access market

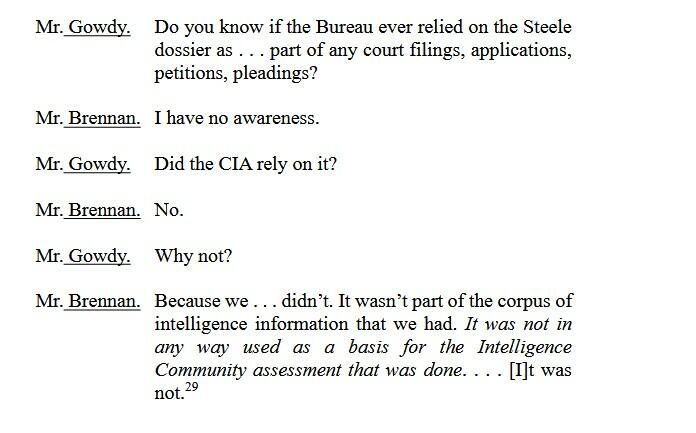

SILVER: 52.43 (3:30 PM)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: OCTOBER 2025 COMEX 100 GOLD FUTURES

SETTLEMENT: 4,336.400000000 USD

INTENT DATE: 10/20/2025 DELIVERY DATE: 10/22/2025

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DEUTSCHE BANK AG 154

118 C MACQUARIE FUTURES US 247

190 H BMO CAPITAL MARKETS 2

299 C TRADESTATION SEC INC 1

323 C HSBC 509

435 H SCOTIA CAPITAL (USA) 339

657 H MORGAN STANLEY 618

709 C BARCLAYS 1140

737 C ADVANTAGE FUTURES 28 1

878 C PHILLIP CAPITAL INC 1

905 C ADM 22

TOTAL: 1,531 1,531

MONTH TO DATE: 55,075

GOLD: NUMBER OF NOTICES FILED FOR OCT/2025: 1531 CONTRACTs NOTICES FOR 153,100 OZ or 4.7620 TONNES

total notices so far: 55,075 contracts for 5,507,500 OR 171.306 tonnes)

SILVER NOTICES: 480 NOTICE(S) FILED FOR 2.4 MILLION OZ/

total number of notices filed so far this month : 6934 CONTRACTS (NOTICES) for 34.670 million oz

INITIAL STANDING FOR OCT: 34.680 MILLION OZ (WHICH INCLUDES ALL QUEUE JUMPING)

+ 2.110 MILLION OZ EXCHANGE FOR RISK

EQUALS

36.790 MILLION OZ..

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 69.490 MILLION OZ (WILL BE HUGE THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

AND NOW OCTOBER: 32.405 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 34.515 MILLION OZ

AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

AND NOW OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S HUGE 3.860 TONNES QUEUE JUMP + YESTERDAY’S HUGE 7.695 TONNES OF QUEUE JUMP WHICH FOLLOWED FRIDAY’S RECORD SETTING, 12.031 TONNES QUEUE JUMP TO WHICH WE ADD: 8.326 TONNES QUEUE JUMP/WEDNESDAY// WHICH FOLLOWED TUESDAY’S RECORD SETTING MONSTER 9.564 TONNES QUEUE JUMP AND WHICH WAS PRECEDED BY 42.549 TONNES QUEUE JUMPING FOR OCT. THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 186.531 TONNES OF GOLD.

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 167/167 TONNES//CERTAINLY MUCH LARGER THIS MONTH

SPREADING OPERATIONS

NOW SWITCHING TO GOLD FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA MEGA SIZED 3,785 CONTRACTS OI TO 172,283 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE A SMALL 136 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 136 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 136 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3785 CONTRACTS AND ADD TO THE SMALL 136 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF 3642 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR LOSS OF $2.85 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 18.23 MILLION PAPER OZ

OCCURRED WITH OUR GAIN IN PRICE.OF $0.94

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENT

Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED UP 52.44 POINTS OR 1.36%

//Hang Seng CLOSED CLOSED UP 168.72 PTS OR 0.65%

// Nikkei CLOSED : UP 130.36 PTS OR 0.27% //Australia’s all ordinaries CLOSED UP 0.70%

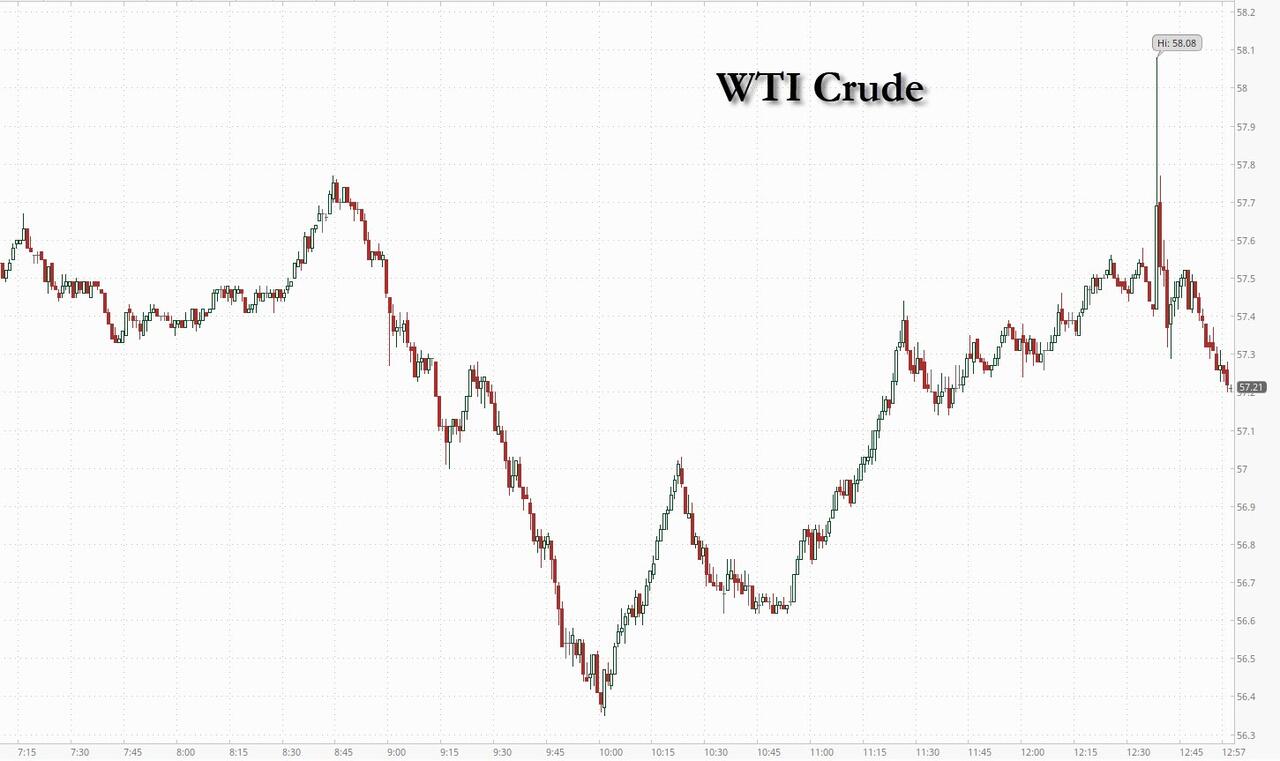

//Chinese yuan (ONSHORE) CLOSED UP TO 7.1191// OFFSHORE CLOSED UP AT 7.1198/ Oil UP TO 58.02 dollars per barrel for WTI and BRENT UP TO 61.82 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING UP TO 7.1191 // OFFSHORE YUAN TRADING UP TO 7.1198 :/ONSHORE YUAN TRADING ABOVE OFF SHORE / AND THUS STRONGER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST SHOCKINGLY FELL BY A STRONG 4033 CONTRACTS TO 475,938 OI DESPITE OUR HUGE GAIN IN PRICE OF $137.70 WITH RESPECT TO MONDAY’S AND THAT MAKES NO SENSE AT ALL // TRADING/ //COMEX CLOSING TIME:… WE LOST ZERO NET LONGS, DESPITE THAT HUGE PRICE GAIN FOR GOLD. AND AS YOU WILL SEE BELOW, OUR GAIN IN PRICE ALSO HAD A FAIR NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (1621). WE MUST HAVE HAD HUGE T.A.S. LIQUIDATION MONDAY. WE HAD A TOTAL LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 2412 CONTRACTS (OR 7.502 TONNES).THEN WE WERE NOTIFIED OF A 1029 CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS ISSUED FOR 102,900 OZ OR 3.200 TONNES OF GOLD.

EXCHANGE FOR PHYSICAL//GOLD ISSUANCE//OCTOBER:

THUS THE TOTAL NUMBER OF CONTRACTS EXCHANGE FOR RISK ISSUED FOR THE MONTH OF OCT FOR GOLD RISES TO 14.553 TONNES OF GOLD UNDER THE GUIDANCE OF 6 ISSUANCES.

