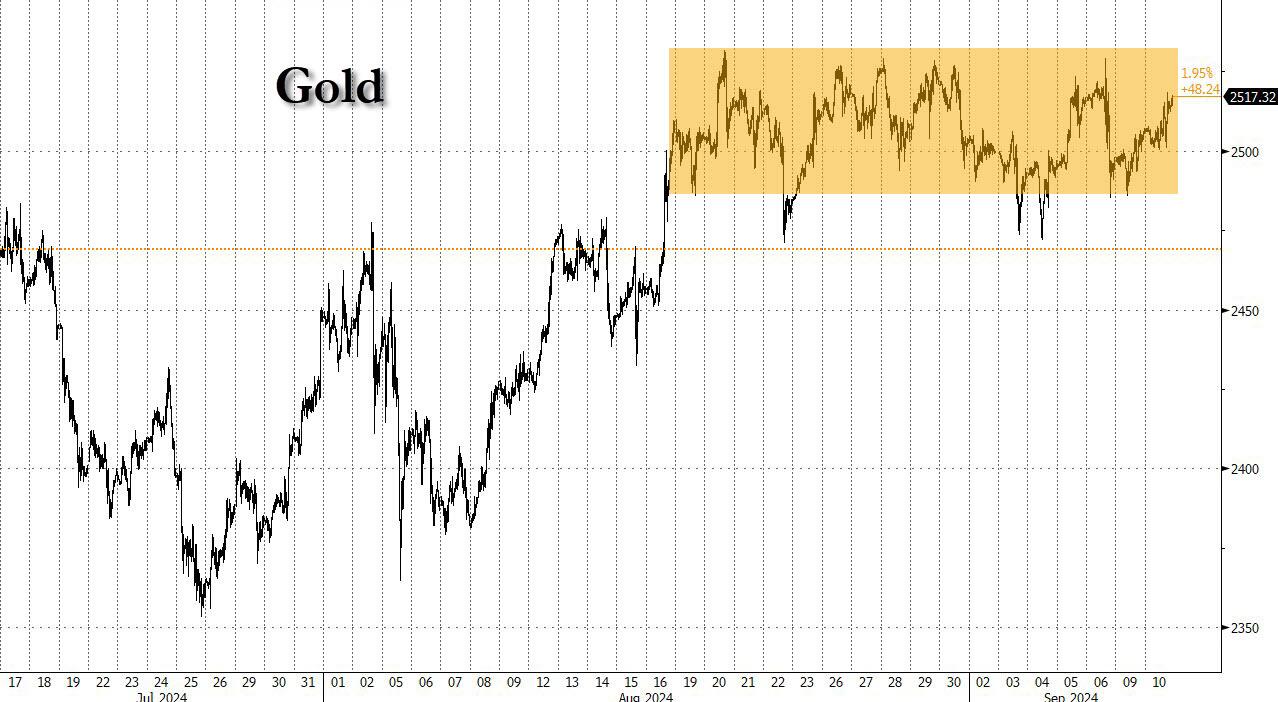

GOLD PRICE CLOSED UP $12.00TO $2515,20

SILVER PRICE DOWN $.06 TO $28.28

Gold ACCESS CLOSED $2515.30

Silver ACCESS CLOSED: $28.40

Friday is OTC/London LBMA options expiry which is much bigger than comex.

Bitcoin morning price:$57,1111UP 363 DOLLARS.

Bitcoin: afternoon price: $58114 up 1366 DOLLARS

Platinum price closing DOWN$3.80 TO $941,80

Palladium price; DOWN $32,70 TO $916.30

END

*CANADIAN GOLD: $3423.88 UP 24.62 CDN dollars per oz( * NEW ALL TIME HIGH 3,431.95 CDN DOLLARS PER OZ//AUG 16 2024)

*BRITISH GOLD: 1,923.45UP 5.77Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1937.75 BRITISH POUNDS/OZ) AUGUST 16/2024

*EURO GOLD: 2,283.00UP 11.91 Euros per oz //* (ALL TIME CLOSING HIGH: 2.283,00EUROS PER OZ//SEPT 10 //.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,501.800000000 USD

INTENT DATE: 09/09/2024 DELIVERY DATE: 09/11/2024

FIRM ORG FIRM NAME ISSUED STOPPED

323 C HSBC 2

363 H WELLS FARGO SEC 18

435 H SCOTIA CAPITAL 2

657 C MORGAN STANLEY 2

661 C JP MORGAN 4

737 C ADVANTAGE 41 13

TOTAL: 41 41

MONTH TO DATE: 3,881

JPMorgan stopped 38/212

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2024. CONTRACT: 41 NOTICES FOR 4100 OZ or 0.1275 TONNES

total notices so far: 3881contracts for 388,100 Oz (12.0216 tonnes)

FOR SEPT:

SILVER NOTICES: 65 NOTICE(S) FILED FOR 325,000 OZ/

total number of notices filed so far this month : 4,799 for 23.995 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $12.00 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ NO CHANGES IN GOLD INVENTORY AT THE GLD:

/ /INVENTORY RESTS AT 862.74 TONNES

INVENTORY RESTS AT 862.74 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $.06 AT THE SLV

SMALL CHANGES IN SILVER INVENTORY AT THE SLV: ..A WITHDRAWAL OF 639,000 OZ OF SILVER AT THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 465.549 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 841 CONTRACTS TO 128,665 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS STRONG LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR STRONG GAIN OF $0.45 IN SILVER PRICING AT THE COMEX ON MONDAY’S TRADING. WE LOST ZERO NET LONGS WITH THE GIN IN PRICE. WE HAD A TINY GAIN OF 3 CONTRACTS ON OUR TWO EXCHANGES. WE HAD AGAIN A HUGE LIQUIDATION OF T.A.S. CONTRACTS DURING MONDAY’S TRADING//. WE HAD CONSIDERABLE SHORT COVERING BY OUR SPECS WITH THE STRONG GAIN IN PRICE. WE HAD A STRONG 560 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY ANOTHER HUGE 1015 CONTRACT T.A.S ISSUANCE. IN ESSENCE WE LOST A FAIR 481 CONTRACTS ON OUR TWO EXCHANGES DESPITE THE HUGE GAIN IN PRICE.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN YESTERDAY. THE ACCUMULATED T.A.S. IS BEING USED TO MANIPULATE PRICES AT THE COMEX NOW EVERY DAY..

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 1015 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS BUT TO NO AVAIL. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.45) AND WERE UNSUCCESSFUL IN KNOCKING ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A TINY GAIN OF 3 TOTAL OI CONTRACTS ON OUR TWO EXCHANGES.

WE HAD A HUGE 560 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 22.765 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 265000 OZ QUEUE JUMP//NEW STANDING ADVANCES TO 24.270 MILLION OZ

//NEW STANDING FOR SILVER//SEPT ADVANCES TO 24.070 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI LOSS //STRONG SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1015 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 284 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT

TOTAL CONTRACTS for 6 DAYS, total 4636 contracts: OR 23.180 MILLION OZ (772 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 23,180 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL PROBABLY BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 23,180 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 841 CONTRACTS DESPITE OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS:560 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 22.765 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE 265,000 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR SEPT ADVANCES TO 24.270 MILLION OZ

WE HAVE A FAIR LOSS OF 481 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE HUGE GAIN IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 1015 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX TRADING//// MASSIVE ATTEMPTED SHORT COVERING FROM OUR SPEC SHORTS WITH THE GAIN IN PRICE MONDAY/ AND ZERO LIQUIDATION OF LONGS. ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER.

THE NEW TAS ISSUANCE MONDAY NIGHT (1015) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND FOR SURE TODAY., .

WE HAD 65 NOTICE(S) FILED TODAY FOR 325,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 1311 OI CONTRACTS TO 506,476 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 1321 CONTRACTS//

WE HAD A FAIR SIZED DECREASE IN COMEX OI (1311 CONTRACTS) OCCURRED DESPITE OUR STRONG GAIN OF $12.95 IN PRICE /MONDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT AT 12.885 TONNES ON FIRST DAY NOTICE FOLLOWED BY MONDAYS STRONG 8,800 OZ QUEUE JUMP

NEW STANDING ADVANCES TO 12.329 TONNES

/ ALL OF THIS HAPPENED WITH OUR $12.95 GAIN IN PRICE WITH RESPECT TO MONDAY’S TRADING. WE HAD A FAIR SIZED GAIN OF 1695 OI CONTRACTS (5.272 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 3006 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 506,476

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1695 CONTRACTS WITH 1311 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 3007 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1695 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL SIZED 656 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3007 CONTRACTS) ACCOMPANYING THE FAIR SIZED DECREASE IN COMEX OI OF 1311 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 1695 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT 12.885 TONNES FOLLOWED BY TODAY’S 8800 OZ QUEUE JUMP

//NEW STANDING ADVANCES TO: /SEPT 12.329TONNES.

