DEC 16/BITCOIN BREAKS $106,000//GOLD CLOSED DOWN $2.800 TO $2653.25//SILVER IS SFLAT AT $30.58//PLATINUM IS UP $13.75 TO $939.25 WHILE PALLADIUM IS DOWN $5.10 TO $945.05//GOLD COMMENTARY TODAY FROM PETER SCHIFF AND ALASDAIR MACLEOD//ALSO THE PODCAST FROM ANDREW MAGUIRE 203 IS A MUST VIEW//ONE WEEK AFTER FRANCE’S GOVERNMENT FALLS, TODAY IT IS THE GERMAN GOVERNMENT THAT FALLS//ISRAEL VS SYRIA/HAMAS HEZBOLLAH UPDATES//CANADA’S FREELAND LEAVES TRUDEAU CABINET// USA PMF PMI FALTERS BUT SERVICE PMI’S GAIN//SWAMP STORIES FOR YOU TONIGHT//

072 H GOLDMAN 88 092 C DEUTSCHE BANK 1 152 C DORMAN TRADING 1 190 H BMO CAPITAL 274 363 H WELLS FARGO SEC 295 624 H BOFA SECURITIES 52 657 C MORGAN STANLEY 41 661 C JP MORGAN 126 117 686 C STONEX FINANCIA 84 34 690 C ABN AMRO 9 1 737 C ADVANTAGE 10 1 905 C ADM 4

TOTAL: 569 569

JPMorgan stopped 126/569

GOLD: NUMBER OF NOTICES FILED FOR DEC/2024. CONTRACT: 569 NOTICES FOR 56,900 OZ 1.7698 TONNES

total notices so far: 22,159 contracts for 2,215,900 Oz (68.923 tonnes)

FOR DEC

SILVER NOTICES: 13 NOTICE(S) FILED FOR 0.065 MILLION OZ/

total number of notices filed so far this month : 8513 for 42.565 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $2.80 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 4.70 TONNES OF GOLD OUT OF THE GLD

INVENTORY RESTS AT 863.90 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $0.00 AT THE SLV

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 4.84 MILLION OZ OUT OF THE SLV/.

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 458.052 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI SHOCKINGLY FELL BY A HUMONGOUS SIZED2045CONTRACTS TO 149,618 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG LOSS OF $0,46 IN SILVER PRICING AT THE COMEX WITH RESPECT TO FRIDAY’S TRADING. WE HAD A HUMONGOUS LOSS OF 1545 TOTAL CONTRACTS ON OUR TWO EXCHANGES WWITH OUR LOSS IN PRICE//FRIDAY’S TRADING.. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS ON FRIDAY COMEX TRADING AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 2 WEEKS. THE RAID WAS CALLED UPON AGAIN TO QUELL MASSIVE DERIVATIVE LOSSES BY OUR BULLION BANKS. THEY SUCCEEDED YESTERDAY

WE HAD A HUGE 500 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY A STRONG 598 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN MONDAY;S TRADING AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE LOST A HUMONGOUS SIZED 1545 CONTRACTS ON OUR TWO EXCHANGES WITH OUR HUGE LOSS IN PRICE. WE HAD A HUGE TAS LIQUIDATION THROUGHOUT FRIDAY’S COMEX SESSION. LAST MONDAY MORNING WE RECEIVED NOTICE OF .5000 MILLION OZ ISSUANCE OF EXCHANGE FOR RISK/ THIS WILL BE ADDED TO THE PREVIOUS EXCHANGE FOR RISK ISSUANCE OF .66 MILLION OZ/NEW EXCHANGE FOR RISK TOTALS FOR THE MONTH: 1.16 MILLION OZ.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN YESTERDAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON FRIDAY NIGHT: A HUGE 598 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS BUT TO NO AVAIL TODAY. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.46) AND WERE SUCCESSFUL IN KNOCKING OFF APPRECIABLE NET SILVER LONGS FROM THEIR PERCH AS WE HAD A HUMONGOUS LOSS IN OI ON OUR TWO EXCHANGES OF 1459 OI. CONTRACTS.

WE HAD A HUGE 500 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 40.435 MILLION OZ (FIRST DAY NOTICE) TO WHICH WE MUST ADD THOSE STUPID “DELIVERIES” CALLED EXCHANGE FOR RISK , TOTALLING 1.16 MILLION OZ. WE ALSO HAD A HUGE 27 CONTRACT QUEUE JUMP FOR 0.135 MILLION OZ AS THESE BOYS WILL TRY THEIR LUCK IN TAKING DELIVERY OVER ON THIS SIDE OF THE PLANET.

// STANDING FOR SILVER//DEC INCREASES TO 43.635 MILLION OZ + .1.16 MILLION OZ EX FOR RISK = 44.795 MILLION OZ

WE HAD:

/ HUMONGOUS SIZED COMEX OI LOSS +// HUGE SIZED EFP ISSUANCE/ VI)MEGA STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 598 CONTRACTS)/ TO WHICH WE ADD 1.16 MILLION OZ EX. FOR RISK //

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 569 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS NOV. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF DEC

TOTAL CONTRACTS for 11DAYS, total 23,165 contracts: OR 115.825 MILLION OZ (2105 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 115.825 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 115.825 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE/ MAY EXCEED MARCH 2022 RECORD OF 209 MILLION OZ)

RESULT: WE HAD AN HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2045 CONTRACTS WITH OUR HUGE LOSS IN PRICE OF SILVER PRICING AT THE COMEX//FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG EFP ISSUANCE CONTRACTS: 500 ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR DEC OF 40.435 MILLION OZ ON FIRST DAY NOTICE, FOLLOWED BY TODAY’S 0.135 MILLION OZ QUEUE JUMP TO WHICH WE ADD 1.16 MILLION OZ OF EXCHANGE FOR RISK/PRIOR EQUALS 44.795 MILLION OZ

//NEW TOTAL STANDING FOR DEC AT 44.795 MILLION OZ

WE HAVE A HUMONGOUS SIZED LOSS OF 2045 OI CONTRACTS ON THE TWO EXCHANGES WITH OUR LOSS IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE 598 CONTRACTS TRYING DESPERATELY TO CONTAIN SILVER’S PRICE RISE,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE FRIDAY COMEX SESSION. BUT THEY STILL NEED THESE ISSUANCE FOR REPLENISHMENT FOR FUTURE TRADING /THE STRONG TA.S. ISSUANCE//LIQUIDATION DISTORTS THE TOTAL OI CONTRACTS STANDING AT THE COMEX. NO NET LONG SPECULATORS WERE BURNED ON THURSDAY

/ HUGE NET SHORT COVERING FROM OUR SPEC SHORTS WITH THE LOSS IN PRICE FRIDAY/ . ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE FRIDAY NIGHT (1598) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE, AND CERTAINLY TODAY.

WE HAD 13 NOTICE(S) FILED TODAY FOR 0.065 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A VERY STRONG SIZED 12,522 OI CONTRACTS TO 478,062 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A SMALL SIZED 86 CONTRACTS//

WE HAD A VERY STRONG SIZED DECREASE IN COMEX OI (12,522 CONTRACTS) OCCURRED WITH OUR LOSS OF $29.65 IN PRICE FRIDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A GOOD INITIAL STANDING IN GOLD TONNAGE FOR DEC AT 57.284 TONNES ON FIRST DAY NOTICE. FOLLOWED BY A STRONG 160 CONTRACT QUE JUMP FOR 16,000 OZ ( 0.4977 TONNES). WE MUST NOW ADD 10.6406 TONNES OF EXCHANGE FOR RISK ISSUED ON 5 OCCASIONS IN THIS ACTIVE DECEMBER CONTRACT MONTH.

