Silver: $15.39 down 3 cents

In the access market 5:15 pm

:

Gold $1141.00

silver $15.41

Even thought gold and silver was down today, the equity shares were up considerably.

The gold comex today had a poor delivery day, registering 4 notices served for 400 oz.

Silver registered 35 notices for 175,000 oz.

A few months ago the comex had 303 tonnes of total gold. Today the total inventory rests at 250.47 tonnes for a loss of 53 tonnes over that period. .

I am deeply concerned that most of the gold that enters as a deposit at the comex are of the kilobar variety i.e. exact multiples of 32.15 oz. We have had again many transactions of this type at the comex.

In silver, the open interest contracted a bit due to the huge raid but it still remains extremely high and today at 170,139 contracts.

The December silver OI lowered to 109,395 which is as expected due to the raid.

Today, we had a huge withdrawal of gold Inventory at the GLD of 2.99 tonnes/ inventory rests tonight at 732.83 tonnes.

In silver, the SLV inventory remained constant tonight.

SLV’s inventory rests tonight at 343.450 million oz.

.

We have a few important stories to bring to your attention today…

Let’s head immediately to see the major data points for today.

First: GOFO rates: May Day!!! May Day!!! we are moving deeper into severe backwardation

All months basically moved more severely into the negative directions. Now, the first 4 month GOFO rates rocketed deeply into the negative.Almost all of the leases are down with the first 3 month GOFOs. On the 22nd of September the LBMA stated that they will not publish GOFO rates. However today we still received today’s GOFO rates.

It looks to me like these rates even though negative are still fully manipulated.

London good delivery bars are still quite scarce.

The backwardation in gold is incompatible with the raid on gold yesterday morning. It does not make any economic sense.

Nov 6 2014

1 Month Rate: 2 Month Rate 3 Month Rate 6 month rate 1 yr rate

-.185% -0.145% -.102% – .0175% + .145% (one year never used)

Nov 5 .2014:

1 Month Rate 2 Month Rate 3 Month Rate 6 month Rate 1 yr rate

-.0875% + -.05% +-02% +.052 % + .1625%

end

Let us now head over to the comex and assess trading over there today,

Here are today’s comex results:

The total gold comex open interest rose by a wide margin of 3101 contracts from 417,377 down to 414,276 with gold down $22.90 yesterday. The raid had a small success to our criminal bankers as some of the fluff left the gold arena. The next delivery month is November and here the OI actually rose by 1 contracts We had 3 delivery notices filed on yesterday so we gained 4 contracts 400 oz of additional gold ounces will stand for the November contact delivery month. The big December contract month saw it’s Oi fall by 9,912 contracts down to 254,366. The estimated volume today was good at 174,679. The confirmed volume yesterday was very good at 290,956.. Strangely on this 5th day of notices, we had only 4 notices filed for 400 oz.

And now for the silver comex results. The total OI fell by 6324 contracts from 176,8463 down to 170,139 as silver was down 51 cents yesterday. No wonder the raid yesterday as the bankers had some success in removing some of the longs. In ounces, this represents a total of 850 million oz or 121.0% of annual global supply. We are now in the non active silver contract month of November and here the OI actually rose by 10 contracts up to 135. We had 8 notices filed on yesterday so we gained 18 contracts or we have an additional 90,000 oz that will stand for the November contract month. The big December active contract month saw it’s OI fall by 6,858 contracts down to 109,395. In ounces the December contract is represented by 547 million oz or 78.1% of annual global production (production = 700 million oz – China). The estimated volume today was very good at 46,326. The confirmed volume yesterday was excellent at 99,327. We also had 35 notices filed today for 175,000 oz.

Data for the November delivery month.

November initial standings

Nov 6.2014

| Gold |

Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 50,244.43 oz(HSBC,,Manfra,)includes 3 kilobars |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 47,104.711 oz (Scotia) |

| No of oz served (contracts) today | 4 contracts( 400 oz) |

| No of oz to be served (notices) | 52 contracts (5200 oz) |

| Total monthly oz gold served (contracts) so far this month | 9 contracts (900 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | 80,224.3 oz |

|

Total accumulative withdrawal of gold from the Customer inventory this month |

514,484.8 oz |

Today, we had 0 dealer transactions

total dealer withdrawal: nil oz

total dealer deposit: nil oz

we had 2 customer withdrawals: and again we had these wonderful kilobar transactions

i) Out of HSBC: 50,147.98 oz

ii) Out of Manfra; 96.45 oz (3 kilobars)

total customer withdrawals : 560,244.43 oz

we had 1 customer deposits:

i) Into Scotia: 47,104.71 oz

total customer deposits : 47,104.71 o oz

We had 0 adjustments:

Total Dealer inventory: 869,309.361 oz or 27.03 tonnes

Total gold inventory (dealer and customer) = 8.052 million oz. (250.47) tonnes)

Several weeks ago we had total gold inventory of 303 tonnes, so during this short time period 53 tonnes have been net transferred out. We will be watching this closely!

Today, 0 notices was issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 4 contracts of which 0 notices were stopped (received) by JPMorgan dealer and 0 notices were stopped by JPMorgan customer account.

To calculate the total number of gold ounces standing for the November contract month, we take the total number of notices filed for the month (9) x 100 oz to which we add the difference between the OI for the front month of November (56) – the number of gold notices filed today (4) x 100 oz = the amount of gold oz standing for the November contract month.

Thus the in initial standings:

9 (notices filed today x 100 oz + (56) OI for November – 4 (no of notices filed today = 6100 oz (.1897 tonnes)

we gained 400 oz of gold standing for the November contract month.

Nov 6/2014:

November silver: initial standings

| Silver |

Ounces |

| Withdrawals from Dealers Inventory | nil oz (Scotia) |

| Withdrawals from Customer Inventory | 937,957.109 oz (Delaware,HSBC) |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | nil |

| No of oz served (contracts) | 35 contracts (170,000 oz) |

| No of oz to be served (notices) | 100 contracts (500,000 oz) |

| Total monthly oz silver served (contracts) | 112 contracts (560,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | 183,382.9. oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 3,096,793.2 oz |

Today, we had 0 deposits into the dealer account:

total dealer deposit: nil oz

we had 0 dealer withdrawal:

total dealer withdrawal: nil oz

We had 2 customer withdrawals:

i)Out of Delaware: 337,920.949 oz

ii) Out of HSBC: 600,036.160 oz

total customer withdrawal 937,957.109 oz

We had 0 customer deposits:

total customer deposits: nil oz

we had 0 adjustments

Total dealer inventory: 66.140 million oz

Total of all silver inventory (dealer and customer) 180.217 million oz.

The total number of notices filed today is represented by 35 contracts or 175,000 oz. To calculate the number of silver ounces that will stand for delivery in November, we take the total number of notices filed for the month (112 ) x 5,000 oz to which we add the difference between the total OI for the front month of November(135) minus (the number of notices filed today (35) x 5,000 oz = the total number of silver oz standing so far in November.

Thus: 112 contracts x 5000 oz + (135) OI for the November contract month – 35 (the number of notices filed today) = amount standing or 1,060,000 oz

we gained 90,000 oz of silver standing.

It looks like China is still in a holding pattern ready to pounce when needed.

end

The two ETF’s that I follow are the GLD and SLV. You must be very careful in trading these vehicles as these funds do not have any beneficial gold or silver behind them. They probably have only paper claims and when the dust settles, on a collapse, there will be countless class action lawsuits trying to recover your lost investment.

There is now evidence that the GLD and SLV are paper settling on the comex.

***I do not think that the GLD will head to zero as we still have some GLD shareholders who think that gold is the right vehicle to be in even though they do not understand the difference between paper gold and physical gold. I can visualize demand coming to the buyers side:

i) demand from paper gold shareholders

ii) demand from the bankers who then redeem for gold to send this gold onto China

vs no sellers of GLD paper.

And now the Gold inventory at the GLD:

Nov 6.2014: we had another huge withdrawal of 2.99 tonnes of gold.

This gold is also heading to Shanghai. If I was a shareholder of GLD I would be quite concerned as there will be no real gold inventory left per outstanding shares.

Nov 5 we had another huge withdrawal of 3.000 tonnes of gold. This gold will be heading to Shanghai/GLD inventory 735.82 tonnes

Nov 4.2014: a huge withdrawal of 2.39 tonnes of gold/GLD inventory/738.82 tonnes

Nov 3.2014: no change in gold inventory at the GLD/741.21 tonnes

Oct 31.2014: no change in gold inventory at the GLD despite the raid/inventory at 741.21 tonnes

October 30.2014: we had another 1.2 tonnes of gold leave the GLD and heading to Shanghai/Inventory 741.21 tonnes

October 29.2014: we had another .99 tonnes of gold removed from the GLD/inventory 742.40 tonnes

Oct 28.2014: we had another withdrawal of exactly 2 tonnes of gold heading to Shanghai; Inventory 743.39 tonnes

Oct 27.2014: no change in gold inventory at the GLD/inventory 745.39 tonnes.

