GOLD: NUMBER OF NOTICES FILED FOR FEBRUARY/2026: 639 CONTRACTs NOTICES FOR 63,900 OZ or 1.9875 TONNES

total notices so far: 28,159 contracts for 2,815,900 OR 87.5863 tonnes)

SILVER NOTICES: 251 NOTICE(S) FILED FOR 1.255 MILLION OZ OZ/

total number of notices filed so far this month : 2765 CONTRACTS (NOTICES) for 13.325 million oz

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 13.645 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVANCES TO 41.675 MILLION OZ

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR 2ND QUEUE JUMP OF 0.840 MILLION OZ//NEW STANDING ADVANCES TO 16.400 MILLION OZ

- MAY: SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.637 TONNES EX FOR RISK//AUG 25: 9.107 TONNES , AUGUST 26: 9.1010 TONNES AND NOW AUGUST 27: 9.0699 TONNES//NEW STANDING ADVANCES TO 107.5117 TONNES OF GOLD NORMAL STANDING (INCLUDES ALL MONTHLY QUEUE JUMPS/EX FOR PHYSICAL TRANSFERS//) +44.696 TONNES EX.FOR RISK = 152.208 TONNES

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 (CME CORRECTED) TONNES OF GOLD TO WHICH WE ADD OUR SECOND QUEUE JUMP OF 4.099 TONNES TO OUR FIRST HUGE QUEUE JUMP OF 5.7260 TONNES/ NEW QUEUE JUMP TOTAL: 9.805 TONNES//NEW STANDING ADVANCES TO 103.393 TONNES

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

AND NOW FEBRUARY: INITIAL STANDING FOR GOLD: 103.393 TONNES!!

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 30.85 TONNES (WHICH WILL BE ANOTHER STRONG)

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF OCT. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 5627 CONTRACTS OI TO 147,993 AND FURTHER FORM TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 987 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 987 CONTRACTS and 0 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 5082 CONTRACTS AND ADD TO THE 987 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF 4640 OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES WITH OUR LOSS OF $1.32 THE RATS ARE FLEEING THE ARENA.

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 21.210 MILLION PAPER OZ

OCCURRED DESPITE OUR LOSS IN PRICE.OF $1.32

2.ASIAN AFFAIRS FEB 3/2025

SHANGHAI CLOSED UP 51.99 PTS OR 1.29%

//Hang Seng CLOSED UP 59.20 PTS OR 0.22%

// Nikkei CLOSED UP 2087.82 PTS OR 3.92%

//Australia’s all ordinaries CLOSED UP 0.10%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.9431

/ OFFSHORE CLOSED UP AT 6.9414 Oil DOWN TO 61.53 dollars per barrel for WTI and BRENT UP TO 65.55 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING UP TO 6.9364 OFFSHORE YUAN TRADING UP TO 6.9335 ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A LARGE SIZED 10,740 CONTRACTS TO 417,776 OI WITH OUR HUGE LOSS IN PRICE OF $100.15 WITH RESPECT TO MONDAY’S // TRADING/ //COMEX CLOSING TIME:… WE LOST HUGE NUMBER OF NET LONGS, WITH THAT PRICE LOSS FOR GOLD. AND AS YOU WILL SEE BELOW, OUR LOSS IN PRICE ALSO HAD A HUGE NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (3747).

WE HAD HUGE T.A.S. LIQUIDATION MONDAY ALONG WITH THE FINALIZATION OF MONTHLY SPREADERS. IT SEEMS THAT THE SPECULATORS WERE SLAUGHTERED WITH OUR FRBNY PROVIDING STILL THE MASSIVE NECESSARY SHORT PAPER AND COVERED MUCH OF THEIR SHORTFALL BUT OTHER CENTRAL BANKERS CONTINUING ON THE LONG SIDE PILING ON AND THEN TENDERING FOR PHYSICAL AT THE END OF THE DAY.

YOU WILL NOTICE THAT THE COMEX OI IS NOW BACK TO A LOWER OI FROM ITS LOW OI OF AROUND 418,000 TO NOW 417,776 AND NOW AMPLE ENOUGH TO GROW AND FROM THIS POINT FORTH IT WILL BE DIFFICULT TO FLEECE. FROM CHINA WE LEARN THAT THE GOLD LEASE RATE IS NOW AROUND 3 TO 4 %

WE THUS HAD A TOTAL LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 6993 CONTRACTS (OR 21.75TONNES).

THEN WE WERE NOTIFIED OF A ZERO CONTRACT EXCHANGE FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS AND THEN WE HAVE 6 ISSUED IN JANUARY: 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, jAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

FEB EXCHANGE FOR RISK: 0 NOTICES SO FAR!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 56+ TONNES OF SHORTAGE.

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS.. THE JANUARY ISSUANCE WAS ADDED TO OUR DAILY TOTALS!! (17.656 TONNES)

FEBRUAY ISSUANCE; ZERO SO FAR!!

DETAILS ON OUR NEW FEBRUARY COMEX CONTRACT MONTH//

IN TOTAL WE HAD A STRONG SIZED LOSS ON OUR TWO EXCHANGES OF 6,993 CONTRACTS WITH OUR HUGE LOSS IN PRICE. HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT OF THE WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THE THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH JANUARY/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER IS A STRONG SIZED T.A.S ISSUANCE CONTRACTS.THE CME NOTIFIES US THAT THEY HAVE ISSUED 2715 T.A.S CONTRACTS AND WILL BE USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS AND IT WAS IN FULL FORCE DURING LAST WEEK AND CONTINUING ON THIS WEEK. IT SURE LOOKS LIKE THE BIS HAS GIVEN THE FRBNY ITS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY WITH ITS 6 ISSUANCES OF EXCHANGE FOR RISK!! IN FEB: 0 ISSUANCES!!

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 9 MONTHS:

- FOR APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNES WHICH FOLLOWED OCT 17 RECORD SETTING: 12.031 TONNE QUEUE JUMP WHICH FOLLOWED THURSDAY’S QUEUE JUMP OF 8.326 TONNES WHICH FOLLOWED WEDNESDAY;S 6.469 WHICH FOLLOWED ALL PREVIOUS QUEUE JUMPS OF 42.549 TONNES TO WHICH WE ADD OUR TOTAL 4679 EXCHANGE FOR RISK CONTRACTS ON 6 OCCASIONS FOR 467,900 OZ OR 14.553 TONNES.! TOTAL STANDING ADVANCES TO 197.511 TONNES OF GOLD

SUMMARY FOR OCTOBER STANDING:

THAT IS;

a) INITIAL STANDING 90.164 TONNES

b) INITIAL EXCHANGE FOR RISK ISSUANCE OF 500 CONTRACTS FOR 50,000 OZ OR 1.555 TONNES

c) ANOTHER 3 CONSECUTIVE EXCHANGE FOR RISK ISSUANCES OF 2150 CONTRACTS FOR 215000 OZ OR 6.687 TONNES

D) AFTER A ONE DAY HIATUS, A 5TH ISSUANCE FOR 1000 CONTRACTS //100,000 OZ OR 3.1104 TONNES

E) AFTER A TWO WEEK HIATUS: ITS 6TH ISSUANCE FOR 1029 CONTRACTS/102,900 OZ OR 3.200 TONNES

TOTAL EXCHANGE FOR RISK OCT 6 OCCASIONS: 14.553 TONNES

TO WHICH WE ADD ALL OUR QUEUE JUMPING IN OCT: TOTAL MONTH;: 92.7648 TONNES

(ALL OF THESE QUEUE JUMPS ARE REPRESENTED BY CENTRAL BANKS DESPERATELY ADDING TO THEIR OFFICIAL RESERVES)

EQUALS

197.5141 TONNES OF GOLD!!

END

8. NOVEMBER:TOTAL TONNES STANDING INCLUDING ALL QUEUE JUMPS AND EXCHANGE FOR RISK ISSUANCE:

INITIAL GOLD STANDING AT THE COMEX IS 5032 CONTRACTS OR 503,200 OZ (15.651 TONNES) FOLLOWED BY ITS TODAY’S QUEUE JUMP OF 2.323 TONNES/ FOLLOWED BY ALL NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR SECOND EXCHANGE FOR RISK OF 1016 CONTRACTS FOR 101600 OZ OR 3.165 TONNES TO OUR FIRST EXCHANGE FOR RISK ISSUANCE OF 1.3966 TONNES/// NEW EXCHANGE FOR RISK: 4.5595 TONNES//NEW TOTAL GOLD STANDING IN NOVEMBER ADVANCES TO 43.9716 TONNES

9. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.1337 TONNES OF QUEUE JUMP WHICH FOLLOWS ALL OTHER NET QUEUE JUMPING OF 37.163 TONNES//STANDING ADVANCES TO 115.257 TONNES TO WHICH WE ADD OUR FOUR ISSUANCES OF EXCHANGE FOR RISK OF 6.559 TONNES/NEW STANDING IS THUS: 121.977 TONNES.

10. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

11.FEB; 0. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE HAD OUR SECOND QUEUE JUMP OF 4.099 TONNES ADDING TO OUR FIRST 5.7260 TONNES QUEUE JUMP// TOTAL OF ALL QUEUE JUMPS: 9.805// STANDING ADVANCES TO 103.393 TONNES

THE FED IS THE OTHER MAJOR SHORT OF AROUND 56+ TONNES OF GOLD OWING TO THE B.I.S. THE OCC ORDERED THE BANKS TO COVER THEIR GOLD LOSSES FROM OCC BETS. THIS IS SUCH A SMALL FRACTION OF WHAT IS OWED!!! THE FRBNY BORROWED GOLD FROM THE BIS TO COVER THOSE HUGE LOSSES OF AROUND 56 TONNES OF GOLD.. THE FED IS VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES IF THEY DO NOT BORROW THIS GOLD. BUT IT IS IMPOSSIBLE/ THAT THE FED IS THE BUYER OF 10.006 TONNES OF EXCHANGE FOR RISK/DECEMBER/EARLY JANUARY!!,(LATEST BIS DATA SHOWS AN INCREASE IN GOLD BORROWING BY THE FRBNY// BUT MAY BE THE BUYER IN JANUARY OF 22.315 TONNES TOTAL IN JANUARY/6 ISSUANCES AS WE NOW HAVE THE BIS DATA FOR GOLD SWAPS FOR DECEMBER 2025 AND HERE WE FIND THAT THE FED ACTUALLY INCREASED THEIR GOLD SWAP LOANS WITH THE BIS TO THE 56 TONNES WHICH I NOW RECORD FOR YOU.!!

THE MAJOR FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE SHORT EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST SEVERAL MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP OTHER CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY. IT SURE DOES LOOK LIKE THE BIS HAS NOT GIVEN THE FED ITS MARCHING ORDERS TO COVER ITS PHYSICAL GOLD SHORT AS THEIR OUTSTANDING LOAN OF 56+ TONNES REMAIN ON THE BOOKS OF THE BIS

THE FRBNY IS STILL NON COMPLIANT WITH RESPECT TO BASEL III BUT IT IS NOT NECESSARY FOR THEM TO BE COMPLIANT ONLY COMMERCIAL BANKERS MUST BE.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + ???? BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD IS SUPPOSED BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

EUROPE IS NOW BASEL III COMPLIANT. THE WEST ( COMEX) IS NOW COMPLIANT EFFECTIVE JULY 1//2025.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF OUR TWO SPREADERS: 1) THE MONTH END SPREADERS AND 2. T.A.S DURING THESE PAST SEVERAL WEEKS IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD, AND THE MASSIVE AMOUNT OF GOLD STANDING EACH AND EVERY MONTH

EXCHANGE FOR PHYSICAL ISSUANCE/JAN//BORROWINGS FROM THE FRBNY:

THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED EXCHANGE FOR PHYSICAL OF 3747 CONTRACTS.

THAT IS A STRONG SIZED 3747 EFP CONTRACT WAS ISSUED: : /APRIL 3747 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3747 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD GENERALLY DELIVERED COMES FROM LONDON BUT THEY ARE OUT!! THUS COMEX BECOMES THE MAJOR SOURCE FOR OUR CENTRAL BANKERS. THE REGULATORY BODY THAT IS SUPPOSE TO CONTROL THESE EFP’S IS THE O.C.C. HEADQUARTERED IN BOTH LONDON AND WASHINGTON. SEEMS NOW THAT THE OCC IS CLAMPING DOWN ON THIS EFP’S CIRCLING AROUND IN LONDON AS THEY ORDERED THE BULLION BANKS TO COVER MUCH OF THEIR DERIVATIVE BETS ON THESE CONTRACTS!! THUS THE FRBNY SAVED OUR BULLION BANKS FROM EXTINCTION WITH THIS BORROWED GOLD FROM THE BIS OF 56+ TONNES

WE HAD :

- HUGE LIQUIDATION OF OUR T.A.S. SPREADERS DURING THE COMEX SESSION + AND DID HAVE HUGE GOVERNMENT LIQUIDATION

- HUGE MONTH END SPREADERS LIQUIDATION /YESTERDAY AS IT FINALIZED OPERATIONS YESTERDAY!!

T.A.S.SPREADER ISSUANCE//FEBRUARY

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT/TUESDAY MORNING WAS A STRONG SIZED 2715 CONTRACTS

THE RAIDS WHETHER ON OPTIONS EXPIRY MONTH OR T.A.S. DRIVEN, ACCOMPLISHES TWO IMPORTANT ASPECTS FOR OUR CROOKS:

- STALLS THE ADVANCE IN PRICE

- LOWERS THEIR ADVANCING DERIVATIVE LOSSES.

THAT SET UP MONDAY’S LOSS IN PRICE IN GOLD WITH A CORRESPONDING LARGE SIZED LOSS OF COMEX OI AND A HUGE EXCHANGE FOR PHYSICAL ISSUANCE..

.

THE COMEX IS IN TOTAL TURMOIL ESPECIALLY THESE PAST 6 MONTHS WITH THE FOLLOWING;

- WITH JULY’S RARE TWO ISSUANCES OF EXCHANGE FOR RISK (LATE IN JULY)

- AND THIS WAS FOLLOWED WITH AUGUST’S 7 ISSUANCES OF EXCHANGE FOR RISK FOR 44.696 TONNES

- TO BE FOLLOWED BY SEPTEMBER’S 7 ISSUANCES FOR EXCHANGE FOR RISK FOR 22.923 TONNES.

- TO BE FOLLOWED BY OCTOBER’S 6 ISSUANCES FOR 14.553 TONNES

- TO BE FOLLOWED BY NOVEMBER’S TWO ISSUANCES FOR 4.5575 TONNES

- AND NOW FOLLOWED BY DECEMBER’S 3 ISSANCES FOR 12.997 TONNES

- THE LONDON BANKING AUDITORS DID REFUSE TO GIVE CERTIFICATION ON THE BANK OF ENGLAND’S SISTER HOLDING OPERATION, THE E.E.A. ON ITS GOLD AND OTHER ASSETS HELD UNDER THE E.E.A.(SEE ROBERT LAMBOURNE’S LETTER OCT 8/HOWEVER THEY DID GIVE THEIR OK NOV 30.

- FRBNY BORROWS ANOTHER 24 TONNES OF GOLD FROM THE BIS IN OCT TO SAVE THE BULLION BANKS FROM EXTINCTION AFTER THE O.C.C ORDERED THE BULLION BANKS TO BE ONSIDE WITH THEIR DERIVATIVES. THE FRBNY IS NOW SHORT 54+ TONNES OF GOLD.

- MASSIVE REMOVAL OF COMEX CONTRACTS FROM PRELIMINARY OI TO FINAL OI//RECORD 33,000 CONTRACTS REMOVED FRIDAY NOV 21//

- MASSIVE T.A.S. CONTRACTS ISSUED FOR 5 CONSECUTIVE DAYS/SIGNALLING A MASSIVE RAID TO BE!

- MASSIVE RAIDS AT THE COMEX CALLED UPON EVERY OPTIONS EXPIRY MONTH INCLUDING JANUARY’S OTC/LBMA DRIVE BY SHOOTING!

JAN 2025:

113.30 TONNES (WHICH INCLUDES 43.408 TONNES EX FOR RISK)

FEB: 2025:

256.607 TONNES (WHICH INCLUDES 18.4567 TONNES OF EX FOR RISK)

MARCH:

STANDING FOR GOLD : 60.33 TONNES + 7.6179 TONNES EX FOR RISK = 67.9479 TONNES WHICH IS EXTREMELY HIGH FOR A NON DELIVERY MONTH.

APRIL:

FINAL STANDING FOR GOLD: 201.573 TONNES + 8.3571 TONNES EX FOR RISK = 209.953 TONNES

MAY: FINAL STANDING 90.235 TONNES WHICH INCLUDES QUEUE JUMPING AND 9.591 TONNES EX FOR RISK.

