TODAY DATA IS INCOMPLETE,.LITTLE EMERGENCY

GOLD $3976.76 (3:30 PM)

SILVER: 49.07 (3:30 PM)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

132 C SG AMERICAS 5

323 C HSBC 126

323 H HSBC 72

332 H STANDARD CHARTERED B 191

363 H WELLS FARGO SECURITI 233

435 H SCOTIA CAPITAL (USA) 680

657 H MORGAN STANLEY 750

661 C JP MORGAN SECURITIES 576

686 C STONEX FINANCIAL INC 6

726 C PLUS500US FINANCIAL 1

732 C RBC CAP MARKETS 645

737 C ADVANTAGE FUTURES 9 4

905 C ADM 8

GOLD: NUMBER OF NOTICES FILED FOR OCT/2025: 1653 CONTRACTs NOTICES FOR 165,300 OZ or 5.1415 TONNES

total notices so far: 35,459 contracts for 3,545,900 OR 110.292 tonnes)

SILVER NOTICES: 89 NOTICE(S) FILED FOR 0.445 MILLION OZ/

total number of notices filed so far this month : 3521 CONTRACTS (NOTICES) for 17.605 million oz

INITIAL STANDING FOR OCT: 13.240 MILLION OZ PLUS 0.455 MILLION OZ QUEUE JUMP EQUATES TO 18.080 MILLION OZ//*INCLUDES ALL QUEUE JUMPING)

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 32.565 MILLION OZ (WILL BE HUGE THIS MONTH)

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

AND NOW OCTOBER: 18.080 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

AND NOW OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH AN INITIAL HUGE 4.878 TONNES QUEUE JUMP FOLLOWED BY LAST 3 DAYS OF QUEUE JUMPS OF 11.5354 TONNES,(TODAY’S QUEUE JUMP = 4.979 TONNES) PLUS 11.353 TONNES OF OUR ISSUANCE EXCHANGE FOR RISK/5 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 123.129 TONNES OF GOLD.

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STILL SMALL TO FAIR

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 77.748 TONNES

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A TINY SIZED 88 CONTRACTS OI TO 166,386 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A MONSTER 768 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 768 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 768 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 88 CONTRACTS AND ADD TO THE MONSTER 768 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF 680 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR GAIN OF $1.75 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 3.400 MILLION PAPER OZ

OCCURRED WITH OUR GAIN OF $1.75 IN PRICE.

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

SHANGHAI CLOSED UP 51.20 POINTS OR 1.32%

//Hang Seng CLOSED CLOSED DOWN 76.87 PTS OR 0.29%

// Nikkei CLOSED : UP 845.45 PTS OR 1.77% //Australia’s all ordinaries CLOSED UP 0.34%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.1231// OFFSHORE CLOSED UP AT 7.1296/ Oil UP TO 62.31 dollars per barrel for WTI and BRENT UP TO 66.03 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING UP TO 7.1231 // OFFSHORE YUAN TRADING UP TO 7.1296 :/ONSHORE YUAN TRADING ABOVE OFF SHORE A 71231/ AND THUS STRONGER/OFF SHORE YUAN TRADING UP TO 7.1296 AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 4937 CONTRACTS TO 490,496 OI WITH OUR STRONG GAIN IN PRICE OF $68.40 WITH RESPECT TO WEDNESDAY’S // TRADING COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, WITH THAT PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (4270). WE HAD NO T.A.S. LIQUIDATION WEDNESDAY. WE HAD A TOTAL GAIN IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 9,207 CONTRACTS (OR 28.63 TONNES).THEN WE WERE NOTIFIED OF A ZERO CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS ISSUED FOR NIL OZ OR 0 TONNES OF GOLD.

THUS THE TOTAL NUMBER OF CONTRACTS EXCHANGE FOR RISK ISSUED FOR THE MONTH OF OCT REMAINS AT 11.353 TONNES OF GOLD UNDER THE GUIDANCE OF 5 ISSUANCES.

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES:

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 4 MONTHS;

(TOTAL EXCHANGE FOR RISK LAST 4 MONTHS 70.097 TONNES//BANK OF ENGLAND TOTAL RESERVES LISTED AT 310 TONNES.)

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY AS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). EARLY IN THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW AN ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPT:

SEPTEMBER: SEVEN ISSUANCES SO FAR TOTALLING 7,370 CONTRACTS OR 737,000 OZ OR 22.923 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

AND NOW OCTOBER: 5 ISSUANCES

WE RECEIVED NOTICE THAT OUR INITIAL EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE WAS FOR 500 CONTRACTS OR 50,000 OZ /1.555 TONNES OF GOLD!!THAT WAS FOLLOWED BY A STRONG 650 CONTRACT ISSUED THURSDAY OCT 2 FOR 2.0217 TONNES AND THAT WAS FOLLOWED THE NEXT DAY BY ANOTHER HUGE 1320 CONTRACT ISSUANCE FOR 13,200 OZ OR 4.1057 TONNES AND THIS WAS FOLLOWED BY SATURDAY’S OCT 4: 180 CONTRACT ISSUANCE FOR 18,000 OZ OR .5596 TONNES:THIS BRINGS US TO TODAY, OCT 8 WITH A HUGE ISSUANCE OF 1000 CONTRACTS FOR 100,000 OZ OR 3.1104 TONNES TOTAL ISSUANCES 5 OCCASIONS FOR 3650 CONTRACTS OR 365,000 OZ OR 11.353 TONNES

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).AT THE BEGINNING OF THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW PREVIOUS DAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: SEVEN ISSUANCES FOR 7370 CONTRACTS SO FAR FOR 737,000 OZ OR 22.923 TONNES OF GOLD!!

OCTOBER: FIRST INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD. THIS WAS FOLLOWED BY AN ISSUANCE OF 650 CONTRACTS OR 65000 OZ OR 2.0217 TONNES. THEN ON OCT 3 WE RECEIVED OUR 3RD NOTICE FOR A HUGE 1320 CONTRACTS OR 132000 OZ OR 4.1057, AND THEN SATURDAY OCT 4, THE CME ISSUED ITS 4 ISSUANCE FOR 180 CONTRACTS FOR 18,000 OZ OR .5594 TONNES. THEN FINALLY OCT 8 FOR 1000 CONTRACTS, OR 100,000 OZ OR 3.1104 TONNES TOTAL ISSUANCE ON 5 OCCASIONS: 11.353 TONNES

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT MUCH ITS GOLD TO BULLION BANKS AND :(EX FOR RISK 9 MONTH TOTALS 129.6 TONNES)//TOTAL RESERVES OF BOE EQUALS 310 TONNES)

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 30 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES LAST MONTH AND THUS THEIR SHORTFALL TO THE BIS IS 30 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!…..(DEC THROUGH OCT//ONLY MISSING JUNE. TOTAL 9 MONTHS ISSUANCE 118.5 TONNES)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE. THE VERY FIRST ISSUE OF EXCHANGE FOR RISK CAME IN MAY 2023. HUGE ISSUANCES BEGAN OCT AND DEC 2024. ROBERT LAMBOURNE, GATA CONSULTANT AND EXPERT ON BIS AND BANK OF ENGLAND ISSUES HAS WRITTEN TO THE BANK OF ENGLAND AUTHORITIES CONCERNING THE REFUSAL OF THE BANK OF ENGLAND’S AUDITORS TO SUPPLY A POSITIVE AUDIT ON THEIR GOLD TONNAGE AND OTHER ASSETS HELD UNDER THE E.E.A. . PLEASE SEE THE LETTER WRITTEN TODAY AND YOU WILL FIND IT UNDER CHRIS POWELL OF GATA’S DISPATCHES. YOU WILL FIND IT FASCINATING!!

