XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

FROM MY no 4 SON STEPHEN //THROUGH AI: ENJOY

118 H MACQUARIE FUTURES US 30

323 C HSBC 16

657 H MORGAN STANLEY 24

661 C JP MORGAN SECURITIES 21 7

732 C RBC CAP MARKETS 2

737 C ADVANTAGE FUTURES 2

905 C ADM 5 1

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2025: 54 CONTRACTs NOTICES FOR 5400 OZ or 0.1679 TONNES

total notices so far: 4040 contracts for 404,000 OR 12.566 tonnes)

SILVER NOTICES: 358 NOTICE(S) FILED FOR 1.790 MILLION OZ/

total number of notices filed so far this month : 11,651 CONTRACTS (NOTICES) for 58.255 million oz

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 21.500 MILLION OZ.

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 59.945 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING) PLUS 3.0 MILLION OZ EX FOR RISK = 62.945 MILLION OZ. THIS IS THE FIRST ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES ANND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

AND NOW SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.9296 TONNES PLUS 0.0000 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 9.586//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 23.1132 TONNES!!

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 37.082 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA HUGE 1222 CONTRACTS OI TO 156,703 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 860 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 860 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 630 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1222 CONTRACTS AND ADD TO THE 860 E.FP. ISSUED

WE OBTAIN A FAIR SIZED LOSS OF 362 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR LOSS IN PRICE OF $0.55 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 1.810 MILLION PAPER OZ

OCCURRED WITH OUR $0.55 LOSS IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS MONDAY MORNING:

SHANGHAI CLOSED UP 4.93 PTS OR 0.13%

//Hang Seng CLOSED UP 262.13 PTS OR 1.01%

// Nikkei CLOSED UP 378.38 PTS OR 0.87% //Australia’s all ordinaries CLOSED UP .16%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1214 OFFSHORE CLOSED UP AT 7.1183/ Oil UP TO 63.19 dollars per barrel for WTI and BRENT UP TO 66.96 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1214 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1183 AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 6340 CONTRACTS TO 509,625 OI WITH OUR HUGE GAIN IN PRICE OF $47.40 WITH RESPECT TO TUESDAY’S // TRADING.. WE OF COURSE, LOST NO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (2211). WE HAD ZERO T.A.S. LIQUIDATION AS WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 8,551 CONTRACTS (OR 26.590 TONNES).THEN WE WERE NOTIFIED, THAT WE HAD A ZER0 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR NIL OZ (0.00 TONNES).

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES THESE PAST 3 MONTHS;

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLYAS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). LAST TUESDAY THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW WEDNESDAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPT:

SEPTEMBER: THREE ISSUANCES SO FAR TOTALLING 3082 CONTRACTS OR 308,200 OZ OR 9.5863 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.591 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).LAST TUESDAY THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW YESTERDAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: THREE ISSUANCES FOR 3082 CONTRACTS SO FAR FOR 308,200 OZ OR 9.586 TONNES OF GOLD!!

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT ITS GOLD TO BULLION BANKS AND NOT:

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 34 TONNES SHORTFALL. IT BOUGHT BACKONLY 4 TONNES AND THUS THEIR SHORTFALL TO THE BIS IS 30 TONNES.

THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!.(DEC THROUGH SEPT//ONLY MISSING JUNE.)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE.

DETAILS ON AUGUST COMEX MONTH//FINAL

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 8551 CONTRACTS WITH OUR STRONG GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 5.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH SEPTEMBER CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A FAIR T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 1656 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DESPERATELY TRYING TO STOP GOLD’S ADVANCE AND THIS ENDS IN FAILURE. FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!!

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS (ALONG WITH AUGUST MONTH- END SPREADERS) IS THE REASON WHY WE ARE HAVING DISTORTED COMEX OPEN INTEREST GAINS AND LOSSES IN OI BUT THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE TOTALS WITH GOLD TONNES STANDING FOR THE FOLLOWING MONTHS:

FOR APRIL AT 209 + TONNES INCLUDING MANY MASSIVE QUEUE JUMPS AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES

AND NOW INITIAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.9296 TONNES QUEUE JUMP TO GO ALONG WITH THE 0.000 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 9.586 TONNES//NEW TOTALS STANDING ADVANCES TO 23.1132 TONNES OF GOLD!!!

THE FED IS THE OTHER MAJOR SHORT OF AROUND 30+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 239 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

SUMMARY AUGUST: TOTAL QUEUE JUMPING AND TOTAL EXCHANGE FOR RISKS ISSUANCE FOR THE MONTH OF AUGUST;

WE HAD A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE TOTAL OF 47.2312 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES THEN AUGUST 12: 2.637 TONNES: AND NOW AUG 25: 9.107 TONNES ISSUANCE MONDAY’S MASSIVE 9.1016 TONNES ISSUANCE/AUGUST 25, AUGUST 26 9.0699 TONNES , YESTERDAYDAY’S (AUGUST 27) 9.0699 TONNES AND FINALLY TODAY’S TODAL OF 6.923 TONNESS/NEW STANDING ADVANCES TO 152.208 TONNES.

SUMMARY SO FAR SEPT: 8.093 TONNES INITIALLY STANDING FOR GOLD COUPLED WITH TODAY;S 0.9296 TONNES QUEUE JUMP AND 0.000 TONNES TODAY// NEW TOTALS OF 9.586 TONNES OF EXCHANGE FOR RISK ISSUANCE/:

THAT IS;

A) 0.0000 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY + 9.586 TONNES EX FOR RISK PRIOR =//TOTAL FOR MONTH: 9.586 TONNES EX FOR RISK!!

B) 0.9296 TONNES TODAY QUEUE JUMP

TOTALS: 23.1132 TONNES INITIALLY STANDING FOR GOLD/SEPT.

EXCHANGE FOR PHYSICAL ISSUANCE/SEPTEMBER

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 2211 EFP CONTRACT WAS ISSUED: : /DEC 2211 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2111 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE OCC HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//TUESDAY

- MONTH END SPREADERS HAVE NOW BEEN FINALIZED AS OF AUGUST 29 AND THEY FOR THE FIRST TIME CAUSED NO DAMAGE TO OUR GOLD PRICE

T.A.S.SPREADER ISSUANCE//SEPT.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT/WEDNESDAY MORNING WAS A FAIR SIZED SIZED 1656 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST MONTH ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING; (AND MONTH END SPREADERS)

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S STRONG GAIN IN PRICE IN GOLD AND A CORRESPONDING HUGE GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS ESPECIALLY WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

2) AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

3) TO BE FOLLOWED BY SEPTEMBER’S 3 ISSUANCES FOR EXCHANGE FOR RISK FOR 9.586 TONNES.

STANDING FOR GOLD LAST 8 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES FOLLOWED TO TODAY’S QUEUE JUMP OF 0.5816TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

AND NOW SEPT:

SEPT: 12.600 TONNES OF GOLD (INCLUDES TODAY’S QUEUE JUMP) + 0.000 TONNES EX FOR RISK TODAY+ 8.6312 TONNES EX FOR RISK PRIOR =_//TOTAL EX FOR RISK// FOR MONTH = 9.586//NEW TOTALS FOR GOLD STANDING SEPT = 23.1132 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING SEPTEMBER CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A HUGE $47.40./ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED GAIN IN OI FROM TWO EXCHANGES. BUT AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION AND THAT GAIN IN OI FOR OUR TWO EXCHANGES WAS DUE TO THE LONGS PILING IT ON TRYING TO OBTAIN BADLY NEEDED GOLD///. THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES (WHICH ARE JOINED BY OUR MONTHLY SPREADERS IN ORDER TO FORMALIZE RAIDS ON OUR PRECIOUS METALS) WHICH OF COURSE NORMALLY ENDS IN TOTAL FAILURE LIKE IT DID WITH LAST WEEK AND THIS WEEKS’S TRADING!! THIS IS THE FIRST TIME THAT THE CROOKS COULD NOT MUSTER A RAID ON OPTIONS EXPIRY LONDON/OTC AUGUST TRADING. THEIR RAID ON OUR PRECIOUS METALS CAUSED NO DAMAGE TO OUR PRICE.