JUNE: FINAL STANDING 62.534 TONNES PLUS 0.1493TONNES OF QUEUE JUMP EQUALS 93.085 TONNES

JULY: 17.947 TONNES INITIAL STANDING FIRST DAY NOTICE PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK/PRIOR + 2.195 EX FOR RISK TODAY = = 41.106 TONNES

AUGUST:INITIAL AMOUNT OF GOLD STANDING: 60.547 TONNES TO WHICH WE ADD OUR 7 MONTHLY ISSUANCES OF: EXCHANGE FOR RISK TOTALLING 44.696 TONNES//NEW STANDING ADVANCES AS FOLLOWS:

107.5117 TONNES NORMAL DELIVERIES (INCLUDES ALL QUEUE JUMPS /EXCHANGE FOR PHYSICAL TRANSFERS) +

5.4432 TONNES EXCHANGE FOR RISK/PRIOR/AUGUST 7

2.413 TONNES EXCHANGE FOR RISK AUGUST 11

PLUS 2.637 TONNES EX FOR RISK AUGUST 12

PLUS: 9.107 TONNES EX FOR RISK AUGUST 25

PLUS 9.1010 TONNES EX FOR RISK AUGUST 26!!

PLUS 9.0699 TONNES EX FOR RISK AUGUST 27

PLUS 6.923 TONNES EX. FOR RISK/AUGUST 28

MONTHLY TOTAL 44.696 TONNES EXCHANGE FOR RISK!MONTH OF AUGUST.

EQUALS

152.208 TONNES TONNES OF GOLD.

SEPT:

SEPT: 25.878 TONNES OF GOLD INITIAL GOLD STANDING TO WHICH WE ADD OUR 22.923 TONNES OF EXCHANGE FOR RISK ISSUED 7 TIMES DURING THE MONTH:

TOTAL EX FOR RISK// FOR MONTH = 22.923//NEW TOTALS FOR GOLD STANDING SEPT ADVANCES TO 48.801 TONNES

THIS IS HUGE FOR A GENERALLY WEAK SEPTEMBER DELIVERY MONTH.

OCTOBER: INITIAL AMOUNT OF GOLD STANDING: 90.164 TONNES OF GOLD FOLLOWED BY TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL PREVIOUS QUEUE JUMPS OF 76.1656 TONNES WHICH MUST BE ADDED TO OUR 6 ISSUANCES OF 14.553 TONNES EXCHANGE FOR RISK//TOTAL NEW STANDING FOR GOLD IN THIS ACTIVE OCTOBER DELIVERY MONTH ADVANCES TO 197.5141 TONNNES.

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.XXXX TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE HAD OUR SECOND QUEUE JUMP OF 54/079 WHICH IS ADDED TO OUR FIRST 5.7260 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB:: 9.805 TONNES///STANDING ADVANCES TO 103.393 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD TRADING BEGINNING FEBRUARY,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $110.15)

WE HAD HUGE T.A.S. SPREADER LIQUIDATION MONDAY // COMEX SESSION// WITH OUR LOSS IN PRICE ////.. BUT OUR SPECULATORS REMAIN RELENTLESS POURING INTO THE COMEX TO WHICH THEY GOT SLAUGHTERED// BUT WITH OTHER EASTERN CENTRAL BANKS TENDERING FOR PHYSICAL MONDAY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD STANDING FOR FEBRUARY. THE COMEX IS ONE BIG MESS!!

MONDAY NIGHT//TUESDAY MORNING

THE CROOKS HOWEVER COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING/TUESDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

A LITTLE REVIEW OF GOLD STANDING THESE PAST 4 MONTHS:

STANDING FOR GOLD OCT THROUGH TO JANUARY:

- ANALYSIS// OCT DELIVERY MONTH GOING FROM FIRST DAY NOTICE// OCT COMEX CONTRACT TO FINALIZATION OCT 31:

OCT AT 90.164 TONNES TO BE FOLLOWED BY ALL PREVIOUS QUEUE JUMPS OF 75.696 TONNES WHICH WE ADD OUR 14.553 TONNES EX FOR RISK/6 OCCASIONS:

/ TOTAL STANDING 197.551 TONNE/OCTOBER FINAL//ABSOLUTELY A MONSTER DELIVERY FOR A NORMALLY QUIET OCT MONTH

2. AND NOW NOVEMBER:

NOVEMBER BEGINS WITH A HUGE 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY OUR TODAY’S QUEUE JUMP OF 2.323 TONNES WHICH FOLLOWED ALL OTHER NOVEMBER QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO ISSUANCES OF EXCHANGE FOR RISK OF 4.5596 TONNES..

NEW STANDING ADVANCES TO 43.9716 ONNES OF GOLD.

3. AND NOW DECEMBER:

3. DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 83.813 TONNES FOLLOWED BY A 0 CONTRACT QUEUE JUMP FOR NIL OZ OR 0.000 TONNES WHICH FOLLOWS OTHER DEC QUEUE JUMPS OF: 0 TONNES///STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559TONNES/NEW STANDING ADVANCES TO 121.977TONNES

4. NOW JANUARY:

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

10. FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE HAD OUR SECOND QUEUE JUMP OF 4.079 TO WHICH WE ADD TO OUR FIRST 5.7260 TONNES QUEUE JUMP// NEW QUEUE JUMP TOTALS: 9.805//STANDING ADVANCES TO: 103.393 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $590.55

WE HAD A HUGE 531 CONTRACTS REMOVED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. AND THIS IS TOTALLY INSANE .(AND I BELIEVE A RECORD REMOVAL PRELIMINARY TO FINAL

INITIAL GOLD COMEX

FEB 2

FEB 2026 CONTRACT MONTH

GOLD

FEB 3

GOLD

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 0 ENTRIES customer withdrawals: NIL |

| Deposit to the Dealer Inventory in oz | 0 ENTRIES |

| Deposits to the Customer Inventory, in oz | DEPOSITS/CUSTOMER 1 entry i) Into aSAHI 130,179.390 OZ oz total deposit 130,179.390 OZ 4049 kilobars xxxxxxxxxxxxxxxxI |

| No of oz served (contracts) today | 639 notice(s) 63,900 OZ 1.9875 TONNES TONNES OF GOLD |

| No of oz to be served (notices) | 5082 contracts 508,200 OZ 15.807 TONNES |

| Total monthly oz gold served (contracts) so far this month | 28,159 notices 2,815,900 oz 87.5863 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month |

dealer deposits: 0

xxxxxxxxxxxxxxxxxxxxx

DEPOSITS/CUSTOMER

1 entry

i) Into ASAHI 130,179.390 OZ oz

total deposit 130,179.390 OZ

(4049 kilobars)

customer withdrawals:

0 entries

they are draining the comex of gold

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ADJUSTMENTs 2

DEALER TO CUSTOMER:

a) International Delaware: 37,122.550

b) JPMorgan: 29,582.848 oz

chaos inside the comex

AMOUNT OF GOLD STANDING FOR FEBRUARY

THE FRONT MONTH OF FEBRUARY STANDS AT 5721 CONTRACTS FOR A LOSS OF 5718 CONTRACTS.

WE HAD 7036 CONTRACTS SERVED ON MONDAY, SO WE GAINED A MONSTER 1318 CONTRACT-

QUEUE JUMP FOR 131,800 OZ OR 4.099 TONNES!!

MARCH SAW A GAIN OF ONLY 1060 CONTRACTS UP TO 4966 CONTRACT OI.

APRIL IS THE NEXT LARGEST DELIVERY MONTH AND IT LOST 5870 CONTRACTS DOWN TO 293,247 CONTRACTS

We had 639 contracts filed for today representing 63,900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 61 notices issued from their client or customer account. The total of all issuance by all participants equate to 639 contract(s) of which 222 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for FEB /2026. contract month, we take the total number of notices filed so far for the month (28,159) to which we add the difference between the open interest for the front month of FEB ( 5721 CONTRACTS) minus the number of notices served upon today (639 x 100 oz per contract) equals 3,192,300 OZ OR (99.293 Tonnes of gold)

thus the INITIAL standings for gold for the FEB contract month: No of notices filed so far (28,159 x 100 oz +we add the difference for front month of FEB (5721 OI} minus the number of notices served upon today (639 x 100 oz) which equals 3,324,100 OR 103.393 TONNES//

new total of gold standing in FEB is 103.393 TONNES//

TOTAL COMEX GOLD STANDING FOR FEB 103.393 TONNES TONNES WHICH IS STRONG FOR THIS NORMALLY VERY NON ACTIVE ACTIVE DELIVERY MONTH OF JANUARY.

volume MONDAY confirmed 447,704 mega mega mammoth/

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,647,430.712 oz 51.24 tonnes pledged gold lowers

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 35,715,533,.004 oz

TOTAL REGISTERED GOLD 18,962,351.559 or 589.80 Tonnes

TOTAL OF ALL ELIGIBLE GOLD 16,773,181.844 OZ//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 17,314.921 oz ((REG GOLD- PLEDGED GOLD)=