DETAILS ON OCTOBER COMEX MONTH//

IN TOTAL WE HAD A STRONG SIZED GAIN ON OUR TWO EXCHANGES OF 9,207 CONTRACTS WITH OUR GAIN IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 6.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE. THE FORCE MAJEURE AT GRASBERG IS CERTAINLY HAVING AN EFFECT ON LEASE RATES IN LONDON WITH RESPECT TO GOLD/SILVER.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH SEPTEMBER/OCT CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A HUGE T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 5313 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE AGAIN LAST NIGHT DESPERATELY TRYING TO STOP GOLD’S ADVANCE. THIS GENERALLY ENDS IN FAILURE AS FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!! SO THE CROOKS DECIDED IT WAS NECESSARY TO RAID AROUND THE BIG INTEREST RATE ANNOUNCEMENT SEPT 17-SEPT 18 AND THEY TRIED AGAIN THIS PAST WEDNESDAY/RIGHT BEFORE FIRST DAY NOTICE, WITH MUCH FAILURE AS THE TOTAL OPEN INTEREST REFUSED TO BUCKLE!! THIS LEADS US TO FIRST DAY NOTICE SEPT 30 AND THE LAST POSSIBLE DAY FOR A RAID AND TRUE TO FORM OUR CROOKS DECIDED TO RAID MUCH TO THE DELIGHT OF OUR BOYS IN LONDON WHO PICKED UP EXTRA AMOUNTS OF GOLD AND TENDERED FROM THIS SHORT PAPER ISSUANCE. THEN MUCH TO MY ANGER THEY DECIDED TO RAID AGAIN ON OCT 2 WITH CHINA OFF THIS WEEK FOR THEIR FALL FESTIVAL (BACK TODAY) AND OF COURSE THE IMPORTANT RELIGIOUS HOLIDAY FOR THE JEWISH PEOPLE OCT 1-2, YOM KIPPUR. AGAIN THIS ENDED IN ABSOLUTE FAILURE AS LONDON AGAIN CAME TO THE RESCUE (MARCHING TO WILLIAM TELL’S OVERTURE) WITH THEIR MASSIVE TENDERING FOR PHYSICAL. YOU CAN JUST VISUALIZE THE MASSIVE HEADACHE THE CROOKS UNDERWENT WITH THIS HUGE PHYSICAL TENDERING FOR GOLD. WITH MUCH FAILURES

THE T.A.S. LIQUIDATION OF THESE T.AS. CONTRACTS CONTINUED THURSDAY AND FRIDAY, OCT 1 AND OCT 2 AND THAT IS THE REASON WHY WE ARE HAVING HUGE DISTORTED COMEX OPEN INTEREST LOSSES IN OI. HOWEVER THIS IS COUPLED WITH MEGA HUGE AMOUNTS OF GOLD STANDING FOR DELIVERY TO CONFUSE THE ISSUE!!!!! AND THIS WAS SURELY ON DISPLAY WITH FIRST DAY NOTICE/OCTOBER COMEX GOLD TOTALS WITH MASSIVE GOLD TONNES STANDING FOR GOLD IN OCTOBER AND THE HUGE QUEUE JUMPING THAT FOLLOWED!

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 7 MONTHS:

FOR APRIL AT 209 + TONNES

AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. (IS THE COMEX RUNNING OUT OF GOLD?)//TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 2.817 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

AND THIS NOW BRINGS US TO OCTOBER WHERE INITIAL AMOUNT OF GOLD STANDING IS 28,988 CONTRACTS FOR 90.114 TONNES OF GOLD TO WHICH WE ADD OUR FIRST MASSIVE QUEUE JUMP OF 4.898 TONNES QUEUE JUMP FOLLOWED BY OCT 4 QUEUE JUMP OF 0.9704 TONNES TO BE FOLLOWED BY OCT 7 QUEUE JUMP OF 3.623 TONNES AND FINALLY OCT 8’S HUGE 6.942 TONNES QUEUE JUMP AND FINALLY TODAY’S HUGE 4.979 TONNES OF QUEUE JUMP //// AND THIS WAS AUGMENTED BY AN UNUSUAL 50,000 CONTRACT EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE AND THEN ON THREE CONSECUTIVE OCCASIONS, OCT 2 THROUGH TO THE OCT 4.THEY TOOK ONE DAY OFF AND THEN ISSUED ITS 5 EXCHANGE FOR RISK ISSUANCE FOR 1000 CONTRACTS OR 100,000 OZ/3.1105 TONNES THE NEW TOTAL ON THESE 5 ISSUANCES IS 3650 CONTRACTS FOR 365,000 OZ OR 11.353 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERIES INCLUDING QUEUE JUMPS. NEW TOTALS FOR GOLD STANDING ADVANCES TO 123.129 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 30+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 243 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

SUMMARY OF GOLD QUEUE JUMPING AND EXCHANGE FOR RISK ISSUANCE: AUGUST THROUGH OCTOBER AND SUBSEQUENT STANDING FOR GOLD.

AUGUST: TOTAL QUEUE JUMPING AND TOTAL EXCHANGE FOR RISKS ISSUANCE FOR THE MONTH OF AUGUST; AND THUS STANDING:

WE HAD A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE TOTAL OF 47.2312 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES THEN AUGUST 12: 2.637 TONNES: AND NOW AUG 25: 9.107 TONNES ISSUANCE MONDAY’S MASSIVE 9.1016 TONNES ISSUANCE/AUGUST 25, AUGUST 26 9.0699 TONNES , YESTERDAYDAY’S (AUGUST 27) 9.0699 TONNES AND FINALLY TODAY’S TODAL OF 6.923 TONNESS/NEW STANDING ADVANCES TO 152.208 TONNES.

SEPTEMBER: TOTAL EXCHANGE FOR RISK AND QUEUE JUMPING; STANDING FOR GOLD

SUMMARY SEPT: 8.093 TONNES INITIALLY STANDING FOR GOLD // 7 ISSUANCES OF 22.923 TONNES OF EXCHANGE FOR RISK ISSUANCE/ SEPT MONTH AND THIS IS ADDED TO OUR NORMAL DELIVERY OF 25.878 TONNES

THAT IS;

A) //TOTAL FOR MONTH EXCHANGE FOR RISK/MONTH: 22.923 TONNES EX FOR RISK!!

B) //NORMAL DELIVERY OF 25.878 TONNES

TOTALS: 48.801 TONNES FINAL STANDING FOR GOLD/SEPT.

AND THIS BRINGS US TO OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 9: 4.979 TONNES OF QUEUE JUMP TO WHICH WE ADD OUR TOTAL 3,650 EXCHANGE FOR RISK CONTRACTS ON 5 OCCASIONS FOR 365,000 OZ OR 11.353 TONNES.! TOTAL STANDING ADVANCES TO 123.129

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

TOTAL EXCHANGE FOR RISK OCT 5 OCCASIONS: 11.353 TONNES

E) A MASSIVE QUEUE JUMP,OCT 3 OF 4.898 TONNES OF GOLD

F) STRONG QUEUE JUMP OCT 4: 0.9704 TONNES

G) A MASSIVE QUEUE JUMP OCT 7 OF 3.623 TONNES

H) A MASSIVE QUEUE JUMP OCT 8 FOR 6.942 TONNES

I) A MASSIVE QUEUE JUMP OCT 9 FOR 4.979 TONNES

EQUALS

123.129 TONNES OF GOLD!!

EXCHANGE FOR PHYSICAL ISSUANCE/OCT

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED EXCHANGE FOR PHYSICAL OF 4270 CONTRACTS.

