GOLD PRICE CLOSED UP $12.95 TO $2503.20

SILVER PRICE UP $.45 TO $28.34

Gold ACCESS CLOSED $2503.00

Silver ACCESS CLOSED: $28.30

Friday is OTC/London LBMA options expiry which is much bigger than comex.

Bitcoin morning price:$55,241 UP 1529 DOLLARS.

Bitcoin: afternoon price: $56,748 up 8 DOLLARS

Platinum price closing UP $22.80 TO $945.00

Palladium price; UP $30.40 TO $949.00

END

*CANADIAN GOLD: $3394.50 UP 6.30 CDN dollars per oz( * NEW ALL TIME HIGH 3,431.95 CDN DOLLARS PER OZ//AUG 16 2024)

*BRITISH GOLD: 1,914.20 UP 12.97 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1937.75 BRITISH POUNDS/OZ) AUGUST 16/2024

*EURO GOLD: 2,267.46 UP 14.82Euros per oz //* (ALL TIME CLOSING HIGH: 2.276.65 EUROS PER OZ//AUGUST 29 //.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,493.500000000 USD

INTENT DATE: 09/06/2024 DELIVERY DATE: 09/10/2024

FIRM ORG FIRM NAME ISSUED STOPPED

323 C HSBC 22

363 H WELLS FARGO SEC 76

435 H SCOTIA CAPITAL 12

523 H INTERACTIVE BRO 1

624 H BOFA SECURITIES 130

657 C MORGAN STANLEY 19

661 C JP MORGAN 38

686 C STONEX FINANCIA 3

737 C ADVANTAGE 79 41

905 C ADM 3

TOTAL: 212 212

MONTH TO DATE: 3,840

JPMorgan stopped 38/212

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2024. CONTRACT: 212 NOTICES FOR 21,200 OZ or 0.6594 TONNES

total notices so far: 3840 contracts for 38,4000 Oz (11.944 tonnes)

FOR SEPT:

SILVER NOTICES: 56 NOTICE(S) FILED FOR 280,000 OZ/

total number of notices filed so far this month : 4,734 for 23,670,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $12.95 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ NO CHANGES IN GOLD INVENTORY AT THE GLD:

/ /INVENTORY RESTS AT 862.74 TONNES

INVENTORY RESTS AT 862.74 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP .45 AT THE SLV

SMALL CHANGES IN SILVER INVENTORY AT THE SLV: ..A WITHDRAWAL OF 46,000 OZ OF SILVER AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 466.188 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 842 CONTRACTS TO 129,446 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR STRONG LOSS OF $0.84 IN SILVER PRICING AT THE COMEX ON FRIDAY’S TRADING. WE LOST ZERO NET LONGS DESPITE THE LOSS IN PRICE. WE HAD A HUGE GAIN OF 2257 CONTRACTS ON OUR TWO EXCHANGES. WE HAD AGAIN A HUGE LIQUIDATION OF T.A.S. CONTRACTS DURING FRIDAY’S TRADING//. WE HAD CONSIDERABLE SHORT COVERING BY OUR SPECS WITH THE LOSS IN PRICE. WE HAD A HUMONGOUS 1415 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY ANOTHER HUGE 1491 CONTRACT T.A.S ISSUANCE. IN ESSENCE WE GAINED A MONSTROUS 2257 CONTRACTS ON OUR TWO EXCHANGES DESPITE THE LOSS IN PRICE.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN YESTERDAY. THE ACCUMULATED T.A.S. IS BEING USED TO MANIPULATE PRICES AT THE COMEX NOW EVERY DAY..

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON FRIDAY NIGHT: 1415 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS BUT TO NO AVAIL. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.84) BUT WERE UNSUCCESSFUL IN KNOCKING ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A HUGE GAIN OF 2844 TOTAL OI CONTRACTS ON OUR TWO EXCHANGES.

WE HAD A HUGE 1415 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 22.765 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 280,000 OZ QUEUE JUMP//NEW STANDING ADVANCES TO 24.070 MILLION OZ

//NEW STANDING FOR SILVER//SEPT ADVANCES TO 24.070 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI GAIN //HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1491 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 587 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT

TOTAL CONTRACTS for 5 DAYS, total 4076 contracts: OR 20.380 MILLION OZ (815 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 20.380 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL PROBABLY BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 20.380 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 842 CONTRACTS DESPITE OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS:1429 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 22.765 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE 280,000 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR SEPT ADVANCES TO 24.070 MILLION OZ

WE HAVE A HUGE GAIN OF OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE LOSS IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 1491 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE FRIDAY COMEX TRADING//// MASSIVE ATTEMPTED SHORT COVERING FROM OUR SPEC SHORTS WITH THE LOSS IN PRICE FRIDAY/ AND ZERO LIQUIDATION OF LONGS. ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER.

THE NEW TAS ISSUANCE FRIDAY NIGHT (1491) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND FOR SURE TODAY., .

WE HAD 56 NOTICE(S) FILED TODAY FOR 280,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 3495 OI CONTRACTS TO 507,787 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE 4269 CONTRACTS//

WE HAD A FAIR SIZED DECREASE IN COMEX OI (3495 CONTRACTS) OCCURRED DESPITE OUR STRONG LOSS OF $17.65 IN PRICE //FRIDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT AT 12.885 TONNES ON FIRST DAY NOTICE FOLLOWED BY FRIDAYS STRONG 7700 OZ QUEUE JUMP

NEW STANDING ADVANCES TO 12.137 TONNES

/ ALL OF THIS HAPPENED WITH OUR $17.65 LOSS IN PRICE WITH RESPECT TO FRIDAY’S TRADING. WE HAD A SMALL SIZED GAIN OF 1177 OI CONTRACTS (3.660 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4692 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 507,787

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1177 CONTRACTS WITH 3795 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 4672 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1177 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 1959 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4672 CONTRACTS) ACCOMPANYING THE FAIR SIZED DECREASE IN COMEX OI OF 3495 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 1177 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT 12.885 TONNES FOLLOWED BY TODAY’S 7700 OZ QUEUE JUMP

//NEW STANDING ADVANCES TO: /SEPT 12.137 TONNES.

/ 3) HUGE T.A.S. LIQUIDATION WITH ZERO NET LONG SPECS BEING CLIPPED,

4) FAIR SIZED COMEX OPEN INTEREST LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1959 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

TOTAL EFP CONTRACTS ISSUED: 27,140 CONTRACTS OF 271,4000 OZ OR 84.42 TONNES IN 5 TRADING DAY(S) AND THUS AVERAGING: 5428 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAY(S) IN TONNES 84.42 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 84.42 DIVIDED BY 3550 x 100% TONNES = 2.42% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 84.42 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPTEMBER. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 842 CONTRACTS OI TO 129,446 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1415 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 1415 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1415 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 842 CONTRACTS AND ADD TO THE 1415 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2257 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 11.285 MILLION OZ OCCURRED DESPITE OUR $0.84 LOSS IN PRICE

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

MONDAY MORNING/SUNDAY NIGHT

SHANGHAI CLOSED DOWN 29.32 PTS OR 1.06% //Hang Seng CLOSED DOWN 247.34 PTS OR 1.42% // Nikkei CLOSED DOWN 175.72 OR 0.48%//Australia’s all ordinaries CLOSED DOWN 0.28%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7,1167 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.1239/ Oil DOWN TO 6820 dollars per barrel for WTI and BRENT DOWN AT 71.61 Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 3495 CONTRACTS TO 507,787 DESPITE OUR STRONG LOSS IN PRICE OF $17.65 WITH RESPECT TO FRIDAY’S TRADING. WE LOST ZERO IN NUMBER LONGS DESPITE THE LOWER PRICE FOR GOLD. THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTH DISTORTS OPEN INTEREST NUMBERS.

THE FED IS THE MAJOR SHORT OF AROUND 157+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS IS SCHEDULED TO HAPPEN LATE SEPT 2024/BEGINNING OF OCTOBER. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER CONTAINMENT.

OUR PHYSICAL LONDONERS ALSO BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT THESE PRICES AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD HUGE T.A.S. LIQUIDATION ON FRIDAY’S HUGE LOSS IN PRICE WITH ZERO LONGS WERE CLIPPED (AS YOU WILL SEE BELOW) BUT WE DID HAVE MAJOR SHORT COVERING. THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF THE SPREADERS // T.A.S DURING THE WEEK IS SURELY DISTORTING COMEX OPEN INTEREST.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE NON ACTIVE DELIVERY MONTH OF SEPTEMBER.… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 4672 EFP CONTRACTS WERE ISSUED: : OCT/DEC 4672 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4672 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 1177 CONTRACTS IN THAT 4672 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A FAIR LOSS OF 3495 COMEX CONTRACTS..AND THIS SMALL GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR HUGE LOSS IN PRICE OF $17.65/FRIDAY COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AS MENTIONED ABOVE. THE RAIDS ON LAST WEDNESDAY, FRIDAY AND THIS PAST TUESDAY AND FRIDAY WERE ORCHESTRATED BY THE FRBNY AS WE ARE NOW FINISHED WITH OPTIONS EXPIRY FOR THE OTC/LONDON LBMA BETS ENDING LAST FRIDAY AFTERNOON. DESPITE THE FED’S HUGE SHORT PREDICAMENT THEY STILL HAVE TIME AND ENERGY TO RAID OUR PRECIOUS METALS. SUCH CROOKS!