541.670 Tonnes // (declining rapidly)

total inventories in gold declining rapidly

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

SILVER/COMEX

FEB 3 2026

INITIAL/

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 5 entries i) out of Asahi: 35,256.200 oz ii) out of HSBC 399,4577.820 oz iii) Out of JPMorgan: 1,235,196.200 oz iv) Out of Loomis: 63,318.970 ooz v) Out of Stonex: 120,726.640 oz total withdrawn 1,853,955.830 oz the comex is being drained of silver |

| Deposits to the Dealer Inventory | 0 ENTRY |

| Deposits to the Customer Inventory | 1 ENTRIES i) Into CNT: 13, 889.270 oz total deposit: 13,889.270 oz |

| No of oz served today (contracts) | 251 CONTRACT(S) ( 1.255 million OZ |

| No of oz to be served (notices) | 515 Contracts (2.575 MILLION oz) |

| Total monthly oz silver served (contracts) | 2765 contracts 13.825 MILLION oz |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

DEPOSITS INTO DEALER ACCOUNTS

0 ENTRY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

1 ENTRIES

1 ENTRIES

i) Into CNT: 13, 889.270 oz

total deposit: 13,889.270 o

t

withdrawals: customer side/eligible

4 entries

i) out of Asahi: 540,939.250 oz

ii) out of CNT 605,421.049 oz

iii) Out of Delaware 34,808.979 oz

iv) Out of JPMorgan: 272,329.700 oz oz

total withdrawn 1,398,898.900 oz

the comex is being drained of silver

the comex is being drained of silver

adjustments: / / 3

first two: dealer to customer:

a) Brinks 1106,923.340 oz

b) CNT 110,990.158 oz

xxxxxxxxxxxxxx

c) customer to dealer Manfra:

271,308.988 oz

net loss of registered into customer acct: 946,604.988 oz

TOTAL REGISTERED SILVER: 103.070MILLION OZ//.TOTAL REG + ELIGIBLE. 403.857 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JANUARY

silver open interest data:

FRONT MONTH OF FEB /2026 OI: 766 OPEN INTEREST CONTRACTS FOR A LOSS OF 465 CONTRACTS.

WE HAD 633 NOTICES FILED ON MONDAY SO WE GAINED A HUGE 168 CONTRACTS OR 0.840 MILLION OZ UNDERWENT A QUEUE JUMP WHERE THEY WILL STAND ON THIS SIDE OF THE POND!!

MARCH LOST 5390 CONTRACTS DOWN TO 86,440. THIS BECOMES THE FRONT MONTH FOR SILVER DELIVERY AND IT LOOKS LIKE WE WILL HAVE A DANDY DELIVERY OF SILVER FOR THIS MONTH.

APRIL LOST 70 CONTRACTS DOWN TO AN OI 346 CONTRACTS.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 251 or 1.255 MILLION oz

CONFIRMED volume; ON MONDAY 368,561 mammoth//

AND NOW FEB. DELIVERIES:

To calculate the number of silver ounces that will stand for delivery in FEBRUARY. we take the total number of notices filed for the month so far at 2765 X5,000 oz = 13.325 MILLION oz

to which we add the difference between the open interest for the front month of FEBRUARY (766) AND the number of notices served upon today (251)x (5000 oz)

Thus the standings for silver for the FEBRUARY 2026 contract month: (2765)Notices served so far) x 5000 oz + OI for the front month of FEB(766) minus number of notices served upon today (251 )x 5000 oz equals silver standing for the JANUARY.contract month equating to 16.400 MILLION OZ

NEW STANDING: 16.400 MILLION OZ WHICH IS HUGE FOR A GENERALLY SMALL DELIVERY MONTH OF FEBRUARY.

New total standing: 16.400 million oz. THE SILVER COMEX IS NOW UNDER MASSIVE SIEGE!! AND THIS IS HAPPENING WITH THE MASSIVE SIEGE ON GOLD AS WELL.

We must also keep in mind that there is considerable silver standing in London coming from our longs in New York that underwent EFP transfers.

There are 103.070 million oz of registered silver

JPMorgan as a percentage of total silver: 169.146/403.851.million: 41.88%

THERE IS NOW A RUN ON THE COMEX SILVER

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS

FEB 3/2026/WITH GOLD UP $270.80 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1087.10 TONNES

FEB 2/2026/WITH GOLD DOWN $100.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.57 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1087.10 TONNES

JAN 30/2026/WITH GOLD DOWN $590.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.43 TONNES OF GOLD OUT OF THE GLD /// ///INVENTORY RESTS AT 1086.63 TONNES

JAN 30/2026/WITH GOLD DOWN $590.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.43 TONNES OF GOLD OUT OF THE GLD /// ///INVENTORY RESTS AT 1086.63 TONNES

JAN 29/2026/WITH GOLD UP $23.65 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.58 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1089.96 TONNES

JAN 28/2026/WITH GOLD UP $218.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.85 TONNES OF GOLD INTO THE GLD /// ///INVENTORY RESTS AT 1087.38 TONNES

JAN 27/2026/WITH GOLD UP $2.55 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1086.53 TONNES

JAN 26/2026/WITH GOLD UP $106.10 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 6.89 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1086.53 TONNES

JAN 23/2026/WITH GOLD UP $69.05 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSUT OF 2.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1079.66 TONNES

JAN 22/2026/WITH GOLD UP $75.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT WITHDRAWAL OF 4.000 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1077.66 TONNES

JAN 21/2026/WITH GOLD UP $74.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 20/2026/WITH GOLD UP $142.90 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 6.86 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1081.66 TONNES

JAN 16/2026/WITH GOLD DOWN $27.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A DEPOSIT OF .57 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.807TONNES

JAN 15/2026/WITH GOLD DOWN $9.85 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 14/2026/WITH GOLD UP $34.35 TODAY/NO CHANGES IN GOLD AT THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 13/2026/WITH GOLD DOWN$11.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 3.43 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1074.737TONNES

JAN 12/2026/WITH GOLD UP $104.90 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A MASSIVE DEPOSIT OF 6.25 TONNES OF GOLD INTO THE GLD/// ///INVENTORY RESTS AT 1070,80TONNES

JAN 9/2026/WITH GOLD UP $49.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.58 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1064.55 TONNES

JAN 8/2026/WITH GOLD DOWN $0.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 7/2026/WITH GOLD DOWN $38.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.00 TONNES OF GOLD FROM THE GLD/// ///INVENTORY RESTS AT 1067.13 TONNES

JAN 6/2026/WITH GOLD UP $47.00 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 5/2026/WITH GOLD UP $122.80 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 5.43 TONNES OF GOLD OUT OF THE GLD// /// ///INVENTORY RESTS AT 1065.13 TONNES

JAN 2/2026/WITH GOLD DOWN $10.10 TODAY/BIG CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.43 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1070.56 TONNES

DEC 31/WITH GOLD DOWN $42.50 TODAY/SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 30/WITH GOLD UP $41.50 TODAY/NO CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,99 TONNES

DEC 29/WITH GOLD DOWN $190.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.86 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1071,13 TONNES

DEC 26/WITH GOLD UP $39.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.61 TONNES OF GOLD INTO THE GLD// /// ///INVENTORY RESTS AT 1068.27 TONNES

DEC 24/WITH GOLD UP $2.15 TODAY/NO CHANGES IN GOLD AT THE GLD: /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 23/WITH GOLD UP $52.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A FRAUDULENT DEPOSIT OF 12.12 TONNES OF GOLD INTO THE GLD/// /// ///INVENTORY RESTS AT 1064.66 TONNES

DEC 22/WITH GOLD UP $80,25 TODAY/NO CHANGES IN GOLD AT THE GLD: // /// ///INVENTORY RESTS AT 1052.54 TONNES

GLD INVENTORY: 1087.10 TONNES, TONIGHTS TOTAL

SILVER

FEB 3 WITH SILVER UP $6.11 A MASSIVE MASSIVE PAPER AND FRAUUDULENT 32.898 CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 531.985 MILLION OZ

FEB 2 WITH SILVER DOWN $1.32 NO CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 499.087 MILLION OZ /

JAN 30 WITH SILVER DOWN $37.04 HUGE CHANGES IN SILVER AT THE SLV:A FRAUDULENT WITHDRAWAL OF 3.625 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 499.087 MILLION OZ /

JAN 29 WITH SILVER UP $2.80 HUGE CHANGES IN SILVER AT THE SLV:A FRAUDULENT WITHDRAWAL OF 6,798 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 502.712 MILLION OZ /

JAN 28 WITH SILVER UP $5.60 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 4.078 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 509.510 MILLION OZ /

JAN 27 WITH SILVER DOWN $7.00 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 4.17 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 513.598 MILLION OZ /