Oct 24.2014: a huge withdrawal of 4.48 tonnes of gold at the GLD/Inventory 745.39 tonnes. This gold is heading to friendly territory: namely Shanghai.

Oct 23.2014: no change in gold inventory at the GLD/Inventory at 749.87 tonnes.

Oct 22.2014: we lost another 2.1 tonnes of gold at the GLD. Inventory rests at 749.87 tonnes. This tonnage no doubt is off to Shanghai.

Oct 21.2014: no change in inventory/GLD inventory rests tonight at 751.96 tonnes.

Today, Nov 6. a huge withdrawal of 3.00 tonnes gold inventory at the GLD

inventory: 732.83 tonnes.

The registered vaults at the GLD will eventually become a crime scene as real physical gold departs for eastern shores leaving behind paper obligations to the remaining shareholders. There is no doubt in my mind that GLD has nowhere near the gold that say they have and this will eventually lead to the default at the LBMA and then onto the comex in a heartbeat (same banks).

GLD gold: 732.83 tonnes.

end

And now for silver:

Nov 6.2014: no change in silver inventory/(as of 6 pm est) inventory rests at 343.45 million oz.

Nov 5 today, the total silver inventory drops of 2.074 million oz/SLV inventory: 343.45 million oz

Nov 4.2014: wow!! we had another addition of 1.151 million oz of silver inventory/SLV inventory rises to 345.524

Please note the difference between GLD and SLV. The GLD has physical gold to send on its way to Shanghai/SLV has no silver to offer to the participants to give to various players..

Nov 3.2014: this is good news: the “actual silver inventory” rose by 958,000 oz to 344.373 oz

(I guess there is no physical silver to raid from the SLV vaults:)

October 31.2014: despite the huge raids yesterday and today: no change in silver inventory at the SLV/inventory at 343.415 million oz

October 30.2014; no change in silver inventory at the SLV/inventory at 343.415 million oz

October 29.2014 no change in silver inventory at the SLV inventory/343.415 million oz

October 28.2014: no change in silver inventory at the SLV/Inventory at 343.415 million oz

Oct 27.2014: no change in silver inventory at the SLV

Oct 24.2014: as of 6 pm, there is no change in silver inventory at the SLV. Note the difference between gold and silver. Gold leaves the vault of GLD as little silver leaves the SLV. (I guess it means that there is no silver to give to the banker participants)/Inventory: 343.415 million oz

Oct 23.2014: no change in silver inventory at the SLV (as of 6 pm est

Inventory: 343.415 million oz

Oct 22.2014: no change in silver inventory at the SLV ( as of 6 pm est)

Inventory: 343.415

Oct 21.2014; no change in silver inventory at the SLV (as of 6 pm est)

Oct 20.2014: we lost 1.15 million oz of silver inventory at the SLV/inventory 343.415 million oz

Oct 17.2014: no change in silver inventory/344.565 million oz

end

And now for our premiums to NAV for the funds I follow:

Note: Sprott silver fund now deeply into the positive to NAV

Sprott and Central Fund of Canada.

(both of these funds have 100% physical metal behind them and unencumbered and I can vouch for that)

1. Central Fund of Canada: traded at Negative 10,1% percent to NAV in usa funds and Negative 10.1% to NAV for Cdn funds

Percentage of fund in gold 61.9%

Percentage of fund in silver:37.50%

cash .6%

( Nov 6/2014)

2. Sprott silver fund (PSLV): Premium to NAV rises to positive 4.89% NAV (Nov 6/2014)

3. Sprott gold fund (PHYS): premium to NAV falls to negative -0.56% to NAV(Nov 6/2014)

Note: Sprott silver trust back hugely into positive territory at 4.89%.

Sprott physical gold trust is back in negative territory at -0.56%

Central fund of Canada’s is still in jail.

end

And now for your most important physical stories on gold and silver today:

Early gold trading form Europe early Wednesday morning:

(courtesy Goldcore/Mark O’Byrne)

U.S. Mint Sells Out of Silver Eagle Coins as Buying Surges

The gulf between the physical precious metals markets and the paper or electronic gold and silver markets is growing again and risks becoming as broad as it has ever been. Demand for gold and particularly silver bullion has been very high across the world in recent weeks.

The sharp price falls in recent days has led to even greater demand and concerns about supply and rising bullion premiums. Now the U.S. Mint is sold out and the Canadian Mint is rationing supplies.

This comes at a time when silver is being hammered in the futures market by entities who are selling enormous volumes of gold and silver futures. They are using leverage and are engaged in a form of naked short selling that is pushing the spot prices for physical delivery lower.

By forcing the price down so dramatically they cause those parties who speculate on a higher price in the precious metals futures markets to capitulate. They also cause some physical owners, weak hands who are nervous regarding gold and silver prices, to sell. Often at the worst times. It also has the effect of dampening spirits in the precious metal markets and creating very negative sentiment.

Sentiment is as poor as we have ever seen it regarding gold and silver amongst many analysts especially in banks, the media and the public.

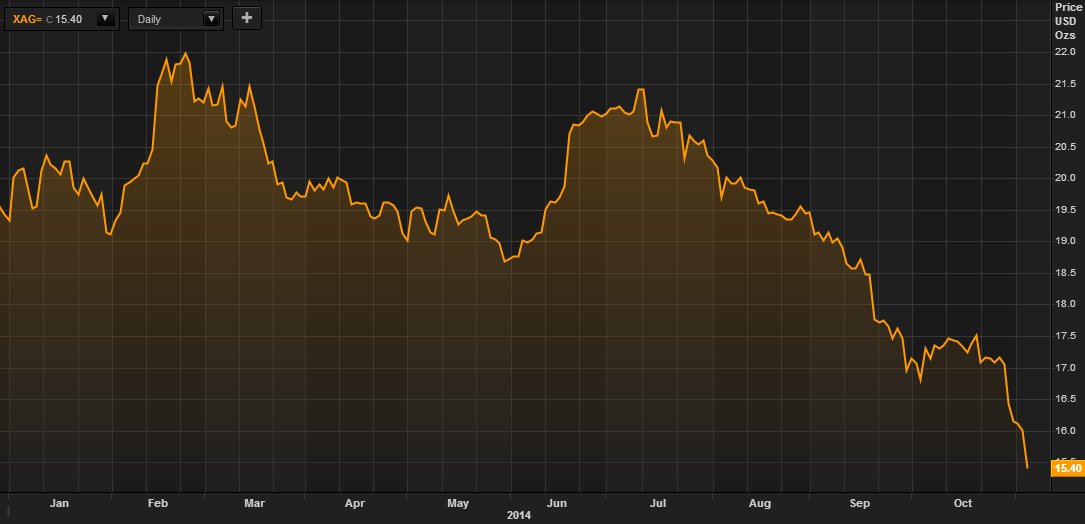

Silver in USD – 5 Years (Thomson Reuters)

However, there is a huge dichotomy as sentiment amongst the hard asset community or those who understand the importance of gold and silver as stores of value is very positive and they are the ones who are accumulating again on this price dip.

Bullion dealers across the western world have been reporting shortages in silver bullion coins and bars. Yesterday the U.S. Mint who, heretofore had not reported any issues regarding supply, announced that they had been cleared out of their entire remaining inventory of 2014 silver eagle coins.

With two months still remaining in the year their stock was cleared out yesterday when dealers, desperate to meet exploding retail demand,bought two million silver eagle coins in only two hours.

So why is demand so robust at a time when the market action suggests that silver is not a desirable asset to own?

Silver in USD – Year to Date 2014 (Thomson Reuters)

The ratio between the price of gold and the price of silver is now at around 74:1. The historical average has been roughly 15:1. Were this mean to be reverted to again, the price of silver would need to rise to around $76 even at these depressed gold prices.

After six years of talk of recovery many people in the west have grown distrustful of the ability and will of their leaders to effect positive change for ordinary people and fear another crisis is imminent.

They are taking matters into their own hands by becoming “their own central bank” as Doctor Marc Faber puts it.

It is worth considering Dr. Faber’s take on Goldman Sachs talking down the precious metals markets.

“I would say Goldman Sachs is very good at predicting lower prices when they want to buy something.” It may be that prices have been forced down specifically because large entities feel the need to begin accumulating physical gold and silver now that QE has been shelved. At least for now.