/NEW STANDING 83.9056 TONNES

/ ALL OF THIS HAPPENED WITH OUR $29.55 LOSS IN PRICE WITH RESPECT TO FRIDAY’S COMEX ///. WE HAD A STRONG LOSS OF 8834 OI CONTRACTS (27.47 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! YOU CAN VISUALIZE THIS WITH THE VIOLENT ACTION AT THE COMEX WITH RESPECT TO 160 CONTRACT QUEUE JUMP TODAY (16,000 OZ) ALONG WITH THE 10.6406 EXCHANGE FOR RISK ISSUANCE THIS MONTH //NEW TOTAL TONNES OF DELIVERY: 83.9056

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 3688 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 478,156

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8834 CONTRACTS WITH 12,522 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 3688 EFP OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 8834 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED BUT CRIMINAL 1262 CONTRACTS ISSUED. WE HAD A HUGE LIQUIDATION OF T.A.S CONTRACTS WITH OUR LOSS IN PRICE FRIDAY AS THE NEED FOR REPLENISHMENT WAS STILL IN ORDER TO CARRY OUT ITS PRICE CONTAINMENT STRATEGY IN FUTURE TRADING.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3688 CONTRACTS) ACCOMPANYING THE STRONG SIZED DECREASE IN COMEX OI OF 12,522 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 8834 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR DEC 55.117 TONNES FOLLOWED BY TODAY.S 16,000 OZ QUEUE JUMP TO WHICH WE ADD THOSE CRAZY EXCHANGE FOR RISK ON 5 PRIOR OCCASIONS OF 10.6406 TONNES//NEW STANDING 83.9056 TONNES

//NEW STANDING DECEMBER: 83.9056 TONNES

/ 3) HUGE T.A.S. LIQUIDATION TRYING TO LOWER GOLD’S PRICE THURSDAY WITH SOME SUCCESS AS WE HAD A $29.55 PRICE LOSS. BUT WE HAD CONSIDERABLE NET LONG SPECS BEING CLIPPED AS WE HAD A SMALL GAIN IN OI ON OUR TWO EXCHANGES. STICKY GOLD’S LONGS ARE NOT FOOLED BY THE RAID IN PRICE AS THEY WERE REWARDED FRIDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL.

4) VERY STRONG SIZED COMEX OPEN INTEREST DECREASE 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1262 T.A.S.CONTRACTS///160 CONTRACT QUEUE JUMP OR 16,000 OZ WILL STAND FOR DELIVERY AT THE COMEX.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

DEC

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC :

TOTAL EFP CONTRACTS ISSUED: 78,770 CONTRACTS OF 7,877,000 OZ OR 245.00 TONNES IN 11 TRADING DAY(S) AND THUS AVERAGING: 7154 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAY(S) IN TONNES 245.00 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 245.00 DIVIDED BY 3550 x 100% TONNES = 6.90% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 245.00 TONNES (we will also have a humdinger of an ex for physical issuance for this month/maybe this time we will surpass March 2022 record of 409 tonnes for the month)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 2045 CONTRACTS OI TO 149,668 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 500 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 500 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 500 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2045 CONTRACTS AND ADD TO THE 500 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1459 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS A HUGE 7.295 MILLION OZ OCCURRED DESPITE OUR HUGE $0.46 LOSS IN PRICE

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS/MONDAY MORNING FRIDAY NIGHT

ASIA TRADING MONDAY MORNING/SUNDAY NIGHT

SHANGHAI CLOSED DOWN 5.55 PTS OR 0.16%

//Hang Seng CLOSED DOWN 175.75 PTS OR 0.88%

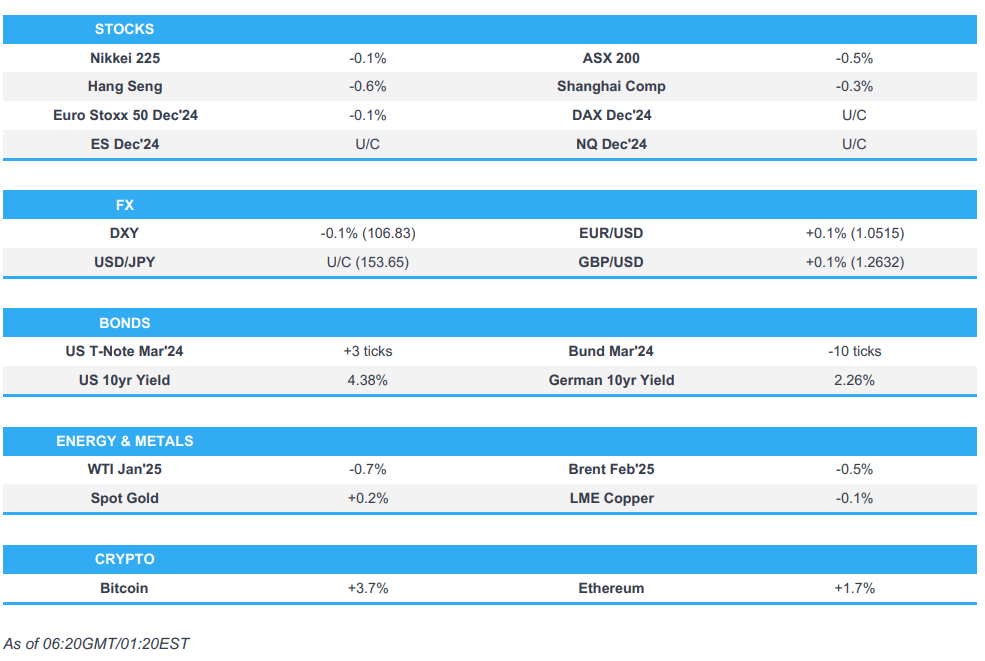

// Nikkei CLOSED DOWN 152.05 OR 0.03%//Australia’s all ordinaries CLOSED DOWN .66%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7.2910 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2909// Oil UP TO 70.64 dollars per barrel for WTI and BRENT UP AT 73.97 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A VERY STRONG SIZED12,522 CONTRACTS TO 478,067 WITH OUR HUGE LOSS IN PRICE OF $29.55 WITH RESPECT TO FRIDAY’S TRADING. , WE LOST SOME NET LONGS WITH OUR STRONG PRICE LOSS FOR GOLD. WE HAD, AS YOU WILL SEE BELOW A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (3688). THUS WE HAD A STRONG LOSS ON OUR TWO EXCHANGES OF 8834 CONTRACTS WITH OUR HUGE LOSS IN PRICE. OUR FRIENDLY PHYSICAL LONDON BOYS HAD A FIELD DAY AGAIN ON FRIDAY AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED RAID AS THEY ABSORBED FULLY THE ATTACK AND OFFERED A THANK YOU NOTE TO THE FED FOR THEIR WONDERFUL LARGESSE. THE LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY THIS ENTIRE PAST WEEK. WE HAD HUGE T.A.S. LIQUIDATION ON FRIDAY.

THE FED IS THE MAJOR SHORT OF AROUND 82+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS IS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES//VIEW ANDREW MAGUIRE LATEST LIVE FROM VAULT PODCAST 197 , 199, 2001,AND FRIDAY NIGHTS 202, AND 203 AS HE TACKLES THIS IMPORTANT TOPIC). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY! ACTUALLY THE FED HAS COAXED THE SPECULATORS TO GO MASSIVELY SHORT WHILE THEY TAKE THE LONG SIDE AFTER THEY COMMENCE THE AVALANCHE IN LOWERING THE PRICE OF GOLD LIKE THESE PAST TWO DAYS OF RAIDS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD CONSIDERABLE T.A.S. LIQUIDATION THROUGHOUT LAST WEEK’S TRADING CULMINATING DURING THE LAST TWO DAYS OF RAIDS.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF THE SPREADERS // T.A.S DURING LAST WEEK IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW DEEP INTO THE ACTIVE DELIVERY MONTH OF DECEMBER.… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 3685 EFP CONTRACTS WERE ISSUED: : /DEC 3685 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3685 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 8834 CONTRACTS IN THAT 3688 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A VERY STRONG LOSS OF 12,522 COMEX CONTRACTS..AND THIS STRONG LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR HUGE LOSS IN PRICE OF $29.55 FRIDAY// COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR FRIDAY NIGHT WAS A FAIR SIZED SIZED 1263 CONTRACTS, AND THESE WILL BE USED TO REPLENISH SUPPLIES.. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK).

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON MONDAY NOV 25, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION (COUPLED WITH THE LIQUIDATION OF CALENDAR SPREADERS ). THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE NOVEMBER’S OPTIONS EXPIRY TRADING. WE HAD CONTINUAL T.A.S. AND FINAL MONTH END SPREADER LIQUIDATION ESPECIALLY ON FRIDAY NOV 29 .THE LIQUIDATION OF T.A.S. SUBSIDED QUITE DRAMATICALLY DURING THE FIRST WEEK AND A HALF OF DECEMBER BUT THAT DRAMATICALLY CHANGED WITH CONSIDERABLE LIQUIDATION YESTERDAY WITH FRIDAY’S COMEX RAID.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: DEC (83.9056 TONNES) WHICH IS HUGE FOR OUR ACTIVE DEC DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 73.265 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 10.6406 TONNES EQUALS 83.9056 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $29.55/)//AND WERE SUCCESSFUL IN KNOCKING OFF SOME NET SPECULATOR LONGS AS WE DID HAVE A STRONG LOSS IN OUR TWO EXCHANGES. AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION FRIDAY. WE ALSO HAD A FAIR T.A.S. ISSUANCE FRIDAY NIGHT (SATURDAY MORNING), AS THE NEED FOR REPLENISHMENT WAS STILL EVER PRESENT. THIS COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING.

