MAY 28//GOLD CLOSED UP $52.00 TO $4502.60//SILVER ROSE $1.02 TO $75.60//PLATINUM WAS UP $1.50 TO $1924.00 WHILE PALLADIUM WAS DOWN $25.00 TO $1367.00//GOLD COMMENTARY COURTESY OF ALASDAIR MACLEOD//COMMODITY REPORTS ON GOLD AND ON COPPER//EUROPEAN REPORTS TONIGHT FROM GERMANY//MAJOR FIGHTING ERUPTS IN THE MIDDLE EAST: UPDATES ON THE IRAN VS ISRAEL /USA WAR//ISRAEL WHACKS BEIRUT//ISRAEL VS HAMAS UPDATES//IMPORTANT COMMENTARY TONIGHT FROM JAY MARTIN ON DOLLAR SWAMPS//OIL UPDATES AND BESSENT THREATENS OMAN ON POSSIBLE TARIFFS ON THE STRAIT OF HORMUZ//USA DATA RELEASES//USA ECONOMIC REPORTS//KING NEWS/SWAMP STORIES FOR YOU TONIGHT//GREG HUNTER INTERVIEW ED DOWD..

099 H DEUTSCHE BANK AG 1 118 H MACQUARIE FUTURES US 1 363 H WELLS FARGO SECURITI 300 555 C BNP PARIBAS SEC CORP 353 624 H BOFA SECURITIES 4 661 C JP MORGAN SECURITIES 1 905 C ADM 52

TOTAL: 356 356

MONTH TO DATE: 8,838

MAY 28

MAY COMEX MONTH

JPMORGAN STOPPED: 1/356

GOLD: NUMBER OF NOTICES FILED FOR MAY/2026: 356 CONTRACTs NOTICES FOR 35,600 OZ or 1.107 TONNES

total notices so far: 8838 contracts FOR 883,800 OZ OR 27.489 TONNES

FOR MAY 28

XXXXXXXXXXXXXXXXXX

SILVER NOTICES: 727 NOTICE(S) FILED FOR 3.635 MILLION OZ /

total number of notices filed so far this month : 6413 CONTRACTS (NOTICES) for 32.065 million oz

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $52.00 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/// NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 1034.853 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP !.02 AT THE SLV: NO CHANGES IN SILVER INVENTORY AT THE SLV: //// : INVENTORY RESTS AT THE SLV AT 487.977 MILLION OZ//

CLOSING INVENTORY RESTS AT:

CLOSING INVENTORY: 487.977 MILLION

SILVER//OUTLINE

SILVER COMEX OI FELL BY A FAIR SIZED 269 CONTRACTS TO AN OI OF 101,475 STILL HIGHER FROM ITS NEW RECORD LOW OF 95,999 SET MAY 1. THE RECORD HIGH OI FOR SILVER IS 244,710, SET FEB 25/2020, AND THIS FAIR LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR LOSS OF $1.61 IN SILVER PRICING AT THE COMEX WITH RESPECT TO WEDNESDAY’S TRADING. ON THE FIRST OF MAY, WE REACHED OUR RECORD LOW OI OF 95,999 SURPASSING EVERY DAY NEW OI LOWS SET DURING THE LAST WEEK OF APRIL 2026.

NOW ON A NET BASIS OUR SPECULATORS HAVE REVERTED BACK TO GOING LONG. THE FRBNY ON A NET BASIS IS PROVIDING THE NECESSARY PAPER TO OUR LONGS ALONG WITH SOME BULLION BANKS AND THEN A HUGE NUMBERS OF LONGS ,OUR CENTRAL BANKERS, TAKE THE LONG SIDE AND TENDER FOR PHYSICAL AT 4 PM EACH NIGHT. BECAUSE OF THE HUGE SHORTFALL IN PHYSICAL SILVER IN LONDON THERE IS A LOTTERY TO SEE WHO GETS ANY OF THE PHYSICAL SILVER AVAILABLE THAT WHICH THEY ARE OBLIGATED TO DELIVER. THEY WAIT PATIENTLY FOR THEIR PHYSICAL METAL AND IF NOBODY GETS ANY THEY THEN COME BACK THE NEXT DAY AND SO ON. THIS IS IN LONDON, THE HOME OF PHYSICAL SILVER!! THE FACT THAT WE ARE WITNESSING MANY EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON HIGHLIGHTS THE FACT THAT THE COMEX IS OUT OF SILVER AS WELL.

WE ARE FINALLY MOVING TO A MUCH HIGHER BASE IN SILVER PRICING AT MAJOR SUPPORT LEVEL OF $70.00. SHORTLY WE WILL AGAIN ATTEMPT TO BREAK

WE HAVE A STRONG SIZED GAIN OF 601 TOTAL CONTRACTS ON OUR TWO EXCHANGES AS THE CME NOTIFIED US OF A HUGE SIZED SIZED 870 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE , WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS IN COMEX TRADING WITH RESPECT TO WEDNESDAY TRADING// WE HAD A HUGE SIZED 941 CONTRACT T.A.S. ISSUANCE!! / THEY DESPERATELY AGAIN TODAY TRYING TO CONTAIN SILVER’S PRICE RISE FOR THE PAST SEVERAL WEEKS (WHERE RAIDS ARE CALLED UPON AGAIN AND AGAIN TRYING TO STOP THE RISE IN SILVER’S PRICE TO ABOVE $100.00 AND TO QUELL ADDITIONAL DERIVATIVE LOSSES TO OUR BANKERS’ MASSIVE TOTALS). THEY SUCCEEDED ON WEDNESDAY WITH SILVER’S LOSS IN PRICE

THE PRICE STILL FINISHED ABOVE THE MAGIC NUMBER OF $70.00 SILVER SPOT PRICE BUT STILL BELOW THE $100.00 MARK CLOSING AT $74.60 DOWN $1.61. WE ARE NOW WITNESSING HAVING MANY HUGE T.A.S ISSUANCES // TODAY’S WAS A HUGE SIZED 941 T.A.S. CONTRACTS !!. THE CROOKS ARE BECOMING MORE DESPERATE TO STOP SILVER BREAKING ABOVE THE 100.00 DOLLAR MARK!! AND NOW THE HUGE SUPPORT LEVEL OF 70 DOLLARS!!.MAMMOTH SIZE T.A.S ISSUANCES ARE BECOMING THE NORM AT THE COMEX NOW!!

THERE IS NO NEXT LINE IN THE SAND ONCE THE 100.00 DOLLAR SILVER IS PIERCED AGAIN. WE HAD A HUGE SIZED 870 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY OUR HUGE SIZED 941 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN FUTURE TRADING//AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE.

IN ESSENCE WE HAD A HUGE SIZED GAIN OF 601 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR LOSS IN PRICE OF $1.61. WE HAD HUGE GOVERNMENT (FRBY) COMEX CONTRACTS TRADING ALL WEEK AND A MAJOR PORTION WILL BE REMOVED BY DAYS END. (I RECORD THIS FOR YOU ON A DAILY BASIS). THE STICKY SPECULATOR LONGS STILL REMAIN STOIC

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE.

THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, THROUGHOUT MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT/THURSDAY MORNING: A HUGE SIZED 941 CONTRACTS. DESPITE MANY COMPLAINTS THAT THESE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED FRBNY BANKERS).

THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS AS ONE UNIT, BUT SELL THE SHORT SIDE FIRST AND THEN LIQUIDATE THE LONG SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS NOW ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1.1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES.

THUS:

INITIAL STANDING FOR JANUARY: 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NEW NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK FOR .100 MILLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ!!

INTIAL STANDING FOR FEBRUARY/SILVER: 13.505 MILLION OZ FOLLOWED BY TODAY’S HUGE 0.005 MILLION OZ QUEUE JUMP / : NEW STANDING FOR SILVER AT THE COMEX ADVANCES TO 25.180 MILLION OZ. BUT WE MUST ADD OUR FIRST EXCHANGE FOR RISK OF 25 CONTRACTS FOR .125 MILLION OZ AND THEN OUR SECOND EXCHANGE FOR RISK OF .0600 MILLION OZ TO OUR THIRD HUGE 2.825 MILLION OZ EXCHANGE FOR RISK!!

INITIAL STANDING FOR MARCH: A SURPRISINGLY LOW 31.076 MILLION OZ/ FOLLOWED BY A TINY QUEUE JUMP OF 1 CONTRACTS OR 0.005 MILLION OZ/NEW STANDING ADVANCES TO 46.060 MILLION OZ

INITIAL STANDING FOR APRIL: 7.120 MILLION OZ FOLLOWED BY TODAY’S 1 CONTRACT QUEUE JUMP WHERE 5,000 OZ WILL TAKE DELIVERY OVER ON THIS SIDE OF THE POND. NEW STANDING FOR SILVER AT THE COMEX THUS ADVANCES SLIGHTLY TO 16.565 MILLION OZ PLUS WE MUST ADD OUR 4TH EXCHANGE FOR RISK ISSUANCE OF 17 CONTRACTS OR 0.085 MILLION OZ. THESE WILL BE ADDED TO OUR OTHER 3 ISSUANCES //NEW TOTAL EXCHANGE FOR RISK//1.165 MILLION OZ// NEW TOTAL SILVER STANDING 17.730 MILLION OZ//

INITIAL STANDING FOR MAY: 31.495 MILLION OZ FOLLOWED BY ANOTHER 3 CONTRACT EXCHANGE FOR PHYSICAL JUMP TO LONDON FOR 0.015 MILLION OZ// AND THEN TO BOOT WE HAD OUR FIRST EXCHANGE FOR RISK ISSUANCE FOR 51 CONTRACTS OR 255,000 OZ MAY 21./STANDING BEFORE EXCHANGE FOR RISK: 32.070 MILLION OZ/NEW STANDING THUS REDUCES TO 32.325 MILLION OZ/.//(32.070 MILLION OZ NORMAL STANDING PLUS .255 MILLION OZ EXCHANGE FOR RISK = 32.325 MILLION OZ)

SUMMARY OF OUR MAY 2026 COMEX CONTRACT MONTH:

WE HAD:

/ FAIR COMEX LOSS+// HUGE SIZED 870 EFP ISSUANCE CONTRACTS (/ VI) A HUGE NUMBER OF T.A.S. CONTRACT ISSUANCE 941 CONTRACTS

XX I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL:REMOVED 66 SILVER CONTRACT//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY.. ACCUMULATION

TOTAL CONTRACTS for 19 DAY(S), total 11,418 contracts: OR 57.090 MILLION OZ (600 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 57.090 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 67.230 MILLION OZ///(THIS MONTH’S ISSUANCE OF EXCHANGE FOR PHYSICAL WILL BE SMALL)

FEB. 58.260 MILLION OZ//EXCHANGE FOR PHYSICAL ISSUANCE/FINAL

MARCH: 67.020 MILLION OZ///QUITE SMALL AND BECOMING SMALLER EACH AND EVERY MONTH.

