XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

FROM MY no 4 SON STEPHEN //THROUGH AI: ENJOY

099 H DEUTSCHE BANK AG 273

118 C MACQUARIE FUTURES US 5

118 H MACQUARIE FUTURES US 164

167 C MAREX 152

323 C HSBC 30

332 H STANDARD CHARTERED B 3

363 H WELLS FARGO SECURITI 36

435 H SCOTIA CAPITAL (USA) 8

624 H BOFA SECURITIES 9

657 H MORGAN STANLEY 5

661 C JP MORGAN SECURITIES 6 4

732 C RBC CAP MARKETS 2

737 C ADVANTAGE FUTURES 1 2

880 C CITIGROUP 13

905 C ADM 7

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2025: 360 CONTRACTs NOTICES FOR 36,000 OZ or 1.1197 TONNES

total notices so far: 3986 contracts for 398,600 OR 11.293 tonnes)

SILVER NOTICES: 11,293 NOTICE(S) FILED FOR 3.795 OZ/

total number of notices filed so far this month : 11,293 CONTRACTS (NOTICES) for 56.465 million oz

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 17.200 MILLION OZ.

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 58.3150 MILLION OZ NORMAL DELIVERY PLUS 3.0 MILLION OZ EX FOR RISK = 61.3650 MILLION OZ. THIS IS THE FIRST ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES ANND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

AND NOW SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.0155 TONNES PLUS 0.9548 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 9.586//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 22.1586 TONNES!!

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 30.205 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A MEGA HUGE 1273 CONTRACTS OI TO 157,925 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 630 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 630 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 630 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1417 CONTRACTS AND ADD TO THE 630 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED GAIN OF 1903 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN IN PRICE OF $0.35 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 9.515 MILLION PAPER OZ

OCCURRED WITH OUR $0.35 GAIN IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS MONDAY MORNING:

SHANGHAI CLOSED DOWN 19.55 PTS OR 0.51%

//Hang Seng CLOSED UP 278.33 PTS OR 1.09%

// Nikkei CLOSED DOWN 184.52 PTS OR 0.42% //Australia’s all ordinaries CLOSED DOWN .51%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1279 OFFSHORE CLOSED UP AT 7.1232/ Oil UP TO 62.92 dollars per barrel for WTI and BRENT DOWN TO 66.70 Stocks in Europe OPENED ALL MOSTLY GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1279 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1232 AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 2128 CONTRACTS TO 503,285 OI WITH OUR HUGE GAIN IN PRICE OF $41.40 WITH RESPECT TO MONDAY’S // TRADING.. WE OF COURSE, LOST NO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (3145). WE HAD ZERO T.A.S. LIQUIDATION AS WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 5273 CONTRACTS (OR 16.401 TONNES).THEN WE WERE NOTIFIED, THAT WE HAD A 307 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 30,700 OZ (0.9548 TONNES).

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES THESE PAST 3 MONTHS;

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLYAS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). LAST TUESDAY THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW WEDNESDAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPT:

SEPTEMBER: THREE ISSUANCES SO FAR TOTALLING 3082 CONTRACTS OR 308,200 OZ OR 9.5863 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).LAST TUESDAY THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW YESTERDAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: THREE ISSUANCES FOR 3082 CONTRACTS SO FAR FOR 308,200 OZ OR 9.586 TONNES OF GOLD!!

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK COULD BE EITHER:

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT ITS GOLD TO BULLION BANKS

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS)

THE COUNTERPARTY TO EITHER THE BANK OF ENGLAND’S OR THE FRBNY ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND OR THE FRBNY, ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH SEPT//ONLY MISSING JUNE.)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE.

DETAILS ON AUGUST COMEX MONTH//FINAL

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 5273 CONTRACTS WITH OUR STRONG GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH SEPTEMBER CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A FAIR T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 1802 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DESPERATELY TRYING TO STOP GOLD’S ADVANCE AND THIS ENDS IN FAILURE. FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!!

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH AUGUST MONTH- END SPREADERS) IS THE REASON WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR THE FOLLOWING MONTHS:

FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES

AND NOW INITIAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0155 TONNES QUEUE JUMP TO GO ALONG WITH THE 0.9548 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 9.586 TONNES//NEW TOTALS STANDING ADVANCES TO 22.1586 TONNES OF GOLD!!!

THE FED IS THE OTHER MAJOR SHORT OF AROUND 34+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 239 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

SUMMARY AUGUST: TOTAL QUEUE JUMPING AND TOTAL EXCHANGE FOR RISKS ISSUANCE FOR THE MONTH OF AUGUST;

WE HAD A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE TOTAL OF 47.2312 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES THEN AUGUST 12: 2.637 TONNES: AND NOW AUG 25: 9.107 TONNES ISSUANCE MONDAY’S MASSIVE 9.1016 TONNES ISSUANCE/AUGUST 25, AUGUST 26 9.0699 TONNES , YESTERDAYDAY’S (AUGUST 27) 9.0699 TONNES AND FINALLY TODAY’S TODAL OF 6.923 TONNESS/NEW STANDING ADVANCES TO 152.208 TONNES.

SUMMARY SO FAR SEPT: 8.093 TONNES INITIALLY STANDING FOR GOLD COUPLED WITH TODAY;S 0.0155 TONNES QUEUE JUMP AND 0.9548 TONNES TODAY// NEW TOTALS OF 9.586 TONNES OF EXCHANGE FOR RISK ISSUANCE/:

THAT IS;

A) 0.9548 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY + 8.6312 TONNES EX FOR RISK PRIOR =//TOTAL FOR MONTH: 9.586 TONNES EX FOR RISK!!

B) 0.0155 TONNES TODAY QUEUE JUMP

TOTALS: 22.1586 TONNES INITIALLY STANDING FOR GOLD/SEPT.

EXCHANGE FOR PHYSICAL ISSUANCE/SEPTEMBER

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 3145 EFP CONTRACT WAS ISSUED: : /DEC 3145 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3145 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//MONDAY

- MONTH END SPREADERS HAVE NOW BEEN FINALIZED AS OF AUGUST 29 AND THEY FOR THE FIRST TIME CAUSED NO DAMAGE TO OUR GOLD PRICE

T.A.S.SPREADER ISSUANCE//SEPT.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A FAIR SIZED SIZED 1802 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST MONTH ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING; (AND MONTH END SPREADERS)

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S STRONG GAIN IN PRICE IN GOLD AND A CORRESPONDING HUGE GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS ESPECIALLY WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

2) AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

3) TO BE FOLLOWED BY SEPTEMBER’S 3 ISSUANCES FOR EXCHANGE FOR RISK FOR 9.586 TONNES.