Despite huge complacency, on par with that seen in 2006 prior to the last crisis, there remains considerable geopolitical, financial and monetary risk throughout the world. The increased demand we have seen in recent days is not likely to be a mere blip on price weakness and will likely continue until prices have risen significantly again.

We strongly advise owning allocated and segregated individual bullion coins and bars stored in the safest vaults in the safest jurisdictions in the world.

Get Breaking News and Updates on the Gold Market Here

MARKET UPDATE

Today’s AM fix was USD 1,144.50, EUR 914.94 and GBP 717.11 per ounce.

Yesterday’s AM fix was USD 1,145.25, EUR 917.30 and GBP 720.96 per ounce.

Gold fell $25.30 or 2.17% to $1,142.40 per ounce yesterday and silver slid $0.75 or 4.68% at $15.28 per ounce.

Gold inched higher on Thursday as a pull back in the U.S. dollar took some pressure off the yellow metal after its downward spiral to four-year lows. Prices remained essentially flat ahead of a European Central Bank meeting later today.

In London, gold for immediate delivery climbed 0.4% to $1,144.90 an ounce as of 10:58 a.m. On the Comex in New York, bullion for December delivery fell 0.1% to $1,144.10 an ounce.

Gold’s 14-day relative strength index (RSI) was under 30 for a fifth day, signaling to some investors that prices will rebound.

Spot silver slipped 0.2% to $15.3035 an ounce. An ounce of gold bought as much as 75.1862 ounces of silver yesterday, the most since January 2009. The ratio was at 74.8179 today. Silver has dropped for its 7th day its longest losing streak since April 2013.

Spot platinum climbed 0.4% to $1,209.75 an ounce after the price fell yesterday to $1,197.13, the lowest in a month. Palladium was little changed at $758.75 an ounce.

Investors await non farm payrolls and expect 235,000 jobs to be added in October, and the jobless rate held at over a six-year low of 5.9%.

As the recent election showed, there is huge discontent regarding the U.S. economy. Middle America does not think the economy has improved. The headline figures disguise a very fragile economy where the middle classes and poor continue to struggle financially.

end

Seth Lipsky: Republicans should start by fixing the Fed

Submitted by cpowell on Thu, 2014-11-06 02:15. Section: Daily Dispatches

By Seth Lipsky

New York Post

Wednesday, November 5, 2014

The Republican sweep offers the new Congress a chance to do a lot of good things, but none is more timely or strategic than monetary reform. Of all the things the Democratic Senate was getting in the way of, it’s the most important.

I’d start with “Audit the Fed.” As recently as September, this passed by an overwhelming bipartisan margin in the House, 333 to 92.

The idea is not simply to look at the Federal Reserve’s books. (They’re audited every year.) It’s to find out what the Fed is doing at home and abroad and how it makes its decisions. …

… For the complete commentary:

http://nypost.com/2014/11/05/gop-should-start-fixing-the-fed/

Lassonde reconsiders, admits BIS may be manipulating gold market

Submitted by cpowell on Wed, 2014-11-05 23:56. Section: Daily Dispatches

7p ET Wednesday, November 5, 2014

Dear Friend of GATA and Gold:

Mining entrepreneur and former World Gold Council Chairman Pierre Lassonde, who lately has been saying that central banks don’t even think about gold —

http://www.gata.org/node/13683

http://www.gata.org/node/13105

http://www.kitco.com/news/video/show/GSA-Investor-Day-2014/558/2014-02-2…

— today applied for a tin-foil hat.

Pressed by Eric King of King World News, Lassonde acknowledged that, as Hong Kong fund manager William Kaye had told KWN a little earlier, the Bank for International Settlements very well might be pushing the gold market around.

“It would not be the first time that we’ve seen this and it won’t be the last time either.” Lassonde told KWN. “There is obviously an entity or trading house who must have a short position and they are using the paper gold market to move the price.”

Things must have gotten beyond obvious. What’s next? Anarchist Doug Casey retracting his claim that central banks are irrelevant? Commodity leter writer Dennis Gartman’s deciding to care about market manipulation, or about anything?

Lassonde’s interview is excerpted at the KWN blog here:

http://kingworldnews.com/kingworldnews/KWN_DailyWeb/Entries/2014/11/5_Pi…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

Dallas Fed president warns Republicans against making central bank account for itself

Submitted by cpowell on Wed, 2014-11-05 22:50. Section: Daily Dispatches

Fed’s Fisher Tells Congress: Don’t Mess with Central Bank

By Matthew Boesler and Michael McKee

Bloomberg News

Wednesday, November 5, 2014

NEW YORK — Senate Republicans should resist the temptation to erode Federal Reserve independence after victory in mid-term elections, Dallas Fed President Richard Fisher said.

“Think about this: Here’s a Congress that can’t even get its own budget together. Do you want them running the central bank?” Fisher, a former deputy U.S. trade representative under President Bill Clinton, said today in an interview on Bloomberg Television.

Republicans who already run the House won command of the Senate yesterday and will take charge of the Senate Banking Committee, which oversees the U.S. central bank, when the next Congress convenes in January.

Lawmakers have sponsored several bills that propose changes in the way the Fed conducts monetary policy and would subject the institution to greater congressional scrutiny. …

… For the remainder of the report:

http://www.bloomberg.com/news/2014-11-05/fed-s-fisher-tells-congress-don..

end

Gold and silver in backwardation in London and in Shanghai

a must read..

(courtesy Bill Kaye/Kingworldnews)

Gold, silver in backwardation as a result of BIS paper dumping, Kaye tells KWN

Submitted by cpowell on Wed, 2014-11-05 21:38. Section: Daily Dispatches

4:35p ET Wednesday, November 5, 2014

Dear Friend of GATA and Gold:

Gold and silver are in backwardation, Hong Kong fund manager William Kaye today tells King World News, which is “typical of what you see when there is overt manipulation.” Kaye attributes the situation to “an awful lot of paper gold intentionally dumped in a programmed algorithm … most likely by the Bank for International Settlements.” An excerpt from the interview is posted at the KWN blog here:

http://kingworldnews.com/kingworldnews/KWN_DailyWeb/Entries/2014/11/5_Sh…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

end

Koos Jansen takes on Reuters for their faulty reporting.

As he reported to you earlier this week: Gold demand from China equates to 61 tonnes this week.

Indian demand for the month of September totaled 94 tonnes. (not including any smuggling figures)

(courtesy Koos Jansen)

The Mainstream Media Versus Gold

One of these weird things happened on Monday November 3, 2014, in the gold space. I published an article in which I reported gold demand in China, measured by withdrawals from the vaults of the Shanghai Gold Exchange (SGE),was exceptionally strong in recent weeks. In week 43 SGE withdrawals accounted for 60 metric tonnes of gold (SGE withdrawals have proven to be the best indicator for Chinese wholesale demand, confirmed by SGE officials). Additionally, I hinted at the fact the Chinese continue to buy more gold whenever the price drops, and the price has been dropping for the past two weeks.

The same day Reuters and the Wall Street Journal reported Chinese gold demand was weakening, regardless of the low prices. Let’s go through their analysis. From the WSJ:

Gold prices in Shanghai normally carry a premium to global prices, but that reversed to a rare discount Monday. The premium, which is attributable to capital controls, was $2 to $3 an ounce to London prices about a week ago.

…“You would not have expected Shanghai gold to be at a discount,” said a leading Hong Kong-based executive with an international bank, who didn’t want to be identified. “The physical buying in gold has dried up.”

From Reuters:

Unusually, prices on the Shanghai Gold Exchange, the world’s biggest platform for physical trade, are at a discount of around $1 an ounce to the global benchmark, slipping from premiums of $1-$2 an ounce last week.

Both these mainstream media are stating SGE gold was trading at a rare discount on November 3, 2014. First of all, an SGE discount isn’t rare at all, it happens all the time. This is incorrect information from the mainstream media.

Second, SGE gold wasn’t trading at a discount on November 3, 2014.

I have two data feeds for charting SGE gold premiums. One is from the SGE itself, published in their weekly Chinese reports, the other one I use is from Sharelynx.com, which has setup an automated Excel sheet for me that daily updates many quotes I track. The next chart is based on the numbers from Sharelynx, updated until November 4, 2014:

As you can see on November 3 the SGE physical contract Au9999 was trading at a premium to London spot (I also double checked the premium manually). The discount reported by the mainstream media is incorrect information.

In the next chart we can see SGE premiums are correlated to SGE withdrawals. Which makes sense as the Chinese buy more gold when the price drops (exhibit 1) and SGE premiums go up when the gold price drops (exhibit 2).