APRIL: 100.895 MILLION OZ///AVERAGE SIZE ISSUANCE

MAY: 28.975 MILLION OZ (ISSUANCE WILL BE QUITE SMALL THIS MONTH)

JUNE: 81.065 MILLION OZ

JULY: 50.925 MILLION OZ (QUITE SMALL)

AUGUST: 59.455 MILLION OZ (QUITE SMALL)

SEPT. 50.510 MILLION OZ.(QUITE SMALL)

OCT; 82.020 MILLION OZ (WILL BE STRONG THIS MONTH)/ OCC WANTS TO REIN IN THESE ISSUANCES!

NOVEMBER: 36.425 MILLION OZ

DEC: 45.765 MILLION OZ

JANUARY 2026: 134.270 MILLION OZ (WILL BE A VERY STRONG MONTH FOR EXCHANGE FOR PHYSICAL!)

FEB : 82.130 MILLION OZ

MARCH: 56.075 MILLION OZ

APRIL; 44.44 MILLION OZ//FINAL.. SMALL THIS MONTH.

MAY 57.090 MILLION OZ

RESULT: WE HAD A FAIR SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 269 CONTRACTS WITH OUR LOSS IN PRICE OF $1.61 IN SILVER PRICING AT THE COMEX// WEDNESDAY,. THE CME NOTIFIED US THAT WE HAD A HUGE SIZED CONTRACT EFP ISSUANCE OF 870 CONTRACTS ISSUED FOR JULY, AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS).

INITIAL STANDING: 31.495 MILLION OZ NOW DECREASES WITH OUR NEXT EXCHANGE EXCHANGE FOR PHYSICAL JUMP TO LONDON FOR 3 CONTRACTS OR 0.015 MILLION OZ//NEW STANDING IS THUS REDUCES TO 32.070 MILLION OZ/BUT WE THEN ADD OUR FIRST EXCHANGE FOR RISK OF 51 CONTRACTS FOR 255,000 OZ..TOTAL STANDING ADVANCES TO 32.325 MILLION OZ//

LAST 14 MONTHS OF SILVER DELIVERIES

WE FINISHED APRIL WITH A STRONG SILVER OZ STANDING OF 16.050 MILLION OZ NORMAL DELIVERY , PLUS OUR 4.00 MILLION EX FOR RISK

FINAL STANDING APRIL: 19.965 MILLION OZ

AND MAY:

NEW STANDING FOR MAY FINISHES AT: 75.615 MILLION OZ. (INCLUDES 5,000 OZ EFP TRANSFER TO LONDON + 12.93 MILLION OZ EXCHANGE FOR RISK ISSUANCE/PRIOR.//NEW TOTAL STANDING 88.540 MILLION OZ

AND JUNE: FINAL 16.995 MILLION OZ

AND JULY: 46.720 MILLION OZ//

AUGUST: 4.70 MILLION OZ INITIAL STANDING PLUS TODAY;S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 10.960 MILLION OZ

SEPTEMBER: 68.040 MILLION OZ NORMAL DELIVERY(INCLUDES ALL QUEUE JUMPING AND EXCHANGE FOR PHYSICAL TRANSFERS) PLUS 3.0 MILLION OZ EX FOR RISK = 71.040 MILLION OZ. (THIS IS THE FIRST AND ONLY ISSUANCE OF EXCHANGE FOR RISK FOR SILVER SINCE MAY.)

OCTOBER: 39.565 MILLION OZ OF NORMAL DELIVERY INCLUDES ALL QUEUE JUMPING

PLUS

2.110 MILLION OZ EXCHANGE FOR RISK//TOTAL OZ STANDING IN OCT ADVAN

NOVEMBER: INITIAL STANDING AT 11.575 MILLION OZ FOLLOWED BY TODAY’S 195,000 OZ QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 9.155 MILLION OZ//STANDING ADVANCES TO 19.670 MILLION OZ/

DECEMBER: INITIAL AMOUNT STANDING FOR DELIVERY: 49.33 MILLION OZ// FOLLOWED BY ANOTHER STRONG 835,000OZ QUEUE JUMP+ DEC. FIRST EXCHANGE FOR RISK 0F .850 MILLION OZ + LAST WEEK.S 495,000 OZ EXCHANGE FOR RISK AND THEN A 3RD ISSUANCE IF 1.00MILLION OZ THEN FINALLY DEC 249ISSUANCE OF 1.35 MILLION OZ EXCHANGE FOR RISK//NEW TOTAL EX FOR RIS IS 3.685 MILLION OZ // STANDING ADVANCES TO 68.415 MILLION OZ//

JANUARY: INITIAL STANDING 22.915 MILLION OZ FOLLOWED BY TODAY’S 1.185 MILLION OZ QUEUE JUMP//NORMAL STANDING ADVANCES TO 49.445 MILLION OZ// TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.100 MILLLION OZ//NEW STANDING ADVANCES TO 49.545 MILLION OZ

FEB: 13.399 MILLION OZ IS OUR INITIAL STANDING FOR SILVER! TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 5,000 OZ AND THEN ADD OUR 3 EXCHANGE FOR RISK FOR 3.010 MILLION OZ STANDING ADVANCES TO 28.190 MILLION OZ!!

MARCH: INITIAL AMOUNT OF SILVER STANDING IS 31.076 MILLION OZ FOLLOWED BY A FINAL 0.210 MILLION OZ QUEUE JUMP //NEW TOTAL STANDING ADVANCES TO 46.060 MILLION OZ

APRIL 2026: INITITAL AMOUNT OF SILVER STANDING 7.120 MILLION OZ FOLLOWED BY TODAY’S 5,000 OZ QUUE JUMP //NEW STANDING ADVANCES TO 16.565MILLION OZ PLUS 1.165 MILLION OZ EXCHANGE FOR RISK.NEW TOTALS 17.730 MILLION OZ

MAY: INITIAL AMOUNT OF SILVER WILLING TO STAND; 31.495 MILLION OZ/ TO WHICH WE ADD OUR NEXT EXCHANGE FOR PHYSICAL JUMP OF 15,000 OZ//NEW STANDING REDUCES TO 32.070 MILLION OZ//(FOLLOWING MANY EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON DURING THIS MAY DELIVERY MONTH). THERE SEEMS TO BE A SCARCITY OF SILVER OVER AT THE COMEX). THEN WE ADD OUR FIRST EXCHANGE FOR RISK OF 51 CONTRACTS FOR 255,000 OZ//STANDING ADVANCES TO 32.325 MILLION OZ//

THE NEW TAS ISSUANCE FOR TODAY (941) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED NO DOUBT WITH FUTURE TRADING!

WE HAD 727 NOTICE(S) FILED TODAY FOR 3.635 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY BANKERS

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 7784 OI CONTRACTS DOWN TO 345,705 OI AND THUS SETTING ITS ALL TIME LOW AT 345,705 MUCH LOWER THAN YESTERDAY’S LOW OI OF 353,489 AND PREVIOUS TO THAT: 354,581 OI SET LAST MONTH AND THIS OI IS MUCH FURTHER FROM TO THE RECORD HIGH (SET JAN 24/2020) AT 799,105 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110. WE HAVE NOW ADVANCED PAST THE PREVIOUS ALL TIME LOWS OF 357,136 SET APRIL 2/.2026AND 354,581 SET AT THE END OF APRIL 2026. WE ARE STILL QUITE A WAY FROM OUR TWO DECADES OLD: 390,000 CONTRACTS LOW SET IN THE YEAR OF 2001 WITH TRADING FOR GOLD AT $260.00. THUS DURING EARLY APRIL WE HAD AN ALL TIME LOW OI IN COMEX (354,531) BUT WITH AN EXTREMELY HIGH PRICE OF GOLD. THE SHORT RATS ARE ABANDONING THE COMEX SHIP, NOBODY WANT TO PLAY IN THIS CROOKED CASINO!! (AND THIS CORRELATES WITH SILVER’S LOW OI OF 101,541 CONTRACTS WITH A MUCH HIGHER SILVER PRICE BASE)

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A SMALL 163 CONTRACTS //.

WE HAD A STRONG LOSS IN COMEX OI (7784 ONTRACTS) . THIS LOSS IN OI OCCURRED WITH OUR LOSS IN PRICE OF $51.00 //,WEDNESDAY///.

LAST 13 MONTHS OF GOLD DELIVERIES: (MAY 2025 THROUGH TO /MAY 2026)

1.MAY SUMMARY FOR MAY TONNES WHICH STOOD FOR DELIVERY:

FINAL STANDING FOR MAY: 70.174 TONNES OF GOLD TO WHICH WE ADD 1. MONDAY’S (MAY 19) 6.221 TONNES EXCHANGE FOR RISK , 2. THEN WE ADD: 1.35 TONNES TO LAST WEEK”S. THEN WE ADD 3. 1.55 TONNES TO EQUAL 9.591 TONNES// NEW EXCHANGE FOR RISK = 9.591 TONNES WHICH MUST BE ADDED TO OUR NORMAL DELIVERY SCHEDULE OF 80.644 TONNES. THUS STANDING FOR MAY INCREASES TO 90.235 TONNES OF GOLD

2 JUNE CONTRACT MONTH: 93.085 TONNES OF GOLD (WHICH INCLUDES ALL QUEUE JUMPING AND 0 EX FOR RISK)

3.JULY INITIIAL STANDING FIRST DAY NOTICE: 17.847 TONNES. PLUS TODAY’S 0 TONNES QUEUE JUMP + 1.555 TONNES EX FOR RISK + 2.195 TONNES EX FOR RISK TODAY = 41.106 TONNES STANDING

4. AUGUST: 60.547 TONNES OF INITIAL GOLD FIRST DAY NOTICE FOLLOWED BY THE NET MONTH’S QUEUE JUMP OF 47.2312 TONNES TO WHICH WE ADD THE FOLLOWING EXCHANGE FOR RISK ISSUANCE RECEIVED FOR THE MONTH: 5.4432 TONNES EX FOR RISK/AUG 7 , AUG 11: 2.413 TONNES EX FOR RISK AND AUG. 12 OF 2.