WEDNESDAY MORNING//TUESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING/ WEDNESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

DETAIL SUMMARY OF NUMBER OF EXCHANGE FOR RISK ISSUANCES: FEB THROUGH SEPTEMBER TRADING:

EXCHANGE FOR RISK CONTRACTS/MONTH FOR FEBRUARY://FINISHES AT 4 ISSUANCES

THE CME ANNOUNCED TO THE WORLD THAT ON FEB 4 THEY ISSUED 100 CONTRACTS OF EXCHANGE FOR RISK TTO THE BANK OF ENGLAND.THEN ,FEB 4 THEY ISSUED THEIR SECOND CONSECUTIVE EXCHANGE FOR RISK OF 500 CONTRACTS FOR 50,000 OZ (1.555 TONNES OF GOLD. FEB 6 WAS THE THIRD ISSUANCE FOR A HUGE 2400 CONTRACTS, 240,000 OZ OR 7.465 TONNES. AND THEN FINALLY FRIDAY NIGHT, THE 4TH EXCHANGE FOR RISK WAS ISSUED REPRESENTED BY 2834 CONTRACTS OR 283,400 OZ OR 8.8149 TONNES OF GOLD WITH THE OWNER OF THOSE CONTRACTS BEING THE BANK OF ENGLAND. THE BANK OF ENGLAND WANTS THEIR GOLD BACK. THIS NEW EXCHANGE FOR RISK WAS ADDED TO PREVIOUS EXCHANGE FOR RISK OF 9.3264 TONNES TO A NEW TOTAL EXCHANGE FOR RISK = 18.1413 TONNES. IN MID WEEK WE HAD ANOTHER .3114 TONNES OF EXCHANGE FOR RISK ISSUANCED//NEW TOTAL 18,4527 TONNES!..FINALLY THIS TOTAL WAS ADDED TO OUR REGULAR DELIVERIES THROUGH THE MONTH. FEBRUARY IS THE SECOND HIGHEST ISSUANCE OF EXCHANGE FOR RISK AS AUGUST BECOMES THE HIGHEST EVER RECORDED AS YOU WILL SEE BELOW!

EXCHANGE FOR RISK CONTRACTS/MONTH FOR MARCH 3 ISSUANCES

EARLY IN THE DELIVERY CYCLE THE CME NOTIFIED US THAT WE HAD OUR FIRST EXCHANGE FOR RISK CONTRACT ISSUANCE IN MARCH FOR 150 CONTRACTS REPRESENTING 15,000 OZ OF GOLD OR .46656 TONNES. THE BANK OF ENGLAND WAS STILL NOT SATISFIED AS THEY NEED TO RETRIEVE ALL OF ITS LOST GOLD THROUGH LEASING! THE 15,000 OZ WAS ADDED TO OUR NORMAL DELIVERY TOTAL.

MARCH ISSUES IT’S THIRD EXCHANGE FOR RISK: TOTAL FOR THE MONTH FINISHED AT 3

TOTAL ISSUANCE OF EXCHANGE FOR RISK MARCH 28 TOTALS 2200 CONTRACTS FOR 6.8429 TONNES OF GOLD. PRIOR ISSUANCE: .7775 TONNES. THUS TOTAL EXCHANGE FOR RISK FOR MARCH : 7.6179 TONNES OF GOLD. MARCH BECOMES THE 4TH CONSECUTIVE MONTH FOR EXCHANGE FOR RISK ISSUANCE.

APRIL, ISSUED ITS 7TH EXCHANGE FOR RISK: 187 CONTRACTS OR 18,700 OZ OR 0.5816 TONNES

SUMMARY EXCHANGE FOR RISK FOR THE MONTH OF APRIL//TOTAL ISSUANCES 7 FOR 8.3571 TONNES OF GOLD!:

ISSUANCE FOR EXCHANGE FOR RISK ON FIRST DAY NOTICE//APRIL MONTH// WAS 700 CONTRACTS FOR 70,000 OZ OR 2.177 TONNES OF GOLD TO WHICH WE ADD (APRIL 4) : 250 CONTRACTS FOR 25,000 OZ OR .777 TONNES, APRIL 7 ISSUANCE OF 280 CONTRACTS FOR 28,000 OZ OR .8709 TONNES THEN APRIL 9 484 CONTRACTS FOR 48400 OZ OR 1.5054 TONNES AND FINALLY MONDAY MORNING APRIL 14 AT 200 CONTRACTS FOR 20,000 OZ OR .5816 TONNES AND NOW APRIL 24: 600 CONTRACTS FOR 60,000 OZ OR 1.866 TONNES AND NOW APRIL 25 187 CONTRACTS FOR 18700 OZ OR .5816 TONNES//NEW FINAL TOTAL ISSUANCE FOR APRIL: 8.3571 TONNES!!. APRIL ISSUANCE OF EXCHANGE FOR RISK MEANS WE NOW HAD 5 CONSECUTIVE MONTHS FOR EXCHANGE FOR RISK ISSUANCE. THESE DELIVERIES WERE ADDED TO OUR NORMAL DELIVERY CYCLE.

MAY ISSUANCE: 3

MAY ISSUANCE OF EXCHANGE FOR RISK NOW TOTALS 3 ISSUANCES FOR 308,350 OZ. THIS TOTALS 9.591 TONNES OF GOLD WHICH WILL BE ADDED TO OUR REGULAR DELIVERY SCHEDULE. THE RECIPIENT OF THIS LARGESS IS THE BANK OF ENGLAND.

JUNE ISSUANCE: ZERO

JULY ISSUANCE; AFTER A TWO MONTH HIATUS AFTER AN INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD (OCCURRED ON JULY 25) THE CME NOTIFIED US OF A SECOND ISSUANCE OF 706 CONTRACTS FOR 70,600 OZ OR 2.195 TONNES WHICH WILL BE ADDED TO OUR OFFICIAL STANDING. THUS 35.176 TONNES OFFICIAL STANDING + 1.555 TONNES EX FOR RISK PRIOR + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES OF GOLD STANDING

AUGUST: 7 ISSUED,

TOTAL EXCHANGE FOR RISK MONTH OF AUGUST 44.696 TONNES, THE HIGHEST MONTHLY EVER COMEX ISSUANCE!!!!!!

THUS 107.5117 TONNES OF NORMAL GOLD STANDING (INCLUDING ALL QUEUE JUMPS/EX FOR PHYS TRANSFERS) + 44.696 TONNES EX FOR RISK = 152.208 TONNES.

SEPTEMBER: 3 ISSUED:

THE CME NOTIFIED US THAT OUR THREE ISSUANCES OF EXCHANGE FOR RISK EQUATES TO 0 CONTRACTS FOR NIL OZ BUT A TOTAL FOR THE MONTH OF 9.586 TONNES. WE WILL PROBABLY HAVE A DOOZY FOR SEPT DELIVERIES AS THE BANK OF ENGLAND WANTS ITS GOLD BACK+ THE MASSIVE QUEUE JUMPING BY OTHER CENTRAL BANKS IS CERTAINLY ON DISPLAY TODAY’S 0.9296 TONNES QUEUE JUMP.

ANALYSIS SEPT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// SEPT COMEX CONTRACT

WE HAVE A STRONG SIZED GAIN TOTAL OF 26.59 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPTEMBER AT 8.093 TONNES. WE HAD THE FOLLOWING QUEUE JUMP OF 0.9296 TONNES OF GOLD ALONG WITH 0.000 TOTAL TONNES OF EXCHANGE FOR RISK TODAY/// TOTAL FOR MONTH TOTALS EX FOR RISK// MONTH = 9.586//NEW TOTAL STANDING FOR GOLD IN SEPT ADVANCES TO: 23.1132 TONNES.

ALL OF THIS HUGE STANDING FOR SEPTEMBER WAS ACCOMPLISHED DESPITE OUR GAIN IN PRICE TO THE TUNE OF $47.40

WE HAD 1486 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 8,551 CONTRACTS OR 855,100 0Z (26.59 TONNES)

confirmed volume TUESDAY 250,429 contracts// fair//

speculators have left the gold arena

INITIAL GOLD COMEX

SEPT CONTRACT MONTH

SEPT 10 /2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 entries . |

| Deposit to the Dealer Inventory in oz | 0- |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 ENTRIES xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 54 notice(s) 5400 OZ 0.1679 TONNES |

| No of oz to be served (notices) | 309 contracts 30,900 OZ 0.9611 TONNES |

| Total monthly oz gold served (contracts) so far this month | 4040 notices 404,000 oz 12.566 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER 0

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

0 entries

ADJUSTMENTs 1

customer account to dealer account 2025.513 oz (63 kilobars)

AMOUNT OF GOLD STANDING FOR SEPTEMBER

THE FRONT MONTH OF SEPTEMBER STANDS AT 363 CONTRACTS FOR A LOSS OF 62 CONTRACTS. WE HAD 360 CONTRACTS FILED ON TUESDAY SO WE GAINED A HUGE 298 CONTRACTS OR 29,800 OZ ENTERTAINED A QUEUE JUMP OF 0.9296 TONNES. WE NOW MUST ADD TO OUR INITIAL 2.333 TONNES OF GOLD STANDING TO TODAY’S QUEUE JUMP OF 0.9296 TONNES AND THEN ADD MONTH SEPT// EX FOR RISK = 9.586//THUS NEW TOTAL OF GOLD STANDING ADVANCES TO 23.1132 TONNES

OCTOBER GAINED 306 CONTRACTS UP TO 61,307

NOVEMBER GAINED 1 CONTRACTS UP TO 2917 CONTRACTS.

