MASSIVE RAID ON OUR PRECIOUS METALS YET NO PHYSICAL TRADED HANDS

ACCESS MARKET

GOLD $4867.00 3:30 PM)

SILVER: 82.50 3;30 PM)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

EXCHANGE: COMEX

DLV615-T CME CLEARING

BUSINESS DATE: 01/29/2026 DAILY DELIVERY NOTICES RUN DATE: 01/29/2026

PRODUCT GROUP: METALS RUN TIME: 00:13:21

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2026 COMEX 100 GOLD FUTURES

SETTLEMENT: 5,318.400000000 USD

INTENT DATE: 01/29/2026 DELIVERY DATE: 02/02/2026

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 23 238

072 H GOLDMAN 500

092 C DEUTSCHE BANK 514

099 H DEUTSCHE BANK AG 2387

104 C MIZUHO SECURITIES US 11

118 C MACQUARIE FUTURES US 490

118 H MACQUARIE FUTURES US 27

132 C SG AMERICAS 40

167 C MAREX 1

190 H BMO CAPITAL MARKETS 2197

323 C HSBC 26

332 H STANDARD CHARTERED B 455

357 C WEDBUSH SECURITIES 2

363 C WELLS FARGO SECURITI 82

363 H WELLS FARGO SECURITI 739

365 C MAREX CAPITAL MARKET 1

435 H SCOTIA CAPITAL (USA) 2549

555 H BNP PARIBAS SEC CORP 1943

624 H BOFA SECURITIES 12

657 C MORGAN STANLEY 103 897

657 H MORGAN STANLEY 737

661 C JP MORGAN SECURITIES 11959 7995

690 C ABN AMRO CLR USA LLC 14

700 C UBS SECURITIES LLC 2379

709 C BARCLAYS 1032 258

726 C PLUS500US FINANCIAL 1

730 C PTG DIVISION OF SGAS 12

732 H RBC CAP MARKETS 1799

880 C CITIGROUP 1500 4

905 C ADM 41

TOTAL: 20,484 20,484

MONTH TO DATE: 20,484

JPMORGAN STOPPED 8995/20,464

GOLD: NUMBER OF NOTICES FILED FOR FEBRUARY/2026: 20,489 CONTRACTs NOTICES FOR 2,048,900 OZ or 63.713 TONNES

total notices so far: 20,484 contracts for 2,048,900 OR 63.713 tonnes)

SILVER NOTICES: 1881 NOTICE(S) FILED FOR 9.405 MILLION OZ OZ/

total number of notices filed so far this month : 1881 CONTRACTS (NOTICES) for 9.405 million oz

SILVER//OUTLINE

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER!@

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 95.399 TONNES OF GOLD.

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

AND NOW FEBRUARY: INITIAL STANDING FOR GOLD: 95.399 TONNES!!

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB.

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 744 CONTRACTS OI TO 156,028 AND CLOSER TO TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 901 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 901 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 744 CONTRACTS AND ADD TO THE 901 E.FP. ISSUED

WE OBTAIN A SMALL SIZED GAIN OF 157 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR GAIN OF $2.80 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 0.785 MILLION PAPER OZ

OCCURRED DESPITE OUR GAIN IN PRICE.OF $2.80

2.ASIAN AFFAIRS JAN 30/2025

SHANGHAI CLOSED DOWN 40.04 PTS OR 0.96%

//Hang Seng CLOSED DOWN 580.98 PTS OR 2.08%

// Nikkei CLOSED DOWN 2.60 PTS OR 0.00%

//Australia’s all ordinaries CLOSED DOWN 0.88%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.9502

/ OFFSHORE CLOSED DOWN AT 6.9492 Oil DOWN TO 64.87 dollars per barrel for WTI and BRENT UP TO 69.01 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING DOWN TO 6.9502 OFFSHORE YUAN TRADING DOWN TO 6.9492 ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

:GOLD

FEB 2

FEB 2026 CONTRACT MONTH

GOLD

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 1 ENTRIES customer withdrawals: i) Out of JPMorgan: 128,607.000 oz 4000 kilobars |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER NIL xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 20489 notice(s) 2,048,900 OZ 63.729 TONNES TONNES OF GOLD |

| No of oz to be served (notices) | 10,182 contracts 1018200 OZ 32.17 TONNES |

| Total monthly oz gold served (contracts) so far this month | 20,489 notices 2,048,900 oz 63.729 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

DEPOSITS/CUSTOMER

customer withdrawals:

Out of JPMorgan:

128,607.000 oz

4000 kilobars

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 4

DEALER TO CUSTOMER:

a) Manfra: 193,731.033 oz

b) JPMorgan: 10,138.442 oz

CUSTOMER TO DEALER

C) Malca 59,222.142 oz oz

d) JPMorgan 10,138.442 oz

net to the dealer (reg 253.295 thousand oz)

chaos inside the comex

AMOUNT OF GOLD STANDING FOR FEBRUARY

THE FRONT MONTH OF FEBRUARY STANDS AT 30,671 CONTRACTS FOR A LOSS OF 8001 CONTRACTS.

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,568,117.821 oz 48.77 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 35,748,596/324 oz

TOTAL REGISTERED GOLD 19,038,541.229 or 592.17 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 16,710,155.095 OZ//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 17,470,424 oz ((REG GOLD- PLEDGED GOLD)=

543.403 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

FEB LOST A HUGE 8001 CONTRACTS DOWN TO 30,671 CONTRACTS

THUS BY DEFINITION, THE INITIAL AMOUNT OF GOLD STANDING FOR FEBRUARY IS AS FOLLOWS

30,671 NOTICES X 100 OZ PER CONTRACT

EQUALS

3,067,100 OZ OR 95.399 TONNES

MARCH GAINED 408 CONTRACTS UP TO 4246

We had 20,489 contracts filed for today representing 2,048,900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 11,959 notices issued from their client or customer account. The total of all issuance by all participants equate to 20,489 contract(s) of which 8985 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for FEB /2026. contract month, we take the total number of notices filed so far for the month (20,489) to which we add the difference between the open interest for the front month of FEB ( 30,671 CONTRACTS) minus the number of notices served upon today (20,489 x 100 oz per contract) equals 3,067,100 OZ OR (95.399Tonnes of gold)

thus the INITIAL standings for gold for the FEB contract month: No of notices filed so far (20,489 x 100 oz +we add the difference for front month of FEB (30,671 OI} minus the number of notices served upon today (20489 x 100 oz) which equals 3,067,100 OR 905.399 TONNES

new total of gold standing in FEB is 95.399 TONNES

TOTAL COMEX GOLD STANDING FOR FEB 95.399 TONNES TONNES WHICH IS STRONG FOR THIS NORMALLY VERY NON ACTIVE ACTIVE DELIVERY MONTH OF JANUARY.

volume THURSDAY confirmed 662,000 mega mega mammoth/

SILVER

FEB COMEX CONTRACT

FEB 2/2026

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 5 entries i) out of Asahi: 162,661.100 oz ii) out of CNT 1126,271.973 oz iii) Out of Delaware 1088.624 oz iv) Out of JPMorgan: 965,414.800 oz v) Out of Loomis; 134,679.156 oz total withdrawn 2,390,115.353 oz everyday at least 2 million oz leaving the comex is being drained of silver |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | 1 ENTRIES DEPOSIT ENTRIES/CUSTOMER ACCOUNT 1 ENTRIES i) Into CNT 23l,582.400 oz total deposit 23,582.400 oz |

| No of oz served today (contracts) | 1881 CONTRACT(S) ( 9.405 million OZ |

| No of oz to be served (notices) | 820 Contracts (4.100 MILLION oz) |

| Total monthly oz silver served (contracts) | 1881 contracts 9.405 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

1 ENTRIES

i) Into CNT 23l,582.400 oz

total deposit 23,582.400 oz

withdrawals: customer side/eligible

5 entries

i) out of Asahi: 162,661.100 oz

ii) out of CNT 1126,271.973 oz

iii) Out of Delaware 1088.624 oz

iv) Out of JPMorgan: 965,414.800 oz

v) Out of Loomis; 134,679.156 oz

total withdrawn 2,390,115.353 oz

everyday at least 2 million oz leaving

the comex is being drained of silver

the comex is being drained of silver

adjustments: / / 4

first 4: dealer to customer:

a) Asahi: 34,903.700 oz

b) Brinks 944,716.700 oz

c) JPMorgan 1,640,683.900 oz

d) Manfra: 929,418.867 oz

e/ customer to dealer CNT 272,290.590 oz

net loss from the dealer 3.277 million oz

TOTAL REGISTERED SILVER: 104.879MILLION OZ//.TOTAL REG + ELIGIBLE. 405.886 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR FEBRUARY

silver open interest data:

FRONT MONTH OF FEB /2026 OI: 2701 OPEN INTEREST CONTRACTS FOR A GAIN OF 129 CONTRACTS.

THUS BY DEFINITION, THE INITIAL AMOUNT OF SILVER WILLING TO STAND AT THE COMEX IN FEBRUARY IS AS FOLLOWS

2701 NOTICES FILED ON FIRST DAY NOTICE X 5000 OZ PER NOTICE

EQUALS

13.505 MILLION OZ

WHICH IS HUGE FOR A FEBRUARY!!

MARCH LOST 1071 CONTRACTS DOWN TO 97,940

APRIL GAINED 67 CONTRACTS UP TO AN OI 408 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1831 or 9.405 MILLION oz

CONFIRMED volume; ON THURSDAY 226,975 mammoth//

AND NOW FEB. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in FEBRUARY. we take the total number of notices filed for the month so far at 1881 X5,000 oz = 9.405 MILLION oz

to which we add the difference between the open interest for the front month of FEBRUARY (2701) AND the number of notices served upon today 1881)x (5000 oz)

Thus the standings for silver for the FEBRUARY 2026 contract month: (9854)Notices served so far) x 5000 oz + OI for the front month of FEB(2701) minus number of notices served upon today (1881 )x 5000 oz equals silver standing for the JANUARY.contract month equating to 13.505 MILLION OZ

NEW STANDING: 13.505 MILLION OZ WHICH IS HUGE FOR A GENERALLY SMALL DELIVERY MONTH OF FEBRUARY.