5.SEPT: INITIAL 8.093 TONNES OF GOLD PLUS TODAY’S QUEUE JUMP OF 0.4883 TONNES PLUS 2.2827 TONNES OF EXCHANGE FOR RISK TODAY//NEW TOTAL EX. FOR RISK/MONTH = 22.923//NEW TOTAL STANDING FOR GOLD SEPT ADVANCES TO = 48.801 TONNES!!

6.OCTOBER: 90.012 TONNES OF INITIAL GOLD STANDING WITH TODAY’S TINY 0.00311 TONNES QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS DURING OCT OF 76.1656 TONNES

THEN WE MUST ADD OUR 14.553 TONNES OF OUR ISSUANCE OF EXCHANGE FOR RISK/6 OCCASIONS//NEW TOTAL OF GOLD STANDING ADVANCES TO 197.5141 TONNES OF GOLD.

7.NOVEMBER BEGINS WITH 15.651 TONNES INITIALLY STANDING FOR DELIVERY FOLLOWED BY TODAY’S QUEUE JUMP OF 2.323 TONNES FOLLOWED BY ALL PREVIOUS QUEUE JUMPS IN OF OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE OF 4.5596 TONNES//NEW STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

8. DECEMBER BEGINS WITH INITIAL STANDING OF 83.813 TONNES OF GOLD FOLLOWED BY TODAY’S 0.0TONNE QUEUE JUMP WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR 4 EXCHANGE FOR RISK FOR DECEMBER OF 6.587 TONNES/NEW STANDING ADVANCES TO 121.977 TONNES

9. JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR FIRST EXCHANGE FOR PHYSICAL TRANSFER OF 0.08709 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEB; INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 93.567 TONNES OF GOLD TO WHICH WE ADD OUR NEXT 0.0248 TONNES 0.1555 TONNES QUEUE JUMP TO 41.2082 TONNES/ NEW NET QUEUE JUMP INCREASES TO 41.233 TONNES// AND THEN WE ADD OUR SIX EXCHANGE FOR RISK: 10,080 CONTRACTS OR 31.251 TONNES//NEW STANDING REDUCES TO 157.878 TONNES

MARCH:: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 8.099 TONNES TO WHICH WE ADD TODAY’S FAIR 4600 OZ QUEUE JUMP (0.2320 TONNES) AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES //NEW STANDING ADVANCES TO 67.6648 TONNES/

APRIL: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY: 52.600 TONNES FOLLOWED BY OUR 345 CONTRACT QUEUE JUMP FOR 34,500 OZ/ (1.073 TONNES)/NEW STANDING ADVANCES TO 70.286 TONNES TO WHICH WE ADD OUR 2ND EXCHANGE FOR RISK OF 1498 CONTRACTS FOR 149800 OZ OR 4.659 TONNES. THE NEW TOTAL EXCHANGE FOR RISK FOR THE MONTH OF APRIL IS 2239 CONTRACTS OR 223900 OZ OR 6.964 TONNES AND THIS WILL BE ADDED TO OUR NORMAL DELIVERY TOTALS (70.762 TONNES) TO GIVE US WHAT WILL STAND IN APRIL (77.726 TONNES)

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 345 CONTRACTS OR 34500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCES FOR 24.635 TONNES/STANDING NOW ADVANCES TO 51.554 TONNES OF GOLD.

E.F.P. ISSUANCE/FOR OPENING MAY. GOLD CONTRACT

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3545 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT A RECORD LOW OF 345,705 BECOMING OUR NEXT REOCRD LOW//MAY 28.2026 EXCEEDING OUR PREVIOUS RECORD LOW OF 353,489 AND WE NOW WITNESSING A LOWER COMEX OI BUT WITH AN EXTREMELY HIGH

SILVER ALSO HAS AN ULTRA SMALL SIZED AND EXTREMELY LOW COMEX OI OF 101,475 CONTRACTS// RISING FROM PREVIOUS ALL TIME LOWS SET DURING THE MONTH OF APRIL AND MAY FIRST.

IN ESSENCE WE HAVE A STRONG LOSS IN TOTAL CONTRACTS IN COMEX GOLD ON THE TWO EXCHANGES OF 4239 CONTRACTS WITH 7721 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 3545 EXCHANGE FOR PHYSICAL OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON.

THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 4239 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A MUCH SMALLER SIZED BUT CRIMINAL 1584 CONTRACTS AND THESE ISSUANCES ARE GENERALLY USED TO INITIATE A RAID WHEN CALLED UPON LIKE YESTERDAY AND TODAY. THE STRING OF 5 CONSECUTIVE HUGE ISSUANCES OF T.A.S. THUS ENDED LAST WEEK.

GOLD PRICE ON TUESDAY FELL BY $51.00

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS CONTRACT (3545 ) ACCOMPANYING THE STRONG LOSS IN COMEX OI OF 7784 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES 4239 CONTRACTS!! WITH THE LOSS IN PRICE.

WE HAVE 1) NOW REVERTED TO OUR NORMAL FORMAT OF BANKER (FRBNY) GOING ON THE SHORT SIDE AND SOME NEWBIE SPECULATORS GOING TO THE LONG SIDE BUT OTHER SPECS GOING ALSO TO THE SHORT SIDE LED BY THE NOSE BY HIGH FREQUENCY TRADERS AND SPREADERS..

STANDING FOR THE LAST 5 MONTHS JANUARY TO MAY:

FINAL STANDING FOR GOLD, JANUARY CONTRACT AT 59.2108 TONNES OF GOLD

FEBRUARY: INITIAL STANDING FOR GOLD: 157.878 TONNES!! WHICH INCLUDES ALL QUEUE JUMPING, THREE EXCHANGE FOR PHYSICAL TRANSFERS TO LONDON AND OUR SIX ISSUANCES EXCHANGE FOR RISK!!

MARCH: INITIAL STANDING AT 8.099 TONNES TO WHICH WE ADD OUR FINAL DAY: 0.2320 TONNES QUEUE JUMP AND THEN ADD +22.3818 TONNES EXCHANGE FOR RISK//NEW STANDING ADVANCES TO 67.6648 TONNES

APRIL: INITIAL STANDING 52.600 TONNES PLUS 27,800 OZ QUEUE JUMP (0.8648TONNES): NEW STANDING ADVANCES TO 70.286 TONNES PLUS OUR TWO EXCHANGE FOR RISK FOR 223,900 OZ OR 6.964 TONNES/NEW STANDING: 77.726 TONNES

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND; 12.24 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP FOR 345 CONTRACTS/34,500 OZ// 1.073 TONNES/ THEN WE MUST ADD OUR EXCHANGE FOR RISK ISSUANCE: TOTAL EXCHANGE FOR RISK MAY// 5 OCCASIONS: 24.635 TONNES///NEW STANDING NOW ADVANCES TO 51.554 TONNES

3) HUGE T.A.S. LIQUIDATION IN THE COMEX SESSION AND SOME GOVT LIQUIDATION // WITH A HUGE LOSS OF EQUITY SHARES/MAY 27 HAVING 1)A $51.00COMEX PRICE LOSS AND WE HAD 2) SPEC LONGS PILING HUGELY ON THE SHORT SIDE// +3. EASTERN CENTRAL BANKERS ALSO PILING INTO THE LONG SIDE. WE HAD A STRONG LOSS OF 4070 CONTRACTS ON OUR TWO EXCHANGES AND AS WELL A STRONG AMOUNT OF GOLD WILL STAND FOR DELIVERY IN MAY. (51.554 TONNES). //, CENTRAL BANKERS TENDERED FOR PHYSICAL WITH THEIR PURCHASES OF CONTRACTS../ ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED FRIDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL

4)A STRONG SIZED COMEX OI LOSS 5) V) FAIR SIZED ISSUANCE OF EXCHANGE FOR PHYSICAL GOLD(3545) AND 6. A FAIR T.A.S. ISSUANCE (1584) FOR RAID PURPOSES.!!!

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL :

TOTAL EFP CONTRACTS ISSUED: 35,378 CONTRACTS OR 3,537,800 OZ OR 110.040 TONNES IN 19 TRADING DAY(S) AND THUS AVERAGING: 1862 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN19 TRADING DAY(S) IN TONNES: 110.040 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2025, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 110.040 TONNES DIVIDED BY 3550 x 100% TONNES = 3.09% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2023 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2024: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES

2025: AND NOW 2026

JAN. 2025: 257.919 TONNES (ISSUANCE WILL BE PRETTY GOOD THIS MONTH BUT MUCH LOWER THAN LAST MONTH)

FEB: 207.21 TONNES//EX FOR PHYSICAL ISSUANCE (WILL BE A FAIR SIZED ISSUANCE THIS MONTH)

MARCH 130.84 TONNES//QUITE SMALL THIS MONTH.

APRIL; 208.57 TONNES. STRONG THIS MONTH

MAY: 113.499 TONNES OF GOLD EFP ISSUANCE//QUITE SMALL THIS MONTH

JUNE: 97.79 TONNES OF GOLD EFP ISSUANCE/EXTREMELY SMALL

JULY : 150.877 TONNES// QUITE SMALL

AUGUST: 175.86 TONNES A LOT LARGER THIS MONTH.

SEPT. 116.13 TONNES VERY SMALL

OCT. 252.72 TONNES//CERTAINLY MUCH LARGER THIS MONTH/VERY STRONG

NOV: 124.74 TONNES

DEC: 190.04 TONNES//GOOD SIZED THIS MONTH FINAL.

TOTAL EXCHANGE FOR PHYSICAL ISSUED FOR YEAR 2025: 2,026.20 TONNES (LOWER THAN LAST YR 2,569.00 TONNES

JANUARY: 209.08 TONNES ( (WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL)

FEB. 176.35 TONNES (WHICH IS A FAIR ISSUANCE)

MARCH: 214.67 TONNES//WILL BE STRONG ISSUANCE THIS MONTH

APRIL; 88.00 TONNES// WILL BE VERY SMALL THIS MONTH

MAY 110.04 TONNES

SPREADERS:

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSIT

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

SILVER:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A FAIR 269 CONTRACTS TO AN OI OF 101,475.