LATE 15 DAYS AGO, FRIDAY NIGHT (EARLY SATURDAY MORNING NOV 30) THE CME ANNOUNCED ANOTHER OF THOSE CRAZY DELIVERIES: THE ISSUANCE OF 250 EXCHANGE FOR RISK CONTRACTS WHICH TOTAL 25000 OZ (.7776 TONNES. HERE THE BUYER ASSUMES THE RISK THAT HE WILL BE DELIVERED UPON IN PHYSICAL METAL. THIS IS ABSOLUTELY INSANE AND A HUGE VIOLATION OF THE TRUE DISCOVERY PRICE MECHANISM WHICH IS THE COMEX MANTRA!. AND THEN GUESS WHAT? THE CME ANNOUNCED ANOTHER EXCHANGE FOR RISK, LATE TUESDAY EVENING/ EARLY WEDNESDAY MORNING, (DEC 5) OF 617 CONTRACTS FOR 61,700 OZ OR GOLD (1.919 TONNES). THEN MUCH TO MY ANGER, THE CME ANNOUNCED A THIRD ISSUANCE FRIDAY NIGHT DEC 7 FOR A MONSTROUS 2254 EXCHANGE FOR RISK CONTRACTS OR 225,400 OZ OR 7.0108 TONNES. NOT TO BE UNDONE, THE CROOKS CONTINUED WITH THEIR NONSENSE WITH ANOTHER 50 CONTRACT EXCHANGE FOR RISK THE MORNING OF DEC 12 FOR 5000 OZ OR .1555 TONNES. AND THIS BRINGS US TO THIS EARLY FRIDAY MORNING WHERE I WAS SHOCKED TO SEE FOR THE FIFTH TIME THIS MONTH AN ENTRY FOR 250 CONTRACTS OF EXCHANGE FOR RISK FOR 25000 OZ OR .7776 TONNES.THUS ALL FIVE OF THESE ISSUANCES WILL BE ADDED TO THE TOTAL GOLD BEING “DELIVERED UPON”. TOTAL EXCHANGE FOR RISK ISSUANCES FOR THE MONTH NOW TOTALS 10.6406. NO EXCHANGE FOR RISK WAS ISSUED EARLY SATURDAY MORNING.

WE HAVE LOST A TOTAL OF 27.20 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR DEC (55.167TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 16,000 OZ OR 0.4977 TONNES, TO WHICH WE MUST ADD OUR 5 ISSUANCES OF EXCHANGE FOR RISK FOR A TOTAL OF 10.6406 TONNES. THUS TAKEN TOGETHER,, THE TOTAL GOLD STANDING FOR THIS VERY ACTIVE DELIVERY MONTH OF DECEMBER IS:

73.265 TONNES (NORMAL DELIVERY) +

10.6406 TONNES (EX FOR RISK)

EQUALS: 83.9056 TONNES

/ STANDING FOR DEC INCREASES TO 83.9056 TONNES

NEW STANDING FOR DECEMBER: 83.9056 TONNES (WHICH IS HUGE FOR OUR VERY ACTIVE DELIVERY MONTH)

ALL OF THIS WAS ACCOMPLISHED WITH OUR HUGE LOSS IN PRICE TO THE TUNE OF $29.55

WE HAD 85 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET LOSS ON THE TWO EXCHANGES 8,834 CONTRACTS OR 874,500 (27.20 TONNES)

confirmed volume FRIDAY 197,109 contracts: fair //// T.A.S. ENHANCED TO A MUCH GREATER EXTENT.

177 GOOD LONDON DELIVERY BARS REMOVED (APPROX. 400 OZ PER BAR)

.

Deposit to the Dealer Inventory in oz

NIL OZ

Deposits to the Customer Inventory, in oz

41,796.300 OZ /BRINKS 800 ,kilobars MANFRA 500 kilobars 1300 kilobars

No of oz served (contracts) today

569 notice(s) 56900 OZ 1.7698 TONNES

No of oz to be served (notices)

1096 contracts 109600 OZ 3.409 TONNES

Total monthly oz gold served (contracts) so far this month

22,159 notices 2,215900 oz 68.923 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

dealer deposits: 0

total dealer deposits: NIL oz

we have 2 customer deposit

i) Into BRINKS 25,720.800 oz (800 kilobars)

ii) Into Manfra: 16,075.500 oz (500 kilobars)

total deposits 41,796.300 oz 1300 kilobars

strictly a paper gold entry.

withdrawals: 1

i)Brinks enhanced: 10,631.801 (177 good London delivery bars)

TOTAL WITHDRAWALS: 10,631,801 oz

adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR DEC.

For the front month of DEC: we have an oi of 1665 contracts having LOST 1454 contracts. We had A HUGE 1614 contracts served on FRIDAY, so we GAINED a strong 160 contracts or 16000 oz (0.4977 TONNES) underwent a MASSIVE queue jump bolting ahead of others to take delivery of gold over on this side of the planet.

JANUARY LOST 12 CONTRACTS TO STAND AT 3643

FEBRUARY LOST 9280 CONTRACTS TO 356,949 .

We had 569 contracts filed for today representing 56900 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 126 notices issued from their client or customer account. The total of all issuance by all participants equate to 569 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 151 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for DEC /2024. contract month, we take the total number of notices filed so far for the month (22,159 x 100 oz ) to which we add the difference between the open interest for the front month of DEC(1665 CONTRACTS) minus the number of notices served upon today (569 x 100 oz per contract( equals 2,355,500 OZ OR 73.265 TONNES. to which we add 10.6406 tonnes of exchange for risk WHICH EQUALS 83.9056 TONNES

thus the INITIAL standings for gold for the DEC contract month: No of notices filed so far (22,159 x 100 oz +we add the difference for front month of DEC (1665 OI} minus the number of notices served upon today (569 x 100 oz which equals 2,355,500 oz (73.265 TONNES) + 10.6406 tonnes of ex. for risk MONTH OF DEC //new total GOLD STANDING 83.9056 TONNES

TOTAL COMEX GOLD STANDING FOR DEC.: 83.9056 TONNES WHICH IS HUGE FOR THIS ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 18,675,121.278 OZ

TOTAL REGISTERED GOLD 8,312,797.698/// 258.56 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,331.169.081 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,434,929 oz (REG GOLD- PLEDGED GOLD)= 200.153 tonnes //

JPMorgan enhanced inventory is 3.592 million oz/1,877,000 oz = 19.15% of entire inventory..

END

SILVER/COMEX

DEC 16. 2024

INITIAL

//2024// THE DEC 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

614,546.300 OZ asahi

.

Deposits to the Dealer Inventory

nil

Deposits to the Customer Inventory

nil oz

No of oz served today (contracts)

13 CONTRACT(S) (65,000 OZ)

No of oz to be served (notices)

214 contracts (1.070 MILLION oz)

Total monthly oz silver served (contracts)

8513 Contracts (42.565 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit/

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0 customer deposits

total customer deposits nil oz

We had 1 withdrawals

i) Out of ASAHI 614,546.300 oz

total withdrawal 614,546.300 oz

JPMorgan has a total silver weight: 135.000million oz/307.724million or 43.97%

adjustment 0

TOTAL REGISTERED SILVER: 76.737MILLION OZ//.TOTAL REG + ELIGIBLE. 307.725 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DEC

silver open interest data:

FRONT MONTH OF DEC /2024 OI: 227 OPEN INTEREST FOR A LOSS OF 97 CONTRACTS. WE HAD

124 CONTRACTS ISSUED ON FRIDAY SO WE HAD A HUGE 27 CONTRACT OR 135,000 OZ QUEUE JUMP WHERE THESE BOYS WILL TRY THEIR LUCK AND TAKE DELIVERY OF PHYSICAL SILVER OVER HERE.