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR FRIDAY NIGHT A FAIR SIZED 1959 CONTRACTS. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE (AND SPREADERS LATE IN THE MONTH). THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S AND THIS WEEK’S TRADING//RAIDS

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: SEPT (11.897 TONNES) WHICH IS HUGE FOR A NON DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 44 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 12.137 TONNES.

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $17.65 ////BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE DID HAVE A STRONG GAIN IN OUR TWO EXCHANGES. WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION. BUT CENTRAL BANK LONGS, SEIZING THE MOMENT, EXERCISED FOR PHYSICAL IN A BIG WAY.

WE HAVE GAINED A TOTAL OI OF 3.660 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPT (12.885 TONNES) ON FIRST DAY NOTICE FOLLOWED BY FRIDAY’S QUEUE JUMP OF A GOOD SIZED 7700 OZ

//NEW STANDING FOR SEPT ADVANCES TO: 12.137 TONNES.

NEW STANDING FOR SEPT: 12.137 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $17.65

WE HAVE REMOVED 4269 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES 1177 CONTRACTS OR 117,700 OZ (3.660

TONNES)

confirmed volume FRIDAY 239,095 contracts poor

//speculators have left the gold arena

END

SEPT 9 SEPTEMBER GOLD CONTRACT

/ /// THE SEPT 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | NIL . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 81,226.710 oz JPMorgan |

| No of oz served (contracts) today | 212 notice(s) 21200 OZ 0.6594 TONNES |

| No of oz to be served (notices) | 62 contracts 6200 OZ 0.1928 TONNES |

| Total monthly oz gold served (contracts) so far this month | 3840 notices 384,000 oz 11.944 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: nil oz

we have 0 customer deposits

total deposits NIL oz

withdrawals:0

TOTAL WITHDRAWALS

NIL

adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPTEMBER

For the front month of SEPT. we have an oi of 274 contracts having LOST 625 contracts. We had 702 notices filed on Friday so we GAINED 77 contracts or 7700 oz will stand at the comex as these boys seek metal on this side of the pond.

OCTOBER GAINED 225 CONTRACTS UP TO 2,494 CONTRACTS

NOVEMBER LOST 2 CONTRACTS TO STAND AT 80

DECEMBER, THE BIGGEST DELIVERY MONTH LOST 3545 CONTRACTS TO 407,259.

We had 212 contracts filed for today representing 21,200 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notice issued from their client or customer account. The total of all issuance by all participants equate to 212 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 38 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for SEPT /2024. contract month, we take the total number of notices filed so far for the month (3840) x 100 oz ) to which we add the difference between the open interest for the front month of SEPT 274( CONTRACTS) minus the number of notices served upon today (212 x 100 oz per contract( equals 390,200 OZ OR 12.137 TONNES.

thus the INITIAL standings for gold for the SEPTEMBER contract month: No of notices filed so far (3840 x 100 oz +we add the difference for front month of SEPT (274 X// , OI} minus the number of notices served upon today (212) x 100 oz which equals 390,200 oz (12.137 TONNES)

TOTAL COMEX GOLD STANDING FOR SEPT.: 12.137 TONNES WHICH IS HUGE FOR THIS NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,780,327.447 oz 55.375 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,037,284.269 OZ

TOTAL REGISTERED GOLD 7,425,642.244 ( 230.96 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,611,592.025 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 5,645,315 oz (REG GOLD- PLEDGED GOLD)= 175.59 tonnes //

END

SILVER/COMEX

SEPT 9/2024

INITIAL

//2024// THE SEPT 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 604,950.900 OZ Delaware asahi . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | nil oz 604,950.900 OZ asahi delaware |

| No of oz served today (contracts) | 56 CONTRACT(S) (280,000 OZ) |

| No of oz to be served (notices) | 80 contracts (0.400 million oz) |

| Total monthly oz silver served (contracts) | 4734 Contracts (23.670 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit/

total dealer deposit : NIL oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 customer deposits:

i) Into ASAHI: 603,881.800 oz

ii) Into Delaware: 1069.100 oz

total customer deposit 604,950.900 oz

JPMorgan has a total silver weight: 134.996million oz/306.575 million or 44.03%

adjustment:2

c) dealer to customer Brinks 492,362.844 oz

d) dealer to customer Delaware 1069.100 oz

withdrawals: 1

i) Out of Delaware 46,321.838 oz

total customer withdrawals: 46,321.838 oz

TOTAL REGISTERED SILVER: 77.302 MILLION OZ//.TOTAL REG + ELIGIBLE. 306.575 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR SEPTEMBER:

silver open interest data:

FRONT MONTH OF SEPT/2024 OI: 136 CONTRACTS HAVING GAINED 46 CONTRACT(S).

WE HAD 10 NOTICES FILED ON FRIDAY, SO WE GAINED 56 CONTRACTS OR 280,000 OZ

UNDERWENT A QUEUE JUMP TO TAKE DELIVERY OF SILVER OVER ON THIS SIDE OF THE POND..

THERE MUST BE ENOUGH SILVER OVER HERE.

OCTOBER SAW ANOTHER LOSS OF 31 OF OPEN INTEREST CONTRACTS AND THUS WE HAVE 1340 OPEN INTEREST CONTRACTS FOR OCTOBER.

NOVEMBER SAW ITS ANOTHER LOSS OF 5 CONTRACTS TO STAND AT 17.

DECEMBER SAW A LOSS OF 460 CONTRACTS UP TO 114,385.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 56 for 280,000 oz

CONFIRMED volume; ON FRIDAY 91,922 strong

To calculate the number of silver ounces that will stand for delivery in SEPT. we take the total number of notices filed for the month so far at 4734 x 5,000 oz = 23.670 MILLION oz

to which we add the difference between the open interest for the front month of SEPT(136) and the number of notices served upon today 56 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT/2024 contract month: 4734 notices served so far) x 5000 oz + OI for the front month of SEPT (136)x number of notices served upon today minus (56)x 5000 oz of silver standing for the SEPT contract month equates to 24.070 MILLION OZ.

New total standing: 24.070 million oz.

There are 77,743 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS//

GLD

SEPT 9 WITH GOLD UP $12.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 6 WITH GOLD DOWN $17.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 5 WITH GOLD UP $18.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 4 WITH GOLD UP $3.45 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 3 WITH GOLD DOWN $4.25 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 5,47 TONNES OF GOLD INTO THE GLD/:/ //////INVENTORY RESTS AT 862.74 TONNES

AUGUST 30 WITH GOLD DOWN $31.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD/:/ //////INVENTORY RESTS AT 857.27 TONNES

AUGUST 29 WITH GOLD UP $23.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 28 WITH GOLD DOWN $14.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 27 WITH GOLD DOWN $1.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 26 WITH GOLD UP $9.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD VAPOUR GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 23 WITH GOLD UP $29.70 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER WITHDRAWAL OF 8.88 TONNES OF GOLD VAPOUR GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 857.85 TONNES

AUGUST 22 WITH GOLD DOWN $28.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 9.43 TONNES OF GOLD VAPOUR GOLD INTO THE GLD./ //////INVENTORY RESTS AT 866.70 TONNES

AUGUST 21 WITH GOLD DOWN $1.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER WITHDRAWAL OF 1.73 TONNES OF GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 857.27 TONNES

AUGUST 20 WITH GOLD UP $9.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 4.03 TONNES OF GOLD VAPOUR INTO THE GLD./ //////INVENTORY RESTS AT 859.00 TONNES

AUGUST 19 WITH GOLD UP $3.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 7.19 TONNES OF GOLD VAPOUR INTO THE GLD./ //////INVENTORY RESTS AT 854.97 TONNES

AUGUST 16 WITH GOLD UP $44.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: //////INVENTORY RESTS AT 847.78 TONNES

AUGUST 15 WITH GOLD UP $13,70 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD OUT OF THE GLD//////INVENTORY RESTS AT 847.78 TONNES

AUGUST 14 WITH GOLD DOWN $26.20 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.03 TONNES OF GOLD OUT OF THE GLD//////INVENTORY RESTS AT 845.76 TONNES

