MAY 6//GOLD CLOSED UP $101.55 TO $3414.80 WHILE SILVER WAS UP A HUGE 92 CENTS TO $33.14//PLATINUM IS UP $28.85 TO $988.70//PLATINUM IS UP $34.20 TO $976.70/THE TWO BIG STORIES: HOUTHIS GIVE UP AND SURRENDER//AND THEN INDIA FIRES ON PAKISTAN//OTHER ISRAEL VS HAMAS UPDATES//HEZBOLLAH UPDATES/RUSSIA VS UKRAINE UPDATE/COVID UPDATES/VACCINE INJURY REPORT/DR PAUL ALEXANDER//MARK CRISPIN MILLER//SLAY NEWS ETC//NEWS ON THE MEETING WITH TRUMP OF THE USA AND CANADA’ CARNEY//SWAMP STORIES FOR YOU TONIGHT..

099 H DEUTSCHE BANK AG 87 118 C MACQUARIE FUTURES US 11 190 H BMO CAPITAL MARKETS 32 323 C HSBC 49 363 H WELLS FARGO SECURITI 18 657 H MORGAN STANLEY 100 661 C JP MORGAN SECURITIES 84 686 C STONEX FINANCIAL INC 1 737 C ADVANTAGE FUTURES 2 1 905 C ADM 7

TOTAL: 196 196 MONTH TO DATE: 12,825

JPMORGAN STOPPED 94/196

MAY

GOLD: NUMBER OF NOTICES FILED FOR MAY/2024. CONTRACT: 196 NOTICES FOR 19,600 OZ 0.6096 TONNES

total notices so far: 12,825 contracts for 1,282,500 OR 39.891 tonnes)

FOR MAY

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 107 NOTICE(S) FILED FOR 0.535 MILLION OZ/

total number of notices filed so far this month : 13,205 CONTRACTS (NOTICES) for 66.025 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $101.55 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 6.32 TONNES OF GOLD OUT OF THE GLD

INVENTORY RESTS AT 937.36 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.92 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: ////A HUGE WITHDRAWAL OF 2.818 MILLION OZ OUT OF THE SLV//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 448.783 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A MEGA HUGE SIZED 1066 CONTRACTS TO 137,571 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR GAIN OF ONLY $0.08 IN SILVER PRICING AT THE COMEX WITH RESPECT TO MONDAY’S TRADING. WE HAD A HUMONGOUS SIZED GAIN OF 1249 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A SMALL 83 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE.. WE HAD A ZERO LIQUIDATION OF T.A.S. CONTRACTS COMEX TRADING MONDAY AS THEY DESPERATELY AGAIN TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $34.40 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY FAILED ON MONDAY WITH SILVER’S SLIGHT GAIN IN PRICE AS THE PRICE IS STILL WELL BELOW THE MAGIC NUMBER OF $34.40 SILVER SPOT PRICE. . BUT THIS WAS COUPLED WITH A STRONG T.A.S. ISSUANCE OF 596 CONTRACTS ISSUED BY THE CME AND THAT SIGNALS DEEP CODE RED THAT THE CROOKS ARE DESPERATE TO STOP SILVER BREAKING OVER THE 34.40 DOLLAR MARK. THUS OUR RAIDS ON OUR PRECIOUS SILVER METAL WILL CONTINUE UNTIL SILVER BREAKS $34.40. WE HAD A SMALL 83 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR STRONG 596 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN TUESDAY’S TRADING/ AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A HUGE SIZED 1149 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR TINY GAIN IN PRICE OF $0.08.

THE CME NOTIFIED US THAT FOR THE FIRST TWO DAYS OF THE MONTH OF MAY, WE HAD TWO CONSECUTIVE ISSUANCE OF EXCHANGE FOR RISK CONTRACTS OF 12.93 MILLION OZ. THESE EXCHANGE FOR RISKS MUST NOW BE ADDED TO OUR NORMAL DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS WITHOUT A DOUBT THE CENTRAL BANK OF INDIA. LOGICALLY ONLY A CENTRAL BANK WOULD ACCEPT THIS CRAZY CONTRACT WHEREBY THE CENTRAL BANK OF INDIA TAKES THE RISK OF DELIVERY FROM A BULLION BANK WHO CANNOT GUARANTEE DELIVERY OF PHYSICAL SILVER TO THEM.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S ESPECIALLY SILVER IS NOW USED TO TEMPER OUR SILVER PRICE RISE OR INITIATE A RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN WITH THIS WEEK’S TRADING ON SILVER AND NOW TODAY TRYING TO KEEP THE SILVER PRICE BELOW $34.40 . THE KEY PRICE TO WATCH IS $34.40. IF IT BREAKS THAT PRICE, THEN WE HEAD FOR $50.00 SILVER.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT/TUESDAY MORNING: A STRONG 569 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.08) AND WERE SUCCESSFUL IN KNOCKING OFF SOME NET SILVER LONGS FROM THEIR PERCH

WE HAD A SMALL 83 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 67.830 MILLION OZ TO WHICH WE ADD OUR 90 CONTRACT QUEUE JUMP OF 0.450 MILLION OZ AND THEN WE MUST ADD THOSE CRAZY CONTRACT EXCHANGE FOR RISK FOR 12.93 MILLION OZ

INITIAL STANDING FOR MAY: 70.080 MILLION OZ WHICH INCLUDES TODAY’S 0.450 MILLION QUEUE JUMP + 12.93 MILLION OZ (EX FOR RISK) EQUALS 83.01 MILLION OZ./

WE HAD:

/ HUGE COMEX OI GAIN+// A SMALL SIZED EFP ISSUANCE (83 CONTRACTS)/ VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 596 CONTRACTS)

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: ADDED 575 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY

TOTAL CONTRACTS for 4 DAYS, total 1644 contracts: OR 8.220 MILLION OZ (411 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 8.2200 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 8.220 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1066 CONTRACTS DESPITE OUR SMALL GAIN IN PRICE OF $0.08 IN SILVER PRICING AT THE COMEX// MONDAY.,. . THE CME NOTIFIED US THAT WE HAD A SMALL 83 CONTRACT EFP ISSUANCE CONTRACTS: 83 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 15.965 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND NOW MAY:

NEW STANDING FOR MAY: 70.080 MILLION OZ. (INCLUDES 0.450 MILLION OZ QUEUE JUMP + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE.//NEW TOTAL STANDING 83.01 MILLION OZ

THE NEW TAS ISSUANCE MONDAY NIGHT (596 ) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND FOR SURE MONDAY TRADING.

WE HAD 107 NOTICE(S) FILED TODAY FOR 0.535 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL. IT IS NOW TIME FOR THE FBI TO ENTER THE COMEX AND ARREST THESE CROOKS EVEN THOUGH THE MAJORITY OF THE TRADING IS GOVERNMENT. THE BANKERS ARE COMPLICIT

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 3810 OI CONTRACTS TO 442,137 AND CLOSER TO TO THE RECORD (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. (ALL TIME LOW OF 390,000 CONTRACTS.) THUS WE HAVE A PRETTY LOW OI IN COMEX WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE SHIP.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A SMALL 492 CONTRACTS //.