/ 3) SMALL T.A.S. LIQUIDATION WITH ZERO NET LONG SPECS BEING CLIPPED,

4) FAIR SIZED COMEX OPEN INTEREST DECREASE 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///SMALL T.A.S. ISSUANCE: 656 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

SEPT.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

TOTAL EFP CONTRACTS ISSUED: 30,140 CONTRACTS OF 3,014,000OZ OR 93.74TONNES IN 6 TRADING DAY(S) AND THUS AVERAGING: 5023 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 6 TRADING DAY(S) IN TONNES 93.74 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 93.74 DIVIDED BY 3550 x 100% TONNES = 2.64% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 93.74 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPTEMBER. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 841 CONTRACTS OI TO 128,605 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1015 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 1015 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1015 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 841 CONTRACTS AND ADD TO THE 1015 E.FP. ISSUED

WE OBTAIN A FAIR SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 481 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 2.405 MILLION OZ OCCURRED DESPITE OUR $0.45 GAIN IN PRICE

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING/MONDAY NIGHT

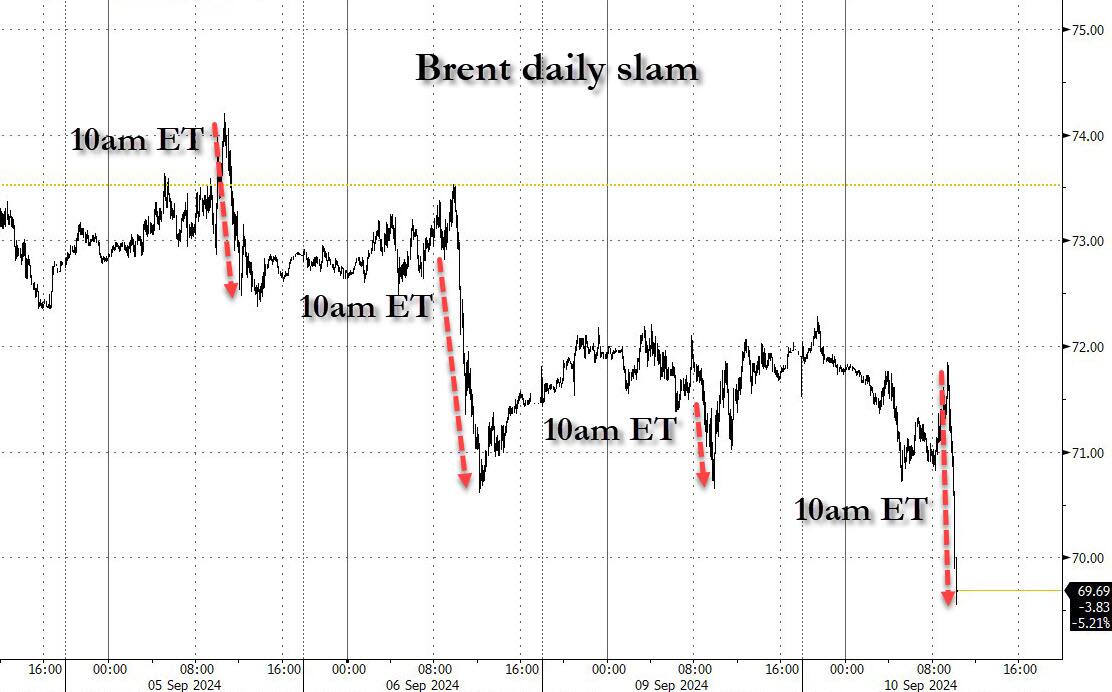

SHANGHAI CLOSED UP 7.70 PTS OR 0.28% //Hang Seng CLOSED UP 37.03 PTS OR 0.22% // Nikkei CLOSED DOWN 56..59 OR 0.18%//Australia’s all ordinaries CLOSED UP 0.31%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7,1191 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.1277/ Oil DOWN TO 67.82 dollars per barrel for WTI and BRENT DOWN AT 70.90 Stocks in Europe OPENED ALL MIXRD

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

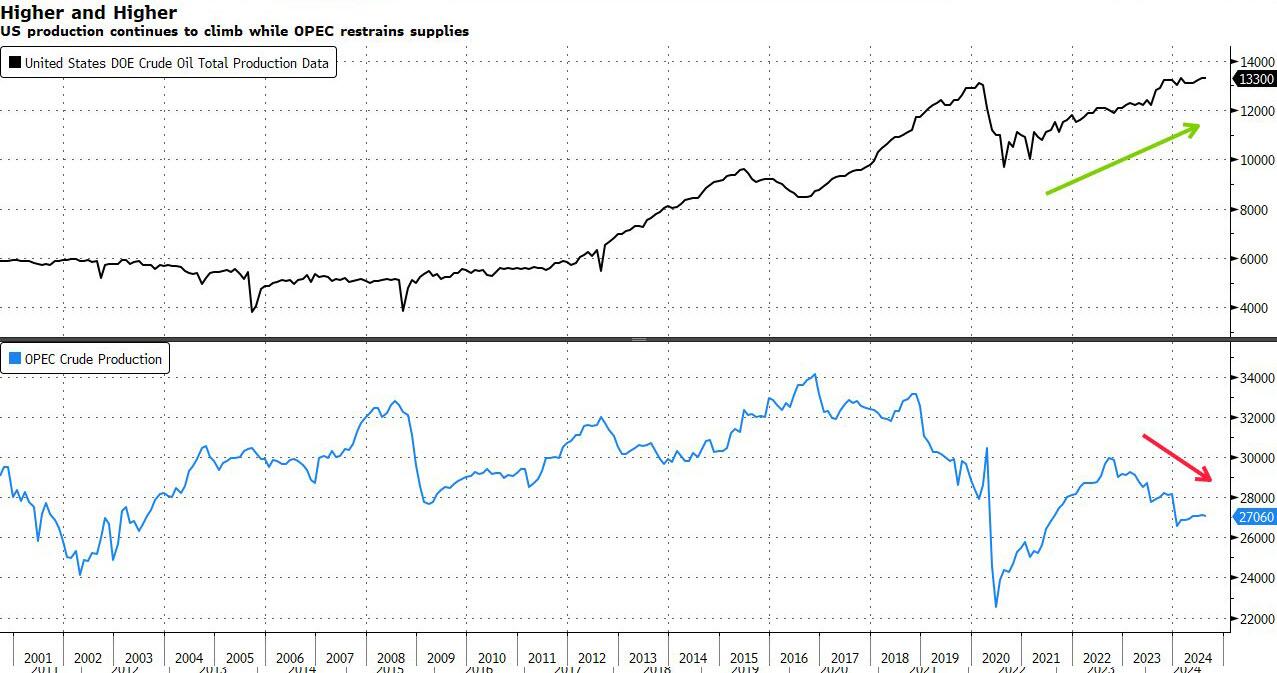

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1311 CONTRACTS TO 506,676 DESPITE OUR STRONG GAIN IN PRICE OF $12.95 WITH RESPECT TO MONDAY’S TRADING. WE LOST ZERO IN NUMBER LONGS WITH THE HIGHER PRICE FOR GOLD. THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTH DISTORTS OPEN INTEREST NUMBERS.

THE FED IS THE MAJOR SHORT OF AROUND 157+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS IS SCHEDULED TO HAPPEN LATE SEPT 2024/BEGINNING OF OCTOBER. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER CONTAINMENT.

OUR PHYSICAL LONDONERS ALSO BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT THESE PRICES AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD A MINOR T.A.S. LIQUIDATION ON MONDAY’S HUGE GAIN IN PRICE WITH ZERO LONGS WERE CLIPPED (AS YOU WILL SEE BELOW) BUT WE DID HAVE MAJOR SHORT COVERING. THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF THE SPREADERS // T.A.S DURING LAST WEEK AND BEGINNING THIS WEEK IS SURELY DISTORTING COMEX OPEN INTEREST.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE NON ACTIVE DELIVERY MONTH OF SEPTEMBER.… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 3007 EFP CONTRACTS WERE ISSUED: : OCT/DEC 3007 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3007 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1695 CONTRACTS IN THAT 3000 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A FAIR LOSS OF 1311 COMEX CONTRACTS..AND THIS FAIR GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $12.95/MONDAY COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AS MENTIONED ABOVE. THE RAIDS ON LAST WEDNESDAY, FRIDAY AND THIS PAST TUESDAY AND FRIDAY WERE ORCHESTRATED BY THE FRBNY AS WE ARE NOW FINISHED WITH OPTIONS EXPIRY FOR THE OTC/LONDON LBMA BETS ENDING LAST FRIDAY AFTERNOON. DESPITE THE FED’S HUGE SHORT PREDICAMENT THEY STILL HAVE TIME AND ENERGY TO RAID OUR PRECIOUS METALS. SUCH CROOKS!

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR FRIDAY NIGHT A STRONG SIZED 3000 CONTRACTS. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE (AND SPREADERS LATE IN THE MONTH). THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S AND THIS WEEK’S TRADING//RAIDS

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: SEPT (12.329 TONNES) WHICH IS HUGE FOR A NON DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 44 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 12.329 TONNES.

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $12.95 ////AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE DID HAVE A FAIR GAIN IN OUR TWO EXCHANGES. WE HAD SOME T.A.S. SPREADER LIQUIDATION. BUT CENTRAL BANK LONGS, SEIZING THE MOMENT, EXERCISED FOR PHYSICAL IN A BIG WAY.

WE HAVE GAINED A TOTAL OI OF 9.3530 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPT (12.885 TONNES) ON FIRST DAY NOTICE FOLLOWED BY MONDAY’S QUEUE JUMP OF A GOOD SIZED 8800 OZ

//NEW STANDING FOR SEPT ADVANCES TO: 12.329 TONNES.

NEW STANDING FOR SEPT: 12.329 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $12.95

WE HAVE REMOVED 4269 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES 1695 CONTRACTS OR 169500 OZ (5.27

TONNES)

confirmed volume MONDAY 298,916contracts GOOD

//speculators have left the gold arena

END

SEPT 10 SEPTEMBER GOLD CONTRACT

/ /// THE SEPT 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | NIL . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | NIL oz |

| No of oz served (contracts) today | 212 notice(s) 21200 OZ 0.6594 TONNES |

| No of oz to be served (notices) | 83 contracts 8300 OZ 0.2582 TONNES |

| Total monthly oz gold served (contracts) so far this month | 3881notices 3881,00 oz 12.0216TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: nil oz

we have 0 customer deposits

total deposits NIL oz

withdrawals:1

jpmorgan 30,102.592 oz removed from eligible

TOTAL WITHDRAWALS

30,102.592 oz

adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPTEMBER

For the front month of SEPT. we have an oi of 124 contracts having LOST 152 contracts. We had 212 notices filed on MONDAY so we GAINED 88 contracts or 8800 oz will stand at the comex as these boys seek metal on this side of the pond.

OCTOBER LOST 558 CONTRACTS UP TO 41,936 CONTRACTS

NOVEMBER GAINED 6 CONTRACTS TO STAND AT 86

DECEMBER, THE BIGGEST DELIVERY MONTH LOST 1063 CONTRACTS TO 406,196.