We had 54 contracts filed for today representing 5400 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 21 notices issued from their client or customer account. The total of all issuance by all participants equate to 54 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 7 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for SEPTEMBER /2025. contract month, we take the total number of notices filed so far for the month (4040 X 100 oz ) to which we add the difference between the open interest for the front month of SEPT ( 363 CONTRACTS) minus the number of notices served upon today (54 x 100 oz per contract) equals 434,900 OZ OR 13.5272 TONNES OF GOLD TO WHICH WE ADD OUR TOTAL EX FOR RISK/SEPT MONTH OF 9.586 TONNES//NEW TOTAL STANDING ADVANCES TO 23.1132 TONNES

thus the INITIAL standings for gold for the SEPTEMBER contract month: No of notices filed so far (4040 x 100 oz +we add the difference for front month of SEPT. (363 OI} minus the number of notices served upon today (54 x 100 oz) which equals 434,900 OZ OR 13.5272 TONNES PLUS 9.586 TONNES EXCHANGE FOR RISK = 23.1132 TONNES.

TOTAL COMEX GOLD STANDING FOR SEPT..: 23.1132 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY INACTIVE ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,041,699.430 oz 63.502 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 38,912,304.554 oz

TOTAL REGISTERED GOLD 21,290,436.068 or 662.21 tonnes

TOTAL OF ALL ELIGIBLE GOLD 17,621,868.486 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 19,246,811 oz ((REG GOLD- PLEDGED GOLD)= 598.65 tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE SEPTEMBER 2025 SILVER CONTRACTS

SEPT 10 2025

INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2 entries: i) Out of Delaware: 110,855.238 oz ii) Out of HSBC 10,1582.190 oz total withdrawal 121,068.428 oz |

| Deposits to the Dealer Inventory | 1 ENTRY i) Into Stonex: 348,856.900 oz total deposit: 348,856.90 oz |

| Deposits to the Customer Inventory | 3 DEPOSIT ENTRIES/CUSTOMER ACCOUNT i)Into Asahi 1,808,400.600 oz ii) into CNT: 384,441.000 oz iii) into stonex: 967.100 oz total deposit 2,193,808.740 oz |

| No of oz served today (contracts) | 358 CONTRACT(S) (1.790 million OZ |

| No of oz to be served (notices) | 338 contracts (1.690 MILLION oz) |

| Total monthly oz silver served (contracts) | 11,651 Contracts (58.255 million oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

1 ENTRY

i) Into Stonex: 348,856.900 oz

total deposit: 348,856.90 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

3 DEPOSIT ENTRIES/CUSTOMER ACCOUNT

i)Into Asahi 1,808,400.600 oz

ii) into CNT: 384,441.000 oz

iii) into stonex: 967.100 oz

total deposit 2,193,808.740 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

2 entries:

i) Out of Delaware: 110,855.238 oz

ii) Out of HSBC 10,1582.190 oz

total withdrawal 121,068.428 oz

ADJUSTMENTs 1 dealer to customer

i) Manfra: 519,405.508 oz

TOTAL REGISTERED SILVER: 196.791 MILLION OZ//.TOTAL REG + ELIGIBLE. 520.707 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR AUGUST

silver open interest data:

FRONT MONTH OF SEPTEMBER /2025 OI: 696 OPEN INTEREST CONTRACTS FOR A LOSS OF 443 CONTRACTS. WE HAD 759 CONTRACTS SERVED ON TUESDAY SO WE GAINED A STRONG 316 CONTRACTS OR 1.5800 MILLION OZ ENTERTAINED A QUEUE JUMP//NEW STANDING FOR SILVER COMEX INCREASES TO 59.945 MILLION OZ. THEN WE MUST ADD OUR INITIAL ISSUANCE OF 600 CONTRACTS FOR EXCHANGE FOR RISK OR 3.0 MILLION OZ//NEW STANDING ADVANCES TO 62.945 MILLION OZ

STANDING FOR SILVER: 61.3650 MILLION OZ

OCTOBER LOST 86 CONTRACTS TO 2347

NOVEMBER GAINED 34 CONTRACTS UP TO 1402.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 358 or 1.790 MILLION oz

CONFIRMED volume; ON TUESDAY 75,348 strong//

AND NOW SEPT. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in SEPTEMBER. we take the total number of notices filed for the month so far at 11,651 X5,000 oz = 58.255 MILLION oz

to which we add the difference between the open interest for the front month of SEPT (696) AND the number of notices served upon today (358 )x (5000 oz)

Thus the standings for silver for the SEPTEMBER 2025 contract month: (11,651) Notices served so far) x 5000 oz + OI for the front month of SEPTEMBER(696) minus number of notices served upon today (358)x 5000 oz equals silver standing for the SEPTEMBER contract month equating to 59.945 MILLION OZ TO WHICH WE ADD OUR INITIAL EXCHANGE FOR RISK SEPT TOTALLING 3.0 MILLION OZ//NEW STANDING ADVANCES TO 62.945 MILLION OZ

New total standing: 62.945 million oz which is HUGE for this active delivery month of SEPT.. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 196.791 million oz of registered silver

JPMorgan as a percentage of total silver: 210.283/520.707 million. 40.59%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

SEPT 10 WITH GOLD DOWN $1.10 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 9 WITH GOLD UP $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.29 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 8 WITH GOLD UP $41.40 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 5 WITH GOLD UP $47.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 2.29 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 4 WITH GOLD DOWN $22.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 6.30 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 984.26 TONNES//

SEPT 3 WITH GOLD UP $43.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 12.88 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 990.56 TONNES//FAIRY TALES

SEPT 2 WITH GOLD UP $79.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 9.74 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 977.68 TONNES

AUGUST 29 WITH GOLD UP $33.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 5.44 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 28 WITH GOLD UP $18.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 27 WITH GOLD UP $12.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 959.92 TONNES

AUGUST 26 WITH GOLD UP $12.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 958.49 TONNES

AUGUST 25 WITH GOLD DOWN $1.05 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 22 WITH GOLD UP $35.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 21 WITH GOLD DOWN $6.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 958.21 TONNES

AUGUST 20 WITH GOLD UP $29.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.16 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 962.21 TONNES

AUGUST 19 WITH GOLD DOWN $16.90 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 965. TONNES

AUGUST 18 WITH GOLD DOWN $4.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 4.01 TONNES OF GOLD INTO THE GLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 15 WITH GOLD DOWN $0.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.86 TONNES OF GOLD//// ///INVENTORY RESTS AT 961.36 TONNES

AUGUST 14 WITH GOLD DOWN $20.80 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 13 WITH GOLD UP $9.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 12 WITH GOLD UP $2.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 4.58 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 964.22 TONNES

AUGUST 11 WITH GOLD DOWN $53.55 TODAY//SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT DEPOSIT OF 0.55 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.64 TONNES

AUGUST 8 WITH GOLD UP $10.00 TODAY//HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 6.30 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 959.09 TONNES

AUGUST 7 WITH GOLD UP $16.10 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.15 TONNES OF GOLD OUT OF THE GLD/://// ///INVENTORY RESTS AT 952.79 TONNES

AUGUST 6 WITH GOLD DOWN $8.15 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.14 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 955.94 TONNES

AUGUST 5 WITH GOLD UP $8.45 TODAY//HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/://// ///INVENTORY RESTS AT 954.80 TONNES

AUGUST 4 WITH GOLD UP $24.65 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.43 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 953.08 TONNES

AUGUST 1 WITH GOLD UP $51.40 TODAY//HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/://// ///INVENTORY RESTS AT 954.51 TONNES/

JULY 31 WITH GOLD DOWN $2.65 TODAY//NO CHANGES IN GOLD AT THE GLD://// ///INVENTORY RESTS AT 956.23 TONNES/

GLD INVENTORY: 979.68 TONNES, TONIGHTS TOTAL

SILVER

SEPT 10 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 9 WITH SILVER DOWN $0.55/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.816 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 486.677 MILLION OZ./

SEPT 8 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 488.493 MILLION OZ./

SEPT 5 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 489.674 MILLION OZ./

SEPT 4 WITH SILVER DOWN $0.68/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 491.308 MILLION OZ./

SEPT 3 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT DEPOSIT OF 1,816 MILLION OZ INTO THE SLV:// ////INVENTORY RESTS AT 494.043 MILLION OZ./

SEPT 2 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF .727 MILLION OZ FROM THE SLV:// ////INVENTORY RESTS AT 492.227 MILLION OZ./

AUGUST 29 WITH SILVER UP $0.80/ HUGE CHANGES AT THE SLV AT DEPOSIT 0F 1.862 MILLION OZ:// ////INVENTORY RESTS AT 492.954 MILLION OZ./

AUGUST 28 WITH SILVER UP $0.48/ NO CHANGES AT THE SLV:// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 27 WITH SILVER UP $0.04/ SMALL CHANGES AT THE SLV: A WITHDRAWAL OF 454,000 OZ FORM THE SLV// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 26 WITH SILVER DOWN $0.19/ NO CHANGES AT THE SLV: // ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 25 WITH SILVER DOWN $0.28/ SMALL CHANGES AT THE SLV: A SMALL DEPOSIT OF 0.363 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 22 WITH SILVER UP $0.92/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 0.908 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.183 MILLION OZ./

AUGUST 21 WITH SILVER UP $0.29/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 1.09 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 492.091 MILLION OZ.//

AUGUST 20 WITH SILVER UP $0.41/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 545,000 OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 493.181 MILLION OZ.//