STANDING FOR GOLD LAST 8 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S QUEUE JUMP OF 0.5816TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

AND NOW SEPT:

SEPT: 12.600 TONNES OF GOLD (INCLUDES TODAY’S QUEUE JUMP) + 0.9548 TONNES EX FOR RISK TODAY+ 8.6312 TONNES EX FOR RISK PRIOR =_//TOTAL EX FOR RISK// FOR MONTH = 9.586//NEW TOTALS FOR GOLD STANDING SEPT = 22.1586 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING SEPTEMBER CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A HUGE $41.40./ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED GAIN IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION AND THAT GAIN IN OI FOR OUR TWO EXCHANGES WAS DUE TO THE LONGS PILING IT ON TRYING TO OBTAIN BADLY NEEDED GOLD///. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES (WHICH ARE JOINED BY OUR MONTHLY SPREADERS IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS) WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE LIKE IT DID WITH LAST WEEK AND THIS WEEKS’S TRADING!! THIS IS THE FIRST TIME THAT THE CROOKS COULD NOT MUSTER A RAID ON OPTIONS EXPIRY LONDON/OTC AUGUST TRADING. THEIR RAID ON OUR PRECIOUS METALS CAUSED NO DAMAGE TO OUR PRICE.

TUESDAY MORNING//MONDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/ TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

DETAIL SUMMARY OF NUMBER OF EXCHANGE FOR RISK ISSUANCES: FEB THROUGH SEPTEMBER TRADING:

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283,400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH. FEBRUARY IS THE SECOND HIGHEST ISSUANCE OF EXCHANGE FOR RISK AS AUGUST BECOMES THE HIGHEST EVER RECORDED AS YOU WILL SEE BELOW!

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH 3 ISSUANCES

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRIL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAD 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE: 3

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AFTER AN INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD (OCCURRED ON JULY 25) THE CME NOTIFIED US OF A SECOND ISSUANCE OF 706 CONTRACTS FOR 70,600 OZ OR 2.195 TONNES WHICH WILL BE ADDED TO OUR OFFICIAL STANDING. THUS 35.176 TONNES OFFICIAL STANDING + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD STANDING

AUGUST: 7 ISSUED,

TOTAL EXCHANGE FOR RISK MONTH OF AUGUST 44.696 TONNES, THE HIGHEST MONTHLY EVER COMEX ISSUANCE!!!!!!

THUS 107.5117 TONNES OF NORMAL GOLD STANDING (INCLUDING ALL QUEUE JUMPS/EX FOR PHYS TRANSFERS) + 44.696 TONNES EX FOR RISK = 152.208 TONNES.

SEPTEMBER: 3 ISSUED:

THE CME NOTIFIED US THAT OUR THREE ISSUANCES OF EXCHANGE FOR RISK EQUATES TO 3082 CONTRACTS FOR 308,200 OZ OR 9.586 TONNES. WE WILL PROBABLY HAVE A DOOZY FOR SEPT DELIVERIES AS EITHER THE BANK OF ENGLAND OR THE BIS (LOANED TO THE FRBNY) WANTS ITS GOLD BACK+ THE MASSIVE QUEUE JUMPING BY OTHER CENTRAL BANKS IS CERTAINLY ON DISPLAY TODAY’S 0.155 TONNES QUEUE JUMP.

ANALYSIS SEPT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// SEPT COMEX CONTRACT

WE HAVE A STRONG SIZED GAIN TOTAL OF 20.416 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPTEMBER AT 8.093 TONNES. WE HAD THE FOLLOWING QUEUE JUMP OF 0.0155 TONNES OF GOLD ALONG WITH 0.9548 TOTAL TONNES OF EXCHANGE FOR RISK TODAY/// TOTAL FOR MONTH TOTALS EX FOR RISK// MONTH = 9.586//NEW TOTAL STANDING FOR GOLD IN SEPT ADVANCES TO: 22.1586 TONNES.

ALL OF THIS HUGE STANDING FOR SEPTEMBER WAS ACCOMPLISHED DESPITE OUR GAIN IN PRICE TO THE TUNE OF $47.10

WE HAD 1291 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 5273 CONTRACTS OR 527300 0Z (16.401 TONNES)

confirmed volume MONDAY 256,986 contracts// fair//

speculators have left the gold arena

INITIAL GOLD COMEX

SEPT CONTRACT MONTH

SEPT 9 /2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1 entries i) Out of Asahi 97,121.681 oz total withdrawal 97,121.681 oz . |

| Deposit to the Dealer Inventory in oz | 0- |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 1 ENTRIES i) Into Loomis 15,201.520 oz total deposit 15,201.520 oz xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 360 notice(s) 36000 OZ 1.1197 TONNES |

| No of oz to be served (notices) | 65 contracts 6500 OZ 0.2021 TONNES |

| Total monthly oz gold served (contracts) so far this month | 3986 notices 398,600 oz 12.398 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER 1

Into Loomis 15,201.520 oz

total deposit 15,201.520 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

1 entries

i) Out of Asahi

97,121.681 oz

total withdrawal 97,121.681 oz

ADJUSTMENTs 1

dealer Brinks to customer account: 30,575.594 oz (951 kilobars)

AMOUNT OF GOLD STANDING FOR SEPTEMBER

THE FRONT MONTH OF SEPTEMBER STANDS AT 425 CONTRACTS FOR A LOSS OF 495 CONTRACTS. WE HAD 500 CONTRACTS FILED ON MONDAY SO WE GAINED A SMALL 5 CONTRACTS OR 500 OZ ENTERTAINED A QUEUE JUMP OF 0.0155 TONNES. WE NOW MUST ADD TO OUR INITIAL 2.333 TONNES OF GOLD STANDING TO TODAY’S QUEUE JUMP OF 0.0155 TONNES AND THEN ADD MONTH SEPT// EX FOR RISK = 9.586//THUS NEW TOTAL OF GOLD STANDING ADVANCES TO 22.1586 TONNES

OCTOBER LOST 1012 CONTRACTS DOWN TO 61,001

NOVEMBER GAINED 57 CONTRACTS UP TO 2916 CONTRACTS.

We had 360 contracts filed for today representing 36,000 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 6 notices issued from their client or customer account. The total of all issuance by all participants equate to 360 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 4 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for SEPTEMBER /2025. contract month, we take the total number of notices filed so far for the month (3986 X 100 oz ) to which we add the difference between the open interest for the front month of SEPT ( 425 CONTRACTS) minus the number of notices served upon today (360 x 100 oz per contract) equals 405,100 OZ OR 12.600 TONNES OF GOLD TO WHICH WE ADD OUR TOTAL EX FOR RISK/SEPT MONTH OF 9.586 TONNES//NEW TOTAL STANDING ADVANCES TO 22.1586 TONNES

thus the INITIAL standings for gold for the SEPTEMBER contract month: No of notices filed so far (3986 x 100 oz +we add the difference for front month of SEPT. (425 OI} minus the number of notices served upon today (360 x 100 oz) which equals 405,100 OZ OR 12.600 TONNES PLUS 9.586 TONNES EXCHANGE FOR RISK = 22.1586 TONNES.