We had 41 contracts filed for today representing 4100 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notice issued from their client or customer account. The total of all issuance by all participants equate to 41 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 2 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for SEPT /2024. contract month, we take the total number of notices filed so far for the month (3881( x 100 oz ) to which we add the difference between the open interest for the front month of SEPT 124 CONTRACTS) minus the number of notices served upon today (41 x 100 oz per contract( equals 396,400 OZ OR 12.329 TONNES.

thus the INITIAL standings for gold for the SEPTEMBER contract month: No of notices filed so far (3881 x 100 oz +we add the difference for front month of SEPT (x124X// , OI} minus the number of notices served upon today (41) x 100 oz which equals 396,400 oz (12.329 TONNES)

TOTAL COMEX GOLD STANDING FOR SEPT.: 12.329 TONNES WHICH IS HUGE FOR THIS NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,780,327.447 oz 55.375 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,067,536.861 OZ

TOTAL REGISTERED GOLD 7,425,642.244 ( 230.96 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,641,694l67OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 5,645,315 oz (REG GOLD- PLEDGED GOLD)= 175.59 tonnes //

END

SILVER/COMEX

SEPT 10/2024

INITIAL

//2024// THE SEPT 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 879,393.119OZ Delaware asahi Loomis Manfra . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 1,193,279,570 oz ASAHI Loomis 604,950.900 OZ asahi delaware |

| No of oz served today (contracts) | 65 CONTRACT(S) (325,000 OZ) |

| No of oz to be served (notices) | 55 contracts (0.275 million oz) |

| Total monthly oz silver served (contracts) | 4799 Contracts (12.995 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit/

total dealer deposit : NIL oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 customer deposits:

i) Into ASAHI: 593,740.100 oz

ii) Into Loomis: 599,535.470 oz

total customer deposit 1,193,279.570 oz

JPMorgan has a total silver weight: 134.996million oz/306.575 million or 44.03%

adjustment:2

c) dealer to customer Loomis 40,659,640oz

d) dealer to customer Delaware 143,288,290 oz

withdrawals: 1

i) Out of Delaware 46,321.838 oz

total customer withdrawals: 46,321.838 oz

TOTAL REGISTERED SILVER: 77.302 MILLION OZ//.TOTAL REG + ELIGIBLE. 306.575 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR SEPTEMBER:

silver open interest data:

FRONT MONTH OF SEPT/2024 OI: 120 CONTRACTS HAVING LOST 3 CONTRACT(S).

WE HAD 56 NOTICES FILED ON MONDAY, SO WE GAINED 53 CONTRACTS OR 265,000 OZ

UNDERWENT A QUEUE JUMP TO TAKE DELIVERY OF SILVER OVER ON THIS SIDE OF THE POND..

THERE MUST BE ENOUGH SILVER OVER HERE.

OCTOBER SAW ANOTHER GAIN OF 37 OF OPEN INTEREST CONTRACTS AND THUS WE HAVE 1377 OPEN INTEREST CONTRACTS FOR OCTOBER.

NOVEMBER SAW ITS ANOTHER GAIN OF 6 CONTRACTS TO STAND AT 23.

DECEMBER SAW A LOSS OF 1252 CONTRACTS UP TO 113,313.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 65 for 325,000 oz

CONFIRMED volume; ON MONDAY 57,488 WEAK

To calculate the number of silver ounces that will stand for delivery in SEPT. we take the total number of notices filed for the month so far at 4799 x 5,000 oz = 23.995 MILLION oz

to which we add the difference between the open interest for the front month of SEPT(120) and the number of notices served upon today 65x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT/2024 contract month: 4799 notices served so far) x 5000 oz + OI for the front month of SEPT (120)x number of notices served upon today minus (65)x 5000 oz of silver standing for the SEPT contract month equates to 24.270 MILLION OZ.

New total standing: 24.270 million oz.

There are 77,743 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS//

GLD

SEPT 10 WITH GOLD UP $12.00ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 9 WITH GOLD UP $12.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 6 WITH GOLD DOWN $17.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 5 WITH GOLD UP $18.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 4 WITH GOLD UP $3.45 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 3 WITH GOLD DOWN $4.25 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 5,47 TONNES OF GOLD INTO THE GLD/:/ //////INVENTORY RESTS AT 862.74 TONNES

AUGUST 30 WITH GOLD DOWN $31.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD/:/ //////INVENTORY RESTS AT 857.27 TONNES

AUGUST 29 WITH GOLD UP $23.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 28 WITH GOLD DOWN $14.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 27 WITH GOLD DOWN $1.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 26 WITH GOLD UP $9.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD VAPOUR GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 23 WITH GOLD UP $29.70 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER WITHDRAWAL OF 8.88 TONNES OF GOLD VAPOUR GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 857.85 TONNES

AUGUST 22 WITH GOLD DOWN $28.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 9.43 TONNES OF GOLD VAPOUR GOLD INTO THE GLD./ //////INVENTORY RESTS AT 866.70 TONNES

AUGUST 21 WITH GOLD DOWN $1.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER WITHDRAWAL OF 1.73 TONNES OF GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 857.27 TONNES

AUGUST 20 WITH GOLD UP $9.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 4.03 TONNES OF GOLD VAPOUR INTO THE GLD./ //////INVENTORY RESTS AT 859.00 TONNES

AUGUST 19 WITH GOLD UP $3.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 7.19 TONNES OF GOLD VAPOUR INTO THE GLD./ //////INVENTORY RESTS AT 854.97 TONNES

AUGUST 16 WITH GOLD UP $44.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: //////INVENTORY RESTS AT 847.78 TONNES

AUGUST 15 WITH GOLD UP $13,70 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD OUT OF THE GLD//////INVENTORY RESTS AT 847.78 TONNES

AUGUST 14 WITH GOLD DOWN $26.20 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.03 TONNES OF GOLD OUT OF THE GLD//////INVENTORY RESTS AT 845.76 TONNES

AUGUST 13 WITH GOLD UP $3.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//////INVENTORY RESTS AT 849.79 TONNES

AUGUST 12 WITH GOLD UP $30.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ////INVENTORY RESTS AT 846.91 TONNES

AUGUST 9 WITH GOLD UP $10.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 846.91 TONNES

AUGUST 8 WITH GOLD UP $31.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.02 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 844.04 TONNES

AUGUST 7 WITH GOLD UP $1.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.16 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 848.06 TONNES

AUGUST 6 WITH GOLD DOWN $13.10 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD” A WITHDRAWAL OF .57 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 844.90 TONNES

AUGUST 2 WITH GOLD DOWN $9.95 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.58 TONNES OF GOLD OUT OF THE GLD//INVENTORY RESTS AT 845.47 TONNES

AUGUST 1 WITH GOLD UP $9.15 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 846.05 TONNES

GLD INVENTORY: 862.74 TONNES, TONIGHTS TOTAL

SILVER

SEPT 10//WITH SILVER DOWN $.06/SMALL CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 639,000 OZ OF SILVER FROM THE SLV./. /: .///./// /INVENTORY AT 465.549MILLION OZ

SEPT 9//WITH SILVER UP $0.45//SMALL CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 46,000 OZ OF SILVER FROM THE SLV./. /: .///./// /INVENTORY AT 466.188 MILLION OZ

SEPT 6//WITH SILVER DOWN $.84//NO CHANGES IN SILVER INVENTORY /: .///./// /INVENTORY AT 466.234 MILLION OZ

SEPT 5//WITH SILVER UP $.55//SMALL CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 0.193 MILLION OZ OF SILVER INTO THE SLV/: .///./// /INVENTORY AT 466.234 MILLION OZ

SEPT 4//WITH SILVER UP $.17//SMALL CHANGES IN SILVER INVENTORY A DEPOSIT OF 0.456 MILLION OZ OF SILVER INTO THE SLV/: .///./// /INVENTORY AT 466.427 MILLION OZ

SEPT 3//WITH SILVER DOWN $.74//HUGE CHANGES IN SILVER INVENTORY A DEPOSIT OF 1.278 MILLION OZ OF SILVER INTO THE SLV/: .///./// /INVENTORY AT 465.971 MILLION OZ

AUGUST30//WITH SILVER DOWN $.42//NO CHANGES IN SILVER INVENTORY: .///./// /INVENTORY AT 464.693 MILLION OZ

AUGUST 29//WITH SILVER UP $.37//SMALL CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 0.558 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 464.693 MILLION OZ

AUGUST 28//WITH SILVER DOWN $0.76//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 2.301 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 465.281 MILLION OZ

AUGUST 27//WITH SILVER DOWN $0.03//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 2.921 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 462.959 MILLION OZ

AUGUST 26//WITH SILVER UP $0.23//SMALL CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 45,000 OZ OUT OF THE SLV. .///./// /INVENTORY AT 465.880 MILLION OZ

AUGUST 23//WITH SILVER UP $0.72//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 1.506 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 465.925 MILLION OZ

AUGUST 22//WITH SILVER DOWN $0.44//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 0.943 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 468.344 MILLION OZ

AUGUST 21//WITH SILVER $0.03//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 1..552 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 468.344 MILLION OZ

AUGUST 20//WITH SILVER $0.24//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 1.369 MILLION OZ FROM THE SLV. .///./// /INVENTORY AT 466.792 MILLION OZ

AUGUST 19//WITH SILVER $0.39//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 1.506 MILLION OZ FROM THE SLV. .///./// /INVENTORY AT 465.423 MILLION OZ

AUGUST 16//WITH SILVER $0.49//NO CHANGES IN SILVER INVENTORY: .///./// /INVENTORY AT 466.929 MILLION OZ

AUGUST 15//WITH SILVER $1.14//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.186 MILLION ON INTO THE SLV.///./// /INVENTORY AT 466.929 MILLION OZ

AUGUST 14//WITH SILVER DOWN $0.40//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 13//WITH SILVER DOWN $0.19//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 12//WITH SILVER UP $.37//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 9//WITH SILVER DOWN $.03//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 8//WITH SILVER UP $.70//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 3.241 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 7//WITH SILVER DOWN $0.27//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.552 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 6//WITH SILVER UP $0.05//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 458.851 MILLION OZ

AUGUST 2//WITH SILVER DOWN $0.01//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 1.243 MILLION OZ OF SILVER OUT OF THE SLV ///./// /INVENTORY AT 460.961 MILLION OZ

AUGUST 1//WITH SILVER DOWN $0.46//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.608 MILLION OZ OF SILVER VAPOUR INTO THE SLV///./// /INVENTORY AT 462.204 MILLION OZ

CLOSING INVENTORY 466.188 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

end

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY//BILL HOLTER:

3.CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHE

END

4. OTHER GOLD COMMENTARIES/:live from the vault

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:silver

6 CRYPTOCURRENCY NEWS

END

ASIA TRADING/TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED UP 7.70 PTS OR 0.28% //Hang Seng CLOSED UP 37.03 PTS OR 0.22% // Nikkei CLOSED DOWN 56..59 OR 0.18%//Australia’s all ordinaries CLOSED UP 0.31%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7,1191 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.1277/ Oil DOWN TO 67.82 dollars per barrel for WTI and BRENT DOWN AT 70.90 Stocks in Europe OPENED ALL MIXRD

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1177

OFFSHORE YUAN: DOWN TO 7.1278

SHANGHAI CLOSED UP 7.70 PTS OR 0.28 %

HANG SENG CLOSED UP 37.13 PTS OR 0.22%

2. Nikkei closed DOWN 56.59 PTS OR 0.18%

3. Europe stocks SO FAR: ALL MOSTLY MIXED

USA dollar INDEX UP TO 101.59 EURO FALLS TO 1.1038 DOWN 5 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +0.898 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 143.05…… JAPANESE YEN NOW RISING AS WE HAVE NOW REACHED THE COLLAPSING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.183/Italian 10 Yr bond yield DOWN to 3.552 SPAIN 10 YR BOND YIELD DOWN TO 3.022

3i Greek 10 year bond yield DOWN TO 3.215

3j Gold at $2506//Silver at: 28.45 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 12/ 100 roubles/dollar; ROUBLE AT 91,00

3m oil into the 68 dollar handle for WTI and 70 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 143.05/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.898 % STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8474 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9349 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.718UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.010 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.685 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 34.06…

10 YR UK BOND YIELD: 3.905 DOWN 4 PTS

10 YR CANADA BOND YIELD: 3.01 8 DOWN 2 BASIS PTS

5 YR CANADA BOND YIELD: 2.807 UP 1 PTS.

2a New York OPENING REPORT

Futures Rise Ahead Of Trump-Harris Debate

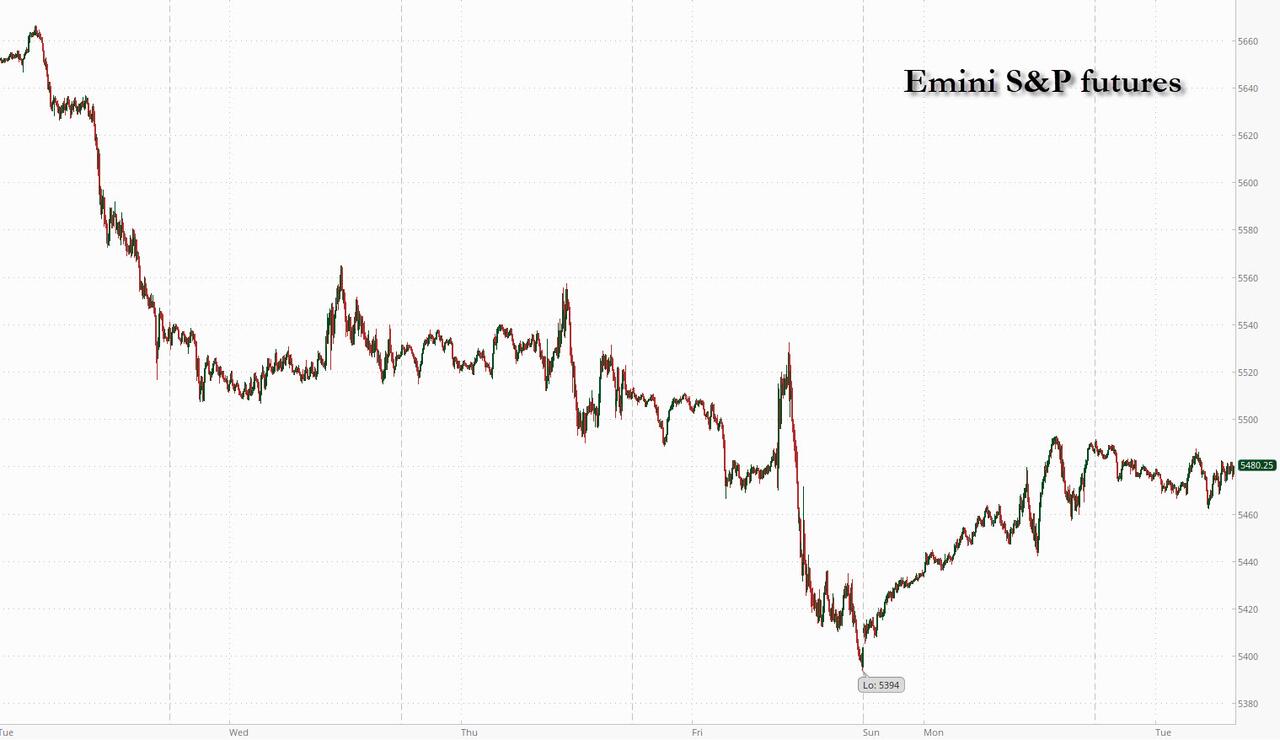

Tuesday, Sep 10, 2024 – 08:16 AM

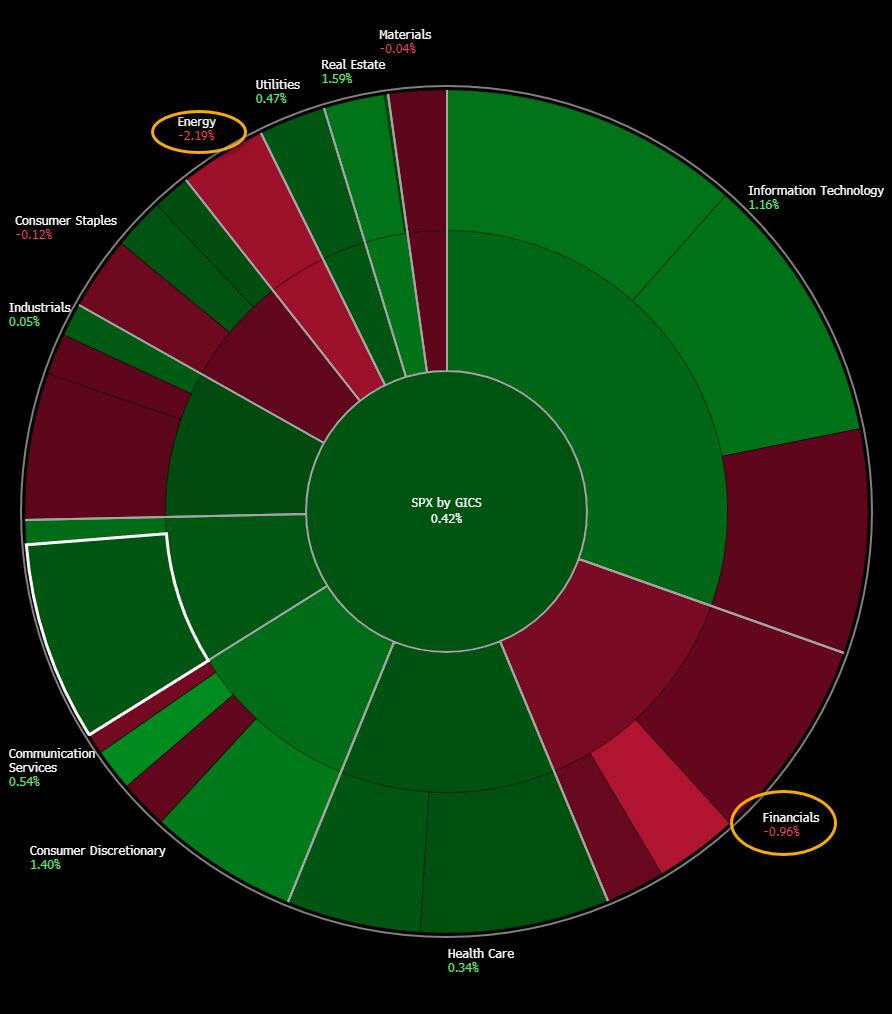

US equity futures rose, trading near session highs after they rebounding off overnight lows as markets head into a crunch period, with key inflation data on Wednesday followed by the Fed’s interest-rate decision next week. As of 8:00am ET, S&P futures were up 0.1% trading in a narrow range after the underlying gauge rose 1.2% on Monday, rebounding from its worst start to the month in data going back to 1953; Nasdaq futures were down 0.2% as Mag7 and Semis are weaker while Financials rise following a Bloomberg report of lower capital requirements. Treasury yields rose a second day, higher by 1-2 bps while the USD held Monday’s gains. Commodities are mixed with metals up, energy down, and Ags mixed. The macro data in focus is on the Small Biz Optimism print (which dropped to 91.2 from 93.7, missing estimates) and the Presidential Debate.

In premarket trading, Oracle jumped 8% after reporting quarterly profit and bookings that topped estimates, signaling that artificial intelligence demand continues to boost its cloud computing business. Apple shares slid 1% after the iPhone maker lost its court fight over a $14.4 billion Irish tax bill. Here are some other notable premarket movers:

- Mission Produce jumps 22% after the avocado supplier reported fiscal third-quarter revenue that topped the average of two analyst estimates compiled by Bloomberg.

- Rubrik drops 6% after the cybersecurity company reported earnings; Bloomberg Intelligence notes that doubts about growth in the second half of the year could linger.

- Viridian Therapeutics gains 8% ahead of a conference call this morning when the company will report topline data for the Thrive phase 3 clinical trial evaluating VRDN-001 in patients with active thyroid eye disease.

As Bloomberg notes, the market mood has been cautious as investors look to balance US recession fears and the likelihood of a soft landing, amid worries the Fed may be falling behind the curve as the labor market cools. Meanwhile, US political risk is back at the forefront, with former President Donald Trump squaring off in a debate with US Vice President Kamala Harris later Tuesday. Meanwhile, according to Nate Silver, Trump’s chance of winning just hit 64.4%, the highest yet.

“We need to see what actually plays out and will have the possibility of impacting markets,” Grace Peters, global head of investment strategy at JPMorgan Private Bank, said on Bloomberg TV. “We will be watching tariffs, trade policy, taxes.”