EFP ISSUANCE 870 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 870 CONTRACTS and 870 ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 0 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 269 CONTRACTS AND ADD TO THE 870 E.FP. ISSUED

WE OBTAIN A STRONG GAIN OF 601 OI OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES DESPITE OUR LOSS OF $1.61

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 3.000 MILLION PAPER OZ

OCCURRED WITH OUR LOSS IN PRICE.OF $1.61

2.ASIAN AFFAIRS MAY 28 /2025

SHANGHAI CLOSED UP 4.91 PTS OR 0.12%

HANG SENG CLOSED DOWN 322.07 PTS OR 1.27%

Nikkei CLOSED DOWN 344.91 PTS OR 0.53%

//Australia’s all ordinaries CLOSED DOWN .39%

//Chinese yuan (ONSHORE) CLOSED UP TO 6.7795

/ OFFSHORE CLOSED UP AT 6.7780 Oil UP TO 90.41 dollars per barrel for WTI and BRENT UP TO 96.10 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN// WITH YUAN TRADING UP (6.7795) OFFSHORE YUAN TRADING UP TO 6.7780 ONSHORE YUAN TRADING BELOW OFF SHORE AND UP ON THE DOLLAR// / AND THUS STRONGER/OFF SHORE YUAN TRADING UP AGAINST US DOLLAR/ AND THUS STRONGER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG 7784 CONTRACTS DOWN TO AN OI OF 345,705 CONTRACTS (OI) , BECOMING OUR NEW LOW OI SET (MAY 28) SURPASSING THE PREVIOUS ALL TIME LOW IN OI OF 353,490 SET MAY 27. THE PREVIOUS LOW OF 354,581 WAS SET APRIL6/2026. PREVIOUS TO THAT THE ALL TIME LOW IN OI WAS 390,000 SET IN THE YEAR 2001 WHEN GOLD WAS TRADING $260.00. THE CME SHOULD BE PROUD OF THEMSELVES AS MANY HAVE ABANDONED THIS CROOKED ARENA!!THUS OUR NEW ALL TIME LOW OF COMEX OI HAS NOW BEEN SET AT 345,868 WITH GOLD AT AN EXTREMELY HIGH $4,400.00 WHICH MAKES ABSOLUTELY NO SENSE!!!

WE HAD HUGE T.A.S. LIQUIDATION DURING WEDSDAY’S OP =EX TRADING (OTC/LONDON OPTIONS EXPIRY TRADING). IT SEEMS THAT SOME OF THE SPECULATORS CONTINUED AGAIN TO GO MASSIVELY ON THE LONG SIDE BUT WITH THE BANKERS NOW TAKING THE LONG SIDE,AND CENTRAL BANKS SUPPLYING THE NECESSARY PAPER, AS WELL AS COVERING THEIR SHORTFALL. THERE ARE ALSO SOME SPECULATORS WHO CONTINUALLY GO TO THE SHORT SIDE AND AND OF COURSE THEY WILL BE ANNHILATED ON CENTRAL BANK COMMAND!!

CENTRAL BANKS ALSO TENDERED THEIR NEW LONG CONTRACTS AT THE END OF THE DAY FOR PHYSICAL GOLD. YOU CAN VISUALIZE THIS WITH THE STRONG AMOUNT OF GOLD STANDING AT THE COMEX FOR THIS MAY CONTRACT MONTH!!

THE VERY STRONG SIZED LOSS ON OUR TWO EXCHANGES OCCURRED WITH OUR LOSS IN PRICE IN GOLD (DOWN $51.00).

WE THUS HAD A STRONG SIZED LOSS IN OI ON BOTH OF OUR EXCHANGES, THE COMEX AND LONDON’S EXCHANGE FOR PHYSICAL EQUATING TO 4239 CONTRACTS (OR 13.195 TONNES) WITH OUR LOSS IN PRICE, AS WE WERE INFORMED OF A FAIR CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE, EQUATING TO 3545 CONTRACTS.

THEN WE WERE NOTIFIED TODAY OF A 0 CONTRACT FOR RISK ISSUANCE IN GOLD CONTRACTS FOR 0 OZ OR 0 TONNES OF GOLD. ON FRIDAY, BY FAR WE HAD THE HIGHEST EVER EXCHANGE FOR RISK EVER ISSUED AT ONE TIME BEATING THE PREVIOUS SINGLE HIGHEST ISSUE BY ONE TONNE. THUS MAY 22 RECORDS THE HIGHEST EVER EXCHANGE FOR RISK AT 12.4416 TONNES. WE HAD OUR FIRST ISSUANCE FOR EXCHANGE FOR RISK IN THE MONTH OF MAY ON MAY 7, THEN OUR 2ND ISSUANCE FOR OUR MAY GOLD MONTH ON MAY 12. THE THIRD ON MAY 18 , THEN MAY 21 OUR 4TH ISSUANCE AND THEN FINALLY FRIAY, OUR 5TH ISSUANCE. THIS GOLD WILL BE ADDED TO OUR NORMAL MAY DELIVERIES TO GIVE US OUR FINAL AMOUNT OF GOLD WILLING TO STAND AT THE COMEX..

HISTORY OF EXCHANGE FOR RISK ISSUANCE THIS YEAR: FEBRUARY THROUGH MAY

FEBRUARY:

DURING THE MIDDLE OF THE FEBRUARY CONTRACT MONTH, WE HAD TWO IDENTICAL MONSTER 3,000 CONTRACT ISSUED FOR THE SAME 9.33 TONNES OF GOLD, AND THESE WERE THE HIGHEST EVER IN TONNAGE EVER ISSUED BY THE COMEX. ALTOGETHER THE TOTAL ISSUANCE FOR FEB TOTALLED SIX.(31.251 TONNES).

MARCH:

THURSDAY MARCH 17 WE RECEIVED ITS INITIAL 2000 CONTRACT EXCHANGE FOR RISK ISSUANCE FOR 6.22 TONNES. LAST FRIDAY: 0 ISSUANCE OF EXCHANGE FOR RISK. BUT ON MONDAY MARCH 23 WE RECEIVED NOTICE OF OUR SECOND EXCHANGE FOR RISK ISSUANCE FOR 2,200 CONTRACTS (220,000 OZ OR 6.843 TONNES) AND NOW FRIDAY WITH A MONSTER 2996 CONTRACTS FOR 9.3138 TONNES. THESE THREE ISSUANCES WILL NOW BE ADDED TO THE REGULAR AMOUNT OF GOLD STANDING, I.E. 22.3818 TONNES TO OUR NORMAL GOLD STANDING TO GIVE US WHAT WILL STAND FOR PHYSICAL GOLD FOR MARCH!

APRIL;: 2 EXCHANGE FOR RISK SO FAR, I.E. 2239 CONTRACTS FOR 223,900 OZ OR 6.964 TONNES AND THIS TOTAL TONNES WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND IN APRIL

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS OR 792,000 OZ OR 24.635 TONNES.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

A LITTLE HISTORY OF EXCHANGE FOR RISK DECEMBER THROUGH TO MAY:

IN DECEMBER WE HAVE RECORDED 5 ISSUANCES OF EXCHANGE FOR RISK/4 FOR DEC AND THE LAST ONE ON DEC 31 FOR JANUARY. WE NOW HAVE 3 CHOICES FOR THE RECIPIENT OF THIS ISSUANCE AND IT MUST BE A CENTRAL BANK. YOU WILL RECALL THAT THE BUYER ASSUMES THE RISK OF THAT DELIVERY. (THUS TOTAL EXCHANGE FOR RISK FOR THE MONTH OF DECEMBER IS 6.56 TONNES/4 OCCASIONS.

MONTH OF JANUARY/EXCHANGE FOR RISK

IN JANUARY THEY HAVE 6 TOTAL ISSUANCE : 3.446 TONNES EARLY, THEN JAN 9 ISSUANCE OF 9,331 TONNES AND THEN JAN 16: 0.1996 TONNES JAN 26: 1.499 TONNES, JAN 27: 3.160 AND FINALLY JAN 29: 4.659 TONNES TONNES//TOTAL EXCHANGE FOR RISK JANUARY 22.315 TONNES WHICH WAS ADDED TO OUR NORMAL DELVERIES.

AND FEBRUARY:

FEB EXCHANGE FOR RISK: NOW 6 ISSUANCES: 10,080 CONTRACTS FOR 1,008,000 OZ OR 31.251 TONNES!

HERE ARE THE CHOICES FOR THE RECIPIENT OF THOSE ISSUANCES:

1 THE CENTRAL BANK OF ENGLAND. BUT THEY RECEIVED CLEARANCE THAT THEIR GOLD IS BACK SO IT IS NOT LIKELY THAT THEY WOULD LIKE TO ADD TO THEIR RESERVES.

2. THE CENTRAL BANK OF THE USA: THE FED. LOGICAL CHOICE AS THEY CLAMOUR TRYING TO REDUCE THEIR 106+ TONNES OF SHORTAGE. HOWEVER THEY SEEM NOT TO BE IN A HURRY TO COVER THEIR HUGE SHORTFALL

3. THE CENTRAL BANK OF CHINA AS THEY BATTLE WITS WITH THE USA.

TOTAL EXCHANGE FOR RISK FOR DECEMBER IS 6.56 TONNES AND THIS WAS ADDED TO OUR NORMAL DELIVERY TOTALS..

THE JANUARY ISSUANCE OF 17.656 TONNES WAS ADDED TO OUR DAILY DELIVERY TOTALS!!

FEBRUARY ISSUANCES 6 FOR; 31.251 TONNES !! AND THIS WAS ADDED TO OUR DELIVERY TOTALS FOR THIS MONTH.

MARCH: CME ANNOUNCES ITS FIRST EXCHANGE FOR RISK FOR 2000 CONTRACTS FOR 200,000 OZ OR 6.22 TONNES OF GOLD DURING THE FIRST WEEK OF MARCH, AND THEN MONDAY, MARCH 22, WE RECEIVED ITS SECOND NOTICE ISSUANCE OF 2200 CONTRACTS OR 220000 OZ (6.843 TONNES). THEN FINALLY WE RECEIVED NOTICE OF OUR THIRD EXCHANGE FOR RISK OF 2996 CONTRACTS OR 9.3188 TONNES. TOGETHER ALL 3 ISSUANCES TOTAL 22.3818 TONNES WHICH WILL BE ADDED TO OUR NORMAL DELIVERY SCHEDULE.