AUGUST 13 WITH GOLD UP $3.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//////INVENTORY RESTS AT 849.79 TONNES

AUGUST 12 WITH GOLD UP $30.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ////INVENTORY RESTS AT 846.91 TONNES

AUGUST 9 WITH GOLD UP $10.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 846.91 TONNES

AUGUST 8 WITH GOLD UP $31.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.02 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 844.04 TONNES

AUGUST 7 WITH GOLD UP $1.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.16 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 848.06 TONNES

AUGUST 6 WITH GOLD DOWN $13.10 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD” A WITHDRAWAL OF .57 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 844.90 TONNES

AUGUST 2 WITH GOLD DOWN $9.95 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.58 TONNES OF GOLD OUT OF THE GLD//INVENTORY RESTS AT 845.47 TONNES

AUGUST 1 WITH GOLD UP $9.15 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 846.05 TONNES

GLD INVENTORY: 862.74 TONNES, TONIGHTS TOTAL

SILVER

SEPT 9//WITH SILVER UP $0.45//SMALL CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 46,000 OZ OF SILVER FROM THE SLV./. /: .///./// /INVENTORY AT 466.188 MILLION OZ

SEPT 6//WITH SILVER DOWN $.84//NO CHANGES IN SILVER INVENTORY /: .///./// /INVENTORY AT 466.234 MILLION OZ

SEPT 5//WITH SILVER UP $.55//SMALL CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 0.193 MILLION OZ OF SILVER INTO THE SLV/: .///./// /INVENTORY AT 466.234 MILLION OZ

SEPT 4//WITH SILVER UP $.17//SMALL CHANGES IN SILVER INVENTORY A DEPOSIT OF 0.456 MILLION OZ OF SILVER INTO THE SLV/: .///./// /INVENTORY AT 466.427 MILLION OZ

SEPT 3//WITH SILVER DOWN $.74//HUGE CHANGES IN SILVER INVENTORY A DEPOSIT OF 1.278 MILLION OZ OF SILVER INTO THE SLV/: .///./// /INVENTORY AT 465.971 MILLION OZ

AUGUST30//WITH SILVER DOWN $.42//NO CHANGES IN SILVER INVENTORY: .///./// /INVENTORY AT 464.693 MILLION OZ

AUGUST 29//WITH SILVER UP $.37//SMALL CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 0.558 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 464.693 MILLION OZ

AUGUST 28//WITH SILVER DOWN $0.76//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 2.301 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 465.281 MILLION OZ

AUGUST 27//WITH SILVER DOWN $0.03//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 2.921 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 462.959 MILLION OZ

AUGUST 26//WITH SILVER UP $0.23//SMALL CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 45,000 OZ OUT OF THE SLV. .///./// /INVENTORY AT 465.880 MILLION OZ

AUGUST 23//WITH SILVER UP $0.72//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 1.506 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 465.925 MILLION OZ

AUGUST 22//WITH SILVER DOWN $0.44//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 0.943 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 468.344 MILLION OZ

AUGUST 21//WITH SILVER $0.03//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 1..552 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 468.344 MILLION OZ

AUGUST 20//WITH SILVER $0.24//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 1.369 MILLION OZ FROM THE SLV. .///./// /INVENTORY AT 466.792 MILLION OZ

AUGUST 19//WITH SILVER $0.39//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 1.506 MILLION OZ FROM THE SLV. .///./// /INVENTORY AT 465.423 MILLION OZ

AUGUST 16//WITH SILVER $0.49//NO CHANGES IN SILVER INVENTORY: .///./// /INVENTORY AT 466.929 MILLION OZ

AUGUST 15//WITH SILVER $1.14//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.186 MILLION ON INTO THE SLV.///./// /INVENTORY AT 466.929 MILLION OZ

AUGUST 14//WITH SILVER DOWN $0.40//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 13//WITH SILVER DOWN $0.19//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 12//WITH SILVER UP $.37//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 9//WITH SILVER DOWN $.03//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 8//WITH SILVER UP $.70//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 3.241 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 7//WITH SILVER DOWN $0.27//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.552 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 6//WITH SILVER UP $0.05//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 458.851 MILLION OZ

AUGUST 2//WITH SILVER DOWN $0.01//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 1.243 MILLION OZ OF SILVER OUT OF THE SLV ///./// /INVENTORY AT 460.961 MILLION OZ

AUGUST 1//WITH SILVER DOWN $0.46//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.608 MILLION OZ OF SILVER VAPOUR INTO THE SLV///./// /INVENTORY AT 462.204 MILLION OZ

CLOSING INVENTORY 466.188 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

end

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY//BILL HOLTER:

3.CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

China is ready with 40,000 tonnes of gold for new trading system, Maguire says

Submitted by admin on Sat, 2024-09-07 21:19 Section: Daily Dispatches

9:17p ET Saturday, September 7, 2024

Dear Friend of GATA and Gold:

U.S. Secretary of State Antony Blinken probably discussed China’s involvement in the de-dollarization movement during his recent visit to that country, London metals trader Andrew Maguire tells this week’s edition of Kinesis Money’s “Live from the Vault” program.

China, Maguire says, may have as much as 40,000 tonnes of gold is its “shadow” banking system, ready for use in the gold-linked international trade currency being prepared by the BRICS nations and Russia

Mainstream financial news organizations, Maguire says, still don’t understand that the classification of gold as a “Tier 1” asset by the Bank for International Settlements has triggered the recent rise in the gold price and facilitated de-dollarization.

The U.S. Federal Reserve, Maguire says, is losing its struggle to keep the “paper” price of gold down because declines in the “paper” price are quickly bought by foreign central banks converting “paper” to physical.

The program is 48 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Reuters still thinks China’s not reporting gold purchases is the same as not purchasing

Submitted by admin on Sat, 2024-09-07 14:30 Section: Daily Dispatches

China’s Central Bank Pauses Gold Purchases for a Fourth Month in August

By Polina Devitt, Qiaoyi Li, and Ryan Woo

Reuters

Saturday, September 7 2024

China’s central bank held back on buying gold for its reserves for a fourth straight month in August, official data showed on Saturday.

China’s gold holdings stood at 72.8 million fine troy ounces at the end of last month. The value of the gold reserves, however, rose to $182.98 billion compared with $176.64 billion at the end of July.

…

Gold prices have been rising this year amid bets that U.S. rate cuts are imminent and due to safe-haven demand driven by geopolitical and economic uncertainty, with central banks making robust purchases.

Gold prices have surged 21% so far this year and are hovering slightly below a record high of $2,531.60 hit on Aug. 20.

Prior to the pause in its purchases, the People’s Bank of China had bought gold for 18 consecutive months. …

… For the remainder of the report:

END

Interviewed by Money Metals, GATA secretary explains central banking’s hostility to gold

Submitted by admin on Sat, 2024-09-07 00:23 Section: Daily Dispatches

12:23a Saturday, September 7, 2024

Dear Friend of GATA and Gold:

Your secretary/treasurer was interviewed this week by Mike Maharrey of Money Metals, explaining the longstanding hostility of central banks to gold and their aggression against the monetary metal, a powerful competitor to their own currencies. GATA’s work is also discussed, along with gold’s hastening progress toward restoration as the world reserve currency.

The interview is 35 minutes long, follows the Money Metals weekly market review, and can be heard or read in transcript form here:

https://www.moneymetals.com/podcasts/2024/09/06/gold-steady-as-stock-market-slumps-irs-audits-003438

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Robert Lambourne: BIS gold swaps rose again in August

Submitted by admin on Fri, 2024-09-06 11:31 Section: Daily Dispatches

By Robert Lambourne

September 6, 2024

The August statement of account for the Bank for International Settlements has just been published:

From this it is possible to estimate the volume of gold swaps undertaken by the BIS at the month end: 157 tonnes at August 31. This is the highest level since May 31, 2023, and compares to an estimate of 116 tonnes for June 30 and an estimate of 148 tonnes at July 31, so swaps have increased during June and July by 41 tonnes.

Since February 29 the volume of swaps has increased by 89 tonnes.

Table 1 below sets out the historical level of monthly gold swaps estimated since August 2018. As is evident from the table there is still a considerable level of gold being traded via these swaps. While gold swaps are down significantly from the 501 tonnes estimated in January 2022, the level seemingly remains quite volatile, suggesting the use of swaps to cover shorter-term trading requirements.

To repeat the regular point made in these GATA reports, it seems that these swaps are undertaken by the BIS for one or more of its central bank customers with the swapped gold being accounted for as being held in a BIS registered sight account at a central bank. Given what is happening in the gold market more generally, it appears reasonable to assume that the Federal Reserve is the BIS’ customer for the swaps transactions. The evidence strongly suggests that the source of this gold is bullion banks and the gold comes from gold registered as being held by gold exchange-traded funds.

