slumps 9% after the Earth-imaging company’s revenue forecast for the current quarter fell short of Wall Street expectations.

Samsara rises 4% after the application software company raised its full-year forecast.

Smartsheet climbs 4% after the software company reported second-quarter results that beat expectations and raised its full-year forecast for adjusted earnings.

UiPath rises 8% after the software company’s full-year revenue forecast came in ahead of estimates.

Friday’s jobs report will help the Fed decide whether the US economy is heading for a soft landing or a recession after a week of mixed numbers that whipsawed markets. Swap traders are fully pricing in 25 basis points of cuts when Fed officials meet in two-weeks time, with a roughly 35% chance of a 50 basis-point reduction.

“There’s likely to be volatility in markets as we work through whether or not we can actually have a soft landing,” said Brent Schutte, chief investment officer at Northwestern Mutual Wealth Management Co. “Investors need to be ready for more volatility, based upon a transition from a rate-hike cycle to a rate-cut cycle.”

As noted in our preview (link here), economists expect today’s report will show a bounce in hiring and a tick lower in the unemployment rate in August, marking a stabilization after July. Payrolls probably rose by 165,000 last month following July’s 114,000 increase, according to the median estimate in a Bloomberg survey of economists. Unemployment probably edged down to 4.2%. “Risk markets are sensitive to growth dynamics rather than to interest rates right now, said Bilal Hafeez, chief executive officer and head of research at Macro Hive. “If we were to see a weak number, risk markets such as equities will take that badly.”

Europe’s Stoxx 600 dropped 0.3% to the lowest in 3 weeks, but was off the lows; even so, the index is headed for the biggest weekly decline in almost a year. A key measure of euro-zone wage growth eased, proving further assurance to ECB officials seeking to lower interest rates next week. Should inflation continue to abate, borrowing costs will be lowered every quarter until they reach 2.5%, according to a Bloomberg survey. Here are the biggest movers Friday:

InPost surges as much as 8.9%, the best performance in Stoxx Europe 600 Index, as improving profitability in France and the UK helped the Polish parcel-locker operator beat 2Q expectations

Sectra gains as much as 10%, reaching a record high, after the Swedish medical imaging and cybersecurity firm reported its latest earnings, which included a 10% beat to 1Q Ebitda

Elis declines as much as 17%, the most since March 2020, after it was said to have made offer for US workwear firm Vestis. Bernstein says the offer may weigh on Elis shares in the short term

Raiffeisen falls as much as 7.7% after suffering another setback at its Russian unit after a court in the country froze its shares in the subsidiary, further complicating efforts to sell it

Rubis falls as much as 8.9% after the fuel distributor reported a sharp drop in first-half earnings. Analysts at CIC said the results missed expectations because of non-recurring items

Volvo Car falls as much as 6.1% to their lowest since January as Goldman Sachs says it sees potential for downside depending on revenue development and better opportunities elsewhere

Planisware shares slip as much as 3.8% as shareholder Ardian Group looks to exit its stake in the French software company to capitalize on the gains booked since its IPO earlier this year

Avanza declines as much as 4.1%, the most in a month, after JPMorgan placed the Swedish retail-trading platform and bank on negative catalyst watch leading into its 3Q report

Baloise Holding falls as much as 3.8% after being downgraded by UBS. Analysts say the insurer is fairly valued and argue reports it could be a takeover target are unlikely to come to fruition

Next 15 plunges as much as 53%, the most on record and to a four-year low, after the consultancy firm warned results will be materially below expectations this year

Cairn Homes shares fall as much as 4.6%, the most since December 2022, after the housebuilder confirmed this morning that CEO Michael Stanley has sold 8 million shares in the company

Earlier in the session, Asian stocks were steady, with the regional gauge poised for its worst week since July, amid muted trading as Hong Kong’s market was halted due to a typhoon. The MSCI Asia Pacific Index added 0.1%, erasing earlier losses, but was set to snap three weeks of gains as risk sentiment abates ahead of the US non-farm payrolls report, due later on Friday. The benchmark is headed for a weekly loss of 2.5% as concern was rekindled of overheating in artificial intelligence stocks. TSMC and Commonwealth Bank of Australia were among the biggest winners. Chinese shares in the mainland slid after news that the US administration plans export controls on critical technologies. Hong Kong scrapped trading for the day as Super Typhoon Yagi passed through the region. Persistent economic weakness in China, that prompted several strategists to lower their outlook on the nation’s stocks, has also quelled enthusiasm for riskier assets.