TOTAL COMEX GOLD STANDING FOR SEPT..: 22.1586 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY INACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,041,599.430 oz 63.502 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 38,912,304.554 oz

TOTAL REGISTERED GOLD 21,288.410.555 or 662.158 tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,623,893.999 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,246,811 oz ((REG GOLD- PLEDGED GOLD)= 598.65 tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE SEPTEMBER 2025 SILVER CONTRACTS

SEPT 9 2025

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1 entries: i) Out of Loomis 1,029,528.720 oz total withdrawal 1,029,528.720 oz |

| Deposits to the Dealer Inventory | 1 ENTRY i) Into Stonex: 1,029,528.720 oz |

| Deposits to the Customer Inventory | 2 DEPOSIT ENTRIES/CUSTOMER ACCOUNT i)Into Asahi 1,208,440.500 oz ii) into Manfra 600,380.921 oz total deposit 1,808,821.427 oz |

| No of oz served today (contracts) | 759 CONTRACT(S) (3.795 million OZ |

| No of oz to be served (notices) | 380 contracts (1.900 MILLION oz) |

| Total monthly oz silver served (contracts) | 11.293 Contracts (56.465 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

1 ENTRY

i) Into Stonex: 1,029,528.720 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

2 DEPOSIT ENTRIES/CUSTOMER ACCOUNT

i)Into Asahi 1178,847.7000 oz

ii) INTO Brinks 240,972.480 oz

total deposit 1,419,820.180 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

1 entries:

i) Out of Loomis 1,029,528.720 oz

total withdrawal 1,029,528.720 oz

ADJUSTMENTs 1 dealer to customer

i) stonex 9952.980 oz

TOTAL REGISTERED SILVER: 196.791 MILLION OZ//.TOTAL REG + ELIGIBLE. 520.707 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR AUGUST

silver open interest data:

FRONT MONTH OF SEPTEMBER /2025 OI: 1139 OPEN INTEREST CONTRACTS FOR A LOSS OF 11 CONTRACTS. WE HAD 519 CONTRACTS SERVED ON MONDAY SO WE GAINED A STRONG 508 CONTRACTS OR 2.54 MILLION OZ ENTERTAINED A QUEUE JUMP//NEW STANDING FOR SILVER COMEX INCREASES TO 58.3650 MILLION OZ. THEN WE MUST ADD OUR INITIAL ISSUANCE OF 600 CONTRACTS FOR EXCHANGE FOR RISK OR 3.0 MILLION OZ//NEW STANDING ADVANCES TO 61.3650 MILLION OZ

STANDING FOR SILVER: 61.3650 MILLION OZ

OCTOBER LOST 78 CONTRACTS TO 2433

NOVEMBER LOST 55 CONTRACTS UP TO 1368.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 759 or 3.793 MILLION oz

CONFIRMED volume; ON MONDAY 75,348 strong//

AND NOW SEPT. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in SEPTEMBER. we take the total number of notices filed for the month so far at 11,293 X5,000 oz = 56.465 MILLION oz

to which we add the difference between the open interest for the front month of SEPT (1139) AND the number of notices served upon today (759 )x (5000 oz)

Thus the standings for silver for the SEPTEMBER 2025 contract month: (11,293) Notices served so far) x 5000 oz + OI for the front month of SEPTEMBER(1139) minus number of notices served upon today (759)x 5000 oz equals silver standing for the SEPTEMBER contract month equating to 58.3650 MILLION OZ TO WHICH WE ADD OUR INITIAL EXCHANGE FOR RISK SEPT TOTALLING 3.0 MILLION OZ//NEW STANDING ADVANCES TO 61.3650 MILLION OZ

New total standing: 61.3650 million oz which is HUGE for this active delivery month of SEPT.. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 196.791 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/520.707 million. 40.59%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

SEPT 9 WITH GOLD UP $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.29 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 8 WITH GOLD UP $41.40 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 5 WITH GOLD UP $47.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 2.29 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 4 WITH GOLD DOWN $22.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 6.30 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 984.26 TONNES//

SEPT 3 WITH GOLD UP $43.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 12.88 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 990.56 TONNES//FAIRY TALES

SEPT 2 WITH GOLD UP $79.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 9.74 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 977.68 TONNES

AUGUST 29 WITH GOLD UP $33.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 5.44 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 28 WITH GOLD UP $18.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 27 WITH GOLD UP $12.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 959.92 TONNES

AUGUST 26 WITH GOLD UP $12.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 958.49 TONNES

AUGUST 25 WITH GOLD DOWN $1.05 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 22 WITH GOLD UP $35.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 21 WITH GOLD DOWN $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 958.21 TONNES

AUGUST 20 WITH GOLD UP $29.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.16 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 962.21 TONNES

AUGUST 19 WITH GOLD DOWN $16.90 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 965. TONNES

AUGUST 18 WITH GOLD DOWN $4.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 15 WITH GOLD DOWN $0.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.86 TONNES OF GOLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 14 WITH GOLD DOWN $20.80 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 13 WITH GOLD UP $9.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 12 WITH GOLD UP $2.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.58 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 11 WITH GOLD DOWN $53.55 TODAY//SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT DEPOSIT OF 0.55 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.64 TONNES

AUGUST 8 WITH GOLD UP $10.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 6.30 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.09 TONNES

AUGUST 7 WITH GOLD UP $16.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.15 TONNES OF GOLD OUT OF THE GLD/://// ///INVENTORY RESTS AT 952.79 TONNES

AUGUST 6 WITH GOLD DOWN $8.15 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 955.94 TONNES

AUGUST 5 WITH GOLD UP $8.45 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 954.80 TONNES

AUGUST 4 WITH GOLD UP $24.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 953.08 TONNES

AUGUST 1 WITH GOLD UP $51.40 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 954.51 TONNES/

JULY 31 WITH GOLD DOWN $2.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

GLD INVENTORY: 979.68 TONNES, TONIGHTS TOTAL

SILVER

SEPT 9 WITH SILVER DOWN $0.55/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.816 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 486.677 MILLION OZ./

SEPT 8 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 488.493 MILLION OZ./

SEPT 5 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 489.674 MILLION OZ./

SEPT 4 WITH SILVER DOWN $0.68/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 491.308 MILLION OZ./

SEPT 3 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT DEPOSIT OF 1,816 MILLION OZ INTO THE SLV:// ////INVENTORY RESTS AT 494.043 MILLION OZ./

SEPT 2 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF .727 MILLION OZ FROM THE SLV:// ////INVENTORY RESTS AT 492.227 MILLION OZ./

AUGUST 29 WITH SILVER UP $0.80/ HUGE CHANGES AT THE SLV AT DEPOSIT 0F 1.862 MILLION OZ:// ////INVENTORY RESTS AT 492.954 MILLION OZ./

AUGUST 28 WITH SILVER UP $0.48/ NO CHANGES AT THE SLV:// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 27 WITH SILVER UP $0.04/ SMALL CHANGES AT THE SLV: A WITHDRAWAL OF 454,000 OZ FORM THE SLV// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 26 WITH SILVER DOWN $0.19/ NO CHANGES AT THE SLV: // ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 25 WITH SILVER DOWN $0.28/ SMALL CHANGES AT THE SLV: A SMALL DEPOSIT OF 0.363 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 22 WITH SILVER UP $0.92/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 0.908 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.183 MILLION OZ./

AUGUST 21 WITH SILVER UP $0.29/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 1.09 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 492.091 MILLION OZ.//

AUGUST 20 WITH SILVER UP $0.41/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 545,000 OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 493.181 MILLION OZ.//