The recently published 2023-24 annual report for the BIS —

— confirms GATA’s estimate of the bank’s gold swaps as of March 31 in Table 1 of 72 tonnes.

The BIS annual report contains information that also confirms certain assumptions used to estimate the swap volumes. This includes confirmation that the BIS continued to hold 102 tonnes of its own gold. The annual report also provides strong support, via its reporting on transactions with related parties, that the source of the swapped gold is bullion banks rather than central banks.

However, the BIS continues to offer no explanation for why it is undertaking gold swaps. The BIS first reported gold swaps in its annual report for 2009-10, so gold swaps have been provided by the BIS for its customer central banks for more than 15 years. See Table 2 below for the year-end level of gold swaps reported by the BIS in its annual reports since March 2010.

*

Table 1 — Gold swaps estimated by GATA from BIS monthly statements of account

Month ….. Swaps

& year … in tonnes

Aug-24 …. /157

Jul-24 …. /148

Jun-24 …. /116

May-24 …. /109

Apr-24 …. /78

Mar-24 …. /72

Feb-24 …. /68

Jan-24 …. /117

Dec-23 …. /121

Nov-23 …./100

Oct-23 …./68

Sep-23 …./96

Aug-23 …./129

Jul-23 …. /103

Jun-23…. /87

May-23 …. /188

Apr-23 …. /135

Mar-23 …. /77*

Feb-23 … /136

Jan-23 … /103

Dec-22 … /0

Nov-22 … /105

Oct-22 ….. /7

Sep-22 …../57

Aug -22 ….. /75

Jul-22 ….. /56

Jun-22 ….. /202

May-22 ….. /270

Apr-22 ….. /315

Mar-22 …. /358

Feb-22 …. /472

Jan-22 ….. /501

Dec-21…. /414

Nov-21…. /451

Oct-21…. /414

Sep-21 …. /438

Aug-21 …. /464

Jul-21 …. /502

Jun-21 …./471

May-21 …./517

Apr-21 …. /472

Mar-21…. /490+

Feb-21 …../552

Jan-21 …. /523

Dec-20 …. /545

Nov-20 …. /520

Oct-20 …. /519

Sep-20…../ 520

Aug-20…../ 484

Jul-20 ….. / 474

Jun-20 …. / 391

May-20 … / 412

Apr-20 …. / 328

Mar-20 …. / 326**

Feb-20 …. / 326

Jan-20 …. / 320

Dec-19 …. / 313

Nov-19 …. / 250

Oct-19 …. / 186

Sep-19 …. / 128

Aug-19 …. / 162

Jul-19 ….. / 95

Jun-19 …. / 126

May-19 …. / 78

Apr-19 ….. / 88

Mar-19 …. / 175

Feb-19 …. / 303

Jan-19 …. / 247

Dec-18 …. / 275

Nov-18 …. / 308

Oct-18 …. / 372

Sep-18 …. / 238

Aug-18 …. / 370

* The estimate originally reported by GATA was 78 tonnes, but the BIS annual report states 77 tonnes. It is believed that slightly different gold prices account for the difference.

+ The estimate originally reported by GATA was 487 tonnes, but the BIS annual report states 490 tonnes, It is believed that slightly different gold prices account for the difference.

** The estimate originally reported by GATA was 332 tonnes, but the BIS annual report states 326 tonnes. It is believed that slightly different gold prices account for the difference.

GATA uses gold prices quoted by USAGold.com to estimate the level of gold swaps held by the BIS at month-ends.

*

There seem to be no new reasons to alter the assumption that the BIS is continuing to enter these swaps on behalf of the Federal Reserve. There is no evidence to suggest that any other major central bank is actively trading this much gold, and some central banks are still accumulating physical gold.

As noted above, the basic transaction that the BIS is believed to undertake is to swap dollars for gold that is transferred from a bullion bank, then to deposit this gold in a gold sight account at a central bank, presumed to be the Fed but almost certainly being the central bank that is using the BIS to execute the gold swap on its behalf.

Given the recent volatility in BIS gold swaps, it seems likely that most are of a short duration. Why a central bank needs the BIS to undertake gold swaps isn’t clear. The swaps are likely connected with short-term trading needs and perhaps are being used to aid suppression of the gold price via the futures markets.

The volatility in the volume of swaps is clear from a review of Table 1 above. Volumes of swaps in 2023 and so far in 2024 remain well below the average seen in the preceding four years but remain significant. The gold price increased from $2,327 at June 28 to $2,447 at July 31 (per USAGold.com). Using the July 31 gold price, the 148 tonnes of gold swaps carried out via the BIS in July are valued at about $11.6 billion. (The corresponding value of the swaps in place as of June 28 was around $8.7 billion.)

So the recent trading in BIS gold swaps has high dollar value and shows that gold remains a significant monetary asset still actively traded on behalf of at least one central bank, presumably the Fed.

As ever with the BIS, it remains unlikely that more information about why it undertakes these transactions will be provided. No such information was provided in the recently published annual report, which covered the year ending March 31, 2024.

GATA’s research on gold price suppression indicates that an active policy of price suppression was implemented around 30 years ago and was primarily intended to suppress interest rates. Recent updates on this research are provided by the presentations GATA secretary/treasurer Chris Powell and Chairman Bill Murphy made in November 2023 at the New Orleans Investment Conference:

https://www.gata.org/node/22886

https://www.gata.org/node/22889

In a more recent dispatch Powell laments that so much of the bullish commentary on gold fails to highlight the regular and repeated efforts to suppress the gold price during the past 30 years. He argues that this bullish commentary provides an incomplete view of the risks as well as the rewards of gold ownership even as the financial outlook for the U.S. government seems fraught amid so much debt:

https://www.gata.org/node/22993

This influential report from 2005 abut “Gibson’s Paradox” remains relevant and highlights work in this area by former U.S. Treasury Secretary and Harvard University President Lawrence Summers:

https://goldensextant.com/gibsonsparadox/

It also remains relevant to highlight the following remarks made in a speech by Summers on September 8, 1999, as reported in the book “The Wealth of Progressive Nations: The Collected Lectures of Lawrence Summers.” The remarks below are an extract of a section of the speech titled “A New Economic Paradigm.”

“Most important of all, the Clinton-Gore administration has established a new paradigm for the management of our nation’s budget, with enormous cumulative benefits for our economy and our citizens. It has become a commonplace to remark on how exceptional today’s 4.2% unemployment rate is relative to any expectation at the beginning of the decade. It is no less remarkable that today, after 8.5 years of expansion, long-term interest rates are around 2 percentage points lower than they were at its start.”

From this it is reasonable to conclude that keeping interest rates “lower” was considered a priority by the Clinton-Gore administration and succeeding at it was thought to be “remarkable.” While this is not proof that gold price suppression was undertaken specifically to reduce interest rates, it shows that reducing interest rates was a priority for the U.S. government.

Further evidence of this priority is provided by an interview with former Treasury Secretary Robert Rubin about his time working in the Clinton administration after January 1993. In answer to a question on the initial decision to prioritize deficit reduction, Rubin remarks: “On the other hand, if interest rates go down as a result, then that will stimulate growth, and we thought that the beneficial effect of lower interest rates would outweigh the contractionary impact of the deficit reduction”:

https://www.pbs.org/wgbh/pages/frontline/shows/clinton/interviews/rubin.html

Hence there is plenty of evidence that keeping interest rates low was a major goal of the Clinton presidency.

In the context of gold price suppression being used to reinforce efforts to reduce interest rates, the following report issued by GATA in 2007 with an analysis of the gold market by Frank Veneroso is a notable reference as it confirms that GATA’s primary assertions about gold price suppression were plausible:

https://www.gata.org/node/5275

… More recent trends in U.S. government deficits …

The remarks of Rubin and Summers on the U.S. government’s priorities in the 1990s are reminders of how far the the financial positions of Western nations have worsened since then.

The worsening trend for Western nations, especially the United States, probably reduces the appeal to the BIS of undertaking gold swaps on behalf of any central bank where a liability to return swapped gold is incurred. The trend possibly also reduces the appeal of any such swaps to the central bank or banks for which the BIS has been acting.

A report issued by GATA in 2012 is worth revisiting as it highlights the acknowledgment of gold price suppression by a former chairman of the BIS, Jelle Zijlstra, a Dutch politician, economist, and central banker. So it seems likely that BIS management understands what the swaps are being used for and why no reasons for the transactions are given.

https://www.gata.org/node/11304

The conundrum facing the Federal Reserve about dollar interest rates has seemingly been resolved for now with the Fed apparently not being ready to reduce rates close to the upcoming presidential election. Further market turmoil driven possibly by Japanese interest rates and currency levels may change this assumption rapidly given the high level of government debt in both countries.