AUGUST 19 WITH SILVER DOWN $0.64/ HUGE CHANGES AT THE SLV: A MAMMOTH DEPOSIT OF 9.173 MILLION OZ OF SILVER VAPOUR ARRIVES AT THE SLV// ////INVENTORY RESTS AT 493.726 MILLION OZ.//

AUGUST 18 WITH SILVER UP $0.06/ NO CHANGES AT THE SLV ////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 15 WITH SILVER DOWN $0.04/ SMALL CHANGES AT THE SLVA WITHDRAWAL OF .909 MILLION OZ FROM THE SLV//////INVENTORY RESTS AT 484.553 MILLION OZ.//

AUGUST 14 WITH SILVER DOWN $0.52/ NO CHANGES AT THE SLV/////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 13 WITH SILVER UP $0.62/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 1.317 MILLION OZ INTO THE SLV:.////INVENTORY RESTS AT 485.462 MILLION OZ.//

AUGUST 12 WITH SILVER UP $0.68/ HUGE CHANGES AT THE SLV// A DEPOSIT OF 2.18 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 484.145 MILLION OZ.//

AUGUST 11 WITH SILVER DOWN $0.56/ HUGE CHANGES AT THE SLV// A WITHDRAWAL OF 3.905 MILLION OZ FORM THE SLV:.////INVENTORY RESTS AT 481.965 MILLION OZ.//

AUGUST 8 WITH SILVER UP $0.20/ NO CHANGES AT THE SLV//:.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 7 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 2.179 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 485.870 MILLION OZ.//

AUGUST 6 WITH SILVER UP $0.02/ SMALL CHANGES AT THE SLV//: A DEPOSIT OF 0.727 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 483.691 MILLION OZ.//

AUGUST 5 WITH SILVER UP $1.51/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 1.119 MILLION OZ OUT OF THE SLV.////INVENTORY RESTS AT 482.964 MILLION OZ.//

AUGUST 4 WITH SILVER UP $0.50/ SMALL CHANGES AT THE SLV//: A WITHDRAWAL OF 0.183 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.083 MILLION OZ.//

AUGUST 1 WITH SILVER UP $0.19/ HUGE CHANGES AT THE SLV//: A WITHDRAWAL OF 2.816 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 484.264 MILLION OZ.//

JULY 31 WITH SILVER DOWN $1.00/ HUGE CHANGES AT THE SLV//: A DEPOSIT OF 0.454 MILLION OZ INTO THE SLV.////INVENTORY RESTS AT 487/398 MILLION OZ.//

CLOSING INVENTORY 485.677 MILLION OZ//

PHYSICAL GOLD/SILVE

1/PETER SCHIFF

JOHN RUBINO

2. MATHEW PIEPENBERG/VON GREYERZ

ALASDAIR MACLEOD

The dollar: Calm before the storm?

Markets expecting falls in interest rates are blind to reality. Lower rates won’t prevent an imploding debt/credit bubble undermining the dollar and its purchasing power.

| Alasdair MacleodSep 10∙Paid |

The chart below shows what will blow apart the credit bubble, putting in chain a series of events which could rapidly undermine the dollar, potentially fatally, and all US investment media. The carnage is bound collapse the other major G7 currencies and their financial markets as well.

In May 2022, the long bond yield smashed through the 40-year downtrend at 3%. The equity bubble continued, with the S&P 500 rising from 4130 to an all-time high of 6550 currently. Admittedly, the headlong rush in the long bond’s yield paused at 5.1% in October, since when it has moved sideways. But as the pecked lines covering from that period illustrate, this is a consolidation and not an end to the uptrend in yields. And very soon, they will start rising again. And technical analysis tells us to expect another rapid rise in the yield, covering a similar distance to the preceding move. That takes it into national bankruptcy territory.

Already, the valuation relationship with equities is more overstretched than it has been since reliable records began, as the next chart shows:

The long bond’s yield is the same as in the first chart but inverted. And as stated above, the S&P 500 Index has continued rising regardless leading to the massive valuation disparity gap indicated by the two-headed arrow. There is no clearer proof of an equity bubble, and bubbles always end in a collapse. Furthermore, the prospect of such a crisis, which is what the charts tells us, is confirmed by gold’s performance. Notice the similar consolidation pattern of the last five months to that of the long bond’s yield. Both gold and the long bond yield can be expected to be rising in synchrony subsequent to their respective corrections:

Let’s think through the implications for a moment. A rising long bond yield tells us that markets are pricing in greater investment risk for buyers of US treasury debt. Investors will require compensation for that risk, which cannot be for risk of outright default because the Fed can always print the government’s way out. Therefore, the risk can only be that the dollar will lose purchasing power.

Gold’s rise confirms this conclusion. If anything, its recent breakout is front running a break above 5.1% yield for the long bond. When that happens, it is bound to collapse the equity bull market.

For a hint of how it may play out and the consequences, we can refer to Germany between 1920 —1923 and the relationship between a credit bubble in its fiat currency (the Reichsmark) and the subsequent consequences for its purchasing power. Along with the other European combatants, Germany abandoned its gold standard just before the First World War, financing its war machine by a combination of debt and money printing and minimal taxation.

That the purchasing power of the Reichsmark fell by about 80% between the end of the war in November 1918 and February-1920 need not detain us. More important was the credit-driven boom between March 1920 and December 1921. Prices were relatively steady, and business and the stock market were booming. The Reichsmark even rose strongly against the dollar, which was still on a gold standard, more than doubling by July 2020 from February that year before ending 70% higher in May 2021. It was the best performing currency at that time.

The inflationary excesses of 1918—1920 had died down, to be replaced with a brief period of great prosperity financed by yet more credit and currency expansion but at a more measured pace. This prosperity was unevenly distributed, favouring the wealthy and speculators, with the stock market trebling before it peaked in December 1921.

The pause in Germany’s inflation crisis rhymes with the dollar’s current conditions following the post-covid inflation in 2021—2022. Since then, there has been a speculative boom, with equities rising to record levels driven by credit expansion. As was the case in Germany’s brief boom, Wall Street has created wealth for speculators while Main Street stagnates.

To complete the analogy, all we need to see is the stock market crash. It is already wildly overvalued relative to bonds. And for a new round of inflation to commence. As Germany was in 1920—1921, we appear to be in the eye of an inflationary storm.

At this point in our analysis, it will be helpful to define inflation properly. It refers to an expansion of credit and debt, not to the consequences for prices. The confusion arises from a fashionable belief that the general level of prices inflates, and not that the purchasing power of a currency declines. It is probably the most misleading error in all economic analysis. What happened in Germany over 100 years ago was a collapse in the Reichsmark’s purchasing power, though it has been misleadingly interpreted as a hyperinflation of prices. Similarly, the fiat dollar’s purchasing power has been declining and rising prices are the consequence.

Not even expert economists and analysts would think to make the comparison of today’s credit conditions and the consequences with those of Germany in 1920—1923. But if Germany’s example is followed, then like the fiat Reichsmark the fiat dollar will collapse entirely. The causes might be different, but the essence of the problem is the same. So what will be the trigger?

Convention suggests that financial crises are triggered by an event, systemic or otherwise. But here is an obvious cause staring us in the face: a growing realisation that the US economy is not just stalling, as recently revised employment figures indicate, but it is descending into recession. The need for the US government to fund its deficit will escalate accordingly, and unexpected demand for extra funding can only increase bond yields.

At the same time, the president’s deliberate policy to weaken the dollar with lower interest rates while imposing tariffs on imported goods will make things far worse.

It is remarkable that the US’s creditors haven’t yet appreciated the dangers facing them, but then they are fully committed to the credit bubble. Like investors in the German stock market between 1920 and December 1921, they have become drunk on their good fortune and oblivious of the bear about to pounce.

Higher bond yields will end up collapsing the dollar

The consequences for the stock market of bond yields soaring are one thing, but the concerns are far wider. As we saw in the US’s 1929—1930 bear market, banks added to the decline by liquidating stocks held as collateral, dumping them onto reluctant markets. But the greater damage will be on corporations needing to refinance debt at rates which are commercially unaffordable or go under. Furthermore, counterparty risks in derivative markets will increase, threatening the stability of the entire shadow banking system.

To these dangers, there can only be one response and that is to follow Germany of the early 1920s: turn on the credit pump and reflate like mad irrespective of the consequences for the dollar. Politics demands it, whatever the Fed thinks. Ahead of the forthcoming credit crisis, it is impossible to see how the currency will be stabilised before it has collapsed. In Germany between 1922 and November 1923, the pre-war Reichsmark valued at 23 cents US finally settled at one trillion to one, or over four trillion to the gold-backed US dollar.

The economic consequences of a repeat of this performance for today’s fiat currencies hardly bear thinking about. The professional classes in Germany lost all their wealth, and along with the labouring classes faced starvation. The only beneficiaries were magnates such as Hugo Stinnes, the inflation king and Fritz Thyssen, who made their fortunes by exporting and earning gold-backed dollars.