JAN 26 WITH SILVER UP $12.92 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 0.454 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 517.758 MILLION OZ /

JAN 23 WITH SILVER UP $4.91 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.998 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 517.758 MILLION OZ /

JAN 22 WITH SILVER UP $3.20 HUGE CHANGES IN SILVER AT THE SLV:A WITHDRAWAL OF 1.812 MILLION OZ FROM THE SLV////. ./ :INVENTORY RESTS AT 519.752 MILLION OZ /

JAN 21 WITH SILVER DOWN $1.44 NO CHANGES IN SILVER AT THE SLV://. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 20 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL DEPOSIT OF 5.166 MILLION OZ INTO THE SLV///. ./ :INVENTORY RESTS AT 521.564MILLION OZ /

JAN 16 WITH SILVER DOWN $4.24 HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE AND CRIMINAL WITHDRAWAL OF 5.401 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 516.298MILLION OZ //

JAN 15 WITH SILVER UP $1.00 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.538 MILLION OZ FROM THE SLV///. ./ :INVENTORY RESTS AT 522.199MILLION OZ //

JAN 14 WITH SILVER UP $4.64 NO CHANGES IN SILVER AT THE SLV: /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 13 WITH SILVER UP $1.70 HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 0.816MILLION OZ OUT OF THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 524,737MILLION OZ //

JAN 12 WITH SILVER UP $5.50 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.229MILLION OZ INTO THE SLV OZ INTO THE SLV. /. ./ :INVENTORY RESTS AT 525,598MILLION OZ //

JAN 9 WITH SILVER UP $4.15 HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 6.119 MILLION OZ INTO THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 524.329MILLION OZ //

JAN 8/WITH SILVER DOWN $2.40/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 518.210MILLION OZ //

JAN 7/WITH SILVER DOWN $2.78/HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 10.481 MILLION OZ OUT OF THE SLV OZ FROM THE SLV. /. ./ :INVENTORY RESTS AT 525.730 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 6/WITH SILVER UP $4.93 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 5/WITH SILVER UP $5.90 /SMALL CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 363,000 OZ FORM THE SLV. /. ./ :INVENTORY RESTS AT 528.691 MILLION OZ //

JAN 2/WITH SILVER UP $0.22 /HUGE CHANGES IN SILVER AT THE SLV: A SMALL WITHDRAWAL OF 0.363 MILLION OZ OUT THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 31/WITH SILVER DOWN $6.41 /HUGE CHANGES IN SILVER AT THE SLV: A MASSIVE DEPOSIT OF 4.806 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 529.054 MILLION OZ //

DEC 30/WITH SILVER UP $6.89 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 2.72 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 524.248 MILLION OZ //

DEC 29/WITH SILVER DOWN $5.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.814 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 526,968 MILLION OZ //

DEC 26/WITH SILVER UP $4.88 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 1.813 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 528.782 MILLION OZ //

DEC 24/WITH SILVER UP $0.95 /HUGE CHANGES IN SILVER AT THE SLV: A WITHDRAWAL OF 3.083 MILLION OZ FROM THE SLV/. ./ :INVENTORY RESTS AT 530.595MILLION OZ //

DEC 23/WITH SILVER UP $2.40 /HUGE CHANGES IN SILVER AT THE SLV: A FRAUDULENT DEPOSIT OF 17.13 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 533.678 MILLION OZ //

DEC 22/WITH SILVER UP $1.28 /HUGE CHANGES IN SILVER AT THE SLV: A DEPOSIT OF 1.541 MILLION OZ INTO THE SLV/. ./ :INVENTORY RESTS AT 516.541 MILLION OZ //

DEC 19/WITH SILVER UP $2.06 /NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

DEC 18/WITH SILVER DOWN $1.13/NO CHANGES IN SILVER AT THE SLV: . ./ :INVENTORY RESTS AT 515.000 MILLION OZ //

CLOSING INVENTORY 531.985 MILLION OZ OF SILVER…

PHYSICAL GOLD/SILVER

1/PETER SCHIFF

JOHN RUBINO

MATHEW PIEPENBERG/EGON VON GREYERZ

ALASDAIR MACLEOD

3. CHRIS POWELL AND HIS GATA DISPATCHES:

Retail demand for gold remains strong in Singapore, Sydney, Thailand

Submitted by admin on Mon, 2026-02-02 10:27 Section: Daily Dispatches

Singaporeans Queueing Up to Buy the Dip in Gold Despite Rout

By Chanyaporn Chanjaroen, Sing Yee Ong, and Nasteho Said

Bloomberg News

via The Business Times, Singapore

Monday, February 2, 2026

People were still queueing up to buy gold in Singapore today even as prices plummeted, showing the extraordinary resilience in retail demand for precious metals.

At the headquarters of UOB, Singapore’s only bank offering physical gold products to retail investors, clients and walk-in buyers crowded into a dedicated lounge for bullion transactions.

“I came to buy because the price of gold dropped today,” said Ng Beng Choo. The 70-something retiree said she had arrived and got a ticket at 9.30 a.m. but was still waiting to be called more than six hours later.

A long-running rally in precious metals kicked into overdrive last month as the Trump administration upended the geopolitical order and renewed its attacks on the U.S. Federal Reserve. Those surges went into reverse on Friday, and the rout continued apace today. At one point gold had dropped by more than a fifth from a record high last week.

But rather than seek to sell, many retail investors appeared to be trying to buy the dip in gold, which fell to near US$4,400 an ounce today. …

… For the remainder of the report:

end

Eldorado Gold to acquire Foran Mining in $2.8 billion deal to raise copper exposure

Submitted by admin on Mon, 2026-02-02 10:47 Section: Daily Dispatches

From Reuters

via MSN News, Redmond, Washington

Monday, February 2, 2026

Eldorado Gold will acquire Canada’s Foran Mining in a deal valuing the copper-focused developer at about C$3.8 billion ($2.79 billion), adding a second near-term growth project and increasing its exposure to copper.

The deal, announced by the companies today, expands Eldorado’s production at a time of strong gold prices and rising demand for copper, a key material used in electrification and clean energy.

The combined company’s asset base will have a roughly 77% exposure in gold and 15% toward copper, with operations and development projects in Canada, Greece, and Turkey.

Eldorado said it plans to step up exploration across the business, including at Foran’s Tesla zone in Saskatchewan.

The enlarged miner expects to generate around $2.1 billion in core profit and $1.5 billion in free cash flow in 2027. …

… For the remainder of the report:

end

Money Metals Exchange chief recalls Warsh’s admission about U.S. meddling in gold

Submitted by admin on Mon, 2026-02-02 19:34 Section: Daily Dispatches

7:33p ET Monday, Febrary 2, 2026

Dear Friend of GATA and Gold:

Interviewed by monetary metals advocate Mario Innecco, Money Metals Exchange President Stefan Gleason recalls a conversation he had about gold eight years ago with President Trump’s new nominee for chairman of the Federal Reserve’s Board of Governors, Kevin Warsh.

Warsh, Gleason says, acknowledged that the U.S. government was involved in the gold market but tried to minimize the extent and how much it mattered.

Gleason also says that while many people sense that something is seriously wrong with the financial system, they don’t have to wait for government to fix it. Instead, Gleason says, they can put themselves on a personal gold standard.

The interview is 34 minutes long and you can find it at the Money Metals internet site here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

4. ANDREW MAGUIRE/LIVE FROM THE VAULT KINESIS / AND TODAY;S 256

LIVE FROM THE VAULT YOU TUBE: 257

5. COMMODITY REPORT//RARE EARTHS/ORANGE JUICE

Florida Freeze Batters Citrus Belt, Inflicts “Significant Damage” To Central Orange Groves

Tuesday, Feb 03, 2026 – 02:20 PM

Floridians were once again warned this week to watch out for falling iguanas as an ultra-rare cold blast sent temperatures plunging to record lows of 22F in Jacksonville and 24F in Orlando. Whenever Arctic air pours into The Sunshine State, its citrus industry inevitably takes a hit, and this deep freeze comes on top of years of damage from greening disease and repeated blows from tropical cyclones that have already decimated the crop.

“There was significant damage to the remaining oranges to be picked in central Florida,” said Jim Roemer, a meteorologist who publishes the WeatherWealth newsletter, quoted by Bloomberg.

Roemer added, “Many key areas were well below 28 degrees for over four hours between Sunday and this morning.”