Despite its opaque rhetoric, the Fed needs to sustain confidence in the U.S. stock market and the Treasuries market when the government’s ever-increasing debt has become so controversial. Forthcoming new debt issuance is being monitored even more closely by investors.

The Treasury Department’s monthly report on June 2024 revenue and expenditure shows a cumulative deficit of $1.3 trillion and points toward a broadly similar level of cash outflows in the current fiscal year to the underlying deficit of about $2.1 trillion in the year prior to September 30, 2023. The higher interest charge being reported virtually each month is one reason for the deficit to increase.

The run rate of gross interest costs reported in the last 12 months has now passed $1 trillion, despite a more muted level of annual interest payments on the approximately $7.2 trillion of Treasury debt held by federal government-sponsored trust funds. This more muted increase is perhaps indicative of the pressure to keep a lid on interest costs.

In these circumstances the room for the Fed to raise interest rates in the next few years seems restricted and hence it seems likely as noted above that the BIS and some of its member central banks might be questioning the role of the BIS in these swaps and the obligation to make future deliveries of gold, since the Fed may be unable to move interest rates high enough to contain inflation.

In this context the relatively stable price of oil is relevant as it seems that strong forces want to keep oil prices subdued despite developments that might be expected to result in higher prices, such as production cuts by major producers and the dangers to shipments through the Red Sea.

With 2024 being a presidential election year in the United States there appear to be strong political incentives to contain oil prices and that even recent moves to consolidate the number of oil producers in the U.S. might have been tacitly encouraged in return for commitments to keep production high.

The success or failure of such efforts might be a clue to the timing of a gold price reset, as there appears to be little effort by the Fed and Treasury Department to acknowledge that federal debt levels have become dangerously high.

The report at the following link, which reviews the possible connection between hedge funds’ basis trades in U.S. Treasuries and the Fed’s program of quantitative tightening, could be read as another sign of how difficult it is to locate purchasers of U.S. Treasuries at current prices:

https://www.gata.org/node/22873

The link below contains a commentary on the apparent enrichment of certain hedge funds and the individuals involved as a result of the apparent support from the Fed to the hedge fund basis trade used to effect “quantitative tightening”:

https://www.gata.org/node/22972

It also seems that the incentives for foreigners to own U.S. Treasuries are diminishing as efforts to confiscate Russian assets appear to be moving forward. Saudi Arabia has apparently warned that any such confiscation may cause it to sell its holding of U.S.Treasuries.

Again, it seems appropriate to note that a report titled “Living with High Public Debt” authored by Serkan Arslanalp and Barry Eichengreen was published in August 2023 by the Federal Reserve Bank of Kansas City. This report reinforces just how difficult it is to handle high federal government debt with spending far in excess of revenue.

The report can be found at the Kansas City Fed’s internet site and at GATA’s:

https://www.kansascityfed.org/Jackson%20Hole/documents/9749/Living_With_High_Public_SA_Sep_2_2023.pdf

https://www.gata.org/sites/default/files/Living_With_High_Public_Debt_Sep_2_2023.pdf

Here is an excerpt from the conclusions:

“Looking forward, the challenges are daunting. Given aging populations, governments will have to find additional finance for healthcare and pensions. They will have to finance spending on defense, climate change abatement, and adaptation, and the digital transition. A growing number of low-income countries are already in debt distress.

“Living with high public debt therefore means avoiding steps that make a bad situation worse. This means minimizing unproductive public spending. It means targeting social transfers as a way of limiting pressures on the expenditure side. It means limiting contingent liabilities by, inter alia, adequately regulating banks and avoiding recapitalization costs.

“It means contemplating tax increases where revenues are low by international standards. It means further developing financial markets where markets are underdeveloped and where a diverse population of local investors in debt securities is absent. It means embracing legal and procedural changes that streamline and speed restructuring for countries whose debts are unsustainable.

“This modest medicine does not make for a happy diagnosis. But it makes for a realistic one.”

In the circumstances vividly described in the report it seems unsurprising that the price of gold has increased so far in 2024. The report offers yet more reason to question whether gold swaps undertaken via the BIS, probably on behalf of the Fed, are being used to suppress the dollar gold price.

... Historical context …

The BIS rarely comments publicly on its gold activities, but its first use of gold swaps was considered important enough to cause the bank to give some background information to the Financial Times for an article published on July 29, 2010, coinciding with publication of the bank’s 2009-10 annual report.

The general manager of the BIS at the time, Jaime Caruana, said the gold swaps were “regular commercial activities” for the bank, and he confirmed that they were carried out with commercial banks and so did not involve central banks. It also seems highly likely that the BIS’ remaining swaps are still all made with commercial banks, because the BIS annual report has never disclosed a gold swap between the BIS and a major central bank.

The swap transactions potentially created a mismatch at the BIS, which may have ended up being long unallocated gold (the gold held in BIS sight accounts at major central banks) and short allocated gold (the gold required to be returned to swap counterparties). This possible mismatch has not been reported by the BIS.

The gold banking activities of the BIS have been a regular part of the services it offers to central banks since the bank’s establishment 90 years ago. The first annual report of the BIS explains these activities in some detail:

http://www.bis.org/publ/arpdf/archive/ar1931_en.pdf

A June 2008 presentation made by the BIS to potential central bank members at its headquarters in Basel, Switzerland, noted that the bank’s services to its members include secret interventions in the gold and foreign exchange markets:

https://www.gata.org/node/11012

The use of gold swaps to take gold held by commercial banks and then deposit it in gold sight accounts held in the name of the BIS at major central banks doesn’t appear ever to have been as large a part of the BIS’ gold banking business as it has been in recent years, although the recent declines suggest this may be changing.

As of March 31, 2010, excluding gold owned by the BIS, there were 1,706 tonnes held in the name of the BIS in gold sight accounts at major central banks, of which 346 tonnes or 20% were sourced from gold swaps from commercial banks.

If the BIS was adopting the level of disclosure made by publicly held companies, such as commercial banks, some explanation of these changes probably would have been required by the accounting regulators. This irony may not be lost on those dealing with regulatory activities at the BIS. Presumably the shrinkage of the BIS’ gold banking business shows that even central banks now prefer to hold their own gold or hold it in earmarked form — that is, as allocated gold.

A review of Table 2 below highlights recent BIS activity with gold swaps, and despite the recent declines, the recent positions estimated from the BIS monthly statements have regularly been large, especially in early 2022, and the volume of trading has been significant.

*

Table 2

March 2010: 346 tonnes

March 2011: 409 tonnes

March 2012: 355 tonnes

March 2013: 404 tonnes.

March 2014: 236 tonnes.

March 2015: 47 tonnes.

March 2016: 0 tonnes.

March 2017: 438 tonnes.

March 2018: 361 tonnes.

March 2019: 175 tonnes

March 2020: 326 tonnes

March 2021: 490 tonnes

March 2022: 358 tonnes

March 2023: 77 tonnes

March 2024: 72 tonnes

—–

Robert Lambourne is a retired business executive in the United Kingdom who consults for GATA about the involvement of the Bank for International Settlements in the gold market and U.S. government debt.

* * *

Join GATA here:

New Orleans Investment Conference

Hilton New Orleans Riverside Hotel

Wednesday-Saturday, November 20-23, 2024

https://neworleansconference.com/powellgata/

* * *

Support GATA by purchasing

Stuart Englert’s “Rigged”

“Rigged” is a concise explanation of government’s currency market rigging policy and extensively credits GATA’s work exposing it. Ten percent of sales proceeds are contributed to GATA. Buy a copy for $14.99 through Amazon —

— or for an additional $3 and a penny buy an autographed copy from Englert himself by contacting him at srenglert@comcast.net.