In FX, the Bloomberg Dollar Spot Index drops 0.2% while the yen has risen to the top of the G-10 FX pile, up 0.5% against the greenback. The Swiss franc is a close second with a 0.3% gain. Currency strategists see a strong chance the yen will test its August high versus the dollar if the payrolls data boost bets for a 50 basis-point move. The Japanese currency rose to trade below 143 against the dollar on Friday. The yen “is where the action will be” if there is any surprise in the figures, said Gareth Berry, a strategist at Macquarie Group Ltd. in Singapore.

In rates, treasuries climbed with US 10-year yields falling 3bps to 3.70%. European government bonds have followed suit although bunds showed little reaction to a downward revision to euro-area second-quarter GDP.

In commodities, oil prices were steady, with WTI trading near $69 a barrel; crude oil is poised for the biggest weekly loss in almost a year on concerns about soft demand and ample supply, even as OPEC+ delayed a planned increase in output by two months. Iron ore remained on track for its worst week since March, with few signs of a recovery for China’s steel market. Spot gold is also little changed near $2,518/oz.

Looking to the day ahead, and the main highlight will be the US jobs report for August at830am. In addition, we’ll get July data on German and French industrial production, along with Italian retail sales. The Fed calendar lists Williams (8:45am) and Waller (11am), the last scheduled events before quiet period lasting until the Sept. 18 policy announcement

Market Snapshot

S&P 500 futures down 0.6% to 5,480.75

STOXX Europe 600 down 0.4% to 510.05

MXAP up 0.1% to 181.95

MXAPJ up 0.2% to 564.89

Nikkei down 0.7% to 36,391.47

Topix down 0.9% to 2,597.42

Hang Seng Index little changed at 17,444.30

Shanghai Composite down 0.8% to 2,765.81

Sensex down 1.1% to 81,256.16

Australia S&P/ASX 200 up 0.4% to 8,013.38

Kospi down 1.2% to 2,544.28

German 10Y yield down 4 bps at 2.17%

Euro little changed at $1.1116

Brent Futures up 0.5% to $73.04/bbl

Brent Futures up 0.5% to $73.03/bbl

Gold spot up 0.0% to $2,517.51

US Dollar Index down 0.17% to 100.94

Top Overnight News

Chinese banks have built a $100 billion short against the US dollar using FX swaps to prop up the yuan — handing easy profits to hedge funds along the way. But the trade exposes the nation’s banks to billions of dollars of potential losses. BBG

Japan’s MUFG said it would consider shifting more of its massive securities portfolio into Japanese gov’t bonds if/when 10-year yields reach 1.2%. BBG

Former BOJ governor Kuroda signals the central bank has a lot of tightening to go before hitting a neutral policy rate. BBG

German industrial production falls short of expectations in Jul, dropping 2.4% M/M (vs. the Street’s -0.5% forecast) and raising the risk of recession for the country. WSJ

The ECB probably won’t accelerate easing in response to a weakening economy, a survey found. After next week’s expected 25-bp cut, respondents see quarterly reductions through next September, then rates remaining at 2.5% through 2026. BBG

Nippon Steel proposed a national security agreement to ease US concerns about its takeover bid, Reuters reported. United Steelworkers said the deal needs reworking. Cleveland-Cliffs’ CEO told CNBC he’s still interested in the rival firm’s assets. BBG

Intel is said to be exploring the sale of part of its stake in Mobileye. Intel also weighing options for its network and edge business: BBG

Qualcomm has reportedly explored buying pieces of Intel’s design business: Reuters

Berkshire Hathaway sold about 18.8mln Bank of America common shares for approximately USD 760mln between Sept 3 and Sept 5, according to an SEC filing

Fed’s Goolsbee says employment and inflation data justify starting the easing process soon and proceeding with multiple rate cuts. Market Watch