Gold, which in all European nation’s common law and that of all their former colonies and dominions by adoption is money without counterparty risk. It is only just beginning to reflect these existential dangers to dollar denominated credit. Unless or until a solution can be magically found to prevent the dollar’s fiat currency value from declining, gold and also silver will be the best refuge from the near-certainty of the ultimate credit chaos.

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 239

a must view:

5. COMMODITY REPORT platinum….

Platinum Explodes Overnight; Four Straight Day’s of ETF Selling in Silver

by Blue Line Futures

Wednesday, Sep 10, 2025 – 6:51

Staying ahead of Gold, Silver, Copper, Bitcoin, and the Commodities markets has never been easier! Get the Blue Line Futures Precious Metals Chart Pack today by registering here:

Futures trading involves a substantial risk of loss and may not be suitable for all investors. Therefore, carefully consider whether such trading suits you in light of your financial condition. Trading advice is based on information taken from trade and statistical services and other sources Blue Line Futures, LLC believes are reliable. We do not guarantee that such information is accurate or complete, and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades. All trading decisions will be made by the account holder. Past performance is not necessarily indicative of future results.

Blue Line Futures is a member of NFA and is subject to NFA’s regulatory oversight and examinations. However, you should be aware that the NFA does not have regulatory oversight authority over underlying or spot virtual currency products or transactions or virtual currency exchanges, custodians or markets. Therefore, carefully consider whether such trading is suitable for you considering your financial condition.

Hypothetical performance results have many inherent limitations, some of which are described below. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown. In fact, there are frequently sharp differences between hypothetical performance results and the actual results subsequently achieved by any particular trading program.

One of the limitations of hypothetical performance results is that they are generally prepared with the benefit of hindsight. In addition, hypothetical trading does not involve financial risk, and no hypothetical trading record can completely account for the impact of financial risk in actual trading. For example, the ability to withstand losses or to adhere to a particular trading program in spite of trading losses are material points which can also adversely affect actual trading results. There are numerous other factors related to the markets in general or to the implementation of any specific trading program which cannot be fully accounted for in the preparation of hypothetical performance results and all of which can adversely affect actual trading results.

ASIAN MARKETS THIS WEDNESDAY MORNING:

SHANGHAI CLOSED UP 4.93 PTS OR 0.13%

//Hang Seng CLOSED UP 262.13 PTS OR 1.01%

// Nikkei CLOSED UP 378.38 PTS OR 0.87% //Australia’s all ordinaries CLOSED UP .16%

//Chinese yuan (ONSHORE) CLOSED UP AT 7.1214 OFFSHORE CLOSED UP AT 7.1183/ Oil UP TO 63.19 dollars per barrel for WTI and BRENT UP TO 66.96 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN TRADING :/ONSHORE YUAN UP IN TRADING AT 7.1214 AND STRONGER//OFF SHORE YUAN TRADING UP TO 7.1183 AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1214

OFFSHORE YUAN: UP TO 7.1183

HANG SENG CLOSED UP 262.13 PTS OR 1.01%

2. Nikkei closed UP 378.38 PTS OR 0.87%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 97.82 EURO FALLS TO 1.1694 DOWN 8 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.566//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.52…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA. JAPAN 30 YR BOND YIELD: 3.232 DOWN 2 BASIS PTS.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.6420 Italian 10 Yr bond yield DOWN to 3.497 SPAIN 10 YR BOND YIELD DOWN TO 3.233

3i Greek 10 year bond yield DOWN TO 3.344

3j Gold at $3645.50 Silver at: 41.10 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 27 /100 roubles/dollar; ROUBLE AT 84.96

3m oil (WTI) into the 63 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.52/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.566% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.//JAPAN 30 YR: 3.234 DOWN 2 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7952 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9336 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.079 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.734 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.544 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 41.28

10 YR UK BOND YIELD: 4.6340 UP 1 PTS ESCALATING RAPIDLY

30 YR UK BOND YIELD: 5.479 UP 0 BASIS PTS

10 YR CANADA BOND YIELD: 3.237 DOWN 0 BASIS PTS

5 YR CANADA BOND YIELD: 2.789 UP 0 BASIS PTS.

2a New York OPENING REPORT

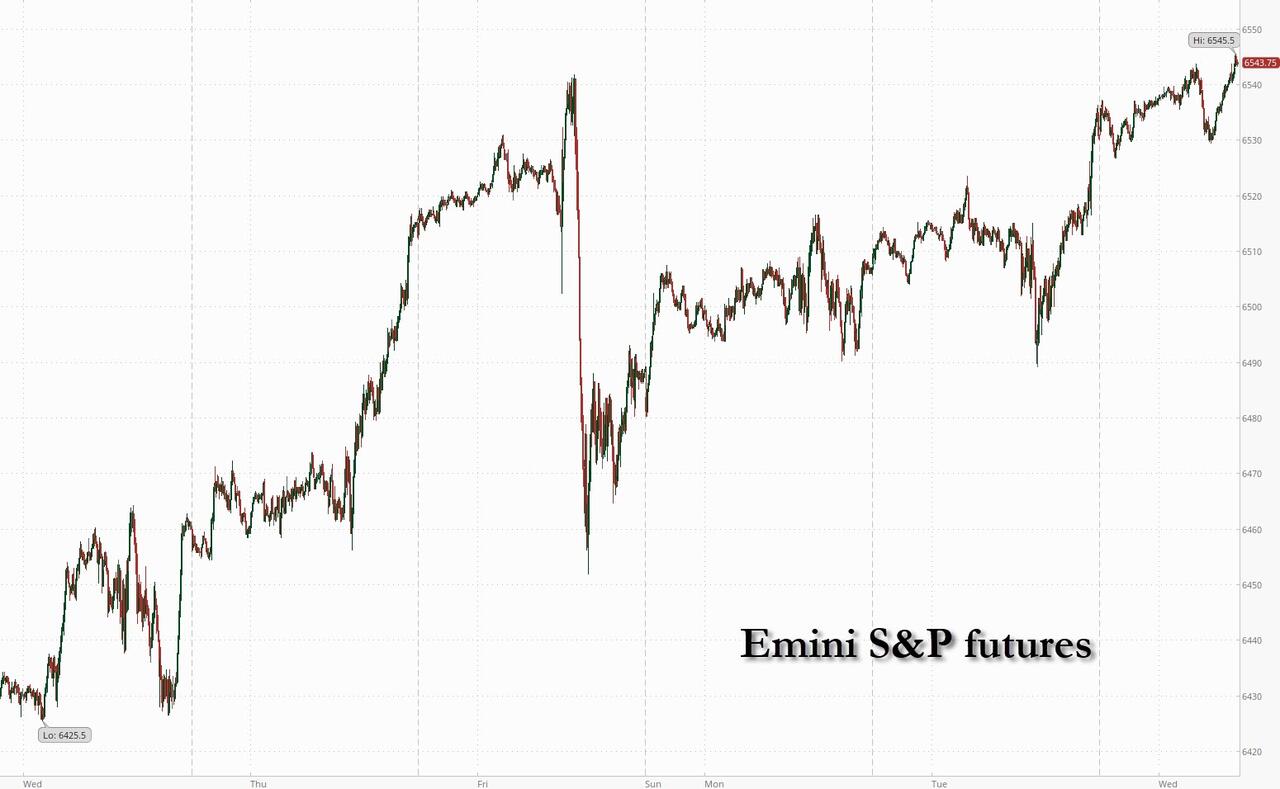

Futures Hit New All Time High After Oracle’s Ridiculous Forecast, PPI Looms

Wednesday, Sep 10, 2025 – 08:30 AM

US stock futures are trading at another record high, with European and Asian also pushing higher after Oracle underpinned the strong sentiment in tech with blowout guidance sending its shares up by 30% in premarket trading, while the market awaits inflation data today and tomorrow. As of 8:15am, S&P futures are 0.3% higher with Nasdaq futures rising 0.4%…

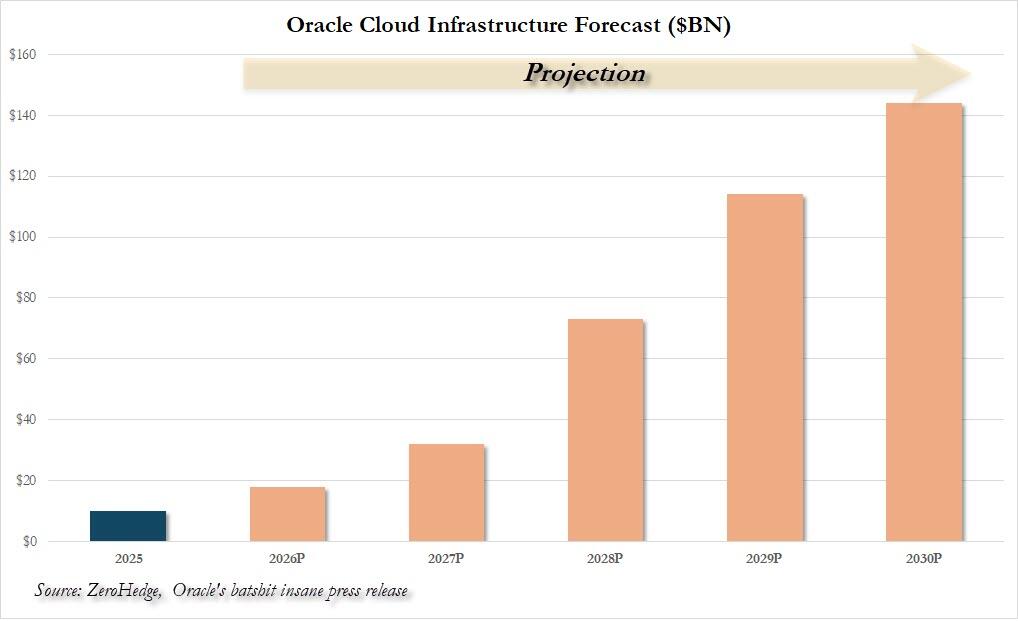

… with all eyes on ORCL as earnings missed across the board, but it was the ridiculous hockeystick guidance – with cloud infra guide going from $18bn in FY25 to $144bn in FY30 – that sent the stock +30% pre-mkt and fueled optimism that the AI infrastructure roll-out is speeding up. Chipmaker Nvidia Corp. and AI infrastructure firms also advanced (NVDA +1.9%, AVGO +2.3%). Large-cap Cyclicals poised to outperform Defensives.