A LITTLE HISTORY ON OUR EXCHANGE FOR RISK ISSUANCES/ GOLD:

HERE IS A CLOSER LOOK AT EXCHANGE FOR RISK ISSUANCES FOR THESE PAST 4 MONTHS;

(TOTAL EXCHANGE FOR RISK LAST 4 MONTHS 70.097 TONNES//BANK OF ENGLAND TOTAL RESERVES LISTED AT 310 TONNES.)

JULY:

SUMMARY: EXCHANGE FOR RISK ISSUANCE IN JULY/2025: 2 ISSUANCES//3.75 TONNES

ON WEDNESDAY MORNING,JULY 23, MUCH TO MY SHOCK, AFTER A TWO MONTH HIATUS,THE CME ANNOUNCED A 500 EXCHANGE FOR RISK CONTRACT ISSUANCE FOR 50,000 OZ OR 1.555 TONNES. THEN JULY 30 THE CME ANNOUNCED (ISSUED) MUCH TO MY HORROR ITS SECOND EXCHANGE FOR RISK FOR 706 CONTRACTS OR 70,600 OZ (2.195 TONNES) AS THE BANK OF ENGLAND WAS NOT SATISFIED AND NEEDS MORE GOLD TO COVER ITS LEASES TO BULLION BANKS. ( IT WAS NOT THE FRBNY WHO ALSO OWES GOLD TO THE BIS AND THEY NEED TO COVER BADLY AS YOU WILL SEE).THE TOTAL EXCHANGE FOR RISK FOR THE MONTH OF JULY WAS RECORDED AT 3.750 TONNES OF GOLD WHICH WAS ADDED TO OUR REGULAR DELIVERY TO GIVE US OUR FINAL TOTALS FOR JULY!

AUGUST:

SUMMARY EXCHANGE FOR RISK ISSUANCE IN AUGUST; 7 ISSUANCES//44.696 TONNES

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES). EARLY IN THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW AN ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPT:

SEPTEMBER: SEVEN ISSUANCES SO FAR TOTALLING 7,370 CONTRACTS OR 737,000 OZ OR 22.923 TONNES.

THESE ISSUANCES WILL OF COURSE BE ADDED TO OUR NORMAL DELIVERIES TO GIVE US OUR TOTAL SEPT STANDING FOR GOLD.

AND NOW OCTOBER: 6 ISSUANCES

WE RECEIVED NOTICE THAT OUR INITIAL EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE WAS FOR 500 CONTRACTS OR 50,000 OZ /1.555 TONNES OF GOLD!!THAT WAS FOLLOWED BY A STRONG 650 CONTRACT ISSUED THURSDAY OCT 2 FOR 2.0217 TONNES AND THAT WAS FOLLOWED THE NEXT DAY BY ANOTHER HUGE 1320 CONTRACT ISSUANCE FOR 13,200 OZ OR 4.1057 TONNES AND THIS WAS FOLLOWED BY SATURDAY’S OCT 4: 180 CONTRACT ISSUANCE FOR 18,000 OZ OR .5596 TONNES:THIS BRINGS US TO OCT 8 WITH A HUGE ISSUANCE OF 1000 CONTRACTS FOR 100,000 OZ OR 3.1104 TONNES. NOW AFTER A TWO WEEK HIATUS, OCT 21: 1029 CONTRACTS FOR 10290 OZ OR 3.200 TONNES TOTAL ISSUANCES 6 OCCASIONS FOR 4679 CONTRACTS OR 467,900 OZ OR 14.553 TONNES

HISTORY: LAST 8 MONTH’S EXCHANGE FOR RISK

IN FEBRUARY:

WE HAD A HUGE FIVE EXCHANGE FOR RISKS ISSUANCES FOR GOLD, TOTALLING 18.4527 TONNES!.

IN MARCH:

THE TOTAL NO. OF EXCHANGE FOR RISK ISSUANCE FOR THE MONTH OF MARCH (3 NOTICES) EQUALED: 7.6179 TONNES OF GOLD WHICH WAS ADDED TO OUR MARCH DELIVERY TOTALS.

IN APRIL:

WE CONCLUDED APRIL WITH 7 ISSUANCE OF EXCHANGE FOR RISK FOR A TOTAL TONNAGE OF 8.3571 TONNES.

IN MAY:

MAY: 3 EX. FOR RISK ISSUED SO FAR FOR 3025 CONTRACTS OR 302,500 OZ OR 9.4054 TONNES. THIS WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US TOTAL STANDING FOR MAY!THIS IS THE 6TH CONSECUTIVE MONTH FOR ISSUANCE OF EXCHANGE FOR RISK//NEW TOTAL EX FOR RISK IS 9.4054 TONNES FOR THE 3 ISSUANCE!

IN JUNE

JUNE: ZERO ISSUED

jULY: 2 OCCASIONS LATE IN JULY: 1206 CONTRACTS FOR 120,600 OZ OR 3.750 TONNES/ISSUED JULY 23/2025 AND JULY 30/2025

AUGUST: 7 ISSUANCES FOR A MONTHLY MONSTER 14,370 CONTRACTS OR 1,437,000 OZ ( 44.696) TONNES).AT THE BEGINNING OF THE MONTH THE CME ISSUED THE 2ND HIGHEST EVER MONTHLY RECORDED ISSUANCE OF 2924 CONTRACTS AND THIS IS FOLLOWED BY THURSDAY’S HUGE ISSUANCE OF 2226 CONTRACTS THUS BECOMING THE 4TH HIGHEST EVER RECORDED BY THE CME, SLIGHTLY BELOW PREVIOUS DAY’S ISSUANCE OF 2924 CONTRACTS. THE HUGE NUMBERS OF EXCHANGE FOR RISK SUGGEST THAT A MAJOR CENTRAL BANK IS DEMANDING ITS GOLD BACK.

SEPTEMBER: SEVEN ISSUANCES FOR 7370 CONTRACTS SO FAR FOR 737,000 OZ OR 22.923 TONNES OF GOLD!!

OCTOBER: FIRST INITIAL ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES OF GOLD. THIS WAS FOLLOWED BY AN ISSUANCE OF 650 CONTRACTS OR 65000 OZ OR 2.0217 TONNES. THEN ON OCT 3 WE RECEIVED OUR 3RD NOTICE FOR A HUGE 1320 CONTRACTS OR 132000 OZ OR 4.1057, AND THEN SATURDAY OCT 4, THE CME ISSUED ITS 4 ISSUANCE FOR 180 CONTRACTS FOR 18,000 OZ OR .5594 TONNES. THEN OCT 8 FOR 1000 CONTRACTS, OR 100,000 OZ OR 3.1104 TONNES AND FINALLY OCT 21; 3.200 TONNES// THUS ON 6 OCCASIONS TOTAL EXCHANGE FOR RISK ISSUANCE; 14.553 TONNES

AS I EXPLAINED ABOVE,:THE RECIPIENT OF EXCHANGE FOR RISK FOR GOLD IS THE BANK OF ENGLAND

here are the only possible candidates who must bring back loaned gold

- THE BANK OF ENGLAND WHO CONTINUES TO LEASE OUT MUCH ITS GOLD TO BULLION BANKS AND :(EX FOR RISK 9 MONTH TOTALS 127.5 TONNES)//TOTAL RESERVES OF BOE EQUALS 310 TONNES)

- THE FEDERAL RESERVE BANK OF NEW YORK (NEED TO RETRIEVE THEIR LEASED/BORROWED GOLD FROM THE BIS).THE FED STILL REFUSES TO BRING BACK MUCH OF ITS 30 TONNES SHORTFALL. IT BOUGHT BACK ONLY 4 TONNES LAST MONTH AND THUS THEIR SHORTFALL TO THE BIS IS 30 TONNES.

HOWEVER, IN OUR CASE, EXCHANGE FOR RISK RECIPIENT IS THE BANK OF ENGLAND. THE COUNTERPARTY TO THE BANK OF ENGLAND EXCHANGE FOR RISK ARE BULLION BANKS THAT CANNOT VERIFY THAT THEIR GOLD IS UNENCUMBERED. THE BUYER, REPRESENTING THE CENTRAL BANK OF ENGLAND ASSUMES THE RISK OF THAT DELIVERY. THIS IS THE 9TH MONTH FOR ISSUANCE OF EXCHANGE FOR RISK !!…..(DEC THROUGH OCT//ONLY MISSING JUNE. TOTAL 9 MONTHS ISSUANCE 130.3 TONNES)……… THE FACT THAT A CENTRAL BANK TAKES THE RISK OF A DELIVERY IS TOTALLY INSANE. THE VERY FIRST ISSUE OF EXCHANGE FOR RISK CAME IN MAY 2023. HUGE ISSUANCES BEGAN OCT AND DEC 2024. ROBERT LAMBOURNE, GATA CONSULTANT AND EXPERT ON BIS AND BANK OF ENGLAND ISSUES HAS WRITTEN TO THE BANK OF ENGLAND AUTHORITIES CONCERNING THE REFUSAL OF THE BANK OF ENGLAND’S AUDITORS TO SUPPLY A POSITIVE AUDIT ON THEIR GOLD TONNAGE AND OTHER ASSETS HELD UNDER THE E.E.A. .AND NOW THE OCC HAS WRITTEN NEW RULES ON BORROWED GOLD AND THE HANDLING OF EXCHANGE FOR PHYSICAL ISSUANCES AS TO NOT BREAK ANY LAWS!!! STRANGE: THEY HAVE BEEN BREAKING LAWS FOR 5 YEARS NOW.