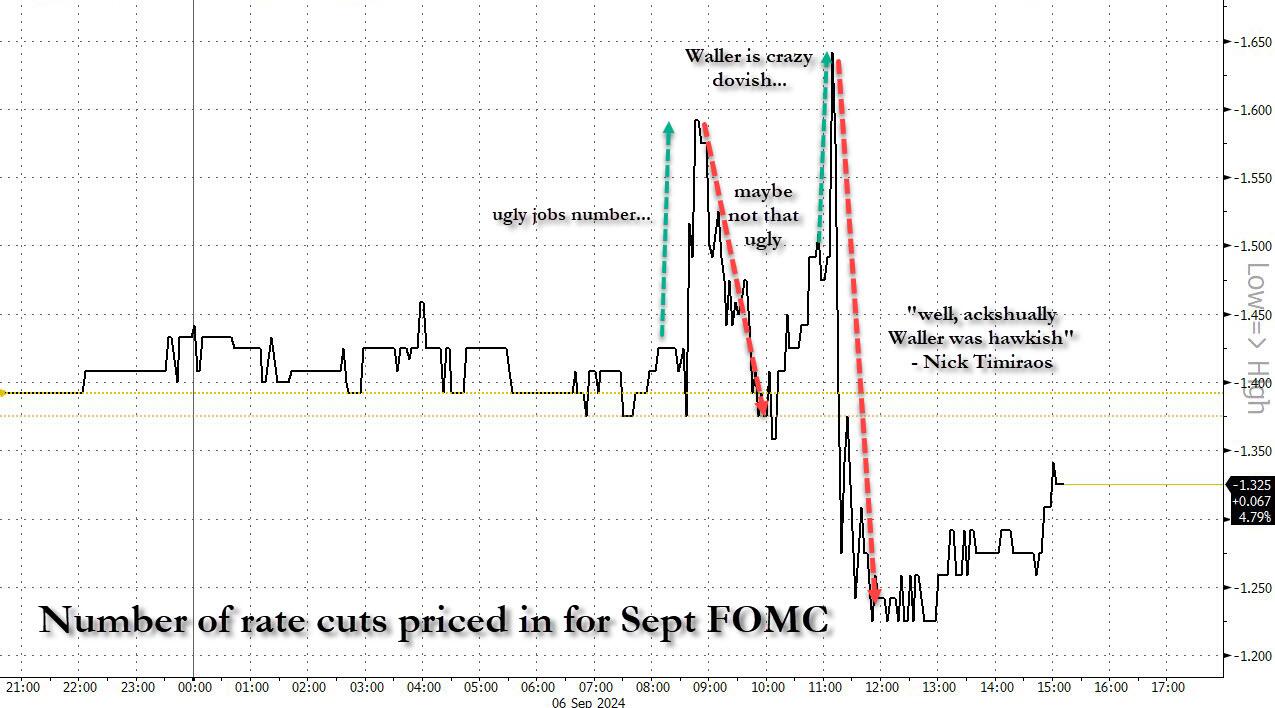

For this morning’s NFP print GIR is looking for headline number of +155k (vs +165k consensus and +114k prior), AHE MoM +.3% (vs +.3% consensus and +.2% prior) and U/E Rate of 4.2% (vs 4.2% consensus and 4.3% prior). After the string of recent weaker economic data points whisper for the print has crept lower to 140kish which is helpful. Vol market pricing in a 120bp move for S&P through the close. Mkt currently pricing in 34bps of cuts for the 9/18 FOMC meeting. We are still firmly in a good (econ data) is good (for stocks) and bad is bad set up. The stock market wants solid economic data and orderly/proactive adjustment cuts in 25bps increments. Powell’s Jackson Hole speech was quite dovish and I think he signaled the September cut is happening (only debate is 25bp or 50bp). If probability of a 50bp cut in Sept grows it will spook the stock market (U/E rate of 4.3% greatly increases the 50bp cut odds). GS GBM

Berkshire Hathaway sold another $760 million of BofA shares since Tuesday, reaping almost $7 billion since the disposals started in July. BBG