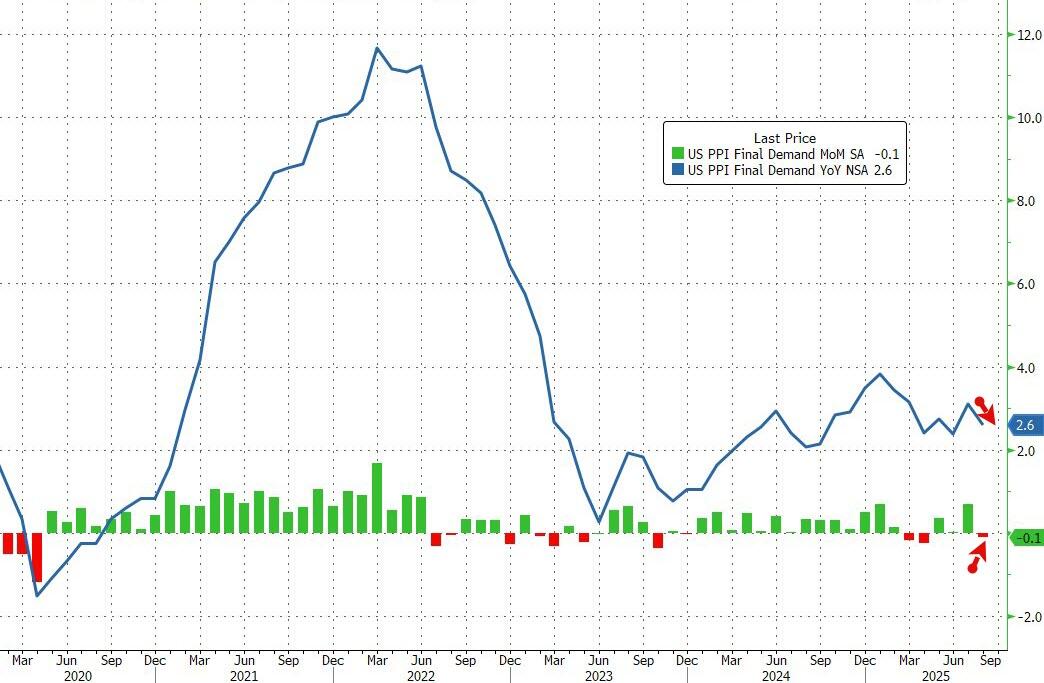

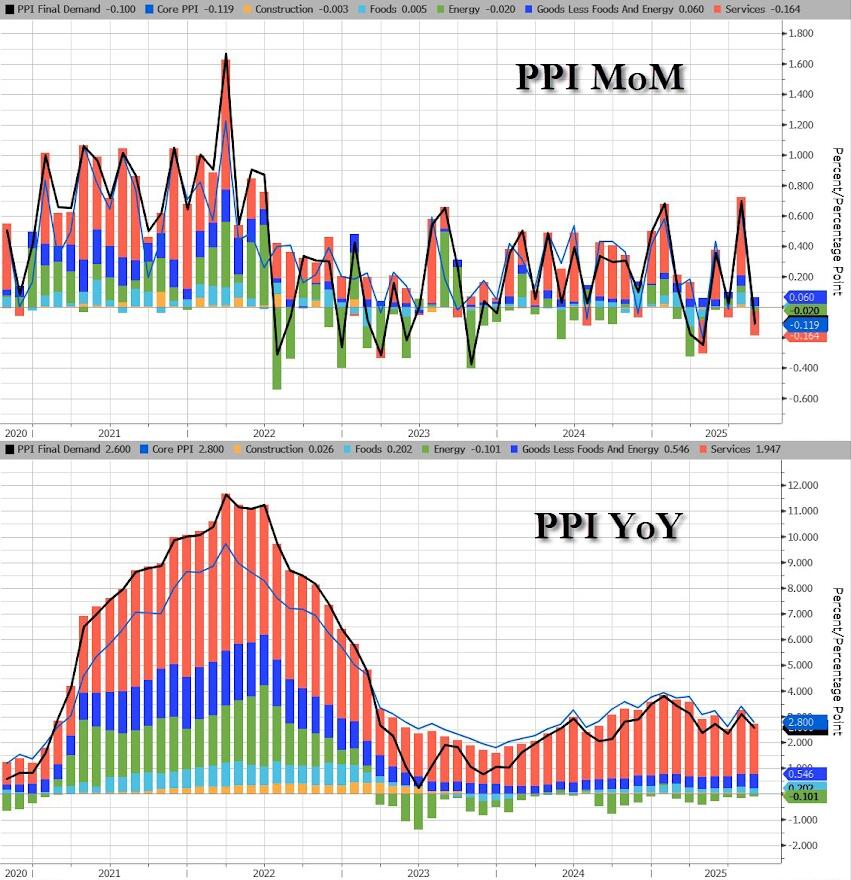

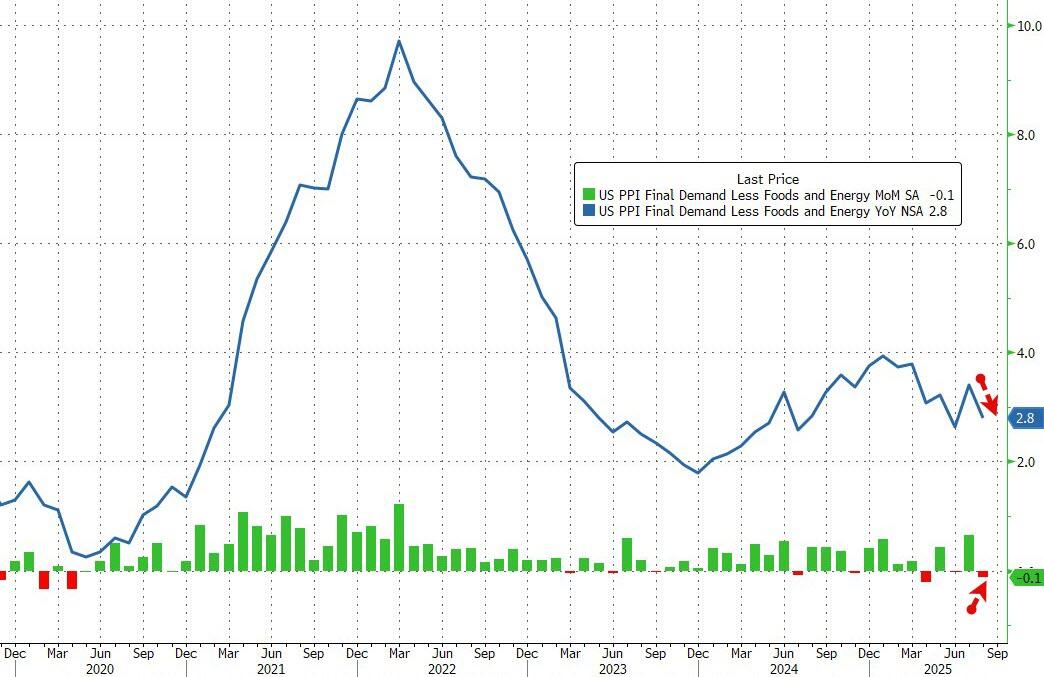

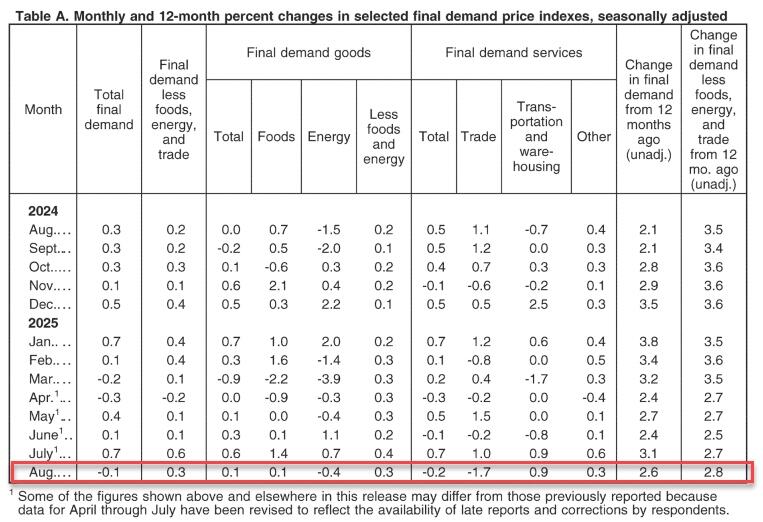

Keep an eye on Poland / Russia as Poland invoked Article 4 of NATO (military defensive consult); for ref, Article 5 is the call to arms of all members, used only once by the US after Sept 11. Trump looks to implement secondary tariffs on India / Russia. The yield curve is twisting steeper with the 30Y yield +1bp and USD is flat. Cmdtys are mostly higher led by crude and precious. Today’s macro data focus is on PPI with CPI tomorrow. TSMC also said its August sales rose 34% to signal sustained, strong demand for AI tech.