2.ASIAN AFFAIRS FEB 3/2025

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

SHANGHAI CLOSED UP 51.99 PTS OR 1.29%

//Hang Seng CLOSED UP 59.20 PTS OR 0.22%

// Nikkei CLOSED UP 2087.82 PTS OR 3.92%

//Australia’s all ordinaries CLOSED UP 0.10%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.9431

/ OFFSHORE CLOSED UP AT 6.9414 Oil DOWN TO 61.53 dollars per barrel for WTI and BRENT UP TO 65.55 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING UP TO 6.9364 OFFSHORE YUAN TRADING UP TO 6.9335 ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER//OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 6.9364

OFFSHORE YUAN: UP TO 6.9335

HANG SENG CLOSED UP 59,20 PTS OR 0.22%

2. Nikkei closed UP 2087,82 PTS OR 3.97%

WEST TEXAS INTERMEDIATE OIL DOWN 61.53

BRENT; 65.55

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 97.38 /// EURO RISES TO 1.1862 UP 15 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +2.253/ UP 2 FULL BASIS PTS/ VERY TROUBLESOME//Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 155.65… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE ENDING OF THE YEN CARRY TRADE AGAIN AND THE REPATRIATION OF YEN DENOMINATED BONDS TRADING IN THE USA/EUROPE. JAPAN 30 YR BOND YIELD: 3.6436 DOWN 1 FULL BASIS PTS. AND STILL VERY TROUBLESOME

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and BRENT DOWN this morning

3h European bond buying continues to push yields HIGHER on all fronts in the EMU. German 10yr bund YIELD UP TO +2.8755 Italian 10 Yr bond yield UP to 3.487 SPAIN 10 YR BOND YIELD DOWN TO 3.235

3i Greek 10 year bond yield UP TO 3.368

3j Gold at $4897.50 Silver at: 86.10 1 am est) SILVER NEXT RESISTANCE LEVEL AT $100.00

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 37/100 roubles/dollar; ROUBLE AT 77.07

3m oil (WTI) into the 61 dollar handle for WTI and 65 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 155.65 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 2.253% UP 2 BASIS PTS STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING//YEN BOND TRADING OVERSEAS REPATRIATED.//JAPAN 30 YR: 3.636 DOWN 1 BASIS PTS.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.7776 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9183 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.295 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.916 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.582 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 43.49 DOWN 1 BASIS PTS/LIRA GETTING KILLED

10 YR UK BOND YIELD: 4.5250 UP 2 PTS

30 YR UK BOND YIELD: 5.296 UP 2 BASIS PTS

10 YR CANADA BOND YIELD: 3.4377 UP 1 BASIS PTS

5 YR CANADA BOND YIELD: 2.939 UP 1 BASIS PTS.

1a New York Opening report

Futures Rise As Tech Gains On Palantir’s “Cosmic Reward”

Tuesday, Feb 03, 2026 – 08:32 AM

Stock futures are higher, led by tech, while metals rebound and global markets more than retrace Friday/Monday losses. Only bitcoin continues to slide on laughable fears that Kevin Warsh will somehow shrink the Fed’s balance sheet. As of 8:00am ET, S&P futures are up 0.3% and Nasdaq futures gain 0.5% after blockbuster results from Palantir renewed the AI trade. Pre-market, Mag7 names are all higher ex-AAPL with PLTR the standout which should aid the Software reboot. Palantir’s forecast for 61% sales growth this year is helping the AI narrative, with CEO Alexander Karp describing the company’s accelerating revenue as “a cosmic reward” for the data analytics firm’s shareholders. Energy, healthcare, and Staples are weaker pre-mkt as all other sectors are big higher. European stocks briefly traded into record territory, while technology stocks led gains in Asia as South Korea’s chipmakers are surging again. Elsewhere, dip-buyers are crowding into metals: gold is +5.5%, silver +9.4% with WTI flat and Ags bid. Bond yields are flat to +1bp with USD flat. Today’s macro focus is on the vote to reopen the government, where Trump told GOP not to block the deal; we also get the January vehicle sales update. NFP / JOLTS have been delayed with release dates to be updated after the gov’t reopens. Earnings remain front and center, with PepsiCo, Pfizer and AMD due today. . Bitcoin remained under pressure.

In premarket trading, Mag 7 stocks are all higher ex-Apple which is again depressed by soaring memory prices (Alphabet +1.2%, Tesla +1.1%, Amazon +0.7%, Microsoft +0.2%, Nvidia +0.7%, Meta +0.1%, Apple -0.7%)

- Gold and silver miners including Newmont (NEM) gain as precious metal prices climb out of a three-day slide. Newmont rises 4%.

- AES Corp. (AES) rises 8% after BlackRock Inc.’s Global Infrastructure Partners is said to team up with EQT AB in a bid to acquire the power company.

- Eaton Corp. (ETN) falls 5% after the power equipment company forecast adjusted earnings per share for 2026 of $13.00 to $13.50, a range with a midpoint below analysts’ expectations.

- Fabrinet (FN) falls 4% after the engineering and manufacturing services company’s results showed component constraints pressuring the datacom business. However, analysts are broadly positive on the prospects going forward.

- HP Inc. (HPQ) slips 2% as CEO Enrique Lores stepped down to lead PayPal Holdings.

- Palantir Technologies Inc. (PLTR) rises 11% after the company forecast revenue for fiscal 2026 that significantly exceeded Wall Street expectations, a boost for the data analytics company after its shares have gotten off to a lackluster start so far this year.

- PayPal Holdings (PYPL) falls 15% after the fintech reported profit and revenue that fell short of expectations. The company also said Chief Executive Officer Alex Chriss will be replaced by HP Inc. CEO Enrique Lores.

- Rambus (RMBS) slides 8% after analysts note that a supply chain hiccup weighed on the semiconductor device company’s first-quarter outlook. The stock has performed strongly of late, rising about 24% so far this year.

- SoFi Technologies (SOFI) climbs 3% after JPMorgan upgraded to overweight. The bank is positive about the company’s execution and “more tenable valuation.”

- Teradyne (TER) soars 20% after the semiconductor manufacturing company forecast revenue for the first quarter that exceeded the average analyst estimate.

In corporate news, Elon Musk confirmed the combination of SpaceX and xAI in a deal that values the enlarged entity at $1.25 trillion, with the company said to still be planning an IPO later this year. Musk’s rationale is that the least expensive way to do AI computations within two to three years will be in space. Bloomberg estimates that xAI is burning through ~$11 billion in cash in 2025, constraining its ability to seek outsized funding rounds similar to OpenAI. In other corporate news, Uber is rolling out its ride-hailing service in the Chinese gambling hub of Macau, expanding into a new Asian market for the first time in years. Watch shares of professional publishers after Anthropic released an AI-powered productivity tool for companies’ in-house legal teams.

Traders’ appetite for risk rebounded after a steep drop in precious metals triggered a pullback from stocks and crypto at the end of last week. Strong US manufacturing data added to optimism, showing that the economy is on a sound footing as the earnings season rolls on.

“There is a lot of liquidity out there and it’s remaining committed to financial assets,” said Guy Miller, chief strategist at Zurich Insurance. “It’s rotating within the markets, and the macro backdrop is supportive of that continuing.”

In politics, Republican opposition to Trump’s deal with Democrats to end the partial government shutdown began to crumble late Monday as two conservative holdouts agreed to end their threatened blockade. And an analysis of results from a state senate district vote in the Fort Worth area showed that a Texas Democrat’s shock win was powered by big shifts among Latino voters.

Looking at earnings season, out of the 178 S&P 500 companies that have reported so far, 79% have managed to beat analyst forecasts, while 16% have missed. PepsiCo reported better-than-expected fourth-quarter profit and announced a $10 billion share buyback. Merck’s forecast for 2026 sales and profit missed Wall Street’s expectations.

Investors will now turn their attention Tuesday to a slate of earnings, including Advanced Micro Devices Inc., after a favorable reception to Palantir’s report. Traders are watching for signs that AMD is challenging Nvidia Corp.’s dominance in the market for artificial-intelligence accelerators as they look more broadly than the Magnificent Seven for winners of the AI trade. AMD has rallied more than 50% since October, while Nvidia remained largely flat.