More from Reuters November 3, 2014:

Since all physical gold trade in China goes through the exchange [SGE], it is seen as a reliable barometer of Chinese demand.

SGE officials, and the China Gold Association, have clearly confirmed withdrawals are the best indicator for Chinese wholesale gold demand. From Scotiabank, September 29, 2014:

First, the withdrawal data reflects the actual gold wholesales in China. In 2013, the total gold withdrawal from the SGE vaults amounted to 2,196.96 tonnes. The President of the SGE Transaction Department said: “This 2,200 tonnes of gold, after leaving our vaults, they entered thousands of Chinese households in the form of jewelry and investment purchases.”

Though Reuters acknowledges all physical gold trade in China goes through the SGE, they refuse to publish the numbers on how much is going through (SGE withdrawals). I think it’s weird mainstream media never report on SGE withdrawals, or the significance of these numbers. If Reuters would have reported on SGE withdrawals on November 3, it would be impossible to commingle with a story of weak Chinese gold demand.

When I first found out about SGE withdrawals in May 2013 I’ve written emails to many mainstream media (Bloomberg, the Financial Times, the Guardian, Reuters, etc.). Hereafter, both Reuters and Bloomberg reported about SGE withdrawals once (that I know of). Bloomberg, 15 July 2013:

The Shanghai Gold Exchange supplied 1,098 metric tons in the six months through June, compared with 1,139 tons for the whole of last year, according to data from the bourse today.

Reuters on 18 October 2013:

Physical deliveries from the Shanghai Gold Exchange totaled 1,709.056 tonnes as of Friday, data on the exchange’s website showed.

After these publications Bloomberg and Reuters stopped reporting on SGE withdrawals. (please comments below if I’ve missed any mainstream media publications on SGE withdrawals).

Reuters reporting on weak Chinese gold demand while SGE withdrawals have been sky high in recent weeks, reminded me of an older article from Reuters. From September 12, 2014:

India’s love affair with gold may be over, as prices slide

Kiran Laxman Salunkhe used to buy jewellery during religious festivals, but sliding gold prices have led the young farmer to break with his family’s traditional investment.

This year Salunkhe has deposited his hard-earned savings at the bank for the first time in a decade…

…”Nowadays it is risky to keep jewellery. Burglaries are rising,” he said. “With a fixed deposit there is no risk.”

That’s right, Reuters’ headline literally stated “India’s love affair with gold may be over”, because Kiran Laxman Salunkhe, a young farmer, stopped buying gold. India’s population is over 1.2 billion people and I’m not so sure if they all stopped buying gold in September to open up a bank account.

Recently India’s custom department came out with the gold import numbers from September (when Kiran Laxman Salunkhe stopped buying gold). India officially imported, excluding smuggling, 94 tonnes of gold, which was the strongest month since June 2013. The indians imported this much gold despite the 10 % import duty.

Of course India’s love for gold is part of their culture and is engraved into the DNA of the Indian population. Reuters’ headline and article in itself were ridiculous. The fact that India actually imported more gold in September than they had over a year makes the article completely incorrect.

Can it be Chinese gold demand is currently very strong, despite the WSJ quotes a leading Hong Kong-based executive with an international bank, who didn’t want to be identified, stating: “The physical buying in gold has dried up”? Yes it can.

Koos Jansen

end

Today the GOFO rates are severely negative for 6 months out.

Zero hedge discusses the meaning of this. Generally when you have

negative GOFO’s rates, it is because of scarcity of metal

(courtesy zero hedge)

Physical Gold Shortage Worst In Over A Decade: GOFO Most Negative Since 2001

The last time there was an systemic physical gold shortage was in July 2013. It is then that, for the first time in 5 years, the 1-month Gold forward offered rate, or GOFO, went negative. We said:

Today, something happened that has not happened since the Lehman collapse: the 1 Month Gold Forward Offered (GOFO) rate turned negative, from 0.015% to -0.065%, for the first time in nearly 5 years, or technically since just after the Lehman bankruptcy precipitated AIG bailout in November 2011. And if one looks at the 3 Month GOFO, which also turned shockingly negative overnight from 0.05% to -0.03%, one has to go back all the way to the 1999 Washington Agreement on gold, to find the last time that particular GOFO rate was negative.

Fast forward to today, when as noted over the past weekthere has been a massive shortage of precious metals – most notably silver which as of this moment is indefinitelyunavailable at the US Mint – as a result of the tumble in the paper price, and following 8 days of sliding and negative 1 month GOFO rates, today the physical metal shortage surged, as can be seen by not only the first negative 6 month GOFO rate since last summer’s much publicized gold shortage when China was gobbling up every piece of shiny yellow rock available for sale, but a 1 month GOFO of -0.1850%: the most negative it has been since 2001!

Said otherwise, the physical shortage is the worst it has been in over a decade, even as the price of paper gold continues to drop!

And for those for whom the topic of GOFO inversion is new, here is how we described the situation last time:

* * *

What is GOFO (Gold Forward Offered Rates)?

GOFO stands for Gold Forward Offered Rate. These are rates at which contributors are prepared to lend gold on a swap against US dollars. Quotes are made for 1-, 2-, 3-, 6- and 12-month periods.

Who provides the rates?

The contributors are the Market Making Members of the LBMA: The Bank of Nova Scotia–ScotiaMocatta, Barclays Bank Plc, Deutsche Bank AG, HSBC Bank USA London Branch, Goldman Sachs, JP Morgan Chase Bank, Société Générale and UBS AG.

When are the rates quoted?

The means are set at 11 am London time. These are the rates shown on the LBMA website. To show derived gold lease rates, the GOFO means are subtracted from the corresponding values of the LIBOR (London Interbank Offered Rates) US dollar means. These rates are also available on the LBMA website.

How are the GOFO means established?

At 10.30 am London time, the Reuters page is cleared of all rates. Contributors then enter their rates for all time periods. A minimum of six contributors must enter rates in order for the means to be calculated. At 11.00 am, the mean is established for each maturity by discarding the highest and lowest quotations in each period and averaging the remaining rates.

What are some uses for GOFO means in the market?

They provide a basis for some finance and loan agreements as well as for the settlement of gold Interest Rate Swaps.

* * *

Unpleasant similarities with Libor and most other fixed (literally and metaphorically) rates aside, what is known is that under normal market conditions, GOFO is always positive, or in other words gold serves as a money-equivalent collateral for a pseudo-secured loan against paper fiat (USD in this case) hence the low interest rate.

Sometimes, however, normality inverts and the rate goes negative and as such serves as a useful indicator of gold market dislocations. Thus, while disagreements exists, one can safely say that what GOFO is, is simply a blended indicator of liquidity, counterparty or collateral (physical availability) stress in the gold market. Since it is next to impossible to isolate just which component is causing the indicated disturbance, it is prudent to be on watch for all three.

The best known example of a complete collapse in the GOFO rate, is the September 1999 Washington Agreement on Gold, which in brief, was an imposed “cap” on gold sales (mostly European in the afteramth of Gordon Brown’s idiotic sale of UK’s gold) to the tune of 400 tons per year. The tangent of the Washington Agreement is quite interesting in its own right. Recall the words of Milling-Stanley from the 12th Nikkei Gold Conference:

“Central bank independence is enshrined in law in many countries, and central bankers tend to be independent thinkers. It is worth asking why such a large group of them decided to associate themselves with this highly unusual agreement…At the same time, through our close contacts with central banks, the Council has been aware that some of the biggest holders have for some time been concerned about the impact on the gold price—and thus on the value of their gold reserves—of unfounded rumours, and about the use of official gold for speculative purposes.

“Several of the central bankers involved had said repeatedly they had no intention of selling any of their gold, but they had been saying that as individuals—and no-one had taken any notice. I think that is what Mr. Duisenberg meant when he said they were making this statement to clarify their intentions.”

Of course, this happened in a time long ago, when the primacy of Fractional reserve banking was sacrosanct, when the first Greenspan credit bubble (dot com) was yet to appear, and when barbarous relics were indeed a thing of the past, only to be proven oh so contemporaryfollowing not one, not two, but three subsequent cheap-credit bubbles which have vastly undermined the religious faith in fiath and central banking, sending the price of gold to all time highs as recently as 2011.

Another subsequent negative GOFO episode occurred in early 2001, which coincided with what has been rumored to be a speculative attack and reversal of the futures market. However, while pushing 1 month rates negative, 3 month rates remained well positive.

Indeed, the only other time when both 1M and 3M GOFOs were both negative or almost so (3M touched on 0.05%) was in the aftermath of the AIG bailout following the Lehman collapse in November 2008.

Fast forward to today, when all GOFOs, from 1M all the way to 6M just went negative.