APRIL: 2 EXCHANGE FOR RISK SO FAR FOR 223,900 OZ OR 6.964 TONNES. AND THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERY TO GIVE US WHAT WILL STAND FOR APRIL!!

MAY: FIVE ISSUANCES SO FAR FOR 7920 CONTRACTS, 792,000 OZ OR 24.635 TONNES OF GOLD. THIS TOTAL WILL BE ADDED TO OUR NORMAL DELIVERIES IN MAY TO GIVE US WHAT WILL STAND IN MAY.

DETAILS ON OUR NEW MAY COMEX CONTRACT MONTH//

IN TOTAL WE HAD A STRONG LOSS ON OUR TWO EXCHANGES OF 4070 CONTRACTS WITH OUR LOSS IN PRICE ($51.00). HOWEVER, OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN THROUGHOUT THIS WEEK AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED ATTACKS VERY EARLY IN THE COMEX SESSIONS AS THEY TRIED TO ABSORB EVERYTHING IN SIGHT FROM THEIR DAILY ATTACKS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY AND OUR SHORT SPECULATORS FOR THEIR THOUGHTFULNESS.

LONDON ANNOUNCED EARLY IN THE YEAR (AND SCARCITY CONTINUES TO THIS DAY) THAT THEY WERE OUT OF GOLD. WRONGLY IT WAS ATTRIBUTED TO THEIR SHIPPING PHYSICAL GOLD TO COMEX FOR STORAGE DUE TO TRUMP’S INITIATION OF TARIFFS. THE TRUTH OF THE MATTER IS THAT THIS GOLD LEFT LONDON TO OTHER CENTRAL BANKS, AND COMEX BANKS HAVE BEEN PAPERING THEIR LOSSES (DERIVATIVE) WITH KILOBAR ENTRIES. BOTH COMEX AND LBMA ARE WITNESSING MASSIVE AMOUNTS OF GOLD LEAVING THEIR VAULTS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTHS OF JUNE THROUGH MAY/ CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY ALTHOUGH THE T.A.S. ISSUANCES IN GOLD HAVE GENERALLY BEEN ON THE LOW SIDE COMPARED TO SILVER WHICH HAVE BEEN HUGE. TODAY’S NUMBER HOWEVER IS A FAIR SIZED T.A.S ISSUANCE CONTRACTS .THE CME NOTIFIES US THAT THEY HAVE ISSUED 1584 T.A.S CONTRACTS. THESE ARE GENERALLY USED FOR RAID PURPOSES TO STOP GOLD’S RISE AND TO TEMPER HUGE LOSSES IN OTC DERIVATIVE BETS

IT SURE LOOKS LIKE THE BIS HAS SOMEHOW LOOKED THE OTHER WAY WITH ITS GOLD SWAPS WITH THE FRBNY AS THIS ENTITY FOR THE FED REFUSES THE BIS MARCHING ORDERS TO COVER AND THAT MAY EXPLAIN THE STRONG NUMBER OF T.A.S. ISSUANCES IN DECEMBER , JANUARY AND THROUGHOUT FEBRUARY TO GO ALONG WITH OUR HUGE NUMBER OF EXCHANGE FOR RISK ISSUED DURING THESE MONTHS INCLUDING FEBRUARY’S 6 EXCHANGE FOR RISK WHICH ALSO INCLUDED TWO MONSTER 9.3312 TONNE ISSUANCE (FEB 10 AND FEB 12). TOTAL EXCHANGE FOR RISK/FEB EQUALS 31.251 TONNES!! AND MARCH’S THREE ISSUANCES FOR 22.3818 TONNES! OTHER CENTRAL BANKS ARE PAYING ATTENTION AS THEY TAKE DELIVERY OF HUGE AMOUNTS OF PHYSICAL GOLD. APRIL HAD 2 EXCHANGE FOR RISK ISSUANCES FOR 6.694 TONNES. AND NOW MAY WITH ITS 5TH ISSUANCE FOR 12.4436 TONNES///TOTAL EXCHANGE FOR RISK FOR MAY: 24.635 TONNES ISSUED MAY 6 ,MAY 12, MAY 18 MAY 21 AND NOW MAY 22..

WE MUST ALSO REMEMBER THAT THE FRBNY IS SHORT 104 TONNES OF GOLD, THIS COMMENCED ON JAN 2 2023 AS THEY REFUSE TO COVER DESPITE THE BIS’S PLEA TO DO SO. WE WILL KNOW IN JUNE WHETHER THEY COVERED ANY OF THEIR SHORTFALL.

HERE IS A SUMMARY OF GOLD STANDING FOR DELIVERY ON OUR LAST 12 MONTHS:

1.APRIL AT 209 TONNES

2. AND THIS CONTINUED INTO MAY WITH FINAL STANDING AT 90.23 TONNES.

3. JUNE WHICH IS A HUGE DELIVERY MONTH , FINAL STANDING WAS RECORDED AT A STRONG 93.085 TONNES. //(TOTAL NET QUEUE JUMPING FOR THE JUNE MONTH: 31.027 TONNES.)

4. IN JULY WE HAD HUGE DELIVERY NOTICES ESPECIALLY FOR A NON ACTIVE DELIVERY MONTH WITH INITIAL STANDING AT 17.947 TONNES PLUS MANY QUEUE JUMPS + 3.75 TONNES EX FOR RISK = 41.106 TONNES OF GOLD // FINAL TOTAL TONNES STANDING JULY: 41.106 TONNES

5. FOR THE MONTH OF AUGUST:

INITIAL AMOUNT OF GOLD STANDING FOR AUGUST: 60.547 TONNES PLUS THE MONTHS HUGE QUEUE JUMPS OF 47.2312 TONNES +44.696 TONNES EX FOR RISK (7 ISSUANCES) //NEW STANDING 152.208 TONNES WHICH IS MONSTROUS!!!

6. FINAL AMOUNT OF GOLD STANDING FOR SEPT; INITIAL STANDING; 2,602 CONTRACTS OR 260,200 OZ FOR 8.093 TONNES OF GOLD FOLLOWED BY TODAY’S 0.4883 TONNES QUEUE JUMP TO GO ALONG WITH TODAY’S 1.244 TONNES OF EXCHANGE FOR RISK ISSUANCE TODAY AND // TOTAL EXCHANGE FOR RISK ISSUANCE SEPT: 22.923 TONNES//NEW TOTALS STANDING ADVANCES TO 48.801 TONNES OF GOLD!!!

7. OCTOBER:

OCTOBER: INITIAL STANDING FOR GOLD: 90.164 TONNES TO WHICH WE ADD OUR LATEST OCT 30 QUEUE JUMP OF 0.00311 TONNES WHICH FOLLOWS OCT 29 QUEUE JUMP OF .4096 WHICH FOLLOWS; OCT 28 QUEUE JUMP OF .5069 TONNES WHICH FOLLOWS OCT 27 OF 0.3048 TONNES WHICH FOLLOWS: OCT 24 OF 0.8615 TONNES, FOLLOWING OCT 23 QUEUE JUMP OF 1.695 TONNES OCT 22 JUMP OF 8.622 TONNES WHICH FOLLOWS OCT 21: 3.8600 TONNES TO OCT 20 QUEUE JUMP OF 7.695 TONNE

SUMMARY FOR OCTOBER STANDING:

NOVEMBER WHERE INITIAL AMOUNT OF GOLD STANDING IS REGISTERED AT 15.651 TONNES OF GOLD FOLLOWED BY TODAY’S QUEUE JUMP OF 2 TONNES AND FOLLOWED BY ALL OTHER NOV QUEUE JUMPS OF 21.3775 TONNES TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCE FOR 4.5596 TONNES.

/STANDING ADVANCES TO 43.9716 TONNES OF GOLD.

DECEMBER: INITIAL AMOUNT OF GOLD STANDING FOR DELIVERY IN THIS ACTIVE MONTH IS 83.813 TONNES FOLLOWED BY TODAY’S 0.05 TONNES QUEUE JUMP. THIS FOLLOWS ALL OTHER QUEUE JUMPING: 37.163 TONNES//NEW STANDING ADVANCES TO 115.390 TONNES TO WHICH WE ADD OUR FOUR EXCHANGE FOR RISK ISSUANCE OF 6.559 TONNES//NEW STANDING THUS INCREASES TO 121.977 TONNES

JANUARY: INITITAL STANDING: 13.785 TONNES TO WHICH WE ADD OUR QUEUE JUMP OF 0.000 TONNES WHICH FOLLOWS ALL OTHER QUEUE JUMPS OF 30.7117TONNES //NEW TOTAL QUEUE JUMPS 30.7117//NORMAL DELIVERY OF GOLD ADVANCES TO 36.8958 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 22.315 TONNES//NEW STANDING ADVANCES TO 59.2108 TONNES.

FEBRUARY: . FEBRUARY: INITIAL STANDING: 93.566 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.0248 TONNES WHICH MUST BE ADDED ALL OTHER QUEUE JUMPS OF 41.2087 TONNES QUEUE JUMP//TOTAL QUEUE JUMP FOR FEB::ADVANCES TO 41.233 TONNES///STANDING ADVANCES TO 126.628 TONNES TO WHICH WE ADD OUR SIX EXCHANGE FOR RISK OF 31.251 TONNES/NEW STANDING RISES TO 157.879 TONNES

MARCH: INITIAL STANDING FOR GOLD: 8.099 TONNES TO WHICH WE ADD OUR NEXT QUEUE JUMP OF 0.2320 TONNES AND THEN WE ADD OUR THREE EXCHANGE FOR RISK OF 22.3818 TONNES////NEW STANDING FOR GOLD ADVANCES TO: 67.6648TONNES WHICH IS ABSOLUTELY HUGE FOR A NON ACTIVE DELIVERY MONTH!!