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

»

4. OTHER GOLD COMMENTARIES/:live from the vault

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:silver

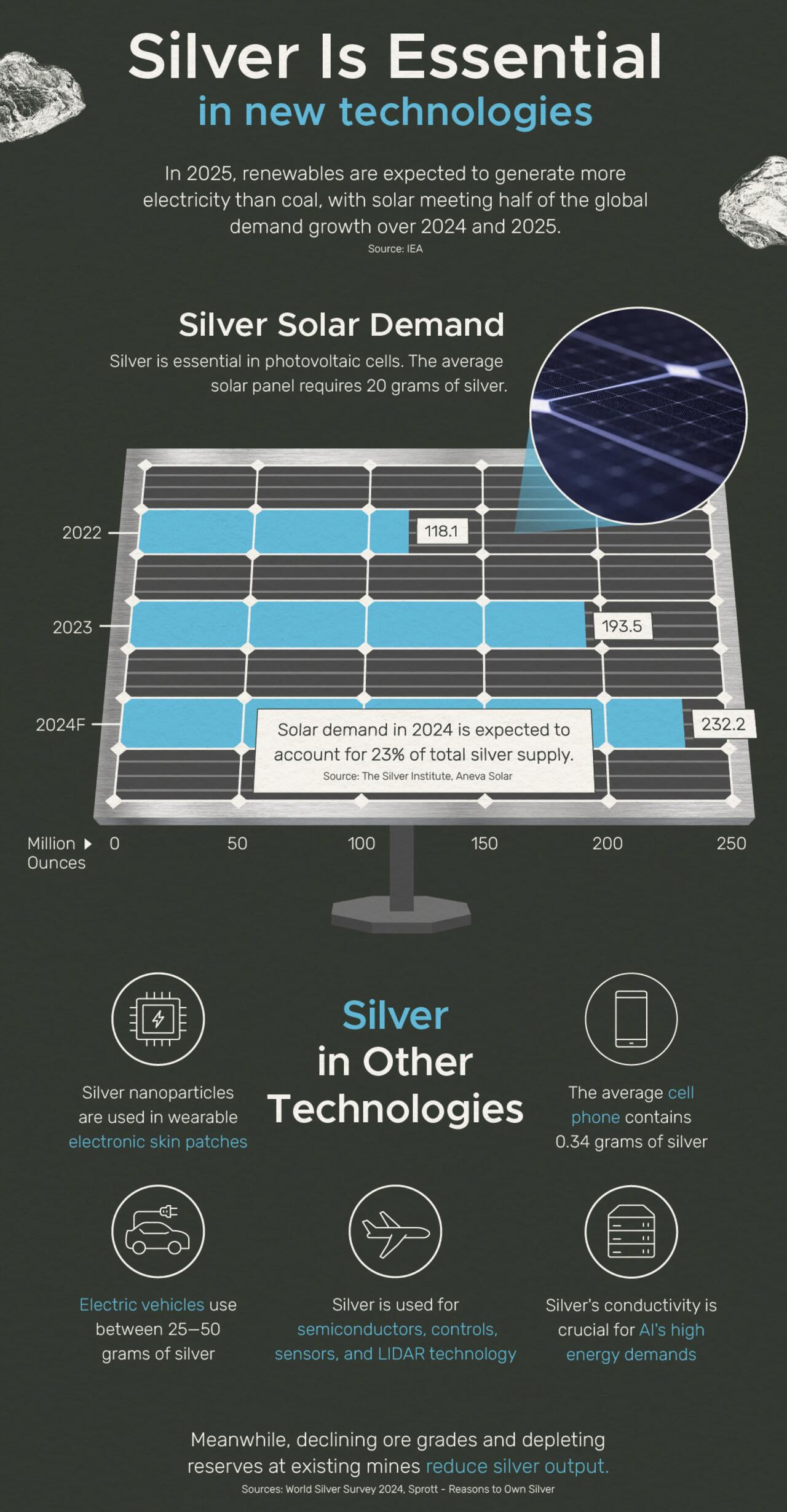

Silver: The Unsung Hero Of The New Economy

Saturday, Sep 07, 2024 – 10:45 PM

Silver demand continues to surge, driven by technologies like solar power and AI.

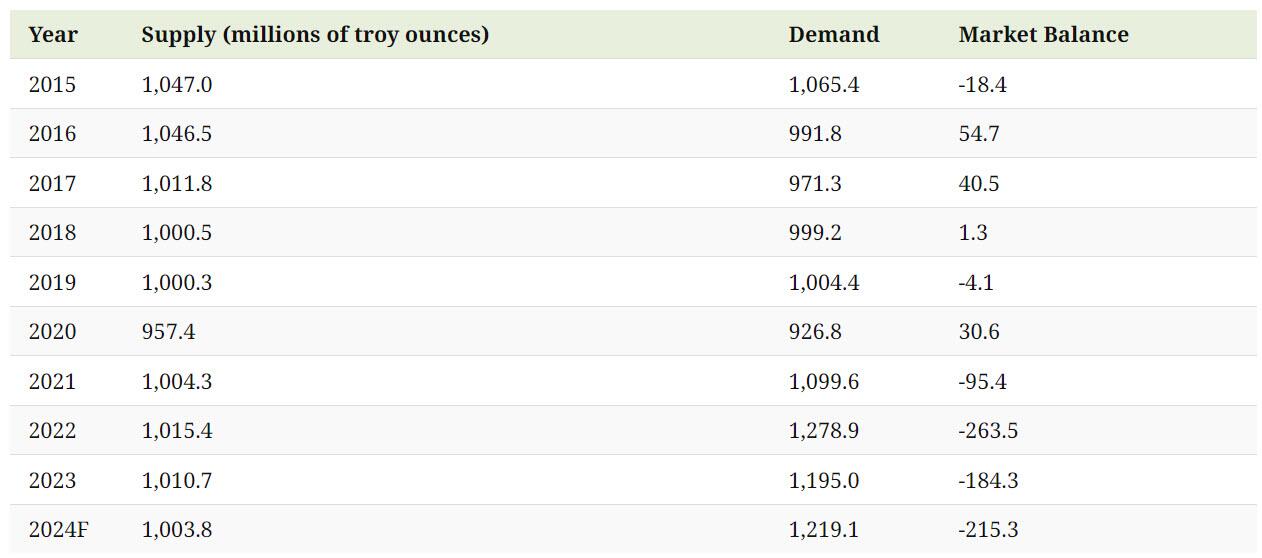

In 2023 alone, the silver market experienced a 15% supply deficit. Furthermore, the market is expected to reach a cumulative deficit of 1,093.4 million ounces from 2020 to 2024.

In this graphic by Outcrop Silver, Visual Capitalist’s Bruno Venditti discusses how new mines are necessary to meet the high demand for the metal.

Silver is Essential for New Technologies

According to Sprott, Silver is second only to oil as one of the most widely used commodities, with more than 10,000 applications worldwide.

The metal is a key component in photovoltaic cells used in solar power. The average solar panel requires 20 grams of silver.

Electric vehicles also use between 25 and 50 grams of silver.

In addition, the metal is essential for semiconductors, controls, sensors, and LIDAR technology in AI-enabled transport. Silver is also critical in healthcare AI, through conductive silver nanoparticles in wearable electronic skin patches.

The average cell phone contains 0.34 grams of silver.