And while both Antal Fekete and Sandeep Jaitly, traditionally two of the most vocal pundits in the arena of gold backwardation and temporal and collateral gold market arbritrage, are likely come up with their own interpretations of what may be causing this historic inversion, the reality is that one can’t know for sure until after the fact. It may be one of many things:

- An ETF-induced repricing of paper and physical gold

- Ongoing deliverable concerns and/or shortages involving one (JPM) or more Comex gold members.

- Liquidations in the paper gold market

- A shortage of physical gold for a non-bullion bank market participant

- A major fund unwinding a futures pair trade involving at least one gold leasing leg

- An ongoing bullion bank failure with or without an associated allocated gold bank “run”

- All of the above

The answer for now is unknown. What is known is that something very abnormal is once again afoot at the nexus of the gold fractional reserve lending market.

end

And now Bill Holter with a very important commentary!!

(courtesy Bill Holter/Miles Franklin)

Why would we do this …now?

Very big news on the banking front, the Federal Reserve is now apparently allowing Chinese bankshttp://www.telegraph.co.uk/finance/newsbysector/banksandfinance/9256036/Federal-Reserve-allows-Chinese-controlled-banks-to-take-stakes-in-US-banks.html to take stakes in U.S. banks. North of our border, Canada is contemplating becoming one of the many, recent, “renminbi hubs”. http://www.theglobeandmail.com/report-on-business/international-business/asian-pacific-business/canadian-renminbi-hub-would-boost-exports-report/article21157379/Why would this be happening? Why would it be happening now?

And now for our more important paper stories

today:

1. Stocks mostly down with Asian bourses with a slightly higher yen values to 114.63

2 Nikkei down 145 points or 0.86% (despite inflating currency)

3. Europe stocks mixed (waiting for Draghi)/Euro rises/ USA dollar index down at 87.57.

3b Japan 10 year yield at .47%/Japanese yen vs usa cross now at 114.63/

3c Nikkei now below 17,000

3d Abe goes all in with another QE/it is now all up to Japan to stimulate the world/will be known as the great Yen massacre!!!

3e The USA/Yen rate crosses the 115 barrier last night (see below)

3fOil: WTI 78.40 Brent: 82.74 /RUSSIA deeply hurt with these low oil prices/also USA shale oil in trouble

3g/ Gold up/yen up; yen above 114 to the dollar/

3h/ Japan is to buy the equivalent of 108 billion usa dollars worth of bonds per MONTH or $1.3 trillion

Japan’s GDP equals 5 trillion usa/thus bond purchases of 26% of GDP

3i Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt.

3j Republican victory gives them control over the senate and house.

Republicans threaten to audit the Fed plus the Canadian–USA Keystone pipeline approval.

3j Gold at $1145 dollars/ Silver: $15.30

4. USA 10 yr treasury bond at 2.36% early this morning.

5. Details Ransquawk/Bloomberg/Deutche bank/Jim Reid

(courtesy zero hedge)/your early morning trading

Futures Flat With All Eyes On ECB’s Mario Draghi, Who Will Promise Much And “Probably Do Nothing”

With last night’s latest Japanese flash crash firmly forgotten until the next time the trapdoor trade springs open and swallows a whole lot of momentum chasing Virtu vacuum tubes, it is time to look from east to west, Frankfurt to be precise, where in 45 minutes the ECB may or may not say something of importance. As Deutsche Bank comments, “Today is the most important day since…. well the last important day as the ECB hosts its widely anticipated monthly meeting.” Whilst not many expect concrete action, the success will be judged on how much Draghi hints at much more future action whilst actually probably doing nothing.

Between June and September the ECB seemed like it was catching up with the curve that many feel it is behind. However last month’s press conference saw many disappointed at Draghi with the feeling he was back-tracking on prior dovishness. Indeed many feel his performance last month contributed to the large falls in markets over the following week so the stakes are fairly high.

As a reminder, Reuters previously reported that “At least seven and possibly as many as 10 of the 24 council members are against U.S.-style quantitative easing.” The article pointed to deep disharmony and there are bound to be questions about it today in the Q&A.

As a result, European equities started the session off on a cautious note, as participants sit on the side-lines ahead of the widely anticipated ECB meeting, with a mixed batch of German earnings failing to provide the DAX with any further direction. This morning saw a host of earnings reports which have dictated the state of play in stock-specific moves, with UK supermarket Morrisons (+8.6%) helping to boost the UK retail sector and German sports maker Adidas (+4.5%) helping provide the DAX with some support as they look to target their troubled Russian and golf units. Elsewhere, fixed income markets remain relatively unmoved despite the modest softness in stocks, with volumes particularly thin ahead of ECB Draghi’s press conference. Nonetheless, Spanish paper was provided some reprieve following a strong triple-tranche auction with all b/c higher than previous and average yields lower than previous. However, the French Tresor failed to endure the same fate as their offering was poorly received by the market and sent their benchmark 10yr lower by 45 ticks.

Looking at Asian markets this morning the Nikkei has been particularly volatile, trading up as much 0.5% to pare back all those gains and trade -0.8% at time of writing. The Yen has reflected this move to trade up against the Dollar having previously hit a seven year low. Elsewhere markets are weaker with bourses in Hong Kong, China and Australia modestly down, the latter reported labour data relatively in line with expectations. Quickly looking at the micro, Bank of China’s debut Basel-III compliant US Dollar deal has closed with the $3bn bond deal attracting $18bn of orders for the 10-year maturity notes.

FX markets have been the main source of focus given the overnight movements in the USD-index. More specifically, JPY initially came under significant selling pressure with USD/JPY breaking above 115.00 for the first time since December 2007, while EUR/JPY surged to a 10-month high and GBP/JPY traded at October 2008 levels. However, the JPY sell-off was then abruptly unwound as major JPY crosses dropped over 1 point across the board to trade relatively flat, attributed to widening spreads and a paucity of orders. Elsewhere, AUD saw some whipsaw price action overnight following the Australian jobs report, as the better than Exp. job gains figure was shrugged off as participants focused on the unemployment rate; highest since September 2002. Furthermore, the RUB sits at record lows against the USD once again after the Russian central bank altered their intervention policy yesterday.

In terms of the day ahead and aside from the focus on the ECB today, participants look at the weekly US jobs report and the EIA natural gas storage change figure. Finally the Fed’s Evans will be speaking publically in Chicago so we will be keeping an eye for any interesting remarks to come out of that.

Bulletin Highlight Summary from RanSquawk and Bloomberg

- European participants hold fire as markets await the latest policy announcements from the ECB, with focus on the central bank’s response to the continuing fall in long-term inflation expectations.

- FX markets continue to be dominated by movements in the USD-index, with USD/JPY seeing an abrupt sell-off overnight as investors book profits.

- Participants look ahead to the stream of upcoming risk events which include the BoE and ECB rate decisions, the weekly US jobs report and the EIA natural gas storage change figure.

- Treasuries gain before ECB rate decision and Draghi press conference; October nonfarm payrolls tomorrow, est. 225k, unemployment rate holding at

- 5.9%.

- Two years after he corralled policy makers to back his plan to save the euro, Draghi is struggling to galvanize similar support for more stimulus to rescue the region’s economy

- Draghi will probably insist at press conference that he can overcome divisions on the Governing Council as officials prepare their final forecasts in 2014

- China’s central bank has published details on its latest tool to provide liquidity as it refrains from across-the- board cuts to benchmark interest rates

- Traders raised expectations for currency price swings to the highest in more than a year as an unexpected stimulus boost from the Bank of Japan roiled markets and prompted speculation its European counterpart will respond

- Obama and Senate Republican leader Mitch McConnell promised Americans yesterday they’d search for common ground, then fired the opening salvos of a new battle over immigration

- Republican Senator Rand Paul yesterday tied Hillary Clinton to Democratic losses in the midterm elections, tweeting with the hashtag “HILLARYSLOSERS” as an opening shot in the 2016 presidential contest

- New York City said it is monitoring 357 individuals for symptoms of Ebola; most are people who arrived in the city from Ebola-affected countries

- Phil Rudd, drummer for AC/DC, has been charged in New Zealand with attempting to procure a murder; Rudd appeared in Tauranga District Court today on the charge and has been bailed until his next appearance on Nov. 27, a court official said

- Sovereign yields mostly lower. Nikkei -0.9%, Shanghai +0.3%. European stocks, U.S. equity-index futures fall. Brent crude and copper lower, gold slides 0.4%

FIXED INCOME & EQUITIES

European equities started the session off on a cautious note, as participants sit on the side-lines ahead of the widely anticipated ECB meeting, with a mixed batch of German earnings failing to provide the DAX with any further direction. This morning saw a host of earnings reports which have dictated the state of play in stock-specific moves, with UK supermarket Morrisons (+8.6%) helping to boost the UK retail sector and German sports maker Adidas (+4.5%) helping provide the DAX with some support as they look to target their troubled Russian and golf units. Elsewhere, fixed income markets remain relatively unmoved despite the modest softness in stocks, with volumes particularly thin ahead of ECB Draghi’s press conference. Nonetheless, Spanish paper was provided some reprieve following a strong triple-tranche auction with all b/c higher than previous and average yields lower than previous. However, the French Tresor failed to endure the same fate as their offering was poorly received by the market and sent their benchmark 10yr lower by 45 ticks.