DETAILS ON OCTOBER COMEX MONTH//

IN TOTAL WE HAD A FAIR SIZED LOSS ON OUR TWO EXCHANGES OF 2412 CONTRACTS DESPITE OUR HUGE GAIN IN PRICE WHICH ABSOLUTEY MAKES NO SENSE!!. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS. LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. DELIVERY OF GOLD CONTRACTS ARE NOW TAKING SEVERAL WEEKS. NO DEFAULT HAS BEEN INITIATED AS DEALERS ARE AFRAID OF LOSS OF THEIR JOBS. SO THIS FRAUD CONTINUES. THE LEASE RATES IN LONDON HAVE NOW INCREASED TO 6.0% LATELY AS GOLD IN LONDON IS STILL EXTREMELY SCARCE. THE FORCE MAJEURE AT GRASBERG IS CERTAINLY HAVING AN EFFECT ON LEASE RATES IN LONDON WITH RESPECT TO GOLD/SILVER.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH OCT CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS HOWEVER A GOOD SIZED T.A.S ISSUANCE AS THE CME NOTIFIES US THAT THEY HAVE ISSUED 2,137 T.A.S CONTRACTS. THESE T.A.S ISSUANCES ARE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE AGAIN ON FRIDAY’S HJUGE RAID, DESPERATELY TRYING TO STOP GOLD’S ADVANCE. THIS GENERALLY ENDS IN FAILURE AS WE WE WILL PROBABLY SEE GOLD//SILVER RISE HUGELY ON MONDAY WHICH IT DID.. HOWEVER THE HUGE RISE IS CAUSING ANOTHER RAID THIS TUESDAY MORNING.

A LITTLE HISTORY ON TAS ATTEMPTED RAIDS: (LIKE TODAY)

AS FOR THE FIRST TIME EVER, THEY FAILED TO RAID AT MONTH’S END AUGUST COMEX AND OTC/LONDON LBMA EXPIRY!! SO THE CROOKS DECIDED IT WAS NECESSARY TO RAID AROUND THE BIG INTEREST RATE ANNOUNCEMENT SEPT 17-SEPT 18 AND THEY TRIED AGAIN RIGHT BEFORE FIRST DAY NOTICE SEPT 30, WITH MUCH FAILURE AS THE TOTAL OPEN INTEREST REFUSED TO BUCKLE!! THIS LEADS US TO FIRST DAY NOTICE SEPT 30 AND THE LAST POSSIBLE DAY FOR A RAID AND TRUE TO FORM OUR CROOKS DECIDED TO RAID MUCH TO THE DELIGHT OF OUR BOYS IN LONDON WHO PICKED UP EXTRA AMOUNTS OF GOLD AND TENDERED FROM THIS SHORT PAPER ISSUANCE. THEN MUCH TO MY ANGER THEY DECIDED TO RAID AGAIN ON OCT 2 WITH CHINA OFF THIS WEEK FOR THEIR FALL FESTIVAL (BACK TODAY) AND OF COURSE THE IMPORTANT RELIGIOUS HOLIDAY FOR THE JEWISH PEOPLE OCT 1-2, YOM KIPPUR. AGAIN THIS ENDED IN ABSOLUTE FAILURE AS LONDON AGAIN CAME TO THE RESCUE WITH THEIR MASSIVE TENDERING FOR PHYSICAL. YOU CAN JUST VISUALIZE THE MASSIVE HEADACHE THE CROOKS UNDERWENT WITH THIS HUGE PHYSICAL TENDERING FOR GOLD.(THE HUGE INCREASE IN QUEUE JUMPING). AND NOW AS WE ARE SET TO BEGIN OPTION EXPIRY WEEK, THE CROOKS HAVE DECIDED TO RAID AGAIN. IT WILL BE QUITE A TRADING WEEK //OTC OPTIONS EXPIRY FRIDAY OCT 31..COMEX EXPIRY TUESDAY OCT 28.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 7 MONTHS:

FOR APRIL AT 209 + TONNES

AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 2.817 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

AND THIS NOW BRINGS US TO OCTOBER WHERE INITIAL AMOUNT OF GOLD STANDING IS 28,988 CONTRACTS FOR 90.114 TONNES OF GOLD TO WHICH WE ADD OUR FIRST MASSIVE QUEUE JUMP OF 4.898 TONNES QUEUE JUMP FOLLOWED BY OCT 4 QUEUE JUMP OF 0.9704 TONNES TO BE FOLLOWED BY OCT 7 QUEUE JUMP OF 3.623 TONNES, THEN OCT 8’S HUGE 6.942 TONNES QUEUE JUMP, OCT 9 HUGE 4.979 TONNES OF QUEUE JUMP, OCT 10 MASSIVE QUEUE JUMP OF 7.504 CONTRACTS(250,900 OZ//7.504 TONNES) AND THEN OCT 13: 4.3919 TONNES// AND THEN OCT 14 WITH A RECORD SETTING 9.564 TONNES AND THEN WEDNESDAY’S MASSIVE 6.469 TONNES QUEUE JUMP AND THEN THURSDAY’S QUEUE JUMP AT 8.326 TONNES. THEN HUGE RECORD SETTING 12.031 TONNES QUEUE JUMP AND THEN TODAY’S 3.8600 TONNES //// AND THIS WAS AUGMENTED BY AN UNUSUAL 50,000 CONTRACT EXCHANGE FOR RISK ISSUED ON FIRST DAY NOTICE AND THEN ON THREE CONSECUTIVE OCCASIONS, OCT 2 THROUGH TO THE OCT 4.THEY TOOK ONE DAY OFF AND THEN ISSUED ITS 5TH EXCHANGE FOR RISK ISSUANCE FOR 1000 CONTRACTS OR 100,000 OZ/3.1105 TONNES AND THEN FINALLY OCT 21 EXCHANGE FOR RISK// FOR 1029 CONTRACTS//102,900 OZ//3.200 TONNES THE NEW TOTAL ON THESE 6 ISSUANCES IS 4679 CONTRACTS FOR 467,900 OZ OR 14.553 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERIES INCLUDING QUEUE JUMPS. NEW TOTALS FOR GOLD STANDING ADVANCES TO 186.531 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 30+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES NOW THAT THEY MUST BECOME COMPLIANT TO BASEL III RULES JULY 1/2023 AS OUTLINED IN ANDREW MAGUIRE’S LATEST LIVE FROM THE VAULT 231 TO 245 EPISODES AS HE TACKLES THIS IMPORTANT TOPIC. THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST THREE MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!IT SURE DOES NOT LOOK LIKE THE BIS HAS GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN REMAINS ON THE BOOKS OF THE BIS. TRUMP WILL PROBABLY BE FURIOUS WITH THE FED IF HE FINDS OUT THAT THEY (FRBNY) HAS BEEN MANIPULATING THE GOLD MARKET FOR THE PAST TWO YEARS. THE FRBNY IS NOW NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH INCLUDING FIRST DAY NOTICE OF GOLD TONNAGE STANDING.

SUMMARY OF GOLD QUEUE JUMPING AND EXCHANGE FOR RISK ISSUANCE: AUGUST THROUGH OCTOBER AND SUBSEQUENT STANDING FOR GOLD.

AUGUST:

AUGUST: TOTAL QUEUE JUMPING AND TOTAL EXCHANGE FOR RISKS ISSUANCE FOR THE MONTH OF AUGUST; AND THUS STANDING:

WE HAD A HUGE 60.547 TONNES OF INITIAL GOLD STANDING FOR AUGUST, FIRST DAY NOTICE FOLLOWED BY THE MONTHS HUGE TOTAL OF 47.2312 TONNES OF QUEUE JUMPS TO WHICH WE ADD AUGUST 7TH,S HUGE 5.443 TONNES EXCHANGE FOR RISK ISSUANCE +LAST SATURDAY’S/MONDAY AUG 10 HUGE 776 CONTRACT EXCHANGE FOR RISK FOR 2.413 TONNES THEN AUGUST 12: 2.637 TONNES: AND NOW AUG 25: 9.107 TONNES ISSUANCE MONDAY’S MASSIVE 9.1016 TONNES ISSUANCE/AUGUST 25, AUGUST 26 9.0699 TONNES , YESTERDAYDAY’S (AUGUST 27) 9.0699 TONNES AND FINALLY TODAY’S TODAL OF 6.923 TONNESS/NEW STANDING ADVANCES TO 152.208 TONNES.

SEPT:

SEPTEMBER: TOTAL EXCHANGE FOR RISK AND QUEUE JUMPING; STANDING FOR GOLD

SUMMARY SEPT: 8.093 TONNES INITIALLY STANDING FOR GOLD // 7 ISSUANCES OF 22.923 TONNES OF EXCHANGE FOR RISK ISSUANCE/ SEPT MONTH AND THIS IS ADDED TO OUR NORMAL DELIVERY OF 25.878 TONNES

THAT IS;

A) //TOTAL FOR MONTH EXCHANGE FOR RISK/MONTH: 22.923 TONNES EX FOR RISK!!