THAT IS A STRONG SIZED 4270 EFP CONTRACT WAS ISSUED: : /DEC 4130 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4270 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON.

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//WEDNESDAY + GOVERNMENT LIQUIDATION

- MONTH END SPREADERS HAVE NOW FINISHED AS IT WAS IN FULL FORCE ON FIRST DAY NOTICE SEPT 30 WITH OUR ATTEMPTED FAILED RAID, FOLLOWED BY ANOTHER RAID OCT 2 AND THAT ENDED IN TOTAL FAILURE! , OCT 7 WE WITNESSED A SMALL RAID TRYING TO STOP GOLD’S ADVANCE TO THE 4000 BARRIER!! EARLY YESTERDAY MORNING THE BARRIER TO 4,000 DOLLAR GOLD WAS PIERCED!!

T.A.S.SPREADER ISSUANCE//OCT

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT/THURSDAY MORNING WAS A HUGE SIZED SIZED 5313 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST MONTH ON OPTIONS EXPIRY WEEK ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING; (AND MONTH END SPREADERS)

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S GAIN IN PRICE IN GOLD AND A CORRESPONDING STRONG GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS ESPECIALLY WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 5 ISSUANCES FOR 11.383 TONNES

- THE LONDON BANKING AUDITORS HAVE SO FAR REFUSED TO GIVE THE GREEN LIGHT ON THE BANK OF ENGLAND’S GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/

GOLD STANDING AT THE COMEX FOR GOLD LAST 9 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

AND NOW OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY;S 4.979 TONNES OF A QUEUE JUMP WHICH MUST BE ADDED TO OUR 5 ISSUANCES OF 11.353 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 123.129 TONNNES.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING OCT,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $68.60./ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE STRONG SIZED GAIN IN OI FROM TWO EXCHANGES OF 9,207 CONTRACTS.. BUT AS EXPLAINED ABOVE WE HAD ZERO T.A.S. SPREADER LIQUIDATION WEDNESDAY .THIS WAS COUPLED WITH GOVERNMENT LIQUIDATING THEIR CONTRACTS OUT OF SEVERE FEAR!!(PRELIMINARY NUMBERS LOWERED TO FINAL SHOWING MASSIVE LIQUIDATION). HOWEVER, ON TUESDAY, WE WITNESSED FOR NO REASON A MASSIVE LIQUIDATION IN PRICE OF OUR GOLD EQUITY SHARES LIKE AGNICO EAGLE AND BARRICK GOLD /// THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS. THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES NOW IN ORDER TO FORMALIZE RAIDS: OUR CROOKS TRIED AGAIN LATE WEDNESDAY-THURSDAY OCT 2 WITH CHINA OUT FOR A WEEK, WITH NOT MUCH LUCK. WITH CHINA COMING BACK TODAY, THURSDAY OCT 9 THE CROOKS NEEDED TO RAID TRYING DESPERATELY TO HALT GOLD’S ADVANCE. I GUESS THAT THEIR LUCK HAS RUN OUT WITH GOLD PIERCING THE 4000 DOLLAR BARRIER YESTERDAY EARLY MORNING.

THURSDAY MORNING//WEDNESDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/ THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

ANALYSIS OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT

WE HAVE A STRONG SIZED GAIN OF A TOTAL OF 23.63 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR OCT AT 90.164 TONNES TO BE FOLLOWED BY TODAY’S HUGE 4.979 TONNES OF QUEUE JUMP TO WHICH WE ADD OUR 11.353 TONNES EX FOR RISK/5 OCCASIONS:

/ NEW TOTAL STANDING 123.129 TONNES.

ALL OF THIS HUGE STANDING FOR OCTOBER WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $68.60

WE HAD A HUGE 2534 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET GAIN ON THE TWO EXCHANGES 9207 CONTRACTS OR 920,700 0Z (28.63 TONNES)

speculators have left the gold arena

INITIAL GOLD COMEX

OCT CONTRACT MONTH

OCT 9 /2025

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 3 entries i) Out of Brinks 113.836 oz ii) Out of HSBC 2000.20 oz iii) Out of Manfra 154,315.858 oz total withdrawal 156,835.744 oz . |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 0 ENTRIES xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 1653 notice(s) 165,300 OZ 5.1415 TONNES |

| No of oz to be served (notices) | 477 contracts 47,700 OZ 1.4836 TONNES |

| Total monthly oz gold served (contracts) so far this month | 35,459 notices 3,545,900 oz 110.292 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

customer withdrawal

3 entries

i) Out of Brinks 113.836 oz

ii) Out of HSBC 2000.20 oz

iii) Out of Manfra 154,315.858 oz

total withdrawal 156,835.744 oz

(.24 tonnes)

ADJUSTMENTs 4

all 4: dealer to customer

i)Asahi 32,168.314 oz

ii) Brinks 107,671.870 oz

iii) JPMorgan: 8077.257 oz

iv) Malca: 13,792.777 o

AMOUNT OF GOLD STANDING FOR OCTOBER

THE FRONT MONTH OF OCTOBER STANDS AT 2130 CONTRACTS FOR A LOSS OF 441 CONTRACTS.

WE HAD 2042 CONTRACTS FILED ON WEDNESDAY SO WE GAINED A MONSTROUS 1601 CONTRACT QUEUE JUMP FOR 160100 OZ OR 4.979 TONNES OF GOLD. THUS OUR NEW NORMAL DELIVERY RISES TO 111.776 TONNES WHICH INCLUDES ALL PREVIOUS QUEUE JUMPS) PLUS OUR 11.353 TONNES EX FOR RISK//NEW TOTAL STANDING FOR GOLD ADVANCES TO 123.129 TONNES

NOVEMBER LOST 177 CONTRACTS DOWN TO 4528 CONTRACTS.

DECEMBER GAINED 1624 CONTRACTS UP TO 390,959 CONTRACTS.

We had 1653 contracts filed for today representing 165,300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 1653 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 576 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for OCT /2025. contract month, we take the total number of notices filed so far for the month (35,459 oz ) to which we add the difference between the open interest for the front month of OCT ( 2130 CONTRACTS) minus the number of notices served upon today (1653 x 100 oz per contract) equals 3,593,600 OZ OR 111.776 TONNES OF GOLD TO WHICH WE ADD OUR 5 ISSUANCES OF 11.353 TONNES OF EXCHANGE FOR RISK //NEW TOTALS STANDING FOR GOLD OCTOBER ADVANCES TO 123.129 TONNES

thus the INITIAL standings for gold for the OCT contract month: No of notices filed so far (35,459 x 100 oz +we add the difference for front month of OCT. (2130 OI} minus the number of notices served upon today (1653 x 100 oz) which equals 3,593,600 OZ OR 111.776 TONNES + 11.353 TONNES EXCHANGE FOR RISK//NEW TOTAL OF GOLD STANDING IN OCTOBER ADVANCES TO 123.129 TONNES

TOTAL COMEX GOLD STANDING FOR OCT..: 123.129 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY SMALL ACTIVE ACTIVE DELIVERY MONTH OF OCT.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,952,857.469 oz 60.680 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 40,097.505.318 oz