The Risk of a Supply Gap

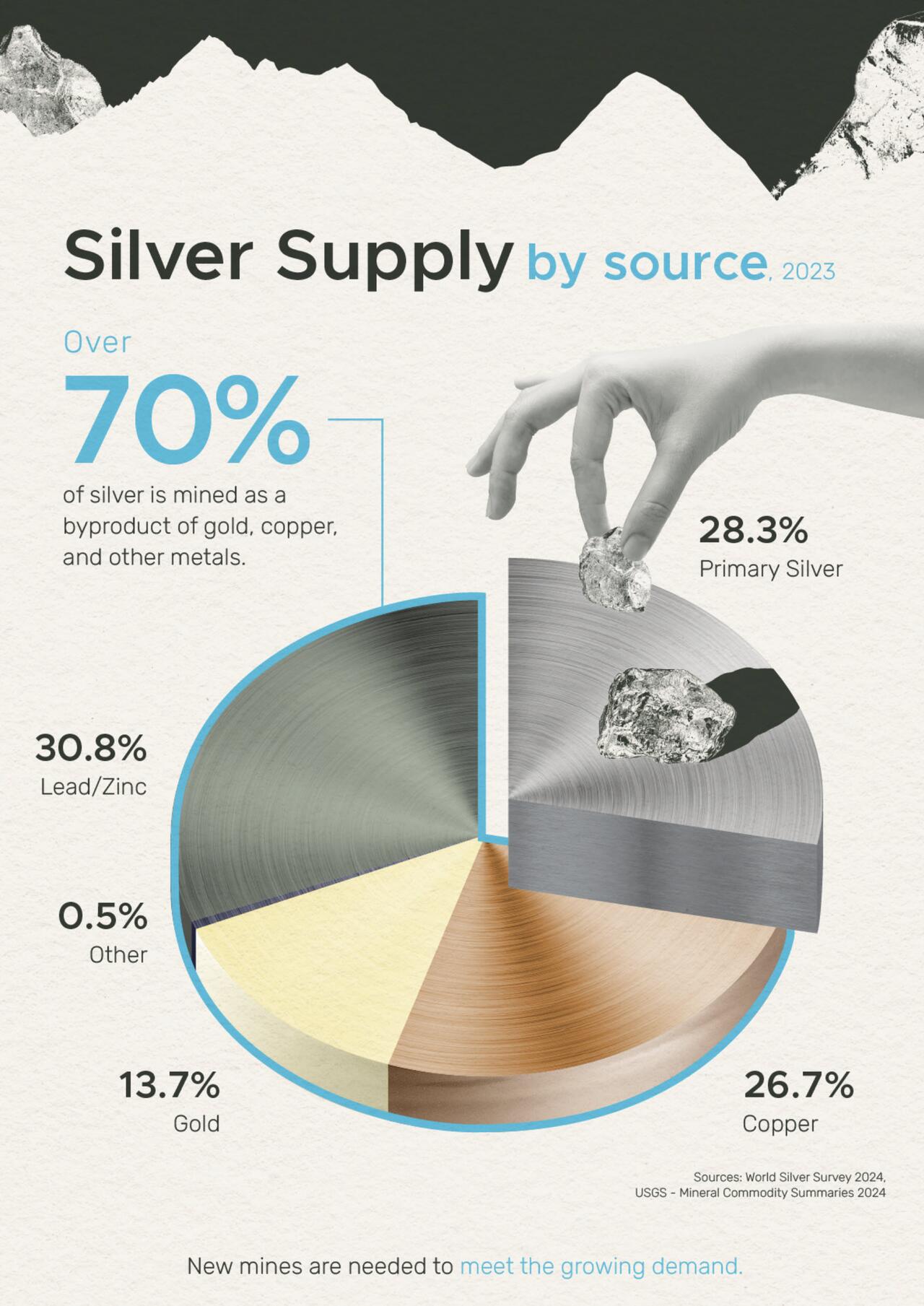

Despite silver’s importance, declining ore grades and depleting reserves at existing mines are reducing the metal output.

The industry also suffers from a lack of investment in primary silver mines. Today, over 70% of silver is mined as a byproduct of gold, copper, and other metals.

Production is also concentrated in three countries—Mexico, Peru, and China—which together account for half of global silver production.

The Future of Silver

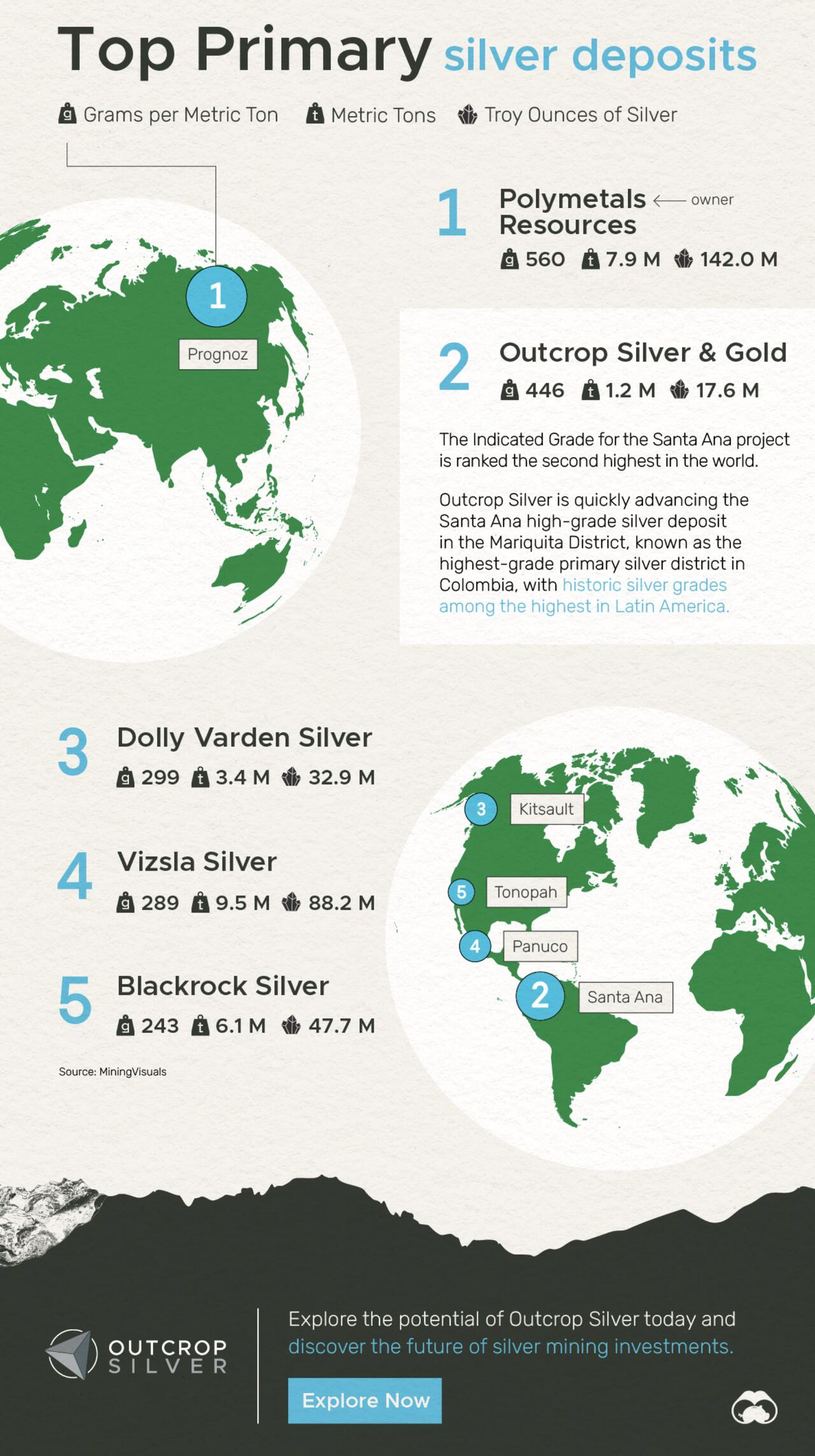

If current circumstances continue, new mines will be necessary to meet the growing demand.

Outcrop Silver is quickly advancing the Santa Ana high-grade silver deposit in the Mariquita District, known as the highest-grade primary silver district in Colombia, with historic silver grades among the highest in Latin America.

The Indicated Grade for the Santa Ana project is ranked the second highest in the world.

6 CRYPTOCURRENCY NEWS

END

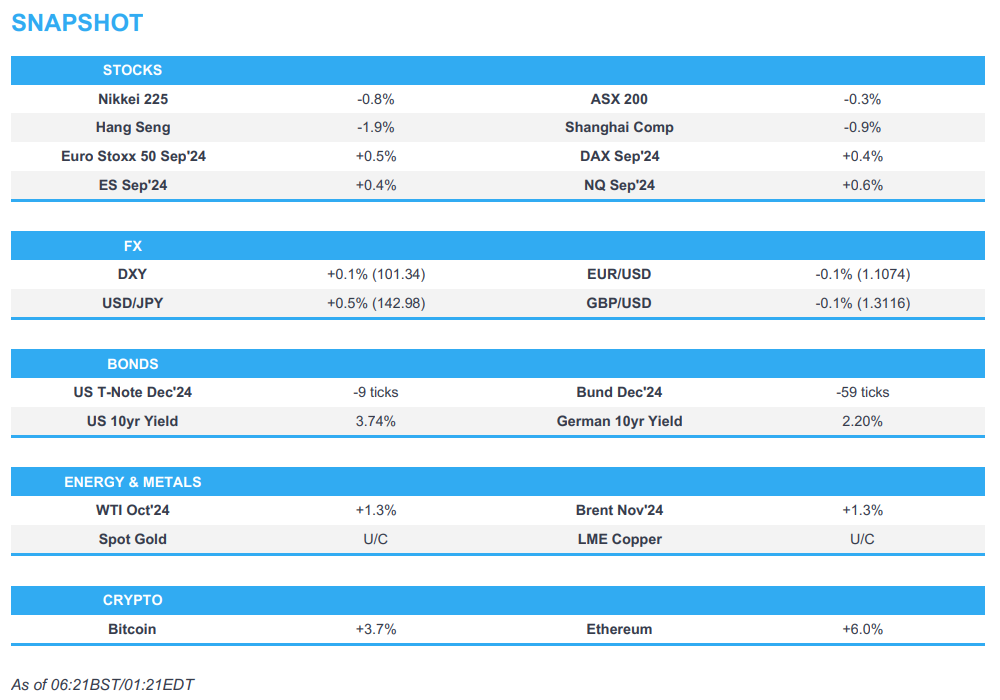

ASIA TRADING/MONDAY MORNING/SUNDAY NIGHT

SHANGHAI CLOSED DOWN 29.32 PTS OR 1.06% //Hang Seng CLOSED DOWN 247.34 PTS OR 1.42% // Nikkei CLOSED DOWN 175.72 OR 0.48%//Australia’s all ordinaries CLOSED DOWN 0.28%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7,1167 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.1239/ Oil DOWN TO 6820 dollars per barrel for WTI and BRENT DOWN AT 71.61 Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS MONDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1167