AUGUST 19 WITH SILVER DOWN $0.64/ HUGE CHANGES AT THE SLV: A MAMMOTH DEPOSIT OF 9.173 MILLION OZ OF SILVER VAPOUR ARRIVES AT THE SLV// ////INVENTORY RESTS AT 493.726 MILLION OZ.//

AUGUST 18 WITH SILVER UP $0.06/ NO CHANGES AT THE SLV ////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 15 WITH SILVER DOWN $0.04/ SMALL CHANGES AT THE SLVA WITHDRAWAL OF .909 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 14 WITH SILVER DOWN $0.52/ NO CHANGES AT THE SLV/////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 13 WITH SILVER UP $0.62/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 1.317 MILLION OZ INTO THE SLV:.////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 12 WITH SILVER UP $0.68/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.18 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 484.145 MILLION OZ.//

AUGUST 11 WITH SILVER DOWN $0.56/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 3.905 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 481.965 MILLION OZ.//

AUGUST 8 WITH SILVER UP $0.20/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 7 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 2.179 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 6 WITH SILVER UP $0.02/ SMALL CHANGES AT THE SLV//: A DEPOSIT OF 0.727 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 483.691 MILLION OZ.//

AUGUST 5 WITH SILVER UP $1.51/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 1.119 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 482.964 MILLION OZ.//

AUGUST 4 WITH SILVER UP $0.50/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 0.183 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.083 MILLION OZ.//

AUGUST 1 WITH SILVER UP $0.19/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.816 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.264 MILLION OZ.//

JULY 31 WITH SILVER DOWN $1.00/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487/398 MILLION OZ.//

CLOSING INVENTORY 485.677 MILLION OZ//

PHYSICAL GOLD/SILVE

1/PETER SCHIFF

JOHN RUBINO

DAVID JENSEN

SPECIAL THANKS TO G. FOR SENDING THIS IMPORT STUFF TO US;

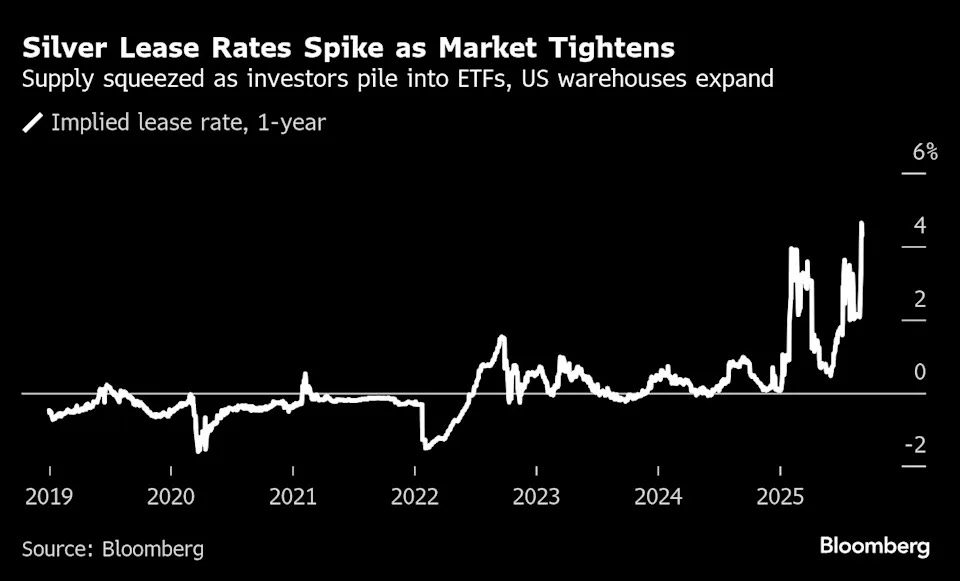

NOW GREATER THAN 5%

SILVER LEASE RATES

Silver Lease Rates Now Running Higher Signal The Global Silver Shortage Is Intensifying

Yesterday, Bloomberg reported that the London 1-year implied silver lease rate has surged above 5% p.a.

On September 4, 2025, Bruce Ikemizu Chief Director of the Japan Bullion Market Association (JBMA) reported that the London 1-month implied silver lease rate had risen to 6.4%.

The ongoing high and increasing lease rate for physical silver bars signals that the 41% price increase in silver so far in 2025 has been driven by an intensifying global shortage of this strategic and monetary metal.

Figure 1 – London Implied Silver Lease Rate (1-Year Lease Term); source: Bloomberg

Figure 2 – Daily Silver Spot Price 2020 – 2025; source: StockCharts.com

As the global shortage of silver continues to compound, we await the inevitable default by bullion banks that have sold physical silver in the London cash / spot market in the form of promissory notes that cannot be delivered.

The end of the London promissory note precious metal price fixing era will the signal a return to real price discovery for precious metals.

The rise in government bond yields accompanied by gold, silver, and platinum shortages and higher prices tells us that bonds (paper) are being sold and precious metals bought as investors seek to protect their savings.

The tremendous leverage between the size of the global debt markets compared to available physical precious metals portends the potential for very large step-changes in metals prices and disruption of the levered paper cash metal market in London.

Best regards,

David Jensen

2. MATHEW PIEPENBERG/VON GREYERZ

ALASDAIR MACLEOD

Debt funding, inflation, and gold

Even though the Fed is expected to reduce its funds rate in a week’s time, the inflation outlook is worsening rapidly, which is why the dollar is weakening and gold rising.

| Alasdair MacleodSep 9∙Paid |

Governments are attempting to contain their long-term debt funding costs, which are due to a combination of a lack of investor demand and bond yields which have risen sharply in recent years. The extra funding cost of long-term maturities over short-term rates is illustrated in the US Treasury yield curve in the chart above. In the case of US treasuries, auctions with longer maturities tend to be disappointing. Doubtless, if longer term funding is used to ensure the debt maturity profile remained containable with respect to maturity roll-overs, long-end yields would be considerably higher.

This explains why the Fed approved a move to reduce the supplementary leverage ratio imposed on big bank balance sheets so long as the extra balance sheet space is invested in treasuries. However, this will only increase bank demand for short-term debt, mainly T-bills maturing in less than a year. But it is worth remembering that this finance is bank credit and not investor-sourced, making it inflationary. But reducing the supplementary leverage ratio is only part of the story.

Almost certainly, the Fed will reduce its funds rate by .25% in a week’s time. Under political pressure, further rate cuts can be expected. This will reduce the cost of T-bill funding even further. A win-win for Trump —or is it?

At this point, it should be made clear that debt is not a bad thing. What matters is how it is funded and how it is used. Simply put, if savers increase their savings to invest in government debt it reduces consumer demand for goods so is deflationary. But if government uses the debt raised to spend in the economy it balances the deflationary effect of an increase in savings.

This is why China’s and Japan’s economies with their high consumer savings rates exhibit low inflation compared with the high-spending low-saving Anglo-Saxon consumers.

Alternatively, if government debt is bought by banks creating credit out of thin air, which is what’s happening here, then it is inflationary. It debases the value of credit in terms of its purchasing power. Because raising extra debt funds excess government spending over its revenue receipts, monetary debasement is obvious. However, it takes a little time for the effect to be reflected in government statistics.