TOTAL REGISTERED GOLD 21,812,144.110 or 678.449 tonnes

TOTAL OF ALL ELIGIBLE GOLD 18,285,361.208 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 1,985,928oz ((REG GOLD- PLEDGED GOLD)= 617.709 tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE OCT. 2025 SILVER CONTRACTS

OCT 10 2025

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 3 entries i) Asahi 532,168.314 oz ii) Brinks 873m357.110 oz iii) CNT 599,785.06 total withdrawal 2,059,649.570 oz |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | 1 entries 1 entries i) Into CNT 1002.00 oz |

| No of oz served today (contracts) | 89 CONTRACT(S) ( 0.445 MILLION OZ |

| No of oz to be served (notices) | 95 contracts (0.475 MILLION oz) |

| Total monthly oz silver served (contracts) | 3521 Contracts (17.605 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

1 entries

i) Into CNT 1002.00 oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

3entries

i) Asahi 532,168.314 oz

ii) Brinks 873m357.110 oz

iii) CNT 599,785.06

total withdrawal 2,059,649.570 oz

adjustments: 4 all dealer to customer

a) Brinks 1,883,186.05 oz

b) CNT 389,614.302 oz

c) Delaware 72,738.573 oz

d) Manfra 161,613.737 oz

TOTAL REGISTERED SILVER: 186.512 MILLION OZ//.TOTAL REG + ELIGIBLE. 528.182 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR OCT.

silver open interest data:

FRONT MONTH OF OCT /2025 OI: 184 OPEN INTEREST CONTRACTS FOR A LOSS OF 430 CONTRACTS.

WE HAD 519 CONTRACTS SERVED ON WEDNESDAY, SO WE GAINED 89 CONTRACTS WHICH UNDERWENT A HUGE QUEUE JUMP OF 0.445 MILLION OZ.

STANDING FOR SILVER OCT ADVANCES TO 18.080 MILLION OZ

NOVEMBER LOST 209 CONTRACTS DOWN TO 2179

DECEMBER LOST 628 CONTRACTS DOWN TO 127,757

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 519 or 2.595 MILLION oz

CONFIRMED volume; ON THURSDAY 109,813 huge//

AND NOW OCT. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in OCTOBER. we take the total number of notices filed for the month so far at 3521 X5,000 oz = 17.605 MILLION oz

to which we add the difference between the open interest for the front month of OCT (184) AND the number of notices served upon today (89 )x (5000 oz)

Thus the standings for silver for the OCTOBER 2025 contract month: (3521) Notices served so far) x 5000 oz + OI for the front month of OCTOBER(184) minus number of notices served upon today (89)x 5000 oz equals silver standing for the OCT.contract month equating to 18.080 MILLION OZ

New total standing: 18.080 million oz which is HUGE for this NON active delivery month of OCT. THE SILVER COMEX IS NOW UNDER SIEGE!!

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 186.512 million oz of registered silver

JPMorgan as a percentage of total silver: 209.936/528.182million. 39.73%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

OCT 9 WITH GOLD DOWN $91.45 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1014.58 TONNES

OCT 8 WITH GOLD UP $68.60 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 7 WITH GOLD UP $29.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 6 WITH GOLD UP $68.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1014.88 TONNES

OCT 3 WITH GOLD UP $38.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 2.86 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1015.74 TONNES

OCT 1 WITH GOLD UP $25.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 1.15 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1012.88TONNES

SEPT 30 WITH GOLD UP $18.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 6.01 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1011.73 TONNES

SEPT 29 WITH GOLD UP $48.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 8.87 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1005.72 TONNES

SEPT 26 WITH GOLD UP $38.40 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 25 WITH GOLD UP $5.70 TODAY/HUGECHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.82 TONNES OF GOLD FROM THE GLD/ . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 24 WITH GOLD DOWN $47.70 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1000.67 TONNES

SEPT 23 WITH GOLD UP $42.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 6/11 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 1001.67 TONNES

SEPT 22 WITH GOLD UP $68.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 14.61 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 994.56 TONNES

SEPT 19 WITH GOLD UP $26.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 18 WITH GOLD DOWN $37.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 975.66 TONNES

SEPT 17 WITH GOLD DOWN $8.30 TODAY/NO CHANGES IN GOLD AT THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 16 WITH GOLD UP $8.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 15 WITH GOLD UP $45.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 974.80 TONNES/

SEPT 12 WITH GOLD UP $12.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 977.95 TONNES/

SEPT 11 WITH GOLD DOWN $7.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD:/// ///INVENTORY RESTS AT 979.96 TONNES//

SEPT 10 WITH GOLD DOWN $1.10 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 9 WITH GOLD UP $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.29 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 8 WITH GOLD UP $41.40 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 5 WITH GOLD UP $47.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 2.29 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 4 WITH GOLD DOWN $22.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 6.30 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 984.26 TONNES//

SEPT 3 WITH GOLD UP $43.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 12.88 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 990.56 TONNES//FAIRY TALES

SEPT 2 WITH GOLD UP $79.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 9.74 TONNES OF GOLD VAPOUR INTO THE GLD// ///INVENTORY RESTS AT 977.68 TONNES

AUGUST 29 WITH GOLD UP $33.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 5.44 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 28 WITH GOLD UP $18.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 962.50 TONNES

AUGUST 27 WITH GOLD UP $12.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 959.92 TONNES

AUGUST 26 WITH GOLD UP $12.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD// ///INVENTORY RESTS AT 958.49 TONNES

AUGUST 25 WITH GOLD DOWN $1.05 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 956.77 TONNES

AUGUST 22 WITH GOLD UP $35.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 956.77 TONNES

GLD INVENTORY: 1014.58 TONNES, TONIGHTS TOTAL

SILVER

OCT 9 WITH SILVER DOWN $0.54 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 2.723 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 495.620 MILLION OZ

OCT 8 WITH SILVER UP $1.75 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 2.723 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 494.985 MILLION OZ

OCT 7 WITH SILVER DOWN $0.89 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 4.538 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 492.262 MILLION OZ

OCT 6 WITH SILVER UP $0.63 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 7.67 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 487.724 MILLION OZ

OCT 3 WITH SILVER UP $1.43 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 8.893 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.394 MILLION OZ

OCT 1 WITH SILVER UP $1.09 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.264 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 504.287 MILLION OZ

SEPT 30 WITH SILVER DOWN $0.34 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.129 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 499.023 MILLION OZ/

SEPT 29 WITH SILVER UP $0.37 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.908 MILLION OZ OF SILVER DEPOSITED OUT OF THE COMEX/: /// ///INVENTORY RESTS AT 493.894 MILLION OZ//

SEPT 26 WITH SILVER UP $1.58 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL DEPOSIT OF 0.681 MILLION OZ OF SILVER DEPOSITED INTOTHE COMEX/: /// ///INVENTORY RESTS AT 494.802 MILLION OZ//

SEPT 25 WITH SILVER UP $1.44 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE WITHDRAWAL OF 3.222 MILLION OZ OF SILVER OUT OF THE COMEX THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 24 WITH SILVER DOWN $0.48 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 3.222 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 497.343 MILLION OZ//

SEPT 23 WITH SILVER UP $0.32 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 5.265 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 22 WITH SILVER UP $1.16 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 19 WITH SILVER UP $0.89 TODAY/HUGE CHANGES IN SILVER A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 18 WITH SILVER DOWN $0.69 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 17 WITH SILVER DOWN $0.03 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.088 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 489.265 MILLION OZ//