A more detailed look at global markets courtesy of Newsquawk

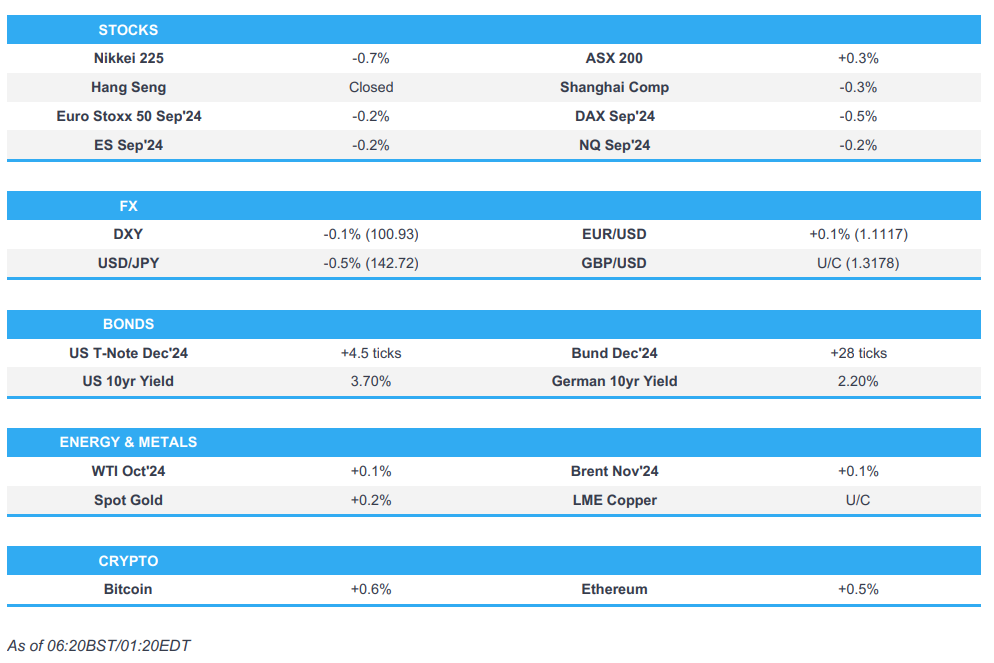

APAC stocks traded without a firm direction following a similar lead from Wall Street, with the tone tentative heading into the much-awaited US jobs report, which could be the determining factor between a 25bps or 50bps cut by the Fed after the central bank shifted its emphasis to the labour market. As a reminder, Fed Vice Chair Williams and Governor Waller will be speaking after the jobs numbers ahead of the Fed’s blackout period set to begin this weekend for the September 18th announcement. ASX 200 just about held onto gains at one point, with Utilities, Financials, Real Estate and Gold names countering the underperformance in Energy and Tech. Nikkei 225 was subdued under the 37k mark (and briefly dipped under 36.5k) with mining and industrial names among the worst performers, whilst Nippon Steel shares fell around 3% amid the ongoing spat with the Biden admin after the US intervened in the Nippon Steel takeover of US Steel amid national security risks. Hang Seng saw its Friday trade scrapped amid a typhoon signal. Shanghai Comp saw subdued trade amid the broader tentative mood across the market and lack of Stock Connect flows. In terms of newsflow, former PBoC Governor Yi Gang offered a bleak prognosis of the Chinese economy, whilst the PBoC drained a net CNY 1.1916tln for the week via open market operations, marking the biggest weekly net cash withdrawal in eight months, according to Reuters calculations.

Top Asian News

Former PBoC Governor Yi Gang, speaking at the Bund Summit, stated that China currently faces weak domestic demand, particularly in consumption and investment. He expressed hope that in the near future, China’s GDP deflator will turn slightly positive. Additionally, Yi hopes that the producer price industry will improve to about zero by the end of this year. He suggests that China should return to a proactive fiscal policy and an accommodative monetary policy.

PBoC injected CNY 141.5bln via 7-day Reverse Repo at a maintained rate of 1.70%.

PBoC drained a net CNY 1.1916tln for the week via open market operations, marking the biggest weekly net cash withdrawal in eight months, according to Reuters calculations.

HKEX confirmed no trading on Friday in securities and derivatives markets due to the issuance of Typhoon Signal No. 8. Stock Connect trading is also suspended for the day. No securities clearing and settlement services will be provided for the day.

Japan Finance Minister Suzuki said there is a need to examine the impact of potential investment tax hikes on the economy and stock prices when asked about the preproposal, according to Reuters.

Toyota (7203 JT) to cut 2026 global EV production to around 1mln units, down 30% from previously announced 1.5mln, via Nikkei.