FX

FX markets have been the main source of focus given the overnight movements in the USD-index. More specifically, JPY initially came under significant selling pressure with USD/JPY breaking above 115.00 for the first time since December 2007, while EUR/JPY surged to a 10-month high and GBP/JPY traded at October 2008 levels. However, the JPY sell-off was then abruptly unwound as major JPY crosses dropped over 1 point across the board to trade relatively flat, attributed to widening spreads and a paucity of orders. Elsewhere, AUD saw some whipsaw price action overnight following the Australian jobs report, as the better than Exp. job gains figure was shrugged off as participants focused on the unemployment rate; highest since September 2002. Furthermore, the RUB sits at record lows against the USD once again after the Russian central bank altered their intervention policy yesterday.

COMMODITIES

Elsewhere, commodity markets remain relatively subdued with precious metals markets largely tracking movements in the USD-index which has since recovered some of its overnight losses. In a similar vein, the energy complex resides in relatively neutral territory as participants now look ahead to the stream of upcoming risk events which include the BoE and ECB rate decisions, the weekly US jobs report and the EIA natural gas storage change figure. In energy specific news, the WSJ writes that the US ban on oil exports is showing signs of easing with BHP Billiton due to sell around USD 50mln of ultralight oil from Texas to foreign buyers without formal government approval.

* * *

DB’s Jim Reid concludes the overnight recap

Today is the most important day since…. well the last important day as the ECB hosts its widely anticipated monthly meeting. Whilst not many expect concrete action, the success will be judged on how much Draghi hints at much more future action whilst actually probably doing nothing. Between June and September the ECB seemed like it was catching up with the curve that many feel it is behind. However last month’s press conference saw many disappointed at Draghi with the feeling he was back-tracking on prior dovishness. Indeed many feel his performance last month contributed to the large falls in markets over the following week so the stakes are fairly high.

There really isn’t much to go on for today with no real concrete leaks in the press. However the past few weeks have seen a series of news articles coming out hinting at what might be on the minds on the ECB. First we had a Reuters report a couple of weeks back suggesting that the ECB is considering purchasing corporate bonds. This helped with the snapback in markets reinforcing the claim that the stakes are high and that markets are still heavily controlled by central bank actions. Then on Tuesday Reuters again influenced the market by highlighting internal problems the ECB is grappling with when it reported on dissent within the council as to the next steps for European monetary policy. As a reminder it suggested that, “At least seven and possibly as many as 10 of the 24 council members are against U.S.-style quantitative easing.” The article pointed to deep disharmony and there are bound to be questions about it today in the Q&A.

With so much in play, our European economists wrote in last week’s Focus Europe that, “Merely repeating the line that the Council remains unanimous in its commitment to other unconventional policies if necessary — that is, no escalation of rhetoric — would disappoint the market.? In terms of what might actually be mentioned today, our economists expect that, ‚at best … Draghi could only endorse corporate bond QE implicitly. He could re-introduce the phrase that the Council is ready to adjust the ‚size and composition? of asset purchases.?? In terms of public QE, they expect that, ‚Rather than acting early to maximize the impact of QE by surprising the market, we see the ECB delaying action to secure a broad enough consensus inside and outside the Council. As time passes, growth and inflation expectations should fall and market stress may rise … we expect public QE, but probably not until later in Q1.? Looking ahead one of their comments in particular stuck out from Focus Europe in light of this week’s Reuters ECB headlines – ‚In a perverse way, we need more stress to trigger a response.? So a difficult meeting today for Mr Draghi, especially if the Reuters story this week is to be believed.

European markets did have a strong day yesterday, helped by the previous day’s US market strength and then helped by stronger than expected Services PMI’s from Spain (55.9 vs 55.3 expected), Italy (50.8 vs 49.4 expected) and France (48.3 vs 48.1 expected) although the slightly disappointing German number (54.4 vs 54.8 expected) meant that the broader eurozone read came in at around expectations (52.3 vs 54.4 expected). The eurozone composite PMI also came in broadly in-line with expectation at 52.1. Over this side of the Channel, the UK Services and Composite PMI’s both disappointed at 56.2 and 55.8 respectively. In terms of market moves – the Stoxx 600 closed the day up +1.6%, led by the FTSE MIB (up +2.6%) and the CAC (up +1.9%). In credit, Main tightened by -1bp whilst Xover fell -10bps. In other European news yesterday Jean-Claude Juncker, the new President of the European Commission, held his first press conference where he announced that the Commission would be presenting proposals for a €300bn investment package to stimulate EU economy’s growth in December, three months earlier than expected, although few other details emerged.

Over in the US, data was mixed with a stronger than expected October ADP employment report (at +230k vs 220k expected) and a +12k upward revision to the previous read, an in-line US Services PMI (at 57.1) and a disappointing October non-manufacturing ISM of 57.1 (vs 58 expected). Diving into some of the details of the ISM, given we have payrolls on Friday, it was interesting to see how strong the ISM non-manufacturing employment sub component series was (rising to 59.6 from 58.5, its highest level since August 2005). Given this, as DB’s Chief US Economist Joe LaVorgna wrote in his comment yesterday, “employment subcomponent of the non-manufacturing ISM survey is loosely correlated with nonfarm payrolls.” So it seems fair to say that yesterday’s strong ADP and ISM employment series data have increased expectations for tomorrow’s NFP number. Joe is expecting a 225k print.

Staying on the US, the midterm elections went largely as expected with the Republicans gaining control of the Senate. Markets reacted positively, the S&P closing +0.6% with the view being that the newly elected Congress would implement something of a business friendly agenda including looser constraints on banks, plans to liberalize energy exports and support over new trade deals. Treasuries were modestly weaker whilst the Dollar continues to surge on with the DXY index +0.5% on the day to 87.44, the highest level since June 2010.

Looking at markets elsewhere, the Central Bank of Russia yesterday announced that they would allow for an effective free float of the rouble. The currency has depreciated significantly recently, losing more than a quarter of its value versus the dollar over the calendar year. The bank have stated that the currency will be determined ‘predominantly by market factors’ although will be subject to one-off interventions if needed.

Meanwhile oil rebounded yesterday as WTI and Brent rallied +1.3% and +0.5%. Sentiment turned around following the latest inventory data showing that stockpiles increased by less than expected last week which was further compounded with a reduction in Libyan output. Markets had also jumped earlier in the day following a report in the Wall Street Journal that news was circulating on Twitter that a pipeline had exploded in Saudi Arabia, with worries over possible terrorism, although the report was later thought not to be credible.

Taking a look at Asian markets this morning the Nikkei has been particularly volatile, trading up as much 0.5% to pare back all those gains and trade -0.8% at time of writing. The Yen has reflected this move to trade up against the Dollar having previously hit a seven year low. Elsewhere markets are weaker with bourses in Hong Kong, China and Australia modestly down, the latter reported labour data relatively in line with expectations. Quickly looking at the micro, Bank of China’s debut Basel-III compliant US Dollar deal has closed with the $3bn bond deal attracting $18bn of orders for the 10-year maturity notes.

Finally there was an interesting article in the FT yesterday reporting that China has proposed lifting some sanctions on foreign investment in the country. The plan is to reduce the number of sectors foreign companies are required to form JV’s with domestic businesses or are limited to minority stakes from 79 to 35 and in effect open up state-owned enterprises to private capital.

In terms of the day ahead and aside from the focus on the ECB today we’ve got factory orders in Germany to look forward to as well as retail PMI prints in Europe and the September industrial production print in the UK. This will then be followed up with the latest Bank of England monetary policy meeting although we expect little in the way of changes. Following up on yesterdays ADP reading we’ve got claims data in the US which our US team are anticipating to be similarly supportive of a healthy job market. Finally the Fed’s Evans will be speaking publically in Chicago so we will be keeping an eye for any interesting remarks to come out of that.

end

Late Wednesday evening/Early Thursday morning: USA/Yen crosses 115 barrier!!