SEPT 16 WITH SILVER DOWN $0.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.500 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 487.177 MILLION OZ//

SEPT 15 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 12 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 11 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 10 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ //

SEPT 9 WITH SILVER DOWN $0.55/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.816 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 486.677 MILLION OZ./

SEPT 8 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 488.493 MILLION OZ./

SEPT 5 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 489.674 MILLION OZ./

SEPT 4 WITH SILVER DOWN $0.68/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 491.308 MILLION OZ./

SEPT 3 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT DEPOSIT OF 1,816 MILLION OZ INTO THE SLV:// ////INVENTORY RESTS AT 494.043 MILLION OZ./

SEPT 2 WITH SILVER UP $0.95/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF .727 MILLION OZ FROM THE SLV:// ////INVENTORY RESTS AT 492.227 MILLION OZ./

AUGUST 29 WITH SILVER UP $0.80/ HUGE CHANGES AT THE SLV AT DEPOSIT 0F 1.862 MILLION OZ:// ////INVENTORY RESTS AT 492.954 MILLION OZ./

AUGUST 28 WITH SILVER UP $0.48/ NO CHANGES AT THE SLV:// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 27 WITH SILVER UP $0.04/ SMALL CHANGES AT THE SLV: A WITHDRAWAL OF 454,000 OZ FORM THE SLV// ////INVENTORY RESTS AT 491.092 MILLION OZ./

AUGUST 26 WITH SILVER DOWN $0.19/ NO CHANGES AT THE SLV: // ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 25 WITH SILVER DOWN $0.28/ SMALL CHANGES AT THE SLV: A SMALL DEPOSIT OF 0.363 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.546 MILLION OZ./

AUGUST 22 WITH SILVER UP $0.92/ SMALL CHANGES AT THE SLV: A SMALL WITHDRAWL OF 0.908 MILLION OZ OF SILVER LEAVES THE SLV// ////INVENTORY RESTS AT 491.183 MILLION OZ./

CLOSING INVENTORY 494.985 MILLION OZ//

PHYSICAL GOLD/SILVE

1/PETER SCHIFF

Libertarian Vs. MAGA: Trump’s Economic Nationalism Reveals Fault-Lines

Thursday, Oct 09, 2025 – 10:25 AM

On September 19, President Trump issued a proclamation imposing a $100,000 one-time fee on new H-1B visa petitions.

He’s also pressing for equity stakes for the federal government in strategic U.S. firms—such as a reported bid for up to 10% ownership of Lithium Americas tied to its DOE loan deals. And the administration already holds stakes in Intel, MP Materials, and others, shifting grants and subsidies toward direct ownership.

The moves have brought an ideological divide on the right to the surface. Namely between the libertarians, capitalists, “free market” guys and MAGA, nationalist, America First camps.

ZeroHedge is putting it on trial, tonight.

Tonight at 7 pm ET, live on the ZeroHedge homepage, X, YouTube, and Rumble:

Peter Schiff vs. Spencer P. Morrison and moderated by Keith Knight.

Topic: Do Trump’s worker-first policies save America—or destroy it?

Peter Schiff has warned broadly about the GOP shift toward protectionism:

On the H-1B surcharge, Schiff argues it may backfire:

Morrison, by contrast, insists the $100K H-1B “fee” is far too weak to protect American labor and was ticked off by Trump/Lutnick’s reversal from it being an annual fee to one-time:

Tune in at 7 pm ET on ZeroHedge / X / YouTube / Rumble. It will subsequently be posted to our Spotify.

JOHN RUBINO

JAMES RICKARDS

2. MATHEW PIEPENBERG/VON GREYERZ

ALASDAIR MACLEOD…

Commodities are massively undervalued

If gold is worth $4k+, where does that leave the entire commodity complex? Answer: they are at their most undervalued since records began!

| Alasdair MacleodOct 9∙Paid |

Our byline heading this article is meant to be provocative, but nevertheless it is broadly true. Its basis is that we know that over long periods of time, a basket of commodities valued in gold is relatively constant. Individual components can vary considerably, even dropping out of a statistical basket or being added to it. The reason for this stability is the constancy of gold’s purchasing power over time.

However, we tend to value commodities in currency, usually the dollars in which they are all priced internationally. This conceals what’s happening to commodity values, because the dollar’s purchasing power has declined since it became completely detached from gold in 1971. To illustrate this point, the chart below shows how a basket of base metals has risen valued in dollars over a long period of time, while being relatively constant in gold:

If you were unaware of the decline in the dollar’s purchasing power, you would think that metal prices have risen thirty-fold since 1900. But as the chart shows, prices in dollars only began to rise relative to prices in gold when the dollar was devalued in 1934, and again at the end of the Bretton Woods agreement in 1971.

Clearly, the price problem is the dollar’s declining value over time. But since everything is priced in dollars, we naturally think that all price volatility is in the commodities. Pricing energy, softs, and agricultural produce in dollars tells the same story, while in gold these values are at all-time lows. The next chart shows the metal basket in our first chart priced in gold only to illustrate the point:

Price distortions at the times of the two world wars need no further explanation. Metals prices between 1950-1970 rose in gold terms partly due to the post-war boom in demand, but also because of the Bretton Woods tie to the dollar, which was being debased in the post-war decades, dragged gold down with it. That is why it failed, firstly with the gold pool debacle in the late ‘sixties, and then when Bretton Woods was suspended in August 1971.

Most of the distortions to commodity values in gold over the 1981—2008 period was due to US attempts to remove credibility from gold as money. The failure of this policy is explained by the fact that even priced in gold, commodity prices remained broadly not too far from their long-term average.

From thereon, the expansion of dollar debt, or put another way its quantitative debasement accelerated. Initially, it was the financial crisis of 2008—2009 which led to soaring commodity dollar prices. It was a case of markets thinking of values solely in dollars, leading to a suppression of their values in gold. And then there were the covid lockdowns in 2020 leading to a new round of dollar debasement.

Since 2008, in real terms, that is measured in gold, base metals have become increasingly suppressed. At only 20% of its long-term value in gold, this basket of base metals is now at its lowest level in 125 years by far. This is an aberration of which markets are as yet unaware. But if base metals are so dramatically undervalued in gold, their future value in declining dollars is bound to soar as their undervaluation corrects.

Therefore, in debasing dollars commodity prices will drive consumer inflation significantly higher over the next two or three years — it is inevitable. Consequently, bond yields which reflect a fiat currency’s future purchasing power are bound to rise substantially. This is at odds with investors’ expectations of lower dollar interest rates by the year-end. But the long-term downtrend from 1980—2020 has been broken, confirming the outlook for higher bond yields.

With gold having risen to over $4000, only now are expectations of lower interest rates being challenged. Unless short-term rates are raised to compensate for the dollar’s decline, the decline will simply accelerate even more. But if the Fed raises interest rates, the Federal government and overindebted parties in the private sector will face insolvency with widespread bankruptcy.

The dilemma cannot be reconciled. We are at an end of the fiat currency era, with its whole edifice about to crumble.