Former BoJ Governor Kuroda said overnight “A nominal neutral rate, which the Bank of Japan is trying to gradually approach, could be less than 2%,” and “A short-term nominal rate may be less than 2%, maybe around 1.5% or maybe less than that.”

S&P Global Ratings says China Vanke (2202 HK) is downgraded to “BB-” amid weakening sales and margins; outlook Negative

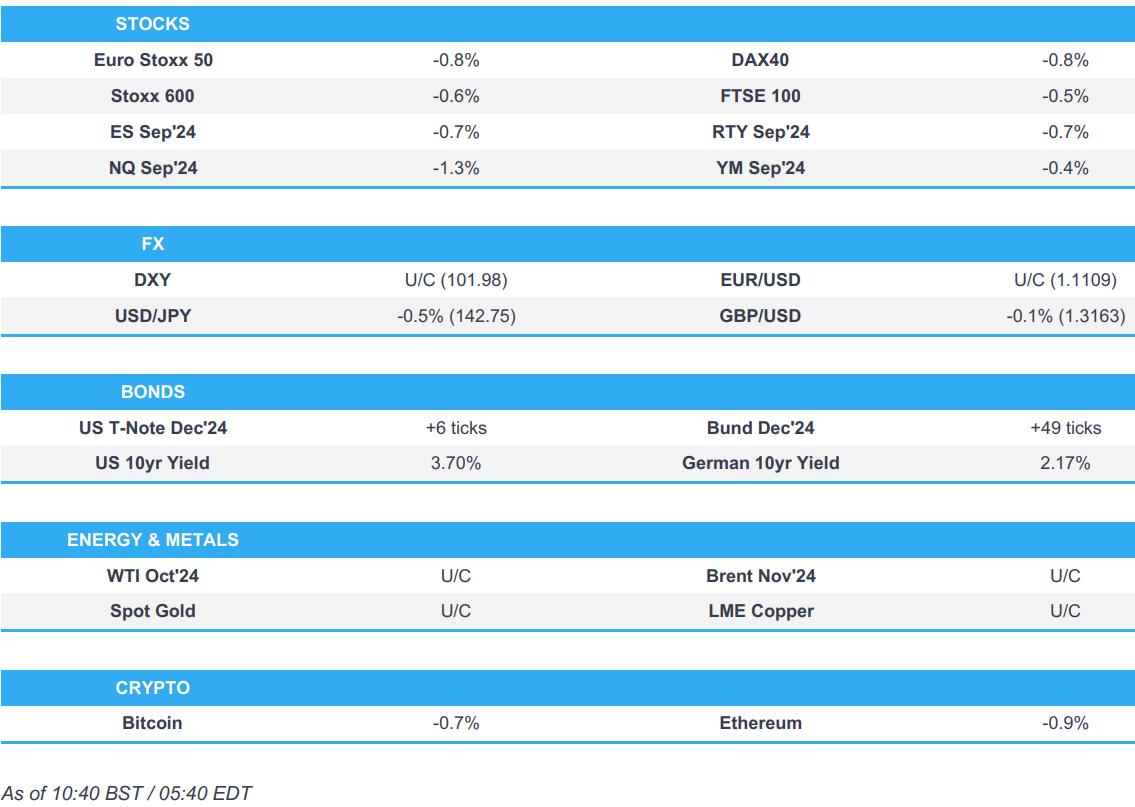

European bourses, Stoxx 600 (-0.3%) opened the session entirely in the red, and sentiment continued to sour as the morning progressed. Indices then found support and traversed worst levels, but with some choppy price action. European sectors hold a strong negative bias; Media takes the top spot, alongside Healthcare. Energy is towards the foot of the pile, hampered by the broader weakness in oil prices. US Equity Futures (ES -0.6%, NQ 1%, RTY -0.5%) are entirely in the red, as traders position themselves ahead of today’s key risk event, the US NFP report.

Top European News

ECB’s Elderson speaks on “Nature-related risk: legal implications for central banks, supervisors and financial institutions”; not pertinent to monetary policy.

FX

DXY is flat ahead of the much-awaited August NFP report, where the headline figure is expected to print at 160k. Should the release come in soft, the YTD low from August 27th sits at 100.51.