APRIL 2026: INITIAL STANDING FOR GOLD: 52.20 TONNES FOLLOWED BY TODAY’S SMALL 500 OZ QUEUE JUMP/ TO WHICH WE ADD OUR TWO EXCHANGE FOR RISK ISSUANCES TOTALLING 223,900 OZ OR 6.964 TONNES//STANDING ADVANCES TO 77.726 TONNES WHICH IS ABSOLUTELY HUGE

MAY: INITIAL AMOUNT OF GOLD WILLING TO STAND: 12.24 TONNES OF GOLD TO WHICH WE ADD OUR NEXT HUGE QUEUE JUMP OF 34,500 OZ (1.073 TONNES) TO WHICH WE ADD OUR FIVE EXCHANGE FOR RISK ISSUANCE FOR 792,000 OZ OR 24.635 TONNES////NEW TOTALS STANDING FOR GOLD ADVANCES TO 51.554 TONNESS

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS 2021-2024

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022: STANDING FOR GOLD/COMEX

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:STANDING FOR GOLD/COMEX

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024/STANDING FOR GOLD/COMEX

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year 2024: 540.30 tonnes

COMEX GOLD TRADING BEGINNING MAY,. CONTRACT;

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $51.00)

WE HAD HUGE T.A.S. SPREADER LIQUIDATION WEDNESDAY // COMEX SESSION// WITH OUR LOSS IN PRICE , OUR LONG SPECULATORS STILL REMAIN RELENTLESS POURING INTO THE COMEX

OTHER EASTERN CENTRAL BANKS TENDERED FOR PHYSICAL EVERY NIGHT WHICH ALSO EXPLAINS THE HUGE NUMBER OF TONNES OF GOLD THAT STOOD FOR GOLD DURING THESE PAST SEVERAL MONTHS

WEDNESDAY NIGHT//THURSDAY MORNING

THE CROOKS COULD NOT STOP OTHER CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL WEDNESDAY EVENING/THURSDAY MORNING AND THUS OUR HUGE NUMBER OF GOLD CONTRACTS STANDING FOR DELIVERY AT THE COMEX. CENTRAL BANKERS WAIT PATIENTLY FOR THE GOLD

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $51.00

WE HAD A SMALL 163 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET LOSS ON THE TWO EXCHANGES : 4239 CONTRACTS OR 423900 OZ OR 13.185 TONNES

Total monthly oz gold served (contracts) so far this month

8838 notices 883,800 oz 27.483 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

dealer deposits: 1

1 ENTRY

i) Into the dealer; Stonex: 16,005.390 oz

total deposit: 16,005.390 oz

DEPOSITS/CUSTOMER

ENTRY: 1

i) Into Brinks 1500.01 oz

total deposit: 1500.01 oz

xxxxxxxxxxxxxxxxxx

comex withdrawal

ENTRIES; 1

ONE CUSTOMER WITHDRAWAL ENTRIES

ENTRIES; 1

i) out of Manfra: 125,293.532 oz

total withdrawal 125,293.532 oz

adjustments: 1

customer to dealer: 1182.718 oz

COMEX IS DRAINING GOLD

chaos inside the comex

THE FRONT MONTH OF MAY OI STANDS AT 356 CONTRACTS HAVING A LOSS OF 1528 CONTRACTS.

WE HAD 1873 CONTRACTS SERVED ON WEDNESDAY SO WE GAINED 345 CONTRACTS OR 34,500 OZ (1.073 TONNES) UNDERWENT A STRONG QUEUE JUMP WHERE THEY WILL TAKE DELIVERY ON THIS SIDE OF THE POND. THIS QUEUE JUMP IS CENTRAL BANK CLAMORING FOR PHYSICAL GOLD EXACTLY AS ANDREW MAGUIRE TOLD US IN HIS LATEST PODCAST. ALL OF THIS GOLD IS ENDING UP IN SHANGHAI GOLD EXCHANGE: (SGE).

.

JUNE IS A HUGE DELIVERY MONTH AND HERE THE OI FELL BY 29,372 CONTRACTS DOWN TO AN OI OF 31,808. JUNE BECOMES THE NEW FRONT MONTH AND WE SHOULD HAVE A STRONG AMOUNT OF GOLD STANDING FOR DELIVERY. WE HAVE 1 DAY LEFT BEFORE FIRST DAY NOTICE FOR THE GENERALLY HUGE DELIVERY MONTH OF JUNE. PROBABLE AMOUNT TO STAND FOR DELIVERY: 20,000 CONTRACTS OR 2.5 MILLION OZ (62.2 TONNES)

JULY GAINED 653 CONTRACTS DOWN TO AN OI OF 2604.

We had 356 contracts filed for today representing 35,600oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 356 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for MAY. /2026. contract month, we take the total number of notices filed so far for the month (8,838) to which we add the difference between the open interest for the front month of MAY 356 CONTRACTS) minus the number of notices served upon today 356 x 100 oz per contract) equals 883,800 OZ OR (27.489Tonnes of gold) to which we add our FIVE exchange for risk issuance for 792,000 oz or 24.635 tonnes//new standing for gold/May again advances to 51.554 tonnes which is a monstrous delivery for a non active delivery month.

THUS: INITIAL total number of gold ounces standing for MAY. /2026. contract month, we take the total number of notices filed so far for the month (8,838) to which we add the difference between the open interest for the front month of MAY( 356 CONTRACTS) minus the number of notices served upon today 356 x 100 oz per contract) equals 883,800 OZ OR (27.489 Tonnes of gold) plus we must add our Five exchange for risk issuances of 792,000 oz or 24.635 tonnes/new standing advances to 51.554 tonness

new total of gold standing in MAY ADVANCES TO 51.554 TONNES//

TOTAL COMEX GOLD STANDING FOR MAY 51.554 TONNES TONNES WHICH IS NOW HUGE FOR THIS NORMALLY NON ACTIVE DELIVERY MONTH OF MAY.

confirmed volume WEDNESDAY confirmed 301,987// fair/rollovers// many have left the arena

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,920,673.577 oz 59.74 tonnes pledged gold lowers

total inventories in gold declining rapidly

total pledged gold: 1,920,673.577 tonnes oz 59.74 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD 28,282,868.635oz

TOTAL REGISTERED GOLD 15,642,763.579 tonnes (486.51 tonnes)

TOTAL OF ALL ELIGIBLE GOLD 12,640,105.086 oz//eligible gold leaving hand over fist

REGISTERED GOLD THAT CAN BE SERVED UPON 13,720,907 oz ((REG GOLD- PLEDGED GOLD)=

426.777 Tonnes //

total inventories in gold declining rapidly

SILVER COMEX

MAY DELIVERY MONTH

MAY 28

MAY DELIVERY MONTH

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

2 ENTRIES

i) Out of Brinks: 676,053.109 oz ii) Out of Delaware 9283.05 oz

total: 689,336.159 oz

Deposits to the Dealer Inventory

1 entries

i) Into Asahi 532,932.701 oz

out of Asahi: 532,932.701 oz

Deposits to the Customer Inventory

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

3 ENTRIES

i) Into Asahi 599,298.400 oz ii) Brinks 8983.000 oz iii) CNT 21,686.980 oz

total: 930,273.575 oz

No of oz served today (contracts)

2 CONTRACT(S) (10,000 OZ

No of oz to be served (notices)

1 Contract (5,000 oz)

Total monthly oz silver served (contracts)

5,686 contracts 28.430 MILLION oz

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

DEPOSITS INTO DEALER ACCOUNTS

1 entries

1 entries

i) Into Asahi 532,932.701 oz

out of Asahi: 532,932.701 oz

DEPOSIT ENTRIES/CUSTOMER ACCOUNT

3 ENTRIES

i) Into Asahi 599,298.400 oz

ii) Brinks 8983.000 oz

iii) CNT 21,686.980 oz

total: 930,273.575 oz

xxxxxxxxxxxxxxxxxxxxxxxxx

withdrawals: customer side/eligible

2 ENTRIES

i) Out of Brinks: 676,053.109 oz ii) Out of Delaware 9283.05 oz

total: 689,336.159 oz

adjustments 1 customer to dealer

i) Asahi 2,082,203.500 oz

ii) Briunks 5011.02 oz

xxxxxxxxxxxxxx

TOTAL REGISTERED SILVER: 84.051 MILLION OZ//.TOTAL REG + ELIGIBLE. 316,490 Million oz

registered silver dropping in numbers

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR MAY

silver open interest data:

FRONT MONTH OF MAY /2026 OI: 728 OPEN INTEREST CONTRACTS FOR A LOSS OF 5 CONTRACTS. WE HAD 2 CONTRACTS SERVED UPON ON WEDNESDAY SO WE AGAIN LOST 3 CONTRACTS OR 0.015 MILLION OZ UNDERWENT AN EXCHANGE FOR PHYSICAL TRANSFER JUMP TO LONDON WHERE THEY WILL TAKE DELIVERY OVER ON THAT SIDE OF THE POND.

JUNE SAW A LOSS OF 295 CONTRACTS DOWN TO 2381 OI CONTRACTS

JULY SAW A LOSS OF 286 CONTRACTS DOWN TO 71,148 CONTRACTS

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 727 or 3.635 MILLION oz

To calculate the number of silver ounces that will stand for delivery in MAY. we take the total number of notices filed for the month so far at 6413 X5,000 oz = 32.065 MILLION oz

to which we add the difference between the open interest for the front month of MAY( 728) AND the number of notices served upon today (727 )x (5000 oz)

Thus the standings for silver for the MAY 2026 contract month: (6,413 )Notices served so far) x 5000 oz + OI for the front month of MAY (728) minus number of notices served upon today (727)x 5000 oz equals silver standing for the MAY..contract month equating to 32.070 MILLION OZ.+TO WHICH WE ADD OUR FIRST EXCHANGE FOR RISK OF 0.255 MILLION OZ//

NEW STANDING REDUCES T0: 32.325 MILLION OZ WHICH IS STILL PRETTY GOOD FOR THIS ACTIVE DELIVERY MONTH OF MAY.

We must also keep in mind that there is considerable silver standing in London coming from our longs

There are ONLY 84.051 million oz of registered silver

JPMorgan as a percentage of total silver: 140.287/316.490 million: 44.23

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42.

The previous record was 224,540 contracts with the price at that time of $20.44.