WE HAD A FAIR SIZED INCREASE IN COMEX OI (3810 CONTRACTS) . THIS OCCURRED DESPITE OUR STRONG GAIN OF $77.95 IN PRICE MONDAY. ON WEDNESDAY/APRIL 17 WE HAD THE HIGHEST EVER SINGLE NOMINAL GAIN IN COMEX GOLD PRICING HISTORY AT $106.35 GAIN.. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER..

WE ALSO HAD A HUMONGOUS INITIAL STANDING IN GOLD TONNAGE FOR APRIL AT 164.7185 TONNES/) TO WHICH WE ADDED + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

FINAL STANDING FOR APRIL; 201.443 TONNES + 8.3571 TONNES EX FOR RISK = 209.800 TONNES

INITIAL STANDING FOR MAY: 40.223 TONNES OF GOLD!

/ ALL OF THIS HAPPENED WITH OUR $77.95 GAIN IN PRICE WITH RESPECT TO MONDAY’S COMEX ///. WE HAD A FAIR SIZED GAN OF 3811 OI CONTRACTS (13.384 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! THE RESULT: A MASSIVE AMOUNT OF GOLD STANDING FOR DELIVERY FOR THE MARCH CONTRACT MONTH AS WELL AS THE SAME FOR APRIL AND NOW MAY….. A MONSTROUS 40.223 TONNES DESPITE IT BEING AN OFF MONTH. CENTRAL BANKERS ARE NOW WAITING PATIENTLY FOR THEIR DELIVERY OF GOLD VIA SLOW MOVING SHIPS.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A TINY SIZED 1 CONTRACT:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 442,629/NOW AT THE LOW END OF THE SCALE DESPITE THE HIGH PRICE OF GOLD!!

SILVER ALSO HAS A LOW COMEX OI OF 137,671 CONTRACTS!!

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3811 CONTRACTS WITH 3810 CONTRACTS INCREASED AT THE COMEX// AND A SMALL SIZED 1 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3811 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED AND CRIMINAL 1641 CONTRACTS ISSUED. WE HAD ZERO T.A.S. LIQUIDATION DURING THE COMEX SESSION MONDAY

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1 CONTRACT) ACCOMPANYING THE STRONG SIZED INCREASE IN COMEX OI OF 3810 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 3811 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG STANDING FOR GOLD FOR MAY AT 40.223 TONNES ( WHICH WHICH INCLUDES OUR 0.6220 TONNES QUEUE JUMP)

NEW STANDING FOR GOLD, MAY CONTRACT ADVANCES TO: 40.223 TONNES OF GOLD.

.

/ 3) ZERO T.A.S. LIQUIDATION IN REMOVING ANY NET SPECULATOR LONGS, AS WE HAD 1)A $77.95 COMEX PRICE GAIN.. WE HAD 2) ZERO NET LONG SPECS BEING CLIPPED WITH OUR GOOD GAIN OF 4303 CONTRACTS ON OUR TWO EXCHANGES// /./ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED MONDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL AND THUS OUR HUGE TONNAGE STANDING FOR GOLD FOR MAY.

4) FAIR SIZED COMEX OI GAIN// 5) SMALL SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER (1 CONTRACTS)///STRONG T.A.S. ISSUANCE: 1641 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2025 INCLUDING TODAY

MAY INITIAL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY :

TOTAL EFP CONTRACTS ISSUED: 2805 CONTRACTS OR 280,500 OZ OR 8.7247 TONNES IN 4 TRADING DAY(S) AND THUS AVERAGING: 701 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN4 TRADING DAY(S) IN TONNES 8.7247 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2024, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 8.7247 TONNES DIVIDED BY 3550 x 100% TONNES = 0.245% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

2024 AND 2025:

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR. 3,597.846 TONNES

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL A SMALL TO FAIR ISSUANCE FOR THE MONTH.

MAY: 8.7247 TONNES OF GOLD EFP ISSUANCE

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 1066 CONTRACTS OI TO 137,571 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 83 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 83 and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 720 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1066 CONTRACTS AND ADD TO THE 83 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1149 CONTRACTS DESPITE THE TINY GAIN IN PRICE OF $0.08 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 6.245 MILLION PAPER OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS TUESDAY MORNING//MONDAY NIGHT

SHANGHAI CLOSED UP 37.08 PTS OR 1.13%

//Hang Seng CLOSED UP 158.03 PTS OR .70%

// Nikkei CLOSED //Australia’s all ordinaries CLOSED DOWN .06%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.2172 OFFSHORE CLOSED UP AT 7.2125 / Oil UP TO 59.27 dollars per barrel for WTI and BRENT UP TO 62,15 Stocks in Europe OPENED MOSTLY ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING S:/ONSHORE YUAN UP TRADING AT 72172 AND STRONGER//

UP 7.2125 AGAINST US DOLLAR/OFFSHORE YUAN AND THUS STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED3810 CONTRACTS TO 442,137 WITH OUR STRONG GAIN IN PRICE OF $77.95 WITH RESPECT TO MONDAY’S // TRADING. WE LOST ZERO NUMBER OF NET LONGS WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A TINY TINY NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1 ).

THE CME ANNOUNCED MONDAY NIGHT, A 0 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 0 OZ OR 0.0 TONNES. TOTAL ISSUANCE FOR MAY IS ZERO. IN THE MONTH OF APRIL WE HAD RECORDED A NEW RECORD 7 ISSUANCES OF EXCHANGE FOR RISK AS THE BANK OF ENGLAND IS GETTING VERY ANTSY ABOUT GETTING ITS GOLD BACK. THUS OUR TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL STOOD AT 8.3571 TONNES OF GOLD WHICH WERE ADDED TO OUR NORMAL APRIL GOLD DELVERIES.

HISTORY: LAST THREE PRIOR MONTH’S EXCHANGE FOR RISK

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

THE RECIPIENT OF ALL OF THESE EXCHANGE FOR RISK CONTRACTS IS THE BANK OF ENGLAND WHO DESPERATELY WANT THEIR LEASED GOLD BACK. THUS WE HAVE TWO SEPARATE ENTITIES (CENTRAL BANKS) DEMANDING THEIR GOLD BACK:

THE BANK OF ENGLAND

THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO THE BANK OF ENGLAND’S EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED AND THUS THE BUYER, THE CENTRAL BANK OF ENGLAND, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 5TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH APRIL)

IN APRIL:

AND NOW WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

MAY: 0 ISSUED SO FAR…

DETAILS ON MAY COMEX MONTH//INITIAL

IN TOTAL WE HAD A GOOD SIZED GAIN ON OUR TWO EXCHANGES OF 3811 CONTRACTS WITH OUR STRONG GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON MONSDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTEMPTED AND FAILED RAID VERY EARLY IN THE COMEX SESSION AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED LATE (JAN 30) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW REVERTED BACK TO 1% BUT GOLD IN LONDON IS STILL EXTREMELY SCARCE. WE CAN NOW SAFELY SAY THAT THERE IS A RUN ON A BANK AND THAT BANK IS THE BANK OF ENGLAND!!!