In Europe, the Stoxx 600 is up 0.2%, having surrendered most of an earlier advance that took the index to an all-time peak. Miners outperform, tracking a rebound in precious metals. Meanwhile, a drop in Publicis Groupe weighed on media shares. Here are the biggest movers Monday:

- Amundi shares advanced as much as 6.4% to a fresh high after Europe’s largest asset manager reported what RBC says is a “solid” update and announced a €500m share buyback

- The Stoxx 600 Basic Resources Index gained 2.4%, with gold and silver advancing as dip buyers crowded into precious metals following an abrupt unwinding of a record-breaking rally

- Plus500 shares rise as much as 8.5%, climbing to a new all-time high, after the trading platform announced its entry into the US retail prediction markets through a deal struck with Kalshi Exchange

- ING Groep shares gain as much as 3.1%, hitting a fresh 2007-high, after analysts at Deutsche Bank upgraded the bank and significantly increased their estimates

- Swatch shares gain as much as 3.2% after Bank of America upgraded to neutral from underperform on optimism that the worst of the decline is over for watchmakers

- R&S jumps as much as 24%, the most on record, after the Swiss transformers manufacturer posted order intakes for the full year that surpassed the consensus estimate

- Demant shares plunge as much as 12% to the lowest in three years after the Danish hearing-aid maker provided guidance for 2026 that was below expectations

- Publicis shares drop as much as 9%. Despite strong results for the fourth quarter and for the full year, analysts note the advertising agency’s conservative growth guidance for 2026 implies a slowdown

- Zalando shares fall as much as 8.5% as Morgan Stanley warned the clothing retailer continued to face risks stemming from social commerce

- Siltronic shares slide as much as 6.8% after the silicon wafer manufacturer warned the challenging market is expected to persist in 2026, which analysts at Jefferies believe will weigh on expectations

- Schaeffler shares drop as much as 4.5% after UBS downgraded the stock to sell from neutral, warning its current market cap reflects far more ambitious adoption curves and economics for its humanoid robots than he sees likely

- Sartorius shares drop as much as 3.6% in Frankfurt, reversing an earlier 4.6% gain. Barclays analysts said it expected “some slight share price weakness today on implied downside risk to consensus estimates”

- De Nora drops as much as 10% as Kepler Cheuvreux trimmed its price target on the Italian water technologies specialist, noting 2026 will be a lackluster year,

Asian stocks extended a rally on Tuesday, more than erasing the previous session’s decline, on a rebound in precious metals and resurgent excitement around artificial intelligence. The MSCI Asia Pacific Index rose as much as 3.1%, and was on pace for the best day since April 10. Most regional markets were in the green, with South Korean’s Kospi surging 6.8% as Samsung Electronics and SK Hynix helped lead the broader Asian benchmark higher. Stocks also rose more than 3% in Japan, and closed higher in Taiwan and Australia as well. Hong Kong shares edged down. Indian equities also rallied after President Donald Trump announced tariff cuts on the country’s goods. Risk sentiment broadly recovered on Tuesday, with investors piling back into semiconductors and AI-related shares. Palantir Technologies forecast fiscal 2026 revenue that significantly beat expectations, while Elon Musk’s SpaceX confirmed a $1.25 trillion merger with xAI.

The rout in metals prices is disruptive for equities in the short term and has “created some spillover effects from a liquidity perspective,” Kinger Lau, chief China equity strategist at Goldman Sachs, said in a Bloomberg Television interview. Equities are expected to continue rising this year, driven by AI implementation and investment that will support earnings growth, he added

In FX, the dollar pared an earlier fall with the yen now the weakest of the G-10 currencies, down 0.2%. The Aussie is still leading after the RBA hiked interest rates.

In rates,treasuries posted a small retreat, with the 10-year yield up one basis point at 4.29%. European government bonds also dip.

In commodities, oil prices are steady with WTI crude futures near $62 a barrel. Spot silver is up 8% to about $86/oz while gold is near $4,900/oz.

Looking at today’s calendar, Wards total vehicle sales are expected during the day. JOLTS jobs data for December was on the schedule but has been delayed by the partial government shutdown. Fed speaker slate includes Barkin (8am) and Bowman (9:40am)

Market Snapshot

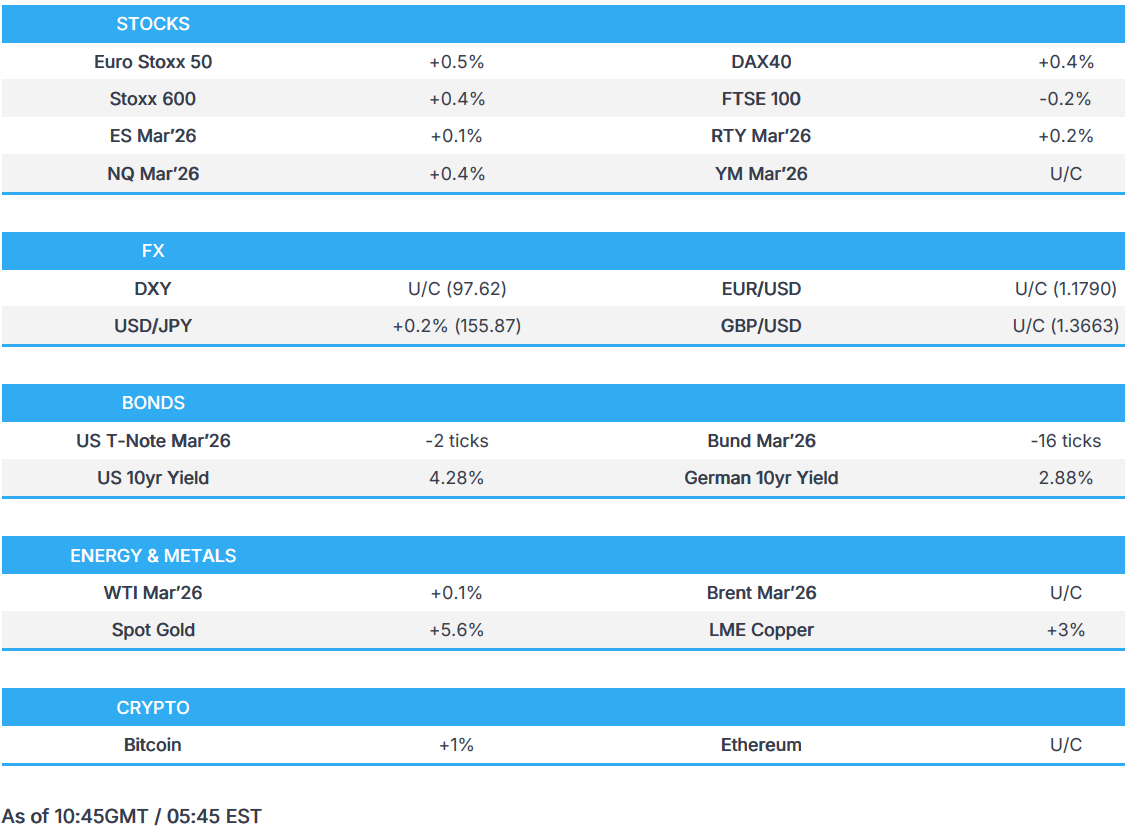

- S&P 500 mini +0.1%

- Nasdaq 100 mini +0.4%

- Russell 2000 mini +0.1%

- Stoxx Europe 600 +0.3%

- DAX +0.4%, CAC 40 +0.1%

- 10-year Treasury yield +1 basis point at 4.29%

- VIX -0.1 points at 16.24

- Bloomberg Dollar Index little changed at 1190.87

- euro little changed at $1.1789

- WTI crude +0.1% at $62.22/barrel

Top Overnight News

- Republican opposition to Trump’s deal with Democrats to end the partial US government shutdown began to crumble late Monday. The president told House holdouts via social media to pass the measure “IMMEDIATELY!” A chamber vote is expected today. BBG

- Elon Musk is merging SpaceX and xAI in a deal valuing the new entity at $1.25 trillion, with SpaceX still planning an IPO later this year, according to people familiar. BBG

- Reports out Monday afternoon said OpenAI is unsatisfied with some of Nvidia’s latest artificial intelligence chips, and it has sought alternatives since last year, eight sources familiar with the matter said, potentially complicating the relationship between the two highest-profile players in the AI boom. RTRS

- US President Trump said announcing the creation of US strategic critical minerals reserve. We are launching Project Vault today. USD 2bln from the private sector. USD 10bln funding from US Exim Bank.

- Australia’s central bank has lifted interest rates for the first time since 2023,one of the first big economies to tighten its monetary policy, in an effort to combat inflation. The Bank increased rates by 25bps to 3.85%. FT

- China has let the interest rate on a one-year policy loan to banks drop to a record low, according to people familiar with the situation, lowering funding costs so as to revive economic growth. BBG

- Demand softened at Japan’s 10-year bond auction as investors grew cautious ahead of a snap election, keeping yields elevated amid equity gains and ongoing fiscal concerns. BBG

- Ukraine has agreed with western partners that persistent Russian violations of any future ceasefire agreement would be met by a coordinated military response from Europe and the US. FT

- French inflation fell more sharply than expected last month to a 5 year low, raising further possibility that eurozone inflation could be below the European Central Bank’s target for longer this year. Consumer prices were 0.4% higher than in January 2025, down from a 0.7% increase in December. WSJ

- Euro-zone banks unexpectedly tightened corporate credit standards at the end of 2025, the ECB said in its quarterly Bank Lending Survey. BBG

- President Trump said he is seeking USD 1bln of damages from Harvard.