New total standing: 13.505 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

THJE 35 NOTICES OWING WAS SERVED AT 10 PM THURSDAY TO BALANCE THE AMT STANDING AT 49.545 MILLION OZ)

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 104.877 million oz of registered silver

JPMorgan as a percentage of total silver: 171.559/408.253.million: 41.91%

THERE IS NOW A RUN ON THE COMEX SILVER

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

JAN 30/2026/WITH GOLD DOWN $590.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.43 TONNES OF GOLD OUT OF THE GLD /// ///INVENTORY RESTS AT 1086.63 TONNES

JAN 29/2026/WITH GOLD UP $23.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1089.96 TONNES

JAN 28/2026/WITH GOLD UP $218.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.85 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1087.38 TONNES

JAN 27/2026/WITH GOLD UP $2.55 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1086.53 TONNES

JAN 26/2026/WITH GOLD UP $106.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 6.89 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1086.53 TONNES

JAN 23/2026/WITH GOLD UP $69.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSUT OF 2.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1079.66 TONNES

JAN 22/2026/WITH GOLD UP $75.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT WITHDRAWAL OF 4.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1077.66 TONNES

JAN 21/2026/WITH GOLD UP $74.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 20/2026/WITH GOLD UP $142.90 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 6.86 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 16/2026/WITH GOLD DOWN $27.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .57 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.807TONNES

JAN 15/2026/WITH GOLD DOWN $9.85 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 14/2026/WITH GOLD UP $34.35 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 13/2026/WITH GOLD DOWN$11.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 12/2026/WITH GOLD UP $104.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.25 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1070,80TONNES

JAN 9/2026/WITH GOLD UP $49.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.58 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1064.55 TONNES

JAN 8/2026/WITH GOLD DOWN $0.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 7/2026/WITH GOLD DOWN $38.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 6/2026/WITH GOLD UP $47.00 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 5/2026/WITH GOLD UP $122.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 2/2026/WITH GOLD DOWN $10.10 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1070.56 TONNES

DEC 31/WITH GOLD DOWN $42.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 30/WITH GOLD UP $41.50 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 29/WITH GOLD DOWN $190.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,13 TONNES

DEC 26/WITH GOLD UP $39.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1068.27 TONNES

DEC 24/WITH GOLD UP $2.15 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 23/WITH GOLD UP $52.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT DEPOSIT OF 12.12 TONNES OF GOLD INTO THE GLD/// /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 22/WITH GOLD UP $80,25 TODAY/NO CHANGES IN GOLD AT THE GLD: // /// ///INVENTORY RESTS AT 1052.54 TONNES

GLD INVENTORY: 1086.53 TONNES, TONIGHTS TOTAL

SILVER

JAN 30 WITH SILVER DOWN $37.04 HUGE CHANGES IN SILVER AT THE SLV:A FRAUDULENT WITHDRAWAL OF 3.625 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 499.087 MILLION OZ /

JAN 29 WITH SILVER UP $2.80 HUGE CHANGES IN SILVER AT THE SLV:A FRAUDULENT WITHDRAWAL OF 6,798 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 502.712 MILLION OZ /

JAN 28 WITH SILVER UP $5.60 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 4.078 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 509.510 MILLION OZ /

JAN 27 WITH SILVER DOWN $7.00 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 4.17 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 513.598 MILLION OZ /

JAN 26 WITH SILVER UP $12.92 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 0.454 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 517.758 MILLION OZ /

JAN 23 WITH SILVER UP $4.91 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.998 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 517.758 MILLION OZ /

JAN 22 WITH SILVER UP $3.20 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.812 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 519.752 MILLION OZ /

JAN 21 WITH SILVER DOWN $1.44 NO CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 20 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL DEPOSIT OF 5.166 MILLION OZ INTO THE SLV///. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 16 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL WITHDRAWAL OF 5.401 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 516.298MILLION OZ //

JAN 15 WITH SILVER UP $1.00 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 522.199MILLION OZ //

JAN 14 WITH SILVER UP $4.64 NO CHANGES IN SILVER AT THE SLV: /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 13 WITH SILVER UP $1.70 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 0.816MILLION OZ OUT OF THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 12 WITH SILVER UP $5.50 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.229MILLION OZ INTO THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 525,598MILLION OZ //

JAN 9 WITH SILVER UP $4.15 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 6.119 MILLION OZ INTO THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 524.329MILLION OZ //

JAN 8/WITH SILVER DOWN $2.40/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 518.210MILLION OZ //

JAN 7/WITH SILVER DOWN $2.78/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 525.730 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 5/WITH SILVER UP $5.90 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 2/WITH SILVER UP $0.22 /HUGE CHANGES IN SILVER AT THE SLV: A SMALL WITHDRAWAL OF 0.363 MILLION OZ OUT THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 31/WITH SILVER DOWN $6.41 /HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE DEPOSIT OF 4.806 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 30/WITH SILVER UP $6.89 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.72 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 524.248 MILLION OZ //

DEC 29/WITH SILVER DOWN $5.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.814 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 526,968 MILLION OZ //

DEC 26/WITH SILVER UP $4.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.813 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 528.782 MILLION OZ //

DEC 24/WITH SILVER UP $0.95 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 3.083 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 530.595MILLION OZ //

DEC 23/WITH SILVER UP $2.40 /HUGE CHANGES IN SILVER AT THE SLV: A FRAUDULENT DEPOSIT OF 17.13 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 533.678 MILLION OZ //

DEC 22/WITH SILVER UP $1.28 /HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.541 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 516.541 MILLION OZ //

DEC 19/WITH SILVER UP $2.06 /NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 18/WITH SILVER DOWN $1.13/NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

CLOSING INVENTORY 499.087 MILLION OZ OF SILVER…

PHYSICAL GOLD/SILVER

1/PETER SCHIFF

JOHN RUBINO

MATHEW PIEPENBURG/EGON VON GREYERZ

ALASDAIR MACLEOD

ling us.

3.CHRIS POWELL AND HIS GATA DISPATCHES

Warsh knows the score about gold price suppression. Will he share it?

Submitted by admin on Fri, 2026-01-30 11:04 Section: Daily Dispatches

11:06a ET Friday, January 30, 2026

Dear Friend of GATA and Gold (and Silver):

Is President Trump’s nominee for chairman of the Federal Reserve, former Fed Board of Governors member Kevin M. Warsh, really a “hawk” on interest rates, as mainstream financial news organizations are claiming as an explanation for the sharp declines in monetary metals prices in the last 24 hours?

While Warsh used to be considered “hawkish” on rates, his more recent statements have been more favorable to reducing them. Would the president be nominating someone he considered a “hawk” on rates after spending months demanding lower rates and deriding Fed Chairman Jerome Powell in the crudest terms for not lowering them faster?

Mainstream news organizations are also hailing Warsh as someone who will defend “central bank independence,” the euphemism for the Fed’s subservience to the investment banking industry.

In any case, two things can be said about Warsh as a matter of indisputable fact, though they aren’t likely to be acknowledged by mainstream news reports.

First is that Warsh knows all about U.S. gold price suppression policy. He volunteered his knowledge to GATA’s lawyer, William J. Olson of Vienna, Virginia, in September 2009 during GATA’s freedom-of-information litigation for access to the Fed’s gold records.

Warsh wrote to Olsen that among the records the Fed was insisting on keeping secret from GATA were records of gold swap arrangements between the Fed and foreign banks:

http://www.gata.org/node/7819

Two years later in December 2011 Warsh wrote an essay in The Wall Street Journal about what he called “financial repression” by governments. Warsh wrote: “Policy makers are finding it tempting to pursue ‘financial repression’ — suppressing market prices they don’t like,” adding, “Efforts to manage and manipulate asset prices are not new”:

http://www.gata.org/node/10839

Soon after Warsh’s essay was published your secretary/treasurer reached him by e-mail at Stanford University in California and asked him if he had learned about “financial repression” through his service at the Fed. Your secretary/treasurer also asked him if he would specify the asset prices being manipulated by policy makers.

Warsh cordially wished your secretary/treasurer a nice day.

So Warsh knows the score about gold price suppression and market rigging by government generally. Will he ever risk sharing it with the public as a matter of democratic accountability? And how long will he be in office as Fed chairman before Trump starts denouncing him as stupid and worse for not following presidential preferences, the fate that has befallen the president’s previous appointee as Fed chairman?

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Fed chief was asked about U.S. ‘losing credibility,’ soaring gold. He punted

Submitted by admin on Thu, 2026-01-29 20:02 Section: Daily Dispatches

By Eva Roytburg

Fortune, New York

Thursday, January 29, 2026

Fed Chair Jerome Powell surprised some investors Wednesday afternoon with his comments about the gold and silver rally. The two precious metals, the most classic of the “safe-haven” assets, have the tangibility and inherent scarcity to act as a hedge in moments of turmoil, particularly when investors worry that politics or policy could undermine the value of the dollar or U.S. government bonds.

That is why the metals’ relentless rally to record highs since late last year — gold is up 84% year over year and silver up a whopping 245% — has drawn attention from analysts. In recent months, market commentary has split the move into two distinct narratives.

“The argument can be made that we’re losing credibility or something,’ Powell acknowledged before insisting that’s “simply not the case.” Just look at where inflation expectations are, he pointed out: “Our credibility is right where it needs to be.”

If investors believed inflation would remain persistently above the Fed’s 2% target, the case for a structural move into gold would be stronger. Instead, Powell noted, short-term inflation expectations have “come way down” while longer-term measures remain consistent with 2% inflation.

“We don’t take much message macroeconomically from that,” Powell said in response to a question from CNN’s Matt Egan about gold and silver during his press conference. Investors feel differently, with gold and silver at the heart of two contentious trades. …

… For the remainder of the report:

* * *

nd

Treasury secretary says Trump administration still pursues ‘strong dollar policy’

Submitted by admin on Wed, 2026-01-28 19:24 Section: Daily Dispatches

Monetary metals investors may say: Please keep at it!