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH OF APRIL AND ONTO MAY, CONTINUED TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A LITTLE LARGER THAN FROM OUR PREVIOUS FEW DAYS AT 1769 CONTRACTS

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS IS WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY AS YOU WILL SEE BELOW ANOTHER MASSIVE QUEUE JUMP OCCURRED ON MAY’S DELIVERY CYCLE AND ANOTHER HUGE QUEUE JUMP MONDAY NIGHT AT 0.628 TONNES

THE TONNAGE STANDING FOR GOLD FOR MAY IS NOW 40.223 TONNES (WHICH INCLUDES TODAY’S MASSIVE QUEUE JUMP)

THE FED IS THE OTHER MAJOR SHORT OF AROUND 22+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 221 EPISODE. AS HE TACKLES THIS IMPORTANT TOPIC. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF IT FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST (FED AND COMEX) MUST BE COMPLIANT BY JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

EXCHANGE FOR PHYSICAL ISSUANCE

THE CME REPORTS THAT THE BANKERS ISSUED A TINY TINY SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A TINY SIZED 1 EFP CONTRACT WAS ISSUED: : /JUNE 1 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 4303 CONTRACTS IN THAT 1 CONTRACT LONG WAS TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A FAIR SIZED GAIN OF 3810 COMEX CONTRACTS..AND THIS GOOD GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR STRONG GAIN IN PRICE OF $77.95 /// MONDAY/ COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE. LOOKS LIKE THE SHORT RATS ARE FLEEING THE ARENA AS EVIDENCED BY THE LOWER OPEN INTEREST AT THE COMEX!

WE HAD NO:

LIQUIDATION OF OUR T.A.S. SPREADERS

ZERO SPEC LIQUIDATION

T.A.S.SPREADER ISSUANCE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A FAIR SIZED 1641 CONTRACTS,

THE RAIDS ON OPTIONS EXPIRY APRIL MONTH AND THE FORTHCOMING MAY OPTIONS EXPIRY IN 3 WEEKS ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

STALLS THE ADVANCE IN PRICE

LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS/DECEMBER THROUGH MARCH, APRIL AND MAY

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE

FINAL STANDING FOR GOLD APRIL

// WE HAD A HUGE AMOUNT OF GOLD TONNAGE STANDING: APRIL (209.573 TONNES//.CME CORRECTED//) WHICH IS HUGE FOR OUR ACTIVE APRIL DELIVERY MONTH. FEB HAD THE HIGHEST STANDING FOR GOLD EVER RECORDED FOR ANY MONTH AT 256.607 TONNES

AND NOW LAST 5 MONTHS OF 2025: STANDING FOR GOLD

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: INITIAL STANDING AT 28.945 INITAL GOLD TONNES STANDING FIRST DAY NOTICE PLUS 0.628 TONNES QUEUE JUMP MAY 6 = 40.223 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

2025 STANDING FOR GOLD/COMEX

January 2025: 70.102 TONNES + 43.208 EXCHANGE FOR RISK= 113.310 TONNES

FEBRUARY:/NEW STANDING ADVANCES TO 238.153TONNES +18.4527 EX FOR RISK

= 256.607 TONNES. THIS IS THE HIGHEST EVER MONTH FOR GOLD STANDING IN COMEX HISTORY

MARCH: 67.9479 TONNES (INCLUDES 7.6179 TONNES EX FOR RISK)

APRIL: 209.953 TONNES (INCLUDES 8.3571 TONNES EX FOR RISK/AND ALL MONTHLY QUEUE JUMPING)

MAY: STANDING NOW 40.223 TONNES

COMEX GOLD TRADING/MAY CONTRACT MONTH

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A STRONG $77.95/ /)AND THEY WERE A UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SPECULATOR LONGS AS WE DID HAVE A FAIR SIZED GAIN IN OI FROM TWO EXCHANGES. AND AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION MONDAY BUT THEY ARE STILL TRYING TO QUELL GOLD’S ATTEMPT AT FURTHER INCREASES ABOVE $3,400 AND STOP HUGE COMEX/OTC DERIVATIVE LOSSES FROM EXPLODING AS IT LOOKS LIKE THEY ARE NOW FAILING AS GOLD ATTEMPTS TO BREACH THAT 3400 DOLLAR BARRIER AS IT IS NOW TRADING EARLY MORNING CLOSE TO THAT LEVEL AT $3395.00 UP $78 DOLLARS ON THE DAY

MONDAY NIGHT/TUESDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING SEVERAL WEEKS TO DELIVER

EXCHANGE FOR RISK EXPLANATION/FEB THROUGH /MAY TRADING

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH.

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK/APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRILL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAVE 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE OF EXCHANGE FOR RISK = ZERO SO FAR!

FINAL STANDING FOR GOLD NOW FOR APRIL:

APRIL: 201.573 TONNES +(8.3571 EX FOR RISK// FOR APRIL DELIVERY MONTH =209.953 TONNES OF THE GOLD. THIS IS THE 2ND HIGHEST AMOUNT OF DELIVERY GOLD WHICH FOLLOWS THE HIGHEST EVER ON AN ACTIVE MONTH GOLD DELIVERY BEING FEB 2025 AT 256.607 TONNES..

ANALYSIS MAY DELIVERY MONTH GOING INTO FIRST DAY NOTICE MAY CONTRACT

WE HAVE GAINED A FAIR SIZED TOTAL OF 13.384 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY FIRST RECORDED AT 28.945 TONNES ON FIRST DAY NOTICE. WE HAD A GOOD 107 CONTRACT QUEUE JUMP FOR 10,700 OZ OR 0.628 TONNES. THIS QUEUE JUMP IS CENTRAL BANKS JUMPING AHEAD OF US MORTALS DEMANDING GOLD FOR THEIR RESERVES. THUS NEW STANDING ADVANCES TO 40.223 TONNES OF GOLD.

THUS MAY STANDING FOR GOLD SO FAR: 39.596 TONNES

ALL OF THIS HUGE STANDING WAS ACCOMPLISHED DESPITE OUR GAIN IN PRICE TO THE TUNE OF $77.95

WE HAD A SMALL 492 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 3811 CONTRACTS OR 381100 0Z (11.85 TONNES)

a)) Out of Brinks: 299,068.602 oz (9302 kilobars) b) Out of HSBC 99,250.137 oz (3087 kilobars)

total withdrawal: 398,318.739 oz(12,390 kilobars)

12.390 tonnes of gold

Deposit to the Dealer Inventory in oz

0 ENTRIES

Deposits to the Customer Inventory, in oz

we have 1 customer entries

we have 1 customer entry deposits i) Into JPMorgan: 11,350.451 oz 353 kilobars

0.353 tonnes

xxxxxxxxxxxxxxxxI

No of oz served (contracts) today

196 notice(s) 19600 OZ 0.6096 TONNES

No of oz to be served (notices)

