Here are the following closes for gold and silver today:

Gold: $1185.90 down $1.30 (comex closing time)

Silver $16.63 down 10 cents (comex closing time)

In the access market 5:15 pm

Gold $1187.80

Silver: $16.67

Gold/Silver trading: see kitco charts on the right side of the commentary

Following is a brief outline on gold and silver comex figures for today:

At the gold comex today, we had a poor delivery day, registering 1 notices serviced for 100 oz. Silver comex filed with 66 notices for 330,000 oz

Several months ago the comex had 303 tonnes of total gold. Today, the total inventory rests at 243.89 tonnes for a loss of 59 tonnes over that period.

In silver, the open interest rose by 298 contracts as Tuesday’s silver price was down by 30 cents. The total silver OI continues to remain extremely high with today’s reading at 173,629 contracts maintaining itself near multi-year highs despite a record low price. This dichotomy has been happening now for quite a while and defies logic. There is no doubt that the silver situation is scaring our bankers to no end.

In silver we had 66 notices served upon for 330,000 oz.

In gold, the total comex gold OI rests tonight at 411,961 for a loss of 2,921 contracts as gold was down $17.10 yesterday. We had 1 notice served upon for 100 oz. Whenever we approach first day notice, the entire open interest for the gold or silver complex collapses.

Today, we had no changes in inventory at the GLD, thus the inventory rests tonight at 715.86 tonnes. The appetite for gold coming from China is depleting not only gold from the LBMA and GLD but also the comex is bleeding gold.

In silver, /we had a huge withdrawal of 1.003 million oz of silver inventory at the SLV/Inventory rests at 316.927 million oz

We have a few important stories to bring to your attention today…

1. Today we had the open interest in silver rise by 298 contracts despite the fact that silver was down in price by 30 cents yesterday. The OI for gold fell by 2921 contracts down to 411,961 contracts as the price of gold was down by $17.10 yesterday. We continually witness open interest contraction once first day notice approaches on an active precious metals contract. In gold we have two days left before first day notice and surprisingly we have over 89,000 contracts remaining as open interest. This is totally unbelievable for two days to go.

(report Harvey)

2,Today we had 2 major commentaries on Greece

(zero hedge/David Stockman )

3. We have another big bankruptcy looming in China, the big bottling company of Coca Cola:

(zero hedge)

Let us now head over to the comex and assess trading over there today.

Here are today’s comex results:

The total gold comex open interest fell by 2921 contracts from 414,882 down to 411,961 as gold was down by $17.10 yesterday (at the comex close). For at least the past 18 months, we have been witnessing a total contraction of open interest in an active precious metals month once we are about to enter first day notice. We are in the active delivery month of May and here the OI fell by 30 contracts falling to 36. We had 0 notices filed upon yesterday. Thus we lost 40 gold contracts or an additional 4,000 oz will not stand for delivery in May. The next big active delivery contract month is June and here the OI fell by 32,688, contracts down to 89,621 which is extremely high for this time in the delivery cycle. June is the second biggest delivery month on the comex gold calendar. First day notice is May 29.2015 so we have 2 trading sessions left. The estimated volume today (which is just comex sales during regular business hours of 8:20 until 1:30 pm est) was good at 344,179. The confirmed volume yesterday (which includes the volume during regular business hours + access market sales the previous day) was good at 346,749 contracts. Today we had 1 notice filed for 100 oz.

And now for the wild silver comex results. Silver OI rose by 298 contracts from 173,331 up to 173,629 as the price of silver was down in price by 30 cents, with respect to Tuesday’s trading. We are into the active delivery month of May where the OI fell by 36 contracts and thus falling to 218. We had 0 contracts filed upon with respect to yesterday’s trading. So we lost 36 contracts or an additional 180,000 oz will not stand for delivery in this active May month. The estimated volume today was good at 37,646 contracts (just comex sales during regular business hours. The confirmed volume on yesterday (regular plus access market) came in at 52,046 contracts which is fair in volume. We had 66 notices filed for 330,000 oz today.

May initial standings

May 27.2015

| Gold |

Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 101.85 oz (HSBC |

| Deposits to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | 2500.000 oz ???HSBC, |

| No of oz served (contracts) today | 1 contracts (100 oz) |

| No of oz to be served (notices) | 76 contracts(7600) oz |

| Total monthly oz gold served (contracts) so far this month | 16 contracts(1600 oz) |

| Total accumulative withdrawals of gold from the Dealers inventory this month | 164,151.8 oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 53,156.2 oz |

Today, we had 0 dealer transactions

total Dealer withdrawals: nil oz

we had 0 dealer deposit

total dealer deposit: nil oz

we had 0 customer withdrawals

total customer withdrawal: nil oz

We had 1 customer deposits:

i) Into HSBC: 2,500.000 oz ???? (not divisible by 32.15)

Total customer deposit: 2500.00 oz

We had 0 adjustments.

Today, 0 notices was issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 1 contract of which 0 notices were stopped (received) by JPMorgan dealer and 0 notices were stopped (received) by JPMorgan customer account

To calculate the total number of gold ounces standing for the May contract month, we take the total number of notices filed so far for the month (16) x 100 oz or 1600 oz , to which we add the difference between the open interest for the front month of May (36) and the number of notice served upon today (1) x 100 oz equals the number of ounces standing.

Thus the initial standings for gold for the May contract month:

No of notices served so far (16) x 100 oz or ounces + {OI for the front month (36) – the number of notices served upon today (1) x 100 oz which equals 5100 oz standing so far in this month of May. (.2830 tonnes of gold)

we lost 4,000 oz of gold standing in this May delivery month.

Total dealer inventory: 372,630.992.022 or 11.59 tonnes

Total gold inventory (dealer and customer) = 7,841,215.16 (243.89) tonnes)

Several months ago the comex had 303 tonnes of total gold. Today the total inventory rests at 243.89 tonnes for a loss of 59 tonnes over that period. Lately the removals have been rising!

end

And now for silver

May silver initial standings

May 27 2015:

| Silver |

Ounces |

| Withdrawals from Dealers Inventory | 130,239.75 oz (CNT,Delaware) |

| Withdrawals from Customer Inventory | nil |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 94,733.98 oz (HSBC) |

| No of oz served (contracts) | 66 contracts (330,000 oz) |

| No of oz to be served (notices) | 152 contracts (760,000 oz) |

| Total monthly oz silver served (contracts) | 2769 contracts (13,845,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | 126,359.680 oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 3,984,024.8 oz |

Today, we had 0 deposits into the dealer account:

total dealer deposit: nil oz

we had 0 dealer withdrawal:

total dealer withdrawal: nil oz

We had 1 customer deposits:

i) Into CNT: 94,733.98 oz

total customer deposit: 94,733.98 oz

We had 2 customer withdrawals:

i) Out of CNT: 126,303.95 oz

ii) Out of Delaware; 3935.80 oz

total withdrawals from customer; 130,239.75 oz oz

we had 1 adjustment

i) Out of CNT:

we had one adjustment whereby 4902.200 oz was adjusted out of the customer of CNT into the dealer account of CNT

Total dealer inventory: 60.854 million oz

Total of all silver inventory (dealer and customer) 178.743 million oz

The total number of notices filed today is represented by 66 contracts for 330,000 oz. To calculate the number of silver ounces that will stand for delivery in May, we take the total number of notices filed for the month so far at (2769) x 5,000 oz = 13,845,000 oz to which we add the difference between the open interest for the front month of April (218) and the number of notices served upon today (66) x 5000 oz equals the number of ounces standing.

Thus the initial standings for silver for the May contract month:

2769 (notices served so far) + { OI for front month of April (218) -number of notices served upon today (66} x 5000 oz = 14,605,000 oz of silver standing for the May contract month.

We lost 36 contracts or 180,000 additional ounces will not stand for delivery in this active May contract month.

for those wishing to see the rest of data today see:

http://www.harveyorgan.wordpress.com orhttp://www.harveyorganblog.com

end

The two ETF’s that I follow are the GLD and SLV. You must be very careful in trading these vehicles as these funds do not have any beneficial gold or silver behind them. They probably have only paper claims and when the dust settles, on a collapse, there will be countless class action lawsuits trying to recover your lost investment.

There is now evidence that the GLD and SLV are paper settling on the comex.

***I do not think that the GLD will head to zero as we still have some GLD shareholders who think that gold is the right vehicle to be in even though they do not understand the difference between paper gold and physical gold. I can visualize demand coming to the buyers side:

i) demand from paper gold shareholders

ii) demand from the bankers who then redeem for gold to send this gold onto China

vs no sellers of GLD paper.