* * *

By Claire Jones, Ian Smith, and Kate Duguid

Financial Times, London

Wednesday, January 28, 2026

The U.S. currency rebounded today after U.S. Treasury Secretary Scott Bessent said Washington was still pursuing a “strong dollar policy” and was not planning an intervention to boost the Japanese yen.

The dollar jumped as much as 0.9% against the euro and 1% against the yen after Bessent said in an interview with CNBC that he expected the U.S. currency to appreciate.

The U.S. always has a strong dollar policy, but a strong dollar policy means setting the right fundamentals,” Bessent said, adding that the administration’s policies were making the U.S. “the best place to come.”

“If we have sound policies, the money will flow in and we are bringing down our trade deficit, so automatically that should lead to more dollar strength over time,” Bessent said.

The remarks come after U.S. President Donald Trump said on Tuesday evening that the recent fall in the U.S. currency was a “great” development, pushing the dollar to its lowest level in four years against a basket of peers. …

… For the remainder of the report:

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS / AND TODAY;S 256

LIVE FROM THE VAULT YOU TUBE: 257

5. COMMODITY REPORT//:silver

2.ASIAN AFFAIRS JAN 30/2025

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

SHANGHAI CLOSED DOWN 40.04 PTS OR 0.96%

//Hang Seng CLOSED DOWN 580.98 PTS OR 2.08%

// Nikkei CLOSED DOWN 2.60 PTS OR 0.00%

//Australia’s all ordinaries CLOSED DOWN 0.88%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 6.9502

/ OFFSHORE CLOSED DOWN AT 6.9492 Oil DOWN TO 64.87 dollars per barrel for WTI and BRENT UP TO 69.01 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING DOWN TO 6.9502 OFFSHORE YUAN TRADING DOWN TO 6.9492 ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS WEAKER//OFF SHORE YUAN TRADING DOWN AGAINST US DOLLAR/ AND THUS WEAKER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 6.9502

OFFSHORE YUAN: DOWN TO 6.9492

HANG SENG CLOSED DOWN 580.98 PTS OR 3.08%

2. Nikkei closed DOWN 2.60 PTS OR 0.00%

WEST TEXAS INTERMEDIATE OIL UP 64.87

BRENT; 69.01

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 96.45 /// EURO FALLS TO 1.1919 DOWN 48 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +2.2560/ DOWN 1 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 154.18… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.640 UP 2 FULL BASIS PTS. AND STILL VERY TROUBLESOME

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and BRENT DOWN this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.8520 Italian 10 Yr bond yield UP to 3.475 SPAIN 10 YR BOND YIELD UP TO 3.222

3i Greek 10 year bond yield UP TO 3.367

3j Gold at $5022 Silver at: 100.22 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble UP 0 AND 49/100 roubles/dollar; ROUBLE AT 75.46

3m oil (WTI) into the 64 dollar handle for WTI and 69 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 153.45 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.2860% UP 3 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.640 UP 2 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7696 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9193 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.269 UP 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.902 UP 5 BASIS PTS/

USA 2 YR BOND YIELD: 3.563 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 43.50 UP 7 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.5240 UP 1 PTS

30 YR UK BOND YIELD: 5.281 UP 1 BASIS PTS

10 YR CANADA BOND YIELD: 3.425 DOWN 1 BASIS PTS

5 YR CANADA BOND YIELD: 2.938 DOWN 1 BASIS PTS.

1a New York Opening report

Stocks Slide, Gold And Bitcoin Tumble After Trump Taps Warsh As Next Fed Chair

Friday, Jan 30, 2026 – 08:41 AM

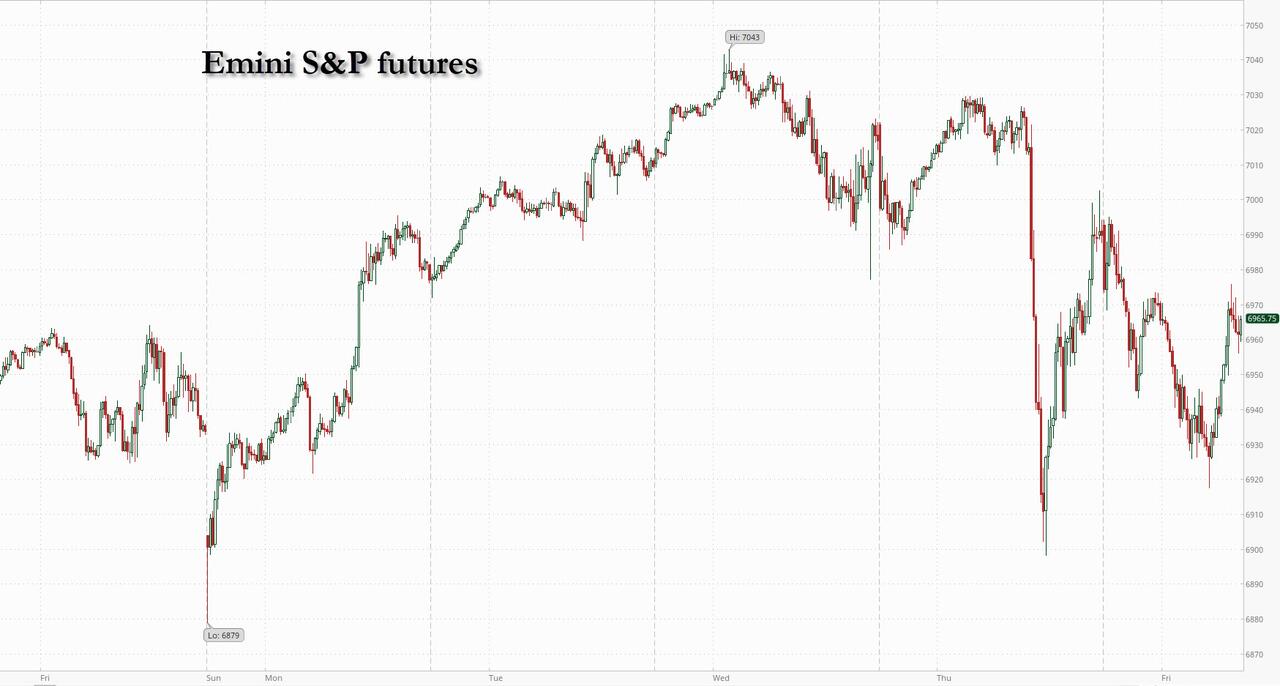

US futures slumped, the dollar rallied sharply, the Treasury curve steepened with 10Y yield rising as high as 4.28% and gold and bitcoin tumbled on what was at first speculation and then confirmation, that President Trump is nominating Kevin Warsh – widely viewed as the most hawkish of the handful of candidates – as the next Fed chair. As of 8:00am ET, S&P futures slid 0.4% but were well off session lows double that, while Nasdaq futures dropped 0.6% as markets brush aside strong Apple results. Pre-market, almost all Mag 7 stocks are lower with META (-1.5%), GOOGL (-1.4%) and NVDA (-1.4%) the biggest laggards; TSLA added +2.0%, the only exception in Mag 7. European stocks are all green while Asian equities join in the risk exodus, with Hong Kong indexes the biggest losers. Kospi flips an early 1.9% rally to a loss before turning positive again. The US Dollar is higher to 96.62; the yield curve steepened (30y +2.8bp vs. 2y -0.6bp) on the market view that Warsh is more hawkish than Trump expects. Commodities are mostly lower: Brent futures tumbled back below $70 a barrel following a three-day rally, while precious metals tumbled – gold fell 5% to 5100, silver plunged -12% under $100 while base metals are higher. US economic calendar includes December PPI (8:30am) and January MNI Chicago PMI (9:45am). Fed speaker slate includes Miran (11:10am), Musalem (1:30pm), Miran (3pm) and Bowman (5pm).

In premarket trading, Mag 7 stocks are mostly lower: Apple (AAPL) slips 0.7% after the iPhone maker warned that rising component costs are threatening to squeeze margins. The company also posted its largest first-quarter sales growth in over four years, driven by strength in its closely-watched iPhone segment (Tesla +2.3%, Microsoft +0.5%, Amazon -0.7%, Nvidia -0.9%, Alphabet -0.5%, Meta -1.2%)

- Precious metals miners tumble, set to extends Thursday’s losses, as gold and silver sell off heavily.

- American Express (AXP) falls 3% after the payment company reported earnings per share for the fourth quarter that missed the average analyst estimate.

- Charter Communications (CHTR) rises 6% after the cable operator reported a gain in pay-TV customers. Its fourth-quarter earnings also beat expectations.

- Deckers Outdoor (DECK) rises 12% after the owner of the Ugg and Hoka footwear brands raised its annual earnings and sales forecast, beating the average analyst estimate. Analysts note strength in the retailer’s direct-to-consumer channels in the US.

- KLA Corp. (KLAC) falls 8% after the chip company reported results for the second quarter and gave an outlook. The stock has surged 39% so far this year as of Thursday’s close.

- MaxLinear (MXL) falls 14% after the semiconductor device company’s results were seen as disappointing in key business lines.

- Olin (OLN) falls 8% after the maker of ammunition and chemicals said it anticipates first quarter 2026 adjusted Ebitda will be lower than fourth quarter levels.

- Sandisk (SNDK) rises 24% as the computer hardware and storage company’s second-quarter revenue beat expectations. Raymond James analyst upgraded the stock to outperform from market perform.

- Schneider National (SNDR) falls 19% after the trucking company reported adjusted earnings per share below Wall Street expectations.

- Market conditions were softer than expected in much of the fourth quarter, creating a “very truncated peak season,” CEO Mark Rourke said.

- SoFi Technologies (SOFI) rises 5% after the online lender reported net interest income and adjusted net revenue above estimates.

- Stryker (SYK) gains 1% after the maker of surgical products gave forecasts for adjusted revenue and organic growth for the full year, where the midpoints of the outlook topped the average analyst estimate.

- Verizon Communications (VZ) rises 1% after the telecom company’s fourth-quarter results beat expectations on key metrics, including wireless customers. It also gave an outlook that is ahead of the consensus on metrics like adjusted earnings and free cash flow.