107 contracts 10,700 OZ 0.3328 TONNES

Total monthly oz gold served (contracts) so far this month

12,825 notices 1,282,500 oz 39.891 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 0 entry

xxxxxxxxxxxxxxxxxxxxx

we have 1 customer entries

we have 1 customer entry deposits i) Into JPMorgan: 11,350.451 oz 353 kilobars

0.353 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals:

withdrawals: 2 entries

a)) Out of Brinks: 299,068.602 oz (9302 kilobars) b) Out of HSBC 99,250.137 oz (3087 kilobars)

total withdrawal: 398,318.739 oz(12,390 kilobars)

12.390 tonnes of gold

adjustments: 1//first: Brinks//dealer to customer:

a) Brinks 32,016.960 oz

AMOUNT OF GOLD STANDING FOR MAY

THE FRONT MONTH OF MAY STANDS AT 303 CONTRACTS FOR A LOSS OF 1125 CONTRACTS. WE HAD 1327 CONTRACTS SERVED ON MONDDAY SO WE GAINED A STRONG 202 CONTRACTS OR 20,200 OZ FOR 0.628 TONNES

JUNE LOST ONLY 1116 CONTRACTS TO 308,187. JUNE BECOMES OUR NEW FRONT MONTH AND THIS MONTH WILL BE A WHOPPER OF A DELIVERY MONTH. THE FRBNY IS QUITE NERVOUS LOOKING AT JUNE OI.

JULY GAINED 59 CONTRACTS TO STAND AT 548

We had 196 contracts filed for today representing 19,600 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 196 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 84 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MAY /2025. contract month, we take the total number of notices filed so far for the month (12,825 X 100 oz ) to which we add the difference between the open interest for the front month of MAY (303 CONTRACTS) minus the number of notices served upon today (196 x 100 oz per contract) equals 1,293,200 OZ OR 40.223 TONNES

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (12,825 x 100 oz +we add the difference for front month of MAY (303 OI} minus the number of notices served upon today (196 x 100 oz) which equals 1,293,200 OZ OR 40.223 TONNES

TOTAL COMEX GOLD STANDING FOR MAY.: 40.223 TONNES WHICH IS HUGE FOR THIS NON ACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR. FEBRUARY HAD THE HIGHEST DELIVERY FOR ANY MONTH AND APRIL WAS SECOND..

JPMorgan has a total silver weight: 208.966million oz/500.643 oz million or 41.48%

TOTAL REGISTERED SILVER: 166.981 MILLION OZ//.TOTAL REG + ELIGIBLE. 500,643Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2025 OI: 918 OPEN INTEREST CONTRACTS FOR A LOSS OF 124 CONTRACTS. WE HAD 214 NOTICES FILED ON MONDAY SO WE GAINED 90 CONTRACTS WHICH UNDERWENT A STRONG QUEUE JUMP OF 0.450 MILLION OZ WHERE THESE BOYS HAVE DECIDED TO TAKE DELIVERY OVER HERE. I MUST REPORT WE HAD 0 EXCHANGE FOR RISK ISSUANCE. THUS THE NEW TOTAL REMAINS AT TWO ISSUANCES OF EXCHANGE FOR RISK IS 12.93 MILLION OZ.

JUNE SAW A GAIN OF 2 CONTRACTS UP TO 3323 CONTRACTS.

JULY LOST 54 CONTRACTS DOWN TO 109,710

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 107 or 0.535 MILLION oz

CONFIRMED volume; ON MONDAY 43,326 fair//

AND NOW MAY DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 13,205 X5,000 oz = 66.025 MILLION oz

to which we add the difference between the open interest for the front month of MAY (918) AND the number of notices served upon today (107 )x (5000 oz)

Thus the standings for silver for the MAY 2025 contract month: (13,205) Notices served so far) x 5000 oz + OI for the front month of MAY(918) minus number of notices served upon today (107)x 5000 oz equals silver standing for the MAY contract month equating to 70.080 MILLION OZ . THEN WE MUST ADD OUR NEW 12.93 TONNES OF EXCHANGE FOR RISK. NEW TOTAL STANDING FOR SILVER: 83.01 MILLION OZ

New total standing: 83.01 million oz which is huge for this NON active delivery month of MAY.

NO WONDER THE COMEX INVENTORY MOVEMENTS ARE GOING CRAZY!!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 166.981million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS

MAY 6 WITH GOLD UP $101.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 6.32 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 937.96 TONNES

MAY 5 WITH GOLD UP $77.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.13 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 944.28 TONNES

MAY 2 WITH GOLD UP $ 18.40 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 945.41 TONNES

MAY 1 WITH GOLD DOWN $ 92,45 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.87 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 944.26 TONNES

APRIL30 WITH GOLD DOWN $14.05 TODAY// NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 947.13 TONNES

APRIL29 WITH GOLD DOWN $13.45 TODAY// NO CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.27 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 946.27 TONNES

APRIL28 WITH GOLD UP $50.20 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.27 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 946.27 TONNES

APRIL25 WITH GOLD DOWN $49.95 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVEV WITHDRAWAL OF 3.911 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 948.56 TONNES

APRIL24 WITH GOLD UP $54.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 952.471 TONNES

APRIL23 WITH GOLD DOWN $124.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE WITHDRAWAL OF 9.47 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 949.70 TONNES

APRIL22 WITH GOLD DOWN $7,75 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.89 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL21 WITH GOLD UP $98.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.88 TONNES OF GOLD OUT OF THE GLD ///INVENTORY RESTS AT 952.28 TONNES

APRIL17 WITH GOLD DOWN $14.85 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 4.02 TONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 957.17 TONNES

APRIL16 WITH GOLD UP $12.90 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL15 WITH GOLD UP $106.35 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 953.15 TONNES

APRIL14 WITH GOLD DOWN $16.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 953.15 TONNES

APRIL11 WITH GOLD UP $67.70 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 13.48 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 949.71 TONNES

/APRIL10 WITH GOLD UP $100.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 937.09 TONNES

APRIL9 WITH GOLD UP $83.50 TODAY// MEGA HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 11.171 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 936.23 TONNES

APRIL8 WITH GOLD UP $17.50 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 6.02 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 926.78 TONNES

APRIL3 WITH GOLD DOWN $27.85 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

APRIL2 WITH GOLD UP $10.00 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.01 TONNES OF GOLD OUT OF THE GLD. ///INVENTORY RESTS AT 931.37 TONNES

APRIL1 WITH GOLD DOWN $3.55 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 933.38 TONNES

MARCH 31 WITH GOLD UP $31.60 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 931.94 TONNES

MARCH 28 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 27 WITH GOLD UP $31.60 TODAY// SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .29 TONNES OF GOLD INTO THE GLD. ///INVENTORY RESTS AT 929.65 TONNES

MARCH 26 WITH GOLD UP $31.60 TODAY// NO CHANGES IN GOLD AT THE GLD: ///INVENTORY RESTS AT 929.36 TONNES

MARCH 25 WITH GOLD UP $13.90 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/ ///INVENTORY RESTS AT 929.07 TONNES

MARCH 24 WITH GOLD DOWN $6.10 TODAY// HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 20.08 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 930.51 TONNES

GLD INVENTORY: 937.96 TONNES, TONIGHTS TOTAL

SILVER

MAY 6 WITH SILVER UP $0.92 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A HUG WITHDRAWAL OF 2.818 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.783 MILLION OZ