With the latest leg of the stock rally driven by hopes that the Fed will rapidly lower rates, investors believe that sticky wholesale and consumer inflation will remain sufficiently contained and give officials room to shore up the jobs market.

The likelihood of lower financing costs is supporting rate-sensitive sectors such as tech, allowing markets to remain resilient against recurring risks ranging from geopolitical tensions to trade wars. Over the past day alone, the S&P 500 advanced despite escalating frictions in the Middle East and Eastern Europe alongside fresh US tariff threats targeting India and China.

“The prospect of far easier financial conditions remains supportive,” said Geoff Yu, FX and macro strategist for EMEA at BNY Mellon. “Barring any really large upside shocks in today and tomorrow’s PPI/CPI figures, it’s really a case of ‘as you were.’”

August’s producer price figures are due at 8:30 a.m. Eastern time, with the consumer inflation report following 24 hours later. Those reports, along with retail figures due Sept. 16, will be the last major data points before Fed Chair Jerome Powell announces next week’s rate decision.

Oracle is poised to add roughly $200 billion in market value if its early surge carries through Wednesday’s session. The company’s outlook underscores how AI developers must continue ramping up spending, with its customer OpenAI alone projecting that trillions of dollars will eventually be needed to build and operate infrastructure.

“I don’t know if their guidance is actually realistic but the market is buying it and buying it fully,” said David Kruk, head of trading at La Financiere de l’Echiquier. “Maybe the outlook has been overbought, it’s hard to tell.”

The renewed excitement over AI and strong corporate earnings are prompting Wall Street strategists to boost their forecasts for the S&P 500. Deutsche Bank’s Binky Chadha lifted his year-end target for the US benchmark to 7,000, signaling potential gains of more than 7% from current levels. Analysts at Barclays also raised their estimate, while Wells Fargo Securities forecasts an 11% increase by the close of next year.

Poland shot down drones that crossed into its territory during a Russian air strike on Ukraine. France has appointed Sebastien Lecornu as prime minister, the fifth in two years and starting on a day of mass protests in the country. French yields are unchanged, bund yields are edging lower and Treasuries are mixed.

In premarket trading, Mag 7 stocks are mixed, with Nvidia outperforming after Oracle’s report (Nvidia +2%, Tesla +0.4%, Alphabet +0.1%, Microsoft +0.7%, Meta -0.1%, Apple -0.4%, Amazon -0.5%).

- Oracle (ORCL) surges 32% after the software company gave a robust forecast for its cloud-infrastructure business, a sign of strong AI-related demand. Stocks tied to AI computing infrastructure are rallying after Oracle forecast faster-than-expected revenue growth in its cloud infrastructure unit. CoreWeave (CRWV) +7%, Arista Networks (ANET) +3%, AMD (AMD) +3%

- Asset Entities (ASST) soars 121% after holders approved a merger with Vivek Ramaswamy’s Strive Enterprises, marking the next step in creating a public Bitcoin treasury company.

- Bill Holdings (BILL) is up 6% after the Financial Times reports Elliott Management has built a large stake in the payments automation company.

- Fifth Third Bancorp (FITB) fall 3% after the bank said it discovered allegedly fraudulent activity at one of its commercial borrowers. The lender will present at an industry conference later on Wednesday.

- GameStop (GME) jumps 10% after the video-game retailer reported Hardware and Accessories net sales for the second quarter that beat the average analyst estimate.

- Nio ADRs (NIO) are down 8% after the Chinese EV maker announced an equity offering of as much as 181.8 million class A shares.

- Synopsys (SNPS) shares are down 22% after the software company reported third-quarter results that featured a weak read on Design IP revenue. It also gave an earnings outlook that was weaker than expected.

- Travere Therapeutics (TVTX) soars 15% after the FDA informed the company that an advisory committee is no longer needed for its supplemental drug application for the treatment of a rare kidney disorder.

In Europe, the Stoxx 600 rises 0.2% with retail and technology shares leading gains, while travel and chemicals stocks are the biggest laggards. Sentiment was boosted by jump for Spanish retailer Inditex which means Spain’s IBEX benchmark is outperforming. Novo Nordisk is rising after announcing 9,000 job cuts, though also cutting guidance. Here are the biggest movers Wednesday:

- Inditex shares gained 6.9%, the most since April, after the Spanish retailer said sales at the start of the third quarter were up 9%. Jefferies analysts note that the firm benefits from strong customer traction

- Anglo American rises as much as 3.7% in London, its highest intraday level since Jan. 20, after Berenberg upgraded to hold from sell after the miner moved to acquire Canada’s Teck Resources

- Novo Nordisk shares gain as much as 3.2%, reversing an earlier 3% drop, after the Danish drugmaker said it will cut 9,000 jobs globally as it tries to regain ground in the competitive market for obesity treatments

- EssilorLuxottica gains as much as 4.5% as Barclays starts coverage of the eye-wear maker with an overweight rating, saying the company offers an “exciting” growth profile

- Haleon shares rise as much as 3.2%, the most in more than four months, after Goldman Sachs upgraded the stock to buy from neutral, citing an attractive valuation

- AB Foods shares drop as much as 12%, the most intraday since March 2020, after the British conglomerate gave a trading update that showed weakness in both its sugar unit and the Primark budget clothing chain

- Vistry shares fall as much as 8.9%, the most since April, as the house-builder delivers first-half results that Goodbody describes as “disappointing”

- Zurich Airport drops as much as 2.3%, the most in almost three months, as Oddo BHF starts coverage with an underperform recommendation, citing both execution and regulatory risks

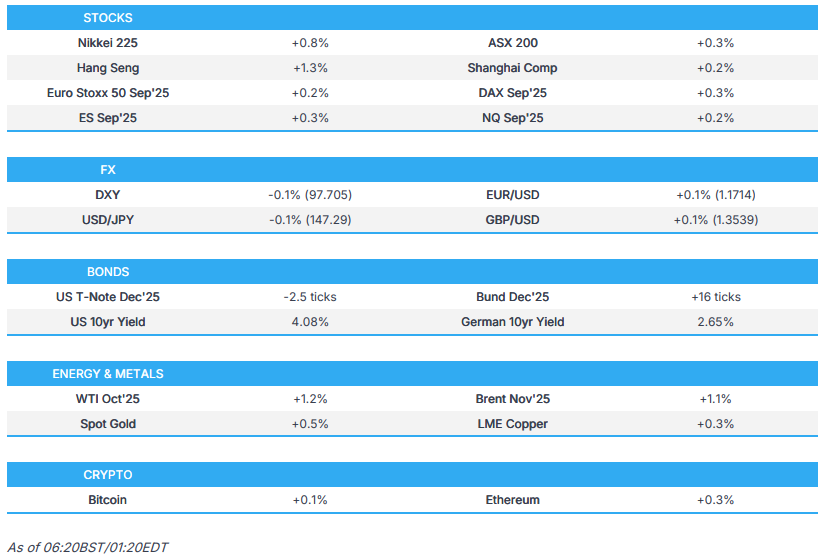

Earlier in the session, Asian stocks rose, on course for a fifth-straight day of gains, with the technology-dominated markets of South Korea and Taiwan leading the charge to close at record highs. The MSCI Asia Pacific Index jumped 1.1% to the highest level since February 2021, with TSMC, Softbank, Tencent and SK Hynix among the biggest boosts. An upbeat cloud-business outlook from Oracle Corp. provided the latest boost for tech sentiment. South Korea’s Kospi closed at a record high, buoyed further by optimism that a proposal to lower the threshold for capital-gains tax will be scrapped. Taiwan’s benchmark also closed at a new all-time high. Elsewhere, key equity gauges advanced more than 1% in Hong Kong and Singapore. Mainland China shares edged up but underperformed their regional peers, as sentiment softened after last week’s military parade and following the strong rally in August.