EUR/USD is sitting just above the 1.11 mark with not much follow-through from yet more soft German data and the appointment of Barnier as French PM. Upside sees the late-August peak at 1.1201, downside sees yesterday’s low at 1.1074.

Flat trade for GBP vs. the USD and EUR, with UK-specific newsflow quiet today. Cable did briefly take out yesterday’s 1.3186 high but is ultimately struggling to move back onto a 1.32 handle

JPY the best performer across the majors after gaining ground vs. the USD in early European trade. No clear fundamental driver behind the move, but comments from ex-BoJ Governor Kuroda that the short-term nominal rate may be less than 2%, could be a factor. USD/JPY has slipped from an overnight peak at 143.48 to a current session low at 142.07.

Antipodeans are mildly diverging. AUD is a touch softer vs. the USD but with AUD/USD near the mid-point of the week’s 0.6685-0.6794 range. Similar price action for NZD/USD with the pair contained within this week’s 0.6169-0.6299 band.

PBoC set USD/CNY mid-point at 7.0925 vs exp. 7.0927 (prev. 7.0989)

Fixed Income

USTs are bid but not to quite the same extent as European peers after the pronounced two-way action seen on Thursday’s data points and as participants await today’s NFP report. USTs are holding around 115-00+ which marks the December contract high and is just three ticks shy of the September contract peak from early August.

Bunds are firmer and above Thursday’s ADP-driven 134.29 best to a fresh 134.61 WTD peak. If the upside continues, resistance features at 134.93 before the figure and then the contract high of 135.66.

Gilts are also benefiting from the general risk tone. Gilts eclipsed the 100.00 mark with nothing of note now until the 100.30 contract high from the 14th of August.

Commodities

Crude was initially firmer, benefiting from the weaker Dollar. Since, oil turned lower, in-fitting with the general risk tone and as markets await US NFP. Brent’Nov currently around USD 72.75/bbl.

Spot gold is little changed and in a narrow range but one that is entirely above USD 2500/oz.

Base metals are steady and unable to benefit from the softer USD which has been overshadowed by the risk tone deteriorating in the European morning.

Kazakhstan expects a significant reduction in oil production during planned repair period at Kashagan oil field (400k BPD) in October.

Citi sees the OPEC+ unwind delay and ongoing geopolitics and financial positioning providing price support at USD 70-72/bbl in Brent. Citi recommends selling on a bounce toward USD 80/bbl Brent, as it looks ahead to move down to the USD 60/bbl range in 2025 as a sizeable market surplus emerges.

Goldman Sachs pushed back their end-2024 copper price target of USD 12,000/t to after 2025 and lowered the 2025 aluminium price forecast to USD 2,540/t (from USD 2,850/t).

Citi maintains 0-3-month price forecasts for copper at USD 9,500/t, aluminium at USD 2,500/t, and zinc at USD 2,800/t; “We reiterate our cautious outlook for the base metals complex until after the US election when we expect more clarity on US and China policy and improving manufacturing sentiment as Fed rate cuts progress.” (Newswires)

Indian gov’t is reportedly considering cutting diesel and petrol prices, via Reuters citing India Today sources.

BofA says that fundamentals for Tin remain solid and sees prices rising to an average of USD 37k/ton by 2026 vs. prev. view of USD 32.5k/ton.

Geopolitics

US Secretary of State Blinken said 90% of the Gaza ceasefire agreement is agreed upon, but critical issues remain where there are gaps; Incumbent on both parties to get to yes on remaining issues.

“The Israeli army withdraws from Jenin and its camp after 10 days of military operations”, according to Sky News