In corporate news, US law enforcement is investigating allegations that Meta personnel can access WhatsApp messages, despite the company’s claims that the chat service is private and encrypted. SpaceX is said to be considering a potential merger with Tesla or an alternative combination with AI firm xAI. An IPO is also possible with SpaceX said to weigh a June listing, around Musk’s birthday, and could seek to raise as much as $50 billion. In other AI news, Amazon is said to be in talks to invest as much as $50 billion in OpenAI and expand an agreement that involves selling computer power to the AI startup.

US stock futures slumped as Trump nominated Kevin Warsh as Fed chair, the candidate who once was vocally in favor of shrinking the Fed’s balance sheet and limiting its influence, hardly what Trump wants as he pushes the Fed to ease financial conditions aggressively.

The choice of Warsh as Trump’s nomination to be the next Federal Reserve chair is viewed as more hawkish than other contenders.

Long viewed as an inflation hawk, his prospects have rippled through markets, with the dollar gaining versus all its major peers while Treasuries fell, led by the long-end as 30-year yields jumped five basis points.

“We advise against overdoing the Warsh hawkish trade across asset markets, and even see some risk of a whipsaw,” wrote Evercore ISI economists led by Krishna Guha. “We see Warsh as a pragmatist, not an ideological hawk in the tradition of the independent conservative central banker.”

Not everyone agreed: “A Fed led by Warsh is likely to pursue a more cautious, gradual approach to monetary policy rather than aggressive rate cuts,” said Dilin Wu, a research strategist at Pepperstone. “Markets that have priced in a more rapid rate cut — particularly high-valuation tech stocks — may face headwinds.”

While Apple earnings reassured tech investors after a volatile Thursday that included a Microsoft selloff that wiped out $357 billion in value, the second-largest loss for a single session in stock market history, the sentiment boost was quickly erased amid fears Warsh could soon pull the punchbowl. Apple reported the fastest year-on-year revenue growth in 16 quarters, bizarrely driven by China where it’s sales had been in steady decline, and is projecting between 13% and 16% sales growth for the March quarter, the highest since March 2021. Focus on the conference call centered on costs, specifically surging memory prices, although Apple’s midpoint of gross margin guidance for fiscal 2Q at 48.5% would be higher than 1Q’s reported 48.5%.

“I see today’s fall in Nasdaq futures as a short-term move and see this as a buying opportunity, should there be a bigger fall,” said David Rainville, portfolio manager at Sycomore AM. “I don’t think that having someone slightly more hawkish than expected at the Fed is a bad thing in itself for tech on the long run.”

Memory prices remain in focus with Sandisk’s blowout guidance, with a surge in after hours trading only adding to gains that have lifted the storage and memory maker more than 1,100% over the last six months. The rally has pushed it to the top of the S&P 500 leaderboard, with the second-, third- and fourth-best performers exposed to the same dynamic.

BofA strategists warn global stocks are overbought, and the proportion of MSCI indexes above key moving averages has breached their sell-signal threshold. Some 89% of MSCI stock indexes traded above their 50-day and 200-day moving averages in the week ended Jan. 28, a Bank of America team led by Michael Hartnett wrote in a note. That breached the 88% threshold that they view as a sell signal. Inflows into US stocks resumed in the week at $9.2 billion according to BofA citing EPFR Global data. Gold had the biggest inflows since October at $6.7 billion.

Elsewhere, Trump also reached a tentative deal with Senate Democrats to avert a disruptive US government shutdown, though lawmakers are almost certain to miss the Friday night deadline to enact the measure. Oil retreated after a three-day rally as risk-off sentiment swept across broader markets, even as Trump’s escalating threats against Iran kept the market on edge.

Colgate-Palmolive, Chevron, Exxon Mobil, American Express and Verizon are among companies expected to report results before the market opens.

European shares rise Friday, supported by positive earnings news, pushing the Stoxx 600 up 0.3% to 608.98. The region’s miners are among the biggest laggards after the copper price retreated from record highs, while travel and leisure shares outperform. Here are the biggest movers Friday:

- Alten shares jump as much as 19%, the most since 2002, after the technology consulting firm reported fourth-quarter revenue growth that analysts described as surprisingly strong

- Electrolux shares jump as much as 22%, their biggest intraday gain on record, after the Swedish home appliances firm reported strong fourth-quarter earnings

- Swatch shares gain as much as 8.1%, the most since October, as analysts note encouraging revenue trends that overshadow an operating profit miss. The Swiss watch maker also said it expects substantial growth

- Adidas gains as much as 6.2%, the most since April, after the sportswear company reported preliminary fourth-quarter operating profit that beat consensus estimates and announced a share buyback program

- Elis gains as much as 3.6% to trade at the highest in over two months, after the French cleaning services group delivered robust organic growth in the fourth quarter, with Southern Europe and Latin America performing strongly

- Raiffeisen shares rise as much as 1.9% after the Austrian lender reported dividends per share for the full year that beat estimates and forecasted a stable return on equity excluding Russia

- Signify slumps as much as 15%, the most since 2020, after the lighting specialist issued a profit warning for 2026, with adjusted Ebita margin now seen significantly below analyst expectations

- SKF falls as much as 7.6%, the most since November, after the Swedish ball-bearings maker reported its latest earnings. Analysts flagged costs and tax effects related to the firm’s announced separation of its automotive arm

- The Stoxx 600 Basic Resources is the worst-performing subsector on the European bourse on Friday, shedding as much as 3.8%, after copper prices sank from a record

- Antofagasta declined as much as 7.1% in London, the most since July, after UBS cut the base metals miner to neutral from buy, saying the catalysts for the stock have mostly “played out”

- Maersk shares fall as much as 2.9% after Nordea downgraded the Danish shipping and logistics firm to sell from hold, seeing downside risk to earnings

- Billerud drops as much as 17%, hitting the lowest since February 2014, as fourth-quarter results from the Swedish paper company miss expectations on continued European weakness

Unlike Europe, Asian equities fell, led by technology stocks, as investors weighed rising costs tied to artificial intelligence and prospects for US rate cuts under a new Federal Reserve chair. The MSCI Asia Pacific index fell as much as 1.2%, with TSMC, Alibaba and Tencent among the biggest drags. Benchmarks in Hong Kong and Taiwan dropped more than 1%. Indonesian equities rebounded after a two-day market rout that led to the bourse’s chief stepping down. Investors are also watching an expected dinner hosted by Nvidia CEO Jensen Huang with key supply-chain partners during his visit to Taiwan. Major earnings next week include Alphabet, Amazon.com and Toyota.

In FX, the US dollar pares of 0.6% to 0.3% as markets ponder the prospect of Kevin Warsh being appointed Fed Chair.

In rates, the US yield curve steepens on expectations he would favor a smaller balance sheet, pushing the 2- to 30-year spread wider by about 4bps. The yield on 10-year Treasuries rose one basis point to 4.25%, having earlier risen as high as 4.28%. Money markets added to bets on a rate cut in June, with two reductions priced in for 2026. JGB futures tick higher after Tokyo inflation cools more than expected and 2-year bond auction passes without drama. Australian curve a touch flatter with 10-year yield down 3 bps. German and UK 10-year yields are both up about a basis point, with Bunds digesting a stronger-than-expected fourth-quarter GDP print and turning focus to CPI, as regional releases point to upside risks.

In commodities, Precious metals have had a volatile session, with spot gold and silver briefly slipping below $5,000 and $100 an ounce respectively before climbing back above them, though both remain sharply lower on the day. Base metals have also come under pressure to a lesser extent, with LME copper down about 1.6%. Oil retreated as risk-off sentiment swept across broader markets, though Trump’s escalating threats against Iran are keeping the market on edge. Brent traded around $70 a barrel on Friday after climbing above that level in the previous session for the first time since July.

The London Metal Exchange suffered a one-hour delay to the start of trading on Friday after a technical problem, causing confusion among traders after a week of intense volatility and eye-watering price gains.

Bitcoin just won’t stop falling, plunging more than 5% as it extended a rout that gathered pace on Thursday. The token is now down more than 30% from an all-time high reached in October. Over $1.5 billion in bullish positions across all tokens have been liquidated in the past 24 hours, according to CoinGlass data.

Today’s US economic calendar includes December PPI (8:30am) and January MNI Chicago PMI (9:45am). Fed speaker slate includes Miran (11:10am), Musalem (1:30pm), Miran (3pm) and Bowman (5pm).