And now the Gold inventory at the GLD:

may 27: no changes in gold inventory at the GLD/Inventory rests at 715.86 tonnes

may 26.2015/we had a slight addition of .600 tonnes of gold to the GLD inventory/inventory rests at 715.86 tonnes

May 22.2015: no changes in gold inventory at the GLD/Inventory rests at 715.26 tonnes

May 21./no changes in gold inventory at the GLD/Inventory rests at 715.26 tonnes

May 20./we had another withdrawal of 2.98 tonnes of gold leaving the GLD. Inventory rests tonight at 715.26 tonnes

May 19/no changes in gold inventory at the GLD/Inventory at 718.24 tonnes

May 18/we lost another 5.67 tonnes of gold inventory at the GLD/Inventory rests at 718.24 tonnes

May 15./no change in gold inventory at the GLD/Inventory rests at 723.91 tonnes

May 14./ a huge withdrawal of 4.41 tonnes of gold/Inventory rests at 723.91 tonnes

May 13.2015: no change in inventory at the GLD/Inventory rests at 728.32 tonnes

May 12/no change in inventory at the GLD/inventory rests at 728.32 tonnes

May 11/ no changes at the GLD/Inventory rests at 728.32 tonnes

May 8/ they should call in the Serious Fraud squad as the owners of the GLD just saw 13.43 tonnes of gold leave its vaults heading for China:

Inventory : 728.32 tonnes

May 27 GLD : 715.86 tonnes.

end

And now for silver (SLV)

May 27/we had another 1.003 million oz withdrawn from the SLV/Inventory rests tonight at 316.927 million oz

May 26.2015: no change in SLV /Inventory rests at 317.93 million oz

May 22.2015: no changes in SLV/Inventory rests at 317.93 million oz

May 21.no changes at the SLV/Inventory rests at 317.93 million oz

May 20/no changes at the SLV. Inventory rests at 317.93 million oz/

May 19.2015: we lost another 1.195 million oz of inventory at the SLV/Inventory rests at 317.93 million oz/

May 18.2015: we lost another 1.625 million oz of inventory at the SLV/Inventory rests tonight at 719.125 million oz

May 15./no change in silver inventory at the SLV/inventory rests tonight at 320.75 million oz

May 14/ a huge withdrawal of 1.912 million oz from the SLV/Inventory at 320.75 million oz.

May 13.2015: no changes at the SLV/Inventory rests at 322.662 million oz

May 12/no changes at the SLV/Inventory rests at 322.662 million oz

May 11/no changes at the SLV/Inventory rest at 322.662 million oz

May 8/ today we lost a huge 2.87 million oz of silver from the SLV/Inventory 322.662

May 7/no change in silver inventory/325.53 million oz

May 6/we had a huge withdrawal of 2.143 million oz of silver from the SLV/325.53 million oz

May 5/no change in silver inventory at the SLV/327.673 million oz

May 27/2015 no change in inventory/SLV inventory 316.927 million oz/

end

And now for our premiums to NAV for the funds I follow:

Note: Sprott silver fund now for the first time into the negative to NAV

Sprott and Central Fund of Canada.

(both of these funds have 100% physical metal behind them and unencumbered and I can vouch for that)

1. Central Fund of Canada: traded at Negative 8.0% percent to NAV in usa funds and Negative 8.2% to NAV for Cdn funds!!!!!!!

Percentage of fund in gold 60.8%

Percentage of fund in silver:38.8%

cash .4%

( May 27/2015)

2. Sprott silver fund (PSLV): Premium to NAV falls to-0.49%!!!!! NAV (May 27/2015)

3. Sprott gold fund (PHYS): premium to NAV rises to -39% to NAV(May 27/2015

Note: Sprott silver trust back into negative territory at -0.49%.

Sprott physical gold trust is back into negative territory at -.39%

Central fund of Canada’s is still in jail.

This morning Sprott formally launches its offer for Central Trust gold and Silver Bullion trust:

SII.CN Sprott formally launches previously announced offers to Central GoldTrust (GTU.UT.CN) and Silver Bullion Trust (SBT.UT.CN) unitholders (C$2.64)

Sprott Asset Management has formally commenced its offers to acquire all of the outstanding units of Central GoldTrust and Silver Bullion Trust, respectively, on a NAV to NAV exchange basis.

Note company announced its intent to make the offer on 23-Apr-15 Based on the NAV per unit of Sprott Physical Gold Trust $9.98 and Central GoldTrust $44.36 on 22-May, a unitholder would receive 4.45 Sprott Physical Gold Trust units for each Central GoldTrust unit tendered in the Offer.

Based on the NAV per unit of Sprott Physical Silver Trust $6.66 and Silver Bullion Trust $10.00 on 22-May, a unitholder would receive 1.50 Sprott Physical Silver Trust units for each Silver Bullion Trust unit tendered in the Offer.

* * * * *

end

Early morning trading from Asia and Europe last night:

Gold and silver trading from Europe overnight/and important physical

stories

(courtesy Mark O’Byrne/Goldcore)

Gold Bullion Is “100% Guarantee from Legal and Political Risks” – Russia

– Gold is a “100% guarantee from legal and political risks”

– Russia’s central bank buys another 300,000 ounces in April

– Russia views its overseas assets as vulnerable

– ‘De-dollarisation’ continues across Asia

– Gold offers protection from growing risks today

Russia’s central bank once again increased its gold holdings substantially in April. They added another 300,000 ounces to their existing stockpile bringing the total up to 40.1 million ounces (see chart below).

It marks the continuation of a policy which was only slightly affected by last year’s rouble crisis following the collapse in the price of oil and Western imposed sanctions.

In an address to Russia’s lower house, a senior policy maker at Russia’s central bank indicated that while gold prices fluctuate they offer invaluable insurance against external factors. Dmitry Tulin, manager of monetary policy said,

“The price of it swings, but on the other hand it is a 100 percent guarantee from legal and political risks.”

Reuters reports that western sanctions “have not targeted government assets abroad” to date and suggest that Russia’s reduction of its exposure to U.S. Treasury bills is a symptom of its fear that state assets will be targeted next.

Of course, Russia’s reducing of its Treasury bill holdings may also be part of the policy of de-dollarisation which Russia and China are energetically pursuing. As may the insatiable appetite of their central banks for gold.

Countries across central Asia continue to buy gold eagerly. The government of Kazakhstan banned the export of mined gold and is stockpiling its reserves – although its current holding of 200 tonnes is dwarfed by those of its Russian and Chinese neighbours.

Gold is absolutely central to monetary policy in Eurasia and Asia. China openly refer to their yuan as “the reserve currency of the world”. While this ambitious slogan may be slightly premature it is likely that by backing the yuan with gold it would become a major reserve currency that would challenge the debt-bloated dollar.

Investors would be wise to take heed of Russia’s attitude to gold as a “100% guarantee”. In the crisis that approaches physical gold held outside the banking system in safe vaults in safe jurisdictions will prove to be such a guarantee to individuals, companies, pension funds, family offices, as well as nations.

Must Read Guide: 7 Key Bullion Storage Must Haves

MARKET UPDATE

Today’s AM LBMA Gold Price was USD 1,187.85, EUR 1,088.07and GBP 770.64 per ounce.

Yesterday’s AM LBMA Gold Price was USD 1,194.00, EUR 1,095.56 and GBP 774.77 per ounce.

Gold fell $19.30 or 1.6 percent yesterday to $1,187.70 an ounce. Silver slipped $0.36 or 2.11 percent to $16.74 an ounce.

Gold in Singapore for immediate delivery was up 0.3 percent at $1,189.65 an ounce while gold in Zurich fell to $1,185.96.

Gold held near a two week high after dipping in the prior session when positive economic data hinted that the U.S. economy may be picking up. The U.S. business investment spending plans increased for its second consecutive month in April and consumer confidence moved upward along with new U.S. home sales that increased last month.

The positive U.S. economic data fuelled the U.S. dollar’s rally which ramped up to an eight year high against the beleaguered Japanese yen.

Greek finance ministers and creditors continue bailout negotiations today. Its payment of 1.6 billion euros is due to the IMF next week and government sources indicate that the nation may not be able to make the payments without a deal.

The ECB kept the cap on emergency liquidity assistance Greek banks can draw from the country’s central bank unchanged at 80.2 billion euros, a banking source told Reuters on Wednesday.

The lack of any solid progress in recent talks has pushed European equities lower yesterday, with the FTSE 100 falling 80 points. Emerging market equities slumped to six-week lows, with sentiment poor due to concerns about the Chinese and indeed the global economy.