MAY 5 WITH SILVER UP $0.08 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL DEPOSIT OF 0.117 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 450.602 MILLION OZ

MAY 2 WITH SILVER DOWN $0.19 /MASSIVE CHANGES IN SILVER INVENTORY AT THE SLV:A HUGE WITHDRAWAL OF 4.545 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 450.424 MILLION OZ

MAY 1 WITH SILVER DOWN $0.43 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 0.683 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 454.972 MILLION OZ

APRIL30 WITH SILVER DOWN $0.65 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 2.364 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 454.289 MILLION OZ

APRIL29 WITH SILVER UP $0.30 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 3.229 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 451.925 MILLION OZ

APRIL28 WITH SILVER DOWN $0.03 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.136 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.696 MILLION OZ

APRIL25 WITH SILVER DOWN $0.44 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE WITHDRAWAL OF 3.639 MILLION OZ OUT OF THE SLV ////: //INVENTORY AT SLV RESTS AT 448.832 MILLION OZ

APRIL24 WITH SILVER DOWN $0.01 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE DEPOSIT OF 4.771 MILLION OZ INTO THE SLV ////: //INVENTORY AT SLV RESTS AT 452.471 MILLION OZ

APRIL23 WITH SILVER UP $0.65 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSSIVE WITHDRAWAL OF 6.27 MILLIO9N OZ FROM THE SLV ////: //INVENTORY AT SLV RESTS AT 447.70 MILLION OZ

APRIL22 WITH SILVER UP $0.15 /NO CHANGES IN SILVER INVENTORY AT THE SLV: ////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL22 WITH SILVER UP $0.30 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL21 WITH SILVER UP $0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.545 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL17 WITH SILVER DOWN $0.56 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.183 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 453.426 MILLION

APRIL16 WITH SILVER UP $0.70 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 3.002 MILLION OZ INTO THE SLV////: //INVENTORY AT SLV RESTS AT 452.243 MILLION

APRIL15 WITH SILVER UP $0.07 /NO CHANGES IN SILVER INVENTORY AT THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL14 WITH SILVER UP $0/23 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 0.273 MILLION OZ OUT OF THE SLV//: //INVENTORY AT SLV RESTS AT 449.241 MILLION

APRIL11 WITH SILVER UP $1.18 /BIG CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.911 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 449.71 MILLION

APRIL10 WITH SILVER UP $0.18 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDDRAWAL OF 0.501 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 447.603 MILLION

APRIL9 WITH SILVER UP $0.96 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.683 MILLION OZ INTO THE SLV//: //INVENTORY AT SLV RESTS AT 448.104 MILLION

APRIL8 WITH SILVER UP $0.35 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.137 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 447,421 MILLION

APRIL3 WITH SILVER DOWN $1.84 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.138 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 446.830 MILLION

APRIL2 WITH SILVER UP 0.15 /SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF .364 MILLION OZ FROM THE SLV//: //INVENTORY AT SLV RESTS AT 447.968 MILLION

APRIL1 WITH SILVER DOWN $0.36 /NO CHANGES IN SILVER INVENTORY AT THE SLV: //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 31 WITH SILVER DOWN $0.28 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A STRONG DEPOSIT OF 0.91000 MILLION OZ INTO THE SLV//// //INVENTORY AT SLV RESTS AT 448.332 MILLION

MARCH 28 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A STRONG WITHDRAWAL OF 1.092 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 447.422 MILLION

MARCH 27 WITH SILVER UP $.60 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 26 WITH SILVER DOWN $0.21 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV” A MASSIVE WITHDRAWAL OF 6.369 MILLION OZ FROM THE SLV//// //INVENTORY AT SLV RESTS AT 448.514 MILLION

MARCH 25 WITH SILVER UP $0.63 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 13.649 MILLION OZ INTO THE SLV// //INVENTORY AT SLV RESTS AT 454.883 MILLION

MARCH 24 WITH SILVER UP $0.04 /HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.728 MILLION OZ FROM THE SLV// //INVENTORY AT SLV RESTS AT 441.234 MILLION

CLOSING INVENTORY 448.783 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

PETER SCHIFF

2, EGON VON GREYERZ

ALASDAIR MACLEOD

3. C Powell and Gata dispatches

4. ANDREW MAGUIRE PODCAST 221

LIVE FROM THE VAULT NO 221 WITH ANDREW MAGUIRE

5B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:COMMODITY//RARE EARTHS

6 CRYPTOCURRENCY NEWS

ASIA TRADING TUESDAY MORNING MONDAY NIGHT

SHANGHAI CLOSED UP 37.08 PTS OR 1.13%

//Hang Seng CLOSED UP 158.03 PTS OR .70%

// Nikkei CLOSED //Australia’s all ordinaries CLOSED DOWN .06%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.2172 OFFSHORE CLOSED UP AT 7.2125 / Oil UP TO 59.27 dollars per barrel for WTI and BRENT UP TO 62,15 Stocks in Europe OPENED MOSTLY ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING S:/ONSHORE YUAN UP TRADING AT 72172 AND STRONGER//

UP 7.2125 AGAINST US DOLLAR/OFFSHORE YUAN AND THUS STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS /TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2172 (CHINESE COMMUNIST PARTY MANIPULATED)

OFFSHORE YUAN: UP TO 7.2125 (CCP MANIPULATED)

SHANGHAI CLOSED UP 37.08 PTS OR 1.13%

HANG SENG CLOSED UP 158.03 PTS OR .70%

2. Nikkei closed

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 99.32// EURO RISES TO 1.1333 UP 21 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.270//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 142.40…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and DOWN FOR UP this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.5345/Italian 10 Yr bond yield UP to 3.624 SPAIN 10 YR BOND YIELD UP TO 3.192%

3i Greek 10 year bond yield UP TO 3.373

3j Gold at $3394.50 Silver at: 33.15 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 18 /100 roubles/dollar; ROUBLE AT 81.12

3m oil into the 59 dollar handle for WTI and 62 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 142.80// 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.270% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8248 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9347 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.341 DOWN 0 BASIS PTS…

USA 30 YR BOND YIELD: 4.838 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.803 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 38.61

10 YR UK BOND YIELD: 4.5801 UP 4 PTS

10 YR CANADA BOND YIELD: 3.223 UP 4 BASIS PTS

5 YR CANADA BOND YIELD: 2.811 UP 2 PTS

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

2a New York OPENING REPORT

Futures Slide On Latest Batch Of Disappointing Earni

Tuesday, May 06, 2025 – 08:31 AM

US equity futures slumped for the second day, dragged down by earnings and a lack of positive news on trade negotiations. As of 8:00am, S&P 500 futures dropped 0.9% as risk is pared into tomorrow’s Fed announcement and the index failed to breach through technical resistance; Ford slumped after suspending its guidance and warned tariffs will reduce 2025 adjusted EBIT by about $1.5 billion; Nasdaq futures 100 dropped 1.1%, with all Mag7 stocks lower as Tesla and Meta led declines. Palantir tumbled 8% after the software firm’s results failed to meet investors’ expectations, while Ford slipped 3% after the carmaker pulled its financial guidance and flagged a tariff impact of about $2.5 billion on 2025 earnings. German stocks tumbled Estoxx 50 after incoming German chancellor Friedrich Merz suffered a shock setback when he fell short of a majority in an initial vote in the lower house of parliament to confirm him as Germany’s next chancellor. The yield curve is twisting steeper as USD comes for sale. Commodities are higher with WTI crude oil futures rebounding more than 2% from Monday’s YTD low close and gold is marching back to its ATHs. Trade Balance data is the macro data focus.