3. CHRIS POWELL AND GATA GOLD DISPATCHES/OTHER GOLD RELATED TOPICS

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS 243/

END

5. COMMODITY REPORT/SILVER

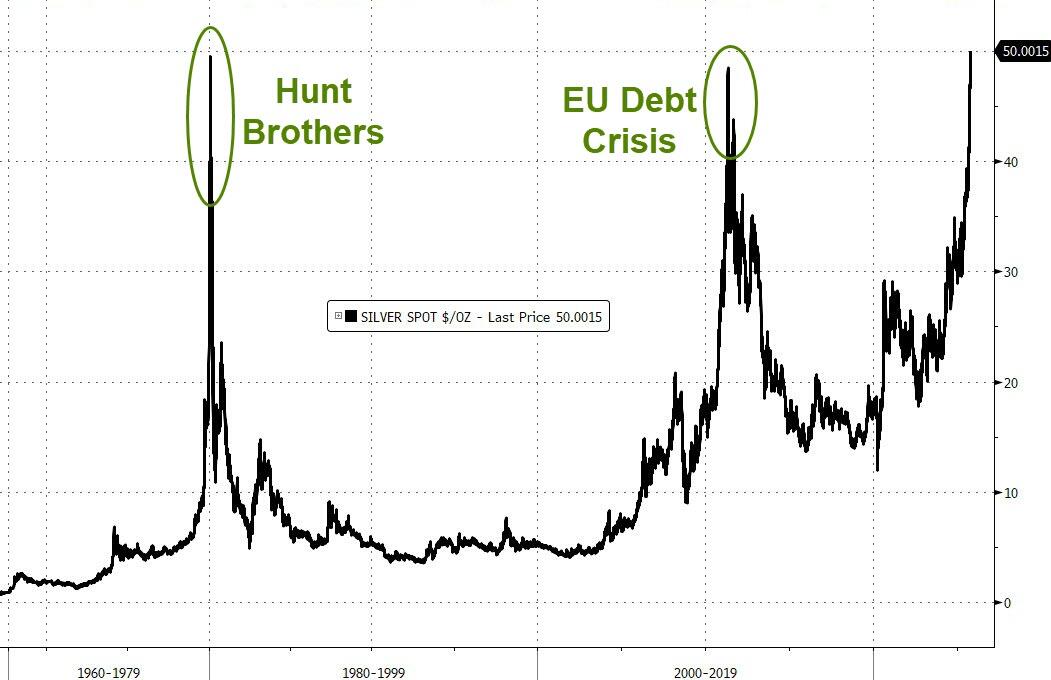

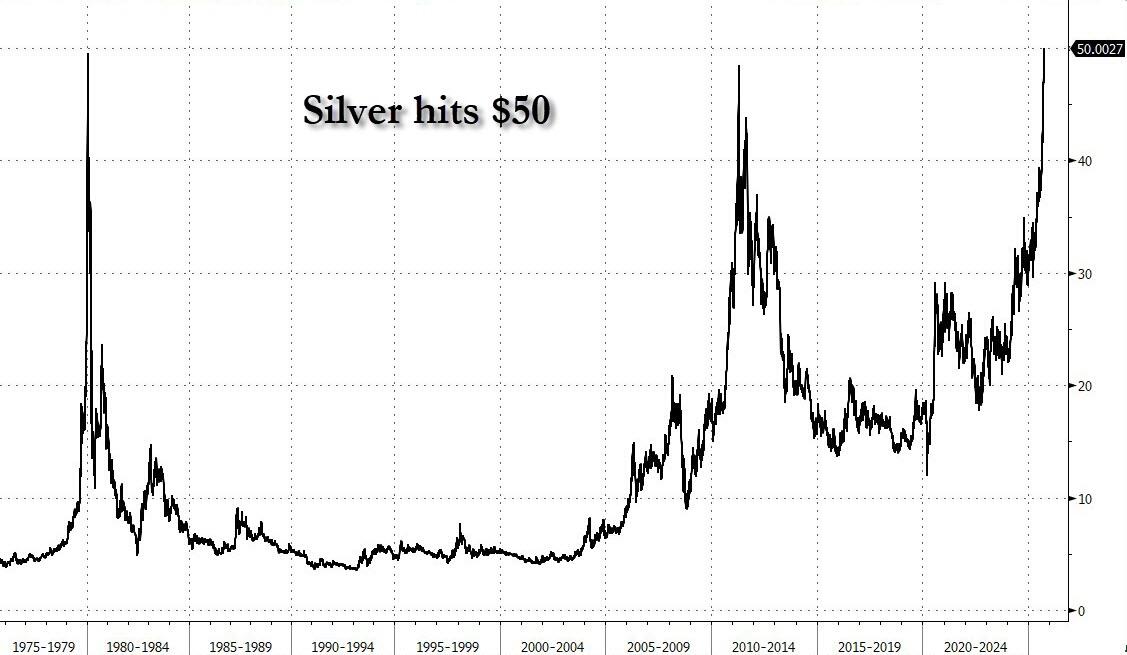

‘Debasement Trade’ Lifts Silver Above $50 For First Time Since 80s’ Hunt Brothers Squeeze

Thursday, Oct 09, 2025 – 09:05 AM

The last few months have seen gold soar to record highs above $4,000 amid the so-called “debasement trade,” with investors flocking to the perceived safety of alternates while pulling away from major currencies.

It’s a monetary regime change – if market participants are trading anything it’s getting rid of a fiat currency (“it’s the denominator, stupid”) for a store of value – and we’re seeing it in spades with Bitcoin and gold:

However, quietly on the side, silver has been outperforming gold…

Source: Bloomberg

Citadel’s Ken Griffin said investors are starting to view gold as a safer asset than the dollar, a development that’s “really concerning” to the billionaire investor.

“The conversation around debasement, irrespective of its realities, has ignited investors enthusiasm towards gold and silver to the point where regression analysis gives way to something more akin to how investors view AI or the technology sector,” said Kieron Hodgson, commodity analyst at Peel Hunt Ltd.

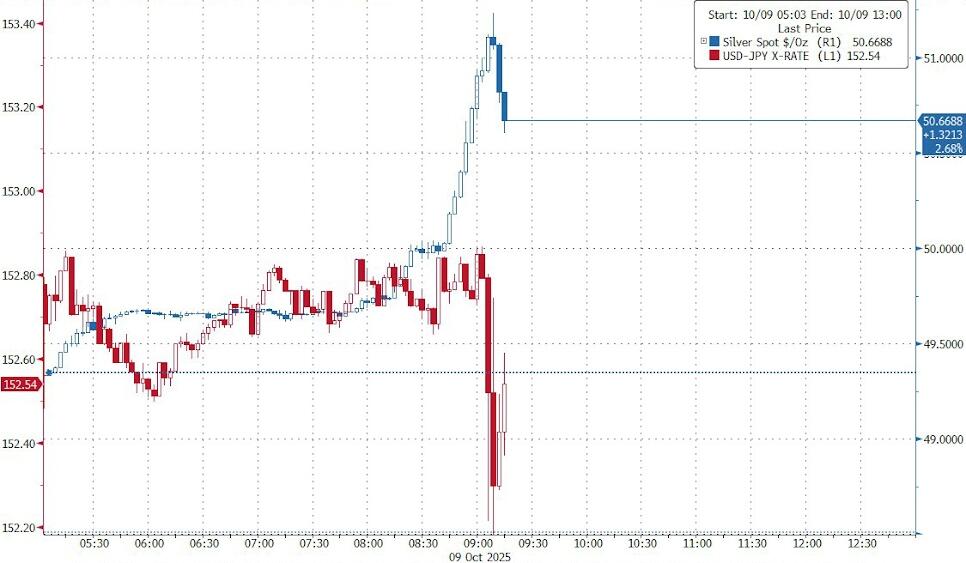

And now that is spreading to bitcoin and silver as the white metal topped $50 this morning…

Silver’s surge takes it back to the highs from 1980…

…when the Hunt brothers, Texan oil billionaires and notorious speculators, whose fear of inflation and belief in the metal as a store of wealth prompted them to try to corner the global market. They stockpiled more than 200 million ounces, driving the price above $50 an ounce before it crashed below $11.