B) //NORMAL DELIVERY OF 25.878 TONNES WHICH INCLUDES ALL QUEUE JUMPING.

TOTALS: 48.801 TONNES FINAL STANDING FOR GOLD/SEPT.

AND THIS BRINGS US TO OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 21 JUMP OF 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 186.531 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT:

F) A MASSIVE QUEUE JUMP,OCT 3 OF 4.898 TONNES OF GOLD

G) STRONG QUEUE JUMP OCT 4: 0.9704 TONNES

H) A MASSIVE QUEUE JUMP OCT 7 OF 3.623 TONNES

I) A MASSIVE QUEUE JUMP OCT 8 FOR 6.942 TONNES

J) A MASSIVE QUEUE JUMP OCT 9 FOR 4.979 TONNES

K) A MASSIVE AND 3RD HIGHEST EVER OCT 10 QUEUE JUMP FOR 7.504 TONNES

L) A MASSIVE QUEUE JUMP OF 4.3919 TONNES

M) A RECORD SETTING QUEUE JUMP OF 9.564 TONNES

N) A HUGE 6.469 TONNES QUEUE JUMP

0) A HUGE 8.326 TONNES QUEUE JUMP

P) A RECORD SETTING 12.031 TONNE QUEUE JUMP THE HIGHEST EVER RECORDED IN COMEX HISTORY SURPASSING TUESDAY’S 9.564 TONNES

Q/ QUEUE JUMP OF 7.695 TONES OF GOLD//

R/ TODAY’S QUEUE JUMP OF 3.8600 TONNE QUEUE JUMP

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

185.531 TONNES OF GOLD!!

EXCHANGE FOR PHYSICAL ISSUANCE/OCT

THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED EXCHANGE FOR PHYSICAL OF 1621 CONTRACTS.

THAT IS A FAIR SIZED 1621 EFP CONTRACT WAS ISSUED: : /DEC 1621 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1621 CONTRACT. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON!

WE HAD :

- ZERO LIQUIDATION OF OUR T.A.S. SPREADERS//MONDAY + GOVERNMENT LIQUIDATION

- MONTH END SPREADERS HAVE NOW FINISHED AS IT WAS IN FULL FORCE ON FIRST DAY NOTICE SEPT 30 WITH OUR ATTEMPTED FAILED RAID, FOLLOWED BY ANOTHER RAID OCT 2 AND THAT ENDED IN TOTAL FAILURE! , OCT 7 WE WITNESSED A SMALL RAID TRYING TO STOP GOLD’S ADVANCE TO THE 4000 BARRIER!! EARLY Y\OCT 8 MORNING THE BARRIER TO 4,000 DOLLAR GOLD WAS PIERCED!! AND THAT SET IN MOTION OUR CROOKS DESPERATE TO CONTROL THEIR HUGE DERIVATIVE LOSSES. (OCT 9 SAW FINALLY AFTER MANY YEARS SILVER PIERCING THE 50 DOLLAR MARK AND THAT WAS WHEN THE CROOKS THREW ANOTHER TEMPER TANTRUM WHEN GOLD FINALLY BROKE THROUGH 4,000 DOLLAR MARK ON OCTO 10 AND THAT FAILED AND FROM THAT POINT GOLD NEVER LOOKED BACK!!

T.A.S.SPREADER ISSUANCE//OCT

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR FRIDAY NIGHT/SATURDAY MORNING WAS A STRONG SIZED SIZED 2137 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR OTHERWISE LIKE LAST MONTH ON OPTIONS EXPIRY WEEK AND THEN OCT 9 AND THEN TODAY OCT 21, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

MECHANICS OF T.A.S CONTRACTS TRADING; (AND MONTH END SPREADERS)

THROUGHOUT THE FEW YEARS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE..

THAT SET UP YESTERDAY’S GAIN IN PRICE IN GOLD AND A CORRESPONDING FAIR GAIN OF COMEX OI AND A STRONG EXCHANGE FOR PHYSICAL ISSUANCE.. THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 3 MONTHS ESPECIALLY WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

- THE LONDON BANKING AUDITORS HAVE SO FAR REFUSED TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/

GOLD STANDING AT THE COMEX FOR GOLD LAST 9 MONTHS OF 2025:

YEAR 2025:

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

AND NOW OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S HUGE., 3.860 TONNES FOLLOWING INITITAL 7.695 TONNES WHICH FOLLOWED FRIDAY’S HUGE: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S 8.326 TONNES, FOLLOWING WEDNESDAY’S HUGE 6.469 TONNES WHICH FOLLOWED TUESDAY;S RECORD SETTING 9.564 TONNES OF A QUEUE JUMP TO WHICH WE ADD ALL OTHER QUEUE JUMPS IN OCT OF 33.009 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 186.531 TONNNES.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING OCT,. CONTRACT;

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A MEGA HUGE $137.70./ /) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE SMALL SIZED GAIN IN OI FROM TWO EXCHANGES OF 966 CONTRACTS.. BUT AS EXPLAINED ABOVE WE HAD HUGE T.A.S. SPREADER LIQUIDATION MONDAY .THIS WAS COUPLED WITH A) GOVERNMENT LIQUIDATING THEIR CONTRACTS OUT OF SEVERE FEAR!!(PRELIMINARY NUMBERS LOWERED TO FINAL SHOWING MASSIVE LIQUIDATION). AND B) MAYBE THE COMMENCEMENT OF MONTH END SPREADER LIQUIDATION /// THE BANKERS ARE QUITE NERVOUS ABOUT BASEL III WITH ITS IMPLEMENTATION COMMENCING JULY 1. THEY ARE VERY CONCERNED WITH THEIR HIGH AMOUNT OF DERIVATIVES LOSSES ON THEIR BOOKS EVEN THOUGH THEY TRANSFERRED THESE LOSSES ONTO THE FED’S BALANCE SHEET.THUS THE REASON THEY NEEDED THESE T.A.S. ISSUANCES NOW IN ORDER TO FORMALIZE RAIDS: OUR CROOKS TRIED AGAIN LATE OCT 2 WITH CHINA OUT FOR A WEEK, WITH NOT MUCH LUCK. WITH CHINA COMING BACK THURSDAY OCT 9 THE CROOKS NEEDED TO RAID TRYING DESPERATELY TO HALT GOLD’S ADVANCE. I GUESS THAT THEIR LUCK HAS RUN OUT WITH GOLD INITIALLY PIERCING THE 4,000 DOLLAR BARRIER OCT 7-8 ALONG WITH THE PIERCING OF SILVER’S MAGIC 50 DOLLAR MARK. GOLD AND SILVER FROM OCT 10 ON NEVER LOOKED BACK ONCE THEY PIERCED THEIR RESPECTIVE BARRIERS OF 4,000 DOLLAR GOLD AND 50 DOLLAR SILVER. THE CROOKS NOW NEED TO RAID ON EVERY OTHER DAY. AS TODAY OCT 21 IS ANOTHER MASSIVE RAID ON OUR PRECIOUS METALS AND EQUITY SHARES.

TUESDAY MORNING//MONDAY NIGHT

THE CROOKS HOWEVER COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/ TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD TO ARRIVE BY BOAT. IT IS NOW TAKING WEEKS TO DELIVER

ANALYSIS OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT

WE HAVE A SMALL SIZED GAIN OF A TOTAL OF 3.004 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR OCT AT 90.164 TONNES TO BE FOLLOWED BY AN INITIAL HUGE 7.695 TONNES/QUEUE JUMP WHICH FOLLOWED A MASSIVE 12.031 TONNES OF QUEUE JUMP AND THEN 61.216 TONNES OF PREVIOUS QUEUE JUMPS TO WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ NEW TOTAL STANDING 186.531 TONNES.

ALL OF THIS HUGE STANDING FOR OCTOBER WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $137.70

WE HAD A HUGE 4688 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE AS WELL.

NET LOSS ON THE TWO EXCHANGES 2412 CONTRACTS OR 241,200 0Z (7.502 TONNES)

speculators have left the gold arena

INITIAL GOLD COMEX

OCT CONTRACT MONTH

OCT 21

OCT CONTRACT MONTH

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1 entries i) Out of Brinks 10,990.473 total withdrawal 10,990.473oz or 0.3418 tonnes of gold// . |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 1531 notice(s) 153,100 OZ 4.7620 TONNES |

| No of oz to be served (notices) | 216 contracts 21600 OZ 0.6718 TONNES |

| Total monthly oz gold served (contracts) so far this month | 55,075notices 5,507,500oz 171.306 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

0 ENTRIES

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

0 entries

customer withdrawals:

1 entries

i) Out of Brinks 10,990.473

total withdrawal 10,990.473oz or 0.3418 tonnes of gold//

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 6

ALL dealer to customer account

a) Asahi: 22,007.135 oz

b) Brinks 200,684.622 oz

c) HSBC 60,838.417 oz

d) JPMorgan 20,543.800 oz

e) Loomis 385.812 oz

f) Malca: 2318.419 oz.

volume at the comex: Monday: 368,326oz (strong)

AMOUNT OF GOLD STANDING FOR OCTOBER

THE FRONT MONTH OF OCTOBER STANDS AT 1747 CONTRACTS FOR A LOSS OF ONLY 920 CONTRACTS.