In premarket trading, Ford slips 2% as the automaker suspended its full-year financial guidance and said President Trump’s tariffs will take a toll on profit, joining rivals stung by volatile global trade policies. Palantir Technologies dropped 7% after the data-analysis software company posted financial results failed to meet investors’ expectations. Magnificent Seven stocks were all in the red: Tesla slips 1.6% as sales kept sliding across Europe’s biggest electric-car markets in April, despite the company rolling out an updated version of its most popular vehicle (Amazon -0.9%, Nvidia -1.4%, Meta -1.2%, Microsoft -0.7%, Apple -0.4%, Alphabet -0.8%). Here are the other notable premarket movers:

Celsius Holdings (CELH) falls about 4% after the energy-drink maker reported first-quarter revenue and adjusted EPS that trailed Wall Street expectations.

Constellation Energy (CEG) drops 6% after the power producer reported adjusted profit and Ebitda for the first quarter that fell short of expectations.

Datadog (DDOG) climbs 2% as the software company forecast revenue for the second quarter, guidance that beat the average analyst estimate.

DoorDash (DASH) falls 3% as the company is buying SevenRooms for $1.2 billion and Deliveroo for $3.9 billion, expanding its global reach and services.

Fabrinet (FN) drops 6% as the maker of optical communications products posted a sequential decline in datacom revenue.

Hims & Hers Health (HIMS) slumps 6% after the telehealth company gave guidance for second-quarter revenue that fell short of expectations. The firm also maintained its full-year sales outlook and Piper Sandler sees a lack of upside in the guidance.

Ichor (ICHR) drops 15% after the maker of fluid delivery subsystems for semiconductor capital equipment posted disappointing gross margins.

SolarEdge (SEDG) rises 13% after the solar equipment maker forecast revenue for the 2Q that beat the average analyst estimate.

Vertex Pharmaceuticals (VRTX) falls 5% after the company reported adjusted earnings per share for the first quarter that missed expectations.

WeRide Inc.’s US-listed shares (WRD) rise 12% after news that Uber Technologies is expanding its autonomous-vehicle partnership with the China-based firm to 15 more cities globally, including in Europe.

In Europe, the Stoxx 600 benchmark snapped a 10-day run of gains to drop 0.6%, its losses accelerating after incoming German chancellor Friedrich Merz failed suffered a shock setback when he fell short of a majority in a parliamentary vote to confirm him as Germany’s next chancellor, preventing his swearing in on Tuesday and pitching Europe’s biggest economy into uncharted territory. While the conservative leader is still expected to take charge of a ruling coalition of his CDU/CSU bloc and the Social Democrats, it was the first time since World War II that an incoming chancellor failed to secure backing from lawmakers in the first round of voting in the Bundestag and triggered chaos in Berlin’s government quarter. Meanwhile, European companies such as Royal Philips NV and Vestas Wind Systems A/S warned of uncertainty fueled by President Donald Trump’s trade tariffs; mining and industrial goods shares leading declines, while food beverage and energy stocks are the biggest outperformers. Here are the biggest movers Tuesday:

Fresenius Medical Care shares gain as much as 6%, to the highest since July 2023, after the kidney dialysis company reported results for the first quarter which some analysts said were better than expected

Vestas shares gain as much as 8.3% on Tuesday after it reported a first quarter orders beat and maintained guidance amid tariff uncertainty, which analysts welcomed

ALK-Abello shares advance as much as 5.7%, to the highest since Nov. 14, after the Danish allergy drugmaker reported better-than-expected revenue for the first quarter

Continental shares rise as much as 4.7% after the German firm more than doubled earnings in the first quarter as its car-parts unit slashed costs and tire sales bounced back from weaker levels last year

Hugo Boss’s shares rise as much as 10% after the suit maker’s earnings beat estimates, which analysts said was a relief, especially against a tough backdrop

Redcare Pharmacy shares fall as much as 9% after first-quarter results from the German online pharmacy provided little in the way of fresh catalysts to sustain a four-day winning streak

Castellum shares slumped as much as 8.6%, the worst performing stock on the Stoxx 600 Real Estate Index, after the Swedish landlord reported 1Q revenue that missed the average analyst estimate

Coloplast shares fall as much as 6.2%, to the lowest since February 2019, after the medical-products maker said CEO Kristian Villumsen stepped down from his role on May 5, with Lars Rasmussen becoming interim CEO

Elis drops as much as 5% despite maintaining its full-year guidance, with analysts expecting little change to current consensus. The French cleaning services group said tariffs aren’t expected to have any direct impact

Philips shares slip as much as 4% in early trading after the Dutch medical-technology firm cut its profitability outlook for the year, to take into account the estimated impact of tariffs

TeamViewer shares slide as much as 10% after reporting results that included various accounting adjustments as well as new acquisition 1E

Evotec shares fall as much as 9.6% as analysts point out the pharmaceutical firm’s results contained a miss in the research and development division and an increase in net debt

The slide in futures suggest that a recent burst of optimism fueled by some US trade concessions may already be fading. On Monday, the S&P 500 halted a nine-day rally that was its longest in about 20 years. While Ford’s warning served as a reminder that damage from the tariff war will become evident over the coming months, a run of firm economic data in recent days has caused traders to dial back bets on Federal Reserve interest-rate cuts.

“For us, it’s not the moment to add on risk,” said Nicolas Sopel, a strategist at Quintet Private Bank. “Even if there are successful negotiations between the US and China, tariffs will most likely be a lot higher than they were before Trump came into power. We will need time to see how deeply these increases impact the US economy,” according to Sopel, who has reduced US equity exposure.

Meanwhile, investors are coming around to the view that the Fed won’t cut interest rates as early or as deeply as earlier anticipated. While it’s expected to leave interest rates on hold this week, money markets have pushed back the timing of the first reduction to July and see three cuts by year-end, rather than the four they had expected a week ago.

“Recent comments from Fed Chair Powell suggest that the Fed will remain in wait-and-see mode over the near term,” Michael Krautzberger, AllianzGI’s chief investment office for fixed income, told clients. He also sees headwinds to the US dollar, and maintains “a short dollar footprint” in portfolios, he added.

Financial leaders at the Milken Institute Global Conference in Beverly Hills said they can live with tariffs and a reworking of trade, but want progress and an end to the chaos soon.

Meanwhile, the Bank of England is set to cut rates this week and may even pave the way for a series of back-to-back reductions in response to the trade war. The European Central Bank will also cut rates further, Governing Council member Yannis Stournaras, said.