US event calendar

08:30: Aug. Change in Nonfarm Payrolls, est. 165,000, prior 114,000

Aug. Change in Private Payrolls, est. 140,000, prior 97,000

Aug. Unemployment Rate, est. 4.2%, prior 4.3%

Aug. Underemployment Rate, prior 7.8%

Aug. Labor Force Participation Rate, est. 62.7%, prior 62.7%

Aug. Average Weekly Hours All Emplo, est. 34.3, prior 34.2

Aug. Average Hourly Earnings MoM, est. 0.3%, prior 0.2%

Aug. Average Hourly Earnings YoY, est. 3.7%, prior 3.6%

Aug. Change in Manufact. Payrolls, est. -2,000, prior 1,000

DB’s Jim Reid concludes the overnight wrap

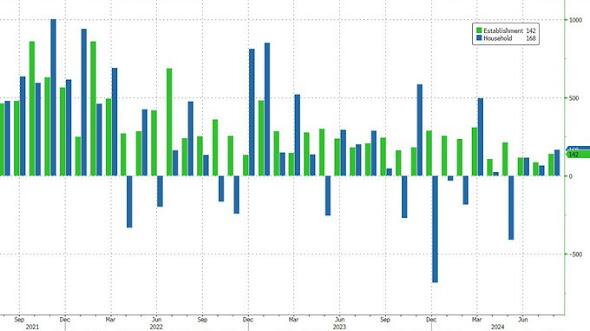

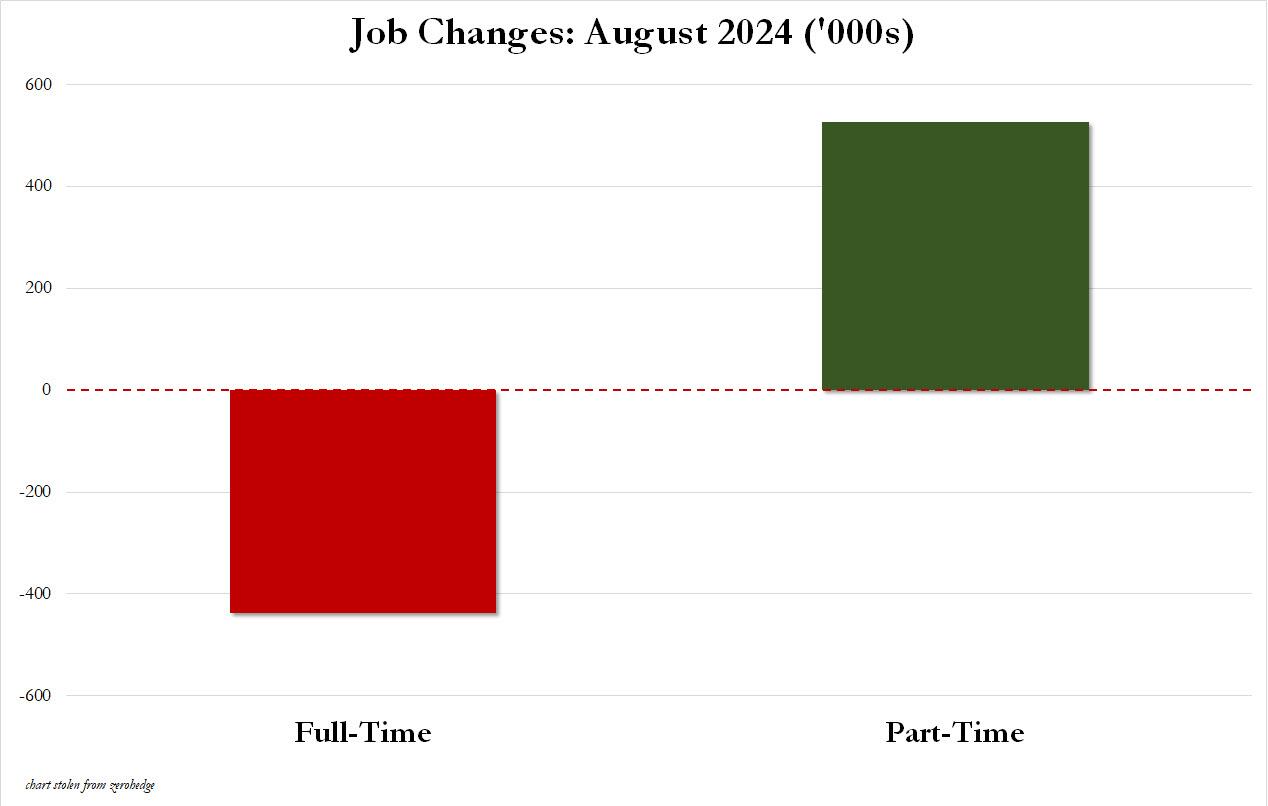

After much anticipation, we have finally arrived at the latest US jobs report day, which is of crucial importance as the Fed decides how much to cut rates this month. It was only five weeks ago that the last jobs report underwhelmed, with payrolls growth down to just +114k alongside negative revision to the previous couple of months. So the big question today is whether that disappointing report was just a blip, or was it the start of a more serious deterioration.