In late European trading gold was at $1,186.10 an ounce down 0.19 percent. Silver was at $16.71 an ounce off 0.21 percent, and platinum was at $1,123.90 an ounce down 0.04%,

end

Quite a commentary…

(courtesy Seth Mason/GATA)

Busted metals traders distract from larger manipulation problem

Submitted by cpowell on Wed, 2015-05-27 02:14. Section: Daily Dispatches

10:14p ET Tuesday, May 26, 2015

Dear Friend of GATA and Gold:

Seth Mason, founder of the Solidus Center, a nonprofit organization that aims to highlight the faults of the Federal Reserve, calls attention to the longstanding price-suppressive effect of the U.S. futures markets on gold and silver prices. Mason concludes that the U.S. Commodity Futures Trading Commission has allowed market rigging on a massive scale for many years. Mason’s commentary is headlined “Busted Metals Traders Distract from Larger Manipulation Problem” and it’s posted at GoldSeek here:

http://news.goldseek.com/GoldSeek/1432669015.php

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

end

(courtesy London’s Financial Times/GATA)

China’s currency ‘no longer undervalued,’ IMF says, clearing entry to SDRs

Submitted by cpowell on Wed, 2015-05-27 01:02. Section: Daily Dispatches

By Tom Mitchell and Shawn Donnan

Financial Times, London

Tuesday, May 26, 2015

The International Monetary Fund has declared that China’s currency is “no longer undervalued,” marking a significant shift after more than a decade of criticism of Beijing’s tight management of the renminbi.

The move amounts to a major vote of confidence in Beijing and the renminbi at a critical time. It also puts the IMF at odds with its biggest shareholder, the United States, which insists that China continues to draw an unfair trade advantage from a renminbi that it considers “significantly undervalued.” …

The renminbi has gained 25 per cent against the US dollar since it was allowed to adjust upward within a narrow band a decade ago, and has held its value even as the dollar has strengthened against other major currencies over the past year.

Speaking in Beijing at the end of a regular review of China’s economy, David Lipton, the IMF’s first deputy managing director, said: “While undervaluation of the renminbi was a major factor causing large imbalances in the past, our assessment is that the substantial real effective appreciation over the past year has brought the exchange rate to a level that is no longer undervalued.” …

Eswar Prasad, the former head of the IMF’s China unit, said the shift by the fund was important as it marked the first time since the Asian financial crisis of the late 1990s that the fund had not deemed the renminbi to be undervalued. It also presaged the likely adoption later this year of the renminbi as one of the small number of major currencies in a basket used to determine the value of the IMF’s de-facto currency, the Special Drawing Rights. …

… For the remainder of the report:

http://www.ft.com/intl/cms/s/0/11e96e1e-03a7-11e5-b55e-00144feabdc0.html

end

(courtesy Times of India/GATA)

Gold smuggling in India rises 900% to record

Submitted by cpowell on Wed, 2015-05-27 00:51. Section: Daily Dispatches

Gold Smuggling at All-Time High, Seizures Total Rs 1,000 Crore

By Deeptiman Tiwary

The Times of India, Mumbai

Wednesday, May 27, 2015

NEW DELHI — For the first time in the history of gold smuggling in India, the seizure in illicit trade has crossed the rupees 1,000 crore mark in one financial year with customs, police, and revenue agencies seizing more than 3,500 kilograms of gold in 2014-15.

In 2012-13 the same figure stood at merely Rs 100 crore with just about 350 kilograms of gold seized. In two years, since the government increased duty on gold to 10 percent to rein in a yawning current account deficit, gold smuggling has grown by 900 percent.

Since as an accepted principle seizures could be less than 10 percent of actual smuggling, the figures look even more ominous.

Sources say gold has also begun to be smuggled in unique ways and from rather unexpected corners. …

… For the remainder of the report:

http://timesofindia.indiatimes.com/india/Gold-smuggling-at-all-time-high…

end

(courtesy Reuters/GATA)

Russia acquires gold as defense against ‘political risks,’ central banker explains

Submitted by cpowell on Wed, 2015-05-27 00:35. Section: Daily Dispatches

By Elena Fabrichnaya and Alexander Winning

Reuters

Tuesday, May 26, 2015

Russia is increasing its gold holdings because gold is a reserve asset free from legal and political risks, a senior central banker said on Tuesday.

The comments by Dmitry Tulin, who manages monetary policy at the central bank, reflect Russian fears that the country’s overseas assets could be frozen as part of a possible toughening of Western sanctions over the Ukraine crisis.

“As you know we are increasing our gold holdings, although this comes with market risks,” Tulin told lawmakers in the lower house of parliament. “The price of it swings, but it is a 100-percent guarantee from legal and political risks.” …

… For the remainder of the report:

http://www.reuters.com/article/2015/05/26/russia-cenbank-gold-idUSL5N0YH…

end

(courtesy Mike Ward/Houston Chronicle/GATA)

Texas could create its own Fort Knox to store gold

By Mike Ward

Houston Chronicle

Tuesday, May 26, 2015

http://www.houstonchronicle.com/news/politics/texas/article/Texas-could-…

AUSTIN, Texas — Texas could get its own version of Fort Knox, the impenetrable repository for the nation’s gold bullion, if the Legislature gets its way.

Under House Bill 483, approved unanimously on Tuesday by the state Senate, Comptroller Glenn Hegar would be authorized to establish and administer the state’s first bullion depository at a site not yet determined.

No other state has its own state bullion depository, officials said.

Sen. Lois Kolkhorst, R-Brenham, said the state and its agencies have more than $1 billion worth of gold that now is kept in secure facilities in other states. She said there is concern that fortune should be in Texas.

An official analysis of the bill explains: “The establishment of a Texas Bullion Depository would allow the state, state agencies, and private individuals to store precious metals utilizing a secure Texas-based depository to reduce reliance on out-of-state facilities and to insulate their assets from unstable market forces.”

The new depository would be operated as an office within the comptroller’s agency.

“Would this be like Fort Knox?” asked Sen. Juan Hinojosa, D-McAllen. “If I have gold in my possession, can I deposit it?”

Yes, Kolkhorst said, the new depository would be available for his deposits and those of other Texans, and would save the state money.

“The state has gold, and several years ago (the University of Texas Investment Management Corp.) purchased just under a billion dollars worth of gold,” she said. “Most of the bullion depositories are in New York — there may be a small one in Delaware — and they charge the state a fee to store each bar of gold.”

The United States Bullion Depository, located at Fort Knox in Kentucky, adjacent to a U.S. Army base by the same name, was built in the late 1930s to hold the nation’s gold reserves. Its name has become synonymous with impenetrable security. In addition to holding the country’s gold reserves, Fort Knox has been used as secure storage for vital documents over the years, including the Declaration of Independence and the U.S. Constitution.

Kolkhorst said UTIMCOin March had 5,610 gold bars in its portfolio, an investment worth $645 million, and was being charged a storage fee of $108 per bar by a bullion depository in New York City, a total of more than $605,000 a year.

HB 483 was filed by Rep. Giovanni Capriglione, R-Southlake, the president of a private equity company, and is co-authored by 31 other colleagues. It passed the House 140-1 this month.

“New York will hate this,” Kolkhorst said of the bill that now goes to Gov. Greg Abbott to be signed into law. “To me, that and the fact that it will save Texas money makes it a golden idea.”

end

(courtesy Wall Street Journal/GATA)

LIBOR riggers included Bank of England’s ‘Hammer’ in their e-mail plotting

Bank of England Official Received Emails Relating to Libor Manipulation, Prosecutor Says

By David Enrich

The Wall Street Journal

Wednesday, May 27, 2015

LONDON — A senior Bank of England official received emails that were part of an alleged campaign to rig benchmark interest rates, according to evidence presented in a London trial today.

Martin Mallett, who at the time was the chief currencies dealer at the Bank of England, was among a couple dozen recipients of emails sent in 2007 by brokers allegedly working at the behest of former bank trader Tom Hayes. The recipients were blind carbon-copied on the messages.

In the emails, the brokers sent out daily suggestions for where a variety of banks should set the London interbank offered rate, or Libor. Mukul Chawla, the prosecutor trying Mr. Hayes, said those emails were used in an attempt to skew interest rates for the benefit of Mr. Hayes, at the time a trader in Tokyo at UBS AG.