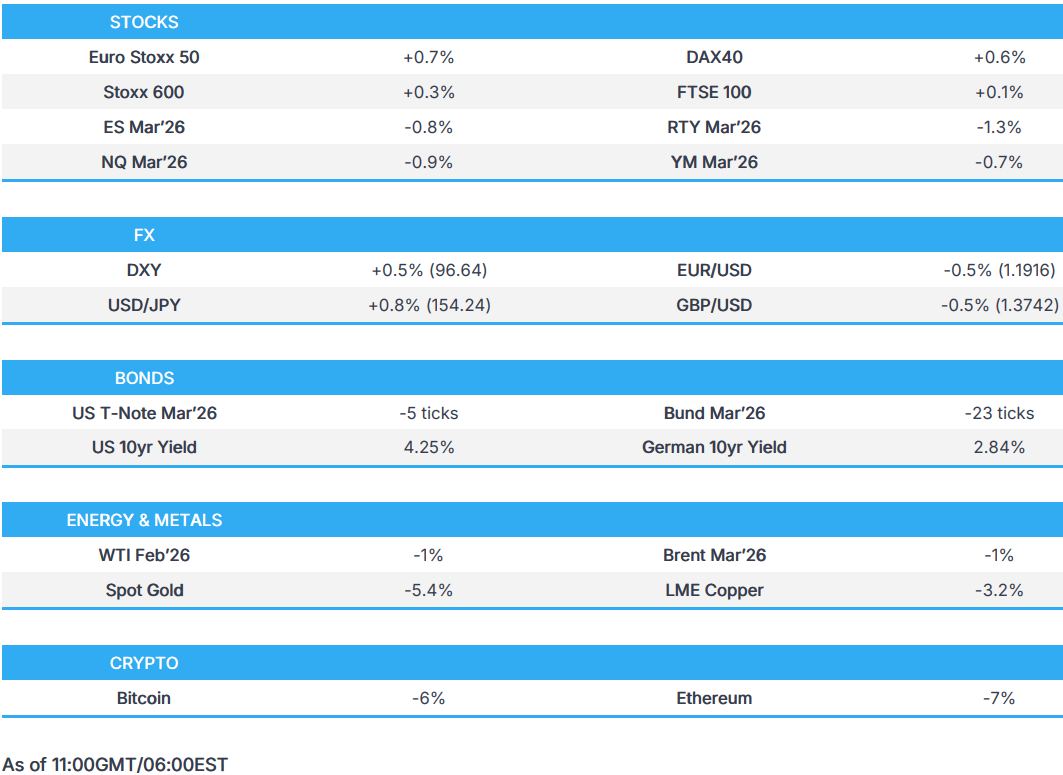

Market Snapshot

- S&P 500 mini -0.4%

- Nasdaq 100 mini -0.6%

- Russell 2000 mini -1.4%

- Stoxx Europe 600 +0.3%

- DAX +0.4%

- CAC 40 +0.3%

- 10-year Treasury yield +2 basis points at 4.25%

- VIX +2.2 points at 19.04

- Bloomberg Dollar Index +0.4% at 1182.92

- euro -0.4% at $1.1919

- WTI crude -1.4% at $64.51/barrel

Top Overnight News

- President Trump said he intends to nominate Kevin Warsh to be the next chair of the Federal Reserve. BBG

- Gold and silver slumped while the dollar rose. A Warsh-led Fed may temporarily cool the greenback-debasement trade by easing concerns over central bank independence. BBG

- President Donald Trump and Senate Democrats reached an agreement to fund the federal government as a Friday midnight deadline for a partial shutdown approaches.: WSJ

- Speaker Johnson said he’s not confident that a government shutdown will be avoided.

- China plans to sell about $29 billion in special bonds to recapitalize some its largest insurers, people familiar said, strengthening the biggest players amid pressure to consolidate. BBG

- Large US companies are set to lay off at least 52,000 workers as the jobs market cools: FT.

- White House said President Trump will sign executive orders at 11:00EST and is participating in a policy meeting at 14:00EST. Trump confirms he’s signing a historic executive order to combat the scourge of addiction and substance abuse.

- China has given its top AI startup DeepSeek approval to buy Nvidia’s H200 artificial intelligence chips with regulatory conditions that are still being finalized. ByteDance, Alibaba, and Tencent had been given permission to purchase more than 400,000 H200 chips in total. RTRS

- Volodymyr Zelenskiy said Ukraine is ready to halt strikes on Russian energy infrastructure if Moscow abides by a US proposal for a weeklong truce. BBG

- Trump warned the UK and Canada against striking new business deals with China, after their leaders visited Beijing this month in an effort to deepen ties. BBG

- The euro-zone’s largest economies all grew at the end of last year. German GDP rose 0.3% in the fourth quarter, beating an initial estimate. Spain reported a speedier-than-expected expansion of 0.8%, while France and Italy also grew. BBG