(courtesy zero hedge)

USDJPY Breaks 115 (+7 Handles In 7 Days), Decouples From Less Exuberant Stock Market

Japanese bond yields have crept slowly higher since the big flush on Monday and Nikkei 225 is 2.6% below its highs on Monday seemingly pinned at 17,000. We note this as Abe & Kuroda’s currency collapses yet another big figure to 115.00 (up 7 handles in 7 days from pre-FOMC) – the highest in over 7 years. The crucial 120 line in the sand should be crossed early next week at this rate… What was the trigger for tonight’s exuberance, we hear you ask, why the Japanese market opening – which sent USDJPY instantly up 40 pips.

JGB yields creeping higher…

As USDJPY loses its beta to stocks…

No mo momo…

If at first you don’t succeed…

And smash Gold for good measure

Charts: Bloomberg

end

Then the following happened late in trading in Japan:

(courtesy zero hedge)

A Snapshot Of Last Night’s Yen And Nikkei Flash Crash

Submitted by Tyler Durden on 11/06/2014 06:38 -0500

Late last night, everything was going great, or horribly wrong depending on whether one still has some frontal lobe neurons left after years of indoctrination at Keynes U, and the USDJPY was soaring, levitating slowly at first then surging and touching 115.50, just 450 pips from the USDJPY 120 “pure insanity” level, when everything went wrong.

This is the blow-by-blow thanks to Bloomberg:

- At 12:50pm Tokyo time, Nikkei 225 Index was sitting pretty, up 0.5% for the day. Then came the tumble.

- Over the next 22 minutes, Nikkei Index lost 1.8% to touch intraday low of 16,725.45

- USD/JPY followed suit, but with a lag, based on data compiled by Bloomberg; currency slid from 115.38 to 114.46 during that period, marking 0.8% drop

- Japanese banks sold down Nikkei to take some money off the table, given its 8% advance since Oct. 31 when BOJ announced its latest easing, which in turn caused USD/JPY to retreat, according to a Tokyo-based FX sales trader

- Nikkei 225 closed down 0.9%, reversing earlier gain of as much as 0.6%

And the chart which quite visibly shows that Japan is now a cardiac-arrest patient in terminal V-Fib.

At least the country which one year ago brought daily flash crashes – and halts – of its entire bond market, is keeping it interesting, and now algos have to wonder just when the next fake market flash crash will tumble, and wipe everyone out, when the upward left of the V-shaped recovery refuses to appear.

But perhaps the one thing that guarantees Japan’s economic death was this, from Bloomberg: Economist Paul Krugman met Japanese Prime Minister Shinzo Abe this morning and said he was worried a further increase in sales tax planned for next Oct. could cause Abenomics to fail, Abe aide Etsuro Honda said. Krugman did not specify how long the delay should be, saying he was concerned increasing the tax as scheduled could mean Abenomics fails. Abe did not give his own view on the tax.

Sorry Paul, Abenomics already failed: here is a chart of Japan’s nominal and real wages – for ordinary Japanese consumers it is just a matter of when not if they panic.Per Goldman: “Real wages (nominal wages less the CPI inflation) registered a large decline of 2.9% yoy, after falling 3.1% in August. Summer consumer spending was sluggish in spite of the largest rise in summer bonuses since 1991, even considering the impact of the consumption tax hike and bad weather. Despite high one-time bonus payments, the continuous decline in real wages, especially the much lower pace of increase in basic wages (which is considered permanent income) relative to inflation rate, is restricting consumer behavior.”

The only good news: Japan has now moved into the Krugmanesque twilight zone, where the only remedy to failure will be doing more of what caused the failure in the first place, thus mercifully accelerating Japan’s implosion into the Keynesian abyss.

end

Early this morning:

ECB Keeps Rates Unchanged

Submitted by Tyler Durden on 11/06/2014 07:48 -0500

While today’s Draghi press conference is expected to be rather contentious, nobody was expecting much if anything from the actual quantitative rates announcement. Sure enough, that’s precisely what the ECB delivered when moments ago it announced it would keep all three rates unchanged, with the Deposit Facility rate continuing its trek through NIRP land at -0.20%.

At today’s meeting the Governing Council of the ECB decided that the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.05%, 0.30% and -0.20% respectively.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 2.30 p.m. CET today.

Next up: the press conference in 45 minutes.

end

The message from Draghi this morning is to expect an expansion on the ECB’s balance sheet (good luck to that)..stocks ramp higher

(courtesy zero hedge)

Stocks Spike, Euro Tumbles As Draghi Jawbones Risk Higher Again

“The main message is ECB assets are set to expand as others contract,” promises ECB’s Mario Draghi, adding that “ABS buying is to begin shortly.” Shrugging off any rumors of mutiny or lack of sovereign QE, the markets bought every stock market and risky bond with both hands and feet. EURUSD plunged under 1.24 – its lowest since August 2012 as peripheral bond spreads tumbled 10-15bps. US Treasury yields pushed higher and stocks knee-jerked higher. The USD index is now up 1% on the week.

The shine is coming off as reality hits

- *DRAGHI SAYS ECB WON’T BUY EU1 TRLN

EUR tumbles sending bond yields and stocks higher… for now

and plunging peripheral bond spreads…

and this is what happened to gold…

Charts: Bloomberg

end

A very important commentary written last night by Ambrose Evans Pritchard. He states that Germany does not want QE and is looking at ways to exit the EMU.

Today we had 100% ECB support for asset backed purchases and to expand the ECB balance sheet..maybe by 1 trillion euros.

here is Ambrose Evans Pritchard’s paper written before the ECB announcement of 100% unanimous support for ECB balance sheet expansion..

(courtesy Ambrose Evans Pritchard/UKTelegraph)

Mario Draghi’s efforts to save EMU have hit the Berlin Wall

If the ECB tries to press ahead with QE, Germany’s central bank chief will resign. If it does not do so, the eurozone will remain stuck in a lowflation trap and Mario Draghi will resign

9:22PM GMT 05 Nov 2014

Mario Draghi has finally overplayed his hand. He tried to bounce the European Central Bank into €1 trillion of stimulus without the acquiescence of Europe’s creditor bloc or the political assent of Germany.

The counter-attack is in full swing. The Frankfurter Allgemeine talks of a “palace coup”, the German boulevard press of a “Putsch”. I write before knowing the outcome of the ECB’s pre-meeting dinner on Wednesday night, but a blizzard of leaks points to an ugly showdown between Mr Draghi and Bundesbank chief Jens Weidmann.

They are at daggers drawn. Mr Draghi is accused of withholding key documents from the ECB’s two German members, lest they use them in their guerrilla campaign to head off quantitative easing. This includes Sabine Lautenschlager, Germany’s enforcer on the six-man executive board, and an open foe of QE.

The chemistry is unrecognisable from July 2012, when Mr Draghi was working hand-in-glove with Ms Lautenschlager’s predecessor, Jorg Asmussen, an Italian speaker and Left-leaning Social Democrat. Together they cooked up the “do-whatever-it-takes” rescue plan for Italy and Spain (OMT). That is why it worked.

We now learn from a Reuters report that Mr Draghi defied an explicit order from the governing council when he seemingly promised to boost the ECB’s balance sheet by €1 trillion. He also jumped the gun with a speech in Jackson Hole, giving the very strong impression that the ECB was alarmed by the collapse of the so-called five-year/five-year swap rate and would therefore respond with overpowering force. He had no clearance for this.

The governors of all northern and central EMU states – except Finland and Belgium – lean towards the Bundesbank view, foolishly in my view but that is irrelevant. The North-South split is out in the open, and it reflects the raw conflict of interest between the two halves.

The North is competitive. The South is 20pc overvalued, caught in a debt-deflation vice. Data from the IMF show that Germany’s net foreign credit position (NIIP) has risen from 34pc to 48pc of GDP since 2009, Holland’s from 17pc to 46pc. The net debtors are sinking into deeper trouble, France from -9pc to -17pc, Italy from -27pc to -30pc and Spain from -94pc to -98pc. Claims that Spain is safely out of the woods ignore this festering problem.

David Marsh, author of a book on the Bundesbank and now chairman of the Official Monetary and Financial Institutions Forum, says the Bundesbank has been quietly seeking legal advice on whether it can block full-scale QE. It is looking at Articles 10.3 and 32 of the ECB statutes, arguably relevant given the scale of liabilities.

The let-out clauses would make QE the sole decision of the 18 national governors – shutting out Mr Draghi – based on the shareholder weightings. Germany would have 26pc of the votes, easily enough to mount a one-third blocking minority. Mr Draghi would not even have a say.

Mr Marsh said this has echoes of the “Emminger Letter” invoked in September 1992 to justify the Bundesbank’s refusal to uphold its obligation to defend the Italian lira in the Exchange Rate Mechanism. The lira crashed. The Italians were stunned. One of them was the director of the Italian Treasury, a young Mario Draghi.