Mr. Mallett, nicknamed “The Hammer,” was sent the emails at his hammer@bankofengland.co.uk address. …

… For the remainder of the report:

http://www.wsj.com/articles/boe-official-received-emails-relating-to-lib…

end

Zero hedge discusses why Russia is purchasing gold:

(courtesy zero hedge)

Why Russia Is On A Gold Buying Spree

Several years ago, Kyle Bass gave the simplest bull casefor gold:

“Buying gold is just buying a put against the idiocy of the political cycle. It’s That Simple”

And since it is this same political cycle that is doing everything in its power to preserve what little credibility it has, and to avoid its naked idiocy from being revealed for all to see, it has done everything in its power to push the price of gold lower.

However, several entities refuse to be fooled by such “cheap” tricks. One is China, whose ravenous apetite for gold has been extensively discussed previously. The other is the Bank of Russia.

According to central bank data, Russia’s gold reserves rose to 40.1 million troy ounces as of May 1 compared with 39.8 million ounces a month earlier. Russia increased its gold holdings for many months in a row last year, as shown by central bank figures and represented in the chart below.

So why is Russia engaging in this gold-buying spree when it likely has more immediately gratifying ways to spend its reserves?

The answer was given by Dmitry Tulin, who manages monetary policy at the central bank, was as concise, as sensible, and as lucid as that given by Bass. From Reuters:

“As you know we are increasing our gold holdings, although this comes with market risks,” Tulin told lawmakers in the lower house of parliament.

“The price of it (gold) swings, but on the other hand it is a 100 percent guarantee from legal and political risks.”

And with global political risks only set to rise, since under central planning politicans are made obsolete and are thus even more prone to “idiocy”, expect Russian gold buying to continue indefinitely.

end

Steve St Angelo is a pretty good analyst. He has a good grasp on the precious metals. Today he tackles the silver market:

(courtesy Steve St Angelo/SRSRocco report)

Something BIG Is About To Happen To Silver

Yes, that’s correct. Something BIG is about to happen to silver. Now, how this plays out is hard to tell. Recently released new data points to a situation that will force a BIG move in the silver market. In addition, there have been some very interesting movements in the flow of silver bullion.

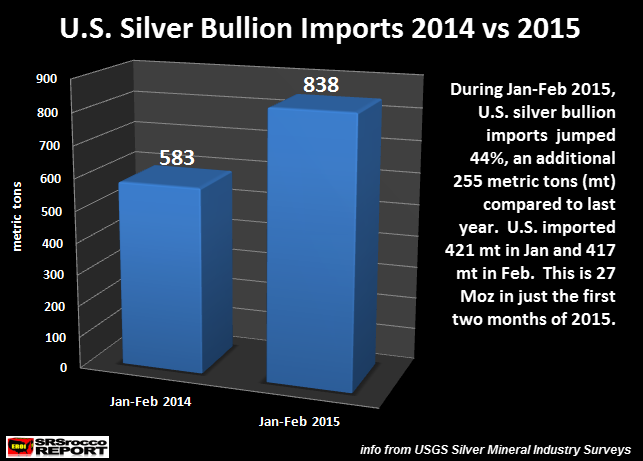

As I mentioned in the article Why Is The U.S. Importing So Much Silver Bullion??, U.S. silver bullion imports surged 44% in the first months of 2015 compared to the same period last year. We can see this in the chart below:

During Jan-Feb 2015, the U.S. imported 838 metric tons (mt) of silver bullion versus 583 mt last year. Moreover, I mentioned that overall demand for silver in the first quarter of 2015 is either flat or down compared to last year. So, why would the U.S. silver market need additional silver bullion if demand is lower? Who is acquiring this silver… and why?

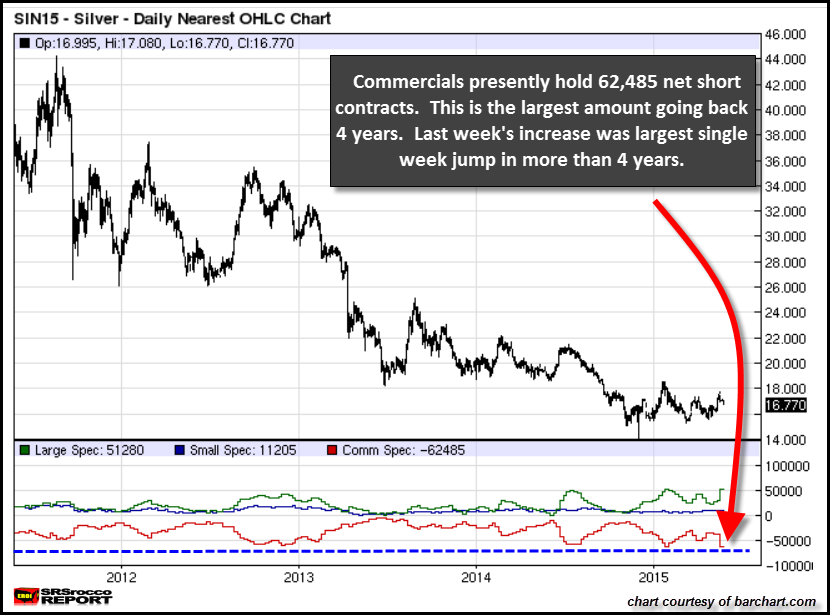

This brings me to the newest data put out by the CFTC. According to the most recent COT Report, the Commercials (big bullion banks) added a massive 18,595 new silver short contracts in just the last week. This is off the charts. If we look at the chart below, we can see just how big this single week increase compares to the changes over the past year:

The RED LINE in the chart below the silver price chart is the change in Commercial net short positions. You will notice that most of the changes in the past were more subtle. The Red Line changes in a stair step pattern, either up or down. The majority of the times, the step changes are very gradual. However, this past week was a huge step down of a net short position of 24,362 contracts.

For all the new folks out there, let me explain this chart a little better. The Red Line represents the net short position of the Commercial bullion banks. As the Red Line heads lower the Commercials are adding more shorts, and as it moves higher, they are reducing shorts. You will notice a particular trend. As the price of silver moves higher, the Commercials add more short positions, which act as more leverage against a higher price.

On the other hand, as the price of silver falls, the Commercial net short position declines as well. Basically, they are liquidating or covering their short positions. If we look at the chart above, we can clearly see that when the Commercial net short position reached a high, so did the price of silver. Here are the corresponding dates:

July 15, 2014 – Commercial Net Shorts = 58,696 – Silver high price = $21.53

Jan. 22, 2015 – Commercial Net Shorts = 61,593 – Silver high price = $18.49

May 19, 2015 – Commercial Net Shorts = 62,485 – Silver high price = $17.74

Each time the Commercials held the highest amount of net short positions, the price of silver peaked. And, as the price fell to a low, the Commercial net short positions bottomed. Not only is the Commercial net short position the highest all year, it’s the highest it’s been in over 4 years:

The blue dotted line represents the current high amount of Commercial net short positions. Now, when the net short positions increase, the line goes lower. The reason for this is the net short is shown as a negative position (in red), and the net long-held by the Large Specs (in green) is shown as a positive position.

So, if we go back all the way to 2011 when silver traded at its record high of $49, the Commercial net shorts weren’t as large as they are today. For some reason, the Commercials were motivated to add the most short positions in one week for more than four years running.

The only other time the Commercial net short position increased similar to this past week was back in June 24, 2014 when it surged 20,059. However, the reason it jumped that much that week was due to the Commercials liquidating 7,733 long contracts while adding 12,326 shorts for a total net short position increase of 20,059. The last weeks silver COT report update showed the Commercials liquidating 5,787 longs and adding 18,575 shorts for a total net short position increase of 24,362… over 4,000 more than the highest in the year.

We also must remember that when the Commercials reduce their long contracts; it acts as an increase to their net short position. That being said, over the past four years the Commercials never added as many short contracts in one week as they did last week.

What does this all mean? Well, if we go by the trend for the past several years, the Commercials are betting that the price of silver is heading lower. How much lower?? Who knows, but the Commercials now have the most net short leverage since their last record net short position on Jan 22nd, when the price went from a high of $18.49 to a low of $15.26, just two months later.

Could Silver Skyrocket Higher On A Massive Short Squeeze?

This is the forecast put forth by Bo Polny of Gold2020Forecast.com. I have spoken with Bo on the phone several times and he has his own method in determining the movement in the precious metals. He sent me this chart showing how the four-year descending triangle for silver was finally broke on May 18th.

Bo believes the price of gold and silver will breakout before the summer, June 21, 2015. So, there you have it. The Commercials have placed their bets looking for the price of silver to move lower, while Bo believes we are going to see a massive short covering rally due to silver breaking out of the four year descending triangle.

With the possibility of Greece exiting the EURO, the situation in the global financial system could become very interesting. There is a good chance the Greek exit could happen quickly. Thus, a BIG move higher in the precious metals prices could possibly be the result. Let’s see how the next month plays out.