Notably, Yen accelerated its weakness when silver broke through $50…

Something’s going on there…

The white metal is used around the world as an investment asset, but also has industrial applications including in solar panels and wind turbines, which collectively account for more than half of the silver sold. Demand is set to exceed supply for the fifth consecutive year in 2025.

“I think the deficits are the slow burn,” said Philip Newman, director of consultancy Metals Focus Ltd.

“Just the size of the deficits have been so remarkable, and it takes time for that to manifest itself in the price.”

Additionally, Bloomberg reports that the silver market in London has tightened to an almost unprecedented degree, with sky-high borrowing costs for the metal.

This year, fears that the US could levy tariffs on silver have spurred a dash to ship the metal to the US, drawing down inventories in London and reducing the amount of material available to borrow.

Much of the stock of silver in London is held in vaults backing exchange-traded funds, and not available to buy or borrow on the market.

“I think when you look at above-ground stocks of silver in London you are looking at an increasingly small share, which is not allocated against ETFs,” Newman said.

As we detailed earlier in the week, it appears the so-called “debasement trade” – driving investors to bet more on gold, silver, and bitcoin – is set to continue with Gold remaining Goldman Sachs’ highest-conviction long commodity recommendation because of the:

a. Additional price upside in our base case (driven by structurally higher central bank gold demand)

b. Large upside risks to our price forecast from potential additional private sector diversification

c. Attractive portfolio hedging properties in downside (tail) scenarios that .are less favorable for equity-bond portfolios than our base case (e.g. global growth slowdown, rising market concerns about DM macro policy)

This price hike is likely to trigger more fears from Citadel’s Griffin who warned, during and interview with Bloomberg’s Francine Lacqua, that “we’re seeing substantial asset inflation away from the dollar as people are looking for ways to effectively de-dollarize, or de-risk their portfolios vis-a-vis US sovereign risk.”

END

SILVER THIS MORNING:

SPECIAL THANKS TO g. FOR UPDATING US ON THIS

AND NOW SILVER LEASE RATES ABOVE 19%

Silver Lease Rate Now At Extreme 19%, London’s Silver Shortage Drives Silver Over $50 /oz Increasing Panic For MetalDavid JensenOct 9 |

ASIAN MARKETS THIS THURSDAY MORNING:

SHANGHAI CLOSED UP 51.20 POINTS OR 1.32%

//Hang Seng CLOSED CLOSED DOWN 76.87 PTS OR 0.29%

// Nikkei CLOSED : UP 845.45 PTS OR 1.77% //Australia’s all ordinaries CLOSED UP 0.34%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.1231// OFFSHORE CLOSED UP AT 7.1296/ Oil UP TO 62.31 dollars per barrel for WTI and BRENT UP TO 66.03 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING UP TO 7.1231 // OFFSHORE YUAN TRADING UP TO 7.1296 :/ONSHORE YUAN TRADING ABOVE OFF SHORE A 71231/ AND THUS STRONGER/OFF SHORE YUAN TRADING UP TO 7.1296 AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.1231

OFFSHORE YUAN: UP TO 7.1296

HANG SENG CLOSED DOWN 76.87 PTS OR 0.29%

2. Nikkei closed UP 845.45 PTS OR 1.79%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 98.61 EURO FALLS TO 1.1627 DOWN 2 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.6920//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 152.55…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA. JAPAN 30 YR BOND YIELD: 3.193 UP 4 BASIS PTS.

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR UP this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.6980// Italian 10 Yr bond yield DOWN to 3.511 SPAIN 10 YR BOND YIELD DOWN TO 3.226

3i Greek 10 year bond yield UP TO 3.369

3j Gold at $4038.00 Silver at: 49.64 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 24 /100 roubles/dollar; ROUBLE AT 81.26

3m oil (WTI) into the 62 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 152.55/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.692% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.//JAPAN 30 YR: 3.193 UP 4 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8007 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9369 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.132 DOWN 0 BASIS PTS…

USA 30 YR BOND YIELD: 4.717 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.589 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 41.72 UP 1 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.7290 UP 1 PTS BUT STILL ESCALATING RAPIDLY

30 YR UK BOND YIELD: 5.524 UP 1 BASIS PTS

10 YR CANADA BOND YIELD: 3.193 UP 1 BASIS PTS

5 YR CANADA BOND YIELD: 2.742 UP 1 BASIS PTS.

2a New York OPENING REPORT

Futures Flat At All Time High, As Silver Tops $50

Thursday, Oct 09, 2025 – 09:06 AM

US equity futures are flat, as the main indexes closed at fresh record highs overnight amid a melt-up that shows no signs of abating, with every small dip being bought and volatility staying low. While plenty of investors have doubts about the AI-driven rally and the tense geopolitical backdrop, the year-end FOMO is the only driver for now. As of 8:30am, S&P futures are flat, while Nasdaq futures trade fractionally in the red, although we are confident the dip-buying algos will promptly pounce on the opportunity. In premarket trading, Delta Air Lines climbed more than 5% after reporting profits that beat estimates. PepsiCo gained on stronger-than-expected revenue and flagged a turnaround at its US beverage unit. Nvidia rose after the US approved several billion dollars worth of its chip exports to the United Arab Emirates. Shares of other Mag 7 names were mixed. Bond yields are higher by 1-2bp across the curve ahead of today’s 30Y auction, with USD flat following a 1.2% move WTD. Ahead of Trump / Xi meeting later this month China expanded its rare earths curbs. In commodities, Energy is mixed with distillates higher and crude/natgas lower. Oil slipped and gold stalled near a record high above $4,000 as traders focused on cooling tensions in the Middle East; Silver topped $50 for the first time and PGMs are stronger. Today’s session has seven Fed speakers and a 30Y bond auction; yesterday’s 10Y auction required a concession. Macro data is delayed again due to the government shutdown.

In premarket trading, Mag 7 stocks are mixed (Microsoft little changed, Alphabet -0.2%, Meta little changed, Apple -0.1%, Amazon -0.2%)

- Tesla (TSLA) falls 1.1% as US auto safety regulators opened a probe into the company over incidents in which its vehicles ran through red lights and violated other traffic laws while using the driver-assistance system known as Full Self-Driving.

- Nvidia (NVDA) rises 1.7% after the US approved several billion dollars worth of Nvidia chip exports to the UAE, an initial step in implementing a controversial deal that could serve as a blueprint for American AI statecraft. Separately Cantor Fitzgerald raised its price target to a Street-high, seeing more growth potential for the chipmaker on the back of AI-related growth.

- Rare earth stocks climb after China unveiled new restrictions on exports ahead of a meeting this month between Donald Trump and Xi Jinping.

- Akero Therapeutics (AKRO) jumps 18% after Novo Nordisk agreed to buy the drug developer for $54 per share in cash at closing, with a contingent value right of $6 per share

- Apogee Therapeutics (APGE) is down 6% after the company offered shares.

- AZZ Inc. (AZZ) falls 7% after the provider of metal-finishing services reported second-quarter sales that missed estimates.