That last report triggered significant market turmoil, and led investors to immediately dial up the likelihood that the Fed would start cutting rates with a 50bp move. However, it’s also worth noting that the turmoil last month came on the back of several other factors, including the BoJ’s hike that week (hence an unwinding of the yen carry trade) along with a very underwhelming ISM manufacturing print the previous day. So the downside surprise in the jobs report was running into a very tough context. By contrast, the data over the weeks since has been a lot more mixed, with plenty for both sides of the debate to focus on.

On the bright side, yesterday brought a further decline in the weekly initial jobless claims, which is one of the timeliest indicators we get on the state of the US labour market. They fell to 227k (vs. 230k expected) over the week ending August 30, which was an 8-week low. In turn, that also pushed the 4-week moving average down to 230k, which is a 12-week low. Bear in mind that four weeks earlier, the 4-week moving average stood at 241k, so that’s seen a clear improvement in the last month. On top of that, we also found out that the ISM services index remained in the expansionary territory in August at 51.5 (vs. 51.4 expected). So again that points away from a sharper downturn.

That said, yesterday also brought some more negative prints. In particular, the ADP’s report of private payrolls for August fell to just 99k (vs. 145k expected). That’s the lowest it’s been since January 2021, and it was also a 5th consecutive monthly decline for that measure. And of course, the previous day we had the JOLTS report for July, where job openings fell to a three-and-a-half year low.

In terms of what to expect today, DB’s US economists are forecasting payrolls rose by +150k in August, which assumes that we get a rebound from the weather issues from last month’s report. Similarly for the unemployment rate, they see that coming down from 4.3% last month to 4.2%. Their take is that some bounce back in the labour market data would support their baseline view that the Fed should start cutting in 25bp increments. But if the jobs report is weaker than expected, then that could motivate a more aggressive start to rate cuts, with a 50bps move in September on the table. We’ll hear from the Fed’s Williams and Waller today, but the blackout period begins tomorrow ahead of the next meeting, so today is the last opportunity we’ll get to hear from Fed officials before their decision.

Going into the report, markets slightly dialled back the chance of a 50bp rate cut, which was down to 41% by the close, although it’s ticked up again overnight to 43% as we go to press. That trend yesterday was supported by the stronger ISM services release, which also saw the prices paid component rise to 57.3 (vs. 56.0 expected). However, the total amount of rate cuts priced over the next 12 months was little changed at 220bps by the close, and 2yr Treasury yields saw a marginal decline to their lowest in nearly two years (-1.1bps to 3.74%). 10yr yields were down -2.8bps to 3.73%, their lowest since June 2023. Overnight that trend has continued, with the 2yr yield down -1.2bps to 3.73%, whilst the 10yr yield is down a further -1.3bps to 3.71%.

US equities also struggled going into the payrolls release, with the S&P 500 (-0.30%) losing ground for a 3rd consecutive day. So September is continuing to live up to its reputation as the weakest month for the index, with the S&P 500 already down -2.57% since it began. Remember if it does end the month lower, it would be the 5th consecutive September that it’s lost ground now. Those losses also came despite a strong performance for the Magnificent 7 (+1.56%). This was led by Tesla (+4.90%), which outperformed after announcing that it plans to launch its advanced driver assistance system in Europe and China in early 2025. But the equity mood was more downbeat otherwise, with the equal-weighted S&P 500 (-0.61%) and the small cap Russell 2000 (-0.61%) underperforming.

Overnight that weaker trend has continued, with futures on the S&P 500 (-0.09%) and the NASDAQ 100 (-0.38%) both pointing towards further losses. In part, this follows an underwhelming outlook from chipmaker Broadcom after the market close, with its shares down by nearly -7% in after-hours trading. Meanwhile in Asia, the major indices have lost ground as well, with declines for the Nikkei (-0.49%), the KOSPI (-0.84%), the Hang Seng (-0.07%), the CSI 300 (-0.27%) and the Shanghai Comp (-0.23%).