As you all know, I am more of a long-term fundamental investor in the precious metals. I believe the peak and decline of global oil production will wreak havoc on the valuations of most paper assets. Owning precious metals during this time will be one of the best investments or stores of wealth. There is no limit to how high the value of gold and silver could reach as the Greatest Paper Ponzi Scheme in history collapses.

Nonetheless, we are going to see a great deal of volatility along the way. Something strange is going on in the silver market that I can’t put my finger on. There is no reason the U.S. should be importing a record amount of silver bullion as Silver Eagle sales are flat year-over-year, industrial silver consumption is likely lower, and the COMEX silver inventories didn’t really increase that much during the first quarter of 2015.

This makes the huge increase in the Commercial Net Short quite interesting. Something BIG is about to happen to silver. The real question is… WHICH WAY WILL IT GO?

end

The following is a link to my latest interview with Greg Hunter. Please watch and feel free to forward or post. Thanks much, Bill

(courtesy Bill Holter/Greg Hunter)

and now Bill Holter’s commentary tonight:

(courtesy Bill Holter/Holter-Sinclair Collaboration)

Bill H:

G.O.T.S.

Jim has asked me to review “G.O.T.S.” (Get Out of The System) with you and comment on it. From a timing standpoint, I can tell you he is as adamant as I’ve ever seen, now, RIGHT NOW you must exit the system! You will not be afforded the opportunity if you are even one second too late!

Dear CIGAs,

For your convenience, here is the GOTS check list.

1. Your equities are held in certificate form or direct registration

2. You have no Federal sponsored retirement funds such as 401K etc.

3. You have no CDs and investments in bonds.

4. You have modest money deposited among selected BRICs countries or BRIC protectorates like Singapore

5. You store your own precious metals.

6. You have no mortgage obligations.

7. You keep cash on hand for 6 months expenses. That is cash, not plastic with credit open

8. You have no consumer debt at all. Pay it down or off.

9. You have a small hobby farm for protein and veggies outside of where you are living with no mortgage debt, set up green.

10. You have a gas, diesel or electric car with high fuel mileage for the farm.

11. You have a generator with large fuel capacity for the farm.

12. 33 1/3% of your liquid net worth is in gold and silver or according to your preference.

The above is by no means a complete checklist. Please keep in mind, not everyone even has the ability to attain the position of this checklist because they simply cannot afford to. In a perfect world, the above checklist would be a “start” only and situated on a private island, preferably with other like minded people.

Let’s break this list down into groups. Numbers 1-4 pertain to your “paper assets”. When the system comes down and is reset, do not count or rely on your paper wealth as an “asset”. There are two problems, first whether your institution will even survive and then of course whether the paper itself retains value. The basic premise is to rely as little as possible on paper and the institutions holding that paper. #4 is notable because having some capital outside of the West and within the BRICS ahead of time will leapfrog any capital controls put in place.

#5 is very important because of the counter party risk issue. Is it really and truly gold and silver that you own? Or is it a piece of paper or a receipt “promising” you gold or silver? Promises are made to broken …and “promises” are the only thing holding the financial system up from total collapse. Better said, it is the “belief” in these promises preventing an outright collapse. I have maintained all along, all that has been done has been to hide the relationship of values between paper currency and gold. Quite simply, more paper exists than is believed and less gold is held than claimed. We will find out the true relationship as the promises are broken!

Numbers 6-8 are all about debt, have as little as possible! For some, this is impossible. Some believe gold will explode in current dollar terms (it will) and their debt will be washed away via inflation (it will not). Jim wrote to me:

“Anyone who knows the real history of Weimar collapse know that the banks were not hurt as mortgages & debts owed were readjusted to value to gold before the collapse to the value of gold after the collapse so you owed the bank the exactly the buying power in terms of the Rentenmark (new currency) after the currency collapsed. Those that owned gold, closed debt obligation ahead of time and GOTS to the greatest degree they could were the winners to the degree they GOTS. they and the banks were the only winners.” I agree with this, there will be no “debt jubilee”. I would also add this, with gold (and especially silver) priced as they are right now, selling metal to pay down debt is not smart because the relationship is skewed. I believe you will have a better gold/dollar relationship at a later date and prior to the issue of a new currency. That said, having zero debt means zero chance of becoming a slave.

Numbers 9-11 are the hardest of all because they require a lot of capital. Being totally self sufficient may only be a dream to you, ignoring this and living in a city will be a nightmare! If the best you can do is to live 30 miles away from a city and in a rural setting, this certainly will be a better choice than living in a metropolis. Remember, food stocks will run out within 3 days and even if you have paper dollar bills, they cannot spend on what does not exist.

A few months back I penned a fictional article referring to how it might begin to go down and can be found here http://blog.milesfranklin.com/fact-or-fiction . By no means was this all inclusive, the exercise was undertaken to make people think. It was meant only as a start for some or a reminder for others of what you may have forgotten. When Jim requested a review, he finished with the following “GOTS = Get out of the system. It is as or more important than owing gold and be in the system.” Please understand what he is saying, “gold will help but it is not a magic bullet”. Gold is meant to get your wealth “from here to there”. In other words, gold will transport wealth from today into tomorrow. It is up to you to live long enough to get there. Sufficient quantities of water, rice, beans and lead will be more helpful than gold or silver in this department! Do the best you can with what you have, do not beat yourself up because you forgot something …you will. Plan with like minded people or neighbors and don’t mistake what is most important, your family and your spirituality. Do what you can even while being laughed at by your friends and family, in the end, they will “get why you GOTS”! And no matter what your faith or who your God is, make your relationship right because when push comes to shove, there are no atheists in a foxhole! For those who have a belief, this is the Absolute GOTS of them all!

Regards, Bill Holter

Holter-Sinclair Collaboration

end

And now overnight trading in stocks and currency in Europe and Asia

1 Chinese yuan vs USA dollar/yuan weakens to 6.2038/Shanghai bourse green and Hang Sang: red

2 Nikkei closed up by 35/10 points or .17%

3. Europe stocks all in the green/USA dollar index up to 97.35/Euro falls to 1.0877/

3b Japan 10 year bond yield: slight falls to .41% !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 123.63/

3c Nikkei still just above 20,000

3d USA/Yen rate now well above the 123 barrier this morning

3e WTI 58.19 and Brent: 63.72

3f Gold down/Yen down

3gJapan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa.

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt. Last night Japan refused to increase it’s QE

3h Oil down for WTI and down for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund falls to 55 basis points. German bunds in negative yields from 4 years out.

Except Greece which sees its 2 year rate rise to 25.05%/Greek stocks up 0.87%/ still expect continual bank runs on Greek banks./Greek default inevitable/

3j Greek 10 year bond yield rises to: 11.82%

3k Gold at 1185.60 dollars/silver $16.68

3l USA vs Russian rouble; (Russian rouble falls 3/4 roubles/dollar in value) 51.49 , the rouble is still the best acting currency this year!!

3m oil into the 58 dollar handle for WTI and 63 handle for Brent/Saudi Arabia increases production to drive out competition.

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/China may be forced to do QE!!

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9496 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0336 well below the floor set by the Swiss Finance Minister.

3p Britain’s serious fraud squad investigating the Bank of England/

3r the 4 year German bund remains in negative territory with the 10 year moving further away from negativity at +.55/

3s Three weeks ago, the ECB increased the ELA to Greece by another large 2.0 billion euros.Two weeks ago, they raised it another 1.1 billion and then last Wednesday they raised it another tiny 200 million euros thus at this point the new maximum was 80.2 billion euros. The ELA is used to replace depositors fleeing the Greek banking system. The bank runs are increasing exponentially. The ECB is contemplating cutting off the ELA which would be a death sentence to Greece and they are as well considering a 50% haircut to all Greek sovereign collateral which will totally wipe out the entire Gr. banking and financial sector.

3t Greece paid the 700 million plus payment to the IMF last Wednesday but with IMF reserve funds. It must be paid back in on June 9.

3 u. If the ECB cuts off Greece’s ELA they would have very little money left to function. So far, they have decided not to cut the ELA

4. USA 10 year treasury bond at 2.16% early this morning. Thirty year rate well below 3% at 2.92% / yield curve flatten/foreshadowing recession.