Amid the rising uncertainty hedge funds have been unwinding their positions to get cash ready for volatility ahead of the Nov. 5 vote, according to Goldman Prime Brokerage data. At Newton Investment Management, head of fixed income Ella Hoxha is avoiding assets exposed to “a weaker cyclical backdrop, potentially wider credit spreads and weaker commodity currencies,” she said in an interview with Bloomberg TV. Since Friday, the firm has been boosting safe assets including US Treasury and Japanese government debt, she said.

European stocks declined but still traded within Monday’s levels. Heath care, autos and energy are the worst-performing sectors in Europe’s Stoxx 600 while the commodity-heavy FTSE 100 lags regional peers with a 0.6% drop. The ECB’s policy meeting later in the week is also weighing on risk appetite. The central bank meets Thursday, where it is expected to deliver a second interest rate cut this year to tackle a faltering economy.

Earlier, Asian stocks were also mixed as a reversal of early losses in China offset declines in Japan and Korea. The MSCI Asia Pacific Index traded in a tight range, with health-care firms among the biggest drags. Japan’s Topix reversed earlier gains to drop for a fifth day as the strong yen weighed on investor sentiment. Chinese stocks rose in late trading, closing slightly higher, though the CSI 300 Index is still hovering near its lowest close since January 2019. Latest data releases have added to worries over spiraling deflation in Asia’s largest economy, while the progress in US legislation that would blacklist some Chinese biotech firms adds to headwinds for the nation’s equities.

In FX, the Bloomberg dollar spot index inches marginally higher ahead of the Trump-Harris presidential debate. Pound steady at $1.30 after UK pay growth cooled to a two-year low in the three months through July. JPY underperforms G-10 FX after a Bloomberg report said that Bank of Japan officials see little need to raise the benchmark rate when board members gather next week. Morgan Stanley sees the euro sliding toward parity with the dollar within months amid risks of aggressive ECB policy easing. The US bank expects the single currency to slump to $1.02 by year-end, a roughly 7% depreciation from its current level of $1.1037. The call is the most bearish among currency analysts surveyed by Bloomberg.

In rates, treasuries are slightly cheaper across the curve amid comparable losses for bunds and gilts following several European bond sales skewed toward longer-dated maturities. Yields are higher by 1bp-2bp across the curve, the 10-year around 3.715% and slightly cheaper vs bunds and gilts in the sector, with curve spreads little changed. Coupon auction cycle begins at 1pm New York time with $58b 3-year new issue, followed by $39b 10-year and $22b 30-year reopenings Wednesday and Thursday. WI 3-year yield at around 3.515% is ~29.5bp richer than last month’s, which stopped through by 0.2bp following a selloff. Calendar events are limited ahead of the presidential debate slated to start at 9pm New York time.

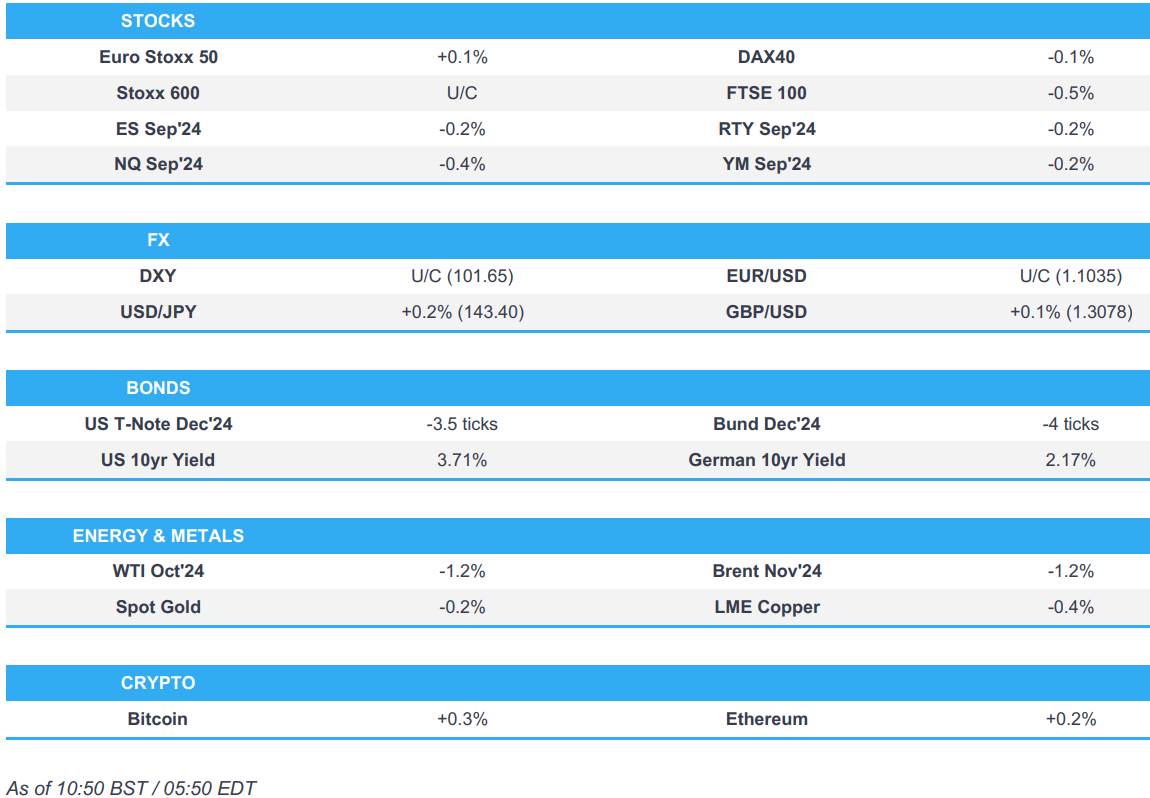

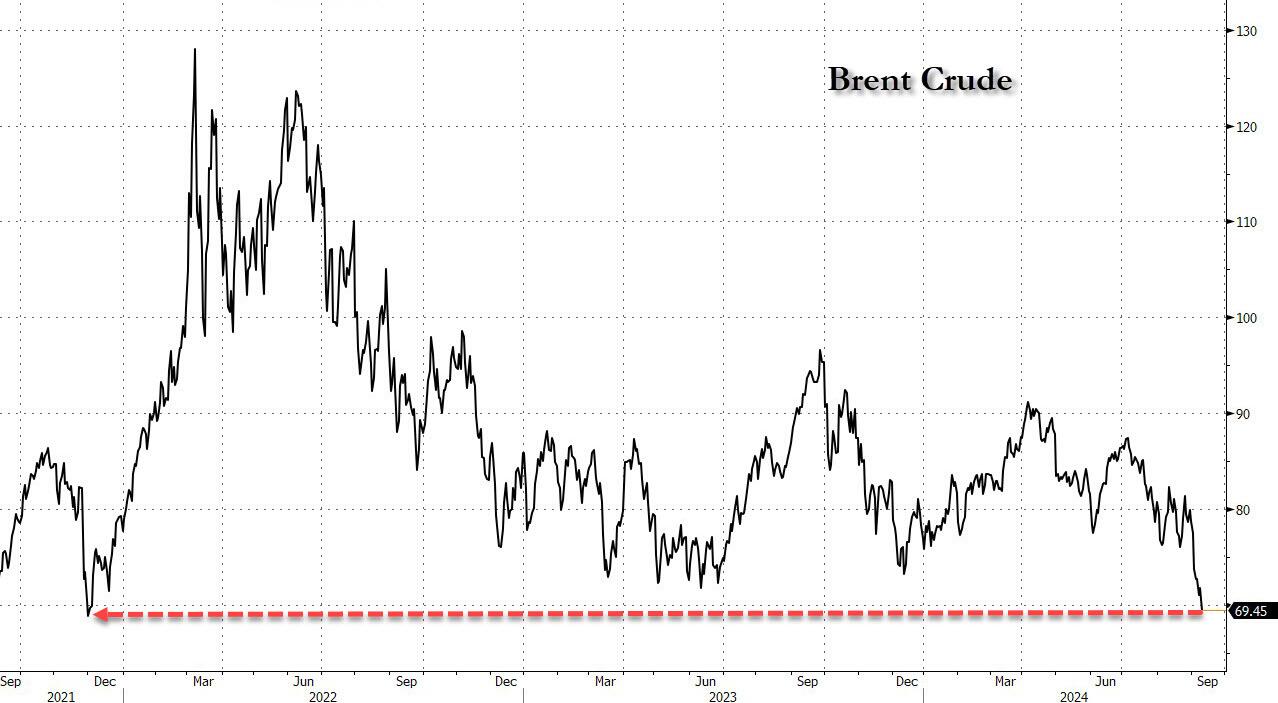

In commodities, Brent crude underperforms commodities with a 1.2% drop to near $71 a barrel. Spot gold falls roughly $5 to trade near $2,502/oz.

Bitcoin continues to edge higher, now sitting above USD 57k whilst Ethereum holds around USD 2.3k.

Looking to the day ahead now, the main highlights will be the TV debate tonight between Kamala Harris and Donald Trump. Otherwise, data releases include UK unemployment and Italian industrial production for July, whilst in the US there’s the NFIB’s small business optimism index for August. Finally from central banks, we’ll hear from Fed Vice Chair for Supervision Barr.