- Costco (COST) is up 1% after the warehouse club reported comparable sales growth that beat analyst estimates for September, helped by a rise in both foot traffic and amount spent per customer.

- Delta Air (DAL) climbs 6% after the carrier updated its adjusted earnings per share forecast for the full year, with the new guidance beating the average analyst estimate.

In corporate news, Warner Music Group is said to be close to an agreement with Netflix to create a slate of movies and documentaries based on the label’s artists and songs. Jefferies has come under scrutiny for its relationship with First Brands.

As we said yesterday, and the day before, and the day before that, and so on, stocks around the world have soared to a fresh record as traders looked past worries of a potential bubble in high-profile tech names and instead focused on corporate resilience and the possibility of further US interest-rate cuts. The optimism now faces another test as earnings season gets underway, with Wall Street banks Goldman Sachs and Citigroup due to report next week. Tesla is the first of the Magnificent Seven set to report on Oct. 22, followed by Alphabet, Microsoft and Meta Platforms Inc. on October 29.

“A liquidity glut and the AI boom keep the party going for equities,” said Barclays strategist Emmanuel Cau. Still, the reluctant bulls driving the rally have plenty of lingering worries, such as Nassim Taleb’s warning that investors should insure against a stock-market crash due to structural issues such as the US debt burden.

“Given how lopsided the expectations have become, given how lofty the valuations have become, I think investors are laser focused on earnings,” Aidan Yao, a strategist at Amundi Investment Institute, said on Bloomberg TV. “They are trying to see if earnings are really catching up into the valuations.”

Elsewhere, the Fed minutes revealed that many members have expressed caution — driven by concerns over percolating US inflation. And traders have been slowly backing away from bets on the trajectory of rate cuts. Gold is taking a breather from its record run, while silver just topped $50 for the first time

In geopolitical news, Trump said Israel and Hamas have signed off on the first phase of a peace plan. A ceasefire in Gaza has gone into effect, Israel Deputy Foreign Affairs Minister Sharren Haskel said subsequently. If the agreement holds, it would mark a major step toward ending the conflict that erupted after Hamas attacked Israel on Oct. 7, 2023 and threw the Middle East region into crisis. Canadian PM Mark Carney pushed back against Trump’s protectionism in the auto industry, saying that the US-Mexico-Canada Agreement strengthens the US industry. China unveiled broad new curbs on its rare earth exports.

European stocks are mixed. The CAC 40 adds 0.3% while the DAX climbs to a fresh record. The FTSE 100 falls 0.4% as HSBC shares slump after the bank proposed taking its Hong Kong subsidiary private. Here are some of the biggest European movers today:

- HelloFresh shares surge as much as 11% as UBS upgrades to buy from neutral and says the firm offers a “compelling risk-reward”

- Sodexo shares advance as much as 3.5% after the food services company announced that Sophie Bellon will step down as CEO

- Suedzucker shares rise as much as 1.8% after analysts at Warburg said the drop in earnings during the first half is not a major surprise

- Volution shares rise as much as 10%, hitting an all-time high, after the firm delivered annual results that were ahead of expectations

- MTG shares gain as much as 11% after it updated its full-year 2025 guidance and announced a SEK400 million share buyback program

- Mobilezone shares rally as much as 12% after agreeing to sell its German business to Freenet

- Polar Capital shares rise as much as 5.9% as assets under management grow 15% in the three months to the end of September

- Emmi shares gain as much as 4.8% as Oddo BHF starts coverage of the Swiss dairy producer with an outperform recommendation

- Lloyds Banking Group shares drop as much as 3.9% after the lender said it will likely have to set aside an additional provision to compensate customers who were missold car loans

- Michelin shares drop as much as 6.5% following a pre-close call ahead of its 3Q sales update scheduled for Oct. 22

- Gerresheimer shares drop as much as 14% after the company cut its outlook for the year yet again

- Sopra Steria shares fall as much as 5.6% after its CEO Cyril Malargé decided to step down

Earlier in the session, Asian stocks rose, as an AI-fueled tech rally resumed following a brief pause and shares in mainland China gained as the market reopened after the Golden Week holidays. The MSCI Asia Pacific Index rose as much as 0.6%, poised for its first gain in three sessions. A sub-gauge of tech shares was the top performer among sectors, rebounding from Wednesday’s declines. It had risen for seven straight days before that. TSMC was the biggest boost to the MSCI Asia measure after a US index of chip stocks jumped to a fresh all-time high on AI euphoria. China’s CSI 300 Index advanced 1.5% to its highest since January 2022 as investors got up to speed on headlines from OpenAI deals to gold’s climb above $4,000. Benchmarks in Japan and Taiwan climbed to fresh records.

In FX, the Bloomberg Dollar Spot Index is flat, in early London trade it pushed up to its highest level since Aug. 5. EUR/USD was slighly lower at 1.1623; its selloff has slowed as French President Emmanuel Macron is set to name a new prime minister by Friday evening, avoiding the need to call a snap election for the time being. USD/JPY steadies around an eight-month high of 153.22; investors contemplate how much the Japanese currency must weaken before authorities intervene again

In rates, treasury yields are within a basis point of Wednesday’s closing levels following similarly rangebound price action in core European bonds. Focal points of US session include 30-year bond reopening, last of three coupon auctions this week. Fed Chair Powell delivers pre-recorded welcoming remarks at its community bank conference at 8:30am New York time, with text release expected. US 10-year, little changed near 4.12%, trades marginally cheaper vs German and UK counterparts; curve spreads are marginally flatter on the day. $22 billion 30-year bond reopening at 1pm New York time follows Wednesday’s middling 10-year note auction, which tailed by 0.8bp. WI 30-year yield near 4.7% is ~5bp cheaper than last month’s, which stopped on the screws.

The Bloomberg Dollar Spot Index . Spot gold loses a few dollars but remains firmly above $4,000/oz.

In commodities, oil slipped and gold stalled near a record high above $4,000 as traders focused on cooling tensions in the Middle East. Israeli markets staged a broad rally, sending the shekel to a three-year high. The Tel Aviv Stock Exchange 35 Index added 1.7%, notching a fresh all-time high, while bond yields fell across the board. WTI crude futures fall 0.2% to $62.40 a barrel. Bitcoin falls 1%.

Looking at today’s calendar, wholesale trade/inventories for August are scheduled for 10 am ET, but govt. data releases are likely to be impacted by the shutdown. Fed’s Bowman, Goolsbee, Barr, Kashkari and Daly are scheduled to speak and Fed Chair Powell gives pre-recorded remarks at Fed community bank conference.

Market Snapshot

- S&P 500 mini little changed

- Nasdaq 100 mini little changed

- Russell 2000 mini -0.3%

- Stoxx Europe 600 -0.2%

- DAX +0.3%

- CAC 40 +0.2%

- 10-year Treasury yield +1 basis point at 4.13%

- VIX +0.1 points at 16.41

- Bloomberg Dollar Index little changed at 1210.88

- euro little changed at $1.1619

- WTI crude +0.3% at $62.72/barrel

Top Overnight News

- Israel and Hamas agreed on terms for the exchange of all hostages held in Gaza for about 2,000 jailed Palestinians. Donald Trump told Fox he expects the hostages to be released “probably” on Monday. A Gaza ceasefire is in effect, Israel’s deputy foreign affairs minister said. A Gaza ceasefire is in effect, Israel’s deputy foreign affairs minister said. BBG