JANUARY SAW A LOSS OF 64 CONTRACTS DOWN TO 2297

FEBRUARY SAW A GAIN OF 32 CONTRACTS TO STAND AT 182

MARCH SAW A LOSS OF 1782 CONTRACTS DOWN TO 120,679

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 13 for 65,000 oz

CONFIRMED volume; ON FRIDAY 67.221 good// t.a.s. enhanced

To calculate the number of silver ounces that will stand for delivery in DEC we take the total number of notices filed for the month so far at 8513x 5,000 oz = 42.565 MILLION oz

to which we add the difference between the open interest for the front month of DEC (227) and the number of notices served upon today (13)x (5000 oz)

Thus the standings for silver for the DEC 2024 contract month: 8513 Notices served so far) x 5000 oz + OI for the front month of DEC(227) minus number of notices served upon today (13)x 5000 oz equals silver standing for the DEC contract month equating to 43.636 MILLION OZ. + to which we add 1.16 million oz of exchange for risk PRIOR////new total 44.795 MILLION OIOZ

New total standing: 44.795 million oz.

There are 76,737 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS//

DEC 16 WITH GOLD DOWN $2.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.70 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 863.90 TONNES

DEC 13 WITH GOLD DOWN $24.55 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.78 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 868.60 TONNES

DEC 12 WITH GOLD DOWN $34.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.59 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 873.38 TONNES

DEC 11 WITH GOLD UP $29.75 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: // : .///INVENTORY RESTS AT 870.79 TONNES

DEC 9 WITH GOLD UP $31.10 ON THE DAY; NO CHANGES IN GOLD AT THE GLD. // : .///INVENTORY RESTS AT 871.94 TONNES

DEC 6 WITH GOLD UP $6.60 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD. A WITHDRAWAL OF 1.71 TONNES OF GOLD FROM THE GLD// : .///INVENTORY RESTS AT 871.94 TONNES

DEC 5 WITH GOLD DOWN $26.80 ON THE DAY; NO CHANGES IN GOLD AT THE GLD./ : .///INVENTORY RESTS AT 873.65 TONNES

DEC 4 WITH GOLD UP $6.15 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD./ : .///INVENTORY RESTS AT 873.65 TONNES

DEC 3 WITH GOLD UP $10.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.59 TONNES OF GOLD FROM THE GLD./ : .///INVENTORY RESTS AT 875.96 TONNES

DEC 2 WITH GOLD DOWN $20.20 ON THE DAY; NO CHANGES IN GOLD AT THE GLD : .///INVENTORY RESTS AT 878.55 TONNES

NOV 29 WITH GOLD UP $16.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD : Z WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD . .///INVENTORY RESTS AT 878.55 TONNES

NOV 27 WITH GOLD UP $18.05 ON THE DAY; NO CHANGES IN GOLD AT THE GLD : . .///INVENTORY RESTS AT 879.41 TONNE

NOV 26 WITH GOLD UP $3.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD : A DEPOSIT OF 1.44 TONNES OF GOLDINTO THE GLD. .///INVENTORY RESTS AT 879.41 TONNES

NOV 25 WITH GOLD DOWN $91.60 ON THE DAY; NO CHANGES IN GOLD AT THE GLD :. .///INVENTORY RESTS AT 877.97 TONNES

NOV 21 WITH GOLD UP $23.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 3.16 TONNES OF GOLD INTO THE GLD/:. .///INVENTORY RESTS AT 875,39 TONNES

NOV 20 WITH GOLD UP $22.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.58 TONNES OF GOLD INTO THE GLD/:. .///INVENTORY RESTS AT 872.23 TONNES

NOV 19 WITH GOLD UP $13.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/:. .///INVENTORY RESTS AT 871.65 TONNES

NOV 18 WITH GOLD UP $44.20 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.56 TONNES OF GOLD INTO THE GLD/:. .///INVENTORY RESTS AT 869.93 TONNES

NOV 15 WITH GOLD DOWN $1.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.25 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 867.37 TONNES

NOV 14 WITH GOLD DOWN $12.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.91 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 868.62 TONNES

NOV 13 WITH GOLD DOWN $19.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 870.63 TONNES

NOV 12 WITH GOLD DOWN $11.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.88 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 871,97 TONNE

NOV 11 WITH GOLD DOWN $75.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.74 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 876.85 TONNES

NOV 8 WITH GOLD DOWN $11.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.87 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 883.46 TONNES

NOV 7 WITH GOLD UP $30.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.45 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 883.46 TONNES

NOV 6 WITH GOLD DOWN $72.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 886.91 TONNES

NOV 5 WITH GOLD UP $4.05 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:.// . // .///INVENTORY RESTS AT 888.63 TONNES

GLD INVENTORY: 863.90 TONNES, TONIGHTS TOTAL

SILVER

DEC 16 WITH SILVER DOWN 0 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 4.84 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 458.052 MILLION OZ

DEC 13 WITH SILVER DOWN 46 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF .536 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 462.892 MILLION OZ

DEC 12 WITH SILVER DOWN 94 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 5.787 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 463.428 MILLION OZ

DEC 11 WITH SILVER UP 10 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.597 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 469.215 MILLION OZ

DEC 10 WITH SILVER DOWN 8 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 1.868 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 471.812 MILLION OZ

DEC 9 WITH SILVER UP $0.91 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 1.367 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 473.680 MILLION OZ

DEC 6 WITH SILVER DOWN $0.00 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 4.329 MILLION OZ/// //INVENTORY AT SLV RESTS AT 475.047 MILLION OZ

DEC 5 WITH SILVER DOWN $0.23 //NO CHANGES IN SILVER INVENTORY AT THE SLV” /// //INVENTORY AT SLV RESTS AT 470.718 MILLION OZ

DEC 4 WITH SILVER UP 26 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV”: A WITHDRAWAL OF 2.206 MILLION OZ FORM THE SLV. /// //INVENTORY AT SLV RESTS AT 470.718 MILLION OZ

DEC 3 WITH SILVER UP 59 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV /// //INVENTORY AT SLV RESTS AT 472.924 MILLION OZ

DEC 2 WITH SILVER DOWN 19 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV. A WITHDRAWAL OF 1,458,000 OZ FROM THE SLV. /// //INVENTORY AT SLV RESTS AT 472.924 MILLION OZ

NOV 29 WITH SILVER UP 51 CENTS //SMALL CHANGES IN SILVER INVENTORY AT THE SLV. A WITHDRAWAL OF 365,000 OZ FROM THE SLV. /// //INVENTORY AT SLV RESTS AT 474.382 MILLION OZ

NOV 27 WITH SILVER DOWN $0.25 //NO CHANGES IN SILVER INVENTORY AT THE SLV.. /// //INVENTORY AT SLV RESTS AT 474.747 MILLION OZ

NOV 26 WITH SILVER UP $0.10 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:.A WITHDRAWAL OF 1.094 MILLION OZ FROM THE SLV./.. /// //INVENTORY AT SLV RESTS AT 474.747 MILLION OZ

NOV 25 WITH SILVER DOWN $0.96 //NO CHANGES IN SILVER INVENTORY AT THE SLV:. . /// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 22 WITH SILVER UP $0.40 //NO CHANGES IN SILVER INVENTORY AT THE SLV:. . /// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 21 WITH SILVER DOWN $0.06 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.729 MILLION OZ FORM THE SLV. . /// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 20 WITH SILVER DOWN $0.22 //NO CHANGES IN SILVER INVENTORY AT THE SLV: . /// //INVENTORY AT SLV RESTS AT 477.572 MILLION OZ

NOV 19 WITH SILVER UP $0.10 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 5,742,000 OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 477..572 MILLION OZ

NOV 18 WITH SILVER UP $0.68 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 1,277,000 OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 471,830 MILLION OZ

NOV 15 WITH SILVER DOWN $0.09 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 3,100,000 OZ OUT OF THE SLV. /// //INVENTORY AT SLV RESTS AT 471,830 MILLION OZ

NOV 14 WITH SILVER DOWN $0.07 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1,504,000 OZ OUT OF THE SLV. /// //INVENTORY AT SLV RESTS AT 473.653 MILLION OZ

NOV 13 WITH SILVER DOWN $0.16 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1,274,000 OZ OUT OF THE SLV. /// //INVENTORY AT SLV RESTS AT 475.157 MILLION OZ

NOV 12 WITH SILVER UP $0.16 //SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 576,000 OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 476.000 MILLION OZ

NOV 11 WITH SILVER DOWN $0.79 //SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 374,000 OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 477.527 MILLION OZ

NOV 8 WITH SILVER DOWN $0.43 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 2.005 MILLION OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 477.846 MILLION OZ

NOV 7 WITH SILVER UP $0.11 //NO CHANGES IN SILVER INVENTORY AT THE SLV: /// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 6 WITH SILVER DOWN $1.41 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.692 MILLION OZ FROM THE SLV/.//// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 5 WITH SILVER UP 0.18 :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.109 MILLION OZ FROM THE SLV/.//// //INVENTORY AT SLV RESTS AT 479,533 MILLION OZ

In a recent discussion with Darcy Ungaro of The Everyday Investor, Peter challenged the widespread narratives surrounding government spending, the Fed’s 2% inflation target, and the policies that perpetuate these problems. Peter and Darcy highlight the underlying structural issues that plague the economy—massive government debt, intentional inflation, and a citizenry oblivious of the true cost of inflation.