Market Snapshot

- S&P 500 futures little changed at 5,481.75

- STOXX Europe 600 up 0.2% to 511.94

- MXAP down 0.2% to 179.60

- MXAPJ up 0.1% to 558.71

- Nikkei down 0.2% to 36,159.16

- Topix down 0.1% to 2,576.54

- Hang Seng Index up 0.2% to 17,234.09

- Shanghai Composite up 0.3% to 2,744.19

- Sensex up 0.7% to 82,145.49

- Australia S&P/ASX 200 up 0.3% to 8,011.94

- Kospi down 0.5% to 2,523.43

- German 10Y yield little changed at 2.18%

- Euro little changed at $1.1035

- Brent Futures down 0.4% to $71.58/bbl

- Gold spot down 0.2% to $2,501.26

- US Dollar Index up 0.13% to 101.69

Top overnight news

- Largest US banks’ capital hike was reduced in half under the latest plan by regulators in which banks would face a 9% increase in capital requirements instead of the 19% that was originally called for by the Fed, FDIC and the Office of the Comptroller of the Currency: BBG

- China’s exports come in ahead of expectations for Aug (+8.7% vs. the Street +6.6%) as companies seek out int’l markets amid soft domestic demand while imports fell short (+0.5% vs. the Street +2.5%). RTRS

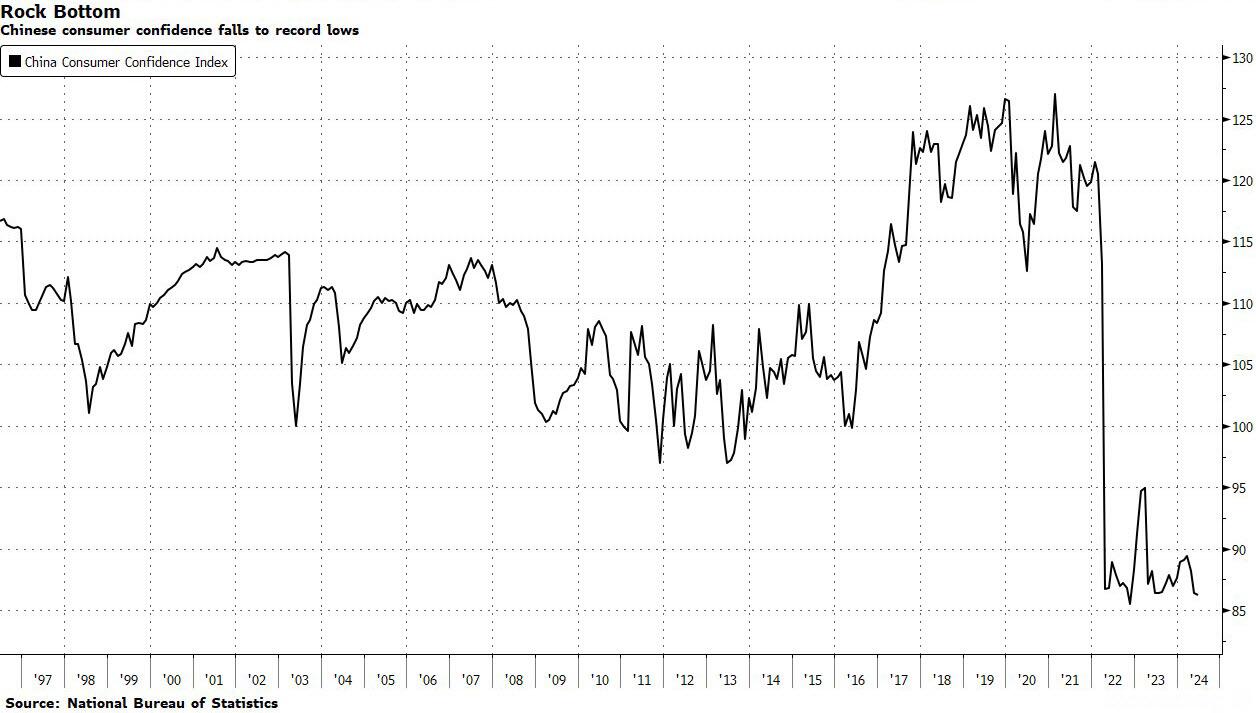

- A deepening selloff in Chinese stocks is exacerbating a crisis of confidence in the world’s second-largest economy, heaping pressure on policymakers to halt the downward spiral. BBG

- China urged by economists to enact a ~$1.4T stimulus plan amid dire economic trends, including intensifying disinflationary pressures. FT

- BOJ officials see “little need” to hike rates at their meeting next week (Bloomberg); UK wage growth eased to +4% in Jul (vs. +4.6% in June), keeping the BOE on a path to continue easing policy (although rates are expected to stay unchanged at next week’s meeting). BBG

- Norway’s underlying inflation continued to ease in Aug (but was inline w/expectations), bolstering expectations for the country’s central bank to cut rates this year. BBG

- Apple and Google lost landmark EU decisions in a win for the bloc’s crackdown on tech companies. Apple was fighting a €13 billion Irish tax bill, while Google had sought to topple a €2.4 billion antitrust fine. BBG

- US regulators scaled back a proposed capital requirement hike for the biggest banks, to 9% from 19%, people familiar said. The move will probably appease banks and may also help Fed Chair Jerome Powell gain support from the central bank’s board. BBG

- Apollo and other PE firms are muscling into the $15 trillion US life insurance and retirement savings market, shaking up traditional insurers as they push back with regulators caught in the middle. BBG

- Tonight’s debate between Kamala Harris and Donald Trump has unnerved investors more than before the June event with Joe Biden. A measure of dollar volatility is near the highest since 2023 and the VIX is on the upswing. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks mostly took impetus from the gains on Wall St where the major indices rebounded amid light newsflow ahead of looming key events, although Chinese markets lagged amid mixed Chinese trade data. ASX 200 was led higher by strength in financials and utilities but with gains capped after weak consumer and business surveys. Nikkei 225 edged higher albeit with trade contained in the absence of any major pertinent catalysts. Hang Seng and Shanghai Comp were mixed as the former was indecisive with Alibaba the biggest gainer after its Stock Connect inclusion, while WuXi AppTec was at the other end of the spectrum after the US House passed the Biosecure Act which would prohibit the US government from contracting with certain biotech firms. Conversely, the mainland lagged behind regional peers amid mixed Chinese trade data and after protectionist measures by the US House which also voted to pass the Countering CCP Drones Act that would bar new drones by DJI from operating in the US.

Top Asian News

- BoJ reportedly sees little need to hike interest rate next week, according to Bloomberg sources; officials are not ruling out another hike later this year or in early 2025 contingent on the economy and market.

- US House passed the Biosecure Act with broad bipartisan support which would prohibit the US government from contracting with, or providing grants to, companies that do business with a “biotechnology company of concern”, while it specifically named five Chinese companies which were BGI Genomics, MGI Tech, Complete Genomics, WuXi AppTec, and Wuxi Biologics.

- US House voted to bar new drones from Chinese drone maker DJI from operating in the US, according to Reuters.

- TSMC (2330 TW/TSM) August (TWD) Revenue 250.87bln, -2.4% M/M

- Chinese August vehicles sales -5% Y/Y (prev. -5.2% in July), Jan-Aug vehicles sales +3% Y/Y (prev. +8% a year ago); NEV sales +30% Y/Y.

- China’s Vice Commerce Minister said China is willing to engage in dialog and consultations to appropriately resolve China-EU economic and trade frictions

European equities, Stoxx 600 (+0.3%) began the session flat/mixed but quickly turned positive as sentiment improved since the cash open. Since, sentiment has deteriorated and indices now sit towards the bottom end of today’s ranges. European sectors are mixed; Real Estate takes the top spot, with Tech also on a firmer footing. Healthcare is the clear underperformer, dragged down by AstraZeneca (-5%) after its lung cancer drug trial failed to significantly improve survival. US equity futures (ES -0.2%, NQ -0.2%, RTY -0.2%) are entirely in the red, paring some of the gains made in the prior session; the NQ marginally lags, hampered by Apple (-1% pre-market), after a EU tax order. EU to lower proposed tariffs on Tesla’s (TSLA) and other EVs from China. Tesla’s tariff rate reportedly to fall to under 8% from 9%, according to Bloomberg sources. Apple (AAPL) has lost fight against EUR 13bln EU tax order to Ireland, according to Reuters; Apple said EU regulators are trying retroactively to change the rules. EU top court dismissed Alphabet’s (GOOG) fight EUR 2.42bln EU antitrust fine.

Top European News

- Kantar: UK Grocery inflation 1.7% (prev. 1.8%), UK Grocery sales +3% in value terms in the 4 weeks to Sep 1st Y/Y.

- Germany’s Chemical Industry Association VCI said Q2 production +3.7% Y/Y, or +8.4% without pharmaceuticals.

FX

- DXY has paused for breath after a two-session winning streak which has taken the index from a 100.58 base on Friday to a current session high at 101.72. Data docket for the remainder of the day is light so the next risk event for the USD comes via the Presidential debate overnight.

- EUR is steady vs. the USD with EUR-specific drivers light in the run up to Thursday’s ECB decision which ultimately may prove to be an event lacking in volatility. If the pair’s recent downtrend resumes, support comes via the 3rd September low at 1.1026.

- GBP is the marginal outperformer across the majors post-UK jobs data which showed a decline in the unemployment rate and a sharp jump in employment. For cable, the pair has moved back above its 21DMA at 1.3080 but failed to sustain a move above 1.31 after topping out at 1.3107.

- JPY is on the backfoot vs. the USD in an extension of yesterday’s price action. For now, the pair has been unable to top yesterday’s best at 143.80.

- Antipodeans are steady for both of the antipodes vs. the USD. AUD is a touch softer post disappointing confidence data which overshadowed broadly encouraging Chinese trade metrics. AUD/USD is back below its 100DMA at 0.6646.

- PBoC set USD/CNY mid-point at 7.1136 vs exp. 7.1140 (prev. 7.0989).

Fixed Income

- USTs have pulled back a touch in-fitting with some of the downside seen in European peers. Tonight’s US Presidential debate could offer some impetus, whereby a strong showing from Trump could reignite some of the bear-steepening bets seen post-his debate with Biden in the summer; US2s10s is still in positive territory whilst the 10yr yield is currently sitting within yesterday’s 3.691-763% range.

- Bunds are a touch softer in a move which coincided with UK jobs data. Fresh macro drivers for the Eurozone are light in the run up to Thursday’s ECB decision which ultimately may prove to be an event lacking in volatility. German 10yr yield is back below the 2.2% mark at 2.178%.

- Gilts are slightly lower, in-fitting with European peers. The main macro update from the UK has come via labour market/earnings data which saw a downtick in unemployment, jump in employment change and slightly softer earnings components. UK 10yr yield is currently contained within yesterday’s 3.856-944% range.

- Orders for Italy’s new BTP are over EUR 108bln, spread set at 13bps over 2053 BTP, according to Reuters.