In FX, the Bloomberg Dollar Spot Index little changed, Norway’s krone is stronger, with euro and Canadian dollar weaker.

In rates, treasuries are mixed in early US trading with front-end yields slightly richer on the day and long-end underperforming, steepening the curve around the 10-year, which is little changed. Focal points of US session include August PPI data in the morning and 10-year note reopening in early afternoon. Front-end yields are 1bp-2bp richer on the day, long-end cheaper by similar amounts and the 10-year near 4.09%, widening 2s10s and 5s30s spreads steeper by 1bp-2bp.French bonds underperform slightly as Lecornu’s first day as prime minister was marked by mass protests against the government’s budget proposals; bunds trade broadly in line with Treasuries. In the US, Treasury auction cycle continues with $39 billion 10-year reopening at 1pm New York time and concludes Thursday with $22 billion 30-year sale. Demand was strong for Tuesday’s 3-year note auction, which stopped through by 0.7bp and produced a record low primary-dealer allotment

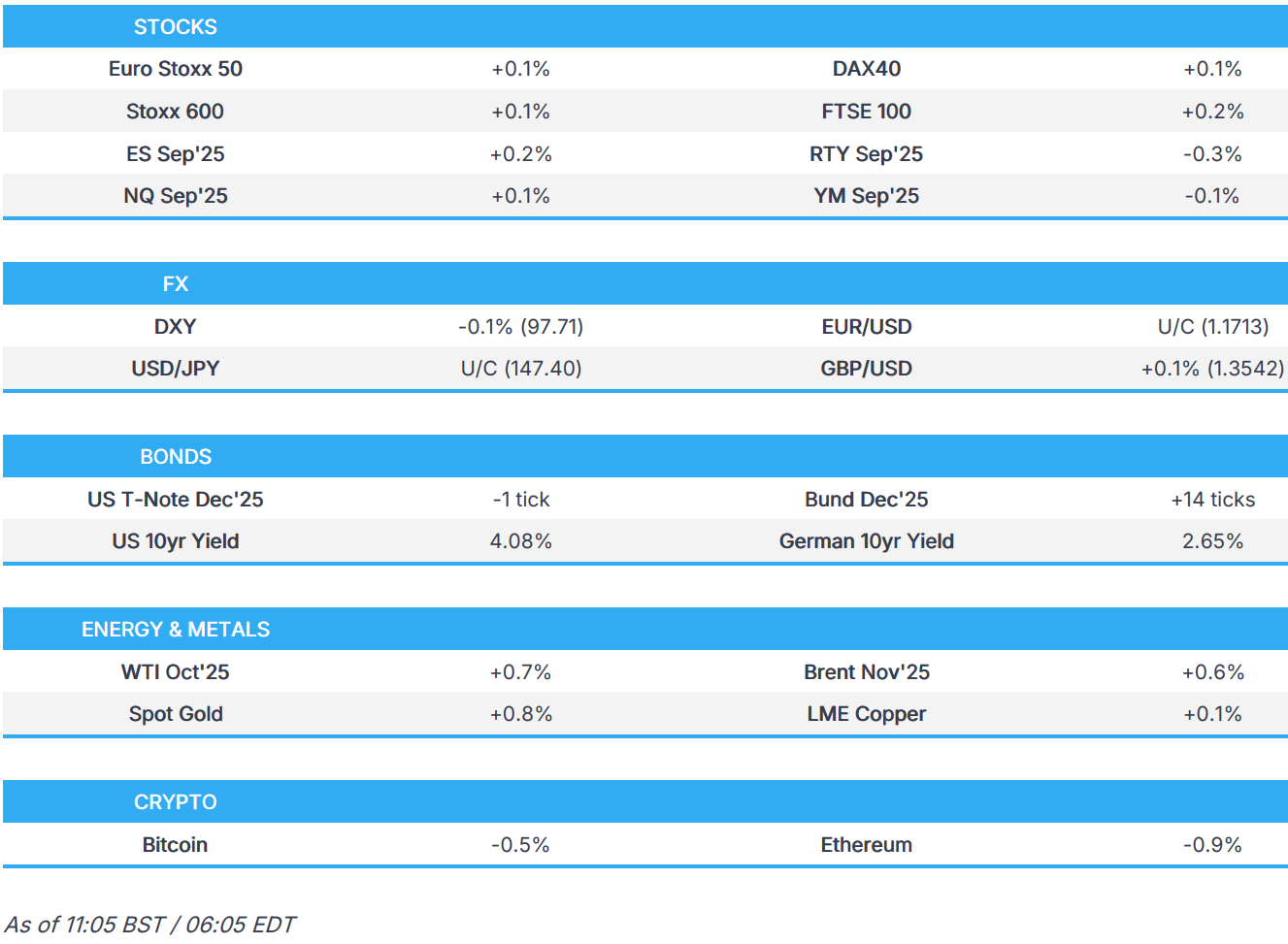

In commodities, brent futures are up 0.9% to $67/barrel while gold is up by about $19/oz to around $3,646/oz.

Looking at today’s calendar, US economic data slate includes August PPI (8:30am) and July wholesale trade sales (10am)

Market Snapshot

- S&P 500 mini +0.2%

- Nasdaq 100 mini little changed

- Russell 2000 mini -0.3%

- Stoxx Europe 600 +0.1%

- DAX little changed

- CAC 40 +0.1%

- 10-year Treasury yield little changed at 4.08%

- VIX +0.2 points at 15.19

- Bloomberg Dollar Index little changed at 1200.72

- euro little changed at $1.1709

- WTI crude +0.8% at $63.16/barrel

Top Overnight News

- US judge temporarily blocked President Trump from removing Federal Reserve Governor Cook.

- NATO fighter jets have shot down Russian drones over Polish airspace for the first time, after what Warsaw described as “unprecedented violation” of its territory that led it to trigger emergency consultations in the alliance. FT

- US employer health insurance costs are projected to rise about 9.2-9.5% in 2026, the steepest increase in at least 15 years: WSJ

- Trump has asked the EU to impose tariffs of up to 100% on India and China as part of a joint effort to increase pressure on Russia to end its war in Ukraine. A second US official said Washington was prepared to “mirror” any tariffs on China and India imposed by the EU, potentially leaded to further increase in US levies on imports from both countries. FT

- Trump is will crack down on pharmaceutical adverts on TV and social media, while he signed a memo requiring pharma ads to disclose all risks.

- White House could impose severe restrictions on drugs from China, delivering a blow to the US pharma industry (which has been racing to buy the rights to drugs created in China) while bolstering the small-cap US biotech industry. RTRS

- US has warned of hidden radios that could be embedded in solar-powered highway infrastructure: RTRS

- Trump and Indian Prime Minister Narendra Modi voiced optimism about reaching a trade deal on Tuesday, softening rhetoric after months of friction over tariffs and Russian oil purchases. CNBC

- US Commerce Secretary Lutnick floats taking a share of university patent money; US should get half the benefit from patients, via Axios.

- China’s consumer prices fell more than expected in August while deflation in wholesale prices persisted, as calls mounted for Beijing to ramp up measures to bolster sluggish domestic demand and cushion weakening exports growth. China’s PPI was inline w/the Street in Aug (-2.9%, a modest improvement vs. -3.6% in Jul) while the CPI undershot the consensus (-0.4% vs. the Street -0.2% and vs. 0.00% in Jul). CNBC

- Oracle shares jumped 30% premarket after providing a blowout outlook for its cloud business. The company is on track to add about $190 billion in market value today. BBG

- U.S. holiday sales are projected to grow at their slowest pace since the pandemic, Deloitte said in a forecast released on Wednesday, as macroeconomic uncertainties weigh on consumer spending. RTRS

- The Supreme Court plans to move quickly on the IEEPA tariff case (oral arguments will be during the first week in November). WaPo

- A judge on Tuesday night blocked President Donald Trump from firing Federal Reserve Governor Lisa Cook as a lawsuit challenging her removal continues. CNBC

Trade/Tariffs

- US President Trump reportedly asked the EU to hit China and India with 100% tariffs to pressure Russian President Putin to end the war, while a US official said that Washington was prepared to mirror any tariffs on China and India imposed by the EU, according to FT.

- US President Trump posted that India and the US are continuing negotiations to address trade barriers and he looks forward to speaking with his very good friend, Indian PM Modi, in the upcoming weeks, while Trump added that he feels certain that there will be no difficulty in coming to a successful conclusion for both nations.

- Indian PM Modi said he is confident India and US trade negotiations will pave the way for unlocking the limitless potential of the India-US partnership, while he added that their teams are working to conclude discussions at the earliest and he looks forward to speaking with US President Trump. It was separately reported that India and US officials are likely to have an exchange of trade delegations soon and an in-person meeting later in September, according to CNBC-TV18.

- US Supreme Court agreed to hear the Trump administration’s appeal of the judicial ruling that invalidated most of President Trump’s tariffs and it fast-tracked the appeal in the tariffs case.

- US Treasury Secretary Bessent is confident that the Supreme Court will back Trump tariffs, while he added there is a fallback tariff plan, though it is more cumbersome.

A more detailed look at global markets courtesy of Newsquawk