Peter begins by pointing to the fundamental problem: profligate politicians have borrowed freely, relying on the reserve currency status of the US dollar and eager lenders worldwide. That global willingness to lend paved the way for politicians to promise generous programs without raising enough revenue to cover them:

The world was dumb enough to loan us the money. But it goes back to the days where the dollar became the reserve currency. And so the world is looking to accumulate dollars and not to just hold them in cash, but to lend them out to generate a return…

These large deficits enable politicians to promise something for nothing, which is how politicians win elections…

And so if you deliver government programs but you don’t raise taxes, commensurate with the cost of those programs, then you get votes.

This $34 trillion figure barely scratches the surface of America’s true liabilities. Unfunded promises, hidden from official tallies, only compound the country’s dire financial position:

But that’s just the tip of the iceberg because politicians didn’t just borrow money and spend it. They actually promised voters all sorts of benefits that have never been funded. So that’s still a debt that’s still a liability. Social Security, Medicare, guaranteed student loans, guaranteed mortgages, guaranteed brokerage accounts, guaranteed pensions – the US government gave all these benefits to Americans but never funded them. … So the government is hopelessly insolvent.

With the debt ballooning, the Federal Reserve faces immense pressure. Peter suggests that while the market expects interest rate cuts, economic reality demands hikes instead:

Well, the markets expect a cut, but a cut is not warranted. In fact, the Fed should continue to hike….

[The debt] is currently financed at very low rates and it would have to be rolled over at much, much higher rates. In addition, we’re adding about a trillion dollars a quarter to the national debt. So that’s another $4 trillion that the government’s going to need to borrow. In addition to the $9 trillion, it’s going to need to refinance. So you’re looking at $13 trillion of debt. I mean, I just don’t think the appetite is there around the world.

Peter recounts the history of the Fed’s 2% inflation target, noting that it was originally intended to be a limit, not a target:

Central banks eventually perverted this whole concept to making a target of inflation. Like you need 2%, that 1% isn’t enough. But that was never part of what New Zealand did. They never said that we needed 2% inflation. They just said if we get 2%, that’s too much. It needs to be, it needs to be less. 2% was the upper end of what they would tolerate for inflation. But it became the target and now it’s really a floor.

It’s in the government’s best interest to have inflation. And so they have to convince the public that it’s good for them… because that’s how they give you something for nothing.

But inflation is a tax. It’s just a tax that the public doesn’t realize they’re paying. And they actually expect us to believe it.

Contrary to what the mainstream says, falling prices benefit consumers. Falling prices don’t destroy commerce any more than rising prices:

Nobody wants health care to be more expensive, education to be more expensive, their insurance to be more expensive. Everybody wants stuff to get cheaper and it’s better.

Now, the other thing they say as well, if prices go down, businesses can’t make any money. Sure, they can. They make more money because their costs are also coming down.

Charts are not infallible, but this one tells us that there is a high degree of inevitability that the yield on the 10-year US Treasury Note is set to rise. Recently, the yield tested the golden cross formed by the 55-day and 200-day moving averages and has subsequently moved higher. The longer-term four decades chart puts this in another worrying perspective:

In August 2022, the chart broke a 42-year downtrend, always contained by the Fed reducing interest rates to rescue the US — and the world’s — economy from the fallout of bursting credit bubbles. Consequently, malinvestments and other economic distortions haven’t been purged from the system and are now rolled up into the biggest credit bubble ever seen. The consequence is heightened credit risk, which is now systemic, reflected in rising borrowing costs.

Part of this story is the debt trap the US Government now faces. Macroeconomic analysis suggests that the Fed will respond by reducing interest rates to contain credit risk and stop the zombie economy from collapsing and taking down the commercial banks. But the error in this line of thinking is to not understand that risk and borrowing costs correlate: in other words, higher interest rates reflect increasing credit risk.

That the four-decade long downtrend in US Treasury yields was finally broken in August 2022 is confirmation that the Fed no longer controls interest rates: the market has taken over. No doubt, as rising rates start bankrupting zombie corporations, and inevitably create a stock market crash, any attempt by the Fed to reduce interest rates will undermine the dollar.

While it is unthinkable for today’s investors that the Fed can lose control over interest rates, there is historical precedent. Three times following the 1844 Bank Charter Act, the Bank of England did precisely that: in 1847 only three years after the charter was granted, 1857, and 1866. The error was to not realise the true function of interest rates, which was to manage the gold reserves, and not influence economic outcomes.

We don’t have a gold exchange standard today, but the same principle applies. If the Fed muscles rates lower at times of high credit risk, it simply undermines the currency. And just as the Bank of England erred after the 1844 Act, we can be certain the Fed will do so in 2025. And just as England’s gold reserves faced a run on those occasions, today the gold price will rise, which put another way will see the dollar’s purchasing power decline at an accelerating rate.

A word to te wise: get out of credit!

3. CHRIS POWELL AND GATA DISPATCHES

Gold’s upward revaluation continues and silver is next, Maguire tells LFTV

Submitted by admin on Sat, 2024-12-14 11:41 Section: Daily Dispatches

11:40a ET Saturday, December 14, 2024

Dear Friend of GATA and Gold:

London metals trader Andrew Maguire, speaking on this week’s edition of Kinesis Money’s “Live from the Vault” program, says gold’s stair-step upward revaluation continues and that silver is setting up for a sharper rise. He adds that President-elect Trump’s plans to impose tariffs on countries he deems hostile to the U.S. dollar will boost gold as well.

The program is 40 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

END

Indonesia’s finance authority says country urgently needs a gold bank

Submitted by admin on Mon, 2024-12-16 10:45 Section: Daily Dispatches

By Nabiila Azzahra Tempo, Jakarta, Indonesia Sunday, December 15, 2024

Indonesia’s Financial Services Authority (OJK) said the need to establish a gold bank in Indonesia is urgent. A gold bank is a form of bullion business activity that is currently being developed by OJK and the government.

The chief executive of the Supervisory Board of Financing Institutions, Venture Capital Companies, Microfinance Institutions, and Other Financial Services Institutions of OJK, Agusman, explained the urgency of organizing bullion business activities.

Agusman said this was necessary considering Indonesia’s position as a producer and one of the largest gold reserve owners in the world but also as an importer to meet domestic gold needs.

With a gold bank, Indonesia will finally be able to record the value of its gold stock and include gold in its financial balance sheet. …

Trafigura saw its net profit for the financial year 2023/2024 ended on September 30 plunge by 62% as the commodity trading giant recorded a loss of $1.1 billion related to serious misconduct by individuals in its Mongolian oil business.

Trafigura booked a net profit of $2.8 billion for FY2024, down from a $7.3 billion profit in FY2023 and $6.8 billion for FY 2022, the oil and metals trading house said on Friday.

The underlying performance was strong, with strong contributions from all three core businesses – Oil and Petroleum Products; Metals, Minerals, and Bulk Commodities; and Gas, Power, and Renewables, said outgoing chief executive Jeremy Weir.

He is stepping down from the CEO role in January 2025 after ten years. Weir will be chairman of Trafigura’s board as of next year and will be succeeded by Richard Holtum as CEO, effective 1 January 2025.

Commenting on the FY2024 performance, Weir said that the strong business performance was “marred by the extremely disappointing discovery of serious misconduct by individuals in our Mongolian oil business, involving deliberate manipulation of data and documents and concealment of overdue receivables.”