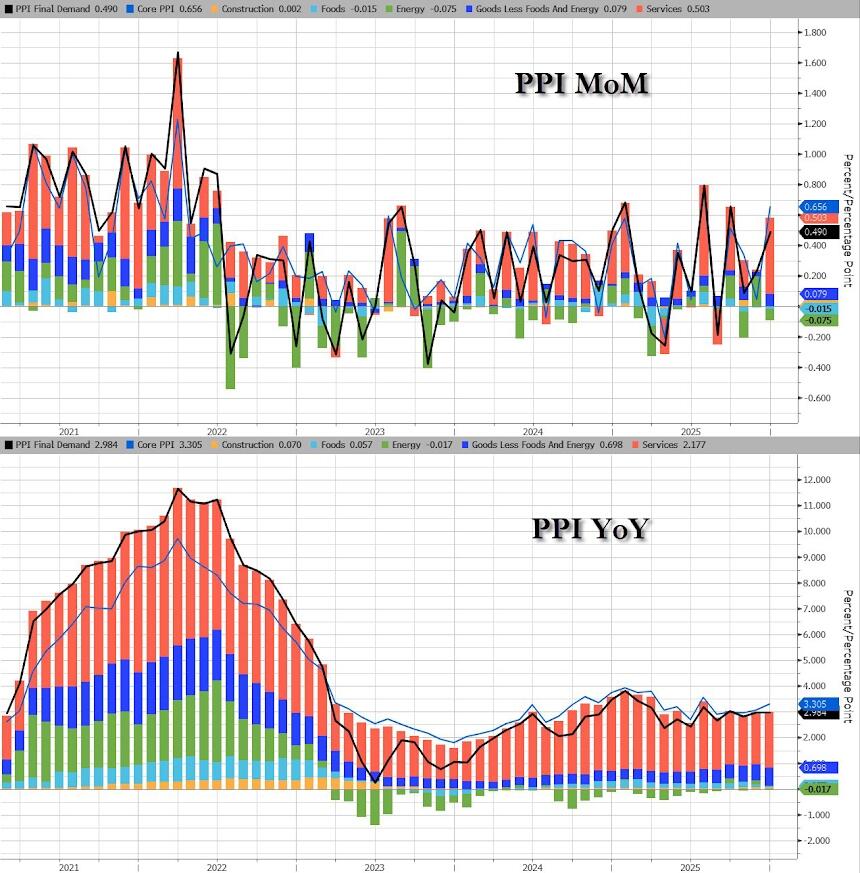

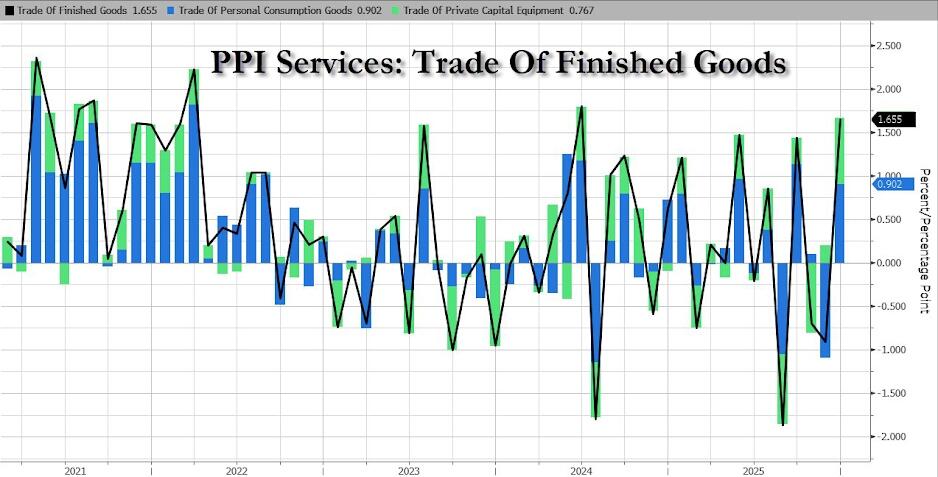

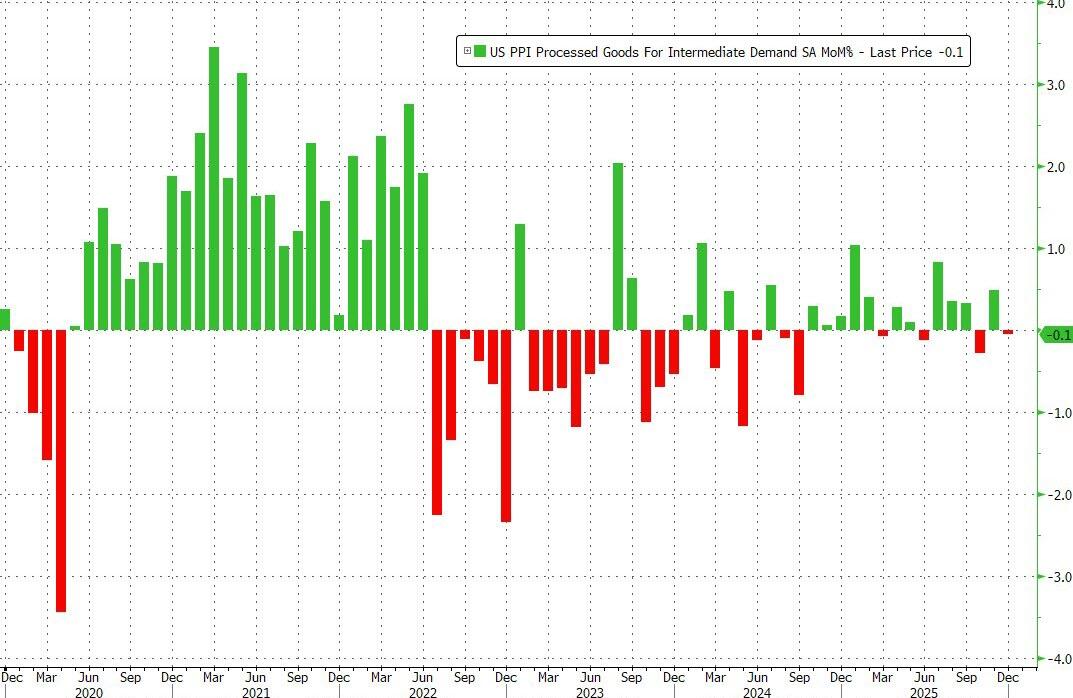

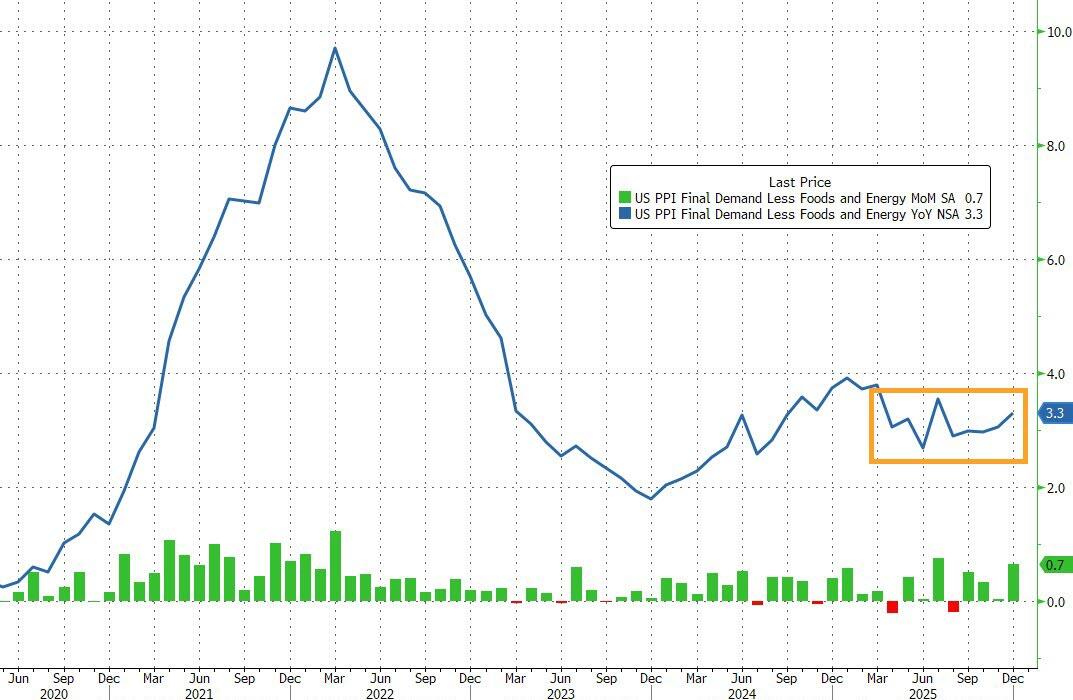

- Headline PPI probably held at 0.2% in December, adding to evidence that tariff price pressure up the supply chain is fading. The core rate likely rose to 0.2% from a flat reading in November. BBG

- Trump sues the IRS and Treasury for $10bln over tax return leaks.

Trade/Tariffs

- China is to lower tariffs on whisky imports to 5% from February 2nd.

- US President Trump said it is ‘very dangerous’ for the UK to get into business with China and even more dangerous for Canada to get into business with China.

- US President Trump threatens to charge Canada a 50% tariff on any and all aircraft sold to the US.

- White House noted that US President Trump signed an executive order declaring a national emergency and establishing a process to impose tariffs on goods from countries that sell or otherwise provide oil to Cuba.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were pressured heading into month-end, as the Apple-related euphoria following record iPhone sales, was dampened as yields gained and the dollar strengthened on reports that the Trump administration is preparing for the nomination of Kevin Warsh as the next Fed Chair. ASX 200 was dragged lower by underperformance in miners and resources stocks as metal prices took a hit. Nikkei 225 swung between gains and losses following a slew of data releases, including softer-than-expected Tokyo CPI, better-than-expected Industrial Production and weak Retail Sales, but with the downside in the index cushioned by a weaker currency. Hang Seng and Shanghai Comp underperformed with little fresh drivers and indirect pressure from US President Trump, who warned of dangers for the UK and Canada regarding getting into business with China, while CK Hutchison shares were hit after reports that the Panama Supreme Court ruled the Co.’s ports contract is unconstitutional.

Top Asian News

- The probe into the Air India crash leans toward deliberate pilot action, Bloomberg reported.

- Hitachi (6501 JT) is reportedly seeking a buyers for its data storage business, according to Bloomberg.

- LG Electronics (066570 KS) final Q4 (KRW) loss 828bln, oper. loss 109bln (prelim. loss 109bln), rev. 23.9tln (prelim. 23.9tln).

European equities (STOXX 600 +0.3%) have opened mostly on a firmer footing. Strength comes amid a rebound in the DAX 40 (+0.7%) after yesterday’s SAP-induced pressure, a narrative added to by strong Adidas (+5.2%) earnings. European sectors are mostly in the green, leading are Banks, Travel & Leisure and Technology. The former have been underpinned by reports that Kevin Warsh is likely to be the next Fed Chair, which has bolstered global yields. Furthermore, the sector benefits from gains in Caixabank (+4.0%) after the Co. announced that it expects NII to grow in 2026. To the downside, Basic Resources has been weighed down by pressure in metal prices, whilst energy has been pinned down by crude as the complex gives back gains.

Top European News

- UK and China weigh a cross-border asset management scheme to deepen market ties, according to SCMP.

- US Treasury said semi-annual currency report concluded no major US trading partners manipulated currency to gain unfair trade advantage during four quarters through June 2025.

FX

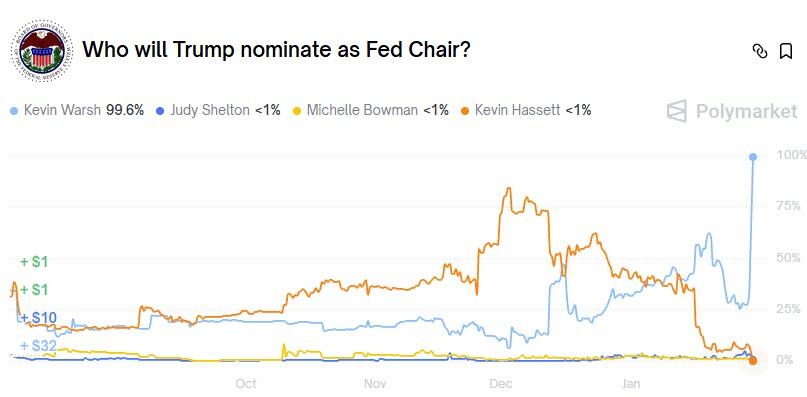

- DXY is on a firmer footing today, following reports that the US administration is leaning towards Kevin Warsh to replace Fed Chair Powell – President Trump said he will make the announcement on Friday. Further details surrounding specific timing is currently light, aside from a couple of appearances towards the later part of the day. As it stands, Warsh’s odds have risen to ~94% (prev. 34% pre-report), whilst Rieder has fallen to ~4% (prev. 34.6% pre-report). DXY currently at the upper end of a 96.16-96.76 range.

- G10s are entirely losing against the firmer Dollar, with clear underperformance in the Aussie as it takes a hit from the pressure seen across underlying metals prices. JPY also towards the bottom of the pile, with USD/JPY currently trading at the upper end of a 152.86-154.38 range. Two factors for the JPY today; a) widening yield differentials as traders weigh a potential Warsh pick, b) softer-than-expected Tokyo CPI, better-than-expected Industrial Production and weak Retail Sales.

- EUR has had a slew of EZ data to digest throughout the day. French GDP contracted a touch from the prior, whilst Spanish, Italy and Germany was a little more upbeat. The German figure itself spurred some minor pressure in the single currency at the time, with the pair then trundling lower as the morning progressed. No move to the EZ GDP metrics, which topped exp. but contracted a touch from the prior. At the same time was the release of several German State CPIs, which on balance was more-or-less in-line with what is expected from the mainland figure due at 13:00 GMT. One point to note is that the NRW state held a bit more of a hawkish skew (0.1% M/M vs prev. 0.0%; mainland expects 0.0%). Currently trades in a 1.1894-1.1974 range.

Fixed Income

- USTs on the backfoot as Kevin Warsh will reportedly be nominated by President Trump later today for the Fed Chair position. Reaction occurring as while Warsh has called for immediate rate cuts, his policy stance is net-hawkish vs the other options available to Trump. While Warsh will likely call for lower policy rates, given his recent commentary and the clear pressure from the administration, the main point of focus will be on the balance sheet, as Warsh has long been critical of QE and a large balance sheet. USTs at a 111-17+ low, a tick above Thursday’s base, which itself is a tick above the WTD 111-15+ low. Amidst this, yields are firmer across the curve, which itself is steeper with action led by the long-end, as while Warsh is a hawkish pick vs the other options, he ultimately will still try to push rates lower in the near term, which may drive inflation and by extension rates higher on a longer horizon.

- That aside, the morning’s stronger-than-expected German Q4 GDP sent Bunds to a 128.07 low with losses of 26 ticks at most. In proximity, we saw the German state CPIs hit ahead of the 13:00GMT mainland figure, the M/M skew was broadly in-line with the mainland consensus, while the Y/Y skew was a hawkish one. For reference, German CPI is expected at 2.0% Y/Y (prev. 1.8%) and 0.0% M/M (prev. 0.0%).

- Gilts gapped lower by 26 ticks before slipping further to a 90.59 trough, given the bias from USTs. Since, the benchmark has rebounded a touch and is holding around 90.90, some 10 ticks above opening levels, but still in the red by c. 15 ticks.

- Japan sold JPY 2.2tln in 2-year JGBs; b/c 3.88x (prev. 3.26x); average yield 1.253% (prev. 1.129%). Lowest accepted price 100.080 vs. prev. 99.920. Weighted average price 100.090 vs prev. 99.942. Tail in price 0.010 vs prev. 0.022.

- Australia sold AUD 1bln 4.25% March 2036 bonds, b/c 3.34, avg. yield 4.8039%.

Commodities

- Crude benchmarks started the Asia-Pac session on the backfoot, partially driven by the stronger greenback, but primarily by comments from President Trump, who said he plans to have talks with Tehran and hopes the US do not have to use the big, powerful ships. WTI dropped to a trough of USD 64.30/bbl following the potential Fed Chair announcement reports re. Warsh, before immediately paring back the entirety of the move. Around 30 minutes later, on the Trump comments, prices steadily dropped, and WTI hit a low of USD 63.65/bbl. Benchmarks have since consolidated in a broad c. USD 1.00/bbl range.

- Precious metals slide as European trade continues, with spot XAU currently trading at USD 5090/oz, nearly USD 500/oz lower from the ATH made in Thursday’s session. The yellow metal briefly lost USD 5k/oz, slipping to a USD 4941/oz trough before rebounding.

- Spot silver has slipped even further and has wiped out the entirety of this week’s gains, to sub-100/oz. This comes following the recent strength in the greenback as Kevin Warsh emerges as the frontrunner for the Fed Chair role, with markets suggesting that he is more hawkish than other candidates such as Rick Rieder. President Trump is set to announce the pick later today.