- UK sells GBP 900mln 0.625% 2045 I/L Gilt: b/c 3.44x (prev. 3.88x) & real yield 1.20% (prev. 1.304%).

- Germany sells EUR 0.462bln vs exp. EUR 0.5bln 2.10% 2029 Green Bobl and EUR 0.485bln vs exp. EUR 0.5bln 0.00% 2050 Green Bund.

Commodities

- Crude is on the backfoot amid quiet newsflow for the complex, and after yesterday’s modestly firmer settlement. Chinese trade data added more concerns regarding Chinese demand after imports missed expectations. Tropical Storm Francine, which is expected to strengthen into a hurricane today before making landfall tomorrow; Brent sits in a USD 70.71-72.28/bbl parameter.

- Precious metals are mixed with spot gold and silver subdued and palladium once again outperforming, albeit off highs in recent trade.

- Base metals tilt lower in subdued trade after the Chinese trade data reinforced weak domestic demand as imports missed forecasts. 3M LME copper trades in a narrow 9,070.50-9,150.50/t range.

- Spot gold is slightly softer, but with trade fairly rangebound in the European morning; XAU currently sits just above USD 2.5k/oz in a narrow USD 2500.26-2507.72/oz range.

- Base metals are almost entirely in the red,

- NHC said Francine is expected to become a hurricane soon with storm surge and hurricane warnings in effect for the Louisiana coast.

- US Coast Guard ordered the closure of Brownsville and other small Texas ports, while the port of Corpus Christi remained open under vessel traffic restrictions, according to an advisory.

- NHC said strong winds and dangerous storm surge expected along the Louisiana coast tomorrow.

- NHC said Francine is likely to become a hurricane today

- Chevron (CVX) announced to evacuate all staff and shut in oil and gas production at two US Gulf of Mexico platforms.

- Shell (SHEL LN) announced to shut oil production at Perdido offshore platform in US Gulf of Mexico citing downstream impacts.

- Goldman Sachs said strong production and disappointing demand pose a downside risk to their US gas price forecast, while it added that Tropical Storm Francine is expected to further reduce power demand and potentially impact LNG exports out of the Gulf.

- China oil industry researcher said China oil products demand is projected to fall by an average of 1.1% annually between 2023-2025.

- India Steel Minister said the Indian steel ministry backs taxing imports

Geopolitics: Ukraine

- Israeli military said it conducted an air strike which targeted a Hamas command centre in Khan Younis, while Hamas media reported the death toll from the Israeli strike on a Gaza tent encampment was at least 40.

- US President Biden was reported to convene his national security team to discuss the impasse in negotiations on the hostage deal, according to Axios’s Barak Ravid citing sources.

- Yemeni Houthis noted that they downed US MQ-9 drone in Saada

Geopolitics: Other

- Moscow’s Vnukovo and Domodedovo Airports stopped flights after reports of nearby drone attacks, while it was separately reported that a fire broke out at a multi-storey residential building in Moscow’s Ramenskoye district as a result of a drone attack.

- North Korean leader Kim said they must prepare North Korea’s nuclear capability and readiness to use it properly at any given time, while they are implementing a nuclear force construction policy to increase the number of nuclear weapons exponentially, according to KCNA.

- Russian forces have attacked energy infrastructure in eight Ukrainian regions in the last 24 hours, according to the energy ministry cited by Reuters.

- Russian Security Council Secretary Shoigu said Russia has enough forces and continues its offensive, according to Ria

US Event Calendar

- 06:00: Aug. SMALL BUSINESS OPTIMISM, est. 93.6, prior 93.7

Central Bank speakers

- 10:00: Fed’s Barr Speaks on Basel III Endgame

- 12:15: Fed’s Bowman Gives Speech on Stress Testing

DB’s Jim Reid concludes the overnight wrap

This week I celebrate 20 years since I left gardening leave, a climb to the top of Kilimanjaro, and my one and only ever half marathon behind, and started at DB. How time flies. It’s been an eventful and enjoyable ride so far and how long it lasts likely depends on a combination of DB’s tolerance and when my kids leave the payroll. The latter date may be greater than the former! We will see.

There have been far more eventful days in those past 20 years than yesterday but after the September stresses so far, risk assets have recovered over the last 24 hours, with the S&P 500 (+1.16%) posting a decent advance after its worst weekly performance since SVB’s collapse. There wasn’t a single catalyst for the recovery, but in a constantly flip-flipping macro narrative the sense yesterday was that last week’s fears about a sharper US downturn were overdone, and the headline data (including payrolls at +142k) still wasn’t consistent with a recession. In the meantime, with confidence growing about the outlook, that led investors to dial back the chance that the Fed would deliver a 50bp cut next week. Tonight we see the long awaited Trump vs Harris TV debate take place at 9pm EST time. So it will be all over a couple of hours before we go to press tomorrow and is the only confirmed debate between the two candidates exactly 8 weeks today until polling day. The election has moved down the pecking order of macro topics of late after dominating mid-summer, likely as Harris reversed what was looking like a strong polling momentum towards a red sweep before Biden stood aside.

In recent days, the general perception from polls, betting odds and forecasting models is that Trump has regained a bit of ground relative to where things stood after the Democratic convention. In particular, there was a lot of focus on a national New York Times/Siena poll, which showed Trump ahead of Harris by 48-47%, and that’s considered a high-quality poll. Now that’s been at the upper end of the recent range for Trump, and the RealClearPolitics average still has Harris ahead by 1.2pts. But given the Republicans have the slight advantage in the Electoral College, Harris likely needs to be a bit further ahead of Trump in the national vote to be confident of victory. Perhaps with tonight’s debate and once we know for certain whether the Fed are going to ease 25 or 50bps next week, we’ll be back to talking about the election more.