WE HAD 2161 CONTRACTS FILED ON MONDAY SO WE GAINED A HUGE 1241 CONTRACT QUEUE JUMP FOR 124,100 OZ OR 3.8600 TONNES OF GOLD, WHICH FOLLOWED LAST FRIDAY’S, HIGHEST EVER QUEUE JUMP RECORDED IN COMEX HISTORY OF 12.54 TONNES TONNES OF GOLD WHICH FOLLOWED BY ALL THE REST OF OCTOBER QUEUE JUMP OF 57.356 TONNES

THUS OUR NEW NORMAL DELIVERY RISES TO 171.978 TONNES WHICH INCLUDES ALL PREVIOUS QUEUE JUMPS) PLUS OUR 14.553 TONNES EX FOR RISK//NEW TOTAL STANDING FOR GOLD ADVANCES TO 186.531 TONNES

NOVEMBER GAINED 173 CONTRACTS UP TO 6045 CONTRACTS.

DECEMBER LOST 3784 CONTRACTS DOWN TO 362,075 CONTRACTS.

We had 1531 contracts filed for today representing 153,100 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 1531 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer an 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for OCT /2025. contract month, we take the total number of notices filed so far for the month (55,075 oz ) to which we add the difference between the open interest for the front month of OCT ( 1747 CONTRACTS) minus the number of notices served upon today (1531x 100 oz per contract) equals 5,529,100 OZ OR 171.978TONNES OF GOLD TO WHICH WE ADD OUR 6 ISSUANCES OF 14.553 TONNES OF EXCHANGE FOR RISK //NEW TOTALS STANDING FOR GOLD OCTOBER ADVANCES TO 186.531 TONNES. NO WONDER THE COMEX IS IN TURMOIL WITH THIS MAMMOTH STANDING FOR GOLD.

thus the INITIAL standings for gold for the OCT contract month: No of notices filed so far (55,075 x 100 oz +we add the difference for front month of OCT. (1747 OI} minus the number of notices served upon today (1531 x 100 oz) which equals 5,529,100 OZ OR 171.978 TONNES + 14.553 TONNES EXCHANGE FOR RISK//NEW TOTAL OF GOLD STANDING IN OCTOBER ADVANCES TO 186.531 TONNES

TOTAL COMEX GOLD STANDING FOR OCT..: 186.531 TONNES TONNES WHICH IS HUGE FOR THIS NORMALLY SMALL ACTIVE ACTIVE DELIVERY MONTH OF OCT.

volume Wednesday confirmed 327,800 contracts huge

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,715,433.186 oz 53.35 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 39,020,901.404oz

TOTAL REGISTERED GOLD 20,381,319.400 or 633.94tonnes

TOTAL OF ALL ELIGIBLE GOLD 18,639,587.064 OZ

END

REGISTERED GOLD THAT CAN BE SERVED UPON 1,866,588 oz ((REG GOLD- PLEDGED GOLD)= 580.58tonnes // (

total inventories in gold declining rapidly

SILVER/COMEX

SILVER/COMEX

THE OCT. 2025 SILVER CONTRACTS

OCT 21 2025

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 4 entries i) Out of CNT 606,586.230 oz ii) Out of Delaware 2,,001.900 oz iii) Out of HSBC 603,051.470 oz iv) Out of Loomis 1,423,444.640 oz total withdrawal 2,635,094.240 oz |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | 2 entries i) Into CNT 653,637.500 oz ii) Into Stonex 599,687,300 oz total deposit 1,253,324.800oz |

| No of oz served today (contracts) | 480 CONTRACT(S) ( 2.4 MILLION OZ |

| No of oz to be served (notices) | 2 contracts (10,000 oz) |

| Total monthly oz silver served (contracts) | 6934 Contracts (34.670 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

2 entries

2 entries

i) Into CNT 653,637.500 oz

ii) Into Stonex 599,687,300 oz

total deposit 1,253,324.800oz

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx)

withdrawals: customer side/eligible

4 entries

i) Out of CNT 606,586.230 oz

ii) Out of Delaware 2,,001.900 oz

iii) Out of HSBC 603,051.470 oz

iv) Out of Loomis 1,423,444.640 oz

total withdrawal 2,635,094.240 oz

adjustments: 3

3 dealer to customer

a) Brinks 316,874.690 oz

b) JPMorgan: 78,712.800 oz

c) Manfra: 347,850.253 oz

comex is in turmoil

TOTAL REGISTERED SILVER: 170.664 MILLION OZ//.TOTAL REG + ELIGIBLE. 503.832 Million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR OCT.

silver open interest data:

FRONT MONTH OF OCT /2025 OI: 480 OPEN INTEREST CONTRACTS FOR A GAIN OF 143 CONTRACTS.

WE HAD 312 CONTRACTS SERVED ON MONDAY, SO WE GAINED 455 CONTRACTS WHICH UNDERWENT A STRONG QUEUE JUMP FOR 2.275 MILLION 0Z

THUS

NORMAL STANDING FOR SILVER OCT ADVANCES TO 34.680 MILLION OZ WHICH INCLUDES TODAY’S STRONG 1.625 MILLION OZ QUEUE JUMP + 2,110 MILLION OZ EX. FOR RISK = 36.790 MILLION OZ WHICH IS MASSIVE FOR A NON DELIVERY MONTH!!

NOVEMBER GAINED 64 CONTRACTS UP TO 2462

DECEMBER LOST 4784 CONTRACTS UP TO 122.583

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 312 or 1.56 MILLION oz

CONFIRMED volume; ON MONDAY 111,261 huge//

AND NOW OCT. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in OCTOBER. we take the total number of notices filed for the month so far at 6934 X5,000 oz = 34.670 MILLION oz

to which we add the difference between the open interest for the front month of OCT (482) AND the number of notices served upon today (480 )x (5000 oz)

Thus the standings for silver for the OCTOBER 2025 contract month: (6934) Notices served so far) x 5000 oz + OI for the front month of OCTOBER(482) minus number of notices served upon today (480)x 5000 oz equals silver standing for the OCT.contract month equating to 34.680 MILLION OZ to which we must add our initial 2.110 million oz exchange for risk issuance//new standing advances to 36.790 which is mammoth for a non active delivery monthj.

New total standing: 36.790 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 170.644 million oz of registered silver

JPMorgan as a percentage of total silver: 208,118/503,832million. 41.37%

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

OCT 21 WITH GOLD DOWN $240.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 11.45TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1058.66 TONNES

OCT 20 WITH GOLD UP $137.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 12.59TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1047.21 TONNES

OCT 17 WITH GOLD DOWN $90.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 12.04TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1034.62 TONNES

OCT 16 WITH GOLD UP $104,45 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.15TONNES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1022,60 TONNES

OCT 15 WITH GOLD UP $41.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2 TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1021.45 TONNES

OCT 14 WITH GOLD UP $33.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.72 TONNEES OF GOLD INTO THE GLD// . /// ///INVENTORY RESTS AT 1018.88 TONNES

OCT 11 WITH GOLD UP $!29.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.72 TONNEES OF GOLD FROM THE GLD// . /// ///INVENTORY RESTS AT 1017.16 TONNES

OCT 10 WITH GOLD UP $26.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WIHTDRAWAL OF 1.14 TONNEES OF GOLD FROM THE GLD// . /// ///INVENTORY RESTS AT 1013.44 TONNES

OCT 9 WITH GOLD DOWN $91.45 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1014.58 TONNES

OCT 8 WITH GOLD UP $68.60 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 7 WITH GOLD UP $29.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.17 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1013.17 TONNES

OCT 6 WITH GOLD UP $68.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.86 TONNES OF GOLD OUT OF THE GLD. . /// ///INVENTORY RESTS AT 1014.88 TONNES

OCT 3 WITH GOLD UP $38.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 2.86 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1015.74 TONNES

OCT 1 WITH GOLD UP $25.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 1.15 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1012.88TONNES

SEPT 30 WITH GOLD UP $18.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 6.01 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1011.73 TONNES

SEPT 29 WITH GOLD UP $48.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MASSIVE DEPOSIT OF 8.87 TONNES OF GOLD VAPOUR ENTERED INTO THE GLD. . /// ///INVENTORY RESTS AT 1005.72 TONNES

SEPT 26 WITH GOLD UP $38.40 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 25 WITH GOLD UP $5.70 TODAY/HUGECHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.82 TONNES OF GOLD FROM THE GLD/ . /// ///INVENTORY RESTS AT 996.85 TONNES

SEPT 24 WITH GOLD DOWN $47.70 TODAY/NO CHANGES IN GOLD AT THE GLD . /// ///INVENTORY RESTS AT 1000.67 TONNES

SEPT 23 WITH GOLD UP $42.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 6/11 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 1001.67 TONNES