Earlier in the session, Asian stocks advanced, as mainland Chinese shares rose on resilient holiday spending data and signs of easing trade tensions with the US. The MSCI Asia Pacific Ex-Japan Index gained as much as 0.7% before paring earlier gains. Communication services and consumer discretionary were among the best performing sectors. Chinese stocks outperformed in the region, as investors’ mood was lifted by strong retail sales and robust airline traffic results during the Labor Day holiday in early May. Traders also dialed up bets on easing tensions after Treasury Secretary Scott Bessent said the US could see “substantial progress in the coming weeks” in trade talks with China. The benchmark CSI 300 Index gained 1% on Tuesday. Hong Kong’s Hang Seng Index rose 0.7

In FX, the Bloomberg’s dollar index steadied after two days of losses, as the news on Merz weighed on the euro. However, the greenback is down nearly 7% this year and data shows traders have been adding to bearish bets. The fallout is being felt worldwide, with wild swings in recent days across Asian currencies, while Hong Kong has ramped up sales of its local currency to protect its foreign-exchange peg. China’s central bank kept the yuan’s daily reference rate little changed at 7.2008 per dollar as local markets reopened on Tuesday; the Taiwan dollar fell after gaining for six straight sessions

In rates, treasuries are mixed, with outperformance at the shorter-end of the curve. US 10-year yields rise 2 bps to 4.36% while two-year yields fall 1 bp; the front-end outperformance has 2s10s spread about 2bp wider on the day, off session highs reached during London morning. Bunds and gilts lag by 1bp and 2.5bp in the sector. The Treasury auction cycle continues with $42 billion 10-year new issue, following good demand for Monday’s 3-year note sale; WI 10-year yield near 4.355% is ~8bp richer than last month’s, which stopped through by 3bp; a $25b 30-year new issue Thursday will complete the cycle

In commodities, oil prices jump, with WTI rising 2.9% to $58.80 a barrel. Spot gold rises $40 to around $3,375/oz. Bitcoin is flat just above $94,000.

Looking at the US calendar, data releases will include US March trade balance data, the final April services and composite PMIs in the Eurozone, as well as March Eurozone PPI and France industrial production. The ECB’s Panetta is due to speak, while earnings releases include AMD, Arista Networks, Ferrari, Constellation Energy and Rivian.

Market Snapshot

S&P 500 mini -0.8%

Nasdaq 100 mini -1.1%

Russell 2000 mini -1.1%

Stoxx Europe 600 -0.9%

DAX -2%

CAC 40 -0.8%

10-year Treasury yield +1 basis point at 4.35%

VIX +1 points at 24.67

Bloomberg Dollar Index little changed at 1220.76

euro +0.2% at $1.1337

WTI crude +1.9% at $58.19/barrel

Top Overnight News

Friedrich Merz fell short of a majority in an initial vote in parliament to confirm him as Germany’s next chancellor, delaying his swearing-in for at least one day and prompting the anti-immigrant AfD to call for new elections. German bunds pared a decline. BBG

President Donald Trump on Monday signed an executive order to incentivize prescription drug manufacturing in the U.S., streamlining the path for pharmaceutical companies to build new production sites stateside as potential tariffs on imported medicines loom. CNBC

The Trump administration blocked Harvard from new research grants from the federal government. Access to the funding, worth over $1 billion a year, won’t be possible until the university shows “responsible management,” Education Secretary Linda McMahon said. BBG

US House Speaker Johnson said House Republicans remained on pace to pass the Trump agenda by Memorial Day or shortly thereafter and stated the Trump agenda is not facing a setback in the US House.

US Defense Secretary Hegseth ordered a reduction in 4-star positions in the military, according to a US official.

China’s Caixin services PMI came in a bit below expectations at 50.7 (vs. the Street 51.8) and per capita consumer spending over the May Day holiday was muted. RTRS

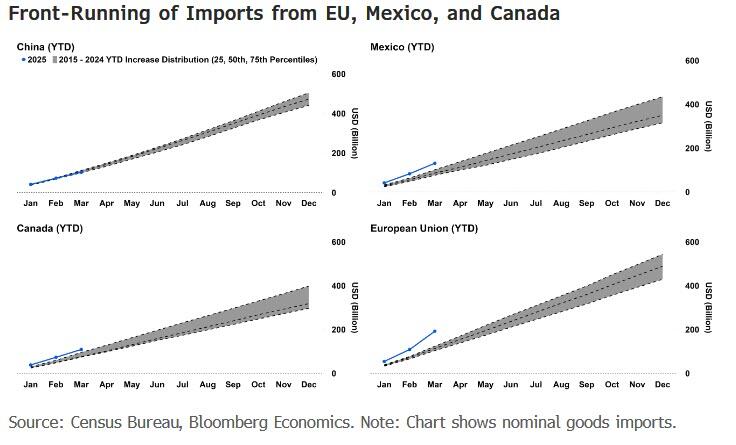

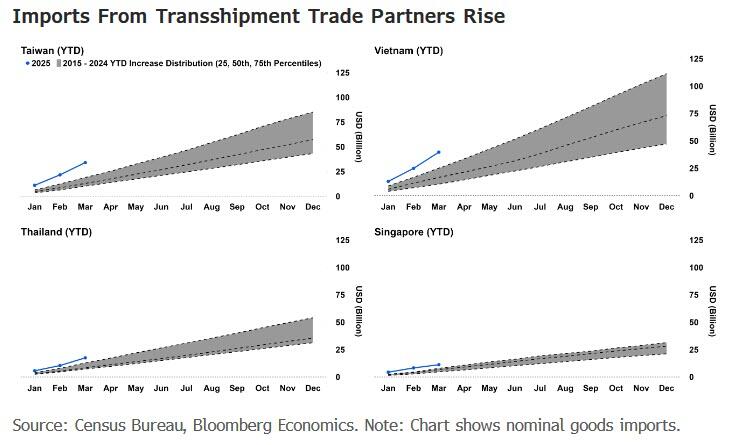

Chinese manufacturers are attempting to avoid the Trump administrations tariffs by fraudulently undervaluing cargo sent to the US, exploiting a system the American authorities have struggled to police. FT

Taiwanese central bank says 80% of FX reserves are US bonds. Taiwan Central Bank FX official says they feel the market has returned to a more stable situation today.

Hong Kong’s de-facto central bank said it sold HK$46.54 billion ($6 billion) into the market on Saturday to prevent the local currency from strengthening beyond its official peg to the U.S. dollar, the first such intervention in more than four years. RTRS

HKMA says has been lowering its duration in US treasury holdings; exchange fund has been diversifying into non-US assets Has been diversifying currency exposure in its investment portfolio to manage risks.