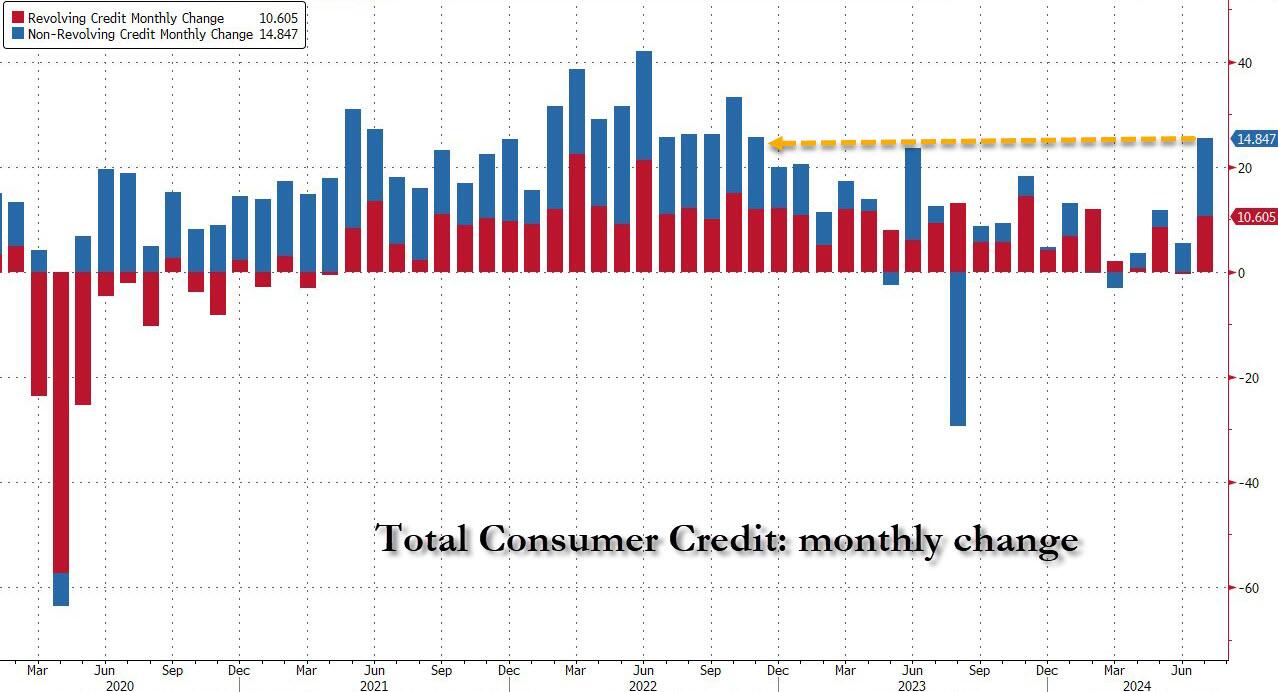

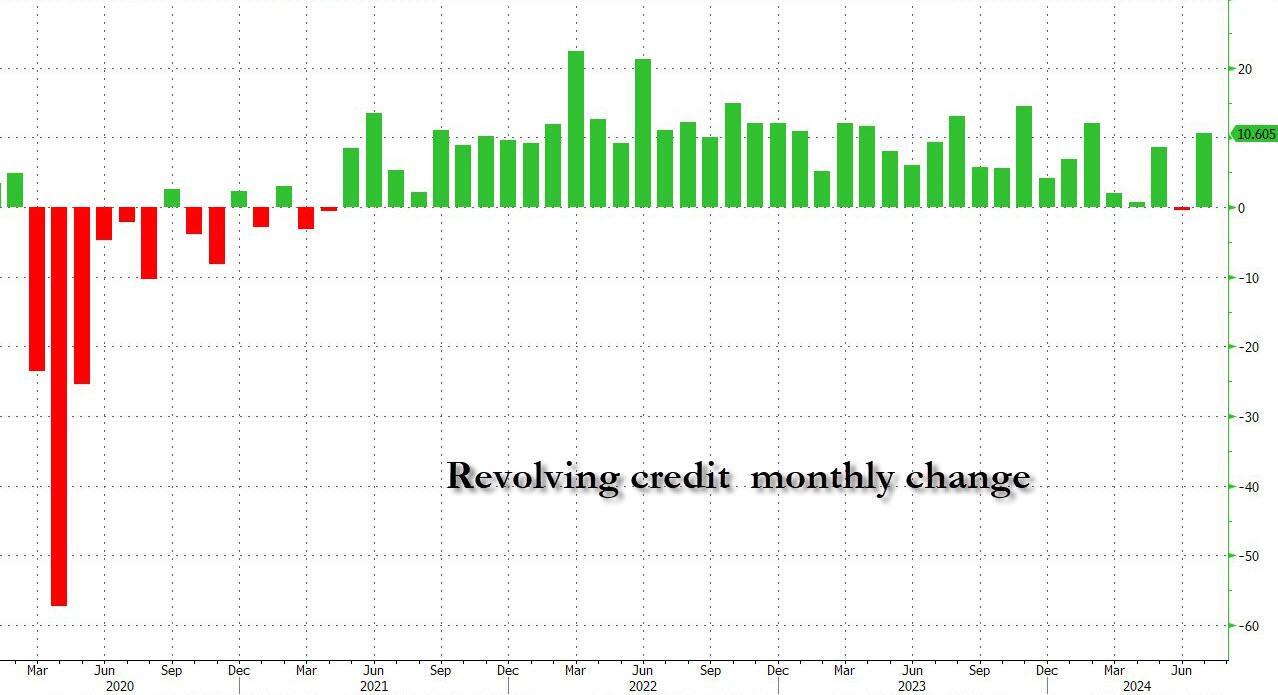

Back to the last 24 hours and the more positive momentum shift was down to sentiment rather than any new data, but investors got a reminder that growth is certainly not currently falling off a cliff given the updated Atlanta Fed’s GDPNow update. The latest reading yesterday included Friday’s jobs report, which lifted the Q3 growth estimate from an annualised +2.1% rate to +2.5%. If realised, that would be the 8th quarter in the last 9 where growth is running at an annualised pace above 2%. Along similar lines, the New York Fed’s Staff Nowcast stood at +2.6% for Q3 on Friday, so still pointing well away from recessionary levels. Adding to the generally resilient cyclical data, yesterday’s US consumer credit release for July (+$25.5bn) showed the strongest monthly rise since October 2022.

Against that backdrop, risk assets posted a recovery on both sides of the Atlantic. For equities, that saw the S&P 500 (+1.16%) post its biggest daily gain in three weeks, after a run of four consecutive declines. This was a broad rebound, with all but one of the 24 industry groups higher on the day, and more cyclical sectors including consumer discretionary (+1.63%), industrials (+1.56%) and information technology (+1.42%) leading the way. The Magnificent 7 advanced +1.37% amidst strong gains from Nvidia (+3.54%) and Tesla (+2.63%). Meanwhile in Europe it was much the same story, with the STOXX 600 (+0.82%) finally making up some ground after falling every day last week.

Elsewhere, as optimism grew on the economy, it led investors to price in a greater chance that the Fed would only cut rates by 25bps next week. Indeed, futures were giving a 50bp cut a 31% probability by the close, which is its joint lowest level over the past two weeks. In turn, that led to a rise in front-end Treasury yields, with the 2yr yield up +2.2bps to 3.67%. However, there was a fresh move lower for the 10yr yield, which fell -0.9bps to 3.70%, which is its lowest closing level since June 2023.

When it comes to next week’s Fed decision, the last big piece of data beforehand will be tomorrow’s CPI release for August, which could help tilt the balance between 25 and 50, particularly if there were a big surprise in either direction. For our US economists’ CPI preview, and to register for their post-release webinar, see here. We’ll have to wait and see what that brings, but yesterday did see the New York Fed release their latest Survey of Consumer Expectations, where inflation expectations were broadly unchanged. The 1yr expectation series remained at 3.0%, 3yr expectations ticked up two-tenths to 2.5%, and the 5yr expectation was unchanged at 2.8%.

Back in the political sphere, former ECB President Mario Draghi published his long-awaited report into European competitiveness yesterday. Among others it called for additional investments of €750-800bn per year, and it said that some “joint funding of investment at the EU level is necessary to maximise productivity growth”. Overall the report contained a fairly blunt message, and Draghi said to reporters that “For the first time since the Cold War we must genuinely fear for our self-preservation”. The reality though is that Europe is struggling for the political capital to rally around delivering the findings of Draghi’s report. So whether the 400 pages in the report can make a difference is a moot political point.

Asian equity markets are relatively quiet this morning with the Hang Seng (+0.09%), Nikkei (+0.01%), and the KOSPI (+0.05%) trading just above flat. Elsewhere, Chinese stocks are lower with the CSI (-0.54%) approaching its lowest close since January 2019 while the Shanghai Composite (-0.53%) is also trading in the red. S&P 500 (-0.14%) and NASDAQ 100 (-0.36%) futures are pulling back a little of yesterday’s gains.

Early morning data showed that China’s export growth in August (+8.7% y/y) surpassed market expectations for a +6.6% gain, and up from the +7.0% increase seen in July. However, import growth slowed to +0.5% y/y in August (v/s +2.5% expected), down from a +7.2% advance in the previous month, thus indicating weakening domestic demand, possible import substitution, and an excess of domestic production. The trade surplus stood at $91.02 billion, (v/s $81.10 expected) and up from $84.65 billion in July.

To the day ahead now, and one of the main highlights will be the TV debate tonight between Kamala Harris and Donald Trump. Otherwise, data releases include UK unemployment and Italian industrial production for July, whilst in the US there’s the NFIB’s small business optimism index for August. Finally from central banks, we’ll hear from Fed Vice Chair for Supervision Barr

2B) European report

European equities are mixed whilst US futures tilt lower, DXY is flat & GBP benefits post-jobs data – Newsquawk US Market Open

Tuesday, Sep 10, 2024 – 06:10 AM

- European equities are mixed, with initial early-morning strength trimmed; US equity futures are modestly in the red with slight underperformance in the NQ following an Apple tax order.

- Apple (AAPL) has lost the fight against the EUR 13bln EU tax order to Ireland, according to Reuters; Apple said EU regulators are trying retroactively to change the rules; AAPL -1.2% in the pre-market.

- DXY is flat, GBP gains post-jobs data which were mixed; Bloomberg reported that the BoJ sees little need to hike rates at its next meeting had little impact on the Yen.

- Bonds are very modestly softer; Gilts are weighed on by the region’s mixed jobs report.

- Crude continues to pull back and towards session lows, XAU and base metals also on the backfoot.

- Looking ahead, EIA STEO, OPEC MOMR, Comments from BoC Governor Macklem, Fed’s Barr, BoE’s Breeden.

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European equities, Stoxx 600 (+0.3%) began the session flat/mixed but quickly turned positive as sentiment improved since the cash open. Since, sentiment has deteriorated and indices now sit towards the bottom end of today’s ranges.

- European sectors are mixed; Real Estate takes the top spot, with Tech also on a firmer footing. Healthcare is the clear underperformer, dragged down by AstraZeneca (-5%) after its lung cancer drug trial failed to significantly improve survival.

- US equity futures (ES -0.2%, NQ -0.2%, RTY -0.2%) are entirely in the red, paring some of the gains made in the prior session; the NQ marginally lags, hampered by Apple (-1% pre-market), after a EU tax order.

- EU to lower proposed tariffs on Tesla’s (TSLA) and other EVs from China. Tesla’s tariff rate reportedly to fall to under 8% from 9%, according to Bloomberg sources.

- Apple (AAPL) has lost fight against EUR 13bln EU tax order to Ireland, according to Reuters; Apple said EU regulators are trying retroactively to change the rules.

- EU top court dismissed Alphabet’s (GOOG) fight EUR 2.42bln EU antitrust fine.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY has paused for breath after a two-session winning streak which has taken the index from a 100.58 base on Friday to a current session high at 101.72. Data docket for the remainder of the day is light so the next risk event for the USD comes via the Presidential debate overnight.

- EUR is steady vs. the USD with EUR-specific drivers light in the run up to Thursday’s ECB decision which ultimately may prove to be an event lacking in volatility. If the pair’s recent downtrend resumes, support comes via the 3rd September low at 1.1026.

- GBP is the marginal outperformer across the majors post-UK jobs data which showed a decline in the unemployment rate and a sharp jump in employment. For cable, the pair has moved back above its 21DMA at 1.3080 but failed to sustain a move above 1.31 after topping out at 1.3107.

- JPY is on the backfoot vs. the USD in an extension of yesterday’s price action. For now, the pair has been unable to top yesterday’s best at 143.80.

- Antipodeans are steady for both of the antipodes vs. the USD. AUD is a touch softer post disappointing confidence data which overshadowed broadly encouraging Chinese trade metrics. AUD/USD is back below its 100DMA at 0.6646.

- PBoC set USD/CNY mid-point at 7.1136 vs exp. 7.1140 (prev. 7.0989).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs have pulled back a touch in-fitting with some of the downside seen in European peers. Tonight’s US Presidential debate could offer some impetus, whereby a strong showing from Trump could reignite some of the bear-steepening bets seen post-his debate with Biden in the summer; US2s10s is still in positive territory whilst the 10yr yield is currently sitting within yesterday’s 3.691-763% range.

- Bunds are a touch softer in a move which coincided with UK jobs data. Fresh macro drivers for the Eurozone are light in the run up to Thursday’s ECB decision which ultimately may prove to be an event lacking in volatility. German 10yr yield is back below the 2.2% mark at 2.178%.

- Gilts are slightly lower, in-fitting with European peers. The main macro update from the UK has come via labour market/earnings data which saw a downtick in unemployment, jump in employment change and slightly softer earnings components. UK 10yr yield is currently contained within yesterday’s 3.856-944% range.

- Orders for Italy’s new BTP are over EUR 108bln, spread set at 13bps over 2053 BTP, according to Reuters.

- UK sells GBP 900mln 0.625% 2045 I/L Gilt: b/c 3.44x (prev. 3.88x) & real yield 1.20% (prev. 1.304%).

- Germany sells EUR 0.462bln vs exp. EUR 0.5bln 2.10% 2029 Green Bobl and EUR 0.485bln vs exp. EUR 0.5bln 0.00% 2050 Green Bund.

- Click for a detailed summary

COMMODITIES

- Crude is on the backfoot amid quiet newsflow for the complex, and after yesterday’s modestly firmer settlement. Chinese trade data added more concerns regarding Chinese demand after imports missed expectations. Tropical Storm Francine, which is expected to strengthen into a hurricane today before making landfall tomorrow; Brent sits in a USD 70.71-72.28/bbl parameter.