Unfortunately, monetary debasement coincides with Trump’s trade tariffs on imported goods, raising input prices for consumers. The combination of bank credit expansion to fund budget deficits and higher trade tariffs is a recipe for an inflation crisis. Yet, macro-economists seem to be unaware of this reality.

At the same time, Main Street is struggling to survive profitably, with the economy already in recession. Take the US budget deficit out of nominal GDP to get a true picture of whether the non-financial private sector is growing or not, and you will find it is already in recession. This leads to declining revenues for the government and increasing welfare commitments raising the budget deficit and its required funding even more.

Therefore, the US Treasury faces a classic debt trap, whereby its funding requirements exceed the notional tax revenues to cover the notional cost. It can only lead to a buyers’ strike, higher bond yields, and a seemingly endless bear market in treasury bonds.

Combined with the impact of higher consumer prices reflected in a rapidly weakening dollar, eventually current declines in the Fed’s funds rate will have to be reversed and raised considerably if the dollar is to be stabilised. In their different ways, this outlook is shared by other G7 nations but nowhere is it more important than for the currency upon which all others are based, however loosely.

Perhaps this reality for the dollar is beginning to dawn on the macro-economic community, which is why gold is rising strongly and taking silver with it. In which case, it is a reassessment which is still in its early days.

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

Only 4 tonnes covered

BIS gold swaps fell from 34 tonnes in July to 30 in August

Submitted by admin on Tue, 2025-09-09 11:17 Section: Daily Dispatches

11:19a ET Tuesday, September 9, 2025

Dear Friend of GATA and Gold:

Gold swaps undertaken by the Bank for International Settlements fell in August by four tonnes, from 34 in July to 30 at the end of last month, according to the bank’s monthly report, published this week —

— and to calculations made from the report by GATA consultant Robert Lambourne.

The report implies that the bank was not recruited to intervene much in the gold market in August on behalf of its member central banks and that there continues to be little interest among them in incurring more gold liabilities or in letting their metal get far from home.

The July 1 report from Lambourne —

— provides some history on the gold swap transactions and their volatility since the bank in 2010 made it possible for its swaps to be calculated.

As recently as January 2022 the bank’s swaps exceeded 500 tonnes but they have fallen sharply since, indicating a profound change of policy toward or outlook on gold among central banks, a trend that seems to have correlated with increasing central bank acquisitions and repatriations, along with gold’s rising price.

But the BIS swaps remain proof that central banks are still active in the gold market surreptitiously as well as openly, the surreptitious part signifying that central banks prefer to conceal interventions whose disclosure would seriously affect prices or explode their plans to influence prices.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 239

a must view:

5. COMMODITY REPORT GOLD/SILVER AND OTHER PRECIOUS METALS/BASE METALS

Anglo American, Teck Resources Mega-Deal Will Create “Compelling, Large-Scale Copper Business”

Tuesday, Sep 09, 2025 – 07:45 AM

Anglo American and Teck Resources have agreed to merge in an all-share transaction to create “Anglo Teck,” a Canada-based miner set to become one of the world’s top five copper producers. The deal marks the largest mining M&A transaction in more than a decade and comes amid a global scramble for rare earth minerals, driven by data center buildouts, power grid upgrades, electric vehicles, and other electrification trends.

Under the proposed mega-merger, Anglo shareholders will hold 62.4% of Anglo Teck, while Teck investors will own 37.6%. The combined company is expected to produce about 1.2 million metric tons of copper annually, driven by Anglo’s 770,000-ton output and Teck’s 545,000 tons.

The deal comes as copper demand rises on the back of global electrification trends, including data center buildouts, the proliferation of EVs, and widespread power grid upgrades to handle the explosion in demand.

At a press conference, Anglo CEO Duncan Wanblad told reporters: “We will have a stronger, more resilient financial platform with scale advantages, including greater flexibility to reallocate capital dynamically to the highest returning opportunities.”

Additional color on the Anglo Teck mega deal:

- Copper Exposure: The new company is expected to derive 70% or more of its revenues from copper, with an annual output forecast to rise from 1.2 million tons to 1.35 million tons by 2027.

- Synergies: Management projects $800M in recurring annual pre-tax savings by year 4, plus $1.4B in EBITDA uplift from integrating the adjacent Collahuasi and Quebrada Blanca mines in Chile, resulting in 175kt of additional copper production annually from 2030 to 2049.

- Portfolio: Anglo Teck combines six world-class copper assets with Anglo’s premium iron ore business in South Africa and Brazil, Teck’s zinc operations in Canada and Alaska, and crop nutrient projects in the UK.

- Listings & Governance: Anglo Teck will be headquartered in Vancouver, with a primary listing on the LSE and secondary listings on the JSE, TSX, and NYSE. Duncan Wanblad (Anglo) will serve as CEO, Teck’s Jonathan Price as deputy CEO, and Sheila Murray as chair. The board will be split evenly.

- Timeline: The boards unanimously support the deal, with completion targeted in 12–18 months, subject to shareholder and regulatory approvals.

Berenberg analysts Richard Hatch and William Dalby told clients earlier, “The combination will result in a compelling, large-scale copper business, we think, with zinc and iron ore exposure, too.”

Anglo American’s London shares jumped the most in 17 months, up nearly 10% by late morning in Europe. U.S.-listed Teck shares were up 14% in premarket trading.

Berenberg analysts noted that Glencore could emerge as a rival bidder but said cultural differences would likely pose a major hurdle. They added that BHP may also show interest, given the scale Teck could bring to its copper business.

“A bidding war could ensue,” the Jefferies analysts told clients.

END

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED DOWN 19.55 PTS OR 0.51%

//Hang Seng CLOSED UP 278.33 PTS OR 1.09%

// Nikkei CLOSED DOWN 184.52 PTS OR 0.42% //Australia’s all ordinaries CLOSED DOWN .51%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1279 OFFSHORE CLOSED UP AT 7.1232/ Oil UP TO 62.92 dollars per barrel for WTI and BRENT DOWN TO 66.70 Stocks in Europe OPENED ALL MOSTLY GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1279 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1232 AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1279

OFFSHORE YUAN: UP TO 7.1232

HANG SENG CLOSED UP 278.33 PTS OR 1.09%

2. Nikkei closed UP 278.33 PTS OR 1.09%

3. Europe stocks SO FAR: ALL MOSTLY GREEN

USA dollar INDEX DOWN TO 97.35 EURO FALLS TO 1.1764 DOWN 4 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.563//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.14…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA. JAPAN 30 YR BOND YIELD: 3.267 UP 4 BASIS PTS.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.6607 Italian 10 Yr bond yield DOWN to 3.511 SPAIN 10 YR BOND YIELD DOWN TO 3.238

3i Greek 10 year bond yield DOWN TO 3.349

3j Gold at $3641.90 Silver at: 41.35 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 74 /100 roubles/dollar; ROUBLE AT 83.21

3m oil (WTI) into the 62 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.14/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.563% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.//JAPAN 30 YR: 3.255 DOWN 1 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7921 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9319 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.065 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.708 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.509 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 41.28