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

Overnight trading early Wednesday morning from Asia and Europe:

(courtesy zero hedge/Jim Reid Deutsche bank)

Futures Flat After News Greek Deal Distant As Ever, Dollar Surge Continues

It had been a painfully quiet session in Asia (where Chinese levitation continues with the Shanghai Composite up another 0.6% oblivious of yesterday’s rout in the US, because as we explained for China it is now critical to blow the world’s biggest stock bubble) and Europe, where the only notable news as that for the first time in months the ECB had not increase the Greek ELA, keeping it at €80.2 billion on conflicting reports that Greek deposit withdrawals had halted even as Kathimerini said another €300MM had been pulled just yesterday, suggesting the ECB has reached the end of its road when it comes to funding nearly two-thirds of what Greek deposits are left in local banks. But the punchline came moments ago when Bloomberg reported that “Greece will likely miss a deadline for a deal with creditors by the end of the week as the two sides have made little progress during talks in recent days.”

The completely “unexpected” news in turn sent the EURUSD sliding back under 1.09 after a brief rebound to a high of 1.0925 overnight. And speaking of FX, moments ago the USDJPY surged to 123.69, a new post-2007 high. In short: the USD rampage continues following the best week in years, and it remains to be seen if this will lead to another US equity and commodity selloff like yesterday, or if today Gartman flopped to bearish, and suddenly a rising dollar is good for stocks again.

Elsewhere in bond markets, Germany had another quasi-failed 30Y auction, receiving just €1.5 billion in buds will below the €2 billion target, selling €1.424 billion of 2.5% 30Y bonds in the final tally.

A closer look at markets shows a European session which has been particularly light in terms of newsflow and data, with major equity indices (Eurostoxx: 0.4%) in the green paring back some of yesterday’s Greece inspired losses. The only notable news regarding Greece from the European morning has been source comments stating the ECB are to keep Greek ELA ceiling on hold at EUR 80.2bln due to a slowdown in withdrawals over the past week, with the ECB also keeping haircuts on Greek collateral unchanged.

In early trade the USD gave back some of yesterday’s gains amid the light European session, bolstering both EUR and GBP but later pared its initial weakness to trade relatively flat. However USD/JPY remains above the 123.00 handle and near 8 year highs with analysts at JP Morgan suggesting a medium term rise in the pair looks set to continue after breaking above the critical 122.04 resistance level yesterday, with the next notable long term target being the 124-126 range.

In terms of Central Bank speakers, overnight Fed vice-chair Fischer (voter, soft dove) said the Fed could decrease the pace of rate hikes if world economic growth declines while Fed’s Lacker (voter, hawk) reiterated that June is a good time to begin considering raising interest rates.

Looking ahead, the notable event of the session will be the BoC rate decision, with participants also looking out for bond auctions from both UK and Germany as well as any Greek comments from today’s G7 meeting.

The weaker greenback has led to strength in the energy sector after yesterday’s slump as prices fell to a 1-month low and recorded their worst day in over 2-months. While the metals complex has seen less of a paring of yesterday’s moves, with spot gold remaining down almost USD 20 on the week.

After yesterday’s macro economic data deluge, there is little on the US econ calendar with just Mortgage Application data shortly.

In summary: ECB Said to Leave Emergency Aid Level for Greek Banks Unchanged. The Italian and Spanish markets are the best-performing larger bourses, German the worst. The euro is stronger against the dollar. Japanese 10yr bond yields fall; German yields increase. Commodities gain, with wheat, corn underperforming and WTI crude outperforming. U.S. mortgage applications due later.

DB’s Jim Reid concludes the overnight wrap

The market was dazzled yesterday by a rare (by recent standards) day of better than expected US data which ironically coincided with one of the best days of the year for US Treasuries as 10yr and 30yr yields fell 7.0bps and 8.6bp respectively. Over the last few weeks US yields have generally edged higher in spite of weak data. Perhaps yesterday there was a feeling that the earlier the Fed rise the less they might end up doing or being allowed to do. However pre-US numbers there was already a reasonable global fixed income flight to quality bid as Greece continued to worry investors, and the Spanish election results continued to gently reverberate. We also heard from Fed VC Fischer who suggested the pace of Fed rises could be slower than expected if the global economy was weaker than anticipated. This is a little bit like saying that if you put on weight after a suit fitting then the suit won’t fit you but hey it seemed to attract attention.

The batch of better data also supported a strong bid for the Dollar as the DXY rose 1.34%, although much like the Treasury move the index was already firming in the European session before marking its highest level in nearly a month. That strength didn’t help equity markets as the S&P 500 and Dow declined -1.03% and -1.04% respectively with energy stocks (-1.58%) leading the losses after a tumble for Brent (-2.75%) and WTI (-2.83%). Gold was also a notable decliner after falling 1.60% to close at $1187/oz. The flight to quality bid was evident in core European bond markets as 10y Bunds ended -5.6bps at 0.544%, while similar maturity yields in France (-3.9bps), Sweden (-6.2bps), Netherlands (-4.3bps) and Switzerland (-3.7bps) all fell. There was clear weakness in the periphery however as 10y Italy (+9.3bps), Spain (+9.5bps) and Portugal (+10.0bps) yields all rose as the Greece/Spain combination added some nervousness to the morning session. European equity markets largely mirrored their US counterparts as the Stoxx 600 (-0.73%), DAX (-1.61%) and CAC (-0.66%) all fell.

In terms of the details on yesterday’s data, it was the April durable goods report which generated much of the headlines. Despite an, as expected, -0.5% mom headline reading, the ex transportation print rose a greater than expected +0.5% mom (vs. +0.3% expected) and the core capex orders rose +1.0% mom, also ahead of expectations of +0.3% with a decent upward revision to the March reading (+1.5% mom from -0.5% previously). Core shipment orders (+0.8% mom vs. +0.2% expected) also saw a similar beat. Other notable releases included a decent jump in the May consumer confidence index, the reading rising 1.1pts (albeit from a downwardly revised March print) to 95.4 (vs. 95.0 expected). New home sales data was also encouraging for April as sales rose +6.8% mom (vs. +5.6% expected) to an annualized rate of 517k, backing up the recent strong housing starts and building permits data. Elsewhere, we also got some now slightly outdated house price data with the March FHFA house price index (+0.3% mom vs. +0.7% expected) and S&P/Case-Shiller index (+0.95% mom vs. +0.90% expected) slightly more mixed. Meanwhile, there was some softness to come out of the flash PMI’s for May as the services print fell 1pt to 56.4 (vs. 56.5 expected) to the lowest reading since January. In turn this meant that we saw the composite fall 0.9pts to 56.1 – also a four month low. Finally, manufacturing indicators were somewhat contrasting for May. The Richmond Fed manufacturing index jumped 4pts to 1 (vs. 0 expected) for the month while the Dallas Fed manufacturing activity index fell 4.8pts to -20.8 (vs. -12.4 expected), the lowest reading since June 2009 although the details suggested a rosier picture for expectations of future business conditions.

Following yesterday’s stronger durable goods orders data, the Atlanta Fed GDPNow model raised its Q2 GDP estimate to +0.8% from +0.7% previously, although the level is still well behind the current market consensus. The data yesterday did little to move the dial on Fed Funds contracts with the Dec-15, Dec-16 and Dec-17 contracts 5bps, 5bps and 4bps lower in yield respectively. Back to Fischer’s comments quickly, as well as noting that the pace of tightening may slow in the face of weaker than expected global growth, the Fed VC also noted that ‘the actual raising of policy rates could trigger further bouts of volatility, but my best estimate is that the normalization of our policy should prove manageable’. After market hours we also learned that the Fed’s Yellen will not be participating at this year’s Jackson Hole event on August 27th-29th, important perhaps for those who were hoping that the meeting could provide some clues ahead of the potentially pivotal September FOMC meeting.

In terms of the follow up in markets in Asia this morning, bourses are largely tracking the weakness in the US and trading lower as we type. The Hang Seng (-0.57%), Kospi (-1.56%) and ASX (-0.78%) in particular have declined. China equity markets are a tad more mixed however, with the CSI 300 -0.49% lower but the Shanghai Comp +0.16%, supported partly by April industrial profits data for the region which showed a +2.6% yoy rise in April and the first positive print since September last year. Meanwhile in Japan, the Nikkei (+0.24%) has reversed earlier losses after BoJ Governor Iwata said that the Central Bank ‘currently expects that the CPI rate is likely to reach around 2% in the first half of fiscal 2016’. Iwata noted that this timing is somewhat delayed from the previous projection, but that the underlying trend in inflation itself has been rising steadily with QQE working as envisaged.