SEPT 22 WITH GOLD UP $68.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A MAMMOTH DEPOSIT OF 14.61 TONNES OF GOLD VAPOUR ENTERED THE GLD. /// ///INVENTORY RESTS AT 994.56 TONNES

SEPT 19 WITH GOLD UP $26.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 18 WITH GOLD DOWN $37.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD /// ///INVENTORY RESTS AT 975.66 TONNES

SEPT 17 WITH GOLD DOWN $8.30 TODAY/NO CHANGES IN GOLD AT THE GLD /// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 16 WITH GOLD UP $8.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 979.95 TONNES

SEPT 15 WITH GOLD UP $45.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 974.80 TONNES/

SEPT 12 WITH GOLD UP $12.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD:/// ///INVENTORY RESTS AT 977.95 TONNES/

SEPT 11 WITH GOLD DOWN $7.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD A DEPOSIT OF .28 TONNES OF GOLD INTO THE GLD:/// ///INVENTORY RESTS AT 979.96 TONNES//

SEPT 10 WITH GOLD DOWN $1.10 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 9 WITH GOLD UP $47.40 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.29 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 979.68 TONNES//

SEPT 8 WITH GOLD UP $41.40 TODAY/NO CHANGES IN GOLD AT THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

SEPT 5 WITH GOLD UP $47.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD ; A FRAUDULENT WITHDRAWAL OF 2.29 TONNES OF PAPER GOLD OUT OF THE GLD// ///INVENTORY RESTS AT 981.97 TONNES//

GLD INVENTORY: 1058.66 TONNES, TONIGHTS TOTAL

SILVER

OCT 21 WITH SILVER DOWN $3.73 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 8.757 MILLION OZ INTO THE SLV /// ///INVENTORY RESTS AT 507.010 MILLION OZ

OCT 20 WITH SILVER UP $0.94 TODAY/HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 2.405 MILLION OZ INTO THE SLV /// ///INVENTORY RESTS AT 498.253 MILLION OZ

OCT 17 WITH SILVER DOWN $2.85 TODAY/NO CHANGES IN SILVER AT THE SLV /// ///INVENTORY RESTS AT 495.848 MILLION OZ

OCT 16 WITH SILVER UP $1.63 TODAY/HUMONGOUS CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 9.982MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.848 MILLION OZ

OCT 15 WITH SILVER UP $0.55 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.681 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 505.830 MILLION OZ

OCT 14 WITH SILVER DOWN $0.07 TODAY/MAMMOTH CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 9.983 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 506.511 MILLION OZ

OCT 11 WITH SILVER UP $1.78 TODAY/SMALL CHANGES IN SILVER AT THE SLV A WITHDRAWAL OF 0.272 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 496.528 MILLION OZ

OCT 10 WITH SILVER UP $1.27 TODAY/HUGE CHANGES IN SILVER AT THE SLV A DEPOSIT OF 1.180 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 496.800 MILLION OZ

OCT 9 WITH SILVER DOWN $0.54 TODAY/HUGE CHANGES IN SILVER AT THE SLV A DEPOSIT OF 0.635 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 495.620 MILLION OZ

OCT 8 WITH SILVER UP $1.75 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 2.723 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 494.985 MILLION OZ

OCT 7 WITH SILVER DOWN $0.89 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 4.538 MILLION OZ OF SILVER INTO THE SLV/: /// ///INVENTORY RESTS AT 492.262 MILLION OZ

OCT 6 WITH SILVER UP $0.63 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 7.67 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 487.724 MILLION OZ

OCT 3 WITH SILVER UP $1.43 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE WITHDRAWAL OF 8.893 MILLION OZ OF SILVER OUT OF THE SLV/: /// ///INVENTORY RESTS AT 495.394 MILLION OZ

OCT 1 WITH SILVER UP $1.09 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.264 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 504.287 MILLION OZ

SEPT 30 WITH SILVER DOWN $0.34 TODAY/HUGE CHANGES IN SILVER AT THE SLV A HUGE DEPOSIT OF 5.129 MILLION OZ OF SILVER DEPOSITED INTO THE SLV/: /// ///INVENTORY RESTS AT 499.023 MILLION OZ/

SEPT 29 WITH SILVER UP $0.37 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL WITHDRAWAL OF 0.908 MILLION OZ OF SILVER DEPOSITED OUT OF THE COMEX/: /// ///INVENTORY RESTS AT 493.894 MILLION OZ//

SEPT 26 WITH SILVER UP $1.58 TODAY/SMALL CHANGES IN SILVER AT THE SLV A SMALL DEPOSIT OF 0.681 MILLION OZ OF SILVER DEPOSITED INTOTHE COMEX/: /// ///INVENTORY RESTS AT 494.802 MILLION OZ//

SEPT 25 WITH SILVER UP $1.44 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE WITHDRAWAL OF 3.222 MILLION OZ OF SILVER OUT OF THE COMEX THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 24 WITH SILVER DOWN $0.48 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 3.222 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 497.343 MILLION OZ//

SEPT 23 WITH SILVER UP $0.32 TODAY/HUGE CHANGES IN SILVER AT THE SLV A MASSIVE DEPOSIT OF 5.265 MILLION OZ OF SILVER VAPOUR ENTERED THE COMEX/: /// ///INVENTORY RESTS AT 494.121 MILLION OZ//

SEPT 22 WITH SILVER UP $1.16 TODAY/NO CHANGES IN SILVER AT THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 19 WITH SILVER UP $0.89 TODAY/HUGE CHANGES IN SILVER A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 18 WITH SILVER DOWN $0.69 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.908 MILLION OZ OUT OF THE SLV: /// ///INVENTORY RESTS AT 488.357 MILLION OZ//

SEPT 17 WITH SILVER DOWN $0.03 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.088 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 489.265 MILLION OZ//

SEPT 16 WITH SILVER DOWN $0.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.500 MILLION OZ INTO THE SLV: /// ///INVENTORY RESTS AT 487.177 MILLION OZ//

SEPT 15 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 12 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 11 WITH SILVER UP $0.46 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ//

SEPT 10 WITH SILVER UP $0.28 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 485.677 MILLION OZ //

SEPT 9 WITH SILVER DOWN $0.55/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.816 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 486.677 MILLION OZ./

SEPT 8 WITH SILVER UP $0.35/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 1.181 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 488.493 MILLION OZ./

SEPT 5 WITH SILVER UP $0.25/ HUGE CHANGES AT THE SLV AT WITHDRAWAL OF 2.735 MILLION OZ OUT OF THE SLV:// ////INVENTORY RESTS AT 489.674 MILLION OZ./

CLOSING INVENTORY 507.010 MILLION OZ OF SILVER

PHYSICAL GOLD/SILVE

1/PETER SCHIFF

JOHN RUBINO

jAMES RICKARDS

2. MATHEW PIEPENBURG/VON GREYERZ

ALASDAIR MACLEOD…

3. CHRIS POWELL AND HIS GATA DISPATCHES

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS /245

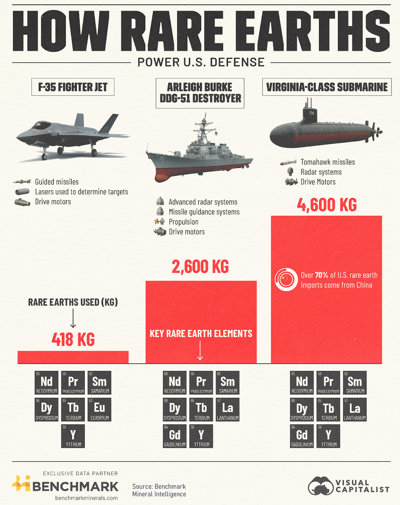

5. COMMODITY REPORT/RARE EARTHS/LITHIUM/MINING

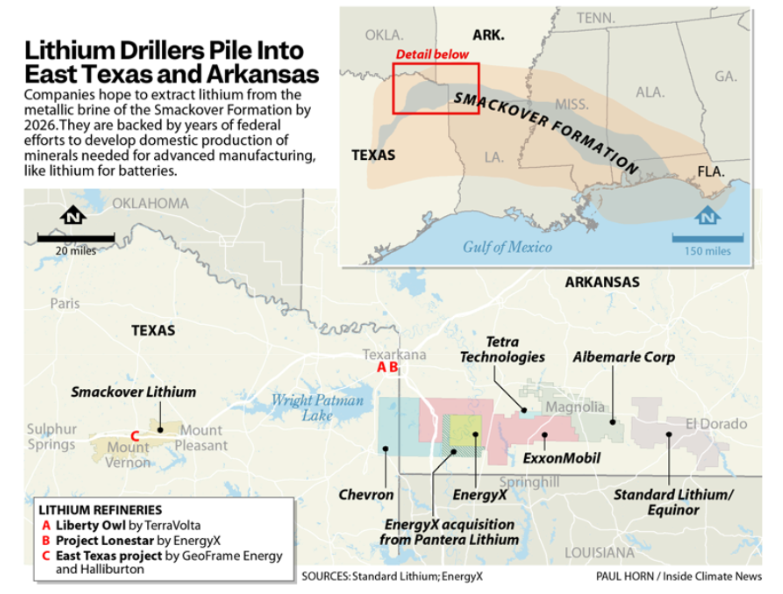

New Generation Of Industries Emerges In Texas As Rare Earths Race Ignites

Monday, Oct 20, 2025 – 08:05 PM

Authored by Dylan Baddour via Inside Climate News (emphasis ours),

Major oil companies are drilling in East Texas again, but not for oil. This time, they’re after lithium for batteries and other rare elements.