- Alongside precious metals, base metals have been hit by the stronger dollar, with 3M LME Copper briefly tagging USD 13.1k/t before slightly paring back losses but remaining below USD 13.5k/t. For context, the red metal was trading at USD 14.53k/t just 18 hours ago.

- OPEC+ likely to keep its pause on oil output increases for March at Sunday meeting, according to sources.

- ArcelorMittal (MT NA) and Liberia sign a new long-term mineral development agreement. “The expansion project, which is nearing completion, will see iron ore shipments increase from historic levels of approximately 5 million tonnes per annum (mtpa) to 20 mtpa in 2026 alongside improvements in product quality to higher grade, higher value ore.”. “The Company is also undertaking feasibility studies for further expansion of its iron ore asset beyond 20 mtpa.”.

- Explosion reported in an oil refinery at northwestern Turkish province of Kocaeli, while causes of the explosion at the oil refinery are unknown, according to Al-Arabiya.

- LME trading has now opened following a delay due to technical issues.

- White House clarifies that US sanctions relief for Venezuela covers refining and other downstream activities, but not upstream production and White House official said more announcements on Venezuela sanctions easing are expected.

- London Metal Exchange delays market opening due to technical issues, according to Bloomberg.

Geopolitics: Ukraine

- Russia’s Kremlin said US President Trump personally asked Russian President Putin to halt strikes on Kyiv until Feb 1 and create favourable conditions for negotiations.

- Ukraine’s President Zelensky said the compromise on territory has not yet been reached; Ukraine will not strike Russian energy infrastructure if Russia halts its attacks on Ukraine’s energy infrastructure. Halting strikes on energy targets is a US initiative and a personal proposal of US President Trump. said he is inviting Putin to Kyiv if Putin “dares”. No official ceasefire agreement on energy target exists between both countries. Reiterates readiness for leaders summit in any format, but not in Moscow or Belarus.

Geopolitics: Middle East

- US President Trump said he plans to have talks with Tehran and there are big, powerful ships going to Iran, he hopes they don’t have to use them. said:He told the Iranians ‘no’ to nuclear weapons, stop killing protesters, and that they have to do something.

- US President Trump said have a team headed to Iran.

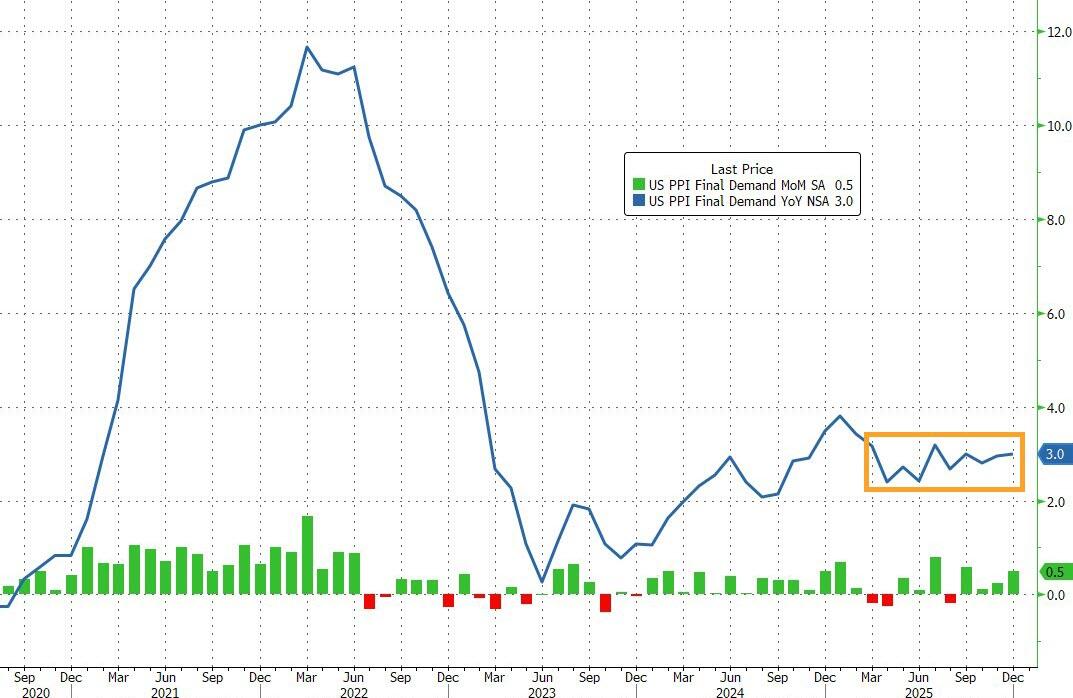

US Event Calendar

- 8:30 am: United States Dec PPI Final Demand MoM, est. 0.2%, prior 0.2%

- 8:30 am: United States Dec PPI Ex Food and Energy MoM, est. 0.2%, prior 0%

- 8:30 am: United States Dec PPI Final Demand YoY, est. 2.76%, prior 3%

- 8:30 am: United States Dec PPI Ex Food and Energy YoY, est. 2.9%, prior 3%

- 9:45 am: United States Jan MNI Chicago PMI, est. 43.65, prior 43.5, revised 42.7

DB’s Jim Reid concludes the overnight wrap

Morning from Milan where Winter Olympics fever was clear from my hotel where a number of the organising committees were setting up yesterday. Unlike Eddie “the Eagle” Edwards I haven’t managed to bluff my way into the Ski Jump to represent team GB next week. My knee surgeon will be relieved. On that topic a couple of weeks ago I suggested I uploaded my scans into AI to ask what was wrong with my knee. It was nearly right and essentially my right knee cap groove has worn away and I’ll probably have a knee cap replacement in the winter (after my back has recovered) that will no doubt be upgraded to a full knee replacement at some point in the next 1-10 years as the rest of the knee is on borrowed time. I have been offered a viscosupplement injection instead that inserts a permanent gel into your knee, although my surgeon said he wouldn’t have it as there hasn’t been enough evidence of its long-term effect on your body! If anyone has had any experience of them let me know. Meanwhile my back surgeon has cleared me to start a gradual return to golf earlier than I thought. So chipping now, three quarter swings in a few weeks and then hopefully ready for the Masters in April. My nerve is still damaged and constantly irritable but he said that could take 12-18 months to repair if it is going to. Frustrating.

One sporting battle that seems to drawing to a close is the race for the Fed Chair nomination. Last night President Trump said he would announce his Fed pick this morning. In the last few hours, Bloomberg reported that the administration was preparing for Kevin Warsh to be nominated, with his odds on Polymarket spiking to 92% as I type. As a reminder, Warsh served as Fed Governor during between 2006 and 2011, a period that included the Fed’s response to the GFC. While his recent comments have been supportive of lower rates, in the past he’s been hawkishly critical of the Fed’s expansive use of its balance sheet. Our US economists published a note on what a Warsh nomination would mean for the Fed shortly before Christmas (see here).

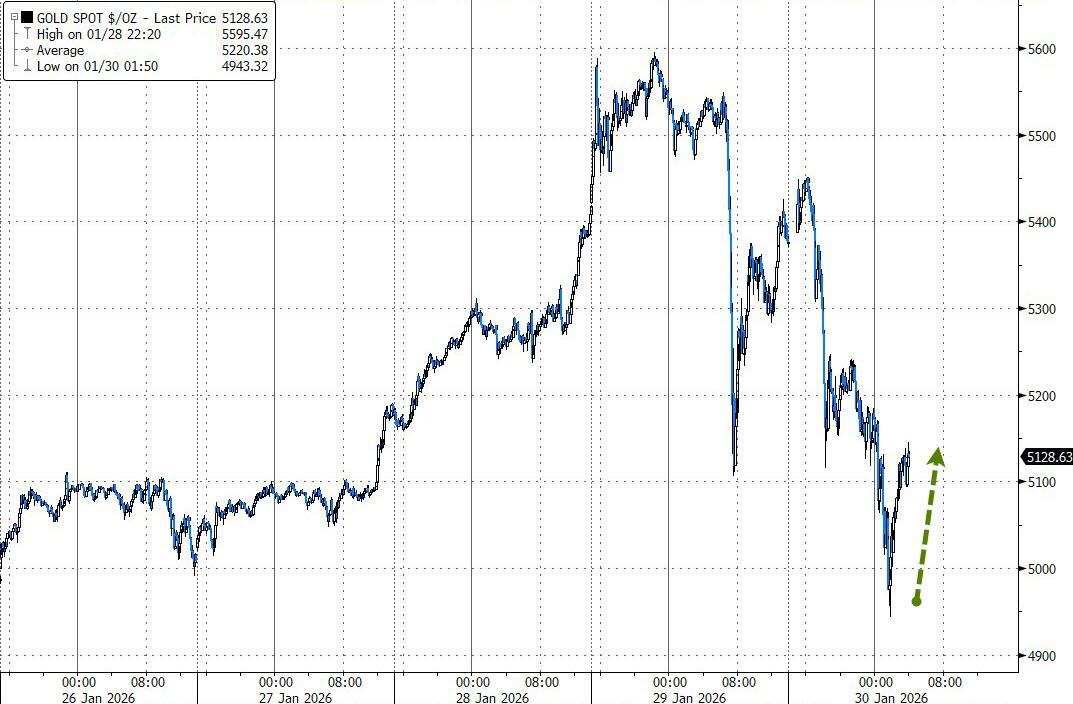

Treasuries and equity futures have reacted negatively in response overnight. While 2yr yields are little changed, 10yr and 30yr yields are +3.4bps and +4.6bps higher as I type, with S&P 500 futures -0.36% lower as I type. So the initial market reaction consistent with a view that the Fed put for asset prices could be less strong under Warsh as Chair than under other candidates. Gold (-3.10%) and oil (-1.30%) have also sold off overnight, while the dollar (+0.31%) is benefitting.