Moving on, talks continued between Greece and its creditors again yesterday but appeared to yield similar results with little suggestion of any material progress or agreement being made. Instead, we heard from Finance Minister Varoufakis who played down fears that the June 5th IMF repayment won’t be made, instead saying that he expects a deal to be made by then which will subsequently release funds for the government to repay its obligations. There were also suggestions, according to the WSJ, that the Greek government has issued a decree ordering the transfer of funds in inactive bank accounts of public sector bodies to be transferred to the Bank of Greece in a bid to raise funds, as well as a proposed tax on undeclared deposits abroad in a sign of how tight the cash position is. In a report put out by the MNI meanwhile, the EC’s Juncker reiterated that June is an ‘obvious deadline’ and that he ‘will do everything to avoid scenarios that include capital controls’. Juncker then went on to say that Greek PM Tsipras is ‘becoming increasingly responsible’ before then questioning his party colleague Varoufakis by saying that he is ‘not helping the process’. Greek officials are due to meet today in Brussels while the saga is expected to be a talking point at the 3-day G7 meeting beginning today.

Following on from the weekend’s regional and local elections in Spain, DB’s Marco Stringa yesterday published a report looking at the impact of what this may now mean for Spain. Marco notes that Spain’s economy is outperforming most euro-area economies and that maintaining medium-term success depends on maintaining economic and political equilibria. Sunday’s local election for the most part confirmed the recent trend in opinion polls that have pointed to an unprecedentedly fragmented parliament and a potentially fragile government. He expects difficult negotiations to now commence and potentially unstable local governments which as a result means we shouldn’t see much improvement in regional deficits (and therefore the general fiscal deficit). Importantly however, Marco notes that this should not necessarily be taken as a map of what will happen after the year-end election. After the general election, the newer parties may have a greater incentive to cooperate and form a coalition. Besides this, both opinion polls and Sunday’s local elections suggest that the likelihood of Podemos being the predominant parliamentary force has decreased materially in his view.

Looking at the day’s calendar, it’s fairly quiet on the whole with the start of the G7 Meeting of finance ministers and central bankers in Dresden potentially generating some Greece related headlines. Aside from that, data wise we’ve got just consumer confidence data for both Germany and France due. After a busy afternoon yesterday for data in the US, there are no notable releases due this afternoon.

end

Another bond default imminent as China’s Coca Cola bottler in trouble:

(courtesy zero hedge)

China’s Third Bond Default Imminent: Coke Supplier To Miss Payment

A little over a month ago, China witnessed its first default by a state-owned enterprise when Baoding Tianwei Group, a subsidiary of state-run China South Industries Group, defaulted on a $14 million coupon payment. That event raised two important issues. First, it suggested that Beijing will not necessarily step in to rescue state-affiliated companies who find themselves in financial trouble and second, it underscored the degree to which China’s $14 trillion corporate debt pile presents a very real risk especially considering the rapidly increasing number of non-performing loans on the books of the country’s banking sector.

Today, we get still more evidence that China may be headed for a debt disaster as a third company has now defaulted on its onshore bonds.

This time it’s soft drink bottle maker Zhuhai Zhongfu Enterprise Co which, as Bloomberg reports, will come up nearly 450 million yuan short when a principal payment for paper issued in 2012 comes due on Thursday. Here’s more:

Zhuhai Zhongfu Enterprise Co., which supplies bottles for Coca-Cola Co. and PepsiCo Inc. in China, can only repay 148 million yuan ($23.9 million) of the 590 million yuan principal, according to a statement to the Shenzhen Stock Exchange Monday. It plans to pay all the 31.152 million yuan of interest. The manufacturer, which isn’t state-owned, sold the 5.28 percent securities in 2012…

Han Huiming, board secretary at Zhuhai Zhongfu, said when reached by phone Tuesday that the company will try to raise funds for the bond payment until the last moment.

The manufacturer, which is based in the southern city of Zhuhai and employees about 4,000 people, said in a May 21 statement that a bank consortium rejected its application for 500 million yuan of loans in May.

The Zhuhai branches of China Everbright Bank Co. and Bank of China Ltd. have limited its freedom to spend the 61 million yuan of capital on its accounts, it said.

Because Zhuhai Zhongfu is having a “liquidity crisis,” the company can’t collect enough money for the payment through its own business operations, according to the statement Monday.

Zhuhai Zhongfu’s orders have declined significantly since 2012 as its biggest clients increased their own production of bottles, according to a report from China International Capital Corp. on May 11. The company’s business with its three largest clients Coca-Cola, PepsiCo and Uni-President China Holdings Ltd. generated only 33 percent of revenue last year, down from 49 percent in 2011, according to CICC. Coca-Cola remains the manufacturer’s biggest customer, according to board secretary Han.

The shift comes as Coca-Cola and PepsiCo are increasingly focusing on cost-cutting to help support operating margins amid waning soft-drink demand, according to Bloomberg Intelligence.

All of the above notwithstanding, the company’s Shenzhen-listed shares had risen more than 120% YTD before they were halted last month with equity ‘investors’ completely ignoring the fundamental story as they have with virtually everything else that changes hands on the exchange which is now trading at a mind-bending 71 times earnings after at least 250 individual names traded limit-up on Tuesday.

Indeed, you didn’t even have to look at an income statement to know how risky of a bet this was because the debt was yielding near 20% before it was delisted last year.

The company’s notes yielded 19.33 percent in the secondary market on June 27 last year before being delisted from the exchange, according to exchange data.

Still, investors remain confident that Beijing, despite rhetoric to the contrary, will be loath to allow onshore defaults as $17 billion in principal payments come due in 2015, a figure that is set to rise exponentially over the next six years. Here’s Bloomberg again:

The People’s Bank of China may coordinate loan support for Baoding Tianwei Group Co. after it became the first state-owned entity to default on a coupon payment in April, OCBC said, citing local media. Restaurant-turned-Internet firm Cloud Live Technology was the first onshore issuer to miss a principal payment in April and has raised funds from “unclear” sources to partly repay noteholders, OCBC said.

Zhuhai Zhongfu, based in the southern city of Zhuhai, is still short 442 million yuan for a bond payment due Thursday, the company said in a statement to the Shenzhen stock exchange Monday. It will try to raise more money by May 26, it said.

Narrowing spreads on onshore bonds suggest investors are still counting on state guarantees, said OCBC, which compared Baoding’s situation with bailouts last year for Shanghai Chaori Solar Energy Science & Technology Co. and a trust product known as China Credit Equals Gold No. 1. The difference between AAA and BBB+ rated yields has fallen to 933 basis points from 942 at the start of the year, while the gap between AAA and AA notes shrank to 114 from 129, according to the report.

Chinese companies must repay an equivalent $16.9 billion of maturing onshore notes in 2015, Koh estimated in the report. That increases every year and will peak at $192.3 billion in 2021. Some 65 percent of institutions expect at least one more onshore default this quarter, according to a Bloomberg survey of 20 banks, brokerages and money managers published on May 18.

Clearly, this is a rather large problem, but as we outlined in “How China’s Banks Hide Trillions In Credit Risk,” the government will often force banks to roll over maturing debt in order to paper over (literally) what is almost certainly a deteriorating situation and in fact, the PBoC recently did a complete 180 on regulations around local government financing via LGFVs in an effort to jumpstart the shadow banking credit creation machine, a move which Fitch calls “an explicit form of regulatory forbearance.”

Whatever the case, it’s becoming increasingly clear that the combination of slumping economic growth and $28 trillion in debt has the potential to trigger a wave of defaults from both state-run and private borrowers, a state of affairs which will test Beijing’s resolve when it comes to projecting stability in the country’s credit markets.

With Greece “Nowhere Close” To Deal, Depositors Pull €300 Million From Banks In Single Day

On Tuesday, Greece postponed a scheduled Eurogroup meeting in Brussels without offering a reason as officials conducted “preparatory” discussions and held an evening teleconference with creditors. Face-to-face meetings will take place today with just 9 days to go until June 5 when Athens will miss a payment to the IMF, triggering an unprecedented default the repercussions of which no one can accurately predict.

Also on Tuesday, Greek FinMin Yanis Varoufakis allegedly told Greek reporters that one measure under consideration to help stem the outflow of deposits from Greek banks was a levy on ATM withdrawals designed to encourage the use of credit cards over cash, a rather ironic suggestion coming from a government crippled by debt. The Finance Ministry was quick to deny that such a levy was being considered because after all, one way to ensure that ATM lines will get quite a bit longer is to suggest that depositors will soon be subject to a levy on withdrawals. Unfortunately, it appears as though the move to dispel the ATM tax “rumor” came too late because according to Kathimerini, deposit flight accelerated meaningfully on Tuesday. Here’s more:

Statements suggesting the imposition of capital control measures over the upcoming long weekend, and Tuesday’s reference by the Finance Ministry to the possible imposition of a levy on cash machine withdrawals – later withdrawn – sent many to the ATM. At the same time, bank officials point to widespread concerns about the possibility of a rift between Greece and its creditors over the government’s failure to repay a scheduled installment to the International Monetary Fund next week.