10 YR UK BOND YIELD: 4.6460 UP 3 PTS ESCALATING RAPIDLY

30 YR UK BOND YIELD: 5.491 UP 3 BASIS PTS

10 YR CANADA BOND YIELD: 3.200 DOWN 0 BASIS PTS

5 YR CANADA BOND YIELD: 2.776 UP 0 BASIS PTS.

2a New York OPENING REPORT

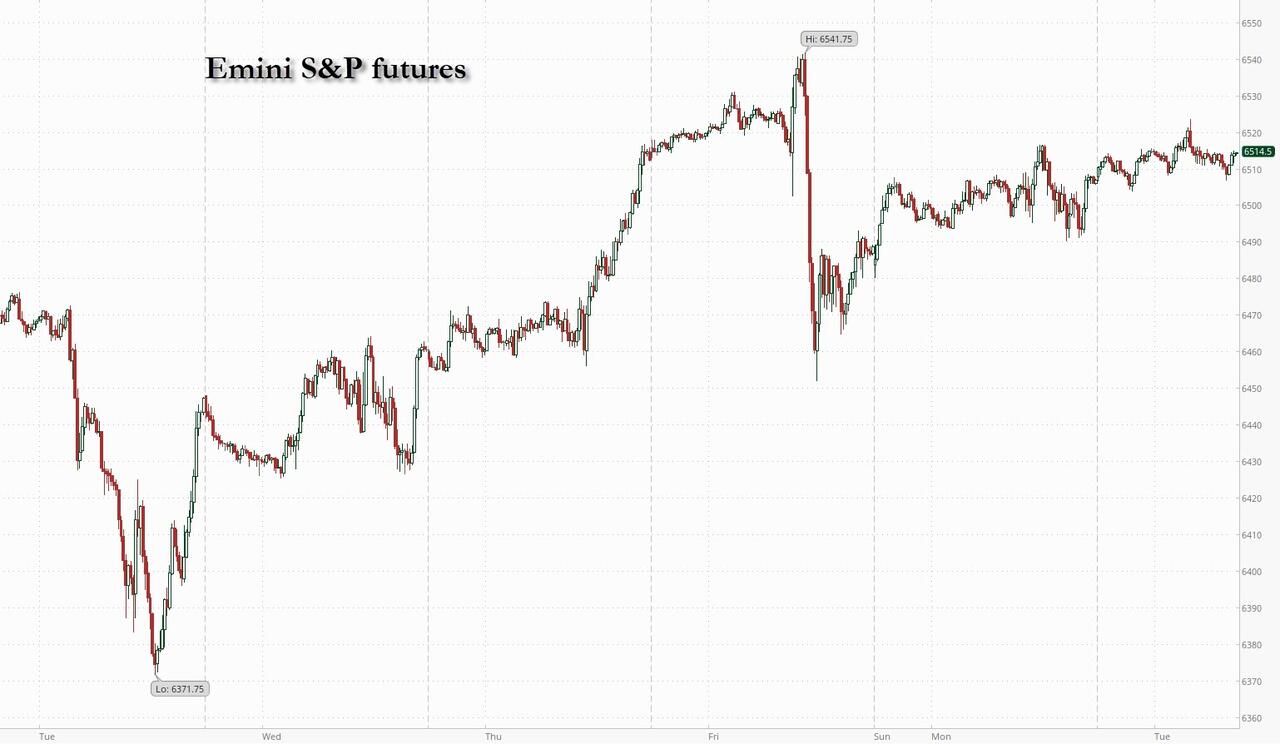

Futures, Yields Rise Ahead Of Another Huge Payrolls Revision

Tuesday, Sep 09, 2025 – 08:36 AM

Futures are higher led by Tech as expectations of Fed rate cuts continued to drive gains, while Treasuries eased after a rally that pushed global bonds into bull-market territory ahead of what is set to be another huge negative benchmark revision to payrolls. As of 8:30am S&P futures are 0.1% higher, while Nasdaq futures gain 0.2% as Mag7 stocks see a muted bid with AVGO/NVDA leading Semis higher. Both Cyclicals and Defensives have caught a bid with Materials buoyed by the Anglo / Teck deal. The yield curve is bear steepening as 10Y yield rise by 2bps to 4.07%; the dollar slid for a third day, with the yen driving advances among major currencies on renewed signals of policy tightening by the Bank of Japan. Commodities are higher with broad-based strength across all 3 complex but notable increases in crude, natgas, coffee, and iron. Today’s macro data focus is on the NFP revision with BBG survey seeing a 700k negative revision to payrolls and the modest beat in the NFIB Small Business Optimism (100.8, vs Exp. 100.5) where the Hiring sub-index has been a leading indicator for future NFP prints.

In premarket trading, Mag 7 stocks post modest gains (Nvidia +0.2%, Tesla +0.2%, Meta +0.4%, Microsoft +0.3%, Amazon -0.09%, Alphabet is flat, Apple -0.4%)..

- Atlassian Corp. (TEAM) rises 5% after announcing it is ending its data center product over the coming three years and will move customers to its cloud platform.

- Brighthouse Financial (BHF) is up 11% after the Financial Times reported that Aquarian Holdings is in late-stage talks with two Middle Eastern investors to finance a takeover of the life insurer.

- Fox Corp. (FOXA) falls 4% and News Corp. (NWSA) declines 4% after Rupert Murdoch and his children resolved a messy family feud with a settlement that gives favored son Lachlan Murdoch broad control and ensures Fox News and the rest of the sprawling media empire retains its conservative slant.

- Planet Labs (PL) is down 10% after after the company said it would offer $300 million of Convertible Senior Notes due 2030. The shares soared 48% in Monday’s regular session.

- Nano Dimension Ltd. (NNDM) rises 2% after initiating a review of strategic alternatives to maximize shareholder value and named David S. Stehlin as its new chief executive officer, replacing Ofir Baharav.

- Nebius (NBIS) jumps 54% after the AI-centric cloud platform company said it will provide Microsoft access to GPU infrastructure capacity at its new data center in Vineland, New Jersey, over five years.

- Sable Offshore (SOC) falls 9% following news that Governor Gavin Newsom seeks to impose further restrictions on California’s offshore oil industry, a setback to Sable and its controversial project off the coast of Santa Barbara County.

- Teck Resources Ltd.’s US-listed shares (TECK) climb 16% after Anglo American PLC agreed to acquire the Canadian miner for 1.3301 shares for each Teck share. Anglo will also pay its investors a $4.5 billion special dividend ahead of the combination. Anglo shares leaped 9.1% in London.

- UnitedHealth Group Inc. (UNH) rises 4% after saying it expects most of its Medicare Advantage members to be in highly rated plans that earn bonus payments next year, a boon for its health insurance business.

The S&P 500 and US bonds have been on a tear as traders increasingly stoked bets that the Fed will kick-off rate cuts this month. Despite clear cracks in the labor market, investors are wagering that the economy is still sufficiently robust to power corporate earnings. Swaps are pricing at least four quarter-point cuts by the time Fed Chair Jerome Powell’s term ends in May. Some are betting that this year’s easing cycle could begin with a jumbo half-point cut this month as job-market weakness outweighs lingering inflation concerns.

As we first discussed two weeks ago, Tuesday’s revisions to Bureau of Labor Statistics data for payrolls for the year through March are expected to reinforce the view of a US jobs slowdown. Later this week, the core consumer price index for August is projected to show an increase of 0.3% for a second month in a row, indicating that progress on reducing price pressures has stalled.