Trafigura publicly disclosed in October 2024 that it had recorded a total loss of $1.1 billion on the discovered fraud in the Mongolian business. Of this loss, $358 million is reflected in the FY2024 results.

“An external investigation remains ongoing. We have reviewed other higher-risk offices and lines of business, and we are confident that these issues are isolated to a self-contained operation in Mongolia,” Weir said.

In accordance with International Accounting Standards (IAS 8), Trafigura has also restated prior year comparative figures to account for the exposure provisions for the Mongolian business.

In oil and petroleum products, “prices periodically disconnected from physical market fundamentals because of factors including the conflict in the Middle East, disruptions to shipping in the Red Sea and the ongoing war in Ukraine,” Trafigura said.

Separately, Trafigura and three other defendants earlier this month went on trial in Switzerland’s top criminal court over allegations of bribery. Trafigura has been charged for failing to take all reasonable measures to prevent payment of more than $5 million in bribes to an Angolan oil official in exchange for oil and shipping contracts more than a decade ago.

END

6 CRYPTOCURRENCY NEWS

Bitcoin Tops $106K, Goes ‘Santa Claus Mode’ As Optimism Grows For US Reserve Status

Monday, Dec 16, 2024 – 11:05 AM

Bitcoin’s price rallied almost 5% over the weekend to set a new all-time high above $106,000 amid speculation that it may become a United States reserve asset.

CK Zheng, chief investment officer of ZK Square, told Cointelegraph that Bitcoin has likely entered “Santa Claus mode,” as many investors fear missing out and look to allocate more capital into the asset class.

He predicted a Bitcoin price tag of $125,000 in early 2025 but warned a possible 30% correction could follow as most of the bullish news from the incoming Trump administration has been “priced in.”

A 30% correction from $125,000 would see Bitcoin retrace to around $87,500.

From a liquidity perspective, we should not be surprised that bitcoin continues to charge higher (but the new year may bring some weakness)…

Bitcoin has also reached a new record relative to gold (1 BTC can now buy 40 oz of gold).

Gracy Chen, CEO of Bitget, writes that while the Santa Claus rally is a well-documented phenomenon in traditional stock markets, its presence in cryptocurrency is less clear.

Cryptocurrencies, known for their volatility and 24/7 trading, don’t always follow equities’ seasonal patterns. A second trend can be applied to this model that has empirically proven a powerful predictor of a Santa Claus rally occurring in Cryptoland: whether or not the market is in a bull run.

It’s safe to say that crypto firmly checks that box right now, thus making a compelling case for a severe rally coming together as the year draws close. In late 2017, for example, BTC rallied by 68% over the two weeks spanning the New Year. Subsequent years have been more muted, in line with the prevailing market mood at the time. But then there’s 2024, which has already broken all crypto records. One wouldn’t bet against it closing out the year on a tear just to complete the clean sweep.

If traders buy into the Santa Claus rally thesis, they don’t need to create a prediction market to speculate on the likelihood — although nothing is stopping them. In crypto, financial freedom comes as a standard. A more intelligent strategy is filling one’s conviction bags before the year-end. Load up on the assets you believe in the most, and then sit back and let the prophecy unfold.

As 2024 closes out, the financial landscape presents a mix of optimism and caution. The global economy has shown resilience, with many sectors rebounding from previous downturns. Consumer spending during the holiday season is expected to be robust, bolstering market sentiment. The only potential dampener could be the escalation of global tensions in the Middle East or Ukraine. Still, barring a major macro event, there’s every reason to expect the current bull market to remain intact.

Even if the Santa Claus rally proves to be a damp squib on this occasion, it’s no biggie: The bags investors have accumulated now are likely to stand them in good stead next year as the crypto market continues to grind higher. They don’t have to leave a glass of milk and some cookies out, but there’s no excuse for not being ready for Santa this Christmas.

It comes as Strike founder and CEO Jack Mallers said US President-Elect Donald Trump could potentially issue an executive order designating Bitcoin as a reserve asset on his first day in office on Jan. 20.

“There’s potential to use a day-one executive order to purchase Bitcoin,” Mallers stated, adding:

“It wouldn’t be the size and scale of 1 million coins but it would be a significant position.”

Meanwhile, Satoshi Action Fund CEO Dennis Porter saida third Bitcoin reserve bill is in the works at the state level, though he didn’t say which state might follow Texas and Pennsylvania’s lead.

“We had Pennsylvania, and we had Texas. And now we have another state coming on board. And they sent me the draft. So I know it’s real,” he said during a Dec. 15 X Spaces.

Porter added he expects at least 10 states to introduce a Bitcoin reserve bill in total.

“Its not going to stop. We’re going to see more and more of these bills come. At least 10, in my opinion.”

Financial analysts are also tipping a 0.25% interest rate cut from the US Federal Reserve on Dec. 18, which could lift Bitcoin’s price even further in the coming months.

Another catalyst behind Bitcoin’s price surge may be one of the new rules by the Financial Accounting Standards Board, which enables institutions to record the value of their crypto assets more realistically. The rule will apply to fiscal years beginning after Dec. 15.

However, bitcoin’s market sentiment is currently in the “Extreme Greed” zone at a score of 83 out of 100, according to the Crypto Fear and Greed Index.

Crypto Fear and Greed Index score for Dec. 16. Source: Alternative.me

// Nikkei CLOSED DOWN 152.05 OR 0.03%//Australia’s all ordinaries CLOSED DOWN .66%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7.2910 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2909// Oil UP TO 70.64 dollars per barrel for WTI and BRENT UP AT 73.97 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS MONDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.2910

OFFSHORE YUAN: DOWN TO 7.2909

SHANGHAI CLOSED CLOSED DOWN 5.55 PTS OR 0.03%

HANG SENG CLOSED CLOSED DOWN 175.75 PTS OR 0.88%

2. Nikkei closed DOWN 12.95 PTS OR 0.03%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 106.65 EURO RISES TO 1.0498 UP 45 BASIS PTS

3b Japan 10 YR bond yield: RISWS TO. +1.059 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 154.06…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.2295 Italian 10 Yr bond yield DOWN to 3.379 //SPAIN 10 YR BOND YIELD DOWN TO 2.912

3i Greek 10 year bond yield DOWN TO 3.055

3j Gold at $2657.65/Silver at: 30.64 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 65/100 roubles/dollar; ROUBLE AT 103.85

3m oil into the 70 dollar handle for WTI and 73 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 154.15 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.059% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.827 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9373 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.367 DOWN 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.578 DOWN 4 BASIS PTS/

USA 2 YR BOND YIELD: 4.226 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 34.96…