The PBOC set the daily yuan reference rate only marginally stronger than on Thursday, sidestepping the offshore yuan’s sizable appreciation during the long weekend. That effectively forces the offshore currency to give up recent gains, MLIV wrote. BBG

Spain’s blackout resulted in a €400 million loss to the economy. BBG

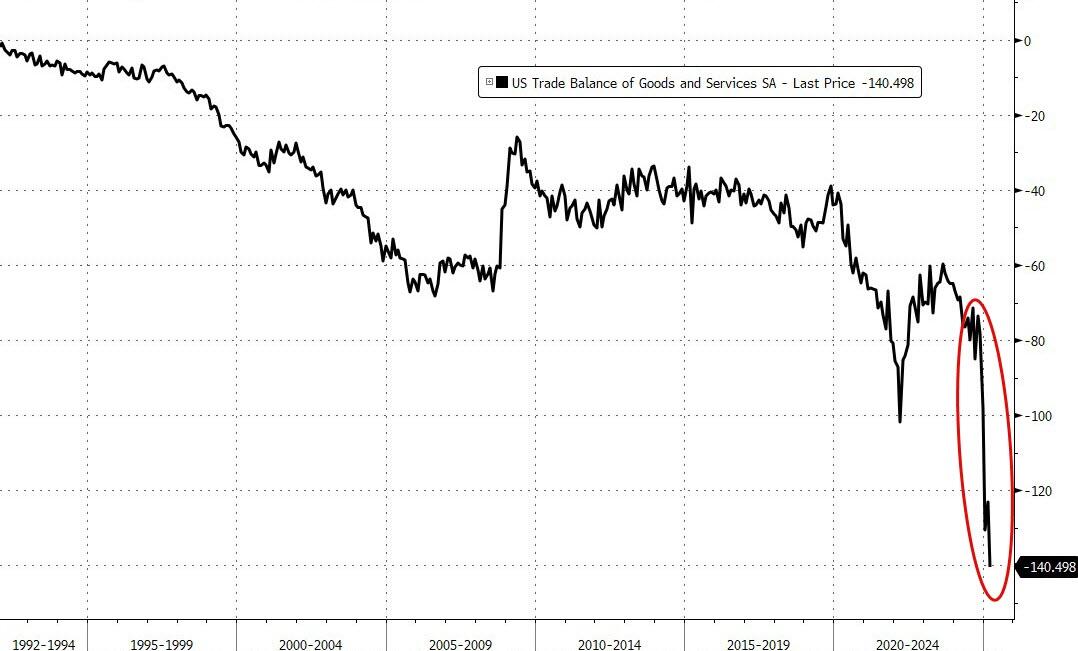

The US trade deficit probably widened in March as firms boosted imports again to front-load products ahead of tariffs. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly higher as Chinese participants returned from the Labor Day holiday but with the gains capped following disappointing Chinese Caixin Services PMI data and as markets in Japan and South Korea remained closed. ASX 200 traded little changed as strength in the commodity-related sectors were predominantly offset by underperformance in financials and defensives, while the larger-than-expected contraction in building approvals clouded over risk appetite. Hang Seng and Shanghai Comp gained on return from the extended weekend and took their opportunity to react to the recent China tariff rhetoric from US President Trump who said that he is willing to lower tariffs on China at some point, while the miss on Caixin Services PMI data did little to derail the positive sentiment in China.

Top Asian News

Chinese President Xi is prepared to work with EU leaders to expand mutual openness and properly handle frictions and differences, according to Xinhua Calls on the EU and China to safeguard fairness and justice.

China said 314mln domestic trips were made during the May holiday which was up 6.4% Y/Y and travel expenditure of domestic tourists rose 8% Y/Y to 180.3bln, according to CCTV.

US House intensified its legislative push against Beijing on Monday in which it advanced a slate of China-related bills targeting industrial espionage, export controls, national security threats and alleged human rights abuses.

Fast fashion platforms Shein and Temu boosted digital advertising in Europe with the most growth seen in France and the UK, while they see increased app downloads in France and the UK as US tariffs hit and Shein also boosted advertising in Brazil where it manufactures goods for Latin America.

HKMA intervened in which it bought USD 7.8bln against the HKD at 7.7500 after the HKD hit the strong end of the trading range.

European bourses (STOXX 600 -0.6%) opened mostly firmer/flat and traded tentatively on either side of the unchanged mark. Thereafter, the risk tone soon slipped after the HKMA said it says has been lowering its duration in US treasury holdings and as Germany’s Merz failed to secure enough votes to become Chancellor; DAX 40 -1.8%. The HKMA update sparked some modest pressure in US equity futures (ES -0.9%, NQ -1%); ahead of a handful of earnings and meetings between the US and Canadian Presidents. As for sectors, its a mixed picture in Europe. Food Beverage & Tobacco takes the top spot, joined closely by Utilities. To the downside, Basic Resources sits right at the foot of the pile – losses largely driven by Anglo American after Peabody said it may terminate its deal for its coal mine assets. For the Pharma industry; US President Trump said he will announce pharmaceutical tariffs over the next two weeks, while he signed an order to reduce regulatory barriers to domestic pharmaceutical manufacturing and will have an announcement next week related to the cost of medicines.

Top European News

Germany’s CDU leader Merz falls short of a majority needed to become Chancellor in first round of voting in parliament; secured 310 Bundestag votes, 316/630 required. On the second round of voting for German Chancellor Merz, Handelsblatt citing sources reports “The second round of voting could be postponed until Friday because the approval of the AfD is necessary for an immediate ballot”. There will not be a second vote on Merz becoming German Chancellor today, via Handelsblatt citing numerous reports and the CDU Secretary General.

EU is set to make it easier for UK professionals to work in the bloc, according to FT.

SNB Chairman Schlegel says is committed to its price stability mandate; biggest challenge at present is uncertainty. Ready to intervene in the FX market as necessary. Swiss inflation is expected to come down. Not ruled out negative rates. Nobody likes negative rates but if have to, are prepared to do it again.

FX

After an attempted recovery last week, the USD has continued to ebb lower after DXY failed to sustain a move above the 100 mark, despite a solid showing for US ISM services. HKMA said it has been lowering its duration in US treasury holdings and has been diversifying into non-US assets. DXY is currently towards the lower end of Monday’s 99.46-100.05 range.

EUR is firmer vs. the broadly weaker USD as Eurozone-specific newsflow remains on the light side. ECB-dove Stournaras noted he does not see inflation if the EU tariff reaction is selective and it seems the ECB will continue with rate cuts. EUR/USD has gained a firmer footing on a 1.13 handle but is yet to approach Monday’s high at 1.1364 with some of the upward momentum for the currency stalled in recent trade after Germany’s CDU leader Merz fell short of a majority needed to become Chancellor in the first round of voting in parliament.

USD/JPY traded indecisively overnight and failed to sustain a brief return to the 144.00 level with price action largely driven by the dollar amid the continued absence of Japanese participants. In European trade, downside was seen for the pair as global equity futures ebbed lower. USD/JPY has delved as low as 142.91 with the next target coming via the 1st May low at 142.88.

GBP is mildly firmer vs. the USD as UK participants return to market. UK newsflow remains light with markets looking ahead to Thursday’s BoE policy announcement. Cable has ventured as high as 1.3333 but is yet to test yesterday’s 1.3336 peak.

Diverging fortunes for the antipodeans with AUD towards the bottom-end of the G10 leaderboard. Overnight trade saw a larger-than-expected contraction in Australian building approvals and a disappointing Chinese services PMI. However, the cause for underperformance vs. NZD is otherwise unclear.

PBoC set USD/CNY mid-point at 7.2008 vs exp. 7.2518 (Prev. 7.2014).

Fixed Income