Lena Komileva, from G+ Economics, says the ECB is heading for a crisis of legitimacy whatever happens. If the bank tries to press ahead with a QE-blitz, Mr Weidmann will resign. If it does not do so, the eurozone will remain stuck in a lowflation trap and the ECB will go the way of the Bank of Japan in the late 1990s, in which case Mr Draghi will resign.

Mr Draghi’s balance sheet pledge was muddled and oversold from the start. Much of it was predicated on banks taking out super-cheap loans (TLTROs) from the ECB, but they have so far spurned it. You cannot make a horse drink. These loans are not the same as QE money creation in any case. They are an exchange for collateral.

The asset purchases are what matter and the package announced so far is modest, bordering on trivial. It is unlikely to exceed €10bn a month as currently designed. The “buyable” market for covered bonds and asset-backed securities is too small to move the macro-economic dial. If the ECB wanted to match the Bank of Japan in its latest effort to drive down the yen and export deflation, it would have to launch €130bn of asset purchases every month (1.4pc of GDP).

Hawks claim that QE would make no difference because interest rates are already near zero, and the German 10-year Bund is already the lowest in history. This is eyewash. Central banks can print money to buy gold, land, oil for strategic reserves (why not?) or Charollais cattle. Or they can print to build roads or windmills. They can hand the money out as cash envelopes. If they did this, even the dimmest wits would see that QE is a monetary device and can always defeat deflation as a mathematical principle. It does not have to work through interest rates, nor should it.

The ECB’s North-South clash mirrors the political breakdown of monetary union after six years of depression and mass unemployment. France’s Front National now has twice as many Euro-MPs as the ruling Socialists. Euro defenders invariably insist that the triumph of Marine Le Pen – currently leading presidential polls at 30pc – has nothing to do with her pledge to restore the franc and take back French economic sovereignty.

Whether or not this is true – and that smacks of presumption – she is snatching enough votes from the Socialists to threaten their survival as a political movement. If they let perma-slump drift on until 2017, they will meet the fate of Greece’s PASOK, and deserve it.

Italy is also edging closer to an inflexion point. The Five Star movement of Beppe Grillo – which won a quarter of the vote in 2013 – has grasped the elemental point that zero inflation and falling nominal GDP is pushing Italy into a debt-compound trap. For a long time Mr Grillo wrestled with the EMU issue. There is no longer any doubt. “We must leave the euro as soon as possible,” he says.

Spain’s insurgent Podemos party has come from nowhere to top the polls at 28pc. It is not anti-euro. Its wrath is directed against a corrupt “Casta”. Yet the party’s reflation drive and furious critique of Spain’s “internal devaluation” is entirely at odds with EMU imperatives, as is its €145bn plan for a universal basic income, which would lift Spain’s fiscal deficit to 20pc of GDP. Podemos reminds one of France’s Front Populaire in 1936. Leon Blum did not perhaps intend to leave the Gold Standard, but he knew his policies would bring it about in short order.

Mr Draghi is of course right to force the issue. The ECB is missing its 2pc inflation target by a mile, with crippling effects on the crisis states. This itself is a violation of the ECB’s legal mandate. The refusal of the German-led hawks to do anything serious about this is indefensible, and remarkably stupid unless their intention is to break up EMU, a possibility one can no longer exclude.

The European Commission’s Autumn forecast this week is a cri de coeur. It warns of a “snowball effect” as deflationary forces causes debt trajectories to accelerate upwards by mechanical effect.

Brussels admits that something has gone horribly wrong, obliquely blaming stagnation on the “policy response to the crisis”. It halved the growth estimate for France to 0.7pc next year, and for Italy to 0.6pc, a ritual with each report.

It says the eurozone faces a “home-grown” malaise, left behind as the US and Britain pull away. “It is becoming harder to see the dent in recovery as the result of temporary factors only. Trend growth has fallen even lower due to low investment and higher structural unemployment,” it said. Now they tell us.

The collapse of investment is not some form of witchcraft. It is entirely due to the folly of deep cuts in public investment – pushed by the Commission itself – at a time of private sector deleveraging, all made much worse by monetary paralysis. Italy’s rate of investment fell by 7.4pc in 2012 and 5.4pc in 2013. Even Germany’s fell 0.7pc in each year.

Tucked away in the report is a nugget that Britain alone accounted for almost all the EU’s growth in 2013, half in 2014, and will still be the biggest contributor by far in 2015. This implies that the UK’s net payments to the EU budget – already up fourfold since 2008 – will become ever more skewed. Or put another way, the more EMU makes a mess of its affairs, the more Britain must pay to prop it up.

Europe’s leaders and officials have run monetary union into the ground. Mr Draghi has bravely tried to bring them to their senses and contain the damage. He seems to have hit the limits of European power politics.

There is another job waiting for him in Rome as Italian president, should he wish to take it. The offer must be tempting, if only for sweet revenge.

His departure would shatter market confidence in the euro overnight. He could then lead his country to recovery, with a correctly-valued lira, and inflict a massive trade shock on his tormentors in the North for good measure.

Rioters clashed with police after it was revealed that Brussels embezzled huge amount of funds after an audit was completed:

(courtesy zero hedge)

While Brussels Burns In “Anti-Austerity” Riots, Here Is The Real Reason For Europe’s Depression

Riot police clashed with demonstrators in the Belgian capital of Brussels on Thursday amid a massive protest against government plans to reform the country’s welfare system. This comes on the heels of violent French, Italian, and Spanish youth protests in recent weeks as the citizens of the non-Germanic European Union decry the ‘austerity’ they have been crushed by. What is odd, though, is externally, there has been ‘no’ austerity with debt loads rising for all these nations and debt/GDP at record highs for most. So where is the disconnect between a people under increasing financial pressure and a sovereign issuing more and more debt at will? The Telegraph has the stunning answer: an audit, published this morning, found that £109 billion out of a total of £117 billion spent by the EU in 2013 was “affected by material error”. Brussels accounts have not been given the all clear for 19 years running. In other words, Brussels ’embezzles’ billions of euros per year, and blames it on austerity. Is it any wonder, Europe is burning?

This is what happens… More than 100,000 marched through Brussels today…

And it turned ugly…

http://www.liveleak.com/ll_embed?f=56430cb47336

When your leaders steal… (as The Telegraph reports)

According to the annual report of the European Court of Auditors, seen by The Telegraph,£5.5 billion of the EU budget last year was misspent because of controls on spending that were deemed to be only “partially effective” by experts.

The audit, published this morning, found that£109 billion out of a total of £117 billion spent by the EU in 2013 was “affected by material error”.

It means that the Brussels accounts have not been given the all clear for 19 years running.

Treasury sources said that the disclosure shows why the EU needs “urgent reform”.

…

“More can and should be done to ensure money is spent according to rules,” it said.

Among the examples of misspent money was funding used to buy helicopters to help Spain defend Europe’s borders against entry by illegal immigrants.

“[Auditors] examined a project in Spain which consisted of the purchase of four helicopters, to be used 75 per cent of their operating time for EU border surveillance and control. However, the ECA found the helicopters were only used 25 per cent of the time for this purpose,” said the report.

In another case, the commission handed out £1.4 million in funding for social development in Moldova “for which no underlying expenditure had been incurred”.

…

“Far too much of the EU budget continues to be spent on poor quality projects with poor oversight. This is not only wasteful but undermines consent for the whole EU project,” said Christopher Howarth, an analyst at the think-tank.

“The EU should radically reform its budget to focus only on those areas where the EU adds value.”

* * *

The bottom line is that Europe’s citizens are being cheated of the benefits of ultra-low interest rates repressed by the ECB that enables their inglorious leaders to issue debt at will and increase the nation’s burdens, by a bureaucratic layer of embezzlement that has been going on – in size – for decades.

end

Vladimir Putin will not be happy with this next move:

“Most Powerful Man In The World”‘s Inner Circle Probed By US Regulators For Money Laundering

Being 2 for 2 in losses this week (The US Election andTime’s “world’s most powerful person), it appears President Obama has fallen back on his regulatory army to take the fight to Vladimir Putin. As WSJ reports, U.S. prosecutors have launched a money-laundering investigation of billionaire Gennady Timchenko – a member of Putin’s inner circle. The allegations are that Timchenko (who was among the first Russian businessmen to be sanctioned by the U.S. following Russia’s intervention in Ukraine’s Crimea region)transferred funds linked to allegedly corrupt deals in Russia through the U.S. financial system. The probe is also examining whether any of Mr. Putin’s personal wealth is connected to allegedly illicit funds.