Credit sector professionals reported that deposit outflows on Tuesday alone came to 300 million euros, against about 100 million euros per day in recent days. They said that while this amount is quite high, the situation is under control as citizens are remaining calm on the positive messages from Greek officials.

On Wednesday the ECB board is expected to decide on a fresh extension of the ELA mechanism following the addition of another 200 million euros last week to a total of 80.2 billion euros. Although pressure by certain ECB council members for a tougher stance toward Greece has grown, sources agree that the ECB will probably avoid making any decisions that could trigger any major developments.

Or perhaps not, because as it turns out, the ECB did not in fact raise the cap on the emergency liquidity lifeline that’s keeping the Greek banking sector afloat, opting instead to keep the ceiling unchanged at €80.2 billion which leaves banks with about €3 billion in remaining liquidity.

Ironically, the ECB cited “very limited deposit withdrawals over past week” as the reason for its decision suggesting that either Greek bank officials are lying about the severity of the outflow or Mario Draghi is deliberately tightening the screws in an effort to help creditors extract concessions from PM Alexis Tsipras. The prevailing assumption had been that the central bank would continue to incrementally raise the ELA cap (the average weekly increase had been around €1.5 billion before last week’s €200 million hike) until Greek banks exhausted their available collateral, said to amount to around an additional €13 billion. That would have allowed banks to offset deposit outflows through the end of July. Now, that assumption looks to be questionable. As a reminder, here’s what the cash situation looks like:

Meanwhile, some officials have now thrown in the towel, with Bloomberg reporting that a deal will not be reached by the end of this month as Greece is “nowhere close” to striking a compromise that’s acceptable to the IMF and the EU:

- GREECE SAID LIKELY TO MISS MAY DEAL DEADLINE AS TALKS STALL

- GREECE SAID TO BE NOWHERE CLOSE TO AGREEMENT WITH CREDITORS

This will come as no surprise to regular readers who will recall that the IMF and the European Commission are now keen to send a strong message in terms of granting no concessions in talks with Greece after anti-austerity parties staged an electoral coup in Spain in Sunday’s regional and municipal vote. By making an example of Greece, the troika can effectively discourage other democratically elected governments from pursuing similar mandates and indeed, we’re now seeing commentary that suggests giving in to Greece’s demands would be worse than Grexit.

Via Bloomberg (note that this is a Portuguese daily interviewing a German official):

The risk of contagion from Greece exiting the euro area is smaller than it was a few years ago, Christoph Schmidt, head of the German government’s council of economic advisers, is cited as saying in an interview done last week with Diario Economico.

Fearing a Greek exit to the point of accepting all the conditions that the Greek government demands would be a lot worse than an exit, paper cites Schmidt as saying.

And BlackRock has a similar message to the Greeks:

A Greek exit from the euro area is less disastrous than making concessions, Het Financieele Dagblad reports citing an interview with BlackRock CEO Larry Fink.

Says that if concessions are made, other countries may also demand them.

As an investor, he would be reassured by a decisive Europe.

Says it’s unacceptable Alexis Tsipras wants to reverse earlier agreements on reforms.

It’s now abundantly clear that the IMF, Brussels, and Berlin will accept nothing less than a wholesale abandonment of Syriza’s anti-austerity platform if Tsipras intends to walk away with a deal. Short of that, Syriza will be left to fight for their political life amid what will surely be a catastrophic economic collapse should the country be forced to revert to a parallel currency.

Either way, Greece’s creditors will have achieved their goal of using financial leverage to suppress the anti-austerity germ — for now.

end

The following is a terrific commentary from David Stockman who knows very well what will happen once Greece fails. This is a must read..

(courtesy David Stockman/)

“Graccident” Will Trigger The Demise Of The ECB And The World’s Toxic Regime Of Keynesian Central Banking

Submitted by David Stockman via Contra Corner blog,

It is not surprising that in a few short months Yanis Varoufakis has proven himself to be a thoroughgoing Keynesian statist. After all, what would you expect from an economics PhD who co-authored books with Jamie Galbraith? The latter never saw an economic malady that could not be cured with bigger deficits, prodigious printing press “stimulus” and ever more intrusive state intervention and redistribution.

In what is apparently a last desperate game theory ploy, however, Varoufakis has done his countrymen, Europe and the world a favor. By informing his Brussels paymasters that they must continue to subsidize his bankrupt Greek state because it is the only way to preserve the European Project and vouchsafe the Euro, the Greek Finance minister blurted out the truth of the matter, albeit perhaps not intentionally:

“It would be a disaster for everyone involved, it would be a disaster primarily for the Greek social economy, but it would also be the beginning of the end for the common currency project in Europe,” he said.

“Whatever some analysts are saying about firewalls, these firewalls won’t last long once you put and infuse into people’s minds, into investors’ minds, that the eurozone is not indivisible,” he added.

He sure got that right. People who believe in democracy and economic liberty anywhere in the world should pray for a Graccident. During the next several weeks, when $1.8 billion in IMF loans come due that Greece cannot possibly pay, there will occur a glorious moment of irony for Syriza.

If it holds firm to its leftwing statist agenda and takes Greek democracy back from the clutches of the EU/IMF apparatchiks, Syriza will strike a blow for democracy and capitalism in one great historic volte-face. That is to say, defiance of the Germans and the troika would amount to a modern monetary Marathon; it would trigger a thundering collapse of the ECB and the cancerous superstate regime built upon it in Frankfurt and Brussels—–and, along with it, cast a mortal blow upon the worldwide Keynesian central banking regime, too.

The hour comes none to soon. In a few short years under Draghi and in the context of Europe’s fiscal and economic enfeeblement, the ECB has been transformed into a hideous reverse Robin Hood machine. So doing, it has gifted financial gamblers and front-runners with hundreds of billions of ill-gotten gains in the euro debt markets.

In the days shortly before Draghi issued his “whatever it takes” ukase, for example, the Italian 10-year bond was trading at 7.1%. So speculators who bought it then have made a cool 350% gain if they were old-fashioned enough to actually buy the bonds with cash. And they are laughing all the way to their estates in the South of France if their friendly prime broker had arranged to hock these deadbeat Italian bonds in the repo market even before payment was due. In that case, Mario’s front-runners are in the 1000% club and just plain giddy.

![]()

While it is extremely difficult to think of a reason that would justify such wanton redistribution to financial gamblers, the ECB rationale is so astoundingly threadbare as to be laughable. In a word, Draghi and his minions claims that Europe’s economic torpor stems from too little inflation and too little borrowing by private households and businesses. Hence, they have no choice except to drastically falsify prices in Europe’s entire $20 trillion bond market in order to rekindle 2% inflation and get economic growth off the flat line.

Oh, puleeze. The Eurozone economies have had no problem whatsoever in generating an ample quotient of inflation ever since the inception of the single currency—-as if that had anything to do with the growth of real production and wealth anyway.

In fact, the european CPI has gained an average of 2.1% per annum during the last decade and one-half. Self-evidently, the temporary flattening of the inflation curve in the last year is a consequence of the plunge of oil and other commodity prices, not anything that could possibly account for Europe’s languishing growth rate.

In fact, the euro area core CPI is up by nearly 1% during the last year, and has gained about 1.5% per annum during the past eight years during which time global oil prices have soared and collapsed twice. Quite simply, low-flation is a myth invented by the Keynesian money printers to justify massive monetization of the public debt.

So there is really nothing behind the low-flation mantra except the spurious argument that consumers will defer purchases unless assured that prices will continue to rise and eat away at their paychecks.

No, Mario, European consumers are not spending owing to the fact that their incomes are not growing. Household “demand” is tepid because take home pay everywhere in the eurozone is being eviscerated by high taxes. And consumers are not borrowing because their balance sheets are already saturated with more debt than they can sustain.

Indeed, private sector borrowing nearly tripled during the decade before the financial crisis. That it has flattened out since then only means that the supply of credit worthy borrowers has been exhausted, not that there exists some mysterious economic malady that can be cured by the ECB’s printing press.

Stated differently, even after accounting for the stagnation of loan growth in the last few years, private sector loans outstanding still represent a 6.0% per annum gain since 1997. And that compares to an average nominal GDP growth rate in the eurozone countries of just 3.3%annually. At some point, every debt addicted economy runs out of balance sheet runway——a condition that Europe attained long ago.