The BLS figures “would be a big change in the job market narrative,” ING rates strategists Michiel Tukker and Benjamin Schroeder wrote in a note. This “could fuel questions of why the Fed shouldn’t cut by 50 basis points this month.”

“This is a supportive combination for equity markets,” said Marija Veitmane, senior multi-asset strategist at State Street Global Markets. “We believe that AI demand is still strong and will continue to support earnings in the sector, pushing returns in the sector — and hence overall equity market performance — higher.”

In Europe, the Stoxx 600 posted modest gains as investors looked out for the next steps in France’s battle to repair its finances. Anglo American Plc rallied more than 9% after agreeing to a tie-up with Canada’s Teck Resources Ltd. Bonds weakened across the board. In France, bonds were little changed as President Emmanuel Macron started his search for a premier capable of steering a budget through a deeply fractured National Assembly. The continued lack of common ground has weighed on sentiment, driving up the country’s risk premium.

“No one was expecting a bloodbath on the markets today, it’s clear that the worst-case scenario of snap elections is not taking place, at least right now,” said Vincent Juvyns, chief investment strategist at ING in Brussels. “So at the moment we’re muddling through, but with a spread with Germany that is at levels of the sovereign debt crisis of 2012.”

Earlier in the session, Asian equities advanced, as tech and Chinese property stocks climbed, and investors continued to eye prospects for interest rate cuts by the Federal Reserve. The MSCI Asia Pacific Index rose as much as 0.8% to the highest since February 2021, with TSMC, Alibaba and Tencent among the biggest boosts. Taiwan’s Taiex jumped more than 1% to a fresh record, and Korea’s Kospi touched a new high for the year. Indonesia led decliners after the nation’s finance minister was abruptly removed. “Further Fed rate cut bets are fueling positive sentiment in Asia today, especially in growth areas like tech that will rally in these conditions,” said Nick Twidale, chief market analyst at AT Global Markets in Sydney. “In the near term, we can push higher and test record levels for Asian stocks, but may see some profit-taking across all markets ahead of key US inflation data.” Indonesia’s Jakarta Composite Index slipped as fiscal concerns mounted after after President Prabowo Subianto replaced Sri Mulyani Indrawati as finance minister. While Purbaya Yudhi Sadewa, who is taking over the role, vowed to keep Indonesia fiscally healthy, Indrawati enjoyed widespread respect among global investors.

In FX, the Bloomberg Dollar Spot Index is down 0.2%. The Japanese yen rose 0.8% against the greenback, taking USD/JPY firmly below 147 after Bloomberg reported Bank of Japan officials are of the view that it may be possible to raise interest rates again this year regardless of domestic political instability. The Aussie dollar also outperforms, rising 0.4% as it benefits from higher iron ore prices.

In rates, treasuries declined, pushing US 10-year yields up 2 bps to 4.06%. Gilts and bunds are also in the red. French 10-year borrowing costs did rise above Italy’s for the first time, although this was down to technical reasons.

In commodities, Oil rose for a second day as investors weighed the prospect for softening demand after Saudi Arabia cut pricing for most of its grades. WTI crude futures rise 1% to near $62.90 a barrel. Spot gold is up almost $20 and flirting with a record. Iron ore climbed for a sixth day and headed for its highest close in more than six months on expectations that Chinese demand will gather momentum. Bitcoin rises 1% to around $113,000.

Looking to the day ahead now, and data releases include French industrial production for July, the US NFIB small business optimism for August, and there’s the preliminary benchmark revision for US payrolls. From central banks, we’ll hear from the ECB’s Nagel and Villeroy, and BoE Deputy Governor Breeden.