BOTH GLD AND SLV ARE MASSIVE FRAUD

MAY 28 /2026/WITH GOLD UP $52.00 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 27 /2026/WITH GOLD DOWN $51.00 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 26 /2026/WITH GOLD DOWN $25.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.9988 TONNES OUT OF THE GLD ./ //:/INVENTORY RESTS AT 1034.853 TONNES

MAY 22 /2026/WITH GOLD DOWN $13.45 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

MAY 21 /2026/WITH GOLD UP $7.60 TODAY/NO CHANGES IN GOLD AT THE GLD: ./ //:/INVENTORY RESTS AT 1036.851 TONNES

MAY 20 /2026/WITH GOLD UP $26.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.999 TONNES OF GOLD OUT OF THE GLD./ //:/INVENTORY RESTS AT 1036.851 TONNES

MAY 19 /2026/WITH GOLD DOWN $46.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.57 TONNES OF GOLD INTO THE GLD./ //:/INVENTORY RESTS AT 1038.85 TONNES

MAY 18 /2026/WITH GOLD DOWN $4.90 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 15 /2026/WITH GOLD DOWN $118.70 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 14 /2026/WITH GOLD DOWN $20.95 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 13 /2026/WITH GOLD UP $18.75 TODAY/NO CHANGES IN GOLD AT THE GLD:/ //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 12 /2026/WITH GOLD DOWN $38.20 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 2.285 TONNES OF GOLD INTO THE GLD// //:/INVENTORY RESTS AT 1036.280 TONNES

MAY 11 /2026/WITH GOLD DOWN $2.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.515 TONNES OF GOLD INTO THE GLD// //:/INVENTORY RESTS AT 1033.995 TONNES

MAY 8 /2026/WITH GOLD UP $22.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 0.283 TONNES OF GOLD INTO THE GLD// //:/INVENTORY RESTS AT 1033.480TONNES

MAY 7 /2026/WITH GOLD UP $15.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.853 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1033.197TONNES

MAY 6 /2026/WITH GOLD UP $124.70 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.718 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1034.05TONNES

MAY 5 /2026/WITH GOLD UP $33.75 TODAY/NO CHANGES IN GOLD AT THE GLD:// //:/INVENTORY RESTS AT 1035.768 TONNES

MAY 4 /2026/WITH GOLD DOWN $106.65 TODAY/NO CHANGES IN GOLD AT THE GLD:// //:/INVENTORY RESTS AT 1035.768 TONNES

MAY 1 /2026/WITH GOLD UP $13.45 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.427 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1035.768 TONNES

APRIL 30/2026/WITH GOLD UP $19.80 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 5.142 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1039.195 TONNES

APRIL 29/2026/WITH GOLD DOWN $45.70 TODAY/NO CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1044.337 TONNES

APRIL 28/2026/WITH GOLD DOWN $85.85 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 2.285 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1044.337 TONNES

APRIL 27/2026/WITH GOLD DOWN $41.10 TODAY/NO CHANGES IN GOLD AT THE GLD: // //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 24/2026/WITH GOLD UP $13.95 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.29 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1046.62 TONNES

APRIL 23/2026/WITH GOLD DOWN 28.35 TODAY/HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 2.000 TONNES OF GOLD FROM THE GLD// //:/INVENTORY RESTS AT 1050.91 TONNES

APRIL 22/2026/WITH GOLD UP 26.40 TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 21/2026/WITH GOLD DOWN 11.90TODAY/NO CHANGES IN GOLD AT THE GLD //:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 17/2026/WITH GOLD UP $71.30 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 1.15 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1052.91 TONNES

APRIL 16/2026/WITH GOLD DOWN $15.00 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.285 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1051.783 TONNES

APRIL 15/2026/WITH GOLD DOWN $24.15 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT 2.289 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1049.478 TONNES

APRIL 14/2026/WITH GOLD UP $83.55 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.714 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1047.192 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 13/2026/WITH GOLD DOWN $50.60 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.514 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1048.906 TONNES

APRIL 10/2026/WITH GOLD DOWN $11.90 TODAY/SMALL CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 0.724 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.42 TONNES

APRIL 9/2026/WITH GOLD UP $42.50 TODAY/HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.429 TONNES OF GOLD FROM THE GLD//:/INVENTORY RESTS AT 1052.990 TONNES

APRIL 8/2026/WITH GOLD UP $88.95 TODAY/NO CHANGES IN GOLD AT THE GLD A//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 7/2026/WITH GOLD UP $5.25 TODAY/HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 3.429 TONNES OF GOLD INTO THE GLD//:/INVENTORY RESTS AT 1054.419 TONNES

APRIL 6/2026/WITH GOLD UP $5.30 TODAY/NO CHANGES IN GOLD AT THE GLD:/INVENTORY RESTS AT 1050.99 TONNES

APRIL 2/2026/WITH GOLD DOWN $132.75 TODAY/HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 3.714 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 1050.99 TONNES

GLD INVENTORY: 1034.853 TONNES, TONIGHTS TOTAL GOLD INVENTORY

SILVER

MAY 28 WITH SILVER UP $1.02: NO CHANGES IN SILVER INVENTORY AT THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 27 WITH SILVER DOWN $1.61: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.176 MILLION OZ OUT OF THE SLV/ // :INVENTORY RESTS AT 487.977 MILLION OZ

MAY 26 WITH SILVER DOWN $0.14: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.131 OF 0.315 MILLION OZ INTO THE SLV/ // :INVENTORY RESTS AT 489.153 MILLION OZ

MAY 22 WITH SILVER DOWN $0.26: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.315 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 488.022 MILLION OZ

MAY 21 WITH SILVER UP $0.64: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

MAY 20 WITH SILVER UP $1.27: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

MAY 19 WITH SILVER DOWN $2.39: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.086 MILLION OZ OUT OF THE SLV:/ // :INVENTORY RESTS AT 488.338 MILLION OZ

MAY 18 WITH SILVER DOWN $0.09: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 489.424 MILLION OZ

MAY 15 WITH SILVER DOWN $7.06: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.9000 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 489.424 MILLION OZ

MAY 14 WITH SILVER DOWN $3,79: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.448 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 487.524 MILLION OZ

MAY 13 WITH SILVER UP $3,62: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.086 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 486.087 MILLION OZ

MAY 12 WITH SILVER DOWN $0.48: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.176 MILLION OZ OF SILVER OZ INTO OF THE SLV// / // :INVENTORY RESTS AT 484.990 MILLION OZ

MAY 11 WITH SILVER UP $5.10: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.995 MILLION OZ OF SILVER PUT OF THE SLV// / // :INVENTORY RESTS AT 483.814 MILLION OZ

MAY 8 WITH SILVER UP $1.25: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.689 MILLION OZ OF SILVER INTO THE SLV// / // :INVENTORY RESTS AT 484.809 MILLION OZ

MAY 7 WITH SILVER UP $2.26: NO CHANGES IN SILVER INVENTORY AT THE SLV: / // :INVENTORY RESTS AT 484.130 MILLION OZ

MAY 6 WITH SILVER UP $3.75: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.724 MILLION OZ INTO THE SLV/ // :INVENTORY RESTS AT 484.130 MILLION OZ

MAY 5 WITH SILVER UP $0.21: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.734 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 483.604 MILLION OZ

MAY 4 WITH SILVER DOWN $3.05: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.734 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 483.604 MILLION OZ

MAY 1 WITH SILVER UP $2.38: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.905 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 484.338 MILLION OZ

APRIL 30 WITH SILVER UP $2.03: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.991 MILLION OZ FROM THE SLV/ // :INVENTORY RESTS AT 485.243MILLION OZ

APRIL 29 WITH SILVER DOWN $1.95: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 28 WITH SILVER DOWN $2.05: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 27 WITH SILVER DOWN $1.39: NO CHANGES IN SILVER INVENTORY AT THE SLV:/ // :INVENTORY RESTS AT 487.234MILLION OZ

APRIL 24 WITH SILVER UP 0.92: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.54 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 487,23MILLION OZ

APRIL 23WITH SILVER DOWN $2.35: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.489 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 488,773MILLION OZ

APRIL 22 WITH SILVER UP 1.43: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262MILLION OZ

aPRIL 21 WITH SILVER DOWN 3.71: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.352 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.262 MILLION OZ

APRIL 17 WITH SILVER UP $3.09: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.453 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.900 MILLION OZ

APRIL 16 WITH SILVER DOWN $1.00: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.132 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.477 MILLION OZ

APRIL 15 WITH SILVER UP $0.01: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.588 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.579 MILLION OZ

APRIL 14 WITH SILVER UP $3.99: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.633 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 490.991 MILLION OZ

APRIL 13 WITH SILVER DOWN 0.79: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.589 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 491.624 MILLION OZ

APRIL 10 WITH SILVER DOWN 0.16: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.724 MILLION OZ OUT THE SLV// // :INVENTORY RESTS AT 492.213 MILLION OZ

APRIL 9 WITH SILVER UP $0.91: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.173 MILLION OZ INTO THE SLV// // :INVENTORY RESTS AT 492.937 MILLION OZ

APRIL 8 WITH SILVER UP $3.50: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 7 WITH SILVER DOWN $0.89: NO CHANGES IN SILVER INVENTORY AT THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 6 WITH SILVER UP $0.41: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A SMALL WITHDRAWAL OF 0.224 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.764 MILLION OZ

APRIL 2 WITH SILVER DOWN $3.57: TINY CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.091 MILLION OZ OUT OF THE SLV // :INVENTORY RESTS AT 490.988 MILLION OZ

At a certain point, Japan won’t be able to just keep dumping dollars and Treasuries to prevent its currency from imploding.

With an economy so sensitive to rate hikes after decades of zero-interest rate policy, the Bank of Japan can’t endlessly jack up the cost of borrowing without risking severe consequences. And, even if Washington could be convinced to do so, the US Treasury and Fed can’t save Japan by buying yen directly without spiking yields and weakening the relative strength of the dollar.

Japan’s repeated attempts to defend the yen through interventions are going to hit a wall of reality built from decades of ultra-loose policy, massive debt, and a collision with unyielding global forces. As Japanese Finance Minister Satsuki Katayama has affirmed, Japan stands ready to act against excessive forex volatility, emphasizing interventions that avoid spiking Treasury yields. But she walks an impossible tightrope. Foreign governments led by Japan and China are offloading Treasuries to defend their currency from oil shocks amid the ongoing conflicts in the Middle East.

As the largest foreign holder of US debt, every yen-support operation out of Japan is a potential accelerant for higher yields. In March alone, Japan shed about $47 billion in Treasuries, dropping to $1.191 trillion, as it battled yen weakness past sensitive levels amid surging energy import costs. They’re liquidating dollar assets to buy yen, directly feeding into a Treasury market already flashing warning signs. Now Treasuries have entered a “danger zone” of surging long-term yields, with the 30-year yield recently pushing above 5.2%, its highest since 2007, while the 10-year climbed toward 4.7%.