- House Rules panel advances the Senate funding package.

Trade/Tariffs

- Kremlin’s Spokesperson said Russia have not heard any statement from India about halting Russian oil purchases, adding that they intend to continue developing their relations with India.

Earnings

- NXP Semiconductors NV (NXPI) Q4 2025 (USD): Adj. EPS 3.35 (exp. 3.31), Revenue 3.34bln (exp. 3.31bln). Q1 Guidance:. EPS 2.77-3.17 (exp. 2.99). Revenue 3.05-3.15bln (exp. 3.09bln).

- OpenAI has determined it needs alternatives to NVIDIA’s (NVDA) latest AI chips in some cases, has sought alternatives since last year. OpenAI is unsatisfied with the speed at which NVIDIA’s hardware can spit out answers to ChatGPT users for complex problems.

- Palantir Technologies Inc. (PLTR) Q4 2025 (USD): Adj. EPS 0.25 EPS (exp. 0.23), Revenue 1.41bln (exp. 1.34bln). Said sales to US businesses in 2026 are expected to grow at least 115% to more than USD 3.14bln.Outlook:. FY revenue 7.182-7.198bln (exp. 6.3bln). FY adj. operating income 4.126-4.142bln (exp. 3.14bln). Q1 adj. operating income 870-874mln (exp. 641mln). Q1 revenue 1.532-1.536bln (exp. 1.33bln).

A more detailed look at global markets courtesy of Newsquawk

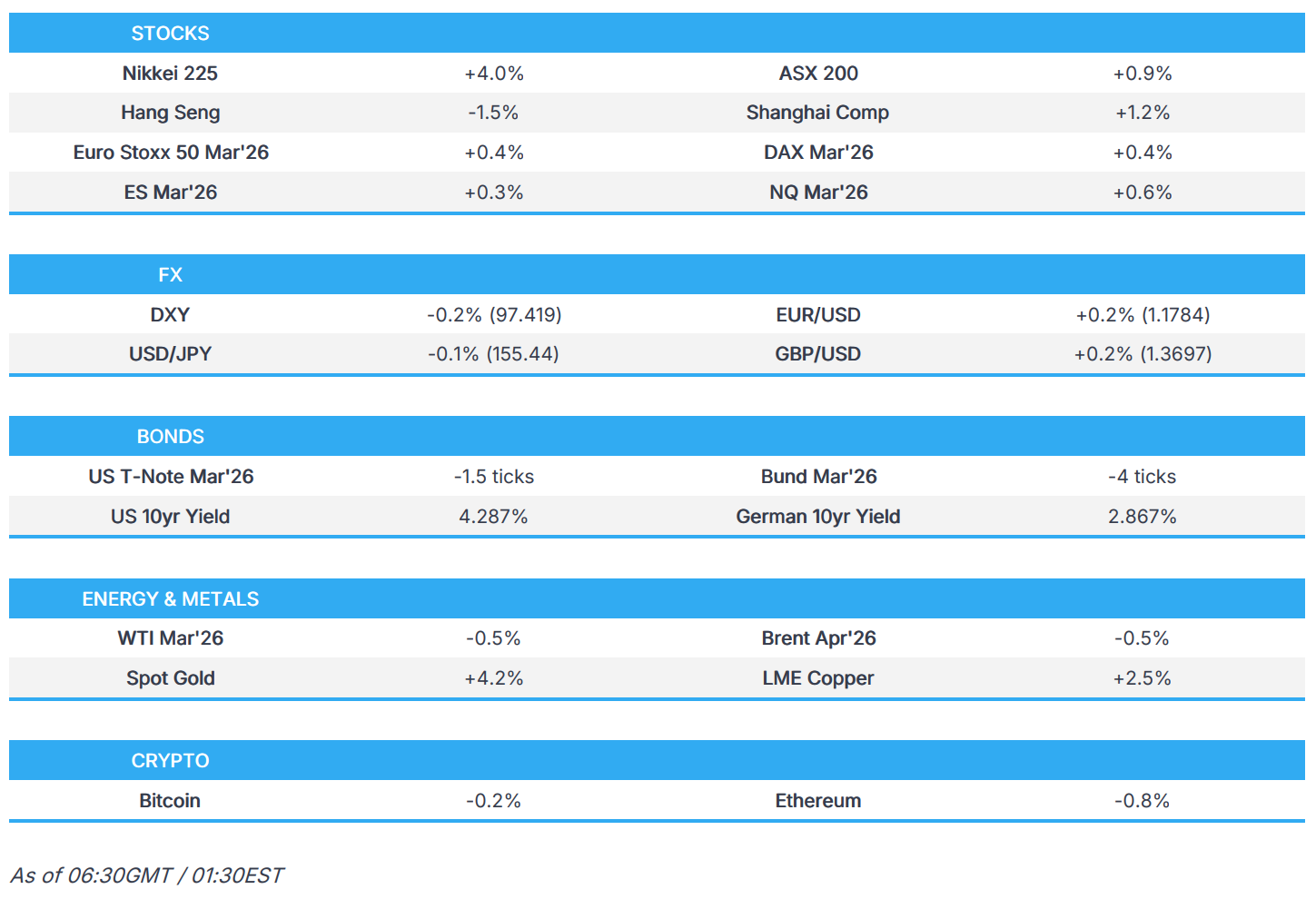

APAC stocks were mostly higher with several bourses firmly recovering from the prior day’s sell-off, as the region took impetus from the positive handover from Wall Street, where markets rallied after a strong ISM Manufacturing report. ASX 200 climbed higher with tech and miners leading the advances, although further upside was capped as the focus turned to the RBA which hiked rates for the first time in over two years and sounded hawkish on inflation. Nikkei 225 surged following recent currency weakness and gained a firm footing above 54,000 to hit a record intraday high. KOSPI outperformed in a turnaround from the prior day’s bloodbath with the Korea Exchange activating a sidecar earlier in the session to briefly halt program trading after a sharp rise in the local benchmark. Hang Seng and Shanghai Comp initially lagged with early pressure seen across tech stocks, despite no immediate obvious catalysts, and with some attributing it to VAT hike concerns, while the Hang Seng TECH Index briefly re-entered bear market territory after dropping more than 20% from its October high. However, Chinese markets then pared their losses alongside the broad rally in Asia.

Top Asian News

- China’s No1/central document includes plans to improve and consolidate soybean production. Intend to stabilise food and oil output. To diversify agricultural product imports.

- Earthquake of magnitude 5.0 hits near the east coast of Honshu, Japan.

- Japanese Finance Minister Katayama continues to refrain from commenting on intervention data and said PM Takaichi talked about FX benefits as a general fact, and didn’t specifically emphasise merits in a weak yen.

- Nintendo (7974 JT) President said memory price rises not having a major impact on earnings.

- Nintendo (7974 JT) – Q3 (JPY): Operating income 155.21bln (exp. 180.7bln), 9M switch sales -66% Y/Y; sees FY net sales 2.25tln (exp. 2.37tln).

European bourses (+0.4%) opened entirely in the green, but sentiment has since waned a touch off best levels, with a couple of indices now slightly in the red. European sectors opened with a positive bias but are now mixed. Basic Resources outperform, led higher by strength in underlying metals prices. Media lags, pressured by losses in Publicis (-7.4%) and ProSiebenSat.1 Media (-2.2%) post-earnings.

Top European News

- French Finance Minister said the G7 needs to agree on a joint instrument to address global macroeconomic imbalances. Joint instruments can have a sectoral focus, such as rare earths.

- French Finance Minister Lescure said that the 2026 budget will reduce the deficit to 5.0% from 5.4%, GDP growth of 1% so far in 2026 is a good start.

FX

- DXY resumed trade overnight on a softer footing following yesterday’s post-ISM recovery (which printed its first expansion in 12 months and at the fastest pace since 2022). The index gradually pared those losses as the morning progressed, to now trade flat, and at the upper end of a 97.34-97.62 range. On the data front, it was also announced that the BLS has delayed the December JOLTS report due today and the January NFP report that was scheduled for Friday owing to the partial government shutdown. With a House vote expected as early as today, the data could be published next week if the vote passes, ING posits.

- Antipodeans are firmer with outperformance in the AUD amid the rebound in risk appetite and metal prices, while further upside was seen after the RBA meeting, where the central bank hiked the Cash Rate by 25bps to 3.85%, as expected, and stated inflation is likely to remain above target for some time. Governor Bullock declined to provide any forward guidance on the future path of interest rates. AUD/USD has come off best levels amid the aforementioned recovery in the DXY but still holds onto most of its gains in a 0.6945-0.7050 current daily range.