Chevron and Halliburton announced East Texas projects this summer. Exxon has acreage across the border in Arkansas. Smackover Lithium, a joint venture of a Norwegian oil giant and a Canadian miner, announced in late September the discovery of the most lithium-rich fluids ever reported in North America, measured deep beneath its Texas claims in a massive brine deposit called the Smackover Formation.

“It’s ripe for development,” said Jamie Liang, a former Wall Street banker and founder of Houston-based lithium startup TerraVolta, which is developing a lithium refinery on the Smackover with federal support. “There’s tremendous growth potential.”

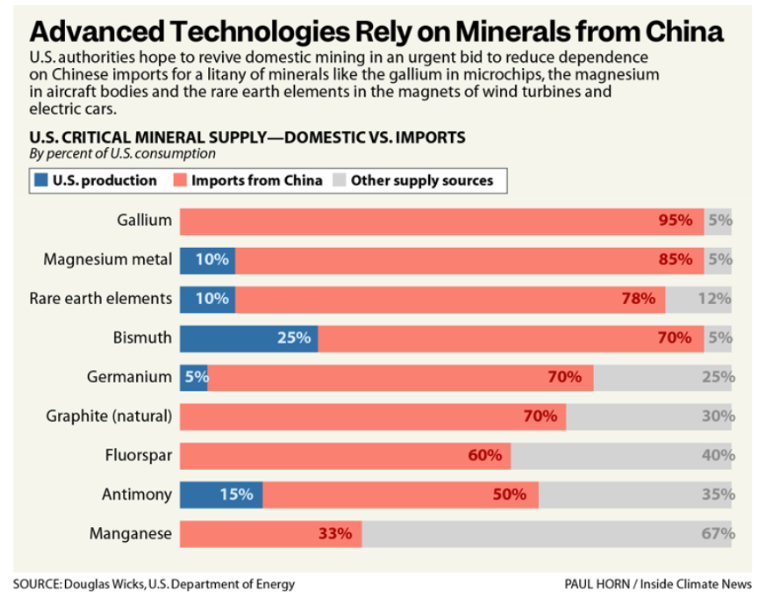

Lithium mining is one of several mineral industries emerging in Texas as part of broad federal efforts to urgently establish American production of the materials required for advanced manufacturing, from batteries and solar cells to wind turbines, microchips and cruise missiles.

Competition with China looms over this effort. For much of this year, the world’s two largest economies have been locked in trade tensions— and much of the ire is linked to minerals used in technology. This month, China announced new export controls on critical mineral products, including lithium battery components. President Trump, in social media posts, described China as “very hostile” and threatened to impose export controls on critical software and add 100 percent tariffs to Chinese imports.

Near Texarkana, the chase for lithium is backed with robust federal support. Liang’s TerraVolta received $225 million from the U.S. Department of Energy in 2024 for its lithium refinery complex. This year the project was selected for fast-tracked permit review.

It will pump up the naturally metallic super-salty fluids from the Smackover, extract lithium and other minerals and then inject the leftover liquids back underground. At least two other lithium refineries are planned in the area and companies have leased tens of thousands of acres for drilling. More will likely follow as long as lithium prices stay strong.

“There’s going to be a very large-scale infrastructure buildout,” Liang said. “You’re going to be drilling wells. You’re going to need those service companies. You’ll need pipelines.”

Elsewhere in Texas, a mine is planned near El Paso for the rare metals used in magnets for electric motors. On the rural Gulf Coast, the Department of Defense has invested almost $300 million in a project that would process rare metals like samarium, used in jet engines, guided munitions and stealth technology. From Houston’s petrochemical complex to the Permian Basin, a flurry of startups, oil majors and mining giants intend to recover minerals from industrial waste like coal ash, discarded electronics, mine tailings and oilfield wastewater in hopes of accelerating U.S. mineral supplies.

Presently, the United States produces a dribble of the raw materials. China broadly owns the global production lines, following decades of investment and securing a dominance that has raised national security concerns as well as financial risk.

The United States has just one operating lithium mine, in Nevada, where a second mine with government backing expects to begin production in 2027. Only one lithium refinery operates in the country, on the Gulf Coast of Texas.

“Our exposure to China is unacceptable,” said Douglas Wicks, a former program director at the Advanced Research Projects Agency of the Energy Department. It raises threats that the outbreak of conflict could leave the United States cut off from essential supply chains.

That’s the biggest reason why federal agencies are pushing so hard to play catch-up and boost American mining, Wicks said. As geopolitical tensions squeeze the flow of globalized commerce, Washington hopes to challenge Beijing’s monopolies in a battle of extraction.

“I think American industry can outproduce them,” said Wicks, who retired this year. The United States has “the deposits to do this.”

However, the United States has to contend with China’s gargantuan economy where the state owns key industries and provides subsidies, preferential finance schemes and other market support. Still, Wicks said, the United States knows how to move quickly. Just consider the recent evolution of American oil and gas. Technical innovations and loosened environmental standards in the shale revolution turned the United States from the world’s largest importers of oil and gas to a major exporter in barely over a decade. Wicks believes the United States can transform again.

In 2023, under the Biden administration, the Pentagon was ordered to establish mineral supply chains independent of China. Since then, billions of dollars have flowed to mining and processing projects across the country, spurring a rush of prospectors and entrepreneurs hoping to cash in on federal grants.

Wisk said, “Now there’s a big push in Texas to ask: ‘Is there something else under the ground other than oil and gas?”

Tiny Concentrations, Big Mines

In the desert of far-west Texas, a company called Texas Mineral Resources Corp. (TMRC) had plans to dig for rare earth elements at a 950-acre Round Top Mountain site. The company won its first Defense Department contract in 2015. In January it reported a “breakthrough,” producing a sample of high-purity dysprosium, which is used in semiconductors and electric vehicle motors. .

These rare elements aren’t actually hard to find. They’re all over the world, but they exist in tiny concentrations that require a tremendous amount of effort to extract in significant volumes. The process also generates large waste streams.

TMRC had said it would crush up 20,000 tons of rock a day. The material then would soak for a month in pools of diluted acid and undergo a series of electromagnetic processes to separate and cull the much-desired minerals. According to TMRC, the rocks hold 15 rare earth elements and other metals including lithium, gallium, hafnium, zirconium and beryllium.

Some processed byproducts “are expected to show hazardous waste characteristics,” and “the waste may contain naturally occurring radioactive material,” according to a 2019 economic assessment by TMRC. It noted “potential impacts to water quality resulting from mine operations and the storage of mine waste.” The operations are located in Hudspeth County, home to about 3,400 people, according to the latest census.

However, financial analysts have warned about TMRC’s viability, amid reports of a growing deficit and lack of revenue. In July, according to analyst reports, TMRC had a “severe liquidity crisis.”

The Round Top site is not an anomaly and, as TMRC struggles, other miners could step in, according to Brent Elliot, a geologist with the Bureau of Economic Geology at the University of Texas at Austin, the state’s official geological survey. There are “many Round Top-like igneous rocks in west Texas to explore,” he said, noting that a recent survey of the area “has shown some hot targets that I’ll go out and investigate.”

Holiday O’Bryan, a 22-year-old PhD student at the University of Texas, plans a career in mining. At a recent conference in Austin on mineral industries, she pointed out that most mining related to new technologies occurs in faraway countries, which often have lower environmental standards and enforcement. America’s surging investment in extraction should be seen in context of the clean innovations it will support. Mining operations will change the landscape—particularly as the Trump administration cuts backs on regulations of federal land—and no one should be surprised by the compromises that the race for rare earths will demand, she said.

“You have to have extraction for these technologies to work,” she said. “In the age of the green energy transition that doesn’t fly very well for someone who is trying to protect the environment.”

U.S. Mining Losses

Before 1990 the United States dominated the world’s mineral markets. But domestic production dropped that decade, in part, because of rising environmental protections at home and enticing low-cost foreign production possibilities. New industries and products emerging in the mid-2010s—smartphones and Tesla cars among them—prompted a re-think of the American economy and future needs. Mining had become a lost opportunity.

“People started looking at what you actually need to be able to build things like electric vehicles,” said Michelle Michot Foss, fellow in energy, minerals and materials at Rice University’s Baker Institute for Public Policy. “We started realizing, oh my gosh, we don’t produce any of this stuff.”

In recent years, it became clear that China had invested in and developed a strategic market, she said. The first Trump administration, within its first year, assessed mineral production as a national security matter.

A federal mandate was laid out in a 2017 Trump executive order, “A Federal Strategy To Ensure Secure and Reliable Supplies of Critical Minerals.” In 2018, 35 minerals were designated “critical” for vulnerable supply chains and essential economic functions.