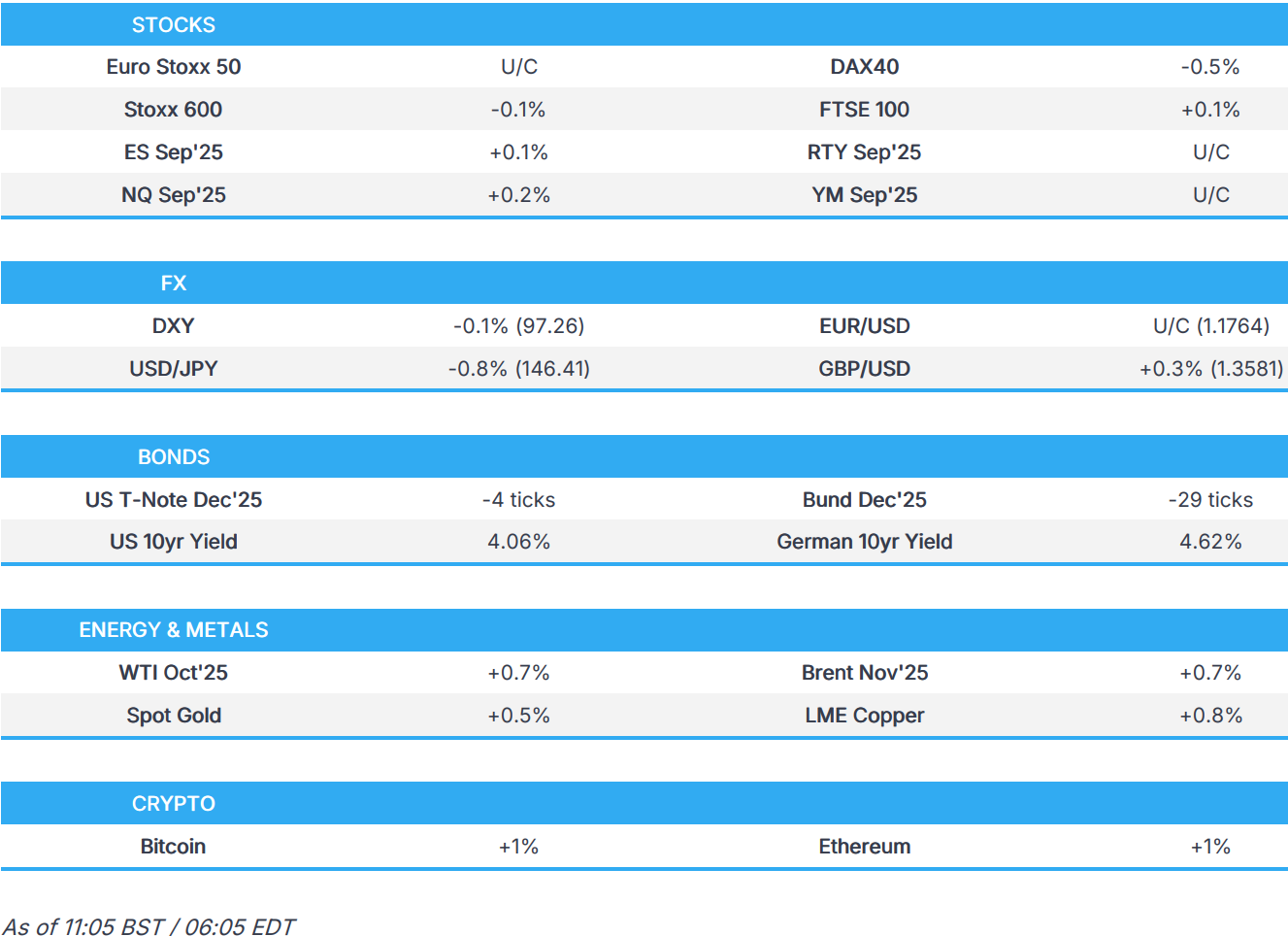

Market Snapshot

- S&P 500 mini +0.1%

- Nasdaq 100 mini +0.2%

- Russell 2000 mini little changed

- Stoxx Europe 600 -0.1%

- DAX -0.5%

- CAC 40 little changed

- 10-year Treasury yield +2 basis points at 4.06%

- VIX +0.1 points at 15.2

- Bloomberg Dollar Index -0.2% at 1196.41

- euro little changed at $1.1765

- WTI crude +1.2% at $63/barrel

Top Overnight News

- The level of U.S. employment for the 12 months through March could be slashed by as many as one million jobs when the government publishes its preliminary nonfarm payrolls benchmark estimate on Tuesday. The payrolls benchmark revision would come on the heels of news last Friday that job growth almost stalled in August and the economy shed jobs in June for the first time in 4-1/2 years. It would suggest the labor market was already struggling before President Donald Trump’s aggressive tariffs on imports. RTRS

- After two federal courts have found that many of the steep emergency tariffs imposed by Trump are illegal, if the Supreme Court rules that Trump did not have the authority to impose the tariffs, the U.S. government could be obligated to refund importers anywhere from $750 billion to $1 trillion, Treasury Secretary Scott Bessent warned. This could potentially place upward pressure on yields. CNBC

- South Korean companies have routinely used unsuitable visas for workers sent to the US to build multibillion dollar advanced manufacturing sites. The admission comes after dramatic raid last week by ICE at a battery plant being built by Hyundai and LG in Georgia, which led to the detention of 475 workers. White House officials warn more such immigration actions are being planned FT.

- The world’s biggest oil and gas companies are cutting jobs, slashing costs, and scaling back investments at the fastest pace since the coronavirus market collapse, as execs brace for a prolonged period of lower crude prices. FT

- Israel ordered Gaza City’s one million residents to leave in advance of a major military offensive. BBG

- US Senate Banking panel to vote on Miran’s Fed nomination on September 10th: BBG

- White House is preparing a report critical on the Bureau of Labor Statistics: WSJ

- Taiwan’s exports hit a record $58.5 billion in August, surging more than 34% from a year ago, boosted by strong tech demand and the AI boom despite new US tariffs. BBG

- BOJ officials are of the view that it may be possible to raise the benchmark interest rate again this year regardless of domestic political instability, as economic conditions have developed in line with expectations. RTRS

- Officials in Europe are considering potential sanctions against China for buying Russian oil. FT

- A measure of France’s borrowing costs exceeded Italy’s for the first time in the euro zone’s history, signaling investor concerns. French PM Francois Bayrou will resign today. BBG

Trade/Tariffs

- Japan’s trade negotiator Akazawa said US tariffs on Japanese goods, including cars, will be lowered by September 16th, according to Reuters citing a post on X. However, Akazawa later commented that tariff discussions with the US are not fully resolved and that Japan must ensure the trade deal is carried out.

- South Korea and the US are to resume working-level talks regarding tariffs, according to Yonhap

- South Korea’s presidential adviser said US trade negotiations are being delayed due to the issue of FX market impacts from the USD 350bln package and have asked the US to help find a solution to the capital market impact, while they told the US that they can’t agree on terms similar to Japan’s USD 550bln deal.

A more detailed look at global markets courtesy of Newsquawk

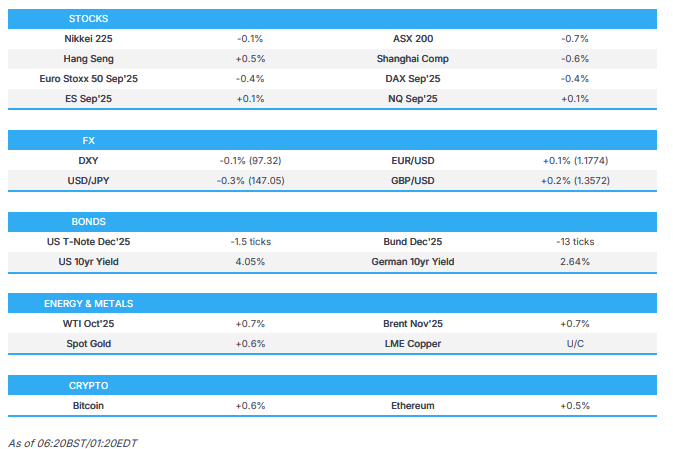

APAC stocks traded mixed as the region failed to fully sustain the mildly positive handover from Wall St, with price action contained amid light fresh catalysts and as participants looked ahead to upcoming events, including inflation data scheduled in the next couple of days. ASX 200 was dragged lower with notable weakness in Energy, Industrials, Real Estate and Financials, with sentiment also not helped by a deterioration in consumer confidence and mixed business surveys. Nikkei 225 initially rallied above the 44,000 levels to print a fresh record high, but then gradually faded its gains as political uncertainty lingered. Hang Seng and Shanghai Comp were mixed with the Hong Kong benchmark led higher by outperformance in real estate and tech, with the former helped as China’s MIIT pledged to accelerate breakthroughs in high-performance chip technology. Conversely, the mainland lagged amid lingering global frictions with EU officials reportedly discussing potential sanctions on China and other parties for the purchase of Russian energy, while Chinese President Xi recently took aim at a ‘certain country’ increasing trade war risks.

Top Asian News

- BoJ reportedly sees some chance of hiking this year, despite the political situation, via Bloomberg citing sources; likely to keep rates unchanged on September 19th. Sees steady progress towards the BoJ price target. Sees the US trade deal as removing some risks to growth. Some officials are even of the view that a hike could be appropriate as early as October.

- Reuters sources report that while political uncertainty in Japan will not derail the BoJ’s normalisation plan, it could impact the timing of the next hike; add, “BoJ does not need to hike in the midst of turbulence”. “no rush…as long as it gets another rate hike done possibly by early next year”.

- Bank of Japan likely to slightly reduce purchases of super-long Japanese government bonds in Q4 2025, according to Reuters sources. BoJ to make final decision on 30 September, influenced by 20-year government bond auction on 17 September and market volatility in super-long JGB yields.

- China’s Ministry of Industry and Information Technology said in a briefing that China is to accelerate breakthroughs in high-performance chip technology and will guide 10-gigabit optical networks from pilot testing to deployment.

- Japanese Finance Minister Kato said he will carefully consider the possibility when asked about entering the LDP leadership race, while he noted that Japan’s economy is showing bright signs, but there is a need to support those suffering from rising prices, including food prices.

- Japanese LDP politician Kono reiterated that if the BoJ delays rate hikes, it would boost inflation, and noted they need to fix a weak yen, so the BoJ needs to hike rates, while he added that a sales tax cut would increase the deficit, and said he is ‘sleeping on’ whether to run for LDP leadership.