OFFSHORE YUAN: DOWN TO 7.1239

SHANGHAI CLOSED DOWN 29.32 PTS OR 1.06 %

HANG SENG CLOSED DOWN 247.34 PTS OR 1.42%

2. Nikkei closed DOWN 175.72 PTS OR 0.48%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 101.59 EURO FALLS TO 1.1042 DOWN 34 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +00.906 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 143.65…… JAPANESE YEN NOW RISING AS WE HAVE NOW REACHED THE COLLAPSING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.2135/Italian 10 Yr bond yield UP to 3.5980 SPAIN 10 YR BOND YIELD UP TO 3.043%

3i Greek 10 year bond yield UP TO 3.244

3j Gold at $2497.00//Silver at: 28.12 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 72/ 100 roubles/dollar; ROUBLE AT 90.80

3m oil into the 68 dollar handle for WTI and 71 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 143.65/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.906 % STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8486 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9372 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.747 UP 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.058 UP 4 BASIS PTS/

USA 2 YR BOND YIELD: 3.694 UP 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 34/05…

10 YR UK BOND YIELD: 3.957 UP 4 PTS

10 YR CANADA BOND YIELD: 3.031 UP 7 BASIS PTS

5 YR CANADA BOND YIELD: 2.861 UP 6 PTS.

2a New York OPENING REPORT

2B) European report

European equities gain, DXY stronger whilst JPY lags given the risk appetite – Newsquawk US Market Open

Monday, Sep 09, 2024 – 05:54 AM

- European equities are entirely in the green, attempting to pare back some of last week’s hefty losses; Tech leads whilst Luxury lags

- Dollar is firmer while JPY lags after GDP revisions and risk appetite, with USD/JPY back above 143

- Bonds are entirely in the red and reside near session lows.

- Crude is on the front foot, precious metals are mixed, and base metals are higher across the board despite softer Chinese inflation.

- Looking ahead, US Employment Trends, Wholesale Sales, NY Fed SCE, Apple iPhone Event, Earnings from Oracle.

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

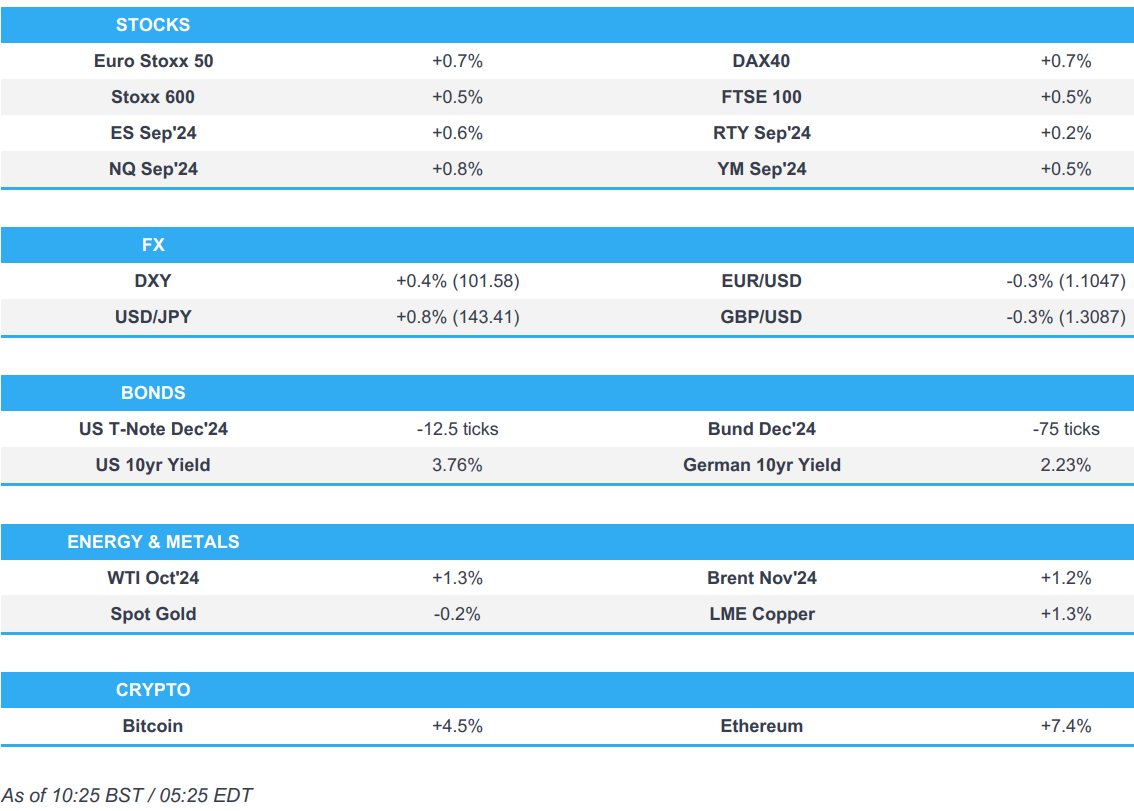

EUROPEAN TRADE

EQUITIES

- European bourses, Stoxx 600 (+0.5%) began the session on a firmer footing and continued to edge higher as sentiment continued to improve as the session progressed.

- European sectors are entirely in the green; Tech is the best performer, propped up by gains in semi-conductor names, as they attempt to pare back some of the last week’s hefty losses; ASML (+2.5%), BE Semi (+2%). Luxury is towards the foot of the pile, hampered by a double broker downgrade for Kering (-2.7%), with poor Chinese inflation metrics also not helping.

- US equity futures (ES +0.6, NQ +0.8%, RTY +0.3%) are entirely in the green, attempting to pare back some of the hefty losses seen in the prior session. Data docket for today is light, but Tech traders will be focused on Apple’s iPhone event later today.

- Apple’s (AAPL) new iPhone will use Arm’s (ARM) next-gen chip technology for AI, according to FT.

- Boeing (BA) said it reached a tentative agreement with the International Association of Machinists and Aerospace Workers and district lodges for a 25% wage hike, according to Reuters. Elsewhere, Dalian Airlines Boeing (BA) 737 flight has suffered engine malfunction on Monday en route from Dalian to Beijing, safely returned to Dalian airport, according to Chinese State Media.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is on the march this morning with USD gains strongest vs. CHF and JPY. DXY has picked itself up from a 100.58 base on Friday to a current session peak of 101.59.

- EUR is losing ground to the USD after slipping back onto a 1.10 handle last Friday. The current session low at 1.1046 is still a bit away from last week’s 1.1026 trough.

- Cable has slipped below the 1.31 mark and slipped under last week’s low at 1.3087 after failing to hold above 1.32 last week. UK-specific newsflow light today, but will see the region’s jobs report on Tuesday.

- JPY is the laggard across the majors after posting a run of four consecutive sessions of gains and following downward revisions to Q2 GDP. USD/JPY has picked itself up from a 141.77 base on Friday to a current session high of 143.43 (still sub-Friday’s peak at 144.04).

- Antipodeans are both softer vs. the USD but NZD more so with NZD/USD extending on Friday’s downside. AUD/USD is seeking some comfort in higher coppers but ultimately is lower vs. the USD following soft Chinese inflation metrics overnight

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are pulling back following a session of gains on Friday in the wake of the August NFP print and comments from Fed’s Waller, Williams and Goolsbee. Today’s data docket remains light, focus is on NY Fed SCE, but traders will ultimately be attentive of the Presidential Debate on Tuesday and CPI on Wednesday. From a yield perspective, the 10yr has recovered to circa 3.75% after briefly taking out the August low @ 3.667%.

- Bunds are following suit to the losses in global fixed-income markets. Fresh EZ-driver remains light. However, this is not set to remain the case with the ECB rate decision on Thursday looming large. From a yield perspective, the German 10yr is back within the 2.2-25% band after a sharp move on Friday which briefly dragged it as low as 2.147%.

- Gilts are on the backfoot after an indecisive session on Friday. In terms of UK specific updates, a monthly REC/KPMG report showed the UK labour market cooled noticeably in August as job placements declined sharply and pay growth slowed. From a yield perspective, the UK 10yr is just below the 3.95% mark.

- China’s Finance Ministry says it will issue up to EUR 2bln of Euro Sovereign Bond in Paris on Sept 23.

- Click for a detailed summary

COMMODITIES

- Crude is on a firmer footing, in what has been a choppy session for the complex thus far. Softer-than-expected Chinese inflation metrics have been unable to cap overnight gains, but also in the context of bullish OPEC+ headlines last week. Brent’Nov currently sits in a USD 71.42-72.21/bbl range.