Prior to this, markets had showed some resilience amid heightened volatility yesterday as several assets mostly recovered after sharp plunges. The S&P 500 (-0.13%) almost fully reversed a -1.54% intra-day slump, though the NASDAQ (-0.72%) did see a decent pullback, driven by the biggest daily decline for Microsoft (-9.99%) since the pandemic turmoil of March 2020. Precious metals saw a volatile day too, with gold (-0.77%) finally ending a run of 8 consecutive daily gains to close at $5,375/oz. At one point it had fallen -5.7% on the day in what seemed like a sudden deleveraging. Given that the total value of Gold in the world is around $37tn, that was a $2.1tn brief slump. Providing some perspective, it was only Monday that we first went above $5000/oz and we’re still about 4% above that level despite the decline this morning. Yesterday’s mood also wasn’t helped by the geopolitical backdrop, as speculation about a potential US strike on Iran helped push Brent crude oil above $70/bbl again.

The tech slump was arguably the biggest story yesterday, which came after Microsoft’s earnings following the previous day’s close. As a reminder, their capital expenditures were above analysts’ estimates, which added to concern about how quickly these would pay off. Together with weak results by business software provider SAP (-16.07%) in Europe this hit a whole bunch of software stocks, with ServiceNow (-9.94%) and Workday (-7.65%) also among the worst performers in the S&P 500. However, the Mag-7 (-0.05%) were little changed, with the group supported by Meta (+10.40%) after their own outlook was better than expected. Moreover, the equal weight S&P 500 was far calmer and closed +0.13% with 287 stocks actually closing higher on the day as the broader equity mood improved.

After the close yesterday, we also heard from Apple, which delivered a solid Q4 sales beat ($143.8bn vs $138.4bn est.) and upbeat Q1 revenue growth guidance (13-16% vs 10% expected), driven by strong sales of the new iPhone 17 and a rebound in China. However, rising costs took some of the shine off that strong top line, with Apple’s shares rising about half a percent in after-hours trading following a +0.72% gain in the regular session. In other overnight tech news, Bloomberg reported that SpaceX is considering a potential merger with either Tesla or Elon Musk’s AI firm xAI.

In the meantime, geopolitical fears continued to ramp up yesterday, which pushed oil prices up to their highest level in months even if they’ve moved a bit lower this morning. For instance, Brent crude (+3.60%) moved up to $70.86/bbl at the US close, their highest level since July. Of course, Trump warned on Wednesday that a “massive Armada” was heading to Iran, but yesterday we then heard from an AP report that Iran had issued a warning to ships at sea that they planned to run a drill that included live firing in the Strait of Hormuz. And with oil prices heading higher, that’s revived concern about inflation, with the US 5yr inflation swap (+2.7bps) closing at a 3-month high of 2.53%.

On the topic of commodities, the rally in precious metals finally showed signs of reversing. Initially, gold prices had looked set for a further gain, reaching an all-time intraday record of $5595/oz as we were going to press yesterday. However, they then sharply reversed course after the US open, plummeting down to $5,106/oz, before paring back those losses to close “only” -0.77% lower on the day at $5,375/oz. So that ended a run of 8 consecutive daily gains for gold, which had been the biggest 8-day advance since Lehman Brothers’ collapse in 2008, at +17.9%. It was a similar story for silver too, which slipped back -0.86% from its record high but a much better close than the -8.4% fall intraday.

Otherwise, another risk that is still in the process of being resolved is the potential for a US government shutdown tonight. For context, this emerged as a key issue last weekend, after Democrats called on funding for the Department of Homeland Security to be taken out of a government funding bill. Last night the White House and Senate Democrats reached a deal that would provide a two-week stopgap for Homeland Security funding while funding other departments until the end of the fiscal year in September. While political agreement now appears to be in place, procedural hurdles may still lead to a brief partial shutdown starting at midnight tonight, especially as the House is not currently in session. Polymarket odds for a shutdown on Saturday are at 67%, having been as low as 35% yesterday.

Meanwhile, the latest US data was slightly underwhelming yesterday, with the weekly jobless claims coming in at 209k (vs. 205k expected) in the week ending Jan 24, alongside a +10k upward revision to the previous week, which now stands at 210k. On top of that, the November trade deficit widened more than expected to $56.8bn (vs. $44.0bn expected). So that helped push the Atlanta Fed’s GDPNow estimate for Q4 down to an annualised +4.2%, down from +5.4% previously.

Earlier in Europe, we saw a similar risk-off move yesterday, with the STOXX 600 down -0.23%, whilst Germany’s DAX (-2.07%) had its worst performance since September after the slump by SAP (-16.07%). However, there was some more promising economic data from Europe, as the European Commission’s economic sentiment indicator for the Euro Area reached a 3-year high of 99.4 (vs. 97.1 expected). Even so, the risk-off tone dominated, and sovereign bonds rallied further as investors priced in a growing chance of an ECB rate cut this year, which is now seen as a 31% chance by the September meeting. So yields on 10yr bunds (-1.8bps), OATs (-0.9bps) and BTPs (-1.9bps) all moved lower in response.

In Asia the Hang Seng (-1.78%), Shanghai Composite (-1.19%) and the CSI (-1.01%) are all underperforming. Elsewhere, the Nikkei (-0.18%) and the S&P/ASX 200 (-0.67%) are also trading in negative territory. The KOSPI (+0.62%) is defying the broader regional trend, supported by strong performances from major chipmakers.

Early morning data indicated that the headline Tokyo CPI inflation decreased to +1.5% year-on-year in January (compared to +1.7% expected), marking its lowest level since February 2022. This represents a slowdown from +2.0% in the previous month. Core inflation, which excludes fresh food, also moderated, rising by +2.0% from a year earlier (versus +2.2% expected) and a previous reading of 2.3%. This moderation aligns core inflation with the Bank of Japan’s 2% target after several months of stronger outcomes. The data alleviates pressure on the BOJ to raise rates again in the near future, despite a still tight labor market. JGBs are 1-2bps lower across the curve and the Yen has fallen -0.65%. So one to watch a week after the Treasury “rate check”.

Looking at the day ahead, data releases will include the Euro Area Q4 GDP reading and the December unemployment rate, whilst in Germany we’ll also get the flash CPI print and unemployment for January. In the US, we’ll get the PPI for December as well. Central bank speakers include the ECB’s Vujcic, and the Fed’s Musalem. Finally, today’s earnings releases include Exxon Mobil and Chevron

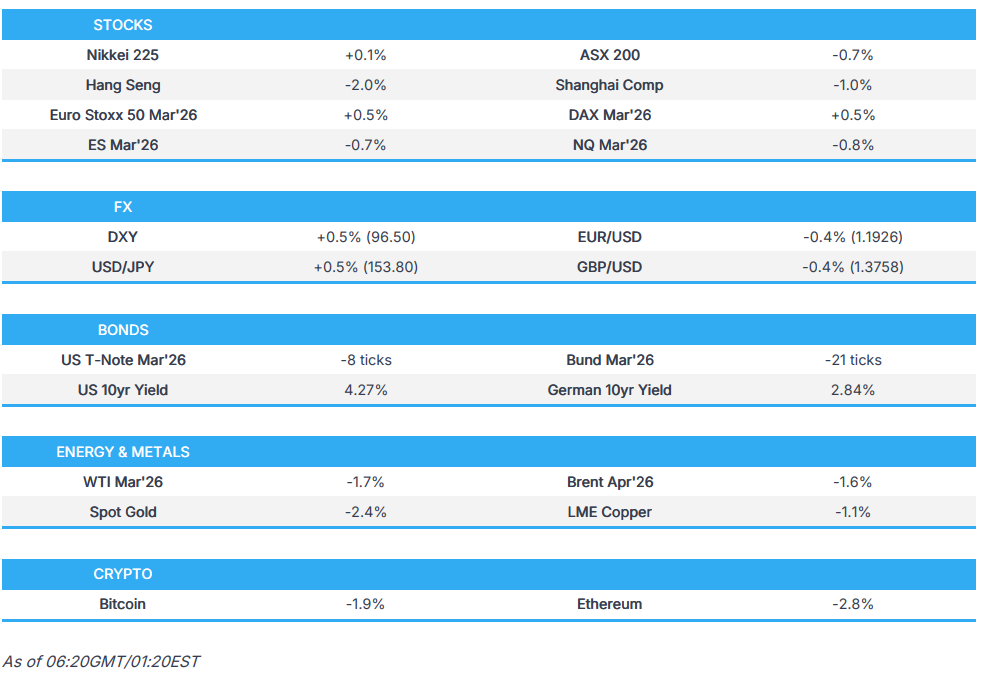

1 b European opening report

US equity futures entirely in the red as markets await Trump’s announcement of the next Fed Chair; Warsh emerges as frontrunner – Newsquawk US Market Open

Friday, Jan 30, 2026 – 06:44 AM

- US President Trump says he will announce his Fed pick on Friday. Reports suggest the administration is leaning towards Warsh.

- DXY bid, USTs lower with the yield curve steeper and US equity futures down (ES -0.8%) amid the Warsh speculation.

- XAU lost the USD 5k/oz handle and XAG below USD 100/oz in a pullback from recent highs and amid USD strength.

- Crude curtailed by the USD, and as Trump plans to meet with Iranian officials

- AUD hit on metal action, JPY digests Tokyo CPI, EUR unaffected by German state CPIs and EZ GDP

- Looking ahead, highlights include German HICP (Jan), Canadian GDP (Dec), US PPI (Dec), Speakers including Fed’s Musalem, Bowman, Miran, Waller.

Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European equities (STOXX 600 +0.3%) have opened mostly on a firmer footing. Strength comes amid a rebound in the DAX 40 (+0.7%) after yesterday’s SAP-induced pressure, a narrative added to by strong Adidas (+5.2%) earnings.

- European sectors are mostly in the green, leading are Banks, Travel & Leisure and Technology. The former have been underpinned by reports that Kevin Warsh is likely to be the next Fed Chair, which has bolstered global yields. Furthermore, the sector benefits from gains in Caixabank (+4.0%) after the Co. announced that it expects NII to grow in 2026. To the downside, Basic Resources has been weighed down by pressure in metal prices, whilst energy has been pinned down by crude as the complex gives back gains.