10 YR UK BOND YIELD: 4.4385 UP 3 PTS

10 YR CANADA BOND YIELD: 3.182 UP 0 BASIS PTS

5 YR CANADA BOND YIELD: 2.975 DOWN 1 PTS.

2a New York OPENING REPORT

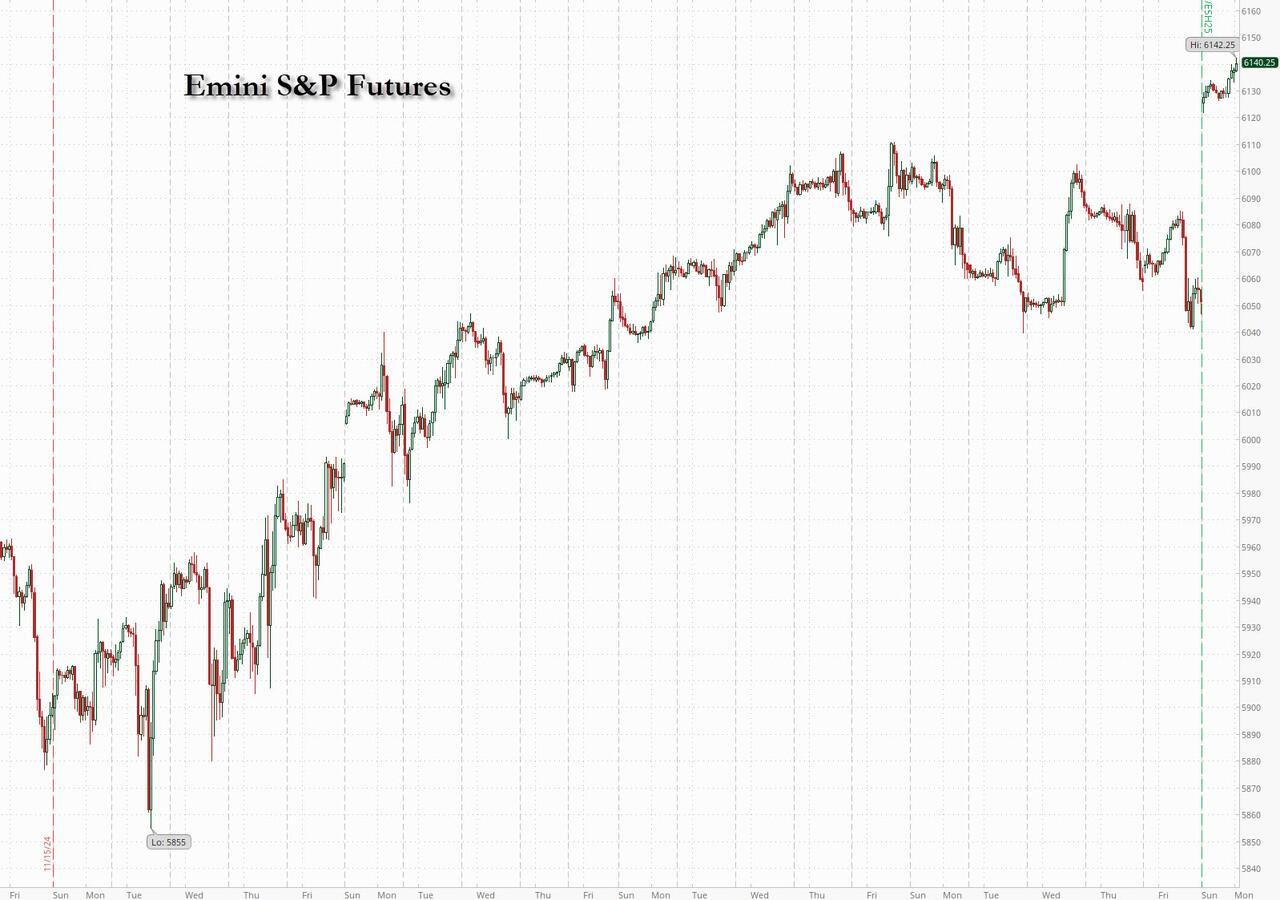

US Futures Jump, Ignore Global Selloff While Focusing On Imminent Rate Cut

Monday, Dec 16, 2024 – 08:27 AM

The last full week of 2024 started off with a burst of US exceptionalism which helped US equity futures shrug off downbeat performances in other global markets as traders prepared for a slate of interest-rate decisions by major central banks due later this week. S&P and Nasdaq futures both traded at record high, as did Bitcoin which hit a fresh all-time high of $106,000. As of 8:00am ET, S&P futures were 0.3% higher and Nasdaq futures gained 0.5% as the panic chase of momentum, which pushed the index at an all-time high on Friday, continued. MicroStrategy advanced more than 6% in premarket trading, fueled by its pending inclusion in the index following the software maker’s transformation into a leveraged bet on Bitcoin. Monday’s US stock performance stands in stark contrast with broad losses in Asia and Europe as weaker-than-expected retail data in China weighed on sentiment. A contraction in the euro-area’s private sector also dragged on European equities. Treasuries climb, pushing US 10-year yields down 2 bps to 4.38%. The Bloomberg Dollar Spot Index falls 0.1%. Oil dipped with WTI falling 0.9% to $70.60 a barrel. Today’s key macro events are the Empire Fed Manfuacturing index and S&P Global PMI prints for the US.

In premarket trading, MicroStrategy leads fellow cryptocurrency-exposed stocks higher on optimism about the company’s upcoming inclusion of the company in the Nasdaq 100 Index. MicroStrategy (MSTR) +4%, Riot Platforms (RIOT) +2%, Mara Holdings (MARA) +2%. On the other end, Super Micro Computer tumbled 15% after the announcement that the stock is to be removed from the Nasdaq 100 in the annual reconstitution of the index. Here are some other notable premarket movers:

Axon (AXON) rises 2% as the stock will be added to Nasdaq 100 Index in annual reconstitution of the index.

Capri Holdings (CPRI) climbs 5% after Women’s Wear Daily reported that the fashion company is working with a bank to find buyers for its Versace and Jimmy Choo brands.

Edgewise Therapeutics (EWTX) gains 23% after the company said its Phase 2 trial of sevasemten in individuals with Becker muscular dystrophy met its primary endpoint.

Ford shares (F) falls 2% as Jefferies turns bearish on the automaker, citing concerns ranging from inventory overhang to looming strategic decisions on the company’s European presence.

Honeywell (HON) advances 3% after saying it’s considering strategic options, including the possible separation of its aerospace business, a month after Elliott Investment Management called for a breakup of the industrial group.

Red Cat (RCAT) rises 14% after the drone tech company announced a strategic partnership with Palantir Technologies.

Teradyne, NetApp and Keysight Technologies all rise after JPMorgan upgraded the three tech hardware firms amid growing demand for their products.

An expected quarter-point rate cut from the Federal Reserve on Wednesday could add fresh support and extend US stocks’ outperformance. The S&P 500 has rallied 27% so far in 2024, with strategist expecting the rally to build further steam in anticipation of favorable economic policies under President-elect Donald Trump and strong earnings.

“Central banks have been helpful in 2024 as they start cutting interest rates when the economy was still strong,” Marija Veitmane, senior multi-asset strategist at State Street Global Equities, told Bloomberg TV. Going forward, “what we need to rely on is earnings and where they can grow the fastest. In the US, we can still see solid growth.”

Wednesday’s Fed decision will be followed by peers in Japan, the Nordics and the UK over the following day. Swaps traders are now pricing in around three quarter-point rate cuts by the Fed over the next 12 months, whereas they’d seen better than 50/50 odds of a fourth one a week ago.

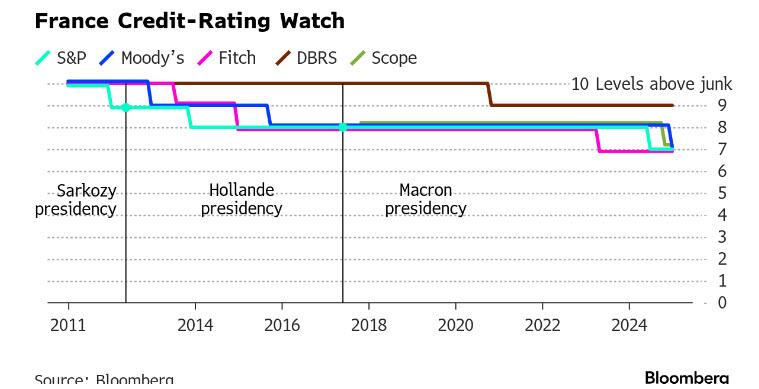

In Europe, the Stoxx 600 is down 0.3% in the wake of disappointing retail-sales data in China, while traders assess the impact of Moody’s Ratings’ France downgrade. Banks are the best performers while Novo Nordisk boosts healthcare stocks after announcing its Catalent deal got the go-ahead. Automakers and consumer goods are the biggest laggards. France’s CAC 40 falls 0.7%, underperforming its regional peers after Moody’s cut the French credit rating on Friday. Here are some of the biggest movers on Monday:

Novo Nordisk shares rise as much as 2.7% after the Danish drugmaker said it can advance with its acquisition of factories from contract development and manufacturing organization Catalent.

Basilea shares rise as much as 9.2% after the Swiss pharma company entered into an exclusive distribution and license agreement with Innoviva for the commercialization of Basilea’s hospital anti-MRSA antibiotic Zevtera in the US.

Johnson Matthey shares rise as much as 6.6%, the most since March, after its largest shareholder, Standard Investments, called on the chemicals company to refresh its board and launch a strategic review of the business following its underperformance in recent years.

Galderma gains as much as 4.7%, the most since Aug. 6 and hitting a record high, after UBS upgraded the Swiss dermatology firm to buy from neutral.

DKSH shares gain as much as 3.5%, the most since July, after the Swiss distribution group saw its recommendation raised to outperform from neutral at BNP Paribas Exane, seeing a “potent mix of margin expansion and balance sheet optimization” driving earnings momentum.

Bunzl shares rise as much as 2.8% after the value-added distributor was upgraded by analysts at RBC Capital Markets, citing a dependable outlook and an undemanding valuation.