Federal funding for mineral industries expanded at pace during the Biden administration. The 2021 Bipartisan Infrastructure Bill and the 2022 Inflation Reduction Act injected billions of dollars into projects around the country. Notably, the 2023 National Defense Authorization Act ordered the military to remove and replace Chinese-processed minerals from its processes within four years, sparking a race to rebuild complex supply chains.

Amid escalating trade tensions in 2024, China banned exports of several key minerals to the United States.

The second Trump Administration so far has allocated billions more dollars toward mineral industries, opened federal lands to mining exploration, ordered expedited permitting for certain projects and imposed tariffs on imports from more than 90 countries. China responded with export controls on 17 minerals used in military manufacturing.

The Modern War Institute at West Point military academy has called that, “a shot across the bow of the U.S. defense industrial base.”

Can America fill the gap? It won’t be easy, said Foss of Rice University. As the U.S. mining sector faded, so did its talent, expertise and a workforce pipeline.

“Nobody knows anything about this,” Foss said. “Not even in the agencies themselves are there good metallurgists anymore… except for down in the bowels of USGS.”

The United States will have to develop more than mines to secure a position in global mineral markets. It needs midstream and downstream industries to process extractions—or the raw material will have to be shipped to China, which has a proficient processing capacity.

Rare earth elements are critical components of the advanced magnets used in electrical motors and generators. For every megawatt of generating capacity, a wind turbine requires 180 kilograms of neodymium, 17 kg of dysprosium and 7 kg of terbium, according to a 2023 report from the National Renewable Energy Laboratory at the Energy Department.

Notably, the first large-scale lithium refinery in the United States is owned by Tesla, the electric car manufacturer, and located near Corpus Christi, Texas.

Launched in December, Tesla’s plant imports ore from Canada’s only lithium mine for processing into battery-grade material. It will eventually use eight million gallons of water per day. That might be difficult given the water shortages there.

About 70 miles north of Tesla’s refinery, another rare earths processing plant, a joint project between an Australian miner, Lynas, and the Defense Department, is also planned.

The Defense Department has invested $288 million since 2021 into Lynas Rare Earths Limited’s plans for a processor near the tiny town of Seadrift, on the shore of San Antonio Bay. If completed, the mining company would oversee the country’s first processor for elements such as samarium, used in ultra-high-temperature magnets for spacecraft, satellites, missile guidance systems, stealth aircraft and electronic warfare technologies.

But there’s a hitch, again, tied to water issues. Lynas aims to discharge wastewater through an existing treatment system at a nearby Dow Chemical plant, according to a draft environmental impact statement dated November 2023. That same month, Texas’ environmental regulators issued a draft wastewater permit amendment for Dow, which would increase daily discharge limits at one of its outfalls from 17 million to 42 million gallons.

The draft permit amendment did not mention Lynas or the reason for the sudden rise in daily discharges..

Diane Wilson, a 78-year-old environmental activist in Seadrift who has battled Dow for decades, filed a challenge to the permit amendment, questioning Dow’s need. Dow’s existing permit allows for about 80 harmful chemicals and metals in the wastewater.

To her surprise, Dow withdrew its application in February this year, shortly after state regulators recommended hearing Wilson’s request.

“They obviously did not want us going to a hearing,” Wilson said about Dow and the mining company. “There is a real secret element here.”

Two months later, Lynas announced its project faced rising costs due to “wastewater challenges,” according to industry news reports. In August, its annual results statement noted “there is significant uncertainty as to whether the construction of the heavy rare earth processing facility at Seadrift, Texas will proceed and, if so, in what form.”

That’s when Wilson said she surmised the Lynas mining project was behind the permit request.

Lynas and Dow did not respond to a request for comment.

Minerals from Waste

In the heart of Houston’s industrial complex, another Australian company, Metallium, announced in August that it had leased a fully permitted site for a first-of-a-kind facility to recover minerals from industrial and electronic waste.

Many critical minerals mined or refined in China ultimately end up in American landfills as discarded consumer electronics. Metallium aims to use flash heating technology developed at Rice University to haul in the abandoned material and extract an array of elements. The facility plans operations in 2026.

Other companies are exploring extraction of critical minerals from old industrial waste including coal ash, mine tailing and the red mud residues buried over decades at alumina processing sites along the coast. One pilot project in San Antonio is extracting the mineral graphite from methane gas.

A small landscape of startups has also cropped up around the tremendous volumes of mineral-rich–and toxic–wastewater that comes up from oil wells.

“We can basically turn an oil well into a mini-mine,” said Jesse Evans, co-founder of a San Antonio-based startup, Maverick Metals.

This year, Maverick began producing a proprietary chemical that is pumped at high pressure into new oil wells during fracking to dissolve metal-bearing rocks that rise to the surface in the brown frothy brine known as “produced water.”

Maverick has processes, equipment and chemicals to extract metals from that wastewater. Most startups in this space focus on lithium, Evans said. But oilfield wastewater also contains trace amounts of other metals like platinum, palladium and gold that are profitable business, he said.

“What makes the lithium space really difficult is competing with China,” he said.

Some Chinese companies are vertically integrated from mine to factory, including Contemporary Amperex Technology Co., Limited, the world’s largest battery manufacturer. Chinese companies also face looser environmental restrictions, lower labor costs and little media scrutiny. Critically, China’s state-run economy can swiftly orchestrate production surges to lower prices and crush competition—and its state-backed companies can operate at a loss for months if not years.

“We play by the rules of capitalism but a different set of rules applies to them,” said Marek Locmelis, an associate professor at the University of Texas at Austin who organizes an annual conference on critical minerals.

Lithium Hopes

Beyond the need for vast water supplies, the lithium pursuit also faces environmental and technical challenges. In Texas, the methods that companies plan to mine lithium haven’t yet been used commercially at scale anywhere in the world.

While traditional hardrock mines require stone crushing and grinding, the Smackover Formation contains a metal-rich brine that allows for quicker extraction.

“If you extract directly from a brine you basically skip the mineral processing step that is energy intensive,” Locmelis said.

Existing lithium brine operations—including Silver Peak in Nevada, the country’s only operating lithium mine—let fluids evaporate in ponds over 18 months to concentrate the minerals. But projects in Texas plan to use new methods that extract metals in several days.

These methods require much less freshwater than hardrock or evaporation mines but will still draw significant volumes from shallow aquifers. While water in East Texas may seem abundant, the area affected by lithium production lacks groundwater conservation districts to manage or track withdrawals, said Vanessa Puig-Williams, Texas water program director at the nonprofit Environmental Defense Fund.

“There is no entity that is managing the production of the fresh groundwater,” she said. “That’s worrisome because there is no oversight.”

One Austin-based lithium startup, EnergyX, plans to use a process of “proprietary lithium-selective adsorbents, membranes, and extractants” which “enables faster, cleaner, and cost-efficient lithium extraction,” said founder Teague Egan.

The process uses about 6,600 gallons of freshwater per ton of lithium produced, Egan said, just a fraction of traditional evaporation methods.

In September, EnergyX announced a site in Texarkana for its demonstration plant, which it plans to operate early next year. The company, backed by automaker General Motors, owns 330 adjacent acres where it plans a commercial-scale refinery. Four units would come online by 2030 to achieve 50,000 tons per year of production.

“Texas—and specifically the Smackover Region—is quickly emerging as one of the central hubs for the U.S. lithium sector,” Egan said. “In 10 years, we believe the Smackover Region will be the largest source of domestically produced lithium.”

His vision hinges on high hopes for strong lithium prices although there is some uncertainty about that.

A trade war with China could crush the American sector. Technical advancements are making smaller batteries with less lithium and could dampen demand. Rapid evolution of recycling technologies could also reduce the need for lithium production. Scientists are developing new designs for energy storage that could eventually see lithium batteries join CD players and USB sticks in the land of obsolescence.

Egan is not dissuaded. He is betting on Northeast Texas “evolving into a full-fledged lithium hub, with upstream brine production integrated directly into downstream refining.”

“The region has the potential to become a global benchmark,” he said. “Just as the oil and gas industry shaped the region’s past, lithium can help define its future.”

ASIAN MARKETS THIS TUESDAY MORNING:

SHANGHAI CLOSED UP 52.44 POINTS OR 1.36%

//Hang Seng CLOSED CLOSED UP 168.72 PTS OR 0.65%

// Nikkei CLOSED : UP 130.36 PTS OR 0.27% //Australia’s all ordinaries CLOSED UP 0.70%

//Chinese yuan (ONSHORE) CLOSED UP TO 7.1191// OFFSHORE CLOSED UP AT 7.1198/ Oil UP TO 58.02 dollars per barrel for WTI and BRENT UP TO 61.82 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING UP TO 7.1191 // OFFSHORE YUAN TRADING UP TO 7.1198 :/ONSHORE YUAN TRADING ABOVE OFF SHORE / AND THUS STRONGER/OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.1191

OFFSHORE YUAN: DOWN TO 7.1198

HANG SENG CLOSED UP 168.72 PTS OR 0.65%

2. Nikkei closed UP 130.36 PTS OR 0.27%

3. Europe stocks SO FAR: ALL GREEN