HSBC and others warn that further repricing of terminal rates could hammer risk assets. The bond vigilantes are waking up to sticky inflation, geopolitical oil spikes, and endless deficits, and Japan dumping more paper to prop up its currency (yet again) adds more powder to the keg. At what point does the feedback loop break?

Peter Schiff has been ringing the alarm bells about Japan unloading US debt. The risks of Tokyo selling US Treasuries to fund stimulus or interventions are clear, at a time when the US can’t afford it:

That will send US bond yields higher and the dollar lower, worsening stagflation.

Japan needs a weaker yen for exports but can’t tolerate a collapse, so it intervenes, selling Treasuries that push yields up and complicate the same dollar dynamics it relies on. It’s a contradiction where the math can only lead to one possible outcome: a race to the bottom. You can perform a high-wire act with no net and get away with it for one show, maybe two shows, or maybe even a hundred. But eventually, the audience is going to witness something horrible. Every time the yen needs to be rescued again, we come a little bit closer to the inevitable end result.

As a young stockbroker, I found that business from late-May onwards into the summer was doubly frustrating. Investment managers from whom I hoped to get buy orders would be “out of office”. While I was at my desk or on the floor of the stockmarket, they would be at Lord’s for test match cricket, followed by Royal Ascot for the racing and socialising, Henly for the rowing regatta, and Wimbledon for tennis. Quite simply, the buyers were out of town and in their absence the market would wilt.

For these reasons, selling in May with a view to returning to the market later in the year made sense. So off I would go to Lords, Ascot, and Wimbledon as well.

This time, there are extra reasons to be cautious.

The first is that equities have become completely detached from the reality of what’s happening to bonds. In general terms, when bond yields rise, that’s bad for equities and when they fall that’s good for equities. This is because bonds set a return hurdle for equities to at least match and even exceed their yield returns, given that equities are higher risk with uncertainty.

If you chart an equity index, such as the S&P 500 and compare it with the long bond’s yield, the correlation should be consistently negative. In other words, a track to higher bond yields will lead to lower stock prices. By inverting the bond yield, the two series should track each other. This is demonstrated in the chart below:

The red (S&P) and blue (long bond yield inverted) should track each other, and since the financialisation of the US economy over 40 years ago, that negative correlation has done just that.

There have been a few aberrations, such as the dot-com bubble in 2000 (arrowed) when investor optimism was so extreme that any student of the South-Sea bubble, or tulipomania will have recognised the psychology. Following the 2008—2009 financial crisis, interest rates and therefore bond yields were continually suppressed by monetary policy making bonds expensive relative to equities, dragging them higher. This reached a peak in 2020 with zero interest and even negative interest rate policies.

When the long bond yield began to soar from 1% in 2020, investors in equities ignored the valuation damage completely. Equities relative to bonds are now more expensive than they have ever been, indicated by the double-headed arrow to the right of the chart. It is over three times as long as the double-headed arrow marking the dotcom bubble. It is a sure sign of a massive equity bubble, which will burst; and when it does the wealth destruction will make 1929—1932 look like a minor event in comparison. It has been driven by easy credit inflating stock values, as the FINRA chart below shows:

These are loans by brokers to their clients. It is essentially retail stock leverage, because hedge funds and other large investors go to the banks and wholesale markets directly. In December 2025, according to the Office for Financial Research hedge fund gross borrowing was estimated at $7.42 trillion split between repos, prime brokerage, and other secured:

While there might be some crossover with FINRA’s figures, they confirm that total credit puffing up equities is massive. Prime brokerage and repo funding have increased very sharply along with the equity market. For anyone making the connection, it will be clear what’s driving this bubble, and that with record amounts of credit fuelling it, when the bubble bursts the consequences will be a spectacular implosion of values.

So far, equity markets have ignored the threat from bond yields. But now, President Trump has upped the ante by starting an unwinnable war on Iran. And Iran is not just going to roll over and open Hormuz. The economic damage is very serious and will lead to a lethal combination of slump and price inflation. That is a certainty which will drive bond yields higher still. The chart below should jerk anyone out of investment complacency:

Whither equities when the long bond yield breaks above 5 ¼%? Then 6%, 7%, 10%…

The one thing this flag pattern tells us is that there is going to be an almighty bond crash as yields surge higher and all that credit fuelling equities is bound to be called in. When that happens, a bear market becomes self-feeding as banks liquidate stock held as collateral into a falling market.

Tomorrow (Friday) is the last chance to sell in May. It could be the best thing to do, liquidate everything and park the proceeds in real money, which is physical gold or silver because the currency is bound to be debased as the entire financial system enters crisis.

Then you should complete the sell-in-May adage and go away, preferably to Ascot and Wimbledon. There’s a test match at Lords (England plays New Zealand next week) if you are a Brit. Other choices are available to sports fans in other nationalities.

I am hearing a lot of talk about the silver price surging to $300-$500 by the end of the summer. It seems that many silver investors are waiting for these prices to CASH IN BIG TIME. But could they?

Check back for new articles and updates at the SRSrocco Report.

END

COMMODITY GOLD

QUITE A STORY:

FBI Arrests CIA Official With $40 Million in Gold Bars, $2 Million In Cash Stashed in His Home

Wednesday, May 27, 2026 – 11:54 PM

In what may be the most bizarre story of the week, if not all of 2026, the NYTimes reports that a senior CIA official was arrested last week after investigators found hundreds of gold bars worth over $40 million stashed in his Virginia residence, a non-fiat fortune that he apparently brought home from work, according to court papers.

The CIA official, David Rush, is being held in jail while he awaits a detention hearing in the coming days on charges of stealing public money by filling out fraudulent time sheets. But, as the NYT admits, the charging documents filed in Alexandria, Va., still leave a lot unanswered about his recent conduct.

The only formal charge lodged against Rush is that he inflated his academic credentials and obtained military leave pay worth tens of thousands of dollars. The authorities say he falsely claimed to be a member of the Navy Reserve when he was discharged.

In a 2009 application for a government position for which he was subsequently hired, Rush allegedly lied about obtaining a bachelor’s degree from Clemson University and a master’s degree from Rensselaer Polytechnic Institute, according to the affidavit. The investigation revealed that Rush never attended or obtained a degree from either institution, according to the affidavit.

The court papers describe Rush as a “former senior executive service-level employee at a United States government agency.” According to NYT sources, he until very recently held a senior position at the CIA.

In a joint statement, the CIA and FBI said the arrest occurred on May 19, after the agency alerted the bureau.

“After a C.I.A. internal investigation identified potential violations of the law, C.I.A. Director John Ratcliffe referred the information to the F.B.I. for a law enforcement investigation,” the statement said.

From last November to March, the court papers say, Rush asked for, and received, “a significant quantity of foreign currency and tens of millions of dollars in gold bars for work-related expenses.”

When the CIA conducted a review of where the gold and currency were stashed, the agency was “unable to locate the gold bars or significant amounts of the foreign currency,” according to court papers.

On May 18, FBI agents searched Rush’s home and found “approximately 303 gold bars, each of which weighed approximately one kilogram,” according to an affidavit. Based on the price of gold, the affidavit said, the estimated value of the gold exceeded $40 million. Investigators also seized nearly three dozen luxury watches, many of them Rolexes.

The affidavit also claims that Rush lied about his military credentials while applying to enter the senior executive service level ranks and committed “timecard fraud” regarding military leave. He allegedly claimed 744 hours of military leave, resulting in $77,000 in compensation, since being honorably discharged from the Navy in 2015, according to the affidavit.

The biggest question of all remains unanswered: the court papers do not indicate why Rush appears to have kept so much gold, and $2 million in U.S. currency, not to mention 35 Rolexes in his home, or what work project would have required him to amass such wealth.

Below is the full charging affidavit from the criminal case (1:2026mj00177 USA vs Rush, Virginia Eastern Court).

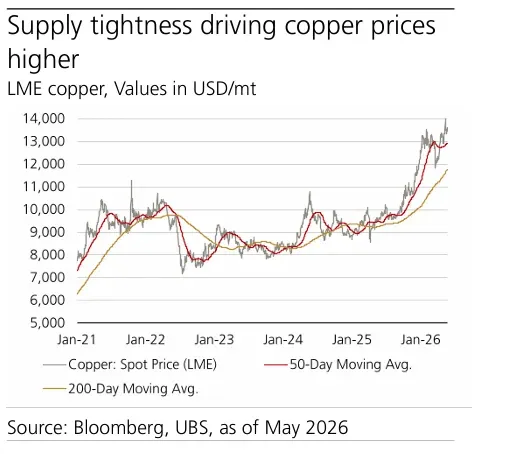

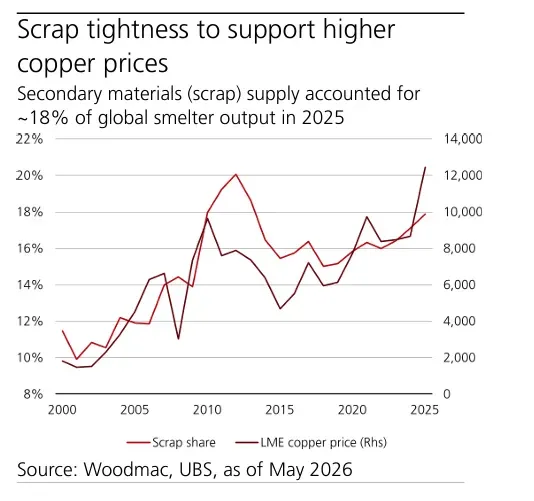

The copper market continues to trade as a supply-constrained industrial system rather than a cyclical commodity market. In a May 22 report titled Higher in Steps, analysts at UBS argue that structural shortages across concentrates, scrap, sulfur, and refined output are forcing prices steadily higher despite mixed global growth signals.

UBS now forecasts copper prices reaching USD 14,000/mt by September 2026, USD 14,500/mt by year-end, USD 15,000/mt by March 2027, and USD 15,500/mt by June 2027. The bank maintains a constructive stance and continues to recommend long exposure to copper, particularly during price pullbacks.

The Market Is Tightening from Multiple Directions

The core thesis behind the report is simple: copper supply growth is struggling to keep pace with electrification-driven demand growth.