Porsche Automobil Holding SE shares drop as much as 3.3% after the German firm withdrew its current year forecast due to the expected impairment of at-equity carrying amounts of its investments in Volkswagen and Porsche AG.

Getlink shares drop as much as 3.6%, the most since June, after the travel infrastructure operator warned it has discovered a second fault on its interconnector between France and the UK.

Earlier in the session, Asian stocks also slumped, dragged lower by shares in mainland China after the country’s retail sales data came below expectations. The MSCI Asia Pacific Index declined 0.2%, with China Eastern Airlines and Australian miner Fortescue Ltd among the biggest losers. Hong Kong and mainland China were among the worst performing markets in the region, while the stock benchmark in Taiwan rose. China’s data dump on Monday showed retail sales for November rose 3% on-year, well below an expectation of a 5% gain. That weighed on sentiment at a time when Beijing has been touting more stimulus to support spending. Home prices fell for a third month in a row, although the decline is slowing. Chip makers Taiwan Semiconductor Manufacturing Co and SK Hynix were among the gainers. A gauge tracking Asian IT shares was up around 0.3%.

The retail-sales data “is a reflection of the dire situation there and how the stimulus efforts have prioritized optics over delivering meaningful economic improvements,” said Charu Chanana, chief investment strategist at Saxo Markets in Singapore. “Even for a tactical recovery, we need more after a series of false starts and the risk of tariffs ahead.”

“This data really verifies that the headwinds for consumers are still very very high,” said Johanna Chua, head of emerging market economics at Citigroup Global Markets in a Bloomberg TV interview.

In FX, the Bloomberg dollar index was little changed after six days of gains. Wall Street is starting to sour on the dollar as President-elect Donald Trump’s policies and the Fed’s interest-rate cuts will likely put pressure on the greenback in the latter portion of 2025. Roughly a half dozen sell-side strategists are now forecasting the world’s reserve currency will peak as early as mid next year before starting to decline. Euro-area PMIs were mixed and largely ignored with the euro little changed versus the dollar. The pound outperforms, rising 0.2% as investors seemed to focus on the services PMI beat rather than the manufacturing PMI miss.

In rates, treasuries hold small gains, tracking bigger rallies in bunds and gilts after mixed European PMI readings and recovering some of last week’s steep loss. US yields are richer by 1.5bp to 3bp across maturities with gains led by front-end and belly, steepening 5s30s spread by ~1bp. 10-year is back around 4.37% after topping 4.4% Friday for the first time since Nov. 22. OATs also lag their German counterparts, widening the 10-year yield spread to around 79 bps, after France was downgraded unexpectedly by Moody’s on Friday. Treasury coupon auctions this week include $13 billion 20-year bond reopening Tuesday and $22 billion 5-year TIPS reopening Thursday. US session includes Empire manufacturing survey and US PMIs, with November retail sales ahead Tuesday before Wednesday’s Fed rate decision. Oil trades lower, also supporting Treasuries.

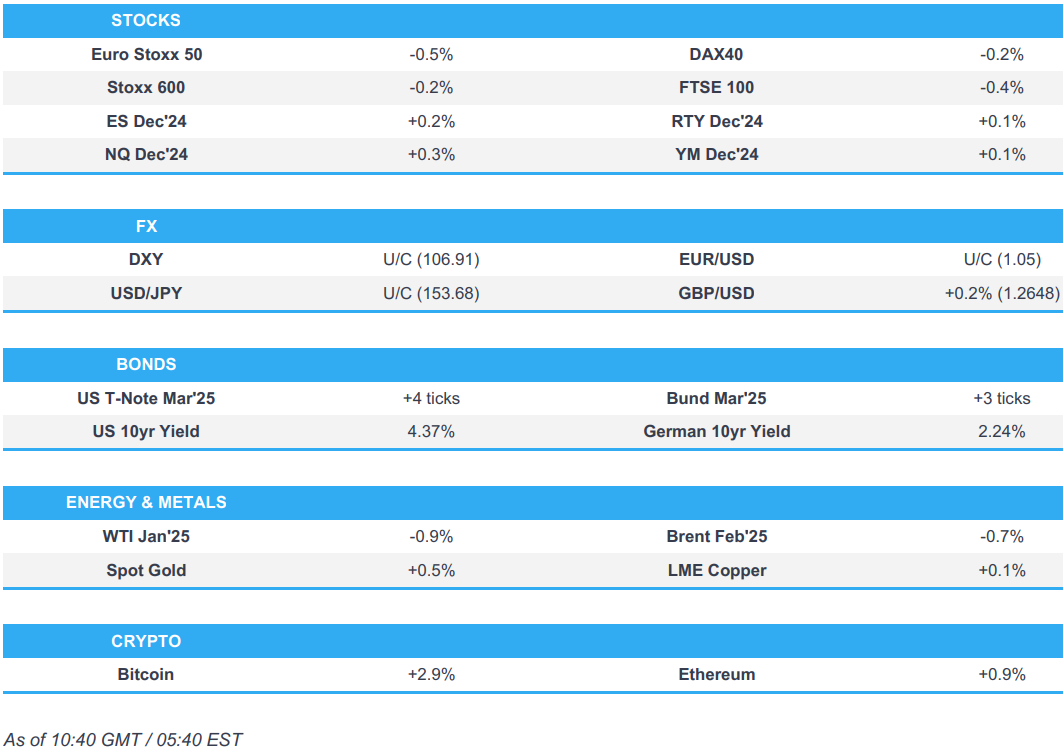

In commodities, oil prices declined, with WTI falling 0.9% to $70.60 a barrel after rising 6.1% last week. Spot gold adds $12 to around $2,660/oz. Bitcoin rallies to a record high.

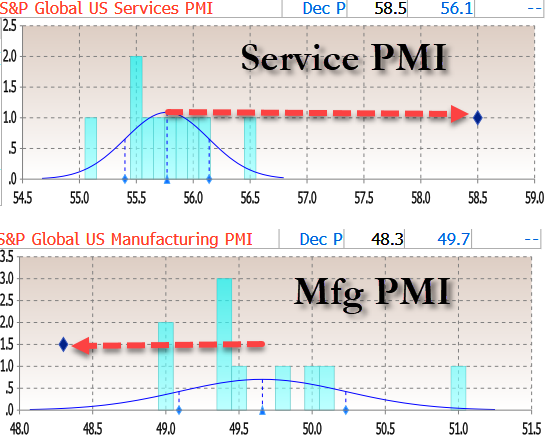

Today’s US economic data calendar includes December Empire manufacturing (8:30am) and S&P Global US manufacturing and services PMIs at 9:45am

Market Snapshot

S&P 500 futures little changed at 6,061.50

STOXX Europe 600 down 0.1% to 515.69

MXAP down 0.2% to 185.09

MXAPJ down 0.2% to 584.05

Nikkei little changed at 39,457.49

Topix down 0.3% to 2,738.33

Hang Seng Index down 0.9% to 19,795.49

Shanghai Composite down 0.2% to 3,386.33

Sensex down 0.4% to 81,777.79

Australia S&P/ASX 200 down 0.6% to 8,249.48

Kospi down 0.2% to 2,488.97

German 10Y yield down 1 bp at 2.25%

Euro up 0.1% to $1.0516

Brent Futures down 0.7% to $73.97/bbl

Gold spot up 0.4% to $2,657.85

US Dollar Index down 0.19% to 106.81

Top Overnight News

US DHHS nominee (under President-elect Trump) RFK Jr. is to attempt to win over the Senate by playing down the vaccine topic and sticking to Trump’s messaging: WSJ

Nasdaq announced that Palantir Technologies (PLTR), MicroStrategy (MSTR), and Axon Enterprise (AXON) will be added to the index, while Illumina (ILMN), Super Micro Computer (SMCI), and Moderna (MRNA) will be removed as part of the annual reconstitution of the Nasdaq-100 Index, which will become effective prior to market open on Monday, December 23rd: RTRS

WSJ’s Timiraos writes, ahead of this week’s FOMC, “Investors widely expect a third-in-a-row rate cut this week. Officials are ready to slow—or even stop—lowering rates after that.”

A surprise retail slowdown in China highlighted the urgency for Beijing to further boost consumer spending. Sales growth slowed sharply last month, though industrial output improved. BBG

China’s regulators pledged to boost efforts to stabilize the housing and equity markets, as well as conduct more effective fiscal policies. Several branches weighed in after a major leadership meeting last week ended in calls for greater stimulus. BBG